Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Kraton Corp | d8k.htm |

March

3, 2011 Kraton Performance Polymers, Inc.

Fourth Quarter 2010 Earnings Conference Call

Exhibit 99.1 |

Forward-Looking Statement Disclaimer

2

This presentation may include “forward-looking statements” that reflect our plans,

beliefs, expectations and current views with respect to, among other things, future events and

financial performance. Forward-looking statements are often characterized by the use

of words such as “believes,” “estimates,” “expects,” “projects,” “may,” “intends,”

“plans” or “anticipates,” or by discussions of strategy, plans or intentions. All

forward-looking statements in this presentation are made based on management's current

expectations and estimates, which involve risks, uncertainties and other factors that could

cause actual results to differ materially from those expressed in forward- looking

statements. Readers are cautioned not to place undue reliance on forward-looking statements. These risks

and uncertainties are more fully described in “Part I. Item 1A. Risk Factors” contained in

our Annual Report on 10-K, as filed with the Securities and Exchange Commission and as

subsequently updated in our Quarterly Reports on Form 10-Q, and include risks related to:

conditions in the global economy and capital markets; our reliance on LyondellBasell Industries

for the provision of significant operating and other services; the failure of our raw materials

suppliers to perform their obligations under long-term supply agreements, or our inability to

replace or renew these agreements when they expire; limitations in the availability of raw

materials we need to produce our products in the amounts or at the prices necessary for us to

effectively and profitably operate our business; competition in our end- use markets, by

other producers of SBCs and by producers of products that can be substituted for our products; our

ability to produce and commercialize technological innovations; our ability to protect our

intellectual property, on which our business is substantially dependent; infringement of our

products on the intellectual property rights of others; seasonality in our Paving and Roofing

business; financial and operating constraints related to our substantial level of indebtedness;

product liability claims and other lawsuits arising from environmental damage or personal

injuries associated with chemical manufacturing; political and economic risks in the various countries in

which we operate; the inherently hazardous nature of chemical manufacturing; health, safety and

environmental laws, including laws that govern our employees’ exposure to chemicals deemed

harmful to humans; regulation of our customers, which could affect the demand for our products

or result in increased compliance costs; international trade, export control, antitrust, zoning

and occupancy and labor and employment laws that could require us to modify our current

business practices and incur increased costs; our relationship with our employees; loss of key

personnel or our inability to attract and retain new qualified personnel; fluctuations in currency

exchange rates ; the fact that we do not enter into long-term contracts with our customers;

a decrease in the fair value of our pension assets, which could require us to materially

increase future funding of the pension plan; and concentration of ownership among our principal

stockholders, which may prevent new investors from influencing significant corporate decisions.

We assume no obligation to update such information. Further information concerning issues that

could materially affect financial performance related to forward looking statements can be found in our periodic

filings with the Securities and Exchange Commission. |

GAAP

Disclaimer 3

This presentation includes the use of both GAAP (generally accepted accounting

principles) and non-GAAP financial measures. The non-GAAP financial

measures are EBITDA and Adjusted EBITDA. The most directly comparable GAAP

financial measure is net income/loss. A reconciliation of the non-GAAP

financial measures used in this presentation to the most directly comparable

GAAP measure is included herein. We consider EBITDA and Adjusted EBITDA

important supplemental measures of our performance and believe they are

frequently used by investors and other interested parties in the evaluation

of companies in our industry. EBITDA and Adjusted EBITDA have limitations as

analytical tools and should not be considered in isolation or as a

substitute for analysis of our results under GAAP in the United States.

