Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - JONES LANG LASALLE INC | d8k.htm |

| EX-99.1 - PRESS RELEASE - JONES LANG LASALLE INC | dex991.htm |

Supplemental Information

Fourth Quarter

Earnings Call 2010

Exhibit 99.2 |

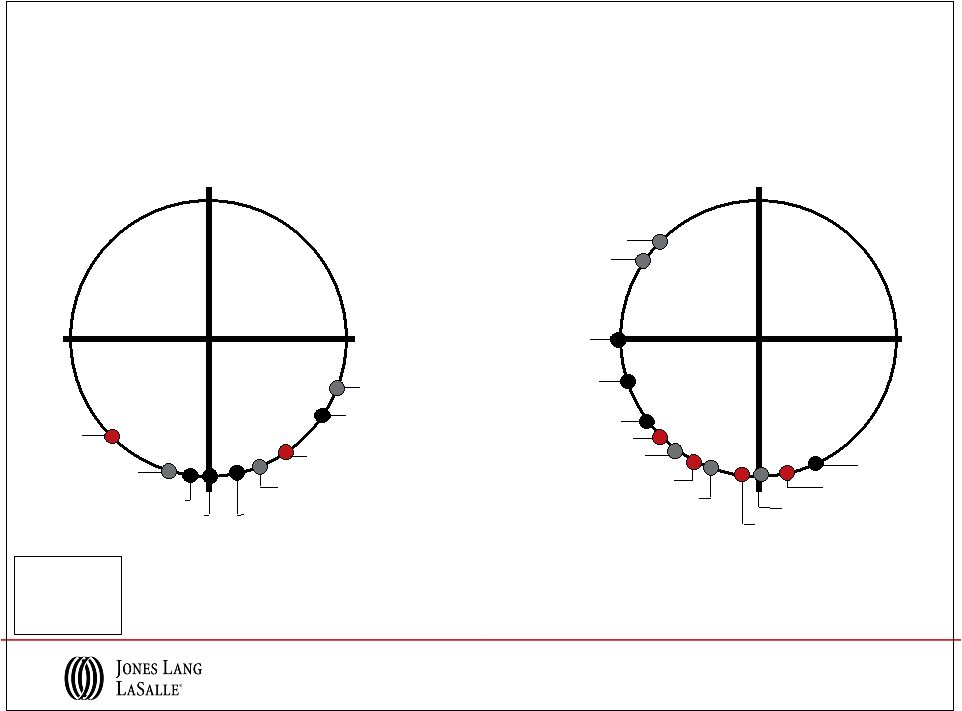

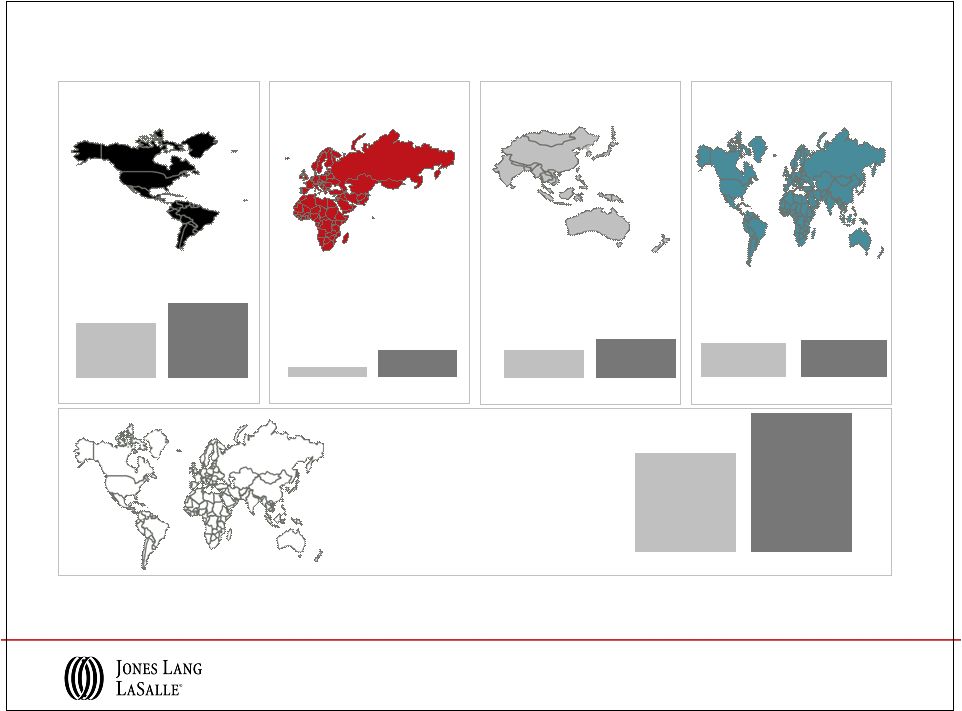

Market & Financial Overview |

3

Americas

EMEA

Asia Pacific

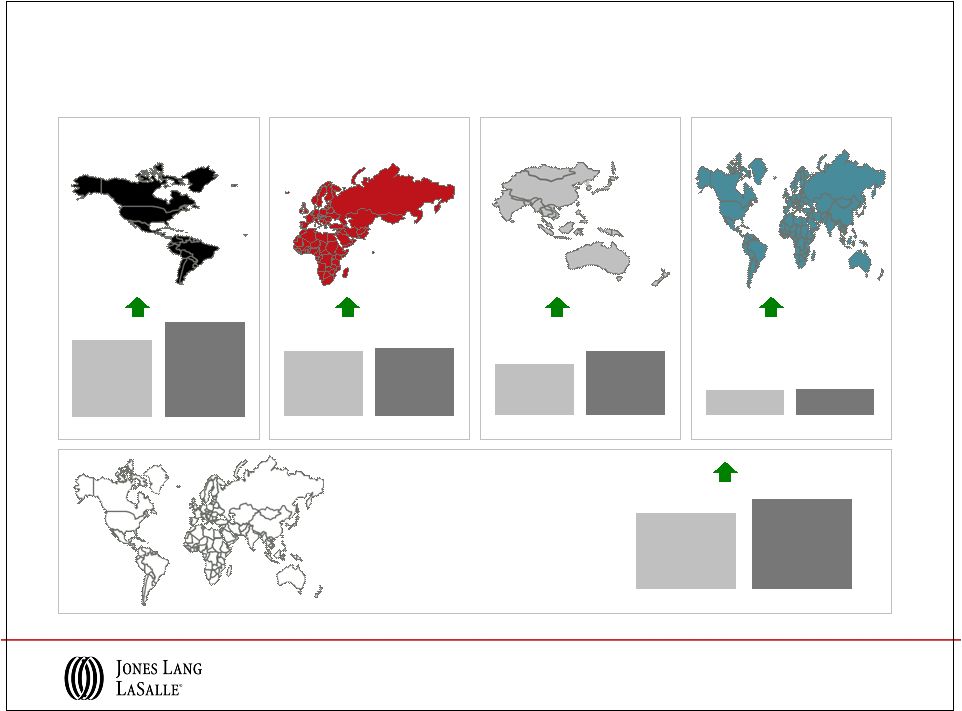

Capital Values

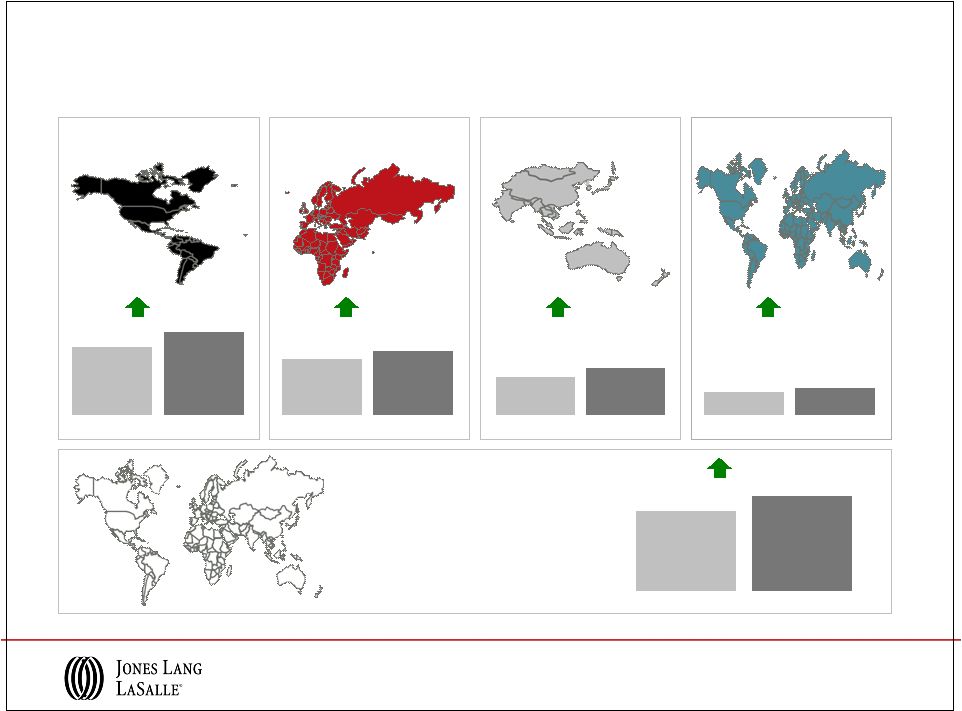

As of Q4 2010

The Jones Lang LaSalle Property Clocks

SM

Beijing, Hong Kong

Moscow

Capital Value

growth slowing

Capital Value

growth

accelerating

Capital Value

bottoming out

Capital Value

falling

New York,

Paris, San Francisco

Sao Paulo,

Seoul, Sydney

London

Shanghai

Detroit

Singapore

Brussels,

Chicago,

Milan

Mumbai, Tokyo

Amsterdam,

Toronto

Dallas

Q4 2009

Washington DC

Berlin, Stockholm

Capital Value

growth slowing

Capital Value

growth

accelerating

Capital Value

bottoming out

Capital Value

falling

Hong Kong,

London,

Sao Paulo

Washington DC

Shanghai

Dallas,

Mumbai, Seoul

Sydney, Tokyo

Singapore

Brussels

Moscow

Berlin, Paris, Stockholm

Amsterdam,

Milan

New York

San Francisco

Chicago, Toronto

Detroit

Beijing

Q4 2010 |

4

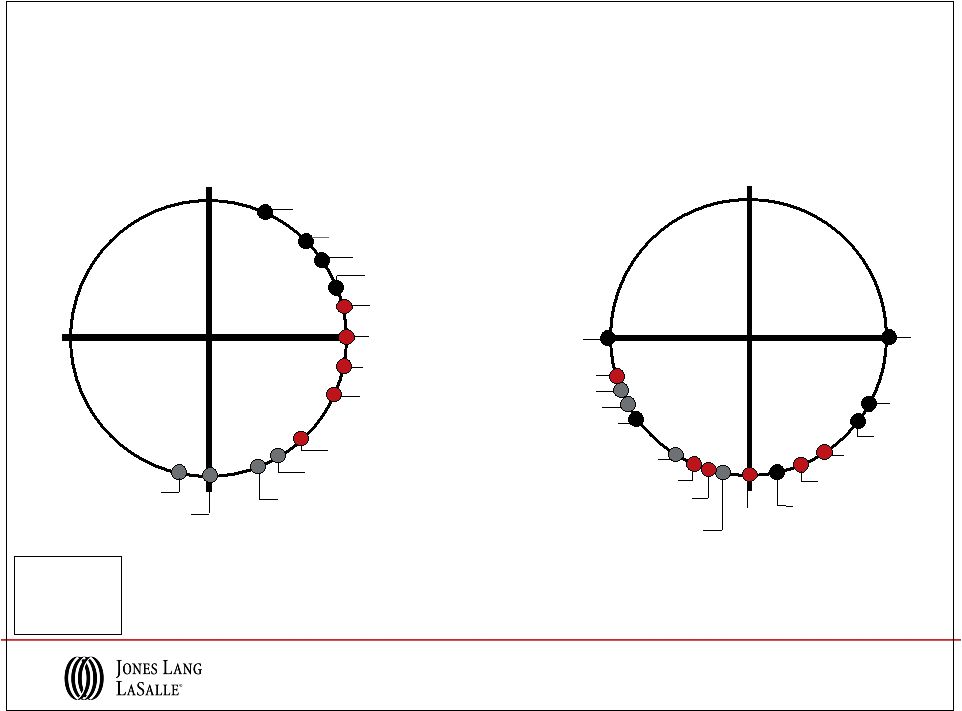

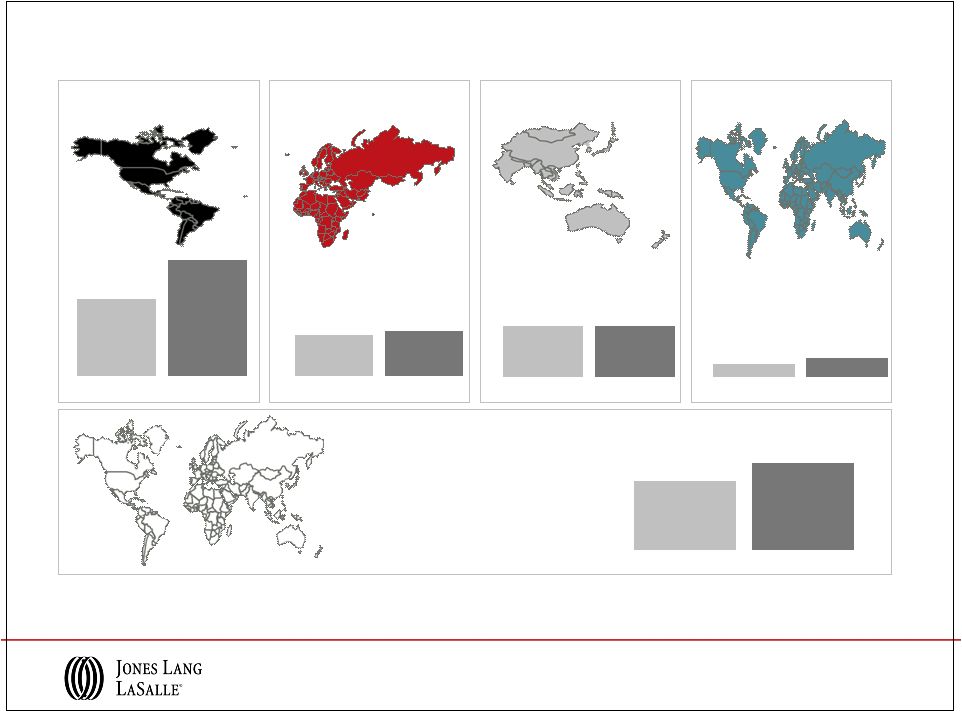

Leasing Market Fundamentals

Q4 2010

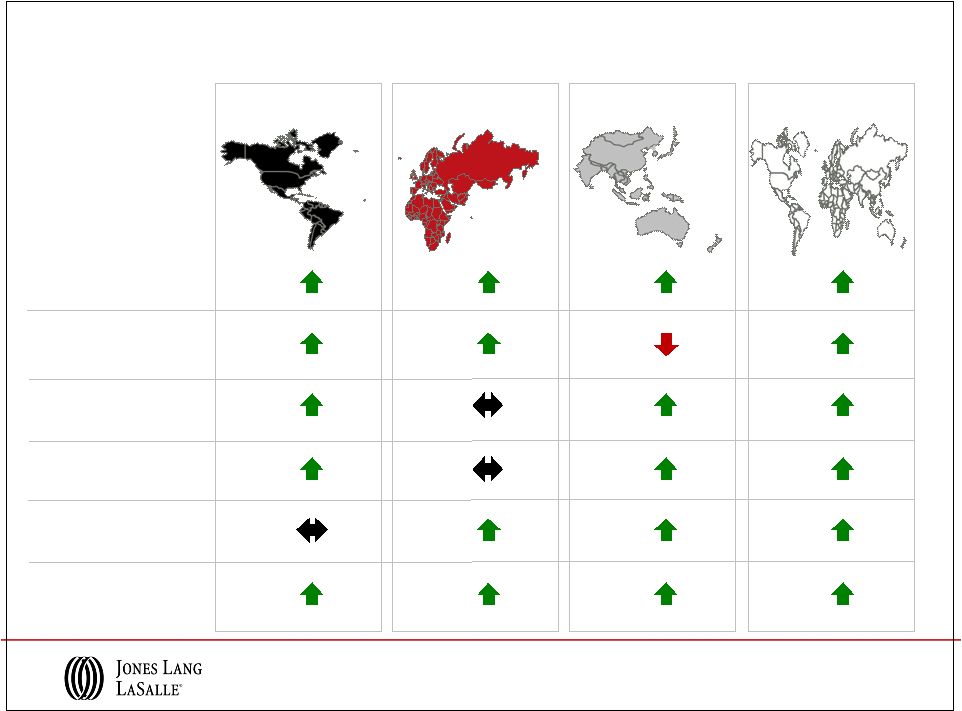

As of Q4 2010

The

Jones

Lang

LaSalle

Property

Clocks

SM

Shanghai

Rental Value

growth slowing

Rental Value

growth

accelerating

Rental Values

bottoming out

Rental Values

falling

Hong Kong, London,

Sao Paulo,

Sydney

Stockholm,

Singapore

Chicago

Mumbai

Amsterdam, Brussels,

Seoul

Toronto

Tokyo

Q4 2009

Dallas, Milan,

San Francisco

Beijing, Moscow

Berlin, Paris,

Washington DC

Detroit

New York

Americas

EMEA

Asia Pacific

Hong Kong

Rental Value

growth slowing

Rental Value

growth

accelerating

Rental Values

bottoming out

Rental Values

falling

Paris,

Tokyo

Shanghai, Sydney

Chicago,

Seoul

Amsterdam,

New York

Berlin,

Mumbai, San Francisco

London

Brussels

Toronto

