Attached files

| file | filename |

|---|---|

| EX-5.1 - OPINION AND CONSENT OF CLARK WILSON LLP - MNP Petroleum Corp | exhibit5-1.htm |

| EX-23.1 - CONSENT OF DELOITTE AG - MNP Petroleum Corp | exhibit23-1.htm |

| EX-99.1 - AUDIT COMMITTEE CHARTER - MNP Petroleum Corp | exhibit99-1.htm |

| EX-21.1 - SUBSIDIARIES - MNP Petroleum Corp | exhibit21-1.htm |

| EX-23.2 - CONSENT OF BDO VISURA INTERNATIONAL AG - MNP Petroleum Corp | exhibit23-2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

MANAS PETROLEUM CORPORATION

(Exact name of registrant as specified in its charter)

Nevada

(State or other jurisdiction of

incorporation or organization)

1311

(Primary Standard Industrial

Classification Code Number)

91-1918324

(I.R.S. Employer Identification Number)

Bahnhofstrasse 9

6341 Baar, Switzerland

Telephone: +41 (44) 718 10 30

(Address,

including zip code, and telephone number,

including area code, of

registrant’s principal executive offices)

Nevada Corporate Services, Inc.

8883 West Flamingo

Road, Suite 102

Las Vegas, NV 89147

Telephone: (702)

947-4100

(Name, address, including zip code, and telephone

number,

including area code, of agent for service)

Copy of Communications To:

Clark Wilson LLP

Attention: Ethan Minsky

Suite 800 - 885 West Georgia

Street

Vancouver, British Columbia V6C 3H1,

Canada

Telephone: (604) 643-3151

As soon as practicable after the effective date of this

registration statement.

(Approximate date of commencement of proposed sale to the public)

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: [X]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] |

| Non-accelerated filer [ ] | Smaller reporting company [X] |

| (Do not check if a smaller reporting company) |

Calculation of Registration Fee

| Title of Each Class of Securities to be Registered |

Proposed Maximum

Aggregate Offering Price(1) |

Amount of Registration Fee |

Common Stock |

$34,500,000(2) |

$4,005.45 |

| (1) |

Estimated solely for the purposes of calculating the amount of the registration fee in accordance with Rule 457(o) under the Securities Act of 1933. |

| (2) |

The proposed maximum aggregate offering price includes amounts attributable to shares that may be issued upon exercise of the over-allotment option by the placement agents. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

2

EXPLANATORY NOTE

This registration statement contains two forms of prospectus: one to be used in connection with the offering of the securities described herein in the United States and one to be used in connection with the offering of such securities in Canada. The form of the U.S. prospectus is included herein and is followed by the alternate and additional pages to be used in the Canadian prospectus. Each of the alternate pages for the Canadian prospectus included herein is labeled “Alternate Page for Canadian Prospectus.” Each of the additional pages for the Canadian prospectus included herein is labeled “Additional Page for Canadian Prospectus”. The form of the U.S. prospectus is identical to the form of the Canadian prospectus except for these alternate and additional pages.

3

|

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted. |

| PROSPECTUS | Subject to Completion |

| ______________, 2011 |

Minimum Offering: <> Shares

Maximum

Offering: <> Shares

Manas Petroleum Corporation

Common Stock

_________________________________

We are offering a minimum of <> shares of our common stock and a maximum of <> shares of our common stock.

Our placement agents, Raymond James Ltd. in Canada and its registered broker-dealer affiliate, Raymond James (USA) Ltd. in the United States, are selling the shares of our common stock on a “reasonable commercial efforts all or nothing” basis as to the minimum number of shares to be sold and a “reasonable commercial efforts” basis thereafter up to the maximum amount. The placement agents must sell the minimum number of shares of our common stock offered (<> shares) if any are sold. The placement agents have agreed to use their reasonable commercial efforts to sell the shares of our common stock being offered. The offering will terminate upon the earlier of: (i) a date mutually acceptable to us and our placement agents after the minimum offering is sold or (ii) <>. Until we sell at least <> shares of our common stock, all subscription proceeds will be held in a separate bank account of the placement agents in trust. If we do not sell at least <> shares of our common stock by <>, all funds will be promptly returned to investors within three business days without interest or deduction.

Our common stock is traded on the OTC Bulletin Board under the symbol “MNAP.OB”. On January 28, 2011, the closing price (last sale of the day) for one share of our common stock was $0.60. We have applied to list the shares of our common stock on the TSX Venture Exchange. Such listing will be subject to our fulfillment of all requirements of the TSX Venture Exchange. There can be no assurance that the shares of our common stock will be listed on the TSX Venture Exchange.

Investing in our common stock involves significant risks. See “Risk Factors” beginning on page 17.

| Per Share | Minimum Offering | Maximum Offering | |||||||

| Public offering price | $ | <> | $ | 20,000,000 | $ | 30,000,000 | |||

| Placement commissions | $ | <> | $ | 1,400,000 | $ | 2,100,000 | |||

| Proceeds to us, before expenses | $ | <> | $ | 18,600,000 | $ | 27,900,000 |

The placement agents may also sell up to an additional <> shares at the public offering price within 30 days from the date of closing of this offering to cover over-allotments.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

![]()

The date of this prospectus is ____________, 2011.

4

[ALTERNATE PAGE FOR CANADIAN PROSPECTUS]

|

A copy of this preliminary prospectus has been filed with the securities regulatory authorities in every province of Canada except Québec, but has not yet become final for the purpose of the sale of securities. Information contained in this prospectus may not be complete and may have to be amended. The securities may not be sold until a receipt for the prospectus is obtained from the securities regulatory authorities. |

No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise. This prospectus constitutes a public offering of these securities only in those jurisdictions where they may be lawfully offered for sale and therein only by persons permitted to sell such securities. We have filed a registration statement on Form S-1 with the United States Securities and Exchange Commission under the United States Securities Act of 1933 with respect to these securities. See “Plan of Distribution”.

PRELIMINARY PROSPECTUS

| New Issue | January 31, 2011 |

Minimum Offering: US$20,000,000 (<> Shares)

Maximum Offering: US$30,000,000 (<> Shares)

Manas Petroleum Corporation

Common Stock

_________________________________

This prospectus qualifies the distribution of a minimum of <> shares of our common stock and a maximum of <> shares of our common stock at a price of US$<> per share for gross proceeds of a minimum of US$20,000,000 and a maximum of US$30,000,000. We have engaged Raymond James Ltd. to act as our agent in connection with the sale of shares of our common stock on a “reasonable commercial efforts” basis.

Our common stock is traded on the OTC Bulletin Board under the symbol “MNAP.OB”. On January 28, 2011, the closing price (last sale of the day) for one share of our common stock on the OTC Bulletin Board was $0.60. We have applied to list the shares of our common stock on the TSX Venture Exchange. Such listing will be subject to our fulfillment of all requirements of the TSX Venture Exchange. There can be no assurance that the shares of our common stock will be listed on the TSX Venture Exchange.

We are offering our common stock for sale concurrently in Canada under the terms of this prospectus and in the United States under the terms of a registration statement on Form S-1 filed with the United States Securities and Exchange Commission. Our common stock is being offered in Canada by Raymond James Ltd. and in the United States by its registered broker-dealer affiliate, Raymond James (USA) Ltd.

