Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT - CASEYS GENERAL STORES INC | form8k.htm |

| EX-99.2 - LETTER TO SHAREHOLDERS OF CASEY'S GENERAL STORES, INC., DATED AUGUST 23, 2010 - CASEYS GENERAL STORES INC | ex99-2.htm |

Exhibit 99.1

|

Investor Contact

Bill Walljasper

Senior VP & Chief Financial Officer

515-965-6505

|

Media Contact

Sard Verbinnen & Co

Paul Caminiti/Andrew Cole/Brooke Gordon

212-687-8080

|

|

Mark Harnett/Charlie Koons

MacKenzie Partners

212-929-5500

|

CASEY’S SENDS LETTER TO SHAREHOLDERS

Details How Casey’s Board of Directors is Creating Far Greater Value for Shareholders than Couche-Tard’s Offer

Urges Shareholders to Vote “FOR” Casey’s Highly Qualified Directors at Annual Meeting

___________________________________________________________________

ANKENY, IOWA – August 23, 2010 – Casey’s General Stores, Inc. (“Casey’s” or the “Company”) (NASDAQ: CASY) today announced that it has filed with the Securities and Exchange Commission a letter sent to Casey’s shareholders from the Company’s President and Chief Executive Officer, Robert J. Myers. Shareholders can find this and other materials related to Casey’s annual meeting of shareholders to be held on September 23, 2010 at www.supportcaseys.com.

The full text of the letter sent to Casey’s shareholders follows:

August 23, 2010

Dear Fellow Shareholder:

A VOTE “FOR” CASEY’S NOMINEES IS A VOTE FOR VALUE –

VOTE YOUR WHITE PROXY CARD TODAY

As you know, our annual meeting of shareholders will be held on September 23, 2010. Casey’s has nominated its current Board of Directors for reelection. Casey’s Board – which includes seven independent members out of eight total directors – has led Casey’s to become a best-in-class operator that consistently outperforms its peers and returns significant value to shareholders. Under the Board’s leadership, Casey’s is executing well on its strategic growth initiatives and creating and delivering far greater value than Alimentation Couche-Tard Inc.’s $36.75 per share offer. Couche-Tard’s proposal to replace our highly qualified, experienced directors with its hand-picked nominees has one purpose – a quick sale of Casey’s to Couche-Tard at a low price. Vote for value today – vote the WHITE proxy card in support of Casey’s nominees. We urge you to discard any blue proxy cards you receive from Couche-Tard.

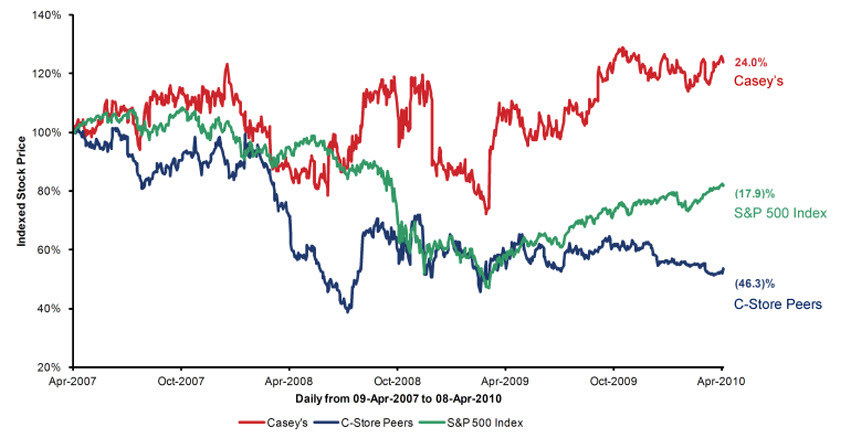

CASEY’S STOCK PRICE HAS CONSISTENTLY OUTPERFORMED ITS PEERS AND THE MARKET

As demonstrated by the chart below, Casey’s has consistently outperformed its convenience store peers and the S&P 500. Over the past three years prior to the announcement of Couche-Tard’s offer on April 9, 2010, our stock price has increased 24%, compared to our peers, which on average are down 46.3%, and the S&P 500, which is down 17.9%, over that same period.