Moscow, Stockholm

Detroit

Dallas

Sao Paulo

Beijing

Milan

Singapore,

Washington DC |

2010 Accomplishments and Trends

Consolidated

5

–

Full-year revenue of more than $2.9 billion

–

Adjusted operating

income

margin

of

9.1%,

adjusted

EBITDA

margin

of

11.5%

–

Leasing revenue increased 28%

–

Strong Capital Markets & Hotels

revenue growth

–

2010 high-impact hires provide

momentum into 2011

–

Larger markets 9-12 months into

cyclical recovery

–

Improved productivity in

transactional businesses

–

Retail, Corporate Solutions,

Tetris provide improved revenue

opportunities

–

Both US and Regional multi-

national corporate wins

–

More than 50M sf

added to

Property Management annuity

base

–

Second-best capital raising

year in LaSalle history: $5B

–

Nearly $3.2B capital invested

–

Focused on performance

Americas

EMEA

Asia Pacific

LaSalle

Balance Sheet

–

$250M of net debt repayment in the year

–

Maintained the firm’s investment-grade ratings |

Q4 Selected Business Wins and Expansions

6

–

AT&T Mobility –

2,300 sites

–

Beaumont Hospitals, Detroit –

8.5M sf

–

SAIC –

10M sf

–

353 N. Clark, Chicago –

$400M

–

300 S. Riverside, Chicago –

$120M

–

Navistar, Chicago –

$33M / 1.2M sf

–

The Northern Trust Company, Chicago –

207K sf

–

Healthfirst, New York –

172M sf

–

Interpublic Group –

3M sf

–

Vasakronen, Stockholm –

€483M

–

Norges, Regent Street, London –

£452M

–

Espace

Saint-Quentin, Paris –

€172M

–

Hotel de Crillon, Paris

–

Le Richmonde, Geneva –

$161M

–

The Shard, London –

595K sf

–

Soyak

Tower, Instanbul

–

538K sf

–

Publicis, Dusseldorf –

129K sf

–

Standard Chartered Bank –

16M sf

–

Alcatel Lucent –

6M sf

–

Colonial First State Property, Australia –

$229M

–

Procter & Gamble, Shanghai –

7.5M sf

–

Dusit

Thani

Phuket, Thailand –

$85M

–

Orchard Funds Management, Australia –

4.3M sf

–

Supertech

Emerald, India –

1M sf

–

Dow Chemical, Shanghai –

290K sf

Americas

EMEA

Asia Pacific |

Financial Information |

$643.7

$728.8

2009

2010

8

FY 2010 Revenue Performance

