Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - UniTek Global Services, Inc. | v192266_ex23-1.htm |

| EX-23.2 - EX-23.2 - UniTek Global Services, Inc. | v192266_ex23-2.htm |

As

filed with the Securities and Exchange Commission on August 13,

2010

Registration

No. 333-

UNITED

STATES

SECURITIES AND

EXCHANGE COMMISSION

Washington, D.C.

20549

FORM

S-1

REGISTRATION

STATEMENT UNDER THE

SECURITIES ACT OF

1933

UniTek

Global Services, Inc.

(Exact name of registrant as

specified in its charter)

|

Delaware

|

4812

|

75-2233445

|

|

(State

or other jurisdiction of

incorporation

or organization)

|

(Primary

Standard Industrial

Classification

Code Number)

|

(I.R.S.

Employer

Identification

No.)

|

1777

Sentry Parkway West

Gwynedd

Hall, Suite 302

Blue

Bell, Pennsylvania 19422

267-464-1700

(Address,

including zip code and telephone number,

including area code, of

registrant’s principal executive

offices)

C.

Scott Hisey

Chief

Executive Officer

1777

Sentry Parkway West

Gwynedd

Hall, Suite 302

Blue

Bell, Pennsylvania 19422

267-464-1700

(Name,

address, including zip code and telephone number,

including area code, of agent

for service)

With copies to:

|

Justin

W. Chairman, Esq.

Morgan,

Lewis & Bockius LLP

1701

Market Street

Philadelphia,

Pennsylvania 19103

Telephone:

(215) 963-5000

Facsimile:

(215) 963-5001

|

R.

Scott Shean, Esq.

B.

Shayne Kennedy, Esq.

Latham

& Watkins LLP

650

Town Center Drive, 20th

Floor

Costa

Mesa, California 92626

Telephone:

(714) 540-1235

Facsimile:

(714) 755-8290

|

Approximate date of commencement of

proposed sale to the public: As soon as practicable after this

registration statement becomes effective.

If any of

the securities being registered on this Form are to be offered on a delayed or

continuous basis pursuant to Rule 415 under the Securities Act of 1933,

check the following box. ¨

If this

Form is filed to register additional securities for an offering pursuant to

Rule 462(b) under the Securities Act, check the following box and list the

Securities Act registration statement number of the earlier effective

registration statement for the same offering. ¨

If this

Form is a post-effective amendment filed pursuant to Rule 462(c) under the

Securities Act, check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same

offering. ¨

If this

Form is a post-effective amendment filed pursuant to Rule 462(d) under the

Securities Act, check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same

offering. ¨

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting company. See

the definitions of “large accelerated filer,” “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act. (Check

one):

|

Large

accelerated filer ¨

|

Accelerated

filer ¨

|

Non-accelerated

filer ¨

(Do

not check if a smaller

reporting

company)

|

Smaller

reporting company x

|

CALCULATION

OF REGISTRATION FEE

|

Title of Each

Class of Securities

to be Registered

|

Proposed Maximum Aggregate

Offering Price(1)(2)

|

Amount of Registration Fee

|

||||||

|

Common stock, par value $0.00002 per

share

|

$ | 86,250,000 | $ | 6,150 | ||||

(1) Estimated

solely for the purpose of calculating the registration fee pursuant to

Rule 457(o) under the Securities Act of 1933, as

amended.

(2) Includes

shares that the underwriter has the option to purchase to cover over-allotment,

if any.

The Registrant hereby amends this

Registration Statement on such date or dates as may be necessary to delay its

effective date until the Registrant shall file a further amendment which

specifically states that this Registration Statement shall thereafter become

effective in accordance with Section 8(a) of the Securities Act of 1933 or

until the Registration Statement shall become effective on such date as the

Commission, acting pursuant to said Section 8(a), may

determine.

The

information in this prospectus is not complete and may be changed. We may not

sell these securities until the registration statement filed with the Securities

and Exchange Commission is effective. This prospectus is not an offer to sell

these securities and is not soliciting an offer to buy these securities in any

state where the offer or sale is not permitted.

|

PRELIMINARY

PROSPECTUS

|

SUBJECT

TO COMPLETION, DATED

|

|

AUGUST

13, 2010

|

UniTek

Global Services, Inc.

Common

Stock

$ per

share

We are

offering shares of our common stock by this

prospectus.

Our

common stock is currently listed on the Over-the-Counter Bulletin Board under

the symbol “UGLB.OB.” As of August 12, 2010, the last reported sale

price of our common stock was $0.75 per share. We are applying to

list our common stock on the NASDAQ Global Market under the symbol “UNTK,”

concurrently with the consummation of this offering.

Investing

in our common stock involves a high degree of risk. You should read this

entire prospectus carefully, including the section entitled “Risk Factors”

beginning on page 9.

|

Per Share

|

Total

|

|||||||

|

Public

offering price

|

$ | $ | ||||||

|

Underwriting

discount and commissions

|

$ | $ | ||||||

|

Proceeds,

before expenses, to us

|

$ | $ | ||||||

Neither the Securities and Exchange

Commission nor any state securities commission has approved or disapproved these

securities or determined if this prospectus is truthful or complete. Any

representation to the contrary is a criminal offense.

We have

granted the underwriter an option, exercisable within 30 days after the date of

this prospectus, to purchase up to additional

shares of our common stock upon the same terms and conditions as the shares

offered by this prospectus to cover over-allotments, if any.

The

underwriter expects to deliver the shares of common stock to purchasers on or

about , 2010.

Roth

Capital Partners

The date of this prospectus

is ,

2010.

TABLE

OF CONTENTS

|

Page

|

|

|

Prospectus

Summary

|

1

|

|

Risk

Factors

|

9

|

|

Cautionary

Statement Regarding Forward-Looking Statements

|

18

|

|

Use

of Proceeds

|

19

|

|

Price

Range of Common Stock

|

20

|

|

Dividend

Policy

|

20

|

|

Capitalization

|

21

|

|

Dilution

|

23

|

|

Selected

Consolidated Financial Data

|

25

|

| Adjusted EBITDA | 28 |

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

29

|

|

Business

|

39

|

|

Management

|

48

|

|

Executive

Compensation

|

53

|

|

Security

Ownership of Certain Beneficial Owners and Management

|

63

|

|

Certain

Relationships and Related Party Transactions, Director

Independence

|

67

|

|

Description

of Securities

|

70

|

|

Material

U.S. Federal Income Tax Considerations for Non-U.S. Holders of Common

Stock

|

73

|

|

Underwriting

|

75

|

|

Legal

Matters

|

77

|

|

Experts

|

77

|

|

Incorporation

by Reference

|

77

|

|

Where

You Can Find More Information

|

78

|

|

Index

to Financial Statements

|

F-i

|

You

should rely only on the information contained or incorporated by reference in

this prospectus and in any free writing prospectus that we have authorized for

use in connection with this offering. Neither we nor the underwriter has

authorized any other person to provide you with additional or different

information. If anyone provides you with different or inconsistent information,

you should not rely on it. Neither we nor the underwriter is making an offer to

sell these securities in any jurisdiction where an offer or sale is not

permitted. You should assume that the information in this prospectus is accurate

only as of the date on the front cover of this prospectus, regardless of the

time of delivery of this prospectus or any sale of our common stock. Our

business, financial condition, results of operations and prospects may have

changed since that date.

