Attached files

| file | filename |

|---|---|

| EX-5.1 - PERPETUAL TECHNOLOGIES, INC. | v212027_ex5-1.htm |

| EX-23.2 - PERPETUAL TECHNOLOGIES, INC. | v212027_ex23-2.htm |

| EX-23.3 - PERPETUAL TECHNOLOGIES, INC. | v212027_ex23-3.htm |

As

filed with the Securities and Exchange Commission on February 18,

2011

Registration No.

333-168028

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

AMENDMENT

NO. 6 TO

FORM

S-1

REGISTRATION

STATEMENT UNDER

THE

SECURITIES ACT OF 1933

CHINA

SLP FILTRATION TECHNOLOGY, INC.

(Exact

name of registrant as specified in its charter)

|

Delaware

|

6770

|

84-1465393

|

||

|

(State or Other Jurisdiction of

|

(Primary Standard Industrial

|

(I.R.S.

Employer

|

||

|

Incorporation or Organization)

|

Classification Code Number)

|

Identification Number)

|

Shishan

Industrial Park

Nanhai

District

Foshan

City

Guangdong

Province, PRC

86-757-86683197

(Address,

including zip code, and telephone number including area code,

of

registrant’s principal executive offices)

Vcorp

Services, LLC

1811

Silverside Road

Wilmington,

Delaware 19801

(888)

528-2677

(Name,

address, including zip code, and telephone number including area

code, of

agent for service)

Copies

to:

|

Louis

A. Bevilacqua, Esq.

|

||

|

Darren

Ofsink, Esq.

|

Joseph

R. Tiano, Esq.

|

|

|

Guzov

Ofsink, LLC

|

Jing

Zhang, Esq.

|

|

|

900

Third Avenue, 5th Floor

|

Pillsbury

Winthrop Shaw

|

|

|

Pittman

LLP

|

||

|

New

York NY 10022

|

2300

N Street, NW

|

|

|

Tel:

(212) 371-8008

|

Washington,

DC 20037

|

|

|

Fax:

(212) 688-7273

|

Telephone

(202) 663-8000

|

|

|

Facsimile

(202) 663-8007

|

Approximate

date of commencement of proposed sale to the public: As soon as practicable

after this Registration Statement becomes effective.

If any of

the securities being registered on this Form are to be offered on a delayed or

continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the

following box: x

If this

Form is filed to register additional securities for an offering pursuant to Rule

462(b) under the Securities Act, check the following box and list the Securities

Act registration statement number of the earlier effective registration

statement for the same offering. ¨

If this

Form is a post-effective amendment filed pursuant to Rule 462(c) under the

Securities Act, check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same

offering. ¨

If this

Form is a post-effective amendment filed pursuant to Rule 462(d) under the

Securities Act, check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same

offering. ¨

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer or a smaller reporting company. See

definitions of “large accelerated filer”, “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act.

|

Large

Accelerated Filer ¨

|

Accelerated

Filer ¨

|

|

Non-Accelerated

Filer ¨

|

Smaller

Reporting Company x

|

|

CALCULATION OF REGISTRATION FEE

|

||||||||

|

Title of Each Class of Securities to Be

Registered

|

Proposed Maximum

Aggregate

Offering Price(1)(2)(3)

|

Amount of

Registration

Fee

|

||||||

|

Common stock, $0.001

par value per share (4)

|

$ | 35,760,019 | (4) | $ | 2,550 | (5) | ||

|

Underwriter’s

warrants and underlying shares of common stock (6)

|

1,822,917 | (7) | 151 | (8) | ||||

|

Total

|

$ | 2,701 | (9) | |||||

|

|

(1)

|

Estimated solely for the purpose

of calculating the registration fee pursuant to Rule 457(o). In accordance

with Rule 457(g) under the Securities Act, because the shares of our

common stock underlying the Underwriter’s Warrants (as defined below) are

registered hereby, no separate registration fee is required with respect

to the warrants registered

hereby.

|

|

|

(2)

|

In accordance with Rule 416(a),

the registrant is also registering hereunder an indeterminate number of

additional shares of common stock that may be issued and resold pursuant

to stock splits, stock dividends, anti-dilution provisions, including the

anti-dilution provisions under the Underwriter’s Warrants (as defined

below), and similar

transactions.

|

|

|

(3)

|

The registration fee for

securities to be offered by us is based on an estimate of the Proposed

Maximum Aggregate Offering Price of the securities, and such estimate is

solely for the purpose of calculating the registration fee pursuant to

Rule 457(o).

|

|

|

(4)

|

We

are registering the following shares of common stock: (i)

4,166,667 shares are being registered in connection with the firm

commitment offering; (ii) 625,000 shares are being registered for issuance

in connection with the underwriter’s over-allotment option and (iii)

369,725 shares being registered under a separate resale prospectus (the

“Resale Prospectus”) for resale by the selling stockholders named in the

Resale Prospectus.

|

The

proposed maximum aggregate offering price for these shares has been calculated

as follows:

|

4,166,667

X $7

|

(the

maximum offering price for these shares)

|

=

|

$29,166,669

|

|

625,000

X $7

|

(the

maximum offering price for these shares)

|

=

|

4,375,000

|

|

369,725

X $6

|

(the

fixed resale price for these shares)

|

=

|

2,218,350

|

|

Total

|

$35,760,019

|

|

|

(5)

|

The

amount of the registration fee for these shares was calculated by

multiplying $35,760,019 by .0000713 for an amount of

$2,550.

|

|

|

(6)

|

We have agreed to issue

warrants to the underwriters (the “Underwriter’s Warrants”) for

nominal consideration. The exercise price of the Underwriter’s

Warrants is equal to 125% of the price of the common stock offered

hereby. The resale of the Underwriter’s Warrants is registered

hereunder. The Underwriter’s Warrants will be exercisable for four years

commencing one year from the effective date of the registration statement

and will therefore cease to be exercisable five years after the effective

date of the registration statement. The shares of our common stock

underlying the Underwriter’s Warrants are deemed to have the same issuance

date as the warrants and are being registered on a delayed or continuous

basis pursuant to Rule 415 under the Securities Act of 1933, as amended.

See

“Underwriting.”

|

|

|

(7)

|

The

proposed maximum aggregate offering price for the underwriter’s warrant is

$1,822,917, which equals 125% of $1,458,333. $1,458,333

represents 5% of $29,166,669 (which represents the offering of 4,166,667

shares of common stock at a proposed maximum offering price of $7 per

share).

|

|

|

(8)

|

We

have calculated the registration fee by multiplying $1,358,696 (the

maximum aggregate offering price included in the calculation of the

registration fee for our previous filing) by .0000713 which amount comes

to $97. The registration fee for the increase of $464,221

($1,822,917 less $1,358,696) in the proposed maximum aggregate price has

been multiplied by .0001161 for a total of $54. Accordingly,

the total comes to $151.

|

| (9) | Previously paid. |

THE

REGISTRANT HEREBY AMENDS THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS

MAY BE NECESSARY TO DELAY ITS EFFECTIVE DATE UNTIL THE REGISTRANT SHALL FILE A

FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THIS REGISTRATION STATEMENT

SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(a) OF THE

SECURITIES ACT OF 1933, AS AMENDED, OR UNTIL THIS REGISTRATION STATEMENT SHALL

BECOME EFFECTIVE ON SUCH DATE AS THE COMMISSION, ACTING PURSUANT TO SAID SECTION

8(a), MAY DETERMINE.

