Attached files

| file | filename |

|---|---|

| EX-31.1 - EX-31.1 - TRC COMPANIES INC /DE/ | a2200138zex-31_1.htm |

| EX-31.2 - EX-31.2 - TRC COMPANIES INC /DE/ | a2200138zex-31_2.htm |

| EX-32.2 - EX-32.2 - TRC COMPANIES INC /DE/ | a2200138zex-32_2.htm |

| EX-23.1 - EX-23.1 - TRC COMPANIES INC /DE/ | a2200138zex-23_1.htm |

| EX-32.1 - EX-32.1 - TRC COMPANIES INC /DE/ | a2200138zex-32_1.htm |

| EX-21 - EX-21 - TRC COMPANIES INC /DE/ | a2200138zex-21.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

PART IV

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý |

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

|

for the fiscal year ended June 30, 2010 |

||

or |

||

o |

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

|

for the transition period from to |

||

Commission file number 1-9947

TRC COMPANIES, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

06-0853807 (I.R.S. Employer Identification No.) |

|

21 Griffin Road North Windsor, Connecticut (Address of principal executive offices) |

06095 (Zip Code) |

Registrant's telephone number, including area code: (860) 298-9692

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Common Stock, $0.10 par value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act. Yes o No ý.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). YES o NO o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý.

The aggregate market value of the registrant's common stock held by non-affiliates on December 25, 2009 was approximately $22,393,000.

On August 31, 2010, there were 19,657,046 shares of common stock of the registrant outstanding.

TRC Companies, Inc.

Index to Annual Report on Form 10-K

Fiscal Year Ended June 30, 2010

2

Certain information included in this report, or in other materials we have filed or will file with the Securities and Exchange Commission (the "SEC") (as well as information included in oral statements or other written statements made or to be made by us), contains or may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (the "1995 Act"). Such statements are being made pursuant to the 1995 Act and with the intention of obtaining the benefit of the "Safe Harbor" provisions of the 1995 Act. Forward-looking statements are based on information available to us and our perception of such information as of the date of this report and our current expectations, estimates, forecasts and projections about the markets in which we operate and the beliefs and assumptions of our management. You can identify these statements by the fact that they do not relate strictly to historical or current facts. They contain words such as "anticipate," "estimate," "expect," "project," "intend," "plan," "believe," "may," "can," "could," "might," or variations of such wording, and other words or phrases of similar meaning in connection with a discussion of our future operating or financial performance, and other aspects of our business, including growth, trends in our business and other characterizations of future events or circumstances. From time to time, forward-looking statements are also included in our other periodic reports on Forms 10-Q and 8-K, in press releases, in our presentations, on our website and in other material released to the public. Any or all of the forward-looking statements included in this report and in any other reports or public statements made by us are only predictions and are subject to risks, uncertainties and assumptions, including those identified below in the "Risk Factors" section, the "Management's Discussion and Analysis of Financial Condition and Results of Operations" section, and other sections of this report and in other reports filed by us from time to time with the SEC as well as in press releases. Such risks, uncertainties and assumptions are difficult to predict and beyond our control and may cause actual results to differ materially from those that might be anticipated from our forward-looking statements. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise. However, any further disclosures made on related subjects in our subsequent reports on Forms 10-K, 10-Q and 8-K should be consulted.

TRC Companies, Inc. (hereinafter collectively referred to as "we" "our" or "us"), was incorporated in 1971. We are a national consulting, engineering and construction management firm that provides integrated services to the environmental, energy, and infrastructure markets, primarily in the United States. A broad range of commercial, industrial and government clients depend on us to design solutions to their toughest business challenges. Our multidisciplinary project teams help our clients (i) implement complex projects from initial concept to delivery and commissioning, (ii) maintain and operate their facilities in compliance with regulatory standards and (iii) manage their assets through decommissioning, demolition, restoration and disposition.

We are headquartered in Windsor, Connecticut and our corporate website is www.trcsolutions.com (information on our website has not been incorporated by reference into this Form 10-K). Through a link on the investor center section of our website, we make available the following filings as soon as reasonably practicable after they are electronically filed with or furnished to the SEC: our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(d) or 15(d) of the Securities and Exchange Act of 1934 (the "Exchange Act") as well as reports filed pursuant to Section 16 of the Exchange Act. All such filings are available free of charge. Under applicable SEC rules, because the

3

aggregate market value of our stock held by non-affiliates was below $50.0 million as of December 25, 2009, the end of our second fiscal quarter, we could have foregone the auditor reporting requirements of Section 404 of the Sarbanes Oxley Act of 2002 for the fiscal year ended June 30, 2010. Nonetheless, we decided to proceed with that process, and the auditors' report on the effectiveness of our internal controls is included in Item 9A. Controls and Procedures.

We incurred net losses applicable to our common shareholders of $22.9 million, $24.1 million and $109.1 million for fiscal years 2010, 2009 and 2008, respectively. The net loss applicable to our common shareholders for fiscal year 2010 included $20.2 million for a goodwill impairment charge and accretion charges on preferred stock of $6.4 million which were partially offset by a net tax benefit of $4.2 million and a $1.7 million gain on extinguishment of debt. The preferred stock accretion charges will continue until the preferred stock converts to common stock in December 2010. The net loss applicable to our common shareholders for fiscal year 2009 included a $21.4 million charge for goodwill and intangible asset write-offs and a provision for income taxes of $3.9 million. The net loss applicable to our common shareholders for fiscal year 2008 included a charge of $77.3 million for goodwill and intangible asset write-offs and a provision for income taxes of $12.3 million which included a valuation allowance against our income taxes due to the uncertainty of realization.

We understand our clients' goals and embrace them as our own, applying creativity, experience, integrity, and dedication to deliver superior solutions to the world's energy, environmental, and infrastructure challenges. We have continued to unify the Company, concentrating on national practices within our operating segments and a national sales and marketing organization, giving us the ability to respond to customer challenges and the current, dynamic market conditions. We are committed to safety, client satisfaction, project execution, and financial performance to help us win work in areas where our success rate is highest and maintain a growing presence in the future direction of our markets. In support of our clients and shareholders, we maintain our focus on technical excellence and excellence in all areas of the project cycle including bidding, sales, performance, and collection.

Our objectives for fiscal year 2011 are:

- •

- Achieve profitable growth in our operating segments. We

are continuing our move to a national focus for each operating segment. Our energy and infrastructure service offerings have been managed and marketed on a national basis since fiscal year 2010, and

we are finalizing the national integration for our environmental service offerings in fiscal year 2011. Our national operating platform is linked to our corporate sales and marketing organization,

providing information exchange on project execution, regulatory trends and market feedback to better deliver and communicate to our markets.

- •

- Improve operating margins and increase positive operating cash

flow. The current uncertain economic conditions require us to continue our focus on efficiency by controlling and reducing operating

costs. In the past several years we have taken steps to consolidate and reduce our general and administrative expenses as well as improve our project margins through increased productivity and better

execution. These enhancements have created a foundation for maintaining or exceeding our current levels of operating margins in the midst of negative economic conditions.

- •

- Attract and retain top talent. We continue to add top performers to expand our expertise. Our objective is to maintain a workplace where top performers in our industry will be challenged by meaningful projects, rewarded for successful performance, and motivated to develop their entrepreneurial and project management skills for the benefit of the entire company.

4

Our services are focused on three operating segments: Energy, Environmental, and Infrastructure.

The Energy segment continues to be our leading operating segment in market potential. We are strategically positioned to serve those key areas within the energy market currently undergoing change and investment. These include shifts in public policy to renewable energy development, development of a smarter and more robust power grid, and end-user demand management. With energy representing one of the main drivers of the domestic economy, we have been one of the leading firms supporting the significant investment associated with the development of new sources of energy and the infrastructure required to deliver new and existing energy sources to consumers. This market, like all other markets dependent upon large capital investment, is influenced by cost and access to capital. While we believe access to private sources of credit and capital will remain constrained through calendar 2010 and possibly into calendar 2011, the American Recovery and Reinvestment Act of 2009 ("ARRA" or "stimulus bill"), targets, among other investments, those specific areas in which we concentrate our energy service offerings: energy efficiency, renewable generation, and transmission and distribution. While we believe ARRA may help bridge the gap currently existing in the credit markets for new energy-related capital projects, it may take several years to realize its full benefit.

Services we provide to energy companies have evolved over the past decade to include support in the licensing and engineering design of new sources of power generation, electrical transmission system upgrades and natural gas and liquid products pipelines and terminals. Energy services are now provided by dedicated staff representing one-quarter of our total employees. As major investor owned utilities continue to consolidate and downsize their engineering and environmental staffs, we expect to continue to see long term growth in these service areas. In addition, we expect to see continued expansion of our expertise in energy efficiency and demand management programs.

Key markets for our energy operating segment are:

- •

- Energy Efficiency. An integral part of the nation's energy plan will consist of more effectively managing our use of finite resources through efficiency, conservation, load management and shifting to renewable energy sources.

- •

- Electric Transmission. Investment in electric transmission and distribution infrastructure represents one of the largest financial commitments facing utilities over the upcoming decade. The age of the transmission and distribution network combined with continuing electric load growth has resulted in heightened concern over the reliability of the nation's transmission grid. Capital programs by utilities for necessary upgrades to the grid system are in the early stages of development and are expected to total several billion dollars.

We develop and manage statewide energy efficiency programs in New York and New Jersey that reduce energy use and cost-effectively manage demand. We provide comprehensive services including program design, program management, quality control, engineering, financial tracking and reporting. In addition to our statewide programs, we also design and manage portfolio energy efficiency programs including a broad range of services from program management to engineering, quality control and construction inspection for a broad spectrum of end users including commercial office buildings, hospitality chains, educational facilities, residential complexes and military installations.

We are also actively focused on the relationship of energy conservation measures to the reduction in carbon footprints, and we are assisting a number of utilities in "greening" their operations against quantifiable objectives.

5

During the past several years we have become one of the leading engineering and environmental licensing service providers supporting the extensive upgrade underway to the nation's electric transmission grid. We provide full scope engineering design, material procurement and construction management services. We also provide essential operations and management support to utilities as the trend towards outsourcing engineering functions continues. Our ability to provide integrated energy and environmental services has proven to be a key factor to our success in obtaining these projects.

The Environmental segment represents our largest operating segment in terms of both profitability and net service revenue ("NSR"). The demand for these services originally arose in response to the significant environmental legislation in the 1970's. Since that time it has largely been a compliance driven market, however mergers and acquisitions and the real estate market created economic drivers as well and enabled us to serve those markets on many fronts including support of property owners on a wide range of issues. We provide substantial support to buyers and sellers in the pre-acquisition due diligence and asset valuation process. Our Exit Strategy program grew to national prominence in response to the need for responsible parties, as well as buyers and sellers, to resolve environmental remediation uncertainties.

We are also a national market leader in the areas of air quality modeling, air emissions testing and monitoring and cultural and natural resource management.

The market drivers for our environmental services are dynamic and include:

- •

- Enforcement and compliance in the contaminated site remediation

market. The Environmental Protection Agency estimates over 29,000 contaminated sites of all sizes still need to be evaluated and

remediated. This fact combined with the emergence of economically distressed assets into the market will provide a strong impetus for assessing and resolving environmental impacts to real estate

assets.

- •

- Natural Gas Related Power Strategies. Natural gas is a

preferred fuel source for domestic power initiatives. While investment in development of new supplies, transmission pipelines and storage facilities is a function of price and economic conditions, we

believe it will become increasingly important in the domestic power mix. We continue to be an industry leader in serving this market based upon our staff experience which includes Federal Energy

Regulatory Commission ("FERC") licensing; federal and state media specific environmental permitting; electrical interconnection engineering; and construction management and oversight. With one of the

most experienced national teams of environmental scientists, we have been responsible for the licensing and construction oversight of several of the largest multi-state gas transmission pipeline

projects in development. We are currently providing services for the permitting of both land-based and offshore Liquefied Natural Gas ("LNG") terminals in the Northeast, Gulf and

Northwest.

- •

- Wind Power and Generation Source Licensing and Permitting. The demand for licensing services and electrical interconnection for new electrical generation sources continues to increase due to several strong market factors. In load congested areas such as the Mid-Atlantic, Northeast, and California, utilities are pursuing development of new sources of electrical supply. Recognizing the importance of fuel diversity, fossil fuel plant development is focusing on both natural gas and coal. Coal plant development projects we are supporting include traditional pulverized coal, waste coal and Integrated Gas Coal Conversion technology.

With over half of the States implementing renewable portfolio standards, we are providing licensing and engineering support to a number of wind power projects. Reflecting the breadth of

6

- •

- Greenhouse gases. There will be continuing pressure on the

United States to reduce greenhouse gas emissions across all segments of the economy. This will provide us opportunities to support clients in the areas of air emissions consulting, project

development, renewable energy permitting, and the development of sustainable business practices. The need to reduce greenhouse gas emissions represents a new starting point for businesses to "green"

their processes and make them more efficient and environmentally friendly.

- •

- Continued need for transaction support. Our ability to

evaluate environmental and regulatory risk in real property and business transfers continues to be one of our core strengths. We forecast a steady need for due diligence activities by public and

private equity investors, financial institutions, regulatory agencies, and property owners as properties and businesses change ownership.

- •

- Environmental compliance. Industrial and commercial

projects must comply with regulations covering, among other things, air quality, water quality, land use, wildlife, wetlands, cultural resources, and natural resource conservation. Many of these

requirements are effective independent of economic circumstances.

- •

- The pressing requirements to modernize our

infrastructure. Modernizing our national transportation and energy delivery systems continues to be a focus of both the public and the

private sectors. Investment in these areas will include attention to the related environmental impacts associated with such modernization.

- •

- Sustainability and Climate Change. The market for climate change related services is being driven domestically from many fronts, most of which are not regulatory in nature. We have seen demand for services emerge in the areas of carbon emission assessment and verification, alternate energy development, and public and private sector programs which are designed around energy conservation and other green initiatives. We believe our expertise in air modeling and measurement, renewable energy project licensing, project environmental impact assessment and project engineering, as well as program design and management, provides us an advantage in this emerging market.

our staff capabilities and experience we are participating in both land-based and offshore wind power developments. Services provided have broadened to include feasibility studies, environmental permitting, site civil engineering, electric transmission interconnect/substation design, construction management and transactional support involving the sale or purchase of existing generation assets. We have provided due diligence and best management practices consulting support with respect to energy assets to a number of leading financial institutions, equity firms and diversified energy companies.

In addition, other market factors are also creating opportunities in the following areas:

- •

- Mercury monitoring of air emissions as a function of emerging legislation.

- •

- Control technology requirements in the Clean Air Act, e.g., the Best Available Retrofit Technology requirements for

certain air emission sources.

- •

- Continued litigation over a variety of air issues such as facility compliance and operations or historic discharge

enforcement and toxic tort claims.

- •

- Indoor environmental exposures such as "sick building syndrome" and microbial issues (mold).

The primary demand for environmental assessment and remediation services is driven by the regulatory obligations of our clients at existing operating facilities and by the real estate transfer and redevelopment process. We expect our assessment and remediation services market to grow as more of our clients adopt newer, more aggressive environmental management strategies as part of evolving

7

corporate philosophies embracing sustainability and environmental accountability. These strategies require voluntary, accelerated assessment and remediation to lower costs and improve environmental conditions which meet increased societal and shareholder demands for better stewardship. While the market for this type of service has broadened due to increased availability of public-sector funded projects, the need for cleanup at affected sites in support of economic redevelopment opportunities has softened somewhat, due to the current conditions in the real estate market. Opportunities to support private sector development-related cleanup projects should expand once economic conditions in real estate and the associated transactional markets improve. We expect our assessment and remediation services market to continue to grow in support of the power generation industry as older facilities are retired or re-powered. Special services we offer are:

- •

- Exit Strategy. Our Exit Strategy program is one of the

most innovative and valuable services we offer our clients. We pioneered this program and created a new national market of environmental risk transfers for contaminated properties. We remain a

national market leader with over 100 sites under contract since inception. Traditionally our Exit Strategy offering has been especially attractive to clients in the following

situations:

- •

- Discontinued Operations. We assume responsibility for the

cleanup of contamination at closed or redundant facilities, allowing our clients to focus on their core business operations.

- •

- Bankruptcy. Debtors and the creditors are seeking the

highest possible value for saleable assets and relief from lingering environmental liabilities. By assuming those liabilities, we can help them achieve a responsible financial solution.

- •

- Acquisitions and Divestitures. We assume responsibility

for existing environmental cleanup liabilities which neither the buyer wants to assume nor the seller wants to retain.

- •

- Multi-Party Superfund Sites. By transferring

responsibility for the cleanup of Superfund sites from groups of potentially responsible parties to us, the cleanup schedule can be accelerated and the legal and administrative cost burden

substantially reduced.

- •

- Brownfield Real Estate Development. By assuming

responsibility for site cleanup and defining the related cost with certainty, our Exit Strategy program aids in the settlement of the commercial issues among interested parties, such as property

owners, lenders, developers, and municipalities, that often stall the redevelopment process.

- •

- RE Power. RE Power is a program where we, in conjunction with a decommissioning and demolition company, provide comprehensive dismantling, cleanup, liability transfer and asset optimization solutions to power and utility companies that elect to decommission and reposition their aging power plant assets. The goal of RE Power is to provide energy companies with a one-stop resource to gain maximum value for power plant assets within any constraints imposed by the power grid and the larger community. This can include safely removing plants from service through demolition and environmental cleanup, and potentially into a redevelopment phase, or preparing the existing power plant for re-powering with more economical fuel sources or more efficient generating equipment.

We offer a wide variety of services to our infrastructure clients primarily related to: (1) rehabilitation of overburdened and deteriorating infrastructure systems, (2) design and construction management associated with new infrastructure projects, and (3) management of risks related to security of public and private facilities. We have a strong geographic presence in the Northeast corridor of the United States as well as Texas, Louisiana and California. Infrastructure related services are

8

managed to recognize the importance of local market presence to maintain a diverse base of projects. The following is a listing of the general types of infrastructure services we offer:

- •

- Construction Management. We provide support to our

clients in the areas of program management, project management, construction engineering and inspection, plant inspections, construction management, estimating and scheduling.

- •

- Transportation. We provide planning, design and

construction management services in support of work on roads, highways, bridges and aviation facilities. In addition to performing basic design engineering, we also incorporate activities associated

with completing environmental studies, marine engineering, seismic analysis, and traffic engineering.

- •

- General Civil Engineering Services, Municipal and Land Development

Engineering. We provide land development support for commercial and residential real estate development projects by providing master

planning, traffic studies, storm water design and management, utility design, and site engineering. We also can provide the basic engineering needs of small municipalities, and our civil engineering

expertise is utilized on projects such as the planning, design and construction management of potable water and wastewater treatment systems; master drainage planning; street, roadway and site

drainage; dam analysis and design; and master drainage planning.

- •

- Geotechnical and Materials Engineering. We provide

subsurface exploration, laboratory testing, geotechnical assessments, seismic engineering and quality assurance testing.

- •

- Hydraulics and Hydrological Studies. We provide aquifer

tests, ground water modeling and yield analysis, scour and erosion studies, design and analysis of storage and distribution systems, Federal Emergency Management Agency studies and watershed modeling.

- •

- Security. We provide vulnerability assessments,

engineering and structural improvements for public and private infrastructure facilities, design and implementation of security and surveillance systems, blast resistance design, disaster recovery

planning, and force protection analysis. Our market emphasis has shifted from providing these services in commercial buildings to a focus upon public and quasi-public infrastructure and energy-related

facilities such as transit systems, utility companies and ports.

- •

- Geographic Information Systems & Mapping. We provide, among other services, data modeling, terrain analysis, shoreline management analysis, total station mapping and resource mapping.

We believe that the long-term market for our infrastructure services will be stable and driven by population growth in certain geographic regions, continued aging and obsolescence of existing infrastructure, capacity shortfalls, and Federal stimulus funding for state and municipal projects. Spending by both private and government clients generally declined in recent years, reflecting economic conditions, and these conditions have not materially improved in the current calendar year. In addition, legislation regarding long term funding for Federal transportation projects still remains unresolved at this time. We expect this trend to continue in the near term with the exception being in the area of construction and construction management for Stimulus Bill-related projects and security-related initiatives. Of particular note is the continued lack of design-related projects in the "pipeline" for both public and private clients. Given the need to rebuild and modernize our aging national infrastructure, however, we do expect increased spending on public infrastructure programs over the intermediate and long term. The timing and extent of recovery in the private sector is, however, more uncertain in the short and mid-term. The pace of spending on private infrastructure projects has diminished and, as a result, during the past fiscal year we have experienced client initiated delays and/or cancellation of some assignments. We are focusing our activities where the pace of infrastructure development has remained somewhat robust, and therefore continue to be optimistic regarding the prospects for this market.

9

No single client accounted for 10% or more of our NSR during fiscal years ended 2010, 2009 and 2008.

Representative clients during the past five years include:

AES Enterprises |

Goodyear Tire and Rubber Company |

SPX Corporation |

|||

AIMCO, Inc. |

Hoffman La Roche, Inc. |

Transwestern Pipeline Company, LLC |

|||

Alcoa |

International Paper |

Waste Management |

|||

Alyeska Pipeline Service Co. |

J-Power |

State Transportation/Authorities; |

|||

ASARCO |

Kinder Morgan |

• California |

|||

BNSF |

LS Power |

• Massachusetts |

|||

British Petroleum (ARCO/Amoco) |

Lockheed Martin |

• New Jersey |

|||

Central Maine Power Company |

Lower Manhattan |

• New York |

|||

Competitive Power Ventures |

Development Corporation |

• Pennsylvania |

|||

Connecticut Resources Recovery |

Magellan Midstream Partners |

• Texas |

|||

Authority |

Mirant |

• West Virginia |

|||

Conoco Phillips |

National Grid |

• Louisiana |

|||

Consolidated Edison |

New York State Energy Research and |

U.S. Government: |

|||

Constellation Energy |

Development Authority |

• Environmental Protection Agency |

|||

Covanta |

Northeast Utilities |

• Department of Defense |

|||

Duke Energy |

NRG |

• Federal Aviation Administration |

|||

El Paso Energy |

Orange County Transportation Authority |

• General Services Administration |

|||

Entergy |

Pfizer |

• Minerals Management Service |

|||

ExxonMobil |

PG&E Corporation |

||||

Florida Gas Transmission |

Sempra Energy |

||||

Florida Power and Light |

Spectra Energy |

||||

The markets for many of our services are highly competitive. There are numerous engineering and consulting firms and other organizations that offer many of the same services offered by us. These firms range in size from small local firms to large national firms that have substantially greater resources than we do. Competitive factors include reputation, performance, price, geographic location and availability of skilled technical personnel. As a mid-size firm, we compete with both the large international firms and the small niche or geographically focused firms.

Despite the competitive nature of our markets, the majority of our work comes from repeat orders from long-term clients, especially where we are one of the leading service providers in the markets we address. For example, we believe that we are one of the top providers of licensing services for large energy projects. Further, we believe we are the market leader in the complete outsourcing of site remediation services through our Exit Strategy program. By continuing to stay in front of emerging trends in our markets we believe our competitive position will remain strong.

As of June 30, 2010, our contract backlog based on gross revenue was approximately $361 million, compared to approximately $387 million as of June 30, 2009. Our contract backlog based on NSR was approximately $222 million as of June 30, 2010, compared to approximately $247 million as of June 30, 2009. The decline in backlog can be most directly attributed to the completion of several large EPC projects in our Energy operating segment as well as the reduction in project awards attributable to the economic slowdown. Approximately 60% of backlog is typically completed in one year. In addition to this net contract backlog, we hold open order contracts from various clients and government agencies. As work under these contracts is authorized and funded, we include this portion in our net contract backlog. While most contracts contain cancellation provisions, we are unaware of any material work included in backlog that will be canceled or delayed.

10

As of June 30, 2010, we had approximately 2,100 full- and part-time employees. Approximately 85% of these employees are engaged in performing professional services for clients. Many of these employees have advanced degrees. Our professional staff includes program managers, professional engineers and scientists, construction specialists, computer programmers, systems analysts, attorneys and others with degrees and experience that enable us to provide a diverse range of services. Other employees are engaged in executive, administrative and support activities. We consider the relationships with our employees to be favorable.

Contracts with the United States Government and Agencies of State and Local Governments

We have contracts with agencies of the United States government and various state agencies that are subject to examination and renegotiation. We believe that adjustments resulting from such examination or renegotiation proceedings, if any, will not have a material impact on our operating results, financial position or cash flows.

Our businesses are subject to various rules and regulations at the federal, state and local government levels. We believe that we are in substantial compliance with these rules and regulations. We have the appropriate licenses to bid and perform work in the locations in which we operate. We have not experienced any significant limitations on our business as a result of regulatory requirements. We do not believe any currently proposed changes in law or anticipated changes in regulatory practices would limit bidding on future projects.

We have a number of trademarks, copyrights and licenses. None of these are considered material to our business as a whole.

Environmental and Other Considerations

We do not believe that our own compliance with federal, state and local laws and regulations relating to the protection of the environment will have any material effect on our capital expenditures, earnings or competitive position.

11

The risk factors listed below, in addition to those described elsewhere in this report, could materially and adversely affect our business, financial condition, results of operations or cash flows.

We incurred significant losses in fiscal years 2010, 2009, and 2008, and may incur such losses in the future. If we continue to incur significant losses or are unable to generate sufficient working capital from our operations or our revolving credit facility, we may have to seek additional external financing.

As reflected in our consolidated financial statements, we incurred net losses applicable to our common shareholders of $22.9 million, $24.1 million and $109.1 million in fiscal years 2010, 2009 and 2008, respectively. Although a main factor in our losses has been non-cash goodwill and intangible asset impairment charges, we are continuing to take actions to be profitable, but if we are unable to improve our operating performance, we may incur additional losses. We depend on our core businesses to generate profits and cash flow to fund our working capital growth. Although the services that we provide are spread across a variety of industries, disruptions such as a general economic downturn or higher interest rates could negatively affect the demand for our services across a variety of industries which could adversely affect our ability to generate profits and cash flows.

We finance our operations through cash generated by operating activities and borrowings under our revolving credit facility with Wells Fargo Capital Finance. During fiscal year 2009 we completed a preferred stock offering with gross proceeds of $15.5 million. While we have rarely used the credit facility since the preferred stock offering, we are dependent on this facility for any short term liquidity needs when available cash and cash equivalents and cash provided by operations are not adequate to support working capital requirements. The credit facility contains covenants which, among other things, require us to maintain minimum levels of earnings before interest, taxes, depreciation, and amortization as defined in the credit agreement ("EBITDA"), maintain a minimum fixed charge coverage ratio, maintain a minimum level of backlog, and limit capital expenditures.

We believe that existing cash resources, cash forecasted to be generated from operations and availability under our credit facility are adequate to meet our requirements for the foreseeable future. The current uncertain state of the economy and the possibility that economic conditions could continue to be uncertain or deteriorate may affect businesses such as ours in a number of ways. While management cannot directly measure it, variability in the economy and any corollary impact on the availability of credit could affect the ability of our customers and vendors to obtain financing for significant purchases and operations and could result in a decrease in their business with us which could adversely affect our ability to generate profits and cash flows. We are unable to predict the likely duration of the current economic uncertainty and its potential impact on our clients. Management will continue to closely monitor the credit markets and our financial performance.

If we must write off a significant amount of intangible assets or long-lived assets, our earnings will be negatively impacted.

Goodwill was approximately $14.9 million as of June 30, 2010. We also had other identifiable intangible assets of $0.6 million, net of accumulated amortization, as of June 30, 2010. Goodwill and identifiable intangible assets are assessed for impairment at least annually or whenever events or changes in circumstances indicate that the carrying value of the assets may not be recoverable. We have recorded goodwill and intangible asset impairment charges of $20.2 million, $21.4 million and $77.3 million in the fiscal years 2010, 2009 and 2008, respectively. A decline in the estimated future cash flows of our reporting units, declines in market multiples of comparable companies and other

12

factors may result in additional impairments of goodwill or other assets which would negatively impact our earnings.

We are and will continue to be involved in litigation. Legal defense and settlement expenses can have a material adverse impact on our operating results.

We have been, and likely will be, named as a defendant in legal actions claiming damages and other relief in connection with engineering and construction projects and other matters. These are typically actions that arise in the normal course of business, including employment-related claims, contractual disputes, professional liability, or claims for personal injury or property damage. We have substantial deductibles on several of our insurance policies, and not all claims are insured. In addition, we have also incurred legal defense and settlement expenses related to prior acquisitions. Accordingly, defense costs, settlements and potential damage awards may have a material adverse effect on our business, operating results, financial position and cash flows in future periods.

Subcontractor performance and pricing could expose us to loss of reputation and additional financial or performance obligations that could result in reduced profits or losses.

We often hire subcontractors for our projects. The success of these projects depends, in varying degrees, on the satisfactory performance of our subcontractors and our ability to successfully manage subcontractor costs and pass them through to our customers. If our subcontractors do not meet their obligations or we are unable to manage or pass through costs, we may be unable to profitably perform and deliver our contracted services. Under these circumstances we may be required to make additional investments and expend additional resources to ensure the adequate performance and delivery of the contracted services. These additional obligations have resulted in reduced profits or, in some cases, significant losses for us with respect to certain projects. In addition, the inability of our subcontractors to adequately perform or our inability to manage subcontractor costs on certain projects could hurt our competitive reputation and ability to obtain future projects.

Our operations could require us to utilize large sums of working capital, sometimes on short notice and sometimes without the ability to recover the expenditures.

Circumstances or events which could create large cash outflows include losses resulting from fixed-price contracts, remediation of environmental liabilities, legal expenses and settlements, project completion delays, failure of clients to pay, income tax assessments including payments that may arise pursuant to the ongoing fiscal year 2003 - 2008 Internal Revenue Service ("IRS") audit if not resolved successfully, and professional liability claims, among others. We cannot provide assurance that we will have sufficient liquidity or the credit capacity to meet all of our cash needs if we encounter significant working capital requirements as a result of these or other factors.

Our services expose us to significant risks of liability and it may be difficult or more costly to obtain or maintain adequate insurance coverage.

Our services involve significant risks that may substantially exceed the fees we derive from our services. Our business activities expose us to potential liability for professional negligence, personal injury and property damage among other things. We cannot always predict the magnitude of such potential liabilities. In addition, our ability to perform certain services is dependent on the availability of adequate insurance.

We obtain insurance from insurance companies to cover a portion of our potential risks and liabilities subject to specified policy limits, deductibles or coinsurance. It is possible that we may not be able to obtain adequate insurance to meet our needs, may have to pay an excessive amount for the insurance coverage we want, or may not be able to acquire any insurance for certain types of business

13

risks. As a result of the recent events in the financial markets, we face additional risks due to the continuing uncertainty and disruption in those markets. Much of our commercial insurance is underwritten by the regulated insurance subsidiaries of Chartis (formerly the American International Group). Chartis has also underwritten almost all of the cost cap and related insurance purchased by Exit Strategy clients which share some specific characteristics that present additional risk. The Exit Strategy related policies all tend to be long term; many are ten years or more. Some policies also serve to satisfy state and federal financial assurance requirements for certain projects, and without these policies alternative financial assurance arrangements for these projects would need to be arranged. Additionally, most of our Exit Strategy projects require us to perform the work in the event insurance limits are exhausted, directly exposing us to financial risks.

Our failure to properly manage projects may result in additional costs or claims.

Our engagements involve a variety of projects, some of which are large-scale and complex. Our performance on projects depends in large part upon our ability to manage the relationship with our clients and to effectively manage the project and deploy appropriate resources, including third-party contractors and our own personnel, in a timely manner. If we miscalculate, or fail to properly manage, the resources or time we need to complete a project with capped or fixed fees, or the resources or time we need to meet contractual obligations, our operating results could be adversely affected. Furthermore, any defects, errors or failures to meet our clients' expectations could result in claims against us.

Our use of the percentage-of-completion method of accounting could result in reduction or reversal of previously recorded revenue and profits.

We account for a significant portion of our contracts on the percentage-of-completion method of accounting. Generally, our use of this method results in recognition of revenue and profit ratably over the life of the contract based on the proportion of costs incurred to date to total costs expected to be incurred. The effect of revisions to revenue and estimated costs, including the achievement of award and other fees, is recorded when the amounts are known and can be reasonably estimated. The uncertainties inherent in the estimating process make it possible for actual costs to vary from estimates, or estimates to change, resulting in reductions or reversals of previously recorded revenue and profit. Such differences could be material.

Our business and operating results could be adversely affected by our inability to accurately estimate the overall risks, revenue or costs on a contract.

We generally enter into three principal types of contracts with our clients: fixed-price, time-and-materials, and cost-plus. Under our fixed-price contracts, we receive a fixed price irrespective of the actual costs we incur and, consequently, we are exposed to a number of risks. These risks include: underestimation of costs, problems with new technologies, unforeseen costs or difficulties, delays, price increases for materials, poor project management or quality problems, and economic and other changes that may occur during the contract period. Under our time-and-materials contracts, we are paid for labor at negotiated hourly billing rates and for other expenses. Profitability on these contracts is driven by billable headcount and cost control. Many of our time-and-materials contracts are subject to maximum contract values and, accordingly, revenue relating to these contracts is recognized as if these contracts were fixed-price contracts. Under our cost-plus contracts, some of which are subject to contract ceiling amounts, we are reimbursed for allowable costs and fees which may be fixed or performance-based. If our costs exceed the contract ceiling or are not allowable under the provisions of the contract or any applicable regulations, we may not be able to obtain reimbursement for all such costs. Accounting for a fixed-price contract requires judgments relative to assessing the contract's estimated risks, revenue and estimated costs as well as technical issues. Due to the size and nature of

14

many of our contracts, the estimation of overall risk, revenue and cost at completion is complex and subject to many variables. Changes in underlying assumptions, circumstances or estimates may adversely affect future period financial performance. If we are unable to accurately estimate the overall revenue or costs on a contract, we may experience a lower profit or incur a loss on the contract.

Our backlog is subject to cancellation and unexpected adjustments and is an uncertain indicator of future operating results.

Our contract backlog based on NSR as of June 30, 2010 was approximately $222 million. We cannot guarantee that the NSR projected in our backlog will be realized or, if realized, will result in profits. In addition, project cancellations or scope adjustments may occur from time to time with respect to contracts reflected in our backlog. These types of backlog reductions could adversely affect our revenue and margins. Accordingly, our backlog as of any particular date is an uncertain indicator of our future earnings.

We are dependent on continued regulatory enforcement.

While we increasingly pursue economically driven markets, our business is materially dependent on the continued enforcement by federal, state and local governments of various environmental regulations. Changes in environmental standards or enforcement could adversely impact our business.

Changes in existing environmental laws, regulations and programs could reduce demand for our environmental services which could cause our revenue to decline.

A significant amount of our business is generated either directly or indirectly as a result of existing federal and state laws, regulations and programs related to pollution and environmental protection. Accordingly, a relaxation or repeal of these laws and regulations, or changes in governmental policies regarding the funding, implementation or enforcement of these programs, could result in a decline in demand for environmental services that may have a material adverse effect on our revenue.

We operate in highly competitive industries.

The markets for many of our services are highly competitive. There are numerous professional architectural, engineering and consulting firms and other organizations which offer many of the services offered by us. We compete with many companies, some of which have greater resources. Competitive factors include reputation, performance, price, geographic location and availability of technically skilled personnel. In addition, many clients use in-house staff to perform the same types of services we do.

We are materially dependent on contracts with federal, state and local governments.

We estimate that contracts with agencies of the United States government and various state and local governments represent approximately 25% of our NSR in fiscal year 2010. Therefore, we are materially dependent on various contracts with such governmental agencies. Companies engaged in government contracting are subject to certain unique business risks. Among these risks are dependence on appropriations and administrative allotment of funds as well as changing policies and regulations. These contracts may also be subject to renegotiation of profits or termination at the option of the government. The stability and continuity of that portion of our business depends on the periodic exercise by the government of contract renewal options, our continued ability to negotiate favorable terms and the continued awarding of task orders to us.

15

The value of our equity securities could continue to be volatile.

Over time our common stock has experienced substantial price volatility. In addition, the stock market has experienced price and volume fluctuations that have affected the market price of many companies that have often been unrelated to the operating performance of these companies. The overall market and the price characteristics of our common stock may continue to fluctuate greatly. The trading price of our common stock may be significantly affected by various factors, including:

- •

- Our financial results, including revenue, profit, days sales outstanding, backlog, and other measures of financial

performance or financial condition;

- •

- Announcements by us or our competitors of significant events, including acquisitions;

- •

- Threatened or pending litigation;

- •

- Changes in investors' and analysts' perceptions of our business or any of our competitors' businesses;

- •

- Investors' and analysts' assessments of reports prepared or conclusions reached by third parties;

- •

- Changes in legislation;

- •

- Broader market fluctuations; and

- •

- General economic or political conditions.

Additionally, volatility or a lack of positive performance in our stock price may adversely affect our ability to retain or attract key employees. Many of these key employees are granted stock options and restricted stock as an element of compensation, the value of which is dependent on our stock price.

We may experience adverse impacts on our results of operations as a result of adopting new accounting standards or interpretations.

Our adoption of, and compliance with, changes in accounting rules, including new accounting rules and interpretations, could adversely affect our operating results or cause unanticipated fluctuations in our operating results.

We are highly dependent on key personnel.

The success of our business depends on our ability to attract and retain qualified employees. We need talented and experienced personnel in a number of areas to support our core business activities. An inability to attract and retain sufficient qualified personnel could harm our business. Turnover among certain critical staff could have a material adverse effect on our ability to implement our strategies and on our results of operations. There is currently a shortage of technical and engineering personnel.

If we fail to maintain an effective system of internal controls, we may not be able to accurately report our financial results or prevent fraud. As a result, investors could lose confidence in our financial reporting, which would harm our business and the trading price of our stock.

Effective internal controls are necessary for us to provide reliable financial reports and prevent fraud. If we cannot provide reliable financial reports or prevent fraud, our operating results could be harmed. We devote significant attention to establishing and maintaining effective internal controls. Implementing changes to our internal controls has required compliance training of our directors, officers and employees and has entailed substantial costs in order to modify our existing accounting systems. Although these measures are designed to do so, we cannot be certain that such measures and

16

future measures will guarantee that we will successfully maintain adequate controls over our financial reporting processes and related reporting requirements. For example, in the past we have had material weaknesses, including a material weakness relating to the policies and procedures relating to the development, documentation and review of contract values and estimates of cost at completion, which we have remediated. However, internal controls that are found to be not operating effectively could affect our operating results or cause us to fail to meet our reporting obligations and could result in a breach of a covenant in our revolving credit facility in future periods. Ineffective internal controls could also cause investors to lose confidence in our reported financial information, which could have a negative effect on the market price of our stock.

Item 1B. Unresolved Staff Comments

None.

We provide our services through a network of approximately 85 offices located nationwide. We lease approximately 630,000 square feet of office and commercial space to support these operations. In addition, a subsidiary of ours owns a 26,000 square foot office/warehouse building in Austin, Texas. This property is subject to a deed of trust in favor of the lenders under our principal credit facility. All properties are adequately maintained and are suitable and adequate for the business activities conducted therein. In connection with the performance of certain Exit Strategy or real estate projects, some of our subsidiaries have taken title to sites on which environmental remediation activities are being performed.

See Note 17—Commitments and Contingencies of the Notes to Financial Statements (Part II, Item 8 of this Form 10-K) for information regarding legal proceedings in which we are involved.

17

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock is traded on the New York Stock Exchange ("NYSE") under the symbol "TRR." The following table sets forth the high and low per share prices for the common stock for fiscal years 2010 and 2009 as reported on the NYSE:

| |

Fiscal 2010 | Fiscal 2009 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

High | Low | High | Low | |||||||||

First Quarter |

$ | 4.97 | $ | 3.50 | $ | 4.46 | $ | 2.18 | |||||

Second Quarter |

3.86 | 2.55 | 3.28 | 1.16 | |||||||||

Third Quarter |

3.11 | 2.57 | 3.63 | 1.59 | |||||||||

Fourth Quarter |

3.56 | 2.66 | 4.45 | 2.32 | |||||||||

As of July 15, 2010, there were 276 shareholders of record and, as of that date, we estimate there were approximately 1,768 beneficial owners holding our common stock in nominee or "street" name.

To date we have not paid any cash dividends on our common stock, and the payment of dividends in the future will be subject to financial condition, capital requirements and earnings. Future earnings are expected to be used for expansion of our operations, and cash dividends are not currently anticipated. The terms of our credit agreement also prohibit the payment of cash dividends.

18

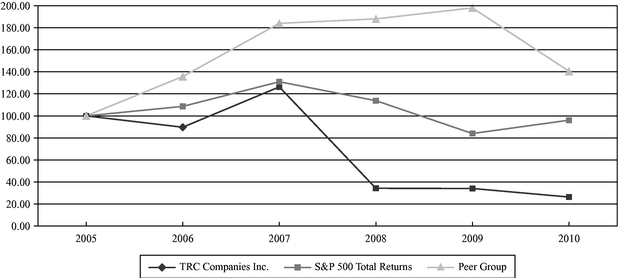

Comparison of Five-Year Cumulative Total Return Among TRC, S&P 500 Total Return Index and Peer Companies

The annual changes for the five-year period shown in the graph below are based upon the assumption (as required by SEC rules) that $100 had been invested in our Common Stock on June 30, 2005. The figures presented assume that all dividends, if any, paid over the performance periods were reinvested.

Comparison

of 5 Year Cumulative Total Return

Assumes Initial Investment of $100

June 2010

Data and graph provided by Zacks Investment Research, Inc. Copyright© 2010, Standard & Poor's, a division of The McGraw-Hill Companies, Inc. All rights reserved.

| |

Year Ended June 30, | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2005 | 2006 | 2007 | 2008 | 2009 | 2010 | |||||||||||||

TRC |

$ | 100 | $ | 90 | $ | 126 | $ | 34 | $ | 34 | $ | 26 | |||||||

S&P 500 Index |

100 | 109 | 131 | 114 | 84 | 96 | |||||||||||||

Peer Group |

100 | 136 | 184 | 188 | 198 | 141 | |||||||||||||

The companies included in the peer group are: Ecology & Environment, Inc.; ENGlobal Corp.; Tetra Tech, Inc.; Versar, Inc.; and, VSE Corp.

19

Item 6. Selected Financial Data

The following table provides summarized information with respect to our operations and financial position. The data set forth below should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our financial statements and the notes thereto.

Statements of Operations Data, for the years ended June 30,

|

2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

(in thousands, except per share data) |

||||||||||||||||

Gross revenue |

$ | 330,575 | $ | 432,517 | $ | 465,079 | $ | 441,643 | $ | 396,091 | |||||||

Less subcontractor costs and other direct reimbursable charges |

100,476 | 177,713 | 196,870 | 185,735 | 158,111 | ||||||||||||

Net service revenue |

230,099 | 254,804 | 268,209 | 255,908 | 237,980 | ||||||||||||

Interest income from contractual arrangements |

596 | 1,859 | 3,944 | 4,747 | 4,054 | ||||||||||||

Insurance recoverables and other income |

8,844 | 19,539 | 6,123 | 4,170 | 1,053 | ||||||||||||

Operating costs and expenses: |

|||||||||||||||||

Cost of services(1) |

203,221 | 227,217 | 241,647 | 231,025 | 228,556 | ||||||||||||

General and administrative expenses(1) |

27,128 | 32,936 | 40,077 | 23,969 | 24,350 | ||||||||||||

Provision for doubtful accounts |

2,344 | 3,952 | 3,708 | 1,318 | 7,971 | ||||||||||||

Goodwill and intangible asset write-offs(2) |

20,249 | 21,438 | 77,267 | — | 2,170 | ||||||||||||

Depreciation and amortization(3) |

8,049 | 7,322 | 8,051 | 8,311 | 6,925 | ||||||||||||

Total operating costs and expenses |

260,991 | 292,865 | 370,750 | 264,623 | 269,972 | ||||||||||||

Operating (loss) income |

(21,452 | ) | (16,663 | ) | (92,474 | ) | 202 | (26,885 | ) | ||||||||

Interest expense |

(1,003 | ) | (2,925 | ) | (3,936 | ) | (4,359 | ) | (4,545 | ) | |||||||

Gain on extinguishment of debt(4) |

1,716 | — | — | — | — | ||||||||||||

Registration penalties(5) |

— | — | — | (600 | ) | — | |||||||||||

Loss from continuing operations before taxes and equity in (losses) earnings |

(20,739 | ) | (19,588 | ) | (96,410 | ) | (4,757 | ) | (31,430 | ) | |||||||

Federal and state income tax (benefit) provision(6) |

(4,210 | ) | 3,871 | 12,296 | (1,337 | ) | (10,488 | ) | |||||||||

Loss from continuing operations before equity in (losses) earnings |

(16,529 | ) | (23,459 | ) | (108,706 | ) | (3,420 | ) | (20,942 | ) | |||||||

Equity in (losses) earnings from unconsolidated affiliates, net of taxes(7) |

(45 | ) | (449 | ) | (505 | ) | (161 | ) | 9 | ||||||||

Loss from continuing operations |

(16,574 | ) | (23,908 | ) | (109,211 | ) | (3,581 | ) | (20,933 | ) | |||||||

Discontinued operations, net of taxes(8) |

— | — | — | (77 | ) | (2,914 | ) | ||||||||||

Net loss |

(16,574 | ) | (23,908 | ) | (109,211 | ) | (3,658 | ) | (23,847 | ) | |||||||

Net loss attributable to noncontrolling interest |

(125 | ) | — | (62 | ) | (24 | ) | — | |||||||||

Net loss applicable to TRC Companies, Inc. |

(16,449 | ) | (23,908 | ) | (109,149 | ) | (3,634 | ) | (23,847 | ) | |||||||

Dividends and accretion charges on preferred stock(9) |

6,431 | 215 | — | 2,233 | 751 | ||||||||||||

Net loss applicable to TRC Companies, Inc.'s common shareholders |

$ | (22,880 | ) | $ | (24,123 | ) | $ | (109,149 | ) | $ | (5,867 | ) | $ | (24,598 | ) | ||

Basic and diluted loss per common share: |

|||||||||||||||||

Loss from continuing operations |

$ | (1.17 | ) | $ | (1.25 | ) | $ | (5.84 | ) | $ | (0.33 | ) | $ | (1.43 | ) | ||

Discontinued operations, net of taxes |

— | — | — | — | (0.19 | ) | |||||||||||

|

$ | (1.17 | ) | $ | (1.25 | ) | $ | (5.84 | ) | $ | (0.33 | ) | $ | (1.62 | ) | ||

Basic and diluted weighted average common shares outstanding |

19,548 | 19,272 | 18,700 | 17,563 | 15,168 | ||||||||||||

Cash dividends declared per common share |

— | — | — | — | — | ||||||||||||

Balance Sheet Data at June 30: |

|||||||||||||||||

Total assets |

$ | 287,795 | $ | 336,896 | $ | 397,319 | $ | 485,982 | $ | 485,403 | |||||||

Long-term debt, including current portion |

9,444 | 12,501 | 39,310 | 42,670 | 40,453 | ||||||||||||

Preferred stock |

8,239 | 1,808 | — | — | 15,000 | ||||||||||||

Shareholders' equity |

27,953 | 48,623 | 57,671 | 161,729 | 145,156 | ||||||||||||

- (1)

- Concurrent with the implementation of our new enterprise resource and planning system in fiscal year 2007, our processes and costs relating to financial, information technology and administrative functions were realigned and are now incurred by corporate functions. Beginning in fiscal year 2008, the related costs are classified as general and administrative expenses.

20

Previously, these processes and related expenses were performed by individuals in field locations and were included in cost of services. Management estimates that $5.6 million of expenses were included in general and administrative expenses in fiscal year 2008 that in the previous year were included in costs of services.

- (2)

- During

fiscal year 2010, we recorded an impairment charge of $20.2 million related to goodwill. During fiscal year 2009, we recorded impairment

charges of $19.3 million related to goodwill and $2.1 million related to certain customer relationships intangible assets. During fiscal year 2008, we recorded impairment charges of

$76.7 million related to goodwill and $0.6 million related to certain customer relationships intangible assets. During fiscal year 2006, we recorded an impairment charge of

$2.2 million related to trade-name intangible assets.

- (3)

- During

fiscal year 2010, we recorded amortization expense of $1.9 million of which $1.6 million was due to the acceleration of amortization

expense relating to certain customer relationship intangible assets.

- (4)

- During

fiscal year 2010, we recorded a $1.7 million gain on extinguishment of debt in connection with the dissolution of

Co-Energy LLC, a consolidated entity.

- (5)

- The

$0.6 million penalty related to our failure to obtain an effective registration statement related to our fiscal year 2006 private placement.

- (6)

- During

fiscal year 2010, we recorded a net tax benefit of $4.2 million primarily due to: (i) the Worker, Homeownership, and Business

Assistance Act of 2009 which amended I.R.C. §172(b)(1)(H), which allows taxpayers to elect to carry back an applicable net operating loss ("NOL") for a period of 3, 4, or

5 years, to offset taxable income in those preceding years enabling us to carry back our fiscal year 2008 NOL for a tax benefit of $2.8 million, which amount was collected in January

2010, and (ii) the re-assessment of our uncertain tax positions based on communications with the IRS relating to our examination including the impact of the NOL law change. The

valuation allowance changed during fiscal years 2010 and 2009 to fully reserve for additional deferred tax assets by ($2.3) million and $1.0 million, respectively. During fiscal year 2008, we

determined that it was more likely than not that our deferred tax assets would not be realized as a result of insufficient expected future taxable income or reversals of existing temporary differences

and recorded a deferred tax provision of $12.1 million which included a valuation allowance to fully reserve for our deferred tax assets as of such date.

- (7)

- The

fiscal years 2009, 2008 and 2007 equity in losses from unconsolidated affiliates includes impairment charges of $0.4 million, $0.5 million

and $0.4 million, respectively.

- (8)

- We

sold our wholly-owned subsidiaries Omni and Bellatrix in fiscal year 2007 and PacLand in fiscal year 2006.

- (9)

- We incurred a charge of approximately $6.4 million and $0.2 million in fiscal years 2010 and 2009, respectively, related to the accretion of the beneficial conversion charge recorded on the preferred stock issued in June 2009. In December 2006, preferred stock which was issued in fiscal 2001 was exchanged for approximately 1.1 million shares of common stock, resulting in a charge of approximately $2.0 million related to the induced conversion of the preferred stock. We incurred a charge of approximately $0.8 million in fiscal year 2006 related to dividend and accretion charges on preferred stock.

21

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

You should read the following discussion of our results of operations and financial condition in conjunction with our consolidated financial statements and related notes included elsewhere in this Annual Report on Form 10-K. This discussion contains forward-looking statements that are based upon current expectations and assumptions that are subject to risks and uncertainties. Actual results and the timing of certain events may differ materially from those projected in such forward-looking statements due to a number of factors, including those discussed in the section entitled "Forward-Looking Statements" on page 3.

OVERVIEW

We are a firm that provides engineering, consulting, and construction management services. Our project teams assist our commercial, industrial and government clients implement environmental, energy and infrastructure projects from initial concept to delivery and operation. We provide our services to commercial organizations and governmental agencies almost entirely in the United States of America.

We derive our revenue from fees for professional and technical services. As a service company, we are more labor-intensive than capital-intensive. Our revenue is driven by our ability to attract and retain qualified and productive employees, identify business opportunities, secure new and renew existing client contracts, provide outstanding service to our clients and execute projects successfully. Our income or loss from operations is derived from our ability to generate revenue and collect cash under our contracts in excess of our direct costs, subcontractor costs, other contract costs, and general and administrative ("G&A") expenses.

The following table presents the approximate percentage of net service revenue ("NSR") by contract type:

| |

Fiscal Year | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2009 | 2008 | |||||||

Time-and-materials |

58 | % | 54 | % | 59 | % | ||||

Fixed-price |

41 | % | 44 | % | 37 | % | ||||

Cost-plus |

1 | % | 2 | % | 4 | % | ||||

In the course of providing our services, we routinely subcontract services. Generally these subcontractor costs are passed through to our clients and, in accordance with accounting principles generally accepted in the United States of America ("U.S. GAAP") and consistent with industry practice, are included in gross revenue. Because subcontractor services can change significantly from project to project, changes in gross revenue may not be indicative of business trends. Accordingly, we also report NSR, which is gross revenue less the cost of subcontractor services and other direct reimbursable costs, and our discussion and analysis of financial condition and results of operations uses NSR as a point of reference.

Our cost of services ("COS") includes professional compensation and related benefits together with certain direct and indirect overhead costs such as rents, utilities and travel. Professional compensation represents the majority of these costs. Our G&A expenses are comprised primarily of our corporate headquarters costs related to corporate executive management, finance, accounting, information technology, administration and legal. These costs are generally unrelated to specific client projects and can vary as expenses are incurred to support corporate activities and initiatives.

22

Our revenue, expenses and operating results may fluctuate significantly from year to year as a result of numerous factors, including:

- •

- Unanticipated changes in contract performance that may affect profitability, particularly with contracts that are

fixed-price or have funding limits;

- •

- Seasonality of the spending cycle, notably for state and local government entities, and the spending patterns of our

commercial sector clients;

- •

- Budget constraints experienced by our federal, state and local government clients;

- •

- Divestitures or discontinuance of operating units;

- •

- Employee hiring, utilization and turnover rates;

- •

- The number and significance of client contracts commenced and completed during the period;

- •

- Creditworthiness and solvency of clients;

- •

- The ability of our clients to terminate contracts without penalties;

- •

- Delays incurred in connection with contracts;

- •

- The size, scope and payment terms of contracts;

- •

- Contract negotiations on change orders and collection of related accounts receivable;

- •

- The timing of expenses incurred for corporate initiatives;

- •

- Competition;

- •

- Litigation;

- •

- Changes in accounting rules;

- •

- The credit markets and their effects on our customers; and

- •

- General economic or political conditions.

Divestitures

In June 2010 we sold our 50% ownership position in Environmental Restoration, LLC, an unconsolidated affiliate formed to develop a habitat mitigation bank. We received cash payments of $25 thousand and a $275 thousand five-year promissory note. Profit on the transaction was deferred as the buyer's initial financial commitment was insufficient to provide economic substance to the transaction. As a result, the profit will be recognized under the installment method, which recognizes profit as collections of principal are received.

In fiscal year 2007 we sold our 50% ownership position in Metuchen Realty Acquisition, LLC, an unconsolidated affiliate. We received cash payments of $3.2 million, and the transaction resulted in a $17 thousand loss during fiscal year 2008.

Operating Segments

During fiscal year 2009 our accounting system was configured to provide revenue and earnings information that allowed us to initiate reporting to our chief operating decision maker ("CODM") under three operating segments. Management established these operating segments based upon the type of project, the client and market to which those projects are delivered, the different marketing strategies associated with the services provided and the specialized needs of the respective clients. Effective in the first quarter of fiscal year 2010, we made certain changes to our operating segments in our continuing efforts to align businesses around markets and customers. Operating segment

23

information for all periods presented has been reclassified to reflect the new operating segment structure. The operating segments are as follows:

Energy: The Energy operating segment provides services to a range of clients including energy companies, utilities, other commercial entities, and state and federal governments. Our services include program management, engineer/procure/construct projects, design, and consulting. Our typical projects involve upgrade and new construction for electrical transmission and distribution systems, energy efficiency program design and management, and alternative energy development. This operating segment also provides services to support energy savings projects for state government entities and end users.