Attached files

Table of Contents

As filed with the Securities and Exchange Commission on June 29, 2010

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

LINC LOGISTICS COMPANY

(Exact name of registrant as specified in its charter)

| Michigan | 4731 | 38-3645748 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(IRS Employer Identification No.) |

11355 Stephens Road

Warren, MI 48089

(586) 467-1500

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

H. E. “Scott” Wolfe

Chief Executive Officer

LINC Logistics Company

11355 Stephens Road

Warren, MI 48089

(586) 467-1500

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

| C. Douglas Buford, Jr. Mitchell, Williams, Selig, Gates & Woodyard, P.L.L.C. 425 W. Capitol Avenue, Ste. 1800 Little Rock, AR 72201 (501) 688-8800 |

Marc D. Jaffe Christopher D. Lueking Latham & Watkins LLP 233 S. Wacker Drive, Suite 5800 Chicago, IL 60606 (312) 876-7700 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “accelerated filer”, “large accelerated filer”, and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | |||

| Non-accelerated filer þ | (Do not check if a smaller reporting company) | Smaller reporting company ¨ | ||

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered |

Proposed maximum aggregate offering price (1)(2) |

Amount of registration fee | ||

| Common stock, no par value |

$115,000,000 | $8,199.50 | ||

| (1) | Estimated pursuant to Rule 457(o) under the Securities Act of 1933, as amended, solely for the purpose of calculating the registration fee. |

| (2) | Includes offering price of shares that the underwriters have the option to purchase to cover over-allotments, if any. |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, Dated June 29, 2010

PRELIMINARY PROSPECTUS

Shares

LINC Logistics Company

Common Stock

$ per share

This is the initial public offering of our common stock. Prior to this offering, there has been no public market for our common stock. We are offering shares of our common stock. We currently expect the initial public offering price to be between $ and $ per share.

We have granted the underwriters an option to purchase up to additional shares of common stock to cover over-allotments.

We intend to apply to have our common stock listed on the NASDAQ Global Select Market under the symbol “LLGX.”

Investing in our common stock involves risks. See “Risk Factors” beginning on page 11.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share |

Total | |||||

| Public Offering Price |

$ | $ | ||||

| Underwriting Discount |

$ | $ | ||||

| Proceeds to LINC Logistics Company (before expenses) |

$ | $ | ||||

The underwriters expect to deliver the shares to purchasers on or about , 2010 through the book-entry facilities of The Depository Trust Company.

| Citi | Stephens Inc. | Stifel Nicolaus |

KeyBanc Capital Markets

, 2010

Table of Contents

[Graphic to come]

Table of Contents

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front of this prospectus.

| Page | ||

| 1 | ||

| 11 | ||

| 28 | ||

| 29 | ||

| 30 | ||

| 31 | ||

| 32 | ||

| Selected Combined and Consolidated Financial and Operating Data |

33 | |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

36 | |

| 58 | ||

| 62 | ||

| 76 | ||

| 80 | ||

| 87 | ||

| 91 | ||

| 92 | ||

| 95 | ||

| Material United States Federal Income Tax Consequences to Non-U.S. Holders |

97 | |

| 100 | ||

| 104 | ||

| 104 | ||

| 105 | ||

| F-1 |

Unless the context requires otherwise, the terms “LINC,” “we,” “Company,” “us” and “our” refer to LINC Logistics Company and its subsidiaries. Logistics Insight Corporation®, LINC, Central Global Express®, and C.T.X.® are trademarks of LINC Logistics Company and its subsidiaries. All other trademarks, service marks or tradenames referred to in this prospectus are the property of their respective owners. This prospectus also contains references to trademarks and service marks of other companies.

The market and industry data and forecasts included in this prospectus are based upon independent industry sources, including Armstrong & Associates and CSM Worldwide. Although we believe that these independent sources are reliable, we have not independently verified the accuracy and completeness of this information, nor have we independently verified the underlying economic or other assumptions relied upon in preparing any data or forecasts.

i

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary may not contain all of the information that may be important to you. You should read this summary together with the entire prospectus, including the more detailed information regarding us and the common stock being sold in this offering and our consolidated financial statements and related notes appearing elsewhere in this prospectus. You should carefully consider, among other things, the matters discussed in the section entitled “Risk Factors.”

Our Business

We are a leading provider of mission-critical third-party logistics solutions that allow our customers and clients to reduce costs and manage their global supply chains more efficiently. We offer a comprehensive suite of supply chain logistics services, including value-added, transportation and specialized services. Our value-added logistics services include material handling and consolidation, sequencing and sub-assembling, kitting and repacking, and returnable container management. We also provide a broad range of transportation services, such as dedicated truckload, shuttle operations and yard management. Our specialized services include air and ocean freight forwarding, expedited ground transportation and final-mile delivery. Historically, our largest end-market has been the automotive segment, where we maintain strong and long-term relationships with our customers. In recent years, we have successfully expanded our business outside of the automotive sector into the industrial products, aerospace, medical equipment and technology sectors. Our revenues in sectors outside of automotive grew at a compound annual rate of 23.9% to $9.5 million, or 17.0% of revenues, for the thirteen weeks ended April 3, 2010 from $5.0 million, or 6.7% of revenues, for the thirteen weeks ended March 31, 2007.

We operate and manage 31 logistics facilities in the United States, Canada and Mexico. Our facilities and services are often directly integrated into and located near the production processes of our customers and represent a critical piece of their supply chains. Our proprietary information technology platform is integrated with our customers’ and their vendors’ information technology networks, allowing real-time end-to-end supply chain visibility. As a result of our close integration with our customers, most of our value-added services are contracted for the duration of our customers’ production programs, which typically last three to five years. In 2009, over 84% of our value-added services revenue was derived from multi-year contracts.

We employ an asset-light business model that lowers our capital expenditure requirements and improves investment returns and cash-flow generation. We believe our asset-light business model is highly scalable and will continue to support our growth with relatively modest capital expenditure requirements. Our asset-light model, combined with a disciplined approach to contract structuring and pricing, creates a highly flexible cost structure that allows us to scale our business up and down quickly in response to changes in demand from our customers. This flexibility helped us to deliver positive operating income in each of the past nine quarters, despite an unprecedented slowdown in demand from our U.S. automotive customers as a result of the global recession and the restructurings of General Motors and Chrysler.

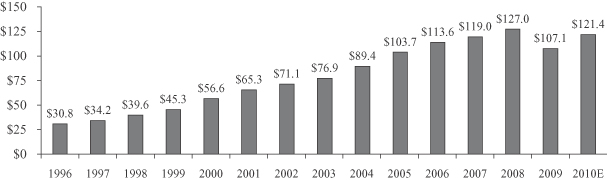

According to Armstrong & Associates, gross revenue for the U.S. third-party logistics (3PL) market grew at a compound annual rate of 12.5% from $30.8 billion in 1996 to $127.0 billion in 2008. Although Armstrong & Associates reports that the U.S. 3PL sector declined 15.7% in 2009 to $107.1 billion, we expect the sector will resume its expansion, driven primarily by the elongation and increasing complexity of supply chains and the continued desire of manufacturers to reduce costs, increase efficiencies and improve customer service. Armstrong & Associates estimated in May 2010 that the U.S. 3PL market will rebound strongly in 2010, increasing 13.4% to $121.4 billion.

1

Table of Contents

For the thirteen weeks ending April 4, 2009 and April 3, 2010 we generated $42.3 million and $56.1 million in revenues and $3.9 million and $8.4 million in Adjusted EBITDA, respectively, representing increases of 32.6% and 116.0%, respectively, over the comparable prior period. See “— Summary Consolidated Financial and Operating Data” for our definition of Adjusted EBITDA and why we present it, and for a reconciliation of net income to Adjusted EBITDA.

Our Strengths

We believe the following strengths position us for sustainable growth:

Leading provider of mission-critical supply chain solutions to the North American automotive industry. Our single-source, comprehensive logistics solutions, extensive expertise serving automotive supply chains, and longstanding customer relationships have contributed to our position as a leading provider of third-party logistics services to the automotive industry. We are a core 3PL provider to many of our customers. For example, we operate the largest receiving and distribution operations for both Ford and Chrysler, delivering inbound components within stringent supply chain schedules. As a leading provider of logistics services to the automotive industry, we are well positioned to benefit from the continuation of favorable outsourcing trends within the automotive sector.

Broad portfolio of integrated third-party logistics services. We provide an extensive range of logistics services that includes value-added warehousing and material handling services, dedicated transportation services, international freight forwarding, and expedited freight delivery. We believe our ability to provide integrated logistics solutions is a competitive advantage as customers continue to seek a single point of contact for logistics services. For example, we can provide an integrated single-source solution incorporating value-added operations, transportation services and specialized logistics services to support one or multiple customer locations. Our broad range of capabilities also provides us with multiple growth platforms and significant cross-selling opportunities.

Unique value proposition based on sophisticated labor strategies. We believe our ability to structure effective labor contracts and to draw from a variety of union, non-union and contract labor pools differentiates us from our competitors, allowing us to provide customized and cost-effective solutions that accommodate our customers’ labor strategies. Our senior operational management team has an average of over 25 years of experience managing contract services in unionized environments. We currently have eight collective bargaining agreements with three different unions. Each collective bargaining agreement with each union covers a single facility with that union, enhancing our flexibility in developing our labor strategies. No single union has represented more than 38.4% of our employees in any given year over the past three years.

Proven customer contract pricing discipline. We use a standard customer contract approval process to evaluate, develop and price contracts for new large program logistics opportunities. This mandatory process includes an evaluation of pricing, capital expenditure requirements, financial return and risk assessment prior to approval. Additionally, a significant percentage of our contracts for value-added services includes a fixed price component that produces a stable revenue stream regardless of a customer’s supply chain activity. Our disciplined contract pricing strategy and ability to include a fixed price component in our contracts has helped us to maintain profitability despite recent volatility in customer demand.

Enduring customer relationships. We have long-term relationships with most of our largest customers. We have provided services to our top five customers for an average of 18 years. Typically our services are directly linked into our customers’ production processes, requiring a high level of integration with our customers’ operations and technology systems, which improves our competitive position and increases our customers’ costs of switching logistics providers. Since December 31, 2006, our customers retained our services for over 80% of the value-added services agreements that were expiring and subsequently renewed with a 3PL provider.

2

Table of Contents

During this same period, over 90% of our revenue has come from contracts with initial terms of at least one year, thereby improving the predictability of our cash flows.

Flexible, asset-light business model. Our asset-light, variable-cost-based operating structure enables us to scale our business up and down in response to changing business conditions and generates strong cash flows and return on capital. Substantially all of our operating facilities are either provided to us by customers, leased by us on a month-to-month basis, or leased by us on terms that match the related customer contracts to the greatest extent possible. Additionally, to accommodate our customers’ freight transportation needs, we use a network of independent tractor owners (owner-operators) and third-party transportation providers in addition to our Company-owned tractors. As of April 3, 2010, owner-operators supplied approximately 29.7% of the tractors used over the road in our transportation services and specialized services operations. We believe that our highly scalable operating platform will continue to support our growth with limited capital expenditure requirements.

State-of-the-art proprietary information technology system. We have developed a proprietary, integrated and scalable information technology platform that allows us to efficiently manage key processes across our customers’ supply chains. The advanced functionality of our IT system enables seamless integration with customers’ and vendors’ IT networks and allows us to provide real-time end-to-end supply chain visibility. We believe that these applications improve our services and quality controls, strengthen our relationships with our customers and enhance our value proposition.

Highly experienced management team. Our management team has a track record of delivering strong, profitable growth. Senior management is comprised of experienced professionals with an average of over 25 years of experience in transportation and logistics services, and related outsourcing businesses, and who have an average of 30 years of experience in the global automotive industry.

Our Strategy

Our goal is to strengthen our position as a leading logistics services provider through the following strategies:

Continue to capitalize on strong industry fundamentals and outsourcing trends. According to Armstrong & Associates, gross revenue for the U.S. 3PL market grew at a compound annual rate of 12.5% from $30.8 billion in 1996 to $127.0 billion in 2008. Although the U.S. 3PL sector declined in 2009 to $107.1 billion according to Armstrong & Associates, we expect the sector will resume its expansion, driven primarily by the elongation and increasing complexity of supply chains as well as the continued desire of manufacturers to reduce costs and increase efficiency by outsourcing non-core functions. In May 2010, Armstrong & Associates estimated the U.S. 3PL sector will rebound strongly in 2010, increasing 13.4% to $121.4 billion. We intend to leverage our integrated suite of logistics services, our network of facilities in the United States, Canada and Mexico, our long-term customer relationships, and our reputation for operational excellence to capitalize on favorable industry fundamentals and growth expectations.

Target further penetration of key customers in the North American automotive industry. The automotive industry is one of the largest users of global outsourced logistics services, providing us growth opportunities with both existing and new customers. We intend to capitalize on anticipated continued growth in outsourcing of higher value logistics services in the automotive sector such as sub-assembly and sequencing, which link directly into production lines and require specialized capabilities, technological expertise and strict quality controls. We believe we are well positioned to capitalize on this increased outsourcing activity as a result of our extensive experience and enduring customer relationships. We regularly pursue opportunities to further penetrate our core automotive customer base by leveraging our position in the supply chains of our original equipment manufacturer (OEM) customers to extend our services to their suppliers and by cross-selling a wide

3

Table of Contents

range of transportation and specialized services to existing customers. We are also targeting and expect to increase our services to Tier I automotive component suppliers and foreign-owned automotive manufacturers operating in North America.

Continue to expand into new industry verticals. We have provided highly complex value-added logistics services to our automotive customers for an average of more than 18 years. These capabilities and our broad portfolio of other logistics services are highly transferable to other vertical markets. In recent years, we have successfully targeted other end-markets where we believe we can leverage the expertise we developed in the automotive sector. New targeted industries include industrial products, aerospace, medical equipment, and technology. Revenues from customers outside of the automotive industry increased from 7.5% of revenues, or $22.4 million, in 2007 to 14.9% of revenues, or $26.5 million, in 2009. We believe our ability to provide a broad range of services in key markets in the U.S. and internationally provides us with additional growth platforms and cross-selling opportunities.

Expand our logistics services capabilities and geographical reach. We intend to continue to expand our portfolio of services in response to customer demands for greater innovation and responsiveness from their logistics providers. We will also continue to pursue high growth sectors within our specialized services, such as expedited ground transportation and international freight forwarding. In addition, we intend to increase penetration of our services into other regions of the United States and in international markets, such as Mexico, where we deliver logistics services to General Motors’ newest automotive assembly plant.

Continue to invest in technological advances to meet customer requirements. With continued outsourcing of supply chain activities, customers are requiring greater advances in information technology to support increasingly complex logistics solutions. We intend to continue to improve our proprietary IT system and expand the technology component of our service portfolio through a combination of internally and externally developed software. We believe that these ongoing technology investments will enhance the differentiation of our services relative to competing providers.

Grow through selected acquisitions. The 3PL industry is highly fragmented, with hundreds of small and mid-sized competitors that are either specialized in specific vertical markets or limited to local and regional coverage. We expect to selectively evaluate and pursue acquisitions that will enhance our service capabilities, expand our geographic network, diversify our customer base and accelerate our earnings growth. Although we regularly evaluate and engage in discussions with potential targets, we do not currently have any agreements in place for material acquisitions.

Risk Factors

Our business is subject to numerous risks, which are highlighted in the section titled “Risk Factors” immediately following this prospectus summary. These risks represent challenges to the successful implementation of our strategy and to the growth and future profitability of our business. Some of these risks are:

| • | our revenue is highly dependent on the automotive industry and any decrease in demand for outsourced services in this industry or our other targeted industries could reduce our revenue and seriously harm our business; |

| • | we derive a significant portion of our revenue from a few major customers, and the loss of one or more of them, or a reduction in their operations, could have a material adverse effect on our business; |

| • | customer manufacturing plant closures could have a material adverse effect on our performance; |

| • | competition and consolidation in the 3PL market may harm our business; and |

| • | our profitability could be negatively impacted by downward pricing pressure from certain of our customers. |

4

Table of Contents

Corporate Information

LINC Logistics Company was incorporated in Michigan on March 11, 2002, to combine certain logistics and transportation businesses of CenTra, Inc. (CenTra). One such business, Logistics Insight Corp., began operations in 1992 and is now one of our wholly-owned subsidiaries. On December 31, 2006, CenTra completed a corporate reorganization through which all entities included in our consolidated financial statements as of and for the year ended December 31, 2006 came under our direct ownership and control. In connection with that reorganization, on December 29, 2006, we declared a $93.0 million cash dividend payable to CenTra, and on December 31, 2006, we distributed a $33.4 million net receivable to CenTra. Immediately following the distribution of the net receivable, CenTra distributed all of our outstanding common stock in a spin-off transaction to its stockholders, Matthew T. Moroun and a trust controlled by Manuel J. Moroun, Matthew T. Moroun’s father.

Our principal executive offices are located at 11355 Stephens Road, Warren, Michigan 48089, and our telephone number is (586) 467-1500. Our website address is www.4linc.com. Information on or accessed through our website is not incorporated into this prospectus and is not part of this prospectus.

5

Table of Contents

The Offering

| Common stock being offered by us |

shares |

| Common stock to be outstanding after this offering |

shares |

| Use of proceeds |

We estimate that our net proceeds from this offering will be approximately $ million. We intend to use approximately $93 million of our net proceeds to satisfy an outstanding $68 million cash dividend payable and a related $25 million dividend distribution promissory note to CenTra, Inc., which was our sole shareholder on December 29, 2006, the record date for the dividend. We may use additional net proceeds to pay down balances on our revolving credit facilities. The balance of our net proceeds will be used for working capital and general corporate purposes. In addition, although we have no specific acquisition plans at this time, we may use a portion of our net proceeds to make acquisitions. See “Use of Proceeds.” |

| Risk factors |

You should read the “Risk Factors” section of this prospectus for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. |

| Proposed NASDAQ Global Select Market symbol |

We intend to apply to have the common stock listed on the NASDAQ Global Select Market under the symbol “LLGX.” |

The number of shares shown to be outstanding after this offering is based on shares outstanding as of , 2010, and excludes shares of common stock available for future issuance under a long-term incentive plan that we expect to be in effect before completing the offering.

We have granted the underwriters an option to purchase up to additional shares of common stock to cover over-allotments.

Except as otherwise indicated, all information in this prospectus assumes:

| • | a -for-1 split of shares of our common stock, which will occur before completing this offering; |

| • | an initial public offering price of $ per share, the midpoint of the range set forth on the cover of this prospectus; and |

| • | no exercise of the underwriters’ over-allotment option. |

6

Table of Contents

Summary Consolidated Financial and Operating Data

The following table sets forth a summary of our consolidated financial and operating data as of and for the periods presented. The table includes certain pro forma information that reflects the impact of our conversion from an S-corporation to a C-corporation in connection with this offering. We derived the summary consolidated statements of income data for the years ended December 31, 2007, 2008, and 2009 from our audited consolidated financial statements included elsewhere in this prospectus. We derived the summary consolidated statements of income data for the thirteen weeks ended April 4, 2009 and April 3, 2010 and summary consolidated balance sheet data as of April 3, 2010 from our unaudited consolidated interim financial statements included elsewhere in this prospectus. We have prepared the unaudited consolidated interim financial statements on the same basis as our audited financial statements and, in our opinion, have included all adjustments, which include only normal recurring adjustments, necessary to present fairly in all material respects our financial position and results of operations.

The information below should be read in conjunction with the information included under the headings “Selected Combined and Consolidated Financial and Operating Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes included elsewhere in this prospectus. The results for any interim period are not necessarily indicative of the results that may be expected for the full year. The following historical financial information may not be indicative of our future performance.

| Year Ended December 31, |

Thirteen Weeks Ended | ||||||||||||||

| 2007 |

2008 |

2009 |

April 4, 2009 |

April 3, 2010 | |||||||||||

| (unaudited) | |||||||||||||||

| (in thousands, except per share amounts and employee and facility counts) | |||||||||||||||

| Statements of Income Data: |

|||||||||||||||

| Revenue |

$ | 299,195 | $ | 247,815 | $ | 177,938 | $ | 42,314 | $ | 56,093 | |||||

| Operating expenses: |

261,706 | 233,413 | 160,316 | 40,207 | 48,923 | ||||||||||

| Operating income |

37,489 | 14,402 | 17,622 | 2,107 | 7,170 | ||||||||||

| Interest expense, net |

3,414 | 2,071 | 1,354 | 369 | 356 | ||||||||||

| Income before provision for income taxes |

34,075 | 12,331 | 16,268 | 1,738 | 6,814 | ||||||||||

| Provision for income taxes |

1,361 | 1,412 | 1,339 | 347 | 395 | ||||||||||

| Net income |

$ | 32,714 | $ | 10,919 | $ | 14,929 | $ | 1,391 | $ | 6,419 | |||||

| Pro Forma Data (unaudited): |

|||||||||||||||

| Income before provision for income taxes |

$ | 34,075 | $ | 12,331 | $ | 16,268 | $ | 1,738 | $ | 6,814 | |||||

| Pro forma provision for income taxes(1) |

14,448 | 4,407 | 6,257 | 669 | 2,528 | ||||||||||

| Pro forma net income |

$ | 19,627 | $ | 7,924 | $ | 10,011 | $ | 1,069 | $ | 4,286 | |||||

| Pro forma earnings per share, basic and diluted |

|||||||||||||||

| Average shares outstanding, basic and diluted |

|||||||||||||||

| Pro Forma as Adjusted Data (unaudited): |

|||||||||||||||

| Pro forma as adjusted earnings per share(2) |

|||||||||||||||

| Basic |

|||||||||||||||

| Diluted |

|||||||||||||||

| Other Data: |

|||||||||||||||

| Adjusted EBITDA(3) |

$ | 45,953 | $ | 30,194 | $ | 27,164 | $ | 3,892 | $ | 8,408 | |||||

| Cash flow from operations |

$ | 42,992 | $ | 19,145 | $ | 16,892 | $ | 6,359 | $ | 7,011 | |||||

| Capital expenditures |

$ | 11,110 | $ | 2,726 | $ | 1,655 | $ | 468 | $ | 563 | |||||

| Cash dividends paid(4) |

$ | 68,000 | $ | 5,600 | $ | — | $ | — | $ | 2,000 | |||||

| Employees at end of period |

2,776 | 1,880 | 1,504 | 1,583 | 1,476 | ||||||||||

| Facilities managed at end of period |

26 | 24 | 26 | 21 | 31 | ||||||||||

7

Table of Contents

| As of April 3, 2010 | |||||

| Actual |

Pro

Forma as Adjusted(5) | ||||

| (unaudited, in thousands) | |||||

| Balance Sheet Data: |

|||||

| Cash and cash equivalents |

$ | 2,718 | |||

| Total assets |

73,306 | ||||

| Total debt |

62,869 | ||||

| (1) | Since January 1, 2007, we have been treated as an S-corporation for U.S. federal income tax purposes. For the years ended 2005 and 2006, we were treated as a C-corporation for income tax purposes. As a result of our S-corporation status, our income since January 1, 2007 has not been subject to U.S. federal income taxes or state income taxes in those states where S-corporation status is recognized. In general, the corporate income or loss of an S-corporation is allocated to its stockholders for inclusion in their personal federal income tax returns and state income tax returns in those states where S-corporation status is recognized. The provision for income taxes in 2007, 2008, 2009 and the thirteen weeks ended April 3, 2010 reflects the amount of entity-level income taxes in those jurisdictions where S-corporation status is not recognized. For the year ended December 31, 2007, as a result of our S-corporation election, our provision for income taxes includes the realization of a U.S. deferred tax expense of $2.5 million resulting from the elimination of a U.S. net deferred tax asset. In connection with this offering, our S-corporation status will be terminated and we will become subject to additional entity-level income taxes that will be reflected in our financial statements. Also, we will reestablish deferred tax accounts eliminated in 2007. As of April 3, 2010, such action, which has been contemplated in the pro forma provision for each of the periods presented, would have resulted in an estimated $1.5 million increase in our provision for income taxes. Pro forma provision for income taxes reflects combined federal, state and local income taxes, as if we had been treated as a C-corporation, using blended statutory federal, state and local income tax rates of 42.4%, 35.7%, 38.5% and 37.1% in 2007, 2008, 2009 and the thirteen weeks ended April 3, 2010, respectively. These tax rates reflect the sum of the federal statutory rate and a blended state rate based on our calculation of income apportioned to each state for each period. |

| (2) | Pro forma as adjusted data is computed by dividing pro forma net income, adjusted for the elimination of approximately $ million in interest expense and the related tax benefit at an effective tax rate of %, assuming the retirement with a portion of the proceeds from this offering of approximately $ million of our outstanding debt, by the number of shares outstanding after this offering. Such outstanding share amounts include shares to be issued in connection with this offering and shares of restricted stock and options to be issued before completion of this offering under our proposed Long-Term Incentive Plan. See “Compensation Discussion and Analysis — Long-Term Incentive Plan.” |

| (3) | We present Adjusted EBITDA as a supplemental measure of our performance. We define Adjusted EBITDA as net income plus (i) interest expense, net, (ii) provision for income taxes and (iii) depreciation and amortization, or EBITDA, adjusted to eliminate the impact of certain items that we do not consider indicative of our ongoing operating performance, including facility closing costs, suspended capital market activity and legal settlement. These further adjustments are itemized below. You are encouraged to evaluate these adjustments and the reasons we consider them appropriate for supplemental analysis. In evaluating Adjusted EBITDA, you should be aware that in the future we may incur expenses that are the same as or similar to some of the adjustments in this presentation. Our presentation of Adjusted EBITDA should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items. |

8

Table of Contents

Set forth below is a reconciliation of net income, the most comparable GAAP measure, to EBITDA and Adjusted EBITDA for each of the periods indicated:

| Year Ended December 31, |

Thirteen Weeks Ended |

|||||||||||||||

| 2007 |

2008 |

2009 |

April 4, 2009 |

April 3, 2010 |

||||||||||||

| (in thousands) | (unaudited, in thousands) | |||||||||||||||

| Net income |

$ | 32,714 | $ | 10,919 | $ | 14,929 | $ | 1,391 | $ | 6,419 | ||||||

| Provision for income taxes |

1,361 | 1,412 | 1,339 | 347 | 395 | |||||||||||

| Interest expense, net |

3,414 | 2,071 | 1,354 | 369 | 356 | |||||||||||

| Depreciation and amortization |

6,664 | 7,432 | 6,952 | 1,785 | 1,597 | |||||||||||

| EBITDA |

44,153 | 21,834 | 24,574 | 3,892 | 8,767 | |||||||||||

| Facility closing costs(a) |

— | 3,023 | 2,590 | — | (359 | ) | ||||||||||

| Suspended capital market activity(b) |

— | 575 | — | — | — | |||||||||||

| Legal settlement(c) |

1,800 | 4,762 | — | — | — | |||||||||||

| Adjusted EBITDA |

$ | 45,953 | $ | 30,194 | $ | 27,164 | $ | 3,892 | $ | 8,408 | ||||||

| (a) | Represents costs incurred as a result of our election in 2008 and 2009 to close five value-added services operations due to the unprecedented contraction in production capacity by our major automotive customers. Such costs include facility lease costs (net of anticipated sublease revenues or comparable offsets), employee severance payments, and other similar expenses. |

| (b) | Represents expenses incurred as a result of our postponed IPO efforts in 2007 due to a decline in the automotive sector, deterioration in economic conditions and the significant downturn in the public equity markets. |

| (c) | Represents expenses accrued in connection with the prospective determination of probable loss amounts in connection with a multi-fatality traffic accident that was likely to exceed insurance limits and which we believe is not reflective of ordinary operations. |

We present Adjusted EBITDA because we believe it assists investors and analysts in comparing our performance across reporting periods on a consistent basis by excluding items that we do not believe are indicative of our core operating performance.

Adjusted EBITDA has limitations as an analytical tool. Some of these limitations are:

| • | Adjusted EBITDA does not reflect our cash expenditures, or future requirements, for capital expenditures or contractual commitments; |

| • | Adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs; |

| • | Adjusted EBITDA does not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debts; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and Adjusted EBITDA does not reflect any cash requirements for such replacements; |

| • | Adjusted EBITDA does not reflect the impact of certain cash charges resulting from matters we consider not to be indicative of our ongoing operations; and |

| • | other companies in our industry may calculate Adjusted EBITDA differently than we do, limiting its usefulness as a comparative measure. |

9

Table of Contents

Because of these limitations, Adjusted EBITDA should not be considered in isolation or as a substitute for performance measures calculated in accordance with GAAP. We compensate for these limitations by relying primarily on our GAAP results and using Adjusted EBITDA only supplementally.

| (4) | Includes only cash dividends previously paid, and thus does not include the $68 million dividend payable or the related $25 million dividend distribution promissory note that are intended to be paid from the proceeds of this offering. |

| (5) | Pro forma as adjusted balance sheet data as of April 3, 2010 are determined by giving effect to (a) the issuance of shares of common stock offered by us (at an assumed initial public offering price of $ per share, the midpoint of the range set forth on the front cover of this prospectus), (b) the cash payment of the $68 million dividend payable to CenTra, which was our sole shareholder on the record date for such dividend, (c) the payment of the related $25 million dividend distribution promissory note, (d) the payment of a $ million S-corporation dividend to our existing shareholders, (e) the repayment of $ million of our indebtedness and (f) a non-cash charge that will result from the termination of the Company’s S-corporation status. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Spin-Off from Related Party and ‘Subchapter S’ Election.” |

10

Table of Contents

The value of your investment will be subject to the significant risks inherent in our business. You should carefully consider the risks and uncertainties described below and other information included in this prospectus before purchasing our common stock. If any of the events described below occur, our business and financial results could be seriously harmed. The trading price of our common stock could decline as a result of any of these risks, and you may lose all or part of your investment.

Risks Relating to Our Business

Our revenue is highly dependent on the North American automotive industry, and may be negatively affected by further downturns in North American automobile production.

A substantial portion of our customers are concentrated in the North American automotive industry. For the fiscal year ended December 31, 2009, and the thirteen weeks ended April 3, 2010, 85.1% and 83.0%, respectively, of our revenue was derived from customers in the North American automotive industry. Our business and growth largely depend on continued demand for our services from customers in this industry.

The global economic crisis that has existed for at least the last two years and continues to exist has resulted in delayed and reduced purchases of automobiles. According to CSM Worldwide, light vehicle production during 2009 decreased by 32% and 43% in North America as compared to 2008 and 2007, respectively. As a result of plant closings and the general downturn in North American automobile production, the revenue we derive from customers in the North American automotive industry decreased from a high of $73.0 million for the thirteen weeks ended June 30, 2007, to $46.5 million for the thirteen weeks ended April 3, 2010, a decline of more than 36.3%. Throughout the period 2008 to 2009, we experienced significant variability in our revenues from automotive industry customers, as General Motors and Chrysler restructured through bankruptcies, and other North American manufacturers re-scaled their operations to adjust to changing market demands.

These unprecedented conditions have negatively impacted our revenues during the last two fiscal years. Further downturns in North American automobile production may similarly affect our revenues in future periods.

Any decrease in demand for outsourced services in the industries we serve could reduce our revenue and seriously harm our business.

Our growth strategy is partially based on the assumption that the trend towards outsourcing logistics services will continue despite potentially adverse economic trends affecting our automotive and other customers. Declines in sales volumes in the industries we serve, particularly the automotive industry, may lead to a declining demand for logistics services.

Production volumes in the automotive industry are sensitive to consumer demand as well as employee and labor relations. Declines in sales volumes, or the expectation of declines, for the industry or for any of our individual customers could result in production cutbacks and unplanned plant shutdowns. Likewise, potential customers may see a risk, based on labor relations issues or other factors, in relying on third-party logistics service providers or may define these activities as their own core competencies and may seek means to deploy excess labor or other resources, and hence may prefer to perform logistics operations themselves. We therefore cannot assure you that the market for logistics services will not decline or will grow as we expect.

Other developments may also lead to a decline in the demand for our services in our targeted industries. For example, consolidation in these industries or acquisitions, particularly involving our customers, may decrease the potential number of buyers of our services. Similarly, the relocation or expansion of automotive or other production operations in locations where we do not have an established presence, or where our competitive position is not as strong, may adversely affect our business, even if production increases worldwide, if we are not

11

Table of Contents

able to effectively service these industries in such locations. Any significant reduction in or the elimination of the use of the services we provide within any of these industries would result in reduced revenue and harm our business.

Many of our customers experience rapid changes in their prospects, substantial price competition and pressure on their profitability. Although such pressures can encourage outsourcing as a cost-reduction measure, they may also result in increasing pressure on us from our automotive and other customers to lower our prices, which could negatively affect our business, results of operations, financial condition and cash flows.

We derive a significant portion of our revenue from a few major customers, and the loss of any one or more of them as customers, or a reduction in their operations, could have a material adverse effect on our business.

A significant portion of our revenue is generated from a limited number of major customers. Approximately 30.0%, 30.3% and 11.5% of our revenue for the fiscal year ended December 31, 2009, was attributable to affiliates of Ford, General Motors and Chrysler, respectively, who together accounted for approximately 71.8% of our revenue for such period. For the thirteen weeks ended April 3, 2010, approximately 31.2%, 24.6% and 12.9% of our revenue was attributable to affiliates of Ford, General Motors and Chrysler, respectively, who together accounted for approximately 68.8% of our revenue for such period. Our contracts with our customers generally contain cancellation clauses, and there can be no assurance that these customers will continue to utilize our services or that they will continue at the same levels. Further, there can be no assurance that these customers will not be further affected by the continuation of the recent downturn in the automotive industry, which would result in a reduction in their operations and corresponding need for our services. Moreover, our customers may lose market share, apart from trends in the automotive industry generally. In recent years, General Motors, Chrysler and Ford have lost market share in the United States. If our major customers continue to lose U.S. market share they may have less need for our services. A reduction in or termination of our services by one or more of our major customers could have a material adverse effect on our business and results of operations.

Customer manufacturing plant closures could have a material effect on our performance.

We derive a substantial portion of our revenue from the operation and management of our operating facilities, which are often located adjacent to a customer’s manufacturing plant and are directly integrated into the customer’s production line process. We may experience significant revenue loss and shut-down costs, including costs related to early termination of leases, causing our business to suffer if our customers closed their plants or significantly modified their capacity or supply chains at a plant that we service.

During the period 2008 to 2010, we discontinued and closed operations at five locations in response to our customers closing their related manufacturing plants and recorded aggregate shut-down charges of $5.3 million as a result of those closings. Although we do not currently operate any facilities linked to other announced plant closures, there can be no assurance that we will not be impacted by any future announcements of plant closures.

Competition and consolidation in the market for third-party logistics services may harm our business.

The third-party logistics industry is intensely competitive, and our business may suffer if we are unable to address pricing pressures and other competitive factors that may adversely affect our revenue and costs relative to our competitors. We face competition from a number of global companies, some of which have greater financial and marketing resources. In the industry sectors and regions in which we are active, we also face competition from certain niche and local logistics providers, some of which have a significant market presence in their respective sectors or regional niche markets. If we cannot successfully compete with our competitors, this could result in reduced revenue and reduced margins, both of which could have a material adverse effect on our operating cash flows and results of operations.

In recent years, the third-party logistics market has seen a growing market presence of larger logistics companies. Many logistics companies are attempting to expand their operations through the acquisition of

12

Table of Contents

contract logistics providers and other transportation service providers. We have a focused strategy in selected industry sectors and regions where we believe we have competitive advantages and therefore a defensible market position. If we cannot maintain or gain sufficient market presence or are unable to differentiate ourselves from our competitors in our selected industry sectors, or regions, or if our strategy fails to achieve its intended results, we may not be able to compete successfully against other companies with global operations or niche-market competitors.

Other competitive factors that could adversely impact our operations and profitability include the following:

| • | the relative degree of leverage and cost of capital among third-party logistics suppliers can be a significant competitive factor, and any increase in either our debt or equity cost of capital as a result of increased borrowing, stock price volatility or our ability to raise capital in support of future growth or acquisitions could have a significant impact on our competitive position; |

| • | some companies hire lead logistics providers to manage their logistics operations, and these lead logistics providers may hire logistics providers on a non-neutral basis which may reduce the number of business opportunities available to us; and |

| • | many customers periodically accept bids from multiple providers for their logistics service needs, and this process may result in the loss of some of our business to competitors and in price reductions. |

Our profitability could be negatively impacted by downward pricing pressure from certain of our customers.

Given the nature of our services and the competitive environment in which we operate, our largest customers exert downward pricing pressure and often require modifications to our standard commercial terms. Due to their size and market concentration, some of our customers utilize competitive bidding procedures involving bids from a number of competitors or otherwise exert pressure on our prices and margins. Likewise, such customers’ increased bargaining power could have a negative effect on the non-monetary terms of our customer contracts, for example, in relation to the allocation of risk or the terms of payment. While we believe our ongoing cost reduction initiatives have helped mitigate the effect of price reduction pressures from our customers, there is no assurance that we will be able to maintain or improve our current levels of profitability.

Under most of our contractual arrangements with our customers, all or a portion of our pricing is based on certain assumptions regarding the scope of services, production volumes, operational efficiencies, the mix of fixed versus variable costs, productivity and other factors. If, as a result of subsequent changes in our customers’ business needs or market forces that are outside of our control, these assumptions prove to be invalid, we could have lower margins than anticipated or our contracts could prove unprofitable. Although certain of our contracts provide for renegotiation upon a material change, there is no assurance that we will be successful in obtaining the necessary price adjustments.

If our customers are able to reduce their total cost structure regarding their employees that provide internal logistics and transportation services, our business and results of operations may be harmed.

A major driver for our customers to use third-party logistics providers instead of their own personnel is their inherent high cost of labor. Third-party logistics service providers such as ourselves are generally able to provide such services more efficiently than otherwise could be provided “in-house” primarily as a result of our lower and more flexible employee cost structure. Historically, this has been the case in the U.S. automotive industry. If, however, the U.S. automotive industry, which has received concessions from the United Auto Worker and other unions, or any other industry we serve, is able to renegotiate the terms of its labor contracts or otherwise reduce its total cost structure regarding its employees, or if it has to make concessions as a result of pressure from the unions with which it deals, we may not be able to provide our customers with an attractive alternative for their logistics needs and our business and results of operations may be harmed.

13

Table of Contents

We face a variety of risks relating to our material handling services.

For certain value-added material handling services, we lease warehouses and distribution facilities on a long-term basis. In one situation, we also assumed employment arrangements from a customer. Such actions may require substantial investments in property, plant and equipment, personnel and management capacity. If we acquire or take over existing facilities of a customer or a competing provider, we may in some jurisdictions assume by operation of law all rights and obligations arising under the existing employment relationships between our customer or the competing provider and the employees employed at such facilities. This may result in additional costs and obligations to be incurred by us, such as wages and employee benefits, which may include severance or other employment-related obligations.

We commit facilities, labor and equipment on the basis of projections of future demand, and our projections may prove inaccurate as a result of changes to economic conditions or a decision by our customers to terminate or not to renew their contracts with us. We generally strive to minimize these risks for our dedicated warehouses and other assets by negotiating coterminous lease agreements, which have the same duration as that of the assets deployed to service the contract. Where we take assignment of existing employment relationships, we typically seek indemnities for employee service liabilities from the previous employer. Our revenue, cash flows and results of operations may be adversely affected if we are unable to secure terms coterminous with our customer commitments or be indemnified for employee service liabilities. This could result in an impairment of goodwill or other assets and adversely affect our cash flow.

Under some of our third-party logistics agreements, we have agreed to reduce our prices over time in accordance with anticipated cost savings and efficiency improvements. If we are compelled to perform our contractual obligations on unfavorable terms (including when such anticipated cost savings and improvements are not realized) our results of operations could be adversely affected.

Our customers may terminate contracts before completion or choose not to renew contracts, which could adversely affect our business and reduce our revenue.

The terms of our customer contracts, particularly for value-added services, often range up to five years. Many of our customer contracts may be terminated by our customers with or without cause, with one to six months’ notice and in most cases without significant penalty. The termination of a substantial percentage of these contracts could adversely affect our business and reduce our revenue. Contracts representing approximately 18.4% of our revenue in the fiscal year ended December 31, 2009, will expire on or before December 31, 2010. Failure to meet contractual or performance requirements could result in cancellation or non-renewal of a contract. In addition, a contract termination or significant reduction in work assigned to us by a major customer could cause us to experience a higher than expected number of unassigned employees or other underutilized resources, which would reduce our operating margin until we are able to reduce or reallocate our headcount or other overcapacity. We may not be able to replace any customer that elects to terminate or not renew its contract with us, which would adversely affect our business and revenues.

Our business is highly dependent on dynamic information technology.

The provision and application of information technology is an important competitive factor in the logistics industry. Among other things, our information systems must frequently interact with those of our customers and transportation providers. Our future success will depend on our ability to employ logistics software that meets industry standards and customer demands. Although there are redundancy systems and procedures in place, the failure of the hardware or software that supports our information technology systems could significantly disrupt client workflows and cause economic losses for which we could be held liable and which would damage our reputation.

14

Table of Contents

We expect customers to continue to demand more sophisticated and fully integrated information technology systems from their logistics providers, which are compatible with their own information technology environment. In addition, our competitors may have or develop information technology systems that permit them to be more cost effective and otherwise better situated to meet customer demands than we are able to develop. Larger competitors may be able to develop or license information technology systems more cost effectively than we can by spreading the cost across a larger customer base, and competitors with greater financial resources may be able to develop or purchase information technology systems that we cannot afford. If we fail to meet the demands of our customers or protect against disruptions of both our and our customers’ operations, we may lose customers, which could seriously harm our business and adversely affect our operating results and operating cash flow.

We license a variety of software that is used in our information technology system. As a result, the success and functionality of our information technology is dependent upon our ability to continue to license the software platforms upon which it is built. There can be no assurances that we will be able to maintain these licenses or replace the functionality provided by this software on commercially reasonable terms or at all. Additionally, while we are not aware of any infringement and we believe that we have all necessary licenses to implement our system, we could be subject to claims of infringement in the future. The failure to maintain these licenses or any significant delay in the replacement of, or interference in, our use of this software or any claims of infringement, even those without merit, could have a material adverse effect on our business, financial condition and results of operations.

A significant labor dispute involving us or one or more of our customers, or that could otherwise affect our operations, could reduce our revenues and harm our profitability.

More than one-half of our employees and a substantial number of the employees of our largest customers are members of industrial trade unions and are employed under the terms of collective bargaining agreements. Each of our unionized facilities has a separate agreement with the union that represents the workers at only that facility, with each such agreement having an expiration date that is independent of other collective bargaining agreements. Labor disputes involving either us or our customers could affect our operations. For example, in February 2008, in connection with their contract renegotiation with American Axle, the UAW initiated a strike that lasted 84 days significantly impacting General Motors. If the UAW and our customers are unable to negotiate new contracts and our customers’ plants experience slowdowns or closures as a result, our revenue and profitability could be negatively impacted. A labor dispute involving another supplier to our customers that results in a slowdown or closure of our customers’ plants to which we provide services could also have a material adverse effect on our business. Significant increases in labor costs as a result of the renegotiation of collective bargaining agreements could also be harmful to our business and our profitability.

In addition, strikes, work stoppages and slowdowns by our employees may affect our ability to meet our customers’ needs, and customers may do more business with competitors if they believe that such actions may adversely affect our ability to provide service. We may face permanent loss of customers if we are unable to provide uninterrupted service. The terms of future collective bargaining agreements also may affect our competitive position and results of operations.

If we are unable to enter new business industries or segments successfully, our future growth prospects could suffer.

Our growth strategy requires us to enter into geographic or business markets in which we have little or no prior experience. In addition to the risks inherent in entering new markets or lines of business, our success in entering such new markets or businesses may be dependent on our ability to create new and appropriate business models. There can be no assurance that we will be able to develop successful business models that can adapt to new lines of businesses in which we have little or no experience.

15

Table of Contents

Our operations in Canada and Mexico make us vulnerable to risks associated with doing business in foreign countries.

As a result of our operations in Canada and Mexico, an increasing portion of our revenue and expenses are expected to be denominated in currencies other than U.S. dollars. International operations are subject to certain risks inherent in doing business abroad, including:

| • | exposure to local economic and political conditions; |

| • | foreign exchange rate fluctuations and currency controls; |

| • | withholding and other taxes on remittances and other payments by subsidiaries; |

| • | investment restrictions or requirements; and |

| • | export and import restrictions. |

Expanding our business in Canada and Mexico, and developing our business relationships with manufacturers in such jurisdictions are important elements of our strategy. As a result, our exposure to the risks described above may be greater in the future. The likelihood of such risks and their potential effect on us may vary from country to country and are unpredictable. However, any such occurrences could be harmful to our business and our profitability, thereby resulting in a decline in the value of our common stock.

We may not be able to execute our acquisition strategy successfully, which could cause our business and future growth prospects to suffer.

One component of our growth strategy is to pursue strategic acquisitions of third-party providers of logistics services, freight brokers and related transportation companies that meet our acquisition criteria. However, this is a new strategy and we have not successfully completed acquisitions in the past, and suitable acquisition candidates may not be available on terms and conditions we find acceptable. In pursuing acquisitions, we compete with other companies, many of which have greater financial resources than we do. If we are unable to secure sufficient funding for potential acquisitions, we may not be able to complete strategic acquisitions that we otherwise find desirable. Further, if we succeed in consummating strategic acquisitions, our business, financial condition and results of operations may be negatively affected because:

| • | the acquired businesses may not achieve anticipated revenue, earnings or cash flows; |

| • | we may assume liabilities that were not disclosed to us or exceed our estimates; |

| • | we may be unable to integrate acquired businesses successfully and realize anticipated economic, operational, and other benefits in a timely manner, which could result in substantial costs and delays or other operational, technical or financial problems; |

| • | acquisitions could disrupt our ongoing business, distract our management and divert our resources; |

| • | we may experience difficulties operating in markets in which we have had little or no direct experience; |

| • | we may lose the customers, suppliers, other commercial partners, key employees and owner-operators of the acquired company; |

| • | we may finance future acquisitions by issuing common stock for some or all of the purchase price, which could dilute the ownership interests of our shareholders; or |

| • | we may incur additional debt related to future acquisitions. |

If we are unable to retain our executive officers, our business and results of operations could be harmed.

We are highly dependent upon the services of our employees. We do not maintain key-man life insurance on any of our executive officers. The loss of the services of any of our executive officers could adversely affect our

16

Table of Contents

operations and future profitability. We also need to continue to develop and retain a core group of managers if we are to realize our goal of expanding our operations and continuing our growth. The market for qualified employees can be highly competitive, and we cannot assure you that we will be able to attract and retain the services of qualified executives, managers or other employees.

A claim in excess of our insurance limits could adversely affect our financial condition.

Except in certain cases in connection with specific customer requirements, we self-insure for potential auto and general liability claims in excess of $1.0 million, as well as all motor cargo liability and material handling claims. One or more significant claims, our failure to reserve adequately for such claims and/or the cost of maintaining our insurance could adversely affect our financial condition and results of operations in the future.

We maintain insurance with a licensed insurance carrier related party against the first $1.0 million of liability for individual auto liability and general liability claims. We self-insure for all amounts over $1.0 million related to auto and general liability claims. In addition, we self-insure for the risk of motor cargo liability claims from our trucking operations and material handling claims for certain of our warehouse operations. In addition, we are responsible for all of the legal expenses related to all claims, or the portion of claims, that we self-insure. We do establish financial reserves for anticipated uninsured losses and these reserves are periodically evaluated and adjusted to reflect our experience.

A portion of our total operating revenue is generated from truckload operations, and vehicle accidents in such business may result in property damage or significant bodily injury or wrongful death to claimants. Accordingly, we maintain, and expect to continue to maintain, financial reserves for open claims that could exceed the $1.0 million policy limits, as well as estimated liability for open motor cargo liability and material handling claims. If we experience claims that are not covered by our insurance or that exceed our insurance limits or reserves, or if we experience claims for which coverage is not provided, it would increase the volatility of our earnings and adversely affect our financial condition and results of operations.

In June 2006, one of our subsidiaries was involved in an automobile accident in Missouri resulting in four fatalities and injuries to several others. Multiple lawsuits were filed. As of December 31, 2008, all of the lawsuits except one had been settled and paid. Our share of the resolved claims was approximately $8.0 million. We maintain a reserve for our estimated loss in the unresolved case. If the damages resulting from that case exceed our reserve, our results of operation could be materially adversely affected.

As a result of increased premiums, we expect our insurance and claims expense to increase over historical levels, even if we do not experience an increase in the number of accident claims. Insurance carriers have significantly raised premiums for many businesses, including logistics services companies. If this continues, the cost of maintaining our insurance would increase. In addition, if we decide to increase our purchased insurance limits in the future, our costs would be expected to increase.

Owner-operators provide the equipment for a substantial portion of our transportation services to our customers, and reductions in the pool of available driver candidates could limit our growth.

A substantial portion of the transportation services that we provide as part of our logistics services are carried out by owner-operators who are generally responsible for paying for their own equipment, fuel and other operating costs. In addition, our owner-operators provide a substantial portion of the tractors used in our business. The following factors recently have combined to create a difficult operating environment for owner-operators:

| • | increases in the prices of new tractors; |

| • | a tightening of financing sources available to owner-operators for the acquisition of equipment; |

| • | increased maintenance expense due to aging equipment; |

17

Table of Contents

| • | high fuel prices; and |

| • | increases in insurance costs. |

In recent years, these factors have caused many owner-operators to join company-owned fleets or to exit the industry entirely. As a result of a smaller available pool of qualified owner-operators, the already strong competition among transportation service providers for their services has intensified. Due to the difficult operating environment and intense competition, turnover among owner-operators in the transportation industry is high. For the twelve months ended April 3, 2010, our owner-operator turnover rate was approximately 46.7%. Additionally, our agreements with our owner-operators are terminable by either party upon short notice and without penalty. Consequently, we regularly need to recruit qualified owner-operators to replace those who have left our fleet. If we are unable to retain our existing owner-operators or recruit new owner-operators, we may have to operate with fewer trucks and may have difficulty meeting customer demands, all of which would adversely affect our growth and profitability.

In the event that the current operating environment for owner-operators worsens, we may be required to adjust our owner-operator compensation package or, alternatively, to acquire more of our own revenue equipment and seat it with employee drivers in order to maintain or increase the size of our fleet. The adoption of either of these measures could materially and adversely affect our financial condition and results of operations. If we are required to increase the compensation of owner-operators, our results of operations would be adversely affected to the extent increased expenses are not recouped under our contracts with our customers. If we elect to purchase more of our own tractors and hire additional employee drivers, our capital expenditures would increase, we would incur additional employee benefits costs and depreciation, interest, and/or equipment rental expenses and our financial return on our assets would decline.

A determination by regulators that owner-operators are employees, rather than independent contractors, could expose us to various liabilities and additional costs.

Tax and other regulatory authorities have sometimes sought to assert that independent contractors in the transportation service industry, such as our owner-operators, are employees rather than independent contractors. There can be no assurance that these interpretations and tax laws that consider these persons independent contractors will not change or that these authorities will not successfully assert this position. If our owner-operators are determined to be our employees, that determination could materially increase our exposure under a variety of federal and state tax, workers’ compensation, unemployment benefits, labor, employment and tort laws, as well as our potential liability for employee benefits. In addition, such changes may be applied retroactively, and if so, we may be required to pay additional amounts to compensate for prior periods. Any of the above increased costs would adversely affect our business and operating results.

Difficulty in attracting and retaining drivers could affect our profitability and our ability to grow.

The trucking and transportation industries periodically experience difficulty in attracting and recruiting qualified drivers, including owner-operators, resulting in intense competition and increased wages for drivers. We have, from time to time, experienced under-utilization and increased expenses due to a shortage of qualified drivers and turnover of owner-operators. If we are unable to continue to attract drivers or contract with owner-operators, we could be required to increase our driver compensation package or under-utilize our vehicles, which could adversely affect our profitability and prospects for future growth.

Our business is subject to general economic and business factors that are largely out of our control, any of which could adversely affect our operating results.

Our business is dependent upon a number of general economic and business factors that may adversely affect our results of operations. Many of these are beyond our control, including fuel prices, new equipment

18

Table of Contents

prices and used equipment values, interest rates, taxes, tolls, license and registration fees and changes in regulatory requirements, all of which could increase our costs, particularly in the industry sectors and regions in which we operate.

We also are affected by recessionary economic cycles and downturns in customers’ business cycles, particularly in the industries where we have a significant concentration of customers, such as the automotive industry. Economic conditions may adversely affect our customers, their need for our services or their ability to pay for our services. Adverse changes in any of these factors could adversely affect our business and results of operations.

Further deterioration in the United States and world economies could exacerbate the difficulties experienced by our customers and suppliers in obtaining financing, which, in turn, could materially and adversely impact our business, financial condition, results of operations and cash flows.

Lending institutions have suffered and may continue to suffer losses due to their lending and other financial relationships, especially because of the general weakening of the global economy and the increased financial instability of many borrowers. Longer-term disruptions in the credit markets could further adversely affect our customers by making it increasingly difficult for them to obtain financing for their businesses. In particular, our automotive industry customers, who typically have related finance companies that provide financing to their dealers and customers, depend on securitization markets that have experienced severe disruptions during the global economic crisis and may face future disruptions. If capital is not available to our customers, or if its cost is prohibitively high, their businesses would be negatively impacted, which could result in their restructuring or even reorganization/liquidation under applicable bankruptcy laws. Any such negative impact, in turn, could materially and negatively affect our revenues and results.

Financial difficulties experienced by any major customer could have a material adverse impact on us if the customer were unable to pay for the services we provide or we experienced a loss of, or material reduction in, business from the customer. As a result of those difficulties, we could experience lost revenues, significant write-offs of accounts receivable, and significant impairment charges.

The profitability of our transportation services may be adversely affected by increased diesel fuel and energy prices.