Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - PDC ENERGY, INC. | pec8k11082010.htm |

| EX-99.1 - EX-99.1 - PDC ENERGY, INC. | pdcrelease2010_1108.htm |

Third Quarter 2010 Results Teleconference

November 8, 2010

Disclaimer

The following information contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These

forward-looking statements are based on Management’s current expectations and beliefs, as well as a number of assumptions concerning future

events.

forward-looking statements are based on Management’s current expectations and beliefs, as well as a number of assumptions concerning future

events.

These statements are based on certain assumptions and analyses made by Management in light of its experience and its perception of historical

trends, current conditions and expected future developments as well as other factors it believes are appropriate in the circumstances. However,

whether actual results and developments will conform with Management’s expectations and predictions is subject to a number of risks and

uncertainties, general economic, market or business conditions; the opportunities (or lack thereof) that may be presented to and pursued by PDC

Energy; actions by competitors; changes in laws or regulations; and other factors, many of which are beyond the control of PDC Energy.

trends, current conditions and expected future developments as well as other factors it believes are appropriate in the circumstances. However,

whether actual results and developments will conform with Management’s expectations and predictions is subject to a number of risks and

uncertainties, general economic, market or business conditions; the opportunities (or lack thereof) that may be presented to and pursued by PDC

Energy; actions by competitors; changes in laws or regulations; and other factors, many of which are beyond the control of PDC Energy.

You are cautioned not to put undue reliance on such forward-looking statements because actual results may vary materially from those expressed

or implied, as more fully discussed in our safe harbor statements found in our SEC filings, including, without limitation, the discussion under the

heading “Risk Factors” in the Company’s 2009 annual report on Form 10-K and in subsequent Form 10-Qs. All forward-looking statements are

based on information available to Management on this date and PDC Energy assumes no obligation to, and expressly disclaims any obligation to,

update or revise any forward looking statements, whether as a result of new information, future events or otherwise.

or implied, as more fully discussed in our safe harbor statements found in our SEC filings, including, without limitation, the discussion under the

heading “Risk Factors” in the Company’s 2009 annual report on Form 10-K and in subsequent Form 10-Qs. All forward-looking statements are

based on information available to Management on this date and PDC Energy assumes no obligation to, and expressly disclaims any obligation to,

update or revise any forward looking statements, whether as a result of new information, future events or otherwise.

The SEC permits oil and gas companies to disclose in their filings with the SEC proved reserves, probable reserves and possible reserves. SEC

regulations define “proved reserves” as those quantities of oil or gas which, by analysis of geosciences and engineering data, can be estimated

with reasonable certainty to be economically producible in future years from known reservoirs under existing economic conditions, operating

methods and government regulations; “probable reserves” as unproved reserves which, together with proved reserves, are as likely as not to be

recovered; and “possible reserves” as unproved reserves which are less certain to be recovered than probable reserves. Estimates of probable

and possible reserves which may potentially be recoverable through additional drilling or recovery techniques are by nature more uncertain than

estimates of proved reserves and accordingly are subject to substantially greater risk of not actually being realized by the Company. In addition,

the Company’s reserves and production forecasts and expectations for future periods are dependent upon many assumptions, including

estimates of production decline rates from existing wells and the undertaking and outcome of future drilling activity, which may be affected by

significant commodity price declines or drilling cost increases.

regulations define “proved reserves” as those quantities of oil or gas which, by analysis of geosciences and engineering data, can be estimated

with reasonable certainty to be economically producible in future years from known reservoirs under existing economic conditions, operating

methods and government regulations; “probable reserves” as unproved reserves which, together with proved reserves, are as likely as not to be

recovered; and “possible reserves” as unproved reserves which are less certain to be recovered than probable reserves. Estimates of probable

and possible reserves which may potentially be recoverable through additional drilling or recovery techniques are by nature more uncertain than

estimates of proved reserves and accordingly are subject to substantially greater risk of not actually being realized by the Company. In addition,

the Company’s reserves and production forecasts and expectations for future periods are dependent upon many assumptions, including

estimates of production decline rates from existing wells and the undertaking and outcome of future drilling activity, which may be affected by

significant commodity price declines or drilling cost increases.

This material also contains certain non-GAAP financial measures as defined under the Securities and Exchange Commission rules.

2

11/08/2010

Rick McCullough

Chairman and Chief Executive Officer

3

11/08/2010

Third Quarter 2010 Highlights

11/08/2010

4

• Financial results were essentially within guidance in spite of lease operating

expense which was up for the quarter due to the expensing of approximately

$2 MM which was budgeted as a capital item

expense which was up for the quarter due to the expensing of approximately

$2 MM which was budgeted as a capital item

• Q3 2010 realized prices of $6.42 per Mcfe compared to Q3 2009 realized

prices of $6.14 per Mcfe

prices of $6.14 per Mcfe

• Production slightly above guidance due to Wattenberg results

• Drilled 39.7 net wells vs. 21.0 net wells in Q3 2009

• Production continues to trend higher as fourth quarter’s production and exit

rate should exceed guidance; oil’s percentage of (2010 exit rate) production

should approach 26% versus 18% of 2009 exit rate production

rate should exceed guidance; oil’s percentage of (2010 exit rate) production

should approach 26% versus 18% of 2009 exit rate production

Third Quarter 2010 Highlights, continued

11/08/2010

5

• Drilling efficiencies continue to improve as a result of optimizing capital costs

and improving operating performance in the Piceance Basin and Wattenberg

Field

and improving operating performance in the Piceance Basin and Wattenberg

Field

• Signed an agreement with a private company to acquire producing assets

and undeveloped acreage located in the Wolfberry oil trend in West Texas for

$40 MM in cash

and undeveloped acreage located in the Wolfberry oil trend in West Texas for

$40 MM in cash

• Amended and restated the Company’s revolving bank loan facility agreement

on November 4, 2010, increasing the borrowing base to $350 MM, adding

additional lenders, amending certain other provisions including a cost

reduction on its borrowing grid, and extending the maturity to November 2015

on November 4, 2010, increasing the borrowing base to $350 MM, adding

additional lenders, amending certain other provisions including a cost

reduction on its borrowing grid, and extending the maturity to November 2015

Bart Brookman

Senior Vice President - Exploration and Production

6

11/08/2010

Q1 2010 Production:

8.1

Bcfe

8.1

Bcfe

Rocky Mountains

Q1 2010 Production:

0.6

Bcfe

0.6

Bcfe

Q2 2010 Production:

0.6

Bcfe

0.6

Bcfe

Q3 2010 Production:

0.6

Bcfe

0.6

Bcfe

2010E Production:

2.5

Bcfe

2.5

Bcfe

Appalachian Basin (PDCM)

Q1 2010 Production:

0.3

Bcfe

0.3

Bcfe

Q3 2010 Production

9.2 Bcfe

Michigan

Basin (1%)

Basin (1%)

Appalachian Basin (7%)

Rocky

Mountains (90%)

Mountains (90%)

Rocky

Mountains (91%)

Mountains (91%)

7

Core Operating Regions

Operations Underway

Q3 2010 Production:

0.1

Bcfe

0.1

Bcfe

2010E Production:

0.5

Bcfe

0.5

Bcfe

Permian Basin

Permian (1%)

11/08/2010

Quarterly Net Production

8

• Q3 actual production exceeded

mid-year guidance

mid-year guidance

• Primarily Wattenberg Field driven

• Improved frac designs

• Production includes increased oil and

gas liquids component

gas liquids component

• Successfully acquired and

integrated Permian assets

integrated Permian assets

• Optimizing production

• Increasing production from

Marcellus

Marcellus

• Q4 production anticipated to be in-

line or above guidance

line or above guidance

• Lower line pressure in Wattenberg

Field

Field

Michigan

(reflected as discontinued operations)

11/08/2010

*Excludes Q4 anticipated acquisitions.

*

Quarterly Drilling Activity

9

• Improved capital efficiencies achieved

in drilling and completion operations

in drilling and completion operations

• Two rigs operating in Wattenberg Field

• One flex rig operating in Piceance Basin

• Significant improvement in spud-to-spud time

11/08/2010

3Q 2010

4Q 2010 Expectations

• Drill five Permian Basin wells

• Drill first horizontal Niobrara well in

Krieger prospect

Krieger prospect

• Spud 4th horizontal Marcellus well

• Operate 3rd vertical rig in Wattenberg

Field

Field

* Excludes Q4 anticipated acquisitions.

*

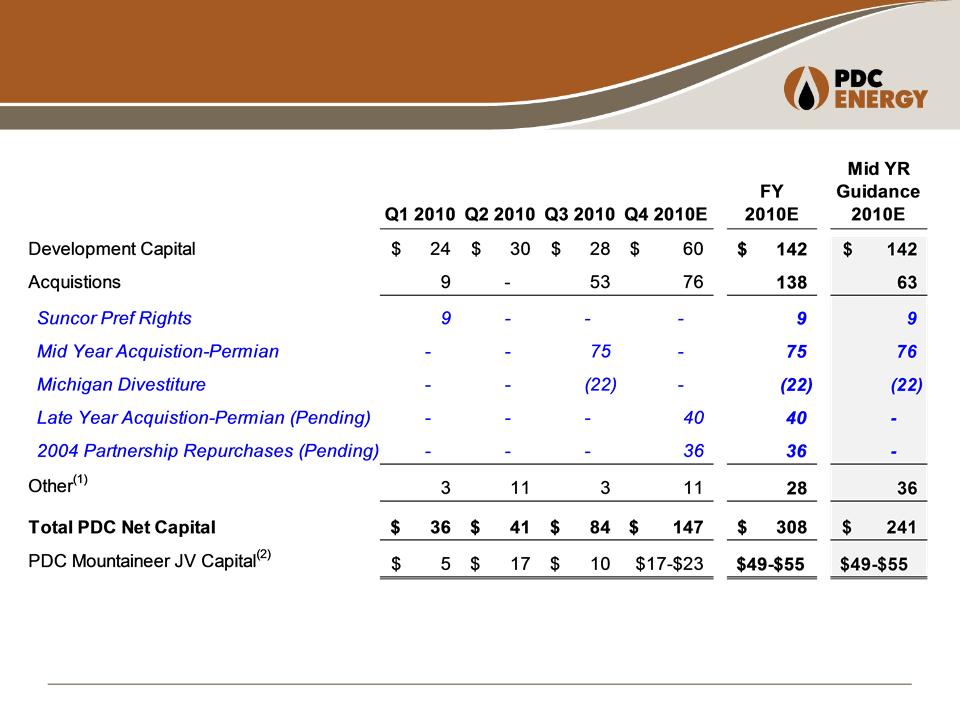

Q3 Capital Expenditure Update

Q1-Q3 Actual & New Estimates for 4Q2010

Q1-Q3 Actual & New Estimates for 4Q2010

$ in Millions

10

11/08/2010

(1) Other capital includes exploration, leasehold, facilities, and miscellaneous.

(2) Marcellus operations funded by our joint venture partner.

11

2010 Production by Area

Billion Cubic Feet Equivalent (Bcfe)

|

Area

|

Q1 2010

Actual |

Q2 2010

Actual |

Q3 2010

Actual |

FY 2010E

|

|

Wattenberg

|

4.0

|

4.0

|

4.1

|

15.9

|

|

Piceance

|

3.0

|

2.8

|

3.2

|

11.9

|

|

NECO

|

1.1

|

1.1

|

1.1

|

4.4

|

|

Michigan*

|

0.3

|

0.4

|

-

|

0.7

|

|

West Texas

|

0.0

|

0.0

|

0.1

|

0.6

|

|

Other

(ND, TX, WY,OH)

|

0.1

|

0.1

|

0.1

|

0.4

|

|

Appalachia

(PDCM) |

0.6

|

0.6

|

0.6

|

2.5

|

|

TOTAL

|

9.1

|

9.0

|

9.2

|

36.4

|

* Michigan production through 6/30/10 reflected as discontinued operations.

11/08/2010

Note: Full-year excludes Q4 anticipated acquisitions.

Growth in Fourth Quarter Production

11/08/2010

12

Mid-Year Guidance Net Production 2010 Exit

Rate

Rate

•Net Production 9.3 Bcfe 107 MMcfe/d

•Oil 360 Mbo 4.3 MMBbl/d

•Gas 7,200 MMcf 80.8 MMcf/d

Fourth Quarter New Activity

•2nd Wolfberry Acquisition(1) 0.1 Bcfe 3.6

MMcfe/d

MMcfe/d

• Oil 17.4 Mbo 0.5 MBbl/d

• Gas 7.3 MMcf 0.2 MMcf/d

•Partnership Purchases(2) 0.1 Bcfe 3.6 MMcfe/d

• Oil 2.2 Mbo 0.07 MBbl/d

• Gas 97 MMcf 3.2 MMcf/d

Updated Fourth Quarter 9.5 Bcfe 114 MMcfe/d

26% oil

26% oil

(1) Wolfberry acquisition production for December 2010 based on current rate estimate.

(2) Partnership production based upon December 2010 post-closing volumes. Assumes PDC successful in outstanding partnership repurchase offer.

Lifting Costs

|

|

Q1 2010

Actual

|

Q2 2010

Actual

|

Q3 2010

Actual

|

FY 2010E

|

|

Direct Costs ($/Mcfe)

|

$0.75

|

$0.98

|

$0.97

|

$0.73 - $0.87

|

|

Indirect Costs ($/Mcfe)

|

$0.29

|

$0.26

|

$0.24

|

$0.27 - $0.31

|

|

Total Lifting Cost ($/Mcfe)

|

$1.04

|

$1.24

|

$1.21

|

$1.00 - $1.18

|

13

• Q3 2010 per unit costs increased as a result of:

• Increased workovers to enhance production (primarily in Piceance Basin)

• Accrual of facility upgrade costs in Piceance Basin and Wattenberg Field

• Total lifting costs include workover expenses of $0.08 in Q1, $0.30 in Q2,

and $0.36 in Q3

and $0.36 in Q3

11/08/2010

Operations Highlights

• Q4 drilling activity in-line with guidance; six active drilling rigs

• Wattenberg production continues to exceed engineering expectations

• Spud first Permian Basin well

• Drilling fourth horizontal well in WV

• First horizontal Niobrara well TD’d on the Krieger Prospect in the DJ Basin

• Approved a ten year mid-stream transportation commitment in WV for future

Marcellus production

Marcellus production

• Four superfracs executed in Piceance Basin with encouraging results

14

11/08/2010

Gysle Shellum

Chief Financial Officer

15

11/08/2010

Summary Financial Results

11/08/2010

16

In Millions, Except for Per Share Data

|

|

Three Months Ended

|

Nine Months Ended

|

||

|

September 30,

|

September 30,

|

|||

|

Measure

|

2010

|

2009

|

2010

|

2009

|

|

O&G Revenues

|

$48.1

|

$42.9

|

$156.1

|

$121.4

|

|

O&G Production & Well Operations Costs

|

$16.7

|

$14.7

|

$48.2

|

$44.2

|

|

O&G Operating Margin

|

$31.4

|

$28.2

|

$107.9

|

$77.2

|

|

Adjusted cash flow from operations(1)

|

$23.6

|

$37.3

|

$101.8

|

$114.7

|

|

Adjusted EBITDA(2)

|

$27.2

|

$36.3

|

$109.3

|

$117.2

|

|

Adjusted EBITDA (per diluted share)(1)

|

$1.40

|

$2.14

|

$5.66

|

$7.55

|

|

DD&A

|

$28.2

|

$31.9

|

$83.0

|

$99.1

|

|

G&A

|

$10.4

|

$9.6

|

$31.0

|

$36.5

|

(1) See appendix for Non-GAAP reconciliation of Adjusted Cash Flow from Operations and Adjusted EBITDA.

Summary Financial Results

11/08/2010

17

|

|

Three Months Ended

|

Nine Months Ended

|

||

|

September 30,

|

September 30,

|

|||

|

Measure

|

2010

|

2009

|

2010

|

2009

|

|

Operating income (loss)

|

$10.3

|

($30.6)

|

$62.3

|

($77.6)

|

|

Net Income (loss) attributable to

.shareholders |

$3.4

|

($24.5)

|

$24.4

|

($63.3)

|

|

Diluted earnings (loss) per share

.attributable to shareholders |

$0.17

|

($1.44)

|

$1.26

|

($4.07)

|

|

|

Three Months Ended

|

Nine Months Ended

|

||

|

September 30,

|

September 30,

|

|||

|

Measure

|

2010

|

2009

|

2010

|

2009

|

|

Adjusted net income (loss) from continuing

operations(1) |

($1.9)

|

($3.4)

|

$5.7

|

($4.0)

|

|

Adjusted earnings (loss) per share from

continuing operations(1)

|

($0.10)

|

($0.20)

|

$0.29

|

($0.26)

|

(1) See appendix for Non-GAAP reconciliation of Adjusted Net Income.

In Millions, Except for Per Share Data

Debt Maturity Schedule

11/08/2010

18

• $350 million revolver matures

in November 2015

in November 2015

• Maturity schedule and increase

reflects:

reflects:

– Mitigation of liquidity risk

– Diversification of funding sources

– Growing support of investing

community in our strategies and

execution

community in our strategies and

execution

• As of September 30, 2010:

– $102 million drawn balance

– $19 million undrawn L.O.C

– $13 million cash balance

– $198 million available liquidity

$203

$102

$ in Millions

2010

2011

2012

2013

2014

2015

2016

2017

2018

Quarterly Realized Hedge Price

11/08/2010

19

As of 9/30/10

Note: Weighted average for full year 2010 is $7.36/Mcfe.

Oil and Gas Per Unit Costs

11/08/2010

20

|

|

Three Months Ended

|

Nine Months Ended

|

||

|

September 30,

|

September 30,

|

|||

|

Measure

|

2010

|

2009

|

2010

|

2009

|

|

Average Lifting Costs(1)

|

$1.21

|

$0.79

|

$1.16

|

$0.78

|

|

DD&A (O&G Properties Only)

|

$2.87

|

$2.79

|

$2.89

|

$2.87

|

(1) Lifting costs represent natural gas and oil lease operating expenses, exclusive of production taxes, on a per unit basis.

Per Mcfe

Third quarter 2010 per unit costs were higher than 2009 third quarter per unit costs due to lower production and

the addition of approximately $0.33 per unit due to the incurrence of approximately $1 million of environmental

maintenance expenses, and well workover expenses of approximately $2 million. When amounts are adjusted

for these items the comparison was $0.88 per unit in 2010 compared to $0.79 per unit in 2009. Most of the

difference in per unit costs was related to lower production volumes in 2010.

the addition of approximately $0.33 per unit due to the incurrence of approximately $1 million of environmental

maintenance expenses, and well workover expenses of approximately $2 million. When amounts are adjusted

for these items the comparison was $0.88 per unit in 2010 compared to $0.79 per unit in 2009. Most of the

difference in per unit costs was related to lower production volumes in 2010.

For the nine months ended September 30, when amounts are adjusted for the incurrence of approximately $2.6

million of environmental maintenance expenses, and well workover expenses of approximately $3.8 million, the

comparison was $0.92 per unit in 2010 versus $0.78 per unit in 2009. Most of this is related to lower production

volumes.

million of environmental maintenance expenses, and well workover expenses of approximately $3.8 million, the

comparison was $0.92 per unit in 2010 versus $0.78 per unit in 2009. Most of this is related to lower production

volumes.

Lance Lauck

Senior Vice President - Business Development

21

11/08/2010

Acquiring Additional Wolfberry Assets

11/08/2010

22

Existing Production with Significant Upside Opportunities

Acquisition Summary - Announced November 3, 2010

• Acquiring 5,760 net acres in the Wolfberry Trend for $40 million

• Contiguous to existing Wolfberry acreage position

• Privately negotiated transaction

• PDC operated assets with essentially a 100% working interest

• Current net production of 330 boe/d from 6 Wolfberry wells

• 7th well on flow-back

• Identified 122 locations on 40-acre spacing; plan to drill first well in December 2010

• Approximately 10 million barrels of oil equivalent (MMBOE) in 2P reserves

• 90% oil and natural gas liquids, delivering full cycle cash margin of $60/BOE

• Effective date of November 1, 2010; Expect to close transaction on November 19, 2010

Doubling Size of Permian Position

11/08/2010

23

Establishes Permian Basin as a Key Development Area for PDC

Key Highlights

• Established a field office in Midland, TX

• Added experienced technical staff to lead Wolfberry development

• Drilling first Wolfberry well on initial acquisition; development ahead of schedule

• Expect to drill five wells by end of 2010

• Full testing of Wolfberry acreage areas expected by early 2011

• Anticipate 20-30 wells drilled in 2011; 1 to 2 rig program

• Workovers and production optimization projects growing base production

• Multi-year production growth expected from Wolfberry development drilling

• Implementing PDC strategy to increase liquids in corporate reserve portfolio

|

|

Nov 2010 Acquisition

|

Total Permian

|

|

Acquisition Cost

|

$40MM

|

$115MM

|

|

Net Wolfberry Acres

|

5,760

|

10,500

|

|

Net Production (Boe/d)

|

330

|

900

|

|

Net 2P Reserves (MMBOE)

|

10.0

|

18.5

|

|

40-acre Drilling Locations

|

122

|

250

|

Appendix

24

11/08/2010

25

11/08/2010

|

|

Three Months Ended

|

Nine Months Ended

|

||

|

September 30,

|

September 30,

|

|||

|

|

2010

|

2009

|

2010

|

2009

|

|

Net Income (loss) from continuing operations

|

$3.2

|

($25.0)

|

$26.0

|

($64.6)

|

|

Unrealized (gain) loss on derivatives, net (1)

|

(11.4)

|

35.0

|

(36.1)

|

95.7

|

|

Provision for underpayment of gas sales

|

3.3

|

-

|

3.3

|

2.6

|

|

Tax effect of above adjustments

|

3.1

|

(13.4)

|

12.5

|

(37.7)

|

|

Adjusted Net Income (loss) from continuing

operations |

($1.9)

|

($3.4)

|

$5.7

|

($4.0)

|

|

Weighted average diluted shares outstanding

|

19,406

|

16,962

|

19,319

|

15,530

|

|

Adjusted diluted earnings (loss) per share

|

($0.10)

|

($0.20)

|

$0.29

|

($0.26)

|

Adjusted Net Income Reconciliation

$ in Millions, Except for Per Share Data

(1) Includes natural gas marketing activities.

26

11/08/2010

|

|

Three Months Ended

|

Nine Months Ended

|

||

|

September 30,

|

September 30,

|

|||

|

|

2010

|

2009

|

2010

|

2009

|

|

Net Cash provided by operating activities

|

$21.4

|

$39.3

|

$116.8

|

$100.0

|

|

Changes in assets and liabilities

|

2.2

|

(2.0)

|

(15.0)

|

14.7

|

|

Adjusted cash flow from continuing

operations |

$23.6

|

$37.3

|

$101.8

|

$114.7

|

|

Weighted average diluted shares outstanding

|

19,406

|

16,962

|

19,319

|

15,530

|

|

Adjusted cash flow per share

|

$1.22

|

$2.20

|

$5.27

|

$7.39

|

Adjusted Cash Flow Reconciliation

$ in Millions, Except for Per Share Data

27

11/08/2010

Adjusted EBITDA Reconciliation

$ in Millions, Except for Per Share Data

|

|

Three Months Ended

|

Nine Months Ended

|

||

|

September 30,

|

September 30,

|

|||

|

|

2010

|

2009

|

2010

|

2009

|

|

Net Income (loss) from continuing operations

|

$3.2

|

($25.0)

|

$26.0

|

($64.6)

|

|

Unrealized (gain) loss on derivatives, net(1)

|

(11.4)

|

35.0

|

(36.1)

|

95.7

|

|

Interest, net

|

8.2

|

9.0

|

23.6

|

26.8

|

|

Income taxes expense (benefit)

|

(1.0)

|

(14.7)

|

12.7

|

(39.8)

|

|

Depreciation, depletion & amortization

|

28.2

|

31.9

|

83.0

|

99.1

|

|

Adjusted EBITDA

|

$27.2

|

$36.3

|

$109.3

|

$117.2

|

|

Weighted average diluted shares outstanding

|

19,406

|

16,962

|

19,319

|

15,530

|

|

Adjusted EBITDA per share

|

$1.40

|

$2.14

|

$5.66

|

$7.55

|

(1) Includes natural gas marketing activities.

Contact Information

Investor Relations

• Peter Schreck, Vice President - Finance and Treasurer

pschreck@petd.com

• Marti Dowling, Manager Investor Relations

mdowing@petd.com

• Heather Davis, Investor Relations Coordinator

hdavis@petd.com

Corporate Headquarters

• PDC Energy

1775 Sherman Street

Suite 3000

Denver, CO 80203

303-860-5800

Website

• www.petd.com

28

11/08/2010