Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2010.

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to ________.

Commission File Number 0-25236

MICREL, INCORPORATED

(Exact name of Registrant as specified in its charter)

|

California

|

94-2526744

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

2180 Fortune Drive, San Jose, CA 95131

(Address of principal executive offices) (Zip Code)

Registrant's telephone number, including area code: (408) 944-0800

Securities registered pursuant to Section 12(b) of the Act: Common Stock, no par value

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files. Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. Large accelerated filer ¨ Accelerated filer x Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of June 30, 2010, the aggregate market value of the voting stock held by non-affiliates of the Registrant was approximately $364 million based upon the closing sales price of the Common Stock as reported on the Nasdaq National Market on such date. Shares of Common Stock held by officers, directors and holders of more than ten percent of the outstanding Common Stock have been excluded from this calculation because such persons may be deemed to be affiliates. The determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of February 22, 2011, the Registrant had outstanding 61,963,755 shares of Common Stock.

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the Registrant’s Proxy Statement for its Annual Meeting of Shareholders to be held on May 26, 2011 are incorporated by reference in Part II and Part III of this Report.

MICREL, INCORPORATED

INDEX TO

ANNUAL REPORT ON FORM 10-K

FOR YEAR ENDED DECEMBER 31, 2010

|

Page

|

||

|

PART I

|

||

|

Item 1.

|

3

|

|

|

Item 1A.

|

14

|

|

|

Item 1B.

|

22

|

|

|

Item 2.

|

22

|

|

|

Item 3.

|

22

|

|

|

Item 4.

|

[Removed and Reserved]

|

22

|

|

PART II

|

||

|

Item 5.

|

23

|

|

|

Item 6.

|

26

|

|

|

Item 7.

|

27

|

|

|

Item 7A.

|

41

|

|

|

Item 8.

|

41

|

|

|

Item 9.

|

41

|

|

|

Item 9A.

|

42

|

|

|

Item 9B.

|

43

|

|

PART III

|

||

|

Item 10.

|

44

|

|

|

Item 11.

|

44

|

|

|

Item 12.

|

45

|

|

|

Item 13.

|

45

|

|

|

Item 14.

|

45

|

|

|

PART IV

|

||

|

Item 15.

|

46

|

|

|

76

|

||

|

77

|

||

PART I

|

BUSINESS

|

The statements contained in this Report on Form 10-K that are not purely historical are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, as amended, including statements regarding the Company’s expectations, hopes, intentions or strategies regarding the future. Forward-looking statements include, but are not limited to statements regarding: future revenues and dependence on standard products sales and international sales; the levels of international sales; the effect of global market conditions on revenue levels, profitability and results of operations: future products or product development; statements regarding fluctuations in the Company’s results of operations; future returns and price adjustments and allowance; future uncollectible amounts and doubtful accounts allowance; future products or product development; future research and development spending and the Company’s product development strategy; the Company’s markets, product features and performance; product demand and inventory to service such demand; competitive threats and pricing pressure; the effect of dependence on third parties; the Company’s future use and protection of its intellectual property; future expansion or utilization of manufacturing capacity; future expenditures; current or future acquisitions; the ability to meet anticipated short term and long term cash requirements; effect of changes in market interest rates on investments; the Company’s need and ability to attract and retain certain personnel; the cost and outcome of litigation and its effect on the Company; the future realization of tax benefits; and share based incentive awards and expectations regarding future stock based compensation expense. In some cases, forward-looking statements can be identified by the use of forward-looking terminology such as "believe," "estimate," "may," "can," "will," "could," "would," "intend," "objective," "plan," "expect," "likely," "potential," "possible" or "anticipate" or the negative of these terms or other comparable terminology. All forward-looking statements included in this document are based on information available to the Company on the date of this report, and the Company assumes no obligation to update any such forward-looking statements, - including those risks discussed under "Risks Factors" and elsewhere in this document. These statements are subject to risks and uncertainties that could cause actual results and events to differ materially from those expressed or implied by such forward-looking statements. Some of the factors that could cause actual results to differ materially are set forth in Item 1 ("Business"), Item 1A ("Risk Factors"), Item 3 ("Legal Proceedings") and Item 7 ("Management's Discussion and Analysis of Financial Condition and Results of Operations".

General

The Company was incorporated in California in July 1978. References to the ''Company'' and ''Micrel'' refer to Micrel, Incorporated and subsidiaries, which also does business as Micrel Semiconductor. The Company's principal executive offices are located at 2180 Fortune Drive, San Jose, California 95131. The Company's telephone number is (408) 944-0800. The Company maintains a corporate website located at www.micrel.com. The Company's annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports are made available, free of charge, on the website noted above as soon as reasonably practicable after filing with or being furnished to the Securities and Exchange Commission.

Micrel designs, develops, manufactures and markets a range of high-performance analog power integrated circuits ("ICs"), mixed-signal ICs and digital ICs. The Company currently ships approximately 3000 standard products. These products address a wide range of end markets including cellular handsets, portable computing, enterprise and home networking, wide area and metropolitan area networks, digital televisions and industrial equipment. For the years ended December 31, 2010, 2009, and 2008, the Company's standard products accounted for 97%, 97%, and 95%, respectively, of the Company's net revenues. The Company also manufactures custom analog and mixed-signal circuits and provides wafer foundry services for customers who produce electronic systems for communications, consumer and military applications.

The Company’s high performance power management analog products are characterized by high power density and small form factor. The demand for high performance power management circuits has been fueled by the growth of portable communications and computing devices, including for example, cellular handsets, portable media players and notebook computers. The Company also has an extensive power management offering for the networking and communications infrastructure markets including cloud, single-board and enterprise servers, network switches and routers, storage area networks and wireless base stations. Recently, the Company entered the solid state lighting market, and is seeing strength in the emergence of solid state drives and analog switches including USB switches.

The Company’s high bandwidth communications circuits are used primarily for enterprise networks, storage area networks, access networks and metropolitan area networks. With form factor, size reductions, and ease of use critical for system designs, Micrel utilizes innovative packaging and proprietary process technology to address these challenges.

The Company’s family of Ethernet products targets the digital home and industrial/embedded networking markets. This product portfolio consists of physical layer transceivers ("PHY"), Media Access Controllers ("MAC"), switches, and System-On-Chip ("SoC") devices that support various Ethernet protocols supporting communication transmission speeds from 10 Megabits per second to a Gigabit per second.

Industry Background

Analog Circuit, Mixed-Signal and Digital ICs Markets

ICs may be divided into three general categories — digital, analog (also known as ''linear'') and mixed-signal. Digital circuits, such as memory and microprocessors, process information in the form of on-off electronic signals and are capable of implementing only two values, "1" or "0." Analog circuits, such as regulators, converters and amplifiers, process information in the form of continuously varying voltages and currents that have an infinite number of values or states. Analog circuits condition, process, and measure or control real world variables such as current, sound, temperature, pressure or speed. Mixed-signal ICs combine analog and digital functions on one chip.