Explanatory

Note

This

Registration Statement includes two forms of prospectus as set forth

below:

|

|

·

|

Prospectus. The first prospectus

relates to an underwritten offering of shares of common stock by China SLP

Filtration Technology, Inc. through the underwriter named on the cover

page of the prospectus.

|

|

|

·

|

Resale

Prospectus. The

second prospectus relates to the resale of 369,725 shares of common stock

by the selling stockholders named therein. These shares will

be offered and sold at a fixed price of $6 until our common stock becomes

quoted on the Over-the-Counter Bulletin Board or listed on an

exchange.

|

None of

the underwriters named or referenced in the prospectus is participating or

acting as underwriter, dealer or broker in connection with the sale of the

shares to be sold pursuant to the resale prospectus.

The

resale prospectus and the prospectus are substantively identical, except for the

following principal differences:

|

|

·

|

each contains different outside

and inside front covers;

|

|

|

·

|

each contains different

“Offering” sections in the “Prospectus Summary” section beginning on page

1 for the prospectus and page A-1 for the resale

prospectus;

|

|

|

·

|

each contains different “Use

of Proceeds” sections on page 25 for the prospectus and Page A-26 for

the resale prospectus.

|

|

|

·

|

the “Capitalization” and

“Dilution” sections on pages 27 and 28, respectively, of the

prospectus are deleted from the resale

prospectus;

|

|

|

·

|

a “Selling Stockholder”

section is included in the resale prospectus beginning on page

A-27;

|

|

|

·

|

references to the prospectus will

be replaced in the resale prospectus with references to the resale

prospectus;

|

|

|

·

|

the “Underwriting” section in

the prospectus beginning on page 98 is deleted from the resale

prospectus and a “Plan of Distribution” is inserted in its place on page

A-97.

|

|

|

·

|

the “Legal Matters” section in

the resale prospectus on page A-103 deletes the reference to counsel

for the underwriters; and

|

|

|

·

|

the outside back cover of the

prospectus is deleted from the resale

prospectus.

|

The

registrant has included in this registration statement, after the financial

statements, a set of alternate pages to reflect the foregoing differences of the

resale prospectus as compared to the prospectus.

The

information in this prospectus is not complete and may be changed. We may not

sell these securities until the registration statement filed with the Securities

and Exchange Commission is effective. This prospectus is not an offer to sell

these securities and is not soliciting an offer to buy these securities in any

jurisdiction where the offer or sale is not permitted.

Subject

to Completion, Dated February 18, 2011

4,166,667

Shares

CHINA SLP FILTRATION

TECHNOLOGY, INC.

Common

Stock

This

is our initial public offering. We are offering 4,166,667

shares of our common stock. No public market currently exists for our common

stock.

We currently

anticipate the public offering price of our common stock will be between $5.00

and $7.00 per share.

We have

applied to have our common stock listed on the NASDAQ Capital Market under the

symbol “SLPC.”

Investing

in our common stock involves a high degree of risk. See the section entitled

“Risk Factors” beginning on page 6.

|

|

Per Share

|

Total

|

|||||

|

Public

offering price

|

$

|

|

$

|

|

|||

|

Underwriting

discount

|

$

|

|

$

|

|

|||

|

Proceeds,

before expenses, to us

|

$

|

|

$

|

|

|||

We have

granted the underwriters a 45-day option to purchase up to 625,000 additional

shares of common stock from us at the initial public offering price less the

underwriting discount and commission.

In

connection with this offering, we have agreed to issue to the underwriters a

warrant to purchase up to 5% of the shares sold pursuant to the offering

(excluding the over-allotment) at $ per share (125% of the price of the

shares sold in the offering), which may be exercised on the

first anniversary of the date of this prospectus and expiring four years

after such anniversary.

Under the

terms of a consulting agreement between us and United Best Investment

Limited, a Hong Kong company controlled by Li Jun, one of our directors, on the

closing of this offering United Best shall receive a fee of $

, which represents 3% of the gross proceeds of this offering.

Delivery

of our shares will be made on or about , 2011.

Neither

the Securities and Exchange Commission nor any state securities commission has

approved or disapproved of these securities or passed upon the accuracy or

adequacy of this prospectus. Any representation to the contrary is a criminal

offense.

Brean

Murray, Carret & Co.

The

date of this prospectus is ,

2011

TABLE

OF CONTENTS

|

Prospectus

Summary

|

1

|

|

Risk

Factors

|

6

|

|

Caution

Regarding Forward Looking Statements and Other Information Contained in

this Prospectus

|

25

|

|

Use

of Proceeds

|

25

|

|

Determination

of Offering Price

|

25

|

|

Dividend

Policy

|

26

|

|

Exchange

Rate Information

|

26

|

|

Capitalization

|

27

|

|

Dilution

|

28

|

|

Market

Price of our Common Stock and Related Stockholder

Matters

|

29

|

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

31

|

|

Our

Corporate History

|

43

|

|

Business

|

47

|

|

Additional

Disclosure Regarding Conversion of Notes and Exercise of

Warrants

|

63

|

|

Management

|

72 |

|

Shares

Eligible for Future Sale

|

78

|

|

Executive

Compensation

|

79

|

|

Certain

Relationships and Related Transactions

|

83

|

|

Security

Ownership of Certain Beneficial Owners and Management

|

85 |

|

Description

of Securities

|

88

|

|

Material

United States Federal Income Tax Considerations

|

91

|

|

Material

PRC Income Tax Considerations

|

95

|

|

Underwriting

|

98

|

|

Legal

Matters

|

104

|

|

Service

of Process and Enforcement of Judgments

|

104

|

|

Experts

|

104

|

|

Where

You Can Find More Information

|

104

|

|

Index

to Financial Statements

|

F-1

|

You

should rely only on the information contained in this prospectus. We have not

authorized anyone to provide you with additional or different information. This

prospectus is not an offer to sell, nor is it seeking an offer to buy, these

securities in any state where the offer or sale is not permitted.

This

prospectus includes market size, market share and industry data that we have

obtained from market research, publicly available information and various

industry publications. The third party sources from which we have obtained

information generally state that the information contained therein has been

obtained from sources believed to be reliable. We have not independently

verified any of the data from third party sources nor have we verified the

underlying economic assumptions relied upon by those third parties. Similarly,

industry forecasts and market research, which we believe to be reliable based

upon management’s knowledge of the industry, have not been verified by any

independent sources.

PROSPECTUS

SUMMARY

This summary highlights selected

information contained elsewhere in this prospectus. This summary does not

contain all the information that you should consider before deciding to invest

in our common stock. You should read the entire prospectus carefully, including

“Risk Factors” beginning on page 6 and our consolidated financial

statements and notes to those consolidated financial statements, before making

an investment decision. Unless otherwise indicated, all share amounts and prices

described in this prospectus have been adjusted to reflect a 1-for-5

reverse stock split of our common stock effected on March 24,

2010.