Casey’s Outperformance Prior to Couche-Tard’s Public Offer (Last 3 Years)

Indexed Stock Price 140% 120% 100% 80% 40% 20% Apr-2007 Oct-2007 Apr-2008 Oct-2008 Apr-2009 Oct-2009 Apr-2010 24% Casey’s (17.9)% S&P 500 Index (46.3)% C-Store Peers Daily from 09-Apr-2010 to 08-Apr-2010 Casey’s C-Store Peers S&P 500 Index

Source: Bloomberg

Note: C-Store Peers include Couche-Tard, Susser and The Pantry

Indexed Stock Price 140% 120% 100% 80% 40% 20% Apr-2007 Oct-2007 Apr-2008 Oct-2008 Apr-2009 Oct-2009 Apr-2010 24% Casey’s (17.9)% S&P 500 Index (46.3)% C-Store Peers Daily from 09-Apr-2010 to 08-Apr-2010 Casey’s C-Store Peers S&P 500 Index

YOUR BOARD IS DELIVERING EXCEPTIONAL TOTAL RETURNS

Casey’s has consistently driven increased shareholder returns. As demonstrated by the chart below, if you had bought Casey’s stock in fiscal 2001, you would have received a cumulative total return on your investment of 247% in 2010. Your average return for each of those years would have been 13%. Such remarkable returns reflect not only Casey’s stock appreciation but also our Board’s commitment to increasing our dividend. Over the past five years, our Board increased the dividend at a compounded annual growth rate of approximately 17.3%, and it increased our dividend again at the start of fiscal 2011. The Company’s dividend payout ratio for the fiscal year ended April 30, 2010 was 15%, the highest ratio among its convenience store peers.

Cumulative Total Returns (2001-2010)

| Implied 2001-2010 Annualized Return³: 13% |

Total Return2: 1% 1% 2% 3% 5% 7% 8% 11% 13% 16% 3% 11% 11% 42% 44% 83% 115% 89% 128% 231% 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 Stock Appreciation Dividend Yield1 4% 13% 13% 45% 49% 90% 123% 100% 141% 247%

Source: Public filings

Note: Fiscal year ending April

1 Calculated as cumulative dividends divided by stock price at the beginning of FY2001 (May 1, 2000). Assumes dividends are not reinvested.

2 Calculated as cumulative share price appreciation plus dividend yield since the beginning of FY2001.

3 Implied compounded annual return assuming total cumulative return of 247% over the period.

Total Return2: 1% 1% 2% 3% 5% 7% 8% 11% 13% 16% 3% 11% 11% 42% 44% 83% 115% 89% 128% 231% 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 Stock Appreciation Dividend Yield1 4% 13% 13% 45% 49% 90% 123% 100% 141% 247%

ANALYSTS AGREE THAT CASEY’S IS CREATING

SUPERIOR VALUE FOR SHAREHOLDERS

Analysts recognize that through the execution of our ongoing strategic growth initiatives and our recapitalization plan, Casey’s is worth more – and is already delivering more value – than Couche-Tard’s lowball offer.

The eight analysts who currently cover the Company have price targets for Casey’s ranging from $39 per share to $50 per share. Despite these indications of the superior value of Casey’s and the fact that only 12% of Casey’s shares had tendered into Couche-Tard’s offer as of August 2nd, Couche-Tard has stated very clearly that it does not value Casey’s at more than $38 per share.

Commenting on the recapitalization plan, one analyst said “Long-term investors should be pleased with greater ownership in what we view as an attractively valued company, which will see upward EPS revisions and ROE following the recap. Over the next 12 months shares could move above $44 following the recapitalization as shareholder returns nearly double and management executes its growth plans funded with impressive cash flow.” (Morgan Keegan, July 28, 2010)