|

Update

on 2010 Business Priorities Innovation-led Top-line

Growth

Capital Investment

Executed $56 million capex program with all projects on

schedule and within budget

Belpre IR conversion

Paulinia IRL expansion

Belpre DCS Phase II

Significant progress in evaluating options for

additional HSBC capacity

Earnings Growth

Q4 revenue up 15% y/y, net income of $10 million

2010 revenue up 27%, net income of $97 million

Q4 Adjusted EBITDA of $34 million

2010 Adjusted EBITDA of $195 million

4

Innovation volume at record level

Performance in PVC alternatives for wire & cable and

medical applications in 2010 above plan

Year end vitality index at 13% |

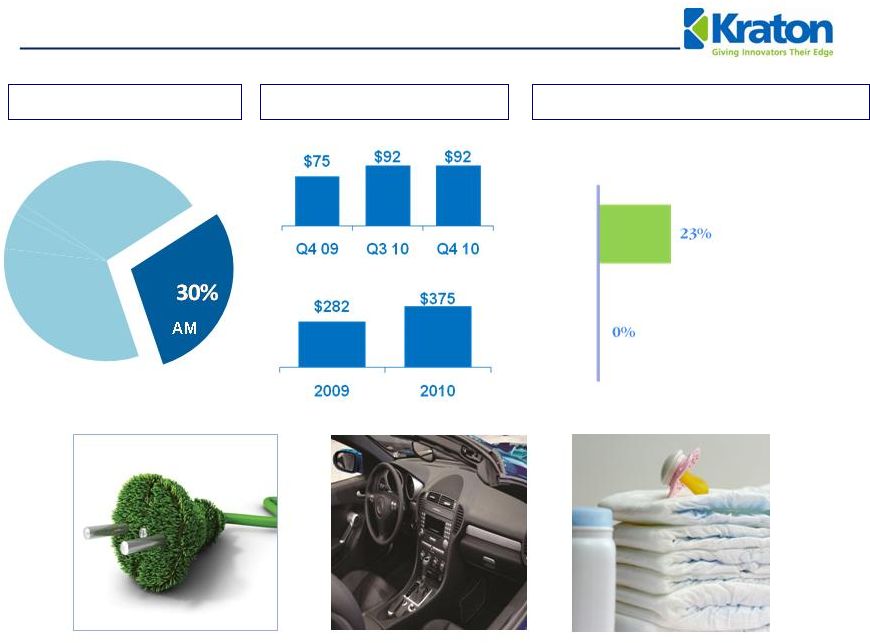

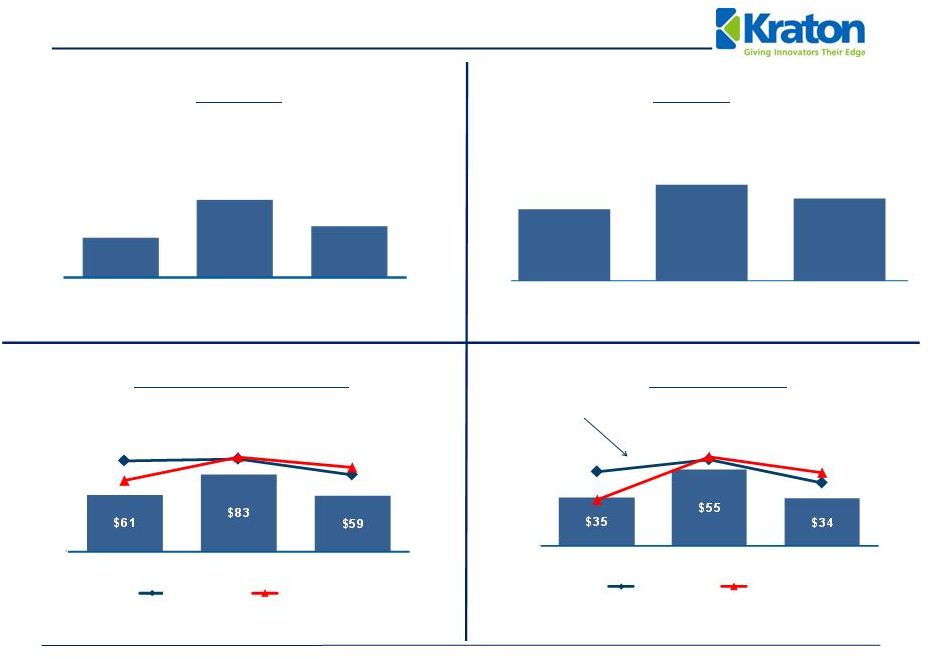

Advanced Materials End Use Review

5

2010 Revenue

Profile

Change in Sales Revenue

End Use Revenue

Change in Sales Revenue

US $ in millions

AM

Q4 2010 vs. Q4 2009

Q4 2010 vs. Q3 2010 |