Analog circuits are used in virtually every electronic system, and the largest markets for such circuits are computers, telecommunications and data communications, industrial equipment, military, consumer and automotive electronics. Because of their numerous applications, analog circuits have a wide range of operating specifications and functions. For each application, different users may have unique requirements for circuits with specific resolution, linearity, speed, power and signal amplitude capability.

Mixed-signal and digital ICs may be divided into six general categories, LSI/MSI logic, data processing, signal processing, memory, FPGA and application specific.

Mixed-signal and digital ICs are used in computer and communication systems and in industrial products. The primary markets for such circuits are consumer, communications, personal and enterprise computer systems, networking and industrial.

As compared with the digital integrated circuit industry, the analog integrated circuit industry has the following important characteristics:

|

·

|

Dependence on Individual Design Teams. The design of analog circuits involves the complex and critical placement of various circuits. Analog circuit design has traditionally been highly dependent on the skills and experience of individual design engineers.

|

|

·

|

Interdependence of Design and Process. Analog designers, especially at companies having their own wafer fabrication facility, are able to select from several wafer fabrication processes in order to achieve higher performance and greater functionality from their designs.

|

|

·

|

Longer Product Cycles and More Stable Pricing. Analog circuits generally have longer product cycles and greater price stability as compared to digital circuits.

|

Analog, mixed-signal and digital ICs are sold to customers as either standard products or custom products.

Recent Trends in Analog Power Management, Mixed-Signal and Digital ICs

Most electronic systems utilize analog circuits to perform power management functions (''power analog circuits'') such as the control, regulation, conversion and routing of voltages and current. The computer and communications markets have emerged as two of the largest markets for power analog circuits. In particular, the recent growth and proliferation of portable, battery-powered devices, such as cellular telephones, digital cameras, portable media players and notebook computers, continue to increase demand and create new technological challenges for power analog circuits.

Cellular telephones, as an example, are composed of components and subsystems that utilize several different voltage levels, require multiple power analog circuits to precisely regulate and control voltage. Manufacturers continue to pack more processing power and functionality into smaller form factors placing severe demands on the battery. To maintain or extend talk times, high performance power management products are required.

The rapid adoption of the Internet for information exchange, in business and consumer markets, has led to a significant increase in the need for broadband communications technology. In recent years, there has been a significant expansion in the number of broadband subscribers for both DSL, cable modem and fiber to the home technologies. The increased bandwidth demand of these users will continue to consume the installed capacity and drive infrastructure upgrades in metropolitan and wide area networks. The additional demand of new wireless services utilizing the transmission of video will further accelerate this trend.

In the networking market, Ethernet has been widely adopted as a communication standard. Ethernet ports are now being provided on equipment ranging from PCs and PC peripherals to other consumer products such as Network Printers, Internet Protocol Set-Top Boxes ("IP-STB"), High-definition ("HD") TV, Blue-Ray DVD players, Personal Video Recorders (PVR), Multimedia Servers, Internet Protocol Phones ("IP-phone"), Analog Telephone Adaptors ("ATA"), Internet Protocol Camera ("IP-camera"), Femto-cell base stations, game consoles, media converters, used to convert signals transmitted optically over fiber to standard cable (copper) and vice versa, and industrial equipment. This is driving rapid growth in both the digital home market to connect multiple PCs and peripherals and the industrial market to connect machinery to central control and monitoring equipment.

Micrel’s Strategy

Micrel seeks to capitalize on the growth opportunities within the high-performance analog, mixed-signal and digital semiconductor markets. The Company's core competencies are its analog design, control theory, packaging and device technology, as well as its in-house wafer fabrication capability. The Company intends to build a leadership position in its targeted markets by pursuing the following strategies:

|

·

|

Served Available Market Expansion: Micrel is presently a trusted partner to key OEMs around the world. The Company intends to use these relationships to increase revenues by providing more products to these key partners. In addition, through collaboration with these key partners, the Company has access to a rich pipeline of new product development innovation opportunities. Through this partnering, the Company now ships approximately 3000 standard products, with net revenues from standard products generating 97% of the Company's total net revenues for the year ended December 31, 2010.

|

|

·

|

Maintain Technological Leadership. Micrel has executed on significant device and process optimizations which have yielded improvements of as much as six times in core specific on resistance ("Rsp") features, improved packaging, and module capability, and improved power density and form factor.

|

|

·

|

Develop/Acquire New Complementary Businesses. The Company seeks to identify complementary business opportunities building on its core strengths in the analog and mixed signal area.

|

|

·

|

Capitalize on In-house Wafer Fabrication Facility. The Company believes that its in-house six-inch wafer fabrication facility provides a significant competitive advantage because it facilitates close collaboration between design and process engineers in the development of the Company's products.

|

|

·

|

Maintain a Strategic Level of Custom and Foundry Products Revenue. Micrel believes that its custom and foundry products business complements its standard products business by generating a broader revenue base and lowering overall per unit manufacturing costs through greater utilization of its manufacturing facilities.

|

|

·

|

Protect Proprietary Technology. The Company seeks to identify and protect its proprietary technology through the acquisition of patents, trademarks and copyrights.

|

Products and Markets

Overview

The following table sets forth the net revenues attributable to the Company's two segments, standard products and other products, consisting primarily of custom and foundry products revenues and revenues from the license of patents, expressed in dollars and as a percentage of total net revenues.

|

Net Revenues by Segment (Dollars in thousands)

|

||||||||||||

|

Years Ended December 31,

|

||||||||||||

|

Net Revenues:

|

||||||||||||

|

Standard Products

|

$ | 289,347 | $ | 212,606 | $ | 246,644 | ||||||

|

Other Products

|

8,019 | 6,281 | 12,716 | |||||||||

|

Total net revenues

|

$ | 297,366 | $ | 218,887 | $ | 259,360 | ||||||

|

As a Percentage of Total Net Revenues:

|

||||||||||||

|

Standard Products

|

97 | % | 97 | % | 95 | % | ||||||

|

Other Products

|

3 | 3 | 5 | |||||||||

|

Total net revenues

|

100 | % | 100 | % | 100 | % | ||||||

The following table presents the Company’s revenues by product line, as a percentage of total net revenues.

|

Net Revenues by Product Line

|

||||||||||||

|

Years Ended December 31,

|

||||||||||||

|

2010

|

2009

|

2008

|

||||||||||

|

As a Percentage of Total Net Revenues:

|

||||||||||||

|

Standard Products:

|

||||||||||||

|

Analog

|

62 | % | 67 | % | 65 | % | ||||||

|

High bandwidth

|

17 | 14 | 15 | |||||||||

|

Ethernet

|

18 | 16 | 15 | |||||||||

|

Total standard products

|

97 | 97 | 95 | |||||||||

|

Foundry, custom and other

|

3 | 3 | 5 | |||||||||

|

Total net revenues

|

100 | % | 100 | % | 100 | % | ||||||

The Company's products address a wide range of end markets. The following table presents the Company's revenues by end market as a percentage of total net revenues.

|

Net Revenues by End Market

|

Years Ended December 31,

|

|||||||||||

|

2010

|

2009

|

2008

|

||||||||||

|

As a Percentage of Total Net Revenues:

|

||||||||||||

|

Industrial

|

39 | % | 36 | % | 37 | % | ||||||

|

High-Speed Communications

|

31 | 28 | 26 | |||||||||

|

Wireless Handsets

|

12 | 16 | 19 | |||||||||

|

Computer

|

15 | 15 | 15 | |||||||||

|

Military & Other

|

3 | 5 | 3 | |||||||||

|

Total net revenues

|

100 | % | 100 | % | 100 | % | ||||||

For a discussion of the changes in net revenues from period to period, see ''Management's Discussion and Analysis of Financial Condition and Results of Operations.''

Standard Products

In recent years, the Company has directed a majority of its development, sales and marketing efforts towards standard products in an effort to address the larger markets for these products and to expand its customer base. The Company offers a broad range of high performance analog, mixed signal, and digital ICs that address high growth markets including cellular telephones, portable electronics, set-top boxes, desktop and notebook computers, networking and communications. The majority of the Company's revenue is derived from power management standard products that, in addition to the above markets, are also used in the industrial, consumer, defense, and automotive electronics markets.

Power Conversion Market. Most electronic equipment includes a power supply that converts and regulates the electrical power source into usable voltage for the equipment. Micrel has multiple power conversion families:

|

·

|

LDOs – LDOs have long been a cornerstone of Micrel’s product offering. LDOs are linear voltage regulators which allow lower voltage devices to be connected to higher voltage power rails. The Company offers numerous LDOs products ranging from low cost portable regulators, to high performance (tight accuracy) high current regulators with supervisory functions.

|

|

·

|

DC/DC converters – The Company’s DC/DC converter products are offered in controller (no switch) and regulator (switches on board) form. Competitive advantages include power density, high voltage capability, and small form factor. The devices are primarily used in solid state drives, cloud servers, networking, portable equipment and base stations.

|

|

·

|

Analog Power Switches – Micrel offers analog switches that range from straight current switching to reverse blocking, current protected and soft start devices with supervisory options. The devices are primarily used in LCD TV, computer USB port and cell phone devices. In addition, the Company offers a family of hot swap controllers including second sources of leading competitive devices which appeal primarily to the networking and telecom markets.

|

|

·

|

PMICs – PMICs combine supervisor, DC/DC, LDO and interfacing requirements in a single IC to save space and cost. The Company has introduced many PMIC devices for key applications ranging from graphics processors to LTE dongles.

|

|

·

|

RF PA bias – Micrel offers digitally controlled output voltage DC/DC converters for power amplifier communications biasing. The devices are primarily used in portable wireless equipment and cell phones. The Company continues to collaborate with its key customers to expand this product offering.

|

|

·

|

Solid State Lighting – Micrel offerings include LED drivers for the portable and non-portable backlighting markets, as well as drivers for solid state architectural and general illumination. These products have been adopted by portable equipment and cell phone manufacturers as an alternative to more costly charge pump solutions.

|

|

·

|

FET Drivers – Micrel produces buffers which allow DC/DC controllers to interface to external switches and provide the power needed to drive these switches.

|

Supervisory Market. Micrel offers supervisory and reference products which protect, monitor and improve the interface of circuitry, especially around microcontroller and processor circuits. Demand for products in this area has been driven by needs in the portable cell phone market to improve interaction between memory and processor segments as well as numerous tracking, sequencing, and monitoring requirements in various networking industrial and portable applications.

General Linear. Micrel offerings include a line of general linear parts ranging from opamps, to thermal measurement devices, timers and other general devices. These types of devices tend to be deployed in many analog circuits to improve operation.

Portable Battery-Powered Computer Market. The Company makes power analog circuits for notebook computers, tablet PCs, and PDAs. Products in this growing market are differentiated on the basis of power efficiency, weight, small size and battery life.

Radio Frequency Data Communications. Micrel's QwikRadio® family of RF receivers and transmitters are designed for use in any system requiring a cost-effective, low-data-rate wireless link. Typical examples include garage door openers, lighting and fan controls, automotive keyless entry and remote controls. Micrel's RadioWire® transceivers provide a higher level of performance for more demanding applications such as remote metering, security systems and factory automation.

Networking and High-Speed Communications Market. The Company's High Bandwidth division develops and produces high speed Physical Media Devices ("PMD") and interface integrated circuits for communications products targeted at fiber optic modules, active cables, backplane management, data and clock management applications.

Ethernet Communications. Micrel's Ethernet division offers a broad range of PHY, MAC, Switch and SoC products for the 10/100/1000 Megabit Ethernet standard. The primary applications for the products are Digital Home Networks, Enterprise, and other Industrial/Embedded Ethernet systems.

The Company's future success will depend in part upon the timely completion, introduction, and market acceptance of new standard products. The standard products business can be characterized as having shorter product lifecycles, greater pricing pressure, larger competitors and more rapid technological change as compared to the Company's custom and foundry products business.

Other Products

Micrel offers various combinations of design, process and foundry services in order to provide customers with the following alternatives:

R&D Foundry. Micrel modifies a process or develops a new process for a customer. Using that process and mask sets provided by the customer, Micrel manufactures fabricated wafers for the customer.

Foundry. Micrel duplicates a customer's process to manufacture fabricated wafers designed by the customer.

Sales, Distribution and Marketing

The Company sells its products through a worldwide network of independent sales representative, independent distributor and stocking representative firms and through direct sales staff.

The Company sells its products in Europe through direct sales staff in the United Kingdom, Germany and France as well as independent sales representative firms, independent distributors and independent stocking representative firms. Asian sales are handled through Micrel sales offices in Korea, Japan, Taiwan, China and Singapore, independent distributors and independent stocking representative firms. The stocking representative firms may buy and stock the Company's products for resale or may act as the Company's sales representative in arranging for direct sales from the Company to an original equipment manufacturer ("OEM") customer.

In 2010, sales to customers in North America, Asia and Europe accounted for 27%, 60% and 13%, respectively, of the Company's net revenues. In 2009, North America, Asia and Europe accounted for 26%, 61% and 13%, respectively, of the Company's net revenues and in 2008, North America, Asia and Europe accounted for 30%, 56% and 14%%, respectively, of the Company's net revenues. The Company's standard products are sold throughout the world, while its custom and foundry products are primarily sold to North American customers. The Company's net revenues by country, including the United States, are included in Note 12 of Notes to Consolidated Financial Statements.

The Company's international sales are primarily denominated in U.S. dollars. Consequently, changes in exchange rates that strengthen the U.S. dollar could increase the price in local currencies of the Company's products in foreign markets and make the Company's products relatively more expensive than competitors' products that are denominated in local currencies, leading to a reduction in sales or profitability in those foreign markets. The Company has not taken any protective measures against exchange rate fluctuations, such as purchasing hedging instruments with respect to such fluctuations.

Customers

For the year ended December 31, 2010, no OEM customer accounted for more than 10% of the Company's net revenues and two worldwide distributors accounted for 19% and 17%, respectively, of the Company's net revenues. For the year ended December 31, 2009, one OEM customer accounted for 12% of the Company's net revenues and two worldwide distributors accounted for 19% and 13%, respectively, of the Company's net revenues. For the year ended December 31, 2008, no OEM customer accounted for more than 10% of the Company's net revenues and one worldwide distributor, accounted for 13% of the Company's net revenues.

Design and Process Technology

Micrel's analog proprietary design technology depends on the skills of its analog design teams. These teams rely on a state of the art Cadence framework, with an emphasis on circuit innovation, control theory and mathematical rigor. Additionally, the Company’s unique device, packaging and testing capabilities allow it to compete on a variety of advantages.

In order for Micrel to compete, it must provide process technologies that are uniquely suited for the products it develops. In the case of Micrel’s Analog business, we are recognized as a technology leader and therefore our process technologies must be state of the art and cost effective.

Micrel recently introduced its world class BCD0.35 technology, and continues to implement many new designs on its CSI0.5 and BCD0.5 processes. These processes are characterized by a rich array on analog device including analog resistors and capacitors, post package trim, optimized ESD, high voltage structures, optimized specific on resistance, true bipolar and in some processes true power bipolar capability at key nodes including 3.3V, 5V and 12V, and BCD capability to 65V. In addition, the Company has unique copper pillar, thick aluminum and copper conduction metals, CSP and thermal pad process capabilities. These capabilities give the Company an advantage compared with many competitors using a fabless model as these simultaneous capabilities are generally not available at most third party foundries.

Additionally Micrel has an array of BCD1.2u and CSI1.2u and above processes, as well as high speed Silicon Germanium capability.

The Company utilizes third-party wafer fabrication foundries for advanced CMOS fabrication processes and other advanced processes that are not available in-house. For the year ended December 31, 2010, approximately 11% of Micrel's wafer requirements were fabricated at third-party foundry suppliers, including all of Micrel's Ethernet networking products.

Research and Development

The ability of the Company to compete will substantially depend on its ability to define, design, develop and introduce on a timely basis new products offering design or technology innovations. Research and development in the analog and mixed-signal integrated circuit industry is characterized primarily by circuit design and product engineering that enables new functionality or improved performance. The Company's research and development efforts are also directed at its process technologies and focus on cost reductions to existing manufacturing processes and the development of new process capabilities to manufacture new products and add new features to existing products. With respect to more established products, the Company's research and development efforts also include product redesign, shrinkage of device size and the reduction of mask steps in order to improve die yields per wafer and reduce per device costs.

The Company's analog, mixed-signal and digital design engineers principally focus on developing next generation standard products for the Company’s targeted markets. The Company's new product development strategy emphasizes a broad line of standard products that are based on customer input and requests.

In 2010, 2009, and 2008, the Company spent $46.3 million, $46.5 million, and $54.9 million, respectively, on research and development. The Company expects that it will continue to spend substantial funds on research and development activities.

Patents and Intellectual Property Protection

The Company seeks patent protection for those inventions and technologies for which such protection is suitable and is likely to provide a competitive advantage to the Company. The Company currently holds 302 United States patents on semiconductor devices and methods, with various expiration dates through 2029. The Company has applications for 47 United States patents pending. The Company holds 54 issued foreign patents and has applications for 67 foreign patents pending.

Supply of Materials and Purchased Components

Micrel currently purchases certain components from a limited group of vendors. The packaging of the Company's products is performed by, and certain of the raw materials included in such products are obtained from, a limited group of suppliers. The wafer supply for the Company’s Ethernet products is primarily dependent upon two large third-party wafer foundry suppliers.

Manufacturing

The Company produces the majority of its wafers at the Company’s wafer fabrication facility located in San Jose, California while a small percentage of wafer fabrication is subcontracted to outside foundries, including 100% of Micrel's Ethernet product wafer requirements. The San Jose facility includes a 57,000 square foot office and manufacturing facility containing a 28,000 square foot clean room facility, which provides production processes. Approximately 70% of the San Jose facility's clean room space is classified as a Class 1 facility, which means that the facility achieves a clean room level of fewer than 1 foreign particle larger than 0.3 microns in size in each cubic foot of space. The remainder of the facility's clean room space is classified as Class 10, achieving fewer than 10 foreign particles larger than 0.3 microns in size in each cubic foot of space. The facility uses six-inch wafer technology. The Company also owns approximately 63,000 square feet of additional adjacent space in San Jose that is used as a testing facility and administrative offices.

Generally, each die on the Company's wafers is electrically tested for performance, and most of the wafers are subsequently sent to independent assembly and final test contract facilities in Malaysia and certain other Asian countries. At such facilities, the wafers are separated into individual circuits and packaged.

Competition

The semiconductor industry is highly competitive and subject to rapid technological change. Significant competitive factors in the market for standard products include product features, performance, price, the timing of product introductions, the emergence of new technological standards, quality and customer support. The Company believes that it competes favorably in all of these areas.

The standard products market for analog ICs is diverse and highly fragmented and the Company encounters different competitors in its various market areas. The Company's principal analog circuit competitors include Linear Technology Corporation, Maxim Integrated Products, Inc., and National Semiconductor Corp. in one or more of its product areas. Other competitors include Texas Instruments, Freescale Semiconductor, Intersil, Fairchild Semiconductor, Advanced Analogictech, Semtech and ON Semiconductor. Most of these companies have substantially greater technical, financial and marketing resources and greater name recognition than the Company. The Company's principal competitors for products targeted at the high bandwidth communications market are ON Semiconductor, Analog Devices, Maxim Integrated Products, Inc., Vitesse Semiconductor Corp., Integrated Device Technology and Mindspeed. The primary competitors for Micrel's Ethernet products are Broadcom Corp., Marvell Technology Group Ltd. and a number of Taiwanese companies.

With respect to the custom and foundry products business, significant competitive factors include product quality and reliability, established relationships between customers and suppliers, timely delivery of products, and price. The Company believes that it competes favorably in all these areas.

Backlog

At December 31, 2010, the Company's backlog was approximately $89 million, substantially all of which is scheduled to be shipped during the first six months of 2011. At December 31, 2009, backlog was approximately $77 million. Orders in backlog are subject to cancellation or rescheduling by the customer, generally with a cancellation charge in the case of custom and foundry products. The Company's backlog consists of distributor and customer released orders requesting shipment within the next six months. Shipments to United States, Canadian and certain other international distributors who receive significant return rights and price adjustments from the Company are not recognized as revenue by the Company until the product is sold from the distributor stock and through to the end-users. Because of possible changes in product delivery schedules and cancellation of product orders and because an increasing percentage of the Company's sales are shipped in the same quarter that the orders are received, the Company's backlog at any particular date is not necessarily indicative of actual sales for any succeeding period.

Environmental Matters

Federal, state and local regulations impose various environmental controls on the storage, handling, discharge and disposal of chemicals and gases used in the Company's manufacturing process. The Company believes that its activities conform to present environmental regulations.

Employees

As of December 31, 2010, the Company had 837 full-time employees as compared to 755 at December 31, 2009. The Company's employees are not represented by any collective bargaining agreements, and the Company has never experienced a work stoppage.

