Attached files

| file | filename |

|---|---|

| 8-K - COPANO ENERGY FORM 8-K - Copano Energy, L.L.C. | form8-k.htm |

September 2010 Investor

Presentation

Presentation

NASDAQ: CPNO

Disclaimer

This presentation includes “forward-looking statements,” as defined in the federal securities laws.

Statements that address activities, or events that Copano believes will or may occur in the future are

forward-looking statements. These statements include, but are not limited to, statements about future

producer activity and Copano’s total distributable cash flow and distribution coverage. These statements

are based on management’s experience and perception of historical trends, current conditions, expected

future developments and other factors management believes are reasonable.

Statements that address activities, or events that Copano believes will or may occur in the future are

forward-looking statements. These statements include, but are not limited to, statements about future

producer activity and Copano’s total distributable cash flow and distribution coverage. These statements

are based on management’s experience and perception of historical trends, current conditions, expected

future developments and other factors management believes are reasonable.

Important factors that could cause actual results to differ materially from those in the forward-looking

statements include the following risks and uncertainties, many of which are beyond Copano’s control:

The volatility of prices and market demand for natural gas and natural gas liquids; Copano’s ability to

continue to obtain new sources of natural gas supply and retain its key customers; the impact on

volumes and resulting cash flow of technological, economic and other uncertainties inherent in

estimating future production and producers’ ability to drill and successfully complete and attach new

natural gas supplies and the availability of downstream transportation systems and other facilities for

natural gas and NGLs; higher construction costs or project delays due to inflation, limited availability of

required resources, or the effects of environmental, legal or other uncertainties; general economic

conditions; the effects of government regulations and policies; and other financial, operational and legal

risks and uncertainties detailed from time to time in Copano’s quarterly and annual reports filed with the

Securities and Exchange Commission.

statements include the following risks and uncertainties, many of which are beyond Copano’s control:

The volatility of prices and market demand for natural gas and natural gas liquids; Copano’s ability to

continue to obtain new sources of natural gas supply and retain its key customers; the impact on

volumes and resulting cash flow of technological, economic and other uncertainties inherent in

estimating future production and producers’ ability to drill and successfully complete and attach new

natural gas supplies and the availability of downstream transportation systems and other facilities for

natural gas and NGLs; higher construction costs or project delays due to inflation, limited availability of

required resources, or the effects of environmental, legal or other uncertainties; general economic

conditions; the effects of government regulations and policies; and other financial, operational and legal

risks and uncertainties detailed from time to time in Copano’s quarterly and annual reports filed with the

Securities and Exchange Commission.

Copano undertakes no obligation to update any forward-looking statements, whether as a result of new

information or future events.

information or future events.

2

Introduction to Copano

Independent midstream company founded in 1992

■ Best in class service to customers

■ Entrepreneurial approach

■ Focus on long-term accretive growth

Provides midstream services in multiple producing areas through

three operating segments

three operating segments

■ South and north Texas

● Conventional, Eagle Ford Shale and Barnett Shale Combo play

■ Central and Eastern Oklahoma

● Conventional, Hunton De-Watering play and Woodford Shale

■ Rocky Mountains

● Powder River Basin

3

Key Metrics

Service throughput volumes approximate 1.8 Bcf/d of natural gas(1)

Over 6,700 miles of active pipelines

8 natural gas processing plants with over 1.1 Bcf/d of combined

processing capacity

processing capacity

One NGL fractionation facility with total capacity of 22,000 Bbls/d

Equity market cap: $1.8 billion(2)

Enterprise value: $2.8 billion(3)

4

(1) Based on 2Q 2010 results. Includes unconsolidated affiliates.

(2) As of August 24, 2010.

(3) As of August 24, 2010. Includes $300 million of convertible preferred equity issued July 2010.

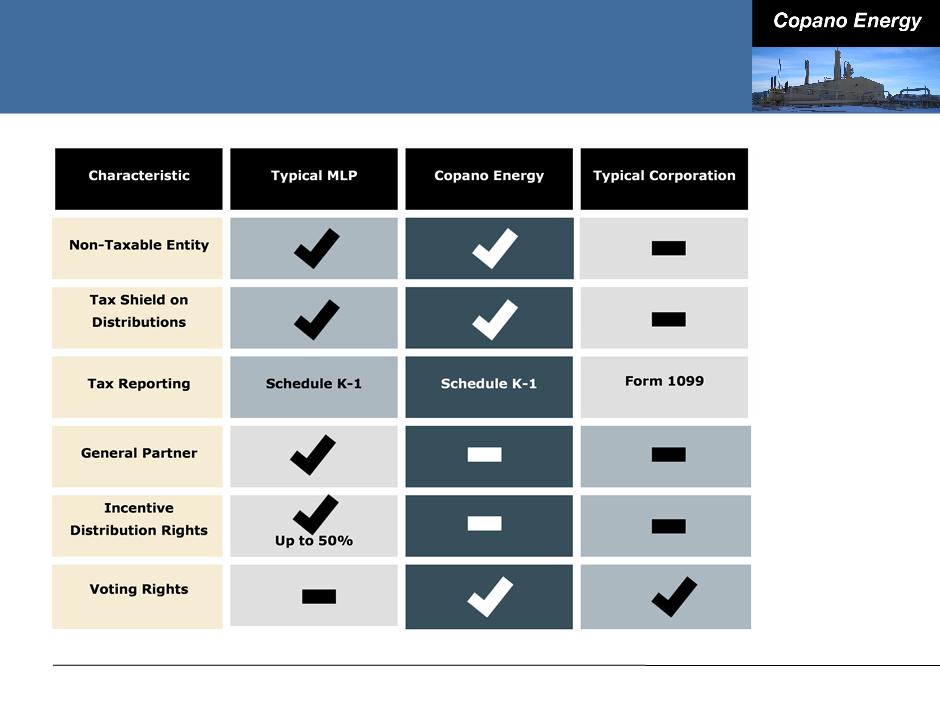

Copano’s LLC Structure

5

Growth Strategy

Goal: to become a diversified midstream company with scale and

stability of cash flows, above-average returns on invested capital

and “investment-grade quality distributions”

stability of cash flows, above-average returns on invested capital

and “investment-grade quality distributions”

Key tenets of growth strategy:

■ Execute on organic growth opportunities around existing assets

■ Explore opportunities beyond traditional gathering and processing

● Be more proactive in seeking assets and opportunities

■ Reduce sensitivity of cash flows to commodity price fluctuations

● Hedging program

● Contracts - increase fee-for-service component

6

Agenda

7

|

2010 Outlook

|

Commodity Prices and

Margin Sensitivities |

|

Financing and

Commodity Risk Management |

Conclusions

|

2010 Outlook

Texas

■ Significant drilling and development activity in the Barnett Shale Combo play

■ Ramp up of Eagle Ford Shale directed drilling

Oklahoma

■ Moderate drilling activity behind the Hunton De-Watering play

■ Strong drilling activity in the Woodford Shale play

Rocky Mountains

■ Minimal new drilling; flat volumes

Commodity prices

■ Lower forward price curves for NGLs and oil compared to early 2010

Total Distributable Cash Flow (Total DCF)

