Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

(Amendment No. 2)

SAnnual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended June 30, 2010

or

oTransition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Transition Period From ____ to ____

Commission file number: 33-60032

Buckeye Technologies Inc.

(Exact name of registrant as specified in its charter)

|

Delaware

|

62-1518973

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

1001 Tillman Street, Memphis, Tennessee

|

38112

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code (901) 320-8100

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange on which Registered

|

|

|

Common Stock, par value $0.01 per share

|

New York Stock Exchange

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No S

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No S

Indicate by check mark whether registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes S No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data file required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. S

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one).

|

Large accelerated filer o

|

Accelerated filer S

|

Non-accelerated filer o

|

Smaller Reporting Company o

|

Indicate by a check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No S

As of December 31, 2009, the aggregate market value of the registrant’s voting common equity held by non-affiliates, computed by reference to the price at which the common equity was last sold, was approximately $360 million.

As of September 1, 2010, there were outstanding 39,353,491 Common Shares of the Registrant.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of Buckeye Technologies Inc.’s 2010 Annual Proxy Statement filed with the Commission in connection with the 2010 Annual Meeting of Stockholders (the “2010 Proxy Statement”) were incorporated by reference into Part III of the Annual Report on Form 10-K filed with the Commission on September 2, 2010.

EXPLANATORY NOTE

Buckeye Technologies Inc. (the “Company”) is filing this Amendment No. 2 to its Annual Report on Form 10-K (this “Amendment No. 2”) to amend its Annual Report on Form 10-K for the fiscal year ended June 30, 2010, as filed with the Securities and Exchange Commission (the “Commission”) on September 2, 2010 (the “Original Form 10-K”), as amended by Amendment No. 1 filed with the Commission on January 21, 2011 (“Amendment No. 1”). Amendment No. 1 amended and restated Item 15 and the Exhibit Index of the Original Form 10-K in response to comments from the Commission relative to certain exhibits to the Original Form 10-K. After the Company filed Amendment No. 1, the Commission requested that the Company provide a “full” amendment to the Original Form 10-K and include all parts of Form 10-K, including those that were not being amended. Accordingly, this Amendment No. 2 includes all parts of Form 10-K, including updated certifications of the Company’s Principal Executive Officer and Principal Financial Officer pursuant to Sections 906 and 302 of the Sarbanes-Oxley Act of 2002.

No other item or disclosures appearing in the Original Form 10-K, as amended by Amendment No.1, is affected by this Amendment No. 2 other than those matters specifically described above. This Amendment No. 2 is presented as of the filing date of the Original Form 10-K and does not reflect events occurring after that date, or modify or update disclosures in any way other than as specifically noted above. Accordingly, this Amendment No. 2 should be read in conjunction with the Company’s other filings made with the Commission subsequent to the date of the Original Form 10-K, including any amendments to those filings.

INDEX

BUCKEYE TECHNOLOGIES INC.

|

ITEM

|

PAGE

|

|

|

PART I

|

||

|

1.

|

Business

|

3

|

|

1A.

|

Risk Factors

|

9

|

|

1B.

|

Unresolved Staff Comments

|

14

|

|

2.

|

Properties

|

14

|

|

3.

|

Legal Proceedings

|

14

|

|

4.

|

(Removed and reserved)

|

15

|

|

PART II

|

||

|

5.

|

Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

17

|

|

6.

|

Selected Financial Data

|

19

|

|

7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

20

|

|

7A.

|

Qualitative and Quantitative Disclosures About Market Risk

|

33

|

|

8.

|

Financial Statements and Supplementary Data

|

34

|

|

9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

34

|

|

9A.

|

Controls and Procedures

|

35

|

|

9B.

|

Other information

|

35

|

|

PART III

|

||

|

10.

|

Directors, Executive Officers and Corporate Governance

|

35

|

|

11.

|

Executive Compensation

|

35

|

|

12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

35

|

|

13.

|

Certain Relationships and Related Transactions, and Director Independence

|

36

|

|

14.

|

Principal Accountant Fees and Services

|

36

|

|

PART IV

|

||

|

15.

|

Exhibits and Financial Statement Schedules

|

36

|

|

Signatures

|

37

|

|

|

OTHER

|

||

|

Index to Consolidated Financial Statements and Schedules

|

F-1

|

|

PART I

Item 1. Business

General

Buckeye Technologies Inc. (sometimes referred to in this report as “we”, “us”, the “Company” or “Buckeye”) is a leading producer of value-added cellulose-based specialty products, headquartered in Memphis, Tennessee. We believe that we have leading positions in many of the high-end niche markets in which we compete. We utilize our expertise in polymer chemistry, leading research and development and advanced manufacturing facilities to develop and produce innovative and proprietary products for our customers. We sell our products to a wide array of technically demanding niche markets in which we believe our proprietary products, manufacturing processes and commitment to customer technical service give us a competitive advantage. We are the only manufacturer in the world offering cellulose-based specialty products made from both wood and cotton and utilizing wetlaid and airlaid technologies. As a result, we believe we produce and market a broader range of cellulose-based specialty products than any of our competitors. We produce precisely tailored products designed to meet individual customer requirements. Our focus on specialty niche markets allows us to establish long-term supply positions with key customers. We operate manufacturing facilities in the United States, Canada, Germany and Brazil.

Cellulose is a natural fiber derived from trees and other plants that is used in the manufacture of a wide array of products. The total cellulose market generally can be divided into two categories: commodity and specialty. Manufacturers use commodity cellulose to produce bulk paper and packaging materials, the markets for which are very large but highly cyclical. Specialty cellulose is used to impart unique chemical or physical characteristics to a diverse range of highly engineered products. Specialty cellulose generally commands higher prices, and demand for specialty cellulose is less cyclical than commodity cellulose. We believe the more demanding performance requirements for products requiring specialty cellulose limit the number of participants in our niche markets. Our focus on niche specialty cellulose markets has enabled us to maintain positive cash flows even during cyclical downturns in the commodity cellulose markets.

Company History

We and our predecessors have participated in the specialty cellulose market for over 85 years and have developed new uses for many cellulose-based products. We began operations as an independent company in March 1993, when we acquired the cellulose manufacturing operations of the Procter & Gamble Company located in Memphis, Tennessee and Perry, Florida (the “Foley Plant”), with Procter & Gamble retaining a 50% limited partnership interest in the Foley Plant. We became a public company in November 1995 and simultaneously acquired and redeemed Procter & Gamble’s remaining interest in the Foley Plant.

In May 1996, we acquired the specialty cellulose business of Peter Temming AG located in Glueckstadt, Germany. That same year, we acquired Alpha Cellulose Holdings, Inc., a specialty cellulose producing facility located in Lumberton, North Carolina. In May 1997, we acquired Merfin International Inc., a leading manufacturer of airlaid nonwovens with facilities located in Canada, Ireland and the United States. In October 1999, we acquired substantially all of the assets of Walkisoft, UPM-Kymmene’s airlaid nonwovens business. The acquisition of Walkisoft added manufacturing facilities in Steinfurt, Germany and Gaston County, North Carolina. In March 2000, we acquired the intellectual property rights to the Stac-Pac® folding technology and the cotton cellulose business of Fibra, S.A. located in Americana, Brazil. In calendar 2001, we commenced operating the world’s largest airlaid nonwovens machine at our Gaston, North Carolina facility and started up a cosmetic cotton fiber line at our Lumberton, North Carolina facility.

