Attached files

| file | filename |

|---|---|

| 8-K - CHINA FUND INC | v207455_8-k.htm |

|

THE CHINA FUND, INC.

(CHN)

|

The Martin Currie

Shanghai team |

IN BRIEF

|

||||||||

|

Net asset value per

share

|

US$35.31

|

At 31 December

2010

|

US$ return

|

||||||

|

Market

price

|

US$32.50

|

China Fund

NAV

|

MSCI

Golden Dragon*

|

||||||

|

Premium/(discount)

|

(7.96

|

%)

|

%

|

%

|

|||||

|

Fund size

|

US$804.4m

|

One month

|

7.2

|

|

3.4

|

|

|||

|

Source:

State Street Bank and Trust Company.

|

Year to

date

|

27.3

|

13.6

|

||||||

|

One year

|

27.3

|

13.6

|

|||||||

|

Three years

%pa

|

5.3

|

(1.3

|

)

|

||||||

|

Past

performance is not a guide to future returns.

Source:

State Street Bank and Trust Company. NAV

performance.

*Source

for index data: MSCI.

|

|||||||||

| MANAGER’S COMMENTARY | |

|

The Fund had a good 2010,

finishing the year up 27.3% against a benchmark return of 13.6%. We were

not helped by our speciality in A-shares; the Shanghai Composite index

fell 14.3% in 2010, dragged down by government controls on the property

market and the huge issuance of new equity. Some 349 new companies listed

in the A-share markets in 2010, raising US$67 billion in capital, which

compares with US$42 billion over the same period in the United States. Our outperformance was driven by

our long-running bias towards domestic consumer and healthcare stocks. One

example, China Medical Systems, in which we first invested in June 2007 as

an AIM-listed ‘orphan stock’, enjoyed a particularly strong finish to the

year and is now our largest holding. We were also helped by our

investments in Taiwan, which was the best-performing

Chinese market in 2010 (TWSE +9%).

We think there is more to come

from Taiwan, which has just entered its Year

100 (the founding of the Republic of China is conventionally dated to an

army mutiny in Wuchang on 10 October 1910). The first day of 2011 also saw

the cross-straits free-trade agreement come into effect. Anyone doubting

the revival of Taiwanese consumption should have accompanied me to the

Leofoo Village theme park in central

Taiwan at the holiday weekend, along

with 30,000 other people (never again!). The consumer stocks, however,

represent one of our main challenges in 2011: although we remain bullish

on the prospects for the growth of Chinese consumption, many stocks we

would like to own are now too expensive. The Chinese market’s

inefficiencies still yield some interesting, cheap stocks, but to locate

them we find ourselves being pushed towards seriously out-of-favour

sectors (property, solar, utilities) and the obscure.

The main macroeconomic threat in

2011 is still inflation; attention so far has focused on food inflation,

which was +11.7% in November, compared with non-food inflation of +1.9%.

This was caused largely by bad weather and should ease with the spring.

The danger is that non-food inflation, as represented in fast-rising wages

and resurgent material prices, may prove more intractable. Beijing city raised its minimum wage by

20.8% and Moutai raised its vodka price by 20% (these two events are not

necessarily related). National monetary policy was officially changed from

‘appropriately loose’ to ‘moderate’, which in real terms meant a

25-basis-point rise in interest rates on Christmas Day, a 50-basis-point

increase in the reserve-requirement ratio (now 19% for big banks) and the

removal of some stimulus measures, such as the tax break on small cars.

This being the case, the ‘renminbi appreciation/hot money’ story will

probably remain in play for a while. The politicians may have been

emboldened by the strong export figures (+34.9% year on year in November)

to allow a slight quickening in the glacial pace of the yuan’s

appreciation against the US

dollar.

|

INVESTMENT STRATEGY

The Fund is 97.4% invested with holdings

in 60 companies.

