Attached files

Table of Contents

As filed with the Securities and Exchange Commission on September 10, 2010

Registration No. 333-168439

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

COMPLETE GENOMICS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 8731 | 20-3226545 | ||||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) | ||||

2071 Stierlin Court, Mountain View, CA 94043

(650) 943-2800

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Clifford A. Reid, Ph.D.

President and Chief Executive Officer

Complete Genomics, Inc.

2071 Stierlin Court

Mountain View, CA 94043

(650) 943-2800

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Alan C. Mendelson Gregory Chin Latham & Watkins LLP 140 Scott Drive Menlo Park, California 94025-1008 Telephone: (650) 328-4600 Facsimile: (650) 463-2600 |

Donald J. Murray Dewey & LeBoeuf LLP 1301 Avenue of the Americas New York, New York 10019-6092 Telephone: (212) 259-8000 Facsimile: (212) 259-6333 | |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer x (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, September 10, 2010

Preliminary Prospectus

Shares

Common Stock

This is the initial public offering of our common stock. No public market currently exists for our common stock. We are offering all of the shares of our common stock offered by this prospectus. We expect the public offering price to be between $ and $ per share.

We have applied to list our common stock on The NASDAQ Global Market under the symbol “GNOM.”

Investing in our common stock involves a high degree of risk. Before buying any shares, you should carefully read the discussion of material risks of investing in our common stock in “Risk Factors” beginning on page 12 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share |

Total | |||||

| Public offering price |

$ | $ | ||||

| Underwriting discounts and commissions |

$ | $ | ||||

| Proceeds, before expenses, to us |

$ | $ | ||||

The underwriters have the option, exercisable on or before the thirtieth day after the date of this prospectus, to purchase up to an additional shares of our common stock at the public offering price, less the underwriting discounts and commissions payable by us, to cover over-allotments, if any. If the underwriters exercise this option in full, the total underwriting discounts and commissions will be $ , and our total proceeds, before expenses, will be $ .

The underwriters are offering the common stock as set forth under “Underwriting.” Delivery of the shares will be made on or about , 2010.

| UBS Investment Bank | Jefferies & Company | |

| Baird | Cowen and Company | |

The date of this prospectus is , 2010.

Table of Contents

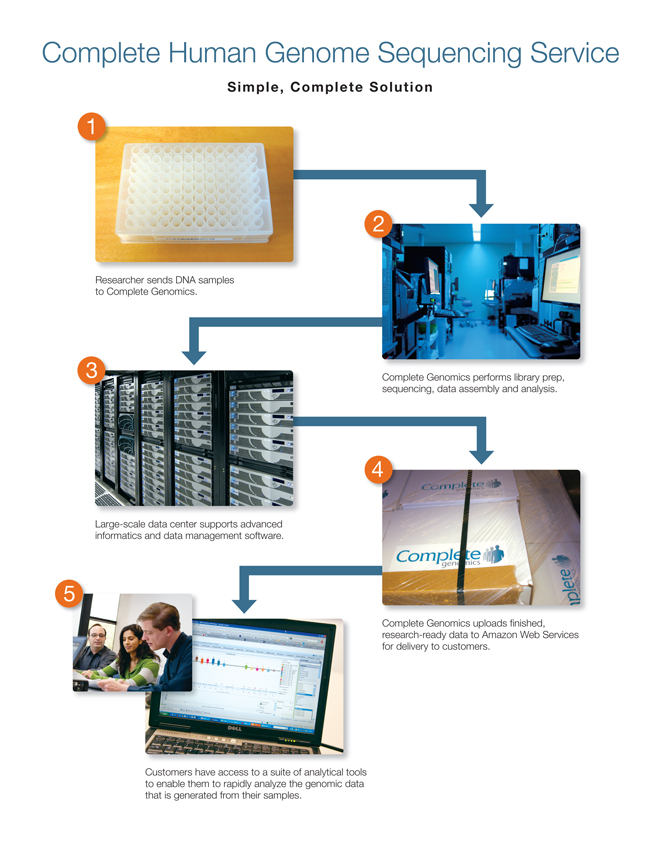

Complete Human Genome Sequencing Service

Simple, Complete Solution

1 Researcher sends DNA samples to complete Genomics.

2 Complete Genomics performs library prep, sequencing, data assembly and analysis.

3 Large-scale data center supports advanced informatics and data management software.

4 Complete Genomics uploads finished, research-ready data to Amazon Web Services for delivery to customers.

5 Customers have access to a suite of analytical tools to enable them to rapidly analyze the genomic data that is generated from their samples.

Table of Contents

You should rely only on the information contained in this prospectus. We have not, and the underwriters have not, authorized anyone to provide you with additional information or information different from that contained in this prospectus. We are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of shares of our common stock.

| 1 | ||

| 12 | ||

| 34 | ||

| 35 | ||

| 36 | ||

| 37 | ||

| 40 | ||

| 44 | ||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

46 | |

| 68 | ||

| 86 | ||

| 97 | ||

| 114 | ||

| 121 | ||

| 125 | ||

| 131 | ||

| Material U.S. Federal Income Tax Consequences to Non-U.S. Holders |

134 | |

| 138 | ||

| 141 | ||

| 144 | ||

| 144 | ||

| 144 | ||

| F-1 |

Through and including , 2010 (25 days after the date of this prospectus), federal securities laws may require all dealers that effect transactions in our common stock, whether or not participating in this offering, to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

Our logo, “Complete Genomics,” “Complete Genomics Analysis Platform,” “CGA Platform,” “cPAL” and “DNB” and other trademarks or service marks of Complete Genomics, Inc. appearing in this prospectus are the property of Complete Genomics, Inc. This prospectus contains additional trade names, trademarks and service marks of other companies. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply relationships with, or endorsement or sponsorship of us by, these other companies.

i

Table of Contents

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information you should consider in making your investment decision. You should read this summary together with the more detailed information, including our financial statements and the related notes, elsewhere in this prospectus. You should carefully consider, among other things, the matters discussed in “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” before making an investment decision. Unless otherwise indicated, “Complete Genomics, Inc.,” “Complete Genomics,” “the Company,” “we,” “us” and “our” refer to Complete Genomics, Inc.

Our Company

We are a life sciences company that has developed and commercialized an innovative DNA sequencing platform, and our goal is to become the preferred solution for complete human genome sequencing and analysis. Our Complete Genomics Analysis Platform, or CGA Platform, combines our proprietary human genome sequencing technology with our advanced informatics and data management software and our innovative, end-to-end, outsourced service model to provide our customers with data that is immediately ready to be used for genome-based research. We believe that our solution will provide academic and biopharmaceutical researchers with complete human genomic data and analysis at an unprecedented combination of quality, cost and scale without requiring them to invest in in-house sequencing instruments, high-performance computing resources and specialized personnel. By removing these constraints and broadly enabling researchers to conduct large-scale complete human genome studies, we believe that our solution has the potential to revolutionize medical research and expand understanding of the basis, treatment and prevention of complex diseases.

We believe that our complete human genome sequencing technology, which is based on our proprietary DNA arrays and ligation-based read technology, is superior to existing commercially available complete human genome sequencing methods in terms of quality, cost and scale. In the DNA sequencing industry, complete human genome sequencing is generally deemed to be coverage of at least 90% of the nucleotides in the genome. Because we have optimized our technology platform and our operations for the unique requirements of high-throughput complete human genome sequencing, we are able to achieve accuracy levels of 99.999% at a total cost that is significantly less than the total cost of purchasing and using commercially available DNA sequencing instruments. We believe that we will be able to further improve our accuracy levels and reduce the total cost of sequencing and analysis, enabling us to maintain significant competitive advantages over the next several years. Because our technology resides only in our centralized facilities, we can quickly and easily implement enhancements and provide their benefits to our entire customer base. Our goal is to be the first company to sequence and analyze high-quality complete human genomes, at scale, for a total cost of under $1,000 per genome.

While our competitors primarily sell DNA sequencing instruments and reagents that produce raw sequenced data, requiring their customers to invest significant additional resources to process that raw data into a form usable for research, we offer our customers an end-to-end, outsourced solution that delivers research-ready genomic data. As the cost of complete human genome sequencing declines, we believe the basis of competition in our industry will shift from the cost of sequencing to the value of the entire sequencing solution. We believe that our integrated, advanced informatics and data management services will emerge as a key competitive advantage as this shift occurs.

Our genome sequencing center, which began commercial operations in May 2010, combines a high-throughput sample preparation facility, a collection of our proprietary high-throughput sequencing instruments and a large- scale data center. Our customers ship us their samples via common carrier services such as Federal Express and

1

Table of Contents

United Parcel Service. We then sequence and analyze these samples and provide our customers with finished, research-ready data, enabling them to focus exclusively on their single highest priority, discovery.

As of March 31, 2010, there had been approximately 24 published and 200 unpublished complete human genomes sequenced worldwide, as reported in the April 2010 edition of Nature. As of July 20, 2010, we have sequenced over 200 complete human genomes year-to-date, including more than 100 in the first three weeks of July 2010, and have an order backlog of over 500 genomes. Our customers include some of the leading global academic and government research centers and biopharmaceutical companies. By the end of 2010, we expect our facility to have the capacity to sequence and analyze over 400 complete human genomes per month. We expect this capacity to increase between two- and three-fold in 2011 as we deploy additional sequencers and increase the throughput of our sequencing process through software refinements and component upgrades. In future years, we plan to construct additional genome centers in the United States and other strategic markets to accommodate an expected growing global demand for high-quality, low-cost complete human genome sequencing on a large scale.

Our Industry

Studying how genes differ between species and among individuals within a species, or genetic variations, helps scientists to determine their functions and roles in health and disease. Improving our understanding of the genome and its functions has driven and, we expect, will continue to drive advancements in medical research and diagnostics. Genetic analysis products comprise instruments and consumables, as well as associated hardware, software and services directly involved in the study of DNA and RNA. Scientia Advisors, a third-party research firm, estimated genomic revenue in 2009 to be approximately $5.8 billion and projects the market to grow to approximately $9.0 billion by 2014.

The primary genetic analysis methods traditionally used by genetic researchers fall into three categories: DNA sequencing, genotyping and gene expression analysis. DNA sequencing is the process of determining the exact order, or sequence, of the individual nucleotides in a DNA strand so that this information can be correlated to the genetic activity influenced by that segment of DNA. Genotyping is the process of examining certain known mutations or variations in the DNA sequence of genes to determine whether the particular variant can be associated with a specific disease susceptibility or drug response. Gene expression analysis is the process of examining the molecules that are produced when a gene is activated, or expressed, to determine whether a particular gene is expressed in a specific biological tissue.

The Importance of Complete Human Genome Sequencing and the Limitations of Existing Technologies

One of the most difficult challenges facing the genetic research and analysis industry is improving our understanding of how genes contribute to diseases that have a complex pattern of inheritance. For many diseases, multiple genes each make a subtle contribution to a person’s predisposition or susceptibility to a disease or response to a drug treatment protocol. Accordingly, we believe that unraveling this complex network will be critical to understanding human health and disease. We believe that sequencing complete human genomes is the most comprehensive and accurate method by which to achieve these objectives and improve our understanding of human disease.

Innovations in DNA sequencing have led to the development of high-throughput sequencing technologies, commonly referred to as next-generation or second-generation sequencing, which produce thousands to millions of sequences at once. Although second-generation sequencing technologies have led to dramatic reductions in cost and improvements in quality and throughput for complete human genome sequencing, they were designed as general-purpose instruments for sequencing the DNA or RNA of plants, animals, bacteria and viruses. We believe the key limitations of using second-generation technologies for sequencing large numbers of complete human genomes include the following:

| § | High Cost. Commercially available DNA sequencing instruments cannot sequence complete human genomes at a price low enough to make large-scale projects affordable to researchers. |

2

Table of Contents

| § | Insufficient Scale and Speed. Commercially available DNA sequencing instruments typically require weeks to sequence a complete human genome, which translates into months or years for large projects. |

| § | Difficulty of Data Management. Many users of commercially available DNA sequencing instruments lack the costly computing resources, storage capacity, network bandwidth and specialized personnel to process and analyze the massive data sets generated by sequencing complete human genomes. |

Our Solution

We have developed a novel approach to complete human genome sequencing. Our solution combines our proprietary sequencing technology, which achieves accuracy levels of 99.999%, with our advanced informatics and data management software and our innovative, end-to-end service model to deliver research-ready genomic data at a total cost that is significantly less than the total cost of purchasing and operating commercially available DNA sequencing instruments.

Proprietary Sequencing Technology

Our patterned DNA nanoball, or DNB, arrays, due to their small size and biochemical characteristics, enable us to pack DNA very efficiently on a silicon chip. In addition, we have developed a highly accurate combinatorial probe-anchor ligation, or cPAL, read technology, which enables us to read DNA fragments efficiently using small concentrations of low-cost reagents, while retaining extremely high single-read accuracy. We believe this unique combination of our proprietary DNB and cPAL technologies is superior in both quality and cost when compared to other commercially available approaches and provides us with significant competitive advantages. As reported in the January 2010 edition of Science, we sequenced a complete human genome at a consumables cost of approximately $1,800 and with a consensus error rate of approximately 1 error in 100,000 nucleotides. Our read accuracy was further validated by one of our customers, the Institute for Systems Biology, or ISB, as published in Science Express in March 2010.

Advanced Informatics and Data Management

Sequencing complete human genomes generates substantial amounts of data that must be managed, stored and analyzed. To address this potential need by our customers, we have built a genomics data processing facility with computing infrastructure for managing both small- and large-scale genomic sequencing projects. Our proprietary assembly software uses advanced data analysis algorithms and statistical modeling techniques to accurately reconstruct over 90% of the complete human genome from approximately two billion 70-base reads. After assembling the genomic data, we use our analysis software to identify and annotate key differences, or variants, in each genome.

By using our analytical tools and data management software, our customers can significantly reduce their investments in computing infrastructure. Our customers are provided with reliable access to assembled and annotated sequence data in multiple formats to ease data sharing and comparative analyses. In addition, our data storage options provide flexibility and allow customers to customize their data management strategy based on their particular business and scientific requirements. We have developed a suite of open source analytical tools, called CGATools, designed to enable our customers to rapidly analyze the data we generate from their samples. We are also developing additional analytical tools, such as a tumor-normal comparison tool designed to allow cancer researchers to compare a cancer genome to the normal genome from which it was derived. As the reagent cost of sequencing declines, we believe that the cost and complexity of data analysis and management will emerge as the primary limiting factor for conducting complete human genome analysis.

Innovative, End-to-End Outsourced Solution

While our competitors primarily sell DNA sequencing instruments and reagents that produce raw sequenced data, our end-to-end, outsourced solution enables our customers to offload to us the complex processes of sample preparation, sequencing, computing and data storage and management. We believe our services will expand the

3

Table of Contents

potential addressable market by enabling a broad base of researchers who may lack sufficient capital and the specialized personnel necessary to build and operate a sequencing laboratory, or who have historically been constrained by the high total cost of sequencing, to conduct large-scale complete human genome studies.

Our end-to-end solution provides the following advantages to our customers:

| § | High-Quality Data. Our technology delivers what we believe is the industry’s highest quality complete human genome data. |

| § | Cost-Savings. Our customers are not required to purchase expensive sequencing instruments and high-performance computing resources or hire the necessary specialized personnel to sequence and analyze large sets of complete human genome data. |

| § | Speed at Scale. Our customers can complete their large-scale projects more quickly by using our services than by using commercially available sequencing instruments. |

| § | Ease of Use. Our customers can avoid the difficulty and time-consuming process of purchasing and operating their own sequencing instruments and can outsource the entire process to us, from sample preparation to delivery of research-ready data. |

| § | Operational Flexibility. By outsourcing their large-scale complete human genome sequencing projects to us, our customers can free up the capacity of in-house instruments to run smaller or more targeted sequencing projects and applications. |

| § | Technological Flexibility. As DNA sequencing technology improves, our customers avoid the risk of their expensive instruments becoming technologically obsolete. |

| § | Enables Customers to Focus on Discovery. Outsourcing offloads the operational burdens of managing large-scale genome sequencing projects and enables our customers to focus their resources on research, which can reduce the time to discovery. |

We have more than 30 past and current customers, which include some of the leading global academic and government research centers and biopharmaceutical companies. In May 2010, we received an order from SAIC-Frederick, Inc., a prime contractor for the National Cancer Institute’s research and development facility in Frederick, Maryland, to sequence 50 tumor-normal pairs, or 100 complete human genomes, over a six-month period. This contract contains an option for SAIC-Frederick to engage us to sequence 564 additional cancer cases, or 1,128 complete human genomes, over an additional 18-month period. In addition, we sequenced complete genomes that enabled ISB to pinpoint the causal gene, and subsequently confirm that gene’s role, in Miller Syndrome. This work has led to a follow-on project with the ISB to sequence an additional 122 genomes. We also worked with Genentech, Inc. (a member of the Roche Group) on a non-small cell lung cancer study that was the first complete human genome sequence of a primary non-small cell lung tumor and matched normal tissue. The data we delivered allowed Genentech to measure the rate of smoking-induced mutations accumulated over time.

Applications for Our Sequencing Service

Potential applications for our complete human genome sequencing service include:

| § | Cancer Research. We believe understanding genetic mutations in cancer patients will guide development of new cancer therapeutics and diagnostics and ultimately enable doctors to select the best course of therapy based on the specific mutations found in a tumor. |

| § | Mendelian Disease Research. By sequencing the complete genomes of families affected with Mendelian diseases, which likely have a significant genetic component, we believe the genetic causes of these diseases can be discovered, which could lead to the development of novel diagnostics and therapeutics. |

4

Table of Contents

| § | Rare Variant Disease Research. Large-scale genomic studies of central nervous system disorders, cardiac disease and certain metabolic disorders may help to identify disrupted pathways and lead to the development of novel diagnostics and therapeutics. |

| § | Clinical Trial Optimization. We believe that selecting or stratifying patients on the basis of their genetic profiles could enable the preferential admission of high responders into clinical trials, lowering costs and resulting in faster clinical trials and drug commercialization. |

In addition to these research studies, we expect future clinical applications to include:

| § | Companion Diagnostics. We believe that therapeutics that are not first-line treatments for the general population may be elevated to first-line treatments or used in combination therapies for subsets of the population that share a common genetic profile. Complete human genome studies may unlock new market opportunities for these therapies or combination therapies. |

| § | Cancer Pathology. We believe that analyzing complex cancer genomes that involve large and unpredictable structural changes will be most reliably and economically implemented using complete human genome sequencing. |

| § | Universal Diagnostics. As medical records technology and public health policy advance, we believe that large numbers of people will have their complete human genomes sequenced and stored in their electronic medical records for use by their physicians in managing their health care decisions. |

Competitive Strengths

We believe that our competitive strengths are as follows:

| § | Proprietary Human Genome Sequencing Technology. Our proprietary sequencing technology achieves accuracy levels of 99.999% at a total cost that is significantly less than the total cost of purchasing and operating commercially available DNA sequencing instruments. |

| § | Fully Integrated Advanced Informatics and Data Management Software. Our solution enables our customers to manage and gain useful information from the massive data sets generated in complete human genome sequencing. |

| § | Highly Scalable and Capital-Efficient Business Model. Consolidating volume across our entire customer base enables us to sequence large numbers of genomes while avoiding the cost and complexity of employing a large field installation and support organization. By implementing a high degree of automation, we have reduced the possibility of human errors that could adversely affect quality and increase costs. |

| § | Unique Insight Into Customer Needs. We interact directly with our customers on their discovery projects, which enables us to develop and enhance our analysis software to meet our customers’ specific needs while expanding our understanding of variation in the human genome. |

| § | Fast and Efficient Deployment of Operational and Technological Enhancements. Because our sequencing operations and data center are centralized, we can rapidly upgrade our technology and deliver the benefits to our customers. In addition, our access to genomic data allows our software engineers to continually refine and improve our software with each genome we sequence. |

| § | Expanded Market Opportunity. We believe our outsourced model will expand the potential addressable market by providing academic and biopharmaceutical researchers who lack sufficient budgets or the specialized personnel necessary to build and operate a sequencing laboratory with access to high-quality, low-cost complete human genome data. |

5

Table of Contents

Our Strategy

We intend to become the leading complete human genome sequencing and analysis company and the preferred platform for human genome discovery by:

| § | continuing to deliver the highest quality genomic data and analysis at a low total cost; |

| § | maintaining and strengthening our technology; |

| § | capitalizing on our scalable model; |

| § | establishing ourselves as the leader in outsourced complete human genome sequencing; |

| § | expanding globally to increase capacity and reach new markets; and |

| § | expanding applications for the use of our technology. |

Risks Associated with our Business

Our business is subject to numerous risks, as discussed more fully in the section entitled “Risk Factors” immediately following this prospectus summary. These risks include the following, among others:

| § | We are an early, commercial-stage company and have a limited operating history. |

| § | We have a history of losses, and we may not achieve or sustain profitability in the future, on a quarterly or annual basis. |

| § | We may need substantial additional capital in the future in order to maintain and expand our business. |

| § | Our only source of revenue is our human genome sequencing service, which is a new business model in an emerging industry, and failure to achieve market acceptance will harm our business. |

| § | Potential customers may have significant reservations about allowing a third party to control the sequencing process or may want to sequence only portions of human genomes, which may prevent our complete human genome sequencing service from achieving market acceptance. |

| § | Our success depends on the growth of markets for analysis of genetic variation and biological function, and the shift of these markets to complete human genome sequencing. |

| § | We face significant competition from large, well-capitalized companies. The emergence of new competitive genome sequencing technologies may also harm our business. |

| § | We must significantly expand our capacity in order to meet projected demand. |

| § | If our Mountain View genome sequencing facility becomes inoperable, we will be unable to perform our genome sequencing services, and our business will be harmed. |

| § | If third parties assert that we have infringed their patents or other proprietary rights or challenge the validity of our patents or other proprietary rights, we may become involved in costly and time-consuming disputes and litigation that could affect our ability to sell our services. |

Corporate Information

We were incorporated in the state of Delaware on June 14, 2005. The address of our principal executive offices is 2071 Stierlin Court, Mountain View, California 94043, and our telephone number is (650) 943-2800. Our website address is www.completegenomics.com. We do not incorporate the information on, or that can be accessed through, our website into this prospectus, and you should not consider it part of this prospectus.

6

Table of Contents

The Offering

| Common stock offered by Complete Genomics |

shares (or shares if the underwriters exercise their over-allotment option in full). |

| Common stock to be outstanding after this offering |

shares (or shares if the underwriters exercise their over-allotment option in full). |

| Proposed NASDAQ Global Market symbol |

“GNOM” |

| Use of proceeds |

We currently intend to use the net proceeds of this offering for capital expenditures to expand the sequencing and computing capacity in our Mountain View and Santa Clara leased facilities, to finance the further development of our sequencing technology and services, for sales and marketing activities and for working capital and other general corporate purposes, including the costs associated with being a public company. Please see “Use of Proceeds.” |

| Risk factors |

See “Risk Factors” starting on page 12 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

The number of shares of common stock to be outstanding after this offering is based on shares outstanding as of September 1, 2010 and excludes:

| § | 2,687,100 shares of common stock issuable upon exercise of options outstanding as of September 1, 2010 with a weighted-average exercise price of $1.72 per share; |

| § | 771,900 shares of common stock reserved for future issuance under our 2006 Equity Incentive Plan as of September 1, 2010, which will become available for issuance under our 2010 Equity Incentive Award Plan after completion of this offering; |

| § | shares of common stock that will be reserved for future issuance under our 2010 Equity Incentive Award Plan, as well as any automatic increases in the number of shares of our common stock reserved for future issuance under this benefit plan, which will become effective immediately prior to the consummation of this offering; |

| § | up to 1,587,302 shares of our common stock that certain investors in our Series E financing will have the right to purchase from us if this offering is consummated before the second or third closing of that financing; |

| § | 1,965,479 shares of common stock subject to warrants outstanding as of September 1, 2010 that will not expire upon completion of this offering, with a weighted-average exercise price of $1.88 per share; and |

| § | 1,318,719 shares of common stock subject to warrants outstanding as of September 1, 2010 that will not expire upon completion of this offering and that are exercisable after September 30, 2010 in the event that we do not ship genomic data for at least 369 genomes between May 1, 2010 and September 30, 2010. |

The number of shares of our common stock outstanding after this offering assumes:

| § | the conversion of all 13,094,629 shares of our convertible preferred stock outstanding on September 1, 2010 into an aggregate of 15,808,361 shares of our common stock, which will be effective immediately prior to the consummation of this offering; |

7

Table of Contents

| § | the exercise, on a net issuance basis, of warrants outstanding as of September 1, 2010, which will expire upon completion of this offering if unexercised, to purchase shares of our common stock, resulting in the issuance of shares of common stock, assuming an initial public offering price of $ per share (the midpoint of the price range set forth on the cover page of this prospectus); and |

| § | the exercise, on a net issuance basis, of warrants outstanding as of September 1, 2010, which will expire upon completion of this offering if unexercised, to purchase shares of our convertible preferred stock, and the conversion of those shares of preferred stock immediately prior to the consummation of this offering, resulting in the issuance of shares of common stock, assuming an initial public offering price of $ per share (the midpoint of the price range set forth on the cover page of this prospectus). |

Except as otherwise indicated, all information in this prospectus reflects or assumes no exercise of the underwriters’ over-allotment option.

We refer to our Series A, Series B, Series C, Series D and Series E preferred stock collectively as “convertible preferred stock” for financial reporting purposes and in the financial tables included in this prospectus, as more fully explained in Note 6 to our financial statements. In other parts of this prospectus, we refer to our Series A, Series B, Series C, Series D and Series E preferred stock collectively as “preferred stock.”

8

Table of Contents

Summary Financial Data

The following tables set forth a summary of our historical financial data as of, and for the periods ended on, the dates indicated. You should read these tables together with our financial statements and the related notes, “Selected Financial Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus. The statement of operations data for the years ended December 31, 2007, 2008 and 2009 are derived from our audited financial statements included elsewhere in this prospectus. The statement of operations data for the six months ended June 30, 2009 and 2010 and for the cumulative period from June 14, 2005 (date of inception) to June 30, 2010, and the balance sheet data as of June 30, 2010 are derived from our unaudited financial statements included elsewhere in this prospectus. The unaudited financial statements have been prepared on a basis consistent with our audited financial statements and include, in the opinion of management, all adjustments, consisting only of normal recurring adjustments, necessary for the fair statement of the financial information in those statements. Our historical results are not necessarily indicative of the results to be expected in any future period, and the results for the six months ended June 30, 2010 are not necessarily indicative of the results to be expected for the year ending December 31, 2010.

The unaudited pro forma and pro forma as adjusted financial data is presented for informational purposes only and does not purport to represent what our results of operations or financial position actually would have been had the transactions reflected occurred on the dates indicated or to project our financial condition as of any future date or results of operations for any future period.

| Years ended December 31, | Six months ended June 30, |

Cumulative period from June 14, 2005 (date of inception) to June 30, 2010 |

||||||||||||||||||||||

| 2007 | 2008 | 2009 | 2009 | 2010 | ||||||||||||||||||||

| (in thousands, except share and per share amounts) | ||||||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||||||

| Revenue |

$ | — | $ | — | $ | 623 | $ | — | $ | 1,425 | $ | 2,048 | ||||||||||||

| Operating expenses: |

||||||||||||||||||||||||

| Start-up production costs(1) |

— | — | 5,033 | 1,013 | 8,985 | 14,018 | ||||||||||||||||||

| Research and development(1) |

10,305 | 23,633 | 22,424 | 10,449 | 11,097 | 71,191 | ||||||||||||||||||

| General and administrative(1) |

1,896 | 3,179 | 4,953 | 2,120 | 4,862 | 15,841 | ||||||||||||||||||

| Sales and marketing(1) |

— | 1,045 | 1,798 | 620 | 2,539 | 5,382 | ||||||||||||||||||

| Total operating expenses(1) |

12,201 | 27,857 | 34,208 | 14,202 | 27,483 | 106,432 | ||||||||||||||||||

| Loss from operations |

(12,201 | ) | (27,857 | ) | (33,585 | ) | (14,202 | ) | (26,058 | ) | (104,384 | ) | ||||||||||||

| Interest expense |

(215 | ) | (974 | ) | (3,465 | ) | (2,051 | ) | (1,144 | ) | (5,809 | ) | ||||||||||||

| Interest and other income (expense), net |

163 | 437 | 1,101 | (70 | ) | 235 | 2,065 | |||||||||||||||||

| Net loss |

$ | (12,253 | ) | $ | (28,394 | ) | $ | (35,949 | ) | $ | (16,323 | ) | $ | (26,967 | ) | $ | (108,128 | ) | ||||||

| Net loss per share, basic and diluted |

$ | (211.00 | ) | $ | (369.36 | ) | $ | (386.56 | ) | $ | (177.96 | ) | $ | (45.09 | ) | |||||||||

| Weighted-average shares of common stock outstanding used in computing net loss per share, basic and diluted |

58,072 | 76,873 | 92,998 | 91,724 | 598,080 | |||||||||||||||||||

| Pro forma net loss per share of common stock, basic and diluted (unaudited)(2) |

$ | (6.59 | ) | $ | (2.53 | ) | ||||||||||||||||||

| Net loss used in computing pro forma net loss per share of common stock, basic and diluted (unaudited)(2) |

$ | (37,037 | ) | $ | (27,202 | ) | ||||||||||||||||||

| Weighted-average shares of common stock outstanding used in computing the pro forma net loss per share of common stock, basic and diluted (unaudited)(2) |

5,619,600 | 10,763,515 | ||||||||||||||||||||||

(footnotes on following page)

9

Table of Contents

| (1) | Includes stock-based compensation expense as follows: |

| Years ended December 31, | Six months ended June 30, |

Cumulative period from June 14, 2005 (date of inception) to June 30, 2010 | ||||||||||||||||

| 2007 | 2008 | 2009 | 2009 | 2010 | ||||||||||||||

| (in thousands) | ||||||||||||||||||

| Start-up production costs |

$ | — | $ | — | $ | 81 | $ | 15 | $ | 105 | $ | 186 | ||||||

| Research and development |

78 | 246 | 992 | 225 | 415 | 1,741 | ||||||||||||

| General and administrative |

22 | 90 | 262 | 78 | 301 | 677 | ||||||||||||

| Sales and marketing |

— | — | 75 | 25 | 68 | 143 | ||||||||||||

| Total stock-based compensation expense |

$ | 100 | $ | 336 | $ | 1,410 | $ | 343 | $ | 889 | $ | 2,747 | ||||||

| (2) | Net loss used in computing pro forma basic and diluted net loss per share of common stock, and the number of weighted-average common shares used in computing pro forma basic and diluted net loss per share of common stock, in the table above assume the conversion of all of our outstanding convertible preferred stock into common stock immediately prior to the consummation of this offering. See Note 2 to our financial statements for an explanation of the method used to compute pro forma basic and diluted net loss per share of common stock and the number of shares used in computing those per share amounts. |

The table below presents our balance sheet data as of June 30, 2010:

| § | on an actual basis; |

| § | on a pro forma basis to give effect to: |

| § | our issuance and sale, during August and September 2010, of an aggregate of 5,274,871 shares of our Series E preferred stock and warrants to purchase an aggregate of 1,318,719 shares of our common stock at an exercise price of $2.69 per share, which will become exercisable after September 30, 2010 in the event that we do not ship genomic data for at least 369 genomes between May 1, 2010 and September 30, 2010; |

| § | the conversion of the convertible notes we issued and sold during April, May, June and August 2010 into shares of our Series E preferred stock, which occurred during August 2010 in connection with our Series E preferred stock financing; |

| § | the conversion of all shares of our convertible preferred stock outstanding on June 30, 2010, together with the shares of Series E preferred stock we issued during August and September 2010, including shares issued in connection with the related conversion of our convertible notes, into an aggregate of 15,808,361 shares of our common stock, which will be effective immediately prior to the consummation of this offering; |

| § | the conversion of all of our warrants for convertible preferred stock into warrants for common stock immediately prior to the consummation of this offering, and the related reclassification of convertible preferred stock warrant liability to additional paid-in capital; |

| § | the exercise, on a net issuance basis, of warrants outstanding as of June 30, 2010, which will expire upon completion of this offering if unexercised, to purchase shares of our common stock, resulting in the issuance of shares of common stock, assuming an initial public offering price of $ per share (the midpoint of the price range set forth on the cover page of this prospectus); and |

| § | the exercise, on a net issuance basis, of warrants outstanding as of June 30, 2010, which will expire upon completion of this offering if unexercised, to purchase shares of our convertible preferred stock, and the conversion of those shares of preferred stock immediately prior to the consummation of this offering, resulting in the issuance of shares of common stock, assuming an initial public |

10

Table of Contents

| offering price of $ per share (the midpoint of the price range set forth on the cover page of this prospectus); and |

| § | on a pro forma as adjusted basis to give further effect to the sale of shares of common stock in this offering at an assumed initial public offering price of $ per share (the midpoint of the price range set forth on the cover page of this prospectus), after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

| June 30, 2010 | |||||||||

| Actual | Pro forma | Pro forma as adjusted(1) | |||||||

| (in thousands) | |||||||||

| Balance Sheet Data: |

|||||||||

| Cash and cash equivalents |

$ | 7,972 | $ | 25,365 | |||||

| Working capital (deficit) |

(20,860 | ) | 13,834 | ||||||

| Total assets |

39,795 | 57,188 | |||||||

| Current and long-term notes payable |

23,179 | 5,878 | |||||||

| Convertible preferred stock warrant liability |

1,318 | — | |||||||

| Convertible preferred stock |

95,844 | — | |||||||

| Total stockholders’ equity (deficit) |

(96,451 | ) | 35,576 | ||||||

| (1) | A $1.00 increase (decrease) in the assumed initial public offering price of $ per share (the midpoint of the price range set forth on the cover page of this prospectus) would increase (decrease) each of pro forma as adjusted cash and cash equivalents, working capital, total assets and stockholders’ equity by approximately $ million, assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same. We may also increase or decrease the number of shares we are offering. An increase (decrease) of 1,000,000 in the number of shares we are offering would increase (decrease) each of pro forma as adjusted cash and cash equivalents, working capital, total assets and stockholders’ equity by approximately $ million, assuming the initial public offering price per share, as set forth on the cover page of this prospectus, remains the same. An increase of 1,000,000 in the number of shares we are offering, together with a $ 1.00 increase in the assumed initial public offering price per share, would increase each of pro forma as adjusted cash and cash equivalents, working capital, total assets and stockholders’ equity by approximately $ million. A decrease of 1,000,000 in the number of shares we are offering, together with a $1.00 decrease in the assumed initial public offering price per share, would decrease each of pro forma as adjusted cash and cash equivalents, working capital, total assets and stockholders’ equity by approximately $ million. The pro forma as adjusted information is illustrative only, and we will adjust this information based on the actual initial public offering price and other terms of this offering determined at pricing. |

11

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the following risk factors, as well as the other information in this prospectus, before deciding whether to invest in shares of our common stock. The occurrence of any of the events described below could harm our business, financial condition, results of operations and growth prospects. In such an event, the trading price of our common stock may decline and you may lose all or part of your investment.

Risks Related to Our Limited Operating History, Financial Condition and Capital Requirements

We are an early, commercial-stage company and have a limited operating history, which may make it difficult to evaluate our current business and predict our future performance.

We are an early, commercial-stage company and have a limited operating history. We were incorporated in Delaware in June 2005 and began operations in March 2006. From March 2006 until mid-2009, our operations focused on research and developing our DNA sequencing technology platform. In December 2009, we recognized our first revenue from the sale of our genome sequencing services. Our limited operating history, particularly in light of our novel, service-based business model in the rapidly evolving genome sequencing industry, may make it difficult to evaluate our current business and predict our future performance. Our lack of a long operating history, and especially our very short history as a revenue-generating company, make any assessment of our profitability or prediction about our future success or viability subject to significant uncertainty. We have encountered and will continue to encounter risks and difficulties frequently experienced by early, commercial-stage companies in rapidly evolving industries. If we do not address these risks successfully, our business will suffer.

Our quarterly operating results may fluctuate in the future. As a result, we may fail to meet or exceed the expectations of research analysts or investors, which could cause our stock price to decline.

Our financial condition and operating results may fluctuate from quarter to quarter and year to year in the future due to a variety of factors, many of which are beyond our control. Factors relating to our business that may contribute to these fluctuations include the following, as well as other factors described elsewhere in this prospectus:

| § | our ability to achieve profitability; |

| § | the size and frequency of customer orders; |

| § | our ability to expand our sequencing operations; |

| § | our need for and ability to obtain capital necessary to operate and expand our business; |

| § | the cost of our sequencing services; |

| § | the demand for the sequencing of complete human genomes; |

| § | the existence and extent of government funding for research and development relating to genome sequencing; |

| § | the emergence of alternative genome sequencing technologies; |

| § | risks associated with expanding our business into international markets; |

| § | our ability to lower the average cost per genome that we sequence; |

| § | our dependence on single-source suppliers; |

| § | our ability to manage our growth; |

| § | our ability to successfully partner with other businesses in joint ventures or collaborations, or integrate any businesses we may acquire with our business; |

12

Table of Contents

| § | our dependence on, and the need to attract and retain, key management and qualified sales personnel; |

| § | our ability to obtain, protect and enforce our intellectual property rights and avoid infringing the intellectual property rights of others; |

| § | our ability to prevent the theft or misappropriation of our know-how or technologies; |

| § | lawsuits brought against us by third parties; |

| § | business interruptions, such as earthquakes and other natural disasters; |

| § | public concerns about the ethical, legal and social concerns related to the use of genetic information; |

| § | our ability to comply with current laws and regulations and new or expanded regulatory schemes; |

| § | our ability to properly handle and dispose of hazardous materials used in our business and biological waste; and |

| § | our ability to use our net operating loss carryforwards to offset future taxable income. |

Due to the various factors mentioned above, and others, the results of any prior quarterly or annual periods are not necessarily indicative of our future operating performance.

We have a history of losses, and we may not achieve or sustain profitability in the future, on a quarterly or annual basis.

We have not been profitable in any quarterly period since we were formed. We incurred net losses of $12.3 million, $28.4 million and $35.9 million for the years ended December 31, 2007, 2008 and 2009, respectively, and $27.0 million for the six months ended June 30, 2010. As of June 30, 2010, our deficit accumulated during the development stage was $108.1 million. Based on our current operating plans and assumptions, we do not expect to achieve profitability on an annual basis in the near future. In addition, we expect our cash expenditures to increase significantly in the near term, including significant expenditures for the expansion of our Mountain View, California sequencing facility and the development of additional sequencing centers, research and development, sales and marketing and general and administrative expenses. In order to continue operations, we must obtain additional debt or equity financing. We may encounter unforeseen difficulties, complications and delays in expanding our Mountain View sequencing facility or in establishing additional genome sequencing centers and other unforeseen factors that require additional expenditures. These costs, among other factors, have had and will continue to have an adverse effect on our working capital and stockholders’ equity. We will have to generate and sustain substantially increased revenue to achieve and maintain profitability, which we may never do. If we are unable to achieve and then maintain profitability, the market value of our common stock will decline.

We may need substantial additional capital in the future in order to maintain and expand our business.

Our future capital requirements may be substantial, particularly as we further develop our business, expand the sequencing and computing capacity in our Mountain View and Santa Clara, California leased facilities and establish additional genome sequencing centers. Historically, we have financed our operations through private placements of preferred stock and convertible debt and borrowings under our credit facility.

We believe that, based on our current level of operations and anticipated growth, the net proceeds from this offering, together with our cash and cash equivalent balances and interest income we earn on these balances, will be sufficient to meet our anticipated cash requirements through at least the next 12 months. However, we may need additional capital if our current plans and assumptions change. Our need for additional capital will depend on many factors, including:

| § | the financial success of our genome sequencing business; |

| § | our ability to increase the sequencing and computing capacity in our Mountain View and Santa Clara leased facilities; |

| § | the rate at which we establish additional genome sequencing centers and whether we can find suitable partners to establish such centers; |

13

Table of Contents

| § | whether we are successful in obtaining payments from customers; |

| § | whether we can enter into collaborations or establish a recurring customer base; |

| § | the progress and scope of our research and development projects; |

| § | the effect of any joint ventures or acquisitions of other businesses or technologies that we may enter into or make in the future; |

| § | the filing, prosecution and enforcement of patent claims; and |

| § | lawsuits brought against us by third parties. |

If our capital resources are insufficient to meet our capital requirements, and we are unable to enter into joint ventures or collaborations with partners able or willing to fund our development efforts or purchase our genome sequencing services, we will have to raise additional funds. If future financings involve the issuance of equity securities, our existing stockholders would suffer dilution. If we raise additional debt financing, we may be subject to restrictive covenants that limit our ability to conduct our business. We may not be able to raise sufficient additional funds on terms that are favorable to us, if at all. If we fail to raise sufficient funds and continue to incur losses, our ability to fund our operations, take advantage of strategic opportunities, further develop and enhance our technology or otherwise respond to competitive pressures could significantly suffer. If this happens, we may be forced to:

| § | slow or halt the expansion of our Mountain View facility and the establishment of additional genome sequencing centers; |

| § | slow the commercialization of our services; |

| § | delay or terminate research or development programs; |

| § | curtail or cease operations; or |

| § | seek to obtain funds through collaborative and licensing arrangements, which may require us to relinquish commercial rights or grant licenses on terms that are not favorable to us. |

The report of our independent registered public accounting firm has expressed substantial doubt as to our ability to continue as a going concern.

In its report accompanying our audited financial statements for the year ended December 31, 2009, our independent registered public accounting firm included an explanatory paragraph stating that our recurring losses from operations and lack of sufficient working capital raise substantial doubt as to our ability to continue as a going concern. A report with this type of explanatory paragraph could impair our ability to finance our operations through the sale of debt or equity securities or to obtain commercial bank loans. Our ability to continue as a going concern will depend, in large part, on our ability to generate positive cash flow from operations and obtain necessary financing, neither of which is certain. As a result, the report of our independent registered public accounting firm for the year ending December 31, 2010 may express substantial doubt about our ability to continue as a going concern. Accordingly, we may need to obtain sufficient financing in the short term, and the failure to do so may adversely affect the value of our common stock.

Risks Related to Our Business

Our only source of revenue is our human genome sequencing service, which is a new business model in an emerging industry, and failure to achieve market acceptance will harm our business.

Since our inception, all of our efforts have been focused on the creation of a technology platform for our human genome sequencing service, which we have only just recently commercialized. We expect to generate all of our revenue from our human genome sequencing service for the foreseeable future. As a result, market acceptance of our human genome sequencing service is critical to our future success.

14

Table of Contents

Providing genome sequencing as a service is a new and unproven business model in a relatively new and rapidly evolving industry. We are using proprietary technology, involving multiple scientific and engineering disciplines, and a novel service model to bring complete human genome sequencing to an unproven market. Historically, companies in this industry have sold sequencing instruments directly to customers, and the customer performs the sequencing itself. We do not know if the purchasers and users of sequencing instruments will adopt our service model. For example, many potential customers want to sequence human genomes for proprietary studies that may lead to discoveries which they would seek to exploit, either commercially or through the publication of scientific literature. Accordingly, these potential customers may have significant reservations about allowing a third party to control the sequencing processes for their proprietary studies. Alternatively, other potential customers may want to sequence only portions of human genomes, rather than complete human genomes. There are many reasons why our services might not become widely adopted, ranging from logistical or quality problems to a failure by our sales force to engage potential customers, and including the other reasons stated in this “Risk Factors” section. As a result, our genome sequencing service may not achieve sufficient market acceptance to allow us to become profitable.

Our success depends on the growth of markets for analysis of genetic variation and biological function, and the shift of these markets to complete human genome sequencing.

We are currently targeting customers for our genome sequencing service in academic and government research institutions and in the pharmaceutical and other life science industries. Our customers are using our service for large-scale human genome studies for a wide variety of diagnostic and discovery applications. These markets are new and emerging, and they may not develop as quickly as we anticipate, or reach their full potential. The development of the market for complete human genome sequencing and the success of our service depend in part on the following factors:

| § | demand by researchers for complete human genome sequencing; |

| § | the usefulness of genomic data in identifying or treating disease; |

| § | the ability of our customers to successfully analyze the genomic data we provide; |

| § | the ability of researchers to convert genomic data into medically valuable information; |

| § | the capacity and scalability of the hardware storage components necessary to store, manage, backup, retain and safeguard genomic data; and |

| § | the development of software tools to efficiently search, correlate and manage genomic data. |

For instance, demand for our genome sequencing service may decrease if researchers fail to find meaningful correlations between genetic variation and disease susceptibility through genome-wide association studies. In addition, factors affecting research and development spending generally, such as changes in the regulatory environment affecting pharmaceutical and other life science companies and changes in government programs that provide funding to companies and research institutions, could harm our business. If our target markets do not develop in a timely manner, demand for our service may grow at a slower rate than we expect, or may fall, and we may not achieve profitability.

To date, relatively few complete human genomes have been sequenced, in large part due to the high cost of large-scale sequencing. Our business plan assumes that the demand for sequencing complete human genomes will increase significantly as the cost of complete human genome sequencing decreases. This assumption may prove to be incorrect, or the increase in demand may take significantly more time than we anticipate. For example, potential customers may not think our cost reductions are sufficient to permit or justify large-scale sequencing. Moreover, some companies and institutions have focused on sequencing targeted areas of the genome that are believed to be primarily associated with disorders and diseases, as opposed to the entire genome. Demand for sequencing complete human genomes may not increase if these targeted sequencing strategies, such as exome sequencing, where selected regions containing key portions of genes are sequenced, prove to be more cost effective or are viewed as a more efficient method of genetic analysis than complete human genome sequencing.

15

Table of Contents

We face significant competition. Our failure to compete effectively could adversely affect our sales and results of operations.

We currently compete with companies that develop, manufacture and market genome sequencing instruments or provide genome sequencing services. We expect competition to increase as our competitors develop new, improved or cheaper instruments or expand their businesses to include sequencing services, and as new companies enter the market with innovative technologies.

The market for genome sequencing technology is highly competitive and is served by several large companies with significant market shares. For example, established companies such as Illumina, Inc., Life Technologies Corporation and Roche Diagnostics Corporation are marketing instruments for genetic sequencing that are directly competitive with our services, and these companies have significantly greater financial, technical, marketing and other resources than we do to invest in new technologies and have substantial intellectual property portfolios and substantial experience in product development and regulatory expertise. Also, there are many smaller companies, such as NABsys, Inc., Oxford Nanopore Technologies, Ltd., Pacific Biosciences, Inc. and Helicos Biosciences Corporation, that are developing sequencing technology that would compete with ours. Moreover, large established companies may acquire smaller companies, such as these, with emerging technologies and use their extensive resources to develop and commercialize such technologies or incorporate such technologies into their instruments and services. For example, Life Technologies recently announced that it entered into a definitive agreement to acquire Ion Torrent Systems, Inc., a chip-based sequencing technology startup.

In addition, there are many research, academic and other non-profit institutions that are pursuing new sequencing technologies. These institutions often have access to significant government and other funding. For example, BGI (formerly known as Beijing Genomics Institute) in the People’s Republic of China offers a service that is similar to ours and is funded by the government of China. In the United States, agencies such as the National Human Genome Research Institute provide funding to institutions to discover new sequencing technology. We may compete directly with these institutions, or these institutions may license their technologies to third parties with whom we would compete.

While many of our existing competitors primarily sell sequencing instruments, they may also begin to provide sequencing services like us. Since these competitors have already developed their own sequencing technology, they will not experience significant technological barriers to entry and can likely enter the sequencing services market fairly quickly and with little additional cost. For example, Illumina has recently announced that it will be providing individual genome sequencing services for as low as $9,500 per genome, and Life Technologies has recently announced a collaboration to build a genome sequencing facility. Illumina also announced that it is pursuing a global program designed to provide researchers with access to academic and commercial institutions that can perform large-scale whole human genome sequencing projects using Illumina’s technology. Furthermore, many of these instrumentation companies have already established a significant market presence and are trusted by customers in the industry. As established instrumentation companies enter the sequencing services market, many potential customers may purchase sequencing services from these companies instead of us, even if we offer superior technology and services.

For more information regarding our existing and potential competitors, please see “Business—Competition.”

The emergence of competitive genome sequencing technologies may harm our business.

The success of our genome sequencing services will depend, in part, on our ability to continue to enhance the performance and decrease the cost of our genome sequencing technology. A number of genome sequencing technologies exist, and new methods and improvement to existing methods are currently being developed, including technology platforms developed by companies that we expect will directly compete with us as providers of sequencing services or instruments. These new technologies may result in faster, more cost-effective and more accurate sequencing methods than ours. For example, our sequencing technology does not currently cover all of the nucleotides in the genome. If competitive technologies emerge that sequence portions of the genome that our technology does not, our business could suffer if those portions contain important genomic

16

Table of Contents

information. We expect to face competition from emerging companies, including NABsys, Oxford Nanopore Technologies and Pacific Biosciences. As a result of the emergence of these competitive sequencing technologies, demand for our service may decline or never develop sufficiently to sustain our operations.

Our industry is rapidly changing, with emerging and continually evolving technologies that increase the efficiency and reduce the cost of sequencing genomes. As new technologies emerge, we believe that the cost and error rates of, and the time required to, sequence human genomes will eventually decrease to a level where competition in the industry will shift to other factors, such as providing related services and analytical technologies. We may not be able to maintain any technological advantage over these new sequencing technologies, and if we fail to compete effectively on other factors relevant to our customers, our business will suffer.

Our order backlog may never be completed, and we may never earn revenue on backlogged contracts to sequence genomes.

In various sections of this prospectus, we have disclosed that, as of July 20, 2010, we have an order backlog for the sequencing of over 500 genomes. This figure represents the number of genomes for which we have executed purchase orders from our customers that we believe are firm and for which we have not yet recognized revenue. We have also disclosed that, as of June 30, 2010, our order backlog for which we believe we will sequence, bill and gain customer acceptance within twelve months was approximately $10.0 million. We may never sequence these genomes or receive revenue from these backlogged orders, and the order backlog we report may not be indicative of our future revenue.

Many events can cause a backlogged order not to be completed. Currently, many orders are considered backlog because we do not presently have sufficient capacity to immediately sequence all the genomes which we have agreed to sequence. If we delay fulfilling customer orders, those customers may seek to cancel their contracts with us or may turn to one of our competitors. For example, we have in the past had a customer cancel a contract with us due, in part, to a delay in sequencing their samples. If our backlogged orders do not result in sales, our operating results will suffer.

We must significantly increase our production capabilities in order to meet expected demand.

We have only just recently commercialized our complete human genome sequencing service, and we have very limited experience in running a commercial-scale production facility. We have only one sequencing facility, and we project that facility to have the capacity to sequence over 400 complete human genomes per month by the end of 2010. This capacity is significantly less than what would be required to achieve profitability, if demand for our sequencing services grows as anticipated. Our business plan assumes that we will be able to increase our capacity multiple fold.

We plan to increase the capacity of our sequencing facility by installing additional sequencing machines, improving our software and purchasing higher resolution cameras to image the DNA arrays. We also plan to construct additional genome sequencing centers in the United States and elsewhere. We may encounter difficulties in expanding our sequencing infrastructure, and we may not build and improve this infrastructure in time to meet the volume, quality or timing requirements necessary to be successful. Manufacturing and supply quality issues may arise, including due to third parties who provide the components of our technology platform. Implementing improvements to our sequencing technology may involve significant changes, which may result in delays, or may not achieve expected results. For example, we are experimenting with increasing the density of the silicon wafers that we use for our DNA arrays by reducing the grid size of those wafers and correspondingly reducing the diameter of our DNA nanoballs, or DNBs, and the sticky spots on those wafers. These experiments may be unsuccessful and may not lead to feasible technological improvements that increase the capacity or reduce the costs of our sequencing services. If capacity or cost limitations prevent us from meeting our customers’ expectations, we will lose revenue and our potential customers may take their business to our competitors.

17

Table of Contents

Our genome sequencing technology platform was developed for human DNA and is not currently optimized to sequence non-human DNA.

Our technology platform was developed and has been optimized for sequencing human DNA, and we do not intend to sequence non-human DNA. We face significant competition from established companies who sell genome sequencing instruments that can sequence both human and non-human DNA. Many of the academic and research institutions that are our target customers conduct studies on both human and non-human DNA. Prospective customers may choose to purchase sequencing instruments from a competitor because of their broader sequencing application. Our competitors may also choose to provide sequencing services for non-human DNA. As a result, there may not be sufficient demand for our human genome sequencing service, which will harm our business.

We depend on a limited number of suppliers, including single-source suppliers, of various critical components for our sequencing process. The loss of these suppliers, or their failure to supply us with the necessary components on a timely basis, could cause delays in the current and future capacity of our sequencing center and adversely affect our business.

We depend on a limited number of suppliers, including some single-source suppliers, of various critical components for our sequencing process. We do not have long-term contracts with our suppliers or service providers. Because we do not have long-term contracts, our suppliers generally are not required to provide us with any guaranteed minimum production levels. As a result, we may not be able to obtain sufficient quantities of critical components in the future.

Although alternative suppliers exist for each of the critical components of our sequencing process, that process has been designed around the functions, limitations, features and specifications of the components that we currently utilize. For example, the cameras in our sequencers are supplied by Hamamatsu Photonics and the optical equipment is supplied by Carl Zeiss, Inc. A failure by either or both of these companies to supply these components would require us to integrate alternative cameras and optical equipment, and potentially integrate other components, into future sequencing instruments. If we are required to integrate new components into future sequencers, we would experience a delay in the deployment of these sequencers, and, as a result, our efforts to expand our sequencing capacity would be delayed.

A delay or interruption by our suppliers may also harm our business. For example, the wafers that comprise the base of our sample slide are fabricated by SVTC Technologies, L.L.C. We have not yet qualified an alternative source for the supply of these wafers, which are critical to our sequencing process, and the custom manner in which these wafers are made may make it difficult to qualify other semiconductor suppliers to manufacture them for us. We recently experienced a significant delay in the delivery, from one of our suppliers, of certain components for our sequencing system, which delayed our planned expansion of our Mountain View sequencing facility. Similarly, an interruption of services by Amazon Web Services, on whom we rely to deliver finished genomic data to our customers, would result in our customers not receiving their data on time.

In addition, the lead time needed to establish a relationship with a new supplier can be lengthy, and we may experience delays in meeting demand in the event we must switch to a new supplier. The time and effort to qualify a new supplier could result in additional costs, diversion of resources or reduced manufacturing yields, any of which would negatively impact our operating results. Our dependence on single-source suppliers exposes us to numerous risks, including the following:

| § | our suppliers may cease or reduce production or deliveries, raise prices or renegotiate terms; |

| § | delays by our suppliers could significantly limit our ability to sequence customer data and delay our efforts to increase our sequencing capacity; |

| § | we may be unable to locate a suitable replacement on acceptable terms or on a timely basis, if at all; and |

| § | delays caused by supply issues may harm our reputation, frustrate our customers and cause them to turn to our competitors for future projects. |

18

Table of Contents

If our Mountain View genome sequencing facility becomes inoperable, we will be unable to perform our genome sequencing services and our business will be harmed.