_________________________________

Price: US$<> per

Share

_________________________________

| Price to Public(1)(2) |

Agent’s Commission(3)(4) |

Net Proceeds to Our Company(5)(6) | ||||

| Per Share | US$ | <> | US$ | <> | US$ | <> |

| Minimum Offering | US$ | 20,000,000 | US$ | 1,400,000 | US$ | 18,600,000 |

| Maximum Offering | US$ | 30,000,000 | US$ | 2,100,000 | US$ | 27,900,000 |

| (1) |

The proceeds from subscriptions will be deposited in a separate bank account of the placement agents in trust until subscriptions for a minimum of <> shares of our common stock are received. |

| (2) |

The public offering price for the shares of our common stock being offered was determined by us with input from Raymond James Ltd. |

5

[ALTERNATE PAGE FOR CANADIAN PROSPECTUS]

| (3) |

Pursuant to the terms and conditions of an agency agreement dated <>, 2011 between our company and Raymond James Ltd., we have agreed to pay Raymond James Ltd. a cash commission of seven percent (7%) of the gross proceeds of this offering and warrants to purchase up to that number of shares of our common stock as is equal to three and one-half percent (3.5%) of the number of shares sold in the offering, exercisable at US$<> per share, for a period of 24 months from the date of closing of this offering. See “Plan of Distribution” for more information about the warrants to be issued to Raymond James Ltd. |

| (4) |

We will pay all of the reasonable expenses (including legal expenses) of Raymond James Ltd. relating to this offering. |

| (5) |

Before deduction of the expenses of this offering, estimated to be approximately US$363,000. |

| (6) |

We have granted the placement agents an over-allotment option, exercisable at any time for a period of 30 days from the date of closing of this offering, to purchase at the offering price up to that number of additional shares of common stock equal to 15% of the number of shares of common stock sold in this offering solely to cover over-allotments, if any, and for market stabilization purposes. If the over-allotment option is exercised in full, the total price to public, the placement agents’ commission and net proceeds to us will be US$<>, US$2,415,000 and US$32,085,000, respectively. A purchaser who acquires common stock forming part of the placement agents’ over-allocation position acquires such securities under this prospectus regardless of whether the over-allocation position is ultimately filled through the exercise of the over-allotment option or secondary market purchases. This prospectus qualifies the grant of the over-allotment option and the distribution of the shares of common stock issuable upon exercise of the over-allotment option. See “Plan of Distribution”. |

Investing in our common stock involves significant risks. See “Risk Factors” beginning on page 17.

Our placement agents, Raymond James Ltd. in Canada and its registered broker-dealer affiliate, Raymond James (USA) Ltd. in the United States, conditionally offer the shares of our common stock on a “reasonable commercial efforts” basis, subject to prior sale, if, as and when issued by us and accepted by our placement agents in accordance with the conditions contained in the agency agreement between our company and Raymond James Ltd. referred to under “Plan of Distribution” subject to approval of certain legal matters on our behalf by Clark Wilson LLP and on behalf of our placement agents by Fraser Milner Casgrain LLP.

The following table summarizes the securities granted by us to our placement agents:

Placement Agent’s Position |

Maximum Number of Securities Available |

Exercise Period |

Exercise Price |

| Warrants |

<> |

24 months following the closing of the offering |

US$<> |

| Over-allotment option |

<> |

30 days following the closing of the offering |

US$<> |

A minimum subscription amount of US$25,000 is required from each subscriber. Subscriptions for the shares of our common stock will be subject to rejection or allotment in whole or in part and the right is reserved to close the subscription books at any time without notice. There may be one or more closings for this offering. We expect the initial closing of this offering to occur on or about <>, 2011. We will not close this offering unless we receive subscriptions for a minimum of <> shares of our common stock. If we have not received subscriptions for a minimum of <> shares of our common stock within 90 days after the declaration of the effectiveness of our registration statement by the United States Securities and Exchange Commission or the issuance of a receipt of this prospectus by Canadian securities regulators, whichever is earlier, we will discontinue this offering. Until the initial closing, all subscription proceeds will be held in a separate bank account of the placement agents in trust. If we have not received subscriptions for a minimum of <> shares of our common stock within the above mentioned 90 days, we will cause our placement agents to return the subscription proceeds to subscribers within three business days without interest or deduction. If there is the initial closing of this offering, one or more additional closings, if necessary, may occur until the earlier of the time that we receive subscriptions for a maximum of <> shares of our common stock and the expiry of the above mentioned 90 days.

In connection with the sale of the shares of our common stock, our placement agents may over-allot or effect transactions which stabilize or maintain the market price of the shares of our common stock at levels other than those which might otherwise prevail in the open market. Such transactions may have the effect of preventing or mitigating a decline in the market price of the shares of our common stock. Such transactions, if commenced, may be discontinued at any time. See “Plan of Distribution”.

6

[ALTERNATE PAGE FOR CANADIAN PROSPECTUS]

We are incorporated under the laws of the state of Nevada in the United States. Some of our directors and all of our officers, and some of the experts named in this prospectus, reside outside of Canada and all or a substantial portion of their assets, and all of our assets, are located outside of Canada. As a result, although we have appointed Michael Velletta as our agent for service of process in Canada, it may not be possible for investors in Canada to bring an action in Canada against directors, officers or experts who are not resident in Canada. It may not be possible for an investor to enforce a judgment obtained in a Canadian court predicated upon the civil liability provisions of Canadian securities laws against our company or those persons.

7

The following table of contents has been designed to help you find important information contained in this prospectus. We encourage you to read the entire prospectus.

TABLE OF CONTENTS

8

[ALTERNATE PAGE FOR CANADIAN PROSPECTUS]

The following table of contents has been designed to help you find important information contained in this prospectus. We encourage you to read the entire prospectus.

TABLE OF CONTENTS

9

[ALTERNATE PAGE FOR CANADIAN PROSPECTUS]

| FINANCIAL STATEMENTS | 96 |

10

EXCHANGE RATE INFORMATION

Unless otherwise indicated, all reference to “dollars”, “$”, “USD” or “US$” are to United States dollars and all reference to “CDN$” are to Canadian dollars.

We measure and report our financial results in United States dollars. The following table sets forth, for the periods indicated, the high, low, average and period-end noon buying rates of United States dollars published by the Bank of Canada. Although obtained from sources believed to be reliable, the data is only for informational purposes, and the Bank of Canada does not guarantee that the data is accurate or complete. No representation is made that the United States dollar amounts have been, could have been or could be converted into Canadian dollars at the noon buying rates on such dates or any other dates.

| Noon Buying Rate (CDN$) | ||||

| Year Ended December 31 | Period Ended | Average | High | Low |

| 2006 | $1.17 | $1.13 | $1.17 | $1.10 |

| 2007 | $0.99 | $1.07 | $1.19 | $0.92 |

| 2008 | $1.22 | $1.07 | $1.30 | $0.97 |

| 2009 | $1.05 | $1.14 | $1.30 | $1.03 |

| 2010 | $0.99 | $1.03 | $1.08 | $0.99 |

On January 28, 2011, the noon buying rate of the Bank of Canada was $1.00 = CDN$1.00.

