Attached files

| file | filename |

|---|---|

| EX-32.1 - EX-32.1 - Astex Pharmaceuticals, Inc | a10-22648_1ex32d1.htm |

| EX-31.1 - EX-31.1 - Astex Pharmaceuticals, Inc | a10-22648_1ex31d1.htm |

| EX-31.2 - EX-31.2 - Astex Pharmaceuticals, Inc | a10-22648_1ex31d2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

(Amendment No. 1)

|

x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

For the Fiscal Year Ended December 31, 2009 |

|

|

|

|

|

OR |

|

|

|

|

|

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 0-27628

SUPERGEN, INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

91-1841574 |

|

(State or other jurisdiction |

|

(IRS Employer |

|

of incorporation or organization) |

|

Identification Number) |

|

4140 Dublin Blvd., Suite 200, Dublin, CA |

|

94568 |

|

(Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including area code: (925) 560-0100

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class: |

|

Name of each exchange on which registered: |

|

Common Stock, $0.001 par value per share |

|

The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer o |

|

Accelerated filer x |

|

|

|

|

|

Non-accelerated filer o |

|

Smaller reporting company o |

|

(do not check if a smaller reporting company) |

|

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x.

The aggregate market value of the voting stock held by non-affiliates of the Registrant (based on the closing sale price of the Common Stock as reported on the Nasdaq Stock Market on June 30, 2009, the last business day of the Registrant’s most recently completed second fiscal quarter) was approximately $117,441,154. This determination of affiliate status is not necessarily a conclusive determination for other purposes. The number of outstanding shares of the Registrant’s Common Stock as of the close of business on March 5, 2010 was 60,215,632.

DOCUMENTS INCORPORATED BY REFERENCE

Items 10, 11, 12, 13 and 14 of Part III incorporate by reference information from the definitive proxy statement for the Registrant’s Annual Meeting of Stockholders.

EXPLANATORY NOTE

SuperGen, Inc. (“SuperGen,” the “Company,” “we,” “us,” or “our”) is filing this Amendment No. 1 on Form 10-K/A (“Amendment”) to its Annual Report on Form 10-K for the year ended December 31, 2009, as filed with the Securities and Exchange Commission on March 15, 2010 (“Form 10-K”).

We are filing this Amendment to re-file the complete text of those items for which we have included supplemental information, as follows:

· Part I, Item 1, Business — our “Patents and Proprietary Technology” section has been supplemented with additional information about our patents;

· Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations — our “Results of Operations” section has been supplemented with additional information about our research and development expenses;

· Part II, Item 9A, Controls and Procedures, has been modified to include additional language;

· Part III, Item 11, Executive Compensation, has been modified to include supplemental information in the Compensation Discussion and Analysis section, as well as a revised Summary Compensation Table.

This Amendment contains currently dated certifications of our Chief Executive Officer and Chief Financial Officer.

This Amendment does not reflect events occurring after the filing of the Form 10-K, or after the filing of the definitive Proxy Statement for our 2010 Annual Meeting of Stockholders, as filed with the Securities and Exchange Commission on April 30, 2010 (the “Proxy Statement”), and does not update disclosures contained in either the Form 10-K or Proxy Statement, or modify or amend the Form 10-K or Proxy Statement except as specifically described in this explanatory note.

SUPERGEN, INC.

2009 ANNUAL REPORT ON FORM 10-K/A

AMENDMENT NO. 1

|

|

|

Page |

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

17 |

|

|

27 |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

29 |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

46 |

||

|

|

|

|

|

S-1 |

||

Special Note Regarding Forward-Looking Statements

Our disclosure and analysis in this report contain forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act, and within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements provide our current expectations or forecasts of future events. When we use the words “anticipate,” “estimate,” “project,” “intend,” “expect,” “plan,” “believe,” “should,” “likely” and similar expressions, we are making forward-looking statements. In particular, these statements include statements such as: our estimates about profitability; our forecasts regarding our revenues and research and development expenses; and our statements regarding the sufficiency of our cash to meet our operating needs. Our actual results could differ materially from those predicted in the forward-looking statements as a result of risks and uncertainties including, but not limited to, delays and risks associated with conducting and managing our clinical trials; the commercial success of Dacogen; developing products and obtaining regulatory approval; our ability to establish and maintain collaboration relationships; competition; our ability to protect our intellectual property; our expectations about the joint development program with GSK; our dependence on third party suppliers; risks associated with the hiring and loss of key personnel; adverse changes in the specific markets for our products; and our ability to launch and commercialize our products. Certain unknown or immaterial risks and uncertainties can also affect our forward-looking statements. Consequently, no forward-looking statement can be guaranteed and you should not rely on these forward-looking statements.

The forward-looking statements reflect our position as of the date of this report, and we undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise. You are advised, however, to consult any further disclosures we make on related subjects in our Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, or other filings. Also note that we provide a cautionary discussion of risks and uncertainties relevant to our business under Item 1A—Risk Factors in this report. These are currently known and material risks that we believe could cause our actual results to differ materially from expected and historical results. Other unknown and immaterial risks besides those listed in this report could also adversely affect us.

We incorporated in March 1991 as a California corporation and changed our state of incorporation to Delaware in May 1997. Our executive offices are located at 4140 Dublin Blvd., Suite 200, Dublin, CA, 94568 and our telephone number at that address is (925) 560-0100. We maintain a website on the internet at www.supergen.com. This is a textual reference only. We do not incorporate the information on our website into this annual report on Form 10-K, and you should not consider any information on, or that can be accessed through, our website as part of this annual report on Form 10-K.

Overview

We are a pharmaceutical company dedicated primarily to the discovery and development of therapies to treat patients with cancer. Historically we acquired products that were developed by other companies and applied additional developmental effort to expand sales or advance these products clinically towards potential approval for marketing. In 2006, Dacogen® (decitabine) for Injection received approval for marketing in the United States, our commercial infrastructure and products were sold, and we acquired a discovery and development company to internally discover and develop our own products. These changes were implemented to mitigate the escalating risk of competitive in-licensing and maximize the return on both existing resources and our incoming royalty and milestone revenue.

Our new drug application (“NDA”) for Dacogen was approved by the United States Food and Drug Administration (“FDA”) in May 2006 for the treatment of patients with myelodysplastic syndromes (“MDS”). In August 2004, we had executed an agreement granting MGI PHARMA Inc. (“MGI”) exclusive worldwide rights to the development, manufacture, commercialization and distribution of Dacogen. In July 2006, MGI executed an agreement to sublicense Dacogen to Janssen-Cilag GmbH, a Johnson & Johnson company, granting exclusive development and commercialization rights in all territories outside North America. Janssen-Cilag companies are responsible for conducting regulatory and commercial activities related to Dacogen in all territories outside North America, while MGI retains all commercialization rights and responsibility for all activities in the United States, Canada and Mexico. MGI was acquired by Eisai Corporation of North America in January 2008.

Our current primary developmental efforts revolve around the products progressing out of our acquisition of Montigen Pharmaceuticals, Inc. (“Montigen”), a small-molecule drug discovery company, in 2006. We initiated Phase I in-human clinical trials in June 2007 and initiated Phase Ib clinical trials in late 2007 for the first Montigen product, amuvatinib (MP-470), a DNA repair suppressor. In early 2009, we initiated clinical trials for a second internally developed product, SGI-1776, a PIM kinase inhibitor.