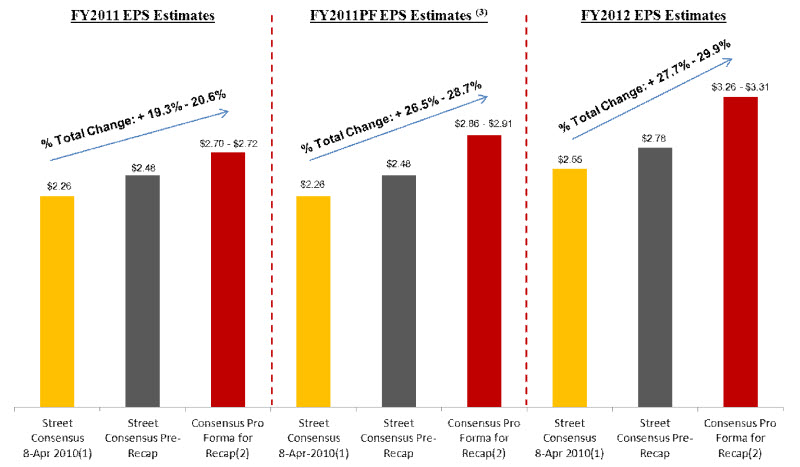

Your Board is already delivering more value than Couche-Tard’s small 16% premium. The continuously increasing equity research analyst EPS estimates for Casey’s for fiscal 2011 and 2012 evidence this fact. Since Couche-Tard’s offer on April 9th, 2010 and our announcement of Casey’s fiscal 2010 financial results (and prior to the announcement of our recapitalization), the consensus analyst EPS estimates increased for 2011 from $2.26 to $2.48 (9.7%) and for 2012 from $2.55 to $2.78 (9.0%).

As the following chart illustrates, simply adjusting these consensus analyst estimates of 2011 and 2012 EPS for the reduction in outstanding shares, additional interest expense and retirement of debt in connection with our recapitalization results in an increased 2011 EPS estimate of $2.70 to $2.72 per diluted share and a 2012 EPS estimate of $3.26 to $3.31 per diluted share. Assuming the recapitalization occurred at the beginning of our 2011 fiscal year, the 2011 EPS estimate would be increased to $2.86 to $2.91 per diluted share.

These increases in EPS estimates since April 8th represent 26.5% to 28.7% for 2011 (assuming the recapitalization occurred at the beginning of the year) and 27.7% to 29.9% for 2012. This far exceeds the 16% control premium offered by Couche-Tard for you to surrender your shares and forgo even more upside in the future.

Positive Impact of Recapitalization Plan on Casey’s

FY2011 EPS Estimates % Total Change: + 19.3% - 20.6% $2.26 $2.48 $2.70 - $2.72 Street Consensus 8-April 2010(1) Street Consensus Pre-Recap Consensus Pro Forma for Recap(2) FY2011PF EPS Estimates(3) % Total Change: + 26.5% - 28.7% $2.26 $2.48 $2.86 - $2.91 Street Consensus 8-April 2010(1) Street Consensus Pre-Recap Consensus Pro Forma for Recap(2) FY2012 EPS Estimates % Total Change: + 27.7% - 29.9% $2.55 $2.78 $3.26 - $3.31 Street Consensus 8-April 2010(1) Street Consensus Pre-Recap Consensus Pro Forma for Recap(2)

Source: IBES, Casey’s press releases, public filings

1 8-Apr-10 was the day prior to the public announcement of Couche-Tard’s unsolicited proposal to acquire Casey’s for $36.00 per share in cash.

2 Assumes $569mm of 5.22% senior unsecured notes funded on August 9, 2010. Assumes $59mm of proceeds used in connection with the prepayment of Senior Notes with interest rates between 6.18% to 7.23% and 7.38% Senior Notes. Assumes $500mm shares repurchased on August 25, 2010 at $38.00 and $40.00 at the low end and high end of the repurchase range, respectively.

3 Pro forma assumes recapitalization transaction occurs at the beginning of FY2011 (April 30, 2010)

FY2011 EPS Estimates % Total Change: + 19.3% - 20.6% $2.26 $2.48 $2.70 - $2.72 Street Consensus 8-April 2010(1) Street Consensus Pre-Recap Consensus Pro Forma for Recap(2) FY2011PF EPS Estimates(3) % Total Change: + 26.5% - 28.7% $2.26 $2.48 $2.86 - $2.91 Street Consensus 8-April 2010(1) Street Consensus Pre-Recap Consensus Pro Forma for Recap(2) FY2012 EPS Estimates % Total Change: + 27.7% - 29.9% $2.55 $2.78 $3.26 - $3.31 Street Consensus 8-April 2010(1) Street Consensus Pre-Recap Consensus Pro Forma for Recap(2)

CASEY’S BOARD IS ACTING IN SHAREHOLDERS’ BEST INTERESTS

Casey’s has a strong history of transparency and good governance. In fact, for the last two years Casey’s was recognized by Forbes.com as one of the 100 most “trustworthy companies” in the United States in an assessment of “true quality of corporate accounting and management practices.”