References

in this prospectus to “China SLP Filtration,” “the Company,” “we,” “us” or “our”

refer to China SLP Filtration Technology, Inc. and its consolidated

subsidiaries, unless the context requires otherwise.

Our

Company

We are a

manufacturer of nonwoven fabrics in China. Nonwoven fabrics, or nonwovens,

are synthetic fabrics, such as felt and polyester, which are neither woven

nor knitted, but instead are made from long fibers, bonded together by

chemical, mechanical, heat or solvent treatment.

We

currently manufacture two types of PET nonwoven fabrics which are used in a wide

range of products, including filtration products, road construction materials,

home furnishings, automobile interior insulation and industrial packaging.

Our current PET products are sold primarily to PRC-based manufacturers

which use our products as raw material components for end-products they sell to

their customers operating in the heavy industrial, automotive, construction and

home furnishing industries.

We

recently developed a process to manufacture PPS nonwoven fabric, which is the

key product line around which our long-term growth strategy is centered.

We believe that this manufacturing process is proprietary and have applied for a

process patent in the PRC and intend to apply for a process patent in the U.S.

and Europe. PPS nonwoven fabric is a heat resistant, corrosion-proof and

flame retardant fabric, and can be used to manufacture dust filter bags for

pollutant dust removal and emissions controls in coal-fired power plants,

garbage incinerators and cement factories.

The PRC

government recently adopted stringent environmental regulations governing the

discharge of carbon and other emissions by coal-fired power plants and other

heavy industrial plants. Under these new regulations, which came into

effect on January 1, 2010, pollutant emissions cannot exceed 50 milligrams per

cubic meter. We believe, based on an article published in China Nonwoven & Industrial

Textile (CNIT) in 2010, that less than 10% of the coal-fired

boilers in China were equipped with dust removal filtration bags and less than

10% of the bag filters in use were made from PPS fiber.

Bag

filters can be used as a cost effective way of meeting the new emission and dust

pollutant standards in the PRC because the installation of bag filters

is significantly cheaper than installing costly pollutant dust removal

equipment, such as engineered scrubbing systems, which we believe could be cost

prohibitive for smaller plant operators.

Based on

lab tests which we conducted internally, we believe that our PPS nonwoven fabric

is superior to other currently available high temperature filtration material

because it is lighter, thicker, stronger, has higher air permeability and

filtration efficiency and is significantly cheaper to produce. Due to

the superior characteristics of our PPS product coupled with the demand created

by these new regulations, we believe that our PPS material will become a market

leader for high temperature filtration applications.

We intend

to continue to manufacture PET nonwovens, but we expect the sales of our PPS

nonwoven fabrics to ultimately eclipse the sales of our existing PET nonwoven

products and become our main product offering.

1

Our

Growth Strategy

Our

growth strategy is as follows:

|

|

·

|

We plan to commence production of

PPS nonwovens in the early part of 2011 for sale to PRC-based operators of

coal-fired power plants, garbage incinerators and other manufacturers that

are not in compliance with new PRC environmental

regulations;

|

|

|

·

|

We plan to expand our PPS

nonwoven manufacturing facilities and install three new production lines

to manufacture PPS nonwoven material, increasing our total annual

manufacturing capacity from 8,000 tons to 11,600 tons of nonwoven

material; and

|

|

|

·

|

We intend to capitalize on our

proprietary technology by developing and commercializing our nonwoven

products for use in numerous

applications.

|

Our

Competitive Strengths

We

believe our competitive strengths are as follows:

|

|

·

|

We offer high quality PET

products with lower production and operational costs than products offered

by our competitors;

|

|

|

·

|

Bag filters made of our PPS

material offer plant operators a cost effective alternative to meet new

emission and dust pollutant standards in the PRC because using PPS bag

filters is significantly cheaper than installing pollutant dust

removal equipment;

|

|

|

·

|

We believe, based on laboratory

tests which we conducted internally, that our PPS material is superior to

other high temperature filtration material currently available for use in

bag filters because it is lighter, thicker, stronger, has higher air

permeability and filtration efficiency, and is significantly cheaper

to produce;

|

|

|

·

|

We can offer our products at

attractive pricing points because our PPS fabric, which like alternative

products is priced according to weight, is lighter than alternative

products; and

|

|

|

·

|

We believe that our proprietary

manufacturing processes give us a competitive advantage over our

competitors and act as a barrier to

entry.

|

Risk

Factors

The

implementation of our growth strategy and our ability to grow based on our

competitive strengths remain subject to a variety of external and internal

challenges. Accordingly, investing in our common stock involves significant

risks. Some of the challenges and risks we face are listed below:

|

|

·

|

We need to raise capital to fully

commercialize our PPS manufacturing process and cannot grow and execute

our strategic plan if we fail to do

so.

|

|

|

·

|

We have a limited operating

history and no experience manufacturing PPS nonwoven fabric so it is

difficult to evaluate our future prospects and historical results of

operations.

|

|

|

·

|

Our success depends in part on

market acceptance of our PPS nonwoven fabric as a preferred material for

use in dust filter bags.

|

|

|

·

|

If we have miscalculated the

future demand for our products, we may wind up unnecessarily spending a

significant amount of funds on the expansion of our PPS manufacturing

facilities.

|

|

|

·

|

We are subject to risks of

conducting business in

China.

|

|

|

·

|

We have significant outstanding

short-term borrowings and we may not be able to obtain extensions when

this debt matures.

|

|

|

·

|

Enforcement against us or our

directors and officers may be difficult and investors could be unable to

collect amounts due in the event we or any of our directors or officers

violates applicable law.

|

2

|

|

·

|

Our executive officers and

directors beneficially own a significant portion of our common stock and

may take actions that are contrary to an investor's interests and could

reduce the value of our

stock.

|

|

|

·

|

We are a “controlled company” as

such term is defined under the Nasdaq Marketplace Rules and our board of

directors does not and will not have a majority of independent directors.

Accordingly, the Company will lack the checks and balances that an

independent Board can bring to management’s decision making

process.

|

You

should carefully consider the risks described in “Risk Factors” beginning on

page 6 before making a decision to invest in our common stock. If any of

these risks actually occurs, our business, financial condition or results of

operations would likely be materially adversely affected. In such case, the

trading price of our common stock would likely decline, and you may lose all or

part of your investment.

Our

Industry

The

nonwoven fabric industry in the PRC is large and growing, driven primarily by

China’s continued economic development. China has experienced rapid economic and

industrial growth in the past 30 years. China’s output of iron and steel,

cement, coal, fertilizer and power generation all currently rank as first or

second in the world (Source:

US Department of Commerce and US Department of the Interior). China’s

consumption of raw materials currently ranks second in the world (Source: Report from the EIA Energy

Information Administration). Due to outdated technology and equipment in

China’s chemical, raw materials and energy industries, China has encountered

problems of inefficient utilization of energy and resources, as well as heavy

pollution due to accelerated urbanization. Reducing emission pollution has been

a focus for the Chinese Central Government for several years and is expected to

remain a focus moving forward. As China’s government imposes stricter policies

on environmental protection, industrial gas and dust emission limits have become

stricter. We believe this creates a significant market opportunity for the

commercialization of our PPS nonwovens materials.

Corporate

Information

Our

executive offices are located at Shishan Industrial Park, Nanhai District,

Foshan City, Guangdong Province, People’s Republic of China, or PRC, and

our telephone number is +86-757-86683197. Our website address is www.silepu.com

and the information contained therein or connected thereto shall not be deemed

to be incorporated into this prospectus or the registration statement of which

it forms a part.

3

The

Offering

|

Common

stock offered by us

|

4,166,667 shares

(4,791,667 shares if the representative of the underwriters

exercises its over-allotment option in full).

|

|

|

Common

stock outstanding immediately after this offering

|

21,814,562 shares,

including (i) 15,265,714 shares of common stock currently outstanding,

(ii) 1,923,809 shares issuable on conversion of the notes in the aggregate

principal amount of $4,040,000, (iii) 4,166,667 shares to be issued in the

offering, and (iv) 193,186 shares to be issued to United Best and 265,186

shares to be issued to Primary Capital on the closing of the

offering.

|

|

|

Use

of proceeds

|

We

intend to use the net proceeds from this offering (i) to repay a

short term loan in the amount of $3.9 million which was used as part of

the purchase price of approximately $9.6 million for the build-out and

purchase of a new production line to manufacture PPS materials which is

currently being installed and is expected to be completed in February

2011; and (ii) to purchase two additional production lines to

manufacture PPS materials. The balance of the net proceeds is

expected to be used for working capital and general corporate

purposes. See “Use of Proceeds” on page 25 for more

information.

|

|

|

Over-allotment

option

|

We

have granted the underwriters an option, exercisable for 45 days after the

date of this prospectus, to purchase up to an additional 625,000 shares of

common stock to cover over-allotments.

|

|

|

Listing

|

We

have applied to have our common stock listed on the NASDAQ Capital

Market.

|

|

|

Lock-up

Agreement

|

We

and each of our directors, executive officers and certain principal

stockholders have agreed, subject to certain exceptions, not to, including

not to announce an intention to, for a period of 90 days from the

date of this prospectus, sell, transfer or otherwise dispose of any shares

of our common stock without the prior written consent of the underwriters’

representative. See “Underwriting.”

|

|

|

Risk

factors

|

Investing

in these securities involves a high degree of risk. As an investor you

should be able to bear a complete loss of your investment. You should

carefully consider the information set forth in the “Risk Factors” section

beginning on page 6.

|

4

Summary

Consolidated Financial Information

In the

table below we provide you with historical consolidated financial data for the

fiscal years ended September 30, 2010 and 2009 and the three month periods ended

December 31, 2010 and 2009, derived from our audited and unaudited consolidated

financial statements included elsewhere in this prospectus. Historical

results are not necessarily indicative of the results that may be expected for

any future period. When you read this historical summary consolidated financial

data, it is important that you read it along with the appropriate historical

consolidated financial statements and related notes and “Management’s Discussion

and Analysis of Financial Condition and Results of Operations” included

elsewhere in this prospectus.

|

Three Months Ended

December 31,

(unaudited)

|

Fiscal Years Ended

September 30,

|

|||||||||||||||

|

2010

|

2009

|

2010

|

2009

|

|||||||||||||

|

Statement

of Operations Data:

|

||||||||||||||||

|

Net

sales

|

$ | 5,780,973 | $ | 5,224,961 | $ | 19,952,422 | $ | 11,849,712 | ||||||||

|

Cost

of sales

|

4,223,562 | 3,611,088 | 13,772,843 | 7,296,327 | ||||||||||||

|

Cost

of sales related party

|

- | - | - | 610,287 | ||||||||||||

|

Gross

profit

|

1,557,411 | 1,613,873 | 6,179,579 | 3,943,098 | ||||||||||||

|

Total

operating expenses

|

812,636 | 274,023 | 2,272,881 | 1,230,611 | ||||||||||||

|

Operating

income

|

744,775 | 1,339,850 | 3,906,698 | 2,712,487 | ||||||||||||

|

Total

other income (expenses)

|

(598,685 | ) | (58,791 | ) | (1,661,598 | ) | (266,835 | ) | ||||||||

|

Income

before income taxes

|

146,090 | 1,281,059 | 2,245,100 | 2,445,652 | ||||||||||||

| Income tax provision | 88,618 | - | 24,023 | - | ||||||||||||

|

Net

income

|

$ | 57,472 | $ | 1,281,059 | $ | 2,221,077 | $ | 2,445,652 | ||||||||

|

Net

income per common share, basic

and diluted

|

$ | 0.00 | $ | 0.09 | $ | 0.15 | $ | 0.17 | ||||||||

|

Pro

forma net income (loss) per common share,

basic

and diluted

|

$ |

0.03

|

$ | 0.09 | * | $ | 0.02 | N/A | ||||||||

|

Basic

shares outstanding

|

15,265,714 | 14,510,204 | 14,979,390 | 14,510,204 | ||||||||||||

|

Diluted

shares outstanding

|

17,189,523 | 14,510,204 | 16,227,061 | 14,510,204 | ||||||||||||

*The

pro forma net income (loss) per common share for the three months ended December

31, 2009 is the actual net income (loss) per common share as there was no

convertible notes transaction being recorded for the period.

|

Balance Sheet Data:

|

As of

December 31,

2010

(unaudited)

|

As of

December

31, 2010

Pro Forma

(unaudited) (1)

|

As of

December 31, 2010

Pro Forma

As adjusted

(unaudited)

(2)

|

|||||||||

|

Current

assets

|

$ | 12,315,773 | $ | 12,215,773 | $ | 30,315,773 | ||||||

|

Total

assets

|

29,161,692 | 29,061,692 | 47,161,692 | |||||||||

|

Current

liabilities

|

11,569,672 | 7,186,765 | 3,286,765 | |||||||||

|

Long-term

debt

|

- | - | - | |||||||||

|

Total

liabilities

|

11,569,672 | 7,186,765 | 3,286,765 | |||||||||

|

Total

stockholders’ equity

|

17,592,020 | 21,874,927 | 43,874,927 | |||||||||

(1) Pro forma information assumes conversion of the convertible notes into common stock on December 31, 2010 and the repayment of the convertible notes in the aggregate principal amount of $100,000 of with cash.

(2) Pro

forma as adjusted amounts represent December 31, 2010 amounts

adjusted to reflect (i) the conversion of our outstanding convertible notes in

the aggregate principal amount of $4,040,000 (the portion of the outstanding

notes with respect to which the maturity date has been extended to June 30,

2011) into 1,923,809 shares of common stock (at a conversion price of

$2.10 (based on an assumed offering price of $6.00)), (ii) receipt of net

proceeds from the offering estimated to be approximately $22,000,000 (based on

the assumed initial public offering price of $6.00 per share), not including any

proceeds from the shares that may be offered pursuant to the underwriters’

over-allotment option, and (iii) repayment of short-term bank loans of $3.9

million.

5

RISK

FACTORS

An

investment in our common stock involves a high degree of risk. You should

carefully consider the risks and uncertainties described below together with all

other information contained in this prospectus, including the matters discussed

under “Caution Regarding Forward Looking Statements and Other Information

Contained in this Prospectus,” before you decide to invest in shares of our

common stock. You should pay particular attention to the fact that we are a

holding company with substantial operations in China and are subject to legal

and regulatory environments that in many respects differ from those of the

United States. If any of the following risks, or any other risks and

uncertainties that are not presently foreseeable to us, actually occur, our

business, financial condition, results of operations, liquidity and our future

growth prospects would be materially and adversely affected. You should also

consider all other information contained in this prospectus before deciding to

invest in shares of our common stock.

Risks

Related to Our Business

We

need to raise capital to fully commercialize our PPS manufacturing process and

may not be able to fully execute on our growth strategy if we fail to do

so.

Our core

growth strategy is to commence production of PPS fabric and bag filters using

our proprietary manufacturing process for sale initially to the numerous

coal-fired power plants and subsequently to operators of garbage incinerators

and other potential users in the PRC that are not in compliance

with environmental regulations. We intend to use the

net proceeds raised in this offering to purchase PPS manufacturing

equipment and to repay a short-term loan used to purchase manufacturing

equipment and may need to raise additional capital in the future through public

or private equity offerings or debt financings. We cannot be certain that

additional funding will be available on acceptable terms, if at all. As of the

date of this prospectus, we believe the U.S. capital markets are facing many

difficulties. Potential sources of additional financing may be unwilling or

unable to provide us with the additional financing we need to fully carry out

our expansion plans. To the extent that we raise additional funds by issuing

equity securities, our stockholders may experience significant dilution and the

price of our common stock could decrease. Any debt financing, if available,

would result in us incurring interest expenses and we may be required to pledge

assets as security for the debt and may be constrained by restrictive financial

or operational covenants. If we are unable to raise additional capital, when

required, or on acceptable terms, we may have to significantly delay, scale back

or discontinue the development or the commercialization of our PPS product,

which would harm our business and future growth prospects.

Management

recently identified a material weakness in our internal control over financial

reporting which required a restatement of our financial statements.

If our internal controls and disclosure controls and

procedures continue to be ineffective, there may be errors in our

financial statements that could require a future restatement, our filings may

not be timely filed and investors may lose confidence in our reported financial

information, which could lead to a decline in our stock price.

Our

management identified material weaknesses and concluded that our internal

controls over financial reporting and our disclosure controls and procedures

were not effective as of March 31, 2010, June 30, 2010, September 30, 2010 and

December 31, 2010, respectively.

A

material weakness (within the meaning of PCAOB Auditing Standard No. 5) is a

deficiency, or a combination of deficiencies, in internal controls over

financial reporting, such that there is a reasonable possibility that a material

misstatement of our annual or interim financial statements will not be prevented

or detected on a timely basis. Because our current accounting department is

relatively new to U.S. GAAP and the related internal control procedures required

of U.S. public companies, our management has determined that they require

additional training and assistance in U.S. GAAP matters. Management has

determined that our internal audit function is also deficient due to

insufficient qualified resources to perform internal audit

functions.

6

These

material weaknesses resulted in our inability to detect accounting errors where

we failed to record on our financial statements a liability of $75,000 owed to

each of United Best and Primary Capital ($150,000 in total) for advisory

services rendered in connection with our private placement of convertible notes,

which closed on February 12, 2010, as selling, general and administrative

expenses for the interim period ended March 31, 2010 and nine month period ended

June 30, 2010. We also noted that a grant of 30,000 restricted shares of

common stock in June 2010 to one of our directors was not reflected in the

originally issued financial statements for the interim period ended June 30,

2010.

The

identification of these errors resulted in the restatement of (i) our interim

financial statements for the three month and nine month periods ended June 30,

2010 and 2009, as set forth in the Quarterly Report on Form 10-Q for the quarter

ended June 30, 2010 filed on August 16, 2010 and in this registration statement

previously filed on July 8, 2010, as amended on September 7, 2010 and October

15, 2010 and (ii) our interim financial statements for the three month and six

month periods ended March 31, 2010 and 2009, as set forth in the Quarterly

Report on Form 10-Q filed on May 24, 2010, as amended on May 26, 2010 and in

this registration statement previously filed on July 8, 2010, as amended on

September 7, 2010 and October 15, 2010. This error was not detected by our

internal control procedures.

We have

taken certain steps to resolve these material weaknesses,

including:

|

|

·

|

In August 2010, we hired

Eric Gan as our new chief financial

officer;

|

|

|

·

|

We are arranging necessary

training for our accounting department

staff;

|

|

|

·

|

We plan to engage external

professional accounting or consultancy firms to assist us in the

preparation of the U.S. GAAP accounts;

and

|

|

|

·

|

We have allocated financial and

human resources to strengthen the internal control structure and we have

been actively working with external consultants to assess our data

collection, financial reporting, and control procedures and to strengthen

our internal controls over financial

reporting.

|

We

believe that the foregoing steps will remediate the material weaknesses

identified above, and we will continue to monitor the effectiveness of these

steps and make any changes that our management deems appropriate. However, there

is no guarantee that these improvements will be adequate or successful or that

such improvements will be carried out on a timely basis. A material weakness in

our internal controls and procedures may lead to further accounting errors,

which in turn may result in further restatements of our financial statements.

Any of these possible outcomes could result in an adverse reaction in the

financial marketplace due to a loss of investor confidence in the reliability of

our reporting process, which could adversely affect the trading price of our

shares.

If

our PPS nonwoven fabric does not achieve wide market acceptance as a preferred

material for use in pollutant dust removal bag filters by operators of coal

fired power plants, incinerators, cement factories and other

potential users, anticipated profits will not materialize and our business will

suffer.

We

recently developed a manufacturing process to manufacture PPS nonwoven fabric.

We intend to commence commercial production of PPS material in the early part of

2011.

PPS

nonwoven fabric has many applications including high temperature filtration of

pollutant emissions and can be used as the material to manufacture high

temperature bag filters for coal-fired power plant emissions, garbage

incinerators and cement factories.

The PPS

material that we plan to produce is lighter, thicker, and stronger, has higher

air permeability and filtration efficiency and is significantly cheaper to

produce than other types of high temperature filtration materials currently

available in the market place.

Although

prototype bag filters made of our PPS product have been tested in laboratories,

they have not been tested on site by any potential end user and we do not expect

to develop prototype products for testing by any potential end user prior to

commence commercial production of PPS products. Our new PPS nonwoven fabric may

never achieve broad market acceptance, due to any number of factors, including

that the product may not be as effective as our initial testing indicates and

competitive material may be introduced which renders our PPS product too

expensive or obsolete.

7

If our

PPS material is not broadly accepted in the marketplace for its intended uses,

we may not achieve a competitive position in the market, anticipated profits

will not materialize and our business will suffer.

We

have a limited operating history and have no experience commercially

manufacturing PPS nonwoven fabric which is a key component of our growth

strategy which makes it difficult to evaluate our future prospects based on

historical results of operations.

Our

operating history is limited. We currently make two types of PET nonwoven

fabrics and we commenced production of one type of PET fabric in 2006 and a

second type of PET fabric in 2009. We have not yet begun to commercially

manufacture PPS nonwoven fabric. We plan to do so in the early part of 2011.

Accordingly, you should consider our future prospects and historical results in

light of the risks and uncertainties experienced by early-stage companies in

evolving markets such as our ability to:

|

|

·

|

develop and successfully

commercialize PPS nonwovens using our proprietary manufacturing

process;

|

|

|

·

|

achieve widespread market

acceptance of our PPS product for use in high temperature pollutant dust

removal bag filters;

|

|

|

·

|

increase awareness of our

products and continue to develop customer

loyalty;

|

|

|

·

|

respond to competitive market

conditions;

|

|

|

·

|

respond to changes in the

regulatory environment;

|

|

|

·

|

manage risks associated with

intellectual property

rights;

|

|

|

·

|

maintain effective control of our

costs and expenses;

|

|

|

·

|

raise sufficient capital to

sustain and expand our business;

and

|

|

|

·

|

attract, retain and motivate

qualified personnel.

|

If we are

unsuccessful in addressing any of these risks and uncertainties, our business

may be materially and adversely affected.

If

we cannot extend or renew our currently outstanding short-term loans or if our

convertible notes are not converted before their maturity date, we will have to

repay these loans with cash on hand or refinance them with another lender or

else face a default and potential foreclosure upon the collateral we

pledged.

In

January 2010, the Chinese government took steps to tighten the availability of

credit including ordering banks to increase the amount of reserves they hold and

to reduce or limit their lending. In addition, our convertible notes in the

principal amount of $4,040,000 mature on June 30, 2011. In December

2010, we repaid our outstanding short-term bank loans totaling RMB 25.4 million

and we applied for and obtained official approval for a six month bank loan in

the amount of RMB 20 million from the Foshan branch of the Agricultural Bank of

China. On December 8, 2010, we obtained a 90 day term loan from

Standard Chartered Bank in amount of RMB 6,000,000 for a term of 90 days which

loans is due in March 2011. We plan to extend this loan for another 90

days. Although these short-term bank loans contain no specific renewal

terms, in China, it is customary practice for banks and borrowers to negotiate

roll-overs or renewals of short-term loans on an on-going basis shortly

before they mature. Although we have renewed our short-term loans in the past,

we cannot assure you that we will be able to renew these loans in the future as

they mature. If we cannot renew them we will have to repay them with cash from

operations. We cannot assure you that our business will generate sufficient cash

to do so.

We expect

that the convertible notes will be converted into our common stock at the

closing of this offering. If, however, the convertible notes are not converted

before their maturity date, we believe we will be able to obtain additional

loans from a bank or raise funds from private sources to pay off the principal

and interest due on the notes. We cannot assure you, however, that this

will be the case and if we are unable to do so and if our business fails to

generate sufficient cash flow from operations to repay these notes, we will be

in default.

8

If we

default on these loans and convertible notes, we will incur interest and

penalties. In addition, as the loans are secured by our buildings and land if we

fail to repay these loans, the lender could take possession of the

collateral.

If

we have miscalculated the future demand for our products, we may end up

unnecessarily spending a significant amount of funds on PPS manufacturing

equipment which ultimately we may not have needed and which we may not be able

to resell.

We are

currently installing a new production line to produce PPS materials and

intend to use the net proceeds of this offering to purchase and install two

additional production lines to manufacture PPS materials. This will

increase our total annual manufacturing capacity from 8,000 tons to 11,600 tons

of nonwoven material. The scope and timing of our expansion plans are based on

our internal projections and estimated demand for our PPS products. If our

projections are incorrect and the actual demand for our PPS products is less

than projected, we may expend a significant amount of capital on equipment

which ultimately may not have been needed.

If we are unable to adequately

protect our intellectual property, we could lose a significant competitive

advantage and

competitors could use our processes and manufacture and market similar products

using similar processes, which could harm our market share and lower our

profits.

We hold a

number of authorized process patents and have a patent application

pending in the PRC for our PPS manufacturing process. We believe that

among our competitive strengths are the proprietary manufacturing processes

which we have developed and believe act as a barrier to entry for our potential

competitors. Our success depends, in part, on our ability to protect these

unique processes against competitors and to defend our intellectual property

rights when they are violated. If our pending patent application for

our PPS manufacturing process is not granted or if we fail to adequately protect

our existing process patents, competitors could use our processes, and

manufacture and market similar products using similar processes, which could

harm our market share and results of operations. Our competitors may challenge,

invalidate or avoid the application of any existing or future patents,

trademarks, or other intellectual property rights that we receive or license. In

addition, patent rights may not prevent our competitors from developing their

own processes that produce products that are similar or functionally equivalent

to our products. If we lose the protection of our intellectual property our

business would suffer.

If

PRC environmental regulations change and our PPS product was unable to meet

those regulatory changes, our PPS product could become obsolete and this would

harm our business and prospects.

To reduce

air pollution in China, the Chinese government recently implemented a policy

which imposes stricter rules on carbon and other emissions by coal-fired power

plants and others. Under these rules which came into effect on January 1, 2010,

carbon and other emissions are required to be less than 50 milligrams per cubic

meter by the end of 2010. Already, some of the larger, more developed cities,

such as Beijing and Tianjin have adopted more stringent rules requiring that

emissions be less than 30 milligrams per cubic meter. (Source: Electric Power, May issue,

2008.) We believe, based on laboratory testing, that our PPS

material satisfies current PRC governmental requirements and the more stringent

local standards. If those regulations were to change and our PPS product

were unable to meet those regulatory changes, our PPS product could become

obsolete and this would harm our business and prospects.

The

introduction by a competitor and market acceptance of a high temperature

resistant pollutant emission filtration material which was superior to our PPS

material would harm our business.

If a

competitor successfully introduces a product which is superior to our PPS

products, and that product achieved wide market acceptance, our PPS product

could become obsolete and the demand for them would decrease

significantly.

9

As

a manufacturer of components our revenues will decrease if there is less demand

for the end products in which our products are incorporated.

Our

existing PET nonwoven products are sold, and we expect our PPS products will be

sold, principally to customers that manufacture a wide range of end-use

products, including filtration products, road construction materials, home

furnishings, automobile interior insulation, and industrial packaging.

Therefore, we are subject to the general changes in economic conditions

affecting those industry sectors. If customers that operate in these industry

sectors experience a downturn in their business or if they utilize substitutes

for our products in their products, demand for our products and our business

results will suffer.

Increases

in the price of raw materials could reduce our profit margins if we cannot pass

the increases on to our customers in the form of higher prices for our

products.

Polyester

is the primary raw material used by us to manufacture most of our products. The

price of polyester fluctuates based on manufacturing capacity, demand and

the price of crude oil, among other things. Our PPS product will be made from

high quality polyphenylene sulfide resin, which we intend to purchase in the

United States. Accordingly, the cost of this raw material will fluctuate with

the value of the RMB against the dollar. Even where we are able to pass along at

least a portion of raw material price increases to some of our customers, there

is often a delay between the time we are required to pay the increased raw

material price and the time we are able to pass the increase on to our

customers. To the extent we are not able to pass along all or a portion of such

increased prices of raw materials, our cost of sales would increase and our

operating income would correspondingly decrease. We cannot assure you that the

price of polyester will not increase in the future or that we will be able to

pass on any increases to our customers.

There are only a small number of

suppliers of the raw materials which are required to manufacture our new PPS

product all of whom are based in the United States or Asia. We have not

entered into any long term supply agreements with any of these suppliers.

High demand for this polyphenylene-sulfide resin may result in us being unable

to obtain sufficient quantities of this polyphenylene-sulfide resin to meet our

customers’ demands for our PPS products which would harm our business.

We

recently developed a manufacturing process to manufacture PPS nonwoven fabric,

which is the key product line around which our long-term growth strategy is

centered. PPS is made from a high quality polyphenylene sulfide

resin which is currently not available in China and we will be required to

import from the United States and Asia. We have identified less than 10

suppliers in the U.S. and Asian market that can provide us with this

high quality polyphenylene-sulfide resin. This exposes us to

volatility in the price and availability of these raw materials. We have

not entered into any long term supply agreement with any of these

potential suppliers so high demand for this polyphenylene-sulfide

resin may result in us being unable to obtain sufficient quantities of this

polyphenylene-sulfide resin to meet our customers’ demands for our PPS products

which would harm our business. Supply interruptions could also arise

from shortages labor disputes or weather conditions affecting suppliers’

production, transportation disruptions, or other reasons beyond our

control. Additionally, these suppliers could also increase pricing

of their products, which would negatively affect our operating results if we

were not able to pass these price increases through to our

customers.

Increases

in energy prices will increase our operating costs and impair our financial

results if we cannot pass cost increases on to our customers in the form of

higher prices for our products.

We use a

significant amount of electricity, gasoline and other energy sources to

manufacture and transport our nonwoven products. We do not hedge our exposure to

higher prices via energy futures contracts. A substantial increase in the price

of fuel and other energy sources would increase our operating costs

and could negatively impact our profitability and cash flows if we cannot

pass the increases on to our customers.

10

Our

manufacturing capacity is limited so a breakdown in our machinery or material

interruption of business could prevent or limit our ability to manufacture our

products and cause us to lose revenue and profits and impair our relationships

with our customers.

We

manufacture all of our existing products and plan to manufacture our new PPS

products at our existing facility. We currently have three production lines in

operation which manufacture PET products and are currently installing a new

production line to manufacture our new PPS products. We plan to purchase

and install two additional production lines with the proceeds from this

offering. Any breakdown or disruption of our machinery, or interruption of

business due to fires, explosion, adverse weather conditions or other

catastrophic event, would result in us being incapable of manufacturing

nonwovens to meet our production requirements. This may cause us to lose revenue

and impair our relationships with our customers. Without our existing production

facilities, we would have no other means of manufacturing products until we were

able to restore the manufacturing capability at the facility or identify an

acceptable contract manufacturer. We do not carry business interruption

insurance to cover lost revenue and profits. Furthermore, any interruption in

production capability may require us to make large capital expenditures to

remedy the situation, which could have a negative effect on our profitability

and cash flows.

Our

insurance is inadequate so we could be exposed to significant losses if any of

our products cause personal injury or illness or if our property is

damaged.

We do not

maintain product liability insurance and our property and equipment insurance

does not cover the full value of our property and equipment, so we could be

exposed to significant losses if any of our products cause personal injury or

illness or if our property is damaged. Any such loss could harm our

business.

Increases

in our environmental compliance costs and violations of environmental

regulations by us could require us to change business practices, increase our

operating costs and lower our profits.

We use a

variety of chemicals in our manufacturing operations. As a result, we are

subject to a broad range of environmental laws and regulations. We

regularly incur costs to comply with these environmental regulations, and those

costs could increase significantly with changes in environmental regulations or

their interpretation or enforcement which could further

increase our operating costs and lower our profits.

Although

we have not been subject to material environmental claims in the past, if we

fail to comply with any present or future environmental regulations, damages,

fines and criminal sanctions could be assessed against us and production could

be suspended and our operations could cease. New regulations could also require

us to acquire costly equipment or to incur other significant expenses which

would lower our profits.

We

rely on Mr. Jie Li, our chief executive officer, to manage our business, and if

we lose his services, our business and prospects could suffer.

We

depend, to a large extent, on the abilities and participation of our current

management team, but have a particular reliance upon Mr. Jie Li, our chief

executive officer, for the direction of our business. The loss of the services

of Mr. Li for any reason could harm our business and prospects. We cannot assure

you that Mr. Li will continue to be available to us, or that we will be able to

find a suitable replacement for Mr. Li. We have entered into an employment

contract with Mr. Li, but that agreement does not guarantee that Mr. Li will

continue to manage the Company. Although we plan to do so following the closing

of this offering, we do not currently have key man insurance on Mr. Li, and if

he were unable to continue as our chief executive officer due to death or

disability and we were unable to replace him for a prolonged period of time, we

could be unable to carry out our long-term business plan, and our future

prospects for growth, and our business, could be harmed.

11

We

may have difficulty establishing adequate management, legal and financial

controls in the PRC, and such difficulties could reduce the value of any

investment in our common stock.

The PRC

historically has not adopted a western style of management and financial

reporting concepts and practices, or modern banking, computer and other control

systems. We may have difficulty in hiring and retaining a sufficient number of

qualified employees to work in the PRC. We may experience difficulty in

establishing management, legal and financial controls, collecting financial data

and preparing financial statements, books of account and corporate records and

instituting business practices that meet Western standards. These deficiencies

could impair our results of operations.

We

may have violated Section 402 of the Sarbanes-Oxley Act of 2002 and Section

13(k) of the Exchange Act and may be subject to sanctions for such

violations.

Section

13(k) of the Exchange Act provides that it is unlawful for a company such as

ours, which has a class of securities registered under Section 12(g) of the

Exchange Act, to directly or indirectly, including through any subsidiary,

extend or maintain credit in the form of a personal loan to or for any director

or executive officer of the Company. Issuers violating Section 13(k) of

the Exchange Act may be subject to civil sanctions, including injunctive

remedies and monetary penalties, as well as criminal sanctions. The imposition

of any of such sanctions on the Company may have a material adverse effect on

our financial position, results of operations or cash flows.

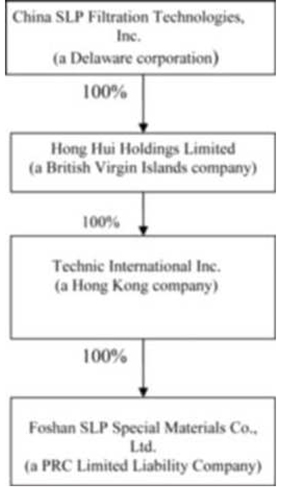

On

February 12, 2010, we entered into a share exchange agreement with the owners of

all of the outstanding shares of Hong Hui, a British Virgin Islands holding

company which was incorporated in the British Virgin Islands on January 6, 2010

and our direct, wholly-owned subsidiary. Under the terms of the share exchange

agreement we issued and delivered to the Hong Hui stockholders a total of

14,510,204 shares of our common stock in exchange for all of the outstanding

shares of Hong Hui. As a result of the share exchange, Hong Hui became our

wholly-owned subsidiary and Foshan S.L.P. Special Material Co., Ltd., a PRC

operating company, became our indirect wholly-owned subsidiary. At that time,

Jie Li, who became our Chief Executive Officer on that date, was indebted on

account of a previous loan in the amount of RMB 200,000 (approximately $29,474)

made by Foshan.

The

existence of indebtedness of Mr. Jie Li at the time the Company acquired Foshan

and the continuation of such indebtedness thereafter may constitute a violation

of Section 13(k) of the Exchange Act (Section 402(a) of Sarbanes-Oxley). As of

September 30, 2010, all loans had been repaid.

We

do not have a Majority of Independent Directors.

Our Board

of Directors comprises of six members, three of whom are “independent” within

the NASDAQ rules. Accordingly, we do not currently have, and following the

closing of this offering we will not have, a Board of Directors the majority of

whom are “independent” within the meaning of the NASDAQ rules and we will lack

the oversight of an independent board.

We

fall within the definition of a “controlled company” under the NASDAQ

Marketplace Rules which provide that a company is considered a "controlled

company" if greater than 50% of its voting power is held by an individual, a

group or another company. In order for a group to exist for purposes of

this rule, the stockholders forming the group are required to publicly file a

notice that they are acting as a group (e.g., Schedule 13D). On December

29, 2010, a group consisting of Bestyield Group Limited, Jie Li, Proudlead

Limited, Law Wawai, Pilot Link International Limited, Yang Wei, Li Shiyi, High

Swift Limited, Han Hung Yuk, China Investment Management, Inc., Song Huaying,

Newise Holdings Limited and Li Jun filed a Schedule 13D disclosing the

existence of a group with respect to their holdings in the Company. As a

“controlled company” we are not subject to the NASDAQ requirements (i) to have a

majority of independent board members; (ii) for independent director oversight

of executive officer compensation (as set forth in Section 5605(d) of the

NASDAQ Marketplace Rule); and (iii) for independent director oversight of

director nomination (as set forth in Section 5605(e) of the NASDAQ

Marketplace Rule).

12

Risks

Related to Doing Business in China

Our

business operations are conducted entirely in the PRC. Because China’s economy

and its laws, regulations and policies are different from those typically found

in the West and are continually changing, we will face risks including those

summarized below.

The

PRC may be more susceptible to political, economic, and social upheaval than

other nations; any such upheaval could cause us to temporarily or permanently

cease operations.

China has

experienced unprecedented growth economically in the past three decades.

Although the country has relaxed some restrictions on individual liberties, the

rule of law is still a relatively new concept. Thus the legal system may not be

equipped to handle complicated social and political problems accompanying the

country’s fast economic growth. China has an extremely large population,

significant levels of poverty, widening income gaps between rich and poor and

between urban and rural residents, large minority ethnic and religious

populations, and growing access to information about the different social,

economic, and political systems to be found in other countries. These conditions

make China unique and may make it susceptible to major structural changes. Such

changes could include a reversal of China’s movement to encourage private

economic activity, labor disruptions or other organized protests,

nationalization of private businesses, internal conflicts between the police or

military and the citizenry, and international political or military conflict. If

any of these events were to occur, it could damage China’s economy and impair

our business.

The

PRC environmental protection laws and regulations require PRC companies,

especially PRC manufacturing companies, to obtain environmental approvals for

the commencement and completion of production lines and pollution emission

permits. Failure to obtain the necessary environmental approvals and permits may

subject us to fines and, in some cases, may even result in the mandated

cessation of production, which may in turn impair our normal business operations

and expansion plans.

In order

to be in compliance with PRC environmental protection laws and regulations, we are required to obtain a

construction commencement approval and a completion examination approval for

each of our three finished production lines. We are also required to

obtain a construction commencement approval from the local environmental

protection bureau for one of our production lines that is currently under

construction. We have obtained the construction commencement approval and

completion examination approval for our three finished production

lines.

On

November 9, 2010, we submitted the application for the construction commencement

approval for the new production line under construction to the local

environmental protection bureau and on November 10, 2010, we received comments

from them requesting us to complete the environment impact assessment of the new

production line before submitting the application for the construction

commencement approval. The environmental impact assessment is currently

being conducted by a third party authorized by the local environmental

bureau. We anticipate that it will be completed within 120 days from

commencement (on or before March 10, 2011), but we cannot assure that

this will be the case. Once the environmental impact assessment is

completed, we intend to resubmit the application for the construction

commencement approval together with the environmental impact assessment to the

local environmental protection bureau. We anticipate that the construction

commencement approval will be issued within 60 days from the submission date but

we cannot assure that this will be the case.

In

addition, we are required a pollution emission permit for the disposal of waste

gases, waste water, waste dust and other waste materials. We do not

currently have a pollution emission permit but we are preparing the application

for this permit and intend to submit the application after the new production

line is completed. The process of obtaining this permit after the

application has been submitted can take up to 5 months.

13

We cannot

assure you that we will be able to obtain the construction commencement approval

or the pollution emission permit in a timely manner or at all. Failure to

obtain this approval and permit may subject us to fines or disrupt our

operations and construction, which may materially and adversely affect our

business, results of operations and financial condition.

We

are subject to comprehensive regulation by the PRC legal system, which is

uncertain. As a result, it may limit the legal protections available to us and

we may not be now, or remain in the future, in compliance with PRC laws and

regulations.

Foshan,

our operating company, is incorporated under and is governed by the laws of the

PRC, where all of our operations are conducted. The PRC government exercises

substantial control over virtually every sector of the PRC economy, including

the production, distribution and sale of nonwovens. In particular, we are

subject to regulations and administration by local and national branches of the

Ministry of Environmental Protection, the Ministry of Commerce, as well as the

General Administration of Quality Supervision, Inspection and Quarantine, the

State Administration of Foreign Exchange, General Administration of Customs, the

State Administration of Taxation and other regulatory bodies. In order to

operate under PRC law, we must have valid licenses, certificates and

permits, which must be renewed from time to time. If we were to fail to obtain

the necessary renewals for any reason, including sudden or unexplained changes

in local regulatory practice, we could be required to shut down all or part of

our operations temporarily or permanently.

Foshan is

subject to PRC accounting laws, which require that an annual audit be performed

in accordance with PRC accounting standards. The PRC foreign-invested enterprise

laws require that our subsidiary, Foshan, submit periodic fiscal reports and

statements to financial and tax authorities and maintain its books of account in

accordance with Chinese accounting laws. If PRC authorities were to determine

that we were in violation of these requirements, we could lose our business

license and be unable to continue operations temporarily or

permanently.

The legal

and judicial systems in the PRC are still rudimentary. The laws governing our

business operations are sometimes vague and uncertain and enforcement of