In October 2009, we entered into a Commercial License and Research Agreement with GlaxoSmithKline (“GSK”). Pursuant to the terms of this agreement, we will collaborate with GSK over a period of five years to discover and develop specific epigenetic therapeutics. At the end of the research term, or earlier if GSK elects, GSK may exercise its option to license from us the compounds that are the result of the joint research effort, in order to continue the development and ultimately commercialize and sell the resulting products worldwide. Upon execution of the agreement, we received an upfront payment of $2 million from GSK, as well as a $3 million investment in shares of our common stock, sold at a 10% premium to market price. GSK is obligated to make certain additional payments to us if and when the compounds reach specified developmental milestones, as well as payments to us if and when the compounds that GSK has licensed achieve certain regulatory milestones. The agreement further provides that, if the licensed compounds derived from the joint research team become products, GSK will pay us sales milestone payments as well as royalties on annual net sales of such products. Total potential development and commercialization milestones payable to us could exceed $375 million. The tiered royalties, into double digit magnitudes, will be paid on a country-by-country and product-by-product basis.

Strategy

We are a pharmaceutical company dedicated to the discovery and development of therapies to treat patients with cancer. Our founding strategy was to acquire rights to late stage clinical products and commercialize these products by executing selective developmental and commercialization strategies that might allow these products to come into the market and be utilized by the widest possible patient populations. The competition for late-stage compounds that can be obtained through licensure or acquisition, that have shown initial efficacy in humans, has increased significantly with most major pharmaceutical companies taking positions in this market. The acquisition of Montigen mitigates the competitive risk of in-licensure and may allow us to out-license selective products to our licensing competitors or other pharmaceutical companies. Our primary objective is to become a leading developer and seller of therapies for patients suffering from cancer. Key elements of our strategy include the following:

Discover and advance into clinical trials at least one product about every twelve to eighteen months. Our drug discovery group has been optimizing our proprietary process called CLIMB™ that allows a small team of chemists and biologists to model difficult or previously unknown cancer targets for computerized drug creation and development. The flexibility and relatively low cost of both human and developmental capital for this type of discovery and development has allowed us to transition from being just a licensee to becoming a potential licensor.

Focus on drug targets that are difficult to screen by traditional methods. Most established pharmaceutical companies use some version of a high through-put screening. However, this methodology does not work well for a wide variety of complex targets. Our modeling process has demonstrated an ability to create lead candidates for these complex targets, including protein-to-protein interaction targets that might be disrupted by small molecules to be used as potential therapeutics.

Capitalize on our existing clinical expertise and regulatory development to maximize the commercial value of our products. Computer and animal models are only modestly predictive of how a product might work in humans. We have acquired significant expertise at planning, managing, and filing clinical data in both the United States and Europe. Proving the concept that a specific drug will translate into an approvable, commercially viable product in humans is a difficult task. Some drug candidates demonstrate this “proof of concept” very early in non-clinical development, while other drug candidates might need to be compared clinically to existing therapies to achieve such a proof of concept. Typically this proof of concept comes in Phase II trials where it is demonstrated that a drug candidate can destroy tumors in specific diseases through a specific process. As product candidates move from non-clinical into Phase I and Phase II clinical studies, the potential value of the drug candidates should increase as the proof of concept is achieved. Historically, products that are in Phase II trials command a higher in-licensing value than products that are still in Phase I trials. We believe our clinical and regulatory expertise facilitates efficient use of our resources to achieve appropriate proof of concept.

CLIMB Discovery Process

Traditional drug discovery processes may require five or more years before presenting a candidate suitable for the clinic. This lengthy timeline leads to high research and development costs. Utilizing our CLIMB platform, we have effectively streamlined the discovery and lead optimization process in order to get potentially life-saving therapeutics to the clinical testing stage of development faster and at a lower cost. CLIMB is SuperGen’s approach to small molecule drug discovery, which merges the rapid screening of compound libraries with computational chemistry and systems biology techniques to identify drug leads that bind to target proteins.

CLIMB is an iterative and evolving process, incorporating techniques from computational design to laboratory bench biology and chemistry, to yield targeted therapeutics for use in the clinic. In traditional small molecule screening, very large physical libraries of millions of compounds may be created and screened in order to identify the few that interact selectively with a disease-related protein target. This approach has worked fairly well for simple or very well characterized targets, but is very time and cost intensive. Since CLIMB works with a virtual library of compounds and compound fragments to screen against target models, we can screen up to three million virtual compounds per day against very complex targets.

CLIMB has been used to create models and identify products that have exhibited considerable activity while physically screening as few as several hundred rationally-selected compounds. This reduces the time from target identification to clinical candidate by several years, and decreases the cost of drug development. As part of CLIMB, our software development team is actively involved in the creation of algorithms to integrate computation, biochemistry, medicinal chemistry and systems biology to improve the predictive properties of our models and streamline the drug discovery process even further.

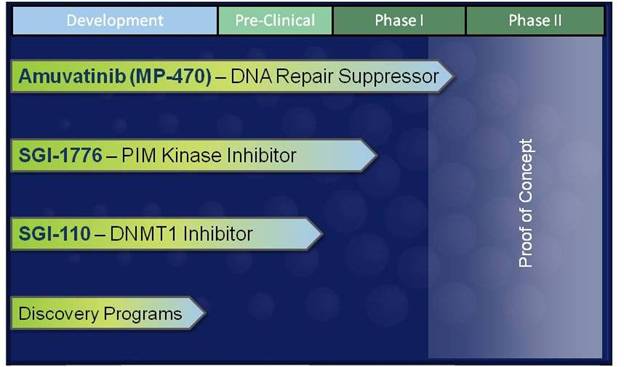

Products in Research and Development

The chart below lists our current products or projects in development:

Amuvatinib (MP-470) — DNA Repair Suppressor

Amuvatinib is a multi-targeted Tyrosine Kinase Inhibitor that is specific for mutant forms of c-kit, PDGFRa, and FLT3. These protein kinase targets are involved in the growth and proliferation of cancer cells. Amuvatinib is also a suppressor of Rad51, a DNA repair protein which is involved in resistance to a variety of chemotherapy agents and radiation. We submitted an Investigational New Drug Application (“IND”) to the FDA in March 2007, and initiated a first-in-human Phase I single agent amuvatinib trial in June 2007.

Amuvatinib has a wide therapeutic window and shows minimal toxicity in the expected therapeutic dose range, despite suppressing several signaling pathways within cells. We have evaluated amuvatinib as a dry powder mix and as a lipid suspension formulation in multiple Phase I studies as a single agent in healthy volunteers and in cancer patients, as well as in combination with five standard of care chemotherapy regimens in different tumor types. Across these studies, over 170 patients/healthy volunteers received at least one dose of amuvatinib. As a single agent in cancer patients, gastrointestinal toxicity was the major adverse event noted at doses up to 1500 mg/day with the dry powder formulation. In the combination trial, preliminary data indicated twelve partial responses and numerous durable stable disease per RECIST criteria, mostly with the paclitaxel/carboplatin and carboplatin/etoposide standard of care chemotherapy regimens in combination with oral amuvatinib. Tumor types demonstrating clinical benefit include neuroendocrine, non-small cell lung, small cell lung, breast and endometrial carcinoma. The safety profile of amuvatinib in combination with standard of care was consistent with historical published data for each chemotherapeutic with no apparent increase in severity or prolongation of reported events.