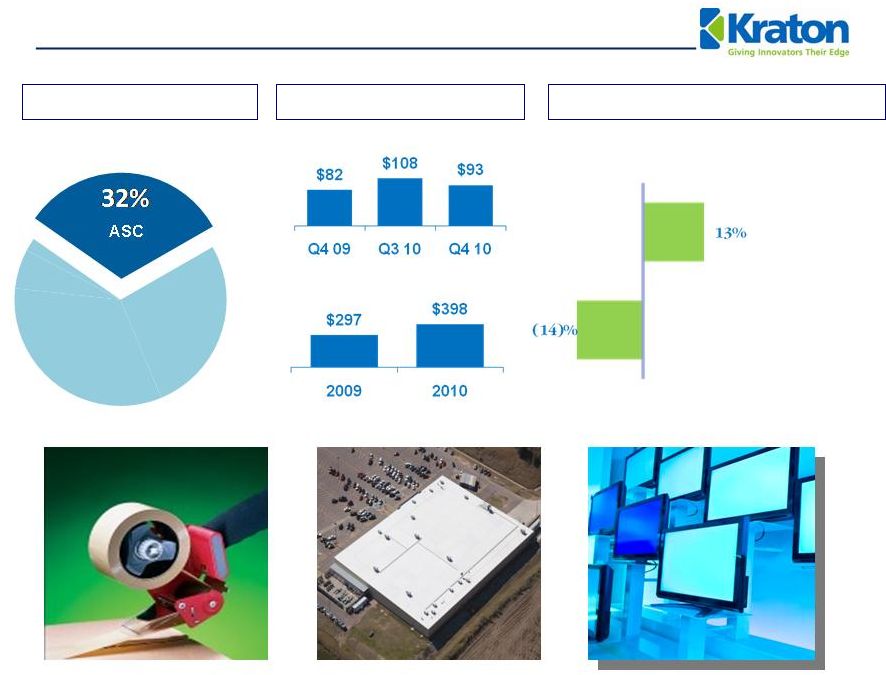

Adhesives, Sealants and Coatings End Use Review

2010 Revenue Profile

Change in Sales Revenue

6

Q4 2010 vs. Q4 2009

Q4 2010 vs. Q3 2010

End Use Revenue

US $ in millions

ASC |

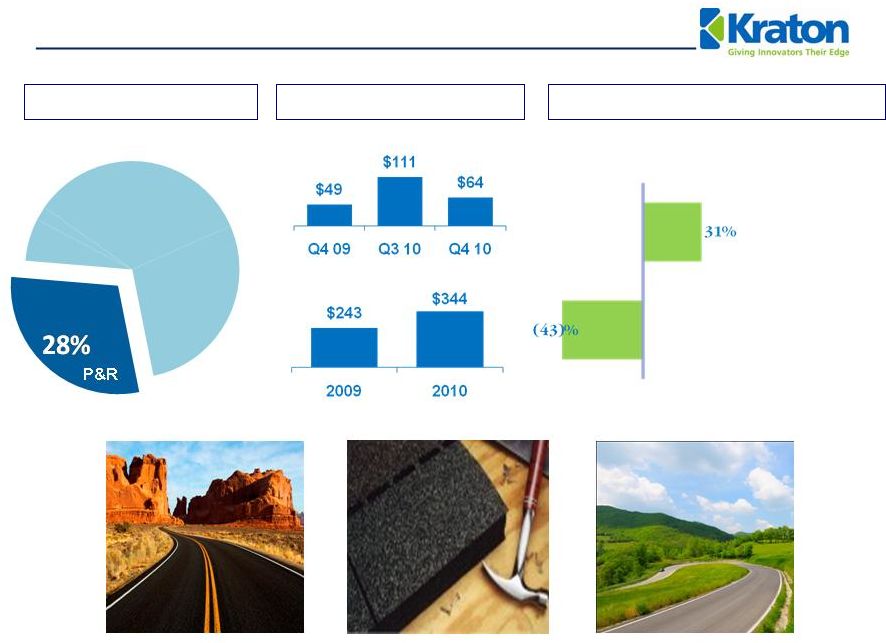

Paving

and Roofing End-Use Review 7

2010 Revenue

Profile

Change in Sales Revenue

End Use Revenue

Change in Sales Revenue

US $ in millions

P&R

Q4 2010 vs. Q4 2009

Q4 2010 vs. Q3 2010 |

Emerging Businesses End Use Review

8

2010 Revenue

Profile

Annual Sales Revenue

End Use Revenue

US $ in millions

US $ in millions

$24

$19

$27

Q4 09

Q3 10

Q4 10

7%EB

$35

$61

$79

2010

2009

2008 |

Innovation-led Top Line Growth

9

Goal -

20% of revenue from innovation

Vitality Index

Innovation volume at record levels

Good technical progress on all innovation platforms

Strong performance in key projects

2010 combined revenue for wire & cable , IV films, self-adhered roofing