Note: Equity losses of $58.9M and $11.4M in 2009 and 2010, respectively, are included

in segment results, however, are excluded from Consolidated totals.

($ in millions; % change in local currency

)

Americas

EMEA

Asia Pacific

$1,031.6

$1,261.5

2009

2010

$538.9

$678.5

2009

2010

$245.4

$207.6

2009

2010

Consolidated

$2,480.7

$2,925.6

2009

2010

LIM

17%

17%

16%

17%

22% |

Asia

Pacific 9

FY 2010 Real Estate Services Revenue

($ in millions; % change in local currency over FY 2009)

Americas

EMEA

Leasing

Capital Markets &

Hotels

Property & Facility

Management

Project &

Development Services

Advisory, Consulting

& Other

Total RES

Operating Revenue

$637.9

$84.1

$269.4

$158.9

$110.9

$1,261.2

28%

120%

19%

1%

1%

22%

$202.6

$141.2

$142.9

$115.0

$127.2

$728.9

22%

37%

8%

11%

7%

17%

$159.4

$80.4

$303.7

$63.5

$71.4

$678.4

34%

25%

6%

35%

11%

17%

$999.9

$305.7

$716.0

$337.4

$309.5

$2,668.5

27%

51%

11%

9%

5%

18%

Total RES

Revenue

Note: Segment and Consolidated Real Estate Services (“RES”) operating

