Attached files

| file | filename |

|---|---|

| 8-K - EMCORE 8-K 10-26-2010 - EMCORE CORP | form8k.htm |

Exhibit 99.1

October 26, 2010

EMCORE Corporation

2010 SRA Annual Fall Growth Stock Conference

Christopher Larocca, Chief Operating Officer

Mark Weinswig, Chief Financial Officer

2

Statements in this presentation which are not historical facts, and the

assumptions underlying such statements, constitute "forward-looking

statements" and assumptions underlying "forward-looking statements" within

the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the

Securities Exchange Act of 1934 including, but not limited to statements

regarding, (a) future product introductions and performance metrics, (b) 2010

and other future financial performance, and (c) future development and growth

in the Company’s markets. Readers should carefully review the risk factors set

forth in EMCORE's Annual Report on Form 10-K for the fiscal year ended

September 30, 2009, other reports filed with the SEC from time to time for a list

of factors that could cause our business prospects, financial condition,

operating results and cash flows to be materially adversely affected . These

forward-looking statements are made as of October 26, 2010, and EMCORE does

not assume any obligation to update these statements.

These forward-looking statements are based on management’s current

expectations or beliefs as of October 26, 2010 and are subject to numerous

assumptions, risks and uncertainties that could cause actual results to differ

materially from those described in the forward-looking statements.

“Safe Harbor” Statement

3

3

EMCORE’s Business Units

Global Communications and Power at the Speed of Light

Fiber Optic Components &

Systems for Broadband, 10G

Ethernet, Datacom & Telecom

Systems for Broadband, 10G

Ethernet, Datacom & Telecom

DataCom Component

Telecom Component

10 GE TRx (LX4, CX4)

Parallel Optical TRx

Fiber Optics

Broadband (EBB)

CATV Tx/Rx

FTTx Tx, PON TRx

RF over fiber links

Fiber-optic gyro

Video Transport

Space and Terrestrial

Solar Power Based on

Multi-Junction Solar Cells

Photovoltaics

Solar Power (EPV)

Space Solar Cells

Space Solar Panels

CPV Solar Cells

Emcore Solar

Power (ESP)

Solar Power System

Based on CPV Cells

4

XM-4 Radio

GEO - Boeing 702

Solar Cell Technology & Applications

5

§ Space Solar Cells

§ Highest efficiency commercially available space solar cells in the

industry

industry

§ Currently offer six generations of space solar cell with minimum

average efficiency of 27.0% to 29.5%

average efficiency of 27.0% to 29.5%

§ Lowest solar cell mass of 84 mg/cm2 and are fully space-

qualified with proven flight heritage

qualified with proven flight heritage

§ Satellite Solar CiC Assemblies

§ Highest efficiency commercially available CiCs in the industry

§ Extensive flight heritage for LEO, MEO, GEO and interplanetary

missions

missions

§ Satellite Solar Panels

§ Fully tested and wired for integration into solar array assemblies

§ Manufactured and tested per mission profile requirements in a

modern Class-10,000 clean room manufacturing high-bay under

continuous temperature and humidity environmental control

modern Class-10,000 clean room manufacturing high-bay under

continuous temperature and humidity environmental control

Overview of Space Solar Products

6

§ Current Status

§ Significant improved financial performance through cost reductions

§ Robust visibility: $126M new orders booked in 2009

§ Strong position (with >50% market share) to serve the commercial satellite markets

§ Outstanding reliability tracking record (zero failure for over 70 launched missions) and

customer recognition (numerous supplier excellence awards)

customer recognition (numerous supplier excellence awards)

§ Growth Strategy

§ Expand government and defense programs through establishment of Trusted Supplier Status

§ Provide more value added products to customers, e.g., solar panels instead of solar cells

§ Develop other applications enabled by the high efficiency of multi-junction solar cells

§ Major Customers

Industry Leader within Space Market

7

§ CPV's energy production is directly

related to the amount of DNI available

related to the amount of DNI available

§ To capture DNI, CPV systems require 2-

axis tracking to remain in direct line of

sight with the sun

axis tracking to remain in direct line of

sight with the sun

§ “Sweet spots” for CPV products are

geographic areas with optimal DNI

conditions and/or attractive incentive

programs such as Spain, Italy, China,

India, Australia, UAE and southwestern

U.S. states

geographic areas with optimal DNI

conditions and/or attractive incentive

programs such as Spain, Italy, China,

India, Australia, UAE and southwestern

U.S. states

CPV Receiver Module

Solar Flux

(1x)