Some of

the industry and market data contained in this prospectus are based on

independent industry publications or other publicly available information, while

other information is based on our internal sources. Although we believe that

each source is reliable as of its respective date, the information contained in

such sources has not been independently verified, and neither we nor the

underwriter can assure you as to the accuracy or completeness of this

information.

TRADEMARKS, TRADE NAMES AND SERVICE

MARKS

UniTek

and UniTek Global Services are trademarks of UniTek Global Services, Inc. All

other service marks, trademarks and trade names referred to in this prospectus

are the property of their respective owners. Solely for convenience, any

trademarks referred to in this prospectus may appear without the ® symbol, but

such references are not intended to indicate, in any way, that the owner of such

trademark will not assert, to the fullest extent under applicable law, its

rights or the right of the applicable licensor to these

trademarks.

PROSPECTUS

SUMMARY

This summary highlights certain

information described in more detail later in this prospectus. This summary is

not complete and does not contain all the information you should consider before

investing in our common stock. You should carefully read the more detailed

information set out in this prospectus, especially the risks related to our

business and investing in our common stock that we discuss under the headings

“Risk Factors” and “Management’s Discussion and Analysis of Financial Condition

and Results of Operations,” as well as the consolidated financial statements and

related notes appearing elsewhere in this prospectus or incorporated by

reference herein. References in this prospectus to “we,” “us,” “our,” “the

Company,” “our Company,” and “UniTek” refer to UniTek Global Services, Inc. and

its consolidated subsidiaries, unless the context requires

otherwise.

UniTek

Global Services

We are a

leading full-service provider of permanently outsourced infrastructure services,

offering an end-to-end suite of technical services to the wireless and wireline

telecommunications, satellite television and broadband cable industries in the

United States and Canada. Our services include network engineering and

design, construction and project management, comprehensive installation and

fulfillment, and wireless telecommunication infrastructure services. Our

primary client base consists of blue-chip, Fortune 200 companies in the media

and telecommunications industry, including such customers as DIRECTV, AT&T,

Clearwire Communications, Ericsson, Sprint, T-Mobile, Comcast, Cox

Communications, Verizon Communications, Charter Communications and Time Warner

Cable. We also serve significant Canadian customers, such as Rogers Cable

and Cogeco Cable. Our clients rely on our services to build and maintain

their infrastructure and networks, and provide residential and commercial

fulfillment services, all of which are critical to our clients’ ability to

deliver voice, video and data services to their end users. The majority of

our services are performed under long-term master agreements.

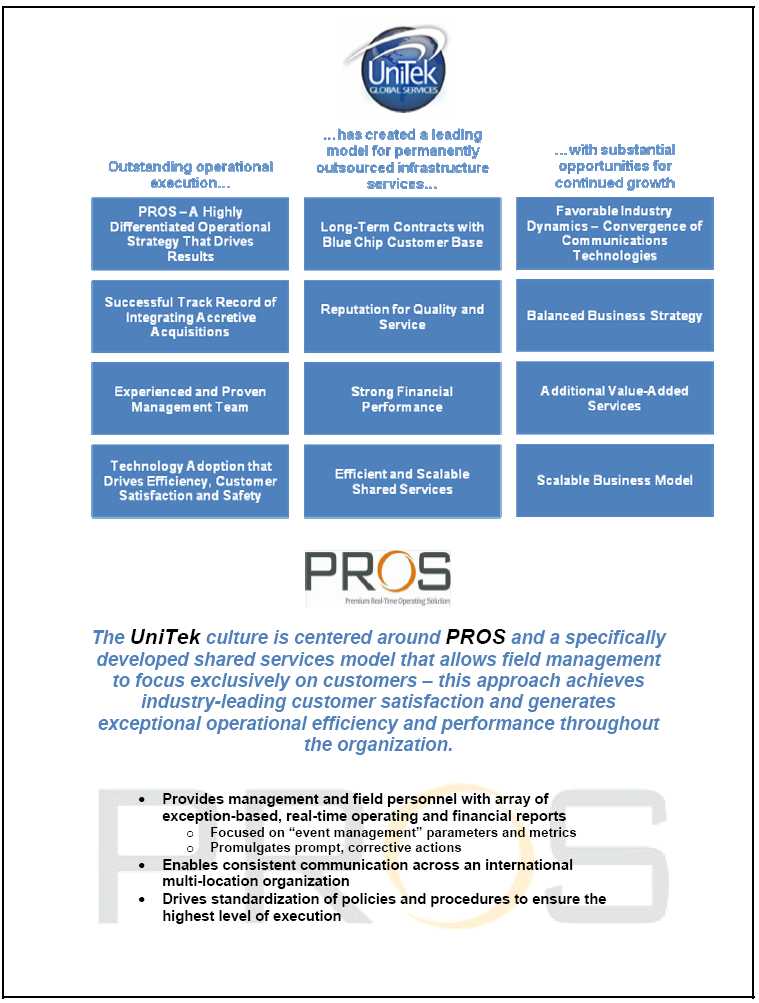

Our

operating philosophy promotes a culture of visibility and accountability and is

focused on achieving efficiencies and surpassing each customer’s performance

standards. All of our operating subsidiaries utilize our shared services

platform, which consists of accounting, fleet management, insurance, safety,

legal and corporate resources at our corporate headquarters. We have developed a

standardized set of technology enabled, real-time monitoring and reporting

capabilities, which we refer to as our Premium Real-time Operating System, or

PROS. We rely on PROS to provide detailed, real-time reports on various

performance metrics. We believe this enables management to respond rapidly

to optimize operational performance. By maintaining a centralized,

technology-enabled shared services function, we believe we can better manage our

business, control costs, and apply universal financial and operational controls

and procedures. Our shared services platform has been engineered to be

highly scalable and we believe that it can support a large increase in business

without significant modifications.

Our

strategy has enabled us to grow and scale our business units across a

diversified set of customers, geographies and end markets by executing to the

highest performance standards. We intend to leverage our high quality

performance, commitment to technology and shared service platform to grow our

revenue and profitability.

We

deliver a broad range of specialized services to our customers,

including:

|

|

·

|

Network

Engineering and Design. We are a provider of turn-key

engineering and design services to the wireless and wireline industries

that require underground plant construction, aerial infrastructure and

multi-dwelling content delivery. We have a suite of network permit, design

and engineering operations that facilitate the construction of fiber cable

placement and splicing from the user’s premises through to the service

providers’ distribution center.

|

|

|

·

|

Construction

and Project Management. We are a full-service provider

to the cable and wireline telecommunications industries of project

management and construction services, including systems engineering,

aerial and underground construction and project

management.

|

|

|

·

|

Installation

and Fulfillment Services. We are a

full-service provider of residential and commercial installation services

to the satellite television and broadband cable industries. We

provide regional fulfillment services including warehousing and logistics,

call centers, inventory management, customer service compliance, fleet

management and risk and safety compliance

services.

|

- 1

-

|

·

|

Wireless

Telecommunications Infrastructure Services. We provide

outsourced project management, construction and infrastructure services to

wireless telecommunication companies nationwide. Our core activities

include communications infrastructure equipment construction, engineering

and installation; radio frequency and network design and engineering;

radio transmission base station installation and modification; and

in-building network design, engineering and construction.

Additionally, we provide site acquisition services where we act as an

intermediary between our clients and property owners and facilitate the

wireless site preparation process from selection through

construction.

|

We report

our results in two segments: Fulfillment and Engineering &

Construction. These reportable segments are based on the services we

provide and the industries we serve. Our Fulfillment segment primarily

serves the satellite television and cable industries, where we provide

outsourced installation, upgrade and network management services. Our

Engineering & Construction segment primarily serves the wireless and

wireline telecommunications industries, where we provide engineering, design,

construction and project management services.

For the

fiscal years 2008 and 2009, we had revenues from continuing operations of $215.8

million and $278.1 million, respectively, representing growth of 28.9%. For the

three months ended April 4, 2009 and April 3, 2010, we had revenues of $68.7

million and $89.0 million, respectively, representing growth of 29.5%. On

January 27, 2010, we consummated a merger with UniTek Holdings, Inc., or

Holdings, pursuant to which our subsidiary merged, the Merger, with and into

Holdings and Holdings became our wholly owned subsidiary. For accounting

purposes, Holdings was considered the accounting acquirer, however, the Merger

was structured so that we were the surviving entity. On a pro forma basis

reflecting the combined companies, our fiscal 2009 revenues were $347.5

million.

Industry

Overview and Opportunity

We

believe the following industry trends will increase the size of the permanently

outsourced infrastructure services industry:

|

|

·

|

Faster

Technology Upgrade Cycles. The evolution of

technology has become more rapid, creating demand for increasingly faster

and more robust voice, video and data services. To support these

next generation services, communication service providers have been

investing a significant amount of capital to increase the capacity and

performance of their networks. In addition, state and local

governments have started to push for technology upgrades and enhanced

services. In February 2009, the American Recovery and Reinvestment

Act, or ARRA, was passed, and local governments, municipalities and others

have begun receiving funds for construction activities, many of which are

directly related to our areas of expertise, such as the engineering and

construction of communications networks. More than $7.0 billion of

the funds to be issued under the ARRA are earmarked to build broadband

facilities throughout the United States. As of May 2010, $2.3

billion had already been awarded to states to underwrite nearly 200

broadband projects across the country. Providers of these services

have historically outsourced the design, construction and maintenance of

their data networks to third parties in order to minimize their fixed

costs and number of employees. As these providers roll-out new

technologies and capabilities, we believe the demand for permanently

outsourced infrastructure services will

increase.

|

|

|

·

|

Wireless

Telecommunications Industry Trends. In the United

States, CTIA-The Wireless Association, or CTIA, estimates that as of

December 2009 there were 285.6 million wireless subscribers using 2.3

trillion annualized minutes. We believe that the opportunity for growth is

significant as the telecommunications industry continues to release

upgrades and new products. According to CTIA, the number of cell sites has

increased from approximately 180,000 in 2005 to approximately 250,000 in

2009. Furthermore, CTIA estimated wireless carriers invested more

than $20.0 billion upgrading their operations and expanding their

networks’ coverage in 2009. The Telecommunication Industry

Association forecasts the number of cell sites to increase to 438,000 in

2013.

|

In

addition, the Federal Communications Commission, or FCC, has issued, and we

expect it will continue to issue licenses that

grant access to new wireless spectrums to new and existing wireless service

providers. A recent example of this is LightSquared, a company funded by

Harbinger Capital to develop a state-of-the-art 4G open wireless broadband

network. In July 2010, LightSquared announced that it had partnered with

Nokia Siemens Networks for network design, equipment manufacturing and

installation and network operations and maintenance services in an agreement

worth approximately $7.0 billion over eight years.

- 2

-

|

·

|

Satellite

Industry Trends.

According to the Satellite Broadcasting & Communications

Association, as of December 2009, there were approximately 32.7 million

satellite television subscribers compared to 30.6 million as of December

2007. As digital video providers in the satellite, cable and

telecommunications industries increase their competition for subscribers,

we believe the number of gross subscriber additions and disconnections

will continue to increase, increasing the demand for our services.

Additionally, satellite providers spend a significant portion of their

retention marketing budgets on subscriber upgrade initiatives, which

typically rely on our fulfillment services in the markets we

service.

|

|

|

·

|

Cable

Industry Trends.

The National Cable & Telecommunications Association, or NCTA,

estimates there were approximately 62.1 million cable subscribers in the

United States in 2009, compared to 66.6 million in 2000. Cable

providers have been able to increase revenues despite a declining

subscriber base by increasing higher-end services, such as high-definition

video, digital video recorders, video-on-demand, high speed data and

telephony. All of these new services require higher capacity

networks, which has driven increased capital expenditures. In fact,

the NCTA estimates that between 2000 and 2009, the cable industry spent

over $131.0 billion on infrastructure

investments.

|

|

|

·

|

Continued

Convergence of Services. The communications

industry is facing increasing demand for current and future

services. Providers are reporting that data traffic, including Web

access, video messaging and other services, has begun to outpace voice

traffic. In order to support all of these services, there is, and

will continue to be, a need to increase the backhaul capacity. According

to Infonetics Research, mobile backhaul spending rose 21% to $7.2 billion

in 2009 and is expected to rise 44% by 2014 to $10.4 billion. The

demand for backhaul links will continue to increase with the convergence

of services. In addition, we believe that downstream demand from

other communications providers, such as internet service providers,

satellite operators and telecommunication resellers, who utilize backhaul

infrastructure to provide their services, will continue to increase.

As demand for these services increases, communication service providers

will need to invest capital to improve their networks to accommodate the

demand for increased capacity, which we expect should in turn increase the

demand for permanently outsourced infrastructure

services.

|

Our

Business Strengths

We

believe the following business strengths position us well to grow our

business:

|

|

·

|

Operational

Execution. Our operating philosophy promotes a culture of

visibility and accountability focused on achieving efficiencies and

surpassing each customer’s performance standards. Combined with our

shared services platform, PROS leads to our operational execution by

creating real-time accountability by enabling rapid detection and

correction of operational issues that could potentially impact

performance, productivity and profitability. We believe that our high

quality operational procedures create high customer satisfaction and

comprehensive employee accountability, setting the foundation for

continuous expansion and growth.

|

|

|

·

|

Single

Source Service Provider. As the communications

market continues to evolve due to high bandwidth driven applications, we

believe the once disparate wireline and wireless industry segments will

continue to converge into a ubiquitous technology landscape. As a

result, these industry segments will need service providers who can bridge

these two merging technologies. We intend to leverage our wireline

and wireless turn-key services to capitalize on our customers’ capital

spend. We believe that our ability to leverage our expertise in many

communications technologies provides us with a competitive advantage as

our customers have build out plans that require this expertise as their

services converge.

|

|

|

·

|

Large

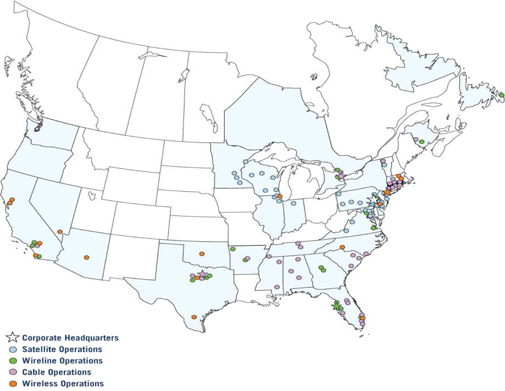

Footprint and Strong Customer Relationships. As of August 4, 2010,

our network includes 102 locations and a workforce of approximately 5,200

across the United States and Canada. Our customer base primarily

consists of blue-chip, Fortune 200 companies in the media and

telecommunications industries, including such customers as DIRECTV,

AT&T, Clearwire Communications, Ericsson, Sprint, T-Mobile, Comcast,

Cox Communications, Verizon Communications, Charter Communications and

Time Warner Cable. We also serve significant Canadian customers,

such as Rogers Cable and Cogeco

Cable.

|

- 3

-

|

·

|

Reputation

for Reliable Customer Service and Technical Expertise. We believe the

strength of our customer relationships is a direct result of our leading

customer service and technical expertise. In addition, we further

differentiate ourselves from our competitors through our integration of

various technologies into our business, including GPS devices in our

fleet, handheld equipment to streamline technician work order closure,

inventory consumption and iPhone deployment to document quality and safety

observations. We believe our reputation for excellent quality,

customer service and technical expertise gives us an advantage in

competing for new contracts as well as in maintaining and extending our

current customer relationships.

|

|

|

·

|

Experienced

Management Team. Our management team,

with an average of approximately 19 years of industry experience, plays a

significant role in establishing and maintaining long-term relationships

with our customers, supporting the growth of our business and managing the

financial aspects of our

operations.

|

Our

Strategy

The key

elements of our business strategy are:

|

|

·

|

Execute on

Existing Backlog. Our backlog

consists of uncompleted portions of services to be performed under

job-specific contracts and the estimated value of future services that we

expect to provide under master service agreements and other long-term

contracts. Many of our contracts are multi-year agreements. We

include in our backlog the amount of services projected to be performed

over the terms of the contracts, where applicable, or based on our

historical experience with customers and our experience in procurements of

this type. As of July 3, 2010, our current three-year backlog was

approximately $735 million. We intend to work closely with our

customers to ensure we execute on our already signed contracts at a

performance level that exceeds our customers’ services

requirements.

|

|

|

·

|

Expand and

Diversify our Backlog. We are

focused on growing and diversifying our backlog through strengthening our

relationships with existing customers and building relationships with new

customers. We will continue to utilize our reputation for quality

and service, together with our differentiated technological capabilities,

to win new contracts from our existing and new

customers.

|

|

|

·

|

Increase

Efficiency through Continued Development of our Technology.

We plan to continue to develop our PROS and other technologies in

an effort to ensure we have the capabilities needed to effectively and

profitably manage our operations.

|

|

|

·

|

Pursue

Selective Acquisitions. We plan to continue to selectively

pursue strategic acquisitions that complement our existing business by (i)

diversifying our service offerings, customers, end markets and

geographies, (ii) adding experienced managers to the UniTek management

team and (iii) strengthening our financial

profile.

|

Proposed

Changes to Our Capital Structure

Proposed

Reverse Stock Split

On August

4, 2010, we received the consent of the requisite number of beneficial owners of

our common stock to amend our Amended and Restated Certificate of Incorporation,

or Charter, to effect a reverse split of our common stock at a ratio not less

than one-to-eight and not greater than one-to-thirty, with the exact ratio to be

set within such range in the discretion of our board of directors without

further approval or authorization of our stockholders, with our board of

directors having the ultimate discretion as to whether or not to proceed with

the reverse split. Our board of directors has determined that, concurrently with

the closing of this offering, the shares of our common stock then outstanding

will be subject to a reverse split on a

one-for- basis.

- 4

-

Expected

Conversion of Series B Preferred

Each

share of our Series B Convertible Preferred Stock, par value $0.00002 per share,

or Series B Preferred, is convertible at any time, at the option of the holder

thereof, into shares of our common stock. According to its terms, each

share of Series B Preferred is (i) convertible into 50 shares of common stock,

subject to standard structural anti-dilution adjustments for stock splits,

dividends and similar events, and (ii) entitled to a two-for-one liquidation

preference in certain circumstances, including the currently contemplated

conversion. See “Description of Securities – Description of Preferred

Stock – Series B Preferred.”

In order

to help facilitate this offering by allowing for a simplified capital structure,

the holders of the Series B Preferred have agreed to convert their stock into

shares of our common stock upon the consummation of this offering. As an

inducement to agree to such conversion, we agreed to modify the conversion

price, while also giving effect to the two-for-one liquidation preference, such

that it will be a price representing a 6.5% discount to the offering price to

the public of the common shares in this offering. Assuming a public

offering price of $ per share, the Series B

Preferred would convert

into shares of our common

stock. The conversion will also be adjusted to give effect to the proposed

reverse split of the shares of our common stock on a

one-for- basis.

Corporate

Information

We were

organized as a corporation under the laws of the State of Delaware in 1987, as

Adina, Inc.

On

January 27, 2010, we entered into a merger agreement with Holdings, pursuant to

which our subsidiary merged with and into Holdings and Holdings became our

wholly owned subsidiary. For accounting purposes, Holdings was considered the

accounting acquirer, however, the Merger was structured so that we were the

surviving entity. On June 4, 2010, we changed our corporate name from

Berliner Communications, Inc. to UniTek Global Services, Inc.

Throughout

this prospectus, we refer to various service marks and trade names that we use

in our business. Other trademarks and service marks appearing in this

prospectus are the property of their respective holders.

In this

prospectus, the terms “UniTek,” “we,” “us,” “our” and “the Company” refer to

UniTek Global Services, Inc. and its consolidated subsidiaries.

Our

principal executive offices are located at 1777 Sentry Parkway West, Blue Bell,

Pennsylvania, 19422 and our telephone number is (267) 464-1700. Our website

address is www.unitekgs.com. The

information contained therein or connected thereto shall not be deemed to be

incorporated into this prospectus or the registration statement of which it

forms a part.

- 5

-

|

The

Offering

|

|||||||||||

|

Common

stock offered by us

|

shares

|

||||||||||

|

Common

stock outstanding

immediately

after this offering

|

shares

(1)

|

||||||||||

|

Use

of proceeds

|

The

proceeds from the sale of common stock offered by this prospectus will be

used to retire a portion of our current indebtedness and the remainder for

working capital and other general corporate purposes. See “Use of

Proceeds.”

|

||||||||||

|

Over-the-Counter

Bulletin Board

trading

symbol

|

“UGLB.OB.”

|

||||||||||

|

Proposed

NASDAQ Global Market trading symbol

|

“UNTK”

|

||||||||||

|

Risk

factors

|

See

“Risk Factors” beginning on page 9 for a discussion of factors you should

carefully consider before deciding to invest in our common

stock.

|

||||||||||

|

(1)

The number of shares of our common stock outstanding immediately after

this offering is based on 136,778,330 shares outstanding as of August 4,

2010 and excludes:

|

|||||||||||

|

·

|

18,095,434

shares of common stock issuable upon exercise of outstanding stock options

at a weighted average exercise price of $2.30 per

share;

|

||||||||||

|

·

|

18,095,434

shares of common stock issuable upon exercise of outstanding stock options

at a weighted average exercise price of $2.30 per

share;

|

||||||||||

|

·

|

8,703,572

shares of common stock issuable upon exercise of outstanding warrants at a

weighted average exercise price of $1.50 per share;

|

||||||||||

|

·

|

the

shares reserved for issuance under our 2009 Omnibus Equity and Incentive

Compensation Plan, under which we are entitled to grant a number of shares

equal to 10% of the issued and outstanding shares of common

stock;

|

||||||||||

|

·

|

shares

issuable pursuant to the underwriter’s over-allotment option;

and

|

||||||||||

|

·

|

the

conversion of all outstanding shares of our Series B Preferred into shares

of common stock, based on an assumed public offering price of $ per

share.

|

||||||||||

|

·

|

that,

concurrently with the closing of this offering, the shares of our common

stock then outstanding will be subject to a reverse split on a one-for-

basis; and

|

||||||||||

|

·

|

that

none of the anti-dilution adjustments provided in any of our outstanding

warrants or convertible preferred shares have been triggered by the

issuance of shares of our common stock in this

offering.

|

||||||||||

- 6

-

|

Reverse

Acquisition Accounting

On

January 27, 2010, Berliner Communications, Inc., or Berliner, BCI East,

Inc., a Delaware corporation and a wholly owned subsidiary of Berliner, or

BCI East, and Holdings entered into an Agreement and Plan of Merger, the

Merger Agreement, pursuant to which BCI East merged with and into Holdings

and Holdings became a wholly owned subsidiary of Berliner. The

stockholders of Holdings received 0.012 shares of our Series A Convertible

Preferred Stock, par value $0.00002 per share, or Series A Preferred, and

0.40 shares of our common stock for each share of Holdings common stock

held by them, and each share of outstanding preferred stock of Holdings

was converted into the right to receive 0.02 shares of our Series B

Preferred. For accounting purposes, Holdings was considered the accounting

acquirer, however, the Merger was structured so that we were the surviving

entity. As a result, the Berliner assets and liabilities as of January 27,

2010, the effective time of the Merger, have been incorporated into our

balance sheets based on the fair market value of the assets acquired.

Further, our results of operations reflect the operating results of

Holdings before the Merger and the combined entity after the date of the

Merger. Upon the completion of the Merger, Berliner changed its

fiscal year end from June 30 to December 31. On June 4, 2010,

Berliner changed its name to UniTek Global Services, Inc.

Consolidated

Summary Financial Data

The

following table presents consolidated summary financial information. The

statement of operations and balance sheet data as of April 3, 2010 and for

the three months ended April 4, 2009, and April 3, 2010, have been derived

from Holdings’ unaudited consolidated financial statements and include the

financial results of Berliner from January 27, 2010 to April 3, 2010, and

in the opinion of management, include all adjustments, consisting only of

normal recurring adjustments, necessary to state fairly the data for such

period. The statement of operations and balance sheet data as of and

for the years ended December 31, 2008 and December 31, 2009 had been

derived from Holdings’ audited financial statements.

As

the accounting acquirer, Holdings’ prior year results are presented for

comparative purposes. The actual results for the quarter ending

April 3, 2010 are of Holdings’ for the entire period and include the

results of operations of Berliner from January 27, 2010. The actual

results for the quarter ended April 4, 2009 include only the results of

Holdings. The actual results for the years ended December 31, 2008

and 2009 are of Holdings’ for the entire period.

All

amounts presented herein are expressed in thousands, except share and

per-share data, unless otherwise specifically noted.

|

||||||||||||||||||

|

Year Ended

|

Three Months Ended

|

|||||||||||||||||

|

December 31,

2008

|

December 31,

2009

|

April 4,

2009

|

April 3,

2010

|

|||||||||||||||

| (audited) | (unaudited) | |||||||||||||||||

|

(amounts

in thousands, except per share data)

|

||||||||||||||||||

|

Statement

of Operations Data:

|

||||||||||||||||||

|

Revenue

|

$ | 215,752 | $ | 278,098 | $ | 68,665 | $ | 88,968 | ||||||||||

|

Gross

profit

|

35,433 | 40,748 | 8,721 | 12,689 | ||||||||||||||

|

Operating

loss

|

(6,701 | ) | (51,421 | ) | (4,283 | ) | (2,915 | ) | ||||||||||

|

Net

loss

|

(23,191 | ) | (65,605 | ) | (7,569 | ) | (8,440 | ) | ||||||||||

|

Net

loss allocable to common stockholders per share:

|

||||||||||||||||||

|

Basic

|

$ | (0.21 | ) | $ | (0.60 | ) | $ | (0.07 | ) | $ | (0.07 | ) | ||||||

|

Diluted

|

$ | (0.21 | ) | $ | (0.60 | ) | $ | (0.07 | ) | $ | (0.07 | ) | ||||||

|

Weighted

average number of shares outstanding:

|

||||||||||||||||||

|

Basic

|

108,835 | 109,096 | 109,093 | 128,576 | ||||||||||||||

|

Diluted

|

108,835 | 109,096 | 109,093 | 128,576 | ||||||||||||||

- 7

-

|

April 3, 2010

|

||||||

|

(unaudited)

|

||||||

|

Balance

Sheet Data:

|

(amounts in thousands)

|

|||||

|

Current

assets

|

$ | 72,819 | ||||

|

Total

assets

|

271,752 | |||||

|

Current

liabilities

|

94,223 | |||||

|

Long-term

debt, net of current portion

|

129,577 | |||||

|

Total

stockholders’ equity

|

31,883 | |||||

- 8

-

RISK

FACTORS

The

following “risk factors” contain important information about us and our business

and should be read in their entirety. Additional risks and uncertainties

not known to us or that we believe to be immaterial could also impair our

business. If any of the following risks actually occur, our business,

results of operations and financial condition could suffer significantly.

As a result, the market price of our common stock could decline and you could

lose all of your investment.

Risks

Related to Our Business

We

have had a history of losses.

We

experienced net losses of $23.2 million in 2008 and $65.6 million in 2009 and,

giving effect to the Merger, a pro forma loss of $77.1 million from continuing

operations in 2009. We cannot predict if we will ever achieve profitability, and

if we do, be able to sustain such profitability. Further, we may incur

significant losses in the future for a number of reasons, including due to the

other risks described in this prospectus, and we may encounter unforeseen

expenses, difficulties, complications and delays and other unknown events.

Accordingly, we may not be able to achieve profitability.

Our

substantial indebtedness could adversely affect our financial

health.

As of

August 4, 2010, we and our subsidiaries have total indebtedness of approximately

$169.9 million (not including intercompany indebtedness but including capital

leases).

Our

substantial indebtedness could have important consequences to our

stockholders. For example, it could:

|

|

·

|

require

us to dedicate a substantial portion of our cash flow from operations to

payments on our indebtedness, thereby reducing the availability of our

cash flow to fund acquisitions, working capital, capital expenditures,

research and development efforts and other general corporate

purposes;

|

|

|

·

|

increase

our vulnerability to and limit our flexibility in planning for, or

reacting to, changes in our business and the industry in which we

operate;

|

|

|

·

|

place

us at a competitive disadvantage compared to our competitors that have

less debt;

|

|

|

·

|

limit

our ability to borrow additional funds;

and

|

|

|

·

|

could

make us more vulnerable to a general economic downturn than a company that

is less leveraged.

|

Additionally, the terms governing our debt

facilities limit our ability, among other things, to:

|

|

·

|

incur additional

indebtedness;

|

|

|

·

|

prepay

indebtedness;

|

|

|

·

|

sell assets, including

capital stock of restricted

subsidiaries;

|

|

|

·

|

agree to payment

restrictions affecting our restricted

subsidiaries;

|

|

|

·

|

consolidate, merge,

sell or otherwise dispose of all or substantially all of our

assets;

|

|

|

·

|

enter into transactions

with our affiliates;

|

|

·

|

incur

liens;

|

|

·

|

guarantee the

obligations or liabilities of others; and

|

|

·

|

designate any of our

subsidiaries as unrestricted subsidiaries or form additional

subsidiaries that are unrestricted subsidiaries.

|

These facilities are secured

by a blanket security interest that covers substantially all of our assets. An

event of default with respect to these facilities could result in, among other

things, the acceleration and demand for payment of all the principal and

interest due and the foreclosure on the collateral. As a result of such a default

or action against collateral, we may be forced into bankruptcy, which may result

in a loss of your investment.

- 9

-

Competition

in the industries we serve could reduce our market share and impact operating

results.

We serve

markets that are highly competitive and fragmented and in which a large number

of multinational companies compete for large, national projects, and an even

greater number of small, local businesses compete for smaller, one-time

projects. Many of our competitors are well-established and have larger and

better developed networks and systems, longer-standing relationships with

customers and suppliers, greater name recognition and greater financial,

technical and marketing resources than we have. These competitors can often

subsidize competing services with revenues from other sources and may be able to

offer their services at lower prices. These or other competitors may also reduce

the prices of their services significantly or may offer backhaul connectivity

with other services, which could make their services more attractive to

customers. Competition may place downward pressure on contract prices and

profit margins. Intense competition is expected to continue in these

markets and, if we are unable to meet these competitive challenges, we could

lose market share to our competitors and experience an overall reduction in our

operating performance and financial results.

We

are vulnerable to the cyclical nature of the telecommunications industry and,

specifically, the capital expenditures of the major telecommunications

providers.

The

demand for our outsourced infrastructure services is dependent upon the

existence of projects with engineering, procurement, construction and management

needs. The wireless telecommunications market, which is one of the

industries in which we compete, is particularly cyclical in nature and

vulnerable to downturns in the telecommunications industry. During times

of economic slowdown, some of our customers reduce their capital

expenditures. Further, customers, primarily in our wired and wireless

communications subsidiaries, sometimes defer or cancel pending projects.

As a result, demand for our services may decline during periods of economic

downturns and could adversely affect our operations and financial

performance.

We

generate a substantial portion of our revenue from a limited number of customers

and, if our relationships with such customers were harmed, our business would

suffer.

During

the year ended December 31, 2009, our four largest customers, as a percentage of

total revenue, were DIRECTV (64%), Comcast (13%), Verizon Communications (8%)

and Rogers Cable (5%). During the three months ended April 3, 2010,

our four largest customers, as a percentage of total revenue, were DIRECTV

(47%), Comcast (13%), Verizon Communications (8%) and Clearwire Communications

(6%).

We

believe that a limited number of clients will continue to be the source of a

substantial portion of our revenue for the foreseeable future. A key

factor in maintaining relationships with such customers is performance on

individual contracts and the strength of our professional reputation. To

the extent that our performance does not meet client expectations, or our

reputation or relationships with one or more key customers are impaired due to

another reason, we may lose future business with such clients, and as a result,

our ability to generate income would be adversely impacted. In addition,

key customers could slow or stop spending on initiatives related to projects we

are performing for them, due to increased difficulty in the credit markets as a

result of the recent economic crisis or other reasons. Since many of our

customer contracts allow our customers to terminate the contract without cause,

our customers may terminate their contracts with us at will and materially

impair our operating results.

We

maintain a workforce based upon current and anticipated workloads. If we

do not receive future contract awards or if these awards are delayed, we may

incur significant costs in adjusting our workforce demands.

Our

estimates of future performance depend on, among other matters, whether and when

we will receive certain new contract awards. While our estimates are based

upon good faith judgment, they can be unreliable and may frequently change based

on newly available information. In the case of larger projects, where

timing is often uncertain, it is particularly difficult to project whether and

when we will receive a contract award. The uncertainty of contract award

timing can present difficulties in matching workforce size with contractual

needs. If an expected contract award is delayed or not received, we could

incur significant costs resulting from retaining more staff than is necessary or

redundancy of facilities. Similarly, if we underestimate the workforce

necessary for a contract, we may not perform at the level expected by the client

and harm our reputation with the client. Each of these may negatively

impact our operating performance and financial results.

We

recognize revenue for fixed price construction contracts using the

percentage-of-completion method; therefore, variations of actual results from

our assumptions may reduce our profitability.

We

recognize revenue and profit on our construction contracts as the work

progresses using the percentage-of-completion method of accounting. Under

this method of accounting, contracts in progress are valued at cost plus accrued

profits less paid revenue and progress payments made on uncompleted

projects. This method relies on estimates of total expected contract

revenue and costs.

- 10

-

Contract

revenue and total cost estimates are reviewed and revised monthly by management

as the work progresses, such that adjustments to profit resulting from revisions

are made cumulative to the date of revision. Adjustments are reflected for

the fiscal period affected by such revisions. If estimates of costs to

complete long-term projects indicate a loss, we immediately recognize the full

amount of the estimated loss. Such adjustments and accrued losses may

negatively impact our operating

results.

If our customers

perform more tasks themselves, our business will

suffer.

Our success also depends

upon the continued trend by our customers to outsource their network design,

deployment and project management needs. If this trend does not continue or is

reversed and telecommunication service providers and network equipment vendors

elect to perform more of these tasks themselves, our operating results may be

adversely affected due to the decline in the demand for our

services.

We

have a lack of liquidity and will require additional capital to fund our

operations and obligations.

As of

July 30, 2010, we had cash balances and availability under existing credit

facilities of approximately $14.0 million. Because we are only minimally

capitalized, we expect to experience a lack of liquidity for the foreseeable

future in our proposed operations. We will adjust our expenses as necessary to

prevent cash flow or liquidity problems. We may need to raise additional funds

to continue to fund our operations and obligations as well as to fund potential

acquisitions. Our capital requirements will depend on several factors,

including:

|

|

·

|

our

ability to enter into new agreements with customers or to extend the terms

of our existing agreements with customers, and the terms of such

agreements;

|

|

|

·

|

the

success rate of our sales efforts;

|

|

|

·

|

costs

of recruiting and retaining qualified

personnel;

|

|

|

·

|

expenditures

and investments to implement our business strategy;

and

|

|

|

·

|

the

identification and successful completion of

acquisitions.

|

We may

seek additional funds through public and private securities offerings and/or

borrowings under lines of credit or other sources. Our inability to raise

adequate funds to support the growth of our business would materially adversely

affect our business. If we cannot raise additional capital, we may have to

implement one or more of the following remedies:

|

|

·

|

curtail

internal growth initiatives;

|

|

|

·

|

forgo

the pursuit of acquisitions; and/or

|

|

|

·

|

reduce

capital expenditures.

|

We do not

know whether additional financing will be available on commercially acceptable

terms when needed, if at all. If adequate funds are not available or are

not available on commercially acceptable terms, our ability to fund our

operations or otherwise respond to competitive pressures could be significantly

delayed or limited.

If we

raise additional funds by issuing equity securities, further dilution to our

stockholders could result, and new investors could have rights superior to those

of our existing stockholders. Any equity securities issued also may provide for

rights, preferences or privileges senior to those of holders of our common

stock. If we raise additional funds by issuing debt securities, these debt

securities would have rights, preferences and privileges senior to those of

holders of our common stock, and the terms of the debt securities issued could

impose significant restrictions on our operations.

If

we experience material delays and/or defaults in customer payments, we may be

unable to cover all expenditures related to such customer’s

projects.

Because

of the nature of some of our contracts, we commit resources to projects prior to

receiving payments from our customers in amounts sufficient to cover

expenditures as they are incurred. Delays in customer payments may require

us to make a working capital investment or obtain advances from our line of

credit. If a customer defaults in making its payments on a project or

projects to which we have devoted significant resources, it could have a

material negative effect on our results of operations and negatively impact the

financial covenants with our lenders.

- 11

-

The

nature of our construction businesses exposes us to potential liability claims

and contract disputes that may negatively affect our results of

operations.

We engage

in construction activities, including engineering and oversight of engineering

firms. Design, construction or systems failures can result in substantial

injury or damage to third parties. Any liability in excess of insurance

limits at locations constructed by us could result in significant liability

claims against us, which claims may negatively affect our results of

operations. In addition, if there is a customer dispute regarding

performance of project services, the customer may decide to delay or withhold

payment to us. If we are ultimately unable to collect on these payments,

our results of operations would be negatively impacted.

We

may experience significant fluctuations in our quarterly results relating to our

ability to generate additional revenue and manage expenditures and other

factors, some of which are outside of our control, which could cause rapid

declines in our stock price.

Our

quarterly operating results have varied considerably in the past, and may

continue to do so, due to a number of factors. Many of these factors are

outside of our control and include, without limitation, the

following:

|

|

·

|

our

ability to attract new customers, retain existing customers and increase

sales to such customers;

|

|

|

·

|

the

commencement, progress, completion or termination of contracts during any

particular quarter;

|

|

|

·

|

the

cyclical nature of the telecommunications

industry;

|

|

|

·

|

the

cost of raw materials we require for our projects;

and

|

|

|

·

|

satellite,

cable and telecommunications market conditions and economic conditions

generally.

|

Due to

these factors and others, our results for a particular quarter, and therefore,

our combined results for the affected year, may not meet the expectations of

investors, which could cause the price of our common stock to decline

significantly.

Our

backlog is subject to reduction and potential cancellation.

Our

backlog consists of uncompleted portions of services to be performed under

job-specific contracts and the estimated value of future services that we expect

to provide under master service agreements and other long-term contracts.

Many of our contracts are multi-year agreements. We include in our backlog the

amount of services projected to be performed over the terms of the contracts,

where applicable, or based on our historical experience with customers and our

experience in procurements of this type. In many instances, our customers

are not contractually committed to procure specific volumes of services under a

contract. Our estimates of backlog and a customer’s requirements

during a particular future period may not prove to be accurate, particularly in

light of the turbulent current economic conditions. If our estimated

backlog is significantly inaccurate, this could adversely affect our financial

results and the price of our common stock.

The failure to successfully identify

or integrate acquisitions could

result in a reduction of

our

operating results, cash flows and liquidity.

We have made, and in the future may

continue to make, strategic acquisitions. Acquisitions may expose us to

operational challenges and risks, including:

|

|

·

|

the

ability to profitably manage additional businesses or successfully

integrate acquired business operations and financial reporting and

accounting control systems into our

business;

|

|

|

·

|

increased

indebtedness and contingent purchase price obligations associated with an

acquisition;

|

|

|

·

|

the

ability to fund cash flow shortages that may occur if anticipated revenue

is not realized or is delayed, whether by general economic or market

conditions, or unforeseen internal

difficulties;

|

|

|

·

|

the

availability of funding sufficient to meet increased capital needs;

and

|

|

|

·

|

diversion

of management’s attention.

|

- 12

-

We may not successfully identify

suitable acquisitions in the future, and in the event we do

commence such a transaction, the failure to successfully

consummate the

acquisition or manage the operational

challenges and risks associated with the acquisition following

the consummation could adversely

affect

our results of

operations, cash flows and liquidity.

If

we do not successfully integrate our business operations with those of Berliner,

our business will be adversely affected.

We will

need to successfully integrate our business operations with those of Berliner in

order to obtain the benefits we expect from the Merger. Integrating these

operations is a complex and time-consuming process. There may be substantial

difficulties, costs and delays involved in any integration of the businesses.

These may include:

|

|

·

|

distracting

management from day-to-day

operations;

|

|

|

·

|

potential

incompatibility of corporate

cultures;

|

|

|

·

|

an

inability to achieve synergies as

planned;

|

|

|

·

|

costs

and delays in implementing common systems and

procedures;

|

|

|

·

|

retaining

existing customers and attracting new

customers;

|

|

|

·

|

retaining

key employees;

|

|

|

·

|

identifying

and eliminating redundant and underperforming operations and

assets;

|

|

|

·

|

managing

tax costs or inefficiencies associated with integrating the operations of

the combined company; and

|

|

|

·

|

making

any necessary modifications to operating control standards to comply with

the Sarbanes-Oxley Act of 2002 and the rules and regulations promulgated

thereunder.

|

The

failure to integrate our business operations with those of Berliner successfully

could have a material adverse effect on our business, financial condition and

results of operations.

We

may incur goodwill and other intangible impairment charges which could reduce

our profitability.

Pursuant

to accounting principles generally accepted in the United States, we are

required to annually assess our goodwill and indefinite-lived intangibles

to determine if they are impaired. In addition, interim reviews must be

performed whenever events or changes in circumstances indicate that impairment

may have occurred. If the testing performed indicates that impairment has

occurred, we are required to record a non-cash impairment charge for the

difference between the carrying value of the goodwill or other intangible assets

and the implied fair value of the goodwill or other intangible assets in the

period the determination is made. Disruptions to our business, end market

conditions, protracted economic weakness and unexpected significant declines in

operating results may result in charges for goodwill and other asset

impairments. We assess the potential impairment of goodwill on an annual

basis, as well as when interim events or changes in circumstances indicate that

the carrying value may not be recoverable. We assess definite-lived

intangible assets when events or changes in circumstances indicate that the

carrying value may not be recoverable. We performed our required annual goodwill

impairment test as of October 3, 2009 and determined that the carrying value of

the telecommunications reporting unit exceeded its fair value and was therefore

impaired. We also completed an impairment test of our long-lived assets at

that date for the telecommunications reporting unit. The results of the

impairment testing caused us to recognize a non-cash asset impairment charge of

$38.4 million. Future impairments could further reduce our

profitability.

Legal proceedings and other

claims could reduce our profitability, cash flows

and liquidity.

We are subject to various claims,

lawsuits and proceedings which arise in the ordinary course of business.

These actions may seek, among other things, compensation for alleged personal

injury, workers’ compensation, employment

discrimination, wage and hour disputes, breach of contract, property damage,

consequential and punitive damages, civil penalties, or injunctive or

declaratory relief. In addition, we generally

indemnify

our customers

for claims related to the services we provide. Claimants may seek

large damage awards. Defending these claims can involve significant legal

costs. When appropriate, we establish reserves against

litigation and claims that we believe to be adequate in

light of current information, legal advice and professional indemnity insurance

coverage, and we adjust such reserves from time to time according to

developments. If reserves are inadequate, insurance coverage proves to be

inadequate or unavailable, or there is an increase in liabilities for which

we self-insure, we could experience a reduction

in our profitability and liquidity. An adverse determination on any such

claim or lawsuit could have a material adverse effect on our business, financial

condition and results of operations. Separately, claims and lawsuits

alleging wrongdoing or negligence by us may harm its reputation or

divert management resources away from operating our

business.

- 13

-

Government

regulations may adversely affect our business.

Our

customers are subject to various regulations of the FCC and other international

regulations. These regulations require that these networks meet certain radio

frequency emission standards and not cause interference to other services, and

in some cases accept interference from other services. FCC regulations

could cause our customers to slow down or delay development and deployment plans

for network build outs, which could impact our financial results.

We maintain a high-deductible

liability insurance program, which exposes us to a substantial portion of

the costs of claims and lawsuits.

Although we maintain insurance policies

with respect to automobile liability, general liability, workers’ compensation and employee

group health claims, those policies are subject to high deductibles.

Because most claims against us do not exceed the

deductibles under its insurance policies, we are effectively self-insured for

substantially all claims. We determine any liabilities for

unpaid claims and associated expenses, including incurred but not reported

losses, and reflect the present value of those liabilities in our balance sheet as other

current and non-current liabilities. The determination of such claims and

expenses and the appropriateness of the related liability is reviewed and

updated quarterly. However, insurance liabilities are difficult to assess and

estimate due to the many relevant factors, including the severity of an injury

or legitimacy of a claim and the determination of our liability in proportion to

other parties. If our insurance claims increase or

costs exceed our estimates of insurance

liabilities, we may experience a decline in

operating results and liquidity.

Increases in our insurance premiums or

collateral requirements could significantly reduce our profitability, liquidity and

availability under our credit

facilities.

Because of factors such as

increases in claims, projected significant increases in medical costs and wages,

lost compensation and reductions in coverage, insurance carriers may be

unwilling to continue to provide us with our current levels of

coverage without a significant increase in insurance premiums or collateral

requirements to cover our deductible obligations. An increase in premiums or

collateral requirements could significantly reduce our profitability and liquidity

as well as reduce availability under our credit facilities.

Our

operating results can be negatively affected by weather conditions.

We

perform most of our services outdoors. Adverse weather conditions may

affect productivity in performing services or may temporarily prevent us from

performing services for our customers. The affect of weather delays on

projects that are under fixed price arrangements may be greater if we are unable

to adjust the project schedule for such delays. A reduction in

productivity in any given period or our inability to meet guaranteed schedules

may adversely affect the profitability of our projects.

We

bear the risk of cost overruns in some of our contracts.

We

conduct our business under varying contractual arrangements, some of which are

long-term and generate recurring revenue at agreed upon pricing. Certain

of our contracts have prices that are established, in part, on cost and

scheduling estimates which are based on a number of assumptions, including,

without limitation, assumptions about future economic conditions, prices and

availability of labor, prices of equipment and materials and other

variables. These assumptions are made more difficult to ascertain by the

current uncertainty in the capital markets and the wide fluctuation in prices

for equipment, fuel and other costs associated with our services.

Specifically, we are affected by the cost of crude oil used for fuel.

Crude oil prices have historically been volatile. We do not enter into

hedge transactions to reduce our exposure to price risks and cannot assure you

that we will be successful in passing on these attendant costs if these risks

were to materialize. If cost assumptions prove inaccurate or circumstances

change, cost overruns may occur and, as a result, we may experience reduced

profits or, in some cases, a loss for those projects affected.

- 14

-

If

we are unable to recruit and retain key managers and employees, our business may

be adversely affected.

We depend

on the services of our executive officers and the senior management of our

subsidiaries. Our management team has an average of approximately 19 years

of experience in our industry; the loss of any of them could negatively affect

our ability to execute our business strategy. Although we have entered

into employment agreements with our executive officers and certain other key

employees, we cannot guarantee that any key management personnel will remain

employed by us. The loss of key management could adversely affect the management

of our operations.

In

addition, the services we deliver to our clients could be delayed or interrupted

if we are unable to attract, train and retain highly skilled employees,

particularly, installation technicians. Competition for these employees is

intense. Because of the complex and technical nature of some of our services,

any failure to attract and retain a sufficient number of qualified employees

could materially harm our business.

We

have in the past and may in the future experience deficiencies, including

material weaknesses, in internal control over financial reporting. Our business

and our share price may be adversely affected if we do not remediate these

material weaknesses or if we have other weaknesses in our internal

controls.

With

respect to fiscal year 2008, Holdings identified control deficiencies, including

a material weakness, in its internal control over financial reporting in which

unbilled accounts receivable and the related revenue were

misstated. Beginning in early 2009, we have remediated the material

weakness and improved the accounting system and internal processes. While we

have made efforts to improve our accounting policies and procedures, additional

deficiencies and weaknesses may be identified. If material weaknesses or

deficiencies in our internal controls exist and go undetected, our financial

statements could contain material misstatements that, when discovered in the

future, could cause us to fail to meet our future reporting obligations and

cause the price of our common stock to decline.

In

addition, in mid-2010, we identified a mathematical error within cash provided

from operations on the Consolidated Statements of Cash Flows of Holdings for the

years ended December 31, 2008 and 2009. As a result of the error, discontinued

operations amounts were inadvertently characterized as loss rather than

income. As a result of the discovery of the error, management has

taken steps to evaluate internal controls and has concluded their design is

appropriate. Management believes that future occurrences of mathematical errors

of this type or a similar type will be prevented as a result of proper execution

of existing controls.

Risks

Related to our Company and our Common Stock

Our

historic stock price has been volatile and purchasers of our common stock could

incur substantial losses.

Historically,

our stock price has been volatile. The stock market in general,

particularly recently, has experienced extreme volatility that has often been

unrelated to the operating performance of particular companies. As a

result of this volatility, investors may not be able to sell our common stock at

or above their respective purchase prices. The market price for our common

stock may be influenced by many factors, including, but not limited to,

variations in our financial results or those of companies that are perceived to

be similar to us, investors’ perceptions of us, the number of our shares

available in the market, future sales of our common stock and securities

convertible into our common stock, and general economic, industry and market

conditions. In addition, in the past two years, the stock market has experienced

significant price and volume fluctuations. This volatility has had a

significant impact on the market price of securities issued by many companies,

including companies in our industry. The changes frequently appear to

occur without regard to the operating performance of the affected