Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - BRYN MAWR BANK CORP | d8k.htm |

Bryn Mawr

Bank Corporation

NASDAQ: BMTC

Second Quarter 2010 Update

Exhibit 99.1 |

1

Safe Harbor

This presentation contains statements which, to the extent that they are not

recitations of historical fact may constitute forward-looking statements within

the meaning of the United States Private Securities Litigation Reform Act of

1995.

Please see the section titled Safe Harbor at the end of the presentation for

more information regarding these types of statements.

|

2

Bryn Mawr

Bank Corporation

Profile

Founded in 1889 –

120 year history

A unique business model with a traditional commercial bank ($1.2

billion)

and a trust company ($3.1 billion) under one roof at June 30, 2010

Upon the acquisition of First Keystone Financial Inc. on July 1,

2010,

commercial bank assets increased to $1.8 billion

Wholly owned subsidiary –

The Bryn Mawr

Trust Company

Located on Philadelphia’s affluent “Main Line”

Celebrated 25 years on the NASDAQ in August 2010 |

3

(*)

Includes 7 limited service retirement

community branches

Bryn Mawr

Bank Corp. (16)

First Keystone Financial, Inc. (8)

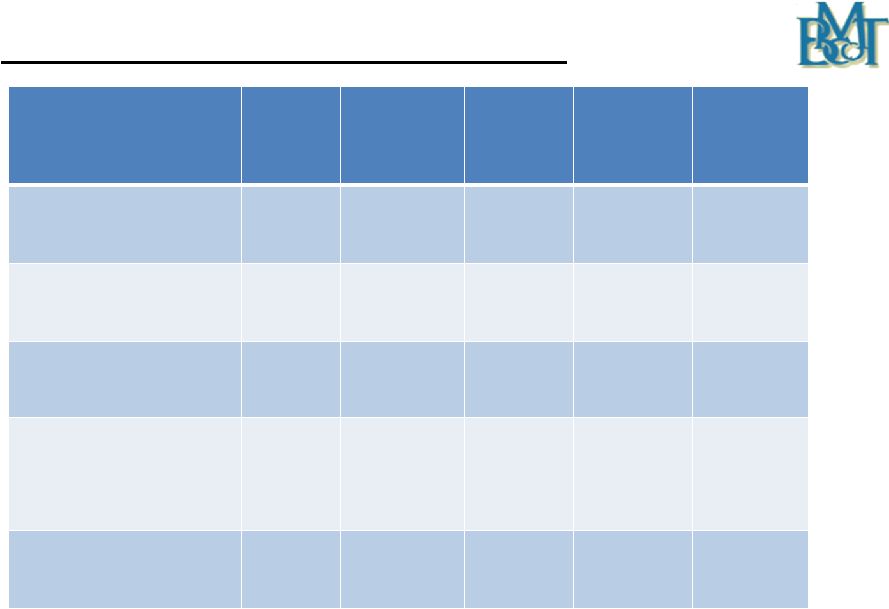

Expanding Southeast PA Footprint

($ in millions)

BMTC

FKFS

Pro Forma *

Assets

$1,281

$483

$1,768

Loans

899

292

1,172

Deposits

953

319

1,274

Branches (*)

16

8

24

Pro Forma Financials

* Estimated |

4

Investment Considerations

A great brand & franchise

Solid financial fundamentals

Excellent credit quality

Outstanding target market demographics

New business initiatives driving growth

Well-capitalized

$3.1 billion wealth management business that provides a significant

source of non-interest income |

5

Experienced Management Team

Chairman, President and CEO –

Ted Peters

Lending –

Joseph Keefer

Wealth

Management

–

Frank

Leto

Retail

Banking

–

Alison

Gers

Finance

–

Duncan

Smith,

CPA

Risk

Management

–

Geoffrey

Halberstadt |

6

Financial Highlights

2

nd

Qtr

2010

1

st

Qtr

2010

4

th

Qtr

2009

3

rd

Qtr

2009

2

nd

Qtr

2009

Portfolio Loans & Leases

($ in millions)

$899

$893

$886

$886

$878

Total Wealth Assets

($ in billions)

$3.10

$3.11

$2.87

$2.71

$2.26

Total Deposits

($ in millions)

$953

$914

$938

$899

$894

Tangible Book Value Per

Share

$11.15

$10.56

$10.40

$10.44

$10.15

Tangible Common Equity

Ratio

9.30%

7.82%

7.51%

7.74%

7.43%

Dividends Declared

$0.14

$0.14

$0.14

$0.14

$0.14 |

7

Financial Highlights -

continued

2

nd

Qtr

2010

1

st

Qtr

2010

4

th

Qtr

2009

3

rd

Qtr

2009

2

nd

Qtr

2009

Net Income

($ in millions)

$2.41

$2.22

$2.64

$2.62

$2.45

Basic Earnings Per

Common Share

$0.25

$0.25

$0.30

$0.30

$0.28

Diluted Earnings Per

Common Share

$0.25

$0.25

$0.30

$0.30

$0.28

Non-performing Loans as

a % of Portfolio Loans

and Leases

1.11%

0.77%

0.78%

0.78%

0.41%

Allowance for Loan and

Lease Losses

1.09%

1.09%

1.18%

1.16%

1.18% |

8

2010 Strategies

Introduce Bryn Mawr

Trust services to First Keystone customers

Focus on the net interest margin

Continued emphasis on strong credit quality

Raise capital as needed

Monitor expenses

Use banking industry turmoil to attract new clients

Opportunistic expansion

Expand our Wealth Management offerings |

Growth Initiatives |

10

Acquisition of First Keystone Financial, Inc. (legal closing completed on

July 1, 2010)

Announced on November 2, 2009

Approximately $500 million in assets

Expands footprint in Delaware and Chester (southeastern PA)

counties with 8 branches

New opportunities for BMTC Wealth Management, Business

Banking, Retail Banking and Mortgage Banking

System conversion was completed on August 23, 2010 and response

has been favorable

8K-A with pro forma financials due by September 14, 2010

Growth Initiatives |

11

Growth Initiatives -

continued

Bryn Mawr

Asset Management

“Lift out”

strategy

Four investment advisers hired

Approximately $200 million in new assets as of June 30, 2010

Additional opportunities being evaluated

Institutional Trust and Escrow Services |

12

BMTC of Delaware

The Delaware Advantage

Generation Skipping Trusts

Directed Trusts

$485 million in assets at June 30, 2010

Branch Office Expansion and Modernization

West Chester Regional Banking Center Branch

Wayne and Paoli branch modernizations completed

Havertown branch modernization scheduled for 2010

Growth Initiatives -

continued |

13

Growth Initiatives -

continued

Small Ticket National Leasing Business

“Lift out”

strategy

Leases outstanding: $40 million at June 30, 2010

Planned lease portfolio reduction of $27 million over the last 12 months.

Goal is to slowly grow the portfolio while maintaining credit quality

Average yield of 10.5%

Quarterly lease charge-offs have continuously decreased since December

31, 2008

Changes made in underwriting standards and collection process have

improved results

Delinquency rate has fallen 72 basis points over the past 12 months

|

14

First

Keystone

Financial,

Inc.

–

Transaction

Summary

Acquirer:

Bryn Mawr

Bank Corporation (NASDAQ: BMTC)

Seller:

First Keystone Financial, Inc. (NASDAQ: FKFS)

Consideration:

Each share of FKFS common stock was exchanged for

0.6973 BMTC shares and $2.06 in cash

Transaction Value:

Board Representation:

Donald Guthrie (Chairman of the FKFS Board of Directors)

joined the BMTC Bank and Holding Company Boards as a

Director

0.6973 BMTC shares

Approximately $32 million (at closing)

Transaction completed on July 1, 2010.

Aggregate

Consideration:

1.63 million shares of BMBC common stock

$4.8 million in cash |

15

First

Keystone

Financial

Inc.

-

Transaction

Highlights

Expands

branch

footprint

into

the

attractive

demographic

markets

of

Delaware

and

Chester

County, Pennsylvania

Important component of strategic plan

Enhances long-term franchise value

Complementary business mix

Both banks have a “community focus”

Significant potential synergies identified in wealth management services and

residential mortgage originations

Transaction elements

Extensive due diligence performed

Conservative credit mark estimated

Achievable cost savings identified

Material earnings per share accretion after expensing merger related costs

Attractive internal rate of return

Pro

Forma

capital

ratios

remain

significantly

above

“well

capitalized”

levels |

Financial Review

Bryn Mawr

Bank Corporation Only

As of June 30, 2010 |

17

Second Quarter 2010 Results

Net Income of $2.4 million

Included are merger and due diligence related costs associated with

the pending merger with First Keystone Financial Inc. of $637

thousand

Diluted earnings per share of $0.25

Wealth Management Assets were $3.1 billion -

up 8.0% from the fourth

quarter of 2009

Revenue from Wealth Management services was $3.9 million -

up 8.4%

from the fourth quarter of 2009 |

18

Second Quarter 2010 Results -

continued

Tax-equivalent net interest margin at 3.80%, a slight decrease from the first

quarter due to lower rates on interest earning assets

Deposit levels of $953.5 million at June 30, 2010 as new core transaction

account openings remain strong

Total loans and leases of $899.3 million at June 30, 2010, an increase of

1.5% from the fourth quarter of 2009

Loan quality strong with non-performing loans and leases of 111 basis

points at June 30, 2010

Investment portfolio was $254.9 million at June 30, 2010 with no

OTTI

charges recorded in the first six months of 2010 or for the years ended

December 31, 2009, 2008 and 2007 |

19

Year to Date Results –

June 30, 2010

Net income of $4.6 million

Included are merger and due diligence related costs associated with

the pending merger with First Keystone Financial Inc. of $985

thousand

Diluted earnings per share of $0.50

Revenue from Wealth Management services was $7.7 million

Tax-equivalent net interest margin at 3.93%

Return on shareholders equity: 8.33%

Return on average assets: 0.76% |

20

Diluted Earnings Per Share

* Excludes $0.10 per share gain on sale of real estate

** Figure includes merger related costs

$1.31

$1.46

$1.48

$1.08

$1.18

$0.50

$0.00

$0.45

$0.90

$1.35

$1.80

2005

2006

2007*

2008

2009**

2010 YTD** |

21

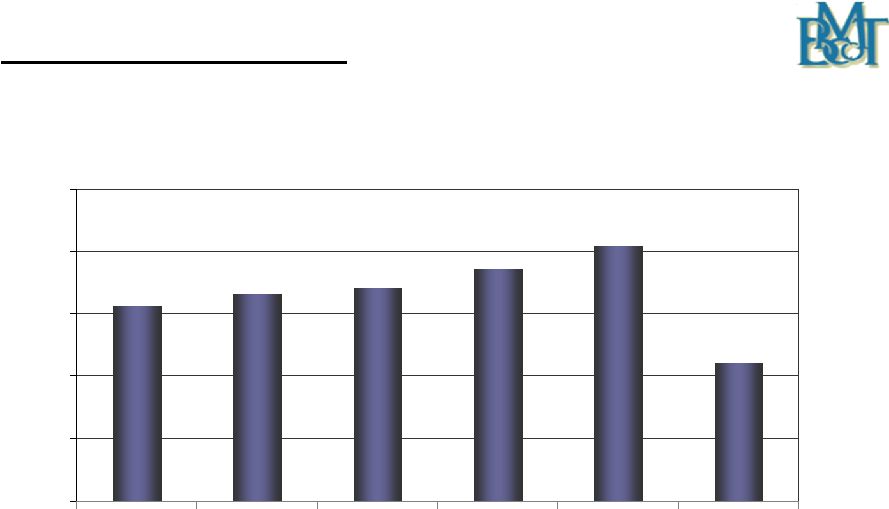

Portfolio Loan & Lease Growth

Total Portfolio Loans & Leases Outstanding

CAGR : 10.5% (2005-2009)

($ in millions)

* Estimated

$595

$681

$803

$900

$886

$899

$1,172

$200

$400

$600

$800

$1,000

$1,200

2005

2006

2007

2008

2009

6/30/10

Pro Forma * |

22

Asset Quality

Asset Quality

2

nd

Qtr

2010

4

th

Qtr

2009

2

nd

Qtr

2009

Non-accrual loans and leases

$9,072

$6,246

$2,913

90+

days

past

due

loans

–

still

accruing

$892

$668

$746

Non-performing loans and leases

$9,964

$6,914

$3,659

Other non-performing assets

$1,970

$1,025

$1,897

Non-performing assets

$11,934

$7,939

$5,556

Non-performing loans and leases / portfolio loans

1.11%

0.78%

0.41%

Non-performing assets / assets

0.94%

0.64%

0.47%

($ in thousands) |

23

Asset Quality

2

nd

Qtr

2010

4

th

Qtr

2009

2

nd

Qtr

2009

Allowance for loan and lease losses

$9,841

$10,424

$10,389

Net loan and lease charge-offs (annualized) /

average loans

0.40%

0.53%

0.64%

Delinquency rate –

loans and leases > 30 days

1.37%

1.10%

0.81%

Delinquent

loans

and

leases

-

30-89

days

$2,481

$2,678

$3,360

Delinquency rate –

loans and leases 30-89 days

0.28%

0.30%

0.38%

TDR’s

excluded from non-performing loans

$2,000

$1,622

$1,562

Allowance for loan and leases losses / loans and

leases

1.09%

1.18%

1.18%

Allowance for loan and lease loss / non-performing

loans and leases

98.8%

150.8%

283.9%

Asset Quality -

continued

($ in thousands) |

24

0.07%

0.12%

0.25%

0.78%

0.78%

1.11%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

2005

2006

2007

2008

2009

6/30/2010 *

Asset Quality -

continued

Non-performing loans and leases as a % of portfolio loans and

leases

* A single commercial relationship in 2010 accounted for 0.64% of the 1.11%.

|

25

Loan Composition at June 30, 2010

$279

$235

$193

$108

$44

$40

Commercial Mortgages

Commercial & Industrial

Home Equity Lines & Loans & Consumer Loans

Residential Mortgages

Construction

Leases

($ in millions) |

26

$31.3

$33.3

$34.2

$37.1

$40.8

$22.2

$0

$10

$20

$30

$40

$50

2005

2006

2007

2008

2009

2010 YTD

Net Interest Income

CAGR: 6.9% (2005-2009)

Note: Not on a tax-equivalent basis

($ in millions) |

27

3.59%

3.72%

3.85%

4.06%

3.80%

3.2%

3.4%

3.6%

3.8%

4.0%

4.2%

Jun-09

Sep-09

Dec-09

Mar-10

Jun-10

Net Interest Margin

On a tax-equivalent basis |

28

Deposit Growth

Average Annual Deposits

($ in millions)

* Estimated

$626

$709

$798

$888

$943

$1,274

$200

$400

$600

$800

$1,000

$1,200

$1,400

2006

2007

2008

2009

2nd Qtr 2010

7/1/2010* |

29

Average Deposits & Borrowed Funds Mix

Second Quarter 2010

$193

$505

$143

$102

$143

$23

Non-Interest Bearing DDA

Savings, NOW & Money Market

Time Deposits

Wholesale Deposits, IND & IDC

Borrowed Funds

Subordinated Debt

($ in millions) |

30

Investment Portfolio as of June 30, 2010

SECURITY DESCRIPTION (AFS)

Amortized

Cost

Fair

Value

Unrealized

Gain / Loss

U.S. Treasury Obligations

$5,013

$5,148

$135

U. S. Government Agency

167,455

168,440

985

State, County & Municipal

25,978

26,316

338

FNMA/FHLMC Mortgage Backed Securities

11,665

12,098

433

GNMA Mortgage Backed Securities

2,490

2,513

23

Foreign Debt Securities

1,250

1,250

-

Bond –

Mutual Funds

38,584

39,123

539

Total Investment Portfolio

$252,435

$254,888

$2,453

Note: Other assets at June 30, 2010 include approximately $8 million of FHLB of

Pittsburgh common stock at cost which is not paying a dividend and cannot be

redeemed. First Keystone Financial has approximately $7 million of FHLB of Pittsburgh stock at July 1, 2010.

($ in thousands)

The combined investment portfolio is estimated to be approximately $356 million on

July 1, 2010 after the acquisition. |

31

Capital Considerations

Bryn Mawr

Bank Corporation elected not to take TARP Capital

Registered Direct Offering closed on May 18, 2010 raising $24.7 million

after deducting fees and expenses

Maintains a “well capitalized”

capital position

Selectively add capital as needed to maintain capital levels and

fund asset

growth and acquisitions

Additional earn out payments for Lau Associates at the end of 2010 and

2011

Active Dividend Reinvestment and Direct Stock Purchase Plan

(DRIP/DSPP) |

32

Capital Position -

Bryn Mawr

Bank Corporation

6/30/2010

12/31/2009

6/30/2009

Tier I

11.50%

9.41%

9.27%

Total (Tier II)

14.50%

12.53%

12.43%

Tier I Leverage

9.98%

8.35%

8.22%

Tangible Common

Equity

9.30%

7.51%

7.43%

Excludes First Keystone Financial, Inc. transaction |

33

Capital Position -

Bryn Mawr

Trust Company (“Bank”)

6/30/2010

12/31/2009

6/30/2009

Tier I

10.72%

9.06%

8.71%

Total (Tier II)

13.73%

12.20%

11.89%

Tier I Leverage

9.29%

8.03%

7.72%

Excludes First Keystone Financial, Inc. transaction |

34

$2.04

$2.18

$2.28

$2.15

$2.87

$3.10

$1.0

$2.0

$3.0

$4.0

2005

2006

2007

2008

2009

6/30/2010

Wealth Management Assets Under Management,

Administration, Supervision and Brokerage

(1)

($ in billions)

(1) Excludes Community Bank’s assets 2005 -

2007 |

35

$11.5

$12.4

$13.5

$13.8

$14.2

$7.7

$2.0

$5.0

$8.0

$11.0

$14.0

$17.0

2005

2006

2007

2008

2009

2010 YTD

Wealth Management Fees

CAGR: 5.4% (2005 –

2009)

($ in millions) |

36

Summary

Outstanding franchise in a stable market

Focus on Wealth Services, Business Banking and Private Banking

Investing in growth opportunities today for earnings growth

tomorrow

Announced acquisition will expand footprint

Sound business strategy, strong asset quality, well capitalized

and solid risk management procedures serve as a foundation for

expansion |

37

This presentation contains statements which, to the extent that they are not

recitations of historical fact may constitute forward-looking statements within

the meaning of the United States Private Securities Litigation Reform Act of

1995. Such forward-looking statements may include financial and other

projections as well

as

statements

regarding

Bryn

Mawr

Bank

Corporation’s

(the

“Corporation”)

that may include future plans, objectives, performance, revenues, growth,

profits, operating expenses or the Corporation’s underlying assumptions. The

words “may”, “would”, “should”,

“could”, “will”, “likely”, “possibly”, “expect,”

“anticipate,”

“intend”, “estimate”, “target”,

“potentially”, “probably”, “outlook”,

“predict”,

“contemplate”,

“continue”,

“plan”,

“forecast”,

“project”

and

“believe”

or

other similar words and phrases may identify forward-looking statements.

Persons reading or present at this presentation are cautioned that such

statements are only predictions, and that the Corporation’s actual future

results or performance may be materially different.

Safe Harbor |

38

Safe Harbor (continued)

Such forward-looking statements involve known and unknown risks and

uncertainties. A number of factors, many of which are beyond the

Corporation’s control, could cause our actual results, events or

developments, or industry results, to be materially different from any future

results, events or developments expressed, implied or anticipated by such

forward-looking statements, and so our business and financial condition

and results of operations could be materially and adversely affected. Such

factors include, among others, our need for capital, our ability

to control

operating costs and expenses, and to manage loan and lease delinquency

rates; the credit risks of lending activities and overall quality of the

composition of our loan, lease and securities portfolio; the impact of

economic conditions, consumer and business spending habits, and real

estate market conditions on our business and in our market area;

changes

in the levels of general interest rates, deposit interest rates,

or net interest

margin and funding sources; changes in banking regulations and policies

and the possibility that any banking agency approvals we might require for

certain activities will not be obtained in a timely manner or at

all or will be |

39

Safe Harbor (continued)

conditioned in a manner that would impair our ability to implement our

business plans; changes in accounting policies and practices; the inability of

key third-party providers to perform their obligations to us; our

ability to attract and retain key personnel; competition in our marketplace;

war or terrorist activities; whether or not we will be able to successfully

integrate First Keystone Bank with The Bryn Mawr

Trust Company; material

differences in the actual financial results, cost savings and revenue

enhancements associated with our acquisition via the merger of First

Keystone Financial, Inc. and First Keystone Bank; and other factors as

described in our securities filings. All forward-looking statements and

information made herein are based on Management’s current beliefs and

assumptions as of the date hereof and speak only as of the date they are

made. The Corporation does not undertake to update forward-looking

statements. |

40

Safe Harbor (continued)

For a complete discussion of the assumptions, risks and uncertainties

related to our business, you are encouraged to review our filings with the

Securities and Exchange Commission, including our most recent annual

report on Form 10-K, as well as any changes in risk factors that we may

identify in our quarterly or other reports filed with the SEC.

This presentation is not an offer to sell securities nor is it soliciting an offer

to buy securities in any state or jurisdiction where the offer or sale would

be unlawful. |

Thank You

Joseph Keefer, EVP

610-581-4869

jkeefer@bmtc.com

Duncan Smith, CFO

610-526 –2466

jdsmith@bmtc.com

Ted Peters, Chairman

610-581-4800

tpeters@bmtc.com

Frank Leto, EVP

610-581-4730

fleto@bmtc.com

Aaron

Strenkoski,

VP

–

Finance,

Investor

Relations

–

610-581-4822

–

astrenkoski@bmtc.com |