Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - People's United Financial, Inc. | d8k.htm |

| EX-99.1 - EXHIBIT 99.1 - People's United Financial, Inc. | dex991.htm |

EXHIBIT 99.2

Investor Presentation dated January 21, 2011

Fourth Quarter 2010

Earnings Review

and

Acquisition Announcement -

Danvers Bancorp (DNBK)

January 21, 2011 |

1

Certain comments made in the course of this presentation by People's United Financial are

forward- looking in nature. These include all statements about People's United

Financial's operating results or financial position for periods ending or on dates occurring

after December 31, 2010 and usually use words such as "expect", "anticipate",

"believe", and similar expressions. These comments represent management's

current beliefs, based upon information available to it at the time the statements are made,

with regard to the matters addressed.

All forward-looking statements are subject to risks and uncertainties that could cause People's

United Financial's actual results or financial condition to differ materially from those

expressed in or implied by such statements. Factors of particular importance to People’s

United Financial include, but are not limited to: (1)

failure of the parties to satisfy the closing conditions in the merger agreement in a timely manner or

at all;

(2)

failure

of

the

shareholders

of

Danvers

Bancorp

to

approve

the

merger

agreement;

(3)

failure

to

obtain governmental approvals for the merger; (4)

disruptions to the parties’

businesses as a result of the

announcement

and

pendency

of

the

merger;

(5)

costs

or

difficulties

related

to

the

integration

of

the

businesses

following

the

merger

with

Danvers

Bancorp

and

recent

acquisitions;

(6)

changes

in

general,

national

or

regional

economic

conditions;

(7)

the

risk

that

the

anticipated

benefits,

cost

savings

and

any

other savings from the transaction may not be fully realized or may take longer than expected to

realize (8)

changes

in

loan

default

and

charge-off

rates;

(9)

reductions

in

deposit

levels

necessitating

increased

borrowings

to

fund

loans

and

investments;

(10)

changes

in

interest

rates

or

credit

availability;

(11)

possible

changes

in

regulation

resulting

from

or

relating

to

the

recently

enacted

financial

reform

legislation;

(12)

changes in levels of income and expense in noninterest income and expense related activities; (13)

competition and its effect on pricing, spending, third-party relationships and revenues.

Forward Looking Statement |

2

Agenda

Fourth Quarter 2010 Results

Integration Update

Acquisition of Danvers Bancorp (DNBK)

Q&A |

3

Net income of $32.0 million, or $0.09 per share

Operating income of $36.7 million, or $0.10 per share, excluding

primarily merger-related expenses

Net interest margin of 3.85%; up 12 bps from Q3 2010

Net charge-offs to average loans decreased to 0.28% from 0.57%

in Q3 2010

NPAs

as a percentage of originated loans, REO and repossessed assets

fell to 2.07% from 2.18% as of Q3 2010

Organic loan growth of $221MM

Fourth Quarter 2010 Results

Overview |

4

Smithtown and RiverBank

transactions closed Nov. 30, 2010

Boston branches, Prudential Center and Financial District, opened mid-

December in 2010

Jeff Tengel became new head of Commercial Banking effective

January 1, 2011 following Brian Dreyer’s retirement at the end of 2010

Repurchased

$114

million

of

stock

in

4Q10

(8.7

million

shares

at

an

average price of $13.08)

2.9 million shares remain under initial share repurchase authorization

Board of Directors has authorized an additional 5% share repurchase

program, approximately 17.5 million shares

Recent Initiatives |

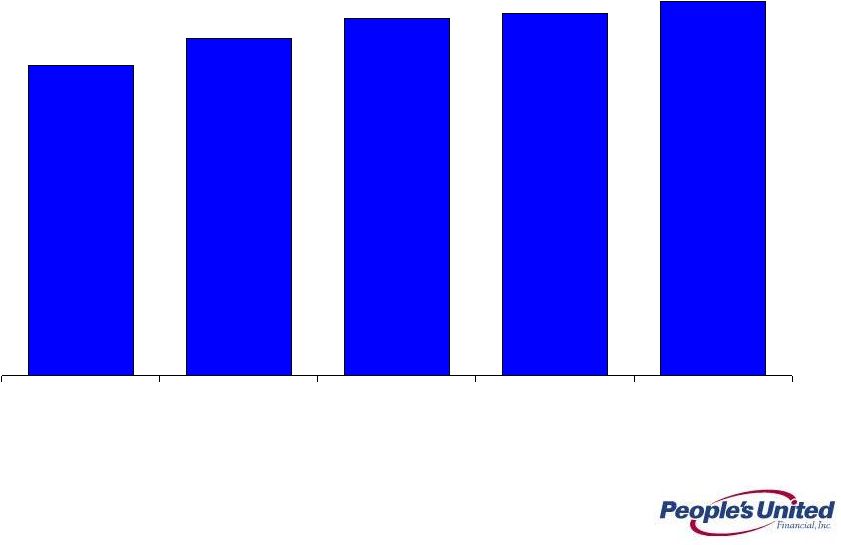

5

Net Interest Margin

5

3.19%

3.47%

3.68%

3.73%

3.85%

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010 |

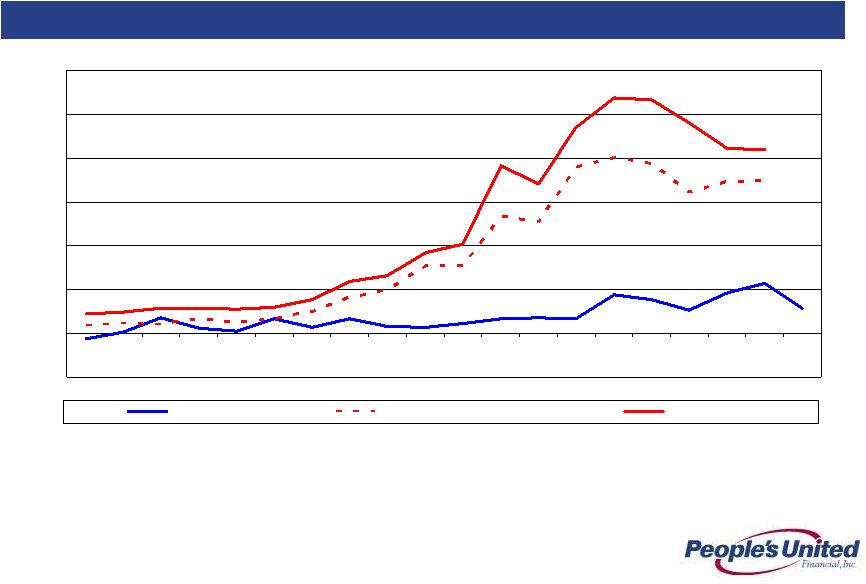

6

2006-2010

0.28

0.57

1.74

2.10

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Q1

2006

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Q3

2007

Q4

2007

Q1

2008

Q2

2008

Q3

2008

Q4

2008

Q1

2009

Q2

2009

Q3

2009

Q4

2009

Q1

2010

Q2

2010

Q3

2010

Q4

2010

PBCT

Peer Group Mean

Top 50 Banks

Fourth Quarter 2010 Results

Net Charge-Offs / Avg. Loans (%) |

7

2006-2010

2.07

2.18

4.86

4.72

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Q3

2007

Q4

2007

Q1

2008

Q2

2008

Q3

2008

Q4

2008

Q1

2009

Q2

2009

Q3

2009

Q4

2009

Q1

2010

Q2

2010

Q3

2010

Q4

2010

PBCT

Peer Group Mean

Top 50 Banks by Assets

Fourth Quarter 2010 Results

NPAs

/ Loans & REO* (%)

Non-performing assets (excluding acquired non-performing loans) as a percentage of

originated loans plus all REO and

repossessed assets; acquired non-performing loans excluded as risk of loss has been considered by virtue of our estimate of

acquisition-date fair value and/or the existence of an FDIC loss

sharing agreement |

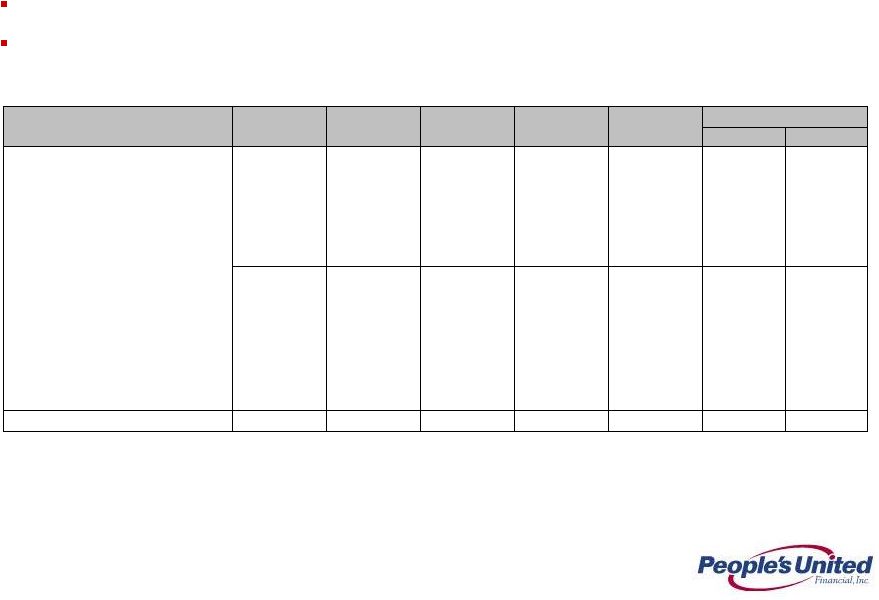

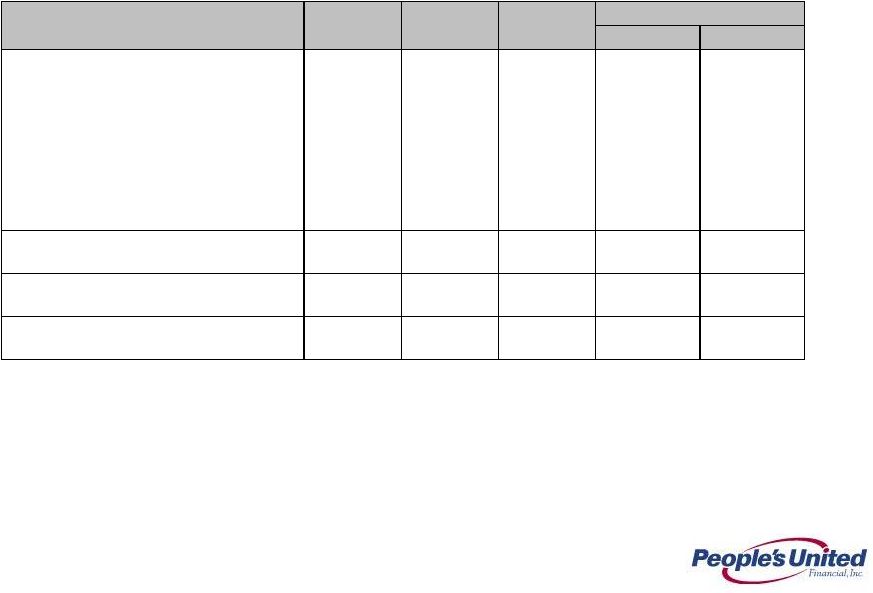

8

Loan Growth

Organic

loan

growth

resumed

with

$221MM

of

growth

in

Q4

2010

Acquisitions

of

Smithtown

and

RiverBank

added

$2.1BN

of

loans

8

Total

Legacy

Commercial real estate

7,306

$

5,618

$

1,365

$

323

$

5,493

$

1,813

$

125

$

Commercial lending

3,096

3,020

40

36

2,922

174

98

PCLC

1,212

1,212

-

-

1,185

27

27

PUEF

888

888

-

-

964

(76)

(76)

Total Commercial 12,502

10,738

1,405

359

10,564

1,938

174

Residential mortgage

2,838

2,573

141

124

2,474

364

99

Home equity and other loans

2,178

2,125

26

27

2,177

1

(52)

Total loans

17,518

$

15,436

$

1,572

$

510

$

15,215

$

2,303

221

$ Inc/(Dec)

($'s in millions)

Q4 2010

Legacy

Smithtown

River

Q3 2010 |

Integration

Update |

10

Focused on Revenue Synergies Throughout the Franchise

By Pursuing Best Practices in All Markets

Northern New England

Retail

Banking

and

Brokerage

Enhance our industry leading loyalty by initiating a New Customer Experience

program – on-boarding and retention focused

Invest in securities and life insurance licensing, product and sales training in

retail bank Introduced People’s Securities brokerage model

Objective is to increase cross-selling to 4.6 products and services per

customer (the current level in Southern NE franchise) from 3.6 products and

services (the current level in Northern NE franchise)