Unless otherwise indicated, foreign currencies are converted to United States dollars using the following exchange rates on January 28, 2011:

Foreign Exchange Rates on January 28, 2011

| Canadian dollars | CDN$/$ | 1.0010 |

| Swiss francs | CHF/$ | 1.0616 |

11

PROSPECTUS SUMMARY

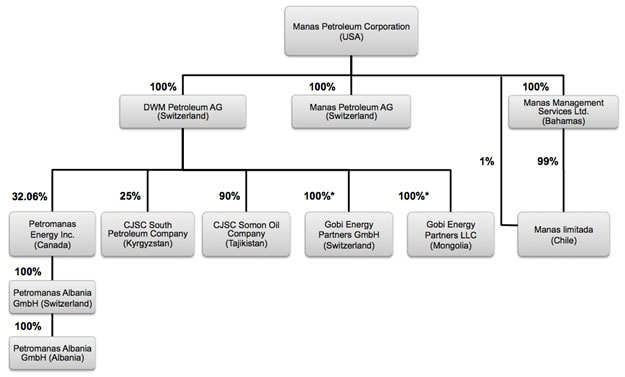

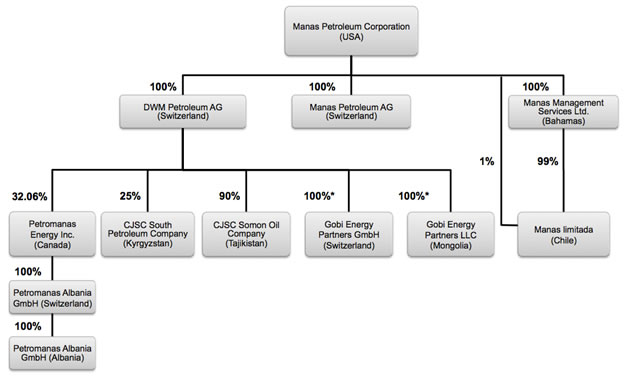

As used in this prospectus, the terms “we”, “us”, and “our” refer to Manas Petroleum Corporation, its wholly-owned subsidiaries DWM Petroleum AG, a Swiss company, Manas Petroleum A.G., a Swiss company, Manas Energia Chile Limitada, a Chilean company, Manas Petroleum of Chile Corporation, a Canadian company, and Manas Management Services Ltd., a Bahamian company, and its partially owned subsidiaries CJSC Somon Oil Company, a Tajikistan company, Gobi Energy Partners GmbH, a Swiss company, and Gobi Energy Partners LLC, a Mongolian company, and its 25% ownership interest in CJSC South Petroleum Company, a Kyrgyz company and its 32.06% ownership interest in Petromanas Energy Inc., a British Columbia company listed on the TSX Venture Exchange in Canada (TSXV: PMI), as the context may require.

The following is a summary of the principal features of this distribution and should be read together with the more detailed information and financial data and statements contained elsewhere in this prospectus.

The Offering

We have engaged Raymond James Ltd. and its U.S. affiliate, Raymond James (USA) Ltd., to conduct this offering on a “reasonable commercial efforts all or nothing” basis as to the minimum number of shares to be sold and a “reasonable commercial efforts” basis as to the balance. The offering is being made without a firm commitment by the placement agents, which have no obligation or commitment to purchase any of the shares of our common stock. See “Plan of Distribution”.

| Minimum shares offered |

<> shares of our common stock |

|

| |

| Maximum shares offered |

<> shares of our common stock |

|

| |

| Shares to be outstanding, if minimum offering is sold(1) |

<> shares of our common stock |

|

| |

| Shares to be outstanding, if maximum offering is sold(1),(2) |

<> shares of our common stock |

|

| |

| Offering price per share |

$<> |

|

| |

| Expected net proceeds, if minimum offering is sold |

$18,600,000 |

|

| |

| Expected net proceeds, if maximum offering is sold(3) |

$27,900,000 |

|

| |

| Use of proceeds |

Proceeds will be used primarily for seismic, drilling, geological and geophysical works, production sharing contract costs and working capital. See “Use of Proceeds”. |

|

| |

| Closing of offering |

The offering contemplated by this prospectus will terminate upon the earlier of (i) a date mutually acceptable to us and our placement agents after the minimum offering is sold or (ii) <>. We will not close the offering if we do not receive subscriptions to purchase at least the minimum offering amount. See “Plan of Distribution”. |

|

| |

| Subscription proceeds |

Subscription proceeds will be held in a separate bank account of the placement agents in trust until the earlier of our receipt of commitments to purchase <> shares of our common stock or <>. |

12

|

Lock-up agreements |

We anticipate that our officers and directors will enter into lock-up agreements with our company and Raymond James Ltd. which provide that such officers and directors will not, directly or indirectly, sell any shares of our common stock held by them for a period beginning on <>, 2011 and ending 120 days from the closing of this offering. |

| (1) |

The calculation of the number of shares of our common stock that will be outstanding after completion of this offering is based on 125,911,710 shares issued and outstanding as of January 31, 2011 and excludes the shares issuable upon exercise of the over-allotment option or any other outstanding warrants or options as of January 31, 2011. |

| (2) |

If the over-allotment option is exercised in full, the number of shares of our common stock that will be outstanding after completion of the maximum offering will be <>, excluding the shares issuable upon exercise of any other outstanding warrants or options as of January 31, 2011. |

| (3) |

If the over-allotment option is exercised in full, the expected net proceeds to our company after completion of the maximum offering will be $32,085,000. |

Our Business

We are in the business of exploring for oil and gas, primarily in Central and East Asia and the Balkans. In particular, we focus on the exploration of large under-thrust light oil prospects in areas where, though there has often been shallow production, their deeper potential has yet to be evaluated. Although we are currently focused primarily on projects located in certain geographic regions, we remain open to attractive opportunities in other areas.

We carry out our operations both directly and through participation in ventures with other oil and gas companies. We have or were involved in projects in Mongolia, Tajikistan and Chile. In addition, we own shares of Petromanas Energy Inc., which is involved in oil and gas activities in Albania, and shares of CJSC South Petroleum Company, which is involved in a project in the Kyrgyz Republic.

To date, we do not have any known reserves on any of our properties, we have no operating income and, as a result, depend upon funding from various sources to continue operations and to implement our growth strategy. Because of our lack of operating revenues, operating losses since inception and need to raise additional funds, our independent registered public accounting firm included an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern in their report on our financial statements for the year ended December 31, 2009.

See “Description of Business”.

Corporate Information

Our principal executive offices are located at Bahnhofstrasse 9, 6341 Baar, Switzerland, and our telephone number is +41 (44) 718 1030. Our website is www.manaspetroleum.com. Information contained on, or that can be accessed through our website is not incorporated by reference into this prospectus, and such information should not be considered to be part of this prospectus.

The following chart reflects our organizational structure as of the date of this prospectus:

13

* We are in the process of restructuring our organization: Currently, DWM Petroleum AG holds record title to 100% of Gobi Energy Partners LLC, of which 26% is held in trust for others (8% is held in trust for each of two investor groups and 10% is held in trust for Shunkhlai Group LLC, a Mongolian oil and gas company). After restructuring, DWM Petroleum AG is to hold 74% of Gobi Energy Partners GmbH and Gobi Energy Partners GmbH is to hold 100% of Gobi Energy Partners LLC.

Directors and Executive Officers

Our directors and executive officers are as follows:

| Name | Position Held with the Company |

| Heinz J. Scholz | Executive Director and Chairman of the Board of Directors |

| Michael J. Velletta | Executive Director |

| Dr. Richard Schenz | Director |

| Dr. Werner Ladwein | Director |

| Peter-Mark Vogel | President and Chief Executive Officer |

| Ari Muljana | Chief Financial Officer and Treasurer |

See “Directors and Executive Officers”.

Share Capital

We are authorized to issue 300,000,000 shares of common stock with a par value of $0.001 per share and no shares of preferred stock. Each share of common stock entitles the holder to one vote on all matters submitted to a vote of the stockholders including the election of directors. See “Description of Securities”.