We completed an additional Phase I pharmacokinetic study in healthy male volunteers to determine the relative bioavailability and define the safety profile of the lipid suspension capsules compared with the dry powder mix capsules. In a randomized, two-way crossover study, exposure levels of amuvatinib following administration of a single dose of the lipid suspension formulation (3 x 30 mg capsules) were higher than those observed following the administration of the single dose dry powder formulation (1 x 100 mg capsule). The relative bioavailability favored the lipid suspension formulation, adjusted for dose, with an overall increase in exposure by twofold.

We are also performing non-clinical studies with collaborators to further our understanding of the mechanisms of amuvatinib in DNA repair pathways, as well as the effects of the drug in combination studies in multiple solid tumor models. Pending full analysis of the responses in the Phase I studies and completion of the ongoing non-clinical programs, we intend to initiate one or more Phase II studies evaluating the safety and efficacy of amuvatinib lipid suspension formulation in tumor types that have demonstrated clinical benefit in the Phase I development program. The initial Phase II study is anticipated to be launched during the second half of 2010.

SGI-1776 — Pim Kinase Inhibitor

Pim kinases are proteins that play a pivotal survival role in cancer cells. Over-expression of Pim kinases in cells prevents programmed cell death that normally occurs when cells malfunction and can lead to unchecked cell survival, or cancer. Our Pim kinase inhibitor, SGI-1776, is a novel, orally administered, small molecule anticancer compound that effectively blocks the pro-survival activity of Pim kinases, allowing these potentially malignant cells to self-abort. Our IND for SGI-1776 received clearance from the FDA in November 2008, and we initiated a Phase I clinical trial to evaluate the safety, tolerability, and pharmacokinetic profile of SGI-1776 in the first half of 2009. The first in-human clinical trial program has enrolled patients with solid tumors with specific emphasis on hormone and docetaxel refractory prostate cancer and refractory non-Hodgkin’s lymphomas. These tumor types have been reported to over-express the Pim kinase family of proteins at a high frequency. Over-expression of Pim-1 kinase has been shown to be a marker of poor prognosis in these tumors. A second Phase I/II study is being planned in patients with refractory acute or chronic myeloid or lymphatic leukemias in which Pim kinases are also over-expressed, and correlated with poor prognosis and drug resistance. This study is anticipated to be launched during the first half of 2010.

SGI-110 — DNMT1 Inhibitor

In normal cells, silencing of unnecessary genes is commonly carried out by DNA methylation through the action of DNA Methyltransferase enzymes. However, this machinery can be usurped during the process of tumorigenesis, resulting in the inactivation of tumor suppressor genes and ultimately cancer. Inhibition of DNMT-1 activity in cancer cells causes the suppressed genes to become unmethylated and re-expressed. These re-expressed tumor suppressor genes interfere with the cancer cells proliferative pathways and lead to cell death. We have developed a compound called SGI-110 which targets and blocks the mechanism by which methylation occurs, thus allowing re-expression of tumor suppressor genes in tumors. SGI-110 is currently in the pre-clinical development stage with an anticipated IND filing in 2010. The initial Phase I/II study will evaluate multiple schedules in relapsed/refractory MDS and acute myeloid leukemia (AML).

Discovery Programs

JAK2 Inhibitor

Janus kinases (JAK) are a family of non-receptor intracellular tyrosine kinases that transduce signaling from type I and II cytokine receptors, which possess no catalytic kinase activity, to the signal transducers and activators of transcription (STAT) proteins which translocate into the nucleus to initiate the growth and

differentiation programs associated with the various receptor cytokine complexes. The JAK/STAT pathways play an important role in a diverse array of cellular processes, including cell survival, proliferation, differentiation and apoptosis. Activation of JAK kinases through mutation or aberrant signaling has been associated with disease progression in immune disorders, myeloproliferative disorders, and cancers.

Axl Inhibitor

Axl kinase is a receptor tyrosine kinase implicated in tumorigenesis. Over-expression of Axl is associated with increased cellular transformation, cell survival, proliferation, migration, angiogenesis, and adhesion. The oncogenic potential of Axl was first discovered in chronic myelogenous leukemia (CML) and has been shown to play a role in the development of acute myelogenous leukemia (AML) and myelodysplasia. Axl kinase is an exciting target for small molecule drug discovery. A series of small molecule inhibitors were discovered and are being developed for potency and selectivity against Axl.

ETK/BMX Inhibitors

Epithelial and endothelial tyrosine kinase (ETK), also known as bone marrow X kinase (BMX), is a nonreceptor tyrosine kinase that plays a central role in the proliferation, differentiation, apoptosis, adhesion, motility, and tumorigenicity of epithelial cells. ETK has been reported to be over-expressed in several aggressive metastatic carcinomas, such as hepatocellular carcinoma, cholangiocarcinoma, and prostate cancer. ETK kinase signals downstream of several important oncogenes, including Src, focal adhension kinase, and phosphatidylinositol 3-kinase and has been shown to be vital to the tumorigenic effects of such proteins. Taken together, these findings suggest ETK is an exciting potential therapeutic target in multiple tumor types. We have designed and developed a novel class of potent small molecule inhibitors with specificity toward ETK. Initial leads from this class of inhibitors have activity against ETK at low nM concentrations in a biochemical ETK kinase assay, and show good selectivity across a diverse panel of kinases.

Products Sublicensed or Sold

Dacogen

In September 2004, we executed an agreement granting MGI exclusive worldwide rights to the development, manufacture, commercialization and distribution of Dacogen. Under the terms of the agreement, MGI made a $40 million equity investment in us and agreed to pay up to $45 million in specific regulatory and commercialization milestones. To date, we have received $32.5 million of these milestones. The Dacogen license has also created for us a royalty income stream on worldwide net sales starting at 20% and escalating to a maximum of 30%.

In July 2006, MGI executed an agreement to sublicense Dacogen to Janssen-Cilag, a Johnson & Johnson company, granting exclusive development and commercialization rights in all territories outside North America. In accordance with our license agreement with MGI, we are entitled to receive 50% of certain payments MGI receives as a result of any sublicenses. We received $5 million, or 50% of the $10 million upfront payment MGI received, and, as a result of both the original agreement with MGI and this sublicense with Janssen-Cilag, we may receive up to $17.5 million in future milestone payments as they are achieved for Dacogen globally. Janssen-Cilag is responsible for conducting regulatory and commercial activities related to Dacogen in all territories outside North America, while MGI retains all commercialization rights and responsibility for all activities in the United States, Canada and Mexico. MGI was acquired by Eisai Corporation of North America in January 2008.

Nipent

We used to sell our drug Nipent in the United States and the European Union (“EU”) for the treatment of hairy cell leukemia, a type of B-lymphocytic leukemia, and it was our principal source of revenue from 1997-2006. We sold the North American rights to Nipent to Mayne Pharma (“Mayne”) in August 2006, and sold the remaining worldwide rights to Nipent to Mayne in April 2007. Mayne was acquired by Hospira, Inc. in February 2007.

Acquisition of New Products and Technologies

We are continually reviewing new product development opportunities in an effort to enhance and create a broader product pipeline for future development.