Segment Information

The Company has two reportable segments: standard products and other product revenues, which consist primarily of custom and foundry products revenues. Segment financial information is presented in Note 12 of Notes to the Consolidated Financial Statements, which is incorporated by reference here.

ITEM 1A. RISK FACTORS

Factors That May Affect Operating Results

If a company’s operating results are below the expectations of public market analysts or investors, then the market price of its Common Stock could decline. Many factors that can affect a company’s quarterly and annual results are difficult to control or predict. Some of the factors which can affect a multinational semiconductor business such as the Company are described below.

Geopolitical and Macroeconomic Risks That May Affect Multinational Enterprises

Weak global economic conditions could have a material adverse effect on the Company’s business, results of operations, and financial condition. While the global economy has partially recovered from the recent economic downturn and the Company has seen improvement in the business climate for semiconductors, there is no guarantee that these conditions will continue to improve or that these conditions will not further decline again in the future. The semiconductor industry has traditionally been highly cyclical and has often experienced significant downturns in connection with, or in anticipation of, declines in general economic conditions. The Company cannot accurately predict the timing, severity or duration of such downturns. A global recession may result in a decrease in orders for the Company’s products, which may materially adversely affect the Company’s revenues, results of operations and financial condition. In addition to reduction in sales, the Company’s profitability may decrease during economic downturns because the Company may not be able to reduce costs at the same rate as its sales decline.

Demand for semiconductor components is increasingly dependent upon the rate of growth of the global economy. Many factors could adversely affect regional or global economic growth. Some of the factors that could slow global economic growth include: volatility in global credit markets, price inflation or deflation for goods, services or materials, a slowdown in the rate of growth of the Chinese economy, a significant act of terrorism which disrupts global trade or consumer confidence, and geopolitical tensions including war and civil unrest. Reduced levels of economic activity, or disruptions of international transportation, could adversely affect sales on either a global basis or in specific geographic regions. For example, recent forecasts suggest a decline in the rate of U.S. economic growth in early 2011, which may impact the growth rate of the semiconductor industry including Micrel. Furthermore, although during 2010 the partial economic recovery contributed to higher than average growth in the semiconductor industry, as the semiconductor industry returns to its normal trend line the growth rate may decline. A slowdown in semiconductor growth rates may exacerbate a near-term slowdown in semiconductor bookings as lead times return to historic levels.

Market conditions may lead the Company to initiate cost reduction plans, which may negatively affect near term operating results. Weaker customer demand, competitive pricing pressures, excess capacity, weak economic conditions or other factors, may cause the Company to initiate actions to reduce the Company’s cost structure to improve the Company’s future operating results. The cost reduction actions may require incremental costs to implement, which could negatively affect the Company’s operating results in periods when the incremental costs or liabilities are incurred.

Tightening of the credit markets may adversely affect the Company’s business in a number of ways. The unprecedented contraction and extreme disruption of the credit and financial markets in the United States, Europe, and Asia led to, among other things, extreme volatility in security prices, severely diminished liquidity and credit availability, rating downgrades of certain investments and declining valuation of others. These economic developments adversely affected the Company’s business in a number of ways. A similar tightening of credit in financial markets may limit the ability of the Company’s customers and suppliers to obtain financing for capital purchases and operations. This could result in a decrease in or cancellation of orders for the Company’s products or reduced ability to finance operations to supply products to the Company. The Company cannot predict the likely duration and severity of disruptions in financial markets and adverse economic conditions in the U.S. and other countries. Further, fluctuations in worldwide economic conditions make it is extremely difficult for the Company to forecast future sales levels based on historical information and trends. Visibility into customer demand is limited due to short order lead times. Portions of the Company’s expenses are fixed and other expenses are tied to expected levels of sales activities. To the extent the Company does not achieve its anticipated levels of sales, its gross profit and net income could be adversely affected until such expenses are reduced to an appropriate level.

The Company has generated a substantial portion of its net revenues from export sales. The Company believes that a substantial portion of its future net revenues will depend on export sales to customers in international markets, including Asia. International markets are subject to a variety of risks, including changes in policy by the U.S. or foreign governments, acts of terrorism, foreign government instability, social conditions such as civil unrest, economic conditions including high levels of inflation or deflation, fluctuation in the value of foreign currencies and currency exchange rates and trade restrictions or prohibitions. Changes in exchange rates that strengthen the U.S. dollar could increase the price of the Company’s products in the local currencies of the foreign markets it serves. This would result in making the Company’s products relatively more expensive than its competitors’ products that are denominated in local currencies, leading to a reduction in sales or profitability in those foreign markets. The Company has not taken any protective measures against exchange rate fluctuations, such as purchasing hedging instruments. In addition, the Company sells to domestic customers that do business worldwide and cannot predict how the businesses of these customers may be affected by economic or political conditions elsewhere in the world. Such factors could adversely affect the Company’s future revenues, financial condition, results of operations or cash flows.

Semiconductor Industry Specific Risks

The volatility of customer demand in the semiconductor industry limits a company’s ability to predict future levels of sales and profitability. Semiconductor suppliers can rapidly increase production output, leading to a sudden oversupply situation and a subsequent reduction in order rates and revenues as customers adjust their inventories to true demand rates. A rapid and sudden decline in customer demand for products can result in excess quantities of certain products relative to demand. Should this occur the Company’s operating results may be adversely affected as a result of charges to reduce the carrying value of the Company’s inventory to the estimated demand level or market price. The Company’s quarterly revenues are highly dependent upon turns fill orders (orders booked and shipped in the same quarter). The short-term and volatile nature of customer demand makes it extremely difficult to accurately predict near term revenues and profits.

The semiconductor industry is highly competitive and subject to rapid technological change, price-erosion and increased international competition. Significant competitive factors include product features; performance and price; timing of product introductions; emergence of new computer and communications standards; and quality and customer support. If the Company is unable to compete favorably in these areas, revenues and profits could be negatively affected.

The short lead time environment in the semiconductor industry has allowed many end consumers to rely on semiconductor suppliers, stocking representatives and distributors to carry inventory to meet short-term requirements and minimize their investment in on-hand inventory. Over the past several years, customers have worked to minimize the amount of inventory of semiconductors they hold. As a consequence, customers are generally providing less order backlog to the Company and other semiconductor suppliers, resulting in short order lead times and reduced visibility into customer demand. As a consequence of the short lead time environment and corresponding unpredictability of customer demand, the Company has increased its inventories over the past five to six years to maintain reliable service levels. If actual customer demand for the Company’s products is different from the Company’s estimated demand, delivery schedules may be impacted, product inventory may have to be scrapped, or the carrying value reduced, which could adversely affect the Company’s business, financial condition, results of operations, or cash flows. In addition, the Company maintains a network of stocking representatives and distributors that carry inventory to service the volatile short-term demand of the end customer. Should the relationship with a distributor or stocking representative be terminated, the future level of product returns could be higher than the returns allowance established, which could negatively affect the Company’s revenues and results of operations.