and protective films was up 350% from 2009.

Innovation

platforms

such

as

slush

molding

and

Nexar™

are

in

qualification

phase

6%

11%

13%

13%

14%

12%

2005

2006

2007

2008

2009

2010 |

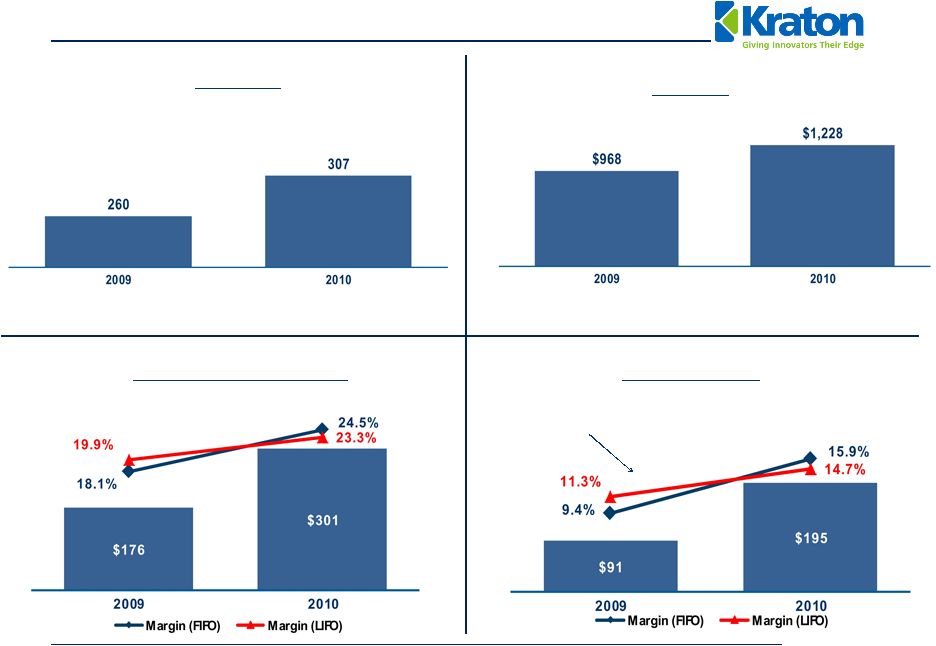

Volume (kT)

Selected Financial Trends –

Q4 2010

(1)

Q4 2009 includes by-product revenue of $12 mln associated with our

Pernis, the Netherlands facility, which was closed in Q4 2009.

(2)

Adjusted EBITDA is GAAP EBITDA excluding management fees, restructuring and

related charges, non-cash expenses, and the gain on extinguishment of

debt. 10

Revenue

(1)

(US $ in Millions)

Gross Profit and Gross Margin

(US $ in Millions)

Adjusted EBITDA

(2)

(US $ in Millions)

Adjusted

EBITDA

Margin

61

81

Volume (kT)

Revenue

(1)

(US $ in Millions)

Selected Financial Trends –

Q4 2010

(1)

Q4 2009 includes by-product revenue of $12 mln associated with our

Pernis, the Netherlands facility, which was closed in Q4 2009.