revenue exclude Equity earnings (losses). |

10

Q4 2010 Revenue Performance

Note: Equity losses of $2.6M and $0.4M in 2009 and 2010, respectively, are included in

segment results, however, are excluded from Consolidated totals.

Americas

EMEA

Asia Pacific

$344.7

$428.5

2009

2010

$225.9

$237.4

2009

2010

$178.3

$223.2

2009

2010

$66.8

$63.5

2009

2010

Consolidated

$815.1

$956.3

2009

2010

($ in millions; % change in local currency )

LIM

24%

11%

18%

4%

18% |

Asia

Pacific 11

Q4 2010 Real Estate Services Revenue

Americas

EMEA

Leasing

Capital Markets &

Hotels

Property & Facility

Management

Project &

Development Services

Advisory, Consulting

& Other

Total RES

Operating Revenue

$228.3

$35.1

$86.1

$48.1

$30.9

$428.5

30%

156%

8%

11%

2%

24%

$69.3

$52.0

$40.7

$32.2

$43.2

$237.4

4%

41%

3%

0%

13%

10%

$62.4

$28.5

$89.4

$18.8

$24.0

$223.1

36%

7%

13%

41%

20%

18%

$360.0

$115.6

$216.2

$99.1

$98.1

$889.0

25%

50%

7%

11%

18%

Total RES

Revenue

7%

($ in millions; % change in local currency over Q4 2009)