During periods when economic growth and customer demand have been less certain, both the semiconductor industry and the Company have experienced significant price erosion. If price erosion occurs, it will have the effect of reducing revenue levels and gross margins in future periods. Furthermore, the trend for the Company’s customers to move their electronics manufacturing to Asian countries has brought increased pricing pressure for Micrel and the semiconductor industry as a whole. Asian based manufacturers are typically more concerned about cost and less concerned about the capability of the integrated circuits they purchase. The increased concentration of electronics procurement and manufacturing in the Asia Pacific region may lead to continued price pressure and additional product advertising costs for the Company’s products in the future.

Many semiconductor companies, including the Company, face risks associated with a dependence upon third parties that manufacture, assemble or package certain of its products. These risks include reduced control over delivery schedules and quality; inadequate manufacturing yields and excessive costs; the potential lack of adequate capacity during periods of excess demand; difficulties selecting and integrating new subcontractors; potential increases in prices; disruption in supply due to civil unrest, terrorism, natural disasters or other events which may occur in the countries in which the subcontractors operate; and potential misappropriation of the Company’s intellectual property. The occurrence of any of these events may lead to increased costs or delay delivery of the Company’s products, which would harm its profitability and customer relationships. The Company does not have long-term supply contracts with any of its third-party vendors. Therefore, the vendors are not obligated to perform services or supply products to the Company for any specific period, in any specific quantities, or at any specific price, except as may be provided in a particular accepted purchase order or guarantee. Additionally, the Company’s wafer and product requirements typically represent a relatively small portion of the total production of the third-party foundries and outside assembly, testing and packaging contractors. As a result, the Company is subject to the risk that a third-party supplier will provide delivery or capacity priority to other larger customers at the expense of the Company, resulting in an inadequate supply to meet customer demand or higher costs to obtain the necessary product supply.

The Company outsources some of its wafer fabrication, most of its test and all of its assembly requirements to third-party vendors. When demand for semiconductors improves, availability of these outsourced services typically becomes tight, resulting in longer than normal lead times and delinquent shipments to customers. The degree to which Micrel may have difficulty obtaining these services could have a negative impact on the Company’s revenues, bookings and backlog. If these lead times are extended, the resulting loss of near-term visibility for our customers could result in their placing higher order levels than their actual requirements which may result in higher levels of order cancellations in the future. There can be no assurance that the Company will be able to accurately forecast demand and moderate its build schedules to accommodate the possibility of an increase in order cancellations.

The markets that the Company serves frequently undergo transitions in which products rapidly incorporate new features and performance standards on an industry-wide basis. If the Company’s products are unable to support the new features or performance levels required by OEMs in these markets, it would likely lose business from existing or potential customers and would not have the opportunity to compete for new design wins until the next product transition. If the Company fails to develop products with required features or performance standards or experiences even a short delay in bringing a new product to market, or if its customers fail to achieve market acceptance of their products, its revenues could be significantly reduced for a substantial period of time.

Because the standard products market for ICs is diverse and highly fragmented, the Company encounters different competitors in various market areas. Many of these competitors have substantially greater technical, financial and marketing resources and greater name recognition than the Company. The Company may not be able to compete successfully in either the standard products or custom and foundry products businesses in the future and competitive pressures may adversely affect the Company’s financial condition, results of operations, or cash flows.

The success of companies in the semiconductor industry depends in part upon intellectual property, including patents, trade secrets, know-how and continuing technology innovation. The success of companies like Micrel may depend on their ability to obtain necessary intellectual property rights and protect such rights. There can be no assurance that the steps taken by the Company to protect its intellectual property will be adequate to prevent misappropriation or that others will not develop competitive technologies or products. There can be no assurance that any patent owned by the Company will not be invalidated, circumvented or challenged, that the rights granted thereunder will provide competitive advantages or that any of its pending or future patent applications will be issued with the scope of the claims sought, if at all. Furthermore, others may develop technologies that are similar or superior to the Company’s technology, duplicate technology or design around the patents owned by the Company. Additionally, the semiconductor industry is characterized by frequent litigation regarding patent and other intellectual property rights. Claims alleging infringement of intellectual property rights have been asserted against the Company in the past and could be asserted against the Company in the future. These claims could result in the Company having to discontinue the use of certain processes or designs; cease the manufacture, use and sale of infringing products; incur significant litigation costs and damages; attempt to obtain a license to the relevant intellectual property and develop non-infringing technology. The Company may not be able to obtain or renew such licenses on acceptable terms or to develop non-infringing technology. Existing claims or other assertions or claims for indemnity resulting from infringement claims could adversely affect the Company’s business, financial condition, results of operations, or cash flows. In addition, the Company relies on third parties for certain technology that is integrated into some of its products. If the Company is unable to continue to use or license third-party technologies in its products on acceptable terms, or the technology fails to operate, the Company may not be able to secure alternative technologies in a timely manner and its business would be harmed.

The significant investment in semiconductor manufacturing capacity and the rapid growth of circuit design centers in China may present a competitive threat to established semiconductor companies due to the current low cost of labor and capital in China. The emergence of low cost competitors in China could reduce the revenues and profitability of established semiconductor manufacturers.

There is intense competition for qualified personnel in the semiconductor industry. The loss of any key employees or the inability to attract or retain qualified personnel, including management, engineers and sales and marketing personnel, could delay the development and introduction of the Company’s products, and harm its ability to sell its products. The Company believes that its future success is dependent on the contributions of its senior management, including its President and Chief Executive Officer, certain other executive officers and senior engineering personnel. The Company does not have long-term employment contracts with these or any other key personnel, and their knowledge of the Company’s business and industry would be difficult to replace.

Companies in the semiconductor industry are subject to a variety of federal, state and local governmental regulations related to the use, storage, discharge and disposal of toxic, volatile or otherwise hazardous chemicals used in its manufacturing process. Any failure to comply with present or future regulations could result in the imposition of fines, the suspension of production, alteration of manufacturing processes or a cessation of operations. In addition, these regulations could restrict the Company’s ability to expand its facilities at their present locations or construct or operate a new wafer fabrication facility or could require the Company to acquire costly equipment or incur other significant expenses to comply with environmental regulations or clean up prior discharges. The Company’s failure to appropriately control the use of, disposal or storage of, or adequately restrict the discharge of, hazardous substances could subject it to future liabilities and could have a material adverse effect on its business.

Company-Specific Risks

In addition to the risks that affect multinational semiconductor companies listed above, there are additional risks which are more specific to the Company such as:

An important part of the Company’s strategy is to continue to focus on the market for high-speed communications ICs. Should demand from the Company’s customers in this end market decrease, or if lower customer demand for the Company’s high bandwidth products materializes, the Company’s future revenue growth and profitability could be adversely affected.

The wireless handset (cellular telephone) market comprises a significant portion of the Company’s standard product revenues. The Company derives a significant portion of its net revenues from customers serving the wireless handset market. Due to the highly competitive and fast changing environment in which the Company’s wireless handset customers operate, demand for the product the Company sells into this end market can change rapidly and unexpectedly. If the Company’s wireless handset customers acceptance of Micrel’s products decreases, or if these customers lose market share, or accumulate too much inventory of completed handsets, the demand for the Company’s products could decline sharply which could adversely affect the Company’s revenues and results of operations.

The Company’s gross margin, operating margin and net income are highly dependent on the level of revenue, average selling prices and capacity utilization that the Company experiences. A decline in average selling prices (“ASPs”) could adversely affect the Company’s revenues, gross margins and results of operations unless the Company is able to sell more units, reduce its costs, and introduce new products with higher ASPs or some combination thereof.

Semiconductor manufacturing is a capital-intensive business resulting in high fixed costs. If the Company is unable to utilize its installed wafer fabrication or test capacity at a high level, the costs associated with these facilities and equipment would not be fully absorbed, resulting in higher average unit costs and lower profit margins.

The Company has invested in certain auction rate securities that may not be accessible for in excess of 12 months and these auction rate securities may experience an other than temporary decline in value, which would adversely affect the Company’s income. At December 31, 2010, the Company held $14.0 million in principal of auction rate notes secured by student loans. As of December 31, 2010, all of these auction rate securities have failed to auction successfully due to sell orders exceeding buy orders. The Company has recorded a $1.8 million pre-tax temporary impairment of these securities to other comprehensive income, a component of shareholders’ equity. If it is determined that the fair value of these securities is other than temporarily impaired, the Company would record a loss, which could be material, in its statement of operations in the period such other than temporary decline in fair value is determined. For additional information regarding the Company’s investments, see Note 1 of Notes to Consolidated Financial Statements.

The Company faces various risks associated with the trend toward increased shareholder activism. In 2008, the Company became engaged in a proxy contest with a large shareholder. This dispute led to a significant increase in operating expenses which appreciably reduced the Company’s operating profit and net income. While this dispute has been resolved, the Company could become engaged in another proxy contest in the future. Another proxy contest would require significant additional management time and increased operating expenses, which could adversely affect the Company’s profitability and cash flows.

The semiconductor industry is characterized by frequent litigation regarding patent and other intellectual property rights. To the extent that the Company becomes involved in such intellectual property litigation, it could result in substantial costs and diversion of resources to the Company and could have a material adverse effect on the Company’s financial condition, results of operation or cash flows.

In the event of an adverse ruling in any intellectual property litigation that might arise in the future, the Company might be required to discontinue the use of certain processes or designs, cease the manufacture, use and sale of infringing products, expend significant resources to develop non-infringing technology or obtain licenses to the infringing technology. There can be no assurance, however, that under such circumstances, a license would be available under reasonable terms or at all. In the event of a successful claim against the Company and the Company’s failure to develop or license substitute technology on commercially reasonable terms, the Company’s financial condition, results of operations, or cash flows could be adversely affected. The Company does not believe that any material and specific risk currently exists related to the loss of use of patents, products or processes.

The complexity of the Company’s products may lead to errors or defects, which could subject the Company to significant costs or damages and adversely affect market acceptance of its products. Although the Company’s customers and suppliers rigorously test its products, these products may contain undetected errors, weaknesses or defects. If any of the Company’s products contain production defects, reliability, quality or compatibility problems that are significant, the Company’s reputation may be damaged and customers may be reluctant to continue to buy its products. This could adversely affect the Company’s ability to retain and attract new customers. In addition, these defects could interrupt or delay sales of affected products, which could adversely affect the Company’s results of operations.

If defects are discovered after commencement of commercial production, the Company may be required to incur significant costs to resolve the problems. This could result in significant additional development costs and the diversion of technical and other resources from other development efforts. The Company could also incur significant costs to repair or replace defective products or may agree to be liable for certain damages incurred. These costs or damages could have a material adverse effect on the Company’s financial condition and results of operations.

The Company will continue to expend substantial resources developing new products, applications or markets and may never achieve the sales volume that it anticipates for these products, which may limit the Company’s future growth and harm its results of operations. The Company’s future success will depend in part upon the success of new products. The Company has in the past, and will likely in the future, expend substantial resources in developing new and additional products for new applications and markets. The Company may experience unforeseen difficulties and delays in developing these products and experience defects upon volume production and broad deployment. The markets the Company enters will likely be highly competitive and competitors may have substantially more experience in these markets. The Company’s success will depend on the growth of the markets it enters, the competitiveness of its products and its ability to increase market share in these markets. If the Company enters markets that do not achieve or sustain the growth it anticipates, or if the Company’s products are not competitive, it may not achieve volume sales, which may limit the Company’s future growth and would harm its results of operations.

If the Company is unable to convert a significant portion of its design wins into revenue, the Company’s business, financial condition and results of operations could be materially and adversely impacted. The Company has secured a significant number of design wins for new and existing products. Such design wins are necessary for revenue growth. However, many of the Company’s design wins may never generate revenues if end-customer projects are unsuccessful in the marketplace or the end-customer terminates the project, which may occur for a variety of reasons. Mergers and consolidations among customers may lead to termination of certain projects before the associated design win generates revenue. If design wins do generate revenue, the time lag between the design win and meaningful revenue is typically from six months to greater than eighteen months. If the Company fails to convert a significant portion of its design wins into substantial revenue, the Company’s business, financial condition and results of operations could be materially and adversely impacted.

If the Company’s distributors or sales representatives stop selling or fail to successfully promote its products, the Company’s business, financial condition and results of operations could be adversely impacted. Micrel sells many of its products through sales representatives and distributors. The Company’s non-exclusive distributors and sales representatives may carry its competitors’ products, which could adversely impact or limit sales of the Company’s products. Additionally, they could reduce or discontinue sales of the Company’s products or may not devote the resources necessary to adequately sell the Company’s products. The Company’s agreements with distributors contain limited provisions for return of products, including stock rotations whereby distributors may return a percentage of their purchases based upon a percentage of their most recent three months of shipments. In addition, in certain circumstances upon termination of the distributor relationship, distributors may return some portion of their prior purchases. The loss of business from any of the Company’s significant distributors or the delay of significant orders from any of them could materially and adversely harm the Company’s business, financial conditions and results of operations.

In addition, the Company depends on the continued viability and financial resources of these distributors and sales representatives, some of which are small organizations with limited working capital. In turn, these distributors and sales representatives are subject to general economic and semiconductor industry conditions. If some or all of the Company’s distributors and sales representatives experience financial difficulties, or otherwise become unable or unwilling to promote and sell the Company’s products, or deliver the Company’s products in a timely manner, its business, financial condition and results of operations could be adversely impacted.

The Company manufactures most of its semiconductors at its San Jose, California fabrication facilities. The Company’s existing wafer fabrication facility, located in Northern California, may be subject to natural disasters such as earthquakes. A significant natural disaster, such as an earthquake or prolonged drought, could have a material adverse impact on the Company’s business, financial condition and operating results. Furthermore, manufacturing semiconductors requires manufacturing tools that are unique to each product being produced. If one of these unique manufacturing tools was damaged or destroyed, the Company’s ability to manufacture the related product would be impaired and its business would suffer until the tool was repaired or replaced. Additionally, the fabrication of ICs is a highly complex and precise process. Small impurities, contaminants in the manufacturing environment, difficulties in the fabrication process, defects in the masks used to print circuits on a wafer, manufacturing equipment failures, and wafer breakage or other factors can cause a substantial percentage of wafers to be rejected or numerous die on each wafer to be nonfunctional. The Company maintains approximately two to three months of inventory that has completed the wafer fabrication manufacturing process. This inventory is generally located offshore at third party subcontractors and can, but may not be sufficient to, act to buffer some of the adverse impact from a disruption to the Company’s San Jose wafer fabrication activity arising from a natural disaster such as an earthquake.

The Company’s results of operations could vary as a result of the methods, estimations and judgments used in applying its accounting policies. The methods, estimates and judgments used by the Company in applying its accounting policies have a significant impact on its results of operations. Such methods, estimates and judgments are, by their nature, subject to substantial risks, uncertainties, assumptions and changes in rulemaking by the regulatory bodies, and factors may arise over time that lead the Company to change its methods, estimates, and judgments. Changes in those methods, estimates and judgments could significantly impact the Company’s results of operations.

Changes in tax laws could adversely affect the Company’s results of operations. The Company is subject to income taxes in the United States and in various immaterial foreign jurisdictions. Significant judgment is required in determining the Company’s worldwide tax liabilities. The Company believes that it complies with applicable tax law. If the governing tax authorities have a different interpretation of the applicable law or if there is a change in tax law, the Company’s financial condition and results of operations may be adversely affected.

|

UNRESOLVED STAFF COMMENTS

|

None

|

PROPERTIES

|

The majority of the Company's manufacturing operations are located in San Jose, California in a 57,000 square foot facility and an adjacent 63,000 square foot facility which are owned by the Company. The Company fabricates the majority of its wafers at this location in a 28,000 square foot clean room facility, which provides all production processes. In addition to wafer fabrication, the Company also uses this location as a testing facility. The Company's main executive, administrative, and technical offices are located in another 57,000 square foot facility in San Jose, California which is owned by the Company.

The Company also leases small sales and technical facilities located in, Richardson, TX; Perkasie, PA; Irvine, CA; San Diego, CA; Hong Kong; Bundang, Korea; Taipei, Taiwan; Shenzhen, P.R. China; Shanghai, P.R. China; Singapore; Yokohama, Japan; Newbury, U.K.; Swindon, U.K.; Livingston, Scotland; Frankfurt, Germany and Villebon, France.

The Company believes that its existing facilities are adequate for its current manufacturing needs. The Company believes that if it should need additional space, such space would be available at commercially reasonable terms.

|

LEGAL PROCEEDINGS

|

The information included in Note 11 of Notes to Consolidated Financial Statements under the caption "Litigation" in Item 15 of Part IV is incorporated herein by reference.

|

[REMOVED AND RESERVED]

|

PART II

|

MARKET FOR THE REGISTRANT'S COMMON EQUITY AND RELATED SHAREHOLDER MATTERS

|

The Company did not sell any unregistered securities during the period covered by this Annual Report on Form 10-K.

The Company’s Common Stock is listed on the NASDAQ Global Select Market under the symbol "MCRL." The range of daily closing sales prices per share for the Company’s Common Stock from January 1, 2009 to December 31, 2010 was:

|

Year Ended December 31, 2010:

|

High

|

Low

|

||||||

|

Fourth quarter

|

$ | 13.77 | $ | 10.02 | ||||

|

Third quarter

|

$ | 11.18 | $ | 8.82 | ||||

|

Second quarter

|

$ | 12.38 | $ | 9.99 | ||||

|

First quarter

|

$ | 10.89 | $ | 7.23 | ||||

|

Year Ended December 31, 2009:

|

High

|

Low

|

||||||

|

Fourth quarter

|

$ | 8.44 | $ | 7.05 | ||||

|

Third quarter

|

$ | 8.34 | $ | 7.00 | ||||

|

Second quarter

|

$ | 7.96 | $ | 6.75 | ||||

|

First quarter

|

$ | 7.94 | $ | 6.29 | ||||

The reported last sale price of the Company’s Common Stock on the NASDAQ Global Select Market on December 31, 2010 was $12.99. The approximate number of holders of record of the shares of the Company’s Common Stock was 389 as of February 22, 2011. This number does not include shareholders whose shares are held in trust by other entities. The actual number of beneficial shareholders is greater than this number of holders of record.

The Company has authorized Common Stock, no par value and Preferred Stock, no par value. The Company has not issued any Preferred Stock.

The information required by this item regarding securities authorized for issuance under equity compensation plans is included under the caption "Equity Compensation Plan Information" in the Company’s Proxy Statement to be filed in connection with the Company’s 2011 Annual Meeting of Shareholders and is incorporated herein by reference.

Dividend Policy

On January 27, 2011, the Company's Board of Directors declared a $0.035 per common share cash dividend, payable February 23, 2011 to shareholders of record on February 9, 2011. During the year ended December 31, 2010, the Company paid cash dividends in the amount of $0.035 per common share per quarter for a total of $8.6 million. During the year ended December 31, 2009, the Company paid cash dividends in the amount of $0.035 per common share per quarter for a total of $8.9 million.

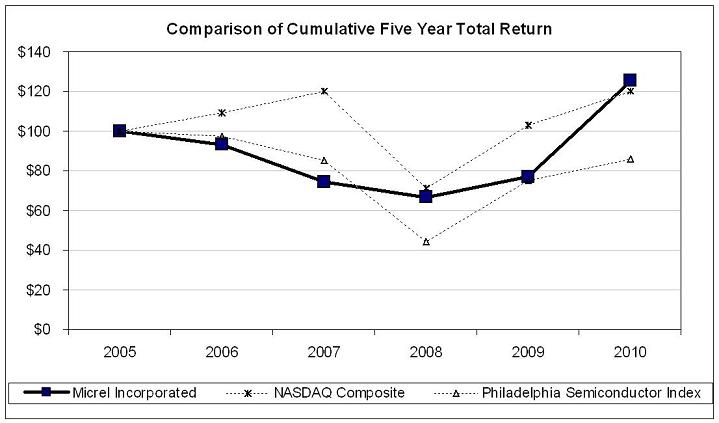

Stock Performance Graph

The following graph compares a $100 investment in Micrel common stock over the five year period from the end of 2005 through the end of 2010, with a similar investment in the NASDAQ Composite and the Philadelphia Semiconductor index. It shows the cumulative total returns over this five year period, assuming reinvestment of dividends.

|

December 30, 2005

|

December 29, 2006

|

December 31, 2007

|

December 31, 2008

|

December 31, 2009

|

December 31, 2010

|

|||||||||||||||||||

|

Micrel Incorporated

|

$ | 100.00 | $ | 93.01 | $ | 74.18 | $ | 66.40 | $ | 77.22 | $ | 125.34 | ||||||||||||

|

NASDAQ Composite

|

$ | 100.00 | $ | 109.52 | $ | 120.27 | $ | 71.51 | $ | 102.89 | $ | 120.29 | ||||||||||||

|

Philadelphia Semiconductor Index

|

$ | 100.00 | $ | 97.40 | $ | 85.10 | $ | 44.25 | $ | 75.06 | $ | 85.89 | ||||||||||||

Issuer Purchases of Equity Securities