(2)

Adjusted EBITDA is GAAP EBITDA excluding management fees, restructuring and

related charges, non-cash expenses, and the gain on extinguishment of

debt. 10

Gross Profit and Gross Margin

(US $ in Millions)

Adjusted EBITDA

(2)

(US $ in Millions)

Adjusted

EBITDA

Margin

67

Q3 10

Q4 10

Q4 09

Q3 10

Q4 10

Q4 09

Q3 10

Q4 10

Q4 09

Q3 10

Q4 10

Q4 09

$251

$335

$288

24.7%

25.2%

22.6%

20.6%

24.3%

19.0%

16.4%

16.9%

13.9%

11.9%

14.0%

8.7%

Margin (FIFO)

Margin (LIFO)

Margin (FIFO)

Margin (LIFO) |

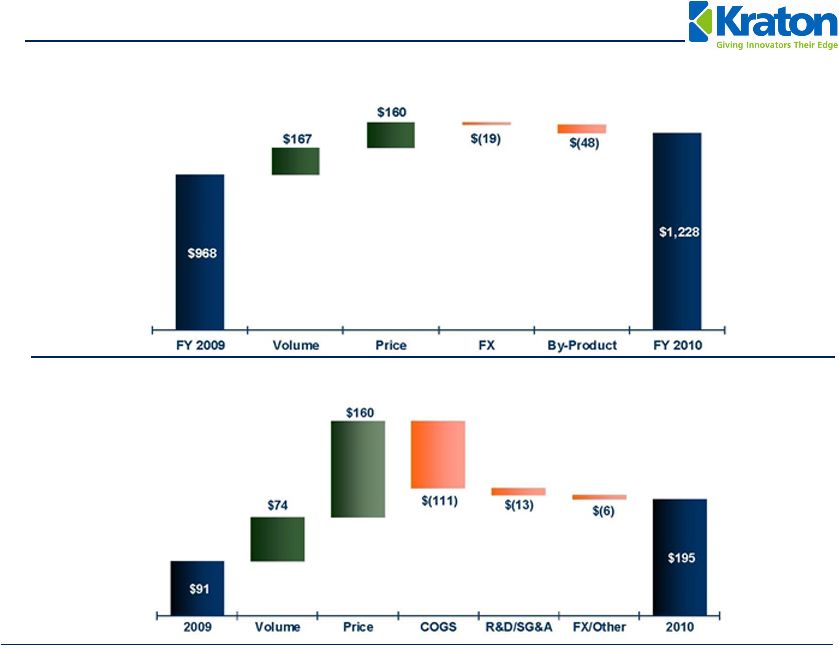

Q4

2010 Operating Revenue Walk Q4 2010 vs. Q3 2010

Q4 2010 vs. Q4 2009

US $ in millions

11 |

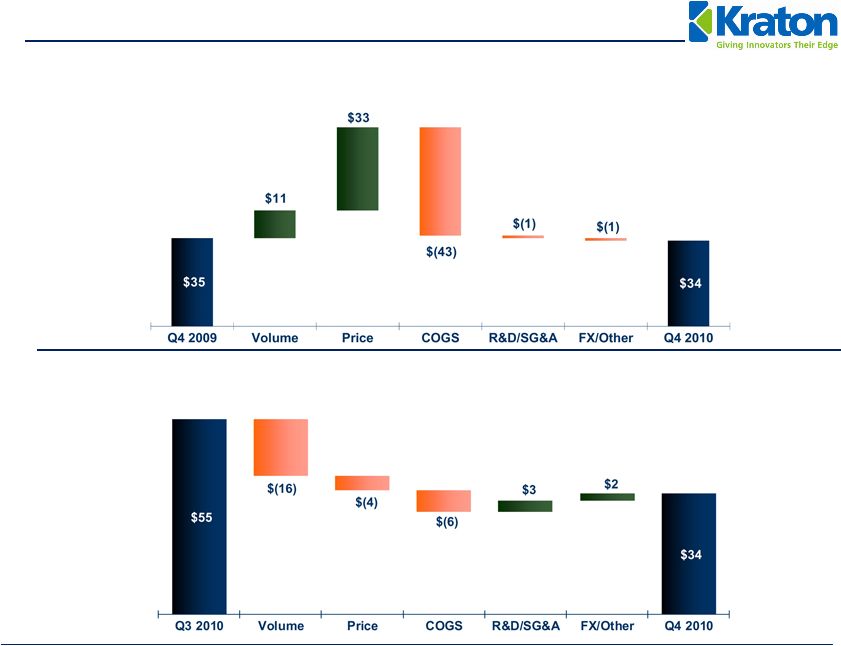

Q4

2010 Adjusted EBITDA (1)

Walk

Q4 2010 vs. Q3 2010

Q4 2010 vs. Q4 2009

US $ in millions

(1)