14

Summary of Financial Data

The following information represents selected financial information for our company for the years ended December 31, 2009 and 2008 and selected financial information for our company for the nine month period ended September 30, 2010. The summarized financial information presented below is derived from and should be read in conjunction with our audited and unaudited financial statements, as applicable, including the notes to those financial statements which are included elsewhere in this prospectus along with the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” beginning on page 58 of this prospectus.

See “Financial Statements.”

Statements of Operations Data |

Nine Month Period Ended September 30, 2010 |

Nine Month Period Ended September 30, 2009 |

From May 25, 2004 (Inception) to September 30, 2010 |

| Total Revenues | Nil | Nil | $1,375,728 |

| Total Operating Expenses | $(6,099,437) | $(7,426,013) | $(55,198,205) |

| Net Income (Loss) | $65,530,401 | $(18,792,985) | $(269,476) |

| Basic Earnings/(Loss) Per Share | $0.54 | $(0.16) | $(0.00) |

Statements of Operations Data |

Year Ended December 31, 2009 |

Year Ended December 31, 2008 |

| Total Revenues | Nil | $635,318 |

| Total Operating Expenses | $(9,501,901) | $(20,956,481) |

| Net Loss | $(21,618,015) | $(30,296,106) |

| Basic Earnings/(Loss) Per Share | $(0.18) | $(0.26) |

| Balance Sheet Data | At September 30, 2010 | At December 31, 2009 | At December 31, 2008 |

| Cash and Cash Equivalents | $3,318,465 |

$804,663 |

$225,993 |

| Working Capital | $3,558,073 | $(7,528,797) | $5,502,560 |

| Total Assets | $64,366,898 | $2,753,648 | $9,163,608 |

| Total Liabilities | $458,047 | $9,782,835 | $9,349,419 |

| Total Stockholders’ Equity (Deficit) | $58,392,304 |

$(7,029,187) |

$(185,811) |

| Retained Earnings (Accumulated Deficit) | $8,798,794 |

$(56,731,607) |

$(44,200,563) |

Risk Factors

An investment in our common stock involves a number of very significant risks. You should carefully consider the information set out under “Risk Factors” and other information in this prospectus before purchasing shares of our common stock. The risks we face include the following:

-

We engage in a significant portion of our operations through ventures (farm-outs and other non-operating interests) that we do not control. We may not be able to materially affect the success of those ventures;

-

There may be ongoing doubt about our ability to continue as a going concern. If we cannot continue to operate our business, you could lose your entire investment in our company;

15

-

Our lack of diversification increases the risk of an investment in us, and our financial condition and results of operations may deteriorate if we fail to diversify;

-

We may not effectively manage the growth necessary to execute our business plan;

-

We may be forced to liquidate one or more subsidiaries due to regulatory requirements which could have a material adverse effect on our business and operations;

-

We are subject to various risks of foreign operations;

-

Substantially all of our assets are located outside the United States and Canada and all but one of our directors and all of our officers are nationals and/or residents of countries other than the United States and Canada, with the result that it may be difficult for investors to enforce within the United States or Canada any judgments obtained against us or our officers or directors.

-

Our articles of incorporation exculpate our officers and directors from any liability to our company or our stockholders;

-

The loss of certain key management employees could have a material adverse effect on our business;

-

There are potential conflicts of interest between our company and some of our directors and officers;

-

We have not discovered any oil and gas reserves, and we cannot assure you that we ever will;

-

Even if we discover and then develop oil and gas reserves, we may have difficulty distributing our production;

-

The oil and natural gas industry is highly competitive and there is no assurance that we will be successful in acquiring leases, equipment and personnel;

-

Prices and markets for oil are unpredictable and tend to fluctuate significantly, which could reduce profitability, growth and the value of our business if we ever begin exploitation of reserves;

-

Our business will suffer if we cannot obtain or maintain necessary licenses or if there is a defect in the chain of title;

-

Amendments to current laws and regulations governing our proposed operations could have a material adverse impact on our proposed business;

-

Penalties we may incur could impair our business;

-

Our inability to obtain necessary facilities could hamper our operations;

-

Emerging markets are subject to greater risks than more developed markets, including significant legal, economic and political risks;

-

Strategic relationships upon which we may rely are subject to change, which may diminish our ability to conduct our operations;

-

Environmental risks may adversely affect our business;

-

Losses and liabilities arising from uninsured or under-insured hazards could have a material adverse effect on our business;

-

Fluctuations in currency exchange rates could have a material adverse impact on our operations;

16

-

The price of our common stock may become volatile, which could lead to losses by investors and costly securities litigation;

-

If we obtain additional financing through the sale of additional equity in our company, the issuance of additional shares of common stock will result in dilution to our existing stockholders;

-

Our directors and executive officers own approximately 31.3% of our outstanding common stock;

-

We do not expect to pay dividends in the foreseeable future;

-

Our stock is a penny stock. Trading of our stock may be restricted by the Securities and Exchange Commission’s penny stock regulations which may limit a stockholder’s ability to buy and sell our stock;

-

The Financial Industry Regulatory Authority sales practice requirements may also limit a stockholder’s ability to buy and sell our stock.

Please read this prospectus carefully. You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. You should not assume that the information set forth in the prospectus is accurate as of any date other than the date on the front of this prospectus.

RISK FACTORS

An investment in our common stock involves a number of very significant risks. You should carefully consider the following risks and uncertainties in addition to other information in this prospectus in evaluating our company and our business before purchasing shares of our common stock. Our business, operating results and financial condition could be seriously harmed as a result of the occurrence of any of the following risks. You could lose all or part of your investment due to any of these risks. You should invest in our common stock only if you can afford to lose your entire investment.

Risks Associated with Our Company

We engage in a significant portion of our operations through ventures (farm-outs and other non-operating interests) that we do not control. We may not be able to materially affect the cost or success of those ventures.

We participate in an oil and gas exploration project in Albania through our ownership interest in Petromanas Energy Inc. In relation to this ownership interest, we are deemed to be a control person as we own approximately 32% of Petromanas Energy Inc’s issued and outstanding common shares; shareholders that own 20% or more of an issuer’s shares are deemed to be a “control person” by regulatory authorities absent evidence to the contrary. We also have minority representation on its board of directors, but we do not control its activities and we believe we do not control Petromanas Energy Inc. We cannot provide any assurance that Petromanas Energy Inc. will make decisions about its business that are reasonable, profitable or in our best interest.

We participate in an oil and gas exploration project in the Kyrgyz Republic through our 25% interest in CJSC South Petroleum Company. Santos Limited, an Australian public company, owns 70% of CJSC South Petroleum Company through its wholly-owned subsidiary, Santos International Holdings Pty Ltd., and Santos International Holdings Pty Ltd. operates the project pursuant to a farm-in agreement. As the operator, Santos International Holdings Pty Ltd. makes most of the decisions about the exploration and development of this project. We cannot assure you that Santos International Holdings Pty Ltd. or its subsidiaries, affiliates, agents or management will make decisions concerning this project that are reasonable, profitable or in our best interest. In addition, if Santos International Holdings Pty Ltd. spends more than $42 million on this project, we may be responsible for 30% of any expenditure in excess of that amount. As a result, we cannot control our potential costs.

There may be ongoing doubt about our ability to continue as a going concern. If we cannot continue to operate our business, you could lose your entire investment in our company.