■ Second half 2010 - improvement compared to first half

■ Beyond 2010 - until volumes from new projects come online in second half of

2011, Total DCF estimated to be lower than comparable 2010 periods due to

current forward prices and lower average strike prices on hedges

2011, Total DCF estimated to be lower than comparable 2010 periods due to

current forward prices and lower average strike prices on hedges

8

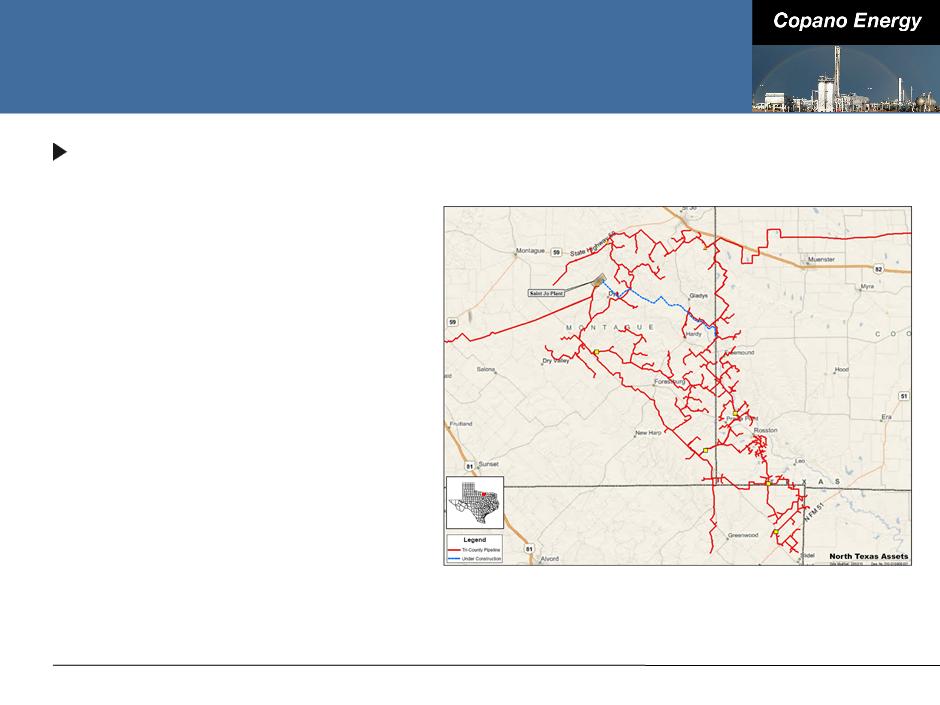

Texas Outlook

Saint Jo gathering system

■ 15 rigs running in the area with

as many as 2 more anticipated

later this year

as many as 2 more anticipated

later this year

● Leasing activity continues

■ Crude oil play with associated

gas requiring a full slate of

midstream services

gas requiring a full slate of

midstream services

■ Based on producer drilling

schedule, expect steady

increase in plant inlet volumes

in 2010

schedule, expect steady

increase in plant inlet volumes

in 2010

● 2Q 2010 average volumes of

approximately 40,000

MMbtu/d vs. 24,000 MMbtu/d

in 1Q 2010

approximately 40,000

MMbtu/d vs. 24,000 MMbtu/d

in 1Q 2010

9

Texas Outlook

Eagle Ford Shale play

■ Copano’s current asset base strategically positioned

● Houston Central complex located within 50 miles of the rich gas core of the

play

play

■ 22,000 BPD fractionator placed in service April 2010

■ 9 Eagle Ford Shale wells connected to date and expect to connect 8 - 10

additional wells over the next three months

additional wells over the next three months

■ Expect Eagle Ford Shale volume increases in 3Q 2010

■ Currently pursuing multiple gathering and related downstream opportunities

10

Texas Recent Developments

Saint Jo plant

■ Earlier this year, executed key producer

contract with highly rated producer

contract with highly rated producer

● Long-term gathering, treating and

processing agreement

processing agreement

● Fee-for-service contract

■ Additional 50 MMcf/d of compression

expected to be in service early 4Q

2010, bringing total plant capacity to

100 MMcf/d

expected to be in service early 4Q

2010, bringing total plant capacity to

100 MMcf/d

● Plant fully committed

● Additional expansion under

consideration

consideration

■ $30 - $35 million in fee-based cash flow

expected by year-end 2010 (on an

annualized basis)

expected by year-end 2010 (on an

annualized basis)

11

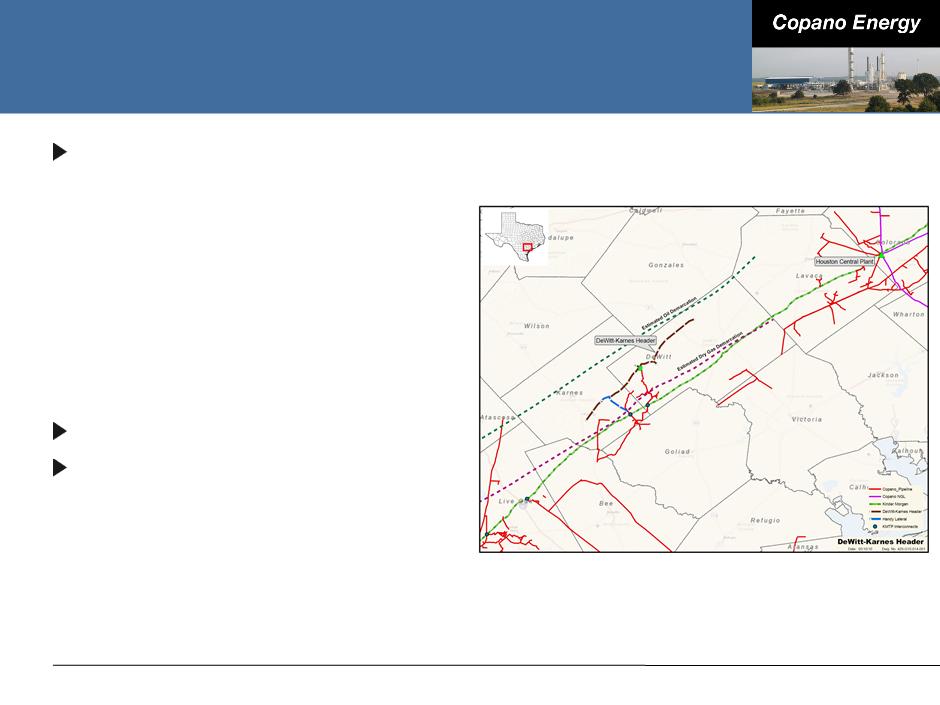

DeWitt-Karnes Header

Nearing completion of

previously announced DeWitt-

Karnes header

previously announced DeWitt-

Karnes header

■ 38 miles of 24” pipe

■ Initially 185 MMcf/d of capacity with

ability to expand to 275 MMcf/d

ability to expand to 275 MMcf/d

■ Active producers in the vicinity

include: Pioneer, ConocoPhillips,

Petrohawk, GeoSouthern and

Enduring Resources

include: Pioneer, ConocoPhillips,

Petrohawk, GeoSouthern and

Enduring Resources

11 rigs running in the area

Average IP rates of wells

connected are approximately

7.6 MMcfe/d

connected are approximately

7.6 MMcfe/d

■ Approximately 3.5 MMcf/d of gas

■ Approximately 500 - 1,000 BPD of

condensate

condensate

12

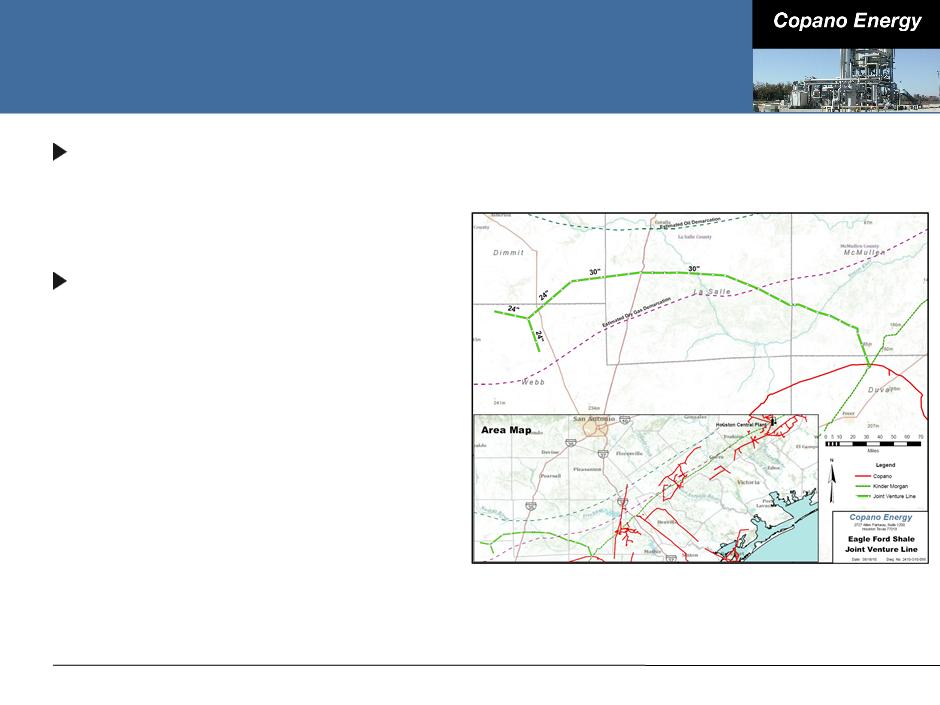

Eagle Ford Gathering Joint Venture

Executed joint venture

agreements with Kinder

Morgan in May 2010

agreements with Kinder

Morgan in May 2010

Gas services agreement

between Copano/Kinder

Morgan joint venture and SM

Energy signed in July 2010

between Copano/Kinder

Morgan joint venture and SM

Energy signed in July 2010

■ Kicked off pipeline construction -

expected to be completed

summer 2011

expected to be completed

summer 2011

■ Approximately 85 miles of 30”

and 24” pipe

and 24” pipe

■ Anticipated capex (net to

Copano) - approximately $68.5

million

Copano) - approximately $68.5

million

13

Texas Fractionation Facility

Responding to NGL transportation and fractionation constraints

along the Texas Gulf Coast, Copano started its fractionator at

Houston Central complex and began to deliver purity products to

market in April 2010

along the Texas Gulf Coast, Copano started its fractionator at

Houston Central complex and began to deliver purity products to

market in April 2010

■ Total capacity of 22,000 Bbls/d

■ Approximate cost of $17 million

■ Estimated fee-based cash flow between $8 and $10 million on an

annualized basis at current throughput volumes

annualized basis at current throughput volumes

Incremental processing and fractionation capacity is expected to

be required to meet producer demands in the Eagle Ford Shale

be required to meet producer demands in the Eagle Ford Shale

14

Oklahoma Outlook

Rich gas (primarily Hunton De-Watering play)

■ Drilling activity increased so far in 3Q 2010

■ 2 rigs currently running in the Hunton and 15 rigs in other rich gas areas

■ Attractive processing upgrade and low geologic risk

■ 3Q 2010 volumes expected to be slightly up vs. 2Q 2010

Lean gas (primarily Woodford Shale)