Due to a decline in demand for cotton content paper, in August 2003 we closed the specialty cotton papers portion of our Lumberton, North Carolina facility. Due to excess airlaid production capacity around the globe, we closed our single-line airlaid nonwovens facility in Cork, Ireland in July 2004. In December 2005, we ceased production at our cotton linter pulp facility in Glueckstadt, Germany. In conjunction with this closure, we upgraded the capability of our Americana, Brazil manufacturing facility, which was completed during fiscal year 2006.

We are incorporated in Delaware and our executive offices are located at 1001 Tillman Street, Memphis, Tennessee. Our telephone number is (901) 320-8100.

3

Products

Our product lines can be broadly grouped into four categories: chemical cellulose, customized fibers, fluff pulp and nonwoven materials. We manage these products within two reporting segments: specialty fibers and nonwoven materials. The chemical cellulose and customized fibers are derived from wood and cotton cellulose materials using wetlaid technologies. Fluff pulps are derived from wood using wetlaid technology. Wetlaid technologies encompass cellulose manufacturing processes in which fibers are deposited using water. Airlaid nonwoven materials are derived from wood pulps, synthetic fibers and other materials using airlaid technology. Airlaid technology utilizes air as a depositing medium for fibers, one benefit of which is an increased ability as compared to wetlaid processes to mix additional feature-enhancing substances into the material being produced. A breakdown of our major product categories, percentage of sales, product attributes and applications is provided below.

|

Product Groups

|

% of Fiscal 2010

Sales

|

Value Added Attributes

|

Market for End Use Applications

|

|

Specialty Fibers

Chemical Cellulose

Food casings

Rayon industrial

cord

Rayon staple fiber

Cellulose ethers

Wood acetate

Cotton acetate

|

33%

|

Purity and strength

Strength and heat stability

Uniform viscosity and dyeability

High viscosity, low viscosity, purity

and safety

Viscosity uniformity and purity

Transparency/clarity, strength and

purity

|

Hot dog and sausage casings

High performance tires and hose reinforcement

Textiles

Personal care products, low fat dairy products, pharmaceuticals and construction materials

Cigarette filters

Liquid crystal display film for computers and television screens and plastic applications

|

|

Customized Fibers

Filters

Specialty cotton

papers

Cosmetic Cotton

Buckeye UltraFiber 500®

|

15%

|

High porosity and product life

Color permanence and tear resistance

Absorbency, strength and softness

Finishing and crack reduction

|

Automotive, laboratory and industrial filters

Personal stationery, premium letterhead and currency

Cotton balls and cotton swabs

Concrete

|

|

Fluff Pulp

Fluff pulp

|

19%

|

Absorbency and fluid transport

|

Disposable diapers, feminine hygiene products and adult incontinence products

|

|

Nonwoven Materials

Airlaid nonwovens

|

33%

|

Absorbency, fluid management and

wet strength

|

Feminine hygiene products, specialty wipes and mops, tablecloths, napkins, placemats, incontinence products and food pads

|

See Note 18, Segment Information, to the Consolidated Financial Statements for additional information on products.

4

Raw Materials

Slash pine timber and cotton fibers are the principal raw materials used in the manufacture of our specialty fibers products. These materials represent the largest components of our variable costs of production. The region surrounding the Foley Plant has a high concentration of slash pine timber, which enables us to purchase adequate supplies of a species well suited to our products at an attractive cost. In order to be better assured of a secure source of wood at reasonable prices, we have entered into timber purchase agreements which allow us to purchase a portion of our wood at market prices that are fixed annually or current market prices as stated in the agreements. Additional information is included in Note 21, Commitments, to the Consolidated Financial Statements.

We purchase cotton linter fiber either directly from cottonseed oil mills or indirectly through agents or brokers. We purchase the majority of our requirements of cotton fiber for the Memphis and Lumberton plants domestically. The majority of the cotton fiber processed in the Americana plant is purchased in Brazil.

Fluff pulp is the principal raw material used in the manufacture of our nonwoven materials products. Approximately 50% of our fluff pulp usage is internally supplied and the remainder is purchased from several other suppliers. In addition to fluff pulp, our nonwovens products are comprised of synthetic fibers, latex polymers, absorbent powders and carrier tissue depending on grade specifications. These raw materials are also purchased from multiple sources.

The cost and availability of slash pine timber, cotton linter fiber and fluff pulp are subject to market fluctuations caused by supply and demand factors. We do not foresee material constraints from pricing or availability for slash pine timber and fluff pulp. We continue to have raw material availability issues for our cotton linter fibers in both North America and Brazil. We have increased our imported cotton linters purchases for specialty cotton fiber production in Memphis in order to minimize the impact of current constraints on North American cotton fiber availability. This raw material availability constraint will limit our growth and increase production costs.

Our manufacturing processes, especially for specialty fibers, require significant amounts of fuel oil and natural gas. These manufacturing inputs are subject to significant changes in prices, which could adversely affect our operating results.

Sales and Customers

Our products are marketed and sold through a highly trained, technically skilled sales force. We maintain sales offices in the United States, Europe and China. Our worldwide sales are diversified by geographic region as well as end-product application. Our sales are distributed to customers in over 60 countries around the world. Our fiscal 2010 sales reflect this geographic diversity, with 39% of sales in North America, 33% of sales in Europe, 16% of sales in Asia, 4% of sales in South America and 8% in other regions. Approximately 86% of our worldwide sales for fiscal 2010 were denominated in U.S. dollars. Our products are shipped by rail, truck and ocean carrier. Geographic segment data and product sales data are included in Note 18, Segment Information, to the Consolidated Financial Statements.

Sales by geographical destination for the three years ended June 30, 2010 were as follows:

(in millions)

|

Sales by Destination

|

|||||||||||||||||||

|

2010

|

2009

|

2008

|

|||||||||||||||||

|

United States

|

$

|

229

|

30

|

%

|

$

|

245

|

32

|

%

|

$

|

257

|

31

|

%

|

|||||||

|

Germany

|

70

|

9

|

67

|

9

|

72

|

9

|

|||||||||||||

|

Italy

|

53

|

7

|

48

|

6

|

62

|

7

|

|||||||||||||

|

China

|

44

|

6

|

14

|

2

|

16

|

2

|

|||||||||||||

|

Mexico

|

34

|

5

|

46

|

6

|

38

|

5

|

|||||||||||||

|

Canada

|

33

|

4

|

31

|

4

|

31

|

4

|

|||||||||||||

|

Japan

|

32

|

4

|

34

|

5

|

39

|

5

|

|||||||||||||

|

France

|

27

|

4

|

29

|

4

|

31

|

4

|

|||||||||||||

|

Brazil

|

25

|

3

|

25

|

3

|

30

|

3

|

|||||||||||||

|

Spain

|

23

|

3

|

20

|

3

|

26

|

3

|

|||||||||||||

|

All other

|

186

|

25

|

196

|

26

|

224

|

27

|

|||||||||||||

|

Total

|

$

|

756

|

100

|

%

|

$

|

755

|

100

|

%

|

$

|

826

|

100

|

%

|

|||||||

The high-end, technically demanding specialty niche markets that we serve require a higher level of sales and technical service support than do commodity product sales. Our sales, product development and customer service professionals work with customers in their plants to design products tailored precisely to their product needs and manufacturing processes. In addition to a

5

Research and Development

Our research and development activities focus on developing new products, improving existing products and enhancing process technologies to further reduce costs and respond to environmental needs. We have research and development pilot plant facilities in Memphis, and we employ engineers, scientists and technicians who are focused on advanced products and new applications to drive future growth. Our pilot plant facilities allow us to produce, test and deliver breakthrough products to the market place on a more cost-effective basis while minimizing interruptions to the normal production cycles of our operating plants.