Adjusted EBITDA is GAAP EBITDA excluding management fees, restructuring and related charges,

non-cash expenses, and the gain on extinguishment of debt.

12 |

Volume (kT)

Selected Financial Trends –

2010 vs. 2009

(1)

2009 includes by-product revenue of $48 mln associated with our Pernis,

the Netherlands facility, which was closed in Q4 2009. (2)

Adjusted EBITDA is GAAP EBITDA excluding management fees, restructuring and

related charges, non-cash expenses, and the gain on extinguishment of

debt. 13

Revenue

(1)

(US $ in Millions)

Gross Profit and Gross Margin

(US $ in Millions)

Adjusted EBITDA

(2)

(US $ in Millions)

Adjusted

EBITDA

Margin |

2010

Operating

Revenue

and

Adjusted

EBITDA

(1)

Walk

Operating Revenue

Adjusted EBITDA

US $ in millions

14

(1)

Adjusted EBITDA is GAAP EBITDA excluding management fees, restructuring and related charges,

non-cash expenses, and the gain on extinguishment of debt.

|

2010

Financial Overview (1)

Adjusted EBITDA is GAAP EBITDA excluding management fees, restructuring and related charges,

non-cash expenses, and the gain on extinguishment of debt.

US $ in Thousands except per share data

15

Fourth Quarter

Full Year

2010

2009

2010

2009

Sales Volume (kT)

67

61

307

260

Total Operating Revenues

$

288,165

$

250,708

$

1,228,425

$

968,004 Cost of Goods Sold

228,793

189,840

927,932

792,472

Gross Profit

59,372

60,868

300,493

175,532

Operating expenses

Research and Development

5,947

6,097

23,628

21,212

Selling, General and Administrative

23,652

22,919

92,305

79,504

Depreciation and Amortization of Identifiable Intangibles

13,178

25,169

49,220

66,751

Gain on Extinguishment of Debt

-

-

-

23,831

Equity in Earnings of Unconsolidated Joint Venture

170

98

487

403

Interest Expense, net

5,506

9,179

23,969

33,956

Income (Loss) Before Income Taxes

11,259

(2,398)

111,858

(1,657)

Income Tax

Expense 960

(882)

15,133

(1,367)

Net Income (Loss)

$

10,299

$

(1,516)

$

96,725

$

(290) Earnings

(Loss)

per

Common

Share

-

Diluted

$

0.32

$

(0.07)

$

3.07

$

(0.01) Adjusted

EBITDA (1)

$

34,311

$

35,044

$

194,906

$

91,359 |

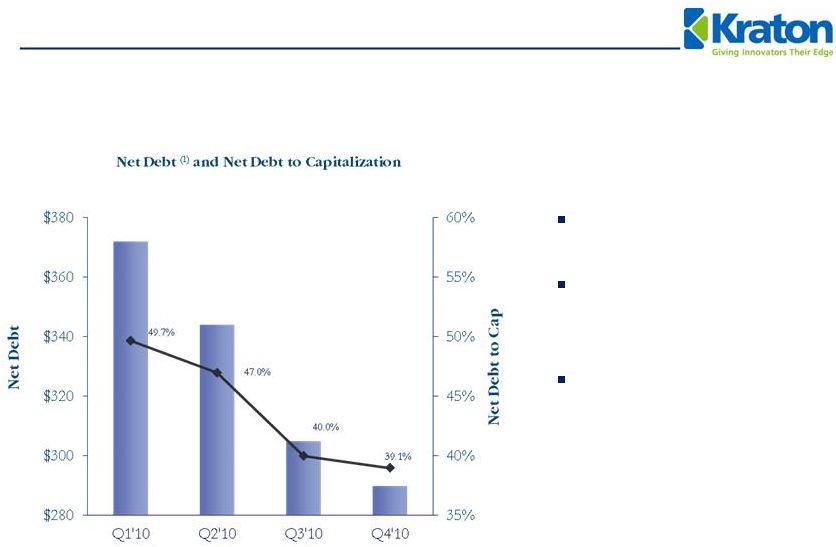

US $

in millions 16

Cash at year end of $93

million.

Net Debt-to-Capitalization

ratio of 39.1% at quarter

end.

Net Debt to Adjusted

EBITDA was 1.49x at

12/31/10.

(1)

Net debt is equal to Long-term debt, less Cash and Cash equivalents.

Balance Sheet |

Debt

Refinancing Increased Liquidity

Attractive Interest Rate

Environment

Old Notes

8.125%

New Notes

6.750%

Extended Maturities

17

Old Revolver

$80 Million

New Revolver

$200 Million

Accordion Feature

$125 Million

Required Payments ($US Millions)

2011

2012

2013

2014

2015+

Old

$2

$109

$108

$163

---

New*

$8

$ 8

$ 11

$ 15

$358

* New bonds mature 2019 |

Selected 2011 Estimates

Working capital (excluding cash) as a % of

revenue

25% to 27%

Capital spending

$80 to $85 million

Interest expense

(1)

~$31 million

Research & development

~$27 million

SG&A

~ $93 million

Depreciation and amortization

~$61 million

Book tax rate

(2)

~9%

18

(1)

Includes

accelerated

write-off

of

deferred

financing

costs

associated

with

the

debt

refinancing

of

$5

million. Total non-recurring items associated with the refinancing were $9

million. (2)

Q1 2011 currently expected to be ~ 14%. |

March 3, 2011

Appendix |

Reconciliation of Net Income/(Loss) to EBITDA and

Adjusted EBITDA

20

US $ in Thousands

Three months Ended

Three months Ended

Twelve months Ended

Twelve months Ended

12/31/2010

12/31/2009

12/31/2010

12/31/2009

Net Income (Loss)

$

10,299

$

(1,516)

$

96,725

$

(290) Add(deduct):

Interest expense, net

5,506

9,179

23,969

33,956

Income tax expense

960

(882)

15,133

(1,367)

Depreciation and amortization expenses

13,178

25,169

49,220

66,751

EBITDA

(1)

$

29,943

$

31,950

$

185,047

$

99,050 EBITDA

(1)

$

29,943

$

31,950

$

185,047

$

99,050 Add(deduct):

Management fees and expenses

-

500

-

2,000

Restructuring and related charges

3,732

2,143

6,387

9,677

Other non-cash expenses

636

451

3,472

4,463

Gain on extinguishment of debt

-

-

-

(23,831)

Adjusted

EBITDA

(2)

$

34,311

$

35,044

$

194,884

$

91,359 Restructuring and related

detail: Cost of goods sold

$

-

$

440 6,107

6,747

Research and development

-

-

-

-

Selling, general and administrative

2,717

1,703

5,371

2,930

Total restructuring and related charges

$

1,864

$

2,144

$

6,427

$

9,677 (1) The EBITDA measure is used by management to evaluate

operating performance. Management believes that EBITDA is useful to investors because it is frequently used by investors and

other interested parties in the evaluation of companies in our

industry. EBITDA is not a recognized term under GAAP and

does not purport to be an alternative to net income (loss) as an indicator of operating performance or to cash flows from operating

activities as a measure of liquidity. Since not all companies use

identical calculations, this presentation of EBITDA may not be comparable to other similarly titled measures of other

companies. Additionally, EBITDA is not intended to be a measure of free

cash flow for management's discretionary use, as it does not consider certain cash requirements such as interest

payments, tax payments and debt service requirements.

(2) Adjusted EBITDA is EBITDA excluding

management fees, restructuring and related charges, non-cash expenses, and the gain on extinguishment of debt. |

March 3, 2011

Kraton Performance Polymers, Inc.

Fourth Quarter 2010 Earnings Conference Call |