Attached files

| file | filename |

|---|---|

| EX-23 - EXHIBIT 23 - Centric Brands Inc. | a2201829zex-23.htm |

| EX-21 - EXHIBIT 21 - Centric Brands Inc. | a2201829zex-21.htm |

| EX-32 - EXHIBIT 32 - Centric Brands Inc. | a2201829zex-32.htm |

| EX-31.1 - EXHIBIT 31.1 - Centric Brands Inc. | a2201829zex-31_1.htm |

| EX-31.2 - EXHIBIT 31.2 - Centric Brands Inc. | a2201829zex-31_2.htm |

| EX-10.27 - EXHIBIT 10.27 - Centric Brands Inc. | a2201829zex-10_27.htm |

Use these links to rapidly review the document

Table of Contents

TABLE OF CONTENTS 2

TABLE OF CONTENTS 3

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended November 30, 2010

Commission file number: 0-18926

JOE'S JEANS INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

11-2928178 (I.R.S. Employer Identification No.) |

2340 South Eastern Avenue, Commerce, California 90040

(Address of principal executive offices, including zip code)

Registrant's telephone number, including area code: (323) 837-3700

Securities

registered pursuant to Section 12(b) of the Act:

Common Stock, $0.10 par value

(Title of Class)

The Nasdaq Stock Market LLC

(NASDAQ Capital Market)

(Name of exchange on which registered)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by checkmark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§229.405 of this chapter) during the preceding 12 months (or such shorter period that the registrant was required to submit and post such files). o Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act.)

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company ý |

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Act.) Yes o No ý

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant based on the closing price of the registrant's common stock on The Nasdaq Stock Market, Inc. as of May 31, 2010, was approximately $105,981,000.00.

The number of shares of the registrant's common stock outstanding as of February 10, 2011 was 64,440,541.

Documents incorporated by reference: None.

FORM 10-K ANNUAL REPORT

FOR THE FISCAL YEAR ENDED NOVEMBER 30, 2010

Forward-Looking Statements

Statements contained in this Annual Report on Form 10-K, or Annual Report, and in future filings with the Securities and Exchange Commission, or the SEC, in our press releases or in our other public or shareholder communications that are not purely historical facts are forward-looking statements. Statements looking forward in time are included in this Annual Report pursuant to the "safe harbor" provision of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements include, without limitation, any statement that may predict, forecast, indicate, or imply future results, performance, or achievements, and may contain the words, "believe", "anticipate", "expect", "estimate", "intend", "plan", "project", "will be", "will continue", "will likely result", and any variations of such words with similar meanings. These statements are not guarantees of future performance and are subject to certain risks and uncertainties that are difficult to predict; therefore, actual results may differ materially from those expressed or forecasted in any such forward-looking statements.

Factors that would cause or contribute to such differences include, but are not limited to, the risk factors contained or referenced under the headings "Business," "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" set forth in this Annual Report. In particular, certain risks and uncertainties that we face include, but are not limited to, risks associated with:

- •

- the risk that we will be unsuccessful in gauging fashion trends and changing customer preferences;

- •

- the risk that changes in general economic conditions, consumer confidence or consumer spending patterns will have a

negative impact on our financial performance or strategies;

- •

- the risks associated with leasing retail space and operating our own retail stores;

- •

- the highly competitive nature of our business in the United States and internationally and our dependence on consumer

spending patterns, which are influenced by numerous other factors;

- •

- our ability to respond to the business environment and fashion trends; continued acceptance of the Joe's®

brand in the marketplace;

- •

- successful implementation of any growth or strategic plans;

- •

- effective inventory management;

- •

- our ability to continue to have access on favorable terms to sufficient sources of liquidity necessary to fund ongoing

cash requirements of our operations, which access may be adversely impacted by a number of factors, including the reduced availability of credit, generally, and the substantial tightening of the

credit markets, including lending by financial institutions, who are sources of credit for us, the recent increase in the cost of capital, the level of our cash flows, which will be impacted by the

level of consumer spending and retailer and consumer acceptance of its products;

- •

- our ability to generate positive cash flow from operations;

- •

- competitive factors, including the possibility of major customers sourcing product overseas in competition with our

products;

- •

- the risk that acts or omissions by our third party vendors could have a negative impact on our reputation;

- •

- a possible oversupply of denim in the marketplace; and

1

- •

- other risks.

Since we operate in a rapidly changing environment, new risk factors can arise and it is not possible for our management to predict all such risk factors, nor can our management assess the impact of all such risk factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Given these risks and uncertainties, readers are cautioned not to place undue reliance on forward-looking statements that only speak as of the date of this filing.

We undertake no obligation to publicly revise these forward-looking statements to reflect events, circumstances or the occurrence of unanticipated events that occur subsequent to the date of this Annual Report. As used in this Annual Report, the terms "we", "us", "our", "Joe's®" and "Joe's Jeans" refer to Joe's Jeans Inc. and our subsidiaries and affiliates, unless the context indicates otherwise.

Overview

We began our operations in April 1987 as Innovo, Inc., or Innovo, a Texas corporation, to manufacture and domestically distribute cut and sewn canvas and nylon consumer products for the utility, craft, sports-licensed and advertising specialty markets. In 1990, Innovo merged into Elorac Corporation, a Delaware corporation, and renamed the company Innovo Group Inc. In October 2007, we renamed our company Joe's Jeans Inc. Initially, we produced craft and accessory products for the consumer marketplace. Since that time, we evolved from producing craft and accessory products to designing and selling apparel products. During this transition, we moved our operations from Tennessee to Los Angeles, California.

Our principal business activity has evolved into the design, development and worldwide marketing of our Joe's® products, which include denim jeans, related casual wear and accessories. Since Joe's® was established in 2001, the brand is recognized in the premium denim industry, an industry term for denim jeans with price points generally of $120 or more, for its quality, fit and fashion-forward designs. We focus on design, development and marketing and rely on third parties to manufacture our apparel products. We sell our products to numerous retailers, which include major department stores, specialty stores, and distributors around the world and through our retail stores.

In October 2007, we completed a merger with JD Holdings, the successor in interest to JD Design LLC, or JD Design, the entity from whom we originally licensed the Joe's® brand. As a result of the merger, we acquired JD Holdings, which included all rights related to the Joe's® brand. This acquisition allowed us to focus our operations on the Joe's® brand and its development. In fiscal 2007, we entered into our first license agreement for handbags and small leather goods bearing the Joe's® brand.

After the acquisition, we focused our business on opening retail stores, improving international sales, increasing sales from our men's collection and enhancing the quality, fit and products available in our collection beyond denim bottoms. We opened our first full price retail store in October 2008 in Chicago, Illinois and currently operate four full price retail stores and thirteen outlet stores in outlet centers around the country. We believe that the retail stores will enhance our net sales and gross profit and the outlet stores will allow us to sell our overstock or slow moving items at higher profit margins. We continue to look for other retail leases for fiscal 2011 and beyond, but remain cautious about our retail store plans.

