Attached files

| file | filename |

|---|---|

| EX-31.1 - MAM SOFTWARE GROUP, INC. | v196812_ex31-1.htm |

| EX-31.2 - MAM SOFTWARE GROUP, INC. | v196812_ex31-2.htm |

| EX-32.2 - MAM SOFTWARE GROUP, INC. | v196812_ex32-2.htm |

| EX-32.1 - MAM SOFTWARE GROUP, INC. | v196812_ex32-1.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

DC 20549

FORM

10-K

|

þ

|

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

|

||

|

SECURITIES

EXCHANGE ACT OF 1934

|

|||

|

FOR

THE FISCAL YEAR ENDED JUNE 30, 2010

|

|||

|

o

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

|

||

|

SECURITIES

EXCHANGE ACT OF 1934

|

FOR THE

TRANSITION PERIOD FROM ___________ TO ___________

Commission

file number 000-27083

MAM

Software Group, Inc.

(Exact

name of registrant as specified in its charter)

|

Delaware

|

84-1108035

|

|

|

(State

or other jurisdiction of incorporation or

organization)

|

(I.R.S.

Employer Identification No.)

|

Maple

Park, Maple Court, Tankersley, Barnsley, UK S75 3DP

(Address

of principal executive offices, including zip code)

Registrant’s

telephone number, including area code: 011-44-124-431-1794

Aftersoft

Group, Inc.

(Former

name, change since last report)

Securities

registered pursuant to Section 12(b) of the Act:

|

Title

of each class:

|

Name

of each exchange on which registered:

|

|

|

None

|

None

|

Securities

registered pursuant to Section 12(g) of the Act:

Common

Stock, $0.0001 par value

(Title of

class)

Indicate

by check mark if the registrant is a well-known seasoned issuer (as defined in

Rule 405 of the Act). Yes ¨ No þ

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act.Yes ¨ No þ

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter periods that the registrant was

required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days.

Yes þ No ¨

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files). Yes ¨ No

¨

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III or this Form 10-K or any amendment to this

Form 10-K. þ

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer or a smaller reporting company. See

the definitions of “large accelerated filer,” “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

¨

|

Accelerated

filer ¨

|

|

Non-accelerated

filer ¨

|

Smaller

reporting company þ

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Act).Yes ¨ No þ

As of

December 31, 2009 approximately 83,773,264 shares of common stock were

outstanding. The aggregate market value of the common stock held by

non-affiliates of the registrant, as of December 31, 2009, the last business day

of the 2 nd

fiscal quarter, was approximately $3,604,179 based on the

average high and low price of $0.06 for the registrant’s common stock as quoted

on the Over-the-Counter Bulletin Board on that date. Shares of common stock held

by each director, each officer and each person who owns 10% or more of the

outstanding common stock have been excluded from this calculation in that such

persons may be deemed to be affiliates. The determination of affiliate status is

not necessarily conclusive.

The

registrant had 85,860,185 shares of its common stock outstanding as of August

31, 2010.

DOCUMENTS

INCORPORATED BY REFERENCE

None

TABLE

OF CONTENTS

|

Page

|

||

|

PART

I

|

1

|

|

|

Item

1.

|

Business

|

1

|

|

Item 1A.

|

Risk

Factors

|

16

|

|

Item 1B.

|

Unresolved

Staff Comments

|

26

|

|

Item

2.

|

Properties

|

26

|

|

Item

3.

|

Legal

Proceedings

|

27

|

|

Item

4.

|

Submission

of Matters to a Vote of Security Holders

|

29

|

|

PART

II

|

30

|

|

|

Item

5.

|

Market

for Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities

|

30

|

|

Item

6.

|

Selected

Financial Data

|

32

|

|

Item

7.

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

32

|

|

Item

7A.

|

Quantitative

and Qualitative Disclosures about Market Risk.

|

56

|

|

Item

8.

|

Financial

Statements and Supplementary Data

|

56

|

|

Item

9.

|

Changes

in and Disagreements with Accountants on Accounting and Financial

Disclosure

|

56

|

|

Item 9A(T).

|

Controls

and Procedures

|

56

|

|

Item 9B.

|

Other

Information

|

57

|

|

PART

III

|

58

|

|

|

Item

10.

|

Directors,

Executive Officers and Corporate Governance

|

58

|

|

Item

11.

|

Executive

Compensation

|

62

|

|

Item

12.

|

Security

Ownership Of Certain Beneficial Owners And Management and Related

Stockholder Matters

|

79

|

|

Item

13.

|

Certain

Relationships and Related Transactions, and Director

Independence

|

83

|

|

Item

14.

|

Principal

Accounting Fees and Services

|

90

|

|

PART

IV

|

91

|

|

|

Item

15.

|

Exhibits,

Financial Statement Schedules

|

91

|

|

SIGNATURES

|

||

|

INDEX

TO EXHIBITS

|

|

|

i

PART

I

|

Item

1.

|

Business

|

Unless

the context indicates or requires otherwise, (i) the term “MAM” refers to MAM

Software Group, Inc. and its principal operating subsidiaries; (ii) the term

“MAM Software” refers to MAM Software Limited and its operating subsidiaries;

(iii) the term “ASNA” refers to Aftersoft Network N.A., Inc. and its operating

subsidiaries;(iv) the term “EXP” refers to EXP Dealer Software Limited and its

operating subsidiaries; and (v) the terms “we,” “our,” “ours,” “us” and the

“Company” refer collectively to MAM Software Group, Inc.

Our

Company

MAM

Software Group, Inc. provides software, information and related services to

businesses engaged in the automotive aftermarket in the US, Canada, UK and

Ireland. The automotive aftermarket consists of businesses associated with the

life cycle of a motor vehicle from when the original manufacturer’s warranty

expires to when the vehicle is scrapped. Products sold by businesses engaged in

this market include the parts, tires and auto services required to maintain and

improve the performance or appeal of a vehicle throughout its useful life. The

Company aims to meet the business needs of customers who are involved in the

maintenance and repair of automobiles and light trucks in three key segments of

the automotive aftermarket, namely parts, tires and auto service.

The

Company’s business management systems, information products and online services

permit our customers to manage their critical day-to-day business operations

through automated point-of-sale, information (content) products, inventory

management, purchasing, general accounting and customer relationship

management.

The

Company’s customer base consists of wholesale parts and tire distributors,

retailers, franchisees, cooperatives, auto service chains and single location

auto service businesses with high customer service expectations and complex

commercial relationships.

The

Company’s revenues are derived from the following:

|

|

·

|

The

sale of business management systems comprised of proprietary software

applications, implementation and training;

and

|

|

|

·

|

Providing

subscription-based services, including software support and maintenance,

information (content) products and online services for a

fee.

|

1

CORPORATE

BACKGROUND

The

Company’s principal executive office is located at Maple Park, Maple Court,

Tankersley, Barnsley, UK S75 3DP and its phone number is

011-44-124-431-1794

In

December 2005, W3 Group, Inc. (“W3”) consummated a reverse acquisition and

changed its corporate name to Aftersoft Group, Inc. W3, which was initially

incorporated in February 1988 in Colorado, changed its state of incorporation to

Delaware in May 2003. On December 21, 2005, an Acquisition Agreement (the

“Agreement”) was consummated among W3, a separate Delaware corporation named

Aftersoft Group, Inc. (“Oldco”) and Auto Data Network, Inc. (“ADNW”) in which W3

acquired all of the issued and outstanding shares of Oldco in exchange for

issuing 32,500,000 shares of Common Stock of W3, par value $0.0001 per share, to

ADNW, which was then the sole shareholder of the Company. At the time of the

acquisition, W3 had no business operations. Concurrent with the acquisition, W3

changed its name to Aftersoft Group, Inc. and its corporate officers were

replaced. The Board of Directors of the Company appointed three additional

directors designated by ADNW to serve until the next annual election of

directors. As a result of the acquisition, the former W3 shareholders owned

1,601,167, or 4.7% of the 34,101,167 total issued and outstanding shares of

Common Stock and ADNW owned 32,500,000 or 95.3% of the Company’s Common Stock.

On December 22, 2005, Oldco changed its name to Aftersoft Software, Inc. and is

currently inactive. On April 21, 2010 shareholders approved the change of the

Company’s name to MAM Software Group Inc.

On August

26, 2006, the Company acquired 100% of the issued and outstanding shares of EXP

from ADNW in exchange for issuing 28,000,000 shares of Common Stock to ADNW with

a market value of $30,800,000. On February 1, 2007, the Company consummated an

agreement to acquire Dealer Software and Services Limited (“DSS”), a subsidiary

of EXP, in exchange for issuing 16,750,000 shares of Common Stock to ADNW with a

market value of $15,075,000.

During

2007, the Company conducted a strategic assessment of its businesses and

determined that neither EXP nor DSS fit within its long-term business model. The

Company identified a buyer for the two businesses in First London PLC (formerly

First London Securities PLC) (“First London”). First London is a UK-based

holding company for a group of businesses engaged in asset management,

investment banking, and merchant banking. First London’s shares were listed for

trading on the London Plus market, but trading is currently suspended. First

London’s areas of specialization include technology, healthcare, and resources,

and its merchant banking operations take strategic, principal positions in

businesses that fall within its areas of specialization.

2

On June

17, 2007, DSS sold all of the shares of Consolidated Software Capital Limited

(“CSC”), its wholly owned subsidiary, to RLI Limited, a company affiliated with

First London (“RLI”). The consideration for this sale consisted of a note from

RLI with a face value of $865,000. On November 12, 2007, as part of the sale of

EXP (see below), the $865,000 note was exchanged for 578,672 shares of First

London common stock having a fair value of $682,000. The transaction resulted in

a loss of $183,000 to the Company.

The

Company sold its interest in EXP and DSS, EXP’s wholly owned subsidiary, on

November 12, 2007. Pursuant to the terms of a Share Sale Agreement (the “EXP

Agreement”), EU Web Services Limited (“EU Web Services”) a subsidiary of First

London, agreed to acquire, and the Company agreed to sell, the entire issued

share capital of EXP it then owned, which amounted to 100% of EXP’s outstanding

stock.

As

consideration for the sale of EXP, including DSS, EU Web Services agreed to

issue to the Company, within 28 days of the closing, 1,980,198 Ordinary shares

(the UK equivalent of common stock), £0.01 par value, in its parent company,

First London. The Ordinary shares received by the Company had an agreed upon

fair market value of $3,000,000 at the date of issuance of such shares. The

Company recorded the shares received at $2,334,000, which represents the bid

price of the restricted securities received, and discounted the carrying value

by 11% (or $280,000) as, pursuant to the EXP Agreement, the shares could not be

sold by the Company for at least 12 months. Further, the EXP Agreement provided

that the Company receive on May 12, 2008 additional consideration in the form

of: (i) Ordinary shares in EU Web Services having a fair market value of

$2,000,000 as of the date of issuance, provided that EU Web Services is listed

and becomes quoted on a recognized trading market within six (6) months from the

date of the Agreement; or (ii) if EU Web Services does not become listed within

the time period specified, Ordinary shares in First London having a fair market

value of $2,000,000 as of May 12, 2008. As EU Web Services did not become listed

within the six-month timeframe, the Company received on August 14, 2008

1,874,414 shares in First London, which had a fair market value of $2,000,000 on

May 12, 2008.

MAM is a

former subsidiary of ADNW, a publicly traded company, the stock of which is

currently traded on the pink sheets under the symbol ADNW.PK. ADNW transferred

its software aftermarket services operating businesses to MAM and retained its

database technology, Orbit. Orbit is a system for supply and collection of data

throughout the automotive industry. To date, Orbit is still in its development

phase, and ADNW will require substantial external funding to bring the

technology to its first phase of testing and deployment.

3

On

November 24, 2008, ADNW distributed a dividend of the 71,250,000 shares of MAM

common stock that ADNW owned at such time in order to complete the

previously announced spin-off of MAM’s businesses. The dividend shares were

distributed in the form of a pro rata dividend to the holders of record as of

November 17, 2008 (the “Record Date”) of ADNW’s common and convertible preferred

stock. Each holder of record of shares of ADNW common and preferred stock as of

the close of business on the Record Date was entitled to receive 0.6864782

shares of MAM’s common stock for each share of common stock of ADNW held at such

time, and/or for each share of ADNW common stock that such holder would own,

assuming the convertible preferred stock owned on the Record Date was converted

in full. Prior to the spin-off, ADNW owned approximately 77% of MAM’s

issued and outstanding common stock. Subsequent to and as a result of the

spin-off, MAM is no longer a subsidiary of ADNW.

The

Company currently has the following wholly owned direct operating subsidiaries:

MAM Software in the UK, and ASNA in the US.

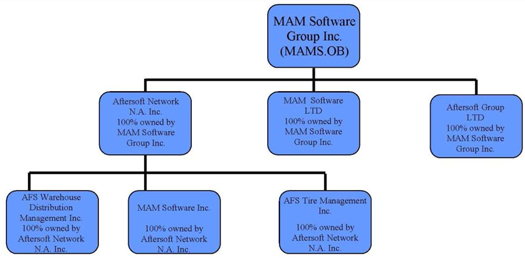

MAM

Software Group, Inc. Organization Chart

4

MAM

Software Ltd.

MAM

Software is a provider of software to the automotive aftermarket in the UK and

Ireland. MAM Software specializes in providing reliable and competitive business

management solutions to the motor factor (also known as jobber), retailing, and

wholesale distribution sectors. It also develops applications for vehicle repair

management and provides solutions to the retail and wholesale tire industry. All

MAM Software programs are based on the Microsoft Windows family of operating

systems. Each program is fully compatible with the other applications in their

range, enabling them to be combined to create a fully integrated package. MAM

Software is based in Tankersley, UK.

Aftersoft

Network N.A., Inc. (ASNA)

ASNA

develops open business management systems, and distribution channel e-commerce

systems for the automotive aftermarket supply chain. These systems are used by

leading aftermarket outlets, including tier one manufacturers, program groups,

warehouse distributors, tire and service chains and independent installers. ASNA

products and services enable companies to generate new sales, operate more cost

efficiently, accelerate inventory turns and maintain stronger relationships with

suppliers and customers. ASNA has three wholly owned subsidiaries operating

separate businesses: (i) AFS Warehouse Distribution Management, Inc. and (ii)

AFS Tire Management, Inc. which are both based in Dana Point, California, and

(iii) MAM Software, Inc., which is based in Allentown,

Pennsylvania.

ASNA

specifically focuses on selling systems to the service and tire segment of the

market, while MAM Software, Inc. focuses on the warehouse and jobber segment of

the market.

Industry

Overview

The

Company serves the business needs of customers involved in the supply of parts,

maintenance and repair of automobiles and light trucks in three key segments of

the automotive aftermarket, namely parts, tires and auto service.

The

industry is presently experiencing a level of consolidation in the lines that

are being sold. The previous distinction of having parts and tires provided by

two distinct suppliers is coming to an end, as our customers’ businesses need to

offer their clients the widest range of products and services under one roof. As

a result, what were previously parts-only stores, jobbers and warehouses, are

now taking in tire inventory as well in order to satisfy their clients’ demands,

and vice-versa. This in turn is causing owners of these businesses to evaluate

their business systems to ensure they can compete over the short, medium and

long term. An increase in the “do-it-yourself” market due to “credit crunch” is

requiring these systems, but at the same time a

need to compete strongly with other parts stores is cutting

margins as businesses attempt to attract new and return business. Longer

warranties are still deferring the length of time until newer vehicles are

entering the aftermarket, except for running spares and service parts, accident

damage, and optional add-ons such as security, entertainment, performance and

customization.

5

Continuing

market conditions related to the overall downturn in the consumer market is also

directly affecting the confidence and ability of businesses to invest in new

systems. The industry’s response to this has been to introduce incentive and

discount programs, but to date it is uncertain whether this approach will be

successful long term.

The

Company believes that growth in the automotive aftermarket will continue to be

driven by the following factors:

|

|

·

|

gradual

growth in the aggregate number of vehicles in

use;

|

|

|

·

|

an

increase in the average age of vehicles in

operation;

|

|

|

·

|

fewer

new vehicles being purchased due to uncertainty in the economy, especially

available credit;

|

|

|

·

|

the

total number of miles driven per vehicle per year;

and

|

|

|

·

|

increased

vehicle complexity.

|

Products

and Services

Meeting

the needs of the automotive aftermarket requires a combination of business

management systems, information products and online services that combine to

deliver benefits for all parties involved in the timely repair of a vehicle. The

Company provides systems and services that meet these needs and help its

customers to meet their customers’ expectations. These products and services

include:

|

|

1.

|

Business

Management Systems comprised of the Company’s proprietary software

applications, implementation and training and third-party hardware and

peripherals;

|

|

|

2.

|

Information

Products such as an accessible catalog database related to parts,

tires, labor estimates, scheduled maintenance, repair information,

technical service bulletins, pricing and product features and benefits

that are used by the different participants in the automotive

aftermarket;

|

6

|

|

3.

|

Online

Services and products that provide online connectivity between

manufacturers, warehouse distributors, retailers and automotive service

providers. These products enable electronic data interchange throughout

the automotive aftermarket supply chain between the different trading

partners. They also enable procurement and business services to be

projected over the internet to an expanded business audience;

and

|

|

|

4.

|

Customer

Support, Consulting and Training that provide phone and online

support, implementation and

training.

|

Business

Management Systems

MAM’s

business management systems meet the needs of warehouse distributors, part

stores and automotive service providers as follows:

Warehouse

Distributors

DirectStep . This

product is designed for and targeted at warehouse distributors that seek to

manage multiple locations and inventories on a single system. ASNA through its

subsidiary, MAM Software, Inc., provides distributors a complete business

management system for inventory management, customer maintenance, accounting,

purchasing and business analytics. The products enable online trading and

services (through ASNA’s OpenWebs product) including price and product

information updating integrated with Autopart and VAST products, which are used

by parts stores and automotive service providers.

Autopart . This is a

UK-developed product that is sold and promoted in the US by MAM Software, Inc.

This product is designed for and targeted at warehouse distributors that seek to

manage multiple locations and inventories on a single system for a regional area

and are also suited to managing single location franchisees or buying group

members. The product provides point of sale, inventory management, electronic

purchasing capabilities and a fully integrated accounting module. It also allows

the parts stores to connect with automotive service providers through our

Openwebs online services product.

Parts

Stores

Autopart . This is a

UK-developed product that is sold and promoted in the US by MAM Software, Inc.

In addition to warehouse distributors, this product is designed for and targeted

at parts store chains that seek to manage multiple locations and inventories on

a single system for a regional area and are also suited to managing single

location franchisees or buying group members. The product provides point of

sale, inventory management, electronic purchasing capabilities and a fully

integrated accounting module. It also allows the parts stores to connect with

automotive service providers through our Openwebs online services

product.

7

Automotive

Service Providers

VAST . This product

is designed for and targeted at large- to medium- sized automotive service and

tire chains that seek to manage multiple locations and inventories for a

regional area is also suited to managing single location stores that are part of

a franchise or a buying group. VAST provides point-of-sale, inventory

management, electronic purchasing and customer relationship management

capabilities. It also allows the service provider to connect with parts and

tires warehouse distributors and parts stores through either ASNA’s online

services and products or other industry connectivity solutions.

Autowork . This is a

UK-developed product that is sold by MAM Software Ltd. This product is designed

for and targeted at small single store automotive installers. The Autowork

product provides estimate, job card, parts procurement and invoice capabilities.

It also allows the automotive installer to connect with parts distributors

through the Company’s online services and products. This product has recently

been made available over the internet as a Software as a Service product (SaaS),

allowing customers to purchase the solution on a monthly basis but without the

need to manage the system. It has been launched under the name of Autowork

Online.

Autopart . This is a

UK-developed product that is sold in both the US and UK. In the US it is sold by

MAM Software, Inc. and in the UK by MAM Software Ltd. This product is designed

for and targeted at parts store chains that seek to manage multiple locations

and inventories on a single system for a regional area. It is also suited to

managing single location franchisees or buying group members. The product

provides point of sale, inventory management, electronic purchasing capabilities

and a fully integrated accounting module. An Autopart PDA module is also

available to allow field sales personnel to record sales activity in real time

on handheld devices while on the road. The PDA module also allows the sales

representative to maintain their stock and synchronize in real time while

traveling, or later, locally, with Autopart directly. It also allows parts

stores to connect with automotive service providers through the ASNA online

services, OpenWebs.

Information

Products

The

Company provides product catalog and vehicle repair information required to

enable point-of-sale transactions. These proprietary database products and

services generate recurring revenues through monthly or annual subscription

fees.

8

MAM

Software Ltd. develops and maintains proprietary information products that

differentiate its products from those of the majority of its competitors in the

UK. In the US and Canada, ASNA develops and maintains a proprietary workflow

capability that integrates information products sourced from its suppliers such

as Activant, WHI and NAPA to its automotive parts and tire customers, including

warehouse distributors, parts stores and automotive service

providers.

MAM

Software Ltd.’s principal information service is AutoCat, which is distributed

either via CDs in the form of AutoCat or via the internet as AutoCat+. Both

forms of Autocat provide access to a database of over 18

million automobile vehicle applications for the UK market.

Business systems software used by the warehouse distributor, parts store and

auto service provider enable the user to access information about parts quickly

and accurately. MAM Software Ltd. charges a monthly or annual subscription fee

for its information products. Customers are provided updates via periodic CDs in

the case of AutoCat or daily via the internet for AutoCat+. In the UK, there are

approximately 8,000 end-users who use our information products.

In

addition, information products developed or resold by ASNA include Interchange

Catalog, a database that provides cross references of original equipment

manufacturer part numbers to aftermarket manufacturer part numbers; Price

Updating, a service that provides electronic price updates following a price

change by the part manufacturer; Labor Guide, a database used by automotive

service providers to estimate labor hours for purposes of providing written

estimates of repair costs to customers; Scheduled Service Intervals, a database

of maintenance intervals; and Tire Sizing, a database that cross-references

various tire products and applications.

Online

Services

Both ASNA

and MAM Software Ltd. offer online e-commerce services in the form of

system-to-system and web browser implementations. These online services connect

the automotive aftermarket from manufacturers through warehouse distributors and

parts stores to automotive service providers for the purpose of purchasing parts

and tires, fleet and national account transaction processing and online product

price information.

OpenWebs(TM)

e-Commerce Gateway Services

In the US

and Canada, ASNA’s e-commerce gateway services use automotive industry standard

messaging specifications to deliver online services that connect the automotive

aftermarket supply chain for the purpose of purchasing parts and tires, fleet

and national account transaction processing, online product and price updating

for parts and tires.

9

OpenWebs(TM)

e-Commerce Browser Services

In the US

and Canada, ASNA’s e-commerce browser services enable warehouse distributors and

parts stores to provide an online service to automotive service providers for

the purpose of purchasing of parts and tires, accessing account information and

other browser-based channel management services.

Autonet

In the

UK, MAM Software Ltd.’s Autonet online services connect manufacturers, warehouse

distributors, parts stores and automotive service providers for the purpose of

purchasing of parts and tires, fleet and national account transaction processing

and product information and price distribution.

AutoCat+

MAM

Software Ltd.’s UK product information database is available for access and

distribution as a Web-driven service called AutoCat+ in which the database and

access software have been enhanced to enable service professionals to look up

automotive products for themselves, view diagrams and select the parts for their

vehicle. This enhanced version of the AutoCat product is used by parts stores

and the professional installer segments of the automotive parts aftermarket in

the UK.

Customer

Support and Consulting and Training

The

Company provides support, consulting and training to its customers to ensure the

successful use of its products and services. The Company believes this extra

level of commitment and service builds customer relationships, enhances customer

satisfaction and maximizes customer retention. These services consist of the

following:

|

|

·

|

Phone

and online support. Customers can call dedicated support lines to speak

with knowledgeable personnel who provide support and perform on-line

problem solving as required.

|

|

|

·

|

Implementation,

education and training consulting. Our consulting and training teams work

together to minimize the disruption to a customer’s business during the

implementation process of a new system and to maximize the customer’s

benefit from the use of the system through

training.

|

ASNA and

MAM Software Ltd. also provide a customer-only section on their intranet sites

that allows customers direct access to newsgroups, on-line documentation and

information related to products and services. New customers enter into support

agreements, and most retain such service agreements for as long as they own the

system. Monthly fees vary with the number of locations and the software modules,

information products and online services subscribed to. The agreements are

generally month-to-month agreements. The Company offers training at both ASNA

and MAM Software Ltd.’s facilities, the customer’s facilities and online for

product updates or introduce specific new capabilities.

10

MAM

Software Ltd.’s UK catalog information product and other information services

are delivered by its AutoCat team, based in Wareham, England. The AutoCat

product team sources, standardizes and formats data collected in an electronic

format from over 130 automotive parts manufacturers. MAM Software Ltd. provides

this data to its customers in either compact discs for the AutoCat product or

via the internet for the AutoCat+ product.

Distribution

There are

two primary vertical distribution channels for aftermarket parts and tire

distribution: the traditional wholesale channel and the retail

channel.

Automotive

Aftermarket Distribution Channels

|

|

·

|

Traditional Wholesale

Channel . The wholesale channel is the predominant distribution

channel in the automotive aftermarket. It is characterized by the

distribution of parts from the manufacturer to a warehouse distributor, to

parts stores and then to automotive service providers. Warehouse

distributors sell to automotive service providers through parts stores,

which are positioned geographically near the automotive service providers

they serve. This distribution method provides for the rapid distribution

of parts. The Company has products and services that meet the needs of the

warehouse distributors, parts stores and the automotive service

providers.

|

|

|

·

|

Retail Channel

. The retail channel is comprised of large specialty retailers,

small independent parts stores and regional chains that sell to

“do-it-yourself” customers. Larger specialty retailers, such as Advance

Discount Auto Parts, AutoZone, Inc., O’Reilly Automotive, Inc. and CSK

Auto Corporation carry a greater number of parts and accessories at more

attractive prices than smaller retail outlets and are gaining market

share. The business management systems used in this channel are either

custom developed by the large specialty retailers or purchased from

business systems providers by small to medium-sized businesses. The

Company has products and services that support the retail

channel.

|

In

addition to these two primary channels, some aftermarket parts and tires end up

being distributed to new car dealers. The business management systems used in

this channel have unique functionality specific to new car dealerships. The

Company sells a small number of products into the auto service provider side of

car dealerships. Aftermarket wholesalers of parts and tires provide online

purchasing capabilities to some new car dealerships.

11

Product

Development

The

Company’s goal is to add value to its customers’ businesses through products and

services designed to create optimal efficiency. To accomplish this goal, the

Company’s product development strategy consists of the following three key

components:

|

|

·

|

Integrating

all of the Company’s products so that its software solutions work together

seamlessly, thereby eliminating the need to switch between

applications;

|

|

|

·

|

Enhancing

the Company’s current products and services to support its changing

customers needs; and

|

|

|

·

|

Providing

a migration path to the Company’s business management systems, reducing a

fear that many customers have that changing systems will disrupt

business.

|

Sales

and Marketing

The

Company’s sales and marketing strategy is to acquire customers and retain them

by cross-selling and up-selling a range of commercially compelling business

management systems, information products and online services.

Within

the parts, tire and auto service provider segments, each division sells and

markets through a combination of field sales, inside sales, and independent

representatives. The Company seeks to partner with large customers or buying

groups and leverage their relationships with their customers or members.

Incentive pay is a significant portion of the total compensation package for all

sales representatives and sales managers. Outside sales representatives focus

primarily on identifying and selling to new customers complemented by an inside

sales focus on selling upgrades and new software applications to its installed

customer base.

The

Company’s marketing approach aims to leverage its reputation for customer

satisfaction and for delivering systems, information and services that improve a

customer’s commercial results. The goal of these initiatives is to maximize

customer retention and recurring revenues, to enhance the productivity of the

field sales team, and to create the cross-selling and up-selling opportunities

for its systems, information products and online services.

12

Research

and Development

The

Company spent approximately $3.0 million in fiscal 2010 on research and

development, with approximately $0.9 million spent by ASNA, $0.3 million by MAM

Software, Inc., and $1.8 million by MAM Software Ltd. The Company spent

approximately $2.9 million in fiscal 2009 on research and development, with

approximately $1.2 million spent by ASNA, $0.4 million by MAM Software, Inc.,

and $1.3 million by MAM Software Ltd.

Patent

and Trademark

MAM

Software holds a UK trademark for its Autonet product. The trademark is a

graphical device that is made up of text saying “Autonet Tailored Internet

Solutions for the Automotive Industry”. It was filed for registration December

8, 2001 and registration was granted August 9, 2002 under ADP number 0812875001

and is due for renewal December 8, 2011.

Customers

During

the year ended June 30, 2010 one customer accounted for 10.1% of the Company’s

total revenues. During the year ended June 30, 2009 no single customer

accounted for more than 10% of the Company’s total revenues. The Company’s top

ten customers collectively accounted for 18% of total revenues during each of

fiscal 2010 and 2009. Some of ASNA’s top customers in North America include

Autopart International, AutoZone, Monro Muffler Brake, Fountain Tire and US

AutoForce. In the UK and Irish markets, MAM Software’s top customers include

Unipart Automotive, Dingbro Ltd, Allparts Automotive and General Traffic

Service.

Competition

In the US

and Canada, ASNA competes primarily with Activant, Inc. and several smaller

software companies, including Autologue, Maddenco, Janco, ASA, Signal Software

and WHI, Inc. (formerly known as Wrenchead Inc.) that provide similar products

and services to the US automotive aftermarket. Additionally, an ongoing

competitive threat to the Company is custom developed in-house systems,

information products and online services. For example, AutoZone, Inc. and

Genuine Parts Company’s NAPA Parts Group both developed their own business

management systems and electronic automotive parts catalogs for their stores and

members, although the Company currently has a partnership agreement with each of

these companies to supply their information products through the Company’s

solutions.

13

In the US

and Canada, the Company expects to compete successfully against its competitors

using two separate and complimentary strategies. First, the Company will

continue to focus on selling and promoting the Company’s complete supply chain

solutions that provide businesses with easy integration of the Company’s

business management information systems into their existing supply chain

structures. Second, the Company will continue its strategy of working with those

businesses that already manage their own supply chains and information products

(catalogs), such as buying groups like NAPA, helping to improve and compliment

their systems with the Company’s products.

ASNA, in

the US and Canada, competes with multiple products across different market

segments, so its competitors vary by segment.

Within

the warehouse distribution segment, the Company will continue to support its

legacy system, Direct Step, a product which the Company developed many years ago

which enables large warehouses with millions of parts to locate, manage, pack

and deliver the parts with ease and efficiency. Direct Step is not a Microsoft

Windows-based technology. The Company’s existing and prospective customers are

moving towards modern solutions which integrate easily with Internet-based

transactions and interactions, and the Company believes that its AutoPart

product provides that solution. The Company has been selling AutoPart

successfully in the UK and Ireland since 2000, and feels that the success this

product in the UK and the successful installation of this product within the US

will enable the Company to promote and benefit quickly from this

product.

The tire

segment is comprised of three distinct elements: retail, wholesale and

commercial. Within the tire segment and the auto service segment, the Company

focuses on client and market requirements, which the Company believes will

enable it to offer its clients the best solution, regardless of the size of a

client’s business. By continually integrating and extending the functionality of

its solutions across the entire supply chain, the Company believes that it will

be able to offer existing and potential clients products that suit their present

and future needs. Management believes that its products will present existing

and potential clients the opportunity to move away from their older existing

systems, which may restrict their market opportunities, and will permit

integration into additional sales channels and reduce the costly maintenance of

older systems.

The auto

parts segment within the auto service space has many competitors who have

developed applications for single location auto service shops. Many of these

have been developed by parts distributors like NAPA and AutoZone. While these

applications do well in a small single location store, they are not widely

distributed in the multi-store location segment of the auto parts business. The

Company’s goal is not to pursue single store locations. Rather, it will focus on

multi-store locations for which its product VAST is highly suited. The Company

believes that this multi-store ability offers strong opportunities to beat the

competition in this area and quickly increase the Company’s customer

base.

14

The last

area that the Company plans to compete in is the e-commerce space, providing new

tools and solutions for this expanding

Internet marketplace. The goal of the

Company’s OpenWebs product is to connect both parts and tire partners together

in a real-time environment so they can perform electronic ordering, gauge

inventory levels as well as disseminate information. Within the tire segment,

the Company feels that it has a competitive advantage. The Company’s observation

has led it to believe that most tire distributors either do not have a

business-to-business solution or have developed solutions from independent

sources. While the parts segment of this market is largely tied to Activant, Inc

at this time, the Company believes that customers are looking for solutions that

simply integrate their supply chain, completely and without further

restrictions. The Company’s OpenWebs solution will allow its customers to

achieve these goals.

In the

UK, MAM Software continues to compete primarily with Activant, Inc. and several

other smaller software companies including EGO and RAMDATA. The Company feels

that it provides a range of solutions that combine proven concepts with

cutting-edge technology that are functional, effective and reliable. The Company

feels that its focus towards continuing to provide solutions that enable

business to find new efficiencies and increase existing efficiencies, as the

Company develops its own products, will provide it an advantage over the

competition. These efforts, together with strong post sales support and ongoing

in depth product and market support, will assist the Company in generating and

maintaining its position within the market.

Several

large enterprise resource planning and software companies, including Microsoft

Corporation, Oracle Corporation and SAP AG, continue to supply Enterprise

Resource Planning (“ERP”) and Supply Chain Management (“SCM”) products to medium

sized original equipment manufacturers and suppliers within the automotive

market, but to date have not focused strongly on the aftermarket. The solutions

that they have developed are mainly focused on the efficient management of the

supply chain and to date do not appear to be looking to supply systems and

solutions into the jobber and service segments of the aftermarket. However there

can be no assurance that those companies will not develop or acquire a

competitive product or service in the future.

Employees

The

Company has 164 full-time employees: 2 at MAM Software Group, Inc., 30 at ASNA,

8 at MAM Software, Inc., and 124 at MAM Software Ltd. The 2 employees in MAM

Software Group, Inc., 1 is a senior executive and 1 is an accountant. ASNA has

30 employees in the US comprised of 2 in management, 1 in sales and marketing,

10 in research and development, 15 in professional services and support and 2 in

general and administration. MAM Software, Inc has 8 employees, 1 in senior

management, 2 in sales and marketing, and 5 in research and development. MAM

Software has 124 employees in the UK comprised of 6 in management, 13 in sales

and marketing, 22 in research and development, 75 in professional services and

support and 8 in general and administration.

15

All of

the Company’s employees have executed customary confidentiality and restrictive

covenant agreements. The Company believes it has a good relationship with its

employees and is currently unaware of any key management or other personnel

looking to either retire or leave the employment of the Company. During 2008,

the Company adopted a 2007 Long Term Stock Incentive Plan, which was approved by

the Company’s Board of Directors and stockholders.

|

Item

1A.

|

Risk

Factors

|

Our

business, financial condition and operating results are subject to a number of

risk factors, both those that are known to us and identified below and others

that may arise from time to time. These risk factors could cause our actual

results to differ materially from those suggested by forward-looking statements

in this report and elsewhere, and may adversely affect our business, financial

condition or operating results. If any of those risk factors should occur,

moreover, the trading price of our securities could decline, and investors in

our securities could lose all or part of their investment in our securities.

These risk factors should be carefully considered in evaluating our

prospects.

WE

HAVE A LIMITED OPERATING HISTORY THAT MAKES IT DIFFICULT TO EVALUATE OUR

BUSINESS AND TO PREDICT OUR FUTURE OPERATING RESULTS.

We were

known as W3 Group, Inc. and had no operations in December 2005, at which time we

engaged in a reverse acquisition; therefore, we have limited historical

operations. Two of our subsidiaries, MAM Software and AFS Tire Management, Inc.

(f/k/a CarParts Technologies, Inc.) have operated since 1984 and 1997,

respectively, as independent companies under different management until our

former parent, ADNW, acquired MAM Software in April 2003 and CarParts

Technologies, Inc. in August 2004. Since the reverse merger in December 2005, we

have been primarily engaged in organizational activities, including developing a

strategic operating plan and developing, marketing and selling our products. In

particular, we had integrated a third subsidiary as a result of the acquisition

of EXP from ADNW in August 2006, its MMI Automotive subsidiary. In February

2007, we acquired DSS from ADNW, which owned a minority interest of DCS

Automotive Limited. On November 12, 2007, we sold EXP and DSS, which was EXP’s

wholly owned subsidiary. As a result of our limited operating history, it will

be difficult to evaluate our business and predict our future operating

results.

16

WE

MAY FAIL TO ADDRESS RISKS WE FACE AS A DEVELOPING BUSINESS WHICH COULD ADVERSELY

AFFECT THE IMPLEMENTATION OF OUR BUSINESS PLAN.

We are

prone to all of the risks inherent in the establishment of any new business

venture. You should consider the likelihood of our future success to be highly

speculative in light of our limited operating history, as well as the limited

resources, problems, expenses, risks and complications frequently encountered by

entities at our current stage of development.

To

address these risks, we must, among other things,

|

|

·

|

implement

and successfully execute our business and marketing

strategy;

|

|

|

·

|

continue

to develop new products and upgrade our existing

products;

|

|

|

·

|

respond

to industry and competitive

developments;

|

|

|

·

|

attract,

retain, and motivate qualified personnel;

and

|

|

|

·

|

obtain

equity and debt financing on satisfactory terms and in timely fashion in

amounts adequate to implement our business plan and meet our

obligations.

|

We may

not be successful in addressing these risks. If we are unable to do so, our

business prospects, financial condition and results of operations would be

materially adversely affected.

WE

MAY FAIL TO SUCCESSFULLY DEVELOP, MARKET AND SELL OUR PRODUCTS.

To

achieve profitable operations, we, along with our subsidiaries, must continue

successfully to improve, market and sell existing products and develop, market

and sell new products. Our product development efforts may not be successful.

The development of new software products is highly uncertain and subject to a

number of significant risks. The development cycle - from inception to

installing the software for customers - can be lengthy and uncertain. The

ability to market the product is unpredictable and may cause delays. Potential

products may appear promising at early stages of development, and yet may not

reach the market for a number of reasons.

17

ADDITIONAL

ISSUANCES OF SECURITIES WILL DILUTE YOUR STOCK OWNERSHIP AND COULD AFFECT OUR

STOCK PRICE.

As of

August 31, 2010, there were 85,860,185 shares of our Common Stock issued

and outstanding and 1,792,662 Series A Preferred Shares issued and

outstanding. Our Articles of Incorporation authorize the issuance of an

aggregate of 150,000,000 shares of Common Stock and 10,000,000 shares of

Preferred Stock, on such terms and at such prices as our Board of Directors may

determine. These shares are intended to provide us with the necessary

flexibility to undertake and complete plans to raise funds if and when needed.

In addition, we may pursue acquisitions that could include issuing equity,

although we have no current arrangements to do so. Any such issuances of

securities would have a dilutive effect on current ownership of MAM stock. The

market price of our Common Stock could fall in esponse to the sale or issuance

of a large number of shares, or the perception that sales of a large number of

shares could occur.

WE

MAY ENCOUNTER SIGNIFICANT FINANCIAL AND OPERATING RISKS IF WE GROW OUR BUSINESS

THROUGH ACQUISITIONS.

As part

of our growth strategy, we may seek to acquire or invest in complementary or

competitive businesses, products or technologies. The process of integrating

acquired assets into our operations may result in unforeseen operating

difficulties and expenditures and may absorb significant management attention

that would otherwise be available for the ongoing development of our business.

We may allocate a significant portion of our available working capital to

finance all or a portion of the purchase price relating to possible acquisitions

although we have no immediate plans to do so. Any future acquisition or

investment opportunity may require us to obtain additional financing to complete

the transaction. The anticipated benefits of any acquisitions may not be

realized. In addition, future acquisitions by us could result in potentially

dilutive issuances of equity securities, the incurrence of debt and contingent

liabilities and amortization expenses related to goodwill and other intangible

assets, any of which could materially adversely affect our operating results and

financial position. Acquisitions also involve other risks, including entering

markets in which we have no or limited prior experience.

AN

INCREASE IN COMPETITION FROM OTHER SOFTWARE MANUFACTURERS COULD HAVE A MATERIAL

ADVERSE EFFECT ON OUR ABILITY TO GENERATE REVENUE AND CASH FLOW.

Competition

in our industry is intense. Potential competitors in the U.S. and Europe are

numerous. Most competitors have substantially greater capital resources,

marketing experience, research and development staffs and facilities than we

have. Our competitors may be able to develop products before us or develop more

effective products or market them more effectively which would limit our ability

to generate revenue and cash flow.

18

THE

PRICES WE CHARGE FOR OUR PRODUCTS MAY DECREASE AS A RESULT OF COMPETITION AND

OUR REVENUES COULD DECREASE AS A RESULT.

We face

potential competition from very large software companies, including Microsoft

Corporation, Oracle Corporation and SAP AG which supply ERP and

SCM products to our target market of small- to medium-sized businesses

servicing the automotive aftermarket. To date we have directly competed with one

of these larger software and service companies. There can be no assurance that

these companies will not develop or acquire a competitive product or service in

the future. Our business would be dramatically affected by price pressure if

these larger software companies attempted to gain market share through the use

of highly discounted sales and extensive marketing campaigns.

IF

WE FAIL TO KEEP UP WITH RAPID TECHNOLOGICAL CHANGE, OUR TECHNOLOGIES AND

PRODUCTS COULD BECOME LESS COMPETITIVE OR OBSOLETE.

The

software industry is characterized by rapid and significant technological

change. We expect that the software needs associated with the automotive

technology will continue to develop rapidly, and our future success will depend

on our ability to develop and maintain a competitive position through

technological development.

WE

DEPEND ON PATENT AND PROPRIETARY RIGHTS TO DEVELOP AND PROTECT OUR TECHNOLOGIES

AND PRODUCTS, WHICH RIGHTS MAY NOT OFFER US SUFFICIENT PROTECTION.

The

software industry places considerable importance on obtaining patent and trade

secret protection for new technologies, products and processes. Our success will

depend on our ability to obtain and enforce protection for products that we

develop under US and foreign patent laws and other intellectual property laws,

preserve the confidentiality of our trade secrets and operate without infringing

the proprietary rights of third parties. Currently, only one of our products is

patented.

We also

rely upon trade secret protection for our confidential and proprietary

information. Others may independently develop substantially equivalent

proprietary information and techniques or gain access to our trade secrets or

disclose our technology. We may not be able to meaningfully protect our trade

secrets which could limit our ability to exclusively produce

products.

We

require our employees, consultants, and parties to collaborative agreements to

execute confidentiality agreements upon the commencement of employment or

consulting relationships or collaboration with us.

These agreements may not provide meaningful protection of our

trade secrets or adequate remedies in the event of unauthorized use or

disclosure of confidential and proprietary information.

19

IF

WE BECOME SUBJECT TO ADVERSE CLAIMS ALLEGING INFRINGEMENT OF THIRD-PARTY

PROPRIETARY RIGHTS, WE MAY INCUR UNANTICIPATED COSTS AND OUR COMPETITIVE

POSITION MAY SUFFER.

We are

subject to the risk that we are infringing on the proprietary rights of third

parties. Although we are not aware of any infringement by our technology on the

proprietary rights of others and are not currently subject to any legal

proceedings involving claimed infringements, we cannot assure you that we will

not be subject to such third-party claims, litigation or indemnity demands and

that these claims will not be successful. If a claim or indemnity demand were to

be brought against us, it could result in costly litigation or product shipment

delays or force us to stop selling such product or providing such services or to

enter into royalty or license agreements.

OUR

SOFTWARE AND INFORMATION SERVICES COULD CONTAIN DESIGN DEFECTS OR ERRORS WHICH

COULD AFFECT OUR REPUTATION, RESULT IN SIGNIFICANT COSTS TO US AND IMPAIR OUR

ABILITY TO SELL OUR PRODUCTS.

Our

software and information services are highly complex and sophisticated and

could, from time to time, contain design defects or errors. We cannot assure you

that these defects or errors will not delay the release or shipment of our

products or, if the defect or error is discovered only after customers have

received the products, that these defects or errors will not result in increased

costs, litigation, customer attrition, reduced market acceptance of our systems

and services or damage to our reputation.

IF

WE LOSE KEY MANAGEMENT OR OTHER PERSONNEL OUR BUSINESS WILL SUFFER.

We are

highly dependent on the principal members of our management staff. We also rely

on consultants and advisors to assist us in formulating our development

strategy. Our success also depends upon retaining key management and technical

personnel, as well as our ability to continue to attract and retain additional

highly qualified personnel. We may not be successful in retaining our current

personnel or hiring and retaining qualified personnel in the future. If we lose

the services of any of our management staff or key technical personnel, or if we

fail to continue to attract qualified personnel, our ability to acquire, develop

or sell products would be adversely affected.

20

IT

MAY BE DIFFICULT FOR SHAREHOLDERS TO RECOVER AGAINST THOSE OF OUR DIRECTORS AND

OFFICERS THAT ARE NOT RESIDENTS OF THE U.S.

Two of

our directors, of whom one are also executive officers, are residents of the UK.

In addition, our significant operating subsidiary, MAM Software is located in

the UK. Were one or more shareholders to bring an action against us in the

US and succeed, either through default or on the merits, and obtain a financial

award against an officer or director of the Company, that shareholder may be

required to enforce and collect on his or her judgment in the UK, unless the

officer or director owned assets which were located in the US. Further,

shareholder efforts to bring an action in the UK against its citizens for any

alleged breach of a duty in a foreign jurisdiction may be difficult, as

prosecution of a claim in a foreign jurisdiction, and in particular a foreign

nation, is fraught with difficulty and may be effectively, if not financially,

unfeasible.

OUR

MANAGEMENT AND INTERNAL SYSTEMS MIGHT BE INADEQUATE TO HANDLE OUR POTENTIAL

GROWTH.

Our

success will depend in significant part on the expansion of our operations and

the effective management of growth. This growth will place a significant strain

on our management and information systems and resources and operational and

financial systems and resources. To manage future growth, our management must

continue to improve our operational and financial systems and expand, train,

retain and manage our employee base. Our management may not be able to manage

our growth effectively. If our systems, procedures, controls, and resources are

inadequate to support our operations, our expansion would be halted and we could

lose our opportunity to gain significant market share. Any inability to manage

growth effectively may harm our ability to institute our business

plan.

21

THE

MARKET FOR OUR COMMON STOCK IS LIMITED AND YOU MAY NOT BE ABLE TO SELL YOUR

COMMON STOCK.

Our

Common Stock is currently quoted on the Over-The-Counter Bulletin Board, and is

not traded on a national securities exchange. The market for purchases and sales

of the Company’s Common Stock is limited and therefore the sale of a relatively

small number of shares could cause the price to fall sharply. Accordingly, it

may be difficult to sell shares quickly without significantly depressing the

value of the stock. Unless we are successful in developing continued investor

interest in our stock, sales of our stock could continue to result in major

fluctuations in the price of the stock.

THE

PRICE OF OUR COMMON STOCK IS LIKELY TO BE VOLATILE AND SUBJECT TO WIDE

FLUCTUATIONS.

The

market price of the securities of software companies has been especially

volatile. Thus, the market price of our Common Stock is likely to be subject to

wide fluctuations. If our revenues do not grow or grow more slowly than we

anticipate, or, if operating or capital expenditures exceed our expectations and

cannot be adjusted accordingly, or if some other event adversely affects us, the

market price of our Common Stock could decline. If the stock market in general

experiences a loss in investor confidence or otherwise fails, the market price

of our Common Stock could fall for reasons unrelated to our business, results of

operations and financial condition. The market price of our stock also might

decline in reaction to events that affect other companies in our industry even

if these events do not directly affect us.

SINCE

OUR STOCK IS CLASSIFIED AS A “PENNY STOCK,” THE RESTRICTIONS OF THE SEC’S PENNY

STOCK REGULATIONS MAY RESULT IN LESS LIQUIDITY FOR OUR STOCK.

The US

Securities and Exchange Commission (“SEC”) has adopted regulations which define

a “Penny Stock” to be any equity security that has a market price (as therein

defined) of less than $5.00 per share

or an exercise price of less than $5.00 per share, subject

to certain exceptions. For any transactions involving a penny stock, unless

exempt, the rules require the delivery, prior to any transaction involving a

penny stock by a retail customer, of a disclosure schedule prepared by the SEC

relating to the penny stock market. Disclosure is also required to be made about

commissions payable to both the broker/dealer and the registered representative

and current quotations for the securities. Finally,

monthly statements are required to be

sent disclosing recent price information for the penny stock held in the

account and information on the limited market in penny stocks. Because the

market price for our shares of common stock is less than $5.00, our securities

are classified as penny stock. As a result of the penny stock restrictions,

brokers or potential investors may be reluctant to trade in our securities,

which may result in less liquidity for our stock.

22

WE

HAVE INSURANCE COVERAGE FOR THE SERVICES WE OFFER. HOWEVER, A CLAIM FOR DAMAGES

MAY BE MADE AGAINST US REGARDLESS OF OUR RESPONSIBILITY FOR THE FAILURE, WHICH

COULD EXPOSE US TO LIABILITY.

We

provide business management solutions that we believe are critical to the

operations of our customers’ businesses and provide benefits that may be

difficult to quantify. Any failure of a customer’s system installed or of the

services offered by us could result in a claim for substantial damages against

us, regardless of our responsibility for the failure. Although we attempt to

limit our contractual liability for damages resulting from negligent acts,

errors, mistakes or omissions in rendering our services, we cannot assure you

that the limitations on liability we include in our agreements will be

enforceable in all cases, or that those limitations on liability will otherwise

protect us from liability for damages. In the event that the terms and

conditions of our contracts which limit our liability are not sufficient, we

have insurance coverage. This coverage of approximately $5,000,000 in the

aggregate in the UK and in the US insures the business for negligent acts, error

or omission, failure of the technology services to perform as intended, and

breach of warranties or representations. It also insures the services that we

supply including, web services, consulting, analysis, design, installation,

training, support, system integration, the manufacture, sale, licensing,

distribution or marketing of software, the design and development of code,

software and programming and the provision of software applications as a

service, rental or lease. However, there can be no assurance that our insurance

coverage will be adequate or that coverage will remain available at acceptable

costs. Successful claims brought against us in excess of our insurance coverage

could seriously harm our business, prospects, financial condition and results of

operations. Even if not successful, large claims against us could result in

significant legal and other costs and may be a distraction to our senior

management.

23

BECAUSE

WE HAVE INTERNATIONAL OPERATIONS, WE WILL BE SUBJECT TO RISKS OF CONDUCTING

BUSINESS IN FOREIGN COUNTRIES.

International

operations constitute a significant part of our business, and we are subject to

the risks of conducting business in foreign countries, including:

|

|

•

|

difficulty

in establishing or managing distribution

relationships;

|

|

|

•

|

different

standards for the development, use, packaging and marketing of our

products and technologies;

|

|

|

•

|

our

ability to locate qualified local employees, partners, distributors and

suppliers;

|

|

|

•

|

the

potential burden of complying with a variety of foreign laws and trade

standards; and

|

|

|

•

|

general

geopolitical risks, such as political and economic instability, changes in

diplomatic and trade relations, and foreign currency risks and

fluctuations.

|

No

assurance can be given that we will be able to positively manage the risks

inherent in the conduct of our international operations or that such operations

will not have a negative impact on our overall financial

operations.

WE WERE NOT IN COMPLIANCE WITH

CERTAIN COVENANTS UNDER OUR SENIOR SECURED NOTE. WE HAVE RECEIVED WAIVERS ON

THREE OCCASIONS OF THESE EVENTS OF DEFAULT FROM THE HOLDER OF THE

NOTE.

During

the fiscal periods ended March 31, 2008, June 30, 2008 and December 31, 2008, we

violated certain covenants related to cash flow ratios under our senior secured

note with ComVest Capital LLC, dated December 21, 2007. ComVest has provided us

a waiver of these events of default on each occasion. As of March 31, 2009 and

June 30, 2009, we were in compliance with the amended loan

covenants.

As of

March 31, 2010, we failed to meet the Earnings Before Interest Depreciation and

Amortization (“EBIDA”) Ratio Covenant of 1.25:1 as required under our senior

secured note with ComVest Capital LLC, dated December 21, 2007, as amended,

which failure constitutes an event of default. The terms of the note

provide that, if any event of default occurs, the full principal amount of the

note, together with interest and other amounts owing in respect thereof to the

date of acceleration, shall become, at ComVest’s election, immediately due and

payable in cash. On June 2, 2010 ComVest charged us a fee of

$25,000 and on June 17, 2010 increased the interest rate on the Term Loan from

11% to 16% and increased the interest rate on the Revolving Credit Facility from

9.5% to 13.5%. The Company has entered into a

forbearance agreement to resolve the default with

ComVest.

24

WE

WILL NEED ADDITIONAL FINANCING OF $3,917,000 TO MAKE THE $2,917,000 BALLOON

PAYMENT DUE IN NOVEMBER 2010 ON OUR TERM LOAN AND $1,000,000 DUE ON THE

REVOLVING CREDIT FACILITY TO CONTINUE AS A GOING CONCERN, WHICH ADDITIONAL

FINANCING MAY NOT BE AVAILABLE ON A TIMELY BASIS, OR AT ALL.

We

prepared our consolidated financial statements as of June 30, 2010 on a

going-concern basis, which contemplates the realization of assets and the

satisfaction of liabilities in the normal course of business. The Company had an

accumulated deficit of $23.4 million and a working capital deficit of $6.7

million at June 30, 2010. These factors, along with the $4,125,000

payments due in November 2010 on our loans, raise substantial doubt about the

Company’s ability to continue as a going concern unless we are able to secure

additional funds.

We may be

required to pursue sources of additional capital to fund our operations through

various means, which may consist of equity or debt financing, including a rights

offering. Future financings through equity investments are likely to be dilutive

to existing stockholders. Also, the terms of securities we may issue in future

capital transactions may be more favorable for our new investors. Newly issued

securities may include preferences, superior voting rights and the issuance of

warrants or other derivative securities, which may have additional dilutive

effects. Further, we may incur substantial costs in pursuing future capital

and/or financing, including investment banking fees, legal fees, accounting

fees, printing and distribution expenses and other costs. We may also be

required to recognize non-cash expenses in connection with certain securities we

may issue, such as convertible notes and warrants, which will adversely impact

our financial results.

As a

result, there can be no assurance that additional funds will be available when

needed from any source or, if available, will be available on terms that are

acceptable to us. If we are unable to raise funds to satisfy our capital needs

on a timely basis, we may be required to cease operations.

WE

MAY NOT BE ABLE OBTAIN ADDITIONAL FUNDING IF NEEDED.

Our

current operations will not generate sufficient cash flows to maintain our

current operations for the next 12 months and repay our ComVest obligations. We

are currently seeking additional funds through debt or equity

financings. Such financings may not be forthcoming. As has been widely reported,

global and domestic financial markets and economic conditions have been, and

continue to be, disrupted and volatile due to a variety of factors, including

the current weak economic conditions. As a result, the cost of

raising money in the debt and equity capital markets has increased substantially

while the availability of funds from those markets has diminished significantly,

even more so for smaller companies like ours. If such conditions and

constraints continue, we may not be able to acquire additional funds either

through credit markets or through equity markets and, even if additional

financing is available, it may not be available on terms we find

favorable. At this time, there are no anticipated sources of

additional funding in place. Failure to secured additional funding when needed

could have an adverse effect on our ability to grow.

25

WE

DO NOT INTEND TO DECLARE DIVIDENDS ON OUR COMMON STOCK.

We will

not distribute dividends to our stockholders until and unless we can develop

sufficient funds from operations to meet our ongoing needs and implement our

business plan. The time frame for that is inherently unpredictable, and you

should not plan on it occurring in the near future, if at all.

|

Item

1B.

|

Unresolved

Staff Comments.

|

Not

applicable.

|

Item

2.

|

Properties.

|

Our

corporate offices are located at Maple Park, Maple Court, Tankersley, Barnsley,

UK S75 3DP.

The main

telephone number is 0-11-44-1244-31-1794. MAM Software Group leases

approximately 400 square feet at its corporate offices and pays rent of $2,685

per quarter.

ASNA has

offices at 34052 La Plaza Drive, Suite 201, Dana Point, California 92629. The

main telephone number is 949-488-8860. ASNA has an office at 3435 Winchester Rd,

Ste 100, Allentown PA 18104 and the phone number at that office is 610-336-9045.

The California offices total approximately 3,400 square feet and are leased at