Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended July 3, 2010

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-10031

NOBEL LEARNING COMMUNITIES, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 22-2465204 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) | |

| 1615 West Chester Pike, Suite 200 West Chester, PA |

19382 | |

| (Address of Principal Executive Offices) | (Zip Code) |

Registrant’s telephone number, including area code: (484) 947-2000

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Stock, par value $.001 per share Series A Junior Preferred Stock Purchase Rights |

Nasdaq Stock Market LLC (Nasdaq Global Market) Nasdaq Stock Market LLC (Nasdaq Global Market) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ¨ Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act).

Large accelerated filer ¨ Accelerated filer x Non-accelerated filer ¨ Small reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of December 26, 2009 (the last business day of the registrant’s most recently completed second fiscal quarter) was approximately $77,783,000 (based upon the closing sale price of these shares on such date as reported by the Nasdaq Global Market). The number of shares of the registrant’s common stock, par value $0.001 per share, outstanding at September 9, 2010, was 10,550,701

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement for the Annual Meeting of Stockholders to be held on November 10, 2010 (the “Proxy Statement”) and to be filed within 120 days after the registrant’s fiscal year ended July 3, 2010 are incorporated by reference in Part III.

Table of Contents

| Item No. |

Page | |||

| PART I | ||||

| 1. |

1 | |||

| 1A. |

10 | |||

| 1B. |

17 | |||

| 2. |

17 | |||

| 3. |

17 | |||

| 4. |

18 | |||

| PART II | ||||

| 5. |

19 | |||

| 6. |

21 | |||

| 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

23 | ||

| 7A. |

54 | |||

| 8. |

55 | |||

| 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

55 | ||

| 9A. |

55 | |||

| 9B. |

58 | |||

| PART III | ||||

| 10. |

59 | |||

| 11. |

59 | |||

| 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

59 | ||

| 13. |

Certain Relationships and Related Transactions, and Director Independence |

59 | ||

| 14. |

59 | |||

| PART IV | ||||

| 15. |

60 | |||

i

Table of Contents

CAUTIONARY STATEMENTS ABOUT FORWARD-LOOKING INFORMATION

Statements included or incorporated herein which are not historical facts are forward-looking statements pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. When the Company uses words such as “believes,” “expects,” “anticipates,” “plans,” “estimates,” “projects,” “may,” “intends,” “seeks” or similar expressions, the Company is making forward-looking statements, but these terms are not the exclusive means of identifying forward-looking statements.

Forward-looking statements reflect management’s current views with respect to future events and financial performance and are based on currently available competitive, financial and economic data and management’s assumptions regarding future events. While management believes that its assumptions are reasonable, forward-looking statements are subject to various known and unknown risks and uncertainties and actual results may differ materially from those expressed or implied herein. In connection with the “safe harbor provisions” of the Private Securities Litigation Reform Act of 1995, the Company notes that certain factors, among others, which could cause future results to differ materially from the forward-looking statements, expectations and assumptions expressed or implied herein are discussed in greater detail under Item 7; “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Item 1A “Risk Factors.” In addition, potential risks and uncertainties include, among others, unemployment rates impacting our current or future enrollments; changes in general economic conditions; the implementation and results of our ongoing strategic initiatives; our ability to compete with new or existing competitors; dependence on senior management and other key personnel; the litigation with the Department of Justice relating to alleged violations of the American with Disabilities Act; and the high concentration of ownership of the Company’s stock among its four largest stockholders. Readers are cautioned that the forward-looking statements reflect management’s analysis only as of the date hereof and the Company assumes no obligation to update or revise these statements or to update the reasons why actual results could differ from those projected in the forward-looking statements, whether as a result of new information, future developments or otherwise.

ii

Table of Contents

| ITEM 1. | BUSINESS. |

General

Nobel Learning Communities, Inc. (collectively with its subsidiaries, the “Company” or “Nobel Learning Communities”) is a national network of nonsectarian private schools, including preschools, elementary schools, middle schools and specialty high schools in 15 states and the District of Columbia. In addition, the Company operates a K-12 distance learning online college prep school. Nobel Learning Communities provides high-quality private education, with small schools and class sizes and attention to individual learning styles. We also offer an array of supplemental educational services, including before-and-after-school programs, the Camp Zone® summer program, learning support programs and camps. Our schools operate under various brand names and are located in the District of Columbia, Arizona, California, Florida, Illinois, Maryland, Nevada, New Jersey, North Carolina, Ohio, Oregon, Pennsylvania, South Carolina, Texas, Virginia, and Washington. As of September 9, 2010, the Company operated 184 schools.

The following trademarks are in use by the Company, all of which have either been registered or are in the process of being registered in the United States Patent and Trademark Office: Chesterbrook Academy®, Merryhill School®, Discovery Isle Child Development Center, Enchanted Care Learning Center, Camelback Desert Schools, The Honor Roll School®, Camp Zone®, Paladin Academy®, Rocking Horse Child Care Centers®, Southern Highlands Preparatory School, Montessori Corner, HighPointe Children’s Academy, Houston Learning Academy™ and Laurel Springs School. We believe that certain of our service marks have substantial value in our marketing in the respective areas in which our schools operate.

Our corporate office is located at 1615 West Chester Pike, Suite 200, West Chester, PA 19382-6223. Our telephone number is (484) 947-2000. Nobel Learning Communities, Inc., a Delaware corporation, was formed on March 30, 1983.

Educational Program and Delivery Model

We deliver research-based, standards-driven curricula in all its schools. The content of our curricula is closely monitored by our Education Department to ensure that changes to national and state standards are reflected in our own national K-12 standards. Our Education Department continually evaluates programs and practices related to early childhood development so that the curriculum reflects the latest and best research-based content for preschoolers. The framework for delivery of this content embraces student-centered learning. Classroom learning is often organized around guided centers, cooperative learning activities, and project-based learning.

Accreditation

We seek to ensure that our schools meet or exceed the standards of appropriate accrediting agencies through an internal quality assurance program. Although not mandated by any governmental or regulatory authority, many of our schools are accredited, or are currently seeking accreditation through the Commission on International and Trans-Regional Accreditation (CITA)/AdvancED and/or with various regional accreditation agencies throughout the United States. Regional accreditation agencies include Middle States Association of Colleges and Schools, North Central Association of Colleges and Schools, Southern Association of Colleges and Schools and Western Association of Colleges and Schools. The company also maintains corporate accreditation through CITA/AdvancED; and is accredited through June 30, 2014.

Preschool Educational Program

Links to Learning, our preschool curriculum, is an integrated series of programs for children ages six weeks to five years that engages the young learner’s senses, mind and body. The components of each program build

1

Table of Contents

upon each other as children grow and develop, ensuring an excellent preparation for elementary school. The program draws from the collective expertise of renowned early-age educators such as Dewey, Piaget and Vygotsky. The Links to Learning Curriculum builds new learning on past experiences, and encourages each child’s interest in discovery and hands-on learning. Links to Learning was created by the Nobel Learning Education Department, a team of highly skilled experts with extensive knowledge of early-age education.

Links to Learning divides skills into distinct academic areas. These areas are: Language and Literacy, Mathematics, The World and Me, My Community and Environment, Art, Music, Wellness and Spanish.

The Links to Learning program features a strong parent communication component. Nobel Learning believes that when parents and teachers work as partners in a child’s education, the learning experience is richer and more meaningful. Parents receive materials each month, containing an overview of the developmental skills that the child has worked on that month. The materials contain samples of their children’s work that was completed in class, as well as a letter outlining suggested activities that can be done with their child at home. The materials also provide a preview of the next month’s skills and lessons. Teachers post weekly and daily skills lists outside the classroom as further support to these activities.

The Links to Learning Curriculum focuses on two vital goals: developing a child’s lifelong love of learning and ensuring that he/she is ready for kindergarten and elementary school. Our Education Department studied the kindergarten standards in all of the states in which there are kindergarten classes and carefully designed the preschool program to meet or to exceed pre-kindergarten expectations. Each preschool has a “Links to Kindergarten” section on its school website so that parents can be assured of a successful transition to kindergarten by matching to the appropriate state standards.

Elementary and Middle School Educational Program

Standards-Based Content

In 2007 Nobel Learning created a standards-based curriculum for kindergarten through eighth grades. To do so, the members of the Education Department researched the standards in 46 states and merged them into one set of national standards. This was done for critical content areas: language arts, writing, math, science, social studies, technology, physical education, wellness, art, music, Spanish, and study skills. Each content area has standards with corresponding objectives of what students need to know and be able to do. Each grade level has a comprehensive curriculum binder that takes each of the content areas and divides the standards and objectives into four quarterly pacing guides. The pacing guides then create a synchronous curriculum for the Company’s national network of schools which provides unique collaborative learning opportunities, such as Learning Without Walls projects and Giving Without Walls, our student-driven social entrepreneurship programs.

Delivery System

The content of the Nobel Learning curriculum is dictated by state standards. The core curriculum contains the content of what we teach. Then, through planning instruction, lessons and personalized learning plans, we integrate 21st century themes and skills into the delivery of that content. The content delivery model includes traditional classroom instruction, as well as 21st century skills projects in grades 1 through 8. These projects are based on the framework provided by the Partnership for the 21st Century Skills organization. Nobel Learning is a professional development affiliate of the Partnership for 21st Century Skills (www.21stcenturyskills.com),the leading advocacy organization focused on infusing 21st century skills into education.

Through project-based learning, we are able to enrich and sometimes accelerate the delivery of our curriculum. All students in grades 1 through 8, in collaboration with their teachers and parents create a Personal Learning Plan for each school year. The Personal Learning Plan is an opportunity for the teacher, parents and student to work together on goals related to their current and future academic success. Our project based learning programs include “Giving Without Walls” projects which allow our 1st through 8th grade students to be active

2

Table of Contents

participants in service-learning opportunities. Student-led service-learning projects integrate meaningful community service with instruction and reflection to enrich the learning experience, teach civic responsibility, and encourage lifelong civic engagement.

“Learning Without Walls” is another project-based learning program that is offered for grades 4 through 8. These projects require students to use 21st Century skills while working with our network schools across the country. The projects challenge students to explore highly relevant, curriculum-based topics, use a variety of technology tools to research their topic and collaborate with students in different parts of the country as they work through the project timeline. The ability to share, to interact, and to work in small regional or larger national teams offers a rich learning environment, in which students are challenged to apply their knowledge in authentic ways to solve real problems.

Assessment

It is essential to continuously monitor students’ academic performance to ensure that they meet or exceed grade-level benchmarks for proficiency. All students in grades 1 through 8 participate in SAT10 testing each spring. Those test results are used to monitor student progress and set achievement goals. In addition, we use an online assessment program in reading and math to give teachers weekly feedback on how each student is performing relative to the recent lessons and concepts in order to personalize lessons and instruction programs for each student based on his or her current needs.

Teachers

We recognize that investing in the quality of our teachers’ capabilities and professionalism is essential to sustaining our students’ high level of academic achievement and our profitability. We sponsor professional development days covering various aspects of teaching and education, using both internal trainers and external consultants. Our educators serve on Company task forces and committees that review and revise curricular guidelines, programs, support materials and teaching methods.

Training

In support of teachers’ professional development, during the 2008/2009 school year we implemented Education Connections. Education Connections is an intranet site dedicated to providing training resources and support for our teachers. The intranet site includes a teacher communication and support area, exemplary lesson plan library, grade level curriculum support and other valuable resources to support and enhance our teachers’ professional development, professional relationships, and satisfaction.

School-based leadership teams (Principals and Assistant Principals) also actively engage in professional development and self-improvement. Staff training is provided by our education department and other experts within the education industry. Through participation in our annual National Principal Conference, seasoned administrators as well as new recruits are kept abreast of up-to-date research, changing trends and sound pedagogical practices. Our Executive Directors and many of our highest performing principals are utilized as trainers to help with professional development and curriculum implementation in our schools.

School Operations

Standards

In order to maintain appropriate standards, our schools share consistent educational goals and operating procedures. While we have a national curriculum, Principals may tailor curricula, within the standards of Nobel Learning Communities’ Education Department guidelines, to meet local and state requirements. Members of our management team visit schools on a regular basis to review program, facility and staff quality. Hiring and retaining quality personnel at our schools and in operational management positions is a critical success factor in driving success in both operational and financial performance.

3

Table of Contents

Our school Principals and Assistant Principals are responsible for all facets of school operations, including curriculum implementation, ensuring student achievement and success, personnel and financial management, community outreach, student discipline and implementing local sales and marketing strategies. The Principals and Assistant Principals are supported by our regional operations, education and human resources teams and our centralized marketing, real estate, facilities and finance organizations.

We operate and review our performance based on both geographic cluster and individual school based performance criteria. Each school has an annual budget and financial and operating information is collected daily. Certain measures of school and cluster performance are reviewed weekly and others are reviewed monthly or quarterly. We determine whether to monitor a particular aspect of performance based on its impact on our operational and financial objectives. For example, net revenue, tuition revenue, certain operating costs and student census information are monitored weekly in relation to our objectives.

Executive Directors

Executive Directors oversee the Principals and schools and report to a Regional Vice President. Executive Directors, along with our Education Department, are responsible for ensuring the qualifications of Principals and Assistant Principals, as well as training and development. School Principals and Executive Directors work closely with regional Education Managers and corporate management, particularly in the regular assessment of program quality and school performance.

We hire qualified candidates and attempt to promote from within when possible. Candidate credentials are reviewed through employment references, criminal background checks and appropriate education verification in order to establish an understanding of the candidates’ skills, professionalism and character. After hiring, it is our policy that employees receive regular performance feedback including a formal annual performance evaluation. Our Principals and Executive Directors may be eligible for incentive compensation based on the performance of their schools.

Private Pay Schools

General Education Schools

The Company operates a complementary dual track strategy. Track 1 is the preschool strategy track in which the Company operates preschools that are generally clustered in geographic areas. Clusters of preschools are placed in geographic markets where the economy and population meet our demographic profile. Track 2 is the K-12 strategy track. This track primarily includes brick and mortar schools which typically start at kindergarten and may go through grade 8. We also operate a K-12 distance learning and online school. We believe that both the preschool strategy track and the K-12 strategy track provide the company with multiple growth opportunities. In markets where our strategy tracks are integrated, students from our preschools can easily matriculate into our elementary/middle school programs.

Many of our preschools and elementary schools allow for early drop-off and late pick-up to accommodate busy parent schedules. In most preschool locations, programs are available for children starting at six weeks of age. We believe that parents can feel comfortable leaving their children at one of our schools knowing the children will receive both a quality education and engage in well-supervised developmental, recreational and enrichment activities.

Our schools also offer athletic activities and supplemental programs, which include day field trips coordinated with our curriculum to zoos, libraries, museums and theaters and, at the middle schools, overnight trips to such places as national parks and historical locations, and select summer trips to European destinations. Schools arrange classroom presentations by parents, community leaders and other volunteers to supplement instruction. We also organize programs that allow students to present to community groups and organizations. To enhance the child’s physical, social, emotional and intellectual growth, schools may provide extra-curricular

4

Table of Contents

experiences (some fee-based) tailored to particular families’ interests. These activities include but are not limited to dance, gymnastics, instrumental music lessons and computer-based technology programs. Additionally, students expand their horizons through participation in science fairs, drama clubs and local and regional academic competitions. Most of our preschools and elementary schools complement their educational programs with enrichment programs, arts programs, before-and-after-school programs and summer programs or camps. In addition to those revenue generating programs, our schools seek to improve margins by providing ancillary services and products, such as portrait photos, books and uniform sales.

Laurel Springs Distance Learning and Online College Prep K-12

In September, 2009, we Acquired Laurel Springs School, a K-12 distance learning private school. Curriculum is delivered to students via text, online and through project-based learning symposiums. Laurel Springs’ students are supported by teachers and staff who work with students on a one-to-one basis. Laurel Springs focuses on the college prep student who wishes to grow and excel academically and personally while keeping a flexible and self-paced schedule. Most students at Laurel Springs are full time, but some students take a course or two while concurrently enrolled in another school. Many of these part time students take courses to get ahead of their traditional course and/or grade path or take courses which are not offered in their school. Courses are mastery based, so students can move through a course at their own pace once they pass a series of assessments.

Marketing

Our primary sources for generating new enrollments include word-of-mouth recommendations from current parents, interactive marketing including search engine marketing, direct mail campaigns, yellow page listings and public relations programs. We utilize a paid search engine marketing program that is customized to generate and track new leads for each individual market and product type. We also market to our own database of parent inquiries through ongoing direct mail and e-mail communications.

Marketing efforts towards continuous improvement of customer acquisition and retention are directed by a central marketing team. Working in conjunction with school operations management and the education team, marketing formulates consistent brand positioning and communication strategies that can be customized to each local area and type of school. The efforts of central marketing are supplemented by community-based activities conducted by our local Executive Directors and Principals.

Our annual marketing calendar is synchronized with the typical customer demand cycle for enrollment. Although marketing campaigns and demand take place throughout the year, we direct the most marketing resources towards our preschool enrollments in late summer and early winter and towards our K+ schools during fall and winter.

The Company has implemented a number of marketing communication tools to strengthen our communications with existing customers and increase customer retention and length of stay. These tools include, but are not limited to, e-mail newsletters, enhanced school specific websites, updated in-school and in-classroom communication materials and parent satisfaction surveys.

Corporate Development—Strategy and Implementation

Our growth strategy in the private education market includes internal growth of our enrollment at existing schools, expansion of current facilities, new school development in both existing and new markets and strategic acquisitions.

Much of our focus is on increasing occupancy and ancillary program revenue in our existing schools and leveraging the investment in those assets. Management has implemented training programs designed to

5

Table of Contents

strengthen Principals’ and Executive Directors’ sales, marketing and customer service skills and invests in school administrative staffing. In addition, to broaden the potential career path opportunities for employees, we have provided employees the ability to move between locations as appropriate opportunities arise. The similar business and education model our schools operate under permits the Company to execute on this career path strategy. As our growth has increased, we now have a number of examples where our Principals or Assistant Principals have transferred to other schools in different geographic markets.

In addition to the focus on improving the performance of existing schools, the Company also identifies opportunities to develop and open new schools and to acquire schools that are consistent with our demographic profile in contiguous geographic markets.

We regularly analyze the performance of our existing school and real estate portfolio to identify schools that are underperforming and/or do not fit our business model or demographic and geographic cluster strategy. We then develop plans either to improve these schools or remove them from our portfolio. This represents an important activity in reallocating capital to the balance of our schools in order to ensure the continued improvement of our program offerings and overall company performance.

New School Development

During Fiscal 2010, we opened four new preschools. For new school development, we typically engage a developer or contractor to build a facility to our specifications. We also look to occupy existing buildings that are appropriate for our schools and that are located in growth areas that meet our demographic requirements. The Company continues, as part of its strategy, to focus on private pay markets supported by complementary demographics. Our new school development strategy builds upon our practice of clustering schools by geographic area. Clusters of schools are placed in geographic markets where the economy and population meet our demographic profile. In several markets, students from our preschools can easily matriculate into our elementary/middle school programs. In addition, we can potentially convert students from our specialty and before-and-after programs to our general education programs. We believe many of our existing markets have opportunity to add new preschools and we seek to acquire K-8 schools in our existing and new geographic markets.

Acquisitions

We expect to use acquisitions to expand our business. Key acquisition criteria include reputation, location in markets meeting our target demographics, growth prospects, quality of personnel and the ability to integrate into existing market clusters or become the platform for new market clusters. Acquisitions are primarily focused on schools that fit our demographic and cluster strategy and which serve the preschool and/or kindergarten through eighth grade markets. From time to time we evaluate opportunities which, while related in educational content, may provide the Company entry into a variety of other business models. These may include companies that have business models that focus on extending our platform through high school, on-line K-12 schools, on-line course delivery, enrichment programs, summer camps, technology based before-and-after school programs, and concepts with a focus on international students.

During the first quarter of Fiscal 2010, the Company acquired the Laurel Springs School (“Laurel Springs”), an online and distance learning school (www.laurelsprings.com). Laurel Springs’ educational program spans the entire K-12 market and has a fully accredited curriculum that includes Honors AP Courses, a Gifted and Talented program, a chapter of the National Honors Society and a strong college preparatory program. Laurel Springs’ student body includes elite athletes, entertainers, and home schooled students. Laurel Springs has served students from all fifty states and a number of foreign countries. The acquisition of Laurel Springs extends our educational programs through high school and provides a distance learning and online K-12 platform.

6

Table of Contents

Also, during the first quarter of Fiscal 2010, the Company completed the acquisition of Gifted Child Studies, Inc. (“GCS”). GCS added one elementary school to the Company’s existing market coverage in the San Diego, California market.

During the fourth quarter of Fiscal 2009, we acquired three Montessori schools in central New Jersey collectively referred to as “Montessori Corner”, the addition of these schools added one elementary school and two preschools to the three Montessori method schools already in the Company’s portfolio of schools. Also during the fourth quarter of Fiscal 2009, the Company acquired the Highpointe Children’s Academy (“Highpointe”). The addition of Highpointe added a preschool and an elementary school and expanded the Company’s existing market coverage in the Dallas, Texas market. During the third quarter of Fiscal 2009 the Company acquired Country Tyme Preschool, which expanded the Company’s existing market coverage in the Southeastern Pennsylvania market. During the first quarter of Fiscal 2009, the Company acquired Southern Highlands Preparatory Schools (“SHPS”) which included a preschool and elementary school and expanded the Company’s existing market coverage in the Las Vegas, Nevada market. SHPS has become a destination middle school for many of our elementary school students from one of our Merryhill elementary schools in that market. Additionally, during the first quarter of Fiscal 2009 the Company acquired Ivy Kids Learning Center School (“Ivy Kids”) which has subsequently been rebranded under the Company’s existing “The Honor Roll School ®” brand. The Ivy Kids acquisition expanded the Company’s existing market coverage in the Houston, Texas market by adding one preschool to a market in which the Company currently operates.

During Fiscal 2008, we acquired Enchanted Care Learning Centers, the acquisition included six standalone facilities offering before-and-after school programs for elementary school-age children under the Kid’s Campus trade name. This acquisition provides the Company opportunities in existing and new geographic markets to further develop its growth strategy. In addition, the Fiscal 2008 acquisition of the Ivy Glen Schools in the Dallas market also provided the company with one standalone before-and-after school program. During Fiscal 2008, the Company further enhanced the value of the Discovery Isle acquisition and the Discovery Isle brand by acquiring two additional schools in the southern California market previously branded as Teddy Bear Treehouse Schools, which were quickly re-branded as Discovery Isle schools. Also during Fiscal 2008, the Company acquired four Learning Ladder preschools, three of which were rebranded under the Company’s existing Chesterbrook Academy brand, and the fourth of which was closed shortly after completing the acquisition. During the fiscal year ended June 30, 2007 (“Fiscal 2007”), we entered a new geographic market with the acquisition of the six Discovery Isle preschools in San Diego, California. In this case, the acquisition provided the Company the opportunity to expand the Discovery Isle preschool brand through the development or acquisition of additional preschools and elementary and/or middle schools that could utilize the Discovery Isle preschools as a feeder system for elementary school students.

7

Table of Contents

The table below summarizes the Company’s recent history of acquisitions:

| Number of facilities acquired | Market | |||||||||||

| Name of Acquisition |

Fiscal Year |

Preschool | PreK & K - 8 |

Before-and-After (2) | Description | (N)ew or (E)xisting | ||||||

| Laurel Springs School |

2010 | — | — | — | Distance Learning | N | ||||||

| Gifted Child Studies, Inc. |

2010 | — | 1 | — | San Diego, CA | E | ||||||

| Montessori Corner |

2009 | 2 | 1 | — | Princeton, NJ | N | ||||||

| HighPointe Childrens Academy |

2009 | — | 1 | — | Dallas, TX | E | ||||||

| Country Tyme |

2009 | 1 | — | — | Limerick, PA | E | ||||||

| Southern Highlands Preparatory Schools |

2009 | 1 | 1 | — | Las Vegas, NV | E | ||||||

| Ivy Kids Early Learning Center |

2009 | 1 | — | — | Missouri City, TX | E | ||||||

| Camelback Desert Schools (1) |

2008 | — | 2 | — | Phoenix, AZ | N | ||||||

| Enchanted Care Learning Centers (2) |

2008 | 9 | — | 6 | Columbus, OH | N | ||||||

| Ivy Glen Schools |

2008 | 3 | — | 1 | Dallas, TX | E | ||||||

| Teddy Bear Treehouse |

2008 | 2 | — | — | San Diego, CA | E | ||||||

| Learning Ladder (3) |

2008 | 4 | — | — | Lancaster, PA | E | ||||||

| Discovery Isle |

2007 | 6 | — | — | San Diego, CA | N | ||||||

| (1) | During the fourth quarter of Fiscal 2009, the Company closed one Camelback Desert School. The results of this school are included in Net income (loss) from discontinued operations in the periods presented in this Form 10K. |

| (2) | Before-and-After facilities are integral to adjacent school facilities and as such are not incremental to total school count |

| (3) | In conjunction with the acquisition of Learning Ladder schools the Company determined one location would be closed. This location was closed during the same quarter that this acquisition was completed. |

Seasonality

Our elementary/middle schools historically have lower operating revenues in the summer due to the end of the traditional academic year and seasonally lower enrollment and related fees in summer programs. Summer revenues of preschools are, to a lesser degree, subject to the same seasonality. Management seeks to reduce the seasonal fluctuations of the Company’s revenue stream by adding to its schools a mix of products and services, such as camp programs, in the lower revenue seasons.

Industry and Competition

Education reform movements in the United States are providing new alternatives to the public schools. These reforms include charter schools, private management of public schools, home schooling, private schools, virtual charter schools, state run virtual schools, virtual private schools and voucher programs. Our strategy is to provide parents a high quality alternative to public schools and traditional child care through our privately owned and operated schools, utilizing proven curriculum in a safe and challenging environment. We consider each of these alternatives to be competition for our schools and the expansion or contraction of funding and/or public support of these alternatives may impact the demand for our product, available real estate and our ability to increase or maintain our operating margins. Additionally, throughout this document, references are made to the child care industry, child care and child care competitors. Many of the companies with which we compete with offer child care services and many of our potential customers need child care services. In many cases, our curriculum-based preschools are suitable substitutes that can satisfy the child care demand while offering the additional educational developmental programs and services delivered in our preschools.

8

Table of Contents

Furthermore, we compete with other for-profit private schools, charter schools, non-profit schools, sectarian schools, private virtual schools, public virtual schools and home schooling. We also face competition with respect to preschool services and before- and-after-school programs from public schools, government-based providers and religiously affiliated community-based or other non-profit programs that may offer such services at little or no cost to parents. We anticipate that, given the perceived potential of the education market, well-financed competition may emerge, including possible competition from the large for-profit child care companies and international school operators. We believe the only large for-profit competitors that integrate preschool, elementary education and school age programs in the U.S. and that currently compete beyond a regional level are privately held Knowledge Learning Corp., Bright Horizons Family Solutions, Inc. and Mini-Skools, Challenger Schools and Learning Care Group. We also face regional competition in each of our markets from operators of individually owned private schools. Finally, public school systems may become stronger competitors at the preschool level if additional states pass or expand universal pre-K legislation that provides public funds for preschool for three and four year olds and does not allow for-profit preschool operators to participate in these programs, or fund payments to for-profit operators at lower than market prices or costs.

While price is an important factor in competing in both the preschool and elementary school markets, we believe that other competitive factors are also important, including trained teachers, location, professionally developed educational programs, qualified and trained school administrators, well-equipped facilities, relationships with local employers and a broad range of ancillary services, including before-and-after-school programs, transportation and infant care. Some of these services are not offered by some of our competitors. We conduct annual tuition rate surveys and believe we are competitively priced in each of our markets.

Regulation

Our schools are subject to national, state and local regulations and licensing requirements. We have policies and procedures in place to assist in complying with such regulations and requirements. These regulations and the administrative bodies in charge of these regulations vary from jurisdiction to jurisdiction and may apply differently within the same jurisdiction to a preschool, elementary or middle school. The regulatory and licensing requirements tend to be more stringent with respect to preschools, as government agencies generally review the fitness and adequacy of buildings and equipment, the ratio of staff personnel to enrolled children, staff training, record keeping, children’s dietary program, daily curriculum and compliance with health and safety standards. In most jurisdictions, these agencies conduct scheduled and unscheduled inspections of the schools and licenses must be renewed periodically. Most jurisdictions establish requirements for background checks or other clearance procedures for new employees of schools. Repeated failures of a school to comply with applicable regulations can subject the school to sanctions, which might include probation or, in more serious cases, suspension or revocation of the school’s license to operate and could also lead to investigations of our other schools located in the same jurisdiction. In addition, this type of action could lead to negative publicity extending beyond that jurisdiction and potentially affecting our other locations. We believe that our operations are in substantial compliance with all material regulations applicable to our business. However, there is no assurance that a licensing authority will not determine a particular school to be in violation of applicable regulations and take action against that school and possibly other schools in the same jurisdiction. In addition, there may be unforeseen changes in regulations and licensing requirements, such as changes in the required ratio of child center staff personnel to enrolled children that could have a material adverse effect on our operations. States in which we operate routinely review the adequacy of regulatory and licensing requirements and implement changes, which may significantly increase our costs to operate in those states.

Environmental Compliance

We are not aware of any existing environmental conditions that currently or in the future could reasonably be expected to have a material adverse effect on our financial position, operating results or cash flows and we have not incurred material expenditures to address environmental conditions at any school. Although we have periodically conducted limited environmental investigations and remedial activities at some of our schools, we

9

Table of Contents

have not undertaken an in-depth environmental review of all of our schools and accordingly, there may be material environmental liabilities of which we are unaware. In addition, no assurances can be given that future laws or regulations will not impose any material environmental liability.

Insurance

We currently maintain comprehensive general liability, workers’ compensation, automobile liability, property, excess umbrella liability, terrorism, student accident insurance and directors’ and officers’ liability insurance. The policies provide a variety of coverages and limits. Companies involved in the education and care of children, however, may not be able to obtain insurance for the total risks inherent in their operations. In particular, general liability coverage can have sublimits per claim for child abuse. Although we believe we have adequate insurance coverage at this time, claims in excess of, or not included within, our coverage may be asserted. In addition, there can be no assurance that in future years we will not become subject to lower limits or a substantial increase in insurance premiums.

Employees

As of September 9, 2010, we employed approximately 4,700 persons. None of the Company’s employees are represented by a labor union. We believe that our relationship with our employees is satisfactory.

Recently the child care industry in general saw an increase in organized labor contracts with child care workers and preschool teachers, especially in states such as Washington and California. While there have been no specific attempts to organize our teachers or other employees, there is no assurance that in future years we or the industry will not be subject to some form of labor organization attempt.

Available Information

All periodic and current reports, registration statements, code of conduct and other material that the Company is required to file with the Securities and Exchange Commission (“SEC”), including the Company’s annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) of the Securities and Exchange Act of 1934 (“the 1934 Act Reports”), are available through the Company’s investor relations page at www.nobellearningcommunities.com. Such documents are available as soon as reasonably practicable after electronic filing of the material with the SEC. The Company’s Internet website and the information contained therein or connected thereto are not intended to be incorporated into this Annual Report on Form 10-K.

The public may also read and copy any materials filed by the Company with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site at www.SEC.gov, which contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

Each of the following risks, individually or in a group, could have a material adverse affect on the Company’s business, results of operations, financial condition or cash flows.

Changing economic conditions, including unemployment rates, as demand for the Company’s products and services are a lagging indicator of the economy

The Company’s revenue and net income are subject to general economic conditions. The Company’s revenues depend, in part, on the number of dual-income families and working single parents who require child

10

Table of Contents

development, child care or educational services. A deterioration of general economic conditions, including a soft housing market and rising unemployment may adversely impact the Company because of the tendency of out-of-work parents to diminish or discontinue utilization of these services. In addition, the Company may not be able to increase tuition at a rate consistent with increases in wages, health insurance and other operating costs or continue tuition increases at historical rates experienced in the industry. Finally, there can be no assurance that demographic trends, including the number of dual-income families in the work force, will continue to lead to increased market share.

Changing social and economic conditions and their impact on public school systems

Recently, the general economy and budget constraints have caused some public school systems to study moving to a four day school week, year round school calendar or shorter school year. To the extent that there are any material changes to the traditional school year schedule, it may impact our business. There is uncertainty as to whether these changes will be implemented in any of our markets and if so, what the impact on our business may be. Additionally, due to state and local economic pressures due to the general economy, many public school systems are changing their policy relating to providing transportation for children within the school district who attend private school. While we have few schools whose students receive transportation through public school systems, there may be some impact on students in some of our schools, should the public school systems change their transportation policies. Finally, in reaction to the recession and budget cuts, many public school systems are re-evaluating policies and programs such as class size, subjects offered, transportation and athletic programs. While we do not yet know the impact of decisions made by numerous local school systems, it is possible that changes in public school programs or policies could impact our schools and enrollments. It is unclear whether any potential impact will be positive or negative to our business.

The Company’s ability to hire and retain qualified Executive Directors, Principals, Teachers and Teachers’ Aides

The Company may experience difficulty in attracting and retaining qualified personnel in various markets necessary to meet growth opportunities. Hiring and retaining qualified personnel may require increased salaries and enhanced benefits in more competitive markets. Difficulties in hiring and retaining qualified personnel may also impact the Company’s ability to obtain additional enrollments, and retain existing enrollment at its preschools and elementary schools. In addition, while the Company’s wage ranges are generally materially above minimum wage, any future changes to federal and state changes to the minimum wage laws may reduce the qualified applicant pool or increase our wage costs.

Recently the child care and preschool industries in general saw an increase in organized labor contacts with child care workers and preschool teachers, especially in states such as Washington and California. While there have been no specific attempts to organize our teachers or other employees, there is no assurance that in future years we or the industry will not be subject to some form of labor organization attempt.

The Company’s ability to retain key individuals in acquired schools and/or successfully identify, acquire, grow and integrate acquired schools’ operations

Acquisitions are an ongoing part of the Company’s growth strategy. Acquisitions involve numerous risks, including potential difficulties in the assimilation of acquired operations, not meeting financial objectives, additional need for capital investment, undisclosed liabilities not covered by insurance or indemnification provisions in the acquisition agreement, diversion of management’s attention in connection with an acquisition and potential loss of key employees of the acquired operation. No assurance can be given as to the success of the Company in identifying, executing and integrating acquisitions in the future or the ability to identify satisfactory acquisition targets and successfully complete any acquisition.

11

Table of Contents

The Company’s inability to defend successfully against or counter negative publicity associated with claims involving alleged incidents at its schools

Because of the nature of its business, the Company is and expects that in the future it will be subject to claims and litigation alleging negligence, inadequate supervision and other grounds for liability arising from injuries or other harm to the children it serves, primarily children. In addition, claimants may seek damages from the Company for child abuse, sexual abuse and other acts allegedly committed by Company employees. There can be no assurance that additional lawsuits will not be filed, that the Company’s insurance will be adequate to cover liabilities resulting from any claim or that any such claim or that the publicity resulting from it will not have a material adverse effect on the Company’s business, results of operations and financial condition including, without limitation, adverse effects caused by increased cost or decreased availability of insurance and decreased demand for the Company’s services.

We currently maintain comprehensive general liability, workers’ compensation, automobile liability, property, excess umbrella liability, terrorism, student accident insurance and directors’ and officers’ liability insurance. The policies provide a variety of coverages and limits. Companies involved in the education and care of children, however, may not be able to obtain insurance for the total risks inherent in their operations. In particular, general liability coverage can have sublimits per claim for child abuse. Although we believe we have adequate insurance coverage at this time, claims in excess of, or not included within, our coverage may be asserted. In addition, there can be no assurance that in future years we will not become subject to lower limits or substantial increase in insurance premiums.

Increased employer costs of employee healthcare benefits and further employer subsidies

Rising healthcare costs and interest in universal healthcare coverage in the United States have resulted in government and private sector initiatives proposing healthcare reforms. On March 10, 2010, The Health Care and Education Reconciliation Act of 2010 was signed into law. Various healthcare reform proposals have also emerged at the state level. We cannot predict what, if any, further healthcare initiatives will be implemented at the federal or state level, or the effect this or any future legislation or regulation will have on us. However, we may be required in the future to provide healthcare benefits to a greater percentage of our employees and to subsidize a greater percentage of the costs of healthcare benefits of our employees. The resulting increased costs could adversely affect our financial condition and results of operations.

Control of a majority of the outstanding common stock of the Company by a small number of stockholders

A limited number of our stockholders can exert significant influence over us. As of September 16, 2010, four stockholders and their affiliates controlled approximately 70% of the Company’s outstanding Common Stock. This share ownership would permit these and other stockholders, if they chose to act together, to exert significant influence over the outcome of stockholder votes, including votes concerning the election of directors, by-law amendments, possible mergers, corporate control contests and other significant corporate transactions.

The effect of anti-takeover provisions in the Company’s Certificate of Incorporation, bylaws and Delaware law and Shareholders’ Rights Plan

The Company’s certificate of incorporation and bylaws contain certain provisions that could make more difficult the acquisition of the Company by means of a tender offer, a proxy contest or otherwise. These provisions establish staggered terms for members of the Company’s Board of Directors and include advance notice procedures for stockholders to nominate candidates for election as directors of the Company and for stockholders to submit proposals for consideration at stockholders’ meetings. In addition, the Company is subject to Section 203 of the Delaware General Corporation Law (“DGCL”) which limits transactions between a publicly held company and “interested stockholders” (generally, those stockholders who, together with their affiliates and associates, own 15% or more of a company’s outstanding capital stock). This provision of the DGCL may have the effect of deterring certain potential acquisitions of Nobel Learning Communities. The Company’s certificate

12

Table of Contents

of incorporation provides for 8,936,170 authorized but unissued shares of preferred stock. The rights, preferences, qualifications, limitations and restrictions of these unissued authorized shares preferred stock may be fixed by the Company’s Board of Directors without any further action by stockholders.

On July 20, 2008, the Company’s Board of Directors adopted a limited duration Shareholder Rights Plan designed to protect the Company’s shareholders in the event of an attempt to acquire control of the Company on terms which do not secure fair value for all of the Company’s shareholders. The Board has adopted a limited duration Plan that expires in four years, rather than the more common ten-year term. The four-year term was selected to provide the Company with an opportunity to maximize long-term shareholder value by enabling management of the Company to execute on its growth strategy, while protecting shareholders from a creeping acquisition or other tactics to gain control of the Company without offering all shareholders an adequate price. In addition, the Plan is not intended to prevent a takeover. Instead, it is intended to encourage anyone seeking to acquire the Company to negotiate with the Company’s Board of Directors prior to attempting a takeover in order to ensure that any takeover reflects an adequate price and is consistent with interests of the Company’s shareholders and other constituencies.

The Company’s ability to find affordable real estate and renew existing locations on terms acceptable to the Company

We may be unable to identify and successfully negotiate or renew existing leases at attractive rents; which may impact the Company’s profitability. In addition, if the Company cannot renew school leases for an appropriate term length, it may impact enrollment should parents become concerned with the length of time a school will remain open in a particular location.

The Company’s ability to obtain the capital required to implement fully its business and strategic plan

Our ability to execute our business and strategic plan is dependent upon the availability of adequate financing sources on acceptable terms. Our efforts to execute our business plan and open or acquire new schools are subject to our ability to finance such growth. Based on current economic events and the related restraint in the capital markets, financing resources may be inadequate to support new school openings or acquisitions, and we may be required to seek additional capital to support such expansion efforts. Such additional capital may take the form of the issuance of debt or equity securities, among other forms. Beyond our existing revolving senior credit facility, we presently have no commitments to provide the Company with any additional capital should we determine that additional capital is required. In the event that management determines that additional capital is required to support the Company’s business and strategic plan, there is no assurance that we will be able to secure such financing on acceptable terms under the current condition of the capital markets. If we are unable to secure needed additional capital, our growth efforts would be curtailed.

Competitive conditions in the preschool and elementary school education and services industry, such as the growth of competitors as possible alternatives to the public school system, including virtual charter schools, charter schools and magnet schools

We compete for individual enrollment in a highly fragmented market. For enrollment, the Company competes with residential based child care (operated out of the caregiver’s home) and center-based child care which may include work-site child care centers, full and part-time child care centers and preschools, private and public elementary schools, and church-affiliated, government subsidized and other not-for-profit providers and schools. In addition, substitutes for organized preschool, child care, and educational services, such as relatives and others caring for a child or home schooling, can represent lower cost alternatives to the Company’s services. Management believes our ability to compete successfully depends on a number of factors, including qualifications of Principals and teachers, quality of care, quality of curriculum, site convenience and cost. We are often at a price disadvantage with respect to these alternative providers, who operate with little or no rental expense, little or no curriculum expense, and generally may not comply or are not required to comply with the

13

Table of Contents

same health, safety, insurance and operational regulations as the Company. Competitors in the private pay education service segment also may offer similar or competing services at a lower price than the Company and some may have access to greater financial resources than the Company. The Company also competes with many not-for-profit providers of child care and preschools, some of which receive government subsidies, as well as elementary schools, some of which are able to offer lower pricing than the Company. In addition, the Company is currently studying the impact, if any, of the rapid expansion of virtual, or on-line, schools on demand for the Company’s elementary and middle school products. There can be no assurance that the Company will be able to compete successfully against current and future competitors.

Government regulations affecting school operations

Our schools or other school and child-care based centers and programs are subject to numerous national, state and local regulations and licensing requirements. Although these regulations vary greatly from jurisdiction to jurisdiction, government agencies generally review, among other things, the adequacy of buildings and equipment, licensed capacity, the ratio of staff to children, educational qualifications of teachers and staff training, record keeping, the dietary program, the daily curriculum, hiring practices and compliance with health and safety standards. Failure of any location to comply with applicable regulations and requirements could subject it to governmental sanctions, which might include fines, corrective orders, probation, or, in more serious cases, suspension or revocation of the location’s license to operate or an award of damages to private litigants and could require significant expenditures by the Company to bring its location into compliance. Many government agencies may publish or publicly report major and/or minor regulatory violations and the Company may suffer adverse publicity, which could result in a loss of enrollment in a school or market. We believe that our operations are in substantial compliance with all material regulations applicable to our business. However, there is no assurance that a licensing authority will not determine a particular school to be in violation of applicable regulations and take action against that school and possibly other schools in the same jurisdiction. In addition, there may be unforeseen changes in regulations and licensing requirements, such as changes in the required ratio of child center staff personnel to enrolled children that could have a material adverse effect on our operations. States in which we operate routinely review the adequacy of regulatory and licensing requirements and implement changes, which may significantly increase our costs to operate in those states.

We have several special purpose high schools that provide our graduates with state-approved high school diplomas. There have been instances in the past when the local school district has determined our education materials or curriculum did not meet requirements for credit in their district thereby limiting our ability to successfully attract students. There is a risk that such determinations may be made in the future with respect to the same or different schools, and that as a result, our enrollment and financial performance in such schools will suffer.

We may not be able to adequately protect our intellectual property, which could adversely affect our business

We rely on a combination of trademarks, copyrights, service marks, trade secrets, and similar intellectual property rights to protect our brands and other intellectual property. Our ability to successfully execute our business strategy depends, in part, on our ability to use our existing intellectual property to enhance brand awareness in current and future markets. There can be no assurance that the actions we have taken to establish and protect our intellectual property will be adequate to prevent infringement, dilution, or other violation of our trademarks by others or to prevent others from claiming that our services infringe, dilute or otherwise violate third party trademarks or other proprietary rights. In some cases, litigation, which can result in substantial costs and diversion of our resources, may be necessary to protect our trademarks and other intellectual property rights or to defend against claims by third parties alleging that we infringe, dilute, misappropriate or otherwise violate third party trademark or other intellectual property rights.

The laws of foreign countries may not protect our intellectual property to the same extent as the laws of the United States. If our efforts to protect our intellectual property are not adequate, or if any third party

14

Table of Contents

misappropriates or infringes on our intellectual property, the value of our brands could be harmed which could adversely affect our business and operating results.

If additional jurisdictions pass “living wage” laws, our operations in those jurisdictions could be negatively impacted

“Living wage” laws set minimum wage rates above the federal minimum wage, adjusted to local cost of living conditions. Currently such laws exist or have recently passed at the state, county or local level in New York, California, Oregon, Washington and North Carolina. In many cases, the laws only cover certain job classifications (e.g., home health care workers in New York City) and are only applicable to companies doing business with or receiving benefits from state or local governments and agencies. Recently, there has been an effort in a number of jurisdictions to extend these benefits to child care workers, primarily in New York and California. Living wage laws, if enacted in jurisdictions where we do business, could increase our costs of operations and have a material, negative impact on our business and financial condition in those areas.

Breaches in data security could adversely affect the Company’s financial condition and operating results

For various operational needs, we receive certain personal information from enrolled and potential students, families and employees, such as names, addresses, credit and debit card numbers, and other information of a sensitive nature. While we have policies and practices that protect our data, a compromise of our systems, whether caused by a third party or by employee error or malfeasance, that results in personal information being obtained by unauthorized persons could adversely affect our reputation and brand, as well as our operations and financial condition, and could result in litigation against us or the imposition of fines and penalties. In addition, any security breach or inadvertent disclosure of personal or confidential information could require us to expend significant additional resources related to the security of information systems, could result in a disruption of our operations, and cause significant harm to our reputation and brand, all of which could reduce demand for our services.

The establishment of government mandated Universal Pre-K or similar programs or benefits that do not allow for participation by for-profit operators or allows for participation at low reimbursement rates

National, state or local child care and early age education benefit programs relying primarily on subsidies in the form of tax credits or other direct financial aid could provide the Company opportunities for expansion in additional markets, especially where these benefits are universal based on residency and age, as opposed to those based on socio-economic need or measures. However, a universal benefit with governmentally mandated or publicly provided child care could reduce the demand for educational services at the Company’s existing locations. Even in situations where the Company was allowed to provide publicly funded early age education programs, the amount of public funding, the rates at which the subsidies are granted, our subsidy participation requirements or restrictions could have a material adverse effect on the Company’s business and financial condition if the Company were to undertake these programs.

The Company’s ability to maintain compliance with operational covenants as defined among the Company and its lenders

The Company is required to meet or exceed certain financial covenants as defined by the 2008 Amended Credit Agreement. As the Company’s revenue and net income are subject to general economic conditions as described above, there may be risks in meeting or exceeding these covenants. The potential risks of not meeting these covenants could include the inability to borrow under the 2008 Amended Credit Agreement, the requirement to repay outstanding borrowings under the 2008 Credit Agreement, a charge from the lenders to amend the 2008 Amended Credit Agreement or to waive the non-compliance, and increased interest costs, certain of which would have a material adverse effect on the Company.

15

Table of Contents

The impact of the recently enacted Dodd-Frank Wall Street Reform and Consumer Protection Act

On July 21, 2010, The Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Financial Reform Act”) was signed into law. The Financial Reform Act includes regulations intended to enhance SEC enforcement authority and provides for additional corporate governance requirements. New regulations associated with the Financial Reform Act may have impacts upon legal entity structures and business lines, corporate governance and organization, operations and IT systems, risk management and internal control frameworks, tax planning, regulatory and public disclosures and legal and compliance demands. We cannot predict what, if any, further initiatives may be required in future periods that impact the scope of this Financial Reform Act. The Company’s efforts to maintain compliance within the scope of the requirements provided by the Financial Reform Act may impact the Company’s business and financial condition.

The impact of the litigation with the U.S. Department of Justice concerning alleged violations of the Americans with Disabilities Act of 1990 on our results of operations or cash flows in future periods

The United States Department of Justice (Disability Rights Section of the Civil Rights Division) (“DOJ”) filed a lawsuit on April 29, 2009 in the U.S. District Court for the Eastern District of Pennsylvania against the Company alleging that the Company violated Title III of the Americans with Disabilities Act of 1990 (“ADA”) by excluding children with disabilities from its schools and programs. The complaint seeks an unspecified amount in compensatory damages and civil penalties, as well as declaratory and injunctive relief.

The Company is committed to complying with and believes it has complied with the ADA in providing access to children with disabilities. The Company believes that the DOJ’s allegations are without merit, and intends to defend against these allegations vigorously.

The Company is not able at this time to estimate the range of loss, if any, arising out this matter since its outcome is uncertain. Although it does not expect that the resolution of the matter will have a material adverse effect on its financial condition, results of operations or cash flows, there can be no assurances in this regard.

Environmental or health related events that could affect schools in areas impacted by such events

We are not aware of any existing environmental conditions that currently or in the future could reasonably be expected to have a material adverse effect on our financial position, operating results or cash flows and we have not incurred material expenditures to address environmental conditions at any school. Although we have periodically conducted limited environmental investigations and remedial activities at some of our schools, we have not undertaken an in-depth environmental review of all of our schools and accordingly, there may be material environmental liabilities of which we are unaware. In addition, no assurances can be given that future laws or regulations will not impose any material environmental liability.

A regional or global health pandemic could severely disrupt our business. A health pandemic is a disease that spreads rapidly and widely by infection and affects many individuals in an area or population at the same time. If a regional or global health pandemic were to occur, depending upon its severity and duration, the Company’s business could be severely affected. Enrollment in our schools could experience sharp declines as parents might avoid taking their children out in public in the event of a health pandemic, and local, regional or national governments might limit or ban public interactions to halt or delay the spread of disease causing business disruptions and the temporary closure of our schools. A health pandemic could impair our ability to hire and retain an adequate level of staff. The impact of a health pandemic on the Company might be disproportionately greater than on other companies that depend less on the interaction of people for the sale of their products and services.

Our financial and operating performance may be adversely affected by acts of God, such as natural disasters, in locations where we own and/or lease school properties. Some types of losses, such as those from earthquakes, hurricanes, terrorism and environmental hazards may be either uninsurable or too expensive to

16

Table of Contents

justify insuring against. Should an uninsured loss or a loss in excess of insured limits occur, we could lose all or a portion of the capital we have invested in a property, as well as the anticipated future revenue from the school. In that event, we might nevertheless remain obligated for any lease obligations, mortgage debt or other financial obligations related to the property. In addition, the degree of preparedness, contingency planning or recovery capability in relation to a major incident or crisis may hinder operational continuity and consequently impact the value and reputation of our business.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS. |

None.

| ITEM 2. | PROPERTIES. |

At September 15, 2010, we operated 184 schools on 5 owned and 179 leased properties in 15 states and the District of Columbia. Our schools are geographically distributed as follows:

| Location |

Number of Schools | |

| Arizona |

1 | |

| California |

38 | |

| District of Columbia |

1 | |

| Florida |

8 | |

| Illinois |

20 | |

| Maryland |

1 | |

| Nevada |

9 | |

| New Jersey |

10 | |

| North Carolina |

17 | |

| Oregon |

3 | |

| Ohio |

9 | |

| Pennsylvania |

23 | |

| South Carolina |

2 | |

| Texas |

17 | |

| Virginia |

19 | |

| Washington |

6 | |

| Total |

184 | |

In addition to the school locations listed above, Laurel Springs School, our online K-12 School, leases one property in California and one property in Oregon. We lease 22,500 square feet of space for our corporate offices in West Chester, Pennsylvania. This space is adequate for our current needs.

The land and buildings that we own are subject to security interests on the real property. Our leased properties are leased under long-term leases which are typically triple-net leases requiring us to pay all applicable real estate taxes, utility expenses, insurance and operating costs. These leases usually contain inflation indexed rent escalators.

| ITEM 3. | LEGAL PROCEEDINGS. |

The DOJ filed a lawsuit on April 29, 2009 in the U.S. District Court for the Eastern District of Pennsylvania against the Company alleging that the Company violated Title III of the ADA by excluding children with disabilities from its schools and programs. The complaint seeks an unspecified amount in compensatory damages and civil penalties, as well as declaratory and injunctive relief.

17

Table of Contents

The Company is committed to complying with and believes it has complied with the ADA in providing access to children with disabilities. The Company believes that the DOJ’s allegations are without merit, and intends to defend against these allegations vigorously.

The Company is not able at this time to estimate the range of loss, if any, arising out of this matter since its outcome is uncertain. Although it does not expect that the resolution of the matter will have a material adverse effect on its financial condition, results of operations or cash flows, there can be no assurances in this regard.

| ITEM 4. | REMOVED AND RESERVED. |

None.

18

Table of Contents

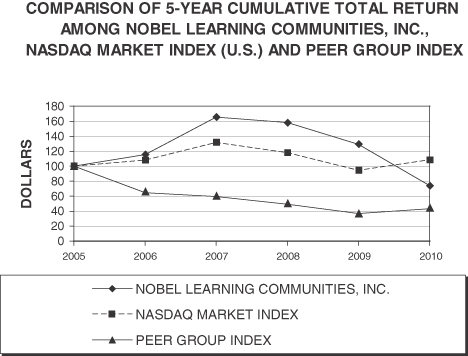

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY |

Market Information

Our common stock trades on The Nasdaq Global Market under the symbol NLCI.

The table below sets forth the quarterly high and low closing sales prices for our common stock as reported by Nasdaq for each quarter during the period from June 28, 2008 through July 3, 2010.

| High | Low | |||||

| Fiscal 2009 (June 29, 2008 to June 27, 2009) |

||||||

| First Quarter |

$ | 16.00 | $ | 12.17 | ||

| Second Quarter |

15.76 | 12.55 | ||||

| Third Quarter |

13.86 | 11.37 | ||||

| Fourth Quarter |

12.50 | 10.73 | ||||

| Fiscal 2010 (June 28, 2009 to July 3, 2010) |

||||||

| First Quarter |

$ | 12.11 | $ | 9.51 | ||

| Second Quarter |