Note: Segment and Consolidated Real Estate Services (“RES”) operating

revenue exclude Equity earnings (losses). |

•

$5

billion

of

net

new

capital

raised,

2

best

year

in

LaSalle

history

•

More than $3 billion invested worldwide in 2010

•

Healthy margins generated from Advisory Fees

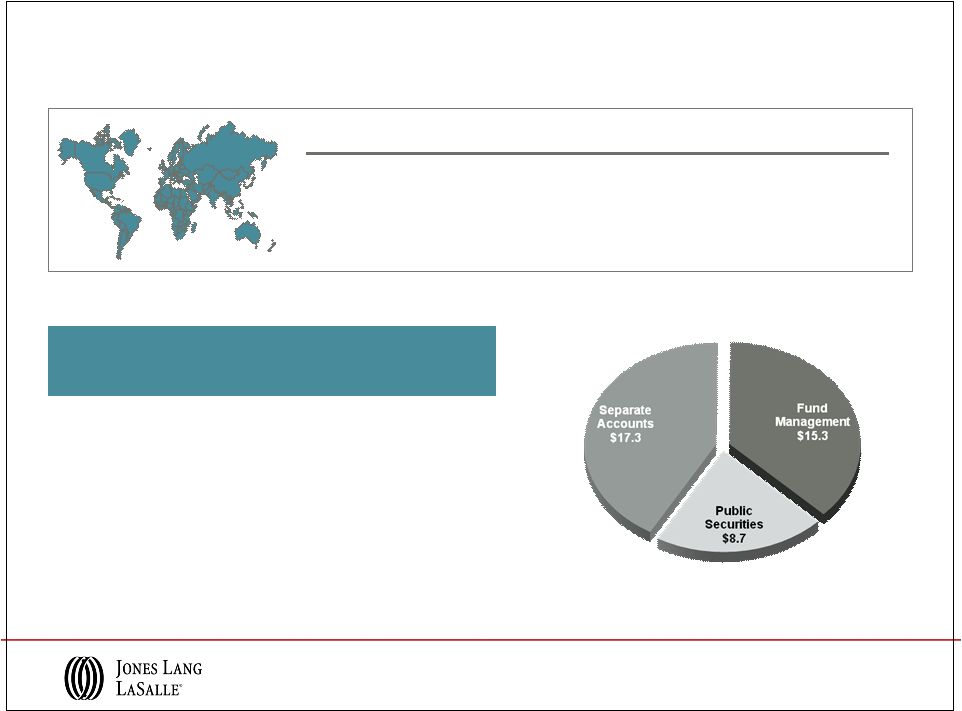

A premier global investment manager

LaSalle Investment Management

2010 Highlights

Product

Assets Under

Management

($ in billions)

Average

Performance

Private Equity

U.K.

$11.3

Above benchmark

Continental Europe

$4.2

Return: +1x equity

North America

$9.8

Above benchmark

Asia Pacific

$7.3

Return: +1x equity

Public Securities

$8.7

Above benchmark

Total Q4 2010 AUM

$41.3 B

AUM by Fund type

Note: AUM data reported on a one-quarter lag

($ in billions)

12

nd |

Solid Cash Flows and Balance Sheet Position

•

Strong cash from earnings growth

•

Net debt repayment of $250 million

•

Paid first deferred Staubach obligation

of $76 million

(2)

•

Renewed and extended credit facility

-

Capacity increased to $1.1 billion,

previously $840 million

-

Maturity extended to September 2015

•

Investment grade ratings affirmed:

Standard & Poor’s:

BBB-

(Outlook: Stable)

Moody’s Investor Services:

Baa2

(Outlook: Stable)

Cash Flows

FY 2010

FY 2009

Cash from Earnings

$316

$244

Working Capital

68

7

Cash from Operations

$384

$251

Primary Uses

Capital Expenses

(1)

(48)

(44)

Acquisitions & Deferred Payment Obligations

(130)

(27)

Co-Investment

(19)

(39)

Dividends

(9)

(8)

Net Cash Outflows

($206)

($118)

Net Share Activity & Other Financing

(23)

201

Net Bank Debt (Borrowings) / Repayments

$155

$334

Balance Sheet

FY 2010

FY 2009

Cash

$252

$69

Short Term Borrowings

28

23

Credit Facility

198

175

Net Bank Debt

($26)

$129

Deferred Business Obligations

299

394

Total Net Debt

$273

$523

($ in millions)

(1)

