Attached files

| file | filename |

|---|---|

| EX-31.2 - SECTION 302 CERTIFICATION/GAERTNER - MACC PEI LIQUIDATING TRUST | exhibit312_122810.htm |

| EX-31.1 - SECTION 302 CERTIFICATION/PRENTICE - MACC PEI LIQUIDATING TRUST | exhibit311_122810.htm |

| EX-32.1 - SECTION 906 CERTIFICATION/PRENTICE - MACC PEI LIQUIDATING TRUST | exhibit321_122810.htm |

| EX-32.2 - SECTION 906 CERTIFICATION/GAERTNER - MACC PEI LIQUIDATING TRUST | exhibit322_122810.htm |

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

||||

|

Form 10-K

|

||||

|

(Mark one)

|

||||

|

R

|

ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|||

|

For the fiscal year ended September 30, 2010

|

||||

|

£

|

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|||

|

For the transition period from _________ to __________

|

||||

|

Commission file number 000-24412

|

||||

|

MACC PRIVATE EQUITIES INC.

|

||||

|

(Exact name of registrant as specified in its charter)

|

||||

|

Delaware

|

42-1421406

|

|||

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|||

|

2533 South Coast Highway 101; Suite 240,

Cardiff-By-The-Sea, California

|

92007

|

|||

|

(Address of principal executive offices)

|

(Zip Code)

|

|||

|

Registrant’s telephone number (760) 479-5080

|

||||

|

Securities registered under Section 12(b) of the Exchange Act:

|

||||

|

None.

|

||||

|

Securities registered under Section 12(g) of the Exchange Act:

|

||||

|

Common Stock, $0.01 par value

|

||||

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes £ No R

|

||||

|

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes £ No R

|

||||

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 (the Exchange Act) during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes R No £

|

||||

|

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes £ No £

|

||||

|

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. £

|

||||

|

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

||||

|

Large accelerated filer £

|

Accelerated filer £

|

|||

|

Non-accelerated filer R

|

Smaller reporting Company £

|

|||

|

(Do not check if a smaller reporting company)

|

||||

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes £ No R

|

||||

|

Aggregate market value of the voting stock held by non-affiliates of the registrant as of December 15, 2010, based upon the value of the price reported by the OTCQB on that date: $1,700,588.

|

||||

|

Number of shares outstanding of the registrant's Common Stock as of December 15, 2010: 2,464,621

|

||||

CAUTIONARY STATEMENTS REGARDING FORWARD-LOOKING STATEMENTS

This Form 10-K of MACC Private Equities Inc. (“MACC” or “we” or “us” or the “Company”) contains forward-looking statements. All statements in this Form 10-K, including those made by MACC’s management, other than statements of historical fact, are forward-looking statements. These forward-looking statements are based on current management expectations that involve substantial risks and uncertainties that could cause actual results to differ materially from the results expressed in, or implied by, these forward-looking statements. Forward-looking statements relate to future events or our future financial performance. We generally identify forward-looking statements by terminology such as “may,” “will,” “should,” “could,” “would,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “intends,” “targets,” “potential,” and “continue,” or the negative of these terms, or other similar words. Examples of forward-looking statements contained in this Form 10-K include statements regarding MACC’s:

|

|

●

|

ability to continue as a going concern;

|

|

|

●

|

ability to pay down debt;

|

|

|

●

|

ability to meet cash flow requirements;

|

|

|

●

|

future financial and operating results;

|

|

|

●

|

business strategies, prospects, and prospects of its portfolio companies;

|

|

|

●

|

ability to operate as a business development company;

|

|

|

●

|

regulatory structure;

|

|

|

●

|

adequacy of cash resources and working capital;

|

|

|

●

|

projected costs;

|

|

|

●

|

competitive positions;

|

|

|

●

|

management’s plans and objectives for future operations; and

|

|

|

●

|

industry trends.

|

These forward-looking statements are based on management’s estimates, projections and assumptions as of the date hereof and include the assumptions that underlie such statements. Any expectations based on these forward-looking statements are subject to risks and uncertainties and other important factors, including those discussed below and in the section titled “Risk Factors.” Other risks and uncertainties are disclosed in MACC’s prior Securities and Exchange Commission (“SEC”) filings. These and many other factors could affect MACC’s future financial condition and operating results and could cause actual results to differ materially from expectations based on forward-looking statements made in this document or elsewhere by MACC or on its behalf. MACC undertakes no obligation to revise or update any forward-looking statements. The forward-looking statements contained in this Form 10-K are excluded from the safe harbor protection provided by Section 27A of the Securities Act of 1933, as amended (the “1933 Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

TABLE OF CONTENTS

|

Part I

|

Page

|

||

|

Item 1

|

Business

|

1 | |

|

Item 1A

|

Risk Factors

|

2 | |

| Item 1B | Unresolved Staff Comments | 11 | |

|

Item 2

|

Properties

|

12 | |

|

Item 3

|

Legal Proceedings

|

12 | |

|

Item 4

|

(Removed and Reserved).

|

12 | |

|

Part II

|

|||

|

Item 5

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

12 | |

|

Item 6

|

Selected Financial Data

|

14 | |

|

Item 7

|

Management’s Discussion and Analysis of Financial Conditions and Results of Operation

|

14 | |

|

Item 7A

|

Quantitative and Qualitative Disclosures About Market Risk

|

23 | |

|

Item 8

|

Financial Statements and Supplementary Data

|

25 | |

|

Item 9

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

51 | |

|

Item 9A

|

Controls and Procedures

|

51 | |

|

Item 9B

|

Other Information

|

52 | |

|

Part III

|

|||

|

Item 10

|

Directors, Executive Officers and Corporate Governance

|

53 | |

|

Item 11

|

Executive Compensation

|

58 | |

|

Item 12

|

Security Ownership of Certain Beneficial Owners and Management

|

60 | |

|

Item 13

|

Certain Relationships and Related Transactions, and Director Independence

|

61 | |

|

Item 14

|

Principal Accountant Fees and Services

|

61 | |

|

Part IV

|

|||

|

Item 15

|

Exhibits and Financial Statement Schedules

|

63 | |

Part I

Item 1. Business.

General

MACC Private Equities Inc. was formed as a Delaware corporation on March 3, 1994. It has elected to be treated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). MACC has no employees, and all of its day to day operations are carried out by its officers and the staff of its investment adviser, Eudaimonia Asset Management, LLC (“EAM” or the “Adviser”) with the assistance of its subadviser, InvestAmerica Investment Advisors, Inc. (“InvestAmerica” or the “Subadviser”). EAM was engaged by MACC in April 2008 to manage any assets which are raised after that date (the “New Portfolio”), and InvestAmerica was engaged by MACC and EAM to assist EAM in continuing to manage the assets which MACC held prior to April 2008 (the “Existing Portfolio”). However, as of the date of this report, no new assets have been raised to create the New Portfolio. In addition, at the annual meeting held on November 30, 2010 the shareholders voted against allowing the MACC to 1) sell or otherwise issue shares of the Company’s common stock at a price below its then-current net asset value per share, and 2) to issue warrants, options or rights to subscribe for or convert into the Company’s common stock. The Board of Directors is evaluating appropriate next steps based on shareholder actions. The Board will continue to review a number of alternatives, including seeking shareholder approval to liquidate. At same time, we will continue to harvest Existing Portfolio assets to continue the repayment of our outstanding debt.

Financial Information

Please refer to “Item 7-Management’s Discussion and Analysis of Financial Condition and Results of Operations” for information about revenues, profit and loss measurements and total assets and liabilities, and “Item 8 - Financial Statements and Supplementary Data” for our financial statements and supplementary data.

MACC’s Operation as a BDC

Under the 1940 Act, a BDC may not acquire any asset other than “Qualifying Assets” as defined under Section 55(a) of the 1940 Act, unless, at the time the acquisition is made, Qualifying Assets represent at least 70% of the value of the BDC’s total assets. The principal categories of Qualifying Assets relevant to MACC’s business are the following:

|

|

(1)

|

Securities purchased in transactions not involving any public offering from the issuer of such securities, which issuer is an eligible portfolio company. An eligible portfolio company is defined in the 1940 Act as any issuer that:

|

|

|

(a)

|

is organized under the laws of, and has its principal place of business in, the United States;

|

|

|

(b)

|

is not an investment company; and

|

|

|

(c)

|

satisfies one of the following:

|

|

|

(i)

|

it does not have any class of securities with respect to which a member of a national securities exchange, broker or dealer may extend or maintain credit;

|

|

|

(ii)

|

it is controlled by a BDC, either alone or as part of a group acting together, and such BDC exercises control over the company and as a result of such control has an affiliated person who is a director of such BDC;

|

|

|

(iii)

|

it has total assets of not more than $4,000,000, and capital and surplus (shareholders’ equity less retained earnings) of not less than $2,000,000;

|

|

|

(iv)

|

it has a class of securities listed on a national securities exchange, with an aggregate market value of outstanding voting and non-voting equity of less than $250 million; or

|

|

|

(v)

|

such other criteria prescribed by the SEC established as consistent with public interest, the protection of investors, and the purposes fairly intended by the policy and provisions of the 1940 Act.

|

|

|

(2)

|

Cash, cash items, government securities, or high quality debt securities maturing in one year or less from the time of investment.

|

|

|

(3)

|

Securities received in exchange for or distributed on or with respect to securities described in (1) above, or pursuant to the exercise of options, warrants or rights relating to such securities.

|

- 1 -

In addition, a BDC must have been organized (and have its principal place of business) in the United States for the purpose of making investments in the types of securities described in (1) above and, in order to count the securities as Qualifying Assets for the purpose of the 70% test, the BDC must make available to the issuers of the securities significant managerial assistance. Making available significant managerial assistance means, among other things, any arrangement whereby the BDC, through its directors, officers or employees offers to provide, and, if accepted, does so provide, significant guidance and counsel concerning the management, operations or business objectives and policies of a portfolio company.

Under the 1940 Act, once a company has elected to be regulated as a BDC, it may not change the nature of its business so as to cease to be, or withdraw its election as, a BDC unless authorized by vote of a majority, as defined in the 1940 Act, of the company’s shares.

Investments and Divestitures

During the fiscal year 2010, MACC sold portfolio investments and collected on installment sales resulting in a net realized loss of $3,185,785. MACC made two follow-on investments of Existing Portfolio companies of $72,342 in order to protect its interests in those positions.

Item 1A. Risk Factors.

AN INVESTMENT IN MACC’S COMMON STOCK IS SUBJECT TO A NUMBER OF RISKS AND SPECIAL CONSIDERATIONS, INCLUDING THE FOLLOWING. THE RISKS SET OUT BELOW ARE THE PRINCIPAL RISK FACTORS ASSOCIATED WITH AN INVESTMENT IN MACC KNOWN TO US, AS WELL AS THOSE FACTORS GENERALLY ASSOCIATED WITH AN INVESTMENT IN A COMPANY WITH INVESTMENT OBJECTIVES, INVESTMENT POLICIES, CAPITAL STRUCTURE OR TRADING MARKETS SIMILAR TO MACC'S.

RISKS RELATED TO OUR INVESTMENTS

Our investments may be risky, and you could lose all or part of your investment.

MACC is designed for long-term investors. Investors should not rely on MACC for their short-term financial needs. The value of the higher risk securities in which MACC invests will be affected by general economic conditions; the securities market; the markets for public offerings and corporate acquisitions; specific industry conditions; and the management of the individual portfolio companies. Additionally, MACC may not achieve its investment objectives.

MACC continues to have an ongoing need to raise cash from portfolio sales to fund operations and pay down outstanding debt. MACC’s effort to sell certain investments has taken longer than initially anticipated while performance of the underlying portfolio companies in certain cases has deteriorated. MACC’s ability to liquidate positions continued to be adversely affected by current credit conditions and the downturn in the financial markets and the global economy throughout the current fiscal year. MACC had a principal of $3,367,928 on its term loan (the “Term Loan”) with Cedar Rapids Bank & Trust (“CRB&T”), on September 30, 2010 which is due and payable on January 10, 2011. On December 13, 2010, the Company paid $693,263 to CRB&T in the form of a principal payment on the outstanding note payable with the CRB&T. The payment was made from proceeds of a portfolio company exit transaction and in accordance with the terms outlined in the Term Loan. Subsequent to the payment, the balance of the Term Loan on December 13, 2010 was $2,663,029. It is expected that MACC will enter into an extension of the Term Loan on or about January 10, 2011 which will extend its maturity date to July 10, 2011.

MACC will need to either extend the due date on the current Term Loan or consider additional sources of financing and additional sales of investments in order to meet current payment and operating requirements. No assurance can be given that MACC will be successful in its efforts to extend its current financing arrangement or raise additional funding in the near term and accordingly these facts raise substantial doubt about MACC’s ability to continue as a going concern. The accompanying financial statements have been prepared assuming that MACC will continue as a going concern.

At MACC’s annual shareholder meeting held on November 30, 2010, shareholders voted against giving MACC the ability to raise additional capital through the issuance of shares of common stock at a price below MACC’s then-current

- 2 -

net asset value per share. In addition, shareholders voted against allowing MACC the ability to issue warrants, options or rights to subscribe for or convert into common stock. Without these authorizations to sell shares at below net asset value or issue options or warrants, MACC’s ability to raise funding through the capital markets is highly unlikely.

An investment strategy focused primarily on privately-held companies presents certain challenges, including the lack of available information about these companies, a dependence upon the talents and efforts of only a few key portfolio company personnel and a greater vulnerability to economic downturns.

As a BDC, MACC invests a large portion of its assets in restricted securities issued by small, private companies, some of which have operated at losses or have experienced substantial fluctuations in operating results. There is generally little or no publicly available information about such companies and MACC must rely on the diligence of its Adviser and Subadviser to obtain the information necessary for its decision to invest in these companies. In order to maintain its status as a BDC, MACC must have at least 70% of its total assets invested in Qualifying Assets. Typically, for their success, such companies depend on the management talents and efforts of one person or a small group of persons, so that the death, disability or resignation of such person or persons could have a materially adverse impact on them. Moreover, smaller companies frequently have narrower product lines and smaller market shares than larger companies and, therefore, may be more vulnerable to competitors’ actions and market conditions, as well as general economic downturns. Such companies may face intense competition, including competition from companies with greater financial resources, more extensive research and development, manufacturing, marketing and service capabilities, and a larger number of qualified managerial and technical personnel. Because these companies will generally have highly leveraged capital structures, reduced cash flow resulting from an adverse business development, shifts in customer preferences, an economic downturn or the inability to complete a public offering or other financing may adversely affect the return on, or the recovery of, MACC’s investment in them. Investment in such companies therefore involves a high degree of business and financial risk, which can result in substantial losses and, accordingly, should be considered highly speculative. No assurance can be given that some of MACC’s investments will not result in substantial or complete losses.

Because our investments are and will continue to typically be privately-issued, they will have limited liquidity, and thus their value is decreased.

All of our Existing Portfolio investments consist of securities acquired directly from their issuers in private transactions. They are usually subject to restrictions on resale and are generally illiquid. Usually there is no established trading market for such securities into which they could be sold. In addition, most of the securities are not eligible for sale to the public without registration under the 1933 Act, which would involve delay and expense. Restricted securities generally sell at a price lower than similar securities that are not subject to restrictions on sale.

As a BDC, we are subject to limitations on our ability to engage in certain transactions with affiliates.

As a result of our election to be regulated as a BDC, we are prohibited under the 1940 Act from knowingly participating in certain transactions with our affiliates without the prior approval of our independent directors or the SEC. The 1940 Act defines “affiliates” broadly to include (i) any person that owns, directly or indirectly, 5% or more of our outstanding voting securities, (ii) any person of which we own 5% or more of their outstanding securities, (iii) any person who directly or indirectly controls us, (iv) our officers, directors and employees, and (v) our Adviser and Subadviser, among others, and we are generally prohibited from buying or selling any security from or to such affiliate, absent the prior approval of our independent directors. The 1940 Act also prohibits “joint” transactions with an affiliate, which could include investments in the same portfolio company (whether at the same or different times), without prior approval of our independent directors. If a person acquires more than 25% of our voting securities, we will be prohibited from buying or selling any security from or to such person, or entering into joint transactions with such person, absent the prior approval of the SEC.

If our investments are deemed not to be Qualifying Assets, we could lose our status as a BDC or be precluded from investing according to our current business plan.

As a result of our election to be regulated as a BDC, we must not acquire any assets other than Qualifying Assets unless, at the time of and after giving effect to such acquisition, at least 70% of our total assets are Qualifying Assets. Qualifying Assets include “eligible portfolio companies.” “Eligible portfolio companies” are generally companies which are organized in the United States, are not investment companies, and which either: (i) do not have securities for which a

- 3 -

broker may extend margin credit, (ii) are controlled by a BDC or a group including a BDC, (iii) are solvent and have assets under $4 million and capital and surplus of at least $2 million, or (iv) (A) do not have a class of securities listed on a national securities exchange, or (B) do have a class of securities listed on a national securities exchange, but have a market capitalization below $250,000,000.

If, for example, we acquire debt or equity securities from an issuer that has outstanding marginable securities at the time we make such an investment, or if we acquire securities from an issuer which otherwise meets the definition of an eligible portfolio company but we purchase the securities in a public offering, these acquired assets cannot be treated as Qualifying Assets. The failure of an investment to meet the definition of a Qualifying Asset could preclude us from otherwise taking advantage of an investment opportunity we find attractive. In addition, our failure to meet the BDC Qualifying Asset requirements could result in the loss of BDC status, which would significantly and adversely affect our business plan by, among other things, requiring us to register as a closed-end investment company.

Our use of leverage may create conflicts of interest and we are exposed to the risks associated with leverage.

In addition to our outstanding loans discussed below, we may borrow additional money to increase our ability to make investments, though we do not anticipate issuing preferred stock in the next twelve months. Lenders from whom we may borrow money or holders of our debt (or preferred, if issued) securities will have fixed dollar claims on our assets that are superior to the claims of our stockholders, and we may grant a security interest in our assets in connection with our debt. Current and potential lenders will not, however, hold any veto or other power to change any of our policies. In the case of a liquidation event, those lenders or note holders (in addition to holders of preferred stock if we issued such stock) would receive proceeds before our stockholders. Though we presently have no plans to do so, if we incur additional debt, the costs associated with such leverage, including commitment fees and interest (in the case of debt) or issuance and dividend costs (in the case of preferred stock), would be borne entirely by holders of our common stock.

Debt, also known as leverage, magnifies the potential for gain or loss on amounts invested and, therefore, increases the risks associated with investing in our securities. The increased potential of gain through the use of leverage also creates a conflict of interest in that it can encourage our Adviser to increase our assets through leverage in an effort to earn management or incentive fees under the Investment Advisory Agreement between with EAM, effective April 29, 2008 (the “Advisory Agreement”), while our common stockholders would incur the costs of utilizing such leverage and bear the risks associated with the debt. Even though the Company, and therefore its common stockholders, would bear the risks and expenses of leverage, the incentive fees payable to the Adviser will not be directly reduced by any interest expense associated with such leverage.

Leverage is generally considered a speculative investment technique. If the value of our assets increases, then leveraging would cause the net asset value attributable to our common stock to increase more than it otherwise would had we not leveraged. Conversely, if the value of our assets decreases, leveraging would cause the net asset value attributable to our common stock to decline more than it otherwise would have had we not leveraged. If an asset purchased with leverage declines in value, the fact that we incurred leverage to finance the purchase of such asset will compound the decrease in our net assets attributable to our common stock and could eliminate our equity in such investment. Similarly, any increase in our revenue in excess of interest expense on our borrowed funds would cause our net income to increase more than it would without the leverage. Any decrease in our revenue would cause our net income to decline more than it would have had we not borrowed funds and could negatively affect our ability to make distributions on our common stock. Our ability to service any debt that we incur will depend largely on our financial performance and the performance of our portfolio companies and will be subject to prevailing economic conditions, competitive pressures and risks of default.

MACC had a principal of $3,367,928 on its Term Loan with CRB&T, on September 30, 2010. The Term Loan has a stated maturity date of January 10, 2011 and is subject to a variable interest rate based on an independent index. The current interest rate applicable to the Term loan is 6.0%. It is expected that MACC will enter into an extension of the Term Loan on or about January 10, 2011 which will extend the maturity date of the Term Loan to July 10, 2011.

We have lost money which impacts our ability to operate.

Due to a number of factors, MACC’s assets have declined in the last several years, along with its share price. These results have negatively impacted our ability to raise capital as part of our strategy to increase assets for the New Portfolio in an effort to decrease our per-share expenses. Most recently, our stockholders have not approved alternative capital

- 4 -

raising proposals to fund a New Portfolio investment strategy. Our decline in assets has also hindered our ability to undertake leverage to increase assets and potential returns. Furthermore, our past performance has limited our liquidity and has caused our financial condition to deteriorate. There can be no assurance that our future performance will improve.

Our quarterly results may fluctuate.

We could experience fluctuations in our quarterly operating results due to a number of factors, including the interest rates payable on the debt investments or the dividend rates on the equity investments we make, the default rates on such investments, the level of our expenses, variations in and the timing of the recognition of realized and unrealized gains or losses and the degree to which we encounter competition in our markets and general economic conditions. As a result of these factors, results for any period should not be relied upon as being indicative of performance in future periods.

Our portfolio may be concentrated in a limited number of portfolio companies.

Our Existing Portfolio consists of a limited number of portfolio companies, and if we raise assets, our New Portfolio may be invested in a small number of issuers. One or two of our portfolio companies may constitute a significant percentage of our total portfolio, especially in the months following any equity offering we commence. An inherent risk associated with such investment concentration is that we may be adversely affected if one or two of our investments perform poorly or if we need to write down the value of any one investment. Financial difficulty on the part of any single portfolio company will expose us to a greater risk of loss than would be the case if we were a more “diversified” company holding numerous investments.

When we are a debt or minority equity investor in a portfolio company, we may not be in a position to control or significantly influence that portfolio company.

When we make minority equity investments or invest in debt, we will be subject to the risk that a portfolio company may make business decisions with which we may disagree, and that the stockholders and management of such company may take risks or otherwise act in ways that do not serve our interests. As a result, a portfolio company may make decisions that could decrease the value of our investments.

Changes in laws or regulations or in the interpretations of laws or regulations could significantly affect our operations and cost of doing business.

We are subject to federal, state and local laws and regulations and are subject to judicial and administrative decisions that affect our operations, including loan originations, maximum interest rates, fees and other charges, disclosures to portfolio companies, the terms of secured transactions, collection and foreclosure procedures and other trade practices. If these laws, regulations or decisions change, we may have to incur significant expenses in order to comply, or we may have to restrict our operations. In addition, if we do not comply with applicable laws, regulations and decisions, or fail to obtain licenses that may become necessary for the conduct of our business, we may be subject to civil fines and criminal penalties, any of which could have a material adverse effect upon our business, results of operations or financial condition.

RISKS RELATED TO OUR BUSINESS

We operate in a highly competitive market for investment opportunities.

Although the Existing Portfolio is static, we compete with public and private funds, commercial and investment banks and commercial financing companies to make the types of investments that we make. Many of our competitors are substantially larger and have considerably greater financial, technical and marketing resources than us. For example, some competitors may have a lower cost of funds and access to funding sources that are not available to us. In addition, some of our competitors may have higher risk tolerances or different risk assessments, allowing them to consider a wider variety of investments and establish more relationships than us. Furthermore, many of our competitors are not subject to the regulatory restrictions that the 1940 Act imposes on us as a result of our election to be regulated as a BDC.

- 5 -

Closed-end investment companies’ shares usually trade below net asset value.

Shares of closed-end investment companies like MACC frequently trade at a discount from net asset value and MACC’s shares have historically traded at a discount from net asset value. At September 30, 2010, MACC’s shares traded at a 65% discount to their net asset value on the OTCQB (as discussed in Item 5). This characteristic of shares of closed-end investment companies is separate and distinct from the risk that our per share net asset value will decline. In addition, due to the following reasons, MACC is not only different from other closed-end funds, but is at greater risk than similar venture capital closed-end funds.

|

|

● |

First, many closed-end funds generally are structured to produce annual dividends to shareholders. MACC, however, has not paid dividends but, rather, retained all income after taxes and expenses to reduce debt or fund additional investments and thus create capital appreciation. The return to holders of MACC’s common stock is thus anticipated to be long-term and capital in nature.

|

|

|

● |

Second, due to several factors, including the small size of MACC relative to fixed expenses, and the fact that much of the income of MACC arises through capital gains rather than ordinary income, MACC has lost money (that is, had net investment expense, rather than net investment income) in each of the last seven years. Many similar funds are structured to earn sufficient current income to achieve operating income (investment income in excess of operating expenses) each year.

|

|

|

● |

Third, at MACC’s annual shareholder meeting held on November 30, 2010, shareholders voted against giving MACC the ability to raise additional capital through the issuance of shares of common stock at a price below MACC’s then-current net asset value per share. In addition, shareholders voted against allowing MACC the ability to issue warrants, options or rights to subscribe for or convert into common stock. Without these authorizations to sell shares at below net asset value or issue options or warrants, MACC’s ability to raise funding through the capital markets is highly unlikely.

|

We may not be able to elect pass-through tax treatment in the future.

Currently, MACC is a taxable entity (a “C corporation”) in order to utilize net operating loss carryforwards generated from a predecessor company as well as its operating losses. In the future, depending on the ability to operate as a going concern, MACC may elect to qualify for pass-through tax treatment contained in Subchapter M of the Internal Revenue Code of 1986, as amended (“Code”). Subchapter M allows certain income to be taxed at the shareholder level only without incurring tax at the corporate level, although MACC may be subject to a corporate level tax on certain built-in gains in existence at the time MACC would first become subject to Subchapter M. It is possible that, for a number of reasons, MACC may be unable to meet Subchapter M requirements, or that it may also cease to qualify for pass-through treatment, or be subject to a four percent excise tax, if it fails to make certain distributions. Under the 1940 Act, MACC is not permitted to make distributions to shareholders unless it meets certain asset coverage requirements with respect to money borrowed and any senior securities issued. Non-availability of pass-through tax treatment may potentially have a materially adverse effect on the total return, if any, obtainable from an investment in MACC’s shares, once net operating loss carryforwards are no longer available and the Subchapter M election has become advantageous.

We are dependent upon our Adviser’s and Subadviser’s key personnel for our future success.

We depend on the diligence, expertise and business relationships of our Adviser and Subadviser. If we commence investing in the New Portfolio, the Adviser will evaluate, negotiate, structure, monitor, and close our investments, subject to supervision by the MACC Board of Directors (the “Board”). Our advisory agreements with EAM and InvestAmerica are short-term in nature and subject to cancellation on sixty days’ notice. Our future success will depend on the continued service of certain key individuals of the Adviser and Subadviser. The departure of one or more of these key individuals could have a material adverse effect on our ability to achieve our investment objectives and on the value of our common stock. We will rely on certain employees of the Adviser and Subadviser, who may devote significant amounts of their time to their respective activities that are not related to MACC. To the extent those employees of the Adviser and Subadviser who are not committed exclusively to us are unable to, or do not, devote sufficient amounts of their time and energy to our affairs, our performance may suffer.

- 6 -

Potential significant conflicts of interest may impact our investment returns.

All of our officers also serve in similar capacities with EAM, which serves as an investment adviser to other accounts, and in the future may serve as investment adviser to other investment funds. In that case, our officers may have obligations to investors in those entities, the fulfillment of which might not be in the best interests of MACC or its stockholders or that may require them to devote time to services for such other entities, which could interfere with the time available to provide services to MACC. Nonetheless, EAM is of the opinion that any such efforts of its officers relative to MACC would be synergistic with and beneficial to the affairs of both MACC and EAM. InvestAmerica and its affiliates also serve as investment advisers to other funds. It is possible that, through the course of identifying and structuring potential New Portfolio investments, EAM may be presented with investment opportunities which could benefit certain investors in the portfolio company to the detriment of our stockholders. For example, if we overvalue a portfolio company investment, our investment could benefit a portfolio company investor by providing capital to the company, and thus its investors, at below market rates.

While EAM intends to allocate investment opportunities in a fair and equitable manner (i.e., pro-rata among its accounts) consistent with our investment objective and strategies, and in accordance with its written allocation procedures so that we will not be disadvantaged in relation to any other client, EAM’s services under the Advisory Agreement are not exclusive. Both EAM and InvestAmerica are free to furnish the same or similar services to other entities, including businesses that may directly or indirectly compete with us, provided they notify us prior to agreeing to serve as investment adviser to another entity.

As a result of regulatory restrictions, we are not permitted to invest in any portfolio company in which the Adviser, the Subadviser or any of their respective affiliates currently has an investment. However, under the terms of an exemptive order granted by the SEC, under certain specified circumstances, we may invest (and make follow on investments) in portfolio companies at the same time and on the same terms as InvestAmerica’s affiliates. All such investments will be reviewed by our independent directors to assure conformity to the exemptive order.

In the course of our investing activities, we pay management and incentive fees to EAM and InvestAmerica. As a result, holders of our common stock invest on a “gross” basis and receive distributions on a “net” basis after expenses, resulting in, among other things, a lower rate of return than one might achieve through direct investments in our portfolio companies. Because of this arrangement, there may be times when the management teams of either EAM or InvestAmerica have interests which differ from those of our stockholders, giving rise to a conflict. For example, if we borrow money or issue debt instruments and thereby increase our assets, which in turn increases the management fee payable to our Adviser, we simultaneously increase our expenses to service such debt and thereby reduce our stockholders’ return on their investment in MACC. Further, the use of leverage increases the likelihood of gain (or loss) which amounts would be subject to the incentive fee we pay to our Adviser.

The incentive fee payable to our Adviser may create conflicting incentives.

Our Adviser will receive an incentive fee based, in part, upon net realized capital gains on our investments. As a result, our Adviser may have an incentive to pursue investments that are likely to result in capital gains as compared to income-producing securities. Such a practice could result in our investing in more speculative or long term securities than would otherwise be the case, which could result in higher investment losses, particularly during economic downturns or longer return cycles.

Under the Advisory Agreement with EAM, the incentive fee is calculated on a “period to period” basis, meaning that changes in the value of portfolio investments in subsequent periods do not retroactively affect incentive fee calculations from prior periods. Further, the Advisory Agreement empowers EAM with the discretion to determine when MACC should dispose of portfolio investments. This formula and authority granted to EAM presents a conflict of interest in that it could prompt EAM to concentrate realized gains or losses in one performance measuring period in an effort to maximize that period’s gain (or another period’s loss), and therefore maximize the incentive fee payment for such period, when MACC would be able to achieve greater gains if they were realized in different periods. In addition to duties imposed on EAM by the 1940 Act and other laws, under the terms of the Advisory Agreement, the Board of Directors has the responsibility to monitor the value of MACC’s portfolio consistent with MACC’s Valuation Procedures. These responsibilities include the appropriateness of and the timing of recognizing unrealized depreciation, reversals of unrealized depreciation, and capital losses and gains, which serves to mitigate the inherent conflict associated with the Adviser’s interest in enhancing the amount of net capital gains with respect to the calculation of the incentive fee.

- 7 -

Our common stock price may be volatile.

The trading price of our common stock may fluctuate substantially. The price of the common stock may be higher or lower than the price you pay for your shares, depending on many factors, some of which are beyond our control and may not be directly related to our operating performance. Additionally, we are no longer listed on NASDAQ and quotations of our stock on the OTCQB (as discussed in Item 5.) may not be indicative of our operating performance. These factors include, but are not limited to, the following:

|

|

● price and volume fluctuations in the overall stock market from time to time;

|

|

|

● significant volatility in the market price and trading volume of securities of BDCs or other financial services companies;

|

|

|

● changes in laws or regulatory policies or tax guidelines with respect to BDCs or regulated investment companies;

|

|

|

● actual or anticipated changes in our earnings or fluctuations in our operating results or changes in the expectations of securities analysts;

|

|

|

● risks associated with possible disruption in our operations due to terrorism;

|

|

|

● general economic conditions and trends;

|

|

|

● loss of a major funding source;

|

|

|

● departures of key personnel; or

|

|

|

● other risks and uncertainties as may be detailed from time to time in our public announcements and SEC filings.

|

Risks Related to the Existing Portfolio

Our Existing Portfolio investments are recorded at fair value as determined in good faith by our Board. As a result, there is and will continue to be uncertainty as to the value of our portfolio investments.

Pursuant to the requirements of the 1940 Act, substantially all of our Existing Portfolio investments are recorded at fair value as determined in good faith by our Board on a quarterly basis, and, as a result, there is uncertainty regarding the value of our portfolio investments. At September 30, 2010, approximately 96% of our total assets represented investments recorded at fair value. Since there will typically be no readily ascertainable market value for the investments in our Existing Portfolio, our Board will determine in good faith the fair value of our investments pursuant to our valuation policy and a consistently applied valuation process.

There is no single standard for determining fair value in good faith. As a result, determining fair value requires that judgment be applied to the specific facts and circumstances of each portfolio investment while employing a consistently applied valuation process for the types of investments we hold. Unlike banks, we are not permitted to provide a general reserve for anticipated loan losses; we are instead required by the 1940 Act to specifically value each individual investment and record unrealized depreciation for an investment that we believe has lost value, including where collection of a debt security or realization of an equity security is doubtful. Conversely, we record unrealized appreciation if we have an indication that the underlying portfolio company has appreciated in value and, therefore, our security has also appreciated in value, where appropriate. Without a readily ascertainable market value and because of the inherent uncertainty of valuation, fair value of our Existing Portfolio investments determined in good faith by the Board may differ significantly from the values that would have been used by another party or had a ready market existed for the Existing Portfolio investments, and the differences could be material.

We adjust quarterly the valuation of our portfolio to reflect the Board’s determination of the fair value of each Existing Portfolio investment. Any changes in fair value are recorded in our statement of operations as “Net change in unrealized depreciation/appreciation on investments.”

An investment strategy that focuses on privately-held companies presents certain challenges, including the lack of available information about these companies, a dependence upon the talents and efforts of only a few key portfolio company personnel, a greater vulnerability to economic downturns and a greater inability to liquidate our investments in an advantageous manner.

As a BDC, we have invested most of our assets in restricted securities issued by small, private companies, some of which have operated at losses or have experienced substantial fluctuations in operating results. There is generally little or no publicly available information about such companies and we must rely on the diligence of our Investment Adviser and

- 8 -

Subadviser to obtain the information necessary to invest in these companies. If our Adviser and Subadviser are unable to obtain all material information about these companies, including with respect to operational, regulatory, environmental, litigation and managerial risks, our Adviser and Subadviser may not make a fully-informed investment decision, and we may lose some or all of the money invested in these companies. In addition, our Adviser and Subadviser may inappropriately value the prospects of an investment, causing us to overpay for such investment and fail to receive an expected or projected return on its investment.

Typically, for their success, such companies depend on the management talents and efforts of one person or a small group of persons, so that the death, disability or resignation of such person or persons could have a materially adverse impact on them. Moreover, smaller companies frequently have narrower product lines and smaller market shares than larger companies and, therefore, may be more vulnerable to competitors’ actions and market conditions, as well as general economic downturns. Such companies may face intense competition, including competition from companies with greater financial resources, more extensive research and development, manufacturing, marketing and service capabilities, and a larger number of qualified managerial and technical personnel. Because these companies will generally have highly leveraged capital structures, reduced cash flow resulting from an adverse business development, shifts in customer preferences, or an economic downturn or the inability to complete a public offering or other financing may adversely affect the return on, or the recovery of, our investment in them. Investment in such companies therefore involves a high degree of business and financial risk, which can result in substantial losses and, accordingly, should be considered highly speculative. No assurance can be given that some of our investments will not result in substantial or complete losses.

Substantially all of these securities will be subject to legal and other restrictions on resale or will otherwise be less liquid than publicly-traded securities. The illiquidity of these investments may make it difficult for us to sell such investments at advantageous times and prices or in a timely manner. In addition, if we are required to liquidate all or a portion of our portfolio quickly, we may realize significantly less than the value at which we previously have recorded our investments. We also may face other restrictions on our ability to liquidate an investment in a portfolio company to the extent that we or one of our affiliates have material non-public information regarding such portfolio company.

The long-term character of our Existing Portfolio investments may negatively impact their current return and capital gains.

Our Existing Portfolio investments yield a current return for most of their lives, but generally only produce a capital gain, if any, from an accompanying equity feature (which typically consists of a warrant for the purchase of common equity securities) after five to eight years. Both the current yield and a capital gain must be achieved on most investments in order to meet our investment goals. There can be no assurance that either a current return or capital gain will actually be achieved on our investments.

Our portfolio companies may incur debt that ranks equally with, or senior to, our investments in such companies.

Portfolio companies in which we invest usually will have, or may be permitted to incur, debt that ranks senior to, or equally with, our investments, including debt investments. As a result, payments on such securities may have to be made before we receive any payments on our investments. For example, these debt instruments may provide that the holders are entitled to receive payment of interest or principal on or before the dates on which we are entitled to receive payments with respect to our investments. These debt instruments will usually prohibit the portfolio companies from paying interest on or repaying our investments in the event and during the continuance of a default under such debt. In the event of insolvency, liquidation, dissolution, reorganization or bankruptcy of a portfolio company, holders of debt instruments ranking senior to our investment in that portfolio company would typically be entitled to receive payment in full before we receive any distribution in respect of our investment. After repaying its senior creditors, a portfolio company may not have any remaining assets to use to repay its obligation to us. In the case of debt ranking equally with our investments, we would have to share on an equal basis any distributions with other creditors holding such debt in the event of an insolvency, liquidation, dissolution, reorganization or bankruptcy of the relevant portfolio company.

There may be circumstances where our debt investments could be subordinated to claims of other creditors or we could be subject to lender liability claims.

If one of our Existing Portfolio companies were to go bankrupt, even though we may have structured our interest as senior debt, depending on the facts and circumstances, including the extent to which we actually provided managerial

- 9 -

assistance to that portfolio company, a bankruptcy court might recharacterize our debt holding and subordinate all or a portion of our claim to that of other creditors. In addition, lenders can be subject to lender liability claims for actions taken by them where they become too involved in the borrower’s business or exercise control over the borrower. It is possible that we could become subject to a lender’s liability claim, including as a result of actions taken if we actually render significant managerial assistance.

We expect our debt investments will generally be unsecured and even if we make a secured loan, if the assets securing a loan we make decrease in value, we may not have sufficient collateral to cover losses.

Generally, our debt investments in Existing Portfolio companies that we make are unsecured. However, when we take a security interest in the available assets of a portfolio company, there is a risk that the collateral securing our investment may decrease in value over time, may be difficult to sell in a timely manner, may be difficult to appraise and may fluctuate in value based upon the success of the business and market conditions, including as a result of the inability of the portfolio company to raise additional capital, and, in some circumstances, our lien could be subordinated to claims of other creditors. In addition, a deterioration in a portfolio company’s financial condition and prospects, including its inability to raise additional capital, may be accompanied by a deterioration in the value of the collateral for the investment. Moreover, we may not have a first lien position on the collateral. Consequently, the fact that investment is secured does not guarantee that we will receive principal and interest payments according to the investment’s terms or that we will be able to collect on the investment should we be forced to enforce our remedies. In addition, a portion of the assets securing our investment may be in the form of intellectual property, if any, inventory and equipment and, to a lesser extent, cash and accounts receivable. Intellectual property, if any, that is securing our investment could lose value if, among other things, the company’s rights to the intellectual property are challenged or if the company’s license to the intellectual property is revoked or expires. Inventory may not be adequate to secure our investment if our valuation of the inventory at the time we made the loan was not accurate or if there is a reduction in the demand for the inventory. Similarly, any equipment securing our loan may not provide us with the anticipated security if there are changes in technology or advances in new equipment that render the particular equipment obsolete or of limited value or if the company fails to adequately maintain or repair the equipment. Any one or more of the preceding factors could materially impair our ability to recover principal in a foreclosure.

The lack of liquidity in our Existing Portfolio investments may adversely affect our business, and if we need to sell any of our investments, we may not be able to do so at a favorable price. As a result, we may suffer losses.

The Existing Portfolio generally consists of investments in debt securities with terms of two to ten years, which we generally hold until maturity, and we do not expect that our related holdings of equity securities in the Existing Portfolio will provide us with liquidity opportunities in the near-term. The illiquidity of these investments may make it difficult for us to sell these investments when desired. In addition, if we are required to liquidate all or a portion of our portfolio quickly, we may realize significantly less than the value at which we had previously recorded these investments. As a result, we do not expect to achieve liquidity in our investments in the near-term. However, to maintain our election to be regulated as a BDC, we may have to dispose of investments if we do not satisfy one or more of the applicable criteria under the 1940 Act. Our investments are usually subject to contractual or legal restrictions on resale or are otherwise illiquid because there is no established trading market for such investments. The illiquidity of a majority of our investments may make it difficult for us to dispose of them at a favorable price, and, as a result, we may suffer losses.

We will be exposed to risks associated with changes in interest rates.

Generally, when market interest rates rise, the values of debt securities decline, and vice versa. During periods of declining interest rates, the issuer of a security may exercise its option to prepay principal earlier than scheduled, forcing us to reinvest in lower yielding securities. This is known as call or prepayment risk. Lower grade securities frequently have call features that allow the issuer to repurchase the security prior to its stated maturity. An issuer may redeem a lower grade obligation if the issuer can refinance the debt at a lower cost due to declining interest rates or an improvement in the credit standing of the issuer.

To protect or maintain our portfolio investments, we may need to increase our investments in portfolio companies.

Following our initial investment, we may make additional debt and equity investments in portfolio companies (“follow-on investments”) to increase our investment in a successful portfolio company, to exercise securities that were

- 10 -

acquired in the original financing, to preserve our proportionate ownership when a subsequent financing is planned or to protect our initial investment when such portfolio company’s performance does not meet expectations.

There is no assurance that we will make, or will have sufficient funds to make, follow-on investments. Additionally, we are subject to limitations relating to our BDC status which may limit our ability to make additional investments in portfolio companies. Any decisions not to make a follow-on investment or any inability on our part to make such an investment may have a negative impact on a portfolio company in need of such an investment, may result in a missed opportunity for us to increase our participation in a successful operation, or may reduce the expected yield on the investment.

At our annual shareholder meeting held on November 30, 2010, shareholders voted against giving us the ability to raise additional capital through the issuance of shares of common stock at a price below our then-current net asset value per share. In addition shareholders voted against allowing us the ability to issue warrants, options or rights to subscribe for or convert into common stock. Without these authorizations to sell shares at below net asset value or issue options or warrants, our ability to raise funding through the capital markets is highly unlikely.

Item 1B. Unresolved Staff Comments

None.

- 11 -

Item 2. Properties.

MACC does not own or lease any properties or other tangible assets. Its business premises and equipment are furnished by EAM. EAM is compensated for its provision of the business premises and equipment to MACC through the management fees paid by MACC to EAM.

Item 3. Legal Proceedings.

There are no items to report.

Item 4. (Removed and Reserved).

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Shareholders

MACC had 1,706 record holders of its common stock at October 15, 2010. MACC does not currently have an equity compensation plan.

Dividends

MACC has no history of paying cash dividends and during fiscal year 2010 MACC did not declare a dividend payment. The payment of dividends, if any, in the future is within the discretion of the Board and will depend upon MACC's earnings, capital requirements, financial condition and other relevant factors. MACC does not presently have any type of dividend reinvestment plan.

Market Prices

The common stock of MACC is traded on the over-the-counter market through the Over-The-Counter Quotation Board (“OTCQB”) under the symbol “MACC.PK.” At the close of business on December 15, 2010, the bid price for shares of MACC's common stock was $0.85. The following high and low bid quotations for the shares during each quarterly period ended on the date shown below of MACC's fiscal years 2010 and 2009 were taken from quotations provided to MACC by the National Association of Securities Dealers Automated Quotation (“NASDAQ”) where MACC traded under the symbol “MACC” until September 15, 2010:

|

High

|

Low

|

|||

|

September 30, 2008

|

$

|

2.16

|

1.20

|

|

|

December 31, 2008

|

1.46

|

0.50

|

||

|

March 31, 2009

|

0.84

|

0.52

|

||

|

June 30, 2009

|

1.74

|

0.40

|

||

|

September 30, 2009

|

1.15

|

0.65

|

||

|

December 31, 2009

|

0.96

|

0.40

|

||

|

March 31, 2010

|

0.90

|

0.52

|

||

|

June 30, 2010

|

0.77

|

0.54

|

||

|

September 30, 2010*

|

1.02

|

0.49

|

||

- 12 -

*MACC began trading on the OTCQB effective September 15, 2010.

Such over-the-counter market quotations reflect inter-dealer prices without retail markup, markdown or commission and may not represent actual transaction.

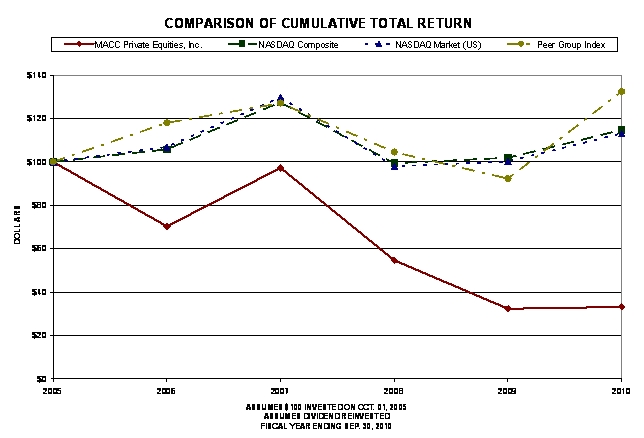

Moreover, below is a chart comparing the semi-annual percentage change in cumulative stockholder return on the Common Stock of MACC since September 30, 2004, with the cumulative total return over the same period of (i) the NASDAQ Stock Market Total Return Index (U.S. Companies), and (ii) MACC’s peer group selected in good faith by MACC and which it composed of the following ten business development companies or other funds known by MACC to have similar investment objectives to the Corporation: Ares Capital Corporation (ARCC), Brantley Capital Corporation (BBDC), Capital Southwest Corp (CSWC), Equus Total Return Inc. (EQS), Gladstone Investment Corporation (GAIN), Harris & Harris Group, Inc. (TINY), MVC Capital (MVC), NGP Capital Resources Company (NGPC), Rand Capital Corp (RAND), and Winfield Capital Corp (WCAP) (the “Peer Group”).

In the graph, the comparison assumes $100 was invested on October 1, 2005, in shares of MACC’s Common Stock and in each of the indices. The comparison is based upon the closing market bid price for shares of MACC’s Common Stock, and assumes the reinvestment of all dividends, if any. The returns of each of the companies in the Peer Group are weighted according to the respective company’s stock market capitalization at the beginning of each period for which a return is indicated.

- 13 -

Item 6. Selected Financial Data.

Selected Financial Data for Fiscal Years ended September 30:

|

2010

|

2009

|

2008

|

2007

|

2006

|

||||||

|

Investment expense, net

|

$

|

(774,214)

|

(576,810)

|

(447,791)

|

(786,487)

|

(1,171,152)

|

||||

|

Net realized (loss)gain on investments

|

(3,185,785)

|

(2,444,130)

|

687,269

|

1,351,456

|

3,645

|

|||||

|

Net change in unrealized depreciation/ appreciation

on investments

|

2,098,690

|

395,347

|

(1,294,629)

|

(662,393)

|

(879,234)

|

|||||

|

Realized loss on other assets

|

---

|

---

|

(30,678)

|

---

|

---

|

|||||

|

Net change in net assets from operations

|

$

|

(1,861,309))

|

(2,625,593)

|

(1,085,829)

|

(97,424)

|

(2,046,741)

|

||||

|

Net change in net assets from operations per common share

|

(0.761)

|

(1.061)

|

(0.441)

|

(0.041)

|

(0.831)

|

|||||

|

Total assets

|

$

|

9,574,785

|

12,516,519

|

15,313,877

|

18,008,787

|

22,830,055

|

||||

|

Total long term debt

|

$

|

3,367,928

|

4,618,659

|

4,750,405

|

6,108,373

|

10,790,000

|

1 Computed using 2,464,621 shares outstanding at September 30, 2010, September 30, 2009, September 30, 2008, September 30, 2007 and September 30, 2006.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operation.

Overview and Looking Ahead

Fiscal year 2010 was another challenging year for MACC. MACC’s stated plan for fiscal year 2010 was to make no new investments in its legacy investment strategy, continue to harvest the value of the investments within the Existing Portfolio, repay its outstanding debt, execute a rights offering and begin making investments in the new portfolio strategy under EAM. Although capital markets in general have continued to improve, the Company and many of its portfolio companies continue to feel the effects of the severe disruptions of the capital markets and economy from 2008 and 2009. Only one Existing Portfolio company was sold during the year while certain portfolio assets were written down to reflect the deterioration of performance of those portfolio companies. MACC also was unable to execute a rights offering and therefore no additional capital was raised to allow for the initiation of the New Portfolio strategy under EAM. The Board has extended the existing advisory agreements while the Board evaluates and examines the future direction of the Company.

MACC continued to experience pressure on its operating cashflow in 2010 as income from existing portfolio assets were insufficient to cover operating expenses. Proceeds from the portfolio sale were applied to outstanding debt and toward operating cashflow needs. MACC’s investment advisor, EAM, continued to voluntarily waive its portion of the management fee in recognition of the fact that the new portfolio strategy continued to be on hold and to help alleviate MACC’s cashflow difficulties.

Operating expenses have been funded primarily from the sale of a portfolio company, dividends, interest and other distributions from MACC’s portfolio companies and from MACC’s bank financing. MACC continues to have an ongoing need to raise cash from portfolio sales to fund operations and pay down outstanding debt.

- 14 -

At the Company’s annual shareholder meeting held on November 30, 2010, shareholders voted against giving the Company the ability to raise additional capital through the issuance of shares of Company common stock at a price below its then-current net asset value per share or the ability to issue warrants, options or rights to subscribe for or convert into Company common stock. Without the authorization to sell shares at below net asset value, the Company’s ability to raise funding through the capital markets has become very limited. In addition, at the Company’s annual shareholder meeting shareholders voted against approving the Amended and Restated investment Advisory Agreement between the Company and its current investment adviser, EAM and against approval of the Amended and Restated Subadvisory Agreement with IAIA. The existing advisory agreements have been extended by the Board.

The Board of Directors is evaluating appropriate next steps based on shareholder actions. The Board will continue to review a number of alternatives, including seeking shareholder approval to liquidate. At same time, we will continue to harvest Existing Portfolio assets to continue the repayment of our outstanding debt.

At September 30, 2010, MACC’s note payable with CRB&T had an outstanding principal amount of $3,367,928 and was due and payable January 10, 2011. On December 13, 2010, the Company paid $693,263 to CRB&T (the “Bank”) in the form of a principal payment on the outstanding note payable with the Bank. The payment was made from proceeds of a portfolio company exit transaction and in accordance with the terms outlined in the note payable. Subsequent to the payment, the balance of the note payable on December 13, 2010 was $2,663,029. It is expected that MACC will enter into an extension of the note payable on or about January 10, 2011 which will extend the maturity date of the Term Loan to July 10, 2011. MACC will need to either extend the due date on the note payable or consider additional sources of financing and additional sales of investments in order to meet current payment and operating requirements. No assurance can be given that MACC will be successful in its efforts to extend its current financing arrangement in the near term and accordingly these facts raise substantial doubt about MACC’s ability to continue as a going concern.

MACC continues to seek additional cash through future sales of portfolio equity and debt securities. Absent financing amendments to the current note payable or additional sources of financing, current working capital and cash will not be adequate for operations at their current levels. If such efforts are not successful, MACC may need to liquidate its current investment portfolio, to the extent possible, which could result in significant realized losses due to the current economic conditions. No assurance can be given that MACC will be successful in its efforts to extend its current financing arrangement in the near term and accordingly these facts raise substantial doubt about MACC’s ability to continue as a going concern.

RESULTS OF OPERATIONS

MACC’s primary activities in 2010 were consistent with the legacy portfolio strategy. MACC made no investments in new portfolio companies and focused on selling Existing Portfolio assets while closely monitoring and reducing where possible current expenses. Total investment income includes income from interest and dividends. Investment expense, net represents total investment income minus net operating expenses. The main objective of portfolio company investments is to achieve capital appreciation and realized gains in the portfolio. These gains and losses are not included in investment expense, net and are reported as separate line items.

Fiscal 2010, Fiscal 2009 and Fiscal 2008

| For the years ended

September 30,

|

|||||||

| 2010 | 2009 | 2008 | |||||

| Total investment income | $ | 395,339 | 586,989 | 955,563 | |||

| Total operating expenses | (1,169,553 | ) | (1,163,799 | ) | (1,403,354 | ) | |

| Investment expense, net | (774,214 | ) | (576,810 | ) | (447,791 | ) | |

|

Net realized (loss) gain on investments

|

(3,185,785 | ) | (2,444,130 | ) | 687,269 | ||

| Net unrealized appreciation (depreciation) on

investments

|

2,098,690 | 395,347 | (1,294,629 | ) | |||

| Realized loss on other assets | --- | --- | (30,678 | ) | |||

| Net (loss) gain on investments and other assets | (1,087,095 | ) | (2,048,783 | ) | (638,038 | ) | |

| Net change in net assets from operations | $ | (1,861,309 | ) | (2,625,593 | ) | (1,085,829 | ) |

| Net asset value: | |||||||

| Beginning of year | 3.17 | 4.23 | 4.67 | ||||

| End of year | 2.41 | 3.17 | 4.23 | ||||

- 15 -

Total Investment Income

During the fiscal year ended September 30, 2010, total investment income was $395,339, a decrease of 33% from fiscal year 2009 total investment income of $586,989. The decrease during the current year was the net result of a decrease in interest income of $180,816, or 46%, and a decrease in dividend income of $3,181, or 2%. The decrease in interest income primarily relates to the repayments of principal on debt portfolio securities, one debt portfolio security which has been placed on non-accrual status during fiscal year 2010, and one debt portfolio security for which the prior period interest accrual has been reserved. This decrease was offset as one debt portfolio security began paying interest in 2010, that had been on non-accrual status in 2009. Dividend income for fiscal year 2010 represents dividends received on three existing portfolio companies, one of which was a distribution from a limited liability company, as compared to dividends received on three portfolio companies, two of which were distributions from limited liability companies, during fiscal year 2009. The timing and amount of dividend income is difficult to predict.

During the fiscal year ended September 30, 2009, total investment income was $586,989, a decrease of 39% from fiscal year 2008 total investment income of $955,563. The decrease during the current year was the net result of a decrease in interest income of $209,156, or 35%, and a decrease in dividend income of $167,065, or 47%. MACC attributes the decrease in interest income primarily to the repayments of principal on debt portfolio securities and on two debt portfolio securities which have been placed on non-accrual of interest status during fiscal year 2009. Dividend income for fiscal year 2009 represents dividends received on three existing portfolio companies, two of which were distributions from limited liability companies, as compared to dividends received on four portfolio companies, two of which were distributions from limited liability companies, during fiscal year 2008. The timing and amount of dividend income is difficult to predict.

Net Operating Expenses

Net operating expenses of MACC increased by 1% in fiscal year 2010 to $1,169,553 from $1,163,799 in fiscal year 2009. The relative increase in net operating expenses is the net result of decreases of $45,041, or 15%, in interest expense, $109,190, or 49%, in management fees (after considering fee waivers), and increases of $129,976, or 43%, in professional fees, and $20,009, or 6%, in other operating expenses. Interest expense decreased due to a decrease in the principal balance of the Note Payable with Cedar Rapids Bank & Trust Company in fiscal year 2010 as compared to fiscal year 2009. Management fees decreased due to the investment adviser, Eudaimonia Asset Management, LLC (“EAM”), having voluntarily waived its management fee of 1% of net assets, effective in May 2009, for an indefinite period. The remaining 1% of the management fee continues to be paid to our subadviser, InvestAmerica Investment Advisors, Inc. (“InvestAmerica”). Professional fees increased primarily due to the legal costs in 2010 compared to 2009 where the costs were related to various capital raising initiatives of the Company. Other operating expenses increased due to the write off of deferred costs associated with our unsuccessful efforts to gain approval for a rights offering partially offset by a decrease in directors fees due to fewer Board of Director meetings held in fiscal 2010.

Net operating expenses of MACC decreased by 17% in fiscal year 2009 to $1,163,799 from $1,403,354 in fiscal year 2008. The relative decrease in net operating expenses is the net result of decreases of $104,381, or 26%, in interest expense, $58,653, or 21%, in management fees, $69,401, or 18%, in professional fees, and $7,120, or 2%, in other operating expenses. Interest expense decreased due to a combination of the decrease in the interest rate and the principal balance of the Note Payable with the Bank in fiscal year 2009 as compared to fiscal year 2008. Management fees decreased due to the investment adviser, EAM, having voluntarily waived its management fee of 1% of net assets, effective in May, for an indefinite period. The remaining 1% of the management fee continues to be paid to our subadviser, InvestAmerica. Professional fees decreased primarily due to the absence of legal costs in 2009 compared to 2008 where the costs were related to changes in the investment advisory structure, the merger and exploration of capital raising options.

- 16 -

Investment Expense, Net