■ Drilling remains active

■ 5 rigs currently running

■ 3Q 2010 volumes expected to be higher than 2Q 2010

15

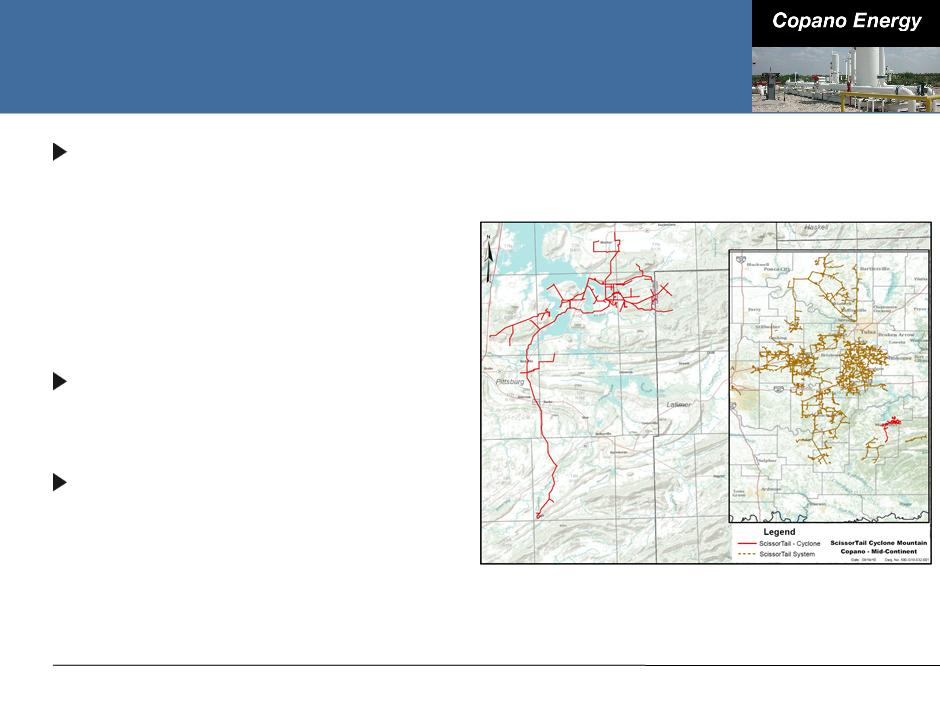

Woodford Shale Activity

Significant drilling activity in the

Woodford Shale around

Copano’s Cyclone Mountain

system

Woodford Shale around

Copano’s Cyclone Mountain

system

■ 2Q 2010 average volumes of

approximately 58,000 MMbtu/d vs.

53,000 MMbtu/d in 1Q 2010

approximately 58,000 MMbtu/d vs.

53,000 MMbtu/d in 1Q 2010

Primarily lean gas that requires

compression and CO2 treating

compression and CO2 treating

Current system capacity

approximately 80 MMcf/d with

plans to expand to 120 MMcf/d

by year-end 2010

approximately 80 MMcf/d with

plans to expand to 120 MMcf/d

by year-end 2010

■ Gathering and treating expansion

project of $10 million to be placed

in service 4Q 2010

project of $10 million to be placed

in service 4Q 2010

16

Rocky Mountains Outlook

Drilling and dewatering will be driven by commodity prices and

producer economics

producer economics

3Q 2010 volumes for Bighorn expected to be slightly lower to flat vs.

2Q 2010

2Q 2010

3Q 2010 volumes for Fort Union expected to be slightly higher vs. 2Q

2010

2010

2010 Adjusted EBITDA expected to be essentially flat vs. 2009

17

Commodity Prices and Margin Sensitivities

18

|

2010 Outlook

|

Commodity Prices and

Margin Sensitivities |

|

Financing and

Commodity Risk Management |

Conclusions

|

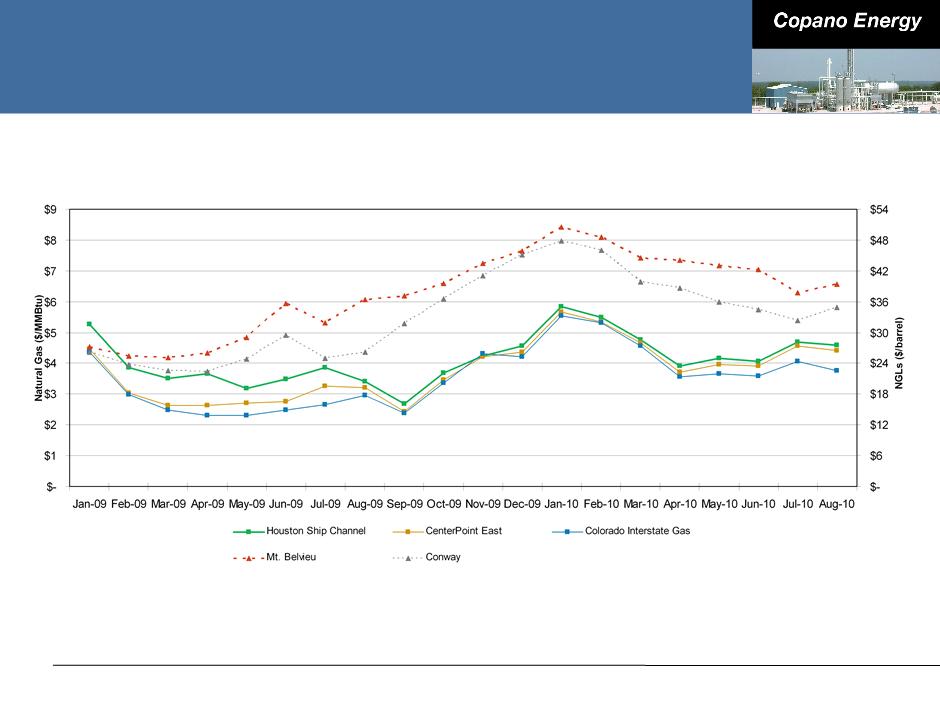

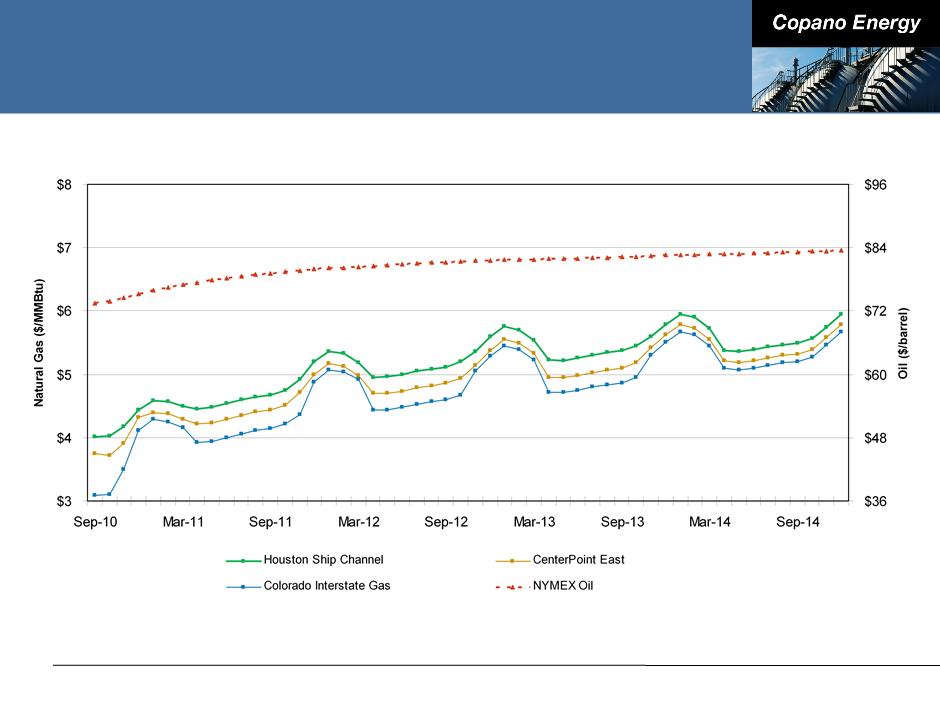

Historical Commodity Prices

19

(1) Aug-10 NGL prices are month-to-date through Aug 20, 2010.

(2) NGL prices for Jan-09 through Jun-10 are calculated based on the weighted-average product mix for the period indicated. NGL prices for Jul-10 through

Aug-10 are calculated based on the second quarter 2010 product mix.

Aug-10 are calculated based on the second quarter 2010 product mix.

Forward Commodity Prices

20

Note: Forward prices as of August 20, 2010

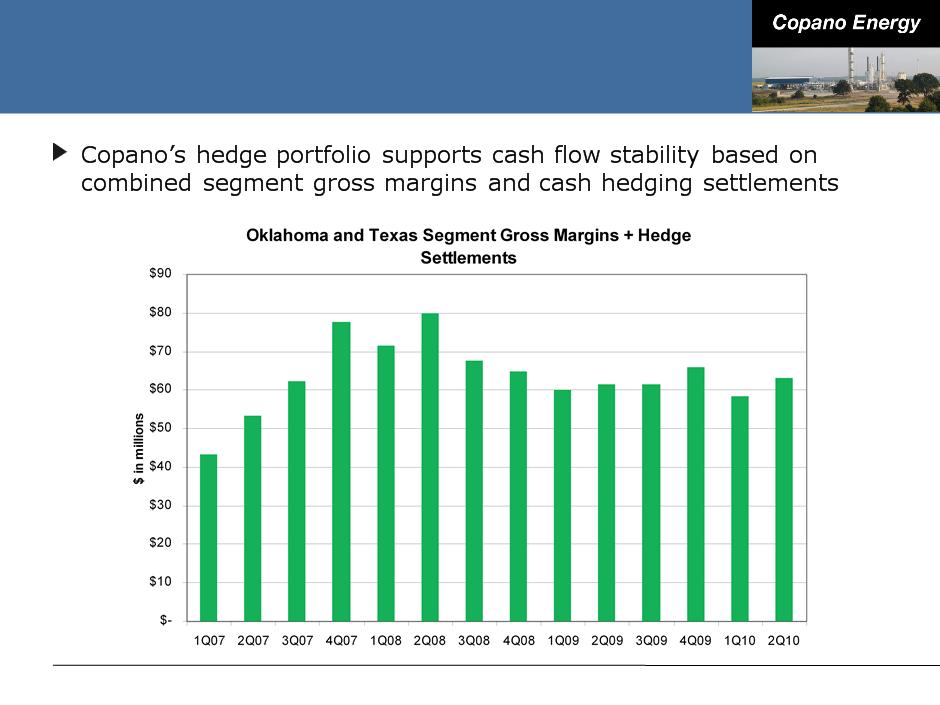

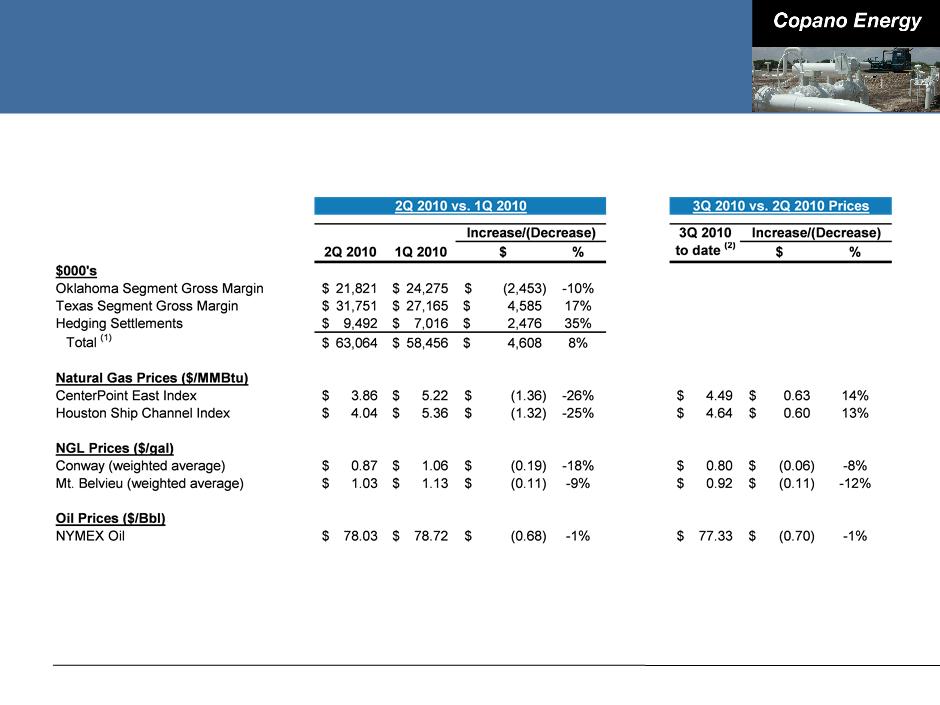

Combined Commodity-Sensitive Segment

Margins and Hedging Settlements

Margins and Hedging Settlements

21

Financing and Commodity Risk Management

22

|

2010 Outlook

|

Commodity Prices and

Margin Sensitivities |

|

Financing and

Commodity Risk Management |

Conclusions

|

2010 Expansion Capex

2010 capital expansion budget increased from $130 million(1) in

January to $172 million(1) today

January to $172 million(1) today

Major areas of focus include:

■ Eagle Ford Shale and Houston Central complex in south Texas

● DeWitt-Karnes pipeline

● Copano/Kinder Morgan joint venture

■ Saint Jo processing plant and pipelines in north Texas

■ Cyclone Mountain system in Oklahoma - Compression and amine treating

expansion

expansion

Expect capital to be invested at a multiple of approximately 5x

Pursuing another $300 million(1) in projects that Copano believes

will develop over the next two years

will develop over the next two years

23

(1) Includes Copano’s net share for unconsolidated affiliates.

Recent Preferred Equity Offering

In July 2010 Copano issued $300 million of convertible preferred

equity to affiliate of TPG Capital

equity to affiliate of TPG Capital

■ Priced at $29.05 per unit - 10% premium to the 30-day volume weighted

average price as of July 19, 2010

average price as of July 19, 2010

■ Distributions paid in-kind for the first three years ($0.72625 per unit)

■ Convertible to common units on a one for one basis beginning July 2013

unless conversion would cause pro forma distribution coverage to fall below

100%

unless conversion would cause pro forma distribution coverage to fall below

100%

■ Copano can force conversion beginning July 2013 if market price for common

units is at least $37.77 per unit

units is at least $37.77 per unit

■ No mandatory redemption

Alignment with a strategic capital partner that has a long-term

investment prospective

investment prospective

Flexible capital to fund Eagle Ford Shale expansion strategy and

other growth initiatives in Texas and Oklahoma

other growth initiatives in Texas and Oklahoma

24

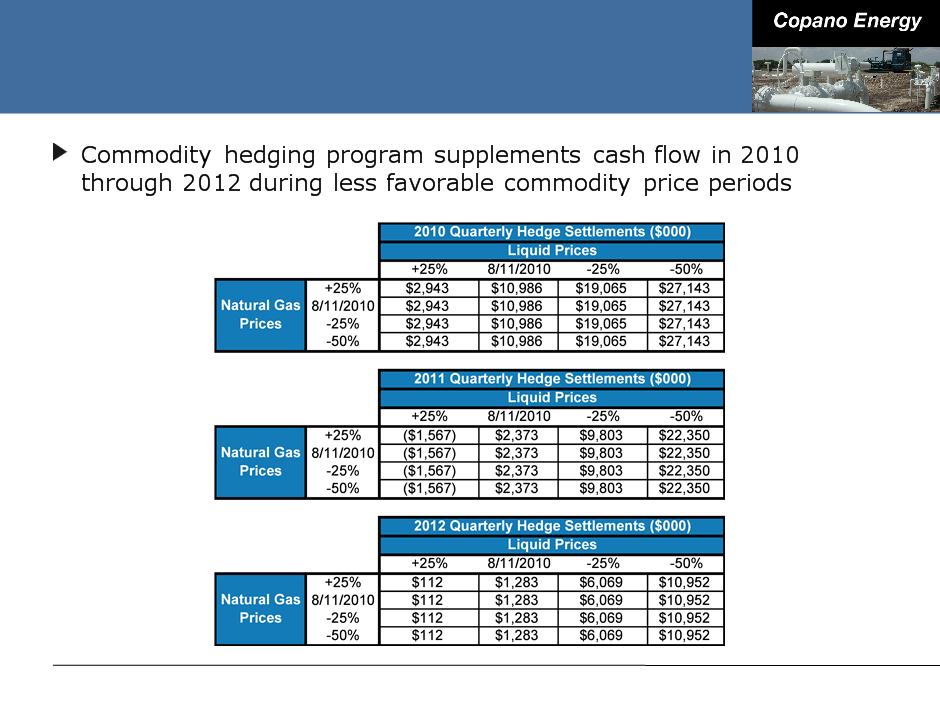

Hedging Strategy

Option-based, product-specific

2010 price exposed volumes are well hedged

■ Between 70% and 80% of propane, butane, natural gasoline and condensate

price exposure is hedged

price exposure is hedged

■ Approximately 40% of ethane price exposure is hedged

■ Expect $32 - $34 million of non-cash amortization expense in 2010 related to

option component of hedge portfolio

option component of hedge portfolio

2011 hedged at or near policy limits, except for ethane

■ During April and August, added puts for WTI, iso-butane and normal butane

for calendar years 2011 and 2012 (total cost of approximately $6.8 million)

for calendar years 2011 and 2012 (total cost of approximately $6.8 million)

Will continue adding to 2012 hedging positions and begin focusing

on 2013 later this year

on 2013 later this year

25

Conclusions

26

|

2010 Outlook

|

Commodity Prices and

Margin Sensitivities |

|

Financing and

Commodity Risk Management |

Conclusions

|

Conclusions

Growth projects recently completed are expected to contribute to

Total DCF as volumes come online

Total DCF as volumes come online

■ Volumes at Saint Jo plant increasing

■ Start-up of fractionator at Houston Central complex

■ Burbank plant in service

■ Portions of DeWitt-Karnes header in service

Significant future growth opportunities

■ Expansion of Saint Jo plant to 100 MMcf/d expected early 4Q 2010

■ Completion of DeWitt Karnes header expected late 3Q 2010

■ Completion of Eagle Ford Gathering joint venture in western Eagle Ford Shale

expected summer 2011

expected summer 2011

■ Anticipating future infrastructure needs, including processing plant

expansions, fractionation expansion and additional gas and liquids pipelines

expansions, fractionation expansion and additional gas and liquids pipelines

Ample liquidity and access to capital to support growth initiatives

27

Appendix

28

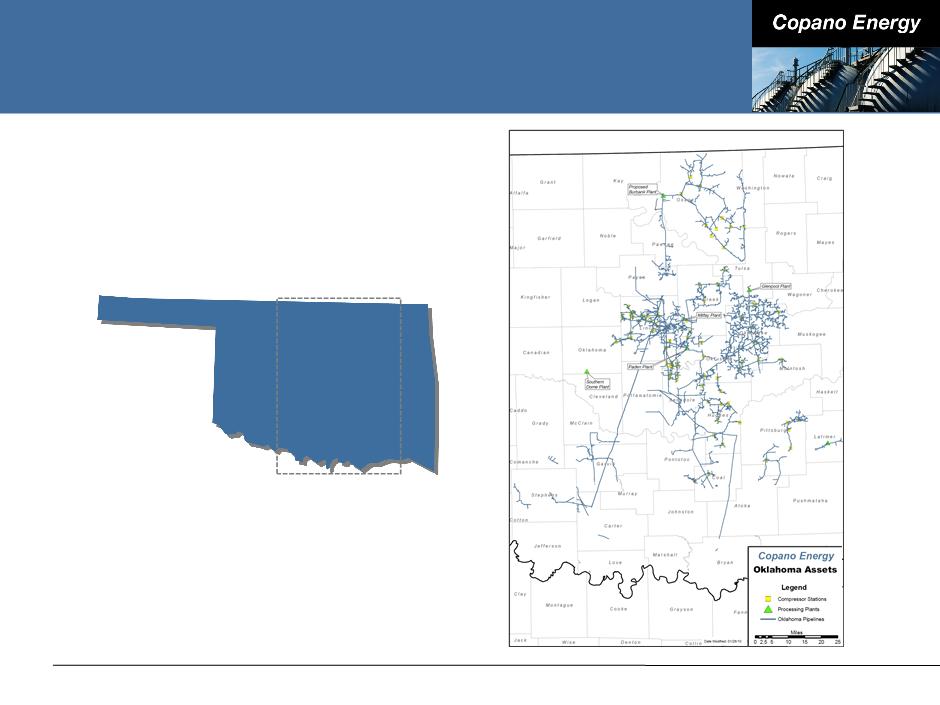

Oklahoma Assets

29

OKLAHOMA

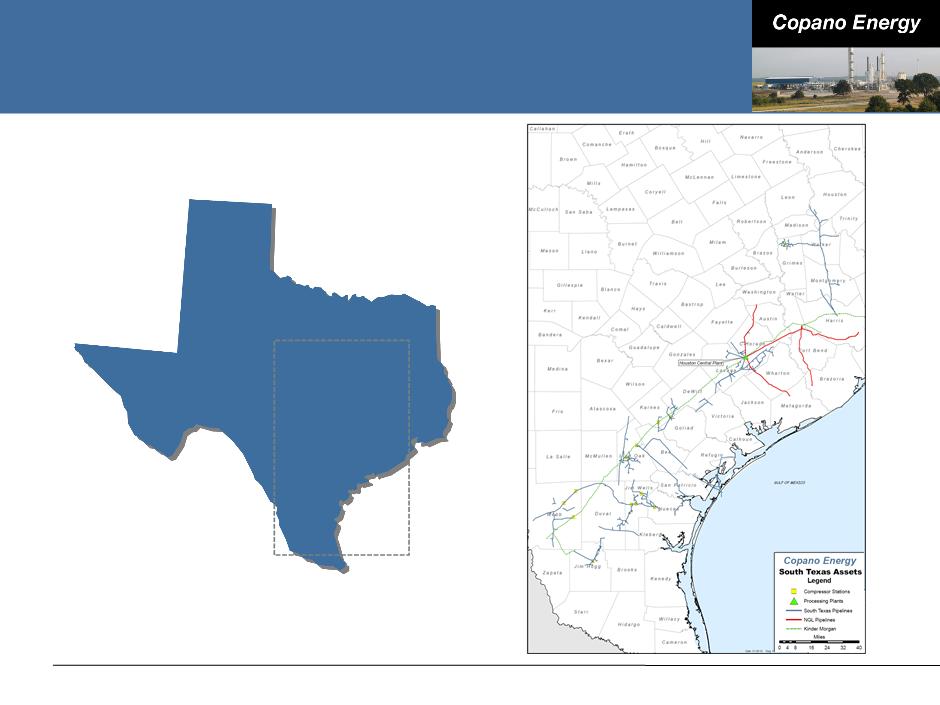

South Texas Assets

30

TEXAS

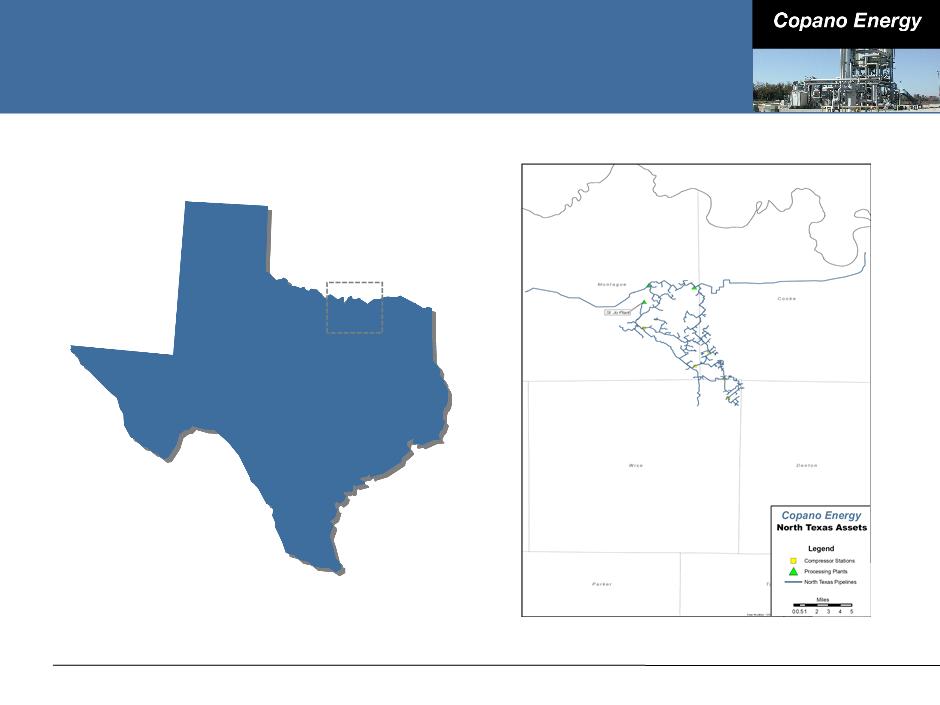

North Texas Assets

31

TEXAS

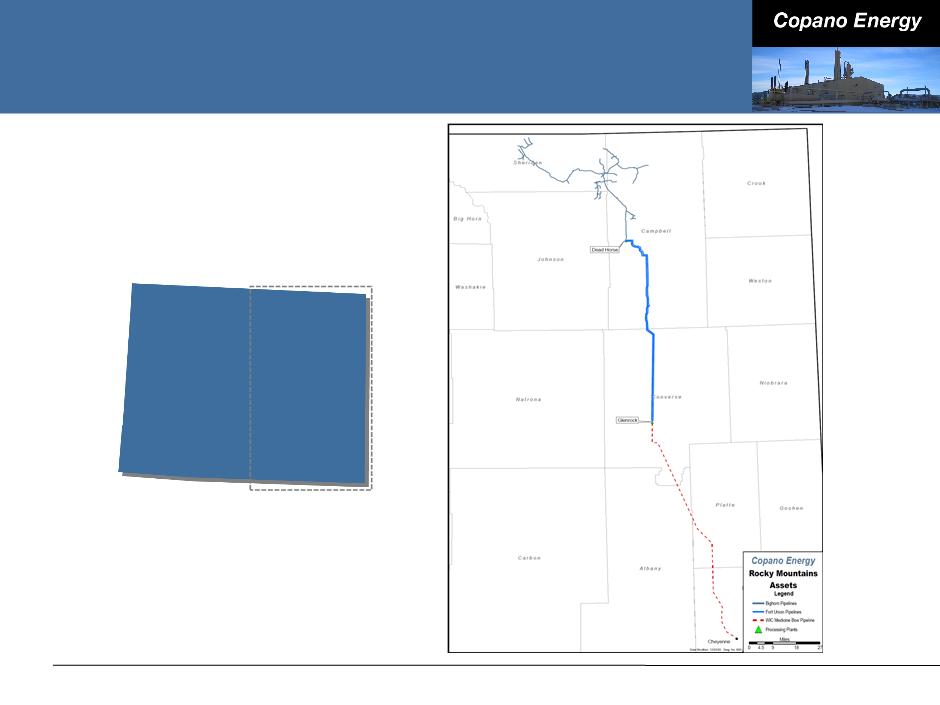

Rocky Mountains Assets

32

WYOMING

Processing Modes

33

|

Full Recovery

|

|

|

|

Texas and Oklahoma - If the value of

recovered NGLs exceeds the fuel and gas shrinkage costs of recovering NGLs |

|

Ethane Rejection

|

|

|

|

Texas and Oklahoma - If the value of ethane

is less than the fuel and shrinkage costs to recover ethane (in Oklahoma, ethane rejection at Paden plant is limited by nitrogen rejection facilities) |

|

Conditioning Mode

|

|

|

|

Texas - If the value of recovered NGLs is less

than the fuel and gas shrinkage cost of recovering NGLs (available at Houston Central plant and at Saint Jo plant) |

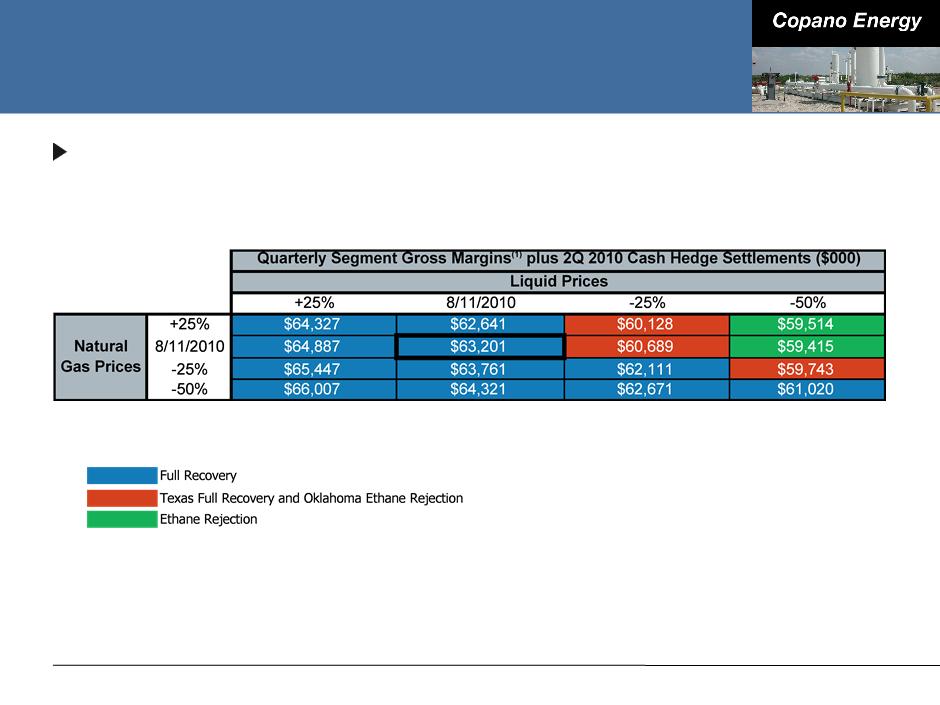

Commodity-Related Margin Sensitivities

Matrix reflects 2Q 2010 wellhead and plant inlet volumes, adjusted

using Copano’s 2010 planning model

using Copano’s 2010 planning model

34

Note: Please see this Appendix for definitions of processing modes and additional details.

(1) Consists of Texas and Oklahoma Segment gross margins.

Combined Commodity-Sensitive Segment

Margins and Hedging Settlements

Margins and Hedging Settlements

35

Note: Weighted average NGL prices are based on Copano product mix for period indicated.

(1) Does not include non-cash expenses included in Corporate and Other for purposes of calculating Total Segment Gross Margin. See Appendix for reconciliation

of Total Segment Gross Margin.

of Total Segment Gross Margin.

(2) Reflects the average of July and August (as of August 23, 2010) prices.

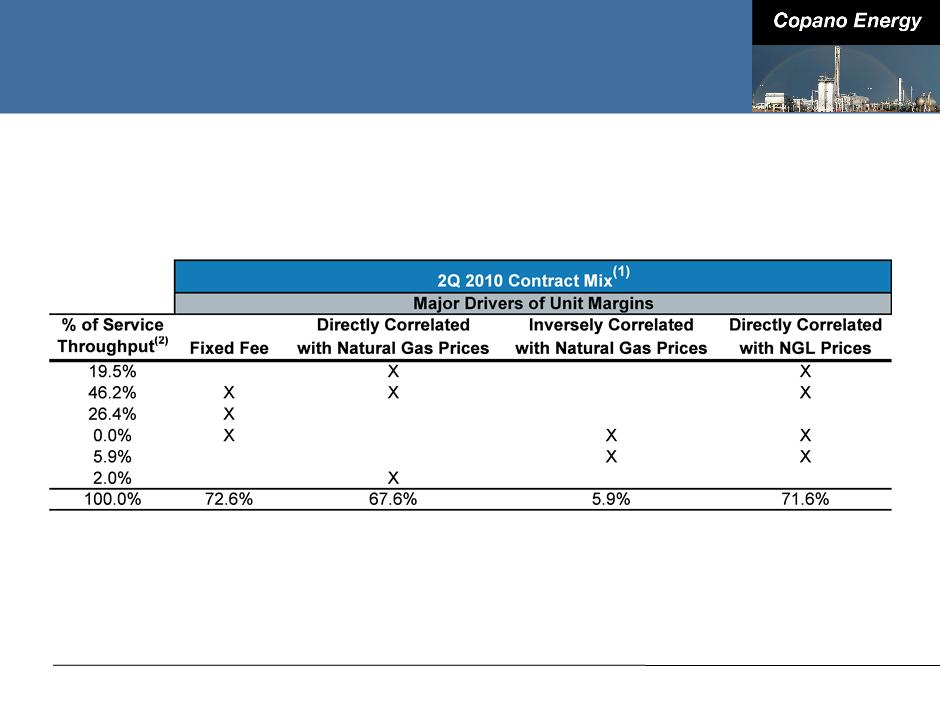

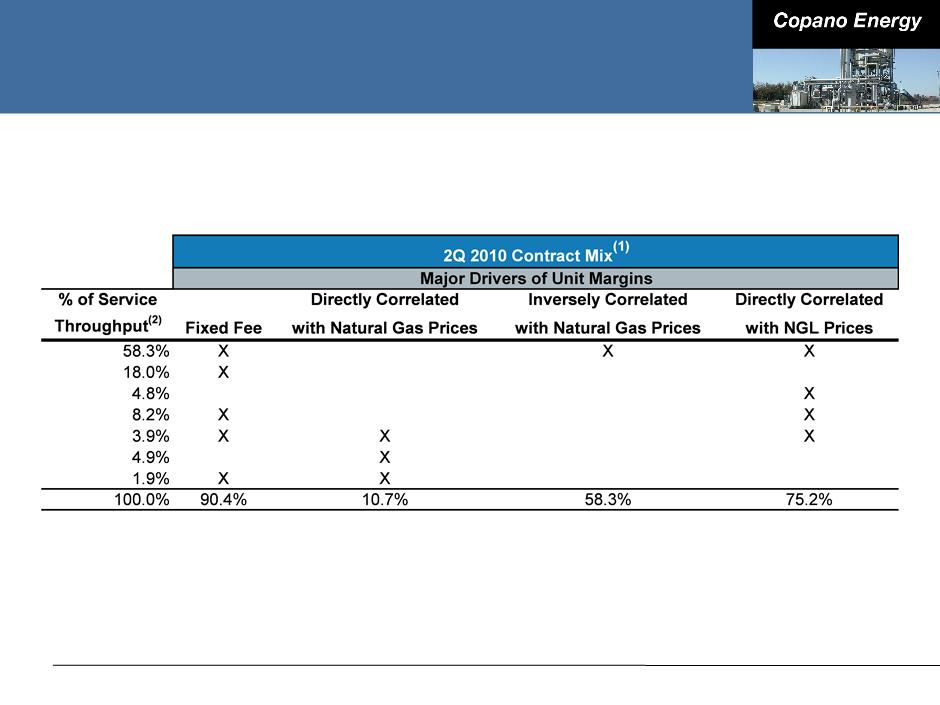

Oklahoma Contract Mix

36

(1) Source: Copano Energy internal financial planning models for consolidated subsidiaries.

(2) Excludes 12,689 MMBtu/d service throughput for Southern Dome, a majority-owned affiliate.

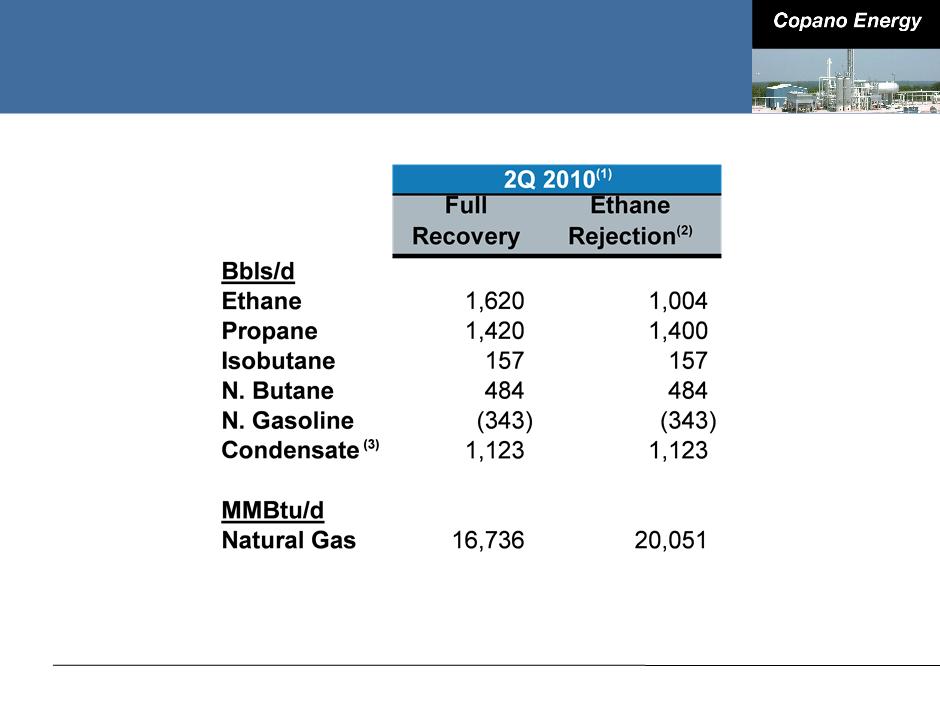

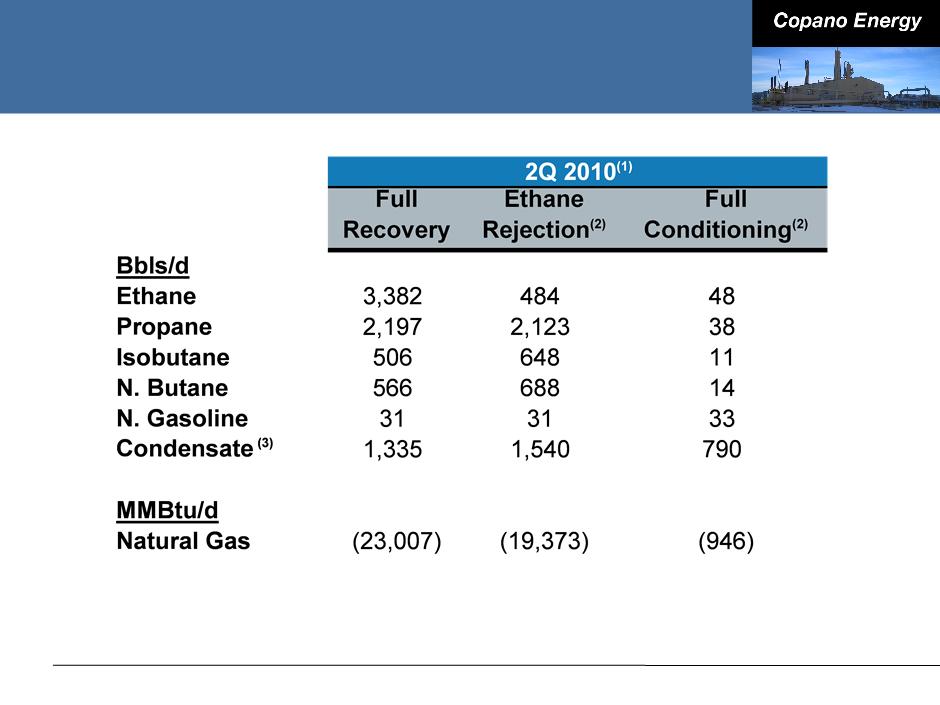

Oklahoma Net Commodity Exposure

37

Note: See explanation of processing modes in this Appendix. Values reflect rounding.

(1) Source: Copano Energy internal financial planning models for consolidated subsidiaries.

(2) Ethane rejection at Paden plant is limited by nitrogen rejection facilities.

(3) Reflects impact of producer delivery point allocations, offset by field condensate collection and stabilization.

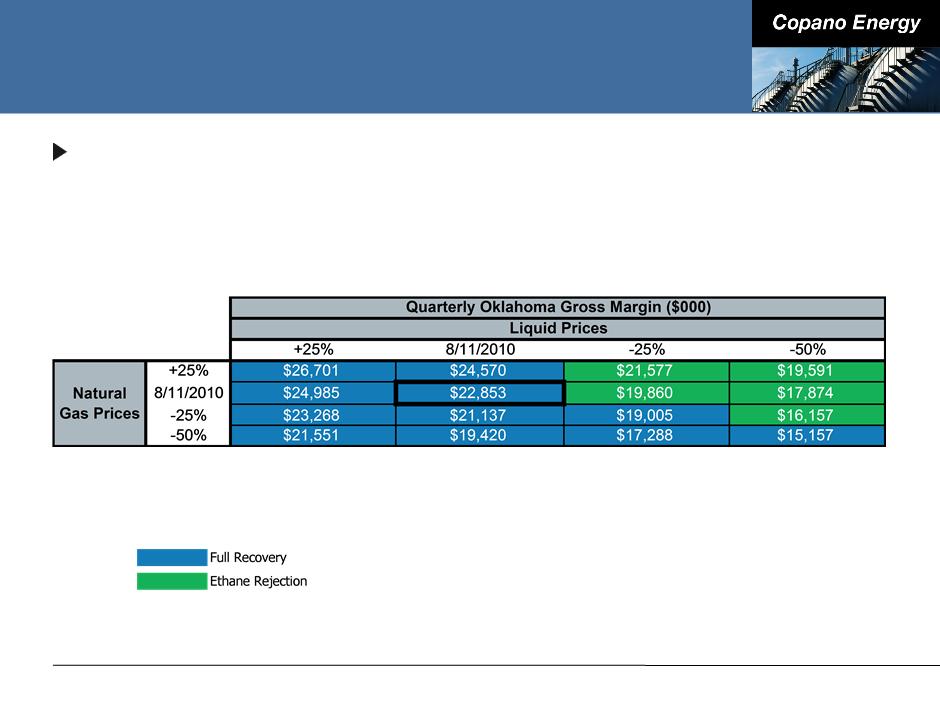

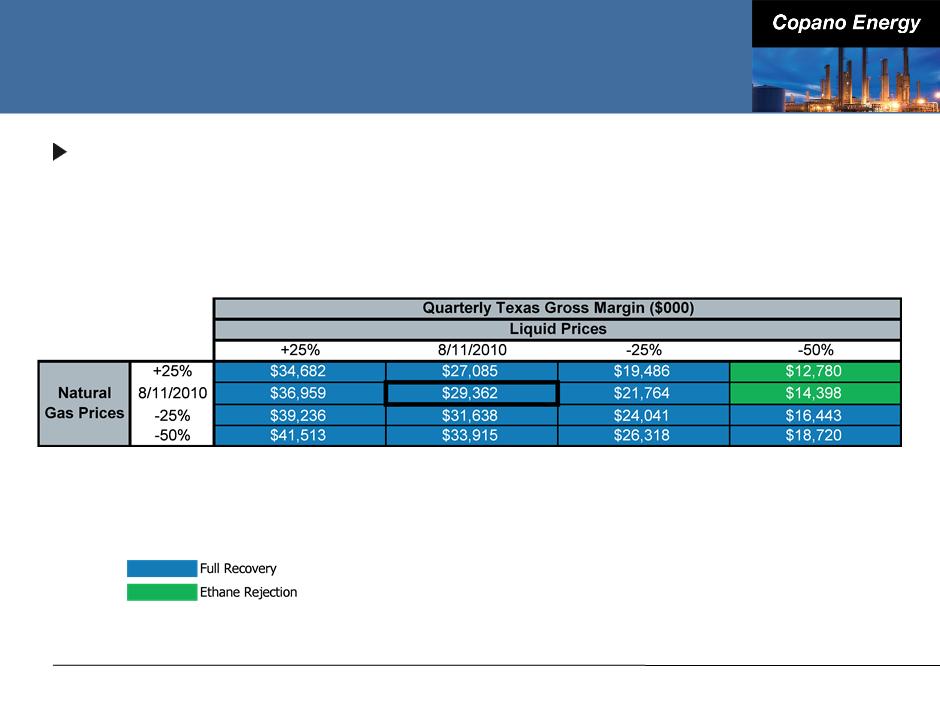

Oklahoma Commodity Price Sensitivities

Oklahoma segment gross margins excluding hedge settlements

■ Matrix reflects 2Q 2010 volumes, adjusted using Copano’s 2010 planning

model

model

38

Note: Please see this Appendix for definitions of processing modes and additional details.

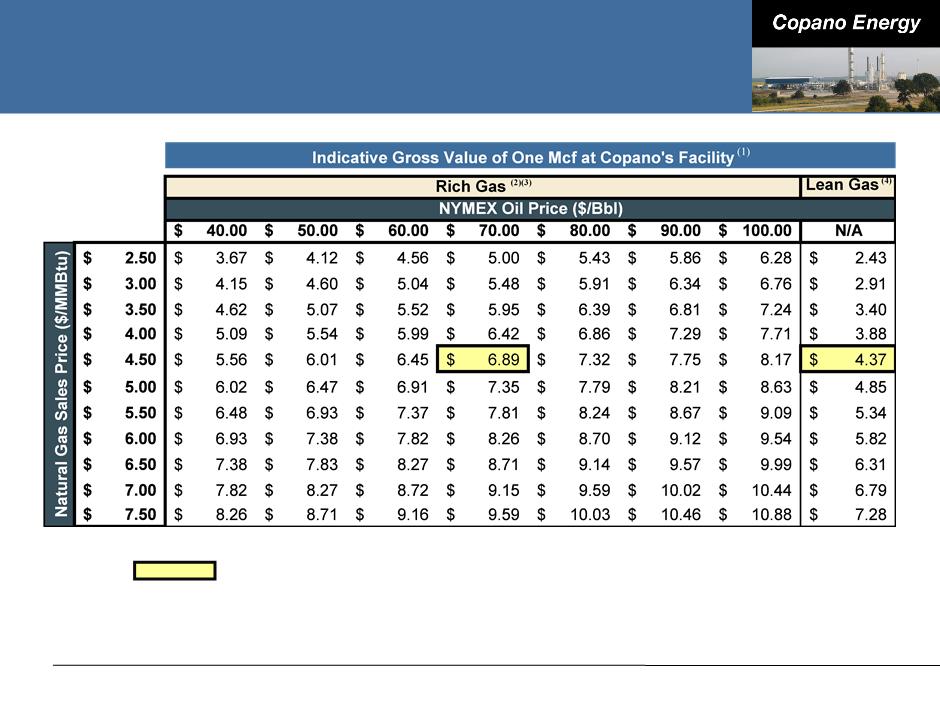

Oklahoma Rich Gas vs. Lean Gas

39

Prices as of 8/19/10

(1) Full value prior to deduction of Copano’s margin. Excludes value of condensate and crude oil recovered by the producer at the wellhead.

(2) Implied NGL prices are based on a six-year historical regression analysis.

(3) Assumes 9 GPM gas with a Btu factor of 1.375 processed at Copano’s cryogenic plant, and field fuel of 6.25%.

(4) Assumes unprocessed gas with a Btu factor of 1.0 and field fuel of 6%.

Texas Contract Mix

40

(1) Source: Copano Energy internal financial planning models for consolidated subsidiaries.

(2) Excludes 54,747 MMBtu/d service throughput for Webb Duval, a majority-owned affiliate.

Texas Net Commodity Exposure

41

Note: See explanation of processing modes in this Appendix.

(1) Source: Copano Energy internal financial planning models for consolidated subsidiaries. Based on 2Q 2010 daily wellhead/plant inlet volumes.

(2) Fractionation at Houston Central processing plant permits significant reductions in ethane recoveries in ethane rejection mode and full ethane rejection in

conditioning mode. To optimize profitability, plant operations can also be adjusted to partial recovery mode.

conditioning mode. To optimize profitability, plant operations can also be adjusted to partial recovery mode.

(3) At the Houston Central processing plant, pentanes+ may be sold as condensate.

Texas Commodity Price Sensitivities

Texas segment gross margins excluding hedge settlements

■ Matrix reflects 2Q 2010 volumes and operating conditions, adjusted using

Copano’s 2010 planning model

Copano’s 2010 planning model

42

Note: Please see this Appendix for definitions of processing modes and additional details.

Rocky Mountains Sensitivities

2Q 2010 Adjusted EBITDA volume sensitivity (positive or negative

impact)

impact)

■ Bighorn: 10,000 MMBtu/d = $245,000(1)

■ Fort Union: 10,000 MMBtu/d = $70,000(1)

43

Note: See this Appendix for reconciliation of Adjusted EBITDA. Values reflect rounding.

(1) Impact on Adjusted EBITDA based on Copano’s interest in the unconsolidated affiliate.

Hedging Impact of Commodity Price

Sensitivities

Sensitivities

44

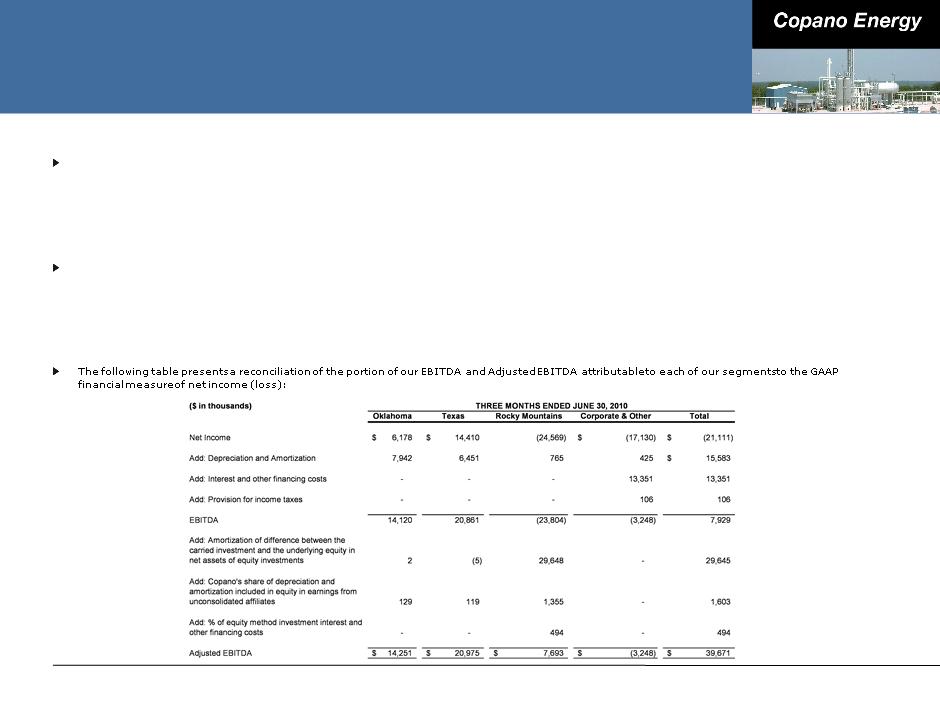

Reconciliation of Non-GAAP Financial

Measures

Measures

Segment Gross Margin and Total Segment Gross Margin

We define segment gross margin, with respect to a Copano operating segment, as segment revenue less cost of sales. Cost of sales includes the

following: cost of natural gas and NGLs purchased from third parties, cost of natural gas and NGLs purchased from affiliates, cost of crude oil purchased

from third parties, costs paid to third parties to transport volumes and costs paid to affiliates to transport volumes. Total segment gross margin is the

sum of the operating segment gross margins and the results of Copano’s risk management activities that are included in Corporate and other. We view

total segment gross margin as an important performance measure of the core profitability of our operations. Segment gross margin allows Copano’s

senior management to compare volume and price performance of the segments and to more easily identify operational or other issues within a segment.

The GAAP measure most directly comparable to total segment gross margin is operating income.

following: cost of natural gas and NGLs purchased from third parties, cost of natural gas and NGLs purchased from affiliates, cost of crude oil purchased

from third parties, costs paid to third parties to transport volumes and costs paid to affiliates to transport volumes. Total segment gross margin is the

sum of the operating segment gross margins and the results of Copano’s risk management activities that are included in Corporate and other. We view

total segment gross margin as an important performance measure of the core profitability of our operations. Segment gross margin allows Copano’s

senior management to compare volume and price performance of the segments and to more easily identify operational or other issues within a segment.

The GAAP measure most directly comparable to total segment gross margin is operating income.

45

Reconciliation of Non-GAAP Financial

Measures

Measures

Adjusted EBITDA

We define EBITDA as net income (loss) plus interest expense, provision for income taxes and depreciation and amortization expense. Because a portion

of our net income (loss) is attributable to equity in earnings (loss) from our equity investees (which include Bighorn, Fort Union, Webb Duval and

Southern Dome), our management also calculates Adjusted EBITDA to reflect the depreciation and amortization expense embedded in equity in earnings

(loss) from unconsolidated affiliates. Specifically, our management determines Adjusted EBITDA by adding to EBITDA (i) the amortization expense

attributable to the difference between our carried investment in each unconsolidated affiliate and the underlying equity in its net assets, (ii) the portion

of each unconsolidated affiliate’s depreciation and amortization expense, which is proportional to our ownership interest in that unconsolidated affiliate

and (iii) the portion of each unconsolidated affiliate’s interest and other financing costs, which is proportional to our ownership interest in that

unconsolidated affiliate.

of our net income (loss) is attributable to equity in earnings (loss) from our equity investees (which include Bighorn, Fort Union, Webb Duval and

Southern Dome), our management also calculates Adjusted EBITDA to reflect the depreciation and amortization expense embedded in equity in earnings

(loss) from unconsolidated affiliates. Specifically, our management determines Adjusted EBITDA by adding to EBITDA (i) the amortization expense

attributable to the difference between our carried investment in each unconsolidated affiliate and the underlying equity in its net assets, (ii) the portion

of each unconsolidated affiliate’s depreciation and amortization expense, which is proportional to our ownership interest in that unconsolidated affiliate

and (iii) the portion of each unconsolidated affiliate’s interest and other financing costs, which is proportional to our ownership interest in that

unconsolidated affiliate.

External users of our financial statements such as investors, commercial banks and research analysts use EBITDA or Adjusted EBITDA, and our

management uses Adjusted EBITDA, as a supplemental financial measure to assess:

management uses Adjusted EBITDA, as a supplemental financial measure to assess:

■ The financial performance of our assets without regard to financing methods, capital structure or historical cost basis;

■ The ability of our assets to generate cash sufficient to pay interest costs and support our indebtedness;

■ Our operating performance and return on capital as compared to those of other companies in the midstream energy sector, without regard to financing or capital

structure; and

structure; and

■ The viability of acquisitions and capital expenditure projects and the overall rates of return on alternative investment opportunities.

46

Definitions of Non-GAAP Financial Measures

Total Distributable Cash Flow

We define total distributable cash flow as net income plus: (i) depreciation, amortization and impairment expense

(including amortization expense relating to the option component of our risk management portfolio); (ii) cash

distributions received from investments in unconsolidated affiliates and equity losses from such unconsolidated affiliates;

(iii) provision for deferred income taxes; (iv) the subtraction of maintenance capital expenditures; (v) the subtraction of

equity in earnings from unconsolidated affiliates and (vi) the addition of losses or subtraction of gains relating to other

miscellaneous non-cash amounts affecting net income for the period, such as equity-based compensation, mark-to-

market changes in derivative instruments, and our line fill contributions to third-party pipelines and gas imbalances.

Maintenance capital expenditures are capital expenditures employed to replace partially or fully depreciated assets to

maintain the existing operating capacity of our assets and to extend their useful lives, or other capital expenditures that

are incurred in maintaining existing system volumes and related cash flows.

(including amortization expense relating to the option component of our risk management portfolio); (ii) cash

distributions received from investments in unconsolidated affiliates and equity losses from such unconsolidated affiliates;

(iii) provision for deferred income taxes; (iv) the subtraction of maintenance capital expenditures; (v) the subtraction of

equity in earnings from unconsolidated affiliates and (vi) the addition of losses or subtraction of gains relating to other

miscellaneous non-cash amounts affecting net income for the period, such as equity-based compensation, mark-to-

market changes in derivative instruments, and our line fill contributions to third-party pipelines and gas imbalances.

Maintenance capital expenditures are capital expenditures employed to replace partially or fully depreciated assets to

maintain the existing operating capacity of our assets and to extend their useful lives, or other capital expenditures that

are incurred in maintaining existing system volumes and related cash flows.

Total distributable cash flow is a significant performance metric used by senior management to compare basic cash flows

generated by us (prior to the establishment of any retained cash reserves by our Board of Directors) to the cash

distributions we expect to pay our unitholders, and it also correlates with the metrics of our existing debt covenants.

Using total distributable cash flow, management can quickly compute the coverage ratio of estimated cash flows to

planned cash distributions. Total distributable cash flow is also an important non-GAAP financial measure for our

unitholders because it serves as an indicator of our success in providing a cash return on investment — specifically,

whether or not we are generating cash flow at a level that can sustain or support an increase in our quarterly distribution

rates. Total distributable cash flow is also used by industry analysts with respect to publicly traded partnerships and

limited liability companies because the market value of such entities’ equity securities is significantly influenced by the

amount of cash they can distribute to unitholders.

generated by us (prior to the establishment of any retained cash reserves by our Board of Directors) to the cash

distributions we expect to pay our unitholders, and it also correlates with the metrics of our existing debt covenants.

Using total distributable cash flow, management can quickly compute the coverage ratio of estimated cash flows to

planned cash distributions. Total distributable cash flow is also an important non-GAAP financial measure for our

unitholders because it serves as an indicator of our success in providing a cash return on investment — specifically,

whether or not we are generating cash flow at a level that can sustain or support an increase in our quarterly distribution

rates. Total distributable cash flow is also used by industry analysts with respect to publicly traded partnerships and

limited liability companies because the market value of such entities’ equity securities is significantly influenced by the

amount of cash they can distribute to unitholders.

47