(1x)

Fresnel Lens

Solar Flux

(500x-1000x)

(500x-1000x)

Direct Normal Irradiance

Concentrator Photovoltaics (CPV)

8

CPV Solar Cells - 60 1x1 cm2

solar cells on a 4” wafer

CPV Solar Cell Receiver - 1x1 cm2 cell

mounted on a heat sink with electric

connectors and a by-pass diode

Gen-III CPV Module - 15 1x1 cm2 CPV

solar cells integrated with 1,090X Fresnel

lens, producing 450W power

Gen-III CPV System - 36 CPV modules on

a tilt-and-roll tracker producing 16.2 kW power

• System operating on sun for approximately 7 months

• Ramping up production tooling and qualification (IEC,

CEC)

CEC)

• Very competitive cost platform allowing pricing against

silicon and thin film in areas with high DNI

silicon and thin film in areas with high DNI

• Clear roadmap for continued cost reductions through

increases in cell efficiencies, material costs, and system

optimization

increases in cell efficiencies, material costs, and system

optimization

Only Vertically Integrated CPV Supplier

9

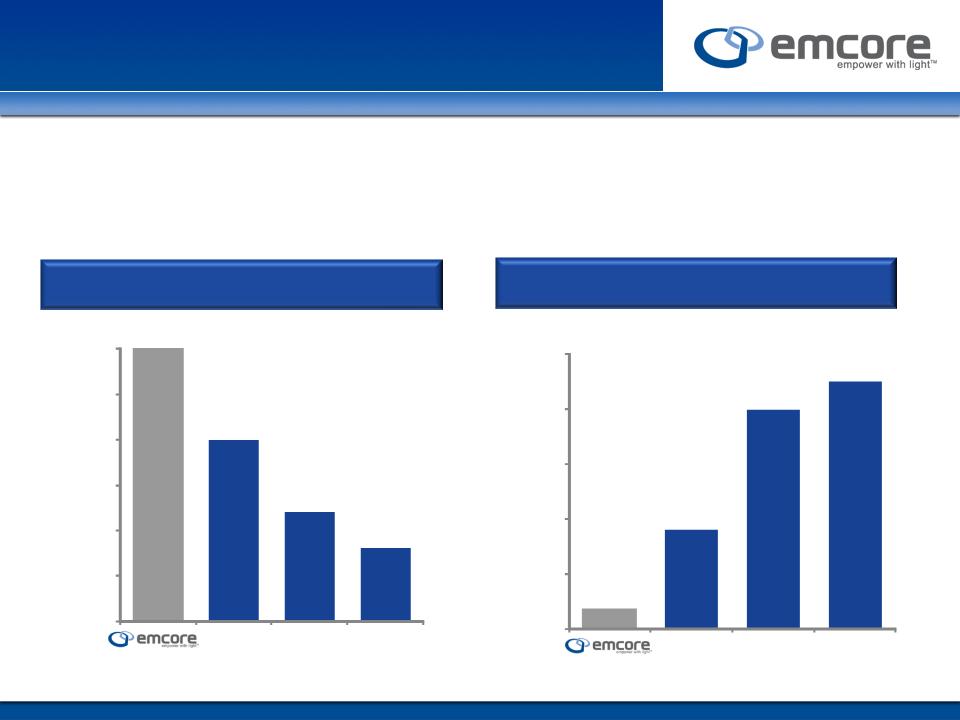

Key Advantages of CPV Technology

Module Efficiency

§ EMCORE Solar's leading efficiencies increase energy density, which lowers

per watt land acquisition costs

per watt land acquisition costs

§ EMCORE Solar’s capex expansion costs are a fraction of competitive

technologies

technologies

Source: Wall street research, company filings, EMCORE Solar management estimates

Gen III

29%

-

30%

15

-

20%

10

-

12%

6

-

8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

c

-

Si

CdTe

a

-

Si

Source: Wall street research, company filings, EMCORE Solar management estimates

Gen III

Capex per Watt

$0.18

$0.90

$2.00

$

2.00

-

$2.50

s

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

CdTe

a

-

Si

c

-

Si

10

CPV Solar Cell Technology Roadmap

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2005

2006-2007

2011 P

33.0%

Concentrator

Triple Junction

(CTJ)