Make no mistake, Couche-Tard is attempting to replace your Board with its hand-picked slate of directors to achieve one purpose: a quick sale of Casey’s to Couche-Tard at a low price. To that end, Couche-Tard continues to make misleading statements about Casey’s Board in an attempt to distract you from the inadequacy of its offer.

The fact is that the Casey’s Board is acting in the best interests of all shareholders. The Board takes its fiduciary duties very seriously. Consistent with its duties, the Board thoroughly reviewed the Couche-Tard offer. Given Couche-Tard’s lowball offer, its statements and actions that clearly demonstrate it is not a buyer of Casey’s above $38 per share, and its questionable behavior – including its allegedly manipulative sale of Casey’s shares – our Board concluded that there is no basis for discussions with Couche-Tard regarding its $36.75 per share offer.

Contrary to Couche-Tard’s suggestion that our recapitalization plan was financial engineering aimed at artificially inflating Casey’s stock price, the recapitalization implements the Board of Director’s decision to create a more efficient and lower cost capital structure, one that will boost returns to equity holders for the remainder of fiscal years 2011, 2012 and for years to come.

In another desperate attempt to distract you from the real issue, Couche-Tard has also mischaracterized the terms of our financing for the recapitalization. Our objective in seeking financing for the recapitalization was to obtain the lowest borrowing cost possible. The terms of the private placement were the result of negotiations toward that goal, and we are pleased to have achieved that goal with the 5.22% rate – the lowest in the company’s history, and secured favorable covenants to enable Casey’s to continue to execute on its strategic plan. The fact is noteholders requested a change in control “make whole” premium in the terms of the financing as a direct result of Couche-Tard’s hostile offer. We don’t believe we could have secured this very attractive financing package without it. We believe that the terms of other financing options would have been less favorable for Casey’s shareholders, and our commitment is to create value for our shareholders, not Couche-Tard’s.

We also note that more than four months after making its offer public, Couche-Tard still has not secured financing, that six events have occurred which violate various conditions to its offer and that Couche-Tard recently added a condition to its offer that is virtually incapable of fulfillment – all of which effectively make Couche-Tard’s offer illusory.

VOTE THE WHITE CARD TODAY -- CASEY’S BOARD WILL DELIVER

FAR GREATER VALUE TO YOU THAN COUCHE-TARD

We encourage you to review the Definitive Proxy Statement and all the materials we have mailed you related to our self tender offer, including the Offer to Purchase and related tender offer documents. The Casey’s Board unanimously recommends that you vote “FOR” the highly qualified slate of Casey’s directors named on the enclosed WHITE proxy card and “AGAINST” Couche-Tard’s Bylaw amendment repeal proposal. We also urge you to discard any blue proxy card sent to you by Couche-Tard or its affiliates. Even a vote against Couche-Tard’s nominees on Couche-Tard’s blue proxy card will cancel any previous proxy submitted by you.

To vote FOR Casey’s nominees, shareholders should sign, date and return the WHITE proxy card as soon as it is received or vote via telephone or internet by following the instructions indicated on the WHITE proxy card. MacKenzie Partners, Inc. is acting as Casey’s proxy solicitor and information agent for the tender offer and can be reached toll-free at (800) 322-2885 or (212) 929-5500. You can also find additional relevant information at www.supportcaseys.com.

We appreciate all the positive feedback we have received from shareholders, and thank you for your support.

Best regards,

Robert Myers

President and Chief Executive Officer

Important Information

In response to the tender offer commenced by Alimentation Couche-Tard Inc. (“Couche-Tard”) referred to in this communication, Casey's General Stores, Inc. (“Casey's”) has filed a solicitation/recommendation statement with the Securities and Exchange Commission (the “SEC”). Investors and security holders are urged to read the solicitation/recommendation statement with respect to the tender offer and, when they become available, any other relevant documents filed with the SEC, because they contain important information. Investors and security holders may obtain a free copy of the solicitation/recommendation statement with respect to the tender offer and other documents (when available) that Casey’s files with the SEC at the SEC’s website at www.sec.gov and Casey’s website at www.caseys.com. In addition, the solicitation/recommendation statement with respect to the tender offer and other documents (when available) filed by Casey's with the SEC may be obtained from Casey's free of charge by directing a request to Casey’s General Stores, Inc., Attn: Investor Relations, Casey’s General Stores, Inc., One Convenience Blvd., P.O. Box 3001, Ankeny, Iowa 50021-8045.