The company declared a US$51.5 million

dividend payout, which was made at the month-end and equated to US$2.27 per

share. We raised cash by taking profits on a number of strong performers

(China

Shineway Pharmaceutical,

Wumart, Intime Department

Store, Hollysys Automation

Technologies). We cut our

A-share weighting by selling Shanghai Airport

and Zhejiang

Commodities, shifting some

additional cash into Taiwan by buying Chinatrust

Bank. (Our A-share

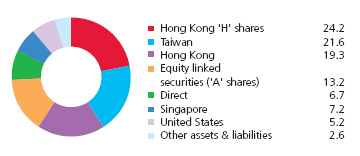

weighting is now 13.2%, compared with our Taiwan weighting of 21.6%). We also subscribed

to the Hong Kong IPO of construction-machinery manufacturer Zoomlion (we are

familiar with the company through our work in the A-share market) and bought the

unloved China

Mobile, which will benefit

from the increasing use of smartphones.

The annual general meeting of the fund

will be held at 10.30am on Thursday, March 3, 2011 at the offices of Clifford

Chance LLP, 31 West 52nd

Street, New York. We welcome investors to come

along.

Chris Ruffle, Martin Currie

Inc*

*Martin

Currie Ltd and Heartland Capital Management Ltd (HCML) have established MC China

Ltd (MCCL), as a joint venture company, to provide investment management or

investment advisory services to the range of China investment

products managed by Martin Currie.

MCCL

has appointed Martin Currie Investment Management Ltd (MCIM), or its affiliates,

as investment manager of Martin Currie’s China investment

products. HCML has seconded both Chris Ruffle and Shifeng Ke to MCIM, or its

affiliates, on a full time basis with the same roles and responsibilities as if

they were full time employees.

31 DECEMBER 2010

|

FUND

DETAILS

|

|

Market cap

|

US$740.4m

|

|

Shares

outstanding

|

22,781,762

|

|

Exchange

listed

|

NYSE

|

|

Listing

date

|

July 10,

1992

|

|

Listed and direct investment

manager

|

Martin Currie

Inc

|

|

Source: State Street Bank and

Trust Company.

|

ASSET ALLOCATION

Source: State Street Bank

and Trust Company

|

INDUSTRY

ALLOCATION

|

|||||

|

The

China Fund,

|

MSCI

Golden

|

||||

|

Inc

%

|

Dragon

%

|

||||

|

Healthcare

|

20.8 | 0.4 | |||

|

Consumer

discretionary

|

19.6 | 6.2 | |||

|

Consumer

staples

|

19.0 | 3.0 | |||

|

Financials

|

16.3 | 36.4 | |||

|

Industrials

|

6.2 | 7.6 | |||

|

Information

technology

|

5.0 | 20.4 | |||

|

Materials

|

3.6 | 7.1 | |||

|

Utilities

|

2.9 | 3.4 | |||

|

Telecommunications

|

2.6 | 6.7 | |||

|

Energy

|

1.4 | 8.8 | |||

|

Other assets &

liabilities

|

2.6 | — | |||

|

*Source:

State Street Bank and Trust Company. Source for index data:

MSCI

|

|||||

|

PERFORMANCE

|

(US$ RETURNS) | |||||||

|

NAV

|

Market

price

|

|||||||

|

%

|

%

|

|||||||

|

One month

|

7.2 | 5.9 | ||||||

|

Year to

date

|

27.3 | 23.6 | ||||||

|

Three years

%pa

|

5.3 | 8.1 | ||||||

|

Past

performance is not a guide to future

returns.

|

||||||||

|

Three

year returns are annualized.

|

||||||||

|

Source:

State Street Bank and Trust Company

|

||||||||

|

15

LARGEST HOLDINGS (50.3%)

|

|||||

|

Fund

%

|

|||||

|

China Medical System

Holdings

|

Healthcare

|

8.7 | |||

|

Huiyin Household

Appliances

|

Consumer

discretionary

|

5.4 | |||

|

Far Eastern Department

Stores

|

Consumer

discretionary

|

4.1 | |||

|

Ping An

Insurance

|

Financials

|

4.0 | |||

|

Wumart

Stores

|

Consumer

staples

|

3.4 | |||

|

Hsu Fu Chi

International

|

Consumer

staples

|

3.3 | |||

|

Shandong Weigao

Group

|

Healthcare

|

3.2 | |||

|

China Fishery

Group

|

Consumer

staples

|

2.9 | |||

|

Ruentex

Development

|

Financials

|

2.8 | |||

|

Sinopharm Medicine

Holding

|

Healthcare

|

2.6 | |||

|

Boshiwa

International

|

Consumer

discretionary

|

2.4 | |||

|

ENN Energy

|

Utilities

|

1.9 | |||

|

FamilyMart

|

Consumer

discretionary

|

1.9 | |||

|

Zong Su

Foods

|

Consumer

staples

|

1.9 | |||

|

China

Bright

|

Healthcare

|

1.8 | |||

|

DIRECT

INVESTMENTS (6.7%) †

|

|||||

|

Fund

%

|

|||||

|

Zong Su

Foods

|

Consumer

staples

|

1.9 | |||

|

China

Bright

|

Healthcare

|

1.9 | |||

|

Hand Enterprise Solutions

(prefered)

|

Information

technology

|

1.8 | |||

|

Qingdao Bright

Moon

|

Industrials

|

1.1 | |||

|

Ugent

Holdings

|

Industrials

|

0.0 | |||

|

China

Silicon

|

Information

technology

|

0.0 | |||

|

Hand Enterprise Solutions (common

stock)

|

Information

technology

|

0.0 | |||

Source:

State Street Bank and Trust Company.

† The Board

has suspended further direct investments until improvements are made in the

policies and procedures pursuant to which direct investments

are made.

|

FUND PERFORMANCE (BASED ON NET

ASSET VALUE)

|

(US$

RETURNS)

|

||||||||||

|

One

month

|

Three

months

|

Calendar year

to

date

|

One

year

|

Three

years

|

Five

years

|

Since

launch

|

|||||

|

%

|

%

|

%

|

%

|

%pa

|

%pa

|

%pa

|

|||||

|

The China Fund,

Inc.

|

7.2

|

7.9

|

27.3

|

27.3

|

5.3

|

27.8

|

13.0

|

||||

|

MSCI Golden

Dragon

|

3.4

|

6.3

|

13.6

|

13.6

|

(1.3

|

)

|

13.1

|

11.0

|

|||

|

Hang Seng Chinese Enterprise

|

(1.1

|

)

|

2.2

|

(1.0

|

)

|

(1.0

|

)

|

(7.6

|

)

|

18.9

|

19.7

|

|

Shanghai Stock Exchange

180

|

0.9

|

7.6

|

(13.0

|

)

|

(13.0

|

)

|

(15.6

|

)

|

29.8

|

n/a

|

|

Past

performance is not a guide to future returns. Actual returns to a shareholder of

The Fund will be based on market price and reflect transactions and

expenses.

Source:

State Street Bank and Trust Company. Launch date 10 July 1992. Three, five year

and since launch returns are all annualized.

Source

for index data: MSCI for the MSCI Golden Dragon and Copyright 2010 Bloomberg LP

for the Hang Seng China Enterprise and the Shanghai Stock Exchange 180. For a

full description of each index please see the index descriptions

section.

PERFORMANCE IN PERSPECTIVE

Past

performance is not a guide to future returns.

Source:

Martin Currie Inc as at 30 November 2010.

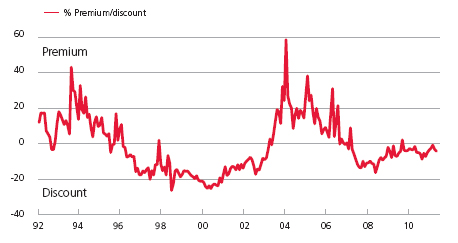

THE CHINA FUND INC.

PREMIUM/DISCOUNT

Past

performance is not a guide to future returns.

Source:

Martin Currie Inc as at 30 November 2010.

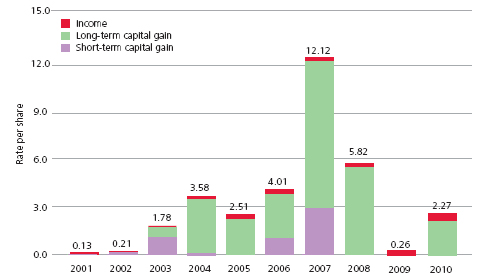

10 YEAR DIVIDEND HISTORY

CHART

|

Total

|

0.13 | 0.21 | 1.78 | 3.58 | 2.51 | 4.01 | 12.12 | 5.82 | 0.26 | 2.27 | ||||||||||||||||||||||||||||||

|

Income

|

0.13 | 0.06 | 0.07 | 0.20 | 0.22 | 0.30 | 0.28 | 0.48 | 0.26 | 0.37 | ||||||||||||||||||||||||||||||

|

Long-term

capital

|

0.00 | 0.00 | 0.67 | 3.27 | 2.29 | 2.73 | 9.00 | 5.34 | 0.00 | 1.90 | ||||||||||||||||||||||||||||||

|

Short-term

capital

|

0.00 | 0.15 | 1.04 | 0.11 | 0.00 | 0.98 | 2.84 | 0.00 | 0.00 | 0.00 |

Past

performance is not a guide to future returns.

Source:

State Street Bank and Trust Company.

|

31 DECEMBER

2010

|

||||||||

|

Asset

Allocation

|

Company (BBG

ticker)

|

Price

|

Holding

|

Value US$

|

% of

portfolio

|

|||

|

Hong Kong H

|

24.2

|

|||||||

|

China Medical System

Holdings

|

867

|

HK

|

HK$7.5

|

72,353,760

|

|

$69,624,176

|

8.7

|

|

|

Wumart

Stores

|

8277

|

HK

|

HK$19.2

|

11,120,000

|

|

$27,466,503

|

3.4

|

|

|

Shandong Weigao Group Medical

Polymer

|

8199

|

HK

|

HK$22.1

|

9,176,000

|

|

$25,970,090

|

3.2

|

|

|

Sinopharm Medicine

Holding

|

297

|

HK

|

HK$27.1

|

6,056,800

|

|

$21,115,914

|

2.6

|

|

|

Boshiwa International

Holding

|

1698

|

HK

|

HK$6.0

|

24,932,000

|

|

$19,308,608

|

2.4

|

|

|

Asian Citrus

Holdings

|

73

|

HK

|

HK$9.6

|

6,677,000

|

|

$8,289,075

|

1.1

|

|

|

Fook Woo

|

923

|

HK

|

HK$3.1

|

19,836,000

|

|

$7,859,632

|

1.0

|

|

|

Zijin Mining

Group

|

2899

|

HK

|

HK$7.2

|

8,340,000

|

|

$7,606,934

|

0.9

|

|

|

ZTE Corp.

|

763

|

HK

|

HK$30.9

|

1,875,689

|

|

$7,468,250

|

0.9

|

|

|

Taiwan

|

21.6

|

|||||||

|

Far Eastern Department

Stores

|

2903

|

TT

|

NT$48.8

|

19,543,604

|

|

$32,677,128

|

4.1

|

|

|

Ruentex Development

Co

|

9945

|

TT

|

NT$51.3

|

12,694,000

|

|

$22,334,718

|

2.8

|

|

|

FamilyMart

|

5903

|

TT

|

NT$98.2

|

4,501,652

|

|

$15,161,704

|

1.9

|

|

|

Uni-President Enterprises

Corp.

|

1216

|

TT

|

NT$43.3

|

10,023,901

|

|

$14,869,196

|

1.8

|

|

|

WPG Holdings

Co

|

3702

|

TT

|

NT$56.3

|

7,457,103

|

|

$14,399,359

|

1.8

|

|

|

China Metal

Products

|

1532

|

TT

|

NT$33.4

|

11,500,347

|

|

$13,174,132

|

1.6

|

|

|

Chinatrust

Financial

|

2891

|

TT

|

NT$21.4

|

17,527,288

|

|

$12,864,506

|

1.6

|

|

|

KGI

Securities

|

6008

|

TT

|

NT$16.7

|

16,984,780

|

|

$9,699,264

|

1.2

|

|

|

Synnex

Technology

|

2347

|

TT

|

NT$78.7

|

3,088,006

|

|

$8,335,228

|

1.0

|

|

|

Taiwan Life 4percent Conv

Bond*

|

n/a

|

NT$120.2

|

2,000,000

|

|

$8,242,073

|

1.0

|

||

|

Yuanta Financial

Holdings

|

2885

|

TT

|

NT$21.8

|

10,520,593

|

|

$7,866,134

|

1.0

|

|

|

Fubon Financial

Holdings

|

2881

|

TT

|

NT$40.0

|

5,195,134

|

|

$7,127,239

|

0.9

|

|

|

Lien Hwa

Industrial

|

1229

|

TT

|

NT$23.5

|

8,724,881

|

|

$7,017,250

|

0.9

|

|

|

Hong Kong

|

19.3

|

|||||||

|

Huiyin Household

Appliances

|

1280

|

HK

|

HK$2.1

|

160,413,750

|

|

$43,749,674

|

5.4

|

|

|

ENN Energy

|

2688

|

HK

|

HK$23.3

|

5,084,000

|

|

$15,206,381

|

1.9

|

|

|

China Mobile

|

941

|

HK

|

HK$77.2

|

1,365,500

|

|

$13,570,241

|

1.7

|

|

|

Natural Beauty

Bio-Technology

|

157

|

HK

|

HK$2.1

|

47,710,000

|

|

$12,766,449

|

1.6

|

|

|

Ports

Design

|

589

|

HK

|

HK$21.5

|

4,549,500

|

|

$12,554,179

|

1.6

|

|

|

Chaoda Modern Agriculture

(Holdings)

|

682

|

HK

|

HK$5.8

|

13,999,357

|

|

$10,553,659

|

1.3

|

|

|

Changsa Zoomlion Heavy

Industries

|

1157

|

HK

|

HK$17.6

|

4,090,821

|

|

$9,241,285

|

1.1

|

|

|

Shangri-La Asia

|

69

|

HK

|

HK$21.1

|

3,061,555

|

|

$8,310,399

|

1.0

|

|

|

China Water

Affairs

|

855

|

HK

|

HK$3.1

|

19,976,000

|

|

$7,940,802

|

1.0

|

|

|

Intime Department Store

Group

|

1833

|

HK

|

HK$11.4

|

5,278,629

|

|

$7,795,795

|

1.0

|

|

|

Golden Meditech

Co

|

801

|

HK

|

HK$1.5

|

35,040,000

|

|

$6,536,262

|

0.8

|

|

|

China Shineway Pharmaceutical

Group

|

2877

|

HK

|

HK$22.3

|

2,222,000

|

|

$6,374,502

|

0.8

|

|

|

Yorkey Optical International

Cayman

|

2788

|

HK

|

HK$1.4

|

5,036,926

|

|

$907,175

|

0.1

|

|

|

FUJI Food & Catering

Services

|

1175

|

HK

|

HK$0.0

|

5,462,000

|

|

$0

|

0.0

|

|

|

Equity Linked Securities ('A'

Shares)

|

13.2

|

|||||||

|

Ping An

Insurance

|

n/a

|

US$8.5

|

3,775,759

|

|

$32,178,495

|

4.0

|

||

|

Zhejiang China Commodities City

Group

|

n/a

|

US$5.3

|

2,771,970

|

|

$14,666,493

|

1.8

|

||

|

Shanghai

Qiangsheng

|

n/a

|

US$1.1

|

10,482,652

|

|

$11,453,492

|

1.4

|

||

|

Shanghai Yuyuan

Tourist

|

n/a

|

US$2.0

|

4,293,036

|

|

$8,762,361

|

1.1

|

||

|

Suning

Appliance

|

n/a

|

US$2.0

|

4,311,019

|

|

$8,527,196

|

1.1

|

||

|

Tangshan Jidong

Cement

|

n/a

|

US$3.6

|

2,354,087

|

|

$8,423,840

|

1.0

|

||

|

Wuliangye

Yibin

|

n/a

|

US$5.3

|

1,403,507

|

|

$7,338,938

|

0.9

|

||

|

Zhejiang

Guyuelongshan

|

n/a

|

US$2.1

|

3,022,849

|

|

$6,261,572

|

0.8

|

||

|

Citic

Securities

|

n/a

|

US$1.9

|

2,475,000

|

|

$4,728,628

|

0.6

|

||

|

China Railway Construction

Group

|

n/a

|

US$1.0

|

3,932,600

|

|

$4,026,982

|

0.5

|

||

|

Direct

|

6.7

|

|||||||

|

Zong Su

Foods

|

n/a

|

US$5,603.0

|

2,677

|

|

$15,000,034

|

1.9

|

||

|

China Bright

|

n/a

|

HK$7.9

|

14,665,617

|

|

$14,980,221

|

1.9

|

||

|

Hand Enterprise Solutions

(preferred)

|

n/a

|

US$1.8

|

8,027,241

|

|

$14,192,162

|

1.8

|

||

|

Qingdao Bright

Moon

|

n/a

|

US$0.3

|

31,827,172

|

|

$9,293,534

|

1.1

|

||

|

Ugent

Holdings

|

n/a

|

HK$0.0

|

177,000,000

|

|

$0

|

0.0

|

||

|

China Silicon

Corp.

|

n/a

|

US$0.0

|

3,014,731

|

|

$0

|

0.0

|

||

|

Hand Enterprise Solutions (common

stock)

|

n/a

|

US$0.0

|

500,000

|

|

$0

|

0.0

|

||

*This is an unlisted convertible bond.

Shares in Taiwan Life are listed on the Taiwan Stock

Exchange.

|

Asset

Allocation

|

Company (BBG

ticker)

|

Price

|

Holding

|

Value US$

|

% of

portfolio

|

|

Singapore

|

7.2

|

||||

|

Hsu Fu Chi

International

|

HFCI SP

|

SG$3.7

|

9,484,000

|

$27,122,481

|

3.3

|

|

China Fishery

Group

|

CFG SP

|

SG$2.2

|

13,255,000

|

$23,136,601

|

2.9

|

|

Financial One

Corp

|

FIN SP

|

SG$0.5

|

12,030,000

|

$4,593,392

|

0.6

|

|

CDW Holding

|

CDW SP

|

SG$0.1

|

51,310,000

|

$3,298,586

|

0.4

|

|

USA

|

5.2

|

||||

|

WuXi PharmaTech

Cayman

|

WX US

|

US$16.1

|

883,490

|

$14,259,529

|

1.8

|

|

Far East Energy

|

FEEC US

|

US$0.7

|

16,392,823

|

$11,474,976

|

1.4

|

|

Hollysys Automation

Technologies

|

HOLI US

|

US$15.2

|

530,200

|

$8,037,832

|

1.0

|

|

Mindray Medical

International

|

MR US

|

US$26.4

|

291,700

|

$7,700,880

|

1.0

|

|

Other assets &

liabilities

|

$20,941,438

|

2.6

|

INDEX

DESCRIPTIONS

MSCI Golden Dragon

Index

The MSCI Golden Dragon is a free

float-adjusted market capitalization index that is designed to measure equity

market performance in the China region. As of May 2005 the MSCI Golden

Dragon Index consisted of the following country indices: China, Hong Kong and Taiwan.

Hang Seng China Enterprise Index

The Hang Seng China Enterprise Index is

a capitalization-weighted index comprised of state-owned Chinese companies

(H-shares) listed on the Hong Kong Stock Exchange and included in Hans Seng

Mainland China index.

Shanghai Stock Exchange 180

Index

The Shanghai Stock Exchange 180 'A'

Share Index is a capitalization-weighted index. The index tracks the daily price

performance of the 180 most representative 'A' share stocks listed on the

Shanghai Stock Exchange.

OBJECTIVE

The investment objective of the Fund is

to achieve long term capital appreciation. The Fund seeks to achieve its

objective through investment in the equity securities of companies and other

entities with significant assets, investments, production activities, trading or

other business interests in China or which derive a significant part of

their revenue from China.

The Fund has an operating policy that

the Fund will invest at least 80% of its assets in China companies. For this purpose, 'China

companies' are (i) companies for which the principal securities trading market

is in China; (ii) companies for which the principal securities trading market is

outside of China or in companies organized outside of China, that in both cases

derive at least 50% of their revenues from goods or services sold or produced,

or have a least 50% of their assets in China; or (iii) companies organized in

China. Under the policy, China will mean the People's Republic of

China, including Hong Kong, and Taiwan

CONTACTS

The China Fund, Inc.

c/o State Street Bank

and Trust Company

2 Avenue de Lafayette

PO Box 5049

Boston, MA 02206-5049

Tel: (1) 888 CHN-CALL

(246 2255)

www.chinafundinc.com

Important

information: This document

is issued and approved by Martin Currie Inc (MC Inc), as investment adviser of

The China Fund Inc (the Fund). MC Inc is authorised and regulated by the

Financial Services Authority (FSA) and incorporated under limited liability in

New York, USA. Registered in Scotland (No BR2575), registered address

Saltire Court, 20 Castle Terrace, Edinburgh, EH1 2ES. Information herein is believed to be

reliable but has not been verified by MC Inc. MC Inc makes no representation or

warranty and does not accept any responsibility in relation to such information

or for opinion or conclusion which the reader may draw from the newsletter.

Martin Currie Ltd and Heartland Capital

Management Ltd (HCML) have established MC China Ltd (MCCL), as a joint venture

company, to provide investment management or investment advisory services to our

China product. MCCL has appointed Martin

Currie Investment Management Ltd (MCIM), or its affiliates, as investment

manager of our China funds. HMCL has seconded both Chris

Ruffle and Shifeng Ke to MCIM or its affiliates on a full time basis with the

same roles and responsibilities as if they were full time

employees.

The Fund is classified as a

'non-diversified' investment company under the US Investment Company Act of 1940

as amended. It meets the criteria of a closed ended US mutual fund and its shares are listed

on the New York Stock Exchange. MC Inc has been appointed investment adviser to

the Fund.

Investors are advised that they will not

generally benefit from the rules and regulations of the United Kingdom Financial

Services and Markets Act 2000 and the FSA for the protection of investors, nor

benefit from the United Kingdom Financial Services Compensation Scheme, nor have

access to the Financial Services Ombudsman in the event of a dispute. Investors

will also have no rights of cancellation under the FSA's Conduct of Business

Sourcebook of the United

Kingdom.

This newsletter does not constitute an

offer of shares. MC Inc, its ultimate and intermediate holding companies,

subsidiaries, affiliates, clients, directors or staff may, at any time, have a

position in the market referred to herein, and may buy or sell securities,

currencies, or any other financial instruments in such markets. The information

or opinion expressed in this newsletter should not be construed to be a

recommendation to buy or sell the securities, commodities, currencies or

financial instruments referred to herein.

The information provided in this report

should not be considered a recommendation to purchase or sell any particular

security. There is no assurance that any securities discussed herein will remain

in an account's portfolio at the time you receive this report or that securities

sold have not been repurchased.

It should not be assumed that any of the

securities transactions or holdings discussed here were or will prove to be

profitable, or that the investment recommendations or decisions we make in the

future will be profitable or will equal the investment performance of the

securities discussed herein.

Investing in the Fund involves certain

considerations in addition to the risks normally associated with making

investments in securities. The value of the shares issued by the Fund, and the

income from them, may go down as well as up and there can be no assurance that

upon sale, or otherwise, investors will receive back the amount originally

invested. There can be no assurance that you will receive comparable performance

returns, or that investments will reflect the performance of the stock examples

contained in this document. Movements in foreign exchange rates may have a

separate effect, unfavorable as well as favorable, on the gain or loss otherwise

experienced on an investment. Past performance is not a guide to future returns.

Accordingly, the Fund is only suitable for investment by investors who are able

and willing to withstand the total loss of their investment. In particular,

prospective investors should consider the following risks:

|

à

|

The companies quoted on Greater Chinese stock exchanges are exposed to the risks of political, social and religious instability, expropriation of assets or nationalisation, rapid rates of inflation, high interest rates, currency depreciation and fluctuations and changes in taxation, which may affect income and the value of investments. |

|

à

|

At present, the securities market and the regulatory framework for the securities industry in China is at an early stage of development. The China Securities Regulatory Commission (CSRC) is responsible for supervising the national securities markets and producing relevant regulations. The Investment Regulations, under which the Fund invests in the People's Republic of China (PRC) and which regulate repatriation and currency conversion, are new. The Investment Regulations give CSRC and State Administration of Foreign Exchange (SAFE) wide discretions and there is no precedent or certainty as to how these discretions might be exercised, either now or in the future. The Fund may, from time to time, obtain access to the securities markets in China via Access Products. Such products carry additional risk and may be less liquid than the underlying securities which they represent. |

|

à

|

During the past 15 years, the PRC

government has been reforming the economic and political systems of the

PRC, and these reforms are expected to continue, as evidenced by the

recently announced changes. The Fund's operations and financial results

could be adversely affected by adjustments in the PRC's state plans,

political, economic and social conditions, changes in the policies of the

PRC government such as changes in laws and regulations (or the

interpretation thereof), measures which may be introduced to control

inflation, changes in the rate or method of taxation, imposition of

additional restrictions on currency conversion and the imposition of

additional import

restrictions.

|

|

à

|

PRC's disclosure and

regulatory standards are in many respects less stringent than standards in

certain Organisation for Economic Co-operation and Development (OECD)

countries, and there may be less publicly available or less reliable

information about PRC companies than is regularly published by or about

companies from OECD

countries.

|

|

à

|

The Shanghai Stock Exchange and

Shenzhen Stock Exchange have lower trading volumes than most OECD

exchanges and the market capitalisations of listed companies are small

compared to those on more developed exchanges in developed markets. The

listed equity securities of many companies in the PRC are accordingly

materially less liquid, subject to greater dealing spreads and experience

materially greater volatility than those of OECD countries. These factors

could negatively affect the Fund's

NAV.

|

|

à

|

The Fund invests primarily in

securities denominated in other currencies but its NAV will be quoted in

US dollars. Accordingly, a change in the value of such securities against

US dollars will result in a corresponding change in the US dollar

NAV.

|

|

à

|

The marketability of quoted shares

may be limited due to foreign investment restrictions, wide dealing

spreads, exchange controls, foreign ownership restrictions, the restricted

opening of stock exchanges and a narrow range of investors. Trading volume

may be lower than on more developed stockmarkets, and equities are less

liquid. Volatility of prices can also be greater than in more developed

stockmarkets. The infrastructure for clearing, settlement and registration

on the primary and secondary markets may be underdeveloped. Under certain

circumstances, there may be delays in settling transactions in some of the

markets.

|

Martin Currie Inc, registered in

Scotland (no BR2575)

Registered office: Saltire Court, 20

Castle Terrace, Edinburgh EH11 2ES Tel: 44 (0) 131 229 5252 Fax: 44 (0) 131 228

5959 www.martincurrie.com

North American office: 1350 Avenue of

the Americas, Suite 3010, New York, NY 10019, USA Tel: (1) 212 258 1900 Fax: (1)

212 258 1919

Authorised and registered by the

Financial Services Authority and incorporated with limited liability in New

York, USA.

Please note: calls to the above numbers

may be recorded.