Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Patriot Coal CORP | d8k.htm |

FINANCIAL

COMMUNITY PRESENTATION

February 9 & 10, 2011

Exhibit 99.1 |

2

Some of the following information contains forward-looking statements within the meaning

of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange

Act of 1934, as amended, and is intended to come within the safe-harbor protection

provided by those sections. Forward-Looking Statements

Certain statements in this presentation are forward-looking as defined in the Private

Securities Litigation

Reform

Act

of

1995.

These

statements

involve

certain

risks

and

uncertainties

that

may

be

beyond our control and may cause our actual future results to differ materially from

expectations. We do not undertake to update our forward-looking

statements. Factors that could affect our results include, but are not limited

to: price volatility and demand, particularly in higher margin products; geologic,

equipment and operational risks associated with mining; changes in general economic

conditions, including coal and power market conditions; coal mining laws and regulations; the

availability and costs of competing energy resources; legislative and regulatory

developments; risks associated with environmental laws and compliance, including

selenium-related matters; developments in greenhouse gas emission regulation and

treatment; labor availability and relations; the outcome of pending or future

litigation; changes in the costs to provide healthcare to eligible active employees and

certain retirees under postretirement benefit obligations; changes in contribution

requirements to multi-employer retiree healthcare and pension funds; reductions of

purchases or deferral of shipments by major customers; availability and costs of

credit; customer performance and credit risks; inflationary trends; worldwide economic

and political conditions; downturns in consumer and company spending; supplier

and

contract

miner

performance

and

the

availability

and

cost

of

key

equipment

and

commodities; availability and costs of transportation; the Company’s ability to replace

coal reserves; the

outcome

of

commercial

negotiations

involving

sales

contracts

or

other

transactions;

our

ability

to

respond

to

changing

customer

preferences;

failure

to

comply

with

debt

covenants;

the

effects

of

mergers, acquisitions and divestitures; and weather patterns affecting energy demand.

The Company undertakes no obligation (and expressly disclaims any such obligation) to

publicly update or revise any forward-looking statement, whether as a result of new

information, future events or otherwise. For additional information concerning

factors that could cause actual results to materially differ from those projected

herein, please refer to the Company’s Form 10-K and Form 10-Q reports.

Patriot Coal Statement on Forward-Looking Information |

3

The Dynamic Global Coal Markets |

4

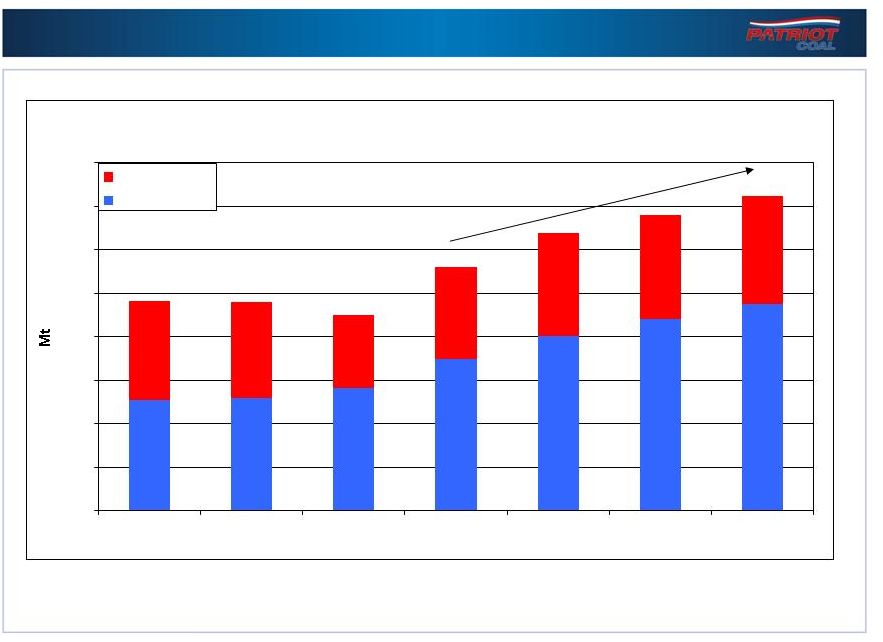

Global seaborne met demand is expected to continue to increase

0

50

100

150

200

250

300

350

400

2007

2008

2009

2010E

2011F

2012F

2013F

World (ex Asia)