In 2006, we completed our acquisition of Montigen, a privately held, oncology-focused drug discovery and development company headquartered in Salt Lake City, Utah. Montigen’s assets included its research and development team, a proprietary drug discovery technology platform and optimization process, CLIMB, and late-stage non-clinical compounds. Pursuant to the terms of the merger agreement, we paid the Montigen stockholders a total of $17.9 million upon the closing of the transaction, consisting of $9.0 million in cash and $8.9 million in shares of SuperGen common stock. In April 2007, we paid the former Montigen stockholders a milestone payment of approximately $10.0 million, which was paid in shares of our common stock. In November 2008, we paid the former Montigen stockholders another milestone payment of approximately $5.2 million, which was paid in a combination of approximately $2.8 million in cash and 1.5 million shares of our common stock. We have an obligation to pay the Montigen stockholders an additional $6.8 million in shares of our stock, contingent upon achievement of one additional regulatory milestone.

Research and Development

Because of the stage of our development and the nature of our business, we expend significant resources on research and development activities. We expended $29.7 million in 2009, $32.7 million in 2008, and $23.4 million in 2007 on research and development activities. We conduct research internally and also through collaborations with third parties, and we intend to maintain our strong commitment to our research and development efforts in the future. Our major research and development projects are focused on our drug discovery and non-clinical activities as well as Phase I and Phase Ib clinical trials for amuvatinib and SGI-1776.

Sales and Marketing

We currently have no employees focused on sales, marketing, and sales support. Our marketing efforts are handled by our Corporate Communications and Business Development group.

Manufacturing

We currently outsource manufacturing of all our drug compounds to qualified United States and foreign suppliers. We expect to continue to outsource manufacturing in the near term. We believe our current suppliers will be able to efficiently manufacture our proprietary compounds in sufficient quantities and on a timely basis, maintaining product quality and compliance with FDA and foreign regulations. We maintain oversight of the quality of our third-party manufacturers through ongoing audits, rigorous review, control over documented operating procedures, and thorough analytical testing by qualified, contracted laboratories. We believe that our current strategy of outsourcing manufacturing is cost-effective because we avoid the high fixed costs of plant, equipment, and large manufacturing staffs.

The FDA must approve our drug manufacturing sites and deem a manufacturer acceptable under current good manufacturing practices (“GMPs”) before release of active pharmaceutical ingredients (“API”) and finished dosage forms for clinical testing.

We intend to continue evaluating our manufacturing requirements and may establish or acquire our own facilities to manufacture our products for distribution if doing so would be cost effective or improve control and flexibility of product supply.

Government Regulation: New Drug Development and Approval Process

Regulation by governmental authorities in the United States and other countries is a significant factor in the manufacture and marketing of pharmaceuticals and in our ongoing research and development activities. All of our drug products will require regulatory approval by governmental agencies prior to commercialization. In particular, human therapeutic products are subject to rigorous non-clinical testing, clinical trials, and other pre-marketing approval requirements by the FDA and regulatory authorities in other countries. In the United States, various federal, and in some cases state statutes and regulations, also govern or have an impact upon the manufacturing, safety, labeling, storage, record-keeping and marketing of such products. The lengthy process of seeking required approvals and the continuing need for compliance with applicable statutes and regulations require the expenditure of substantial resources. Regulatory approval, when and if obtained, may be limited in scope which may significantly limit the indicated uses for which a product may be marketed. Further, approved drugs, as well as their manufacturers, are subject to ongoing review and inspections which could reveal previously unknown problems with such products, which may result in restrictions on their manufacture, sale or use or in their withdrawal from the market.

The process for new drug approval has three major stages, discovery, non-clinical and clinical:

Drug discovery. In the initial stages of small molecule drug discovery, potential biological targets are identified, these targets are characterized, and then large numbers of potential compounds are screened for activity. This drug discovery process can take several years. Once a company defines a lead compound, the next steps are to conduct further preliminary studies on the mechanism of action, in vitro (test tube) screening against particular disease targets and some in vivo (animal) screening. If results are satisfactory, the compound progresses from discovery to non-clinical development.

Non-clinical testing. During the non-clinical testing stage, laboratory and animal studies are conducted to show biological activity of the compound against the disease target and the compound is evaluated for safety. These tests can take several years to complete and must be conducted in compliance with Good Laboratory Practice (“GLP”) regulations. If the compound passes these hurdles, animal toxicology studies are initiated. If the results demonstrate acceptable levels of toxicity, the compound emerges from non-clinical testing and moves into the clinical phase.

Clinical testing — The Investigational New Drug Application. After appropriate animal testing is evaluated and the candidate molecule is found to have an acceptable safety profile, we may decide to expand the development programs to a clinical setting. To accomplish this in the United States an IND is submitted to the FDA. IND applications include the known chemistry of the compound, how the compound is manufactured, the results of animal studies and other previous experiments, the method by which the drug is expected to work in the human body, a proposed clinical development plan and how, where and by whom the proposed new clinical studies will be conducted. Health authorities in Europe and the rest of the world require a similar clinical trial application. If the controlling authority does not object, we may initiate human testing. All clinical trials must be conducted in accordance with globally-accepted standards of good clinical practices (“GCPs”). This means we have specific obligations to protect trial subjects and potential patients, monitor the study, collect the data and prepare a report of the study. Clinical trial applications must be updated with new information obtained during the course of the trials.

Clinical protocols must be approved by independent reviewers, referred to as Institutional Review Boards (“IRB”) in the United States and Ethical Committees (“EC”) in Europe. The IRB/EC is charged with providing an independent assessment of the appropriateness of the study, particularly focusing on the safety of the patients that might enroll in the study. The IRB’s/EC’s responsibilities continue while the study is ongoing, focusing on protecting the rights and safety of those enrolled in the study.

We have an obligation to provide progress reports on clinical trials at least annually to the FDA. The FDA may, at any time during a clinical trial, impose a “clinical hold” if it has serious safety concerns about a trial. If this occurs, the clinical trial cannot continue until the FDA is satisfied that it is appropriate to proceed.

Clinical Development Plan. Clinical trials are typically conducted in three sequential phases, but the phases may overlap.

· Phase I clinical trials. After an IND becomes effective, Phase I human clinical trials can begin. These trials generally involve 20 to 40 heavily pre-treated cancer patients who may have a wide variety of cancers and typically take approximately one year to complete. These trials are designed to evaluate a drug’s safety profile and may include studies to assess the optimal safe dosage range. Phase I clinical studies may evaluate how a drug is absorbed, distributed, metabolized and excreted from the body. Phase I studies may be expanded to Phase Ib trials that test the research compound in combination with other agents to define the combined safety and dosing parameters.

· Phase II clinical trials. In Phase II clinical trials, studies are conducted in patients who have the specific targeted disease. The primary purpose of these trials is to demonstrate preliminary efficacy of the drug in the target patient population. These studies typically take a few years to complete. Once trial data is obtained that a specific dose and schedule is creating clinical efficacy that appears to be superior to other treatments, advancement to Phase III can begin.

· Phase III clinical trials. These trials are typically large, involving several hundred or even thousands of patients. Phase III trials typically compare an investigational agent against a control product or the standard of care, which could be a product or treatment already approved for use in that disease. The data generated in these studies are monitored regularly by clinical monitors as well as the participating physician. There are specific requirements for the reporting of any adverse reactions that may result from the use of the drug. Clinical monitors visit the sites regularly and transmit the data back to the company for analysis and ultimately for presentation to the FDA.

Marketing application. Companies have the opportunity to interact with health authorities during the course of a drug development program. Most companies take advantage of this access to gain further insights about the kind of data that will be expected in their marketing application. After completion of the clinical trial phase, a company must compile all of the chemistry, manufacturing, non-clinical and clinical data into a marketing application. In the United States, this is called an NDA; in the EU it is called a Marketing Authorization Application (“MAA”). This is a significant amount of information, often in excess of 100,000 pages, and it will be independently reviewed by these health authorities.

Both the FDA and the European Medicines Evaluation Agency (“EMEA”) review these submissions for overall content and completeness before accepting them for review and may request additional information. Once an application is accepted for filing, each agency independently begins its in-depth review. In both the United States and Europe, there are specified timeframes for the completion of review. This process may be extended if an agency requests additional information or clarification regarding the data provided in the submission.

In the United States, the FDA may refer the application to an appropriate advisory committee for a recommendation as to whether the application should be approved, but the FDA is not bound by this recommendation. The review process concludes with the issuance of a “complete response” letter from the FDA. If FDA evaluations of the NDA and the manufacturing facilities are favorable, the FDA will approve the application. If the FDA’s evaluation of the NDA submission or manufacturing facilities is not favorable, the FDA will reject the application in the complete response. This complete response will describe specific deficiencies, and, when possible, will outline recommended actions the applicant might take to get the application ready for approval. When and if any deficiencies are corrected, and actions are completed to the FDA’s satisfaction, the FDA will issue an approval letter authorizing commercialization of the drug for specific indications. The review and approval process in Europe has substantial similarities to that outlined for the United States.

Marketing approval. Once a health authority grants marketing approval for a drug, it can then be made available in that country or region. Periodic safety reports must be submitted to health authorities as a way to monitor the use of new drugs introduced to the market. Regulatory agencies around the world place great emphasis on pharmacovigilance, the process of monitoring the safety of a drug when it is released for general use, as the real world setting is very different from the controlled environment of clinical trials.

Phase IV clinical trials and post marketing studies. In addition to studies that might have been requested by health authorities as a condition of approval, clinical trials may be conducted to generate more information about the drug after initial approval of the product; including use for additional indications, the use of new dosage forms or new dosing regimens. These studies may generate approved label changes and publications that provide further information to patients and the medical community.

Fast Track. The FDA Modernization Act of 1997 specifies that the FDA can assign a fast track designation to a new drug or biologic product that is intended for the treatment of a serious or life-threatening condition and has the potential to address unmet medical needs for such a condition. Under this program, the sponsoring company may request this designation at any time during the development of the product. The FDA must determine whether the product qualifies within 60 days of receipt of the sponsoring company’s request. For a product designated as fast track, the FDA has the ability to define a faster review, including allowing the sponsor to provide the NDA in discrete sections. This process is called a “rolling” NDA and is intended to accelerate the review and approval process.

Priority Review. This is a designation by the FDA for a review period of 6 months, instead of the standard 10 months defined by federal regulation.

Accelerated Approval. This is a program intended to make promising products for life-threatening diseases available on the market on the basis of preliminary evidence prior to formal demonstration of patient benefit.

Approvals in the European Union. In 1993, the EU established a system for the registration of medicinal products in the EU whereby marketing authorization may be submitted at either a centralized or decentralized level. The centralized procedure is administered by the EMEA and is mandatory for the approval of biotechnology products and is available, at the applicant’s option, for other innovative products. The centralized procedure provides for the granting of a single marketing authorization that is valid in all EU member states. A mutual recognition procedure is available at the request of the applicant for all medicinal products that are not subject to the mandatory centralized procedure, under a decentralized procedure.

Approvals outside of the United States and European Union. Applications to market a new drug product must be made to virtually all countries prior to marketing. The approval procedure and the time required for approval vary from country to country and may involve additional testing and cost. There can be no assurance that approvals will be granted on a timely basis or at all. In addition, pricing approval is required in many countries and there can be no assurance that the resulting prices would be sufficient to generate an acceptable return on investment.

Off-Label Use. Drugs are approved for a specific use (“label use”) that is then set forth in the document (“label”) accompanying the dispensed drug. Physicians may prescribe drugs for uses that are not approved in the product’s label. Such “off-label” prescribing may be used by physicians across medical specialties. The FDA does not regulate the behavior of physicians in their choice of treatments but it does limit a manufacturer’s communications on the subject of off-label use. Companies cannot promote FDA approved drugs for off-label uses, nor can companies promote the use of a drug before it is approved.

Other Government Regulations

As a United States-based company, in addition to laws and regulations enforced by the FDA, we are also subject to regulation by other agencies under the Occupational Safety and Health Act, the Environmental Protection Act, the Toxic Substances Control Act, the Resource Conservation and Recovery Act and other present and potential future federal, state or local laws and regulations. These agencies have specialized responsibilities to monitor the controlled use of hazardous materials such as chemicals, viruses and various radioactive compounds.

Market Exclusivity

The commercial success of a product, once it is approved for marketing, will depend primarily on a company’s ability to create and sustain market share and exclusivity. Market exclusivity can be gained and maintained by a number of methods, including, but not limited to: patents, trade secrets, know-how, trademarks, branding and special market exclusivity provided by regulations.

Orphan Drug Designation

The United States, European Union, Japan and Australia have all enacted regulations to encourage the development of drugs intended to treat rare diseases. Orphan drug designation must be requested before submitting an application for marketing approval. After the granting of an orphan drug designation, the chemical identity of the therapeutic agent and its potential treatment use are disclosed publicly. If and when a product with orphan drug status receives marketing approval for the orphan indication, the product is entitled to marketing exclusivity, which means the regulatory authority may not approve any other applications to market the same drug for the same indication for seven years in the United States, ten years in Europe and Japan and four years in Australia.

Data Exclusivity and Generic Copies

There is an abbreviated regulatory review and approval process for a generic copy of an approved innovator drug product. The generic copy can be approved on the basis of an application that is usually limited to manufacturing and biologic equivalence data, by referring to the non-clinical and clinical data that were the bases of approval of the innovator product. The copy can be approved after expiration of relevant patents and any regulatory exclusivity afforded by special circumstances. A new chemical entity has 5 and 10 years of regulatory exclusivity in the United States and European Union, respectively, precluding approval of a generic copy. Additional exclusivity can be afforded in the United States by approval of a product or use that has orphan drug status (7 years), or that requires review of new clinical data (3 years), or that is an expansion of use to a pediatric population (6 months). These exclusivities are independent, and could run sequentially, effectively extending the period of regulatory exclusivity. There is no assurance that such special regulatory exclusivities are applicable for our compounds. Separate from regulatory data exclusivity is the exclusivity conferred by the Hatch Waxman Act based on patent protection of the drug. A company seeking to market a generic might, after the lapse of regulatory data exclusivity, successfully challenge the patent protection of the marketed drug, thereby shortening its exclusive marketing period.

Patents and Proprietary Technology

Patents are very important to us in establishing proprietary rights to the products we develop or license. The patent positions of pharmaceutical and biotechnology companies, including ours, can be uncertain and involve complex legal, scientific, and factual questions. See “Risk Factors—Our ability to protect our intellectual property rights will be critically important to the success of our business, and we may not be able to protect these rights in the United States or abroad.”

We actively pursue patent protection when applicable for our proprietary products and technologies, whether they are developed in-house or acquired from third parties. We attempt to protect our intellectual property position by filing United States and foreign patent applications related to our proprietary technology, inventions and improvements that are important to the development of our business. Importantly, we are prosecuting a number of patent applications directed to various compounds in our pipeline, including those from our Discovery group. Additionally, we have been granted patents and have received patent licenses relating to our proprietary formulation technology, non-oncology and non-core technologies.

There can be no assurance that the patents granted or licensed to us will afford adequate legal protection against competitors or provide significant proprietary protection or competitive advantage. The patents granted or licensed to us could be held invalid or unenforceable by a court, or infringed or circumvented by others. In addition, third parties could also obtain patents that we would need to license or circumvent. Competitors or potential competitors may have filed patent applications or received patents, and may obtain additional patents and proprietary rights relating to proteins, small molecules, compounds, or processes that are competitive with the products we are developing.

In general, we obtain licenses from various parties we deem necessary or desirable for the development, manufacture, use, or sale of our products or product candidates. Some of our proprietary products are dependent upon compliance with other licenses and agreements. These licenses and agreements may require us to make royalty and other payments, to reasonably exploit the underlying technology of applicable patents, and to comply with regulatory filings. If we fail to comply with these and other terms in these licenses and agreements, we could lose the underlying rights to one or more of these potential products, which would adversely affect our product development and harm our business.

We also have patents, licenses to patents and pending patent applications outside of the United States, such as in Europe, Australia, Japan, Canada, China, Israel and India. Limitations on patent protection in these countries, and the differences in what constitutes patentable subject matter in these countries outside the United States, may limit the protection we have on patents issued or licensed to us outside the United States. In addition, laws of foreign countries may not protect our intellectual property to the same extent as would laws in the United States. To minimize our costs and expenses and maintain effective protection, we focus our foreign patent and licensing activities primarily in the European Union, Canada, Australia and Japan. In determining whether or not to seek a patent or to license any patent in other specific foreign countries, we weigh the relevant costs and benefits, and consider, among other things, the market potential and profitability, the scope of patent protection afforded by the law of the jurisdiction and its enforceability, and the nature of terms with any potential licensees. Failure to obtain adequate patent protection for our proprietary drugs and technology would impair our ability to be commercially competitive in these markets.

SuperGen has 120 issued patents and 271 pending patent applications. Of the total patents and pending patent applications those that relate to each of our material commercial product or product candidate are described in further detail below:

· Decitabine, a product we have exclusively licensed to Eisai: there are 11 issued patents and 30 patent applications, having projected expiration dates ranging from June 5, 2022 to September 27, 2024, granted or pending in the jurisdictions of the U.S., Australia, Canada, Europe, Japan, China, India and Hong Kong.

· SGI-110, our DNMT1 inhibitor: there is one issued patent and seven patent applications, each having a projected expiration date of September 29, 2025, granted or pending in the jurisdictions of the U.S., the European Patent Office (the “EPO”), Israel, China, South Africa, Malaysia, Vietnam and New Zealand.

· Amuvatinib, our TK Inhibitor and DNA Repair Suppressor: there are four issued patents and eight patent applications, having projected expiration dates ranging from October 14, 2024 to March 1, 2027, granted or pending in the jurisdictions of the U.S., the EPO, Australia and Canada.

· SGI-1776, our PIM kinase inhibitor: there is one issued patent and 11 patent applications, each having a projected expiration date of November 6, 2027, granted or pending in the jurisdictions of the U.S., the EPO, Hong Kong, India, Malaysia, Brazil, Canada, Japan, Russia, Vietnam and China.

· Our discovery JAK2 inhibitor: there are 17 patent applications, having projected expiration dates ranging from February 29, 2028 to July 25, 2029, pending in the jurisdictions of the U.S., the EPO, Taiwan, Australia, Brazil, Canada, China, Indonesia, India, Japan, Korea, Mexico, New Zealand and Hong Kong.

· Our discovery AXL inhibitor: there are 13 patent applications, having projected expiration dates ranging from April 11, 2028 to February 8, 2030, pending in the jurisdictions of the U.S., the EPO, Australia, Canada, China, Japan, Korea, New Zealand and Taiwan.

· Relating to our GlaxoSmithKline discovery collaboration: there are three patent applications, having projected expiration dates of February 26, 2030, pending in the jurisdictions of the U.S., the Patent Cooperation Treaty participants and Taiwan.

Trade Secrets and Trademarks

We also rely on trade secret protection for certain proprietary technology. To protect our trade secrets and our other confidential information, we pursue a policy of having our employees and consultants execute proprietary information agreements upon commencement of employment or consulting relationships with us. These agreements provide that all confidential information developed or made known to the individual during the course of the relationship is confidential except in specified circumstances. Further, we minimize the dissemination of our trade secrets by limiting the knowledge of staff only to the specific knowledge of a trade secret to what they need to know, and protective sequestering of trade secrets behind, for example, locks and passwords.

Competition

The pharmaceutical industry in general and the oncology sector in particular is highly competitive and subject to significant and rapid technological change. There are many companies, both public and private, including well-known pharmaceutical companies that are engaged in the discovery and development of products for some of the applications that we are pursuing. Some of our competitors and probable competitors include ArQule, Array BioPharma, Astex Tx, Crystal Genomics, Exelixis, Infinity, Plexxikon, Vertex, Sanofi-Aventis, Bristol-Myers Squibb Company, Celgene, Eli Lilly & Co., GSK, Novartis AG, Pfizer, and others.

Many of our competitors have substantially greater financial, research and development, and manufacturing resources than we do and may represent substantial long-term competition for us. Some of our competitors have received regulatory approval for products or are developing or testing product candidates that compete directly with our product candidates. For example, amuvatinib faces competition from a multitude of other investigational drugs which are multi-targeted tyrosine kinase inhibitors and inhibitors of the DNA repair pathway. We also expect that there will be other inhibitors of Pim kinases that will emerge as competition for SGI-1776 as well as other investigational drugs progressing through our discovery pipeline. In addition, Dacogen faces competition from 5-aza-cytidine and other drugs in development to treat MDS.

Many of these competitors, either alone or together with their customers and partners, have significantly greater experience than we do in discovering products, undertaking non-clinical testing and clinical trials, obtaining FDA and other regulatory approvals, and manufacturing and marketing products. Accordingly, our competitors may succeed in obtaining patent protection, receiving FDA or other foreign marketing approval or commercializing products before we do. If we elect to commence commercial product sales of our product candidates, we could be at a disadvantage relative to many companies with greater marketing and manufacturing capabilities, areas in which we have limited or no experience.

Factors affecting competition in the pharmaceutical industry vary depending on the extent to which competitors are able to achieve an advantage based on superior differentiation of their products’ greater institutional knowledge or depth of resources. If we are able to establish and maintain a competitive advantage based on the ability of CLIMB to discover new drug candidates more quickly and against targets not accessible by many competitors, our advantage will likely depend primarily on the ability of our CLIMB technology to make accurate predictions about the effectiveness and safety of our drug candidates as well as our ability to effectively and rapidly develop investigational drugs.

Extensive research and development efforts and rapid technological progress characterize the industry in which we compete. Although we believe that our proprietary drug discovery capabilities afford us a competitive advantage relative to other discovery and development companies competing in oncology, we expect competitive intensity in this pharmaceutical segment to continue and increase over time. Discoveries by others may render CLIMB and our current and potential products noncompetitive. Our competitive position also depends on our ability to attract and retain qualified scientific and other personnel at all our geographic locations, develop effective proprietary products, implement development plans, obtain patent protection and secure adequate capital resources.