36.0%

2nd Generation

Concentrator

Triple

Junction

(CTJ2)

42.0%

Inverted

Meta-

Morphic

Morphic

(IMM)

39.0%

3rd Generation

Concentrator

Triple

Junction

(CTJ3)

45.0%

2nd

Generation

(IMM2)

2012 P

30.0%

32.5%

35.0%

37.5%

40.0%

42.5%

45.0%

2008-2010

Year

45.0% - 50.0%

3rd

Generation

(IMM3)

>2013 P

Year-End Average Cell Efficiency

47.5%

50.0%

11

1550nm Transmitters,

Video Receivers,

PON Transceivers,

EDFA’s

Video Receivers,

PON Transceivers,

EDFA’s

RF Satellite Links

Tx/Rx/Delay Lines,

FOG’s, THz, Lithium

Niobate Devices

Tx/Rx/Delay Lines,

FOG’s, THz, Lithium

Niobate Devices

Analog Video,

HDTV/DTV Video, Mobile

Video and

IP Transport

HDTV/DTV Video, Mobile

Video and

IP Transport

CATV Transmitters &

Receivers, Subassembly

Boards, Lasers,

Photodiodes

Receivers, Subassembly

Boards, Lasers,

Photodiodes

SPECIALTY

VIDEO

FTTx

CATV

Comprehensive Broadband Products

12

● 2.5 & 5Gb/s per ch parallel

Optic Tx / Rx in SNAP-12

● 4-lane parallel TxRx OMC

● TxRx-based optical cable

Optic Tx / Rx in SNAP-12

● 4-lane parallel TxRx OMC

● TxRx-based optical cable

● 10 Gb/s VCSELs & PDs

● 10Gb/s DFB & PDs

● GPON TO Cans

● 1-10 Gb/s TOSA/ROSA

● 10Gb/s DFB & PDs

● GPON TO Cans

● 1-10 Gb/s TOSA/ROSA

Components

LAN / SAN

Parallel Optics

Telecom Transport

Telecom / Datacom Products

● Xenpak/X2 LX4, CX4, LR,

SR, ER TxRxs

● 1/2/4 Gb/s SFF/SFP TxRx

● SFP+ and XFP TxRxs

SR, ER TxRxs

● 1/2/4 Gb/s SFF/SFP TxRx

● SFP+ and XFP TxRxs

13

Fiber Optics Growth Strategy

§ Grow Business through Disruptive New Products

§ Tunable XFP transceivers and tunable TOSAs

§ m-ITLA for 40 and 100 Gb/s Telecom transponders

§ CXP pluggable modules and active cables based on parallel optic engines

§ Full-band Unicast QAM transmitters for HFC infrastructure

§ R-FOG transceivers to increase the bandwidth of HFC network

§ Fiber optic gyro transceivers

§ Expand Market Share of Current Product Portfolio

§ Nine product lines are being qualified by a leading OEM located in China

§ Increase penetration to international customer base

§ Grow Optical Components by Leveraging Low-cost Manufacturing Base

§ PON components

§ LAN/SAN optical components

14

Key Investment Considerations

§ Space Solar

§ Market and technology leader

§ Robust visibility & growth potential through government programs

§ Terrestrial CPV Solar

§ The only vertically integrated player from “cell-through-system”

§ Low-cost manufacturing through JV and advanced technology roadmap enabling price

competitiveness and business growth

competitiveness and business growth

§ Broadband Fiber Optics

§ Market and technology leader

§ CATV infrastructure upgrade continues within the HFC network

§ Telecom/Datacom Fiber Optics

§ Launch of disruptive tunable laser technology platform

§ New product introduction to capture new markets and applications

The Company Is Poised to Grow and Deliver Improved Profitability

October 26 2010

EMCORE Corporation

2010 SRA Annual Fall Growth Stock Conference

Christopher Larocca, Chief Operating Officer

Mark Weinswig, Chief Financial Officer