Attached files

| file | filename |

|---|---|

| EX-31.2 - CERTIFICATION OF CFO PURSUANT TO SECTION 302 - ZALE CORP | a2200315zex-31_2.htm |

| EX-4.2(B) - FIRST AMENDMENT TO CREDIT AGREEMENT - ZALE CORP | a2200315zex-4_2b.htm |

| EX-4.4(B) - FIRST AMENDMENT TO INTERCREDITOR AGREEMENT - ZALE CORP | a2200315zex-4_4b.htm |

| EX-31.1 - CERTIFICATION OF CEO PURSUANT TO SECTION 302 - ZALE CORP | a2200315zex-31_1.htm |

| EX-23.1 - CONSENT OF ERNST & YOUNG LLP - ZALE CORP | a2200315zex-23_1.htm |

| EX-32.2 - CERTIFICATION OF CFO PURSUANT TO SECTION 906 - ZALE CORP | a2200315zex-32_2.htm |

| EX-32.1 - CERTIFICATION OF CEO PURSUANT TO SECTION 906 - ZALE CORP | a2200315zex-32_1.htm |

| EX-10.16 - BASE SALARIES AND TARGET BONUS FOR THE NEO - ZALE CORP | a2200315zex-10_16.htm |

| EX-10.12 - OFFER LETTER TO RICHARD LENNOX - ZALE CORP | a2200315zex-10_12.htm |

| EX-10.15 - SEPARATION AND RELEASE AGREEMENT WITH MARY KWAN - ZALE CORP | a2200315zex-10_15.htm |

| EX-10.10(B) - OFFER LETTER TO THEO KILLION - ZALE CORP | a2200315zex-10_10b.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

For the fiscal year ended July 31, 2010

Zale Corporation

A Delaware Corporation

IRS Employer Identification No. 75-0675400

SEC File Number 1-04129

901 W. Walnut Hill Lane

Irving, Texas 75038-1003

(972) 580-4000

Zale Corporation's common stock, par value $0.01 per share, is registered pursuant to Section 12 (b) of the Securities Exchange Act of 1934 (the "Act") and is listed on the New York Stock Exchange. Zale Corporation does not have any securities registered under Section 12(g) of the Act. Zale Corporation is required to file reports pursuant to Section 13 of the Act. Zale Corporation (1) has filed all reports required to be filed by Section 13 or 15(d) of the Act during the preceding 12 months, and (2) has been subject to such filing requirements for the past 90 days.

Zale Corporation was not required to submit electronically and post on the Company's website Interactive Data Files required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months due to the Rule not being applicable to the Company for the current and previous periods.

Disclosure of the delinquent filers pursuant to Item 405 of Regulation S-K will not be contained in our definitive Proxy Statement, portions of which are incorporated by reference in Part III of this Form 10-K.

The aggregate market value of Zale Corporation's common stock (based upon the closing sales price quoted on the New York Stock Exchange) held by non-affiliates as of January 31, 2010 was $49,778,255. For this purpose, directors and officers have been assumed to be affiliates. As of October 1, 2010, 32,107,792 shares of Zale Corporation's common stock were outstanding.

Zale Corporation is a smaller reporting company filer and is not a well-known seasoned issuer.

Zale Corporation is not a shell company.

DOCUMENTS INCORPORATED BY REFERENCE.

Portions of Zale Corporation's definitive Proxy Statement for the 2010 Annual Meeting of Stockholders to be held on December 3, 2010 are incorporated by reference into Part III.

ZALE CORPORATION AND SUBSIDIARIES

General

We are, through our wholly owned subsidiaries, a leading specialty retailer of fine jewelry. At July 31, 2010, we operated 1,218 specialty retail jewelry stores and 672 kiosks located mainly in shopping malls throughout the United States of America, Canada and Puerto Rico.

We were incorporated in Delaware in 1993. Our principal executive offices are located at 901 W. Walnut Hill Lane, Irving, Texas 75038-1003. Our telephone number at that address is (972) 580-4000, and our internet address is www.zalecorp.com.

During the fiscal year ended July 31, 2010, we generated $1.6 billion of revenues. We compete in the approximately $61 billion U.S. and Canadian retail jewelry industry by leveraging our established brand names, economies of scale and geographic and demographic diversity. We have significant brand name recognition as a result of each of our brands' long-standing presence in the industry and our national and regional advertising campaigns. We believe that brand name recognition is an important advantage in jewelry retailing as jewelry products are generally unbranded and consumers must trust in a retailer's reliability, credibility and commitment to customer service.

Our business has changed significantly over the past few years. In November 2007, we sold our Bailey Banks & Biddle brand to Finlay Enterprises, Inc. We have closed a total of 265 underperforming locations during the last two fiscal years, of which 198 were fine jewelry stores and 67 were kiosks. In May 2010, we enhanced our liquidity by securing a $150 million Senior Secured Term Loan and extending our revolving credit agreement. In May 2010, we also entered into an agreement with TD Financing Services, Inc. ("TDFS"), a wholly-owned subsidiary of Toronto-Dominion Bank, to provide financing for our Canadian customers to purchase merchandise through private label credit cards. The agreement with TDFS replaced the agreement with Citi Cards Canada Inc., which expired on June 30, 2010. In September 2010, we entered into a five year agreement to amend and restate various terms of the Merchant Services Agreement with Citibank (South Dakota), N.A. ("Citibank"), to provide financing for our U.S. customers beginning October 1, 2010. The previous agreement with Citibank was scheduled to expire in March 2011.

Business Segments

We report our operations under three business segments: Fine Jewelry, Kiosk Jewelry and All Other. An overview of each business segment follows below. During fiscal year 2010, our Fine Jewelry segment generated $1.4 billion, or approximately 85 percent of our revenues. During fiscal year 2010, the Kiosk Jewelry segment revenues represented approximately $226 million, or 14 percent of our revenues.

Fine Jewelry

Our Fine Jewelry segment is comprised of five brands, predominantly focused on the value-oriented consumer as our core customer target. Each brand specializes in fine jewelry and watches, with merchandise and marketing emphasis focused on diamond products. Zales Jewelers® is our national brand in the U.S. providing moderately priced jewelry to a broad range of customers. Zales Outlet® operates in outlet malls and neighborhood power centers and capitalizes on Zales Jewelers'® national advertising and brand recognition. Gordon's Jewelers® is a value-oriented regional jeweler. Peoples Jewellers®, our national brand in Canada, provides customers with an affordable assortment and an accessible shopping experience. Mappins Jewellers® offers Canadian customers a broad selection of merchandise from engagement rings to fashionable and contemporary fine jewelry. In addition, we have made a strategic decision to expand our Fine Jewelry segment through the e-commerce sites, www.zales.com, www.zalesoutlet.com and www.gordonsjewelers.com.

1

Zales Jewelers and Gordon's Jewelers

Zales, our U.S. based flagship, is a leading brand name in jewelry retailing in the U.S., operating 675 stores in 50 states and Puerto Rico with an average store size of 1,685 square feet. Gordon's operates 192 stores in 29 states and Puerto Rico with an average store size of 1,521 square feet.

Zales is positioned as "The Diamond Store Since 1924" given its emphasis on diamond jewelry especially in the bridal and fashion segments. The Zales brand complements its merchandise assortments with promotional strategies to increase sales during traditional gift-giving periods and throughout the year. We believe that the prominence of diamond jewelry in our product selection and Zales' reputation for customer service for over 85 years fosters an image of product expertise, quality and trust among consumers.

Gordon's was founded in 1905 and its customers share similar demographic characteristics with the Zales customer. Accordingly, we have taken steps to position the brand to leverage our corporate strengths while focusing on product differentiation that will cater to local demographics. Gordon's features items in every major jewelry category including exclusive bridal designs, branded watches, gemstones, gold merchandise, and diamond fashion and solitaire products.

Zales Jewelers' and Gordon's Jewelers' combined revenues accounted for 60 percent of our total revenues, with an average transaction value of $396 in fiscal year 2010. Additionally, both brands operate as multi-channel retailers and serve internet customers through e-commerce sites: www.zales.com and www.gordonsjewelers.com, which accounted for approximately four percent of our total revenues in fiscal year 2010. Internet sales totaled $63.8 million in fiscal year 2010 compared to $56.2 million in fiscal year 2009.

Peoples Jewellers and Mappins Jewellers

In Canada, we operate 215 stores in nine provinces and enjoy the largest market share of any specialty jewelry retailer in Canada. Canadian operations consist of two brands, Peoples Jewellers and Mappins Jewellers, and accounted for 16 percent of our total revenues in fiscal year 2010. The average store size is 1,613 square feet with an average transaction value of $303 in fiscal year 2010.

Peoples Jewellers and Mappins Jewellers are two of the most recognized brand names in Canada. Peoples was founded in 1919 and offers jewelry at affordable prices, attracting a wide variety of Canadian customers. Using the trademark "Peoples the Diamond Store" in Canada, Peoples emphasizes its diamond business while also offering a wide selection of gold jewelry, gemstone jewelry and watches. Since 2000, the Peoples brand has built recognition through an aggressive television campaign. Over the past five years, Peoples had the largest television campaign of any Canadian jewelry retailer. Mappins Jewellers differentiates itself by offering exclusive merchandise primarily in its bridal assortments.

Zales Outlet

We operate 136 Zales Outlet stores in 35 states and Puerto Rico, sales from which accounted for 10 percent of our total revenues in fiscal year 2010. The average store size is 2,330 square feet, with an average transaction value of $438 in fiscal year 2010.

The outlet concept has evolved into three differentiated formats: power strip centers, traditional outlet malls and destination centers. Zales Outlet was established as an extension of the Zales brand and capitalizes on Zales' national advertising and brand recognition. Our stores feature items in every major jewelry category including branded watches, gemstones, gold merchandise, and diamond fashion and solitaire products. The merchandise assortment in a typical Zales Outlet store caters to the higher-income, female customer, offering 20 to 70 percent off traditional retail prices.

2

Kiosk Jewelry

The Kiosk Jewelry segment operates under the brand names Piercing Pagoda®, Plumb Gold™, and Silver and Gold Connection® (collectively, "Piercing Pagoda") through mall-based kiosks, and targets the opening price point jewelry customer. In May 2010, we expanded our presence in the Kiosk Jewelry segment through our e-commerce site, www.pagoda.com. At July 31, 2010, Piercing Pagoda operated 672 locations in 41 states and Puerto Rico. The Kiosk Jewelry segment specializes in gold and silver products, including entry level diamond merchandise, that capitalize on the latest fashion trends.

At the entry-level price point, the Kiosk Jewelry segment targets a young, fashion forward customer. The Kiosk segment offers an extensive collection of bracelets, earrings, charms, rings, and 14 karat and 10 karat gold chains, as well as a selection of silver and diamond jewelry, all in basic styles at moderate prices. In addition, trained associates perform ear-piercing services on site.

Kiosks are generally located in high traffic areas that are easily accessible and visible within regional shopping malls. The kiosk locations average 188 square feet in size, with an average transaction value of $40 in fiscal year 2010.

All Other

We provide insurance and reinsurance facilities for various types of insurance coverage, which are marketed primarily to our private label credit card customers, through Zale Indemnity Company, Zale Life Insurance Company and Jewel Re-Insurance Ltd. These three companies are the insurers (either through direct written or reinsurance contracts) of our customer credit insurance coverage. In addition to providing merchandise replacement coverage for certain perils, credit insurance coverage provides protection to the creditor and cardholder for losses associated with the disability, involuntary unemployment, leave of absence or death of the cardholder. Zale Life Insurance Company also provides group life insurance coverage for our eligible employees. Zale Indemnity Company, in addition to writing direct credit insurance contracts, has certain discontinued lines of insurance that it continues to service. Credit insurance operations are dependent on our retail sales through our private label credit cards. In fiscal year 2010, 36 percent of our private label credit card purchasers purchased some form of credit insurance. Under the current private label arrangement with Citibank, our insurance affiliates provide insurance to holders of our U.S. private label credit card and receive payments for such insurance products. On May 7, 2010, we entered into a five year Private Label Credit Card Program Agreement (the "TD Agreement") with TDFS to provide financing for our Canadian customers to purchase merchandise through private label credit cards beginning July 1, 2010. In addition, TDFS will provide credit insurance for our Canadian customers and will receive 40 percent of the net profits and the remaining 60 percent will be paid to us. The TD Agreement replaced the agreement with Citi Cards Canada Inc., which expired on June 30, 2010. In fiscal year 2010, the All Other segment accounted for approximately one percent of our total revenues.

Industry and Competition

Jewelry retailing is highly fragmented and competitive. We compete with a large number of independent regional and local jewelry retailers, as well as with other national jewelry chains. We also compete with other types of retailers who sell jewelry and gift items such as department stores, discounters, direct mail suppliers, online retailers and television home shopping programs. Certain of our competitors are non-specialty retailers, which are larger and have greater financial resources than we do. The malls where most of our stores are located typically contain competing national chains, independent jewelry stores and/or department store jewelry departments. We believe that we also are competing for consumers' discretionary spending dollars and, therefore, compete with retailers who offer merchandise other than jewelry or giftware. Therefore, we compete primarily on the basis of our reputation for high quality products, brand recognition, store location, distinctive and value-oriented merchandise, personalized customer service and ability to offer private label credit card programs to customers wishing to finance

3

their purchases. Our success also is dependent on our ability to both create and react to customer demand for specific merchandise categories.

The U.S. and Canadian retail jewelry industry accounted for approximately $61 billion of sales in 2009, according to publicly available data. We have a three percent market share in the combined U.S. and Canadian markets. The largest jewelry retailer in the combined U.S. and Canadian markets is believed to be Wal-Mart Stores, Inc. Other significant segments of the fine jewelry industry include national chain department stores (such as J.C. Penney Company, Inc.), mass merchant discount stores (such as Wal-Mart Stores, Inc.), other general merchandise stores, specialty retail jewelers (such as Signet Jewelers Limited) and apparel and accessory stores. The remainder of the retail jewelry industry is comprised primarily of catalog and mail order houses, direct-selling establishments, TV shopping networks (such as QVC, Inc.) and online jewelers.

We hold no material patents, licenses, franchises or concessions; however, our established trademarks and trade names are essential to maintaining our competitive position in the retail jewelry industry.

Operations by Brand

The following table presents revenues, average sales per location and the number of locations for each of our brands for the periods indicated.

| |

Year Ended July 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

Revenues (in thousands)

|

2010 | 2009 | 2008 | |||||||

Zales and Gordon's (including zales.com and gordonsjewelers.com) |

$ | 963,077 | $ | 1,110,419 | $ | 1,362,672 | ||||

Zales Outlet |

154,747 | 168,497 | 191,526 | |||||||

Peoples and Mappins(a) |

260,683 | 256,710 | 321,972 | |||||||

Piercing Pagoda (including pagoda.com)(b) |

226,187 | 232,809 | 249,489 | |||||||

Insurance revenues |

11,611 | 11,309 | 12,382 | |||||||

|

$ | 1,616,305 | $ | 1,779,744 | $ | 2,138,041 | ||||

Average Sales Per Location (in thousands)(c):

|

||||||||||

Zales and Gordon's |

$ | 1,034 | $ | 1,061 | $ | 1,251 | ||||

Zales Outlet |

1,147 | 1,149 | 1,350 | |||||||

Peoples and Mappins |

1,212 | 1,213 | 1,622 | |||||||

Piercing Pagoda |

338 | 330 | 328 | |||||||

- (a)

- Reflects

all revenue from Canadian operations, which constitutes all of our foreign operations. Long-lived assets from foreign operations

totaled approximately $35.4 million, $40.6 million and $47.0 million at July 31, 2010, 2009 and 2008, respectively.

- (b)

- In

May 2010, we commenced operations of an e-commerce site for Piercing Pagoda.

- (c)

- Based on merchandise sales for locations open a full 12 months during the applicable year.

4

| |

Locations by Brand | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

Year Ended July 31, 2010

|

Locations Opened During Period |

Locations Closed During Period |

Locations at End of Period |

|||||||

Zales and Gordon's |

— | 28 | 867 | |||||||

Zales Outlet |

— | 4 | 136 | |||||||

Peoples and Mappins |

6 | 3 | 215 | |||||||

Piercing Pagoda |

— | 12 | 672 | |||||||

|

6 | 47 | 1,890 | |||||||

Year Ended July 31, 2009

|

||||||||||

Zales and Gordon's |

3 | 153 | 895 | |||||||

Zales Outlet |

6 | 9 | 140 | |||||||

Peoples and Mappins |

5 | 1 | 212 | |||||||

Piercing Pagoda |

— | 55 | 684 | |||||||

|

14 | 218 | 1,931 | |||||||

Year Ended July 31, 2008

|

||||||||||

Zales and Gordon's |

19 | 45 | 1,045 | |||||||

Zales Outlet |

8 | 2 | 143 | |||||||

Peoples and Mappins |

16 | 1 | 208 | |||||||

Piercing Pagoda |

4 | 58 | 739 | |||||||

|

47 | 106 | 2,135 | |||||||

Business Segment Data

Information concerning sales and segment income attributable to each of our business segments is set forth below in Item 6, "Selected Financial Data," Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations," and in the "Notes to Consolidated Financial Statements," all of which are incorporated herein by reference.