Research and development costs of $6.8 million, $7.5 million and $8.2 million were charged to expense as incurred for the years ended June 30, 2010, 2009 and 2008, respectively.

Competition

There are relatively few specialty fibers producers when compared with the much larger commodity paper pulp markets. The technical demands and unique requirements of the high-purity chemical cellulose or customized fiber pulp user tend to differentiate suppliers on the basis of their ability to meet the customer’s particular set of needs, rather than focusing only on pricing. The high-purity chemical cellulose and customized fiber markets are less subject to price variation than commodity paper pulp markets. Major competitors include Rayonier Inc., Borregaard, Sateri International Group (”Sateri”), Neucel Specialty Cellulose Ltd., Sappi Saiccor, Tembec Inc., and Archer Daniels Midland Company.

We believe that the number of producers is unlikely to grow significantly due to the substantial investment required to enter the mature specialty fibers market and due to sufficient existing capacity. However, Sateri reportedly added 250,000 tons of specialty pulp capacity in Brazil (Bahia) during 2008/2009 and is supplying this new volume into the market now. Fortress Paper Ltd. has announced plans to convert a bleached paper mill in Thurso, Quebec to a chemical cellulose mill sometime in 2011. Demand from China for chemical cellulose to support its growing viscose rayon staple fiber market is strong and we expect this demand to continue consistent with the growth of China’s middle class. Thus, this additional chemical cellulose capacity is expected to be readily consumed by China’s growth.

Although global demand for fluff pulp is growing by 3% to 5% annually, we expect fluff pulp prices over the longer term to vary directly with commodity paper pulp prices because fluff pulp is often produced in mills that also produce commodity paper pulp. Over longer periods of time, fluff pulp prices are higher than commodity pulp prices by $40 to $60 per air dry metric tonne on average, but short term variances can be more significant. We use 40,000 to 50,000 metric tons of fluff pulp annually from our Perry, Florida wood cellulose facility as a key raw material in our airlaid nonwovens business. We believe that we currently produce approximately 5% of the world’s supply of fluff pulp. Major competitors include AbitibiBowater Inc., International Paper Company, GP Cellulose, LLC, Rayonier, Weyerhaeuser Corp. and Domtar Corp. We believe the current global output of fluff pulp is approximately 5.1 million tons annually. We understand that future increases in output at Domtar’s Plymouth mill and a conversion project to produce fluff at GP Cellulose’s recently acquired Alabama River Mill could add 300,000 to 500,000 tons of fluff output in the next two years.

Demand for airlaid nonwovens grew significantly in the 1990’s. Since then, significant capacity expansion in 2001, primarily in North America, resulted in the market being oversupplied. Buckeye is a leading supplier of airlaid nonwoven materials worldwide. The markets in which we compete also utilize nonwovens materials produced with technologies other than airlaid such as spunlace. Major nonwovens competitors include Ahlstrom Oyi, Fiberweb Plc, P.H. Glatfelter Company, Duni AB, GP Cellulose, LLC, Kimberly-Clark Corporation and Polymer Group, Inc.

While the North American industry is operating in an environment of excess supply, the European market has been more balanced. Glatfelter announced the new line at their Falkenhagen, Germany facility with an annual capacity in the range of 15,000 to 20,000 metric tons came online in 2009. Additionally, Lycell started up a new airlaid line in Finland in early 2010 reportedly with an annual capacity of approximately 8,000 metric tons. We understand that Fiberweb permanently shut down an airlaid line in Italy in January 2009. In other parts of the world, Fiberweb has started up a second machine in China, which we understand has approximately 10,000 metric tons of annual capacity, and we understand that Sambo started up a 10,000 metric tons per year line in South Korea last year.

6

Intellectual Property

At June 30, 2010 and 2009, we had intellectual property assets recorded totaling $13.2 million and $14.8 million, respectively. These assets include patents, licenses, trademarks and trade names, the majority of which were obtained in the acquisition of airlaid nonwovens businesses and Stac-Pac® technology. We intend to protect our patents and file applications for any future inventions that are deemed to be important to our business operations. The Stac-Pac® packaging technology, a proprietary system for packaging low-density nonwoven materials in compressed cube-shaped bales, is an example of technology we acquired to further differentiate us from our airlaid nonwovens competitors. Stac-Pac® bales facilitate our customers’ high-speed production lines with a continuous flow of material. Stac-Pac® units also reduce freight costs by compressing more material in a bale than can be shipped in a traditional roll form, which enables us to ship the bales more effectively in trucks and containers. Additional information is included in Note 1, Accounting Policies, to the Consolidated Financial Statements.

|

Seasonality

|

Our overall business generally is not seasonal to a substantial extent, although we ship slightly lower specialty fiber volume in the July – September quarter and slightly lower nonwovens volume is shipped in the October – December quarter.

Employees

As of August 15, 2010, we employed approximately 1,400 employees, of whom approximately 73% are employed at our facilities in the United States. Approximately 54% of the U.S. employees are represented by unions at two plants in Perry, Florida and Memphis, Tennessee. Our Foley Plant’s labor agreement is in effect through April 1, 2012. The agreement for the Memphis Plant is in effect through March 18, 2013. At our Canadian facility, the labor agreement expired on June 30, 2009, but was automatically extended until negotiations are completed. A national union provides employee representation for non-management workers at our specialty fibers plant in Americana, Brazil. A works council provides employee representation for non-management workers at our nonwoven materials plant in Steinfurt, Germany. Our plants in Gaston, King and Lumberton, North Carolina are not unionized.

None of our facilities has had labor disputes or work stoppages in recent history. The Foley and Memphis Plants have not experienced any work stoppages due to labor disputes in over 30 years and 50 years, respectively. We consider our relationships with our employees and their representative organizations to be good. An extended interruption of operations at any of our facilities, however, could have a material adverse effect on our business.

Environmental Regulations and Liabilities

Our operations are subject to extensive general and industry-specific federal, state, local and foreign environmental laws and regulations, particularly those relating to air and water quality, waste disposal and the cleanup of contaminated soil and groundwater. We devote significant resources to maintaining compliance with these laws and regulations. Such environmental laws and regulations at the federal level include the Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended, the Clean Air Act of 1990, as amended, the Clean Water Act of 1972, as amended, the Resource Conservation and Recovery Act of 1976, as amended, the Toxic Substances Control Act of 1976, as amended, and the Safe Drinking Water Act of 1974, as amended. These environmental regulatory programs are primarily administered by the U.S. Environmental Protection Agency (“EPA”). In addition, the individual states and foreign countries in which we operate have adopted and may adopt in the future equivalent or more stringent environmental laws and regulations or have enacted their own parallel environmental programs. We closely monitor our environmental compliance with current environmental requirements and believe that we are in substantial compliance.

We expect that, due to the nature of our operations, we will be subject to increasingly stringent environmental requirements, including standards applicable to wastewater discharges and air emissions, such as emissions of greenhouse gases, and general permitting requirements for our manufacturing facilities. We also expect that we will continue to incur substantial costs to comply with such requirements. Any failure on our part to comply with environmental laws or regulations could subject us to penalties or other sanctions that could materially affect our business, results of operations or financial condition. We cannot currently assess, however, the impact that more stringent environmental requirements may have on our operations or capital expenditure requirements. We do not anticipate that capital expenditures in connection with matters relating to environmental compliance will have a material effect on our results of operations during fiscal year 2011.

7

The Foley Plant, located in Perry, Florida, discharges treated wastewater into the Fenholloway River. Under the terms of an agreement with the Florida Department of Environmental Protection (“FDEP”), approved by the EPA in 1995, we agreed to a comprehensive plan to attain Class III (“fishable/swimmable”) status for our discharge into the Fenholloway River under applicable Florida law (the “Fenholloway Agreement”). The Fenholloway Agreement established a schedule for the filing of necessary permit applications and approvals to implement the following activities, among others: (i) make process changes within the Foley Plant to reduce the coloration of its wastewater discharge, (ii) restore certain wetlands areas, (iii) install a pipeline to relocate the wastewater discharge point into the Fenholloway River to a point closer to the mouth of the river, and (iv) provide oxygen enrichment to the treated wastewater prior to discharge at the new location. Since finalization of the Fenholloway Agreement, we have completed the required process changes within the Foley Plant. In making these in-plant process changes, we incurred significant capital expenditures. Based on the anticipated National Pollutant Discharge Elimination System (“NPDES”) permit conditions, we have incurred and, once a final NPDES permit is issued, expect to incur significant capital expenditures.

We expect to incur additional capital expenditures related to our wastewater treatment and discharge of between $40 million and $60 million over at least five years, possibly beginning as early as fiscal year 2012. The amount and timing of these capital expenditures may vary depending on a number of factors, including when the final NPDES permit is issued and its final terms and conditions. For additional information on environmental matters, see Note 22, Contingencies, to the Consolidated Financial Statements. These possible expenditures could have a material adverse effect on our business, results of operations or financial condition.

The Foley Plant is also subject to FDEP and EPA air emission standards. In 2007, new EPA boiler air emission regulations (boiler Maximum Achievable Control Technology (“MACT”) standards) applicable to the Foley Plant were vacated following a public legal challenge. EPA re-proposed those regulations in April 2010. The public comment period for that proposed rule ended on August 23, 2010, but EPA has not issued its final regulation for the boiler MACT. These regulations may impact both bark boilers at the Foley Plant. However, since EPA has not promulgated a final rule, it is difficult to predict the potential capital expenditures associated with these pending regulations.

Other Information

Our website is www.bkitech.com. We make available, free of charge, through our website under the heading “Investor Relations,” proxy materials, annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to Section 13(a) or Section 15(d) of the Securities Exchange Act of 1934, as amended. The information on our website is not part of or incorporated by reference in this Annual Report on Form 10-K or any other report that we may file with the Commission.

These reports are also available as soon as reasonably practicable after we electronically file such materials with, or furnish such materials to, the Securities and Exchange Commission, or the SEC. The public may also read and copy any materials we file with the SEC at the SEC’s Public Reference Room at Station Place, 100 F Street NE, Washington, D.C. 20549. The public may obtain information about the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an internet site that contains reports, proxy and information statements and other information filed electronically by us, which are available at http://www.sec.gov.

Safe Harbor Provisions

This document contains both historical and forward-looking statements. All statements other than statements of historical fact are, or may be deemed to be, “forward-looking” statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are not based on historical facts, but rather reflect management’s current expectations concerning future results and events.

These forward-looking statements generally can be identified by the use of statements that include phrases such as "believe," "expect," "anticipate," "intend," "plan," "foresee," "likely," "will" or other similar words or phrases. Similarly, statements that describe management’s objectives, plans or goals are or may be forward-looking statements. These forward-looking statements involve known and unknown risks, uncertainties and other factors that are difficult to predict and which may cause the actual results, performance or achievements to be different from any future results, performance and achievements expressed or implied by these statements.

8

The following important factors, among others, including those set forth below in Item 1A of this Annual Report on Form 10-K, could affect future results, causing these results to differ materially from those expressed in our forward-looking statements: dependence on a single customer; the ability to obtain additional capital, maintain adequate cash flow to service debt as well as meet operating needs; maintaining satisfactory labor relations; an inability to predict the scope of future environmental compliance costs or liabilities; pricing fluctuations and worldwide economic conditions; competition; and fluctuations in the costs and availability of raw materials.

Any forward-looking statements included in this document are only made as of the date of this document and we do not intend nor undertake to publicly update any forward-looking statements to reflect subsequent events or circumstances except as we may be required by law to do so.

Item 1A. Risk Factors

Our operations are subject to a number of risks including those listed below and discussed elsewhere in this Annual Report on Form 10-K (particularly in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations). If any of the events described in the following risk factors actually occur, it could materially affect our results of operations and financial condition.

Risks related to our industry

We are subject to the cyclical changes caused by general global and industry conditions.

The demand and pricing of our products, particularly fluff pulp, are influenced by the much larger market for papermaking pulps which is highly cyclical. The markets for most cellulose and absorbent products are sensitive to both changes in general global economic conditions and to changes in industry capacity. Both of these factors are beyond our control. The price of these products can fluctuate significantly when supply and demand become imbalanced for any reason. Our financial performance can be heavily influenced by these pricing fluctuations and the general cyclicality of the industries in which we compete. Furthermore, a general economic downturn in a particular country or on an international scale could reduce the overall sales within our industry, thereby likely reducing our sales. We cannot assure you that current prices will be maintained, that any price increases will be achieved, or that industry capacity utilization will reach favorable levels. The demand, cost and prices for our products may fluctuate substantially in the future and downturns in market conditions could have a material adverse effect on our business, results of operations and financial condition.

Competition and surplus capacity could adversely affect our operating results and financial condition.

The markets for our products are all competitive. Actions by competitors can affect our ability to sell our products and can affect the volatility of the prices at which our products are sold. Other actions by competitors, such as reducing costs or adding low-cost capacity, may adversely affect our competitive position in the products we manufacture and, consequently, our sales, operating income and cash flows. New competitors and the expansion of existing competitors could create a surplus capacity of the goods that we sell, which might cause us to either lose sales or lower the prices of our goods. Actions by our competitors and any surplus capacity could cause our sales and profits to decline, affecting our operating results and financial condition.

Market fluctuations in the availability and cost of energy and raw materials are beyond our control and may adversely affect our business.

Energy, chemicals, and raw material costs, including fuel oil, natural gas, electricity, cotton linters, wood, and caustic and other chemicals are a significant operating expense. The prices and availability of raw materials and energy can be volatile and are susceptible to rapid and substantial changes due to factors beyond our control such as changing economic conditions, currency fluctuations, weather conditions, political unrest and instability in energy-producing nations, and supply and demand considerations. We have raw material availability issues at our Memphis and Americana specialty fiber plants. We have the option to import cotton linters purchases for our Memphis specialty cotton fiber production in order to minimize the impact of current constraints on North American cotton fiber availability. We have limited production at our Americana, Brazil and Memphis specialty fibers facilities because of raw material constraints. This raw material availability constraint will limit growth and increase our production costs. Energy and chemical costs which had increased substantially in recent years, resulting in increased production costs for our products, have recently moderated. Increases in production costs could have a material adverse effect on our business, financial condition and results of operations. In addition to increased costs, it is possible that a disruption in supply of natural gas or other fossil fuels could limit our ability to operate our facilities.

