Attached files

| file | filename |

|---|---|

| EX-21 - Sutor Technology Group LTD | v197494_ex21.htm |

| EX-23 - Sutor Technology Group LTD | v197494_ex23.htm |

| EX-32.1 - Sutor Technology Group LTD | v197494_ex32-1.htm |

| EX-31.1 - Sutor Technology Group LTD | v197494_ex31-1.htm |

| EX-32.2 - Sutor Technology Group LTD | v197494_ex32-2.htm |

| EX-31.2 - Sutor Technology Group LTD | v197494_ex31-2.htm |

| EX-10.14 - Sutor Technology Group LTD | v197494_ex10-14.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

(Mark

One)

x ANNUAL REPORT PURSUANT TO

SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the

fiscal year ended: June 30,

2010

o TRANSITION REPORT PURSUANT

TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the

transition period from ____________ to _____________

Commission

File No. 000-51908

SUTOR

TECHNOLOGY GROUP LIMITED

(Exact

name of registrant as specified in its charter)

|

Nevada

|

87-0578370

|

|

|

(State

or other jurisdiction of incorporation or

organization) |

(I.R.S.

Employer Identification

No.)

|

No

8, Huaye Road

Dongbang

Industrial Park

Changshu,

215534

People’s

Republic of China

(Address

of principal executive offices)

(86)

512-52680988

(Registrant’s

telephone number, including area code)

Securities

registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which

registered

|

|

|

Common

Stock, par value $0.001 per share

|

NASDAQ

Capital Market

|

Securities

registered pursuant to Section 12(g) of the Exchange Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act.Yes o No x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act.Yes o No x

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days. Yes x No o

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Website, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files). Yes o No o

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. o

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company. See the definitions of “large accelerated filer,”

“accelerated filer” and “smaller reporting company” in Rule 12b-2 of the

Exchange Act.

|

Large

Accelerated Filer o

|

Accelerated

Filer o

|

|

Non-Accelerated

Filer o (Do not

check if a smaller reporting company)

|

Smaller

reporting company x

|

Indicate

by check mark whether registrant is a shell company (as defined in Rule 12b-2 of

the

Act).

Yes o No x

As of

December 31, 2009 (the last business day of the registrant’s most recently

completed second fiscal quarter), the aggregate market value of the shares of

the registrant’s common stock held by non-affiliates (based upon the closing

sale price of such shares as reported on the NASDAQ Capital Market) was

approximately $20.2 million. Shares of the registrant’s common stock held

by each executive officer and director and each by each person who owns 10% or

more of the outstanding common stock have been excluded from the calculation in

that such persons may be deemed to be affiliates of the registrant. This

determination of affiliate status is not necessarily a conclusive determination

for other purposes.

There

were a total of 40,695,602 shares of the registrant’s common stock outstanding

as of September 24, 2010.

None.

SUTOR

TECHNOLOGY GROUP LIMITED

Annual

Report on FORM 10-K

For the Fiscal

Year Ended June 30, 2010

TABLE

OF CONTENTS

|

PART I

|

|||

|

Item 1.

|

Business.

|

2

|

|

|

Item 1A.

|

Risk Factors.

|

11

|

|

|

Item 1B.

|

Unresolved Staff Comments.

|

21

|

|

|

Item 2.

|

Properties.

|

21

|

|

|

Item 3.

|

Legal Proceedings.

|

22

|

|

|

Item 4.

|

(Removed and Reserved).

|

22

|

|

|

PART II

|

|||

|

Item 5.

|

Market for Registrant’s Common Equity, Related

Stockholder Matters and Issuer Purchases of Equity

Securities.

|

22

|

|

|

Item 6.

|

Selected Financial Data.

|

23

|

|

|

Item 7.

|

Management’s Discussion and Analysis of Financial

Condition and Results of Operations.

|

23

|

|

|

Item 7A.

|

Quantitative and Qualitative Disclosures About

Market Risk.

|

33

|

|

|

Item 8.

|

Financial Statements and Supplementary

Data.

|

33

|

|

|

Item 9.

|

Changes in and Disagreements with Accountants on

Accounting and Financial Disclosure.

|

33

|

|

|

Item 9A.

|

Controls and Procedures.

|

33

|

|

|

Item 9B.

|

Other Information.

|

34

|

|

|

PART III

|

|||

|

Item 10.

|

Directors, Executive Officers and Corporate

Governance.

|

34

|

|

|

Item 11.

|

Executive Compensation.

|

39

|

|

|

Item 12.

|

Security Ownership of Certain Beneficial Owners

and Management and Related Stockholder Matters.

|

40

|

|

|

Item 13.

|

Certain Relationships and Related Transactions,

and Director Independence.

|

42

|

|

|

Item 14.

|

Principal Accounting Fees and

Services.

|

44

|

|

|

PART IV

|

|||

|

Item 15.

|

Exhibits, Financial Statement

Schedules.

|

44

|

|

Special

Note Regarding Forward Looking Statements

In addition to historical

information, this report contains forward-looking statements within the meaning

of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the

Securities Exchange Act of 1934, as amended. We use words such as “believe,”

“expect,” “anticipate,” “project,” “target,” “plan,” “optimistic,” “intend,”

“aim,” “will” or similar expressions which are intended to identify

forward-looking statements. Such statements include, among others, those

concerning market and industry segment growth and demand and acceptance of new

and existing products; any projections of sales, earnings, revenue, margins or

other financial items; any statements of the plans, strategies and objectives of

management for future operations; and any statements regarding future economic

conditions or performance, as well as all assumptions, expectations,

predictions, intentions or beliefs about future events. You are cautioned that

any such forward-looking statements are not guarantees of future performance and

involve risks and uncertainties, as well as assumptions, which, if they were to

ever materialize or prove incorrect, could cause the results of the Company to

differ materially from those expressed or implied by such forward-looking

statements. Potential risks and uncertainties include, among other things,

factors such as:

|

·

|

Downturns

in the steel industry;

|

|

·

|

Competition

and competitive factors in the markets in which we

compete;

|

|

·

|

Our

heavy reliance on Shanghai

Huaye;

|

|

·

|

Increases

in our raw material costs;

|

|

·

|

General

economic and business conditions in China and in the local economies in

which we regularly conduct business, which can affect demand for the

Company’s products and services;

and

|

|

·

|

Changes

in laws, rules and regulations governing the business community in China

in general and the steel industry in

particular.

|

Additional

disclosures regarding factors that could cause our results and performance to

differ from results or anticipated performance are discussed in Item 1A, “Risk

Factors” included herein. All statements other than statements of historical

fact are statements that could be deemed forward-looking statements. We assume

no obligation and do not intend to update these forward-looking statements,

except as required by law.

Use

of Terms

Except as

otherwise indicated by the context, references in this report to:

|

·

|

“Company,”

“we,” “us” and “our” are to the combined business of Sutor Technology

Group Limited, a Nevada corporation, and its subsidiaries: Sutor BVI,

Changshu Huaye, Jiangsu Cold-Rolled and Ningbo

Zhehua;

|

|

·

|

“Sutor

BVI” are to our wholly-owned subsidiary Sutor Steel Technology Co., Ltd.,

a BVI company;

|

|

·

|

“Changshu

Huaye” are to our wholly-owned subsidiary Changshu Huaye Steel Strip Co.,

Ltd., a PRC company;

|

|

·

|

“Jiangsu

Cold-Rolled” are to our wholly-owned subsidiary Jiangsu Cold-Rolled

Technology Co., Ltd., a PRC

company;

|

|

·

|

“Ningbo

Zhehua” are to our wholly-owned subsidiary Ningbo Zhehua Heavy Steel Pipe

Manufacturing Co., Ltd., a PRC

company;

|

|

·

|

“Shanghai

Huaye” are to Shanghai Huaye Iron & Steel Group Co., Ltd., a PRC

company of which Lifang Chen, our major shareholder and chief executive

officer, and her husband Feng Gao, are 100% owners, and its

subsidiaries;

|

|

·

|

“SEC”

are to the United States Securities and Exchange

Commission;

|

|

·

|

“Securities

Act” are to the Securities Act of 1933, as amended, and “Exchange Act” are

to the Securities Exchange Act of 1934, as

amended.

|

|

·

|

“China”

and “PRC” are to People’s Republic of

China;

|

|

·

|

“BVI”

are to the British Virgin Islands;

|

|

·

|

“RMB”

are to Renminbi, the legal currency of China;

and

|

|

·

|

“U.S.

dollar,” “$” and “US$” are to the legal currency of the United

States.

|

PART

I

|

ITEM

1.

|

BUSINESS.

|

We are

one of the leading Chinese private manufacturers of fine finished steel products

used by steel fabricators and in other applications. We utilize a variety of

processes and technological methodologies to convert steel manufactured by third

parties into fine finished steel products. Our product offerings are focused on

higher margin, value-added finished steel products, specifically, hot-dip

galvanized steel (“HDG Steel”), and prepainted galvanized steel (“PPGI”). In

addition, we produce acid pickled steel (“AP Steel”), and cold-rolled steel,

which represent the less processed of our finished products. As a

result of our acquisition of Ningbo Zhehua in November 2009, our product

offerings have expanded to include welded steel pipe products. A

large portion of our AP Steel and cold-rolled steel is used for our production

of HDG Steel and PPGI products. Our vertical integration has allowed us to

maintain more stable margins for our HDG Steel and PPGI products.

We sell

most of our products to customers who operate primarily in the solar energy,

appliances, automobile, construction, infrastructure, medical equipment and

water resource industries. Most of our customers are located in China. Our

primary export markets are Europe, Middle East, South America and Hong

Kong.

Through

our manufacturing facilities located in Changshu, China, we currently have three

HDG Steel production lines, one PPGI production line, one AP Steel production

line and one cold-rolled steel line. Our current annual designed production

capacity is approximately 700,000 metric tons, or MT, for HDG Steel, 200,000 MT

for PPGI, 500,000 MT for AP Steel and 250,000 MT for cold-rolled steel. Ningbo

Zhehua, our subsidiary located in Ningbo, currently has an annual capacity of

400,000 MT for welded steel pipe products.

History

and Corporate Structure

We were

incorporated on May 1, 1997 in the State of Nevada under the name Bronze

Marketing, Inc. and changed our name to Sutor Technology Group Limited effective

March 6, 2007 as a result of our reverse acquisition of Sutor BVI in February

2007. From inception until December 31, 2002, we engaged in the business of

providing inventory financing to facilitate the marketing and sale of bronze

sculptures and other artwork. The business was not successful and we

discontinued our active business operations as of December 31, 2002. From

December 31, 2002 until the reverse acquisition of Sutor BVI on February 1,

2007, we engaged in no active business operations.

On

February 1, 2007, we acquired Sutor BVI through a share exchange transaction

pursuant to which the stockholders of Sutor BVI transferred all capital stock of

Sutor BVI to us in exchange for 85.2% ownership of our Company. Our acquisition

of Sutor BVI was accounted for as a recapitalization effected by a share

exchange, wherein Sutor BVI is considered the acquirer for accounting and

financial reporting purposes. The assets and liabilities of the acquired entity

have been brought forward at their book value and no goodwill has been

recognized.

In

November 2009, our subsidiary Changshu Huaye acquired 100% equity interest in

Ningbo Zhehua for the total purchase price of RMB 45,172,855.34 (approximately

$6.6 million).

2

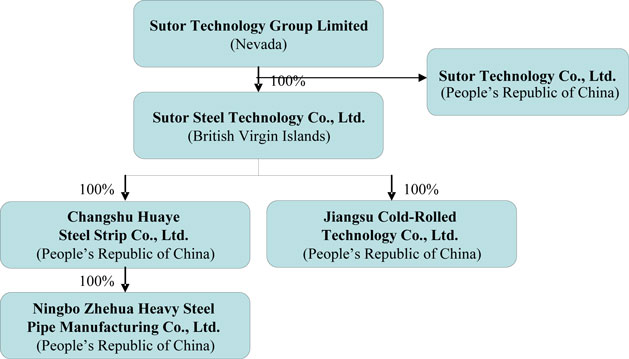

The

following chart reflects our organizational structure as of the date of this

annual report:

.

Reportable

Segment Information

Our three

reportable operating segments are categorized according to our three

subsidiaries:

|

|

·

|

Changshu

Huaye, which manufactures and sells HDG Steel and PPGI

products;

|

|

|

·

|

Jiangsu

Cold-Rolled, which manufactures and sells HDG Steel, AP Steel and

cold-rolled steel; and

|

|

|

·

|

Ningbo

Zhehua, which manufactures and sells welded steel pipe

products.

|

Changshu

Huaye and Jiangsu Cold-Rolled are located adjacent to each other in Changshu,

China and use largely the same management resources. Ningbo Zhehua is located in

Ningbo, China. For additional information about each segment, see Item 7,

“Management’s Discussion and Analysis of Financial Condition and Result of

Operations” and Note 11, “Segment Information” to the consolidated financial

statements included elsewhere in this annual report.

Our

Products

Our

current products include HDG Steel, PPGI, AP Steel, cold-rolled steel and welded

steel pipe products. Our HDG Steel and PPGI products are primarily manufactured

by Changshu Huaye and our AP Steel and cold-rolled steel products are primarily

manufactured by Jiangsu Cold-Rolled. Jiangsu Cold-Rolled added two new HDG Steel

production lines and has started to manufacture HDG of both cold-rolled

steel and hot-rolled steel since the end of September 2008. Ningbo Zhehua

manufactures our welded steel pipe products.

We were

certified ISO 9001:2000 for our quality management system in 2005, ISO

14001:2004 for our environmental management system in 2008, and GD/T28001:2001

for our occupational health and safety management system in 2008.

3

The

following table set forth sales information about our product mix in last two

fiscal years.

(All

amounts, other than percentage, in millions of U.S. dollars)

|

Fiscal Years Ended June 30,

|

||||||||||||||||

|

2009

|

2010

|

|||||||||||||||

|

Product

|

Revenue

|

Percent of Sales

|

Revenue

|

Percent of Sales

|

||||||||||||

|

HDG

Steel

|

$ | 108.3 | 25.2 | % | $ | 228.69 | 47.8 | % | ||||||||

|

PPGI

|

144.8 | 33.7 | % | 78.6 | 16.4 | % | ||||||||||

|

AP

Steel

|

49.1 | 11.4 | % | 40.3 | 8.4 | % | ||||||||||

|

Cold-Rolled

Steel

|

30.3 | 7.1 | % | 57.8 | 12.1 | % | ||||||||||

|

Welded

Steel Pipe Products

|

88.3 | 20.5 | % | 62.4 | 13.0 | % | ||||||||||

|

Other

|

9.0 | 2.1 | % | 10.9 | 2.3 | % | ||||||||||

|

Total

|

$ | 429.8 | 100.0 | % | $ | 478.69 | 100.0 | % | ||||||||

HDG

Steel

Using a

technology called hot-dip galvanizing, we manufacture corrosion-resistant and

zinc-coated HDG Steel in different dimensions and using different materials and

specifications requested by our customers. HDG Steel products are manufactured

from steel substrate of cold-rolled or hot-rolled picked coils by applying zinc

to the surface of the material to enhance its corrosion protection. HDG Steel

products are principally used in the electrical household appliance and

construction markets.

We

produce not only common industrial specifications, but also extreme

specifications that we believe only a few other large PRC state-owned steel

manufacturers can produce. The following table compares our technical

manufacturing capabilities for most of our products:

|

Width (mm)

|

Thickness (mm)

|

Galvanized Layer Weight (g/m2 )

|

||||

|

Our

Specification Scope

|

700-1250

|

0.18-1.5

|

70-280

|

|||

|

Industrial

Common Specification Scope

|

700-1250

|

0.3-1.2

|

100-180

|

We also

are technologically capable of manufacturing more extreme specifications of up

to 1300mm wide and 0.16mm thick HDG of cold-rolled steel. As a result, we

maintain a competitive advantage in extreme specification technology in terms of

thickness and the weight of the galvanized layer of our products. We have the

flexibility to adjust production specifications to meet changes in market

demand.

Sales of

HDG Steel products to third parties amounted to approximately 58,496 MT in

fiscal year 2010, representing approximately 7.6% of our total revenue. The

remaining HDG Steel products, which represent a majority of our HDG Steel

products, were used for our production of PPGI products. Currently, our HDG

Steel products are manufactured by Changshu Huaye and Jiangsu Cold-Rolled.

Changshu Huaye produces only HDG of cold-rolled steel. Jiangsu Cold-Rolled added

two new HDG Steel production lines which are capable of galvanizing both

hot-rolled and cold-rolled steel with both zinc and aluminum. These two new

production lines became operational at the end of September 2008. The addition

of the new production lines significantly expanded our production capacity of

HDG Steel, which increased designed production capacity from 300,000 MT per year

to 700,000 MT per year.

With the

new production lines, we offer HDG of hot-rolled steel, which we believe is more

cost-efficient than production of HDG of cold-rolled steel because production of

HDG steel products occurs directly on hot-rolled steel and, therefore, avoids

the procedure of cold rolling hot-rolled steel. HDG of hot-rolled steel is

generally thicker than HDG of cold-rolled steel with a specification range of

1.5mm to 4.5mm in terms of thickness.

PPGI

Products

PPGI

products are typically made to order based on customer specifications. Our PPGI

products’ specification generally ranges from 700mm to 1250mm in width and from

0.2mm to 1.2mm in thickness. Our PPGI products are used mostly in solar energy,

appliances and construction materials. We produce our PPGI by color-coating on

HDG of cold-rolled steel and then coating them in various colors, including

ivory white, ocean blue, pink and any other color according to customer

requirements. Our PPGI production line is equipped with the latest twice baking

and coating technology, which together with indirect heating, enhances the color

coated layers adhesion to the galvanized zinc layer.

4

Sales of

PPGI products amounted to approximately 96,676 MT in fiscal year 2010,

representing approximately 16.4% of our total revenue. Through our vertical

integration strategy, we currently self-supply approximately 66.2% of HDG of

cold-rolled steel to our PPGI production.

AP

Steel

Our AP

Steel production line became operative in September 2006. Acid pickling is a

process that removes scales and oxides from the steel surface by pickling, cold

rolling and annealing. AP Steel products are used mostly as a raw material for

cold-rolled steel strip, HDG Steel, as well as components of automobile and

manufacturing equipment. AP steel products come in several different dimensions

and using different materials and different specifications.

Most of

our AP Steel products are used for our own production of HDG Steel and full-hard

cold-rolled steel. We also sell a small portion of our AP Steel products to the

market. In fiscal year 2010, our sales of AP Steel products to third parties

were approximately 16,724 MT, representing approximately 2.2% of our total

revenue.

Full-Hard,

Cold-rolled Steel Products

Our

manufacturing of full-hard, cold-rolled steel products commenced in January

2007. Full-hard cold-rolled steel strips are treated in an annealing process and

are used to produce HDG of cold-rolled steel. We produce full-hard cold-rolled

steel strips through a reverse cold rolling mill.

We use

most of the full-hard cold-rolled steel strips for our production of HDG of

cold-rolled steel. The remaining undergoes the annealing process and is sold to

the market. Our sales of full-hard cold-rolled steel products to third parties

amounted to approximately 24,110 MT in fiscal year 2010, representing

approximately 3.1% of our total revenue. In addition, approximately 66.2% of

cold-rolled steel products were used for our own production.

Welded

Steel Pipe Products

Our

subsidiary Ningbo Zhehua has one advanced JCOE production line for

large-diameter, double-side, submerged-arc welded steel pipes, three US Lincoln

production lines for spiral seam, double-side, submerged-arc welded steel pipes

and two REF production lines for roll-bending, double-side, submerged-arc welded

steel pipes. Ningbo Zhehua is specialized in manufacturing

large-diameter, double-side, submerged-arc welded steel pipes and spiral seam

steel pipes. The finished products are extensively used for oil and gas

transmission, municipal water supply projects, sewage treatment projects, and

piling. Sales of welded steel pipe products amounted to approximately

117,000 MT in fiscal year 2010, representing approximately 13.1% of our total

sales revenue.

Manufacturing

Our

manufacturing facilities are located in Changshu and Ningbo, China. Our

facilities in Changzhou currently have three HDG Steel production lines, one

PPGI production line, one AP Steel production line and one cold-rolled steel

line. Our facilities in Ningbo have six welded steel pipe production lines. Our

current annual designed production capacity is approximately 700,000 MT for HDG

Steel, 200,000 MT for PPGI, 500,000 MT for AP Steels, 250,000 MT for cold-rolled

steel and 400,000 MT for welded steel pipe products.

We

utilize modern automated production technology which is strictly maintained.

There are generally only 15 workers on a continuous cold-rolled galvanizing line

and 11 workers on the PPGI production line per shift. The chart below

demonstrates our production process.

5

Raw

Materials and Suppliers

The

principal raw materials used in producing our products are steel coil, zinc, oil

paint and acid. We source our raw materials from various suppliers, including

our affiliate Shanghai Huaye which supplied approximately 68.1% of our raw

materials in fiscal year 2010. We believe that our suppliers are sufficient to

meet our present needs.

Steel

coil accounted for approximately 90% of total production cost in fiscal year

2010. We generally purchase steel coil after receiving orders from customers and

are generally able to pass on increased cost to customers. We purchase steel

strips from Chinese companies, both state-owned enterprises and private

companies. State-owned enterprises can ensure consistent large supply, but do

not react quickly to the fluctuations in prevailing market prices. Private

companies normally react quickly to price changes, but are not as reliable as

state-owned enterprises in terms of consistent supply. By sourcing raw materials

from a combination of state-owned enterprises and private companies, we enjoy

both a reliable source of raw materials and competitive prices.

Zinc is

an important raw material for HDG of cold-rolled steel and accounted for

approximately 7.8% of our total production costs of HDG Steel in fiscal year

2010. We have established long-term relationships with several Chinese

suppliers. We compare the prevailing domestic prices and choose the lower price

and can generally pass price fluctuations onto customers. Zinc prices are

closely guided by the London Metal Exchange quotation, are the most volatile

among those of all of our raw materials.

Our

global sourcing network is designed to ensure the highest quality-to-price ratio

of the raw materials we purchase. Our internal specialists collect Chinese

domestic and global market information everyday and track domestic and global

market price fluctuations closely, which allows us to react rapidly to any price

change.

Customers

We sell

most of our steel products to customers who operate in the solar energy,

appliances, automobile, construction, infrastructure, medical equipment and

water resource industries.

6

Approximately

51.0% of our revenue was derived from Shanghai Huaye and its affiliates in

fiscal year 2010. We currently do not have a long-term written contract with

Shanghai Huaye and plan to negotiate the terms of each transaction based on then

current market condition. We believe such arrangement will afford us more

flexibility and allow us to obtain more favorable price based on the changing

market. We believe we have a good relationship with Shanghai Huaye and expect

Shanghai Huaye to remain as our major customer in the foreseeable

future. We plan to further expand our sales channel and increase our

direct sale to end customers in the future. Other than Shanghai Huaye, none of

our customers accounted for more than 10% of our total revenue in fiscal year

2010.

Sales

and Marketing

China is

our most important market. Domestic sales represented approximately 88.8% of our

total revenue in fiscal year 2010. Within China, the biggest market for our

products is eastern China, which includes Shanghai and the Zhejiang and Jiangsu

provinces. Since September 2004, we have exported our products to Europe, Middle

East, South America, and Hong Kong. Our foreign sales accounted for

approximately 10.6% and 11.2% of our total revenue in fiscal years 2009 and

2010, respectively.

Our sales

network covers most provinces and regions in China. We are developing a

diversified sales network which allows us to effectively market products and

services to our customers. We sold approximately 49.0% of our products through

our own sales and marketing department in fiscal year 2010. Our sales and

marketing department consists of approximately 55 employees as of the date of

this annual report.

Research

and Development

We

believe that the development of new products and production methods is important

to our success. We established our high-performance steel sheet research center

in 2007 which was recognized as the “Jiangsu Province Foreign Invested Research

Center” by the Jiangsu Science and Technology Bureau. As of June 30, 2010, our

research and development personnel consisted of approximately 99

employees.

We

recently set up Sutor Technology Co., Ltd., a wholly-owned subsidiary

incorporated in China, and plan to consolidate all R&D activities into this

subsidiary in the future. We plan to build a facility in the new subsidiary

to be used solely for research and development of new products and technologies.

We expect the new subsidiary will help attract talent and enhance our leading

position in the fine processed steel industry in China. The new subsidiary is

anticipated to enjoy preferential tax treatment when in full

operation.

Competition

Competition

within the steel industry, both in China and worldwide, is intense. We compete

with both large state-owned enterprises and smaller private companies. In

addition, we also face competition from international steel

manufacturers.

Even

though the demand for fine finished steel products has increased in recent

years, due to the over expansion of the total production capacity of HDG Steel

and PPGI products, supply for low-end HDG steel and PPGI products has outpaced

demand. Due to the high requirements for production technology and equipment, we

believe that demand for high-end HDG Steel and PPGI market remains strong.

Currently, only our Company and a few large state-owned enterprises are capable

of producing high-end HDG Steel and PPGI products in China.

Private

steel product manufacturers in China generally focus on low-end products. Many

of our competitors are much smaller than us and use older equipment and

production techniques. In contrast, our products are aimed at the high-end

markets so we attempt to manufacture them with superior quality and broader

range of specifications. We use advanced manufacturing equipment that we

have purchased from developed countries, such as France and Italy, and employ

engineers and researchers who are experienced with different production

techniques. This allows us to provide a broad array of products in terms of

thickness, zinc layer weight and width of steel coil, which helps us target

high-end customers whose manufacturing specifications are extreme. In addition,

through cooperation of our strategic partners, we have also established a

vertically integrated business model that provides processing, distribution and

customized logistic solutions. We believe this business model is difficult to

duplicate and few private companies have this capability.

7

There are

several state-owned steel manufacturers that produce comparable products to our

products. As compared with those competitors, we believe we differentiate

ourselves by the following:

|

|

·

|

We

satisfy customers’ orders with shorter lead times and guarantee lead times

for urgent orders, even very small orders, in as short as one or two

days;

|

|

|

·

|

We

have flexibility in sales arrangements and can take orders in a variety of

sizes;

|

|

|

·

|

We

operate more efficiently than our state-owned competitors and have lower

total labor costs, therefore, lower product prices;

and

|

|

|

·

|

We

provide more customer-oriented

services.

|

We also

compete with international steel product manufacturers in the global market,

such as Mitel Corporation and Posco Steel. As compared to our competitors in

Europe, Korea and the United States, we believe we have lower production costs

and can offer more competitive pricing. In addition, competitors in developing

countries lag behind due to low product quality and limited product

specification ranges. We began exporting our products in September 2004 and our

products are now sold to Europe, Middle East, South America and Hong Kong. Our

export sales accounted for approximately 11.2% of our total sales for fiscal

year 2010.

Our

operating subsidiaries, Changshu Huaye and Jiangsu Cold-Rolled, are both located

in Changshu, which provides us a transportation cost advantage. Changshu is

situated in the eastern coastal part of China, the largest market for coated

steel products in China. In addition, our affiliate Shanghai Huaye has a

logistic center in Changshu port, which provides us convenient and low cost

transportation for both raw materials and finished products. Further, our

subsidiary Ningbo Zhehua is located in Ningbo which is one of the largest and

most important sea port cities in China with easy access to both domestic and

international markets.

Intellectual

Property

Our

success depends, in part, on our ability to maintain and protect our proprietary

technology and to conduct our business without infringing on the proprietary

rights of others. We rely primarily on a combination of patents, trademarks and

trade secrets, as well as employee and third-party confidentiality agreements,

to safeguard our intellectual property. As of June 30, 2010, we held 23 patents

and had 36 patent applications pending.

Most of

our products are sold with the trademark of “ ,”

which is known by Chinese and international clients. In August 2005, Shanghai

Huaye agreed to transfer the trademark of “

,”

which is known by Chinese and international clients. In August 2005, Shanghai

Huaye agreed to transfer the trademark of “ ” to us

without consideration. Such transfer was approved by the Trademark office of the

State Administration for Industry and Commerce of China in August 2006. As a

result, we have all the legal rights for the trademark, the term of which

expires in July 2015.

” to us

without consideration. Such transfer was approved by the Trademark office of the

State Administration for Industry and Commerce of China in August 2006. As a

result, we have all the legal rights for the trademark, the term of which

expires in July 2015.

,”

which is known by Chinese and international clients. In August 2005, Shanghai

Huaye agreed to transfer the trademark of “” to us

without consideration. Such transfer was approved by the Trademark office of the

State Administration for Industry and Commerce of China in August 2006. As a

result, we have all the legal rights for the trademark, the term of which

expires in July 2015.All our

key employees, especially engineers, have signed confidentiality and

non-competition agreements with us. In addition, all our employees are obligated

to protect our confidential information. Where appropriate for our business

strategy, we will continue to take steps to protect our intellectual property

rights.

Employees

As of

June 30, 2010, we had approximately 657 full-time employees. Approximately 251

are employees of Changshu Huaye, approximately 172 are employees of Jiangsu

Cold-Rolled and approximately 234 are employees of Ningbo Zhehua.

The

following table sets forth the number of our full-time employees by

function.

|

Function

|

Number of Employees

|

|

|

Manufacturing

|

369

|

|

|

General

and administration

|

134

|

|

|

Marketing

and sales

|

55

|

|

|

Research

and development

|

99

|

8

We

believe that we maintain a good working relationship with our employees and we

have not experienced any significant labor disputes or any difficulty in

recruiting staff for our operations. Our employees are not covered by a

collective bargaining agreement. We have not experienced any work

stoppages.

We are

required under PRC law to make contributions to the employee benefit plans at

specified percentages of the after-tax profit. In addition, we are required by

the PRC law to cover employees in China with various type of social insurance.

We believe that we are in material compliance with the relevant PRC

laws.

Regulation

General

Regulation of Business

As a

producer of steel products in China, we are regulated by the national and local

laws of the PRC.

We are

subject to various governmental regulations related to environmental protection.

The major environmental regulations applicable to us include: the Environmental

Protection Law of the PRC, the Law of PRC on the Prevention and Control of Water

Pollution, Implementation Rules of the Law of PRC on the Prevention and Control

of Water Pollution, the Law of PRC on the Prevention and Control of Air

Pollution, Implementation Rules of the Law of PRC on the Prevention and Control

of Air Pollution, the Law of PRC on the Prevention and Control of Solid Waste

Pollution, and the Law of PRC on the Prevention and Control of Noise

Pollution.

We

believe that we are in material compliance with all registrations and

requirements for the issuance and maintenance of all licenses required by the

governing bodies, and that all license fees and filings are

current.

Taxation

On March

16, 2007, the National People’s Congress of China passed the Enterprise Income

Tax Law, or the EIT Law, and on November 28, 2007, the State Council of China

passed its implementing rules, both of which took effect on January 1, 2008. The

EIT Law and its implementing rules impose a unified earned income tax, or EIT,

rate of 25.0% on all domestic-invested enterprises and foreign invested

enterprises, or FIEs, unless they qualify under certain limited

exceptions. As a result, our PRC operating subsidiaries Changshu

Huaye and Ningbo Zhehua were and are subject to an earned income tax of 25.0% in

2009 and 2010. Our subsidiary Jiangsu Cold-Rolled’s tax holiday will expire at

the end of 2011, therefore, it is and will be subject to an EIT rate of 12.5% in

calendar years 2010 and 2011 and will be subject to an EIT rate of 25% starting

in calendar year 2012.

In

addition to the changes to the current tax structure, under the EIT Law, an

enterprise established outside of China with “de facto management bodies” within

China is considered a resident enterprise and will normally be subject to an EIT

of 25% on its global income. The implementing rules define the term “de facto

management bodies” as “an establishment that exercises, in substance, overall

management and control over the production, business, personnel, accounting,

etc., of a Chinese enterprise.” If the PRC tax authorities subsequently

determine that we should be classified as a resident enterprise, then our

organization’s global income will be subject to PRC income tax of

25%. For detailed discussion of PRC tax issues related to resident

enterprise status, see Item 1A, “Risk Factors – Risks Related to Doing Business

in China – Under the New Enterprise Income Tax Law, we may be classified as a

“resident enterprise” of China. Such classification will likely result in

unfavorable tax consequences to us and our non-PRC stockholders.”

Foreign

Currency Exchange

All of

our sales revenue and expenses are denominated in RMB. Under the PRC foreign

currency exchange regulations applicable to us, RMB is convertible for current

account items, including the distribution of dividends, interest payments, trade

and service-related foreign exchange transactions. Currently, our PRC operating

subsidiaries may purchase foreign currencies for settlement of current account

transactions, including payments of dividends to us, without the approval of the

PRC State Administration of Foreign Exchange, or SAFE, by complying with certain

procedural requirements. Conversion of RMB for capital account items,

such as direct investment, loan, security investment and repatriation of

investment, however, is still subject to the approval of SAFE. In particular, if

our PRC operating subsidiaries borrow foreign currency through loans from us or

other foreign lenders, these loans must be registered with SAFE, and if we

finance the subsidiaries by means of additional capital contributions, these

capital contributions must be approved by certain government authorities,

including the PRC Ministry of Commerce, or MOFCOM, or their respective local

branches. These limitations could affect our PRC operating

subsidiaries’ ability to obtain foreign exchange through debt or equity

financing.

9

Dividend

Distributions

Our

revenues are earned by our PRC subsidiaries. However, PRC regulations

restrict the ability of our PRC subsidiaries to make dividends and other

payments to their offshore parent company. PRC legal restrictions

permit payments of dividend by our PRC subsidiaries only out of their

accumulated after-tax profits, if any, determined in accordance with PRC

accounting standards and regulations. Each of our PRC subsidiaries is

also required under PRC laws and regulations to allocate at least 10% of our

annual after-tax profits determined in accordance with PRC GAAP to a statutory

general reserve fund until the amounts in such fund reaches 50% of its

registered capital. These reserves are not distributable as cash

dividends. Our PRC subsidiaries have the discretion to allocate a portion of

their after-tax profits to staff welfare and bonus funds, which may not be

distributed to equity owners except in the event of liquidation.

In

addition, under the EIT Law, the Notice of the State Administration

of Taxation on Negotiated Reduction of Dividends and Interest Rates,

which was issued on January 29, 2008, and the Notice of the State Administration

of Taxation Regarding Interpretation and Recognition of Beneficial Owners under

Tax Treaties, which became effective on October 27, 2009, dividends from

our PRC operating subsidiaries paid to us through our subsidiaries may be

subject to a withholding tax at a rate of 10%. Furthermore, the ultimate tax

rate will be determined by treaty between the PRC and the tax residence of the

holder of the PRC subsidiary. Dividends declared and paid from before

January 1, 2008 on distributable profits are grandfathered under the EIT Law and

are not subject to withholding tax.

The

Company intends on reinvesting profits, if any, and does not intend on making

cash distributions of dividends in the near future.

Environmental

Matters

Our

manufacturing facilities are subject to various pollution control regulations

with respect to noise, water and air pollution and the disposal of waste and

hazardous materials. We are also subject to periodic inspections by local

environmental protection authorities. Our operating subsidiaries have received

certifications from the relevant PRC government agencies in charge of

environmental protection indicating that their business operations are in

material compliance with the relevant PRC environmental laws and regulations. We

are not currently subject to any pending actions alleging any violations of

applicable PRC environmental laws.

Seasonality

Our

operating results and operating cash flows historically have not been subject to

seasonal variations. This pattern may change, however, as a result of new market

opportunities or new product introductions.

Available

Information

Our

internet website is at www.sutorcn.com. Our

Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on

Form 8-K, including exhibits, and amendments to those reports filed or furnished

pursuant to Sections 13(a) and 15(d) of the Exchange Act, are available free of

charge on our website as soon as reasonably practicable after such reports are

electronically filed with, or furnished to, the SEC. Copies of these reports may

also be obtained free of charge by sending written requests to our Secretary,

Sutor Technology Group Limited, No 8, Huaye Road, Dongbang Industrial Park

Changshu, China, 215534. The information posted on our website is not part of

this or any other report we file with or furnish with the SEC. Investors can

also read and copy any materials filed by us with the SEC at the SEC’s Public

Reference Room which is located at 100 F Street, NE, Washington, DC 20549.

Information about the operation of the Public Reference Room can be obtained by

calling the SEC at 1-800-SEC-0330. Our filings can also be accessed at the

SEC’s website: www.sec.gov.

10

|

RISK

FACTORS.

|

RISKS

RELATED TO OUR BUSINESS

We

maintain a close business relationship with Shanghai Huaye and any disruption of

this relationship or the financial stability of Shanghai Huaye could damage our

business.

Our company

and Shanghai Huaye, which is 100% owned by our major shareholder, Chairperson

and CEO, Lifang Chen and her husband Feng Gao, have a close business

relationship. Approximately 51.0% of our revenue was derived from

Shanghai Huaye and its affiliates in fiscal year 2010, which distribute our

products. In addition, a large portion of our raw materials were supplied

by Shanghai Huaye in fiscal year 2010. We believe that the larger

size of Shanghai Huaye gives it greater bargaining power than us and our

arrangement with Shanghai Huaye allows us to leverage its bargaining power and

purchase raw materials at relatively lower purchase prices from suppliers. We do

not have long-term written contracts with Shanghai Huaye. In the

past, Shanghai Huaye also has provided credit support on our behalf and

guaranties for our benefit in connection with loans to us from third party

lenders.

If our

business relationship with Shanghai Huaye changes negatively or Shanghai Huaye’s

financial condition deteriorates, this would harm our business in many

ways. We would be forced to rely on other third parties for raw

materials and product distribution if Shanghai Huaye ceases to be a supplier of

our raw materials and/or a distributor of our products at current

levels. We may not be able to negotiate terms with these third

parties that are as favorable as our arrangements with Shanghai

Huaye. If this happens, our revenues could decrease, our production

costs could increase and our profit margin could be strained. In

addition, a material adverse change in the financial condition and

creditworthiness of Shanghai Huaye could impair our existing credit facilities

and ability to obtain loans in the future.

Any

decrease in the availability, or increase in the cost, of raw materials could

materially affect our earnings.

Our

operations depend heavily on the availability of various raw materials and

energy resources, including steel coil, zinc, oil paint, electricity and natural

gas. Steel coil has historically made up approximately 90.0% of our total cost

of sales. The availability of raw materials and energy resources may decrease

and their prices may fluctuate greatly. We purchase a large portion of our raw

materials from our affiliate Shanghai Huaye and we have long-term relationships

with several other suppliers. However, if Shanghai Huaye or any other important

suppliers are unable or unwilling to provide us with raw materials on terms

favorable to us, we may be unable to produce certain products. This could result

in a decrease in profit and damage to our reputation in our industry. In the

event our raw material and energy costs increase, we may not be able to pass

these higher costs on to our customers in full or at all. Any increase in the

prices for raw materials or energy resources could materially increase our costs

and therefore lower our earnings.

Our

industry is highly fragmented and competitive, and increased competition could

reduce our operating income.

The steel

manufacturing and processing business is highly fragmented and competitive. We

compete with a number of other steel manufacturers and processors in China, on a

region-by-region basis, and with foreign steel manufacturers on a world wide

basis. Our goal is to market our products to customers who demand the highest

quality products and precision in the end product so we compete primarily on the

precision and range of achievable tolerances, the quality of our products and

the raw materials used in our products. We compete with companies of various

sizes, some of which have more established brand names and relationships in

certain markets we serve than we do. Increased competition could force us to

lower our prices or offer services at a higher cost to us, which could reduce

our margins and operating income.

A

downturn or negative changes in the highly volatile steel industry will harm our

business and profitability.

The steel

industry as a whole is cyclical and pricing can be volatile as a result of

general economic conditions, energy costs, labor costs, competition, import

duties, tariffs and currency exchange rates. These macroeconomic factors have

historically resulted in wide fluctuations in the steel industry both in China

and globally. In our case, future economic downturns, stagnant economies or

currency fluctuations in China or globally could decrease the demand for

products or increase the amount of imports of steel into China, which could

negatively impact our sales, margins and profitability.

11

We

may be exposed to potential risks relating to our internal controls over

financial reporting and our ability to have the operating effectiveness of our

internal controls attested to by our independent auditors.

As

directed by Section 404 of the Sarbanes-Oxley Act of 2002, the SEC adopted rules

requiring public companies to include a report of management on the Company’s

internal controls over financial reporting in their annual reports and, for

companies that are not small reporting companies, the independent registered

public accounting firm auditing a company’s financial statements to attest to

and report on the operating effectiveness of such company’s internal controls.

Our management had previously identified material weaknesses in our internal

control over financial reporting in fiscal years 2008 and 2009. Although our

management believes that our internal control over financial reporting was

effective as of June 30, 2010, we can provide no assurance that we will comply

with all of the requirements imposed thereby and we will receive a positive

attestation from our independent auditors in the future, when required. In the

event we identify significant deficiencies or material weaknesses in our

internal controls that we cannot remediate in a timely manner or we are unable

to receive a positive attestation from our independent auditors with respect to

our internal controls, investors and others may lose confidence in the

reliability of our financial statements.

We

may be unable to fund the substantial ongoing capital and maintenance

expenditures that our operations require.

Our

operations are capital intensive and our business strategy may require

additional substantial capital investment. We require capital for building new

production lines, acquiring new equipment, maintaining the condition of our

existing equipment and complying with environmental laws and regulations. We

plan to fund our capital expenditures from operating cash flow and our credit

facilities and may require additional debt or equity financing. We cannot assure

you, however, that financing will be available or, if financing is available, it

may result in increased interest and amortization expense, increased leverage,

dilution and decreased income available to fund further expansion. In addition,

future debt financings may limit our ability to withstand competitive pressures

and render us more vulnerable to economic downturns. If we are unable to fund

our capital requirements, we may be unable to implement our business plan, and

our financial performance may suffer.

Our

level of indebtedness may make it more difficult for us to fulfill all of our

debt obligations and may reduce the amount of cash available for maintaining and

growing our operations, which could have an adverse effect on our

revenues.

Our major

source of liquidity is borrowing through short-term bank and private loans. Our

total debt under existing loans as of June 30, 2010 was approximately $85.6

million, of which approximately $82.1 million are short-term loans to

non-related third party. We expect to renew our short-term loans when they

become due, our inability to renew these loan upon maturity may cause us working

capital constraints. This substantial indebtedness could also impair our

financial condition and our ability to fulfill all of our debt obligations,

especially during a downturn in our business, in the industry in which we

operate or in the general economy. Our indebtedness and the incurrence of any

new indebtedness could (i) make it more difficult for us to satisfy our existing

obligations, which could in turn result in an event of default on such

obligations, (ii) require us to seek other sources of capital to finance cash

used in operating activities, thereby reducing the availability of cash for

working capital, capital expenditures, acquisitions, general corporate purposes

or other purposes, (iii) impair our ability to obtain additional financing in

the future for working capital, capital expenditures, acquisitions, general

corporate purposes or other purposes; (iv) diminish our ability to withstand a

downturn in our business, the industry in which we operate or the economy

generally, (v) limit our flexibility in planning for, or reacting to, changes in

our business and the industry in which we operate, or (vi) place us at a

competitive disadvantage compared to competitors that have proportionately less

debt. If we are unable to meet our debt service obligations, we could be forced

to restructure or refinance our indebtedness, seek additional equity capital or

sell assets.

We may be

unable to obtain financing or sell assets on satisfactory terms, or at all,

which could cause us to default on our debt service obligations and be subject

to foreclosure on such loans. Additionally, we could incur additional

indebtedness in the future and, if new debt is added to our current debt levels,

the risks above could intensify.

Unexpected

equipment failures may damage our business due to production curtailments or

shutdowns.

Our

manufacturing processes are extremely specialized and depend on critical pieces

of equipment, such as air knife machines, welding tools and apparatus,

color-coating machines, roll mills, ABB roll and tension knives. This machinery

is highly specialized and cannot be repaired or replaced without significant

expense and time delay. On occasion, our equipment may be out of service as a

result of unanticipated failures which may result in material plant shutdowns or

periods of reduced production. Interruptions in production capabilities will

inevitably increase production costs and reduce our sales and earnings. In

addition to equipment failures, our facilities are also subject to the risk of

catastrophic loss due to unanticipated events such as fires, explosions or

adverse weather conditions. Furthermore, any interruption in production

capability may require us to make large capital expenditures to remedy the

situation, which could have a negative effect on our profitability and cash

flows. Although we have business interruption insurance, we cannot provide any

assurance that the insurance will cover all losses that we experience as a

result of the equipment failures. In addition, longer-term business disruption

could result in a loss of customers. If this were to occur, our future sales

levels, and therefore our profitability, could be adversely

affected.

12

Our

revenue will decrease if there is less demand for construction materials or

electrical household appliances.

Our

products often serve as key components in construction materials and electrical

household appliances. Therefore, we are subject to the general changes in

economic conditions affecting the construction and household appliance segments

of the economy. Demand for our products is typically affected by a number of

economic factors, including, but not limited to, consumer interest rates,

consumer confidence, retail trends, sales of existing homes, and the level of

mortgage financing. If there is a decline in economic activity in China and the

other markets in which we operate or a decrease of sales of construction

materials and electrical household appliances, demand for our products and our

revenue will likewise decrease.

Environmental

regulations impose substantial costs and limitations on our

operations.

We are

subject to various national and local environmental laws and regulations in

China concerning issues such as air emissions, wastewater discharges, and solid

waste management and disposal. These laws and regulations can restrict or limit

our operations and expose us to liability and penalties for non-compliance.

While we believe that our facilities are in material compliance with all

applicable environmental laws and regulations, the risks of substantial

unanticipated costs and liabilities related to compliance with these laws and

regulations are an inherent part of our business. It is possible that future

conditions may develop, arise or be discovered that create new environmental

compliance or remediation liabilities and costs. While we believe that we can

comply with existing environmental legislation and regulatory requirements and

that the costs of compliance have been included within budgeted cost estimates,

compliance may prove to be more limiting and costly than

anticipated.

If

our customers and/or the ultimate consumers of products that use our products

successfully assert product liability claims against us due to defects in our

products, our operating results may suffer and our reputation may be

harmed.

Our

products are widely applied in the manufacturing of many products, including

electrical household appliances, medical instruments and large industrial

equipment. Significant property damage, personal injuries and even death can

result from malfunctioning products. If our products are not properly

manufactured or installed and/or if people are injured as a result of our

products, we could be subject to claims for damages based on theories of product

liability and other legal theories in some jurisdictions in which our products

are sold. The costs and resources to defend such claims could be substantial

and, if such claims are successful, we could be responsible for paying some or

all of the damages. We do not have product liability insurance. The publicity

surrounding these sorts of claims is also likely to damage our reputation,

regardless of whether such claims are successful. Any of these consequences

resulting from defects in our products would hurt our operating results and

stockholder value.

We

might fail to adequately protect our intellectual property and third parties may

claim that our products infringe upon their intellectual property.

As part

of our business strategy, we intend to accelerate our investment in new

technologies in an effort to strengthen and differentiate our product portfolio

and make our manufacturing processes more efficient. As a result, we believe

that the protection of our intellectual property will become increasingly

important to our business. Currently, we have one patent application pending. We

expect to rely on a combination of patents, trade secrets, trademarks and

copyrights to provide protection in this regard, but this protection might be

inadequate. For example, our pending or future patent applications might not be

approved or, if allowed, they might not be of sufficient strength or scope.

Conversely, third parties might assert that our technologies infringe their

proprietary rights. In either case, litigation could result in substantial costs

and diversion of our resources, and whether or not we are ultimately successful,

the litigation could hurt our business and financial condition.

13

Expansion

of our business may strain our management and operational infrastructure and

impede our ability to meet any increased demand for our fine finished steel

products.

Our

growth strategy includes growing our operations by meeting the anticipated

growth in demand for existing products, introducing new product offerings, and

identifying and acquiring or investing in suitable candidates on acceptable

terms. In 2009, we acquired a 100% ownership interest in Ningbo Zhehua. In

addition, our subsidiary, Jiangsu Cold-Rolled, has recently completed

construction of several new production lines and has been put into operation,

but lacks a proven operational history. Over time, we may acquire or make

investments in other providers of products that complement our business and

other companies in our industry. Growth in our business may place a significant

strain on our personnel, management, financial systems and other resources. Our

business growth also presents numerous risks and challenges,

including:

|

|

·

|

our

ability to successfully and rapidly expand sales to potential customers in

response to potentially increasing

demand;

|

|

|

·

|

our

ability to integrate and retain key management, sales, research and

development, production and other

personnel;

|

|

|

·

|

our

ability to incorporate the acquired products or capabilities into our

offerings from an engineering, sales and marketing

perspective;

|

|

|

·

|

integration

and support pre-existing supplier, distribution and customer

relationships;

|

|

|

·

|

adverse

effects on our reported operating results due to possible write-down of

goodwill associated with

acquisitions;

|

|

|

·

|

potential

disputes with sellers of acquired businesses, technologies, services,

products and potential liabilities;

|

|

|

·

|

the

costs associated with such growth, which are difficult to quantify, but

could be significant; and

|

|

|

·

|

rapid

technological change.

|

To

accommodate this growth and compete effectively, we may need to obtain

additional funding to improve information systems, procedures and controls and

expand, train, motivate and manage existing and additional employees. Funding

may not be available in a sufficient amount or on favorable terms, if at all. If

we are not able to manage these activities and implement these strategies

successfully to expand to meet any increased demand, our operating results could

suffer.

We

depend heavily on key personnel, and turnover of key employees and senior

management could harm our business.

Our

future business and results of operations depend in significant part upon the

continued contributions of our key technical and senior management personnel,

including Lifang Chen, our Chief Executive Officer, Yongfei Jiang, our Chief

Financial Officer, and Naijiang Zhou, our Vice President of Finance. They also

depend in significant part upon our ability to attract and retain additional

qualified management, technical, marketing and sales and support personnel for

our operations. If we lose a key employee, if a key employee fails to perform in

his or her current position, or if we are not able to attract and retain skilled

employees as needed, our business could suffer. Significant turnover in our

senior management could significantly deplete our institutional knowledge held

by our existing senior management team. We depend on the skills and abilities of

these key employees in managing the manufacturing, technical, marketing and

sales aspects of our business, any part of which could be harmed by turnover in

the future.

Ms.

Lifang Chen’s association with Shanghai Huaye could pose a conflict of

interest.

Ms.

Lifang Chen, our chairman and beneficial owner of 74.5% of our common stock,

also beneficially owns 100% of Shanghai Huaye, which is a major distributor of

our products and provider of our raw materials. As a result, conflicts of

interest may arise from time to time. We will attempt to resolve any such

conflicts of interest in our favor. Our officers and directors are accountable

to us and our shareholders as fiduciaries, which requires that such officers and

directors exercise good faith and integrity in handling our

affairs.

14

We

may be exposed to liabilities under the Foreign Corrupt Practices Act, and any

determination that we violated the Foreign Corrupt Practices Act could have a

material adverse effect on our business.

We are

subject to the Foreign Corrupt Practice Act, or FCPA, and other laws that

prohibit improper payments or offers of payments to foreign governments and

their officials and political parties by U.S. persons and issuers as defined by

the statute for the purpose of obtaining or retaining business. We have

operations, agreements with third parties and make sales in China, which may

experience corruption. Our activities in China create the risk of unauthorized

payments or offers of payments by one of the employees, consultants, sales

agents or distributors of our company, because these parties are not always

subject to our control. It is our policy to implement safeguards to discourage

these practices by our employees. Also, our existing safeguards and any future

improvements may prove to be less than effective, and the employees,

consultants, sales agents or distributors of our Company may engage in conduct

for which we might be held responsible. Violations of the FCPA may result in

severe criminal or civil sanctions, and we may be subject to other liabilities,

which could negatively affect our business, operating results and financial

condition. In addition, the government may seek to hold our Company liable for

successor liability FCPA violations committed by companies in which we invest or

that we acquire.

RISKS

RELATED TO DOING BUSINESS IN CHINA

Adverse

changes in political and economic policies of the PRC government could impede

the overall economic growth of China, which could reduce the demand for our

products and damage our business.

We

conduct substantially all of our operations and generate most of our revenue in

China. Accordingly, our business, financial condition, results of operations and

prospects are affected significantly by economic, political and legal

developments in China. The PRC economy differs from the economies of most

developed countries in many respects, including:

|

|

·

|

a

higher level of government

involvement;

|

|

|

·

|

a

early stage of development of the market-oriented sector of the

economy;

|

|

|

·

|

a

rapid growth rate;

|

|

|

·

|

a

higher level of control over foreign exchange;

and

|

|

|

·

|

the

allocation of resources.

|

As the

PRC economy has been transitioning from a planned economy to a more

market-oriented economy, the PRC government has implemented various measures to

encourage economic growth and guide the allocation of resources. While these

measures may benefit the overall PRC economy, they may also have a negative

effect on us.

Although

the PRC government has in recent years implemented measures emphasizing the

utilization of market forces for economic reform, the PRC government continues

to exercise significant control over economic growth in China through the

allocation of resources, controlling the payment of foreign currency-denominated

obligations, setting monetary policy and imposing policies that impact

particular industries or companies in different ways.

Any

adverse change in economic conditions or government policies in China could have

a material adverse effect on the overall economic growth in China, which in turn

could lead to a reduction in demand for our services and consequently have a

material adverse effect on our business and prospects.

Uncertainties

with respect to the PRC legal system could limit the legal protections available

to you and us.

We

conduct substantially all of our business through our operating subsidiary in

the PRC. Our operating subsidiaries are generally subject to laws and

regulations applicable to foreign investments in China and, in particular, laws

applicable to foreign-invested enterprises. The PRC legal system is based on

written statutes, and prior court decisions may be cited for reference but have

limited precedential value. Since 1979, a series of new PRC laws and regulations

have significantly enhanced the protections afforded to various forms of foreign

investments in China. However, since the PRC legal system continues to rapidly

evolve, the interpretations of many laws, regulations and rules are not always

uniform and enforcement of these laws, regulations and rules involve

uncertainties, which may limit legal protections available to you and us. In

addition, any litigation in China may be protracted and result in substantial

costs and diversion of resources and management attention. In addition, all of

our executive officers and all of our directors are residents of China and not

of the United States, and substantially all the assets of these persons are

located outside the United States. As a result, it could be difficult for

investors to affect service of process in the United States or to enforce a

judgment obtained in the United States against our Chinese operations and

subsidiaries.

15

If

we are found to have failed to comply with applicable laws, we may incur

additional expenditures or be subject to significant fines and

penalties.

Our

operations are subject to PRC laws and regulations applicable to us. However,

many PRC laws and regulations are uncertain in their scope, and the

implementation of such laws and regulations in different localities could have

significant differences. In certain instances, local implementation rules and/or

the actual implementation are not necessarily consistent with the regulations at

the national level. Although we strive to comply with all the applicable PRC

laws and regulations, we cannot assure you that the relevant PRC government

authorities will not later determine that we have not been in compliance with

certain laws or regulations.

In

addition, our facilities and products are subject to many laws and regulations.

Our failure to comply with these and other applicable laws and regulations in

China could subject us to administrative penalties and injunctive relief, as

well as civil remedies, including fines, injunctions and recalls of our

products. It is possible that changes to such laws or more rigorous enforcement

of such laws or with respect to our current or past practices could have a

material adverse effect on our business, operating results and financial

condition. Further, additional environmental, health or safety issues relating

to matters that are not currently known to management may result in

unanticipated liabilities and expenditures.

The

PRC government exerts substantial influence over the manner in which we must

conduct our business activities.

The PRC

government has exercised and continues to exercise substantial control over

virtually every sector of the Chinese economy through regulation and state

ownership. Our ability to operate in China may be harmed by changes in its laws

and regulations, including those relating to taxation, import and export