Casey's has filed with the SEC a definitive proxy statement and white proxy card in connection with its 2010 Annual Meeting of Shareholders and is mailing the definitive proxy statement and white proxy card to its shareholders. Investors and security holders are urged to read the definitive proxy statement and, when they become available, any other relevant documents filed with the SEC, because they contain important information. Investors and security holders may obtain a free copy of the definitive proxy statement and, when available, other documents that Casey’s files with the SEC at the SEC’s website at www.sec.gov and Casey’s website at www.caseys.com. In addition, the definitive proxy statement and, when available, other documents filed by Casey’s with the SEC may be obtained from Casey’s free of charge by directing a request to Casey’s General Stores, Inc., Attn: Investor Relations, Casey’s General Stores, Inc., One Convenience Blvd., P.O. Box 3001, Ankeny, Iowa 50021-8045.

Additional Information

This communication is for informational purposes only and is neither an offer to purchase nor the solicitation of an offer to sell any securities. Casey’s has filed an issuer tender offer statement on Schedule TO and related exhibits regarding its self-tender offer for up to $500 million in value of shares of Casey’s common stock with the SEC. Investors and security holders are urged to read the issuer tender offer statement and related exhibits and, when they become available, any other documents filed with the SEC with respect to Casey’s self tender offer because they contain important information. Investors and security holders may obtain a free copy of the issuer tender offer statement and the related exhibits as well as any other documents (when available) that Casey’s files with the SEC at the SEC's website at www.sec.gov and Casey’s website at www.caseys.com. In addition, the issuer tender offer statement and the related exhibits and other documents (when available) filed by Casey’s with the SEC may be obtained from Casey’s free of charge by directing a request to Casey’s General Stores, Inc., Attn: Investor Relations, Casey’s General Stores, Inc., One Convenience Blvd., P.O. Box 3001, Ankeny, Iowa 50021-8045.

Certain Information Concerning Participants

Casey’s, its directors and executive officers may be deemed to be participants in the solicitation of Casey’s security holders in connection with its 2010 Annual Meeting of Shareholders. Security holders may obtain information regarding the names, affiliations and interests of such individuals in Casey’s Annual Report on Form 10-K for the year ended April 30, 2010, which was filed with the SEC on June 29, 2010, and its definitive proxy statement for the 2010 Annual Meeting of Shareholders, which was filed with the SEC on August 12, 2010. To the extent holdings of Casey’s securities have changed since the amounts printed in the definitive proxy statement for the 2010 Annual Meeting of Shareholders, such changes have been or will be reflected on Statements of Change in Ownership on Form 4 filed with the SEC. These documents (when available) may be obtained free of charge from the SEC’s website at www.sec.gov and Casey’s website at www.caseys.com.

Forward-Looking Statements

This communication contains various “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements represent our expectations or beliefs concerning future events that may not prove to be accurate. The words “believe,” “expect,” “anticipate,” “intend,” “estimate,” “project” and similar expressions are used to identify forward-looking statements. We caution you that these statements are further qualified by important factors that could cause actual results to differ materially from those in the forward-looking statements, including the risk that our cash balances and cash generated from operations and financing activities will not be sufficient for our future liquidity and capital resource needs, competition in the industry in which we operate, changes in the price or supply of gasoline, tax increases or other changes in the price of or demand for tobacco products, potential liabilities and expenditures related to compliance with environmental and other laws and regulations, the seasonality of demand patterns, weather conditions, future actions by Couche-Tard in connection with its unsolicited tender offer to acquire Casey’s, the risk that disruptions or uncertainty from Couche-Tard’s unsolicited tender offer will divert management’s time and harm Casey’s relationships with our customers, employees and suppliers; the increased indebtedness that the Company has incurred to purchase shares of our common stock in our self tender offer; the price at which we ultimately determine to purchase shares of our common stock in our self tender offer and the number of shares tendered in such offer; the price and time at which we may make any additional repurchases of our common stock following completion of our self tender offer as well as the number of shares acquired in such repurchases and the terms, timing, cost and interest rate on any indebtedness incurred to fund such repurchases; and the other risks and uncertainties included from time to time in our filings with the SEC. We further caution you that other factors we have not identified may in the future prove to be important in affecting our business and results of operations. We ask you not to place undue reliance on any forward-looking statements because they speak only of our views as of the statement dates. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise.