Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Bridge Capital Holdings | v210660_8k.htm |

FIG Partners’ 2nd Annual West Coast

Bank CEO Forum

Bank CEO Forum

Daniel P. Myers

President

Chief Executive

Officer

February 10,

2011

Thomas A. Sa

Executive Vice President

Chief Financial Officer and Chief

Strategy Officer

2

2

Forward Looking

Statements

Certain matters discussed herein

constitute forward-looking statements within the

meaning of the Private Securities Litigation Reform Act of 1995, and are subject to

the safe harbors created by that Act. Forward-looking statements describe future

plans, strategies, and expectations, and are based on currently available

information, expectations, assumptions, projections, and management's judgment

about the Bank, the banking industry and general economic conditions. These

forward looking statements are subject to certain risks and uncertainties that could

cause the actual results, performance or achievements to differ materially from

those expressed, suggested or implied by the forward looking statements. These

risks and uncertainties include, but are not limited to: (1) competitive pressures in

the banking industry; (2) changes in interest rate environment; (3) general

economic conditions, nationally, regionally, and in operating markets; (4) changes

in the regulatory environment; (5) changes in business conditions and inflation; (6)

changes in securities markets; (7) future credit loss experience; (8) the ability to

satisfy requirements related to the Sarbanes-Oxley Act and other regulation on

internal control; (9) civil disturbances or terrorist threats or acts, or apprehension

about the possible future occurrences of acts of this type; and (10) the involvement

of the United States in war or other hostilities. The reader should refer to the more

complete discussion of such risks in Bridge Capital Holdings reports on Forms 10-

K and 10-Q on file with the SEC.

meaning of the Private Securities Litigation Reform Act of 1995, and are subject to

the safe harbors created by that Act. Forward-looking statements describe future

plans, strategies, and expectations, and are based on currently available

information, expectations, assumptions, projections, and management's judgment

about the Bank, the banking industry and general economic conditions. These

forward looking statements are subject to certain risks and uncertainties that could

cause the actual results, performance or achievements to differ materially from

those expressed, suggested or implied by the forward looking statements. These

risks and uncertainties include, but are not limited to: (1) competitive pressures in

the banking industry; (2) changes in interest rate environment; (3) general

economic conditions, nationally, regionally, and in operating markets; (4) changes

in the regulatory environment; (5) changes in business conditions and inflation; (6)

changes in securities markets; (7) future credit loss experience; (8) the ability to

satisfy requirements related to the Sarbanes-Oxley Act and other regulation on

internal control; (9) civil disturbances or terrorist threats or acts, or apprehension

about the possible future occurrences of acts of this type; and (10) the involvement

of the United States in war or other hostilities. The reader should refer to the more

complete discussion of such risks in Bridge Capital Holdings reports on Forms 10-

K and 10-Q on file with the SEC.

3

3

3

3

Why Are We

Different?

Business banking focus

True business line diversification

commercial/industrial technology structured

finance

SBA cash

management international trade services CRE/construction

management international trade services CRE/construction

Early & proactive risk

recognition and management

Positioned to prosper as economic

recovery takes hold

Solid core business

franchise

A business banking franchise that is

the

Professional Business Bank of

Choice

for small and middle market

companies, and emerging technology businesses,

in the markets we serve

in the markets we serve

4

4

4

4

Bridge Bank

Franchise

Funding-driven approach to building

the business

Experienced board and management

Disciplined execution of our

business plan

No subprime, GSE, CDO, SIV exposure

Reduced exposure to construction and

land

Full range of corporate banking

products delivered through

experienced advisors

experienced advisors

Unique & effective use of

banking technology

Attractive Silicon Valley market and

other expansion

opportunities

opportunities

Ranked No. 1 for largest non-real

estate C&I portfolio1

1 American Banker Magazine, American

Bankers Association, Published January 21, 2011; Independent banks with less

than $1 billion of assets.

7

7

7

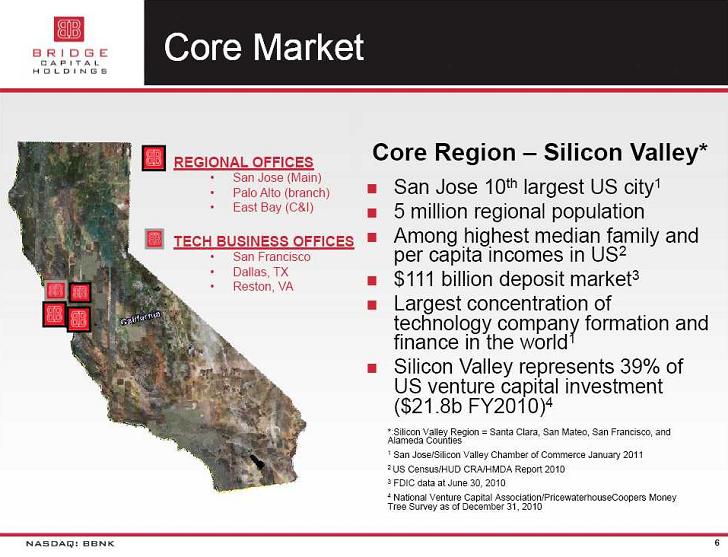

% Deposits

Santa Clara,

San Mateo,

Alameda

Counties

Market

Opportunity

Silicon Valley Region Deposits:

$110.7 Billion

7

Adjusted to reflect roll-ups of WAMU

to Chase, Wachovia to WFB, UCBH to East West and Merrill to BofA

Source: FDIC; as of June 30,

2010

8

8

8

8

The

Environment

SIGNS OF STABILITY:

Residential Real Estate

Technology Sector

Loan Demand

AREAS OF CONCERN:

Unemployment

Commercial Real Estate

Venture Capital Funding Levels

Government / Regulation

Deleveraging

10

10

10

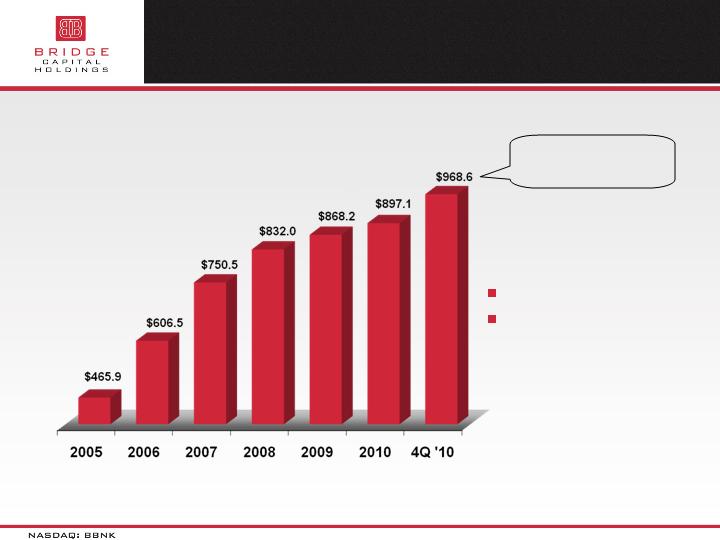

Average Total Assets

($M)

Expanding Market

Presence

Core deposit driven

Purely organic

growth

$1b total

assets

EOP Q4’10

11

11

11

Focus on Core

Funding Sources

11

$ millions

(EOP)

Deposit Mix

95% core deposits

Cost of funds

40 bps FY ’10

31 bps Q4 ‘10

12

12

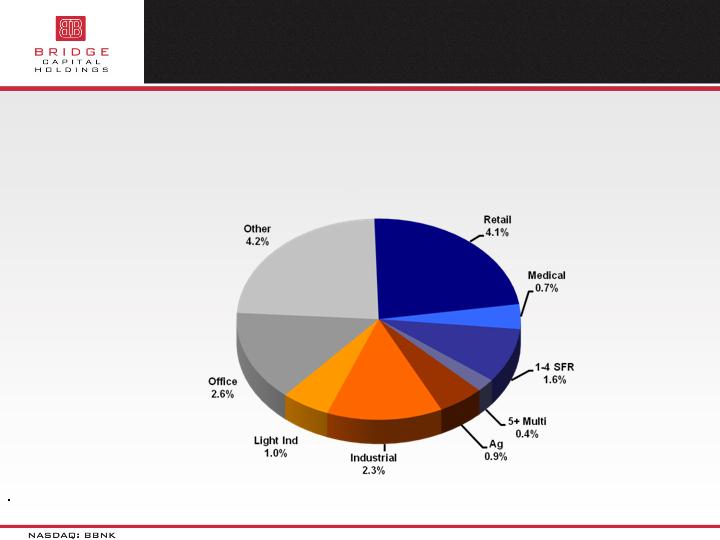

Diversification of

Lending Activity

12

Loan Mix as of December 31,

2010

60%

non-real estate

$652 Million

@ 12-31-10

Peer Average*

Non-Real Estate % of Total Loans –

22%*

*US Public Banks $500M-$1.5B TA; SNL

as of September 30, 2010

13

Loan Portfolio

Diversification

13

BBNK RE = 40% (60%

Non-RE)

Peer* RE = 78% (22%

Non-RE)