As described in the audit report of our independent registered public accounting firm for the year ended December 31, 2009 and in note 2 to our consolidated financial statements for the years ended December 31, 2009 and 2008, included in this prospectus, the circumstances raised substantial doubt about our ability to continue as a going concern. Our consolidated financial statements do not reflect any adjustments that might result if we are unable to continue our business. As of the date of this prospectus, management believes that there is no substantial doubt about our ability to continue as a going concern.

17

We anticipate that we will continue to incur substantial operating losses unless and until we are able to sell or farm out additional resource properties or identify and develop oil and/or natural gas reserves in commercially exploitable quantities on one or more of our properties and begin production. Based on our business plan for the next 12 months ending December 31, 2011, we anticipate that we will need approximately $8,280,000 to fund our operations (including our monthly operating expenses of approximately $265,000 for basic operational activities and approximately $5,100,000 for our exploration activities). We believe that we have sufficient cash on hand to fund our basic operational activities until December 2011, but we will require further funds in order to conduct our planned exploration activities and/or continue our operations beyond December 2011. As we cannot assure a lender that we will be able to discover oil or gas in commercially feasible quantities or that we would be able to successfully develop any such discovery, we will probably find it difficult to raise debt financing from traditional sources. We have historically depended upon the sale of debt and equity securities to provide the cash needed to fund our operations, but we cannot assure you that we will be able to continue to do so. In light of our operating history, we may not be able to obtain additional equity or debt financing on acceptable terms if and when we need it. Even if financing is available, it may not be available on terms that are favorable to us or in sufficient amounts to satisfy our requirements. If we require, but are unable to obtain, additional financing in the future, we may be unable to implement our business plan and our growth strategies, respond to changing business or economic conditions, withstand adverse operating results, and compete effectively. More importantly, if we are unable to raise further financing when required, our operations may have to be scaled back or even ceased altogether and our business would be negatively affected.

Our lack of diversification increases the risk of an investment in us, and our financial condition and results of operations may deteriorate if we fail to diversify.

We have or were involved in projects in Mongolia, Tajikistan and Chile. In addition, we own shares of Petromanas Energy Inc., which is involved in oil and gas activities in Albania, and shares of CJSC South Petroleum Company, which is involved in a project in the Kyrgyz Republic. We lack diversification, in terms of both the nature and geographic scope of our business. As a result, we will likely be impacted more acutely by factors affecting our industry or the regions in which we operate than we would if our business were more diversified.

We may not effectively manage the growth necessary to execute our business plan.

Our business plan anticipates an increase in the number of our strategic partners, equipment suppliers, manufacturers, dealers, distributors and customers. This growth will place significant strain on our current personnel, systems and resources. We expect that we will be required to hire qualified employees to help us manage our growth effectively. We believe that we will also be required to improve our management, technical, information and accounting systems, controls and procedures. We may not be able to maintain the quality of our operations, control our costs, continue complying with all applicable regulations and expand our internal management, technical information and accounting systems to support our desired growth. If we fail to manage our anticipated growth effectively, our business could be adversely affected.

We may be forced to liquidate one or more subsidiaries due to regulatory requirements which could have a material adverse effect on our business and operations.

Substantially all of our licenses and assets are owned by our subsidiaries. These subsidiaries are formed in various countries pursuant to local law and regulation. In some cases, local regulation could result in the forced liquidation of one or more of these subsidiary companies. If any of our subsidiaries is liquidated before we can transfer its assets, the licenses and assets held by it could revert to the respective government. If this happens, our business could be harmed.

18

We are subject to various risks of foreign operations.

None of our projects are located in the United States or Canada. We have or were involved in projects in Mongolia, Tajikistan and Chile. In addition, we own shares of Petromanas Energy Inc., which is involved in oil and gas activities in Albania, and shares of CJSC South Petroleum Company, which is involved in a project in the Kyrgyz Republic. As such, our business is subject to governmental, political, economic, and other uncertainties in Mongolia, Tajikistan, the Kyrgyz Republic, Chile and Albania including, by way of example and not in limitation, expropriation of property without fair compensation, changes in energy policies or the personnel administering them, delays caused by the extensive bureaucracy, nationalization, currency fluctuations and devaluations, exchange controls and royalty increases, changes in oil or natural gas pricing policy, renegotiation or nullification of existing concessions and contracts, changes in taxation policies, economic sanctions, restrictions on the repatriation of currency and the imposition of specific drilling obligations and the other risks arising out of foreign governmental sovereignty over the areas in which our operations (or those of our venture partners) are conducted, as well as risks of loss due to civil strife, acts of war, guerrilla activities, insurrections, the actions of national labour unions, terrorism and abduction.

Our operations (and those of our venture partners) may also be adversely affected by laws and policies of the United States affecting foreign trade, taxation and investment. In the event of a dispute arising in connection with our operations (and those of our venture partners) in foreign countries, we may be subject to the exclusive jurisdiction of foreign courts or may not be successful in subjecting foreign persons to the jurisdictions of the courts of the United States or enforcing judgments in such other jurisdictions. We may also be hindered or prevented from enforcing our rights with respect to a governmental instrumentality because of the doctrine of sovereign immunity. Accordingly, our exploration, development and production activities (or those of our venture partners) could be substantially affected by factors beyond our control, any of which could have a material adverse effect on our business or our company.

Substantially all of our assets are located outside the United States and Canada and all but one of our directors and all of our officers are nationals and/or residents of countries other than the United States and Canada, with the result that it may be difficult for investors to enforce within the United States or Canada any judgments obtained against us or our officers or directors.

Substantially all of our assets are located outside the United States and Canada. In addition, all but one of our directors and all of our officers are nationals and/or residents of countries other than the United States and Canada, and all or a substantial portion of such persons’ assets are located outside of North America. As a result, it may be difficult for investors to enforce within the United States or Canada any judgments obtained against us or our officers or directors, including judgments predicated upon the civil liability provisions of the securities laws of the United States and Canada. Consequently, you may be effectively prevented from pursuing remedies against us or them under applicable securities laws.

Our articles of incorporation exculpate our officers and directors from any liability to our company or our stockholders.

Our articles of incorporation contain a provision limiting the liability of our officers and directors for their acts or failures to act, except for acts involving intentional misconduct, fraud or a knowing violation of law. This limitation on liability may reduce the likelihood of derivative litigation against our officers and directors and may discourage or deter our stockholders from suing our officers and directors based upon breaches of their duties to our company.

The loss of certain key management employees could have a material adverse effect on our business.

The nature of our business, to perform technical exploration and development depends, in large part, on our ability to attract and maintain qualified key personnel. Competition for such personnel is intense, and we cannot assure you that we will be able to attract and retain them. Our development now and in the future will depend on the efforts of key management figures, such as Heinz Scholz, the Chairman of our board of directors, Peter-Mark Vogel, President and Chief Executive Officer, and Michael J. Velletta, Executive Director. The loss of any of these key people could have a material adverse effect on our business. We do not currently maintain key-man life insurance on any of our key employees.

19

There are potential conflicts of interest between our company and some of our directors and officers.

Some of our directors and officers are also directors and officers of other companies. Conflicts of interest could arise as a result of this. In addition, one of our officers and one of our directors have informed our company that they propose to pursue non-petroleum resource opportunities in Mongolia. As of the date of this prospectus and to the knowledge of our directors and officers, there are no existing conflicts of interest between our company and any of these individuals but situations may arise where directors and/or officers of our company may be in competition with our company. Any conflicts of interest will be subject to and governed by the law applicable to directors’ and officers’ conflicts of interest. In the event that such a conflict of interest arises at a meeting of our directors, a director who has such a conflict is required to abstain from any discussion and vote for or against the approval of such participation or such terms. As a result, our board of directors will be deprived of that person’s experience and expertise, which could adversely affect the outcome.

Risks Associated with Our Business

We have not discovered any oil and gas reserves, and we cannot assure you that that we ever will.

We are in the business of exploring for oil and natural gas and the development and exploitation of any oil and gas that we might find in commercially exploitable quantities. Oil and gas exploration involves a high degree of risk that the exploration will not yield positive results. These risks are more acute in the early stages of exploration. We have not discovered any reserves, and we cannot guarantee that we ever will. Even if we succeed in discovering oil or gas reserves, these reserves may not be in commercially viable quantities or locations. Until we discover such reserves, we will not be able to generate any revenues from their exploitation and development. If we are unable to generate revenues from the development and exploitation of oil and gas reserves, we will be forced to change our business or cease operations.

Even if we discover and then develop oil and gas reserves, we may have difficulty distributing our production.

If we are able to produce oil and gas, we will have to make arrangements for storage and distribution of that oil and gas. We would have to rely on local infrastructure and the availability of transportation for storage and shipment of oil and gas products, but any readily available infrastructure and storage and transportation facilities may be insufficient or not available at commercially acceptable terms. This could be particularly problematic to the extent that operations are conducted in remote areas that are difficult to access, such as areas that are distant from shipping or pipeline facilities. Furthermore, weather conditions or natural disasters, actions by companies doing business in one or more of the areas in which we will operate, or labor disputes may impair the distribution of oil and gas. These factors may affect the ability to explore and develop properties and to store and transport oil and gas and may increase our expenses to a degree that has a material adverse effect on operations.

The oil and natural gas industry is highly competitive and there is no assurance that we will be successful in acquiring leases, equipment and personnel.

The oil and natural gas industry is intensely competitive. Although we do not compete with other oil and gas companies for the sale of any oil and gas that we may produce, as there is sufficient demand in the world market for these products, we compete with numerous individuals and companies for desirable oil and natural gas leases, suitable properties for drilling operations and necessary drilling equipment, qualified personnel and access to capital. Many of these individuals and companies with whom we compete have substantially greater technical, financial and operational resources and staff than we have. If we cannot compete for personnel, equipment and oil and gas properties, our business could be harmed.

Prices and markets for oil are unpredictable and tend to fluctuate significantly, which could reduce profitability, growth and the value of our business if we ever begin exploitation of reserves.

Our revenues and earnings, if any, will be highly sensitive to the price of oil and gas. Prices for oil and gas are subject to large fluctuations in response to relatively minor changes in the supply of and demand for oil and gas, market uncertainty and a variety of additional factors beyond our control. These factors include, without limitation, governmental fixing, pegging, controls or any combination of these and other factors, changes in domestic, international, political, social and economic environments, worldwide economic uncertainty, the availability and cost of funds for exploration and production, the actions of the Organization of Petroleum Exporting Countries, governmental regulations, political stability in the Middle East and elsewhere, war, or the threat of war, in oil producing regions, the foreign supply of oil, the price of foreign imports and the availability of alternate fuel sources. Significant changes in long-term price outlooks for crude oil or natural gas could, if we ever discover and exploit any reserves of oil or natural gas, have a material adverse effect on revenues as well as the value of our licenses or other assets.

20

Our business will suffer if we cannot obtain or maintain necessary licenses or if there is a defect in the chain of title.

Our operations require that we obtain and maintain licenses and permits from various governmental authorities. Our ability to obtain, maintain or renew such licenses and permits on acceptable terms is subject to extensive regulation and to changes, from time-to-time, in those regulations. Also, the decision to grant or renew a license or permit is frequently subject to the discretion of the applicable government. If we cannot obtain, maintain, extend or renew these licenses or permits our business could be harmed.

Also, although title reviews have been conducted on our existing properties, such reviews do not guarantee or certify an unforeseen defect in the chain of title will not arise to defeat our claim which could result from the loss of title and a reduction of the revenue received, if any.

Amendments to current laws and regulations governing our proposed operations could have a material adverse impact on our proposed business.

We are subject to substantial regulation relating to the exploration for, and the development, upgrading, marketing, pricing, taxation, and transportation of, oil and gas. Amendments to current laws and regulations governing operations and activities of oil and gas exploration and extraction operations could have a material adverse impact on our proposed business. In addition, we cannot assure you that income tax laws, royalty regulations and government incentive programs related to the oil and gas industry generally or to us specifically will not be changed in a manner which may adversely affect us and cause delays, inability to complete or abandonment of projects.

Penalties we may incur could impair our business.

Failure to comply with government regulations could subject us to civil and criminal penalties, could require us to forfeit property rights or licenses, and may affect the value of our assets. We may also be required to take corrective actions, such as installing additional equipment, which could require substantial capital expenditures. We could also be required to indemnify our employees in connection with any expenses or liabilities that they may incur individually in connection with regulatory action against them. As a result, our future business prospects could deteriorate due to regulatory constraints, and our profitability could be impaired by our obligation to provide such indemnification to our employees.

Our inability to obtain necessary facilities could hamper our operations.

Oil and gas exploration and development activities depend on the availability of equipment, transportation, power and technical support in the particular areas where these activities will be conducted, and our access to these facilities may be limited. To the extent that we conduct our activities in remote areas or in under-developed markets, needed facilities may not be readily available, which could increase our expenses. Demand for such limited equipment and other facilities or access restrictions may affect the availability of such equipment and may delay exploration and development activities. The quality and reliability of necessary facilities may also be unpredictable and we may be required to make efforts to standardize our facilities, which may entail unanticipated costs and delays. Shortages or the unavailability of necessary equipment or other facilities will impair our activities, either by delaying our activities, increasing our costs or otherwise.

Emerging markets are subject to greater risks than more developed markets, including significant legal, economic and political risks.

In recent years Mongolia, Tajikistan, the Kyrgyz Republic, Chile and Albania have all undergone substantial political, economic and social change. As in any emerging market, Mongolia, Tajikistan, the Kyrgyz Republic, Chile and Albania do not possess as sophisticated and efficient business, regulatory, power and transportation infrastructures as generally exist in more developed market economies. Investors in emerging markets should be aware that these markets are subject to greater risks than more developed markets, including in some cases significant legal, economic and political risks. Investors should also note that emerging economies are subject to rapid change and that the information set out herein may become outdated relatively quickly. We cannot predict what economic, political, legal or other changes may occur in these or other emerging markets, but such changes could adversely affect our ability to carry out exploration and development projects.

21

Particularly, the legal systems of Mongolia, Tajikistan, the Kyrgyz Republic, Chile and Albania are less developed than those of more established jurisdictions, which may result in risk such as: the lack of effective legal redress in the courts, whether in respect of a breach of law or regulation, or, in an ownership dispute, a higher degree of discretion on the part of governmental authorities, the delays caused by the extensive bureaucracy, the lack of judicial or administrative guidance on interpreting applicable laws and regulations, inconsistencies or conflicts between and within various laws, regulations, decrees, orders and resolutions, or relative inexperience of the judiciary and courts in such matters.

Strategic relationships upon which we may rely are subject to change, which may diminish our ability to conduct our operations.

