Attached files

| file | filename |

|---|---|

| 8-K - LCI INDUSTRIES | v193176_8k.htm |

A Leading National Supplier of a Wide Variety of

Components for RVs and Manufactured Homes

EXHIBIT 99.1

Drew Industries Incorporated

(NYSE: DW)

This presentation contains certain “forward-looking statements” within the meaning of the Private Securities Litigation

Reform Act of 1995 with respect to financial condition, results of operations,

business strategies, operating efficiencies or

synergies, competitive position, growth opportunities for existing products, plans and objectives of management, markets

for the Company’s Common Stock and other matters. Statements in this presentation

that are not historical facts are

“forward-looking statements” for the purpose of the safe harbor provided by Section 21E of the Securities Exchange Act of

1934 and Section 27A of the Securities Act of 1933.

Forward-looking statements, including, without limitation, those relating to our future business prospects, revenues,

expenses, income (loss), cash flow, and financial condition, whenever they occur in this

presentation, are necessarily

estimates reflecting the best judgment of our senior management at the time such statements were made, and involve a

number of risks and uncertainties that could cause actual results to differ materially from those suggested

by forward-

looking statements. The Company does not undertake to update forward-looking statements to reflect circumstances or

events that occur after the date the forward-looking statements are made. You should consider forward-looking

statements,

therefore, in light of various important factors, including those set forth in this presentation and in our Form 10-K

for the year ended December 31, 2009 and in our subsequent filings with the SEC.

There are a number of factors, many of which are beyond the Company’s control, which could cause actual results and

events to differ materially from those described in the forward-looking statements.

These factors include, in addition to the

matters described in this presentation, pricing pressures due to domestic and foreign competition, costs and availability of

raw materials (particularly steel and steel-based components, vinyl, aluminum, glass

and ABS resin), availability of credit

for financing the retail and wholesale purchase of manufactured homes and recreational vehicles (“RVs”), availability

and costs of labor, inventory levels of retail dealers and manufacturers, levels

of repossessed manufactured homes and

RVs, the disposition into the market by the Federal Emergency Management Agency (“FEMA”), by sale or otherwise, of

RVs or manufactured homes purchased by FEMA, changes in zoning regulations for manufactured

homes, sales declines

in the RV or manufactured housing industries, the financial condition of our customers, the financial condition of retail

dealers of RVs and manufactured homes, retention of significant customers, interest rates, oil and gasoline

prices, and the

outcome of litigation. In addition, national and regional economic conditions and consumer confidence affect the retail

sale of RVs and manufactured homes.

Forward-Looking Statements

- 1 -

Drew’s Products – Components

for RVs and Manufactured Homes

$546 Million of Sales for the12 Months Ended June 30, 2010

RV Chassis, Slide-outs and Other

Chassis Parts:

$243 million

RV Windows and Doors:

$110 million

Other Products:

$5 million

MH & RV Bath Products:

$18 million

Specialty Trailers:

$5 million

RV and MH Axles:

$37 million

MH Chassis and Chassis Parts:

$25 million

MH Windows and Screens:

$57 million

- 2 -

RV Furniture Products:

$46 million

Drew’s Segments – LTM 6/2010

MH = $96 million

18%

RV = $450 million

82%

90+% for towable RVs

- 3 -

Revenues - $546 million

Segment Operating Profit - $52 million

RV = $43 million

83%

MH = $9 million

17%

Supplier to Industry Leaders

Outstanding customer service and national coverage, with 24

production facilities (approximately 2.3 million sq. ft.), make us a key

partner with our customers, including:

- 4 -

Cavco (NASDAQ: CVCO)

Champion (privately owned)

Clayton (owned by Berkshire Hathaway)

Palm Harbor (Nasdaq: PHHM)

Skyline (NYSE: SKY)

Forest River (owned by Berkshire Hathaway)

Heartland Recreational Vehicles, LLC (privately owned)

Jayco/Starcraft (privately owned)

Skyline (NYSE: SKY)

Thor (NYSE: THO)

RV

MH

(1)

EBITDA is operating profit plus depreciation, amortization and goodwill impairment (see page 35).

(2)

During 2005 & 2006, the Company experienced a significant increase in business from both its RV and

manufactured housing customers arising from the need for emergency housing caused by the Gulf Coast

hurricanes. Sales of hurricane-related products aggregated approximately $40 million, or 6 percent, of

consolidated net sales in 2005, and approximately $20 million, or 3 percent, of consolidated sales in 2006.

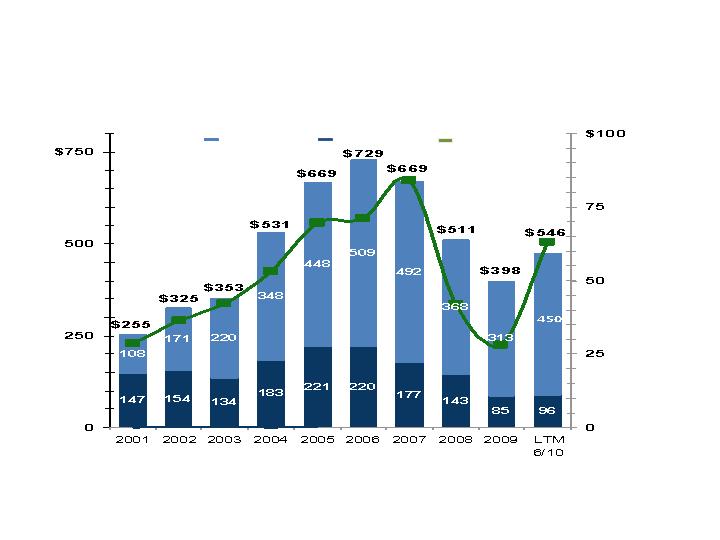

MH Segment sales(2)

RV Segment sales(2)

EBITDA(1)

- 5 -

Financial Performance

Sales and EBITDA(1) (in millions)

Sales

EBITDA

(1)

EBITDA is operating profit plus depreciation, amortization and goodwill impairment (see page 36).

(2)

The Company’s operations are somewhat seasonal, as sales in the second and third quarters are traditionally

stronger than the first and fourth quarters, consistent with the industries which the Company

supplies.

However, because increases in RV dealer inventories earlier this year, and the uncertain economic

environment, seasonal industry trends may be different than in prior years.

MH Segment sales

RV Segment sales

EBITDA(1)

- 6 -

Financial Performance – Quarterly(2)

Sales and EBITDA(1) (in millions)

Sales

EBITDA

$159

$151

$124

$77

$71

$101

$122

$105

$146

$174

Consolidated more than 35 production facilities into other

existing facilities since 2006, improving operating efficiencies

Cautiously added back $1 million of annualized fixed costs as

demand improved.

These facility consolidations, along with reductions in salaried

staff, changes in insurance, IT improvements, along with other

cost saving measures have saved us:

What Drew Has Done -

Cost Reductions

- 7 -

What Drew Has Done -

Strengthened Balance Sheet

- 8 -

(1)

The Company completed two acquisitions in the first quarter of 2010 which utilized $21

million in cash (see page 15).

What Drew Has Done -

Acquisitions and Growth

- 9 -

Business Strategy

Maximize profitability and return on assets through

Market share growth

New product introductions

Strategic acquisitions

Operational efficiencies

This strategy accomplished through

Outstanding customer service

Motivating management through strong profit incentives

Low cost manufacturing:

Optimizing production efficiencies and implementing stringent

cost controls

Facility consolidations and fixed cost reductions

Working capital management

R & D efforts

Disciplined and patient acquisition philosophy

- 10 -

Content Per New Towable RV

RV Segment

operating

profit margin 8.7% 10.0% 11.6% 9.7% 9.6% 8.3% 12.2% 6.7% 5.0% 9.6%

- 11 -

See Page 21 for Industry Information

- 90+% of RV Segment sales are for Travel Trailers and

Fifth-Wheel RVs

- 100% market share in existing products would yield

$3,900 to $4,300 per Towable RV

At industry production levels for the last 12 months ended June 2010, each $100 increase in content

adds $19 million in sales for Drew.

100% market share in existing products would yield

$3,600 to $4,000 per home

Content Per New Manufactured Home

MH Segment

operating

profit margin 10.4% 10.7% 10.5% 10.4% 10.3% 8.7% 8.1% 7.2% 3.8% 9.5%

See Page 17 for Industry Information

- 12 -

Acquisition Criteria

- 13 -

Drew is a disciplined and patient acquirer

Gain market share or add products from other suppliers

through asset acquisitions

Complimentary to our core RV (including specialty

trailers) and MH markets

Seek products or technologies that we can expand

through our nationwide customer base and factory

network

Become a more extensive supplier to our customers

New Product Introductions

- 14 -

Began

production of

entry doors

for RVs

Introduce RV

slide-out

mechanisms

Began

Production of

axles for

towable RVs

1997

2008 2009 2010

2001

2006

2004

2007

ACQUIRE

LIPPERT

COMPONENTS:

Primarily steel chassis

& parts for MH

ACQUIRE

BETTER BATH:

Adding thermo-

formed products

ACQUIRE

HAPPIJAC:

Adding

patented bed

lifts for RVs

ACQUIRE

EXTREME

ENGINEERING:

Expanding specialty

trailer product line

ACQUIRE

SEATING

TECHNOLOGY:

Adding furniture

for RVs

ACQUIRE COACH

STEP:

Adding electric steps

for motorhomes

ACQUIRE

EQUA FLEX:

Introduced RV

suspension

products

Expand

into steel

chassis for

towable

RVs

ACQUIRE

QUICKBITE TM

:

Adding a new

innovative

coupler

Began

production of

entry doors for

MH

ACQUIRE ZIEMAN:

Adding specialty

trailers

ACQUIRE

LEVEL-UP TM:

Leveling

system for

fifth-wheel RVs

ACQUIRE

SCHWINTEK:

Adding wall-slide

mechanism and

leveling devices

for motorhomes

2010 Acquisitions

- 15 -

Schwintek – March 16, 2010:

Purchase price $20 million cash plus earn-out

New wall slide-out design:

Attached to the wall, exerting force near the top and the

bottom of the wall as opposed to bottom only

More space efficient; mechanism inside of wall rather than in

the chassis space

Significantly lighter

Minimizes need for user adjustments and reduces potential

warranty issues

Aluminum cylinder for use in leveling devices for

motorhomes

Power roof lift for tent campers

Level-Up TM System – February 18, 2010:

Purchase price $1 million cash plus earn-out

Innovative six-point leveling system for fifth-wheel RVs

Cost per sq. ft. is $41 for MH vs.

$93 for site-built homes

Average retail price of

$65,100 for a 1,595 sq. ft. MH

9 million manufactured

homes across the U.S.

Improved quality,

appearance and safety

Studies have shown that MHs built since 1995 sustain

no more damage in hurricanes than site-built homes

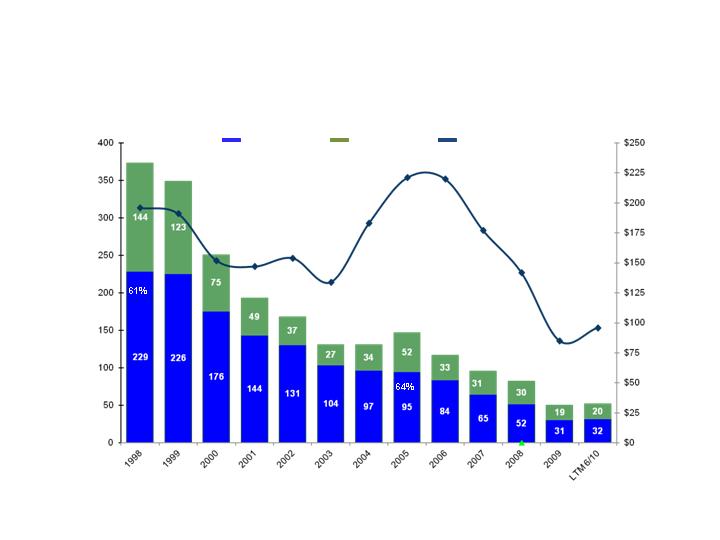

Industry production was down 87% from 1998 to 2009,

but increased 8% in the first six months of 2010 as

compared to the first six months of 2009.

Manufactured Housing (MH) Market

- 16 -

- 17 -

MH – Industry Production

Single-Section

Multi-Sections

Drew’s MH Sales

65%

70%

75 %

$177

78%

80%

74%

72%

63%

68%

$220

$221

$185

$134

$154

$147

$152

$191

$196

(Units in thousands, Dollars in millions)

373

349

96

82

117

147

131

131

168

193

Industry

Units

Drew

Sales

$142

50

$85

251

63%

52

62%

$96

MH: Favorable Factors

- 18 -

INDUSTRY:

Demand

Demand for quality, affordable housing is likely to increase

Baby boomers retiring in increasing numbers

Dealer and manufacturer inventory levels are reasonable

Financial

Subprime market woes could help MH

Pre-2003, MH was 20+% of Single Family housing starts

In peak "Sub-prime era”, MH was about 8% to 11% of Single Family

housing starts

2008 to 2009, MH was about 13% of Single Family housing starts

Availability of financing is still an issue

DREW:

Drew remains profitable in MH Segment: 9.5% operating profit

margin for the 12 months ended June 30, 2010

Sales up 35% in the second quarter of 2010, far exceeding

the 17% increase in industry-wide production levels

Increased focus on aftermarket driving sales growth

Added new product line - entry doors in late 2009

92% of industry 2009 unit sales

69% of 2009 wholesale dollar

sales, or $2.8 billion

Retail cost $4,000 to $100,000 per

unit. Average about $23,000

RV Market

8% of industry 2009 unit sales

31% of 2009 wholesale dollar

sales, or $1.3 billion

Retail cost $41,000 to $400,000+

per unit. Average about $121,000

Travel trailer

Fifth-wheel travel trailer

Travel trailer with

expandable ends

Folding camping trailer

Sport utility RV

“Toy Hauler”

Type C Motorhome

Truck camper

TOWABLE RVS (90+% of Drew’s RV Segment revenues)

MOTORHOMES (3% of Drew’s RV Segment revenues)

Type B Motorhome

Type A Motorhome

- 19 -

Shift in U.S. culture toward more RV-related

activities

College and NFL football games

NASCAR events

More active, shorter, environmentally

friendlier vacations

More economical

family vacations

Typical RV family vacation

is less expensive

Many RVs are “parked” over the long-term as

second homes

How RVs Are Used

- 20 -

90+% of Drew’s RV product sales are for Travel Trailers and 5 th Wheel RVs

(1) Projection for 2010 is the latest published by the RVIA (May 2010). During the first six months of 2010,

111,600 travel trailer and fifth-wheel RVs were produced.

(Units in thousands, Sales in millions)

- 21 -

Travel Trailers & 5th Wheel

Other Towables

Motorhomes

Drew’s RV Sales

166

257

293

321

300

311

321

370

384

391

353

237

RVs - Industry Wholesale Shipments

Industry

Units

Drew

Sales

230

- 22 -

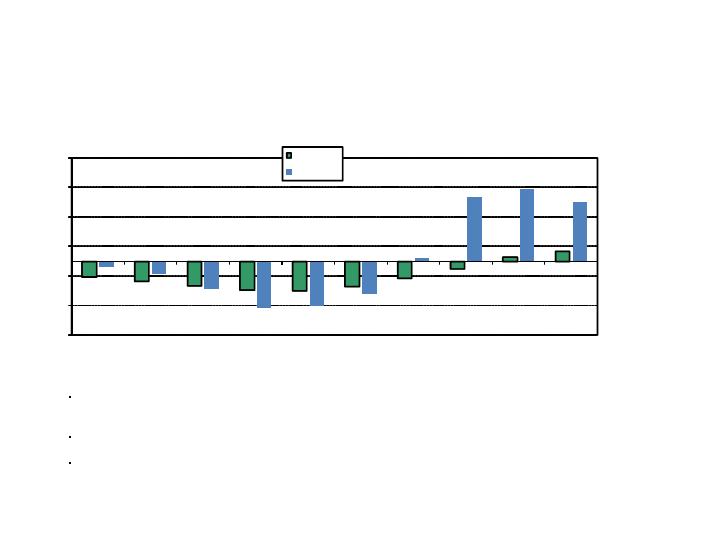

Recent RV Industry Trends

Due to strong sell-through, industry-wide retail sales exceeded wholesale production for April and May

2010.

Second quarter 2010 retail data includes information for April & May only, as June is not yet available.

All data includes Canada as well as US.

Travel Trailers and 5th Wheel RVs, Drew’s primary RV market

Year over

Year

Change

-

21%

-

27%

-

33%

-

39%

-

40%

-

34%

-

23%

-

10%

6%

14%

-

8%

-

18%

-

38%

-

63%

-

61%

-

44%

5%

88%

99%

80%

-

100%

-

60%

-

20%

20%

60%

100%

140%

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Retail

Wholesale

RV recovery from recession

Demographic tailwind

Exploring related industries

Affordable housing

The Future

-23-

Stock Price History

Drew has 22 million shares outstanding and a

market capitalization of approximately $485

million as of August 2, 2010

(December 31, unless noted)

- 24 -

Operating Results

Year Ended December 31, (except as noted)

FINANCIAL PERFORMANCE

(1)

Sales declines in 2008 and 2009 due to reductions in industry-wide shipments of RVs and Manufactured

Homes.

(2)

Excludes certain “extra expenses” recorded by the Company during 2009 and 2008, resulting primarily from

plant closings and start-ups, staff reductions and relocations, increased bad debts and

obsolete inventory

and tooling. These expenses were largely due to the unprecedented conditions in the RV and

manufactured housing industries. Also excludes charges for goodwill impairment recorded during the fourth

quarter of 2008 and the first

quarter of 2009, and charges for executive retirement in the fourth quarter of

2008 (see pages 37 and 38).

(3)

EBITDA is operating profit plus depreciation, amortization and goodwill impairment (see page 35).

- 25 -

Results By Segment

(1)

Sales declines due to reductions in industry-wide shipments of RVs and Manufactured Homes.

(2)

Excludes certain “extra expenses” recorded by the Company during 2009 and 2008, resulting

primarily from plant closings and start-ups, staff

reductions and relocations, increased bad debts

and obsolete inventory and tooling. These expenses were largely due to the unprecedented

conditions in the RV and manufactured housing industries (see pages 39 and 40).

- 26 -

FINANCIAL PERFORMANCE

Year Ended December 31, (except as noted)

Operating Results

Three Months Ended June 30,

- 27 -

FINANCIAL PERFORMANCE

(1)

Excludes certain “extra expenses” recorded by the Company during the three months

ended June 30, 2009, resulting primarily from plant closings and staff reductions. These

expenses

were largely due to the unprecedented conditions in the RV and manufactured

housing industries. Also excludes charges for goodwill impairment during the first quarter of

2009 (see page 38).

Operating Results

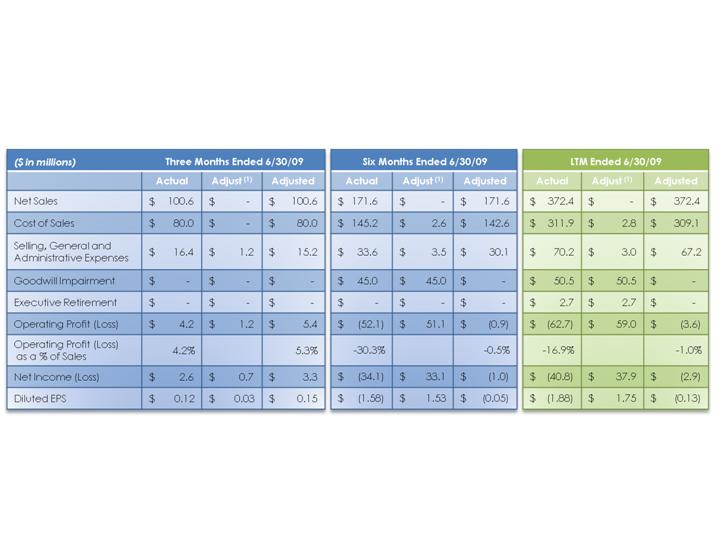

Six Months Ended June 30,

- 28 -

FINANCIAL PERFORMANCE

(1)

Excludes certain “extra expenses” recorded by the Company during the six months ended

June 30, 2009, resulting primarily from plant closings, staff reductions, increased bad debts,

and obsolete

inventory and tooling. These expenses were largely due to the

unprecedented conditions in the RV and manufactured housing industries. Also excludes

charges for goodwill impairment during the first quarter of 2009 (see page 38).

Results By Segment

Three Months Ended June 30

- 29 -

FINANCIAL

PERFORMANCE

(1) Excludes certain “extra expenses” recorded

by the Company during the three months ended

June 30, 2009, resulting primarily from plant closings and staff reductions. These expenses were

largely due to the unprecedented conditions in the RV and manufactured housing industries

(see page 40).

Results By Segment

Six Months Ended June 30,

- 30 -

FINANCIAL

PERFORMANCE

(1) Excludes certain “extra expenses” recorded

by the Company during the six months ended June

30, 2009, resulting primarily from plant closings, staff reductions, increased bad debts, and

obsolete inventory and tooling. These expenses were largely due to the unprecedented

conditions in the

RV and manufactured housing industries (see page 40).

Balance Sheet

- 31 -

FINANCIAL

PERFORMANCE

(1) Days sales in accounts receivable is the most recent month’s net sales divided by

accounts receivable, net, at the end of the period.

(2) Inventory turns is cost of goods sold for the last twelve months divided by average

inventory for the last twelve months.

Financial Strength

(1)

EBITDA is operating profit plus depreciation, amortization and goodwill impairment (see page 35).

(2)

Excludes a goodwill impairment charge of $5.5 million ($3.4 million after tax).

(3) Excludes a goodwill impairment charge of $45.0 million ($29.4 million after tax).

- 32 -

FINANCIAL

PERFORMANCE

Analyst Coverage

- 33 -

CJS Securities

Torin Eastburn – (914) 287-7600

Thompson Research Group

Kathryn Thompson – (615) 891-6206

Janney Montgomery Scott LLC

Liam D. Burke – (202) 955-4305

Sidoti & Company, LLC

Scott Stember – (212) 453-7017

Avondale Partners, LLC

Bret Jordan – (617) 314-0487

Thank you!

Joseph S. Giordano III

Chief Financial Officer

914-428-9098

joe@drewindustries.com

OR

VISIT OUR WEBSITE:

www.drewindustries.com

For more information contact:

- 34 -

Fredric M. Zinn

President and CEO

914-428-9098

fred@drewindustries.com

Reconciliation of Operating

Profit to EBITDA

- 35 -

FINANCIAL

PERFORMANCE

Reconciliation of Operating Profit

to EBITDA - Quarterly

- 36 -

FINANCIAL

PERFORMANCE

Reconciliation of Adjusted

Results to Actual

FINANCIAL

PERFORMANCE

(1)

During 2009 and 2008, the Company recorded “extra” expenses resulting primarily from plant closings and

start-ups, staff reductions and relocations, increased bad debts and obsolete inventory

and tooling. These

expenses were largely due to the unprecedented conditions in the RV and manufactured housing industries. In

addition, the Company recorded charges for goodwill impairment during the fourth quarter of 2008 and the first

quarter

of 2009, and charges for executive retirement in the fourth quarter of 2008.

- 37 -

Reconciliation of Adjusted

Results to Actual

FINANCIAL

PERFORMANCE

(1)

During 2009 and 2008, the Company recorded “extra” expenses resulting primarily from plant closings and

start-ups, staff reductions and relocations, increased bad debts and obsolete inventory

and tooling. These

expenses were largely due to the unprecedented conditions in the RV and manufactured housing industries. In

addition, the Company recorded charges for goodwill impairment during the fourth quarter of 2008 and the first

quarter

of 2009, and charges for executive retirement in the fourth quarter of 2008.

- 38 -

Reconciliation of Segment Adjusted

Operating Profit to Actual

FINANCIAL

PERFORMANCE

(1)

During 2009 and 2008, the Company recorded “extra” expenses resulting primarily from plant closings and

start-ups, staff reductions and relocations, increased bad debts and obsolete inventory

and tooling. These

expenses were largely due to the unprecedented conditions in the RV and manufactured housing industries.

- 39 -

See page 41 for a reconciliation of segment actual results to consolidated actual results.

Reconciliation of Segment Adjusted

Operating Profit to Actual

FINANCIAL

PERFORMANCE

(1)

During 2009 and 2008, the Company recorded “extra” expenses resulting primarily from plant closings and

start-ups, staff reductions and relocations, increased bad debts and obsolete inventory

and tooling. These

expenses were largely due to the unprecedented conditions in the RV and manufactured housing industries.

- 40 -

See page 41 for a reconciliation of segment actual results to consolidated actual results.

FINANCIAL PERFORMANCE

- 41 -

Reconciliation of Segment Results

to Consolidated