*US Public Banks $500M-$1.5B TA; SNL

as of September 30, 2010

December 31, 2010

14

14

14

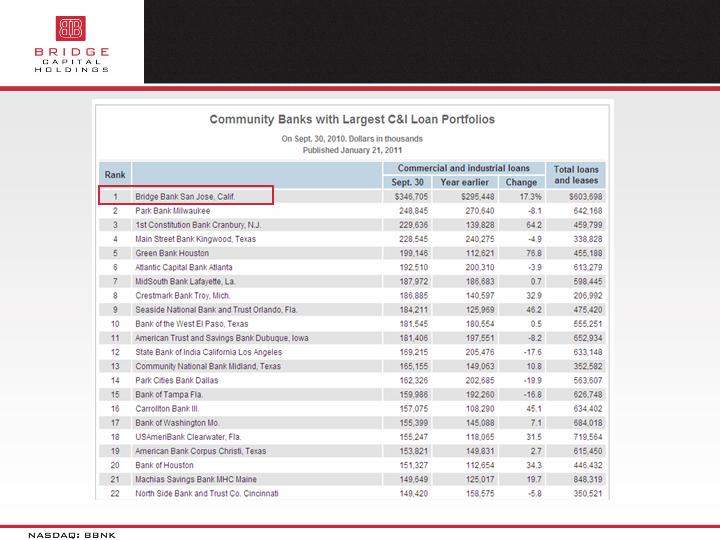

Ranked #1 for Largest

C&I Portfolio

(Non-Real

Estate)

Source: American Banker

magazine, American Bankers Association, Independent banks with less than $1

billion of assets.

Land &

Construction Outstanding as a

% of Bank Regulatory Capital In ($MM’s)

% of Bank Regulatory Capital In ($MM’s)

56.6%

Jun-09

$94.0

$79.7

80.9%

Mar-09

$117.2

$97.8

100.4%

Dec-08

$49.0

$39.4

39.2%

Jun-10

$47.5

38.9%

Mar-10

$37.3

Dec-09

$33.4

$46.6

38.6%

$34.3

$20.6

181.5%

Sep-09

$66.4

Dec-10

$49.8

$40.7

39.6%

Sep-10

$128.1

$105.3

110.1%

Sep-08

$142.1

$101.0

Jun-08

$161.2

$102.3

$12.8

28.0%

$52.9

Construction

Land

% of Regulatory Capital

Regulatory

Threshold

Threshold

100%

15

Total CRE

Outstanding as a % of Bank

Regulatory Capital In ($MM’s)

Regulatory Capital In ($MM’s)

Dec-10

Sep-10

$120.8

$39.4

96.8%

Jun-10

$118.1

$37.3

96.6%

Mar-10

$115.3

$34.3

95.6%

Dec-09

$120.7

$20.6

101.2%

Sep-09

$131.7

$52.9

112.3%

Jun-09

$165.0

$79.7

142.1%

Mar-09

$185.1

$97.8

158.5%

Dec-08

$202.4

$105.3

173.9%

Sep-08

$211.8

$101.0

$41.1

Jun-08

$239.1

$102.3

269.3%

97.4%

$9.1

$40.7

$122.4

CRE Investment & Unsecured Loans

to Developers

Construction

Land

% of Regulatory Capital

Regulatory

Threshold

Threshold

300%

16

17

17

Land &

Construction Breakdown

(8%)

(8%)

Total Loan

Portfolio

Construction

(6.1%)

Land

(1.4%)

17

All percentages stated as percent of

total loan portfolio

Const Reduced 64%*

Land Reduced 86%*

* = Amount of Commitments Reduced

from June 30, 2008 to December 31, 2010

18

CRE Breakdown

(18%)

41% = Owner Occupied

59% = Investor

18

Current @ origination

LTV = 46%* 50%**

DSC = 1.39x* 1.49x**

CAP = 7.4%* 6.6**

= LTV, DSR, CAP = CRE portfolio

weighted averages for Q4 2010

** = LTV, DSR, CAP = CRE portfolio

weighted averages at loan origination

19

19

19

High Quality

Business

Peer*

Average

3.75%

= *US Public Banks $500M-$1.5B TA;