Our ability to discover reserves, to participate in drilling opportunities and to identify and enter into commercial arrangements depends on developing and maintaining close working relationships with industry participants and government officials and on our ability to select and evaluate suitable properties and to consummate transactions in a highly competitive environment. We may not be able to establish these strategic relationships or, if established, we may not be able to maintain them. In addition, the dynamics of our relationships with strategic partners may require us to incur expenses or undertake activities we would not otherwise be inclined to undertake in order to fulfill our obligations to these partners or maintain our relationships. If our strategic relationships are not established or maintained, our business prospects may be limited, which could diminish our ability to conduct our operations.

Environmental risks may adversely affect our business.

All phases of the oil and gas business present environmental risks and hazards and are subject to environmental regulation pursuant to a variety of laws and regulations. Environmental legislation provides for, among other things, restrictions and prohibitions on spills, releases or emissions of various substances produced in association with oil and gas operations. The legislation also requires that wells and facility sites be operated, maintained, abandoned and reclaimed to the satisfaction of applicable regulatory authorities. Compliance with such legislation can require significant expenditures and a breach may result in the imposition of fines and penalties, some of which may be material. The application of environmental laws to our business may cause us to curtail our production or increase the costs of any production, development or exploration activities.

Losses and liabilities arising from uninsured or under-insured hazards could have a material adverse effect on our business.

If we develop and exploit oil and gas reserves, those operations will be subject to the customary hazards of recovering, transporting and processing hydrocarbons, such as fires, explosions, gas leaks, migration of harmful substances, blowouts and oil spills. An accident or error arising from these hazards might result in the loss of equipment or life, as well as injury, property damage or other liability. We have not made a determination as to the amount and type of insurance that we will carry. We cannot assure you that we will obtain insurance on reasonable terms or that any insurance we may obtain will be sufficient to cover any such accident or error. Our operations could be interrupted by natural disasters or other events beyond our control. Losses and liabilities arising from uninsured or under-insured events could have a material adverse effect on our business, financial condition and results of operations.

Fluctuations in currency exchange rates could have a material adverse impact on our operations.

All of our current operations are located in foreign countries. Domestic oil and natural gas product sales are denominated in the currency of the nation where the product is produced, as are operating and capital costs incurred.

22

Fluctuations in the value of the U.S. dollar or the local currency may cause a negative impact on revenue and costs. These types of fluctuations could have a material adverse impact on our operations.

Risks Associated with Our Common Stock

The price of our common stock may become volatile, which could lead to losses by investors and costly securities litigation.

The trading price of our common stock is likely to be highly volatile and could fluctuate in response to factors such as:

-

actual or anticipated variations in our operating results;

-

announcements by us or our competitors of significant acquisitions, strategic partnerships, joint ventures, capital commitments, or other business developments, such as oil or gas discoveries;

-

adoption of new accounting standards affecting our industry;

-

additions or departures of key personnel;

-

sales of our common stock or other securities in the open market;

-

conditions or trends in our industry; and

-

other events or factors, many of which are beyond our control.

The stock market has experienced significant price and volume fluctuations, and the market prices of stock in exploration stage companies have been highly volatile. In the past, following periods of volatility in the market price of a company’s securities, securities class action litigation has often been initiated against the company. Litigation initiated against us, whether or not successful, could result in substantial costs and diversion of our management’s attention and resources, which could harm our business and financial condition.

If we obtain additional financing through the sale of additional equity in our company, the issuance of additional shares of common stock will result in dilution to our existing stockholders.

We are authorized to issue 300,000,000 shares of common stock and, as of January 31, 2011, 125,911,710 shares of our common stock were issued and outstanding. Our board of directors has the authority to issue additional shares of common stock up to the authorized capital without the consent of any of our stockholders. Our board of directors may choose to issue some or all of such shares to acquire one or more businesses or to provide additional financing in the future. The issuance of any such shares may result in a reduction of the book value or market price of the outstanding shares of our common stock. If we do issue any such additional shares, such issuance will cause a reduction in the proportionate ownership and voting power of all other stockholders. Further, any such issuance may result in a change of control of our company.

Our directors and executive officers own approximately 31.3% of our outstanding common stock.

In the aggregate, our directors and executive officers own approximately 31.3% of our outstanding common stock and they have the right to exercise options and warrants that would permit them to acquire, in the aggregate, up to an additional 3.2% of our common stock within the next 60 days. As a result, our directors and executive officers as a group may have a significant effect in delaying, deferring or preventing any potential change in control of our company, be able to strongly influence the actions of our board of directors even if they were to cease being our directors and control the outcome of actions brought to our stockholders for approval. Such a high level of ownership may adversely affect the voting and other rights of other stockholders.

23

We do not expect to pay dividends in the foreseeable future.

We do not intend to declare dividends for the foreseeable future, as we anticipate that we will reinvest any future earnings in the development and growth of our business. Therefore, investors will not receive any funds unless they sell their common stock, and stockholders may be unable to sell their shares on favorable terms or at all. We cannot assure you of a positive return on investment or that you will not lose the entire amount of your investment in our common stock.

Our stock is a penny stock. Trading of our stock may be restricted by the Securities and Exchange Commission’s penny stock regulations which may limit a stockholder’s ability to buy and sell our stock.

Our stock is a penny stock. The Securities and Exchange Commission has adopted Rule 15g-9 which generally defines “penny stock” to be any equity security that has a market price (as defined) of less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exceptions. Our securities are covered by the penny stock rules, which impose additional sales practice requirements on broker-dealers who sell to persons other than established customers and “accredited investors”. The term “accredited investor” refers generally to institutions with assets in excess of $5,000,000 or individuals with a net worth in excess of $1,000,000 or annual income exceeding $200,000 or $300,000 jointly with their spouse. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document in a form prepared by the Securities and Exchange Commission which provides information about penny stocks and the nature and level of risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction and monthly account statements showing the market value of each penny stock held in the customer’s account. The bid and offer quotations, and the broker-dealer and salesperson compensation information, must be given to the customer orally or in writing prior to effecting the transaction and must be given to the customer in writing before or with the customer’s confirmation. In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from these rules, the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written agreement to the transaction. These disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for the stock that is subject to these penny stock rules. Consequently, these penny stock rules may affect the ability of broker-dealers to trade our securities. We believe that the penny stock rules discourage investor interest in and limit the marketability of our common stock.

The Financial Industry Regulatory Authority sales practice requirements may also limit a stockholder’s ability to buy and sell our stock.

In addition to the “penny stock” rules described above, the Financial Industry Regulatory Authority, or “FINRA”, has adopted rules that require that in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative low-priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer’s financial status, tax status, investment objectives and other information. Under interpretations of these rules, FINRA believes that there is a high probability that speculative low-priced securities will not be suitable for at least some customers. The FINRA requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may limit your ability to buy and sell our stock and have an adverse effect on the market for shares of our common stock.

FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. Forward-looking statements are statements that relate to future events or future financial performance. In some cases, you can identify forward looking statements by the use of terminology such as “may”, “should”, “intend”, “expect”, “plan”, “anticipate”, “believe”, “estimate”, “project”, “predict”, “potential”, or “continue” or the negative of these terms or other comparable terminology. These statements speak only as of the date of this prospectus. Examples of forward-looking statements made in this prospectus include statements pertaining to, among other things:

-

the quantity of potential natural gas and crude oil resources;

-

potential natural gas and crude oil production levels;

24

-

capital expenditure programs;

-

projections of market prices and costs;

-

supply and demand for natural gas and crude oil;

-

our need for, and our ability to raise, capital; and

-

treatment under governmental regulatory regimes and tax laws.

These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including:

-

our ability to establish or find resources or reserves;

-

our need for, and our ability to raise, capital;

-

volatility in market prices for natural gas and crude oil;

-

liabilities inherent in natural gas and crude oil operations;

-

uncertainties associated with estimating natural gas and crude oil resources or reserves;

-

competition for, among other things, capital, resources, undeveloped lands and skilled personnel;

-

political instability or changes of laws in the countries in which we operate and risks of terrorist attacks;

-

incorrect assessments of the value of acquisitions;

-

geological, technical, drilling and processing problems;

-

other factors discussed under the section entitled “Risk Factors” beginning on page 17 of this prospectus.

These risks, as well as risks that we cannot currently anticipate, could cause our company’s or our industry’s actual results, levels of activity or performance to be materially different from any future results, levels of activity or performance expressed or implied by these forward looking statements.

Although we believe that the expectations reflected in the forward looking statements are reasonable, we cannot guarantee future results, levels of activity or performance. Except as required by applicable law, including the securities laws of the United States and Canada, we do not intend to update any of the forward looking statements to conform these statements to actual results.

USE OF PROCEEDS

The gross proceeds from this offering will be $20,000,000 if we sell the minimum number of shares of our common stock and $30,000,000 if we sell the maximum number of shares of our common stock that we are offering (assuming no exercise of the over-allotment option). After deducting the cash commission of 7% of the gross proceeds from this offering and the estimated offering expenses of $363,000 payable by us, we expect to receive net proceeds of approximately $18,237,000 from this offering if we sell the minimum number of shares of our common stock and $27,537,000 if we well the maximum number of shares of our common stock offered (assuming no exercise of the over-allotment option).

We intend to use the net proceeds of this offering as follows, and we have ordered the specific uses of proceeds in order of priority. We do not expect that our priorities for fund allocation would change if the amount we raise in this offering exceeds the size of the minimum offering but is less than the maximum offering. To the extent we raise an amount between the maximum offering and the minimum offering, we expect to utilize the net proceeds from this offering in order of such priority.

25

| Minimum Offering | Maximum Offering | |||

| Description of Use | Dollar Amount | Percentage of | Dollar Amount | Percentage of |

| Net Proceeds | Net Proceeds | |||

| Seismic | $5,550,000 | 30% | $5,550,000 | 20% |

| Drilling | $6,400,000 | 35% | $12,260,000 | 45% |

| Geological and Geophysical | $250,000 | 1% | $450,000 | 2% |

| Production Sharing Contract Costs (environmental, education, etc.) |

$1,242,600 |

6% |

$1,863,900 |

7% |

| Working Capital | $4,794,400 | 26% | $7,413,100 | 27% |

| Totals(1) | $18,237,000 | 100% | $27,537,000 | 100% |

| (1) |

Assuming no exercise of the over-allotment option. Any proceeds received from the exercise of the over-allotment option will be used to provide general working capital to fund ongoing operations. |

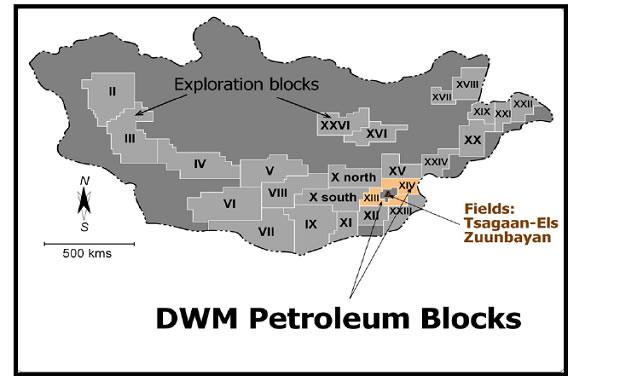

Seismic

We intend to use $5.55 million for seismic in Mongolia. In 2011, we anticipate that the seismic program will comprise the acquisition of 833 km of additional 2-D data at a cost of $3.35 million in the first phase. This includes 303 km on Block XIII and 530 km on Block XIV. A second phase of 2-D seismic acquisition in 2011 to 2012 would include a total of 232 km with 138 km on Block XIII and 94 km on Block XIV.

Drilling

Drilling costs primarily consist of mobilization, well heads, operational costs of the drilling crew and rental of drill rig as well as supporting material. We are currently in negotiations with three rig providers.

Maximum Offering

We intend to use $12.26 million for drilling in Mongolia, allowing us to complete one of the two production sharing contract commitments (three exploration wells). The drilling prospects have not been determined yet.

Minimum Offering

We intend to use $6.40 million for drilling in Mongolia, allowing us to complete one exploration well in one of our blocks in Mongolia. The drilling prospects have not been determined yet.

Geological and Geophysical

Some of the proceeds are intended to be used for geological and geophysical campaign including seismic processing and interpretation.

Maximum Offering

$450,000 is intended to be used in Mongolia for geological surveys, field work, data processing, mapping conducted through the office in Mongolia which is planned to be registered and for independent technical and environmental reports.

Minimum Offering

$250,000 is intended to be used in Mongolia for geological surveys, field work, data processing, mapping conducted through the office in Mongolia which is planned to be registered and for independent technical and environmental reports.

26

Production Sharing Contract Costs

Production sharing contract costs include environmental and educational costs.

Maximum Offering

We intend to use $1.24 million for costs related to environmental and education purposes.

Minimum Offering

We intend to use $1.86 million for costs related to environmental and education purposes.

Working Capital

Cash funds which are planned to be used within 3 months will be held on our fiduciary call bank account to which we have access within 24 hours. We plan to invest funds that we believe will be needed within the next three to 12 months in highly rated (AA or more) and liquid interest-bearing government securities, and we plan to invest funds that we believe will not be needed during the next 12 months in highly rated (AA or more) and liquid interest bearing government or corporate securities. In general, the investment policy that we propose to follow is intended to secure the amount of the funds. The supervision of the investment of these funds is planned to be provided by Peter-Mark Vogel, our President and Chief Executive Officer and Ari Muljana, our Chief Financial Officer.

Due to the nature of the oil and gas industry, budgets are regularly reviewed in light of the success of the expenditures and other opportunities which may become available to us. In addition, our ability to carry out operations will depend upon the decisions of other venture partners. Accordingly, while we intend to spend funds available as stated above, there may be circumstances where, for sound business reasons, a reallocation of funds may be necessary. Also, if we require funds in excess of the amounts raised in this offering, we may consider opportunities to partner with third parties at a project level. For our business objectives that we expect to accomplish using the net proceeds of this offering, see “Description of Business.”

Any proceeds received from exercise of the warrants issued to Raymond James Ltd. as compensation and exercise of the over-allotment option will be used to provide general working capital to fund ongoing operations.

Business Objectives and Milestones

Business Objectives

We are an exploration stage company. Our growth strategy is focused on petroleum exploration and development primarily in selected Central Asian countries of the former Soviet Union and in the Balkan region. In addition to our focus on these regions, we also take an opportunistic view on projects outside the above regions.

Our goal is to increase shareholder value through the successful acquisition and exploration of oil and gas resources. We intend to acquire or explore oil and gas resources either through our own operations or through participation in focused partnerships and joint ventures.

We have no operating income and, as a result, depend upon continued funding from other sources to continue operations and to implement our growth strategy.

Milestones

Significant milestones for measuring success of our operation and activities planned by our company in 2011 include: