Attached files

| file | filename |

|---|---|

| EX-31.2 - CERTIFICATION PURSUANT TO 17 CFR 240.13(A)-14(A) - NEDAK ETHANOL, LLC | form10qex312_081210.htm |

| EX-32.1 - CERTIFICATION PURSUANT TO 18 U.S.C. SECTION 1350 - NEDAK ETHANOL, LLC | form10qex321_081210.htm |

| EX-31.1 - CERTIFICATION PURSUANT TO 17 CFR 240.13(A)-14(A) - NEDAK ETHANOL, LLC | form10qex311_081210.htm |

| EX-32.2 - CERTIFICATION PURSUANT TO 18 U.S.C. SECTION 1350 - NEDAK ETHANOL, LLC | form10qex322_081210.htm |

| EX-10.1 - SIXTH SUPPLEMENT AND FORBEARANCE AGREEMENT - NEDAK ETHANOL, LLC | form10qexh101_081210.htm |

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

|||

|

Form 10-Q

|

|||

|

(Mark one)

|

|||

|

R

|

QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

||

|

For the quarterly period ended June 30, 2010

|

|||

|

£

|

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

||

|

For the transition period from _________ to __________

|

|||

|

Commission file number 000-52597

|

|||

|

NEDAK ETHANOL, LLC

|

|||

|

(Exact name of registrant as specified in its charter)

|

|||

|

Nebraska

|

20-0568230

|

||

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

||

|

87590 Hillcrest Road, P.O. Box 391, Atkinson, Nebraska 68713

|

|||

|

(Address of principal executive offices)

|

|||

|

(402) 925-5570

|

|||

|

(Registrant’s telephone number, including area code)

|

|||

|

__________________________________________________________________

|

|||

|

(Former name, former address and former fiscal year, of changed since last report)

|

|||

|

Indicate by check mark whether the registrant has (1) filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes R No £

|

|||

|

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the proceeding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes £ No R

|

|||

|

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

|||

|

Large accelerated filer £ Accelerated filer £ Non-accelerated filer £ Smaller reporting company R

|

|||

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes £ No R

|

|||

|

As of August 1, 2010, the issuer had 5,233 Common and 185.5 Class A Preferred Membership Units issued and outstanding.

|

|||

TABLE OF CONTENTS

|

PART I—FINANCIAL INFORMATION

|

|||

|

Item Number

|

Item Matter

|

Page Number

|

|

|

Item 1.

|

Condensed Unaudited Financial Statements.

|

1

|

|

|

Item 2.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations.

|

16

|

|

|

Item 4T.

|

Controls and Procedures.

|

28

|

|

|

PART II—OTHER INFORMATION

|

|||

|

Item 1.

|

Legal Proceedings.

|

28

|

|

|

Item 2.

|

Unregistered Sales of Equity Securities and Use of Proceeds.

|

28

|

|

|

Item 3.

|

Defaults Upon Senior Securities.

|

28

|

|

|

Item 5.

|

Other Information.

|

29

|

|

|

Item 6.

|

Exhibits.

|

29

|

|

|

Signatures

|

30

|

||

i

PART I—FINANCIAL INFORMATION

Item 1. Financial Statements.

|

NEDAK ETHANOL, LLC

|

||||||||

|

Condensed Unaudited Balance Sheets

|

||||||||

|

June 30,

2010

|

December 31,

2009

|

|||||||

|

ASSETS (Note 7)

|

||||||||

|

Current Assets

|

||||||||

|

Cash and equivalents

|

$

|

434,758

|

$

|

1,853,959

|

||||

|

Restricted short term investment (Note 6)

|

1,163,581

|

1,153,708

|

||||||

|

Restricted cash (Notes 7, and 8 and 10)

|

4,014,435

|

997,656

|

||||||

|

Accounts receivable

|

1,517,409

|

1,149,804

|

||||||

|

Commodity broker receivable

|

13,532

|

94,391

|

||||||

|

Inventory (Notes 3 and 9)

|

1,962,395

|

2,971,319

|

||||||

|

Derivative financial instruments (Notes 4 and 9)

|

-

|

5,325

|

||||||

|

Prepaid expenses and other

|

917,165

|

622,443

|

||||||

|

Total current assets

|

10,023,275

|

8,848,605

|

||||||

|

Property and Equipment

|

||||||||

|

Land and improvements

|

4,408,272

|

4,408,272

|

||||||

|

Buildings

|

9,121,024

|

9,102,173

|

||||||

|

Plant equipment

|

73,204,195

|

73,204,195

|

||||||

|

Office equipment

|

200,575

|

200,575

|

||||||

|

Vehicles

|

560,383

|

468,617

|

||||||

|

87,494,449

|

87,383,832

|

|||||||

|

Less accumulated depreciation

|

(9,262,675)

|

(6,233,212)

|

||||||

|

Net property and equipment

|

78,231,774

|

81,150,620

|

||||||

|

Other Assets

|

||||||||

|

Deposits

|

300,000

|

300,000

|

||||||

|

Debt issuance costs, net of accumulated amortization of $573,775 and $419,256 as of June 30, 2010 and December 31, 2009

|

1,187,460

|

1,341,979

|

||||||

|

Total other assets

|

1,487,460

|

1,641,979

|

||||||

|

Total Assets

|

$

|

89,742,509

|

$

|

91,641,204

|

||||

|

LIABILITIES AND MEMBERS’ EQUITY

|

||||||||

|

Current Liabilities

|

||||||||

|

Current maturities of long-term debt (Notes 2, 7 and 8)

|

$

|

6,296,789

|

$

|

3,205,471

|

||||

|

Accounts payable

|

||||||||

|

Trade

|

1,495,633

|

1,834,787

|

||||||

|

Corn

|

2,113,664

|

2,688,561

|

||||||

|

Accrued liabilities (Note 2)

|

3,802,570

|

2,401,015

|

||||||

|

Reclassification of long-term debt to current (Notes 2, 7 and 8)

|

41,887,475

|

45,873,529

|

||||||

|

Total current liabilities

|

55,596,131

|

56,003,363

|

||||||

|

Long-Term Debt, net of Current Maturities (Notes 2, 7, 8 and 10)

|

18,750

|

18,750

|

||||||

|

Commitments and Contingencies (Notes 2, 6 and 10)

|

||||||||

|

Members’ Equity (Note 5)

|

||||||||

|

Preferred Units, 185.5 and 185.4 units issued and outstanding as of June 30, 2010 and December 31, 2009, respectively

|

1,854,503

|

1,854,428

|

||||||

|

Common Units, net of offering costs, 5,233 units issued and outstanding

|

49,839,281

|

49,839,281

|

||||||

|

Accumulated deficit

|

(17,566,156)

|

(16,074,618)

|

||||||

|

Total members’ equity

|

34,127,628

|

35,619,091

|

||||||

|

Total Liabilities and Members’ Equity

|

$

|

89,742,509

|

$

|

91,641,204

|

||||

|

See Notes to Condensed Unaudited Financial Statements.

|

||||||||

1

|

NEDAK ETHANOL, LLC

|

||||

|

Condensed Unaudited Statements of Operations

|

||||

|

Three Months Ended June 30,

|

||||

|

2010

|

2009

|

|||

|

Revenues

|

$

|

21,444,494

|

$

|

11,978,882

|

|

Cost of Goods Sold

|

23,195,969

|

14,827,531

|

||

|

Gross Loss

|

(1,751,475)

|

(2,848,649)

|

||

|

General and Administrative Expenses

|

610,043

|

732,291

|

||

|

Operating Loss

|

(2,361,518)

|

(3,580,940)

|

||

|

Other Income (Expense)

|

||||

|

Interest income

|

9,226

|

12,109

|

||

|

Interest expense

|

(867,407)

|

(854,061)

|

||

|

Other expenses

|

1,194

|

-

|

||

|

Total other income (expense), net

|

(856,987)

|

(841,952)

|

||

|

Net Loss

|

$

|

(3,218,505)

|

$

|

(4,422,892)

|

|

Weighted Average Common Units

Outstanding—Basic & Diluted

|

5,233

|

5,233

|

||

|

Net Income (Loss) Per Common Unit—Basic & Diluted (Note 5)

|

$

|

(615.04)

|

$

|

(845.19)

|

|

See Notes to Condensed Unaudited Financial Statements.

|

||||

2

|

NEDAK ETHANOL, LLC

|

||||

|

Condensed Unaudited Statements of Operations

|

||||

|

Six Months Ended June 30,

|

||||

|

2010

|

2009

|

|||

|

Revenues

|

$

|

42,375,739

|

$

|

25,285,079

|

|

Cost of Goods Sold

|

44,101,079

|

30,709,680

|

||

|

Gross Loss

|

(1,725,340)

|

(5,424,601)

|

||

|

General and Administrative Expenses

|

1,066,941

|

1,242,819

|

||

|

Operating Loss

|

(2,792,281)

|

(6,667,420)

|

||

|

Other Income (Expense)

|

||||

|

Gain from litigation settlement (Note 10)

|

3,000,000

|

-

|

||

|

Interest income

|

17,694

|

28,404

|

||

|

Interest expense

|

(1,718,406)

|

(1,627,648)

|

||

|

Other expenses

|

1,455

|

-

|

||

|

Total other income (expense), net

|

1,300,743

|

(1,599,244)

|

||

|

Net Loss

|

$

|

(1,491,538)

|

$

|

(8,266,664)

|

|

Weighted Average Common Units

Outstanding—Basic & Diluted

|

5,233

|

5,233

|

||

|

Net Loss Per Common Unit—Basic & Diluted (Note 5)

|

$

|

(285.03)

|

$

|

(1,579.72)

|

|

See Notes to Condensed Unaudited Financial Statements.

|

||||

3

|

NEDAK ETHANOL, LLC

|

|||||||||||||||

|

Condensed Unaudited Statements of Cash Flows

|

|||||||||||||||

|

Six Months Ended June 30,

|

|||||||||||||||

|

2010

|

2009

|

||||||||||||||

|

Cash Flows from Operating Activities

|

|||||||||||||||

|

Net loss

|

$

|

(1,491,538)

|

$

|

(8,266,664)

|

|||||||||||

|

Adjustments to reconcile net loss to net cash used in operations:

|

|||||||||||||||

|

Depreciation and amortization

|

3,183,982

|

3,187,089

|

|||||||||||||

|

Lower of cost or market adjustment on inventory

|

452,784

|

-

|

|||||||||||||

|

Change in fair value of derivative financial instruments

|

5,325

|

-

|

|||||||||||||

|

Gain from litigation settlement

|

(3,000,000)

|

-

|

|||||||||||||

|

Change in operating assets and liabilities:

|

|||||||||||||||

|

Receivables

|

(286,746)

|

(2,103,683)

|

|||||||||||||

|

Inventory

|

556,140

|

(733,332)

|

|||||||||||||

|

Prepaid expenses and other

|

(294,722)

|

(77,805)

|

|||||||||||||

|

Deposits

|

-

|

(300,000)

|

|||||||||||||

|

Accounts payable

|

(814,051)

|

4,853,908

|

|||||||||||||

|

Accrued liabilities

|

1,401,555

|

1,076,826

|

|||||||||||||

|

Net cash provided by (used in) operating activities

|

(287,271)

|

(2,363,661)

|

|||||||||||||

|

Cash Flows from Investing Activities

|

|||||||||||||||

|

Capital expenditures

|

(110,617)

|

(165,325)

|

|||||||||||||

|

Net change in restricted cash and investments

|

(26,652)

|

(3,537,645)

|

|||||||||||||

|

Net cash used in investing activities

|

(137,269)

|

(3,702,970)

|

|||||||||||||

|

Cash Flows from Financing Activities

|

|||||||||||||||

|

Proceeds from construction loan

|

-

|

779,376

|

|||||||||||||

|

Payment on construction loan

|

(894,736)

|

-

|

|||||||||||||

|

Sale of Preferred Units

|

75

|

1,844,428

|

|||||||||||||

|

Proceeds from Delta-T letter of credit

|

-

|

3,995,000

|

|||||||||||||

|

Payment on tax increment financing

|

-

|

(139,000)

|

|||||||||||||

|

Payments for deferred offering costs

|

-

|

(10,568)

|

|||||||||||||

|

Debt issuance costs

|

(100,000)

|

-

|

|||||||||||||

|

Net cash provided by (used in) financing activities

|

(994,661)

|

6,469,236

|

|||||||||||||

|

Increase (Decrease) in Cash and Equivalents

|

(1,419,201)

|

402,605

|

|||||||||||||

|

Cash and Equivalents—Beginning of Period

|

1,853,959

|

94,691

|

|||||||||||||

|

Cash and Equivalents—End of Period

|

$

|

434,758

|

$

|

497,296

|

|||||||||||

|

See Notes to Condensed Unaudited Financial Statements.

|

|||||||||||||||

4

NEDAK ETHANOL, LLC

Notes to Condensed Unaudited Financial Statements

June 30, 2010

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The unaudited interim condensed financial statements of NEDAK Ethanol, LLC (the “Company”) reflect all adjustments consisting only of normal recurring adjustments that are, in the opinion of management, necessary for fair presentation of financial position, results of operations and cash flows. The results for the three and six month periods ended June 30, 2010 is not necessarily indicative of the results that may be expected for a full fiscal year. Certain information and footnote disclosures normally included in annual financial statements prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) are condensed or omitted pursuant to the rules and regulations of the Securities and Exchange Commission (“SEC”), although the Company believes that the disclosures made are adequate to make the information not misleading. The accompanying balance sheet as of December 31, 2009 is derived from the audited financial statements as of that date. These condensed unaudited financial statements should be read in conjunction with the Company’s audited financial statements and notes thereto included in the annual report for the year December 31, 2009, filed as an exhibit to the Form 10-K filed with the SEC.

Nature of Business

The Company operates a 44 million gallon per year ethanol plant in Atkinson, Nebraska, and produces and sells fuel ethanol and distillers grains, a co-product of the ethanol production process. Sales of ethanol and distillers grains began in January 2009.

Accounting Estimates

Management uses estimates and assumptions in preparing these financial statements in accordance with GAAP. Those estimates and assumptions affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities, and the reported revenues and expenses. The Company uses estimates and assumptions in accounting for the following significant matters, among others: the allowance for doubtful accounts, useful lives of property and equipment, the valuation of inventory and inventory purchase commitments and long-lived asset impairments including the assumptions used to estimate future cash flows, the ability to raise capital, and the ability to comply with certain provisions within the Company’s credit agreements. Actual results may differ from estimated amounts, and such differences may be material to the Company’s financial statements. The Company periodically reviews estimates and assumptions, and the effects of revisions are reflected in the period in which the revisions are made.

2. LIQUIDITY AND MARKET UNCERTAINTIES

The Company has certain risks and uncertainties that it experiences during volatile market conditions such as what the ethanol industry experienced during 2008 and which continued through 2009 and into 2010. These volatilities can have a severe impact on operations.

In 2009, the Company completed construction of its ethanol production facilities with nameplate capacity of 44 million gallons per year and a remote rail load-out facility. In accordance with the Company’s policy for evaluating impairment of long-lived assets, management has estimated that the projected future undiscounted cash flows from operations of these facilities exceed their carrying value as of June 30, 2010; therefore, no impairment loss was recognized. In determining the projected future undiscounted cash flows, the Company has made significant assumptions concerning the future viability of the ethanol industry, the future price of corn in relation to the future price of ethanol and the overall demand for ethanol in relation to production and supply capacity.

The Company’s operating and financial performance is largely driven by the prices at which it sells ethanol and the net cost of corn. The price of ethanol is influenced by factors such as supply and demand, the weather, government policies and programs, unleaded gasoline prices and the petroleum markets as a whole. Excess ethanol supply in the market, in particular, puts downward pressure on the price of ethanol. The Company’s largest cost of production is

5

NEDAK ETHANOL, LLC

Notes to Condensed Unaudited Financial Statements

June 30, 2010

corn. The Company’s cost of corn is generally impacted by factors such as supply and demand, the weather, government policies and programs, and risk management techniques used to protect against the price volatility. The Company is subject to significant risk that its operating margins may be reduced or eliminated due to the relative movements in the market prices of its products and major manufacturing inputs. As a result, market fluctuations in the price of or demand for these commodities can have a significant adverse effect on the Company’s operations and profitability. Due to the current conditions of these commodity markets, the Company may continue to generate negative margins.

As of June 30, 2010, the Company was in default of its Credit Agreement and its Tax Increment Financing, as further discussed in Notes 7 and 8. For this reason, the Company has reclassified amounts owing under these loans as current liabilities. Such treatment of the Company’s long term debt will continue, as required by GAAP, until such defaults are cured.

Because of these events and market conditions, there is an increased level of uncertainty with respect to the Company’s ability to obtain sufficient cash flows from operations or debt or equity financing sufficient to cover the liquidity needed for ongoing operations. The Company’s efforts to secure working capital include:

|

|

·

|

The Company has received notice that an application for a United States Department of Agriculture (“USDA”) Value Added Producers Grant for working capital of $300,000 on November 30, 2009 was accepted and expects to receive funding after receipt of instructions from the local USDA office.

|

|

|

·

|

The Company and its lender have received conditional approval from the USDA of an application for a Business and Industries Guaranteed Loan (the “B&I Loan”) in the amount of $5,000,000 for additional working capital. Final USDA approval for the B&I Loan is conditioned on reaching a 40% net worth ratio and final approval by the Company’s lender. As of June 30, 2010, the Company’s net equity was 38% of its total assets. The lender has also indicated it will require certain other conditions, including an additional capital contribution to the Company.

|

|

|

·

|

At the end of the second quarter of 2010, the Company has expanded efforts to mitigate the liquidity shortfall needed for ongoing operations and the working capital required by effective risk management practices to include discussions with firms offering tolling arrangements for production volumes and other contracting alternatives to improve risk management results and reduce working capital as well as additional sources of capital.

|

|

|

·

|

The Company has continued discussions with the lenders to identify alternative actions to resolve defaults under the Credit Agreement and Tax Increment Financing including obtaining additional capital and changes to marketing strategies to reduce market risk.

|

Exclusive of the reclassification of the majority of the Company’s long term debt to current liabilities, the Company would have had negative working capital of $3,685,381, which includes restricted cash and investments of $5,178,016, and which includes only Current Maturities of Long Term Debt that represent normal amortization of principal, as of June 30, 2010. As reported in the Balance Sheet, the reclassification of long term debt to current liabilities resulted in negative working capital of $45,572,856 as of June 30, 2010.

Accrued liabilities include accrued board compensation of $772,250 and $742,500 as of June 30, 2010 and December 31, 2009, respectively, and accounts payable-corn include amounts owing to the Company’s grain procurement agent totaling approximately $735,642 and $815,000 as of June 30, 2010 and December 31, 2009, respectively, which have had favorable payment terms. If these favorable payment terms cease, more cash may be required.

These financial statements have been prepared assuming the Company will continue as a going concern. Until the Company is able to obtain additional working capital from the above options, for which no assurance can be given, or from operations, in addition to modifying the Credit Agreement covenants or refinancing the construction loan, there is substantial doubt as to whether the Company can continue to operate as a going concern.

6

NEDAK ETHANOL, LLC

Notes to Condensed Unaudited Financial Statements

June 30, 2010

3. INVENTORY

Inventory consists of the following:

|

June 30, 2010

|

December 31, 2009

|

|||

|

Raw Materials

|

$

|

322,961

|

$

|

1,561,766

|

|

Work in Process

|

504,374

|

567,410

|

||

|

Finished goods

|

1,135,060

|

842,143

|

||

|

Total

|

$

|

1,962,395

|

$

|

2,971,319

|

4. DERIVATIVE FINANCIAL INSTRUMENTS

The Company seeks to hedge a portion of its future corn and natural gas purchases to the extent considered necessary for minimizing risk from market price fluctuations. However, as of June 30, 2010, the Company had no open positions for corn on the Chicago Board of Trade to hedge its forward corn commitments and no open positions for natural gas. Derivative financial instruments recorded on the balance sheet represent the current fair value of the instruments.

There were no derivative financial instruments as of June 30, 2010. The following table provides details regarding the Company’s derivative financial instruments as of December 31, 2009, none of which are designated as hedging instruments:

|

Instrument

|

Balance Sheet Location

|

Assets

|

Liabilities

|

|||||

|

December 31, 2009

|

Commodity contracts

|

Derivative financial instruments

|

$

|

5,325

|

$

|

-

|

The following table demonstrates the Company’s gains from derivative financial instruments in the statements of operations, none of which are designated as hedging instruments:

|

Derivatives not

|

Location of Gain

|

Amount of Gain

|

||||

|

Designated as Hedging

|

Recognized in

|

Recognized in

|

||||

|

Instruments

|

Income

|

Income

|

||||

|

Six months ended June 30, 2010

Three months ended June 30, 2010

|

|

Commodity contracts

Commodity contracts

|

Cost of goods sold

Cost of goods sold

|

$

|

707,266

18,304

|

|

|

Six months ended June 30, 2009

Three months ended June 30, 2009

|

Commodity contracts

Commodity contracts

|

|

Cost of goods sold

Cost of goods sold

|

-

-

|

5. MEMBERS’ EQUITY

As of June 30, 2010, there were 185.5 preferred membership units (“Preferred Units”) at $10,000 per unit. The Preferred Units entitle the holders thereof, among other things, to receive a preferred cumulative distribution of 10% (“Preferred Return”) before holders of common membership units receive distributions. Following the third anniversary of the issuance of the Preferred Units, the Company may redeem Preferred Units for the original purchase price plus any accrued but unpaid distributions. The accumulated undeclared Preferred Return as of June 30, 2010 was $225,412, and the total liquidation preference of the Preferred Units as of June 30, 2010 was $2,079,915.

Losses are generally allocated to all units based upon their respective percentage of units held, except that losses are not allocated to Preferred Units if the Preferred Return has not been achieved. For purposes of computing the net

7

NEDAK ETHANOL, LLC

Notes to Condensed Unaudited Financial Statements

June 30, 2010

loss per common unit for the three and six months ended June 30, 2010 and 2009, no losses were allocated to the Preferred Units since the Preferred Return has not been achieved.

6. LINE OF CREDIT

In March 2006, the Company entered into a line of credit agreement in favor of its natural gas transporter (see Note 10) to reserve pipeline space. The Company may draw up to $150,000. Interest is payable upon the lender’s demand or in May 2011 at a rate of 3.35%. In August 2007, the Company entered into a line of credit agreement in favor of its natural gas transporter for the service of transporting gas. The Company may draw up to $923,828. Interest is payable upon the lender’s demand at a rate of 3.75%. These agreements are secured by restricted short term investments totaling $1,163,581 as of June 30, 2010 and $1,153,708 as of December 31, 2009. As of June 30, 2010 and December 31, 2009, there were no borrowings outstanding on the lines of credit.

7. LONG-TERM DEBT

|

June 30, 2010

|

December 31, 2009

|

|||

|

Construction loan under Credit Agreement

|

$

|

41,605,264

|

$

|

42,500,000

|

|

Members’ notes payable

|

18,750

|

18,750

|

||

|

Tax increment financing note (Note 8)

|

6,579,000

|

6,579,000

|

||

|

48,203,014

|

49,097,750

|

|||

|

Less current maturities under original terms

|

(6,296,789)

|

(3,205,471)

|

||

|

Less reclassified long-term debt to current

|

(41,887,475)

|

(45,873,529)

|

||

|

$

|

18,750

|

$

|

18,750

|

Construction Loan under Credit Agreement

In February 2007, the Company entered into a senior credit facility (“Credit Agreement”) with AgCountry Farm Credit Services, FLCA (“Lender”) for a multiple advance construction loan totaling $42,500,000. The Company was required to make interest payments during the construction phase at the thirty-day LIBOR plus 3.4%, but not less than 6.0%. The interest rate was 6.0% as of June 30, 2010. The performance test of the plant was completed in June 2009, but three significant equipment deficiencies prevented final acceptance at that time. The Credit Agreement provides that the construction loan is to be converted at final acceptance to a permanent ten year term loan of $32,500,000 and a $10,000,000 revolving term loan. The Company is in negotiations with Lender to convert the loan to long term financing.

The Credit Agreement requires the Company to maintain certain financial covenants, including minimum working capital of $6,000,000, minimum current ratio of 1.20:1.00, minimum tangible net worth of $41,000,000, minimum owners’ equity ratio of 50%, and a minimum fixed charge coverage ratio of 1.25:1.00, and also includes restrictions on distributions and capital expenditures. As of June 30, 2010, the Company was not in compliance with the working capital covenants (working capital was $(3,685,381) exclusive of the debt reclassification), the current ratio requirement (a current ratio of 0.73:1.00 without debt reclassification), the tangible net worth requirement (tangible net worth was $38,844,143) and the fixed charge coverage ratio (intended to be an annual measure, but using year to date measures and six months of principal payment that ratio is 0.67 : 1.00). The Credit Agreement contains certain prepayment fees in the first four years of the scheduled payments, and the loan is secured by substantially all the Company’s assets.

Under the terms of the Credit Agreement, the Company is required to make level monthly principal payments of approximately $447,368 beginning April 1, 2010 and ending on February 1, 2018. If the B&I Loan is granted, the amount and terms of conversion of the construction loan to a Term Loan and a Revolving Term Loan for working capital may change. Two principal payments were made in April, 2010 for the April 1 and May 1, 2010 payments. The Company has not made payments due on June 1, July 1 or August 1 in order to conserve working capital. The Lender has the ability to make payments of both principal and interest from the restricted cash held on account at the

8

NEDAK ETHANOL, LLC

Notes to Condensed Unaudited Financial Statements

June 30, 2010

Lender. However, the Lender has not yet started to do so as of July 30, 2010. This leaves principal and interest payments unpaid and delinquent.

Under the terms of the Credit Agreement, the Company must pay a commitment fee of 0.25% on the unused portion of the revolving promissory note upon conversion to the revolving term loan. In addition, the Company was required to establish and fully fund a $2,400,000 Debt Service Reserve Account on or prior to the loan conversion date, no later than August 1, 2009. At such time, the commitment amount would have been reduced to an amount not to exceed $7,600,000 and the Debt Service Reserve Fund would no longer be required to be funded. This requirement was not met. The Company and Lender are discussing amendments to the terms of the Credit Agreement which may modify the foregoing provisions.

The Company executed a Fourth Supplement and Forbearance Agreement to Master Credit Agreement on March 27, 2009 (the “Fourth Supplement”). In connection with the Fourth Supplement, the Lender required the Company to obtain $1,000,000 of equity or subordinate debt capital by April 30, 2009, which was guaranteed by the Company’s board of directors in addition to the Preferred Units purchased by the Directors discussed in Note 5. The Lender extended this April 30, 2009 date to June 30, 2009 by which time the Company only received $844,428. The payment terms of the additional loan fee of $250,000 from the third amendment to the Credit Agreement were modified to provide that the fee will be paid in five $50,000 quarterly installments beginning on or before January 1, 2010. In addition, the Company undertook to achieve and maintain indefinitely 100% name plate production on or before May 1, 2009. The Fourth Supplement also provided that the interest on the unpaid principal amount of the construction and term loans accrues at a variable interest rate equal to LIBOR plus 5.40%, but not less than 6.00%. In addition to the Fourth Supplement, the Lender delayed required compliance by the Company of certain financial covenants in the Credit Agreement until after September 30, 2009 as well as delayed the requirement to make excess cash flow payments until December 31, 2009. On July 24, 2009, the Lender again declared the Company in default, due to delinquent payment of fees and interest, deficiency in the raising of equity or subordinated debt, and failure to achieve nameplate production by May 1, 2009.

On September 30, 2009, the Company executed a Fifth Supplement and Forbearance Agreement to the Master Credit Agreement (“Fifth Supplement”) with the Lender, which (i) extended the dates to pay loan fees of $250,000 to begin on January 1, 2010 with $50,000 per quarter through January 1, 2011 and restructure fees of $100,000 with an additional payment of $100,000 payable on or before June 30, 2010, (the first payment of $50,000 was made on January 31, 2010 and the Company has instructed the Lender to take subsequent payments from the restricted cash held on account at the Lender), (ii) extended the first principal payment until April 1, 2010, (iii) provided for the release of $2,000,000 of restricted cash for the purchase of corn, and (iv) requires the Company to fund a loan reserve fund under the Credit Agreement in the amount of $2,000,000 if the Company receives the B&I Loans for $5,000,000 of working capital.

On August 6¸2010, the Company executed a Sixth Supplement and Forbearance Agreement to the Master Credit Agreement (the “Sixth Supplement”), under which the Company agreed that Lender could apply the $3,945,087 it holds as collateral under the Credit Agreement to our current obligations under the Credit Agreement, including monthly payments, penalties and interest. The Company also agreed to provide the Lender with a comprehensive plan within 30 days of the date of the Sixth Supplement to resolve the Company’s working capital deficiencies by the end of the forbearance period. In exchange for the foregoing, Lender agreed to refrain from exercising its rights under the Credit Agreement until the earlier of October 1, 2010 or the date of any default under the Sixth Supplement.

The Company and the Lender remain in discussions to revise the Credit Agreement covenants and resolve outstanding defaults under the Credit Agreement. The B&I Loan is pending the Company meeting the net worth requirement set by USDA and resolution with the Lender regarding its conditions for extension of the loan. In light of continuing poor margins in the ethanol industry, the Lender has indicated the Company should focus on mitigation of risk and obtaining additional capital.

9

NEDAK ETHANOL, LLC

Notes to Condensed Unaudited Financial Statements

June 30, 2010

Note Payable to Members

In May 2004, each of the initial 15 members loaned the Company $1,000. The unsecured loans bore interest at 5% per annum with principal and interest due on April 8, 2009. On April 8, 2009, the notes were amended and restated to add accrued interest in the amount of $3,750 to the principal. The unsecured notes, which are classified as long-term debt as of June 30, 2010, continue to bear interest at 5% per annum with principal and interest due on April 8, 2012.

8. TAX INCREMENT FINANCING

In September 2007, the City of Atkinson, Nebraska, (“Issuer”) issued a tax increment financing Note (the “TIF Note”), the net proceeds of which in the amount of $4,939,925 were paid to the Company through a loan (the “TIF Loan”) to reimburse the Company for certain infrastructure improvements relating to the plant. Repayment of the Loan is secured by the Company’s pledge to the lender of the TIF Note (“TIF Lender”) and other obligations relating to the TIF Note. The original amount of the TIF Note was $6,864,000 and bears interest of 9.5%.

In connection with the issuance of the Note, the Issuer and the Company entered into a Redevelopment Contract (“Contract”). Under the Contract, the Note proceeds are to be used for Project costs, for the establishment of special funds held by the Note trustee for interest and principal payments and reserves (the “Capitalized Interest Fund” and the “Debt Service Reserve Fund”), and for debt issuance costs. The Company may not convey, assign, or transfer the project prior to the expiration of a 15 year period without the prior written consent of the Issuer. As of June 30, 2010 and December 31, 2009, the Capitalized Interest Fund was approximately $57,000 and $52,500 respectively, and is included in restricted cash on the balance sheet.

The Note is due in semi-annual increments which commence at $139,000 and increase to $444,000, with a final maturity in December 2021. Interest on the Note is payable semi-annually on September 1 and December 1. The interest rate resets on September 1, 2012 and September 1, 2017 to a rate equal to the 5-year U.S. Treasury Constant Maturity index plus 4.75% for the applicable five-year period and the remainder of the term of the TIF Loan, respectively. The Company has the option to redeem or purchase the Note in whole or in part. As of June 30, 2010 and December 31, 2009, the Company had $6,579,000 outstanding on the TIF Loan.

On July 6, 2009, the Lender notified the Company that the Debt Service Reserve Fund was deficient, constituting a default under the TIF Loan. The primary reason for this default was the extended delays and losses associated with startup of the Company’s ethanol plant. In order to enable resolution of the Company’s default, the Company and the TIF Lender entered into a Forbearance Agreement dated December 31, 2009 (the “Agreement”).

Under the Agreement, the Company agreed to authorize a transfer from the Debt Service Reserve Fund to satisfy the Company’s principal payment due to TIF Lender on December 31, 2009. With the authorization of payment to TIF Lender from the Debt Service Reserve Fund, the Company became current on all required payments to TIF Lender, but has violated covenants in the TIF Loan requiring immediate replenishment of the Debt Service Reserve Fund. Moreover, the Company agreed to and is attempting to seek the consent of Lender to (i) grant a security interest and Deed of Trust in favor of the TIF Lender upon the Company receiving, or being denied, the B&I Loan, (ii) grant a security interest in all reserve funds established under the TIF Loan and (iii) amend to the TIF Loan documents to (a) reduce the TIF Loan’s interest rate from 9.5% to 6.0% for three years, and upon expiration of the three years, the interest rate will revert to 9.5%, (b) reduce the Debt Service Reserve Fund to an amount equal to 12 months of principal payments, (c) make the Debt Service Reserve Fund funding contingent on the Company’s previous year’s profitability and (d) require the financial covenants and ratios in the TIF Loan documents to be consistent with the financial covenants and ratios to be agreed upon with Lender.

Under the Agreement, the TIF Lender agreed to refrain from exercising any of its rights or remedies under the TIF Loan, including acting on Company’s failure to maintain a sufficient amount in its Debt Service Reserve Fund or meet TIF Loan covenants, for a period beginning on December 31, 2009 and ending on the earlier of (a) March 31, 2010 or (b) 30 days following the approval of the proposed B&I Loans. This Forbearance Agreement expired, and the TIF Lender extended the standstill date to May 15, 2010. The Company and the TIF Lender failed to extend the

10

NEDAK ETHANOL, LLC

Notes to Condensed Unaudited Financial Statements

June 30, 2010

Agreement or reach other arrangements containing similar forbearance obligations by May 15, 2010, and the Company received a Notice of Default dated June 30, 2010 from the TIF Lender indicating that the Company was in default under the TIF Note due to nonpayment of $464,768 owing on June 1, 2010, and that the Debt Service Reserve Fund remained deficient by an amount of $588,553. Because of these defaults, the TIF Lender may (i) charge the Company an interest rate of 4% over the interest rate the Lender would otherwise be able to charge the Company, (ii) charge the Company a late charge of 5% for payments which are more than 10 days overdue, (iii) accelerate the entire amount of principal outstanding under the TIF Loan (which was $6,579,000 as of June 30, 2010) and (iv) exercise any other rights available to it under Agreement or at law. Due to these defaults, the TIF Loan is classified as a current liability.

9. FAIR VALUE MEASUREMENTS

Accounting standards establish a framework for measuring fair value. That framework provides a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (level 1 measurements) and the lowest priority to unobservable inputs (level 3 measurements). The three levels of the fair value hierarchy are described below:

Level 1: Inputs to the valuation methodology are unadjusted quoted prices for identical assets or liabilities in active markets that the Company has the ability to access.

Level 2: Significant other observable inputs other than Level 1 prices such as quoted prices for similar assets or liabilities; quoted prices in markets that are not active; or other inputs that are observable or can be corroborated by observable market data.

Level 3: Inputs to the valuation methodology are unobservable and significant to the fair value measurement.

The asset’s or liability’s fair value measurement level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement. Valuation techniques used need to maximize the use of observable inputs and minimize the use of unobservable inputs.

The following table summarizes by level, within the fair value hierarchy, the Company’s assets (liabilities) that were measured at fair value on a recurring basis as of December 31, 2009:

|

Commodity contracts

|

Level 1

|

Level 2

|

Level 3

|

Total

|

||||

|

December 31, 2009

|

$

|

5,325

|

-

|

$

|

-

|

$

|

5,325

|

There were no assets or liabilities measured at fair value on a recurring basis as of June 30, 2010.

Certain assets and liabilities are measured at fair value on a nonrecurring basis; that is, the items are not measured at fair value on an ongoing basis but are subject to fair value adjustments in certain circumstances (for example, when there is evidence of impairment).

The following table summarizes by level, within the fair value hierarchy, the Company’s assets that were measured at fair value on a nonrecurring basis during the six months ended June 30, 2010:

|

Inventory

|

Level 1

|

Level 2

|

Level 3

|

Total

|

||||

|

June 30, 2010

|

$

|

-

|

$

|

-

|

$

|

1,962,395

|

$

|

1,962,395

|

11

NEDAK ETHANOL, LLC

Notes to Condensed Unaudited Financial Statements

June 30, 2010

Inventory was reduced by $134,444 as of June 30, 2010 to reflect its fair value, based upon the estimated selling price of ethanol and distillers grains, less estimated transportation costs, and production costs for work in process and raw materials.

The carrying values of cash and cash equivalents, restricted cash, restricted short-term investments, accounts receivable, the commodity broker receivable, derivative financial instruments and accounts payable are recorded at or approximate fair value. Management determined it is not practicable to estimate the fair value of the notes payable and long-term debt since these agreements contain unique terms, conditions, and restrictions, which were negotiated at arm’s length, and there was no readily determinable similar instrument on which to base an estimate of fair value.

10. COMMITMENTS AND CONTINGENCIES

Construction Contract

The Company entered into an Engineering, Procurement and Construction Services Fixed Price Contract dated August 9, 2006 with Delta-T Corporation (“Delta-T”), which has been amended with several supplements, amendments and change orders (collectively, the “Delta-T Contract”). The Delta-T Contract provided, among other things: (i) guarantee of Delta-T’s performance by Delta-T’s parent, Bateman Litwin NV (“Bateman”), (ii) the provision by Delta-T of letters of credit in the amounts of $4,000,000 and $5,500,000 for the benefit of Lender and the Company, respectively, and (iii) a promissory note in the amount of $5,000,000 made by the Company in favor of Delta-T. Disputes between the parties respecting the letters of credit and other matters resulted in the filing by Delta-T of an action in the District Court of Douglas County, Nebraska, in which the court temporarily restrained the Company and Lender from making a draw on one of the letters of credit. The parties amended the Delta-T Contract on September 1, 2009 (the “Amendment”). The Amendment settled certain asserted claims by both parties and provided the following, among other things: (i) Delta-T would repair certain plant emissions equipment, (ii) Delta-T would extend the $5,500,000 letter of credit to September 30, 2010 with conditions added to draw on such letter of credit, (iii) Delta-T was relieved of previously agreed upon punch list responsibility with certain exceptions, (iv) Delta-T relinquished all rights to the $3,995,000 of proceeds held by Lender from the September 2009 draw against the $4,000,000 letter of credit, (v) the $5,000,000 promissory note in Delta-T’s favor was extinguished, (vi) Delta-T agreed to dismiss its legal action and dissolve the temporary restraining order, and (vii) except as provided above, no further payments or transfer of funds shall be made to or from Delta-T and the Company. The extinguishment of the $5,000,000 promissory note and other contract liabilities were recorded as reductions to property and equipment. The receipt of the $3,995,000 cash, less $228,433 for costs expected to be incurred, was recognized as gain in other income during the fourth quarter of 2009.

On March 19, 2010, the Company, Delta-T, Bateman and Bateman Engineering Inc. (“Bateman Engineering”) entered into a Settlement Agreement and Mutual Release (the “Settlement Agreement”), under which, among other things, (i) Delta-T and Bateman authorized the Company to draw $3,000,000 from a letter of credit, and (ii) the Company released Delta-T and Bateman from all warranties and other claims under the Delta-T Contract. The Settlement Agreement settled all outstanding disputes among the Company, Bateman and Delta-T relating to the Delta-T Contract and construction of the Company’s ethanol plant. The receipt of the $3,000,000 was recognized as a gain in other income during the three months ended March 31, 2010, and is included in restricted cash as of June 30, 2010.

Plant Management Agreement

In July 2007, the Company entered into an agreement with an unrelated party for the operation and management of the Company’s plant. The Company pays a fixed monthly payment of approximately $120,434 for such services, which will be adjusted annually. The Company is currently paying for process chemicals at a fixed rate per denatured gallon of ethanol produced. The Company also has future obligations for an incentive program that is in effect for the first five years of operation following the Delta-T settlement discussed above. The agreement will terminate on December 31, 2014 unless terminated by either party giving 180 days prior written notice. The

12

NEDAK ETHANOL, LLC

Notes to Condensed Unaudited Financial Statements

June 30, 2010

Company incurred approximately $372,000 and $742,000 for these services for the three and six month periods ended June 30, 2010 and $260,000 and $526,000 for these services for the three and six month periods ended June 30, 2009, respectively.

Utility Contracts

In March 2006, the Company entered into an agreement with a natural gas provider for the procurement, and management of natural gas transportation and supply. The Company pays for the natural gas based on actual consumption along with a monthly management fee of $0.07 per MMBtu delivered. The agreement was automatically renewed for an additional two-year term in February 2008. As of March 31, 2010 this contract was allowed to expire and the Company has entered into a consulting agreement with a management services company who is negotiating for gas supply on the Company’s behalf and making recommendations as to methods and sources of gas procurement on a week by week basis. The new management monthly fee is $3,683 which replaces the $0.07 per MMBtu variable cost.

In May 2006, the Company entered into an agreement, secured by the Company’s line of credit discussed in Note 6, with a natural gas transporter for the transportation of natural gas. The Company pays the maximum transportation rate unless otherwise agreed for the maximum daily transportation quantity of 2450 MMBtu per day. The agreement is for a ten year period beginning September 2007 and may be extended for another primary term if agreed to by both parties.

In September 2007, the Company entered into an agreement, secured by the Company’s line of credit discussed in Note 6, with a natural gas transporter to expand the pipeline capacity. The Company pays the maximum transportation rate unless otherwise agreed for the maximum daily transportation quantity of 1,000 MMBtu per day. The agreement is for a ten year period beginning September 2007 and may be extended for another primary term if agreed to by both parties.

In April 2010, the Company entered into an agreement to expand the transport reservation by an additional 500 MMBtu per day, bringing the guaranteed transport volume to 3,950 MMBtu per day. This additional reservation is for a period of one year and ends in March 2011.

Transportation Agreement

In July 2007, the Company entered into an agreement with a fuel carrier for the transportation of ethanol from the plant to the load out facility. The Company pays a base fee per gallon unloaded plus a surcharge if above the diesel fuel base. The agreement has a three year term which commenced July 2007 and will automatically renew for additional one-year terms unless terminated by either party by written notice no less than 180 days prior to the ending date of the initial three-year term or of any renewal term.

Marketing Agreements

Ethanol

In November 2006, the Company entered into a marketing agreement with an unrelated party for the sale of its ethanol. The Company pays the marketer a fixed rate fee of $0.01 per net gallon of denatured ethanol for the services provided. The agreement will continue until December 2010. The agreement will automatically renew for an additional one year unless the Company gives four months’ written notice.

The marketer leases rail cars to the Company with varying terms under this agreement, which leases may survive the actual marketing agreement by many years. The Company has lease agreements for 141 rail cars under this agreement. There are 45 cars under leases that expire before the end of 2011 and carry an average monthly rental cost of $352. The remaining 96 cars have expiration dates between March 31, 2017 and August 31, 2020 with average monthly rental costs of $707.

13

NEDAK ETHANOL, LLC

Notes to Condensed Unaudited Financial Statements

June 30, 2010

Revenues from sales to this marketer were approximately $17,472,000 and $34,603,000 for the three and six month periods ended June 30, 2010 and $9,114,000 and $18,737,000 for the three and six month periods ended June 30, 2009, respectively. Accounts receivable from this marketer were $995,986 and $674,671 as of June 30, 2010 and December 31, 2009, respectively.

As of June 30, 2010, the Company has forward contracted sales of ethanol for 4,540,000 gallons of ethanol under variable price arrangements.

Distillers Grains

In January 2007, the Company entered into a marketing agreement with an unrelated party to purchase all of the Company’s modified wet distillers grains (“MWDG”). The marketer is to operate in good faith to obtain a market competitive price. The marketer pays the Company the selling price, less a marketing fee equal to $1.50 per ton of MWDG sold at $50 a ton or less or 3.0% of the price of MWDG sold over $50 a ton. The agreement will continue until March of 2011 and renew for an additional two years thereafter unless either party has given four months written notice. Revenue from this marketer was approximately $2,432,919 and $4,869,669 for the three and six month periods ended June 30, 2010 and $1,575,000 and $3,716,000 for these services for the three and six month periods ended June 30, 2009, respectively. Accounts receivable from this marketer were $228,681 and $332,092 as of June 30, 2010 and December 31, 2009, respectively.

Grain Procurement

In December 2006, the Company entered into an agreement with an unrelated party to supply corn required for its production of ethanol. As of January 2009, the parties no longer operate under this agreement. However, the agent continues to provide services to the Company on an at-will basis for nearly all contracts with local producers for the delivery of corn to the Company. The agent is paid a service fee of $0.04 per bushel of grain delivered, and the Company also executes some contracts directly with producers (which include directors) for some of its corn. In the ordinary course of business, the Company will enter into forward purchase contracts for its corn purchases. Management considers these forward contracts to be normal purchases since the corn will be delivered in quantities expected to be used by the Company over a reasonable period in the normal course of business. Purchases directly from the agent totaled approximately $4,381,000 and $1,377,000 for the quarters ended June 30, 2010 and 2009, respectively.

As of June 30, 2010, the Company had commitments on forward purchase contracts to purchase 1,141,277 bushels of corn at an average price of $3.43 per bushel totaling $3,915,000 for delivery between July 1, 2010 and July 2011. Also, the Company had commitments on un-priced forward purchase contracts for 1,272,403 bushels, for delivery between July 2010 and September 2010. The final price for these contracts will be determined based on cash price at the time of delivery.

Environmental Liabilities

The Company’s operations are subject to environmental laws and regulations adopted by various governmental entities in the jurisdiction in which it operates. These laws require the Company to investigate and remediate the effects of the release or disposal of materials at its location. Accordingly, the Company has adopted policies, practices, and procedures in the areas of pollution control, occupational health, and the production, handling, storage, and use of hazardous materials to prevent material environmental or other damage, and to limit the financial liability which could result from such events. Environmental liabilities are recorded when the liability is probable and the costs can be reasonably estimated.

The Company has received Notices of Violation (“NOV”) from the Nebraska Department of Environmental Quality (“NDEQ”) arising from failures of emission equipment designed and installed by Delta-T. That equipment includes

14

NEDAK ETHANOL, LLC

Notes to Condensed Unaudited Financial Statements

June 30, 2010

the plant’s regenerative thermal oxidizer (“RTO”) used to control emissions from the dryer and the CO2 Scrubber used to control emissions from the ethanol process.

The RTO had not performed according to the design specified in the Delta-T Contract, and the Company continues to assess methods to resolve the problem. The CO2 Scrubber failed in original compliance testing, and equipment modifications and process adjustments were made, including chemical injection, to remediate the issue. During the startup operations of the plant beginning in January 2009 and continuing through the date of the original compliance testing, Delta-T had operated the plant without these modifications and as a result, the Company received an NOV in January 2010 which asserted that due to the failure of the CO2 Scrubber, the Company’s operation of the plant violated the operating permit issued by the NDEQ.

While the Company believes it has resolved all of the operational shortfalls cited in the NOVs, it is possible the NDEQ or the Nebraska Office of the Attorney General could assess fines against the Company as a result of having operated the plant with the equipment before it was operating in compliance. As a result of subsequent negotiations and problem solving in cooperation with the NDEQ, the Company believes that the possibility of any material penalties being assessed is remote.

15

Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations.

Forward Looking Statements

This quarterly report on Form 10-Q of NEDAK Ethanol, LLC (the “Company,” “we” or “us”) contains forward-looking statements that involve future events, our future performance and our expected future operations and actions. In some cases you can identify forward-looking statements by the use of words such as “may,” “should,” “anticipate,” “believe,” “expect,” “plan,” “future,” “intend,” “could,” “estimate,” “predict,” “hope,” “potential,” “continue,” or the negative of these terms or other similar expressions. These forward-looking statements are only our predictions and involve numerous assumptions, risks and uncertainties. Our actual results or actions may differ materially from these forward-looking statements for many reasons, including the following factors:

|

|

·

|

Overcapacity in the ethanol industry;

|

|

|

·

|

Fluctuations in the price and market for ethanol and distillers grains;

|

|

|

·

|

Availability and costs of products and raw materials, particularly corn and natural gas;

|

|

|

·

|

Our ability to obtain the debt and equity financing necessary to operate our plant and our ability to meet the associated covenants;

|

|

|

·

|

Changes in our business strategy, capital improvements or development plans;

|

|

|

·

|

Mechanical difficulties in operation of the plant;

|

|

|

·

|

Changes in the environmental regulations that apply to our plant site and operations and our ability to comply with environmental regulations;

|

|

|

·

|

Our ability to hire and retain key employees for the operation of the plant;

|

|

|

·

|

Changes in general economic conditions or the occurrence of certain events causing an economic impact in the agricultural, oil or automobile industries;

|

|

|

·

|

Changes in the weather and economic conditions impacting the availability and price of corn and natural gas;

|

|

|

·

|

Changes in federal and/or state laws (including the elimination of any federal and/or state ethanol tax incentives);

|

|

|

·

|

Changes and advances in ethanol production technology; and competition from alternative fuel additives;

|

|

|

·

|

Lack of transport, storage and blending infrastructure preventing ethanol from reaching high demand markets;

|

|

|

·

|

Our ability to generate free cash flow to invest in our business and service our debt;

|

|

|

·

|

Volatile commodity and financial markets;

|

|

|

·

|

Changes in interest rates and lending conditions; and

|

|

|

·

|

Results of our hedging strategies.

|

Our actual results or actions could and likely will differ materially from those anticipated in the forward-looking statements for many reasons, including the reasons described in this report. We are not under any duty to update the forward-looking statements contained in this report. We cannot guarantee future results, levels of activity, performance or achievements. We caution you not to put undue reliance on any forward-looking statements, which speak only as of the date of this report. You should read this report and the documents that we reference in this report and have filed as exhibits completely and with the understanding that our actual future results may be materially different from what we currently expect. We qualify all of our forward-looking statements by these cautionary statements.

Overview, Status and Recent Developments

We completed full startup of our ethanol plant in June 2009, and have the capacity to annually process approximately 17 million bushels of corn, through a dry milling process, into approximately 44 million gallons of ethanol per year. We also produce approximately 340,000 tons of wet distillers grains annually. We are currently operating at approximately 108% capacity.

Our profitability is driven by the relationship between the cost of our primary input, corn, and the price at which we can sell our primary product, ethanol (“Crush Margin”). We use a conversion rate of 2.8 gallons produced per bushel of corn to report Crush Margins in this quarterly report. Our plant needs approximately 47,000 bushels of

16

corn per day as the feedstock for its dry milling process. The grain supply for our plant is obtained primarily from local markets. The price and availability of corn are subject to significant fluctuations depending upon a number of factors that affect commodity prices in general, including crop conditions, weather, governmental programs and foreign purchases. Often the market price of ethanol has tended to track the market price of corn. However, at the same time, the market price for energy (gasoline in particular) has provided a ceiling for the market price of ethanol without regard to the price of corn. We therefore anticipate that our plant’s profitability will be negatively impacted during periods of high corn prices, especially when the market prices for energy are low. As of July 31, 2010, our flat price cash bid for August 2010 corn was $3.49 a bushel.

Our original business plan and resulting equity and financing arrangements provided for a minimum of $10,000,000 of working capital for our commodities risk management practice. In the first half of 2010, we have been unable to take advantage of certain opportunities because of the lack of adequate working capital when the commodities market offered a Crush Margin that could have improved our financial results. We did experience profitable operations during those short periods when spot market pricing and costs for ethanol and corn yielded sales revenue and raw material costs with a profitable Crush Margin. As we have previously reported, adequate working capital and liquidity have not been available and as a result, we have been forced to remain in those spot markets and have generated losses from operations for the first half of 2010. These losses accumulated at a time when other ethanol producers were able to operate with profits from risk management activities which more than offset negative margins inherent in the spot markets for ethanol and corn.

Notwithstanding limitations on our risk management due to the lack of working capital, we have continued to address plant and equipment capability variables and improvements in operating and administrative cost structures which we expect to enhance our future financial performance.

Throughout 2009, our production capabilities were tested and we ended the year with only 82% of nameplate production, reflecting portions of 2009 during which certain equipment necessary for full production was not operable. By the end of the first quarter of 2010, we had addressed the equipment limitations and reached approximately 100% nameplate production for the quarter. During the second quarter of 2010, we achieved 108% nameplate production.

We have recently compared our cost structure to a peer group comprised of single site ethanol producers with similar capacities. After comparing that information throughout recent months of steady production at full capacity, we believe that our cost structure—excluding interest and depreciation—is generally competitive. As a new plant, we have an interest burden and depreciation burden that are not shared with older peers, but other costs are comparable throughout our operating statements.

Because we believe our cost structure is generally competitive, we have determined that achieving the capability to better manage commodity price risks is the most important factor of our business for the foreseeable future. Our efforts to date have focused on mitigation of commodity risk through traditional hedging matching corn purchases and ethanol sales contracts. However, our ability to effectively utilize these methods has been restricted by limited working capital, which we have attempted to remedy by acquiring additional liquidity and working capital through new equity or financing. At the end of the second quarter of 2010, we began discussions with several firms offering tolling agreements and other alternate marketing arrangements. In contrast to our current practice of contracting for the purchase of corn and sale of ethanol through separate companies, under a tolling agreement the tolling partner both provides the corn (and may provide the natural gas) and markets the ethanol and distillers grains produced. Payments to the ethanol plant under a tolling agreement vary. In some cases, the ethanol plant is paid a flat processing fee per gallon of ethanol produced. In other cases, the ethanol plant receives a payment based on the crush margin between the cost of inputs and value of outputs. We are also exploring marketing arrangements in which separate contracts for purchase of corn and sale of ethanol and distillers grains with a single company, along with an agreement to net the amounts due under all of the contracts. In both cases the ethanol plant benefits from reduced working capital needs because the value of inventory and accounts receivable are held by the tolling partner. In addition, the agreements can provide the ethanol producer access to additional risk management tools to be implemented by the marketing partner. We cannot provide any assurance whether we will undertake a tolling arrangement which is acceptable to us.

17

We believe that both product delivery infrastructure and demand for ethanol must improve in order to increase Crush Margins in the long term. Ethanol annual productive capacity has continually grown since 1980. According to the Renewable Fuels Association, in 2002 ethanol production in the U.S. surpassed two billion gallons, by 2007 production further increased to 6.5 billion gallons, and in 2009 it topped ten billion gallons. The Renewable Fuels Association indicates that total ethanol production capacity is now approximately 12 billion gallons. Currently, the renewable fuel standard (“RFS”) supports demand at volumes effectively equal to national production capacity. Furthermore, current ethanol prices should encourage blending demand since ethanol costs less than reformulated blend stock for oxygenate blending (“RBOB”). However, the physical distribution infrastructure does not allow for efficient movement of ethanol to all areas of the country. Also, a United States Environmental Protection Agency (“EPA”)-imposed limit of 10% blend for use in vehicles that are not designed as flex-fuel vehicles continues to depress the market price and demand for ethanol. We believe that these two obstacles will improve in the medium term.

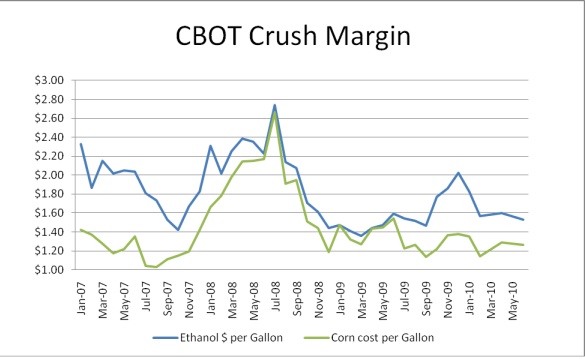

The first half of 2010 (like the first half of 2009) did not follow the historical trends in the ethanol industry of summer increases of Crush Margins. Crush Margins were characteristically poor in the first quarter of the year, although unusually strong demand in the beginning of the first quarter 2010 supported a strong margin during part of our 2010 first quarter. However, winter weather later in the first quarter caused reduced driving demand for gasoline, the Chicago Board of Trade (“CBOT”) Crush Margin declined from $0.47 at December 31, 2009 to $0.29 as of April 30, 2010. At the end of the first quarter, the Crush Margin was $0.31. During the second quarter, there were two short periods during which Crush Margins increased temporarily, but each time the corn/ethanol gap closed again to historically low levels. We believe that the lower Crush Margins have caused primarily by continued uncertainty in the US economic recovery and slow increases of demand for automobile fuels. In the last days of the second quarter 2010, the EPA again delayed its ruling on whether to allow an increase from 10% to 12%-15% blend of ethanol in regular unleaded gasoline to be used in all vehicles. On June 30, 2010, the Crush Margin was $0.264.

In the following graph, the variance in the relationship between the CBOT cost of corn and the price of ethanol for the previous three plus years is demonstrated. It is clear that the industry margins began to deteriorate in the third quarter of 2007, which were exacerbated with the global economic distress of 2008. Some stability returned to the corn market in the third quarter of 2009, but continued distress in the general economy kept the Crush Margin tight until the end of 2009. In the fourth quarter of 2009, the Crush Margin improved for a short time as the fuel blenders ran low of ethanol inventories and some recovery in the larger economy pushed demand up, and around Thanksgiving it peaked around $0.65 and it continued strong clear into February 2010. This high Crush Margin in the first quarter of 2010 is remarkable because the Crush Margin is historically the lowest at this time of year in the ethanol industry.

The unusual 2010 market activity continued in the late spring of 2010, when the Crush Margin failed to increase with the traditional Memorial Day driving demand increase. We believe that the continuing weakness in the U.S. economy is currently keeping the Crush Margin excessively tight.

18

|

Our secondary source of revenue is the sale of distillers grains. Because distillers grains compete with other protein-based animal feed products, the price of distillers grains may decline when the prices of competing feed products are low. Downward pressure on commodity prices, such as soybeans and corn, will generally cause the price of competing animal feed products to decline, resulting in downward pressure on the price of distillers grains, which will result in lower revenues for ethanol producers. In addition, local supply and demand can also impact prices of distillers grains in our market area. In 2009, a single large ethanol plant in northeast Nebraska started production. The new plant reportedly has the ability to dry its distillers grains, but the majority of the distillers grains produced by it during start up were sold as wet distillers grains. As a result, the price of wet distillers grains in eastern Nebraska has been depressed, which significantly impacted the price of wet distillers grains received by us. We currently anticipate an increase in revenues from the sale of distillers grains in 2010 over the level achieved in 2009, however no assurances can be made.

Other key factors affecting our profitability are federal and state laws requiring environmental and plant safety controls. Finally, with the development of full operations, we have undertaken, where possible, a risk management strategy hedging our corn and natural gas with the use of commodity derivative contracts to balance our risk of loss caused by market volatility. Our lack of working capital hindered our ability to hedge and therefore maximize Crush Margins in the second quarter of 2010, as we otherwise may have been able to lock in a higher Crush Margin for the second quarter of 2010 through such hedging in the first quarter of 2010. Accordingly, we believe our results of operations for the second quarter of 2010 were not as favorable due to these challenges.

Results of Operations

Throughout the first half of 2010, we have experienced significant improvements in production rates and consistency of throughput. In the month of June 2010, our plant achieved 111% of nameplate capacity with a method and standard operating procedure that provides us with some confidence that we will be able to continue to do so in the future.

Comparison year-to-year Second Quarter and First Half Production

|

Production

|

Second Quarter

|

2010 Increase / (Decrease)

|

First Half of Year

|

2010 Increase / (Decrease)

|

||

|

2010

|

2009

|

2010

|

2009

|

|||

|

Ethanol (000’s gallons)

|

11,903

|

6,426

|

5,477

|

23,037

|

14,018

|

9,019

|

|

Distillers Grain (000’s tons)

|

81

|

35

|

46

|

161

|

109

|

52

|

|

Corn (000’s bushels ground)

|

4,268

|

2,279

|

1,989

|

8,274

|

5,030

|

3,244

|

|

Yield (Denatured gal/BU)

|

2.79

|

2.82

|

(0.03)

|

2.78

|

2.79

|

(0.01)

|

19

Summary of Monthly 2010 year-to-date operations:

|

Ethanol Gallons Produced (000’s)