SNL as of December 31, 2010

Net Interest

Margin

20

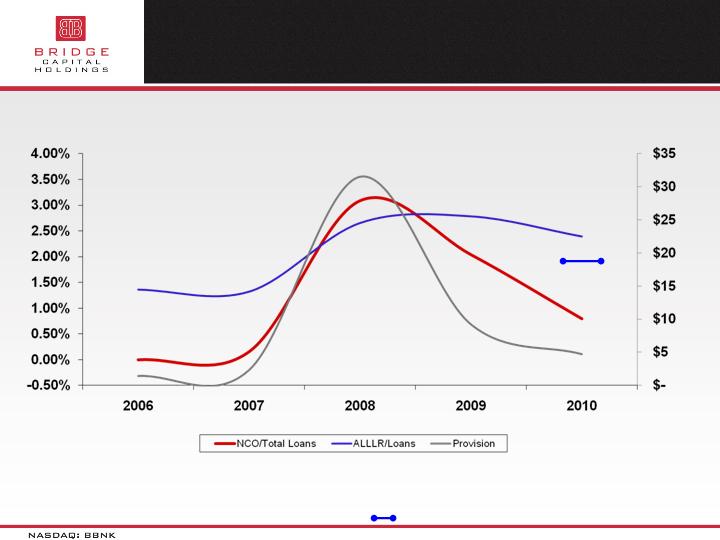

Credit Quality

Trends

20

21

PEER*

(ALLL/Loans)

Reserves Remain High

While

Credit Losses

Moderate

= SNL Data: US Public Banks Total

Assets $0.5B to $1.5M as of December 31, 2010

1.98%

22

22

Operating

Leverage

$MM

23

*

BBNK

Revenue/Employee

146% of Peer*

Group Avg

Revenue/Employee

146% of Peer*

Group Avg

*= Average Rev/Empl of US Public

Banks $500M-$1.5B TA; SNL as of as of September 30, 2010

Revenue

Per

Employee

($000)

Per

Employee

($000)

Effective Revenue

Generation

302.2

207.6

$100

$150

$200

$250

$300

$350

2003

2004

2005

2006

2007

2008

2009

2010

BBNK

Peer

24

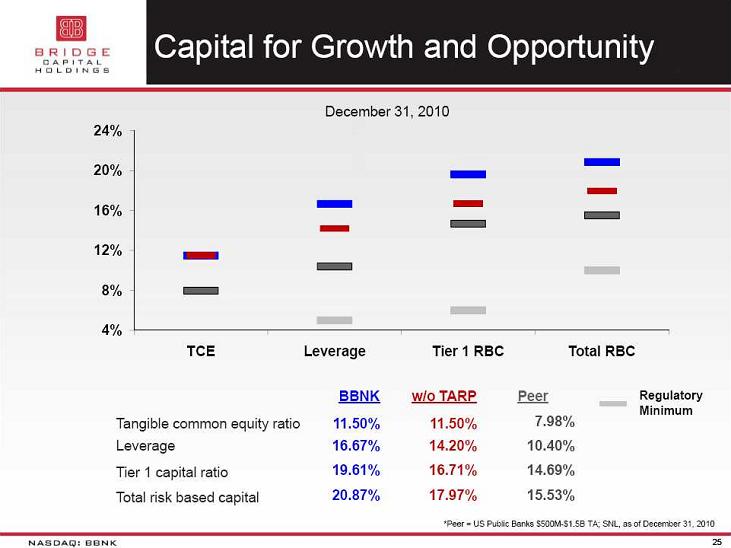

BBNK Capital

Structure

24

26

26

26

26

2010

Summary

Operating profit of $2.6 million

54% growth from 2009 to 2010

Surpassed $1.0 billion in total

assets

Substantially improved TCE ratio

$3M savings per year from

preferred-to-common conversion

Secured $30M private placement

Continued strong growth in core

deposits

Improving credit quality

NCOs reduced 56% from prior year

NPA’s including TDR’s reduced by 31%

NIM expanded to 4.99% from 4.58% in

2009

Robust new business activity

$474 million in new credit

commitments

360+ new client

relationships

27

27

27

Net Income &

EPS

$1.27

$1.57

($000, except per diluted share

amounts)

$0.85

$0.46

$0.24

Excludes Recognition of Deferred Tax

Asset of $1.9M in FY 2003

($1.15)

($0.42)

$0.06

Preferred

Dividends

Dividends

‘09 $4,203

‘10 $1,955

28

Potential Tailwinds

Ahead…

Utilization rates on LOC at low ebb

Have continued to add new

commitments

Utilization currently in the range

of 35-40%

As economy improves rate could move

up to 45%+

Natural asset-sensitivity

Positioned for rising rate

environment

Ready funding source for increased

loan demand

Lower levels of credit stress

Potential recoveries

Normalizing of credit costs

Continued organic growth

Loan balance increased 13% in 2010

28

29

29

29

29

Investment

Summary

Improving fundamentals provide

strong foundation for

increasing profitability

increasing profitability

Growing core deposit franchise

Increasing loan demand

Improved operating leverage

Expanding net interest margin

Improving credit quality with

manageable exposure to

CRE

CRE

Strong capital position provides

opportunity to pursue

attractive growth opportunities in our markets

attractive growth opportunities in our markets

Increasing presence in market with

attractive long-

term growth potential

term growth potential

30

30

Thank You / Q &

A