Store Operations

Our stores are designed to differentiate our brands, create an attractive environment, make shopping convenient and enjoyable, and maximize operating efficiencies, all of which enhance the customer experience. We focus on store layout, with particular focus on arrangement of display cases, lighting, and choice of materials to optimize merchandise presentation. Promotional displays are changed periodically to provide variety or to reflect seasonal events.

Each of our stores is led by a store manager who is responsible for store-level operations, including overall store sales and personnel matters. Administrative matters, including purchasing, distribution and payroll, are consolidated at the corporate level to maintain efficiency and lower operating costs. In addition to selling jewelry, watches and gift items, each store also offers standard warranties and return policies, and provides extended warranty coverage that may be purchased at the customer's option. In order to facilitate sales, stores will hold merchandise in layaway, generally requiring a deposit of not less than 10 percent of the purchase price at the inception of the layaway transaction.

We have implemented inventory control systems, extensive security systems and loss prevention procedures to maintain low inventory losses. We screen employment applicants and provide our store personnel with training in loss prevention. Despite such precautions, we experience theft losses from time to time, and maintain insurance to cover such external losses.

5

We believe it is important to provide knowledgeable and responsive customer service and we maintain a strong focus on connecting with the customer, both through advertising and in-store communications and service. Our goal is to form and sustain an effective relationship with the customer from the first sale by maintaining a customer connection. We have a centralized customer service call center to effectively address customer service issues at lower aggregate cost.

We continue to focus on the level and frequency of our employee training programs, particularly with store managers and jewelry consultants. We provide selling and merchandise product training for all store personnel. During fiscal year 2010, we significantly expanded Diamond Council of America training to our store managers, district managers, regional directors and certain jewelry consultants.

Purchasing and Inventory

We purchase the majority of our merchandise in finished form from a network of established suppliers and manufacturers located primarily in the United States, India, Southeast Asia and Italy. We have a direct sourcing team that purchases products from 18 countries and we operate a manufacturing subsidiary that is our largest supplier of finished products. At the end of fiscal year 2010, approximately four percent and 14 percent of our total inventory represented raw materials and finished goods related to our manufacturing program and distribution center, respectively. All purchasing is done through buying offices at our corporate headquarters ("Store Support Center"). Consignment inventory has historically consisted of test programs, merchandise at higher price points or merchandise that otherwise does not warrant the risk of ownership. Consignment merchandise can be returned to the vendor at any time or converted to owned inventory if it meets certain sales thresholds. We had $81.1 million and $71.5 million of consignment inventory on hand at July 31, 2010 and 2009, respectively. During fiscal years 2010 and 2009, we purchased approximately 20 percent and 12 percent, respectively, of our finished merchandise from our top five vendors with no single vendor exceeding six percent in 2010. If our supply with these top vendors were disrupted, particularly at certain critical times during the year, our sales could be adversely affected in the short term until alternative supply arrangements could be established.

As a specialty retail jeweler, we could be affected by industry-wide fluctuations in the prices of diamonds, gold and other metals and stones. The supply and prices of diamonds in the principal world markets are significantly influenced by a single entity, Diamond Trading Company, which has traditionally controlled the sale of a substantial majority of the world's supply of diamonds and sells rough diamonds to worldwide diamond cutters at prices determined in its sole discretion. The availability of diamonds to Diamond Trading Company and our suppliers is to some extent dependent on the political environment in diamond-producing countries and on continuation of prevailing supply and marketing arrangements for raw diamonds. Until alternate sources are developed, any sustained interruption in the supply of diamonds could adversely affect us and the retail jewelry industry as a whole. The inverse is true with respect to any oversupply from diamond-producing countries, which could cause diamond prices to fall.

Proprietary Credit

Our private label credit card program helps facilitate the sale of merchandise to customers who wish to finance their purchases rather than use cash or other payment sources. We offer revolving and interest free credit plans under our private label credit card program. Approximately 40 percent of our U.S. sales, excluding Piercing Pagoda, which does not offer proprietary credit, were financed by proprietary credit in fiscal years 2010 and 2009. Our Canadian propriety credit card sales represented approximately 24 percent and 30 percent of Canadian total sales for fiscal years 2010 and 2009, respectively. In fiscal year 2010, our proprietary credit offerings included same-as-cash, revolving and interest free programs, all of which allowed our sales personnel to provide the customer a variety of financing options.

In March 2001, we entered into a 10-year agreement with Citibank under which Citibank issues private label credit cards branded with appropriate trademark, and provides financing for our U.S.

6

customers to purchase merchandise in exchange for payment by us of a merchant fee based on a percentage of each credit card sale. The merchant fee varies according to the credit plan that is chosen by the customer (i.e., revolving, interest free, same-as-cash). The agreement also enables us to write credit insurance. In September 2010, we entered into a five year agreement to amend and restate various terms of the Merchant Services Agreement with Citibank, to provide financing for our U.S. customers beginning October 1, 2010. The agreement with Citibank was scheduled to expire in March 2011.

In May 2010, we entered into a five year Private Label Credit Card Program Agreement with TDFS to provide financing for our Canadian customers to purchase merchandise through private label credit cards beginning July 1, 2010. The agreement with TDFS replaced the agreement with Citi Cards Canada Inc., which expired on June 30, 2010.

Employees

As of July 31, 2010, we had approximately 12,800 employees, of whom approximately 14 percent were Canadian employees and less than one percent of whom were represented by unions. Additionally, we usually hire temporary employees during November and December of each year, the Holiday season.

Seasonality

As a specialty retailer of fine jewelry, our business is seasonal in nature, with our second quarter, which includes the holiday months of November through January, accounting for a proportionally greater percentage of annual sales, earnings from operations and cash flow than the other three quarters. Other important periods include Valentine's Day and Mother's Day. We expect such seasonality to continue.

Information Technology

Our technology systems provide information necessary for: (i) store operations; (ii) inventory control; (iii) profitability monitoring by certain measures (merchandise category, buyer, store); (iv) customer service; (v) expense control programs; and (vi) overall management decision support. Significant data processing systems include point-of-sale reporting, purchase order management, replenishment, warehouse management, merchandise planning and control, payroll, general ledger, sales audit and accounts payable. Bar code ticketing and scanning are used at all point-of-sale terminals to ensure accurate sales and margin data compilation and to provide for inventory control monitoring. Information is made available online to merchandising staff on a timely basis, thereby increasing the merchants' ability to be responsive to changes in customer behavior. We are also improving the connectivity between stores and our Store Support Center to enhance operating effectiveness.

Our information technology systems and processes allow management to monitor, review and control operational performance on a daily, monthly, quarterly and annual basis for each store and each transaction. Senior management can review and analyze activity by store, amount of sale, terms of sale or employees who sell the merchandise.

We have a data center operations services agreement with a third party for the management of our client server systems, Local Area Network operations, Wide Area Network management and e-commerce hosting. In June 2010, we entered into a new services agreement that supersedes the agreement that was scheduled to expire in 2012. The new agreement requires fixed payments totaling $24.1 million over a 74-month period plus a variable amount based on usage. We believe that by outsourcing our data center operations, we are better able to focus our resources on developing and executing the strategic initiatives discussed in the Business section.

We have historically upgraded, and expect to continue to upgrade, our information systems to improve operations and support future growth. We estimate we will make capital expenditures of approximately $7 million in fiscal year 2011 for enhancements to our information systems and infrastructure.

7

Regulation

Our operations are affected by numerous federal and state laws that impose disclosure and other requirements upon the origination, servicing and enforcement of credit accounts and limitations on the maximum amount of finance charges that may be charged by a credit provider. In addition to our private label credit cards, credit to our customers is provided primarily through bank cards such as Visa®, MasterCard®, and Discover®. Regulations implementing the Credit Card Accountability Responsibility and Disclosure Act of 2009 imposed new restrictions on credit card pricing, finance charges and fees, customer billing practices and payment application that have negatively impacted the availability of credit to our customers. Any change in the regulation of credit which would materially limit the availability of credit to our traditional customer base could adversely affect our results of operations or financial condition.