9

Market fluctuations in the availability and cost of transportation are beyond our control and may adversely impact our business.

Our business depends on the transportation of a large number of products, both domestically and internationally. An increase in transportation rates or fuel surcharges and/or a reduction in transport availability in truck, rail and international shipping could negatively impact our ability to provide products to our customers in a timely manner. An increase in international shipping rates or fuel surcharges or a reduction in the availability of vessels could negatively impact our costs and our ability to provide products to our international customers in a timely manner. While we have had adequate transportation availability, there is no assurance that such availability can continue to be effectively managed in the future.

Risks related to our business

Exposure to commodity products creates volatility in pricing and profits.

If our research and development efforts do not result in the commercialization of new, proprietary products, we will continue to have significant exposure to fluff pulp, which could result in volatility in sales prices and profits.

Our indebtedness levels could adversely affect us.

As of June 30, 2010, our total debt was approximately $237.5 million and our total debt, as a percentage of total capitalization, was 35%. Our level of debt could have a significant adverse future effect on our business. For example:

- we may have limited ability to borrow additional amounts for working capital, capital expenditures, acquisitions, debt service requirements, execution of our growth strategy, research and development costs or other purposes;

- a substantial portion of our cash flow may be used to pay principal and interest on our debt, which will reduce the funds available for working capital, capital expenditures, acquisitions and other purposes;

- our senior secured credit facility covenants require us to meet certain financial objectives and impose other restrictions on business operations. These covenants and those contained in the indenture governing our senior notes limit our ability to borrow additional funds or dispose of assets and limit our flexibility in planning for and reacting to changes in our business;

- we may be more vulnerable to adverse changes in general economic, industry and competitive conditions and adverse changes in government regulation;

- our debt level and the various covenants contained in the indenture related to our senior notes and the documents governing our other existing indebtedness may place us at a relative competitive disadvantage as compared to certain of our competitors; and

- our borrowings under our senior secured credit facility are at floating rates of interest, which could result in higher interest expense in the event of an increase in interest rates.

Our ability to pay principal of and interest on our senior notes, to service our other debt and to refinance indebtedness when necessary depends on our financial and operating performance, each of which is subject to prevailing economic conditions and to financial, business and other factors beyond our control.

We cannot assure you that we will generate sufficient cash flow from operations or that we will be able to obtain sufficient funding to satisfy all of our obligations. If we are unable to pay our debts, we will be required to pursue one or more alternative strategies, such as selling assets, refinancing or restructuring our indebtedness or selling additional equity capital. However, we cannot assure you that any alternative strategies will be feasible at the time or prove adequate. Also, certain alternative strategies will require the consent of our senior secured lenders before we engage in any such strategy.

Changes in credit ratings issued by nationally recognized statistical rating organizations could adversely affect our cost of financing and have an adverse effect on the market price of our securities.

Credit rating agencies rate our debt securities on factors that include our operating results, actions that we take, their view of the general outlook for our industry and their view of the general outlook for the economy. Actions taken by the rating agencies can include maintaining, upgrading or downgrading the current rating or placing the company on a watch list for possible future downgrading. Downgrading the credit rating of our debt securities or placing us on a watch list for possible future downgrading could limit our access to the credit markets, increase our cost of financing, and have an adverse effect on the market price of our securities.

10

A material disruption at one of our manufacturing facilities could prevent us from meeting customer demand, reduce our sales or negatively affect our results of operation and financial condition.

Any of our manufacturing facilities, or any of our machines within an otherwise operational facility, could cease operations unexpectedly due to a number of events, including:

- unscheduled maintenance outages;

- prolonged power failures;

- an equipment failure;

- a chemical spill or release;

- explosion of a boiler;

- labor difficulties;

- disruptions in the transportation infrastructure, including roads, bridges, railroad tracks and tunnels;

- fires, floods, windstorms, earthquakes, hurricanes or other catastrophes;

- terrorism or threats of terrorism;

- governmental regulations; and

- other operational problems.

We may be required to pay significant export taxes or countervailing and anti-dumping duties for exported products.

We may experience reduced revenues and margins on some of our businesses as a result of export taxes or countervailing and anti-dumping duty applications. It is possible that countervailing duty and antidumping tariffs, or similar types of tariffs could be imposed on us in the future. These tariffs could have a material adverse effect on our business, financial results and financial condition.

The impacts of climate-related initiatives, at the international, federal and state levels, remain uncertain at this time.

Currently, there are numerous international, federal and state-level initiatives and proposals addressing domestic and global climate issues. Within the U.S., most of these proposals would regulate and/or tax, in one fashion or another, the production of carbon dioxide and other “greenhouse gases” to facilitate the reduction of carbon compound emissions to the atmosphere, and provide tax and other incentives to produce and use more “clean energy.” For example, in 2009 the U.S. House of Representatives passed the Markey-Waxman bill (HR 2454), which would establish a so-called “cap and trade” regime and new permitting requirements to regulate greenhouse gas generation, as well as provide an incentive for the production and use of clean energy. To date, the U.S. Senate has not passed any comparable legislation. In sum, we believe that the potential for climate change legislation on the federal level is unknown. In addition, in late 2009, the U.S. EPA issued an “endangerment finding” under the Clear Air Act (“CAA”) with respect to carbon dioxide, which could lead to the regulation of carbon dioxide as a criteria pollutant under the CAA and have significant ramifications for us and the industry in general. On the international front, the United Nations Climate Change Conference in Copenhagen, which took place in December 2009, did not result in any significant progress toward a binding agreement to replace the Kyoto Protocol, which expires in 2012.

We are dependent upon attracting and retaining key personnel.

We believe that our success depends, to a significant extent, upon our ability to attract and retain key senior management and operations management personnel. Our failure to recruit and retain these key personnel could adversely affect our financial condition or results of operations.

Our failure to maintain satisfactory labor relations could have a material adverse effect on our business.

If our negotiations with the representatives of the unions, to which many of our employees belong, are not successful, our

11

Employee representation is provided by a national union for non-management workers at our specialty fibers plant in Americana, Brazil, and a works council at our nonwoven materials plant in Steinfurt, Germany. Our plants in Gaston, Lumberton and King, North Carolina are not unionized.

The failure to renegotiate labor agreements in a timely manner could lead to a curtailment or stoppage of work at our factories. If we negotiated a labor agreement on unfavorable terms, our production costs will increase. A reduction in production or increasing the costs of production would lower our profits and harm our business.

Compliance with extensive general and industry specific environmental laws and regulations requires significant resources, and the significant associated costs may adversely affect our business.

Our operations are subject to extensive general and industry-specific federal, state, local and foreign environmental laws and regulations, particularly those relating to air and water quality, waste disposal and the cleanup of contaminated soil and groundwater. We devote significant resources to maintaining compliance with these laws and regulations. Such environmental laws and regulations at the federal level include the Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended, the Clean Air Act of 1990, as amended, the Clean Water Act of 1972, as amended, the Resource Conservation and Recovery Act of 1976, as amended, the Toxic Substances Control Act of 1976, as amended, and the Safe Drinking Water Act of 1974, as amended. These environmental regulatory programs are primarily administered by the U.S. Environmental Protection Agency (“EPA”). In addition, the individual states and foreign countries in which we operate have adopted and may adopt in the future equivalent or more stringent environmental laws and regulations or have enacted their own parallel environmental programs. We closely monitor our environmental compliance with current environmental requirements and believe that we are in substantial compliance.

We expect that, due to the nature of our operations, we will be subject to increasingly stringent environmental requirements, including standards applicable to wastewater discharges and air emissions, such as emissions of greenhouse gases, and general permitting requirements for our manufacturing facilities. We also expect that we will continue to incur substantial costs to comply with such requirements. Any failure on our part to comply with environmental laws or regulations could subject us to penalties or other sanctions that could materially affect our business, results of operations or financial condition. We cannot currently assess, however, the impact that more stringent environmental requirements may have on our operations or capital expenditure requirements. We do not anticipate that capital expenditures in connection with matters relating to environmental compliance will have a material effect on our earnings during fiscal year 2011.

Compliance with recently passed legislation may adversely affect our business.

In March 2010, Congress passed the Patient Protection and Affordable Care Act and the Health Care and Education Affordability Reconciliation Act (collectively, the “Acts”). Among other things, the Acts contain provisions that will affect employer-sponsored health care plans, impose excise taxes on certain plans, and reduce the tax benefits available to employers that receive the Medicare Part D subsidy. We are currently reviewing provisions of the Acts and their impact on our company-sponsored plans. We are currently unable to estimate costs associated with compliance with the Acts.

Because approximately 70% of our sales are to customers outside the United States, we are subject to the economic and political conditions of foreign nations.

We have manufacturing facilities in four countries and sell products in approximately 60 countries. For the fiscal year ended June 30, 2010, sales of our products outside the United States represented approximately 70% of our sales. The global economy and relative strength or weakness of the U.S. dollar can have a significant impact on our sales. In addition, although approximately 83% of our sales are denominated in U.S. dollars, it is possible that as we expand globally, we will face increased risks associated with operating in foreign countries, including:

- the risk that foreign currencies will be devalued or that currency exchange rates will fluctuate;

|

|

-

|

the risk that limitations will be imposed on our ability to convert foreign currencies into U.S. dollars or on our foreign subsidiaries' ability to remit dividends and other payments to the United States;

|

12

|

|

-

|

the risk that our foreign subsidiaries will be required to pay withholding or other taxes on remittances and other payments to the United States or that the amount of any such taxes will be increased;

|

- the risk that certain foreign countries may experience hyperinflation; and

- the risk that foreign governments may impose or increase investment or other restrictions affecting our business.

Any of these risks could have a material adverse effect on our business, results of operations or financial condition.

Risks related to ownership of our common stock

The price of our common stock may be volatile.

The market price of our common stock may be influenced by many factors, some of which are beyond our control, including those described above under “Risks Related to our Industries and Business” and the following:

- actual or anticipated fluctuations in our operating results or our competitors’ operating results;

|

|

-

|

announcements by us or our competitors of new products, capacity changes, significant contracts, acquisitions or strategic investments;

|

- our growth rate and our competitors’ growth rates;

- the financial market and general economic conditions;

|

|

-

|

changes in stock market analyst recommendations regarding us, our competitors or our industry generally, or lack of analyst coverage of our common stock;

|

|

|

-

|

sales of our common stock by our executive officers, directors and significant stockholders or sales of substantial amounts of common stock; and

|

- changes in accounting principles.

In addition, there has been significant volatility in the market price and trading volume of securities of companies operating in our industry that often has been unrelated to the operating performance of particular companies.

Some companies that have had volatile market prices for their securities have had securities litigation brought against them. If litigation of this type is brought against us, it could result in substantial costs and would divert management’s attention and resources.

13

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

Corporate Headquarters. Our corporate headquarters, research and development laboratories, and pilot plants are located in Memphis, Tennessee.

Specialty Fiber Plants

Memphis Plant. The Memphis Plant is located on approximately 75 acres adjacent to the headquarters complex and has a capacity of approximately 100,000 annual metric tons of cotton cellulose. As of June 30, 2010, the Memphis Plant operated at about 50% of its capacity.

Foley Plant. The Foley Plant is located at Perry, Florida, on a 2,900 acre site and has a capacity of approximately 465,000 annual metric tons of wood cellulose. In connection with the acquisition of the Foley Plant, we also own 13,000 acres of real property near the plant site. As of June 30, 2010, the Foley Plant operated at approximately 100% of its capacity.

Lumberton Plant. The Lumberton Plant is located in Lumberton, North Carolina on a 65-acre site and has a capacity of approximately 8,000 annual metric tons of cosmetic cotton fiber. As of June 30, 2010, the Lumberton Plant operated at approximately 100% of its capacity.

Americana Plant. The Americana Plant is located in the city of Americana in the state of Sao Paulo, Brazil on 27 acres and is part of a multi-business industrial site with a capacity of approximately 40,000 annual metric tons of cotton cellulose. As of June 30, 2010, the Americana Plant operated at about 30% of its capacity.

Nonwovens Plants

The stated capacity of airlaid nonwovens machines is based upon an assumed mix of products. The flexible nature of airlaid technology allows for a wide range of materials to be produced. Machine production capability has typically been lower than the stated capacity, often by factors of 10-20%, when adjusted to reflect the actual product mix. Based on current product mix, utilization of our airlaid machines worldwide, as of June 30, 2010, was approximately 75% of their capacity.

Delta Plant. The Delta Plant is located in Delta, British Columbia on a 12-acre industrial park site and has a total capacity of approximately 30,000 annual metric tons of airlaid nonwovens (26,000 based on current production mix) from two production lines.

Steinfurt Plant. The Steinfurt Plant is located in Steinfurt, Germany on an 18-acre site and has a total capacity of approximately 30,000 annual metric tons of airlaid nonwovens from two production lines.

Gaston Plant. The Gaston Plant is located in Gaston County near Mt. Holly, North Carolina on an 80-acre site and has a total capacity of approximately 60,000 annual metric tons of airlaid nonwovens (43,000 annual metric tons based on current production mix) from two production lines.

King Plant. The King Plant is located in King, North Carolina and converts airlaid materials and wetlaid papers into wipes, towels and tissues for industrial and commercial uses.

We own our corporate headquarters, the Memphis Plant, the Foley Plant, the Lumberton Plant, the Americana Plant, the Delta Plant, the Steinfurt Plant and the Gaston Plant. We lease buildings that house the King Plant, the sales offices in Europe and China and distribution facilities in Savannah, Georgia. All of the facilities located in the United States are pledged as collateral for certain debt agreements.

We believe that our specialty fibers and nonwoven materials manufacturing facilities and administrative buildings are adequate to meet current operating demands.

Item 3. Legal Proceedings

We are involved from time to time in routine legal matters and other claims incidental to our business. We review outstanding claims and proceedings internally and with external counsel as necessary to assess the probability and amount of potential loss. These assessments are re-evaluated at each reporting period and as new information becomes available to determine whether a

14

Item 4. (Removed and Reserved)

Executive Officers of the Registrant

The names, ages and positions held by our executive officers on September 1, 2010 are:

|

Name

|

Age

|

Position

|

Elected to Present Position

|

|

John B. Crowe

|

63

|

Chairman of the Board, Chief Executive Officer and Director

|

July 2006

|

|

Kristopher J. Matula

|

48

|

President, Chief Operating Officer and Director

|

July 2006

|

|

Charles S. Aiken

|

60

|

Sr. Vice President, Energy and Sustainability

|

October 2003

|

|

Sheila Jordan Cunningham

|

58

|

Sr. Vice President, General Counsel and Secretary

|

April 2000

|

|

Steven G. Dean

|

54

|

Sr. Vice President and Chief Financial Officer

|

July 2007

|

|

Douglas L. Dowdell

|

52

|

Sr. Vice President, Specialty Fibers

|

February 2006

|

|

Paul N. Horne

|

55

|

Sr. Vice President, Product and Market Development

|

February 2006

|

|

Marko M. Rajamaa

|

49

|

Sr. Vice President, Nonwovens

|

October 2006

|

John B. Crowe

Chairman of the Board, Chief Executive Officer and Director

Mr. Crowe has served as Chairman of the Board and Chief Executive Officer since July 1, 2006. He served as President and Chief Operating Officer from April 2003 to July 2006. He was elected as a director of Buckeye in August 2004. He served as Senior Vice President, Wood Cellulose from January 2001 to April 2003. He served as Vice President, Wood Cellulose Manufacturing from January 1998 to January 2001. Prior to joining us, he was Executive Vice President/General Manager of Alabama River Pulp and Alabama Pine Pulp Operations, a division of Parsons and Whittemore, Inc. and was Vice President and Site Manager of Flint River Operations, a subsidiary of Weyerhauser Company. From 1979 to 1992, he was an employee of Procter & Gamble.

Kristopher J. Matula

President, Chief Operating Officer and Director

Mr. Matula has served as President and Chief Operating Officer since July 1, 2006. He was elected as a director of Buckeye in April 2007. He served as Executive Vice President and Chief Financial Officer from October 2003 to July 2006. He served as Senior Vice President, Nonwovens and Corporate Strategy from April 2003 to October 2003. He served as Senior Vice President, Nonwovens from January 2001 to April 2003. He served as Senior Vice President, Commercial - Absorbent Products from July 1997 to January 2001 and as Vice President, Corporate Strategy from April 1996 to July 1997. Prior to joining Buckeye in 1994, he held various positions with Procter & Gamble and General Electric.

Charles S. Aiken

Senior Vice President, Energy and Sustainability

Mr. Aiken has served as Senior Vice President, Energy and Sustainability since January 1, 2010. He served as Senior Vice President, Manufacturing from October 2003 to January 2010. He served as Senior Vice President, Nonwovens Manufacturing from April 2000 to October 2003. He served as Vice President, Business Systems from April 1998 to April 2000 and as Vice President, Foley Plant from June 1995 to April 1998. He was an employee of Procter & Gamble from 1977 to March 1993.

Sheila Jordan Cunningham

Senior Vice President, General Counsel and Secretary

Ms. Cunningham has served as Senior Vice President, General Counsel and Secretary since April 2000. She served as Vice President, General Counsel and Secretary from April 1998 to April 2000. She served as Assistant General Counsel from March 1997 to April 1998 and as Secretary from July 1997 to April 1998. Prior to joining us, she was a partner in the law firm of Baker, Donelson, Bearman, Caldwell, & Berkowitz, P.C.

Steven G. Dean

Senior Vice President and Chief Financial Officer

Mr. Dean has served as Senior Vice President and Chief Financial Officer since July 1, 2007. He served as Vice President and Chief Financial Officer from July 2006 to July 2007. He served as Vice President and Controller from February 2006 to July 2006. Mr. Dean served as Company Controller from December 2005 to February 2006. Previously, he served as Controller for

15

Douglas L. Dowdell

Senior Vice President, Specialty Fibers

Mr. Dowdell has served as Senior Vice President, Specialty Fibers since February 1, 2006. He served as Senior Vice President, Nonwovens from February 2005 to February 2006. He served as Vice President, Nonwovens from October 2003 to February 2005. He served as Vice President, Absorbent Wood Fiber Sales from February 2002 to October 2003. He served as Vice President, Nonwovens Business Development from February 2001 to February 2002. He served as Vice President, Absorbent Products Business Development from August 2000 to February 2001. Prior to August 2000 he held several positions in the Company including: Manager, Absorbent Fiber Sales; Manager, Business Development; and Manager, Wood Procurement. He was an employee of Procter & Gamble from 1988 to March 1993.

Paul N. Horne

Senior Vice President, Product and Market Development

Mr. Horne has served as Senior Vice President, Product and Market Development since February 1, 2006. He served as Senior Vice President, Cotton Cellulose from January 2001 to February 2006. He served as Senior Vice President, Commercial - Specialty Cellulose from July 1997 to January 2001 and as Vice President, North and South American Sales from October 1995 to July 1997. He was an employee of Procter & Gamble from 1982 to March 1993.

Marko M. Rajamaa

Senior Vice President, Nonwovens

Mr. Rajamaa has served as Senior Vice President, Nonwovens since October 26, 2006. He served as Vice President, Nonwovens from February 2006 to October 2006 and as Vice President, Nonwovens Sales – Europe and Middle East from January 2002 to February 2006. Previously, he served as Manager, Nonwoven Sales, Europe, Middle East and Africa from 1999 to 2002. Prior to joining Buckeye in 1999, he held various sales management positions with Walkisoft / UPM-Kymmene.

16

PART II

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock is traded on the New York Stock Exchange under the symbol BKI. There were approximately 7,125 shareholders on August 20, 2010, based on the number of record holders of our common stock and an estimate of the number of individual participants represented by security position listings. The table below sets forth the high and low sales prices for our common stock.

|

Year Ended June 30

|

|||||||||||||

|

2010

|

2009

|

||||||||||||

|

High

|

Low

|

High

|

Low

|

||||||||||

|

First quarter (ended September 30)

|

$

|

11.32

|

$

|

4.56

|

$

|

10.51

|

$

|

7.29

|

|||||

|

Second quarter (ended December 31)

|

12.09

|

8.12

|

8.71

|

3.14

|

|||||||||

|

Third quarter (ended March 31)

|

13.08

|

10.18

|

4.74

|

1.65

|

|||||||||

|

Fourth quarter (ended June 30)

|

15.17

|

9.95

|

5.66

|

2.15

|

|||||||||

We did not make any dividend payments during the years ended June 30, 2010 or 2009. On August 3, 2010, our Board of Directors declared a quarterly dividend of $0.04 per share of common stock. The dividend is payable on September 15, 2010 to stockholders of record as of the close of business on August 16, 2010. Each quarterly dividend payment is subject to review and approval by our Board of Directors, and we evaluate our dividend payment amount on an annual basis at the end of each fiscal year. Our 2013 notes limit the funds available to make dividend payments. We did not repurchase any shares of our common stock during the year ended June 30, 2010 and we repurchased 0.1 million shares during the year ended June 30, 2009. At June 30, 2010, we have remaining approximately 5.6 million shares that we are authorized by our Board of Directors to repurchase. The amount we distribute as dividends and the number of shares that we ultimately repurchase will depend on our financial results and ability to comply with certain conditions under our most restrictive debt agreements at the time of distribution or repurchase.

See the table labeled ‘Equity Compensation Plan Information” to be contained in the 2010 Proxy Statement, incorporated by reference in Part III, Item 12 of this Annual Report on Form 10-K.

Part II, Item 12 of this Annual Report on Form 10-K is incorporated herein by this reference.

17

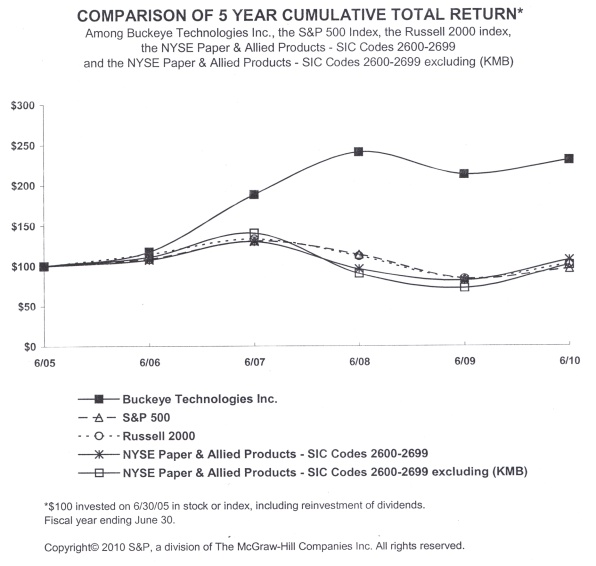

Performance Graph

The line graph below compares the cumulative total stockholder return on our common stock with the cumulative total return of the Standard & Poor’s 500 Index, the Russell 2000 Index, the New York Stock Exchange (“NYSE”) Paper & Allied Products peer group, and the New York Stock Exchange (“NYSE”) Paper & Allied Products peer group excluding KMB for the five fiscal years ended June 30, 2010. The graph and table assume that $100 was invested on June 30, 2005 in each of our common stock, the Standard & Poor’s index, the Russell 2000 Index, the NYSE Paper & Allied Products peer group and the NYSE Paper & Allied Products peer group excluding KMB and that all dividends were reinvested.

|

|

2005

|

2006

|

2007

|

2008

|

2009

|

2010

|

||

|

Buckeye Technologies Inc.

|

100.00

|

117.48

|

188.45

|

241.08

|

213.41

|

231.03

|

|

|

S&P 500

|

100.00

|

108.63

|

131.00

|

113.81

|

83.98

|

96.09

|

|

|

Russell 2000

|

100.00

|

114.58

|

133.41

|

111.80

|

83.84

|

101.85

|

|

|

NYSE Paper & Allied Products – SIC Codes 2600-2699 (U.S. & Foreign Cos.) excluding KMB

|

100.00

|

107.22

|

130.01

|

96.03

|

81.56

|

106.82

|

|

|

NYSE Paper & Allied Products - SIC Codes 2600-2699 (U.S. & Foreign Cos.)

|

100.00

|

110.80

|

140.46

|

90.14

|

72.26

|

100.68

|

|

18

We are transitioning from the S&P 500 as our broad-based index to the Russell 2000. We believe that the Russell 2000 index provides a more relevant benchmark for a company of our size. Buckeye Technologies Inc. is included in the Russell 2000 index. We are also transitioning our peer group from NYSE Paper and Allied Products SIC codes 2600 – 2699 to NYSE Paper and Allied Products SIC Codes 2600 – 2699 excluding Kimberly-Clark Corporation (“KMB”). We believe that due to KMB’s large market capitalization relative to the other companies in the peer group, the peer group results are skewed towards KMB’s results and as such are not as relevant a benchmark for our performance.

Item 6. Selected Financial Data

Selected Financial Data

|

In thousands, except per share data

|

Year Ended June 30

|

|||||||||||||||

|

2010(a)

|

2009(b)

|

2008(c)

|

2007 (d)

|

2006 (e)

|

||||||||||||

|

Operating Data:

|

||||||||||||||||

|

Net sales

|

$

|

756,426

|

$

|

754,529

|

$

|

825,517

|

$

|

769,321

|

$

|

728,485

|

||||||

|

Operating income (loss)

|

146,466

|

(22,639

|

)

|

100,333

|

81,211

|

44,420

|

||||||||||

|

Net income (loss)

|

114,574

|

(65,388

|

)

|

47,102

|

30,118

|

1,980

|

||||||||||

|

Basic earnings (loss) per share

|

$

|

2.95

|

$

|

(1.69

|

)

|

$

|

1.21

|

$

|

0.80

|

$

|

0.05

|

|||||

|

Diluted earnings (loss) per share

|

$

|

2.90

|

$

|

(1.69

|

)

|

$

|

1.20

|

$

|

0.79

|

$

|

0.05

|

|||||

|

Balance sheet data:

|

||||||||||||||||

|

Total assets

|

$

|

852,454

|

$

|

792,384

|

$

|

1,009,225

|

$

|

951,822

|

$

|

948,213

|

||||||

|

Total long-term debt and capital leases (including current portion)

|

$

|

237,332

|

$

|

327,465

|

$

|

394,268

|

$

|

445,893

|

$

|

522,090

|

||||||

|

Ratio of earnings to fixed charges (f)

|

7.3x

|

(52,264

|

)

|

$

|

2.9x

|

2.1x

|

$

|

(497

|

)

|

|||||||

|

(a)

|

Includes a pretax charge of $3,353 ($2,095 after tax) for restructuring costs. Includes a pretax benefit of $77,677 ($76,791 after tax) for alternative fuel mixture credits. Includes a pretax charge of $2,606 ($1,629 after tax) for early extinguishment of debt. Includes an after tax benefit of $5,415 for investment tax credits on prior period energy project expenditures.

|

|

(b)

|

Includes a pretax charge of $138,008 ($127,598 after tax) for goodwill impairment. Includes a pretax benefit of $54,232 ($39,644 after tax) for alternative fuel mixture credits. Includes a pretax benefit of $401 ($261 after tax) for early extinguishment of debt.

|

|

(c)

|

Includes a pretax charge of $623 ($392 after tax) for early extinguishment of debt.

|

|

(d)

|

Includes a pretax benefit of $2,000 ($1,274 after tax) from a water conservation partnership payment. Includes $1,867 ($1,171 after tax) from reversal of accrued interest related to cancellation of a contingent note. Includes a pretax charge of $1,249 ($812 after tax) for restructuring costs and $832 ($521 after tax) for early extinguishment of debt.

|

|

(e)

|

Includes a pretax charge of $5,616 ($3,497 after tax) for restructuring and impairment costs.

|

|

(f)

|

Earnings were inadequate to cover fixed charges during fiscal years 2009 and 2006. Amount reflects the deficit of earnings to fixed charges. See Exhibit 12.1 for computation.

|

19

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following Management's Discussion and Analysis of Results of Operations and Financial Condition ("MD&A") summarizes the significant factors affecting our results of operations, liquidity, capital resources and contractual obligations, as well as discussing our critical accounting policies. This discussion should be read in conjunction with the Consolidated Financial Statements, Notes to the Consolidated Financial Statements, and other sections of this Annual Report on Form 10-K. Our MD&A is composed of four major sections; Executive Summary, Results of Operations, Financial Condition and Critical Accounting Policies and Estimates. Unless otherwise indicated, references to a year (e.g., “2010”) refers to our fiscal year ended June 30 of that year.

Executive Summary

We manufacture and distribute value-added cellulose-based specialty products used in numerous applications, including disposable diapers, personal hygiene products, engine, air and oil filters, concrete reinforcing fibers, food casings, cigarette filters, rayon filaments, acetate plastics, thickeners and papers. Our products are produced in the United States, Canada, Germany and Brazil, and we sell these products in approximately 60 countries worldwide. We generate revenues, operating income and cash flows from two reporting segments: specialty fibers and nonwoven materials. Specialty fibers are derived from wood and cotton cellulose materials using wetlaid technologies. Our nonwoven materials are derived from wood pulps, synthetic fibers and other materials using an airlaid process.