YTD

Capital

Expenditures

for

2010

and

2009

net

of

tenant

improvement

allowances

received

were

$46

million

and

$36

million,

respectively

(2)

$78

million

due

less

$2

million

deferred

in

accordance

with

the

merger

agreement

2010 Highlights

13 |

Appendix |

15

FY 2010 Adjusted EBITDA

*

Performance

Americas

EMEA

Asia Pacific

$133.8

$183.9

2009

2010

$14.1

$38.3

2009

2010

$44.3

$62.4

2009

2010

$53.0

$47.4

2009

2010

Consolidated

$238.6

$336.7

2009

2010

($ in millions)

LIM

* Refer to slide 18 for Reconciliation of GAAP Net Income (Loss) to EBITDA and adjusted

EBITDA for the twelve months ended December 31, 2010, and 2009, for details relative to

these adjusted EBITDA calculations. Segment adjusted EBITDA is calculated

by adding the segment’s Depreciation and amortization and non-cash co-investment charges to its

reported Operating income (loss), which excludes Restructuring charges.

Consolidated adjusted EBITDA is the sum of the adjusted EBITDA of the four segments less net income

attributable to non-controlling interests and dividends on unvested common stock. |

16

Q4 2010 Adjusted EBITDA

*

Performance

Americas

EMEA

Asia Pacific

LIM

$52.2

$78.7

2009

2010

$23.5

$25.6

2009

2010

$28.9

$28.7

2009

2010

$7.9

$10.4

2009

2010

Consolidated

$112.1

$143.1

2009

2010

($ in millions)

* Refer to slide 18 for Reconciliation of GAAP Net Income (Loss) to EBITDA and adjusted

EBITDA for the three months ended December 31, 2010, and 2009, for details relative to

these adjusted EBITDA calculations. Segment adjusted EBITDA is calculated

by adding the segment’s Depreciation and amortization and non-cash co-investment charges to its

reported Operating income (loss), which excludes Restructuring charges.

Consolidated adjusted EBITDA is the sum of the adjusted EBITDA of the four segments less net income

attributable to non-controlling interests and dividends on unvested common stock. |

17

($ in millions)

Reconciliation of GAAP Net Income (Loss) to

Adjusted Net Income

Note: Basic shares outstanding are used in the calculation of GAAP EPS for the twelve

months ending December 31, 2009, as the use of dilutive shares outstanding would

cause that EPS calculation to be anti-dilutive. 2010

2009

2010

2009

GAAP net income (loss)

84.4

$

52.0

$

153.5

$

(4.1)

$

Shares (in 000's)

44,235

43,671

44,084

38,543

GAAP earnings (loss) per share

1.91

$

1.19

$

3.48

$

(0.11)

$

GAAP net income (loss)

84.4

$

52.0

$

153.5

$

(4.1)

$

Restructuring, net of tax

0.7

8.1

4.9

35.6

Non-cash co-investment charges, net of tax

0.7

2.8

7.9

38.5

Adjusted net income

85.8

$

62.9

$

166.3

$

70.0

$

Shares (in 000's)

44,235

43,671

44,084

40,106

Adjusted earnings per share

1.94

$

1.44

$

3.77

$

1.75

$

Three Months Ended

December 31,

Twelve Months Ended

December 31, |

18

($ in millions)

Reconciliation of GAAP Net Income (Loss) to

EBITDA and Adjusted EBITDA

2010

2009

2010

2009

Net income (loss)

84.4

$

52.0

$

153.5

$

(4.1)

$

Interest expense, net of interest income

10.1

11.5

45.8

55.0

Provision (benefit) for income taxes

28.2

15.5

49.0

5.7

Depreciation and amortization

18.6

18.7

71.6

83.3

EBITDA

141.3

$

97.7

$

319.9

$

139.9

$

Non-cash co-investment charges

0.9

3.6

10.4

51.3

Restructuring

0.9

10.8

6.4

47.4

Adjusted EBITDA

143.1

$

112.1

$

336.7

$

238.6

$

Three Months Ended

December 31,

December 31,

Twelve Months Ended |