Asia

Source: McCloskey

Expanding Seaborne Met Demand |

5

Exports are negative

Drivers of Global Coal Demand

Global met & thermal coal demand driven by China & India

-75

-50

-25

0

25

50

75

100

125

150

175

China

India

2005

Note: Imports are positive

2010 |

6

Russia, Vietnam

Indonesia, S. Africa,

Why Global Coal Supply is Constrained

Global supply constraints are tightening markets

Australia

Infrastructure constraints limit

long

-term supply increase

Record rainfall threatens to

reduce production by 15 -

20Mt in 2011

Infrastructure needed to

supply global demand

China

Constrained rail & truck

infrastructure makes

shipping within China

difficult

Indigenous met coal is

lower quality

Formerly a net exporter,

currently a net importer

India

Plentiful indigenous coal reserves, but

lower quality

Poor transportation infrastructure

Indonesia, S. Africa,

Russia, Vietnam

Dom

estic

demand increases are

absorbing coal production historically

exported

Declining exports

US

Depleting eastern reserves

Difficult permitting

Stricter implementation of

safety rules

Supply increases will be

difficult

Colombia

Heavy La Nina rains are limiting

production and exports

Australia

Infrastructure constraints limit

Record rainfall threatens to

reduce production by 15

20Mt in 2011

Infrastructure needed to

supply global demand

China

Constrained rail & truck

infrastructure makes

shipping within China

difficult

Indigenous met coal is

lower quality

Formerly a net exporter,

currently a net importer

India

Plentiful indigenous coal reserves, but

lower quality

Poor transportation infrastructure

Dom

estic

demand increases are

absorbing coal production historically

exported

Declining exports

US

Depleting eastern reserves

Difficult permitting

Stricter implementation of

safety rules

Supply increases will be

difficult

Colombia

Heavy La Nina rains are limiting

production and exports |

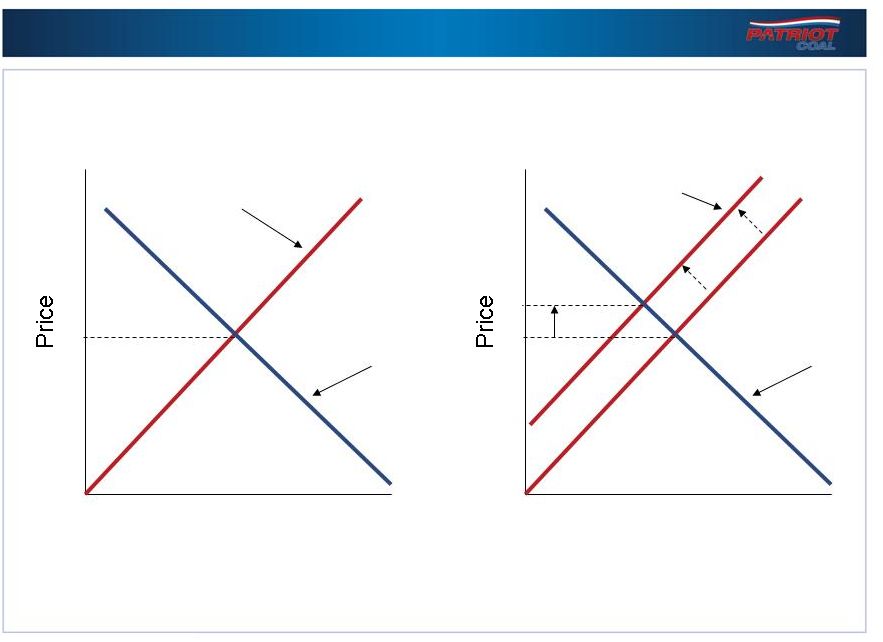

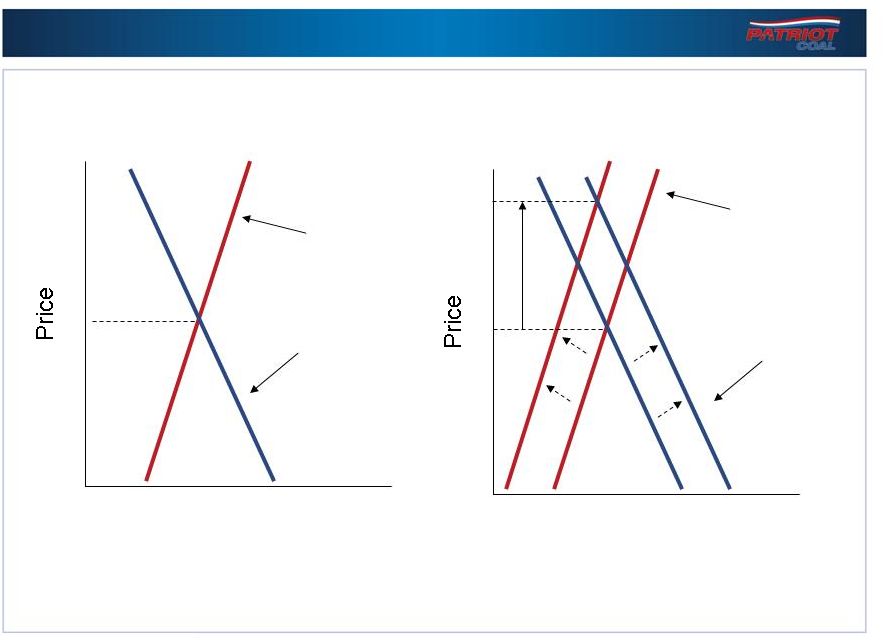

7

Typical Determination of Price

Quantity

Supply

Demand

Quantity

Supply

Demand

Price increases as supply contracts |

8

Coal Market Determination of Price

Prices are rapidly rising due to the steep supply & demand curves

Quantity

Supply

Demand

Quantity

Supply

Demand |

9

How Markets React to Higher Price

Thermal & met markets are co-dependent

–

Near-

to intermediate-term, coal production is a closed

system

Both metallurgical and thermal prices are rising

–

Met prices are rising very rapidly

Coal producer reactions

–

More thermal coal crosses over to met

–

Longer-term, more met mines will be opened or re-opened to

increase supply

Customer reactions

–

Use lower quality met coal

–

Re-direct higher quality met coal to higher priced steel

–

Increase use of electric arc furnaces for steel production

•

Uses scrap steel instead of met coal |

10

Scrap Steel Price Dynamics

Scrap steel prices have been steadily rising

0

100

200

300

400

500

600

700

No1 Heavy Melting Export Index, fob East Coast

Shredded Steel Scrap, fob East Coast

No1 Heavy Melting US Index, fob Pittsburgh,

Philadelphia, Chicago

Updated:

1/27/201 |

11

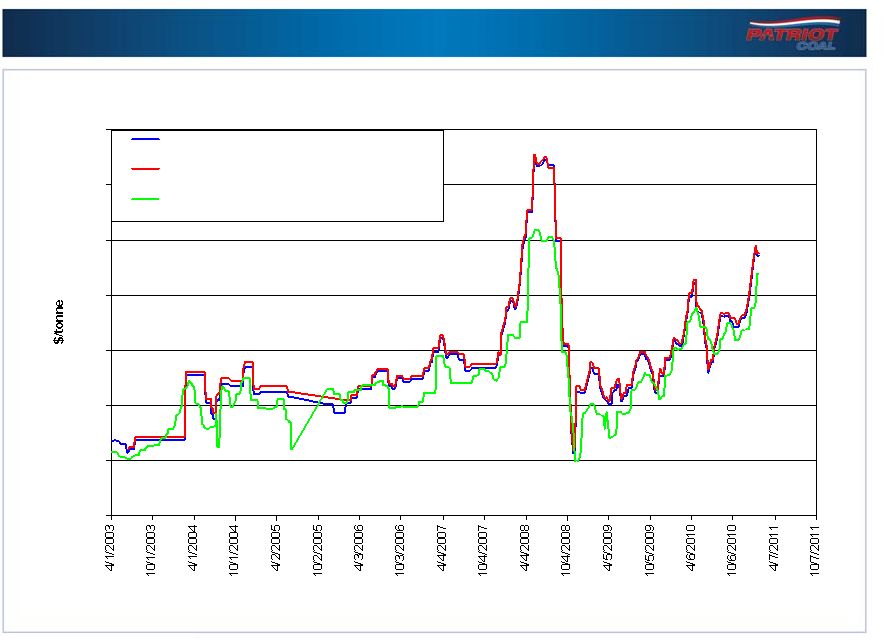

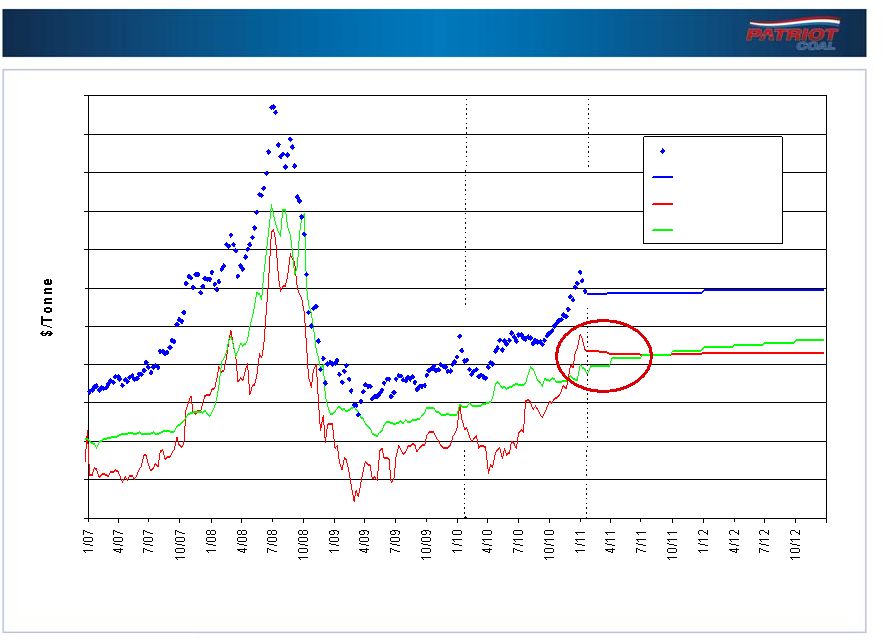

Higher European Thermal Import Prices

Higher global thermal prices provide opportunity for U.S. exports

0

20

40

60

80

100

120

140

160

180

200

220

API2 Prompt Quarter

API2 Forward, 1/31/11

CAPP Netback

CAPP Prompt & Forward

Updated:

02/02/11

Source: McCloskey

0

20

40

60

80

100

120

140

160

180

200

220

API2 Prompt Quarter

API2 Forward, 1/31/11

CAPP Netback

CAPP Prompt & Forward

Updated:

02/02/11

Source: McCloskey |

12

Higher U.S. industrial production will create more coal demand

-

2

4

6

8

10

12

14

16

18

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11E

12E

13E

14E

15E

16E

Note: Data provided by CSM Worldwide

Rebounding U.S. Automobile Production |

13

How PCX Will Participate in

Strong Coal Markets |

14

Bolt-on

Acquisitions

Increased

Market Cap

Organic

Growth

Expanding

Revenues

& Cash Flow

Transformational

M&A

Patriot’s Growth Cycle

PCX

Foundation of

Strength &

Potential |

15

PCX –

Strength & Potential

1.8 billion tons of proven and probable

reserves

Multiple basins, mining operations & shipping

options

Leading producer of metallurgical coal

Highest Btu basins –

CAPP, NAPP, ILB

Strong safety culture

Significant leverage to rising prices

Meaningful EBITDA upside in 2012 & 2013

from expiration of legacy contracts

Project pipeline to capitalize on opportunities

Organic metallurgical coal growth

7 new mines in next 2 years

Targeting more than 11.0 million tons

production by 2013

Targeting 40.0 million tons total production

within 5 years

Proven M&A track record

Expanding

Revenue

& Cash Flow

Organic Growth

and M&A

Foundation of

Strength &

Potential |

16

Product Diversification

0%

25%

50%

75%

100%

APP

CAPP thermal

NAPP

ILB

ILB

Underground

Surface

2010 Tons Sold

30.9 Million Tons

Mining Method

67%

Reserves

1.8 Billion Tons

Diverse locations, products & mining methods

Significant met coal exports

2010 Met Shipments

Domestic

Export

Met |

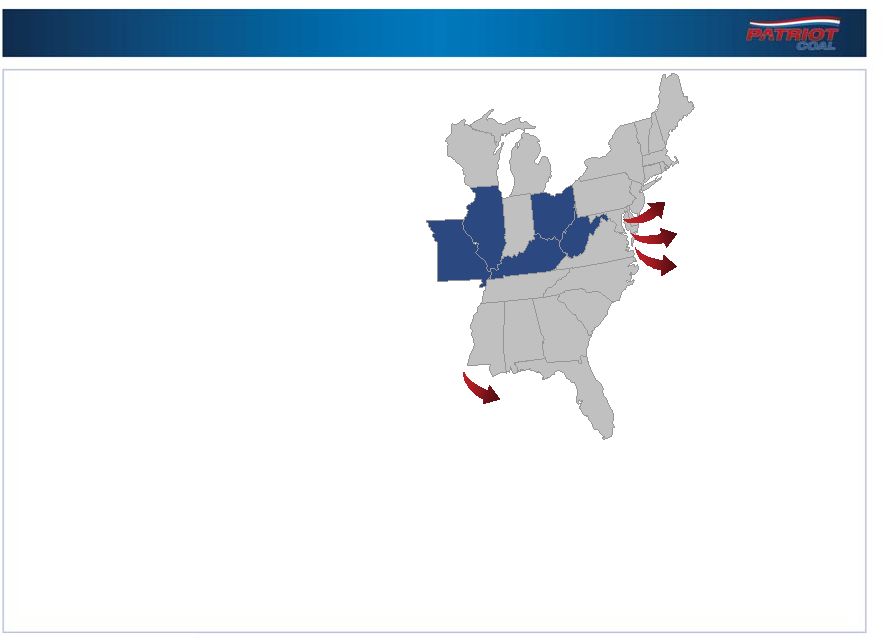

17

Advantage of Diversity

Multiple Basins & Coal Qualities:

Northern Appalachia Thermal

Federal

Central Appalachia Metallurgical

Kanawha Eagle

Panther

Rocklick

Wells

Central Appalachia Thermal

Big Mountain

Blue Creek

Campbell’s Creek

Corridor G

Logan County

Paint Creek

Illinois Basin Thermal

Bluegrass

Dodge Hill

Highland

Multiple quality & transportation options

Transportation Optionality:

Rail

Barge

East Coast & Gulf exports

IL

OH

KY

WV

MO

New Orleans

Baltimore

Newport News

Norfolk |

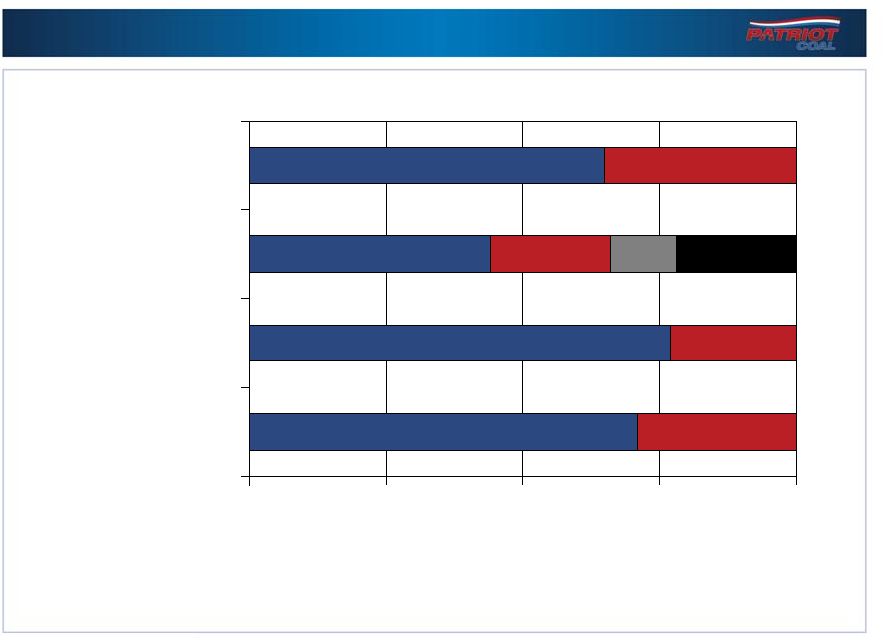

18

0

2

4

6

8

10

12

14

16

18

Metallurgical

Appalachia

Thermal

Illinois Basin

Priced

Unpriced

Leverage to Higher Pricing in 2011

48 -

53

40

Illinois Basin

$65 -

$85

TBD

Current

Market

59

$127

Priced

Business

Metallurgical

Appalachia

Thermal

Significant leverage to higher pricing in 2011

50% Rocklick

& Wells; 50%

Panther-type |

19

48 –

53

49

Illinois Basin

$70 -

$90

NA

Current

Market

$57

NA

Priced

Business

Metallurgical

Appalachia

Thermal

Significant leverage to higher pricing in 2012

Leverage to Higher Pricing in 2012

0

2

4

6

8

10

12

14

16

18

Metallurgical

Appalachia

Thermal

Illinois Basin

Priced |

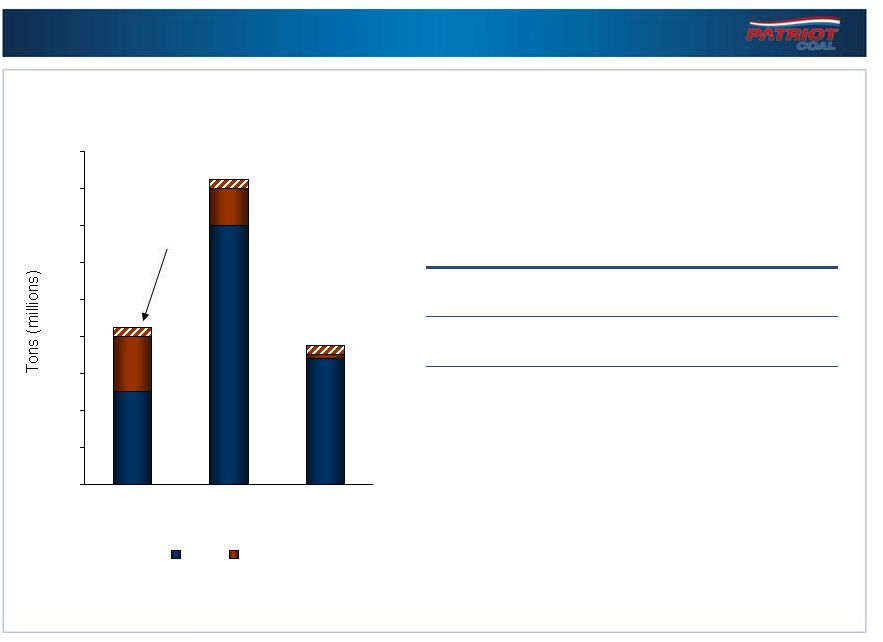

20

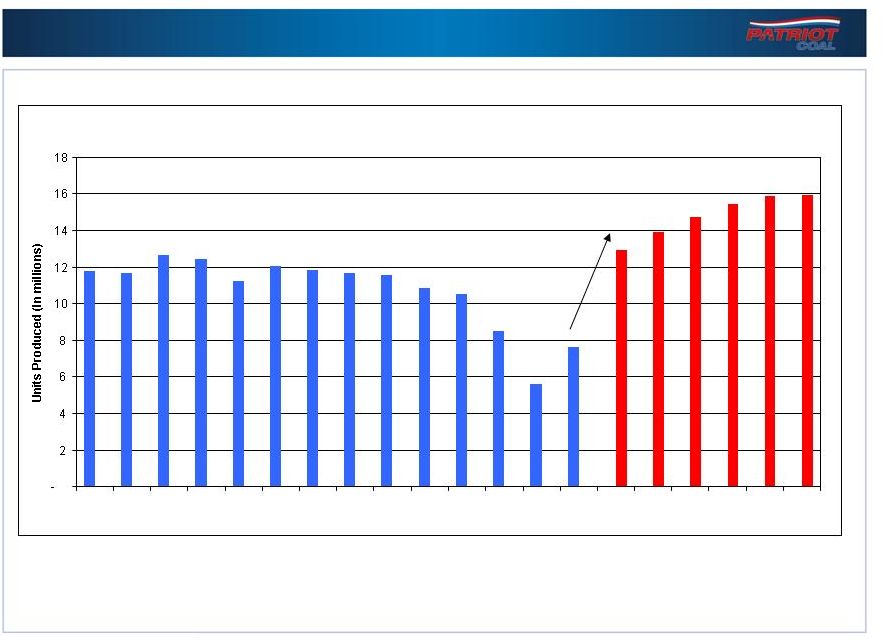

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2005

2006

2007

2008

2009

2010

2011

2012

2013

Patriot Met Coal Expansion Plans

Opening 7 new met mines to meet rising worldwide demand

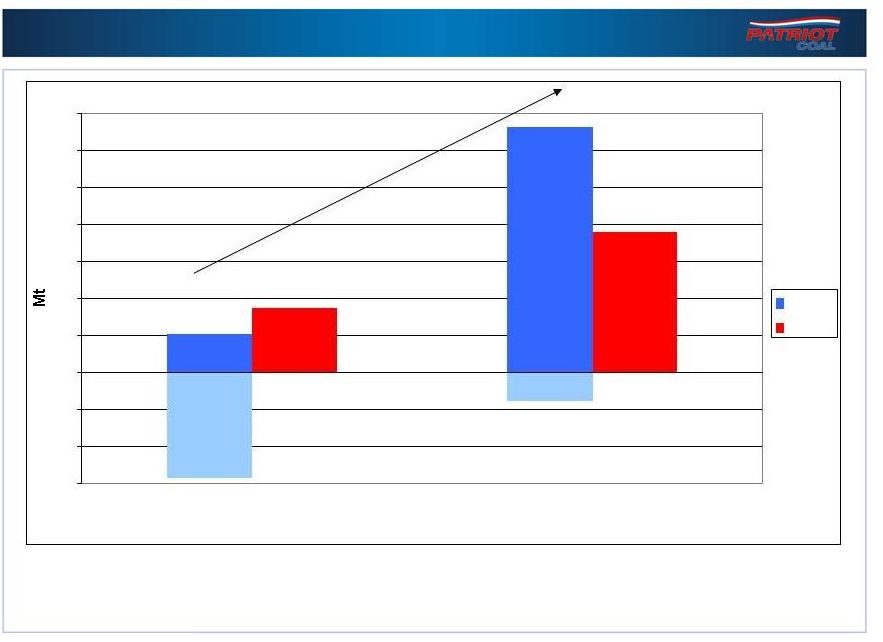

+60% increase |

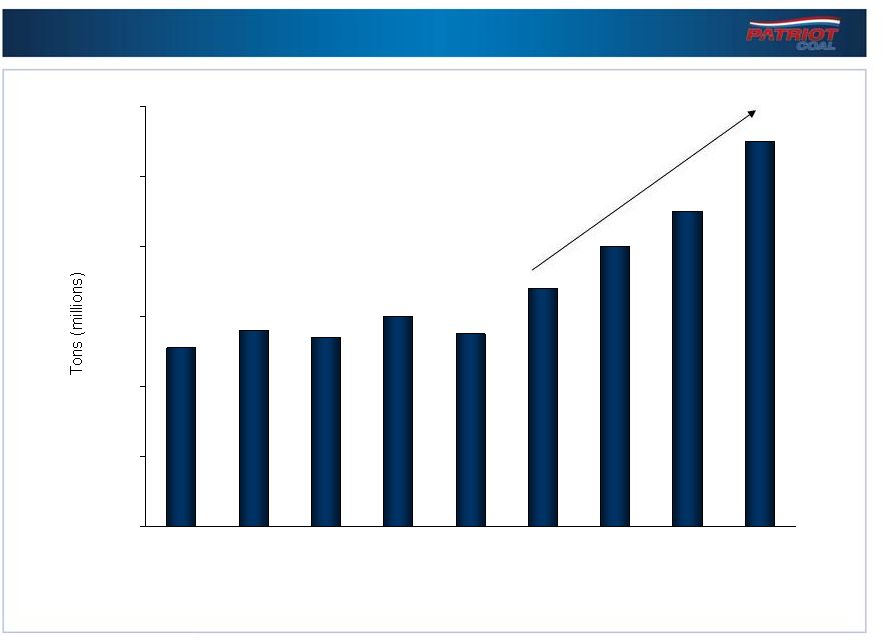

21

0%

5%

10%

15%

20%

25%

30%

35%

2009

2010

2011

2012

2013

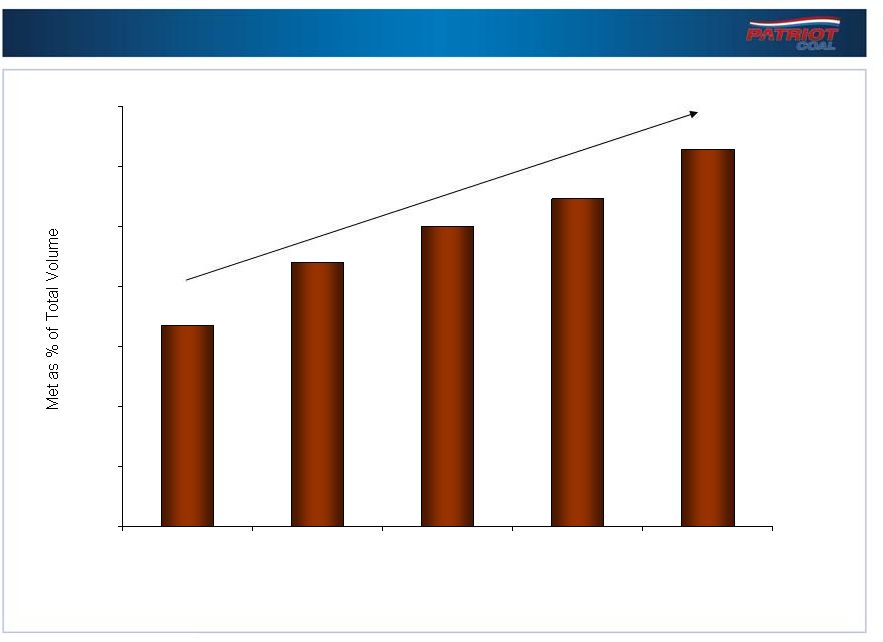

Increasing Met Exposure

Expanding high-margin met coal as a percent of total production

+85% increase |

22

Impact of Legacy Thermal Contracts

$0

$50

$100

$150

$200

Current

Market

Less

$5.00/ton

Current

Market

Current

Market

Plus

$5.00/ton

6.5

million

tons

to

be

repriced

over

the

next

24

months

$0

$50

$100

$150

$200

Current

Market

Less

$5.00/ton

Current

Market

Current

Market

Plus

$5.00/ton

2012

2013 |

23

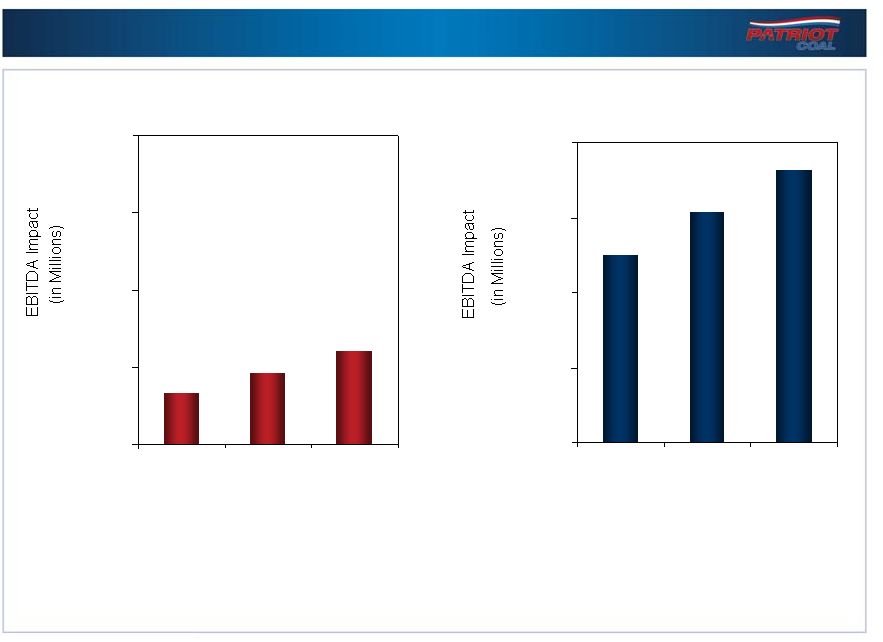

Price Sensitivity

Increase in Price per Ton

Higher prices have a dramatic impact on EBITDA

* Assumes 23 million tons thermal, 8 million tons met, 15% taxes/royalties

Thermal

Met

$0

$100

$200

$300

$400

$500

$5

$10

$15

$20 |

24

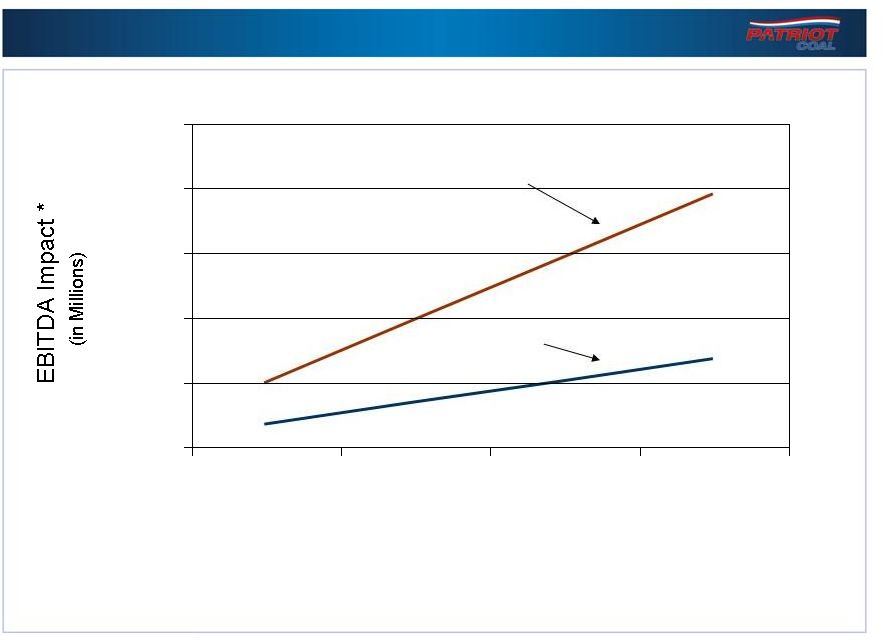

Financial Metrics

EBITDA

(in Millions)

EBITDA per ton

28% increase

$0

$25

$50

$75

$100

$125

$150

2008

2009

2010

50% increase

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00 |

25

Bolt-on

Acquisitions

Increased

Market Cap

Organic

Growth

Expanding

Revenues

& Cash Flow

Transformational

M&A

Patriot’s Growth Cycle

PCX

Foundation of

Strength &

Potential |

FINANCIAL

COMMUNITY PRESENTATION

February 9 & 10, 2011

Contact:

Janine Orf

Director, Investor Relations

314.275.3680

jorf@patriotcoal.com |

27

$(48.0)

(0.5)

12.8

(57.4)

(15.2)

(63.0)

121.5

(188.1)

$141.9

2010

-

-

Income tax provision

$127.2

16.6

(38.1)

(20.2)

(35.1)

298.6

(205.3)

$110.7

2009

-

Restructuring & Impairment Charge

249.5

Sales Contract Accretion, net

$142.7

17.2

(23.6)

(19.2)

(125.4)

$44.2

2008

EBITDA

Net Income (Loss)

Interest Income

Reclamation & Remediation

Obligation Expense

Depreciation, Depletion &

Amortization

Interest Expense

Reconciliation of EBITDA to Net Income

($ in Millions) |