Attached files

Table of Contents

As filed with the Securities and Exchange Commission on September 21, 2010

Registration No. 333-168609

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT No. 1

to

FORM S-1

REGISTRATION STATEMENT

Under

The Securities Act of 1933

Panther Expedited Services, Inc.

(Exact name of Registrant as specified in its charter)

| Delaware | 4731 | 20-2825225 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

4940 Panther Parkway

Seville, Ohio 44273

(330) 769-5830

(Address, including zip code and telephone number, including area code, of Registrant’s principal executive offices)

Andrew C. Clarke

President and Chief Executive Officer

Panther Expedited Services, Inc.

4940 Panther Parkway

Seville, Ohio 44273

(330) 769-5869

(Name, address, including zip code and telephone number, including area code, of agent for service)

Copies to:

| Mark A. Scudder, Esq. Scudder Law Firm, P.C., L.L.O 411 South 13th Street, Suite 200 Lincoln, Nebraska 68508 (402) 435-3223 |

Andrew Keller, Esq. Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, New York 10017-3954 (212) 455-2000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 (the “Securities Act”) check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ |

Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ |

(Do not check if a smaller reporting company)

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered |

Proposed maximum aggregate offering price(2) |

Amount of registration fee(3) | |||

| Common Stock, par value $0.01 per share offered by the Company |

$ | 100,000,000.00 | $7,130.00 | ||

| Common Stock, par value $0.01 per share offered by the selling stockholders(1) |

$ | 15,000,000 | $1,069.50 | ||

| Total |

$ | 115,000,000 | $8,199.50 | ||

| 1. | See “Underwriting.” |

| 2. | Estimated solely for the purpose of calculating the amount of the registration fee pursuant to Rule 457(o) under the Securities Act. |

| 3. | Pursuant to Rule 457(p) under the Securities Act, the registration fee of $8,199.50 that would otherwise be payable under Rule 457 is hereby offset against the Registrant’s registration fee of $26,750.00 paid to the SEC in advance of a previously filed Registration Statement on Form S-1 (Registration No. 333-134704) on June 2, 2006 in relation to shares of common stock that were then supposed to be registered thereunder. Subsequently, it was determined not to register the offer and sale of these shares and these shares were never sold. Accordingly, no registration fee is being paid herewith. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act, or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated September 21, 2010

Preliminary Prospectus

shares

Panther Expedited Services, Inc.

Common stock

This is an initial public offering of shares of our common stock. The estimated initial public offering price is between $ and $ per share.

We intend to apply to list our common stock for trading on the under the symbol “PTHR.”

| Per share | Total | |||||

| Initial public offering price |

$ | $ | ||||

| Underwriting discounts and commissions |

$ | $ | ||||

| Proceeds to us, before expenses |

$ | $ | ||||

The selling stockholders have granted the underwriters an option for a period of days to purchase from us up to additional shares of common stock at the initial public offering price, less the underwriting discounts and commissions. The selling stockholders are not offering any shares other than those contemplated by the overallotment option, and we will not receive any of the proceeds from any sale of the shares of common stock by the selling stockholders pursuant to that option.

Investing in our common stock involves a high degree of risk. See “Risk factors” beginning on page 15.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock to purchasers on .

| J.P. Morgan | Goldman, Sachs & Co. |

| UBS Investment Bank |

BB&T Capital Markets |

| WR Securities |

, 2010

Table of Contents

Table of Contents

| ii | ||

| iii | ||

| 1 | ||

| 15 | ||

| 35 | ||

| 37 | ||

| 38 | ||

| 39 | ||

| 41 | ||

| 43 | ||

| 48 | ||

| Management’s discussion and analysis of financial condition and results of operations |

51 | |

| 73 | ||

| 76 | ||

| 94 | ||

| 104 | ||

| 117 | ||

| 121 | ||

| 123 | ||

| 130 | ||

| Material United States federal income tax consequences to non-U.S. holders |

132 | |

| 135 | ||

| 142 | ||

| 142 | ||

| 142 | ||

| F-1 | ||

You should rely only on the information contained in this prospectus or in any free writing prospectus that we authorize to be delivered to you. Neither we nor the underwriters have authorized anyone to provide you with additional or different information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. We and the underwriters are not making an offer to sell these securities in any jurisdiction where an offer or sale is not permitted. You should assume that the information in this prospectus is accurate only as of the date on the front cover, regardless of the time of delivery of this prospectus or of any sale of our common stock. Our business, prospects, financial condition and results of operations may have changed since that date.

i

Table of Contents

Until , (25 days after the commencement of the offering), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to unsold allotments or subscriptions.

This prospectus contains market data related to our business and industry and forecasts that we obtained from industry publications and surveys and our internal sources. SJ Consulting Group, Inc., or SJ Consulting, was our primary independent source of industry and market data, whom we hired to provide analysis of our industry. Some data and other information also are based on our good faith estimates, which are derived from our review of internal surveys and independent sources. The market and industry data contained in this prospectus have been included herein with the permission of the authors, as necessary.

Although we believe that all industry publications and reports cited herein are reliable, neither we nor the underwriters have independently verified the data. Our internal data and estimates are based upon information obtained from our customers, suppliers, trade and business organizations, contacts in the industry in which we operate, and management’s understanding of industry conditions. We believe that such information is reliable and take such publications and reports into account when operating our business. However, we have not had such information verified by independent sources.

ii

Table of Contents

“Average shipments per business day” means the total number of shipments during the relevant period divided by the total number of business days in the period.

“Average number of employees” means our total number of employees at the end of each month during the relevant period divided by the number of months in such period.

“Average revenue per shipment” means our total revenues in the referenced period divided by the total number of shipments for which revenues were recognized over the same period.

“CSA 2010” means the Federal Motor Carrier Safety Administration’s new Comprehensive Safety Analysis 2010 program that ranks both fleets and individual drivers on seven categories of safety-related data. CSA 2010 will eventually replace the current Safety Status Measurement System used by the Federal Motor Carrier Safety Administration.

“C-TPAT” means the Customs-Trade Partnership Against Terrorism, a program designed to improve cross-border security between the United States and Canada and the United States and Mexico. Carrier members of the C-TPAT are entitled to shorter border delays and other priorities over non-member carriers.

“Cartage company” is a local carrier that provides pick-up and delivery services as well as relatively short-haul freight transportation services at the origin and destination of shipments.

“DOT” means Department of Transportation or the U.S. government department responsible for establishing the nation’s overall transportation policy.

“EDI” or “Electronic Data Interchange” is a structured transmission of data between organizations by electronic means.

“Elite Services” is our term for highly specialized services and customized handling for customers with special needs such as temperature-control and temperature-control protocol validation, government certifications, special security, emergency recoveries or distributions and heavy-weight and oversized shipments.

“Expedited carrier” means a carrier specializing in the safe delivery of time-sensitive freight, involving pick-up and delivery of freight within narrow time windows.

“Federal Aviation Administration” is an agency of the United States Department of Transportation with the authority to regulate and oversee all aspects of civil aviation in the U.S.

“Federal Motor Carrier Safety Administration” or “FMCSA” was established within the Department of Transportation on January 1, 2000 with the mission to ensure safety in motor carrier operations and to prevent commercial motor vehicle-related fatalities and injuries.

“FMC” means the U.S. Federal Maritime Commission, which is responsible for the regulation of ocean-borne transportation in the foreign commerce of the United States.

“Freight forwarder” is a person or company that organizes air and ocean and shipments for shippers. An air freight forwarder provides pick-up and delivery service, consolidates shipments into larger units, prepares bills of lading in its own capacity and tenders shipments to the airlines on behalf of its customers. Air freight forwarders do not generally operate their own aircraft. Because the air freight forwarder tenders the shipment, the airlines consider the forwarder to be the actual

iii

Table of Contents

shipper. An ocean freight forwarder dispatches shipments from the United States via carriers and books or otherwise arranges space for those shipments on behalf of shippers. Ocean freight forwarders also prepare and process the documentation and perform related activities pertaining to those shipments. A specialized subset of ocean freight forwarders are companies registered as a non-vessel operating common carriers or “NVOCCs.” An NVOCC is a common carrier that holds itself out to the public to provide ocean transportation, issues its own bills of lading or equivalent documents, but does not operate the vessels by which ocean transportation is provided. An NVOCC is the shipper party in relation to the involved ocean common carrier.

“Geofencing” means routing a shipment across a mandatory, defined route with satellite monitoring and automated alerts concerning any deviation from the route.

“Gross profit percentage” means our revenues, minus purchased transportation costs, divided by revenues over the referenced period and is used as an indicator of our success in managing transportation costs and our margin available to cover all of our other costs.

“Ground expedite” is the segment of the freight transportation market that provides time-sensitive transportation of freight.

“Hazardous material” means a substance or combination thereof which, because of its quantity, concentration, physical or chemical characteristics, may cause or pose a substantial hazard to human health or the environment when improperly packaged, stored, transported or otherwise managed.

“Indirect air carrier” means any person or entity within the United States not in possession of a Federal Aviation Administration air carrier operating certificate, that undertakes to engage indirectly in air transportation of property and uses for all or any part of such transportation the services of a passenger air carrier.

“Lean supply chain” means an operational strategy oriented toward delivering the shortest possible cycle time by eliminating waste and reducing incidental work, characterized by just-in-time materials and inventory, short cycle times and sequential workflows.

“Loaded mile” means a mile that is driven for a customer, for which we are compensated.

“Logistics” involves the integration of information, transportation, inventory, warehousing, material handling and packaging and, as needed, security. Logistics is a channel of the customer’s supply chain that adds value of time and place utility.

“Owner operator” means an independent contractor who has been contracted by us to supply one or more tractors and drivers for our use. Owner operators are generally compensated on a per-mile basis and must pay their own operating expenses, such as fuel, maintenance and driver costs and must meet our specified safety standards.

“Premium freight logistics” means arranging the door-to-door transportation of freight requiring specialized services, whether because of time critical requirements, special handling requirements, high value freight, the need for special permits, the complexity of the movement of the shipment, the need to access multiple modes of transportation, or otherwise.

“Qualcomm units” are satellite-based tracking and communication systems that allow us to track the movement of, and communicate with, our owner operators.

iv

Table of Contents

“Third-party carrier network” means the carriers we use to handle loads not transported by our owner operators and includes cartage agents, smaller expedited carriers, air freight carriers, and ocean shipping lines.

“Third-party logistics provider” or “3PL” means a third party provider that specializes in integrated operations, warehousing and transportation services that can be scaled and customized to a customer’s needs based on market conditions and the demands and delivery service requirements for the customers.

“Truckload brokerage” means the customer shipments for which we contract with third-party truckload carriers to haul traditional non-premium freight at the request of the customer.

“Truckload carrier” means a carrier that generally dedicates an entire trailer to one customer from origin to destination.

“TSA” means the U.S. Transportation Security Administration, which was created in the wake of September 11, 2001, to strengthen the security of the U.S. transportation system.

“XML” or “Extensible Markup Language” is a set of rules for encoding documents in machine-readible form. It is defined in the XML 1.0 Specification produced by the W3C, and several other related specifications, all gratis open standards.

v

Table of Contents

This summary highlights information contained elsewhere in this prospectus. It is not complete and may not contain all the information that may be important to you. You should read the entire prospectus carefully before making an investment decision, especially the information presented under the heading “Risk factors” and our consolidated financial statements and the related notes included elsewhere in this prospectus. Unless otherwise stated, all references to “us,” “our,” “we,” “Panther,” the “Company” and similar designations refer to Panther Expedited Services, Inc., and its subsidiaries.

Our company

We are one of North America’s largest expedited transportation providers with an expanding platform in premium freight logistics and freight forwarding. We offer single-source ground, air and ocean shipping solutions for time-sensitive, high-value and service-critical freight, with on-demand pick up and delivery to and from anywhere in the world. Our diversified, non-asset based transportation network consists of approximately 1,075 exclusive-use owner-operator vehicles, over 1,600 third-party ground carriers that provide additional North American capacity and over 500 air and ocean cargo carriers that provide global reach. During the twelve months ended June 30, 2010, we handled shipments for over 10,000 customers. We operate throughout nearly all segments of the supply chain for customers in diverse industries. In addition, many of the largest transportation and third-party logistics companies in the world turn to us for transportation solutions they cannot provide for customers on their own. Our proprietary, integrated and scalable information technology platform enables our customers to better manage their supply chain performance and expenses by optimizing cost and service decisions. We believe it also allows us to deliver superior customer service, operate more efficiently, and offer our owner operators enhanced productivity. Our non-asset based business model allows us to expand organically without the capital investments required by our asset-based competitors. This creates the opportunity to generate significant cash flows and to react quickly based on business opportunities and challenges.

1

Table of Contents

Our objective is to grow our revenues and profitability substantially. Since 2006, we have undertaken a number of initiatives to utilize our historical core strength in expedited ground freight as a platform to grow an expanded array of premium freight logistics offerings. Our initiatives include hiring Andrew C. Clarke as President to guide our growth, expanding our industry vertical markets to broaden our customer base and geographic footprint, acquiring our customer-facing shipping quote optimization engine, acquiring West Coast sales and operations in freight forwarding and intensifying the marketing of our air freight, ocean and other services. We believe these initiatives have been highly successful, contributing to the following progress between 2006 and the first six months of 2010:

| Strategic initiative | 2006(1) | 2010(1) | ||||

| Build comprehensive suite of service categories offered | 92% U.S. ground expedited 8% Elite Services |

66% North American ground expedited 16% Elite Services 14% air and ocean freight 4% all other | ||||

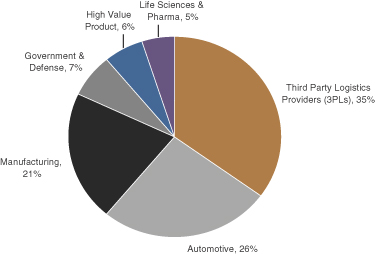

| Diversify customer base | 53% automotive 21% 3PL 21% manufacturing 5% government, life science, high value |

35% 3PL, excluding automotive 26% automotive, including auto 3PL 21% manufacturing 18% government, life science, high value | ||||

| Enhance technology platform | Real-time track and trace Web-based transactions |

Real-time track and trace Web-based transactions One CallSM Solution Network optimization Geofencing EDI and XML integration | ||||

| Embed in customers’ supply chains | Top ten customers average 1.9 services | Top ten customers average 3.0 services | ||||

| Expand addressable market | Primarily U.S. expedited transportation | Expedited transportation Premium freight logistics Freight forwarding

Total addressable market |

$3.0 billion $22.7 billion $4.6 billion (domestic) $176.0 billion (global) $206.3 billion | |||

| (1) | Percentage amounts based on revenue. Information reflects 2005 as the base year. 2010 numbers are results realized through the first six months of 2010 with the exception of the addressable market sizes, which are based on 2009 estimates by SJ Consulting. |

As a public company with a strengthened balance sheet, we expect to expand our North American owner-operator fleet, hire experienced freight forwarding sales personnel in targeted gateway cities and pursue selected acquisitions. We believe that the ongoing execution of our strategic plan will help us embed our services as an essential component of our customers’ supply chains, cross-sell solutions and achieve substantial growth.

We believe we have a strong and expanding transportation and logistics network. From our base in owner-operator expedited ground transportation, we have expanded our network to include third-party carriers, air and ocean freight forwarders, and cartage companies. For the six months ended June 30, 2010, we derived approximately 66% of our revenues from North American expedited ground transportation. The balance of our revenues were generated from our growing domestic and international air and ocean freight services, our Elite Services, which involve highly specialized solutions and customized handling for customers with special needs, and truckload brokerage services. We provide our North American ground services through exclusive-use owner operators of

2

Table of Contents

straight trucks, tractor-trailers and cargo vans, supplemented with capacity from approximately 1,600 third-party carriers. The owner operators are exclusively contracted to us, while the third-party carriers operate independently and are allocated shipments when our network optimization technology dictates or we require additional capacity. In the first six months of 2010, owner operators generally handled between 70% and 90% of our weekly ground freight volume, with third-party carriers handling the balance and affording us flexible capacity to serve customers.

Our competitive strengths

We believe our competitive strengths collectively afford us advantages against non-asset based competitors that lack our exclusive owner-operator capacity as well as asset-based and fixed network providers that lack our flexibility. We believe our competitive strengths include the following:

Leader in single-source premium freight logistics.

Our non-asset based network offers customers customized, global shipment alternatives without the constraints of either a fixed-asset or fixed-schedule network or limited geography. This affords us greater ability to offer to customers multiple solutions to optimize their shipping dollar with service and cost certainty. In addition, our North American ground franchise and owner-operator capacity provide a strong foundation for cross-selling our growing suite of services.

Proprietary IT platform.

Our information technology platform combines sophisticated software with local knowledge of shipping schedules and capacity providers to enable us to quickly accept customer orders, manage network density, and optimize our network. We offer customers a fully automated, web-based fulfillment process supported by a specialized staff to manage complex customer requirements. Our One Call SM Solution evaluates over 200,000 multi-modal shipping alternatives and presents the customer with the best shipment options based on time, service level, security and pricing priorities. For our owner operators, our web-based network optimization software helps position them for productivity and success by statistically predicting future demand levels. We believe that these applications strengthen our relationships with our customers and owner operators and enhance our productivity.

Non-asset based business model promotes scalable operations.

Our non-asset based business model provides us with significant flexibility to expand without making large capital investments. We obtain 100% of our network capacity from owner operators, third-party ground carriers, air freight carriers, ocean shipping lines and other transportation asset providers. These providers supply assets such as trucks, container ships and aircraft and bear virtually all transportation-related expenses in exchange for a specified payment per shipment or per mile. Our model capitalizes on the incentives that owner operators and third-party providers have as business owners to operate reliably, safely and productively. In each of the past three years, our capital expenditures (excluding acquisitions) have been approximately one percent of revenues.

3

Table of Contents

Industry vertical focus.

We employ industry experts in key vertical markets where specialized knowledge, experience and relationships can help solve our customers’ most pressing transportation challenges. Each industry expert has sales and marketing responsibility over markets such as (i) third party logistics providers or “3PLs”, (ii) automotive, (iii) manufacturing, (iv) government and defense, (v) high value products, and (vi) life science and pharmaceuticals. In the premium freight logistics market, where every shipment is critical, we believe our industry experts’ knowledge of our customers’ businesses provides a competitive advantage. For example, we are able to offer secret clearance and specialized equipment for Department of Defense shipments, customized cold-chain solutions that comply with Food and Drug Administration protocols for pharmaceuticals and hazmat and chain of custody assurance for the pharmaceuticals industry.

Comprehensive premium package that is difficult to replicate.

We believe our expedited, premium freight logistics and freight forwarding markets have time and cost hurdles confronting competitors that seek to establish a single-source solution. First, stringent service requirements, which include 24 hours a day, 7 days a week, 365 days a year availability, on-demand pick up and delivery within narrow time windows and a high level of customized service, make it difficult for carriers with asset-intensive, owned networks or a primary focus on traditional freight transportation to provide the type of flexibility and service required by our customers in the premium freight logistics market. Second, our extensive network of North American and global ground, air and ocean carriers would be difficult to replicate without considerable investments in time, relationships and technology. Third, a competitive technology platform would require significant capital investments, resources and time to develop and deploy. Fourth, obtaining a full suite of certifications as a motor carrier, broker, freight forwarder, non-vessel operating common carrier and indirect air carrier, as well as clearance for C-TPAT, Department of Defense and other security agencies, requires time and expertise.

Our growth strategy

We believe our business model has positioned us well for continued growth and for profitability, which we intend to pursue through the following initiatives:

Broader penetration of existing accounts.

Our comprehensive suite of services positions us to expand our share of transportation expenditures of existing accounts through cross-selling opportunities. Since 2006, our account penetration has expanded to 3.0 services per top ten customer (by revenue) from 1.9 services. In the first six months of 2010, over 1,000 customers used more than one service. In the first six months of 2010, nine of our top ten customers utilized our air and ocean freight forwarding offerings, which we introduced in 2007. Customers that use multiple services are more profitable and more frequent users. We will continue to mine our database of 10,000 current and 30,000 historical customers to supply leads to our sales force and commit our North American capacity to large customers based on a total relationship approach.

4

Table of Contents

Expand customer base within targeted industries.

We are leveraging our expertise and anchor relationships in target industries to gain additional customers in those industries. Since 2006, we have expanded our operations to cover six targeted industries and hired experts to oversee our operations in these industries. Our industry experts have developed detailed operating protocols that can be adapted readily to specific customer requirements and have specific sales goals for their markets. In addition, our industry experts have deep knowledge of each facet of the customer experience from shipment booking through planning, tracking and delivery. We believe our industry experts provide a significant competitive advantage in many of the targeted industries that demand highly specialized transportation solutions.

Expand our North American network.

We are expanding our North American network by actively recruiting owner operators and third-party carriers.

| • | Owner operators. Our exclusive owner-operator capacity is a competitive advantage, and we are actively seeking to expand our owner-operator fleet. We seek to offer our owner operators a more attractive package than our competitors. We also offer technology that provides our owner operators visibility of all shipments in our system as well as “hot spots” where they can reposition their vehicles to quickly pick up the next load. In addition, we are highly focused on our owner operators’ quality of life concerns and maintain good relations with our owner operators. We also have identified attributes of successful fleet operators and are actively recruiting small business owners to invest in additional fleets. |

| • | Third party carrier network. Our third-party carrier network allows us to grow revenue independent of the size of our owner-operator fleet. Since 2006, we have expanded our third-party network to over 1,600 third-party ground carriers. Our flexible network of third party carriers allows us to capture significant revenue beyond what our exclusive owner operators can handle. |

Grow international air and ocean freight forwarding.

Since 2008, we have developed an international capability by offering air and ocean freight forwarding services. We see tremendous opportunity in this $176 billion (as of 2009) global market. In the first six months of 2010 we handled shipments to or from 38 countries, and international shipments contributed 6.5% of our revenue. We are pursuing this market aggressively by soliciting North American customers for their international business as part of our single-source solution. We have targeted 10 international gateway cities in the United States (New York, Atlanta, Miami, Chicago, Dallas, Houston, San Diego, Los Angeles, San Francisco, and Seattle) where we are hiring experienced international sales people and investing in building our brand in these markets. Because our international business is non-asset based, the expansion cost is relatively small compared with asset-based network operators.

Pursue selected acquisitions.

Over the past five years we completed three acquisitions and successfully integrated their operations. These acquisitions expanded our owner-operator network, enhanced our air freight forwarding capabilities, provided a West Coast sales and operations footprint and brought us our

5

Table of Contents

network optimization software. We intend to continue to evaluate and pursue selected acquisitions with an emphasis on businesses that we expect to expand our geographic coverage, increase our network density, accelerate our expansion into new industry verticals, or expand our service capabilities.

Industry opportunity

The global freight transportation industry includes a broad range of transportation modes and service levels. Within this industry, Panther operates in three key growing markets, expedited transportation, premium freight logistics and freight forwarding.

Expedited transportation services are used by clients for time-critical services and are characterized by very stringent pick-up and delivery windows, advanced technology and high levels of customer service. Examples of such time-critical requirements are just-in-time deliveries of spare parts and components to manufacturers, specific delivery windows for large retail chains with significant penalties for delayed deliveries, and special shipments of new electronic product releases for holiday shopping seasons. Expeditors typically provide 24 hours a day, 7 days a week and 365 days a year availability, on demand pick-up within 90 minutes of request and delivery within 15 minutes of customer-specified times, and real-time tracking and tracing. Service providers in the expedited market include pure expeditors that maintain a dedicated network for expedited shipments and larger carriers that offer expedited services as a part of a broader transportation offering. Due to the critical nature of the service provided and the added level of reliability, speed, visibility and personalized service, expedited freight services command significant price premiums over traditional, non-expedited modes of transportation. The expedited transportation market is estimated by SJ Consulting to be $3.0 billion in 2009 with a growth rate of 14.0% in 2010 and then returning to a more normalized annual growth rate of 7.1% for the years 2011 to 2014.

As supply chain requirements of shippers have evolved in recent years, we have seen increased focus on the premium freight logistics market, which is characterized by stringent customer-specific delivery requirements in addition to time-definite pick-up and delivery windows. Premium freight logistics include door-to-door transportation of freight requiring specialized services, whether because of time critical requirements, special handling requirements, high value freight, special permit needs or any additional complexities that need customized solutions. While requirements vary from sector to sector, we believe there is an increasing demand for specialized services such as temperature controlled freight with Food and Drug Administration protocol compliant cold-chain solutions, advanced security solutions as well as shipment tracking and visibility, backed by highly personalized service and sophisticated technology. These specialized services result in the potential to command premium pricing. The premium freight logistics market as defined by us corresponds to the premium freight transportation market as defined and estimated by SJ Consulting. SJ Consulting estimates that market to be $22.7 billion for 2009 with a growth rate of 10.0% for 2010 and then returning to a more normalized annual growth rate of 7.5% for the years 2011 to 2014.

The freight forwarding market is comprised of non-asset based transportation providers that arrange for multimodal transportation of heavyweight, non-local freight. The domestic freight forwarding market is estimated by SJ Consulting to be $4.6 billion with projected revenue for 2010 at $5.1 billion, with a growth rate of 10.0% for 2010 and returning to a more normalized

6

Table of Contents

growth rate of 4.8% for the years 2011 to 2014. The global freight forwarding market is estimated by SJ Consulting to be $176 billion in 2009 with a growth rate of 19.5% in 2010 and then returning to a more normalized annual growth rate of 10.3% for the years 2011 to 2014.

Key trends

The expedited, premium freight logistics and freight forwarding segments are expected to benefit from a variety of trends including the following:

Increased outsourcing. Companies are increasingly focused on core competencies and improved customer service that result in the need for third party expert solutions backed by advanced technology capabilities.

LEAN supply chains and low inventory levels. Companies are continuing to advance their supply chains and to focus on just-in-time delivery. These companies also have a heightened desire to keep inventories and working capital low. As a result, they increasingly need and value efficient expedited solutions.

Complex supply chains. The growing need for integrated supply chain solutions is driving the need for premium logistics experts that have the ability to offer enhanced real-time visibility, reduced supply chain disruptions and comprehensive customer service.

Shortened product cycles. As product cycles change and the life cycle of products continue to contract, we believe that companies will continue to seek out premium providers with the ability to react quickly and efficiently to meet their needs as their supply chains change with their business models.

Continued globalization. Companies with expanding global operations are confronted with increased regulatory and security requirements as well as production and distribution challenges, creating demand for sophisticated providers with the ability to manage these complexities.

Competition

Panther’s competitive landscape is highly fragmented. In the expedited services and premium freight logistics segments, quality of service, technological capabilities and industry expertise are critical differentiators. In particular, companies with advanced technological systems that offer optimized shipping solutions, real-time visibility of shipments, verification of chain of custody procedures and advanced security carry significant operational advantages and create enhanced customer value. In addition, we believe that as supply chains become more geographically complex and diverse, carriers that are able to offer broader geographic coverage stand to gain over other providers.

Risks related to our business

Investing in our common stock involves a high degree of risk, and our ability to successfully operate our business is subject to numerous risks, including those that generally are associated with our industry. You should carefully consider the risk and uncertainties summarized below, the risks described under “Risk factors,” the other information contained in this prospectus, and our consolidated financial statements and the related notes before you decide whether to purchase our common stock.

7

Table of Contents

| • | Our business is subject to general economic and business factors that are largely out of our control, such as recessionary economic cycles, changes in inventory levels, excess transportation capacity and downturns in customer business cycles, any of which could have a materially adverse effect on our operating results. |

| • | We operate in highly competitive and fragmented segments of our industry and the effects of that competition could adversely affect our profitability. |

| • | We have a history of net losses. We can make no assurances that we will achieve profitability, or if we do, we may not be able to sustain or increase profitability in the future. |

| • | Our owner operators are critical to the execution of our ground services. If we are unable to attract and retain the number of owner operators necessary to support our customers’ freight volumes, we may not be able to grow or maintain our revenues. |

| • | If we fail to develop, implement, maintain, upgrade, enhance and integrate our information technology systems, demand for our services could decrease and our business may be seriously harmed. |

| • | If we are unable to maintain the high level of service we provide to our customers, we may experience damage to our reputation and a resulting loss of business. |

| • | If we are unable to expand the number of our sales and customer service employees, or if a significant number of our sales and customer service employees leave us, our ability to increase our revenues could be negatively impacted. |

| • | We operate in a highly regulated industry and increased costs of compliance with, liability for violation of or changes in existing or future regulations could have a materially adverse effect on our business and profitability. |

Our equity sponsor

Funds managed by Fenway Partners beneficially own, through a special purpose LLC, approximately 75.8% of our common stock and will be our largest stockholder upon consummation of this offering. In addition, Fenway Partners is expected to receive $1.9 million in accrued but unpaid management fees and $5.1 million as a management agreement termination fee, of which $5.0 million will be payable contemporaneously with this offering and $2.0 million of which will be payable in 2011. Fenway Panther Holdings, LLC, an entity affiliated with Fenway Partners, will participate as a selling stockholder to the extent the underwriters’ over-allotment is exercised and will receive shares of common stock as a result of the conversion of the unpaid accumulated preferred stock dividends to common stock and the conversion of all of our outstanding preferred stock to common stock. For more information related to Fenway Partners’ ownership of us, its ability to elect our directors, and its transactions with us, see “Risk factors — Certain relationships and related party transactions” and “Principal and selling stockholders.”

Fenway Partners is a leading private equity investment firm based in New York, with funds under management of more than $1.6 billion. Founded in 1994, Fenway Partners provides active oversight and strategic guidance to improve the operating and financial performance of its

8

Table of Contents

portfolio companies. Fenway Partners’ focus is on building long-term value in partnership with management through direct investments in leading middle-market companies in two core industry segments, transportation/logistics and branded consumer products.

Panther

Panther Transportation, our predecessor and current subsidiary, began its operations in 1992. We were incorporated in Delaware on May 6, 2005 and became the parent company of Panther Transportation on June 10, 2005. We conduct all of our business through our subsidiaries. Our principal executive offices are located at 4940 Panther Parkway, Seville, Ohio 44273 and our telephone number is (330) 769-5830. We maintain an Internet website at www.pantherexpedite.com. We have not incorporated by reference into this prospectus the information on our website and you should not consider it to be a part of this prospectus.

9

Table of Contents

The offering

| Issuer |

Panther Expedited Services, Inc. |

| Common stock offered by us |

shares |

| Over-allotment option |

The selling stockholders have granted the underwriters an option to purchase up to an additional shares of common stock within 30 days of the date of this prospectus in order to cover over-allotments, if any. |

| Common stock to be outstanding after this offering |

shares |

| Offering price |

We expect the offering price to be between $ and $ per share. |

| Risk factors |

Investing in our common stock involves a high degree of risk. See “Risk factors” for a discussion of factors you should carefully consider before investing in our common stock. |

| Use of proceeds |

We estimate that our net proceeds from this offering will be approximately $ million (assuming an initial public offering price of $ per share, the midpoint of the filing range set forth on the cover of this prospectus and after deduction of underwriting discounts and estimated expenses payable by us). We will not receive any proceeds from the sale of shares of our common stock by the selling stockholders pursuant to the underwriters’ over-allotment option. |

We intend to use our net proceeds from this offering to repay a portion of the amounts outstanding under our existing senior secured credit facility (the “Credit Facility”), redeem our 17% senior subordinated notes, repay a note payable to the sellers of Elite Logistics, LLC, pay Fenway Partners accrued but unpaid management fees and a termination fee payable under our management agreement with Fenway Partners, and pay all or a portion of the dividends accumulated on our cumulative preferred stock. See “Use of proceeds.”

| Dividend policy |

We have no current plans to pay any cash dividends in the foreseeable future. |

| Proposed listing symbol |

“PTHR” |

| Directed share program |

At our request, the underwriters have reserved for sale, at the initial public offering price, up to shares offered by this prospectus to our directors, officers, employees, business associates and related persons. |

10

Table of Contents

Contemporaneously with this offering, we intend to amend our certificate of incorporation to (1) increase the number of authorized shares of common stock to shares, (2) effect a -for-one stock split of our outstanding common stock, (3) to convert all outstanding shares of preferred stock that are not purchased with the proceeds of this offering to common stock on a -for-one basis and (4) to convert any accumulated dividends on our cumulative preferred stock to common stock to the extent not paid with the proceeds of this offering. Following this offering and the amendment of the certificate of incorporation, we will only have shares of our common stock outstanding.

Unless otherwise indicated, all information contained in this prospectus assumes:

| • | the underwriters’ option to purchase additional shares of common stock from the selling stockholders is not exercised; and |

| • | that the common stock to be sold in this offering is sold at $ , which is the midpoint of the range set forth on the cover of this prospectus. |

Unless otherwise indicated, the number of shares of common stock to be outstanding after this offering:

| • | gives effect to the proposed -for-one stock split of our common stock; |

| • | gives effect to the proposed conversion of all our outstanding shares of preferred stock into shares of common stock at a -to-one conversion ratio; |

| • | assumes that $ of dividends accumulated on the cumulative preferred stock are paid in cash and the remaining $ of dividends accumulated on the cumulative preferred stock are converted into common shares on the basis of an initial public offering price of $ per share, the midpoint of the filing range set forth on the cover of this prospectus; |

| • | gives effect to the assumed exercise of all our outstanding warrants to purchase shares of our common stock; |

| • | includes shares of issued unvested common stock issued under our incentive compensation plans other than our Cash Incentive Plan; |

| • | includes shares of common stock to be issued under our Cash Incentive Plan in connection with the offering; |

| • | excludes shares of common stock issuable upon the exercise of outstanding stock options at a weighted average exercise price of $ per share; and |

| • | excludes shares of common stock available for additional grants under our incentive compensation plans. |

The share amounts and per share dollar amounts included in the consolidated financial statements and the accompanying notes have also been adjusted to reflect for the above actions retroactively unless otherwise indicated.

11

Table of Contents

Summary consolidated financial and other data

The following table sets forth our summary consolidated financial and other data for the periods and as of the dates indicated. The summary consolidated statement of operations data for the fiscal years ended December 31, 2006, 2007, 2008 and 2009 are derived from our audited consolidated financial statements with 2007 through 2009 being included elsewhere in this prospectus. The summary statement of operations data for the six months ended June 30, 2009 and 2010 and the summary consolidated balance sheet data for the six-month period ended June 2010 have been derived from our unaudited condensed consolidated financial statements included elsewhere in this prospectus. These unaudited consolidated financial statements have been prepared on the same basis as our audited consolidated financial statements, and in the opinion of management, include all adjustments, consisting of normal recurring accruals, which we consider necessary for a fair presentation of the results of operations for these periods. The historical results presented below are not necessarily indicative of the results expected for any future period. This information should be read in conjunction with the consolidated financial statements and related notes included elsewhere in this prospectus and the information contained in “Use of proceeds,” “Capitalization,” “Selected consolidated financial data,” and “Management’s discussion and analysis of financial condition and results of operations.”

| (in thousands, except per share data or as otherwise noted) | Year

ended December 31, |

Six months

ended June 30, |

||||||||||||||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2009 | 2010 | |||||||||||||||||||||||

| (unaudited) | ||||||||||||||||||||||||||||

| Consolidated statement of operations data: |

||||||||||||||||||||||||||||

| Revenues |

$ | 170,363 | $ | 190,293 | $ | 189,961 | $ | 157,832 | $ | 66,397 | $ | 95,009 | ||||||||||||||||

| Operating expenses: |

||||||||||||||||||||||||||||

| Purchased transportation |

118,260 | 134,707 | 135,612 | 115,279 | 49,163 | 69,927 | ||||||||||||||||||||||

| Personnel and related benefits |

15,544 | 18,466 | 19,394 | 19,159 | 9,603 | 11,760 | ||||||||||||||||||||||

| Insurance and claims |

2,951 | 3,935 | 3,211 | 6,213 | 2,475 | 2,016 | ||||||||||||||||||||||

| Depreciation |

923 | 865 | 1,179 | 1,579 | 812 | 703 | ||||||||||||||||||||||

| Amortization of intangibles(1) |

7,674 | 7,840 | 7,827 | 8,077 | 4,038 | 4,038 | ||||||||||||||||||||||

| Goodwill and intangibles impairment(2) |

— | — | — | 33,498 | 33,498 | — | ||||||||||||||||||||||

| Other operating expenses |

10,221 | 12,382 | 12,637 | 12,150 | 5,773 | 6,281 | ||||||||||||||||||||||

| Total operating expenses |

155,573 | 178,195 | 179,860 | 195,955 | 105,362 | 94,725 | ||||||||||||||||||||||

| Operating income (loss) |

14,790 | 12,098 | 10,101 | (38,123 | ) | (38,965 | ) | 284 | ||||||||||||||||||||

| Interest expense |

12,449 | 11,344 | 12,730 | 14,003 | 6,461 | 7,984 | ||||||||||||||||||||||

| Other expenses (income) |

1,862 | (141 | ) | (319 | ) | (71 | ) | (31 | ) | (32 | ) | |||||||||||||||||

| Income (loss) before taxes |

479 | 895 | (2,310 | ) | (52,055 | ) | (45,395 | ) | (7,668 | ) | ||||||||||||||||||

| Income tax provision (benefit) |

101 | 815 | (213 | ) | (8,761 | ) | (7,639 | ) | (2,776 | ) | ||||||||||||||||||

| Net income (loss) |

$ | 378 | $ | 80 | $ | (2,097 | ) | $ | (43,294 | ) | $ | (37,756 | ) | $ | (4,892 | ) | ||||||||||||

| Less undeclared cumulative preferred dividends(3) |

$ | (3,300 | ) | $ | (3,809 | ) | $ | (4,370 | ) | $ | (5,015 | ) | $ | (2,421 | ) | $ | (2,779 | ) | ||||||||||

| Net income (loss) available to common stockholders |

$ | (2,922 | ) | $ | (3,729 | ) | $ | (6,467 | ) | $ | (48,309 | ) | $ | (40,177 | ) | $ | (7,671 | ) | ||||||||||

| Average number of shares outstanding |

||||||||||||||||||||||||||||

| Basic and diluted |

3,026,550 | 3,046,343 | 3,061,136 | 3,107,210 | 3,105,570 | 3,108,822 | ||||||||||||||||||||||

| Earnings (loss) per share available to common stockholders: |

||||||||||||||||||||||||||||

| Basic and diluted income (loss) per share |

$ | (0.97 | ) | $ | (1.22 | ) | $ | (2.11 | ) | $ | (15.55 | ) | $ | (12.94 | ) | $ | (2.47 | ) | ||||||||||

| Pro Forma Earnings (loss) per share available to common stockholders(4) |

||||||||||||||||||||||||||||

| Basic and diluted income (loss) per share |

||||||||||||||||||||||||||||

| Cash flow data: |

||||||||||||||||||||||||||||

| Cash flow provided by operating activities |

8,294 | 10,372 | 4,407 | 1,172 | 3,666 | 968 | ||||||||||||||||||||||

| Cash flow used in investing activities |

(9,580 | ) | (7,743 | ) | (6,638 | ) | (778 | ) | (406 | ) | (787 | ) | ||||||||||||||||

| Cash flow (used in) provided by financing activities |

1,323 | (3,001 | ) | 2,760 | (2,153 | ) | (3,356 | ) | (500 | ) | ||||||||||||||||||

| Capital expenditures |

438 | 1,634 | 2,301 | 953 | 479 | 932 | ||||||||||||||||||||||

| Key performance indicators: |

||||||||||||||||||||||||||||

| Average shipments per business day |

743 | 868 | 757 | 687 | 600 | 737 | ||||||||||||||||||||||

| Average revenue per shipment |

$ | 917 | $ | 871 | $ | 995 | $ | 911 | $ | 894 | $ | 1,031 | ||||||||||||||||

| Average number of employees |

256 | 319 | 368 | 341 | 345 | 364 | ||||||||||||||||||||||

| Gross profit percentage |

30.6% | 29.2% | 28.6% | 27.0% | 26.0% | 26.4% | ||||||||||||||||||||||

| Adjusted EBITDA(5) |

23,783 | 25,139 | 23,052 | 8,812 | 1,163 | 6,270 | ||||||||||||||||||||||

12

Table of Contents

| As of June 30, 2010 | ||||||

| (in thousands) | Actual | As adjusted(6) | ||||

| (unaudited) | ||||||

| Consolidated balance sheet data: |

||||||

| Cash and cash equivalents |

$ | 120 | $ | |||

| Total assets |

$ | 162,146 | $ | |||

| Total debt |

$ | 113,894 | $ | |||

| Cumulative preferred stock |

$ | 21,385 | $ | |||

| Total stockholders’ equity |

$ | 11,920 | $ | |||

| (1) | We incur non-cash amortization related to the amortization of our finite-lived intangible assets. As a result of the acquisition of Panther, a portion of the purchase price was allocated to our intangible assets based upon their fair market values. The finite-lived intangible assets, which include our proprietary information systems platform and our customer relationships, are being amortized using the straight-line method over estimated useful lives of seven years and eighteen years, respectively. |

| (2) | As a result of our testing of our goodwill and other indefinite lived intangibles in 2009, non-cash impairment charges were recorded reducing the carrying value of our goodwill and trade name by $28.1 million and $5.4 million, respectively. See “Management’s discussion and analysis of financial condition and results of operations.” |

| (3) | Our cumulative preferred stock ranks senior in right of payment to all other classes or series of our capital stock as to dividends, and upon liquidation, dissolution, or winding up of Panther. The holders of our cumulative preferred stock are entitled to receive, when, as and if declared by our Board of Directors, cumulative preferential dividends on each share of cumulative preferred stock at a rate of 14% per year of the liquidation preference of $1,000 on each share of stock. Dividends on our cumulative preferred stock accrue whether or not we have earnings or the dividends are declared. Upon any voluntary or involuntary liquidation, dissolution, or winding up of Panther, each holder is entitled to payment of an amount equal to the liquidation preference of $1,000 per share of our cumulative preferred stock plus accrued and unpaid dividends before any distribution is made to the holders of other securities, including the common stock. |

| In January 2006, we issued 2,239 additional shares of cumulative preferred stock for $2.4 million in a private placement to third-party investors and repurchased 44,015 shares of the outstanding cumulative preferred stock for $47.2 million, including $3.2 million of cumulative preferred stock dividends. In connection with our January 2006 refinancing, the dividend rate on our outstanding cumulative preferred stock increased from 12% to 14%. |

| In connection with this offering, all of the dividends accumulated on the outstanding cumulative preferred stock will be paid in cash or converted to common stock and all the outstanding cumulative preferred stock will be redeemed or converted to common stock. See “Use of proceeds.” |

| (4) | For a description of the adjustments used to arrive at Pro Forma Earnings (loss) per share and a reconciliation to Earnings (loss) per share, see “Unaudited pro forma consolidated financial data.” |

| (5) | We use the term “Adjusted EBITDA” throughout this prospectus. Adjusted EBITDA, as we define this term, is not presented in accordance with GAAP. We use Adjusted EBITDA as a supplement to our GAAP results in evaluating certain aspects of our business, as described below. |

We define Adjusted EBITDA as net income (loss) plus (1) interest expense (less interest income), (2) income tax provision (benefit), (3) depreciation of property and equipment, (4) amortization of intangibles, (5) goodwill and intangibles impairment, (6) management fees and Board of Director fees and expenses, (7) stock option expense and (8) other adjustments expense.

Our Board of Directors and executive management team focus on Adjusted EBITDA as a key measure of our performance, for business planning and for incentive compensation purposes. Adjusted EBITDA assists us in comparing our performance over various reporting periods on a consistent basis because it removes from our operating results the impact of items that, in our opinion, do not reflect our core operating performance. Our method of computing Adjusted EBITDA is the same as that used in our debt covenants under our Credit Facility and also is routinely reviewed by management for that purpose. For a reconciliation of our Adjusted EBITDA to our net income (loss), the most directly related GAAP measure, please see the table below.

Our President and Chief Executive Officer, who is our chief operating decision-maker, and our compensation committee traditionally have used Adjusted EBITDA thresholds in setting performance goals for our senior management. We believe such performance goals provide an incentive to improve profitability and thereby increase long-term stockholder value.

The annual bonuses for executive management are based on Adjusted EBITDA. At the same time, some or all of these executives have responsibility for monitoring our financial results generally, including the items included as adjustments in calculating Adjusted EBITDA (subject ultimately to review by our Board of Directors in the context of the Board of Directors’ review of our quarterly financial statements). While many of the adjustments involve mathematical application of items reflected in our financial statements, others involve a degree of judgment and discretion. While we believe that all of these adjustments are appropriate and while the quarterly calculations are subject to review by our Board of Directors in the context of the Board of Directors’ review of our quarterly financial statements and certification by our Chief Financial Officer in a compliance certificate provided to the lenders under our Credit Facility, this discretion may be viewed as an additional limitation on the use of Adjusted EBITDA as an analytical tool.

13

Table of Contents

We believe our presentation of Adjusted EBITDA is useful because it provides investors and securities analysts the same information that we use internally for purposes of assessing our core operating performance.

Adjusted EBITDA is not a substitute for net income (loss) cash flows from operating activities, operating margin, or any other measure prescribed by GAAP. There are limitations to using non-GAAP measures such as Adjusted EBITDA. Although we believe that Adjusted EBITDA can make an evaluation of our operating performance more consistent because it removes items that, in our opinion, do not reflect our core operations, other companies in our industry may define Adjusted EBITDA differently than we do. As a result, it may be difficult to use Adjusted EBITDA or similarly named non-GAAP measures that other companies may use to compare the performance of those companies to our performance.

Because of these limitations, Adjusted EBITDA should not be considered a measure of the income generated by our business or discretionary cash available to us to invest in the growth of our business. Our management compensates for these limitations by relying primarily on our GAAP results and using Adjusted EBITDA supplementally.

A reconciliation of GAAP net income (loss) to Adjusted EBITDA for each of the fiscal periods indicated is as follows:

| (in thousands) | Year

ended December 31, |

Six

months ended June 30, |

||||||||||||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2009 | 2010 | |||||||||||||||||||||

| (unaudited) | ||||||||||||||||||||||||||

| Net income (loss) |

$ | 378 | $ | 80 | $ | (2,097 | ) | $ | (43,294 | ) | $ | (37,756 | ) | $ | (4,892 | ) | ||||||||||

| Plus interest expense |

12,449 | 11,344 | 12,730 | 14,003 | 6,461 | 7,984 | ||||||||||||||||||||

| Plus taxes |

101 | 815 | (213 | ) | (8,761 | ) | (7,639 | ) | (2,776 | ) | ||||||||||||||||

| Plus depreciation |

923 | 865 | 1,179 | 1,579 | 812 | 703 | ||||||||||||||||||||

| Plus amortization of intangibles |

7,674 | 7,840 | 7,827 | 8,077 | 4,038 | 4,038 | ||||||||||||||||||||

| Plus goodwill and intangibles impairment |

— | — | — | 33,498 | 33,498 | — | ||||||||||||||||||||

| Plus management fees and Board of Director fees and expenses |

1,783 | 3,459 | 2,798 | 2,771 | 1,404 | 964 | ||||||||||||||||||||

| Plus stock option expense |

474 | 736 | 828 | 429 | 345 | 249 | ||||||||||||||||||||

| Plus other adjustments(7) |

— | — | — | 510 | — | — | ||||||||||||||||||||

| Adjusted EBITDA |

$ | 23,783 | $ | 25,139 | $ | 23,052 | $ | 8,812 | $ | 1,163 | $ | 6,270 | ||||||||||||||

| (6) | The balance sheet data as of June 30, 2010 is presented on an actual basis and on an as adjusted basis to give effect to the sale of shares of common stock by us in this offering at an assumed initial offering price of $ per share, after deducting underwriting discounts and commissions and estimated offering expenses to be paid by us, and the application of proceeds as described in “Use of proceeds.” |

| (7) | Sales adjustment reserve relating to a one-time reversal of revenues due to customer settlements. |

14

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the following risks, as well as the other information included in this prospectus, before deciding to invest in our common stock. If any of the following risks actually occur, they may materially harm our business, financial condition and results of operations. As a result, the trading price of our common stock could decline and you might lose part or all of your investment.

Risks related to our business and industry

Our business is subject to general economic and business factors that are largely out of our control, any of which could have a materially adverse effect on our operating results.

Our business is dependent on a number of factors that may have a negative impact on our results of operations, many of which are beyond our control. We believe that some of the most significant of these factors are economic changes that affect supply and demand in transportation markets, such as:

| • | recessionary economic cycles; |

| • | changes in our customers’ inventory levels and in the availability of funding for their working capital; |

| • | excess transportation capacity in comparison with shipping demand; and |

| • | downturns in our customers’ business cycles. |

Further, the demand for expedited shipping correlates with the overall level of domestic spending in the United States, which in turn is influenced by factors such as inflation, consumers’ spending habits, employment rates and other macroeconomic factors over which we have no control. The risks associated with these factors are heightened when the U.S. and global economy are weakened. Some of the principal risks during such times are as follows:

| • | we may experience low overall freight levels, which may impair our ability to grow, or which may reduce, our revenue; |

| • | certain of our customers may face credit issues and cash flow problems; |

| • | in an effort to cut costs, customers may change their outsourcing and shipping strategies and other providers may be selected; |

| • | reductions in inventories may reduce freight volumes and the need for our services; and |

| • | customers may bid out freight or select competitors that offer lower rates from among existing choices in an attempt to lower their costs and we might be forced to lower our rates or lose freight. |

We also are subject to increases in costs that are outside of our control that could materially impact our revenues and profitability. Such cost increases include, but are not limited to, interest rates, taxes, tolls, fuel, license and registration fees and healthcare and benefits costs for our employees.

15

Table of Contents

In addition, events outside our control, such as strikes or other work stoppages at customer, port, border or other shipping locations or actual or threatened armed conflicts or terrorist attacks, efforts to combat terrorism, military action against a foreign state or group located in a foreign state or heightened security requirements could lead to reduced economic demand, reduced availability of credit or temporary closing of shipping locations or U.S. borders. Such events or enhanced security measures in connection with such events could impair our operating efficiency and productivity and result in higher operating costs.

We operate in highly competitive and fragmented segments of our industry and our business may suffer if we are unable to adequately address factors adversely affecting our revenues and expenses relative to our competitors.

Competition within the freight industry is intense and the segments of the freight transportation industry in which we participate are highly competitive and very fragmented. Certain segments of the freight transportation industry historically have had few barriers to entry. Through our array of premium freight logistics services, we compete against other non-asset based logistics companies as well as asset-based carriers; freight forwarders that dispatch shipments via asset-based carriers; smaller expedited carriers; integrated transportation companies that operate their own aircraft; cargo sales agents and brokers; internal shipping departments at companies that have substantial transportation requirements; associations of shippers organized to consolidate their members’ shipments to obtain lower freight rates; and smaller niche service providers that provide services in a specific geographic market, industry segment or service area.

Numerous competitive factors could impair our ability to maintain or improve our current profitability. These factors include the following:

| • | we may compete with other expedited, freight forwarding and logistics transportation providers of varying sizes and, to a lesser extent, standard transportation providers, some of which have access to larger fleets, broader coverage networks, a wider ranges of services and greater capital resources than we do; |

| • | the continuing trend toward consolidation in the freight transportation industry may create more large competitors with greater financial resources and other competitive advantages related to size with whom we may have difficulty competing; |

| • | many of our competitors periodically reduce their freight rates to gain business, especially during times of reduced growth in the economy, which may limit our ability to maintain or increase freight rates or to maintain or expand our business or may require us to reduce our freight rates; |

| • | in recent years a number of shippers have reduced the number of carriers they use by selecting core carriers as approved service providers, and some of our customers may not select us as a core carrier; |

| • | many customers periodically solicit bids from multiple providers for their shipping needs and this process may depress freight rates or result in a loss of business to competitors; |

| • | advances in technology may require us to increase investments in order to remain competitive and our customers may not be willing to accept higher freight rates to cover the cost of these investments; |

16

Table of Contents

| • | establishment by our competitors of cooperative relationships to increase their ability to address shippers’ needs; and |

| • | we face intense competition in attracting and retaining qualified owner operators from the available pool of drivers and fleets, which may require us to increase owner-operator compensation or take other measures to remain an attractive option for owner operators. |

We have a recent history of net losses.

For the years ended December 31, 2009 and 2008 and for the six months ended June 30, 2010 we incurred net losses of $43.3, $2.1 million and $4.9 million, respectively. Achieving profitability depends upon numerous factors, including the level of domestic spending and our ability to expand our overall volume and control expenses while maintaining or increasing our rates. We might not achieve profitability or, if we do, we may not be able to sustain or increase profitability in the future.

Increases in owner operator compensation or other difficulties attracting and retaining qualified owner operators could adversely affect our profitability and ability to maintain or grow our fleet.

A significant portion of our ground transportation services is provided to our customers through our owner operators, who are responsible for maintaining their own equipment and paying their own fuel, insurance, licenses and other operating costs. Our owner operators provide all of the vans, straight trucks and tractors they use in our ground expedited business. Owner operators make up a relatively small portion of the pool of all professional drivers in the United States. Turnover and bankruptcy among owner operators often limit the pool of qualified owner operators and increases competition for their services. Thus, our continued reliance on owner operators could limit our ability to grow our ground transportation fleet.

From time to time we have experienced difficulty in attracting and retaining sufficient numbers of qualified owner operators and such shortages may recur in the future. Additionally, our agreements with owner operators are terminable by either party upon short notice and without penalty. Consequently, we regularly need to recruit qualified owner operators to replace those who have left our fleet. If we are unable to retain our existing owner operators or recruit new owner operators, our business and results of operations could be adversely affected.

The compensation we offer our owner operators is subject to market conditions and we may find it necessary to continue to increase owner-operator compensation in future periods, which may be more likely to the extent economic conditions continue to improve. If we are unable to continue to attract and retain a sufficient number of owner operators, we could be required to adjust our compensation packages or operate with fewer trucks and face difficulty meeting shipper demands, all of which would adversely affect our profitability and ability to maintain our size or grow.

CSA 2010 could adversely affect our profitability and operations, our ability to maintain and grow our fleet of owner operators and our customer relationships.

Under CSA 2010, drivers and fleets will be evaluated and ranked based on certain safety-related standards. The methodology for determining a carrier’s DOT safety rating will be expanded to include the on-road safety performance of the carrier’s drivers. As a result, certain current and potential owner operators may no longer be eligible to drive for us, our fleet could be ranked poorly as compared to our peer firms, and our safety rating could be adversely impacted.

17

Table of Contents

A reduction in eligible owner operators or a poor fleet ranking may result in difficulty attracting and retaining qualified owner operators, and could cause our customers to direct their business away from us and to carriers with higher fleet rankings, which would adversely affect our results of operations.

The new safety-related standards are scheduled to be implemented in the beginning of December 2010, and enforcement is scheduled to begin in 2011. These implementation and enforcement dates have already been delayed and may be subject to further change. The FMCSA recently made it possible for motor carriers to preview their initial safety ratings under CSA 2010 before implementation begins. One reason that carriers are able to see their initial ratings early is to enable them to review and update data in FMCSA records. We are in the process of reviewing and correcting portions of the data; however, two of our seven initial scores indicate potential deficiencies that we may not be able to fully rectify prior to implementation of CSA 2010.

We believe that based upon the results of our CSA 2010 ratings preview we will continue to have a satisfactory DOT rating which currently is the highest safety rating a motor carrier can have. However, the CSA 2010 scores are preliminary and are subject to change by the FMCSA. There is a possibility that a drop in our CSA 2010 ratings could adversely impact our DOT safety rating. We are preparing for CSA 2010 in a number of ways including reviewing all existing safety programs and using technology to educate and monitor our owner operators.

The FMCSA also is considering revisions to the existing rating system and the safety labels assigned to motor carriers evaluated by the DOT. If we were to receive a conditional or unsatisfactory DOT safety rating, it could adversely affect our business because some of our customer contracts require a satisfactory DOT safety rating, and a conditional or unsatisfactory rating could negatively impact or restrict our operations. In addition, there is a possibility that a drop to conditional status would significantly increase our insurance costs. Under the revised rating system being considered by the FMCSA, all motor carrier safety ratings, including ours, would be evaluated more regularly and our safety rating would reflect a more in-depth assessment of safety-based violations.

Finally, proposed FMCSA rules and practices followed by regulators may require our owner operators to install electronic, on-board recorders in their tractors if we experience unfavorable compliance with these pending rules or if we receive an adverse change in safety rating. Such installation could cause an increase in owner operator turnover, adverse information in litigation and cost increases for our owner operators.

If we are unable to maintain the high level of service we provide to our customers, we may experience damage to our reputation and a resulting loss of business.

Our reputation is based on the level of personalized customer service that we provide, tailored to our customers’ shipping needs and we compete with other premium transportation providers based on our reliability, delivery time, security, visibility and personalized service. Our customers, in turn, pay a premium for this level of service. If this level of service deteriorates; if we are prevented from delivering on our promises of timeliness, reliability and security; or if we are unable to attract and retain the professional customer service staff that our business model demands, our business may suffer.

18

Table of Contents

If our owner operators and third-party carriers do not meet our needs or expectations or those of our clients, our business could suffer.