Attached files

| file | filename |

|---|---|

| EX-99.2 - RECONCILIATIONS OF NON-GAAP FINANCIAL MEASURES TO GAAP FINANCIAL MEASURES - AMEDISYS INC | dex992.htm |

| 8-K - FORM 8-K - AMEDISYS INC | d8k.htm |

November 2010

Exhibit 99.1

Investor Presentation

Leading Home Health Care & Hospice |

Leading Home Health & Hospice

Forward-looking statements

This presentation may include forward-looking statements as defined by the

Private Securities Litigation Reform Act of 1995. These forward-looking

statements are based upon current expectations and assumptions about our

business that are subject to a variety of risks and uncertainties that could

cause actual

results

to

differ

materially

from

those

described

in

this

presentation.

You

should not rely on forward-looking statements as a prediction of future events.

Additional

information

regarding

factors

that

could

cause

actual

results

to

differ

materially from those discussed in any forward-looking statements are described

in reports and registration statements we file with the SEC, including our

Annual Report on Form 10-K and subsequent Quarterly Reports on Form

10-Q and Current Reports on Form 8-K, copies of which are available

on the Amedisys internet

website

http://www.amedisys.com

or

by

contacting

the

Amedisys

Investor

Relations department at (800) 467-2662.

We disclaim any obligation to update any forward-looking statements or any

changes in events, conditions or circumstances upon which any

forward-looking statement may be based except as required by law.

2

www.amedisys.com

NASDAQ: AMED

We encourage everyone to visit the

Investors Section of our website at

www.amedisys.com, where we

have posted additional important

information such as press releases,

profiles concerning our business

and clinical operations and control

processes, and SEC filings.

We intend to use our website to

expedite public access to time-

critical information regarding the

Company in advance of or in lieu of

distributing a press release or a

filing with the SEC disclosing the

same information. |

Leading Home Health & Hospice

Management team

William F. Borne, Chairman and CEO

Founder and CEO since 1982

28 years leading the industry

Michael D. Snow, Chief Operating Officer

30 years leading health care operations

Wellmont, HealthSouth, HCA

Tim Barfield, Chief Development Officer

15 years of corporate development experience

Gov. Bobby Jindal , Vinson & Elkins, The Shaw Group

Dale E. Redman, CPA, Chief Financial Officer

34 years of senior level financial experience

Winward Capital, United Companies Financial

3

Jeffrey D. Jeter, Chief Compliance Officer

14 years of health care law and compliance expertise

Former Medicaid prosecutor, LA AG for DOJ

Michael O. Fleming, Chief Medical Officer

29 years as a family physician

Former President of AAFP, first industry CMO

G. Patrick Thompson, Chief Information Officer

23 years of corporate administration experience

Arthur Andersen, Turner Industries, The Shaw Group

David R. Bucey, General Counsel

24 years of experience in corporate law

Coca-Cola Company, McKenna Long & Aldridge |

Leading Home Health & Hospice

91%

9%

Home Health

Hospice

Company overview

1

4

•

Founded in 1982, publicly listed

1994

•

609 locations in 45 states

•

Leading provider of home health

services

-

Services include skilled nursing

and therapy services

•

Growing hospice business

•

95% of Home Health revenue is

episodic based (both Medicare &

non-Medicare)

17,200 employees

Home Health:

-

Daily visits = 35,000

-

9.1 million visits run rate in 2010

Hospice:

-

Average daily census = 2,816

-

Average length of stay = 87 days

2010 revenue guidance = $1.645 billion

1

For the quarter ended September 30, 2010

2

Provided as of the date of our Form 8-K filed with the Securities and Exchange

Commission on October 26, 2010. Stats

Revenue Mix

2 |

Leading Home Health & Hospice

Home Health Division

5

•

Industry leader

–

Strong national footprint –

537 locations across

45 states as of September 30

–

$369 million revenue in 3Q 2010

•

Strong clinical quality

•

Experienced divisional leadership

•

World-class technology platform + enhancing

operating platform

•

Well positioned to capitalize on organic and

market opportunities

Clinical Focus

Industry

Leading

Technology

Consolidator |

Leading Home Health & Hospice

Hospice Division

6

•

Solid trajectory of internal growth

–

28% YTD growth in 2010; 21% growth over 2009

–

$36 million revenue in 3Q 2010

•

Record patient census

–

Average daily census = 2,800+

•

Operational efficiencies and quality care

processes drive strong margins

–

Operating income margin = 20%

•

Partnered with the country’s largest and leading

Home Health company

–

Offering comprehensive continuum of at-home care

–

Collective resources to drive operational and clinical

excellence

–

Cross referral opportunities to drive growth

Essential to the

Care

Continuum

Experts in Pain

& Symptom

Management

Significant

Growth

Opportunity |

Leading Home Health & Hospice

2.0%

8.6%

33.9%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

+ 65 Population

Medicare Home Health

Spend

AMED Revenue

2005 -

2010 Compounded Annual Growth Rate

Strong Historical Industry Growth

7

1

Provided as of the date of our Form 8-K filed with the Securities and Exchange

Commission on October 26, 2010. Even Stronger Amedisys Growth

•

Employee headcount grew from 6,200 in 2005 to 17,000 today

•

221 Care Centers sites in 2005 to 609 today

•

$381M in revenues in 2005 to $1.645M projected for 2010

|

Leading Home Health & Hospice

Stronger Future Growth Expected

8

Sources: Centers for Disease Control and Prevention and CBO August 2010 Baseline

and Company historical information First Baby Boomer Turns 65 on 1/1/2011

•

A new baby boomer will turn 65 every eight seconds for the next 19 years

2.0%

8.6%

33.9%

3.2%

9.4%

?

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

+ 65 Population

Medicare Home Health Spend

AMED Revenue

2005-2010

2010-2020

Compounded Annual Growth Rate |

Leading Home Health & Hospice

$30

$32

$35

$38

$42

$45

$49

$54

$59

$64

$70

$507

$524

$566

$569

$617

$652

$684

$741

$771

$805

$878

$-

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Home Health & Hospice Spend

Medicare Spend

Medicare market size

9

Total Medicare vs. Home Health and Hospice

Spend

Source:

CBO's

March

2009

Baseline:

Medicare

home

health

revenue,

offset

by

cuts

in

Health

Care

Reform

Bills.

Kaiser

Family

Foundation

fact sheet August 2010. National Health Expenditure Projections, September

2010. •

Overall Medicare spend is expected to increase 68% during the next nine years

•

Medicare home health & hospice spend growing faster (119%), but only a fraction

of total Medicare spend |

Value

Proposition Home Health is the Low Cost Alternative

10

$50

Home Health

$5,765

Hospital

$544

Skilled Nursing

Facility

*

$5,293

Home Health

$28,191

Hospital

$14,688

Skilled Nursing Facility

Average cost per length of stay:

4.9 days

Hospital

Average length of stay:

Average per diem cost:

27 days

Skilled Nursing

Facility

106 days

Home Health

Leading Home Health & Hospice

Source: National Association for Home Health & Hospice, Medpac June 2010 Data Book

|

Leading Home Health & Hospice

2010 Challenges/Actions

•

Challenges

–

Volume short fall

•

Driven by decline in recertification rate

–

Exacerbated by recent trend in cost structure

•

Higher percent of salaried clinicians than historical norm

•

Had just completed investment in field resources

•

Actions

–

Portfolio Management

•

Closing/Merging 39 care centers

•

Reducing start-up pipeline

–

Operational Changes

•

Expanding home health to 11 regions headed by single VP’s

•

Expanding to two hospice regions

•

Increase field level decision making

•

Enhancing on-boarding and training

–

Cost Structure

•

Pay per visit back to historical norms

•

Focus on staffing and administrative efficiencies

–

Admit Growth

•

Ultimately drives long term success

•

Expand clinical programs

11

$18-22 million EBITDA improvement |

Leading Home Health & Hospice

Our Long

Term Strategy

12

Clinical

Excellence

Growth

Efficiency |

13

Quality Care Initiatives

“Research & Development”

Care Transition

Encore

Telehealth

Care Team Conference

Research & Development

Leading Home Health & Hospice

Improve Patient

Outcome -

Reduce ER &

Hospitalization |

Leading Home Health & Hospice

Focus on Clinical Outcomes

14

Amedisys

vs. Footprint –

Outcomes December 2009

•

Exceeded or met 11 out of 12 outcomes vs. footprint

•

Awarded $3.6 million in pay for performance demonstration project from CMS

1

Lower % is better

Source: Medicare 52

55

61

72

71

50

67

32

23

66

1

87

44

50

43

61

62

40

55

31

23

65

1

82

0

10

20

30

40

50

60

70

80

90

100

% of Patients

Amedisys

Footprint |

Leading Home Health & Hospice

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2006

2007

2008

2009

3Q10 YTD

Internal Episodic Admit Growth

Home Health Growth -

Internal

15

Historical

•

Specialty programs

•

Professional sales force / Mercury

Doc

•

Blanket start-ups

•

Clinical outcomes

Future

•

Specialty programs

•

Continued referral source communication

enhancements

•

Targeted start-ups

•

Clinical differentiation

•

Health system & hospital partnerships

Internal Admit Growth

1

1

Internal episodic-based admit growth is the

percent increase in our base/start-up episodic-based admissions for the period as a percent of the total episodic-based admissions of the prior period. |

Leading Home Health & Hospice

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2007

2008

2009

3Q10 YTD

Internal Episodic Admit Growth

Hospice Growth -

Internal

16

Hospice: Aggressive build (current share is ~1.2%)

•

$15 billion industry in the United States (NHPCO)

•

US hospice patient volumes projected to grow by 40% over next 5 years (NHPCO)

•

Building best hospice in the country based on clinical superiority

•

Duke School of Medicine’s Institute on Care at the End of Life

Internal Episodic Admit Growth

1

1

Internal episodic-based admit growth is the percent increase in our base/start-up

episodic-based admissions for the period as a percent of the total episodic-based admissions of the prior period. |

Leading Home Health & Hospice

Growth –

External

17

•

Acquisitions: Home Care

–

Continue to review opportunities

–

Focused

on

strategic

expansion

–

CON

markets,

footprint

expansion,

market

depth,

hospital

system joint ventures

–

Positioned well for increase in opportunities expected in 2011

•

Acquisitions: Hospice

–

Continue

to

pursue

opportunities

–

robust

pipeline

–

Focused

on

geographic

expansion

into

Amedisys

home

health

markets

and

market

depth

•

Other

–

Exploring

revenue

diversification

strategies

and

care

management

expansion

opportunities

–

Both internally developed or acquired |

Leading Home Health & Hospice

Consolidation Opportunities

18

•

Home health and hospice industries are highly fragmented

–

10,500 home health provider numbers

–

3,400 hospice provider numbers

•

Small market share of publicly traded companies

–

Account for 15% of home health Medicare revenue market

–

Account for 12.5% of hospice Medicare revenue market

•

Most are single-site, small, local or regional providers

–

Independently-owned agencies

–

Visiting nurse associations

–

Facility and hospital-based |

Leading Home Health & Hospice

Efficiency

19

•

Flexible Labor Structure

–

Increase pay per visit structure

–

Quicker adherence to staffing ratios

•

Infrastructure Investment

–

Upgrading accounting and HR system to Peoplesoft

•

More back office efficiency

•

Greater scalability

–

Field computer refresh

•

Enhancing field wireless communication

–

Continued investment in state-of-the-art operating system

–

Rolling out hospice point of care in 2011 |

Leading Home Health & Hospice

Valuation Headwinds

•

Regulatory focus on industry and Amedisys

–

Senate

Finance

Committee

industry

inquiry

(information requested from all four publicly

traded companies)

–

Securities

Exchange Commission investigation of all four publicly traded companies

–

Department of Justice investigation

•

Industry reimbursement challenges

–

Decline in 2011 reimbursement of 5.2%

–

Decline in 2012 reimbursement of 2.9% proposed

–

Rebasing in 2014

•

Amedisys

operational challenges and opportunities

20 |

Leading Home Health & Hospice

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2005 -2008 Average

2009

2010

Current

Healthcare Providers /1

Home Health /2

Amedisys

Historical Multiples

21

•

Home health component trading off its historical norms versus the larger

healthcare services sector

•

Amedisys

at a substantial discount to rest of the home health companies

Source: Bloomberg

*Composed of healthcare providers reported in Oppenheimer’s weekly

index Historical Healthcare Services Industry Multiples

|

Leading Home Health & Hospice

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

2006 -2008 Average

2009

2010 YTD /1

Healthcare Services /2

Home Health /3

Amedisys

Historical Revenue Growth

22

•

Historically, industry and Amedisys

growth much greater than wider health

care services sector

Historical Healthcare Services Revenue Growth

Source: Bloomberg

/1 2010 YTD revenue for 6 months ended 6/30/10; growth is calculated comparing 2010 YTD revenue to

2009 revenue for same period /2 Composed of healthcare providers reported in

Oppenheimer’s weekly index /3 Home Health peer group includes Gentiva, Almost Family and

LHC Group ; revenues from Gentiva’s divested CareCentrix business are backed out of revenues for the

measurement period |

Leading Home Health & Hospice

Review

•

High industry growth rate

•

Low cost sector in high cost healthcare industry

•

Substantial cost saving initiatives underway

•

Growth far in excess of historical industry norms

•

Scalable infrastructure

•

Reimbursement cuts to drive industry consolidation

•

Strong liquidity and capital position

•

Clinical quality and innovation

23

Tremendous

Opportunities |

Leading Home Health & Hospice

Financial Review

24 |

Leading Home Health & Hospice

Financial highlights

25

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

2004

2005

2006

2007

2008

2009

2010

Projected Revenue

Actual Revenue

EPS |

Leading Home Health & Hospice

26

Summary financial results

($ in millions, except per share data)

2008

2009

3Q09

3Q10

Net revenue

$1,187.4

$1,513.5

$388.3

$404.7

Period-over-period growth

70.1%

27.5%

20.7%

4.2%

Gross margin

624.8

789.0

204.6

198.4

Percent of revenue

52.6%

52.1%

52.7%

49.0%

CFFO

150.7

247.7

88.6

47.2

Adjusted EBITDA

1

181.4

261.8

69.1

51.9

Percent of revenue

15.3%

17.3%

17.8%

12.8%

Adjusted Fully-diluted EPS

2

$3.31

$4.89

$1.29

$0.89

1

Adjusted EBITDA is defined as net income attributable to Amedisys, Inc. before provision for

income taxes, net interest (income) expense, and depreciation and amortization plus certain

adjustments (i.e. TLC integration costs incurred in 2008 and/or certain items incurred in 2010

which are detailed in our Form 8-K filed with the Securities and Exchange Commission on October

26, 2010). Adjusted EBITDA should not be considered as an alternative to, or more meaningful

than, income before income taxes, cash flow from operating activities, or other traditional

indicators of operating performance. This calculation of adjusted EBITDA may not be comparable

to a similarly titled measure reported by other companies, since not all companies calculate

this non-GAAP financial measure in the same manner.

2

Adjusted diluted earnings per share is defined as diluted earnings per share plus the earnings

per share effect of certain adjustments (i.e. TLC integration costs incurred in 2008 and/or certain

items incurred in 2010 which are detailed in our Form 8-K filed with the Securities and

Exchange Commission on October 26, 2010). Adjusted diluted earnings per share should not be

considered as an alternative to, or more meaningful than, income before income taxes, cash

flow from operating activities, or other traditional indicators of operating performance. This

calculation of adjusted diluted earnings per share may not be comparable to a similarly titled

measure reported by other companies, since not all companies calculate this non-GAAP financial

measure in the same manner.

|

Leading Home Health & Hospice

27

Summary performance results

2008

2009

3Q09

3Q10

Agencies at period end

528

586

569

609

Period-over-period growth

49.2%

11.0%

12.7%

7.0%

Total visits

7,004,200

8,702,146

2,236,590

2,260,608

Period-over-period growth

62.8%

24.2%

19.0%

1.1%

Episodic-based admissions

199,371

231,782

57,767

63,472

Period-over-period growth

53.8%

16.3%

8.6%

9.9%

Episodic-based completed

episodes

353,076

411,975

105,107

104,997

Period-over-period growth

60.6%

16.7%

10.7%

-0.1%

Episodic-based revenue per

episode

$2,854

$3,166

$3,189

$3,294

Period-over-period growth

7.3%

10.9%

11.2%

3.3% |

Leading Home Health & Hospice

28

Summary balance sheet

Dec. 31, 2009

Sep. 30, 2010

Assets

Cash

$ 34.5

$ 128.0

Accounts Receivable, Net

150.3

136.5

Property and Equipment

91.9

117.8

Goodwill

786.9

790.4

Other

108.8

91.2

Total Assets

$ 1,172.4

$ 1,263.9

Liabilities and Equity

Debt

$ 215.2

$ 192.7

All Other Liabilities

220.9

223.0

Equity

736.3

848.2

Total Liabilities and Equity

$ 1,172.4

$ 1,263.9

Leverage Ratio

Leverage Ratio, Net of Cash

0.8x

0.7x

0.7x

0.3x |

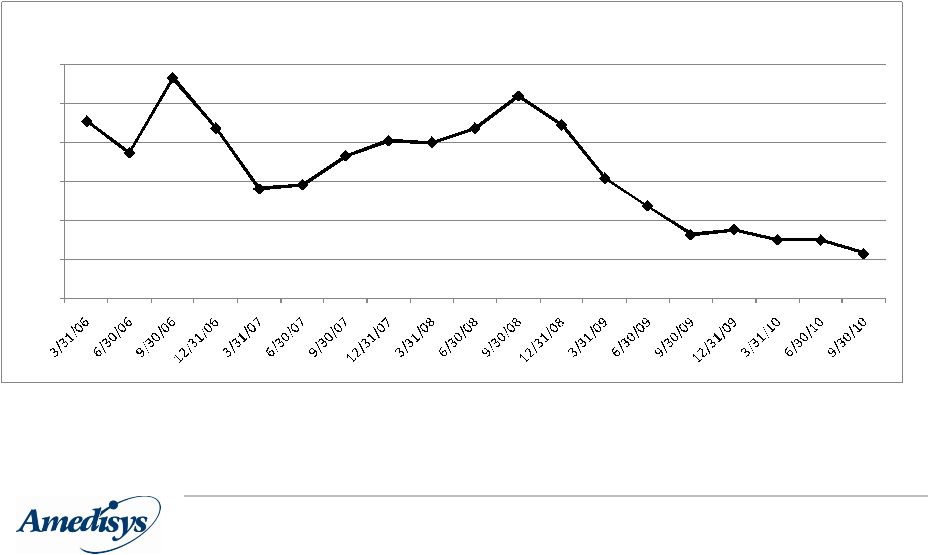

Leading Home Health & Hospice

47.7

43.7

53.3

46.8

39.1

39.6

43.3

45.2

45.0

46.8

51.0

47.2

40.4

36.9

33.2

33.9

32.6

32.5

30.8

25.0

30.0

35.0

40.0

45.0

50.0

55.0

DSO -

Net

(2)

29

Days revenue outstanding (DSO)

(1)

Our calculation of days revenue outstanding, net at March 31, 2008 is derived by dividing our

ending net patient accounts receivable (i.e. net of estimated revenue adjustments, allowance for doubtful accounts and

excluding the patient accounts receivable assumed in the TLC Health Care Services, Inc.

(“TLC”) and Family Home Health Care, Inc. & Comprehensive Home Healthcare Services, Inc. (“HMA”) acquisitions) by our average

daily net patient revenue, excluding the results of TLC and HMA for the three-month period

ended March 31, 2008. (2)

Our calculation of days revenue outstanding, net is derived by dividing our ending net patient

accounts receivable (i.e. net of estimated revenue adjustments and allowance for doubtful accounts) by our average daily net

patient revenue for the three-month period.

(1) |

Leading Home Health & Hospice

30

Liquidity

•

Cash balance at 9/30/10 = $128M

•

Available

line

of

credit

(LOC):

9/30/10

=

$235M

•

2010

Estimated

CFFO

-

Cap

Ex

=

$170M |

Leading Home Health & Hospice

31

Guidance

1

Calendar Year 2010

Net revenue:

$1.625 -

$1.645 billion

EPS:

$4.20 -

$4.35

Diluted shares

:

28.5 million

2

3

1

Guidance excludes the effects of future acquisitions, if they are made.

2

Provided as of the date of our Form 8-K filed with the Securities and Exchange Commission on

October 26, 2010. 3

Without adjustment for any shares that may be repurchased under our Share Repurchase Program. |

Leading Home Health & Hospice

Key references

32

Open Letter to Shareholders:

http://www.amedisys.com/pdf/Letter_to_Shareholders.pdf

Wyatt Matas Report: (upon request)

kevin.leblanc@amedisys.com

Avalere Study:

http://www.amedisys.com/pdf/avalere_results_051109.pdf

|

Leading Home Health & Hospice

Contact information

Kevin B. LeBlanc

Director of Investor Relations

Amedisys, Inc.

5959 S. Sherwood Forest Boulevard

Baton Rouge, LA 70816

Office: 225.292.2031

Fax: 225.295.9653

kevin.leblanc@amedisys.com

33 |