Attached files

| file | filename |

|---|---|

| 8-K - 8-K FOR UBS CONFERENCE PRESENTATION - TEMPLE INLAND INC | tin8k20100915.htm |

1

Our job is to be the best

UBS Global Paper and Forest Products

Conference

Conference

September 15, 2010

2

This presentation contains “forward-looking statements” within the meaning of the federal

securities laws. These statements reflect management’s current views with respect to future

events and are subject to risk and uncertainties. We note that a variety of factors and uncertainties

could cause our actual results to differ significantly from the results discussed in the forward-

looking statements. Factors and uncertainties that might cause such differences include, but are

not limited to: general economic, market, or business conditions; the opportunities (or lack

thereof) that may be presented to us and that we may pursue; fluctuations in costs and expenses

including the costs of raw materials, purchased energy, and freight; changes in interest rates;

demand for new housing; accuracy of accounting assumptions related to impaired assets,

pension and postretirement costs, contingency reserves and income taxes; competitive actions by

other companies; changes in laws or regulations; our ability to execute certain strategic and

business improvement initiatives; the accuracy of certain judgments and estimates concerning the

integration of acquired operations; and other factors, many of which are beyond our control.

Except as required by law, we expressly disclaim any obligation to publicly revise any forward-

looking statements contained in this presentation to reflect the occurrence of events after the date

of this presentation.

securities laws. These statements reflect management’s current views with respect to future

events and are subject to risk and uncertainties. We note that a variety of factors and uncertainties

could cause our actual results to differ significantly from the results discussed in the forward-

looking statements. Factors and uncertainties that might cause such differences include, but are

not limited to: general economic, market, or business conditions; the opportunities (or lack

thereof) that may be presented to us and that we may pursue; fluctuations in costs and expenses

including the costs of raw materials, purchased energy, and freight; changes in interest rates;

demand for new housing; accuracy of accounting assumptions related to impaired assets,

pension and postretirement costs, contingency reserves and income taxes; competitive actions by

other companies; changes in laws or regulations; our ability to execute certain strategic and

business improvement initiatives; the accuracy of certain judgments and estimates concerning the

integration of acquired operations; and other factors, many of which are beyond our control.

Except as required by law, we expressly disclaim any obligation to publicly revise any forward-

looking statements contained in this presentation to reflect the occurrence of events after the date

of this presentation.

This presentation includes non-GAAP financial measures. The required reconciliations to

GAAP financial measures are included on our website, www.templeinland.com.

GAAP financial measures are included on our website, www.templeinland.com.

3

Create Superior and Sustainable Value

• Maximize ROI

• Profitably grow our business

Scorecard

• Corrugated Packaging

– 10.8% first half 2010 ROI

– Positioned for record earnings in the second half of

2010

2010

– Fifth consecutive year of above cost of capital returns

• Building Products

– Positive first half EBIT

– First half EBITDA of $27 million

4

5

Corrugated Packaging Segment Highlights

• 7 mills

- 3.9 million tons

• 60 converting facilities

- 3.7 million tons

• # 3 industry producer

Business Highlights

Financial Highlights

|

($ in Millions)

|

|

2006

|

2007

|

2008

|

2009

|

|

Revenue

|

|

$2,977

|

$3,044

|

$3,190

|

$3,001

|

|

EBIT

|

|

$255

|

$287

|

$225

|

$347

|

|

Investment

|

|

$2,039

|

$2,004

|

$1,990

|

$2,109

|

|

ROI

|

|

12.5%

|

14.3%

|

11.3%

|

16.5%

|

|

EBITDA

|

|

$408

|

$429

|

$371

|

$492

|

6

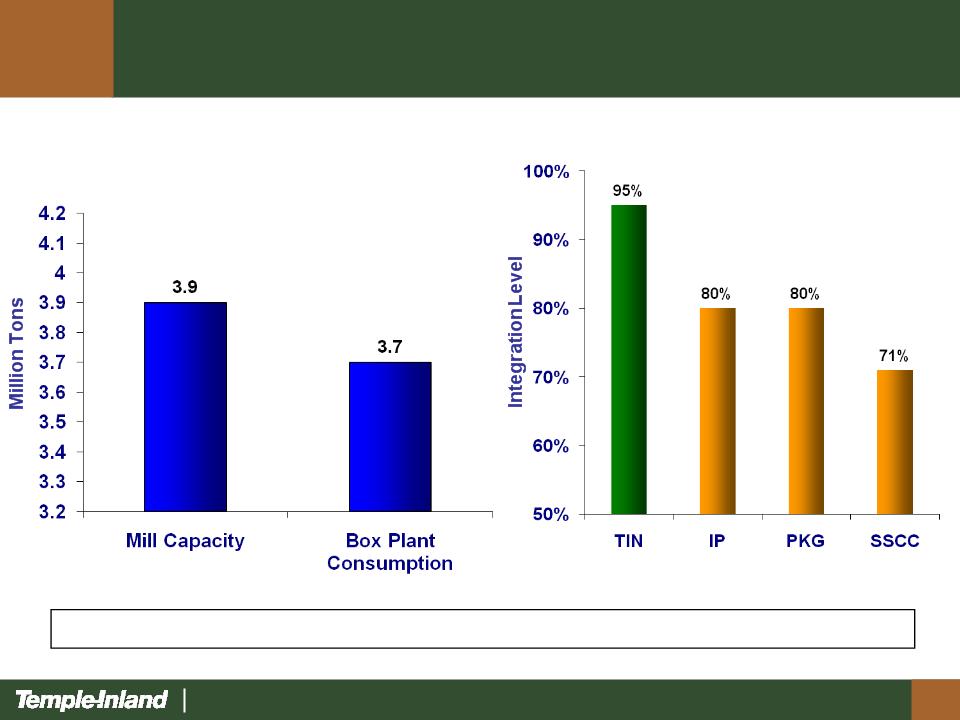

Corrugated Packaging Strategic Initiatives

• Maintain high integration level

- Box plant consumption = mill capacity

• Drive for low cost

- Asset utilization and manufacturing excellence

• Improve mix and margins

- Sales excellence

• Profitably grow business

- Organically / Acquisition

Lowering Costs, Improving Efficiencies and Growing Profitably

7

Integration Level - Highest in the Industry

Source: Company reports

Temple-Inland is the most integrated producer of corrugated containers

Drive For Low Cost

• Lower mill cost

– Targeted capital to enhance reliability, reduce

energy consumption and enhance mix

flexibility

energy consumption and enhance mix

flexibility

• Lower box plant cost

– Box Plant Transformation I and II

8

9

Box Plant Transformation I (2006-2010)

• EBIT (Lower Costs) $80MM/Year

– Fewer Plants 4

– Fewer Machines 88

– Fewer Positions 1,157

• Investment $174MM

• ROI 46%

10

Box Plant Transformation II (2010-2013)

• EBIT (Lower Costs) $100MM/Year

– Fewer Plants 12

– Fewer Machines 65

– Fewer Positions 900

• Investment $250MM

• ROI 40%

11

Improve Mix and Margins

• Customer segmentation

• Target richer segment of customer

portfolio

portfolio

12

Profitably Grow Our Business

• PBL acquisition

– $20 million of synergies

– $30 million from white-top

– 60% ROI

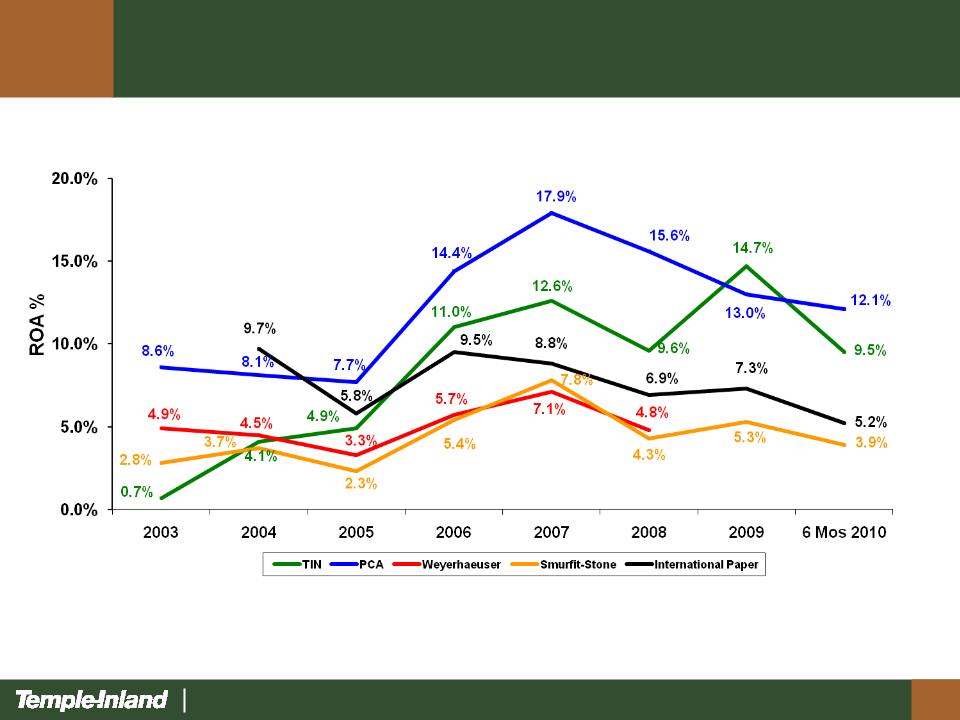

Corrugated Packaging

Comparative Peer Group Returns

Comparative Peer Group Returns

Notes: (1) As reported by segment excluding special items for TIN, IP and Weyerhaeuser. For TIN and IP, the asset base was adjusted to include acquisitions made in Q3 2008.

(2) For PCA, EBIT = Gross profit-selling and administrative expenses. (3) For SSCC, EBIT as reported by segment; total assets reported for the company beginning in 2007.

For prior years, total assets = segment assets + other assets of $3.3 billion.

13

North American Corrugated Packaging

Industry Fundamentals

Industry Fundamentals

• Low inventories

• High operating rates

• Positive demand

• Improved linerboard pricing

14

15

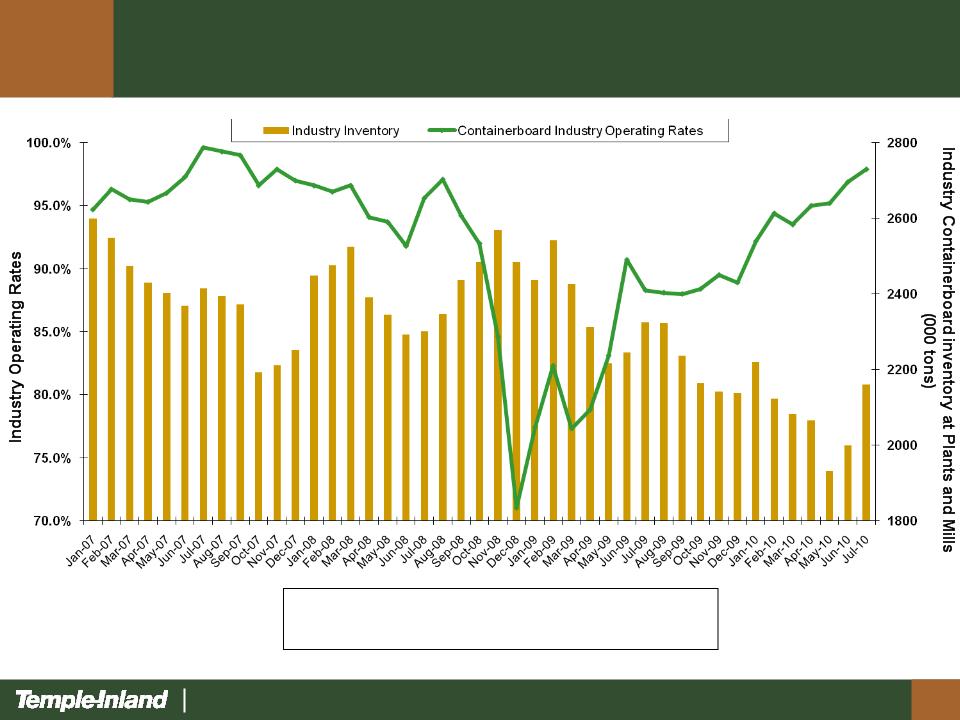

Source: Fibre Box Association and AF&PA

July 2010 inventories were lowest

July level since 1979

Rising Industry Operating Rates

and Lower Inventories

and Lower Inventories

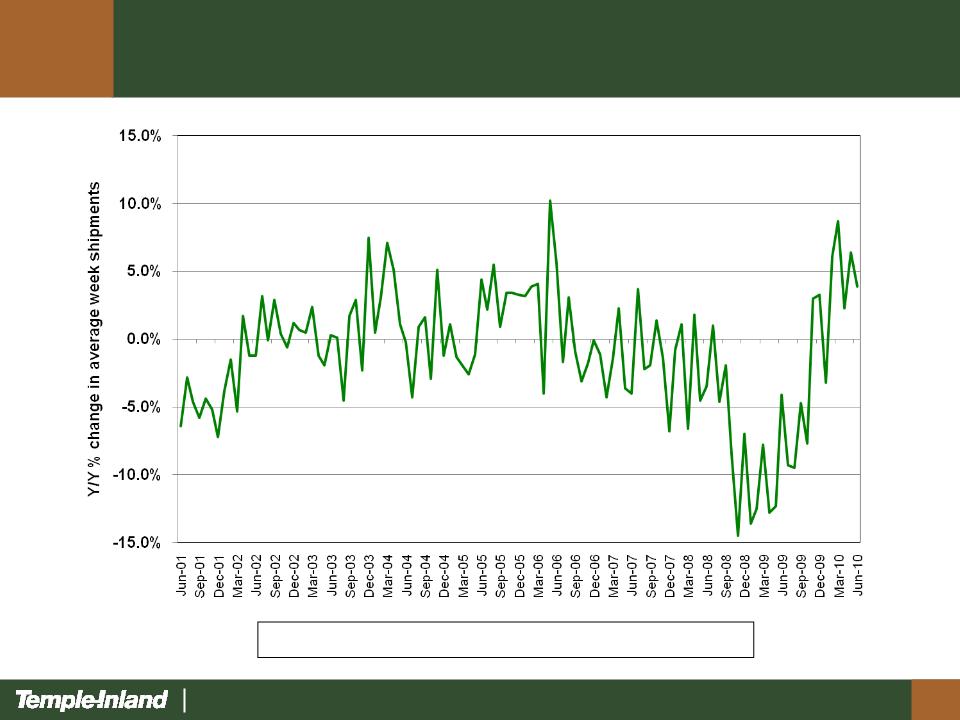

Improving Box Demand

16

Year-to-date industry box demand is up 3.2%

Source: Fibre Box Association

17

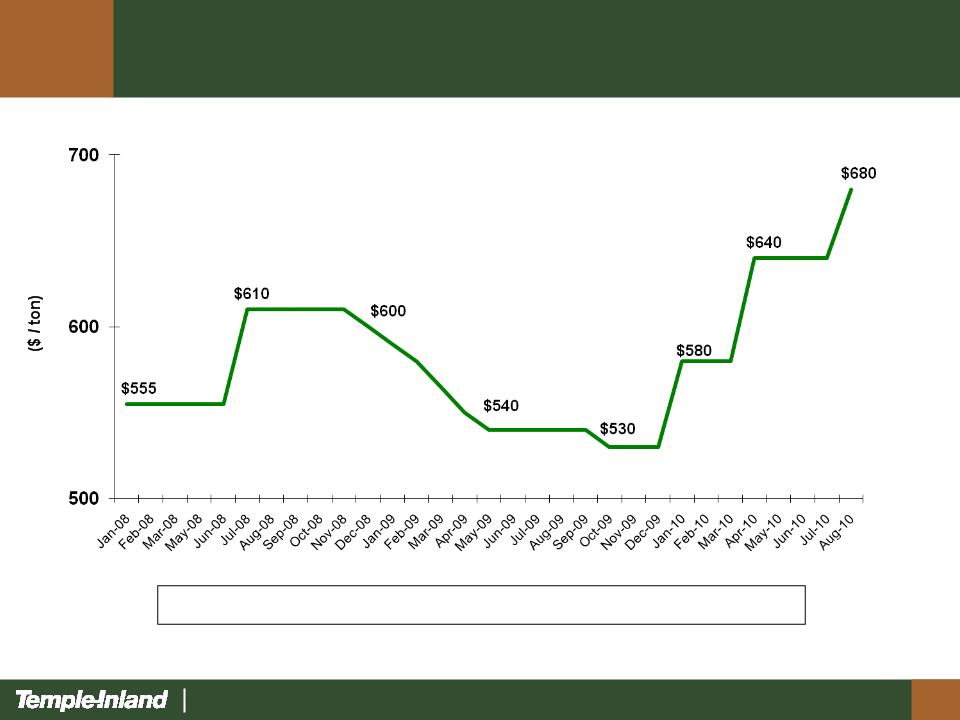

Improving Linerboard Pricing

Linerboard prices have risen 28% in the last 12 months

Source: Pulp and Paper Week

18

Corrugated Packaging Summary

• Simple, effective strategy…execution = results

• Track record of success

• Improved industry fundamentals

19

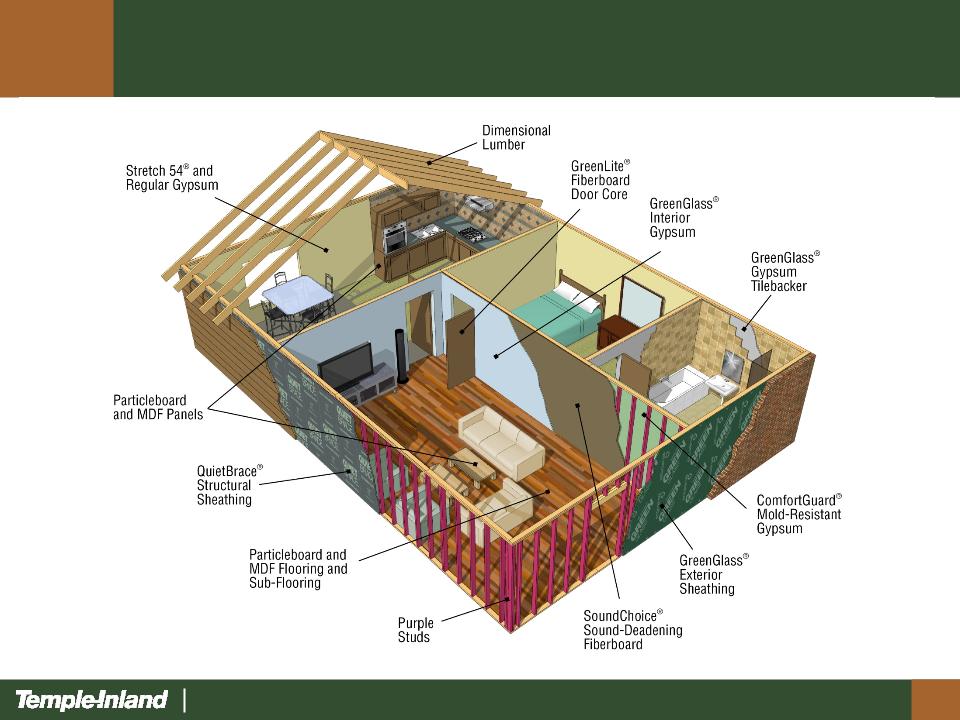

Building Products

• Portfolio of Products

– Lumber

– Gypsum

– Particleboard

– MDF

• Lowest quartile cost converting

operations

operations

• Located near large, high-growth

markets

markets

Financial Highlights

Business Highlights

|

($ in Millions)

|

2006

|

2007

|

2008

|

2009

|

|

Revenue

|

$1,119

|

$806

|

$694

|

$576

|

|

EBIT

|

$221

|

$8

|

($40)

|

($27)

|

|

Investment

|

$586

|

$562

|

$560

|

$535

|

|

ROI

|

37.7%

|

1.4%

|

(7.1%)

|

(5.0%)

|

|

EBITDA

|

$265

|

$53

|

$8

|

$17

|

|

Housing Starts (000’s)

|

1,812

|

1,342

|

900

|

553

|

20

Building Products Strategic Initiatives

• Deliver tailored portfolio of building products

– Products for new home, repair and remodeling

and commercial markets

and commercial markets

• Drive low cost

– Manufacturing excellence

• Serve preferred markets

– Favorable demographics

• Profitably grow business

21

Tailored Products

22

Low Cost Operations

Buna

Pineland

Diboll

Rome

DeQuincy

Lumber

Competitive

Position

1st

Quartile

2nd

Quartile

3rd

Quartile

4th

Quartile

Gypsum

Competitive

Position

Cumberland

Fletcher

W. Memphis

McQueeney

Panels

Competitive

Position

Monroeville

Hope

Diboll

Thomson

PB

MDF

El Dorado

Mt. Jewett

80% of Building Products operations are in lowest cost quartile

1st

Quartile

2nd

Quartile

3rd

Quartile

4th

Quartile

1st

Quartile

2nd

Quartile

3rd

Quartile

4th

Quartile

Source: Beck & RISI studies and internal analysis

23

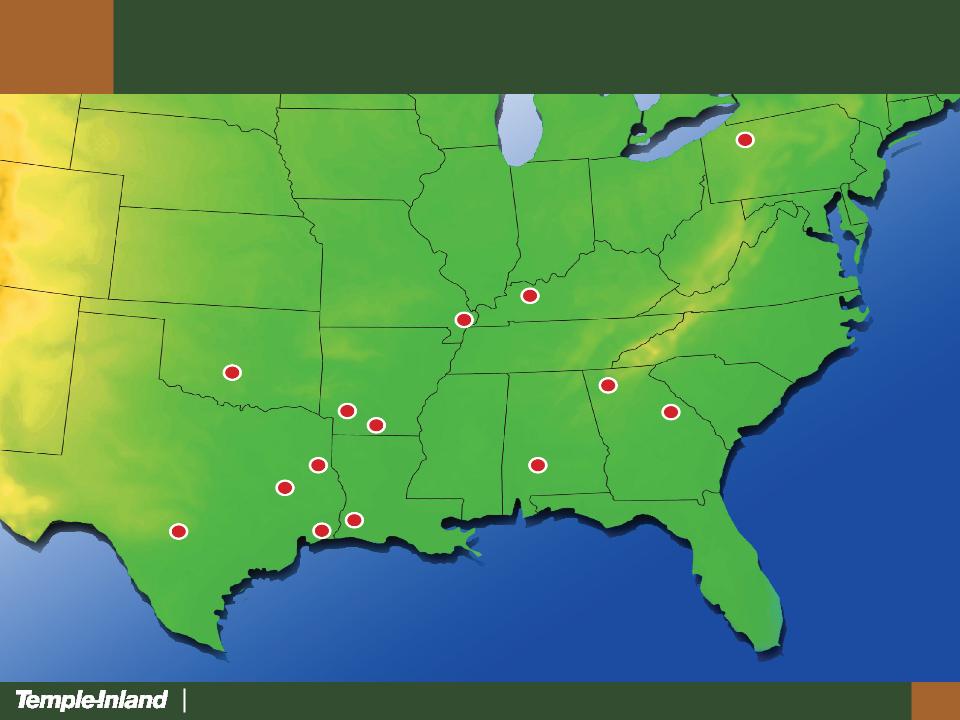

Building Products Facilities

Mt. Jewett

Cumberland City

West Memphis

Fletcher

El Dorado

Hope

Rome

Thomson

Pineland

Diboll

Monroeville

DeQuincy

Buna

McQueeney

24

Housing Starts

TIN EBITDA

2006

2007

2008

2009

2010

25

Financial Priorities

• Return cash to shareholders

– Dividend increased 10% to annual

rate of $0.44 per share in Q1 2010

rate of $0.44 per share in Q1 2010

• Reduce debt

• Invest in our business

• Profitably grow

26

Create Superior and Sustainable Value

• Maximize ROI

• Profitably grow our business

27

Our job is to be the best