Upper

Middle-Market

Commercial

Banking

Larger corporate lending capabilities >$25MM per loan

Insurance brokerage capability

Southern New England

Build out small business capabilities

Market business services: payroll processing, merchant services,

business credit card,

401k administration

Emphasize private banking and wealth management |

11

Financial Federal Integration Update

Financial Federal unit, renamed People’s United Equipment Finance

While portfolio loan balances are down, we’re not losing market share as

construction market remains depressed

Yield and fee income continue to exceed expectations

Loss experience has also been better than expected

At announcement we had targeted 0% cost savings but through the elimination of

headcount and public company expenses we have reduced non-interest

expense by 13%

The

business

is

well

positioned

and

we

are

cautiously

optimistic

about

an

up-tick

in

construction activity during the second half of 2011 |

12

Massachusetts Integration Update

Butler Bank (Lowell, MA)

Retained 93% of deposits since April 2010 closing

System conversion scheduled for the first week of February

RiverBank

(N. Andover, MA)

Cost

savings

of

30%

identified

at

announcement

-

on

track

to

realize

that

target

Integrated the commercial lending group and actively training branch

personnel System conversion scheduled for first week of February

De novo branches (Downtown Boston, MA)

Early feedback, deposit gathering and lending referral activity has been

excellent |

13

Long Island Integration Update

Bank of Smithtown (Smithtown, NY)

Our

brand

of

banking,

with

its

focus

on

the

customer

experience,

is

being

received

well on Long Island by customers and employees

Initiated de novo C&I effort on Long Island in December

Building

out

Commercial

Real

Estate

Finance

(CREF)

infrastructure

–

primary

goal is

to manage existing portfolio

Expanding the workout function

System conversion scheduled for June-July time period

|

People’s United

Financial Announces Acquisition of

Danvers Bancorp (DNBK) |

15

Immediately adds desired scale to our existing Boston MSA presence

–

Pro

forma

PBCT

becomes

7

th

largest

bank

in

Massachusetts

and

Boston

MSA

–

Pro

forma

PBCT

becomes

2

nd

largest

bank

in

Essex

County,

MA

Excellent platform for commercial lending growth

–

Boston

is

the

second largest MSA within our footprint behind New York City MSA

–

49% of Danverbanks’

loans are C&l

loans

–

Adds

23

commercial

lenders

to

the

10

we

now

have

based

in

Boston

MSA

–

Asset-based lending unit can be expanded significantly

–

Complements our existing Massachusetts and New Hampshire footprint

Danvers Bancorp’s CEO, Kevin Bottomley, to join People’s United Board of

Directors and act as strategic leader of our Boston growth effort

Exceeds People’s United’s financial hurdles

–

> 15% IRR

–

Significant operating EPS accretion

Transaction Rationale

Transaction gives People’s United, New England’s largest independent bank,

scale in Boston, New England’s economic center

|

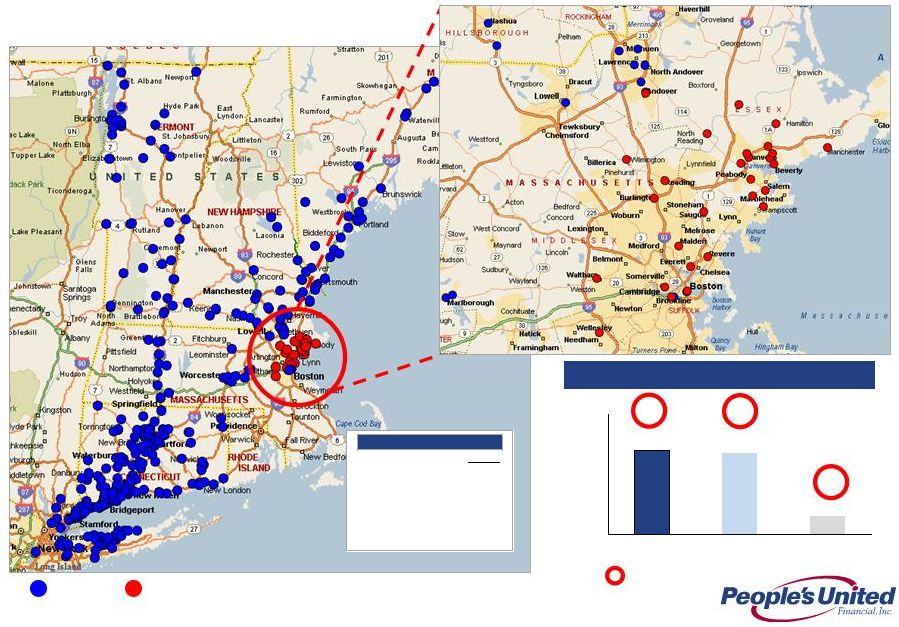

16

Solidifying Eastern Massachusetts Footprint

Source: SNL Financial

*Financials as of 9/30/2010

**Projected change from 2010-2015

Median 2010 HH Income

PBCT

DNBK

Financial Highlights*

($ in millions)

DNBK

Assets

$2,631

Gross Loans

1,745

Deposits

2,040

Branches

28

16.0

16.9

12.4

Projected HHI Growth**

$70,905

$70,175

$54,442

$50,000

$57,500

$65,000

$72,500

$80,000

PBCT

DNBK

Nation |

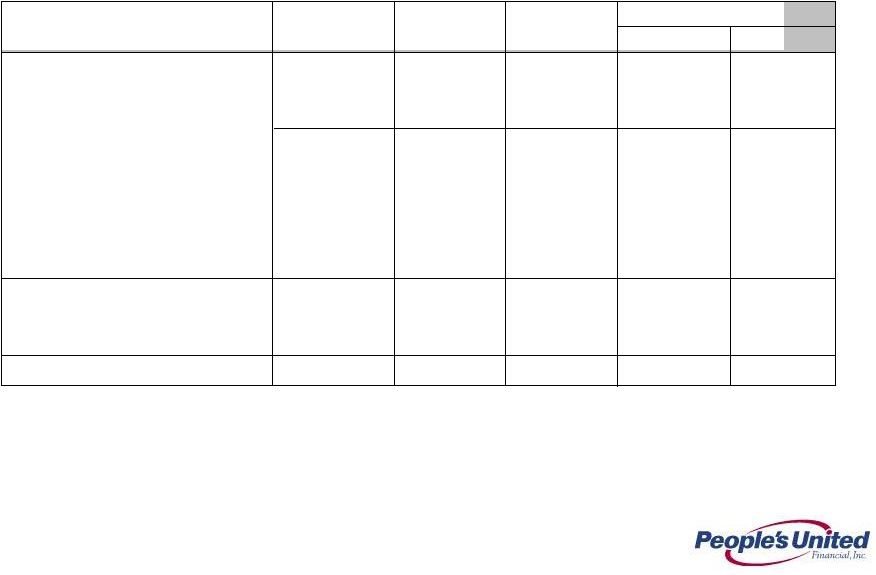

17

Essex County, MA

Massachusetts*

Positions People’s United for further growth in Eastern Massachusetts

Adds Scale in Targeted Expansion Markets

Source: SNL Financial; Deposits data as of 6/30/2010

* Excludes Bank of New York Mellon

Deposits

Market

Branch

in Market

Share

Rank

Institution (ST)

Count

($M)

(%)

1

Bank of America Corp. (NC)

280

44,234

25.4

2

Royal Bank of Scotland Group

257

24,494

14.1

3

Banco Santander SA

230

13,623

7.8

4

Toronto-Dominion Bank

159

8,716

5.0

5

Eastern Bank Corporation (MA)

95

6,162

3.5

6

Independent Bank Corp. (MA)

71

3,702

2.1

Pro Forma

59

3,598

2.1

7

Middlesex Bancorp MHC (MA)

33

3,572

2.1

8

Boston Private Financial (MA)

9

2,375

1.4

9

Berkshire Hills Bancorp Inc. (MA)

37

2,014

1.2

10

Danvers Bancorp Inc. (MA)

28

2,000

1.1

11

Brookline Bancorp Inc. (MA)

26

1,927

1.1

12

Century Bancorp Inc. (MA)

23

1,857

1.1

13

Salem Five Bancorp (MA)

22

1,757

1.0

14

Cambridge Financial Group Inc (MA)

16

1,744

1.0

15

Cape Cod Five Cents Svgs Bk (MA)

15

1,688

1.0

16

People's United Financial Inc. (CT)

31

1,598

0.9

17

Webster Financial Corp. (CT)

24

1,387

0.8

18

First Republic Bank (CA)

2

1,364

0.8

19

Meridian Interstate Bncp (MHC) (MA)

20

1,361

0.8

20

Citigroup Inc. (NY)

31

1,342

0.8

Totals (1-20)

1,409

126,915

72.9

Totals (1-178)

2,214

174,070

100.0

Deposits

Market

Branch

in Market

Share

Rank

Institution (ST)

Count

($M)

(%)

1

Toronto-Dominion Bank

32

2,034

12.4

Pro Forma

24

2,032

12.3

2

Eastern Bank Corporation (MA)

24

1,674

10.2

3

Salem Five Bancorp (MA)

17

1,573

9.6

4

Banco Santander SA

29

1,573

9.6

5

Danvers Bancorp Inc. (MA)

17

1,539

9.3

6

Bank of America Corp. (NC)

20

1,197

7.3

7

Inst for Svgs in Newburyport (MA)

7

883

5.4

8

Royal Bank of Scotland Group

15

570

3.5

9

People's United Financial Inc. (CT)

7

493

3.0

10

Newburyport Five Cents SB (MA)

7

445

2.7

Totals (1-10)

175

11,981

72.7

Totals (1-41)

258

16,469

100.0

Boston MSA*

Deposits

Market

Branch

in Market

Share

Rank

Institution (ST)

Count

($M)

(%)

1

Bank of America Corp. (NC)

203

40,046

28.9

2

Royal Bank of Scotland Group

214

23,830

17.2

3

Banco Santander SA

165

10,594

7.6

4

Toronto-Dominion Bank

108

6,469

4.7

5

Eastern Bank Corporation (MA)

87

5,878

4.2

6

Middlesex Bancorp MHC (MA)

30

3,479

2.5

Pro Forma

58

3,368

2.4

7

Independent Bank Corp. (MA)

45

2,529

1.8

8

Boston Private Financial (MA)

9

2,375

1.7

9

Danvers Bancorp Inc. (MA)

28

2,000

1.4

10

Brookline Bancorp Inc. (MA)

26

1,927

1.4

15

People's United Financial Inc. (CT)

30

1,368

1.0

Totals (1-10)

915

99,127

71.5

Totals (1-134)

1,512

138,676

100.0 |

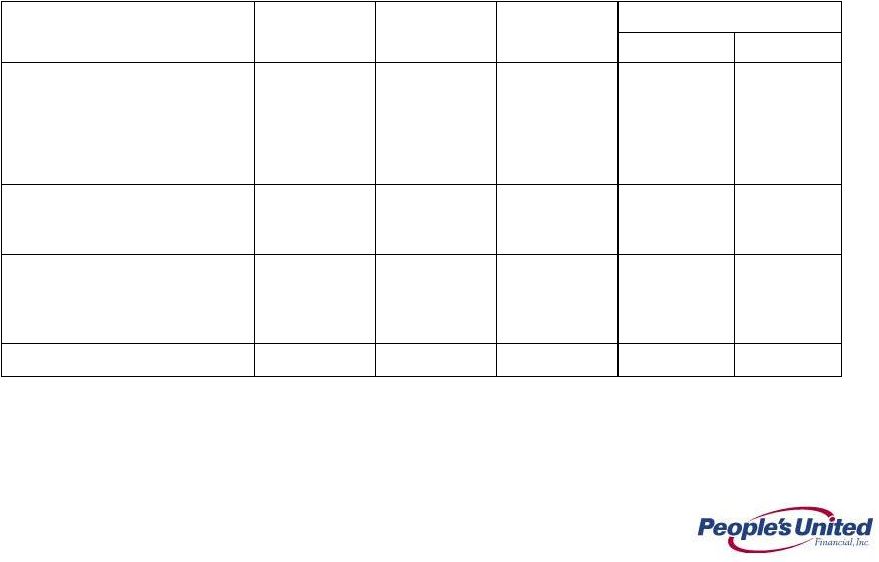

18

Completed

October 2009

Loans

$263M

Deposits

$415M

Danvers Bancorp, Inc. Overview

ROAA

0.64

ROAE

5.7

Net Interest Margin

3.49

Efficiency Ratio

71.1

TCE / TA

10.01

NPA / (Loans + OREO)

1.10

LLR / Loans

0.95

LTM NCO / Avg. Loans

0.16

Select Balance Sheet Ratios (%)

Profitability (%)

Source: SNL Financial

Financial data as of 9/30/2010

Headquarters

Danvers, MA

Established

March 1850

Branches

28

Conversion Date

12/13/2007

Overview

Recent Acquisition: Beverly National Bank

Chairman, President & CEO

Kevin T. Bottomley

Executive VP & COO

James J. McCarthy

EVP & Chief Lending Officer

John O’Neill

Executive VP & CFO

L. Mark Panella

Executive Management

Assets

$2,631

Net Loans

1,728

Deposits

2,040

Tangible Common Equity

260

Balance Sheet ($MM) |

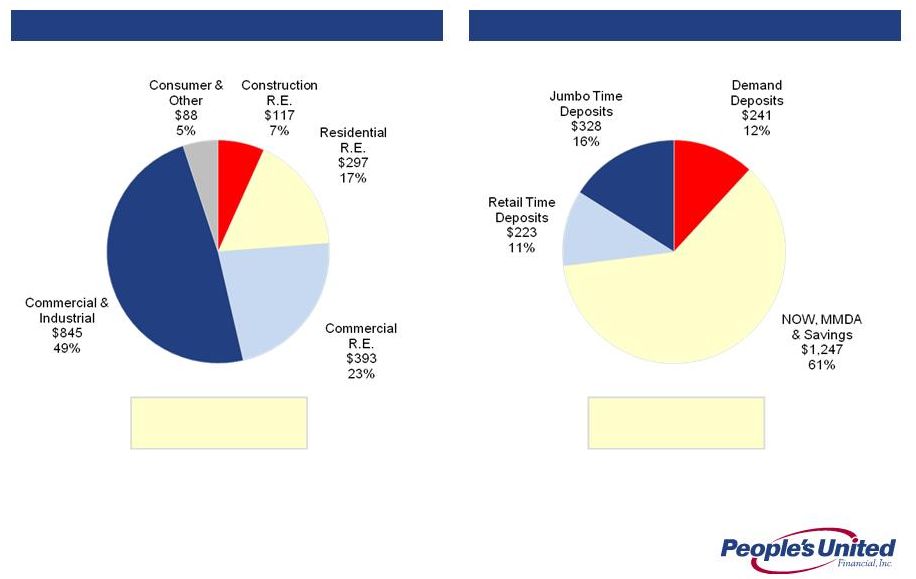

Diversified Loan Portfolio and Attractive Funding Mix

Source: Company Financials

Financial data as of 9/30/2010

*Excludes loans held for sale

($ in millions)

($ in millions)

19

5.66%

$1,741M

1.24%

$2,040M

Deposits

Loans

Yield on Loans:

Total Loans*:

Cost of Deposits:

Total Deposits: |

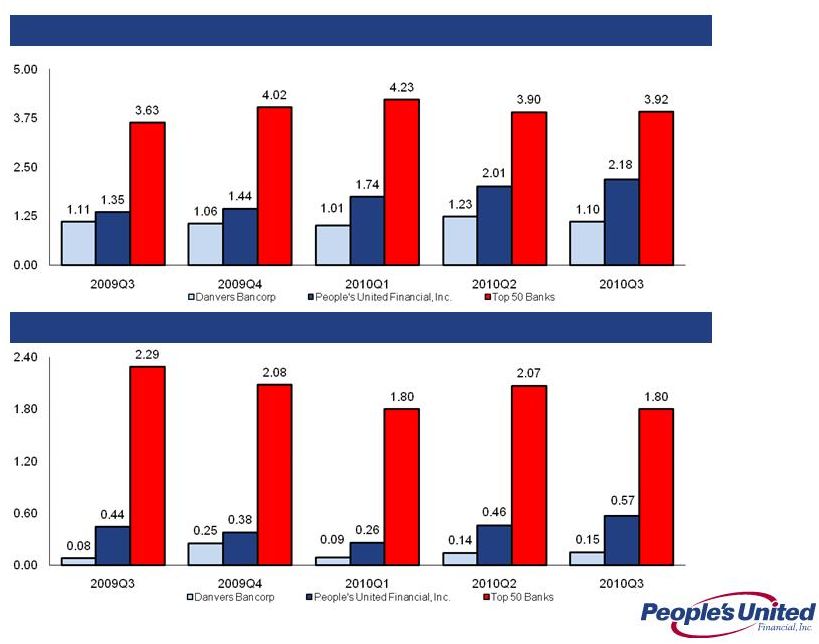

Exceptional Asset Quality

20

NPAs

/ Loans + OREO (%)

NCOs / Average Loans (%)

Source: SNL Financial

Note: PBCT Non-performing assets (excluding acquired non-performing loans) as a percentage of

originated loans plus all REO and repossessed assets; acquired non- performing loans excluded

as risk of loss has been considered by virtue of our estimate of acquisition-date fair value and/or the existence of an FDIC loss sharing

agreement |

21

Price & Structure

•

$23.00

•

$493MM

•

55% stock / 45% cash

Summary of Key Terms

Price per share:

Deal value:

Consideration:

Pricing Multiples

•

38% or ~$20MM after tax (30% excluding ESOP, SERP and restricted

stock eliminations)

•

Identified but not assumed

•

$44MM after-tax

•

1.5%

Cost savings:

Revenue synergies:

Merger-related expenses:

Gross Loan mark:

Key Assumptions

Price / tangible book:

Core deposit premium:

•

1.86x

•

13.9%

Closing & Other

Extensive due diligence:

Approvals:

Expected close:

Board representation:

•

Completed

•

Danvers shareholders; Regulatory approvals

•

2

nd

quarter 2011

•

Kevin Bottomley

to join People’s United Board of Directors |

22

Pro Forma Impact

* PBCT financials as of 12/31/2010; DNBK financials as of 9/30/2010

** Balance sheet figures do not include the impact of purchase accounting

adjustments ^ Pro forma levels at estimated close of transaction

PBCT*

DNBK*

Pro Forma**

Assets ($Bn)

25.0

2.6

27.6

Loans ($Bn)

17.5

1.7

19.2

Deposits ($Bn)

17.9

2.0

19.9

Branches

340

28

368

Tangible common equity ratio

14.1%

~12.0%

Tangible book value per share

$9.30

~$8.68

2012 operating EPS accretion

~$0.08

TBV dilution value earn back period

~7 years

Internal rate of return

>15%

^

^ |

23

Summary

We are excited about growth and confident in our position

Competitive Strength

Focused on revenue synergies throughout our footprint

Further leveraging the brand

Conservative underwriting

Pro forma Tangible Common Equity Ratio of ~12.0%

Efficient capital deployment

Closed 4 deals (Financial Federal, Butler, RiverBank and Smithtown) – all

above our 15% IRR hurdle - in 2010

Announced the acquisition of Danvers Bancorp – above our 15%

IRR hurdle

Paid out $218MM in 2010 dividends

Repurchased $191MM of stock or 14.3MM shares at a weighted average

price of $13.35

Extended period of low interest rates, multi-year de-leveraging process and

tougher regulatory environment are encouraging consolidation

Significantly more asset sensitive than peers

|

Q & A

|

Appendix

|

26

Quarterly Income Statement

26

$ Fav(unfav)

%

Net Interest Income

189.8

$

175.8

$

147.5

$

14.0

$

8%

Provision for Loan Losses

10.9

21.8

13.6

10.9

50

Non-Interest Income

75.9

75.9

71.7

-

-

Non-interest Expense: Operating

199.9

188.9

167.7

(11.0)

(6)

Non-Operating Expense

7.0

5.3

4.5

(1.7)

(31)

Total Non-Interest Expense

206.9

194.2

172.2

(12.7)

(7)

Income Before Taxes

47.9

35.7

33.4

12.2

Net Income

32.0

24.1

24.9

7.9

33

Net Operating Income

36.7

27.7

28.0

9.0

33

Earnings Per Share

0.09

0.07

0.07

0.02

29

Operating Earnings Per Share

0.10

0.08

0.08

0.02

29

vs. Q3 2010

($'s in millions, except EPS)

Q4 2010

Q3 2010

Q4 2009

34 |

27

Non-Interest Income

27

$ Fav(unfav)

%

Investment management fees

7.9

$

7.6

$

7.9

$

0.3

$

4%

Insurance revenue

6.9

8.3

7.0

(1.4)

(17)

Brokerage commissions

2.9

2.8

2.9

0.1

4

Total wealth management

17.7

18.7

17.8

(1.0)

(5)

Bank service charges

30.7

31.5

32.2

(0.8)

(3)

Merchant services income

6.4

6.9

6.3

(0.5)

(7)

Gain on Residential Loan Sales

4.2

2.4

3.0

1.8

76

Net security loss

(1.0)

-

(0.1)

(1.0)

N/M

Operating lease income

5.8

5.4

3.9

0.4

7

Loan Penalties/Late Charges

5.7

4.2

2.1

1.5

36

Other non-interest income

6.4

6.8

6.5

(0.4)

(6)

Total non-interest income

75.9

75.9

71.7

-

-

Total ex net security loss

76.9

75.9

71.8

1.0

1

($'s in millions)

Q4 2010

Q3 2010

Q4 2009

vs. Q3 2010 |

28

Non-Interest Expense

28

vs. Q3 2010

$ Increase

%

Compensation and benefits

98.3

$

93.2

$

89.2

$

5.1

$

5%

Occupancy and equipment

28.1

28.0

28.0

0.1

0

Professional/outside service fees

19.8

18.5

10.0

1.3

7

Other non-interest expense

60.7

54.5

45.0

6.2

11

Total non-interest expense

206.9

194.2

172.2

12.7

7

Non-operating Expense

7.0

5.3

4.5

1.7

31

Operating non-interest expense

199.9

188.9

167.7

11.0

6

Q4 2010

Q3 2010

Q4 2009

($'s in millions) |

29

Average Earning Assets

29

$ Inc/(Dec)

%

Commercial real estate

6,054

$

5,465

$

5,352

$

589

$

11

Commercial lending

5,087

5,096

4,011

(9)

(0)

Total Commercial 11,141

10,561

9,363

580

5

Residential mortgage

2,611

2,463

2,609

148

6

Home equity and other loans

2,170

2,184

2,259

(14)

(1)

Total loans

15,922

15,208

14,231

714

5

Investments

3,875

3,748

4,351

127

3

Total earning assets

19,797

18,956

18,582

841

4

vs. Q3 2010

($'s in millions)

Q4 2010

Q3 2010

Q4 2009 |

30

Average Funding Mix

30

$ Inc/(Dec)

%

Deposits:

Non-interest-bearing

3,634

$

3,432

$

3,321

$

202

$

6%

Savings/Now/PMA

8,249

7,930

7,145

319

4

Time

4,648

4,439

4,807

209

5

Total deposits

16,531

15,801

15,273

730

5

Sub-debt / Other borrowings

705

374

343

331

89

Total funding liabilities

17,236

16,175

15,616

1,061

7

Stockholders' equity

5,335

5,404

5,106

(69)

(1)

Total Funding

22,571

21,579

20,722

992

5

($'s in millions)

Q4 2010

vs. Q3 2010

Q3 2010

Q4 2009 |

31

Non-Performing Assets

31

NPA's - Total

663

$

371

$

206

$

- Originated

303

312

206

- Acquired

360

59

N/A

Allowance for Loan Losses

173

173

173

NPA's / Total Loans, REO &

Repossessed assets - Originated

2.07%

2.18%

1.44%

Originated NPL's / Originated Loans

1.68%

1.77%

1.19%

Allowance / Originated Loans

1.18%

1.21%

1.21%

Allowance / Originated NPL's

70%

69%

102%

Net Loan Charge-Offs / Avg Loans

0.28%

0.57%

0.38%

($ in millions)

Q4 2010

Q3 2010

Q4 2009 |

32

Home Equity Portfolio

Credit Statistics

Weighted Average:

Loan to value¹

55%

FICO scores¹

759

Net charge-offs:

0.23%

Non-accrual:

0.48%

High Quality Consumer Portfolio

Ending Balance: $5.0 billion

% of Loans: 29%

Residential Mortgage Portfolio

Credit Statistics

Weighted Average:

Loan to value¹

60%

FICO scores¹

726

Net charge-offs:

0.30%

Non-accrual:

3.17%

1-4 Family

Residential

57%

Home Equity

Loans & Lines

39%

Indirect

Auto

3%

Other

1%

As

of

December

31,

2010

(1) Excludes the impact of the former Butler Bank, former RiverBank and former Bank of

Smithtown |

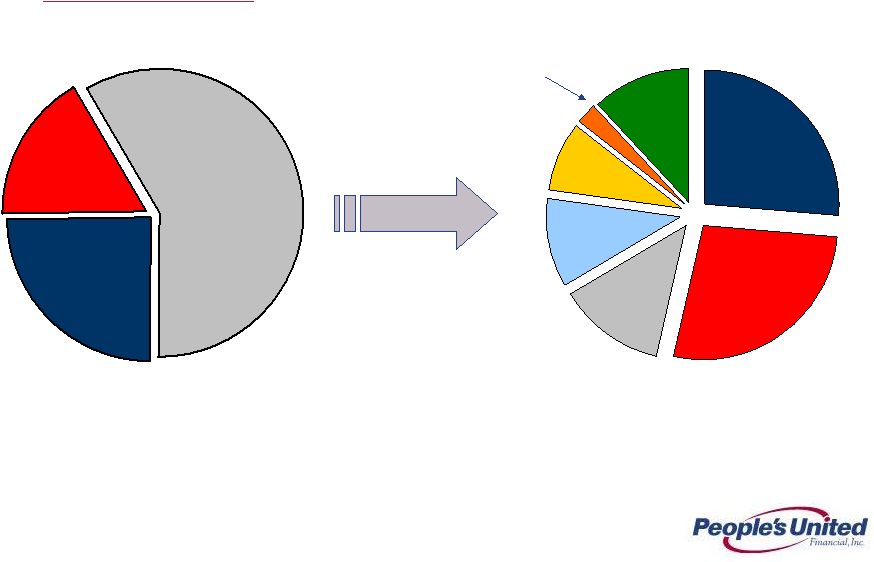

33

Retail

25%

Office

30%

Industrial

10%

Residential

13%

Hospitality

8%

Other

11%

Land

3%

Well Balanced Commercial Portfolio

As of December 31, 2010

Ending Balance: $12.5 billion

% of Loans: 71%

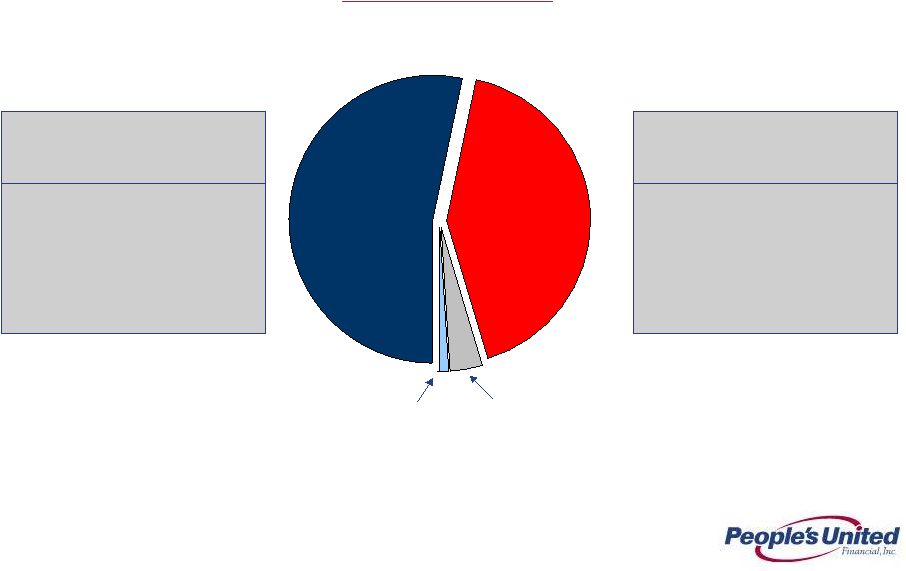

$5.4 billion CRE¹

(1) Excludes portfolios acquired on November 30, 2010

CRE, By Sector

Commercial

Real Estate

58%

General C&I

25%

Equip. Fin.

17% |

34

We

expect

that

interest

rates

will

not

rise

in

2011.

However,

we

do

expect

rates

to

rise

in

2012 and beyond

Given short term interest rates are so low and are expected to remain low this year, we

have again added to our securities portfolio

For Q3 2010 we were 3.0x as asset sensitive as our peers

For every 100bps increase in the Fed Funds rate, our net interest income will

increase by ~$40MM on an annualized basis

Notes:

1.

Analysis is as of 6/30/10 filings

2.

Data as of 6/30/10 SEC filings, where exact +100bps shock up scenario data was not

provided PBCT interpolated based on data disclosed 3.

Data as of 6/30/10 filings, where exact +200bps shock up scenario data was

not provided PBCT interpolated based on data disclosed Asset

Sensitivity Net Interest Income at Risk

1

Analysis involves PBCT estimates, see notes below

Lowest Amongst

Highest Amongst

Core

PBCT Multiple to

Scenario

Our Peers

Our Peers

Peer Median

PBCT

Peer Median

Shock Up 100bps

2

-0.6%

4.8%

2.0%

6.0%

3.0x

Shock Up 200bps

3

0.4%

9.6%

4.4%

13.3%

3.0x

Change in Net Interest Income |

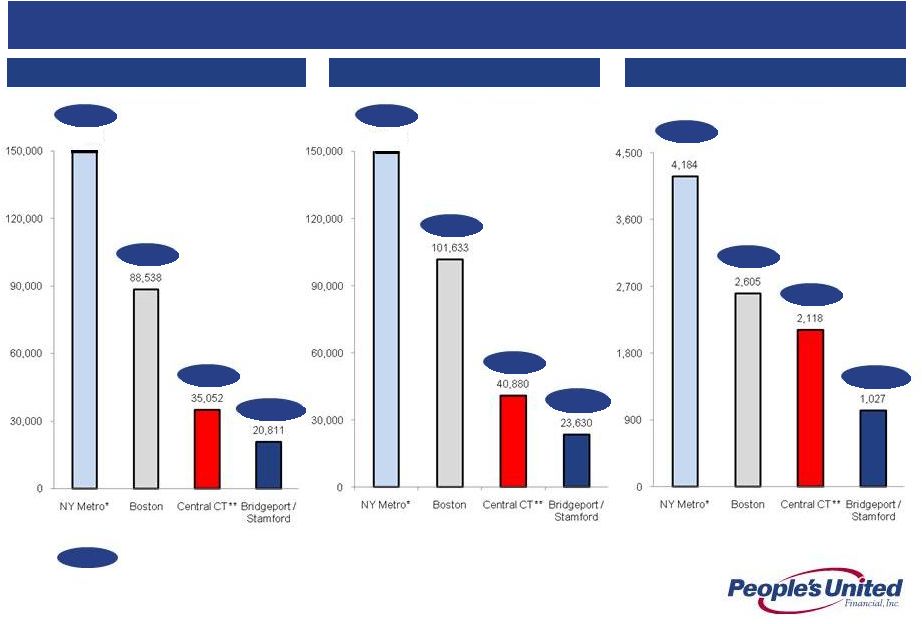

< 20 Employees

Commercial Market Opportunity by MSA

> 500 Employees

< 500 Employees

Pro Forma Deposit Market Share

Number of firms by size

People’s United is growing in NYC Metro and Boston Metro,

areas rich with potential commercial, non-commodity relationships

0.2%

2.4%

6.3%

17.8%

0.2%

2.4%

6.3%

17.8%

0.2%

2.4%

6.3%

17.8%

428,577

471,661

Source: SBA firms and employment by MSA 2007

* NY Metro area includes New York, Northern New Jersey, and Long Island MSA

** Central Connecticut includes New Haven and Hartford MSAs

35 |

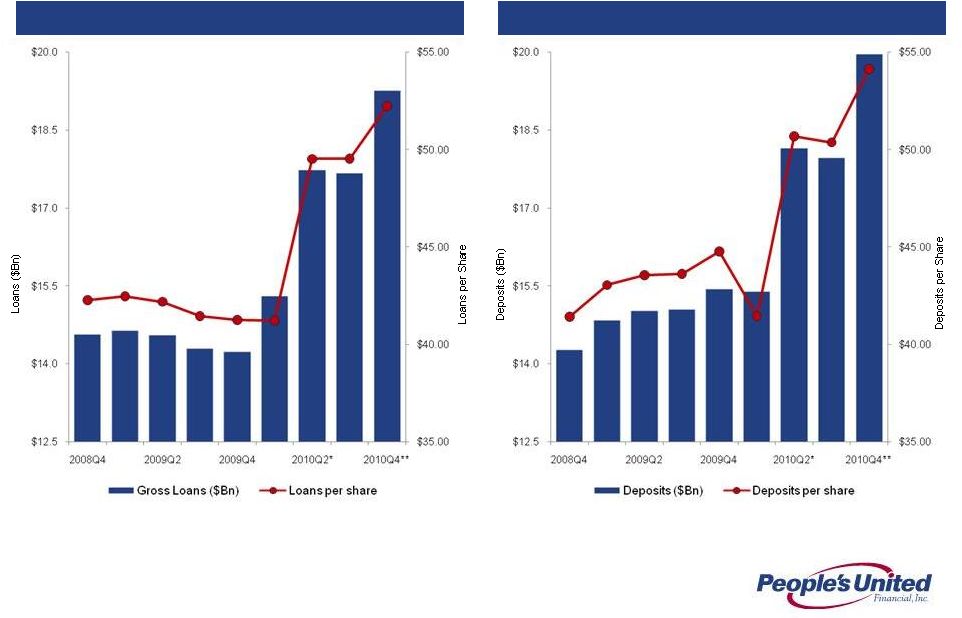

36

Loans and Deposits

Source: SNL Financial

* Pro forma for SMTB & LSBX acquisitions

** Pro forma for DNBK acquisition

Loans

Deposits |

37

Peer Group

Company Name

Ticker

State

1

Associated Banc-Corp

ASBC

WI

2

Astoria Financial Corporation

AF

NY

3

BOK Financial Corporation

BOKF

OK

4

City National Corporation

CYN

CA

5

Comerica Incorporated

CMA

TX

6

Commerce Bancshares, Inc.

CBSH

MO

7

Cullen/Frost Bankers, Inc.

CFR

TX

8

First Horizon National Corporation

FHN

TN

9

Flagstar Bancorp, Inc.

FBC

MI

10

Fulton Financial Corporation

FULT

PA

11

Hudson City Bancorp, Inc.

HCBK

NJ

12

M&T Bank Corporation

MTB

NY

13

Marshall & Ilsley Corporation

MI

WI

14

New York Community Bancorp, Inc.

NYB

NY

15

Synovus Financial Corp.

SNV

GA

16

TCF Financial Corporation

TCB

MN

17

Valley National Bancorp

VLY

NJ

18

Webster Financial Corporation

WBS

CT

19

Zions Bancorporation

ZION

UT |

38

Additional Information

Participants in the Transaction

People’s United, Danvers Bancorp and their respective directors, executive officers and certain

other members of management and employees may be soliciting proxies from Danvers Bancorp

stockholders in favor

of

the

merger

with

Danvers

Bancorp.

Information

regarding

the

persons

who

may,

under

the

rules

of

the SEC, be considered participants in the solicitation of the Danvers Bancorp stockholders in

connection with the proposed merger will be set forth in the proxy statement/prospectus when it

is filed with the SEC. You can find information about the executive officers and directors of

People’s United in its Annual Report on Form 10-K for the year ended December 31, 2009

and in its definitive proxy statement filed with the SEC on March 23, 2010. You can find

information about Danvers Bancorp’s executive officers and directors in its Annual Report

on Form 10-K for the year ended December 31, 2009 and in its definitive proxy statement

filed with the SEC on April 16, 2010. You can obtain free copies of these documents from

People’s United or Danvers Bancorp using the contact information above.

In connection with the proposed merger with Danvers Bancorp, Inc. (“Danvers Bancorp”),

People’s United will file with the Securities and Exchange Commission (the “SEC”)

a Registration Statement on Form S-4 that will include a proxy statement of Danvers Bancorp

that also constitutes a prospectus of People’s United. Danvers Bancorp will mail the

proxy statement/prospectus to its stockholders. Investors and security holders are urged to

read the proxy statement/prospectus regarding the proposed merger when it becomes available

because it will contain important information. You may obtain a free copy of the proxy

statement/prospectus (when available) and other related documents filed by People’s United

and Danvers Bancorp with the SEC at the SEC’s website at www.sec.gov. The proxy

statement/prospectus (when it is available) and the other documents may also be obtained for free

by accessing People’s United website at www.peoples.com under the tab “Investor

Relations” and then under the heading “Financial Information” or by accessing

Danvers Bancorp’s website at www.danversbank.com under the tab “Investor

Relations” and then under the heading “SEC Filings”. |

For more information,

investors may contact: Peter Goulding, CFA

peter.goulding@peoples.com

(203) 338-6799 |