Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - ALTERRA CAPITAL HOLDINGS Ltd | d8k.htm |

| EX-10.1 - AMENDMENT NO. 5 TO CREDIT AGREEMENT WITH THE BANK OF NOVA SCOTIA - ALTERRA CAPITAL HOLDINGS Ltd | dex101.htm |

Investor Presentation

Second Quarter 2010

Exhibit 99.1 |

2

Cautionary Note Regarding Forward-Looking Statements

This presentation may include forward-looking statements that reflect Alterra’s current views

with respect to future events and financial performance. Statements that include the words

“expect,” “intend,” “plan,” “believe,” “project,” “anticipate,”

“will,” “may” and similar statements of a future or forward-looking nature

identify forward-looking statements. All forward- looking statements address matters

that involve risks and uncertainties. Accordingly, there are or will be important factors that

could cause actual results to differ materially from those indicated in such statements and you should not place

undue reliance on any such statements.

Alterra believes that these factors include, but are not limited to, the following: (1) the adequacy

of loss reserves and the need to adjust such reserves as claims develop over time; (2) the

failure of any of the loss limitation methods employed; (3) the effects of emerging claims and

coverage issues; (4) changes in general economic conditions, including changes in capital and

credit markets; (5) the effect of competition and cyclical trends, including with respect to demand and pricing

in the insurance and reinsurance markets; (6) any lowering or loss of financial ratings; (7) the

occurrence of natural or man-made catastrophic events with a frequency or severity

exceeding expectations; (8) the loss of business provided to Alterra by its major brokers; (9)

the effect on Alterra’s investment portfolio of changing financial market conditions

including inflation, interest rates, liquidity and other factors; (10) tax and regulatory changes and

conditions; (11) the integration of Harbor Point Limited or new business ventures Alterra may

enter into; and (12) retention of key personnel, as well as management’s response to any

of the aforementioned factors. The foregoing review of important factors should not be construed as exhaustive and should be read in

conjunction with the other cautionary statements that are included herein and elsewhere,

including the Risk Factors included in Alterra’s most recent report on Form 10-K and

Form 10-Qs filed subsequent to, and other documents on file with the Securities and

Exchange Commission. Any forward-looking statements made in this presentation are qualified by these cautionary

statements, and there can be no assurance that the actual results or developments anticipated by

Alterra will be realized or, even if substantially realized, that they will have the expected

consequences to, or effects on, Alterra or its business or operations. Alterra undertakes no

obligation to update publicly or revise any forward-looking statement, whether as a result

of new information, future developments or otherwise. |

Max Capital

Group Ltd. and Harbor Point Limited have merged to form

Alterra Capital Holdings Limited |

Alterra means

“high ground” We have chosen Alterra as our new brand name

as we believe the company will be a provider of

superior security for our clients

A market leader at the pinnacle of our industry |

5

P&C Sector Offers Tremendous Value Opportunity

P&C stocks are trading at 25 year low price to book multiples

The fundamental environment remains challenging BUT we are

getting closer to the inflection point as. . .

Profitable growth opportunities are tough to find

Continued historic low interest rates are pressuring investment returns

Cash flow levels deteriorate

Major industry loss events generate high catastrophe losses

Reserve redundancies at many companies are diminishing

Players beginning to self-assess lines or strategy

Excess capital positions are managed through aggressive share

repurchase

Attractive time to build positions as low sector valuation levels

provide downside protection

Alterra

valuation

even

more

compelling

at

0.74x

times

book

value

at

June

30,

2010

____________________

Based on stock price as of 8/27/2010. |

6

Platform Positioned to Grow Shareholder Value

Alterra

–

A Winning Combination

Formed by the merger of Max Capital and Harbor Point in May 2010

Enhances position with clients and brokers

Combines “best in class" reinsurance group with a global specialty

platform

Provides diversified and stable earnings over time

Established platforms in all major insurance markets

Delivers flexibility to optimize portfolio composition

Larger capital base with approximately $3 billion in equity

Enhances financial flexibility

Strong and deep management and underwriting teams

Committed to growth in book value |

7

Global Diversified Platform

Global underwriter of specialty insurance and

reinsurance

Multiple

operating

platforms

-

Bermuda,

Dublin,

United

States, Lloyd's, Latin America

Diversified business profile across specialty classes

of business

Opportunistic and disciplined underwriting strategy

Strong culture of risk management

Analytical and quantitative underwriting orientation

5 year average combined ratio, with cats, of 86.2%

Strong, liquid balance sheet with conservative

reserving track record

Shareholders equity ~ $3 billion at 6/30/10

Low operating and financial leverage provides

enhanced flexibility

Focus

on

capital

management

–

returned

$367

million

or

~12%

of

proforma

12/31/09

shareholders'

equity(1) in 2010 through dividends and share

repurchases

Rated “A”

(Excellent) by AM Best

____________________

(1) Shareholders' equity of Max Capital and Harbor Point on a

combined pro forma basis.

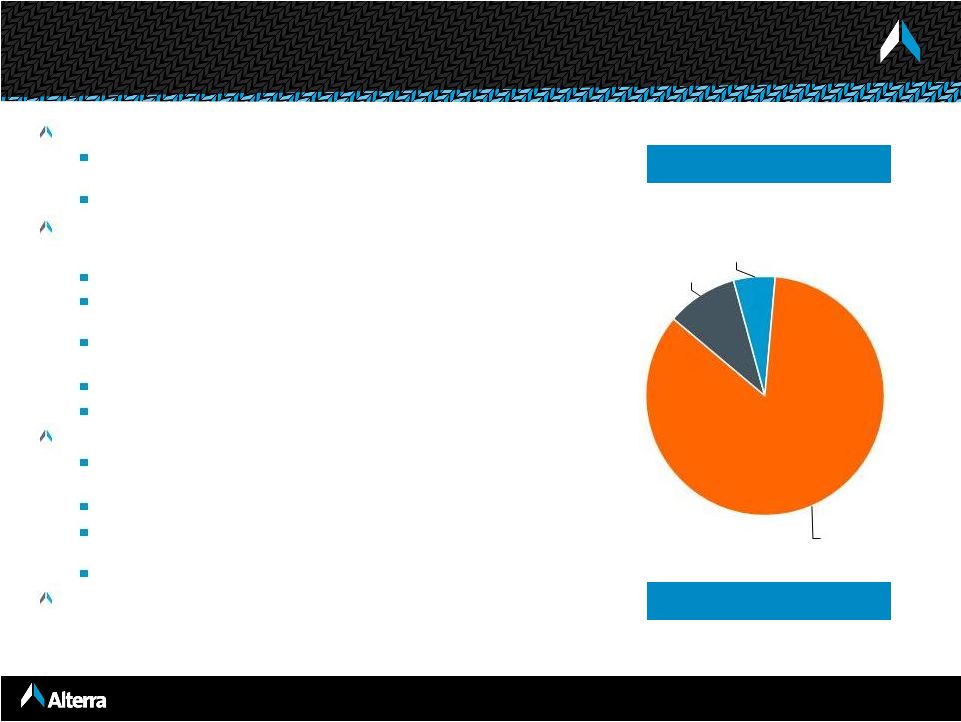

Short- Tail

50%

Long-Tail

50%

2009 Pro Forma

Insurance

39%

Reinsurance

61% |

8

Second Quarter Results

Second quarter 2010 net operating

diluted EPS of $0.64 per share

P&C gross premiums written grew

12% to $398.2 million driven by the

inclusion of Harbor Point and the

continued build-out of our Lloyd’s and

U.S. Specialty businesses

Net investment income up 27.6% to

$53.3 million reflects additional cash

and invested assets from the merger

and the shift from cash to fixed income

picking up additional yield

Combined ratio of 83.3% with solid

underwriting profits across the

organization

Catastrophe losses from Q2 events of

$20.3 million represent < 0.6% of

shareholders’

equity

Diluted book value per share of $24.55

at 6/30/10

P&C GPW

(12% increase)

Operating

Diluted EPS

(1)

Operating ROE

14.6%

10.1%

Combined ratio

90.8%

83.3%

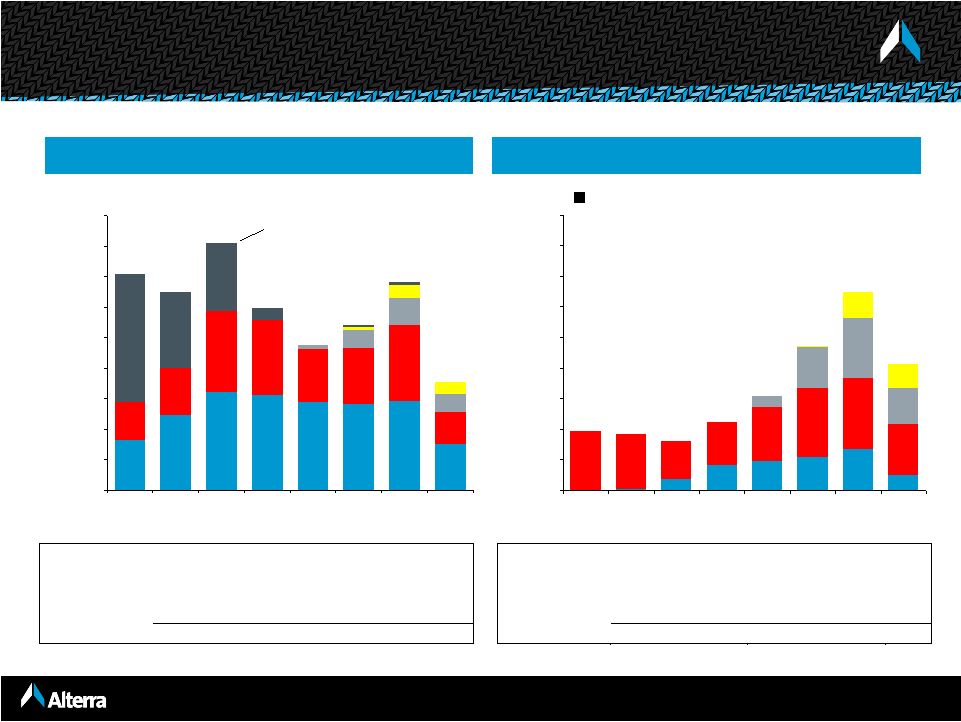

Profitable Growth in Gross Premiums Written…

…With Solid Operating EPS

$0.64

$0.83

Q2 '09

Q2 '10

$398.2

$355.5

Q2 '09

Q2 '10

(1)

Excludes $0.61 per share of negative goodwill gain net of merger and acquisition expenses.

|

9

2004

Insurance

Property

2003

Insurance

Excess Liability

Professional Liability

2005

Reinsurance

Property / Property Cat

Harbor Point formed

2006

Insurance

Aviation

2008

Lloyd's Insurance

Financial Institutions

Prof. Indemnity

Lloyd's Reinsurance

Accident / Health

Property

2007

U.S. E&S Insurance

Property

Inland Marine

U.S. Casualty

Reinsurance

Multi Peril Crop

Experienced &

highly quantitative

underwriting teams

Lead underwriters average over 20 years in the

business

High percentage of employees hold

professional designations

2009

Lloyd's

Casualty (non U.S.)

A&H Insurance

U.S. Specialty

Professional Liability

Latin America

Reinsurance

2002

Traditional Re

Workers' Comp

Medical Malpractice

GL / PL

Aviation

Identifying & Recruiting "Franchise Players" Has Been

Instrumental In Our Success

2010

Alterra

formed

by the merger of Max

Capital and Harbor Point |

10

Reinsurance

Insurance

Lloyd’s

U.S. Specialty Insurance

Major

Classes

Agriculture

Aviation

General casualty

Life and annuity

Marine and energy

Medical malpractice

Professional liability

Property

Surety, credit & political risk

Whole account

Workers’ comp

Aviation

Excess liability

Professional liability

Property

Aviation

Accident and Health

Financial institutions

International casualty

treaty

Personal accident treaty

Professional liability

Property treaty

General liability

Marine

Miscellaneous

professional liability

Property

Operating

Regions

Australia

Canada

European Union

Japan

Latin America

New Zealand

United States

European Union

United States

Denmark

Japan

Latin America

United Kingdom

United States

Offices

Bermuda

Bogotá

Buenos Aires

Dublin

London

New Jersey

Bermuda

Dublin

Hamburg

Zurich

Copenhagen

Leeds

London

Rio de Janeiro

Tokyo

Atlanta

Dallas

New York

Philadelphia

Richmond

San Francisco

Sebastopol

Local Knowledge Global Reach |

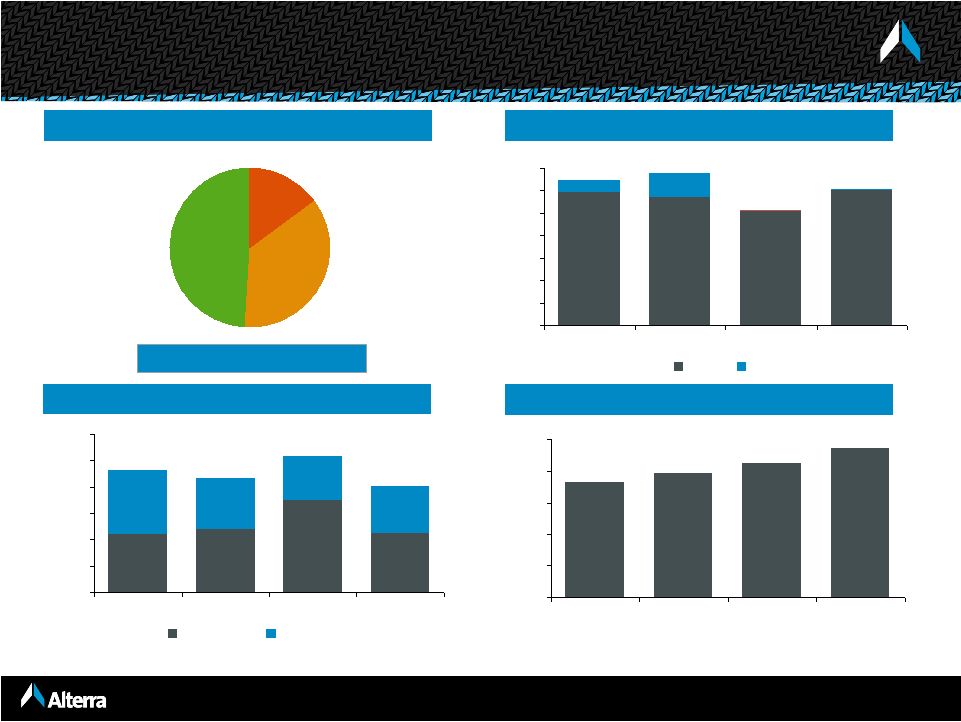

11

9%

4%

9%

4%

7%

5%

19%

28%

6%

9%

Insurance

(22% of pro forma 2009 GPW)

Reinsurance

(55% of pro forma 2009 GPW)

Professional

Liability

Property

Excess

Liability

Aviation

General Casualty

Property

Aviation

Workers Comp.

Professional Liability

Other

Med. Mal.

Marine & Energy

Agriculture

2009 GPW: $427.7 million

2009 pro forma GPW: $1,060.4 million

H1 2010 GPW: $198.7 million

H1 2010 GPW: $657.8 million

= pro forma

16%

27%

42%

15%

Auto

$198.7

$427.8

$389.4

$382.9

$396.6

$0.0

$200.0

$400.0

$600.0

$800.0

$1,000.0

$1,200.0

2006

2007

2008

2009

H1 '10

$423.6

$345.2

$419.5

$489.0

$274.4

$0.0

$200.0

$400.0

$600.0

$800.0

$1,000.0

$1,200.0

2006

2007

2008

2009

H1 '10

$1,060.4

$657.8

____________________

Note:

Pro forma gross premium written (“GPW”) represents the combined GPW of Max Capital

and Harbor Point net of intercompany eliminations of GPW. Alterra Has a Strong

Market Position in Specialty Classes … |

12

U.S. Specialty

(15% of pro forma 2009 GPW)

Alterra

at Lloyd’s

(7% of pro forma 2009 GPW)

…With an Attractive Position in the U.S. Market and Lloyd’s

Professional

Liability

Property

Marine

General

Casualty

Property

Aviation

Fin. Institutions

Prof. Liability

Accident

& Health

47%

1%

21%

31%

47%

15%

18%

2%

18%

H1 2010: $174.4 million

H1 2010: $120.9 million

2009: $285.5 million

2009: $129.0 million

Launched in 2007

Nationwide niche E&S underwriter

91% non-admitted

2009 combined ratio = 99.5%

Acquired in November 2008

Direct and reinsurance

3 syndicates under management

2009 combined ratio = 86.3% |

13

29%

2%

3%

5%

15%

4%

21%

3%

6%

5%

5%

1%

Long-Tail

Short-Tail

North America

Europe

Other

Other Short-Tail

Agriculture

Marine & Energy

Property

Aviation

Auto

Professional

Liability

Medical Malpractice

General Casualty

Workers’

Comp /

Clash

Life + A&H

Whole Account

Reinsurance

Insurance

(1)

6%

16%

78%

Mixed

39%

61%

2009 pro forma GPW = $1,946 million

H1 2010 pro forma GPW = $1,153 million

____________________

Note: 2009 and 2010 pro forma data after intercompany eliminations of gross premiums

written. (1) Includes Reinsurance segment (54.5%), Life &

Annuity reinsurance (2.2%) and reinsurance written through Lloyd’s platform (4.2%).

Diversified Balanced Business Mix

Global Platform

Line of Business |

14

____________________

Source: Company filings.

Diversified reinsurers include RE, AXS, ACGL, TRH, PRE, AWH, ENH, AHL, PTP, AGII, ALTE and ORH

for historical years . Property focused reinsurers include RNR, VR, MRH, FSR and IPCR for historical years.

Diversified Reinsurers

Property Focused Reinsurers

Median

201%

55%

61%

89%

66%

94%

Median

116%

84%

82%

95%

84%

92%

Alterra

106%

86%

88%

92%

88%

92%

Diversified Platforms Generate More Consistent Margins

Alterra

has performed well within its diversified peer group with less volatility than property

focused reinsurers |

15

Peer PML’s

as a Percent of Common Equity

12.3%

12.0%

14.8%

8.9%

24.6%

23.1%

20.6%

21.8%

11.2%

15.0%

17.7%

18.0%

18.1%

19.3%

19.6%

32.2%

30.0%

29.6%

29.1%

0%

10%

20%

30%

40%

VR

FSR

ENH

AXS

ACGL

RE

AHL

PTP

TRH

AWH

1-in-100 Year (if disclosed)

1-in-250 Year

____________________

Note:

RNR,

MRH

and

PRE

do

not

disclose

their

PMLs

for

either

1-in-100

year

events

or

1-in-250

year

events.

(1)

1-in-100 PML and 1-in-250 for U.S. hurricane is $886 mm and $1,159 mm,

respectively. Maximum zonal aggregate is $2.0 billion for U.S. hurricane and California earthquake.

(2)

Self-imposed limit of 25% of total capital.

(3)

1-in-100 PML for U.S. hurricane is $1,091 mm based on an industry loss modeled at $121

billion. 1-in-250 for U.S. hurricane is $1,456 mm based on an industry loss modeled at $195 billion.

(4)

Tri-county Florida is the largest zonal exposure. Northeast wind was $733 mm.

Self-imposed limit of 25% of common equity. (5)

Self-imposed limit of 16% of total capital.

(6)

1-in-100 PML for U.S. wind is $309 mm. 1-in-250 for U.S. quake is $287

mm, and 1-in-250 for U.S. wind of $390 mm. Historically, 1-in-100 was approximately 12% of total capital.

6/30/10

Com. Equity:

$3,602.9

$1,196.3

$2,650.6

$4,995.3

$4,073.0

$6,035.6

$2,950.3

$2,927.0

$2,105.4

$4,049.6

$3,468.5

(1)

(2)

(2), (3)

(4)

(5)

(6) |

16

1.2%

1.3%

1.3%

2.4%

2.1%

2.1%

2.5%

3.2%

3.3%

4.4%

4.1%

4.1%

4.1%

5.4%

6.1%

0.1%

0.2%

0.3%

0.4%

0.3%

0.6%

0.6%

0.6%

0.8%

0.9%

1.0%

0.2%

1.5%

1.3%

1.5%

1.6%

2.4%

2.4%

2.5%

3.1%

3.8%

3.8%

4.4%

5.0%

5.0%

5.1%

5.5%

7.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Initial Estimate

Revised Estimate

2

Losses

$305.7

$95.1

$105.0

$306.0

$60.0

$317.0

$122.7

$112.2

$125.0

$124.0

$77.7

$63.0

$26.0

$58.0

$43.0

____________________

Source: Company filings and press releases; losses are generally

disclosed net of tax and net of reinstatement premiums.

(1)

Q2 net losses reflect only losses from the Chilean earthquake.

Initial losses include the Chilean earthquake and Windstorm Xynthia.

(2)

Q2 net losses reflect Q1 estimates plus reported development, if

any.

(3)

Initial loss estimate reflects 50% to 90% of Reuters consensus net

operating earnings prior to the earthquake, based on disclosure that net income would remain positive for the quarter.

(4)

Initial estimates based on Chile and Xynthia, ultimate losses include the

Chilean, Haitian, and Baja earthquakes, Xynthiaand the Australian hailstorms. Based on international catastrophe losses being two-thirds of

total catastrophe losses as disclosed in the earnings conference

call.

(5)

Initial estimate is as of the first quarter conference call. Both

initial and revised estimates reflect only the Chilean earthquake.

(6)

Pro forma; includes losses from Harbor Point and Max Capital prior to the

merger. Expressed as a percentage of combined 12/31/09 equity prior to the special dividend.

(1)

(2)

(1)

(2)

(3)

(1)(4)

(1)

(2)

(2)(5)

(6)

Chilean Earthquake / Windstorm Xynthia

Ultimate Net Losses as a % of 12/31/09 Common Equity ($ in millions)

Less exposed to swings in the cat market |

17

3

(1)

(3)

(2)

Losses

$256

$140

$276

$140

$135

$165

$287

$384

$171

$125

$148

$155

$113

$257

$50

(4)

____________________

Source: Company filings, as of 12/31/08. Losses are generally disclosed net of reinstatement

premiums. (1)

Results reflect Ike only.

(2)

Equity includes preferred, which subsequently converted to common.

(3)

Equity includes preferred, which subsequently converted to common.

(3)

TRH does not disclose specific losses but did lose "$169.7 million principally relating to

Hurricane Ike." $170

$305

Revised Estimate

Initial Estimate

(2)

Ike

/

Gustav

Ultimate

Net

Losses

as

a

%

of

6/30/08

Common

Equity

($

in

millions)

3.4%

3.8%

3.0%

4.2%

5.2%

6.0%

6.4%

7.2%

5.2%

7.8%

3.7%

5.3%

6.7%

8.3%

10.1%

6.6%

8.0%

4.4%

4.3%

0.0%

0.6%

2.2%

3.0%

4.3%

0.3%

2.6%

0.7%

0.3%

0.8%

0.8%

1.8%

0.8%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

12.4%

11.0%

10.1%

8.9%

8.9%

8.4%

8.1%

8.1%

7.8%

7.2%

7.0%

6.3%

6.0%

5.0%

4.8%

4.6%

3.4%

VR

FSR

RNR

MRH

IPCR

PTP

ACGL

AXS

PRE

HP

AHL

ENH

ORH

TRH

AWH

RE

MXGL

Less exposed to swings in the cat market (cont’d) |

18

Florida wind

1 in 100 year event -

$370 million net loss

Industry loss -

$104 billion

California earthquake

1 in 250 year event -

$398 million net loss

Industry loss -

$41 billion

Europe wind

1 in 100 year event -

$239 million net loss

Industry loss -

$17 billion

PML’s

In-force as of July 1, 2010 |

19

Highlights

Insurance

Focus on the higher risk classes that are less price sensitive

Growth will be limited to select profitable opportunities

Benefit from strong client relationships with high renewal retentions in the mid 80’s

Reinsurance

Diverse portfolio with high ratings positions us well

Pull back where pricing softens

Latin America

Emerging market with significant natural organic growth

Seasoned team with strong market relationships and profitable track record

Lloyd’s/London

Continue to recruit new teams to build out the diversity of the platform

Recent additions in international casualty reinsurance and marine and personal accident

US Specialty

Market conditions getting more competitive

Strong distribution relationships help to generate a flow of business

Selectively underwrite new business

Declining volume in more commodity classes

Strategy to Navigate the Soft Cycle |

20

$149.6

$293.7

$282.6

$289.0

$313.7

$321.0

$245.9

$163.2

$108.0

$247.1

$184.1

$173.5

$243.2

$265.2

$154.0

$126.4

$56.6

$88.4

$59.8

$12.3

$41.9

$43.7

$7.0

$10.0

$9.4

$40.7

$225.4

$248.7

$419.7

$0.0

$100.0

$200.0

$300.0

$400.0

$500.0

$600.0

$700.0

$800.0

$900.0

$543.0

$709.3

$648.6

$811.6

$597.6

$469.0

$682.9

$356.1

2003

2004

2005

2006

2007

2008

2009

H1 '10

Lloyd's

--

--

--

--

--

NM

15.0%

U.S. Specialty

--

--

--

--

274.7%

46.5%

9.0%

Reinsurance

(6.1%)

(30.7%)

11.6%

27.1%

27.4%

2.6%

(13.4%)

Insurance

--

--

141.7%

13.4%

13.5%

25.7%

(15.2%)

Total

(5.0%)

(12.8%)

39.6%

38.1%

52.7%

38.2%

(2.7%)

____________________

(1)

Excludes non-traditional, which is composed of structured contracts that Max stopped

writing in 2003. Short tail lines contributed to 83% of total growth

over the 3 years to 2009

Strong Cycle Management Discipline

Long Tail (GPW)

Short Tail (GPW)

($ in millions)

Non-Traditional

Year over year growth:

Year over year growth:

Lloyd's

--

--

--

--

--

NM

101.1%

U.S. Specialty

--

--

--

--

386.2%

47.8%

35.4%

Reinsurance

(1)

21.8%

72.2%

(8.3%)

(28.7%)

6.1%

34.2%

(20.6%)

Insurance

50.7%

30.5%

(2.3%)

(7.9%)

(2.2%)

3.9%

(8.6%)

Total

38.1%

46.6%

(5.0%)

(14.7%)

12.4%

26.1%

(2.5%)

$49.1

$134.1

$106.7

$94.0

$82.9

$34.3

$2.2

$166.4

$231.9

$226.0

$177.4

$139.6

$125.1

$180.5

$192.3

$117.8

$197.1

$134.5

$35.9

$79.1

$85.3

$1.9

$0.0

$100.0

$200.0

$300.0

$400.0

$500.0

$600.0

$700.0

$800.0

$900.0

$192.3

$182.7

$159.4

$222.5

$307.3

$469.1

$648.4

$412.4

2003

2004

2005

2006

2007

2008

2009

H1 '10 |

21

Conservative Reserve Position with High % of IBNR

50%

44%

36%

34%

28%

24%

24%

56%

64%

66%

72%

76%

76%

76%

50%

$278

$189

$1,471

$1,240

$279

$232

$1,987

$1,275

$0

$500

$1,000

$1,500

$2,000

$2,500

Q2 2010

Q4 2009

Q2 2010

Q4 2009

Q2 2010

Q4 2009

Q2 2010

Q4 2009

Case

IBNR

24%

Insurance

Reinsurance

Alterra at Lloyd's

U.S. Specialty

($ in millions)

____________________

Note: Includes the results of Harbor Point from May 12, 2010, the closing date of

the merger. |

22

43%

39%

27%

31%

29%

57%

61%

73%

69%

71%

$3,773

$3,178

$2,938

$2,334

$2,335

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

2006

2007

2008

2009

Q2 2010

Case Reserves

IBNR

Favorable Reserve

Development

$5.9

$45.1

$90.8

$77.2

$41.2

Development as a % of

Net Reserves

0.3%

1.9%

3.0%

2.4%

1.1%

Consistently Favorable

Reserve Development

Net Loss Reserves

($ in millions)

____________________

Note: Reserve development and net reserves prior to May 12, 2010 are for Max Capital

only. |

23

High Quality Conservative Investment Portfolio

Alterra

maintains a high quality, liquid portfolio

94.4% of portfolio in fixed income/cash, which consists of highly

rated securities

Assets are generally matched to liabilities

Cycle

management

extends

to

investments

–

current

posture

is defensive

Cash balance reduced to $741.7 million or 9.6% of portfolio

Current average fixed income duration of approximately

3.98 years including the impact of cash (4.41 without cash)

60.3% of the cash and fixed maturities portfolio is held in cash,

government / agency-backed securities, or AAA securities

70.8% of fixed income portfolio rated AA or better

Hedge fund investments are marked-to-market

Minimal exposure to selected asset classes

CMBS

of

$357.4

million

(4.6%

of

portfolio)

–

average

rating

of

AA+/Aa1

ABS of $98.3 million (1.3% of portfolio)

RMBS

of

$1,115.6

million

(14.4%

of

portfolio)

–

91.2%

agency-

backed

No CDO’s, CLO’s, SIV’s

or other highly structured securities

Fixed income portfolio has had meaningfully lower OTTI

losses than peers

Carrying Value $7.7 billion

June 30, 2010

Fixed Income

84%

Cash

10%

Hedge Funds

6% |

24

0.25x

0.50x

0.75x

1.00x

1.25x

1.50x

1.75x

2.00x

8/27/00

10/6/01

11/16/02

12/27/03

2/5/05

3/17/06

4/27/07

6/6/08

7/17/09

8/27/10

Valuations Have Trended to a Historical Low

Price to Trailing Book Value (10 Years)

Average: 1.24x

Peers: 0.79x

Current valuations

are at a 36%

discount to the

long term average

Alterra: 0.74x

Alterra trades at a

40% discount to

the long term peer

average |

25

We believe we can generate an average ROE of 13% to 15% across the cycle

____________________

Note:

Primary price / book multiple as of 8/27/10.

Alterra

Offers a Compelling Story

Well established operating platforms provide full access to business

Diversified portfolio of business across casualty and property lines

Specialty orientation with a balance of insurance vs. reinsurance

Opportunistic approach –

nimble and responsive to market trends

Defensive, high quality investment portfolio

Invested asset leverage will drive more consistent returns

Balance sheet strength with low leverage / financial flexibility

Attractive

entry

point

–

current

price

/

book

value

of

0.74x |

26

Alterra

means "high ground" —

a place of security

Alterra

Capital Holdings Limited

Bermuda

Ireland

United States

Lloyd’s

Latin America |

27

Appendices |

28

June 30,

December 31,

2010

2009

Cash & Fixed Maturities

7,296

$

4,944

$

Other Investments

437

315

Premium Receivables

780

567

Losses Recoverable

962

1,001

Other Assets

500

513

Total Assets

9,975

$

7,341

$

Property & Casualty Losses

3,773

$

3,178

$

Life & Annuity Benefits

1,209

1,373

Deposit

Liabilities 148

153

Funds Withheld

120

140

Unearned Premium

1,090

628

Bank Loan

200

-

Senior Notes

90

90

Other Liabilities

418

213

Total Liabilites

7,048

$

5,775

$

Shareholders' Equity

2,927

1,565

9,975

$

7,340

$

Strong

Balance Sheet

($ in millions)

(1)

Results for the six months ended June 30, 2010 includes results from Harbor Point

following the close of the merger on May 12, 2010. |

29

Half Year Results Comparison

($ in millions)

Six months ended

(1)

Pro forma six months ended

(2)

June 30,

June 30,

June 30,

June 30,

2010

2009

2010

2009

Gross Premiums Written

770

$

831

$

1,153

$

1,227

$

Net Premiums Earned

488

419

706

684

Net Investment Income

102

82

126

119

Net Realized and Unrealized Gains (Losses) on Investments

(8)

40

-

43

Other Than Temporary Impairment Charges

(1)

(2)

(1)

(2)

Other Income

-

2

1

3

Total Revenues

581

541

832

847

Total Losses, Expenses & Taxes

441

453

702

664

Net Income

140

$

88

$

130

$

183

$

Net Operating Income

99

$

95

$

Property & Casualty Underwriting

Loss Ratio

58.6%

65.4%

Expense Ratio

27.6%

24.9%

Combined Ratio

86.2%

90.3%

(1) Results for the six months

ended June 30, 2010 include results from Harbor Point following the close of the merger on May 12, 2010.

(2)

Pro forma information is provided for informational purposes only, to present a summary of the

combined results of operations assuming the amalgamation with Harbor Point had occurred on

January 1, 2009. The pro forma information assumes the elimination of intercompany transactions and the amortization of certain

acquisition accounting fair value adjustments. The pro forma information does not necessarily

represent results that would have occurred if the amalgamation had taken place on January 1,

2009, nor is it necessarily indicative of the future results. |

30

Six months ended June 30, 2010

($ in millions)

Differences in table due to rounding. Includes results from Harbor Point following the close of

the merger on May 12, 2010. (1)

Property and Casualty only.

Diversified Operating

Platform

Life &

Property & Casualty

Annuity

Corporate

Consolidated

Alterra

at

Insurance

Reinsurance

U.S. Specialty

Lloyd's

Total

Reinsurance

Gross premiums written

$198.7

$274.4

$174.4

$120.9

$768.5

$1.7

$0.0

$770.1

Reinsurance premiums ceded

(84.8)

(58.7)

(56.1)

(33.2)

(232.8)

(0.1)

0.0

(232.9)

Net premiums written

$113.9

$215.7

$118.3

$87.7

$535.7

$1.5

$0.0

$537.2

Earned premiums

196.9

270.5

149.9

77.7

695.1

1.7

0.0

696.7

Earned premiums ceded

(90.9)

(35.0)

(68.6)

(14.6)

(209.1)

(0.1)

0.0

(209.2)

Net premiums earned

$106.0

$235.5

$81.4

$63.2

$486.0

$1.5

$0.0

$487.5

Net investment income

$12.4

$24.6

$2.7

$5.1

$44.8

$25.5

$31.4

$101.7

Net realized and unrealized gains (losses) on investments

0.2

0.2

0.0

(1.5)

(1.0)

4.1

(11.4)

(8.4)

Net impairment losses recognized in earnings

0.0

0.0

0.0

0.0

0.0

0.0

(0.7)

(0.7)

Other income

0.0

0.2

0.1

0.4

0.6

0.0

0.1

0.6

Total revenues

$118.6

$260.4

$84.1

$67.1

$530.3

$31.1

$19.4

$580.7

Net losses and loss expenses

$73.2

$132.5

$50.4

$28.7

$284.8

$0.0

$0.0

$284.8

Claims and policy benefits

0.0

0.0

0.0

0.0

0.0

31.6

0.0

31.6

Acquisition costs

0.5

47.6

12.8

11.8

72.8

0.3

0.0

73.0

Interest expense

0.5

5.1

0.0

0.0

5.5

4.0

3.3

12.9

Net foreign exchange losses

0.0

0.5

0.0

(3.9)

(3.4)

0.0

0.3

(3.1)

Merger and acquisition expenses

0.0

0.0

0.0

0.0

0.0

0.0

(49.8)

(49.8)

General and administrative expenses

12.4

23.8

16.5

8.5

61.2

1.3

24.7

87.2

Total losses and expenses

86.6

209.5

79.7

45.1

420.9

37.2

(21.5)

436.5

Income before taxes

$32.0

$51.0

$4.4

$22.0

$109.4

($6.1)

$40.9

$144.2

Loss ratio

69.1%

56.3%

62.0%

45.4%

58.6%

Acquisition cost ratio

0.5%

20.2%

15.7%

18.7%

15.0%

General and administrative expense ratio

11.6%

10.1%

20.2%

13.5%

12.6%

Combined ratio

(1)

81.2%

86.6%

97.9%

77.6%

86.2% |

31

Shareholders’

Equity ($ in millions)

Premiums Written ($ in millions)

Combined Ratio

2009 Gross Premiums Written

Casualty

Property

Specialty

NPW

GPW

Loss & LAE Ratio

Expense Ratio

Total = $608 Million

49%

36%

15%

$642.6

$672.5

$511.7

$607.5

$601.9

$506.8

$567.9

$590.4

$0

$100

$200

$300

$400

$500

$600

$700

2006

2007

2008

2009

49.1%

38.7%

33.3%

36.3%

44.3%

69.9%

47.3%

43.7%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

2006

2007

2008

2009

86.0%

92.8%

103.2%

80.6%

$1,889.7

$1,691.5

$1,579.0

$1,461.9

$0

$400

$800

$1,200

$1,600

$2,000

2006

2007

2008

2009

Historic Harbor Point –

Financial Highlights |

32

Property

Casualty

Specialty

Total

2009 GPW: $296 million

2009 GPW: $221 million

2009 GPW: $91 million

2009 GPW: $608 million

Per Risk

Catastrophe

Excess of Loss

Crop

Quota Share

Marine/Energy

Credit

Multi-line

Aviation

Property

Casualty

Specialty

Quota

Share

5%

20%

75%

14%

86%

26%

16%

4%

31%

23%

49%

36%

15%

$220.9

$225.3

$313.4

$220.4

$0

$100

$200

$300

$400

2006

2007

2008

2009

$295.9

$246.6

$282.3

$296.3

$0

$100

$200

$300

$400

2006

2007

2008

2009

$90.8

$39.8

$76.8

$126.0

$0

$100

$200

$300

$400

2006

2007

2008

2009

$607.5

$511.7

$672.5

$642.6

$0

$100

$200

$300

$400

$500

$600

$700

$800

2006

2007

2008

2009

Historic Harbor Point –

Financial Highlights (Cont’d) |

33

Premiums Written ($ in millions)

2009 Gross Premiums Written

Shareholders’

Equity ($ in millions)

Combined Ratio

Loss & LAE Ratio

Expense Ratio

U.S. Specialty

Max at Lloyd’s

Life & Annuity

Reinsurance

Insurance

Reinsurance

Total = $1,375 million

36%

31%

3%

9%

21%

$865.2

$1,078.3

$1,254.3

$1,375.0

$634.7

$796.6

$840.2

$894.5

$0

$300

$600

$900

$1,200

$1,500

2006

2007

2008

2009

18.7%

24.2%

23.0%

25.7%

62.4%

68.9%

64.0%

67.7%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

2006

2007

2008

2009

88.2%

86.4%

91.9%

88.1%

NPW

GPW

$1,564.6

$1,280.3

$1,583.9

$1,390.1

$0

$400

$800

$1,200

$1,600

$2,000

2006

2007

2008

2009

Historic Max –

Financial Highlights |

34

14.7%

(10.0%)

20.7%

17.3%

1.0%

15.8%

(20.0%)

(10.0%)

0.0%

10.0%

20.0%

30.0%

2004

2005

2006

2007

2008

2009

88%

92%

88%

86%

106%

94%

0%

20%

40%

60%

80%

100%

120%

2004

2005

2006

2007

2008

2009

$3.62

($2.54)

$4.81

$3.52

$0.19

$2.70

($4.00)

($2.00)

$0.00

$2.00

$4.00

$6.00

2004

2005

2006

2007

2008

2009

Gross Premiums Written ($ in millions)

P&C Combined Ratio

Operating Diluted EPS(1)

Operating ROE

(1)

Excludes merger and acquisition related revenue and expenses.

$44

$242

$302

$45

$275

$212

$0

$300

$600

$900

$1,200

$1,500

Life

P&C

$1,044

$1,246

$865

$1,078

$1,254

$1,375

2004

2005

2006

2007

2008

2009

Historic Max Results |

35

$1,565

$1,280

$1,584

$1,390

$1,186

$903

$28.01

$22.94

$27.54

$23.06

$20.16

$19.70

$0

$300

$600

$900

$1,200

$1,500

$1,800

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

Shareholders' Equity

Book Value per Share

2004

2005

2006

2007

2008

2009

$0.38

$0.36

$0.32

$0.24

$0.18

$0.12

$0.00

$0.10

$0.20

$0.30

$0.40

2004

2005

2006

2007

2008

2009

Investment

Leverage

Shareholders' Equity

Book Value per Share

Invested Assets ($ in millions)

Shareholders Equity and BVPS ($ in millions)

Operating Cash Flow ($ in millions)

Dividends

$5,259

$3,515

$4,228

$4,536

$5,123

$5,357

3.4x

3.9x

3.6x

3.3x

3.2x

4.2x

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

Invested Assets

Leverage

2004

2005

2006

2007

2008

2009

$193

$482

$228

$405

$442

$799

$0

$200

$400

$600

$800

$1,000

2004

2005

2006

2007

2008

2009

Historic Max Results (cont’d) |