Beginning in 2009, we began to refine our collection pieces and re-launched several categories as sub-brands with their own unique branding along with the Joe's® logo or name. Beginning in the fall of fiscal 2009, we launched a line of unisex woven shirts in different fits and fabrications called The Shirt

2

by Joe's, which was followed by The T, The Pant, The Bag and The Belt by Joe's. We believe that these additional products added to our core and fashion denim will be a growth driver for our overall business as we move into fiscal 2011.

Principal Products and Revenue Sources

Our principal apparel products bear the Joe's® brand name. Our Joe's® product line includes women's and men's denim jeans, pants, shirts, sweaters, jackets and other apparel products. We also offer women's handbags and clutches, children's products, shoes, belts and leather goods under various license agreements and receive royalty payments based upon net sales of these products. Joe's® products are marketed to U.S. retailers through third party showrooms located in New York and Los Angeles and to international retailers through international distributors or agents in the various countries. Joe's® women's product line represents our largest source of revenue and consists primarily of denim jeans and pants in a variety of different fits, fabrics, washes and detailing. Every season, we offer new and core basic styles to appeal to trendsetters and fashion-forward consumers. We believe our attention to fitting different body types gives us an advantage in the marketplace, as we can offer the consumer a product designed and tailored to fit her needs. We have branded the different fit styles so that the consumer can differentiate and choose from the variety carried by the retailer. Our fit styles include:

- •

- Best Friend—a relaxed loose fit;

- •

- Chelsea—an ultra slim fit;

- •

- Cigarette—a straight and narrow fit;

- •

- Ex-Lover—a relaxed fit;

- •

- Honey—a curvy fit;

- •

- Icon Muse—a high waist fit;

- •

- Provocateur—a petite fit with a shorter inseam;

- •

- Rocker—a lean flare fit;

- •

- Socialite—a classic bootcut fit;

- •

- Stardust—a super flare fit;

- •

- Starlet—a slim legged bootcut fit;

- •

- Twiggy—a taller fit with a longer inseam; and

- •

- Visionaire—a high waist bootcut fit.

In addition to our traditional five pocket denim jeans, we began offering in late fiscal 2009, a line of denim leggings and jeggings for women, unisex woven shirts in a variety of fabrications, tees, pants and knit tops. These products have performed well at retail and we continue to explore offering other product categories.

For our men's denim line, we carried over the concept from our women's line of offering a variety of different fits, fabrics, washes and detailing in our product selection. Similar to our women's line, we offer certain core basic styles every season in addition to new styles in our men's line. We also brand the fit styles, which include the Brixton, the Classic, the Outsider, the Rebel and the Rocker.

Children's product offerings include basic denim bottoms, tops, t-shirts and jackets for infants, toddlers, girls and boys. In the latter half of 2009, we licensed this category to a third party in exchange for certain guaranteed minimums and royalty payments based upon net sales. We believe that licensing

3

this product category will enhance our ability to produce and sell these products without requiring any additional capital investment or incremental operating expenses by us.

Product Design, Development and Sourcing

Our product development for Joe's® is managed internally by a team of designers led by Joe Dahan, our Creative Director. This design team is responsible for the creation, development and coordination of the product group offerings within each collection. We typically develop four collections per year for spring, summer, fall and holiday, with certain core basic styles offered throughout the year. Joe Dahan is an instrumental part of our design process. When we acquired the Joe's® brand, we also entered into an employment agreement with Joe Dahan. However, the loss of Mr. Dahan as an employee would not change any rights we have to the Joe's® brand. While his current employment agreement contains customary provisions related to continued employment, we believe that should Mr. Dahan's employment terminate, we would be able to find alternative sources for the development and design of our Joe's® products. See "Risk Factors—Our future success depends on our ability to attract and retain talented personnel and retain our key employees, including our chief executive officer and creative director."

We rely on third party manufacturers to manufacture all of our products for distribution. We manufacture our products in numerous countries, with most of our denim production in Mexico, Morocco and the United States, and our knits and other production in China, Hong Kong, India, Portugal, Peru, Mexico and Korea . We do not have a long-term supply agreement with any of our third party manufactures or contractors, but we believe that there are a number of overseas and domestic contractors that could fulfill our requirements in the event that one of our existing manufacturers would not be able to do so. We purchase products in various stages of production from partial to completed finished goods. We control production schedules in order to ensure quality and timely deliveries.

In fiscal 2010, we moved our corporate headquarters and outsourced a portion of our warehouse and distribution services for the picking, packing and shipping of our Joe's® products to retailers to a third party under an outsourcing agreement. After the end of fiscal 2010, we moved the warehouse and distribution services to the same building as our corporate headquarters and assumed all aspects of warehousing and distribution services internally.

We purchase fabric from independent vendors located domestically and internationally. Our raw materials are principally blends of fabrics, yarns and threads and are available from multiple sources. Our primary suppliers include Candiani and Italdenim for fabrics and American Zabin, Button Accessory, Revolution Group and COATS Mexico for trims. We have not experienced any material shortage of raw material to meet our needs. We continue to explore alternate inventory strategies designed to improve our gross margins. However, there can be no assurance that any change in sourcing will result in enhanced profit margins, similar quality or timely deliveries, but we do believe that continuing to monitor this expense can be beneficial for the growth of our Joe's® brand.

In the event we terminate any of our relationships with third parties or the economic climate or other factors result in a significant reduction in the number of contractors, our business could be negatively impacted. At this time, we believe that we would be able to find alternative sources for production if this were to occur; however, no assurances can be given that a transition would not involve a disruption to our business.

We generally purchase our products in U.S. dollars. However, because we use some overseas or non-U.S. suppliers, the cost of these products may be affected by changes in the value of the relevant currencies. Certain of our apparel purchases in the international markets will be subject to the risks associated with the importation of these types of products. See "Business—Import and Export Restrictions and Other Governmental Regulations."

4

While we attempt to mitigate our exposure to manufacturing risks, the use of independent suppliers reduces our control over production and delivery and exposes us to customary risks associated with sourcing products from independent suppliers. Transactions with foreign manufacturers and suppliers are subject to the typical risks of doing business abroad, generally, such as the cost of transportation and the imposition of import duties and restrictions. The countries in which our products are manufactured may, from time to time, impose new quotas, duties, tariffs or other restrictions, or adjust presently prevailing quotas, duties or tariff levels, which could affect our operations and our ability to import products at current or increased levels. We cannot predict the likelihood or frequency of any such events occurring. See "Business—Import Restrictions and Other Governmental Regulations." Furthermore, the inability of a manufacturer to ship orders of our products in a timely manner or to meet our quality standards could cause us to miss the delivery date requirements of our customers for those items, which could result in cancellation of orders, refusal to accept deliveries or a reduction in purchase prices. Due to the seasonality of our business, and the apparel and fashion business in particular, the dates on which customers require shipments of products from us are critical, as styles and consumer tastes change so rapidly and particularly from one season to the next. Because quality is a leading factor when customers and retailers accept or reject goods, any decline in quality by our third-party manufacturers could be detrimental not only to a particular order, but also to our future relationship with that particular customer.