Employees

As of December 31, 2009, we had 80 full-time employees. We use consultants and temporary employees to complement our staffing. Our employees are not subject to any collective bargaining agreements, and we consider our relations with employees to be good.

Executive Officers

|

Name |

|

Age |

|

Position |

|

James S. J. Manuso, Ph.D. |

|

61 |

|

President, Chief Executive Officer and Director |

|

Mohammad Azab, M.D., M.Sc., MBA |

|

54 |

|

Chief Medical Officer |

|

Michael Molkentin |

|

55 |

|

Chief Financial Officer |

James S.J. Manuso, Ph.D., has served as our president and chief executive officer since January 1, 2004, as our chief executive officer-elect from September 2003 to December 2003 and as a director since February 2001. Dr. Manuso is co-founder and immediate past president and chief executive officer of Galenica Pharmaceuticals, Inc. Dr. Manuso co-founded and was general partner of PrimeTech Partners, a biotechnology venture management partnership, from 1998 to 2002, and co-founder and managing general partner of The Channel Group LLC, an international life sciences corporate advisory firm. He was also president of Manuso, Alexander & Associates, Inc., management consultants and financial advisors to pharmaceutical and

biotechnology companies. Dr. Manuso was a vice president and director of Health Care Planning and Development for The Equitable Companies (now Group Axa), where he also served as acting medical director. He currently serves on the boards of Novelos Therapeutics, Inc. (NVLT:OB) and privately-held KineMed, Inc. Previously, he served on the boards of Merrion Pharmaceuticals Ltd. (MERR:IEX; Dublin, Ireland), Inflazyme Pharmaceuticals, Inc., Symbiontics, Inc., Quark Biotech, Inc., Galenica Pharmaceuticals, Inc., and Supratek Pharma, Inc. Dr. Manuso earned a B.A. with Honors in Economics and Chemistry from New York University, a Ph.D. in Experimental Psychophysiology from the Graduate Faculty of The New School University, a Certificate in Health Systems Management from Harvard Business School, and an Executive M.B.A. from Columbia Business School. Dr. Manuso is the author of over 30 chapters, articles and books on topics including health care cost containment and biotechnology company management. He has taught and lectured at Columbia, New York University, Georgetown, Polytechnic University, and Waseda University (Japan). He has delivered invited addresses at meetings of the American Management Association, the American Medical Association, the Securities Industry Association, the Biotechnology Industry Organization, and many other professional associations. Dr. Manuso previously served as vice president and a member of the Board of Trustees of the Greater San Francisco Bay Area Leukemia & Lymphoma Society.

Mohammad Azab, M.D., M.Sc., MBA, joined SuperGen as chief medical officer in July 2009. He possesses more than 20 years of experience in worldwide drug development, clinical research, and medical affairs, resulting in eight approved drugs, including six in oncology. Most recently, he was president and chief executive officer of Intradigm Corporation, a privately held Palo Alto, CA company developing siRNA cancer therapeutics. Previously, Dr. Azab served as executive vice president of research and development, and chief medical officer, of Vancouver, British Columbia-based QLT Inc., where he led clinical development for now-approved drugs in oncology, gastro-intestinal, and ophthalmologic indications. Prior to this, he served as oncology drug team leader at UK-based Zeneca Pharmaceuticals, now Astra Zeneca, where he held responsibilities in global clinical development and regulatory submissions. In this capacity, he managed the approval of drugs for prostate, breast, colorectal, and lung cancer indications. Before Zeneca, Dr. Azab was an international medical manager in oncology at Sanofi Pharmaceuticals, now Sanofi-Aventis, in Gentilly, France. Dr. Azab received his medical degree in 1979 from Cairo University. He practiced as a medical oncologist and received post-graduate training and degrees in oncology research and statistics from the University of Paris-Sud and the University of Pierre and Marie Curie in France. He has published more than 100 medical papers and abstracts. He is an active member of the American Society of Clinical Oncology, the American Association of Cancer Research, and the European Society of Medical Oncology. Dr. Azab received an MBA, with Distinction, from the Richard Ivey School of Business, University of Western Ontario.

Michael Molkentin joined us as chief financial officer and corporate secretary in October 2003. Prior to joining us, Mr. Molkentin served as interim chief financial officer at Aradigm Corporation from May 2000 to September 2002. From January 1995 to April 2000, Mr. Molkentin served as division controller for Thermo Finnigan Corporation, a subsidiary of Thermo Electron. Mr. Molkentin served in a variety of financial management positions with technology companies, including field controller of Vanstar Corporation, controller of Republic Telcom Systems, Inc. and corporate controller of Computer Automation, Inc. Mr. Molkentin is a CPA and received a B.B.A. in accounting from Bernard M. Baruch College in New York City, New York.

Segment and Geographic Area Financial Information

We operate in one business segment — human therapeutics. We had no product revenue in 2009 or 2008. In 2007, 100% of our product revenue was from the EU.

Available Information

We are subject to the information requirements of the Securities Exchange Act of 1934 (the “Exchange Act”). Therefore, we file periodic reports, proxy statements, and other information with the Securities and Exchange Commission (“SEC”). Such reports, proxy statements, and other information may be obtained by visiting the Public Reference Room of the SEC at 100 F Street, NE, Washington, DC 20549 or by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains a website (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically.

Financial and other information about us is available on our website at www.supergen.com. We make available on our website, free of charge, copies of our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after filing such material electronically or otherwise furnishing it to the SEC. Information on our website does not constitute a part of this annual report on Form 10-K.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

You should read the following discussion together with our consolidated financial statements and related notes included elsewhere in this report. The results discussed below are not necessarily indicative of the results to be expected in any future periods. Our disclosure and analysis in this section of the report also contain forward-looking statements. When we use the words “anticipate,” “estimate,” “project,” “intend,” “expect,” “plan,” “believe,” “should,” “likely” and similar expressions, we are making forward-looking statements. Forward-looking statements provide our current expectations or forecasts of future events. In particular, these statements include statements such as: our estimates about profitability; the percentage of royalties we expect to earn on Dacogen sales under our agreement with MGI/Eisai; our forecasts regarding our research and development expenses; our expectations about the joint development program with GSK; and our statements regarding the sufficiency of our cash to meet our operating needs. Our actual results could differ materially from those predicted in the forward-looking statements as a result of risks and uncertainties including, but not limited to: the commercial success of Dacogen; delays and risks associated with conducting and managing our clinical trials; developing products and obtaining regulatory approval; ability to establish and maintain collaborative relationships; competition; ability to obtain funding; ability to protect our intellectual property; our dependence on third party suppliers; risks associated with the hiring and loss of key personnel; adverse changes in the specific markets for our products; and our ability to launch and commercialize products. Certain unknown or immaterial risks and uncertainties can also affect our forward-looking statements. Consequently, no forward-looking statement can be guaranteed and you should not rely on these forward-looking statements. For a discussion of the known and material risks that could affect our actual results, please see the “Risk Factors” section of this report. We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise. Readers should carefully review the Risk Factors section as well as other reports or documents we file from time to time with the Securities and Exchange Commission.

Overview

We are a pharmaceutical company dedicated to the discovery and development of novel cancer therapeutics in epigenetic and cell signaling modulation. We develop products through biochemical and clinical proof of concept to partner for further development and commercialization. We have a number of Aurora-A and Tyrosine Kinase inhibitors and DNA methyltransferase clinical and pre-clinical products under development. In 2006, Dacogen received approval for marketing in the United States, during 2006 and 2007 we sold the North American and remaining worldwide rights to Nipent to Mayne Pharma, in 2006 we acquired a drug discovery and development company to complement our ongoing licensing efforts, and in October 2009 we entered into a multi-year collaboration with GlaxoSmithKline to discover and develop cancer therapeutics based on epigenetic targets. These changes were implemented to mitigate the ongoing risk of competitive in-licensing and to maximize the return on both existing resources and our incoming royalty and milestone revenue.

Since our incorporation in 1991 we have devoted substantially all of our resources to our product development efforts. Our past development efforts have been focused primarily on the key compounds of Dacogen and Nipent.

Dacogen. Dacogen is approved by the FDA for the treatment of patients with MDS. In September 2004, we executed an agreement granting MGI/Eisai exclusive worldwide rights to the development, manufacture, commercialization and distribution of Dacogen. Under the terms of the agreement, MGI/Eisai made a $40 million equity investment in our company and agreed to pay up to $45 million in specific regulatory and

commercialization milestone payments. To date, we have received $32.5 million of these milestone payments, including $20 million upon first commercial sale of Dacogen in the U.S. in May 2006. In accordance with our agreement with MGI/Eisai, we are entitled to receive a royalty on worldwide net sales starting at 20% and escalating to a maximum of 30%. Our royalty revenues have increased from $22.3 million in 2007, to $38.4 million in 2008, and $41.2 million in 2009. We recognize royalty revenue when the royalty statement is received from MGI/Eisai because we do not have sufficient ability to accurately estimate Dacogen sales prior to that time.

In July 2006, MGI/Eisai executed an agreement to sublicense Dacogen to Janssen-Cilag, a Johnson & Johnson company, granting exclusive development and commercialization rights in all territories outside North America. In accordance with our agreement with MGI/Eisai, we are entitled to receive 50% of certain payments MGI/Eisai receives as a result of any sublicenses. We received $5 million, 50% of the $10 million upfront payment MGI/Eisai received, and, as a result of both the original agreement with MGI/Eisai and this sublicense with Janssen-Cilag, we may receive up to $17.5 million in future milestone payments as they are achieved for Dacogen globally. Janssen-Cilag companies will be responsible for conducting regulatory and commercial activities related to Dacogen in all territories outside North America, while MGI/Eisai retains all commercialization rights and responsibility for all activities in the United States, Canada and Mexico.

Nipent. Nipent is approved by the FDA and EMEA for the treatment of hairy cell leukemia. Nipent was marketed by us in the United States until August 2006, and distributed in Europe through March 2007.

On August 22, 2006, we closed a transaction with Mayne Pharma (USA), Inc., whereby Mayne acquired the North American rights to Nipent and our SurfaceSafe cleaning system. Pursuant to the Asset Acquisition Agreement, we received cash proceeds of $13.4 million upon closing of the transaction. In addition to the initial payment and holdbacks, we had the right to receive annual deferred payments totaling $14.1 million over the following five years based on achievement of specific sales targets. These annual deferred payments might be accelerated under certain circumstances, including a change of control of Mayne. Such a change of control occurred in February 2007 when Mayne was acquired by Hospira, Inc. and we received $10.3 million of the deferred payments. We continued to maintain our commercial operations organization to support the sales and marketing of Nipent during the six month transition period, which ended on February 21, 2007. We were reimbursed by Mayne/Hospira for all Nipent sales and marketing costs during the transition period, including employee salaries and overhead.

In April 2007, we closed another transaction with Mayne/Hospira, completing the sale of the remaining worldwide rights for Nipent for total consideration of up to $8.3 million. We received an initial up-front payment of $3.75 million as a condition of the closing, plus an additional $389,000 for the carrying value of the remaining Nipent inventory. The balance of the purchase price is payable in five annual installments on the anniversary of the closing date.

In September 2007, we received a sales milestone payment of $1.8 million from Mayne/Hospira and in December 2007 received $6 million in supply holdback payments. In February 2008, we received a $1 million indemnification holdback from Mayne/Hospira relating to the sale of the North American rights. In May 2008, we received $400,000, the first annual installment payment relating to the sale of the remaining worldwide rights, and in November 2008 we received the remaining $250,000 indemnification holdback. In March 2009, we received $500,000, the second annual installment payment relating to the sale of the remaining worldwide rights. We do not expect to receive any further payments from the sale of the North American rights.

Montigen Acquisition. In April 2006, we acquired Montigen, a privately-held oncology-focused drug discovery and development company headquartered in Salt Lake City, Utah. Montigen’s assets included its research and development team, a proprietary drug discovery technology platform and optimization process known as CLIMB, and late-stage non-clinical compounds targeting Aurora-A Kinase and members of the Tyrosine Kinase receptor family.

Pursuant to the terms of the merger agreement with Montigen, we paid the Montigen stockholders a total of $17.9 million upon the closing of the transaction in cash and shares of SuperGen common stock. The merger agreement also specified an additional $22 million due to the Montigen stockholders, payable in shares of SuperGen common stock, contingent upon achievement of specific regulatory milestones. The first Montigen compound was cleared in April 2007 by the FDA to begin Phase I clinical trials, which triggered the first milestone payment to the former Montigen stockholders of approximately $10 million which we paid in shares of our common stock. A second Montigen compound was cleared in November 2008 by the FDA to begin Phase I clinical trials, which triggered a milestone payment of $5.2 million, which we paid in a combination of cash and shares of our common stock.

GSK Collaboration. In October 2009, we entered into a multi-year collaboration with GSK to discover and develop cancer therapeutics based on epigenetic targets. Epigenetics refer to the regulation of genes with mechanisms other than changes to the underlying DNA sequence. Epigenetic processes are widely believed to play a central role in the development and progression of almost all cancers. Pursuant to the terms of the transaction, we will collaborate with GSK over a period of five years to discover and develop specific epigenetic therapeutics. At the end of the research term, or earlier if GSK elects, GSK may exercise its option to license from us the compounds that are the result of the joint research effort, in order to continue the development and ultimately commercialize and sell the products worldwide.

In connection with the transaction, we received $5 million upfront, inclusive of a $3 million purchase by GSK of shares of our common stock, priced at a premium to market. In addition, GSK is obligated to make certain payments to us if and when the compounds reach specified developmental milestones, as well as payments to us if and when the compounds that GSK has licensed achieve certain regulatory milestones. The agreement further provides that, if the licensed compounds derived from the joint research team become products, GSK will pay us sales milestone payments as well as royalties on annual net sales of such products. The royalties will be paid on a country-by-country and product-by-product basis. Total potential development and sales milestones payable to us could exceed $375 million. In addition, we may receive tiered royalties into double digit magnitudes, payable on net sales of any resulting products.

All of our current products are in the development or clinical trial stage, and will require substantial additional investments in research and development, clinical trials, regulatory and sales and marketing activities to commercialize these product candidates. Conducting clinical trials is a lengthy, time-consuming, and expensive process involving inherent uncertainties and risks, and our studies may be insufficient to demonstrate safety and efficacy to support FDA approval of any of our product candidates.