We are subject to the jurisdiction of various state and other taxing authorities. From time to time, these taxing authorities conduct reviews or audits of the Company.

The sale of insurance products is also regulated. Our three wholly owned insurance companies are required to file reports with various insurance commissions, and are also subject to regulations relating to capital adequacy, the payment of dividends and the operation of their businesses generally. State laws also impose registration and disclosure obligations with respect to the credit and other insurance products that we sell to our customers. In addition, the providers of our private label credit programs are subject to disclosure and other requirements under state and federal law and are subject to review by the Federal Trade Commission and the state and federal banking regulators.

Merchandise in the retail jewelry industry is frequently sold at a discount off the "regular" or "original" price. We are subject to federal and state regulations requiring retailers offering merchandise at promotional prices to offer the merchandise at regular or original prices for stated periods of time. Additionally, we are subject to certain truth-in-advertising and various other laws, including consumer protection regulations that regulate retailers generally and/or the promotion and sale of jewelry in particular.

Available Information

We provide links to our filings with the Securities and Exchange Commission ("SEC") and to the SEC filings (Forms 3, 4 and 5) of our directors and executive officers under Section 16 of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), free of charge, on our website at www.zalecorp.com, under the heading "SEC Filings" in the "Investor Relations" section. These links are automatically updated, so the filings are available immediately after they are made publicly available by the SEC. These filings also are available through the SEC's EDGAR system at www.sec.gov.

Our certificate of incorporation and bylaws as well as the charters for the compensation, audit, nominating and corporate governance committees of our Board of Directors and the corporate governance guidelines are available on our website at www.zalecorp.com, under the heading "About Zale Corporation" in the "Corporate Governance" section.

We have a Code of Business Conduct and Ethics (the "Code"). All of our directors, executive officers and employees are subject to the Code. The Code is available on our web site at www.zalecorp.com, under the heading "About Zale Corporation" in the "Corporate Governance" section. Waivers of the Code, if any, for directors and executive officers would be disclosed in a SEC filing on Form 8-K or, to the extent permitted by law, on our website.

8

We make forward-looking statements in this Annual Report on Form 10-K and in other reports we file with the SEC. In addition, members of our senior management make forward-looking statements orally in presentations to analysts, investors, the media and others. Forward-looking statements include statements regarding our objectives and expectations with respect to our financial plan, sales and earnings, merchandising and marketing strategies, acquisitions and dispositions, share repurchases, store opening, renovation, remodeling and expansion, inventory management and performance, liquidity and cash flows, capital structure, capital expenditures, development of our information technology and telecommunications plans and related management information systems, e-commerce initiatives, human resource initiatives and other statements regarding our plans and objectives. In addition, the words "plans to," "anticipate," "estimate," "project," "intend," "expect," "believe," "forecast," "can," "could," "should," "will," "may," or similar expressions may identify forward-looking statements, but some of these statements may use other phrasing. These forward-looking statements are intended to relay our expectations about the future, and speak only as of the date they are made. We disclaim any obligation to update or revise publicly or otherwise any forward-looking statements to reflect subsequent events, new information or future circumstances.

Forward-looking statements are not guarantees of future performance and a variety of factors could cause our actual results to differ materially from the anticipated or expected results expressed in or suggested by these forward-looking statements.

If the general economy performs poorly, discretionary spending on goods that are, or are perceived to be, "luxuries" may not grow and may decrease.

Jewelry purchases are discretionary and may be affected by adverse trends in the general economy (and consumer perceptions of those trends). In addition, a number of other factors affecting consumers such as employment, wages and salaries, business conditions, energy costs, credit availability and taxation policies, for the economy as a whole and in regional and local markets where we operate, can impact sales and earnings. The economic downturn that began in 2008 has significantly impacted our sales and the continuation of this downturn, and particularly its worsening, would have a material adverse impact on our business and financial condition.

The concentration of a substantial portion of our sales in three relatively brief selling periods means that our performance is more susceptible to disruptions.

A substantial portion of our sales are derived from three selling periods—Holiday (Christmas), Valentine's Day and Mother's Day. Because of the briefness of these three selling periods, the opportunity for sales to recover in the event of a disruption or other difficulty is limited, and the impact of disruptions and difficulties can be significant. For instance, adverse weather (such as a blizzard or hurricane), a significant interruption in the receipt of products (whether because of vendor or other product problems), or a sharp decline in mall traffic occurring during one of these selling periods could materially impact sales for the affected period and, because of the importance of each of these selling periods, commensurately impact overall sales and earnings.

Most of our sales are of products that include diamonds, precious metals and other commodities. A substantial portion of our purchases and sales occur outside the United States. Fluctuations in the availability and pricing of commodities or exchange rates could impact our ability to obtain, produce and sell products at favorable prices.

The supply and price of diamonds in the principal world market are significantly influenced by a single entity, which has traditionally controlled the marketing of a substantial majority of the world's supply of diamonds and sells rough diamonds to worldwide diamond cutters at prices determined in its sole

9

discretion. The availability of diamonds also is somewhat dependent on the political conditions in diamond-producing countries and on the continuing supply of raw diamonds. Any sustained interruption in this supply could have an adverse affect on our business.

We also are affected by fluctuations in the price of diamonds, gold and other commodities. A significant change in prices of key commodities could adversely affect our business by reducing operating margins or decreasing consumer demand if retail prices are increased significantly. In addition, foreign currency exchange rates and fluctuations impact costs and cash flows associated with our Canadian operations and the acquisition of inventory from international vendors.

A substantial portion of our raw materials and finished goods are sourced in countries generally described as having developing economies. Any instability in these economies could result in an interruption of our supplies, increases in costs, legal challenges and other difficulties.

Our sales are dependent upon mall traffic.

Our stores and kiosks are located primarily in shopping malls throughout the U.S., Canada and Puerto Rico. Our success is in part dependent upon the continued popularity of malls as a shopping destination and the ability of malls, their tenants and other mall attractions to generate customer traffic. Accordingly, a significant decline in this popularity, especially if it is sustained, would substantially harm our sales and earnings. In addition, even assuming this popularity continues, mall traffic can be negatively impacted by weather, gas prices and similar factors.

We operate in a highly competitive and fragmented industry.

The retail jewelry business is highly competitive and fragmented, and we compete with nationally recognized jewelry chains as well as a large number of independent regional and local jewelry retailers and other types of retailers who sell jewelry and gift items, such as department stores and mass merchandisers. We also compete with internet sellers of jewelry. Because of the breadth and depth of this competition, we are constantly under competitive pressure that both constrains pricing and requires extensive merchandising efforts in order for us to remain competitive.

Any failure by us to manage our inventory effectively will negatively impact our financial condition, sales and earnings.

We purchase much of our inventory well in advance of each selling period. In the event we misjudge consumer preferences or demand, we will experience lower sales than expected and will have excessive inventory that may need to be written down in value or sold at prices that are less than expected, which could have a material adverse impact on our business and financial condition.

Any failure of our pricing and promotional strategies to be as effective as desired will negatively impact our sales and earnings.

We set the prices for our products and establish product specific and store-wide promotions in order to generate store traffic and sales. While these decisions are intended to maximize our sales and earnings, in some instances they do not. For instance, promotions, which can require substantial lead time, may not be as effective as desired or may prove unnecessary in certain economic circumstances. Where we have implemented a pricing or promotional strategy that does not work as expected, our sales and earnings will be adversely impacted.

10

Because of our dependence upon a small concentrated number of landlords for a substantial number of our locations, any significant erosion of our relationships with those landlords or their financial condition would negatively impact our ability to obtain and retain store locations.

We are significantly dependent on our ability to operate stores in desirable locations with capital investment and lease costs that allow us to earn a reasonable return on our locations. We depend on the leasing market and our landlords to determine supply, demand, lease cost and operating costs and conditions. We cannot be certain as to when or whether desirable store locations will become or remain available to us at reasonable lease and operating costs. Several large landlords dominate the ownership of prime malls, and we are dependent upon maintaining good relations with those landlords in order to obtain and retain store locations on optimal terms. From time to time, we do have disagreements with our landlords and a significant disagreement, if not resolved, could have an adverse impact on our business. In addition, any financial weakness on the part of our landlords could adversely impact us in a number of ways, including decreased marketing by the landlords and the loss of other tenants that generate mall traffic.

Any disruption in, or changes to, our private label credit card arrangements may adversely affect our ability to provide consumer credit and write credit insurance.

We rely on third party credit providers to provide financing for our customers to purchase merchandise and credit insurance through private label credit cards. Any disruption in, or changes to, our credit card agreements would adversely affect our sales and earnings.

Significant restrictions in the amount of credit available to our customers could negatively impact our business and financial condition.

Our customers rely heavily on financing provided by credit card companies to purchase our merchandise. The availability of credit to our customers is impacted by numerous factors, including general economic conditions and regulatory requirements relating to the extension of credit. Numerous federal and state laws impose disclosure and other requirements upon the origination, servicing and enforcement of credit accounts and limitations on the maximum amount of finance charges that may be charged by a credit provider. Regulations implementing the Credit Card Accountability Responsibility and Disclosure Act of 2009 imposed new restrictions on credit card pricing, finance charges and fees, customer billing practices and payment application that have negatively impacted the availability of credit to our customers. Future regulations or changes in the application of current laws could further impact the availability of credit to our customers. If the amount of available credit provided to our customers is significantly restricted, which recently has been the trend, our sales and earnings would be negatively impacted.

We are dependent upon our revolving credit agreement and other third party financing arrangements for our liquidity needs.

We have a revolving credit agreement and a Senior Secured Term Loan that contain various financial and other covenants. Should we be unable to fulfill the covenants contained in these loans, we would be unable to fund our operations without a significant restructuring of our business.

If the credit markets deteriorate, our ability to obtain the financing needed to operate our business could be adversely impacted.

We utilize a revolving credit agreement to finance our working capital requirements, including the purchase of inventory, among other things. If our ability to obtain the financing needed to meet these requirements was adversely impacted as a result of continued deterioration in the credit markets, our business could be significantly impacted. In addition, the amount of available borrowings under our revolving credit agreement is based, in part, on the appraised liquidation value of our inventory. Any declines in the appraised value of our inventory could impact our ability to obtain the financing necessary to operate our business.

11

Acquisitions and dispositions involve special risk, including the risk that we may not be able to complete proposed acquisitions or dispositions or that such transactions may not be beneficial to us.

We have made significant acquisitions and dispositions in the past and may in the future make additional acquisitions and dispositions. Difficulty integrating an acquisition into our existing infrastructure and operations may cause us to fail to realize expected return on investment through revenue increases, cost savings, increases in geographic or product presence and customer reach, and/or other projected benefits from the acquisition. In addition, we may not achieve anticipated cost savings or may be unable to find attractive investment opportunities for funds received in connection with a disposition. Additionally, attractive acquisition or disposition opportunities may not be available at the time or pursuant to terms acceptable to us and we may be unable to complete acquisitions or dispositions.

Ineffective accounting controls can have adverse impacts on the Company.

Under Federal law, we are required to maintain an effective system of internal controls over financial reporting. Should we not maintain an effective system, it would result in a violation of those laws and could impair our ability to produce accurate and timely financial statements. In turn, this could result in increased audit costs, a loss of investor confidence, difficulties in accessing the capital markets, and regulatory and other actions against us. Any of these outcomes could be costly to both our shareholders and us.

Changes in estimates, assumptions and judgments made by management related to our evaluation of goodwill and other long-lived assets for impairment could significantly affect our financial results.

Evaluating goodwill and other long-lived assets for impairment is highly complex and involves many subjective estimates, assumptions and judgments by our management. For instance, management makes estimates and assumptions with respect to future cash flow projections, terminal growth rates, discount rates and long-term business plans. If our actual results are not consistent with our estimates, assumptions and judgments by our management, we may be required to recognize impairments.

Additional factors that may adversely affect our financial performance.

Increases in expenses that are beyond our control including items such as increases in interest rates, inflation, fluctuations in foreign currency rates, higher tax rates and changes in laws and regulations, may negatively impact our operating results.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

We lease a 430,000 square foot facility, which serves as our corporate headquarters and primary distribution facility. The lease for this facility extends through March 2018. The facility is located in Las Colinas, a planned business development in Irving, Texas, near the Dallas/Fort Worth International Airport. Our Canadian distribution operation is conducted in a leased 26,280 square foot facility in Toronto, Ontario with a lease term through November 2014. We also lease a 20,000 square foot distribution and warehousing facility in Irving, Texas, with a lease term through June 2011, which serves as the Piercing Pagoda distribution center.

We rent our store retail space under leases that generally range in terms from 5 to 10 years and may contain minimum rent escalation clauses, while kiosk leases generally range from three to five years. Most of the store leases provide for the payment of base rentals plus real estate taxes, insurance, common area

12

maintenance fees and merchants association dues, as well as percentage rents based on the store's gross sales.

We lease 18 percent of our store and kiosk locations from Simon Property Group and 14 percent of our store and kiosk locations from General Growth Management, Inc. No other lessor accounts for 10 percent or more of our store and kiosk locations.

The following table indicates the expiration dates of our leases as of July 31, 2010:

Term Expires

|

Stores | Kiosks | Other(a) | Total | Percentage of Total |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

2011 |

9 | 5 | — | 14 | 0.7 | % | ||||||||||

2012 |

197 | 184 | 1 | 382 | 20.2 | % | ||||||||||

2013 |

156 | 221 | 1 | 378 | 20.0 | % | ||||||||||

2014 |

175 | 181 | — | 356 | 18.8 | % | ||||||||||

2015 and thereafter |

681 | 81 | 2 | 764 | 40.3 | % | ||||||||||

|

1,218 | 672 | 4 | 1,894 | 100.0 | % | ||||||||||

- (a)

- Other includes the Store Support Center, distribution centers and storage facilities.

Management believes that substantially all of the store leases expiring in fiscal year 2011 that it wishes to renew (including leases which expired earlier and are currently being operated under month-to-month extensions) will be renewed. We expect that leases will be renewed on terms not materially different than the terms of the expiring or expired leases. Management believes our facilities are suitable and adequate for our business as presently conducted.

ITEM 3. LEGAL PROCEEDINGS AND OTHER MATTERS

Information regarding legal proceedings is incorporated by reference from Note 19 to our consolidated financial statements set forth, under the heading, "Contingencies," in Part IV of this report.

ITEM 4A. EXECUTIVE OFFICERS OF THE REGISTRANT

The following individuals serve as our executive officers of the Company. Executive officers are elected by the Board of Directors annually, each to serve until his or her successor is elected and qualified, or until his or her earlier resignation, removal from office or death.

Name

|

Age | Position | |||

|---|---|---|---|---|---|

Theo Killion |

59 | Chief Executive Officer | |||

Matthew W. Appel |

54 | Executive Vice President and Chief Financial Officer | |||

Gilbert P. Hollander |

57 | Executive Vice President and Chief Merchant and Sourcing Officer | |||

Richard A. Lennox |

45 | Executive Vice President, Chief Marketing and E-Commerce Officer | |||

Executive Officers

The following is a brief description of the business experience of the Company's executive officers for at least the past five years.

Mr. Theo Killion has served as Chief Executive Officer of the Company since September 23, 2010. He served as President of the Company from August 5, 2008 to September 23, 2010, and as Interim Chief Executive Officer from January 13, 2010 to September 23, 2010. From January 23, 2008 to August 5, 2008, Mr. Killion served as Executive Vice President of Human Resources, Legal and Corporate Strategy. From

13

May 2006 to January 2008, Mr. Killion was employed with the executive recruiting firm Berglass+Associates, focusing on companies in the retail, consumer goods and fashion industries. From April 2004 through April 2006, Mr. Killion served as Executive Vice President of Human Resources at Tommy Hilfiger. From 1996 to 2004, Mr. Killion served in various management positions with Limited Brands.

Mr. Matthew W. Appel was named Executive Vice President of the Company effective May 2009 and appointed Chief Financial Officer of the Company on June 15, 2009. From March 2007 to May 2009, Mr. Appel served as Vice President and Chief Financial Officer of ExlService Holdings, Inc. Prior to ExlService Holdings, Inc, Mr. Appel was Vice President, BPO Product Management from 2006 to 2007 and Vice President, Finance and Administration BPO from 2003 through 2005 at Electronic Data Systems Corporation. From 2001 to 2003, Mr. Appel was the Senior Vice President, Finance and Accounting BPO at Affiliated Computer Services, Inc. Mr. Appel began his career with Arthur Andersen, where he spent seven years in their audit practice. Mr. Appel is a certified public accountant and certified management accountant.

Mr. Gilbert P. Hollander was appointed Executive Vice President and Chief Sourcing Officer in September 2007, and was given the additional title of Chief Merchant Officer on January 13, 2010. Prior to that appointment, Mr. Hollander served as President, Corporate Sourcing/Piercing Pagoda beginning in May 2006, and was given the additional title of Group Senior Vice President in August 2006. From January 2005 to August 2006, he served as President, Piercing Pagoda. Prior to and up until that appointment, Mr. Hollander served as Vice President of Divisional Merchandise for Piercing Pagoda, to which he was appointed in August 2003. Mr. Hollander served as Senior Vice President of Merchandising for Piercing Pagoda from February 2000 to August 2003. Prior to February 2000, Mr. Hollander held various management positions within Piercing Pagoda beginning in May of 1997.

Mr. Richard A. Lennox was named Executive Vice President, Chief Marketing Officer of the Company effective August 2009. Prior to joining the Company, Mr. Lennox served as Executive Vice President, Marketing Director at J. Walter Thompson—New York. Mr. Lennox started at J. Walter Thompson in 1989 and held various senior level marketing positions. He began his career in 1987 with AGB—London.

14

ITEM 5. MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock is listed on the New York Stock Exchange under the symbol "ZLC." The following table sets forth the high and low sale prices as reported on the NYSE for our common stock for each fiscal quarter during the two most recent fiscal years.

| |

2010 | 2009 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

High | Low | High | Low | |||||||||

First |

$ | 8.20 | $ | 4.73 | $ | 30.89 | $ | 14.03 | |||||

Second |

$ | 5.51 | $ | 2.08 | $ | 15.99 | $ | 1.17 | |||||

Third |

$ | 3.80 | $ | 1.83 | $ | 5.25 | $ | 0.92 | |||||

Fourth |

$ | 3.27 | $ | 1.39 | $ | 5.92 | $ | 3.04 | |||||

As of October 1, 2010, the Company's outstanding shares of common stock were held by approximately 570 holders of record. We have not paid dividends on the common stock since its initial issuance on July 30, 1993, and do not anticipate paying dividends on the common stock in the foreseeable future. In addition, our revolving credit agreement and our Senior Secured Term Loan limit our ability to pay dividends or repurchase our common stock. At July 31, 2010, we had borrowing availability under the revolving credit agreement of approximately $241.7 million. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources" and "Notes to Consolidated Financial Statements—Long-Term Debt."

15

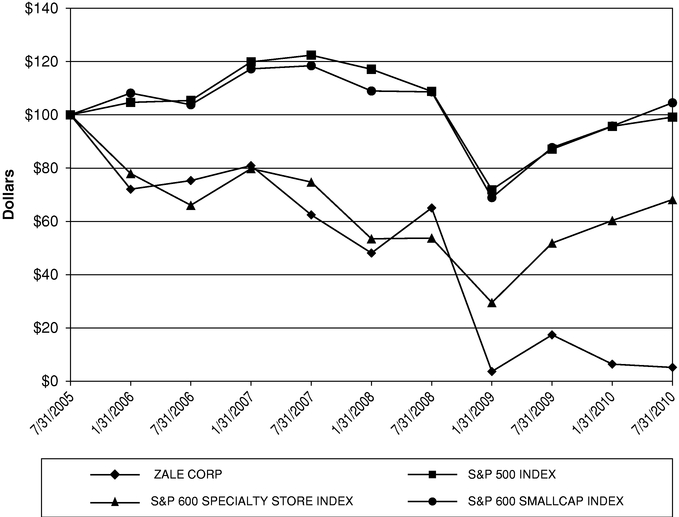

Corporate Performance Graph

The following graph shows a comparison of cumulative total returns for the Company, the S&P 500 Index, the S&P 600 Specialty Store Index and the S&P 600 Smallcap Index for the period from July 31, 2005 to July 31, 2010. The comparison assumes $100 was invested on July 31, 2005 in the Company's common stock and in each of the three indices and, for the S&P 500 Index, the S&P 600 Specialty Store Index and the S&P 600 Smallcap Index, assumes reinvestment of dividends. The Company has not paid any dividends during this period.

| |

7/31/05 | 1/31/06 | 7/31/06 | 1/31/07 | 7/31/07 | 1/31/08 | 7/31/08 | 1/31/09 | 7/31/09 | 1/31/10 | 7/31/10 | |||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Zale Corporation |

$ | 100.00 | $ | 72.09 | $ | 75.32 | $ | 80.94 | $ | 62.44 | $ | 48.12 | $ | 65.06 | $ | 3.65 | $ | 17.41 | $ | 6.41 | $ | 5.18 | ||||||||||||

S&P 500 |

100.00 | 104.67 | 105.38 | 119.86 | 122.38 | 117.10 | 108.80 | 71.86 | 87.09 | 95.68 | 99.14 | |||||||||||||||||||||||

S&P Smallcap Spec |

100.00 | 77.96 | 66.06 | 79.80 | 74.75 | 53.47 | 53.74 | 29.50 | 51.85 | 60.32 | 68.19 | |||||||||||||||||||||||

S&P 600 Smallcap |

100.00 | 108.15 | 103.78 | 117.25 | 118.42 | 108.94 | 108.62 | 68.93 | 87.70 | 95.79 | 104.51 | |||||||||||||||||||||||

The stock price performance depicted in the above graph is not necessarily indicative of future price performance. The Corporate Performance Graph shall not be deemed "soliciting material" or to be "filed" with the SEC, nor shall such information be incorporated by reference into any future filing by the Company under the Securities Act or the Exchange Act, except to the extent that the Company specifically incorporates the graph by reference in such filing.

16

ITEM 6. SELECTED FINANCIAL DATA

The following selected financial data is qualified in its entirety by our consolidated financial statements (and the related notes thereto) contained elsewhere in this Annual Report on Form 10-K and should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations." The statement of operations data and balance sheet data for each of the fiscal years ended July 31, 2010, 2009 and 2008 has been derived from our audited consolidated financial statements. The statement of operations and balance sheet data for each of the fiscal years ended July 31, 2007 and 2006 has been derived from our unaudited consolidated financial statements. During fiscal year 2008, we sold Bailey Banks & Biddle. As a result, their operations are reflected as discontinued operations in the following consolidated statements of operations. All amounts in the following table are in thousands, except per share amounts.

| |

Year Ended July 31, | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2009 | 2008 | 2007 | 2006 | |||||||||||||

Revenues |

$ | 1,616,305 | $ | 1,779,744 | $ | 2,138,041 | $ | 2,152,785 | $ | 2,153,955 | ||||||||

Costs and expenses: |

||||||||||||||||||

Cost of sales(a) |

802,172 | 948,572 | 1,089,553 | 1,029,553 | 1,044,876 | |||||||||||||

Selling, general and administrative(b) |

846,205 | 934,249 | 991,772 | 974,855 | 974,284 | |||||||||||||

Depreciation and amortization |

50,005 | 58,947 | 60,244 | 56,595 | 54,670 | |||||||||||||

Other charges (gains)(c) |

33,370 | 46,940 | (10,700 | ) | 9,658 | (1,900 | ) | |||||||||||

Operating (loss) earnings |

(115,447 | ) | (208,964 | ) | 7,172 | 82,124 | 82,025 | |||||||||||

Interest expense |

15,657 | 10,399 | 12,364 | 18,969 | 11,185 | |||||||||||||

Other gains(d) |

(6,564 | ) | — | (3,500 | ) | — | — | |||||||||||

(Loss) earnings before income taxes |

(124,540 | ) | (219,363 | ) | (1,692 | ) | 63,155 | 70,840 | ||||||||||

Income tax (benefit) expense |

(28,750 | ) | (53,015 | ) | 4,761 | 16,812 | 16,725 | |||||||||||

(Loss) earnings from continuing operations |

(95,790 | ) | (166,348 | ) | (6,453 | ) | 46,343 | 54,115 | ||||||||||

Earnings (loss) from discontinued operations, net of taxes |

2,118 | (23,155 | ) | 7,084 | 11,143 | (6,061 | ) | |||||||||||

Net (loss) earnings |

$ | (93,672 | ) | $ | (189,503 | ) | $ | 631 | $ | 57,486 | $ | 48,054 | ||||||

Basic net (loss) earnings per common share: |

||||||||||||||||||

(Loss) earnings from continuing operations |

$ | (2.99 | ) | $ | (5.21 | ) | $ | (0.15 | ) | $ | 0.95 | $ | 1.11 | |||||

Earnings (loss) from discontinued operations |

0.07 | (0.73 | ) | 0.16 | 0.23 | (0.13 | ) | |||||||||||

Basic net (loss) earnings per share |

$ | (2.92 | ) | $ | (5.94 | ) | $ | 0.01 | $ | 1.18 | $ | 0.98 | ||||||

Diluted net (loss) earnings per common share: |

||||||||||||||||||

(Loss) earnings from continuing operations |

$ | (2.99 | ) | $ | (5.21 | ) | $ | (0.15 | ) | $ | 0.95 | $ | 1.10 | |||||

Earnings (loss) from discontinued operations |

0.07 | (0.73 | ) | 0.16 | 0.22 | (0.12 | ) | |||||||||||

Diluted net (loss) earnings per share |

$ | (2.92 | ) | $ | (5.94 | ) | $ | 0.01 | $ | 1.17 | $ | 0.98 | ||||||

Weighted average number of common shares outstanding: |

||||||||||||||||||

Basic |

32,062 | 31,899 | 42,361 | 48,694 | 48,808 | |||||||||||||

Diluted |

32,062 | 31,899 | 42,476 | 48,995 | 49,211 | |||||||||||||

Balance Sheet Data: |

||||||||||||||||||

Working capital |

$ | 383,006 | $ | 460,885 | $ | 613,665 | $ | 774,778 | $ | 628,743 | ||||||||

Total assets |

1,160,381 | 1,230,972 | 1,415,260 | 1,600,144 | 1,449,639 | |||||||||||||

Long-term debt |

284,684 | 310,500 | 326,306 | 227,306 | 202,813 | |||||||||||||

Total stockholders' investment |

308,020 | 373,793 | 566,471 | 880,414 | 783,960 | |||||||||||||

- (a)

- In

fiscal years 2009 and 2006, cost of sales includes charges of $13.5 million and $18.7 million, respectively, related to inventory

impairments.

- (b)

- Fiscal year 2006 amount includes $12.1 million in executive severance costs.

17

- (c)

- Fiscal

year 2010 includes $33.4 million related to costs associated with store closures and store impairments. Fiscal year 2009 includes

$46.9 million related to costs associated with store closures, store impairments and goodwill impairments. Fiscal year 2008 includes a $12.6 million benefit associated with a change in

our vacation policy and a $1.9 million store impairment charge. Fiscal year 2007 includes a $7.2 million derivative loss and a $2.5 million charge related to store impairments.

Fiscal year 2006 includes asset impairment charges.

- (d)

- Fiscal year 2010 includes a gain of $8.3 million related to a decrease in the fair value of the warrants issued in connection with the Senior Secured Term Loan and a $1.7 million charge related to debt issuance costs attributable to the warrants. Fiscal year 2008 includes a gain of $3.5 million related to the sale of our interest in a diamond known as the "Incomparable Diamond."

Segment Data

We report our business under three segments: Fine Jewelry, Kiosk Jewelry and All Other. The All Other segment includes insurance and reinsurance operations. Operating earnings by segment are calculated before unallocated corporate overhead, interest and taxes but include an internal charge for inventory carrying cost to evaluate segment profitability. Unallocated costs are before income taxes and include corporate employee related costs, administrative costs, information technology costs, corporate facilities costs and depreciation and amortization. All amounts in the following table are in thousands.

| |

Year Ended July 31, | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Selected Financial Data by Segment

|

2010 | 2009 | 2008 | 2007 | 2006 | |||||||||||||

Revenues: |

||||||||||||||||||

Fine Jewelry(a) |

$ | 1,378,507 | $ | 1,535,626 | $ | 1,876,170 | $ | 1,876,580 | $ | 1,864,195 | ||||||||

Kiosk(b) |

226,187 | 232,809 | 249,489 | 262,627 | 276,619 | |||||||||||||

All Other |

11,611 | 11,309 | 12,382 | 13,578 | 13,141 | |||||||||||||

Total revenues |

$ | 1,616,305 | $ | 1,779,744 | $ | 2,138,041 | $ | 2,152,785 | $ | 2,153,955 | ||||||||

Depreciation and amortization: |

||||||||||||||||||

Fine Jewelry |

$ | 35,558 | $ | 42,407 | $ | 42,832 | $ | 39,933 | $ | 38,172 | ||||||||

Kiosk |

4,120 | 4,899 | 5,296 | 5,625 | 5,571 | |||||||||||||

All Other |

— | — | — | — | — | |||||||||||||

Unallocated |

10,327 | 11,641 | 12,116 | 11,037 | 10,927 | |||||||||||||

Total depreciation and amortization |

$ | 50,005 | $ | 58,947 | $ | 60,244 | $ | 56,595 | $ | 54,670 | ||||||||

Operating (loss) earnings: |

||||||||||||||||||

Fine Jewelry(c) |

$ | (84,818 | ) | $ | (192,683 | ) | $ | 18,909 | $ | 100,531 | $ | 87,450 | ||||||

Kiosk(d) |

13,133 | 2,465 | 9,905 | 6,170 | 19,212 | |||||||||||||

All Other |

4,731 | 5,706 | 5,641 | 6,780 | 6,443 | |||||||||||||

Unallocated(e) |

(48,493 | ) | (24,452 | ) | (27,283 | ) | (31,357 | ) | (31,080 | ) | ||||||||

Total operating (loss) earnings |

$ | (115,447 | ) | $ | (208,964 | ) | $ | 7,172 | $ | 82,124 | $ | 82,025 | ||||||

Assets(f): |

||||||||||||||||||

Fine Jewelry(g) |

$ | 820,353 | $ | 868,227 | $ | 987,369 | $ | 1,250,967 | $ | 1,108,569 | ||||||||

Kiosk(h) |

85,631 | 107,457 | 118,601 | 120,660 | 119,395 | |||||||||||||

All Other |

33,643 | 24,842 | 27,234 | 25,406 | 22,228 | |||||||||||||

Unallocated |

220,754 | 230,446 | 282,056 | 203,111 | 199,447 | |||||||||||||

Total assets |

$ | 1,160,381 | $ | 1,230,972 | $ | 1,415,260 | $ | 1,600,144 | $ | 1,449,639 | ||||||||

Capital expenditures: |

||||||||||||||||||

Fine Jewelry |

$ | 9,945 | $ | 18,702 | $ | 59,289 | $ | 47,433 | $ | 48,644 | ||||||||

Kiosk |

— | 420 | 3,266 | 3,036 | 7,750 | |||||||||||||

All Other |

— | — | — | — | — | |||||||||||||

Unallocated |

4,705 | 9,235 | 22,582 | 28,791 | 20,026 | |||||||||||||

Total capital expenditures |

$ | 14,650 | $ | 28,357 | $ | 85,137 | $ | 79,260 | $ | 76,420 | ||||||||

- (a)

- Includes $260.7, $256.7, $321.9, $272.0 and $229.6 million in fiscal years 2010, 2009, 2008, 2007 and 2006, respectively, related to foreign operations.

18

- (b)

- Includes

$2.8 million and $7.7 million in fiscal years 2007 and 2006, respectively, related to foreign operations. All foreign locations were

closed in fiscal year 2007.

- (c)

- Fiscal

year 2010 includes $32.3 million related to charges associated with store closures and store impairments. Fiscal year 2009 includes

$46.5 million related to charges associated with store closures, store impairments and goodwill impairments. Fiscal year 2009 also includes $13.5 million related to an inventory

impairment charge. Fiscal year 2008 includes a $1.9 million store impairment charge. Fiscal year 2007 includes a $2.0 million store impairment charge. Fiscal year 2006 includes

$22.1 million related to inventory impairment and asset impairment charges.

- (d)

- Fiscal

year 2010 includes a $1.1 million related to charges associated with store impairments. Fiscal year 2009 includes $0.4 million related

to costs associated with store closures. Fiscal year 2007 includes a $0.5 million charge related to store impairments. Fiscal year 2006 includes $1.2 million related to inventory

impairment and asset impairment charges.

- (e)

- Fiscal

year 2008 includes a $12.6 million benefit associated with a change in our vacation policy. Fiscal year 2007 includes a $7.2 million

derivative loss. Fiscal year 2006 includes $5.3 million related to asset impairment charges, a $13.4 million benefit related to the settlement of certain retirement plan obligations,

$12.1 million for executive severance, $2.4 million related to accrued percentage rent and a $1.7 million derivative loss. Also includes credits of $55.5, $60.1, $66.8, $66.7 and

$57.0 million in fiscal years 2010, 2009, 2008, 2007 and 2006, respectively, to offset internal carrying costs charged to the segments.

- (f)

- Assets

allocated to segments include fixed assets, inventories, goodwill and investments held by our insurance operations. Unallocated assets include cash,

prepaid assets such as rent, corporate office improvements and technology infrastructure.

- (g)

- Includes

$35.4, $40.6, $47.0, $37.5 and $28.8 million of fixed assets in fiscal years 2010, 2009, 2008, 2007 and 2006, respectively, related to

foreign operations.

- (h)

- Includes $0.5 million of fixed assets in fiscal years 2006 related to foreign operations. All foreign locations were closed in fiscal year 2007.

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

For important information regarding forward-looking statements made in this Management's Discussion and Analysis of Financial Condition and Results of Operations see "Item 1A—Risk Factors."

Overview

We are a leading specialty retailer of fine jewelry in North America. At July 31, 2010, we operated 1,218 fine jewelry stores and 672 kiosks located primarily in shopping malls throughout the United States of America, Canada and Puerto Rico.

We report our business under three operating segments: Fine Jewelry, Kiosk Jewelry and All Other. Our Fine Jewelry segment is comprised of five brands, predominantly focused on the value-oriented consumer. Each brand specializes in fine jewelry and watches, with merchandise and marketing emphasis focused on diamond products. These five brands have been aggregated into one reportable segment. The Kiosk Jewelry segment operates under the brand names Piercing Pagoda®, Plumb Gold™, and Silver and Gold Connection® through mall-based kiosks and is focused on the opening price point customer. The Kiosk Jewelry segment specializes in gold and silver products that capitalize on the latest fashion trends. The All Other segment includes our insurance and reinsurance operations, which offer insurance coverage primarily to our private label credit card customers.

Comparable store sales declined by 6.6 percent during fiscal year 2010. Gross margin increased by 370 basis points to 50.4 percent for the year ended July 31, 2010 compared to the same period in the prior year. The improvement in gross margin was primarily the result of a decline in merchandise discounts. Cost of sales for fiscal year 2010 includes an $8.3 million charge for certain slow moving inventory, compared to $15.2 million in the same period in the prior year, which increased gross margin by approximately 35 basis points. Operating margin improved by 460 basis points to a loss of 7.1 percent compared to a loss of 11.7 percent in the same period in the prior year.

19

On May 10, 2010, we entered into an agreement to amend and restate various terms of the revolving credit agreement with Bank of America N.A. and certain other lenders. The Amended and Restated Revolving Credit Agreement (the "Revolving Credit Agreement") consists of two tranches: (a) an extended tranche totaling $530 million, including seasonal borrowings of $88 million, maturing on April 30, 2014 and (b) a non-extending tranche totaling $120 million, including seasonal borrowings of $20 million, maturing on August 11, 2011. The commitments under the agreement from both tranches total $650 million, including seasonal borrowings of $108 million. The Revolving Credit Agreement is secured by a first priority security interest and lien on merchandise inventory, credit card receivables and certain other assets and a second priority security interest and lien on all other assets.

On May 10, 2010, we entered into a $150 million Senior Secured Term Loan (the "Term Loan") and a Warrant and Registration Rights Agreement (see below) with Z Investment Holdings, LLC, an affiliate of Golden Gate Capital. The Term Loan matures on May 10, 2015 and is secured by substantially all current and future intangible assets and a second priority security interest on merchandise inventory and credit card receivables. The proceeds received were used to pay down amounts outstanding under the Revolving Credit Agreement after payment of debt issuance costs incurred pursuant to the Revolving Credit Agreement and the Term Loan.

In connection with the execution of the Term Loan, we entered into a Warrant and Registration Rights Agreement (the "Warrant Agreement") with Z Investment Holdings, LLC. Under the terms of the Warrant Agreement, we issued 6.4 million A-Warrants and 4.7 million B-Warrants (collectively, the "Warrants") to purchase shares of our common stock, on a one-for-one basis, for an exercise price of $2.00 per share, which was below market value at the date of issuance. The Warrants, which are currently exercisable and which expire seven years after issuance, represent 25 percent of our common stock on a fully diluted basis (including the shares issuable upon exercise of the Warrants, and excluding certain out-of-the-money stock options) as of the date of the issuance. The fair value of the Warrants totaled $21.3 million as of the date of issuance.

On September 24, 2010, we amended the Term Loan with Z Investment Holdings, LLC. The amendment eliminated the Minimum Consolidated EBITDA covenant and our option to pay a portion of future interest payments in kind subsequent to July 31, 2010. As a result, all future interest payments will be made in cash. In consideration for the amendment, we paid Z Investment Holdings, LLC an aggregate of $25.0 million, of which $11.3 million was used to pay down the outstanding principal balance of the Term Loan, $1.2 million was a prepayment premium and $12.5 million was an amendment fee.

On May 7, 2010, we entered into a five year Private Label Credit Card Program Agreement (the "TD Agreement") with TD Financing Services Inc. ("TDFS"), a wholly-owned subsidiary of Toronto-Dominion Bank, to provide financing for our Canadian customers to purchase merchandise through private label credit cards beginning July 1, 2010. In addition, TDFS will provide credit insurance for our customers and will receive 40 percent of the net profits, as defined, and the remaining 60 percent will be paid to us. The TD Agreement replaced the agreement with Citi Cards Canada Inc., which expired on June 30, 2010.

On September 23, 2010, we entered into a five year agreement to amend and restate various terms of the Merchant Services Agreement with Citibank, to provide financing for our U.S. customers beginning October 1, 2010. The agreement with Citibank was scheduled to expire in March 2011.

During the fiscal year ended July 31, 2010, the average Canadian currency rate appreciated by approximately 12 percent relative to the U.S. dollar. Due to our Canadian operations being reported at the average U.S. dollar equivalent, the appreciation in the Canadian dollar resulted in a $27.9 million increase in reported revenues compared to fiscal year 2009, substantially offset by an increase in reported cost of sales and selling, general and administrative expenses of $13.1 million and $11.0 million, respectively. In addition, as a result of the appreciation in the Canadian dollar, we recorded gains associated with the settlement of Canadian accounts payable totaling $2.8 million during the fiscal year ended July 31, 2010 compared to losses of $7.6 million during the same period in the prior year.

20

Net earnings associated with lifetime warranties totaled $49.8 million for the year ended July 31, 2010, compared to $28.3 million for the same period in the prior year. The increase in net earnings is the result of a change in our warranty product from a two-year warranty to a lifetime warranty in fiscal year 2007. The revenues related to lifetime warranties are recognized on a straight-line basis over a five year period. As a result, revenues recognized will not be comparable until fiscal year 2012, when five years of revenue will be included in the consolidated statement of operations.

Comparable store sales include internet sales and exclude revenue recognized from warranties and insurance premiums related to credit insurance policies sold to customers who purchase merchandise under our proprietary credit programs. The sales results of new stores are included beginning with their thirteenth full month of operation. The results of stores that have been relocated, renovated or refurbished are included in the calculation of comparable store sales on the same basis as other stores. However, stores closed for more than 90 days due to unforeseen events (e.g., hurricanes, etc.) are excluded from the calculation of comparable store sales.

From time to time, we include non-GAAP measurements of financial information in Management's Discussion and Analysis of Financial Condition and Results of Operations. We use these measurements as part of our evaluation of the performance of the Company. In addition, we believe these measures provide useful information to investors, particularly in evaluating the performance of the Company in the current fiscal year as compared to prior periods.

Results of Operations

The following table sets forth certain financial information from our audited consolidated statements of operations expressed as a percentage of revenues and should be read in conjunction with our consolidated financial statements and notes thereto included elsewhere in this Form 10-K.

| |

Year Ended July 31, | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2009 | 2008 | |||||||||

Revenues |

100.0 | % | 100.0 | % | 100.0 | % | ||||||

Costs and expenses: |

||||||||||||

Cost of sales |

49.6 | 53.3 | 51.0 | |||||||||

Selling, general and administrative |

52.4 | 52.5 | 46.4 | |||||||||

Depreciation and amortization |

3.1 | 3.3 | 2.8 | |||||||||