We also require our independent manufacturers to operate in compliance with applicable laws and regulations; however, we have no control over the ultimate actions of our independent manufacturers. Despite our lack of control, we have internal operating guidelines to promote ethical business practices and our employees periodically visit and monitor the operations of our independent manufacturers. We also use the services of a third party independent labor consulting service to conduct random, on-site audits as required by state labor laws to help minimize our risk and exposure to unacceptable labor practice violations.

Merger Agreement, License Agreements and Trademarks

In February 2001, we acquired license rights to the name Joe's Jeans™, the JD stylized logo and the Joe's® mark for most apparel and accessory products from JD Holdings, the successor-in-interest to JD Design. The license agreement contained a 10-year term with two 10-year renewal periods and required us to pay a three percent royalty on the net sales of Joe's® products to JD Holdings. However, as we began to focus our operations on the Joe's® brand, we believed that by owning all rights to the Joe's® marks outright, we would eliminate any risks associated with the potential termination of the license agreement and be able to control the direction of the brand and our company. On February 6, 2007, we entered into a merger agreement with JD Holdings to acquire JD Holdings, which included all right, title and interest in the Joe's® brand and related marks. In exchange for the business of JD Holdings, after approval by our stockholders, we issued to Joe Dahan, the sole stockholder of JD Holdings, 14,000,000 shares of our common stock and $300,000 in cash. As part of the merger consideration, we are also obligated to pay Mr. Dahan a percentage of our gross profits above $11,251,000 until 2017. Mr. Dahan will be entitled to the following: (i) 11.33 percent of the gross profit from $11,251,000 to $22,500,000; (ii) 3 percent of the gross profit from $22,501,000 to $31,500,000; (iii) 2 percent of the gross profit from $31,501,000 to $40,500,000; and (iv) 1 percent of the gross profit above $40,501,000.

We believe that selectively licensing the Joe's® brand for certain product categories will broaden and enhance the products available under the brand name. Also, by licensing categories, we will not incur significant capital investments or incremental operating expenses while providing us with royalty payments on net sales. There are certain minimum net sales that the licensees are required to meet and the agreements generally have certain terms with renewal rights. As of February 10, 2011, we had four active license agreements for bags, belts, children's products and shoes.

5

In addition to the common law rights associated therewith, we own a variety of pending applications and registrations throughout the world for a variety of trademarks and service marks, among which include "Joe's" and "JD" logos and "Joe's Jeans" as applied to apparel, footwear and/or other fashion accessories in numerous classes as well as for retail store services for such goods.

In addition to the above, in the United States, we own five registrations for certain pocket stitch designs for jeans. As of February 10, 2011, we own approximately ten U.S. registrations (excluding the aforementioned five registrations for certain pocket stitch designs for jeans) and about ten pending U.S. applications, all of which have successfully passed through publication and have been allowed.

With respect to foreign jurisdictions, we own, as of February 10, 2011, a variety of registrations and pending applications for the above-referenced marks as applied to apparel, footwear and related fashion accessories. Approximately43 trademark registrations have issued in jurisdictions such as Australia, Canada, China, the European Community which comprises 27 member countries, Hong Kong, India, Japan, South Korea, Mexico, New Zealand, Russia, Switzerland and Turkey. We continue to prosecute four trademark applications in Mexico that we believe are necessary in order to protect and enforce our rights.

Sales, Distribution and Outsourcing Agreements

Domestically, we sell our Joe's® products to retailers and specialty stores through independent third party showrooms located in Los Angeles and New York and through our own retail stores. At the showrooms, retailers review the latest collections offered and place orders. The showroom representatives provide us with purchase orders from the retailers and other specialty store buyers. Pursuant to our arrangement with each of these showrooms, we pay sales commissions at an agreed upon percentage of sales less discounts, returns and other credit allowances.

We sell our Joe's® products internationally through distributors and sales agents in various countries that are managed by us and consultants based in Europe. For Japan, in 2007, we entered into a Distribution and Licensing Agreement with Itochu Corporation, or Itochu, pursuant to which Itochu agreed to distribute existing products and develop and manufacture additional products specifically for Japan that expires in May 2011. We believe that by working directly with our distributors and agents abroad rather than through a third party, we will be able to exercise more control and guidance over their sales. Further, we expect to benefit in sales and profitability over the long term from selling our products directly to the distributors or through agents rather than through a third party. However, as we develop our internal structure to support our international business, we continue to evaluate our options and review relationships in the international marketplace to create a strategy to improve and grow international sales.

From time to time, we have outsourced our product fulfillment services, including our warehousing, distribution and customer service needs for our Joe's® products. In fiscal 2010, we moved some of these customer service and warehouse and distribution functions in-house and continued to rely on third party for other aspects of these services. After the end of fiscal 2010, we moved our warehouse to the same building as our corporate headquarters and assumed all aspects of warehousing and distribution internally.

Advertising, Marketing and Promotion

Historically, our advertising campaign for our Joe's® brand has been limited to strategic placement of advertising in areas of high concentration of fashion advertising through billboard advertisement in Los Angeles, California, space on the tops of taxi cabs in New York City and, to a limited extent, print ads in magazines. Since January 2008, we have an agreement to locate short term billboard advertising space in various locations in and around New York City and Los Angeles. In addition, we utilize a public relation firm to strategically place our products in magazines, editorials and with stylists. Sales

6

through existing retail channels are enhanced by visual merchandising. For example, many of our customers' stores have denim focus areas located within a department that are dedicated to selling and showcasing our Joe's® merchandise on a year round basis. We also have an internal visual merchandiser who works with our retail stores and other customers to create the Joe's® presentation of products to enhance sales.

Customers

Our Joe's® products are sold to consumers through high-end department stores and boutiques located throughout the world and through our own retail stores.

We currently sell to domestic department stores such as Macy's Inc., which includes Bloomingdale's and Macy's, Neiman Marcus, Nordstrom, Saks Fifth Avenue, Von Maur, Lord & Taylor, Dillard's and Belk stores and specialty retailers such as American Rag, Anthropologie, Atrium, Barneys New York, Bergdorf Goodman, Henri Bendel, Lisa Klein, Ron Herman, Fred Segal and Scoop NYC in the United States. We sell internationally to retailers such as Galleries Lafayette, Le Bon Marche and Le Printemps in France, Barney's Japan, Isetan and Mitsukoshi in Japan, Top Shop, Harvey Nichols and Selfridges & Co. in the United Kingdom, Ztampz in Hong Kong and Gio Moretti in Italy.

The Joe's® website, www.joesjeans.com, has been established to promote and advance the brand's image and to allow consumers to review and purchase online the latest collection of products. The information available on Joe's® website is not intended to be incorporated into this Annual Report. We currently use both online and print advertising to create brand awareness with customers as well as consumers.

We do not enter into long-term agreements with any of our customers. Instead, we receive individual purchase order commitments from our customers. A decision by the controlling owner of a group of stores or any other significant customer, whether motivated by competitive conditions, financial difficulties or otherwise, to decrease the amount of merchandise purchased from us, or to change their manner of doing business with us, could have a material adverse effect on our financial condition and results of operations. See "Risk Factors—A portion of our net sales and gross profit is derived from a small number of large customers."

For fiscal 2010, our ten largest customers and customer groups accounted for approximately 62 percent of our net sales. While this is a high percentage of sales attributable to three customer groups, we believe that we would be able to find alternative customers to purchase our products in the event of the loss of any of these existing customers. For example, our largest customers included Nordstrom Inc. and Macy's Inc. which includes Bloomingdale's and Macy's.

Seasonality of Business and Working Capital

Products are designed and marketed primarily for four principal selling seasons: spring, summer, fall/back-to-school and winter/holiday. Typically, we have approximately a 12 to 14 week turnaround time between the time we book an order and when we ship it. Our primary booking periods for the retail sales seasons are as follows:

Retail Sales Season

|

Primary Booking Period | |

|---|---|---|

| Spring | September - November | |

| Summer | November - March | |

| Fall/Back-to-School | February - May | |

| Winter/Holiday | June - August |

7

We have historically experienced and expect to continue to experience seasonal fluctuations in our net sales. A significant amount of our net sales are realized during the third and fourth quarter when we ship orders taken during earlier months. For fiscal 2010, we funded our liquidity needs through cash from operations and cash availability under our financing agreements with CIT Commercial Services, a unit of CIT Group Inc., or CIT. If sales are materially different from seasonal norms, our annual operating results could be materially affected. Accordingly, our results for the individual quarters are not necessarily indicative of the results to be expected for the entire year. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources" for further discussion of our financing agreements with CIT.

Credit and Collection

We currently extend credit to a majority of our larger customers, who purchase our products from us at wholesale prices. Our decision to extend credit is based on factors such as credit approval by CIT under our factoring arrangements, past credit history, reputation of creditworthiness within our industry and timelines of payments made to us. We generally extend this credit without requiring collateral. A small percentage of our customers are required to pay by either cash before delivery, credit card or cash on delivery, or C.O.D., which is also based on such factors as lack of credit history, reputation (or lack thereof) within our industry and/or prior payment history. For those customers to whom we extend credit, typical terms are net 30 to 60 days. Based on industry practices, financial awareness of the customers with whom we conduct business and business experience of our industry, our management exercises professional judgment in determining which customers will be extended credit. We are exposed to some collection risk for receivables which were factored with recourse where CIT did not accept the credit risk. However, the aggregate amount of exposure is generally low and, therefore, we believe that the credit risk associated with our extension of credit is minimal.

Backlog

Although we may, at any given time, have significant business booked in advance of ship dates, customers' purchase orders are typically filled and shipped within two to six weeks. As of November 30, 2010, we had backlog of $22,540,000 compared to $23,500,000 as of November 30, 2009. The amount of outstanding customer purchase orders at a particular time is influenced by numerous factors, including the product mix, timing of the receipt and processing of customer purchase orders, shipping schedules for the product and specific customer shipping windows. Due to these factors, a comparison of outstanding customer purchase orders from period to period is not necessarily meaningful and may not be indicative of eventual actual shipments.

Competition

The apparel industry in which we operate is fragmented and highly competitive in the United States and on a worldwide basis. We compete for consumers with a large number of apparel companies similar to ours. Our primary branded competitors include True Religion, Seven for All Mankind, Citizens of Humanity, Rock & Republic and J Brand. We do not hold a dominant competitive position, and our ability to sell our products is dependent upon the anticipated popularity of our designs and brand name, the price and quality of our products and our ability to meet our customers' delivery schedules. We believe the range of fits and uniqueness of our designs differentiates us from our competitors and we believe that we are competitive with companies producing goods of like quality and pricing. We believe that we can maintain our competitive position through new product development, creating product identity and brand awareness and competitive pricing. Many of our competitors may possess greater financial, technical and other resources and the intense competition and the rapid changes in consumer preferences constitute significant risk factors in our operations. As we expand

8

globally, we will continue to encounter additional sources of competition. See "Risk Factors—We face intense competition in the denim industry."

Import and Export Restrictions and Other Governmental Regulations

Transactions with our foreign manufacturers and suppliers are subject to the general risks of doing business abroad. Imports into the United States are affected by, among other things, the cost of transportation and the imposition of import duties and restrictions. The countries in which our products might be manufactured may, from time to time, impose new quotas, duties, tariffs or other restrictions, or adjust presently prevailing quotas, duties or tariff levels, which could affect our operations and our ability to import products at current or increased levels. We cannot predict the likelihood or frequency of any such events occurring. The enactment of any additional duties, quotas or restrictions could result in increases in the cost of our products generally and might adversely affect our sales and profitability.

Our import operations are subject to international trade agreements and regulations such as the North American Free Trade Agreement and other bilateral textile agreements between the United States and a number of foreign countries, including Morocco, Hong Kong, China, Taiwan and Korea. Some of these agreements impose quotas on the amount and type of goods that can be imported into the United States from these countries. Such agreements also allow the United States to impose, at any time, restraints on the importation of categories of merchandise that, under the terms of the agreements, are not subject to specified limits. Some of our imported products are also subject to United States customs duties and, in the ordinary course of business, we are from time to time subject to claims by the United States Customs Service for duties and other charges.

Human Resources

As of February 10, 2011, we had 281 total employees, which included 154 full-time, 101 part- time and 26 temporary employees. We consider our relationships with our employees to be good.

Financial Information about Geographic Areas

See "Notes to Consolidated Financial Statements—Note 9—Segment Reporting and Operations by Geographical Areas" for discussion of financial information about geographical areas.

Manufacturing and Distribution Relationships

Our denim products are manufactured by contractors located in Mexico, Morocco and Los Angeles, California. Our non-denim products are primarily manufactured in the United States, Peru, Portugal, and Asia, including Hong Kong, China, India and Korea. Our products are distributed out of Los Angeles or directly from the factory to the customer. The following table represents the percentage of denim and non-denim products manufactured in the various countries or on the geographic continent as a percentage of all products manufactured during the fiscal year.

| |

2010 | 2009 | |||||

|---|---|---|---|---|---|---|---|

United States |

22.4 | % | 12.5 | % | |||

Mexico |

46.4 | % | 59.8 | % | |||

Europe |

0.6 | % | 0.0 | % | |||

Asia |

20.0 | % | 7.2 | % | |||

Morocco |

10.6 | % | 20.5 | % | |||

|

100 | % | 100 | % | |||

9

Available Information

Our website address is www.joesjeans.com. We make available on or through our website, without charge, our Annual Report, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, as soon as reasonably practicable after such reports are electronically filed with or furnished to the SEC. Although we maintain a website at www.joesjeans.com, we do not intend that the information available through our website be incorporated into this Annual Report. In addition, any materials filed with, or furnished to, the SEC may be read and copied at the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549 or viewed on line at www.sec.gov. Information regarding the operation of the Public Reference Room can be obtained by calling the SEC at 1-800-SEC-0330.

The following risk factors should be read carefully in connection with evaluating our business and the forward-looking statements contained in this Annual Report. Any of the following risks could materially adversely affect our business, our operating results, our financial condition and the actual outcome of matters as to which forward-looking statements are made in this Annual Report.

Our success will depend on our success in increasing sales, opening and operating our retail stores and expanding our product offerings.

Our ability to operate profitably depends on our ability to implement our strategic plan with success. During fiscal 2010, we recognized growth for our Joe's® brand through increases in our international sales, our men's and women's domestic and retail sales and by diversifying our product offering to include products such as shirts, tees and pants. We sell our Joe's® products internationally through individual distribution and agent agreements in various countries. In addition, for countries such as Japan, we have specific distribution and licensing agreements to distribute, develop and manufacture products specifically for the Japanese market. We believe that by working directly with our distributors and agents abroad, we can exercise more control and guidance over sales.

From season to season, we have expanded our product offering by offering a variety of products other than denim bottoms. For example, we offered a full collection of fashion items for both men and women, such as woven shirts, leggings, outerwear, cashmere scarves, knit tops and sweaters, fashion jackets, trouser pants in fabrics other than denim and other licensed product categories. We believed that offering additional products would create synergy and allow us to generate additional revenue due to brand name recognition established by our denim business. In addition, by providing a more extensive array of products, we believed it would assist us in creating successful retail stores.

We opened our first retail stores during fiscal 2008 and have an avenue to showcase our other products and increase our sales channels. Currently, we operate four full price stores and 13 outlets. We also expect to enter into additional leases and open additional stores throughout 2011 in various locations throughout the country. We believe that the retail stores will enhance our net sales and gross profit and the outlet stores will allow us to sell our overstock or slow moving items at higher profit margins. We continue to look for other retail leases, but remain cautious about our retail store plans.

Since we have primarily been a wholesaler, opening and operating retail stores requires us to develop retailing skills and capabilities and increase our expenditures. We will be required to enter into leases, increase our rental expenses and make capital expenditures for these stores. These commitments may be costly to terminate, and these investments may be difficult to recapture if we decide to close a store or change our strategy. We must also offer a broad product assortment, appropriately manage retail inventory levels, install and operate effective retail systems, execute effective pricing strategies and integrate our stores into our overall business mix. Finally, we will need to hire and train additional

10

qualified employees and incur additional costs to operate these stores, which will increase our operating expenses. If we do not manage these items properly, it could have a material adverse impact on our financial condition and results of operations.

While we believe that we are putting in place the mechanisms necessary to implement successfully these strategies, there can be no assurance that we will be able to achieve our level of expectations. Further, there can be no assurance that these initiatives will result in profitability for us in the short term or in the future.

Leasing real estate exposes us to possible liabilities and losses.

We enter into leases in connection with our retail stores. Accordingly, we are subject to all of the risks associated with leasing real estate. Store leases generally require us to pay a fixed minimum rent and a variable amount based on a percentage of annual sales at that location. We generally cannot terminate our leases and have restrictions in connection with assigning or subletting our leases. If an existing or future store is not profitable, and we decide to close it, we may be committed to perform certain obligations under the applicable lease, including paying rent for the balance of the applicable lease term. As each of our leases expire, if we do not have a renewal option, we may be unable to renegotiate a renewal on commercially acceptable terms, if at all, which could cause us to close stores in desirable locations. In addition, we may not be able to close an unprofitable store due to an existing operating covenant, which may cause us to operate the location at a loss and prevent us from finding a more desirable location.

Our business may be negatively impacted as a result of the current uncertainty in the United States' economy.

The United States general economy has been in the midst of extraordinary economic uncertainty. Our business depends on the general economic environment and levels of consumer spending that affect not only the ultimate consumer, but also retailers, our largest direct customers. Purchases of high-fashion apparel and accessories tend to decline in periods of recession or uncertainty regarding future economic prospects, when consumer spending, particularly on discretionary items, and disposable income decline. Many factors affect the level of consumer spending in the apparel industries, including, among others: prevailing economic conditions, levels of employment, salaries and wage rates, energy costs, interest rates, the availability of consumer credit, taxation and consumer confidence in future economic conditions. During periods of recession or economic uncertainty, we may not be able to maintain or increase our sales to existing customers, make sales to new customers, open and operate new retail stores, or maintain or improve our earnings from operations as a percentage of net sales. As a result, our operating results may be adversely and materially affected by downward trends in the United States or global economy.

The distress in the financial markets has also resulted in extreme volatility and declines in security prices and diminished liquidity and credit availability. There can be no assurance that our liquidity and our ability to access the credit or capital markets will not be affected by changes in the financial markets and the global economy. Continuing turmoil in the financial markets could make it more difficult for us to access capital, sell assets, refinance our existing indebtedness, enter into agreements for new indebtedness or obtain funding through the issuance of our securities.

In addition, the reduced availability of credit is having a significant negative impact on businesses around the world, and the impact of this reduced availability on our suppliers and other vendors cannot be predicted. The inability of suppliers and other vendors to access liquidity, or the insolvency of suppliers and other vendors, could lead to their failure to deliver our merchandise or other services that we require. Worsening economic conditions could also impair our ability to collect amounts as they become due from our customers, or other third parties that do business with us. We also face the

11

increased risk of order reductions or cancellations when dealing with financially ailing customers or customers struggling with economic uncertainty.

We face risks associated with constantly changing fashion trends, including consumer's response to our Joe's® brand.

Our success will depend on our ability to anticipate, gauge and respond to changing consumer demand and fashion trends in a timely manner. Any failure on our part to anticipate, identify and respond effectively to changing consumer demands and fashion trends could adversely affect the acceptance of our products and leave us with a substantial amount of unsold inventory or missed opportunities in the marketplace. If that occurs, we may be forced to rely on markdowns or promotional sales to dispose of excess, slow-moving inventory, which may negatively affect our ability to achieve profitability. At the same time, a focus on tight management of inventory may result, from time to time, in our not having an adequate supply of products to meet consumer demand and may cause us to lose sales.

We attempt to minimize our risk associated with delivering items through early order commitments by retailers. We must generally place production orders with manufacturers before we have received all of a season's orders and orders may be cancelled by retailers before shipment. Therefore, if we fail to anticipate accurately and respond to consumer preferences, we could experience lower sales, excess inventories or lower profit margins, any of which could have a material adverse effect on our results of operations and financial condition.

Our business could be negatively impacted by a change in consumer demand for denim in the marketplace.

Denim, including premium denim, an industry term for denim jeans with a typical retail price of approximately $120 or more, has been increasingly popular and growing in sales over the past few years as a consumer discretionary purchase both domestically and internationally. However, because consumer demands and fashion trends are subject to cyclical variations as well as the fact that the general economy and future economic prospects can often affect consumer spending habits, a change in any one of the following:

- •

- consumer demand,

- •

- consumer purchases of discretionary items,

- •

- general economic conditions, or

- •

- fashion trends,

which may result in lower sales, excess inventories or lower profit margins for our Joe's® products, any of which could have a material adverse effect on our results operations and financial condition.

We face intense competition in the denim industry.

We face a variety of competitive challenges from other domestic and foreign fashion-oriented apparel producers, some of whom may be significantly larger and more diversified and have greater financial and marketing resources than we have. We do not currently hold a dominant competitive position in any market. We compete with other denim manufacturers such as True Religion, Seven for All Mankind, Citizens of Humanity, Rock & Republic and J Brand and other larger competitors primarily on the basis of:

- •

- anticipating and responding to changing consumer demands in a timely manner,

- •

- maintaining favorable brand recognition,

- •

- developing innovative, high-quality products in sizes, colors and styles that appeal to consumers,

12

- •

- appropriately pricing products,

- •

- providing strong and effective marketing support,

- •

- creating an acceptable value proposition for retail customers,

- •

- ensuring product availability and optimizing supply chain efficiencies with manufacturers and retailers, and

- •

- obtaining sufficient retail floor space and effective presentation of our products at retail.

Furthermore, some of our competitors are privately held corporations and may have resources available to them that we, as a public company, do not have. Therefore, it may be difficult for us to effectively gauge consumer response to our products and how our products are competing with these and other competitors in the marketplace.

A portion of our net sales and gross profit is derived from a small number of large customers.

Our 10 largest customers and customer groups accounted for approximately 62 percent of our net sales during fiscal 2010. We do not enter into any type of long-term agreements or firm commitment orders with any of our customers. Instead, we enter into a number of individual purchase order commitments with our customers. A decision by the controlling owner of a group of stores or any other significant customer, including our limited number of private label customers, whether motivated by competitive conditions, financial difficulties or otherwise, to decrease the amount of merchandise purchased from us, or to change their manner of doing business with us, could have a material adverse effect on our financial condition and results of operations if we are unable to find an alternative customer for our products in a timely manner.

Our business could be negatively impacted by the financial health of our retail customers.

We sell our product primarily to retail and distribution companies around the world based on pre-qualified payment terms. Financial difficulties of a customer could cause us to curtail business with that customer, in addition to the customer's decision to decrease the level of its orders, to cancel orders previously placed in advance of shipment dates or to cease carrying our products. We may also assume more credit risk relating to that customer's receivables. We are dependent primarily on lines of credit that we establish from time to time with customers, and should a substantial number of customers become unable to pay to us their respective debts as they become due, we may be unable to collect some or all of the monies owed by those customers.

In recent years, the retail industry has experienced consolidation or other ownership changes that have resulted in one entity controlling several different stores. This consolidation can result in fewer customers for our products or the closing of some stores or the number of "doors" which carry our products. As a result, the potential for consolidation or ownership changes, closing of retail outlets and fewer customers could negatively impact sales of our products and have a material adverse effect on our financial condition and results of operations.

Our business could suffer as a result of a manufacturer's inability to produce our goods on time and to our specifications or if we need to replace manufacturers.

We do not own or operate any manufacturing facilities and therefore depend upon independent third parties for the manufacture of all of our products. We enter into a number of purchase order commitments each season specifying a time for delivery, method of payment, design and quality specifications and other standard industry provisions, but do not have long-term contracts with any manufacturer. The inability of a certain manufacturer to ship orders of our products in a timely manner or to meet our quality standards could cause us to miss the delivery date requirements of our

13

customers for those items, which could result in cancellation of orders, refusal to accept deliveries or a reduction in purchase prices, any of which could have a material adverse effect on our financial condition and results of operations. Because of the seasonality of our business, and the apparel and fashion business in particular, the dates on which customers need and require shipments of products from us are critical, as styles and consumer tastes change so rapidly in the apparel and fashion business, particularly from one season to the next. Further, because quality is a leading factor when customers and retailers accept or reject goods, any decline in quality by our third-party manufacturers could be detrimental not only to a particular order, but also to our future relationship with that particular customer.

We compete with other companies for the production capacity of our manufacturers. Some of these competitors have greater financial and other resources than we have, and thus may have an advantage in the competition for production and import quota capacity. If we experience a significant increase in demand, or if an existing manufacturer of ours must be replaced, we may have to expand our third-party manufacturing capacity. We cannot assure you that this additional capacity will be available when required on terms that are acceptable to us or similar to existing terms which we have with our manufacturers, either from a production standpoint or a financial standpoint.

Increases in the price of raw materials or their reduced availability could increase our cost of goods and decrease our profitability.

The principal fabrics used in our business are cotton, blends, synthetics and wools. The prices we pay our suppliers for our products are dependent in part on the market price for raw materials—primarily cotton—used to produce them. The price and availability of cotton may fluctuate substantially, depending on a variety of factors, including demand, crop yields, weather, supply conditions, transportation costs, work stoppages, government regulation, economic climates and other unpredictable factors. Increases in raw material costs, together with other factors, will make it difficult for us to sustain the level of cost of goods savings we have achieved in recent years and result in a decrease of our profitability unless we are able to pass higher prices on to our customers. Moreover, any decrease in the availability of cotton could impair our ability to meet our production requirements in a timely manner.

We are dependent on our relationships with our vendors.

We purchase our raw materials, including fabric, yarns, threads and trims, such as zippers, buttons and tags from a variety of vendors. While we are not reliant exclusively on one or more particular vendor for the supply of the raw materials or component parts required to meet our manufacturing needs, we depend on our relationships and these vendors to ensure our supply of these raw materials or component parts. Any problems or disputes with these vendors could result in us having to source these raw materials or component parts from another vendor, which could delay production, and in turn have a material adverse effect on our financial condition and results of operations.

Our licensees may not comply with our product quality, manufacturing standards, marketing and other requirements.

We license our trademarks to third parties for manufacturing, marketing and distribution of bags, belts, children's products and shoes. We believe that licensing the Joe's® brand for certain product categories will broaden and enhance the products available under the brand name. While our agreements with our licensees cover product design, product quality, sourcing, manufacturing, marketing and other requirements, our licensees may not comply fully with those agreements. Non-compliance could include marketing products under our brand names that do not meet our quality and other requirements or engaging in manufacturing practices that do not meet our standards. These activities could harm our brand equity, our reputation and our business.

14

In order to effectively manage growth, we are dependent on our financing arrangements and our cash flow from operations.

Our primary sources of liquidity are: (i) cash from sales of our Joe's® products; and (ii) cash from sales of our accounts receivables and advances against inventory. We are dependent on credit arrangements with suppliers and factoring and inventory based agreements for working capital needs. From time to time, we have conducted equity financing through private placement transactions and obtained increases in our cash availability from CIT Commercial Services, Inc., a unit of CIT Group, or CIT. During fiscal 2010, our primary methods to obtain the cash necessary for operating needs were through the sales of Joe's® products, sales of our accounts receivable pursuant to our factoring agreements and obtaining advances under our inventory security agreements with CIT. CIT has from time to time experienced economic uncertainty regarding its continued ability to operate, including filing a petition for bankruptcy in 2009. However, during this time period, CIT continued to fund us with no change to our arrangements with them. We cannot give you any assurance that should CIT experience uncertainty or insufficient cash flows again that they will continue to be able to fund us in the future.

As of November 30, 2010, our cash availability with CIT was approximately $827,000 under our agreements. This amount fluctuates on a daily basis based upon invoicing and collection related activity by CIT on our behalf. CIT has the ability to terminate the agreements we have with them upon notice or require additional collateral to secure its advances. We do not have any provisions in the agreements that protect us in the event of a default by CIT. If CIT elects to terminate the agreements, we could be forced to pay our liability with CIT and CIT may also elect to take possession of the pledged collateral, which includes raw materials through finished goods and receivables. Although we have undertaken numerous measures to increase sales and cash flow, control inventory costs and operate more efficiently so that we may be able to fund our operations for fiscal 2011, we may experience losses and negative cash flows. We cannot give you any assurance that we will in fact continue to operate profitably in the future. We believe in the event our agreements with CIT are terminated, we will be able to find alternative sources for obtaining the case for our operating needs, including, entering into factoring or inventory security agreements with another lender.

Most of our tangible assets are pledged under our agreements with CIT.

In addition to being dependent on our financing agreements with CIT, we have pledged to CIT as collateral most of our tangible assets, which include raw materials such as fabric and trim, finished goods, and our receivables. In the event we default or CIT elects to terminate the agreements, we would be required to pay our liability to CIT. If we were unable or unwilling to pay all or part of our liability, CIT could exercise its rights under the agreements to the pledged collateral and sell any or all of these tangible assets. In the event CIT elects this remedy, our operations and our sales could be materially adversely impacted by the sale of or our inability to utilize these assets in our normal business operations.

As a result of our completion of the merger with JD Holdings and the issuance of 14,000,000 shares of our common stock, Mr. Dahan may be able to exert significant influence and control over us as a result of his percentage of stock ownership, position as an executive officer and membership on our Board of Directors.

As a result of the completion of the merger and the issuance of the 14,000,000 shares of our common stock, Mr. Dahan beneficially owns approximately 17 percent of our total shares outstanding and is our largest stockholder. In addition, Mr. Dahan is an executive officer and a member of our Board of Directors. As a result, he is in a position to exert significant influence and control over us as a result of his voting power, position as an executive officer and membership on our Board of Directors. We are not aware of any intent by Mr. Dahan to influence or control our affairs as result of

15

his percentage ownership of our common stock and his position as both an executive officer and member of our Board of Directors.

Our future success depends on our ability to attract and retain talented personnel and retain our key employees, including our chief executive officer and creative director.

Our future success depends in part on our ability to attract and retain talented personnel. To date, we have not had any difficulty in attracting or retaining personnel to fill open or new positions, however, in the future, we may need to expand our infrastructure to support any anticipated growth. We may need to provide incentives, both short term and long term, to attract and retain personnel. Incentives can range from bonuses, grants of options or restricted stock to perquisites unique to the industry. All such incentives will result in an increase in certain expenses. More particularly, growth and payment of incentives to personnel and expenditures to expand our infrastructure to support our growth will cause our selling, general and administrative expenses to increase if we cannot maintain or decrease other expenses. An increase in our selling, general and administrative expenses may cause us to be less profitable. There can be no assurance that we will be able to maintain or decrease other expenses, therefore, a decrease in profit may have a material adverse impact on our financial condition and results of operations.

Our chief executive officer, Marc Crossman, has substantial experience and expertise in our business and has made significant contributions to our growth and success. The unexpected loss of his services could adversely affect us. We are protected to a limited extent by a key man term life insurance policy that we maintain on our behalf for Mr. Crossman; however, there can be no assurance that his departure would trigger protection under this policy. In May 2008, we entered into a written employment agreement with Mr. Crossman whereby he is employed by us as our President and Chief Executive Officer. His initial employment term is for two years with automatic renewal for additional two year periods if neither party elects not to renew the agreement upon 180 days advanced notice. If Mr. Crossman should leave us, his absence would likely have a substantial impact on our ability to operate on a daily basis because we would be forced to find and hire similarly experienced personnel to fill one or more of his positions and daily operations may suffer temporarily as a result of this immediate void.

Mr. Dahan's departure could materially adversely affect our operations because his experience, design capabilities and name recognition in the apparel industry is important to our business and we rely heavily on Mr. Dahan's capabilities to design, direct and produce product for the Joe's® brand. However, the loss of Mr. Dahan would not have any effect on our ownership of the brand. While we believe that we would be able to find a suitable replacement to design, direct and produce product for the Joe's® brand, we do not know the effect a new or different designer would have on the products and consumer's response to those new products. Therefore, loss of Mr. Dahan's services could have an impact on our ability to operate on a daily basis.

In the event we seek additional capital through equity or debt offerings, our existing stockholders may be diluted or we may be unable to find additional capital on terms favorable to us and our stockholders.

In the event that we need additional working capital for our projected operations, we may seek capital through debt or equity offerings which could result in the issuance of additional shares of our capital stock and/or rights to acquire additional shares of our capital stock. Those additional issuances of capital stock would result in a reduction of the percentage of ownership interest held by our existing stockholders. Also, the addition of a substantial number of shares of our common stock into the market or the registration of any other securities may significantly and negatively affect the prevailing market price for our common stock. Finally, we may not be able to find additional capital on terms favorable to us through existing markets or investors due to market conditions, our historical performance or our stock price.

16

Our common stock price is volatile and may decrease.

The trading price and volume of our common stock has historically been subject to fluctuations in response to factors such as the following, some of which are beyond our control:

- •

- annual and quarterly variations in actual or anticipated operating results,

- •

- operating results that vary from the expectations of securities analysts and investors,

- •

- changes in expectations as to our future financial performance, including financial estimates by securities analysts and

investors,

- •

- changes in market valuations of other denim apparel companies,

- •

- announcements of new product lines by us or our competitors, announcements by us or our competitors of significant

contracts, acquisitions or dispositions of assets, strategic partnerships, joint ventures or capital commitments,

- •

- additions or departures of key personnel or members of our board of directors, and

- •

- general conditions in the apparel industry.

In the 52 week period prior to the filing of this Annual Report, the closing price of our common stock has ranged from $1.53 to $3.45. In addition, stock markets generally have experienced price and volume trading volatility in recent years. This volatility has had an effect on the market prices of securities of many companies for reasons unrelated to the operating performance of the specific companies. These broad market fluctuations may negatively affect the market price of our common stock.

Our directors and management beneficially own a large percentage of our common stock.

Our executive officers and directors beneficially own approximately 23 percent of our common stock, including options exercisable and restricted common stock units vesting within 60 days of February 10, 2011 in the aggregate. More specifically, Joe Dahan beneficially owns approximately 17 percent of our common stock. Because of this level of stock ownership, in the aggregate, certain persons may be in a position to directly or indirectly control our affairs.

The seasonal nature of our business makes management more difficult, severely reduces cash flow and liquidity during parts of the year and could force us to curtail our operations.

Our business is seasonal. The majority of our marketing and sales activities take place from late fall to early spring. Historically, our greatest volume of shipments and sales occur from late spring through the summer, which coincides with our second and third fiscal quarters. This requires us to build-up inventories during our first and second fiscal quarters when our cash flow is weakest. Historically speaking, our cash flow is strongest in the third and fourth fiscal quarters. Unfavorable economic conditions affecting retailers during the fall and holiday seasons in any year could have a material adverse effect on our results of operations for the year. We are likely to experience periods of negative cash flow throughout each year, including, a drop-off in business commencing each December, which could force us to curtail operations if adequate liquidity is not available. We cannot assure you that the effects of such seasonality will diminish in the future. For fiscal 2010, we funded inventory purchases through cash from operations and cash availability under our financing agreements with CIT.

If an independent manufacturer of ours fails to use acceptable labor practices, our business could suffer.

While we require our independent manufacturers to operate in compliance with applicable laws and regulations, we have no control over the ultimate actions of our independent manufacturers. Despite our lack of control, we have internal and vendor operating guidelines to promote ethical

17

business practices and our staff periodically visits and monitors the operations of our independent manufacturers. We also use the services of a third party independent labor consulting service to conduct on site audits as required by state labor laws to help minimize our risk and exposure to unacceptable labor practice violations. The violation of labor or other laws by one of our independent manufacturers or the divergence of an independent manufacturer's labor practices from those generally accepted as ethical in the United States, could interrupt or otherwise disrupt the shipment of finished products to us or damage our reputation. Any of these, in turn, could have a material adverse effect on our financial condition and results of operations. In particular, the laws governing garment manufacturers in the State of California impose joint liability upon us and our independent manufacturers for the labor practices of those independent manufacturers. As a result, should one of our independent manufacturers be found in violation of state labor laws, we could suffer financial or other unforeseen consequences.

Our trademark and other intellectual property rights may not be adequately protected outside the United States and some of our products are targets of counterfeiting.

We believe that our trademarks and other proprietary rights are important to our success and our competitive position. We may, however, experience conflict with various third parties who acquire or claim ownership rights in certain trademarks as we expand our product offerings and expand the number of countries where we sell our products. We cannot ensure that the actions we have taken to establish and protect these trademarks and other proprietary rights will be adequate to prevent imitation of our products by others or to prevent others from seeking to block sales of our products as a violation of their trademarks and proprietary rights. Also, we cannot assure you that others will not assert rights in, or ownership of, trademarks and other proprietary rights of ours or that we will be able to successfully resolve these types of conflicts to our satisfaction. In addition, the laws of certain foreign countries may not protect proprietary rights to the same extent as do the laws of the United States.

Our Joe's® products are sometimes the target of counterfeiters. As a result, there are often products that are imitations or "knock-offs" of our Joe's® products that can be found in the marketplace or consumers can find products that are confusingly similar to ours. We intend to continue to vigorously defend our trademarks and products bearing our trademarks, however, we cannot assure you that our efforts will be adequate to prosecute and block all sales of infringing products from the marketplace.

Our ability to conduct business in international markets may be affected by legal, regulatory, political and economic risks.

Our ability to capitalize on growth in new international markets and to maintain the current level of operations in our existing international markets is subject to risks associated with international operations. Some of these risks include:

- •

- the burdens of complying with a variety of foreign laws and regulations,

- •

- unexpected changes in regulatory requirements, and

- •

- new tariffs or other barriers to some international markets.

We are also subject to general political and economic risks associated with conducting international business, including:

- •

- political instability,

- •

- changes in diplomatic and trade relationships, and

- •

- general economic fluctuations in specific countries or markets.

18

We cannot predict whether quotas, duties, taxes, or other similar restrictions will be imposed by the United States, Mexico, the European Union, Canada, China, Japan, India, South Korea or other countries upon the import or export of our products in the future, or what effect any of these actions would have on our business, financial condition or results of operations. Changes in regulatory or geopolitical policies and other factors may adversely affect our business in the future or may require us to modify our current business practices.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

Our principal place of business is located in Commerce, Los Angeles County, California. The following table sets forth information with respect to our principal place of business:

Location

|

Use | Ownership Status |

Approximate Area in Square Feet |

Lease Expiration | |||||

|---|---|---|---|---|---|---|---|---|---|

Commerce, California |

Warehouse, design and administrative offices | Leased | 89,230 | December 31, 2013 | |||||

We operate 17 retail store locations under non-cancelable operating lease agreements expiring on various dates through 2021 or ten years from the opening date of the store. These facilities are all located in the United States. As of November 30, 2010, we had 17 stores open and operating and signed leases to open three additional stores. Our retail square footage as of November 30, 2010 was approximately 37,586 square feet in the aggregate. Our retail stores range in size from 1,469 to 3,025 square feet.

We believe that our existing facilities are well maintained, in good operating condition and are adequate for our present level of operations.

(a) We are a party to lawsuits and other contingencies in the ordinary course of our business. We do not believe that we are a party to any material pending legal proceedings or that it is probable that the outcome of any individual action would have an adverse effect in the aggregate on our financial condition. We do not believe that it is likely that an adverse outcome of individually insignificant actions in the aggregate would be sufficient enough, in number or in magnitude, to have a material adverse effect in the aggregate on our financial condition.

(b) None.

ITEM 4. (REMOVED AND RESERVED)

19

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

(a) Our common stock is currently traded under the symbol "JOEZ" on The Nasdaq Capital Market maintained by The Nasdaq Stock Market, Inc., or Nasdaq. The following chart sets forth the high and low interday quotations for our common stock on the Nasdaq market for the periods indicated. This information reflects inter-dealer prices, without retail mark-up, mark-down or commissions, and may not necessarily represent actual transactions. No representation is made by us that the following quotations necessarily reflect an established public trading market in our common stock:

| |

High | Low | |||||

|---|---|---|---|---|---|---|---|

Fiscal 2010 |

|||||||

First Quarter |

$ | 2.33 | $ | 1.10 | |||

Second Quarter |

$ | 3.45 | $ | 1.90 | |||

Third Quarter |

$ | 2.36 | $ | 1.81 | |||

Fourth Quarter |

$ | 2.20 | $ | 1.55 | |||

Fiscal 2009 |

|||||||

First Quarter |

$ | 0.50 | $ | 0.25 | |||

Second Quarter |

$ | 0.72 | $ | 0.22 | |||

Third Quarter |

$ | 1.05 | $ | 0.44 | |||

Fourth Quarter |

$ | 1.59 | $ | 0.63 | |||

As of November 30, 2010, there were 865 record holders of our common stock. We have never declared or paid a cash dividend and do not anticipate paying cash dividends on our common stock in the foreseeable future. In deciding whether to pay dividends on our common stock in the future, our board of directors will consider certain factors they may deem relevant, including our earnings and financial condition and our capital expenditure requirements.

20

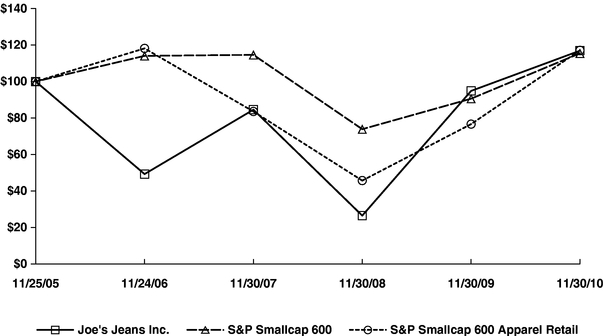

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among Joe's Jeans Inc., the S&P Smallcap 600 Index

and S&P Smallcap 600 Apparel Retail Index

- *

- $100 invested on 11/25/05 in stock or 11/30/05 in index, including reinvestment of dividends.

Indexes calculated on month-end basis.