Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - China Nutrifruit Group LTD | exhibit21.htm |

| EX-23.1 - EXHIBIT 23.1 - China Nutrifruit Group LTD | exhibit23-1.htm |

| EX-32.2 - EXHIBIT 32.2 - China Nutrifruit Group LTD | exhibit32-2.htm |

| EX-31.2 - EXHIBIT 31.2 - China Nutrifruit Group LTD | exhibit31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - China Nutrifruit Group LTD | exhibit31-1.htm |

| EX-32.1 - EXHIBIT 32.1 - China Nutrifruit Group LTD | exhibit32-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO

SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: March 31, 2010

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________to _____________

Commission File No. 001-34440

CHINA NUTRIFRUIT GROUP LIMITED

---------------------------------------------------------------------------------------------------------------------------------------

(Exact name of registrant as specified in its charter)

| Nevada | 87-0395695 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

5th Floor, Chuangye Building, Chuangye Plaza

Industrial Zone 3, Daqing Hi-Tech Industrial Development Zone

Daqing, Heilongjiang China 163316

(Address of principal executive

offices)

(86) 459-8972870

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

| Title of each class | Name of each exchange on which registered |

| Common Stock, par value $0.001 per share | NYSE Amex LLC |

Securities registered pursuant to Section 12(g) of the Exchange Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

oIndicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer o | Accelerated Filer o |

| Non-Accelerated Filer (Do not check if a smaller reporting company) o | Smaller reporting company x |

Indicate by check mark whether registrant is a shell company (as

defined in Rule 12b-2 of the Act).

Yes o No x

As of September 30, 2009 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of the shares of the registrant’s common stock held by non-affiliates (based upon the closing price of such shares as reported on the NYSE AMEX) was approximately $20.3 million. Shares of the registrant’s common stock held by each executive officer and director and each by each person who owns 10% or more of the outstanding common stock have been excluded from the calculation in that such persons may be deemed to be affiliates of the registrant. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

There were a total of 36,718,772 shares of the registrant’s common stock outstanding as of June 25, 2010.

DOCUMENTS INCORPORATED BY REFERENCE

None.

| CHINA NUTRIFRUIT GROUP LIMITED | ||

| Annual Report on FORM 10-K | ||

| For the Fiscal Year Ended March 31, 2010 | ||

| TABLE OF CONTENTS | ||

| PART I | ||

| Item 1. | Business. | 1 |

| Item 1A. | Risk Factors. | 13 |

| Item 1B. | Unresolved Staff Comments. | 13 |

| Item 2. | Properties. | 25 |

| Item 3. | Legal Proceedings | 25 |

| Item 4. | (Removed and Reserved) | 25 |

| PART II | ||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity | |

| Securities | 25 | |

| Item 6. | Selected Financial Data | 26 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 27 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk. | 36 |

| Item 8. | Financial Statements and Supplementary Data | 36 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure. | 36 |

| Item 9A. | Controls and Procedures. | 36 |

| Item 9B. | Other Information. | 37 |

| PART III | ||

| Item 10. | Directors, Executive Officers and Corporate Governance | 37 |

| Item 11. | Executive Compensation. | 41 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. | 42 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 42 |

| Item 14. | Principal Accounting Fees and Services | 44 |

| PART IV | ||

| Item 15. | Exhibits, Financial Statement Schedules. | 45 |

Special Note Regarding Forward Looking Statements

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Such statements include, among others, those concerning our expected financial performance; strategic and operational plans; management forecast; economies of scales; litigation; potential and contingent liabilities; management’s plans; taxes; as well as all assumptions, expectations, predictions, intentions or beliefs about future events. You are cautioned that any such forward-looking statements are not guarantees of future performance and that a number of risks and uncertainties could cause actual results of the Company to differ materially from those anticipated, expressed or implied in the forward-looking statements. The words “believe,” “expect,” “anticipate,” “project,” “targets,” “optimistic,” “intend,” “aim,” “will” or similar expressions are intended to identify forward-looking statements. All statements other than statements of historical fact are statements that could be deemed forward-looking statements. Risks and uncertainties that could cause actual results to differ materially from those anticipated include risks related to our views on the growth of the fruit industry, particularly the specialty fruit industry; general economic conditions, our ability to overcome competition in the Chinese fruit processing market; the impact that a downturn or negative changes in the industries in which our products are sold could have on our business and profitability; any decrease in the availability, or increase in the cost, of raw materials and energy; our ability to simultaneously fund the implementation of our business plan and invest in new projects; economic, political, regulatory, legal and foreign exchange risks associated with international expansion; loss of key members of our senior management; and unexpected changes to China’s political or economic situation and legal environment. Additional disclosures regarding factors that could cause our results and performance to differ from results or performance anticipated by this Report are discussed in Item 1A. “Risk Factors.”

Readers are urged to carefully review and consider the various disclosures made by us in this Report and our other filings with the SEC. These reports attempt to advise interested parties of the risks and factors that may affect our business, financial condition and results of operations and prospects. The forward-looking statements made in this Report speak only as of the date hereof and we disclaim any obligation to provide updates, revisions or amendments to any forward-looking statements to reflect changes in our expectations or future events.

Use of Terms

Except as otherwise indicated by the context, all references in this report to: (i) “we,” “the Company,” “us,” “our company,” “our,” and “China Nutrifruit” are to the combined businesses of China Nutrifruit Group Limited and its consolidated subsidiaries; (ii) “Fezdale” are to Fezdale Investments Limited, a British Virgin Islands corporation, our direct, wholly-owned subsidiary; (iii) “Solar Sun” are to Solar Sun Holdings Limited, a Hong Kong corporation, our indirect, wholly-owned subsidiary; (iv) “Jumbo Gloss” are to Jumbo Gloss Limited, a British Virgin Islands corporation, our direct wholly-owned subsidiary; (v) “Longheda” are to Daqing Longheda Food Company Limited, a Chinese corporation, our indirect, wholly-owned subsidiary; (vi) “Securities Act” are to the Securities Act of 1933, as amended; (vii) “Exchange Act” are to the Securities Exchange Act of 1934, as amended; (viii) “RMB” are to Renminbi, the legal currency of China; (ix) “U.S. dollar,” “$” and “US$” are to the legal currency of the United States; (x) “China,” “Chinese” and “PRC” are to the People’s Republic of China; and (xi) “BVI” are to the British Virgin Islands.

PART I

ITEM 1.

BUSINESS.

Business Overview

We are a holding company and conduct all our operations through our indirect, wholly-owned subsidiary, Longheda, which is a leading producer of premium specialty fruit-based products in China. We develop, process, market and distribute a variety of food products processed primarily from premium specialty fruits grown in Northeast China, including golden berries, crab apple, blueberries and raspberries. Our products include fruit concentrate, nectar, and glazed fruits as well as fresh fruits.

We sell our products through an extensive nationwide sales and distribution network covering 20 provinces and 47 cities in China. As of March 31, 2010, this network was comprised of 75 distributors. Our processed fruit products are mainly sold to food producers for further processing into fruit juice and other fruit related foods, and our fresh fruits are mainly sold to fruit supermarkets.

1

Our manufacturing facility is located in Daqing City and Mu Dan Jiang City, Heilongjiang Province, China where abundant supply of various premium specialty fruits is readily available. We have five fruit processing lines with an aggregate capacity of 17,160 tons.

Our sales revenue grew by 29.2% in the fiscal year ended March 31, 2010 to $72.9 million from $56.4 million in the fiscal year ended March 31, 2009. Net income increase by 326.1% in the fiscal year ended March 31, 2010 to $19.3 million from $4.1 million in the fiscal year ended March 31, 2009. Our gross margin for the fiscal year ended March 31, 2010 was 45.6% .

Corporate History and Structure

We are a Nevada holding company and conduct substantially all of our business in China through our operating subsidiary, Longheda. We indirectly own all of the equity in Longheda as a result of our 100% ownership of Fezdale and Fezdale’s intermediate ownership of Solar Sun. Both Fezdale and Solar Sun are intermediate holding companies and have no other significant assets and operations. Longheda was incorporated in China in 2004. Subsequently, in a series of transactions between 2007 and 2008, Solar Sun acquired 100% ownership of Longheda. Jumbo Gloss is a private limited liability company that was established on October 13, 2009 under the laws of the British Virgin Islands. As of the date of this Report, Jumbo Gloss has no business operations.

The following chart reflects our organizational structure as of the date of this report.

We were originally incorporated in the State of Utah on April 22, 1983 under the name Portofino Investment, Inc. In January 1984, we changed our name to Fashion Tech International, Inc. In April 1999, our stockholders approved a merger with Fashion Tech International, Inc., a Nevada corporation, to change the domicile of the Company from Utah to Nevada.

2

We were a developmental-stage company from inception to January 1, 1984, when we became the holding company of certain operating or development-stage subsidiaries. From April 1, 1985 to August 14, 2008, we re-entered development-stage status.

On August 14, 2008, we acquired Fezdale in a reverse acquisition transaction, which involved a financing transaction and a related share exchange transaction whereby all of our current business operations were acquired by Fezdale. In the share exchange transaction, 100% of the issued and outstanding shares of Fezdale were exchanged for 30,166,878 shares of our common stock, thereby making the existing stockholders of Fezdale owners of 83.5% of our stock and also making Fezdale our wholly owned subsidiary. In the related financing transaction, we completed a private placement in which we sold 3,085,840 newly issued shares of our common stock for $8.58 million.

Our Industry

According to a report on China’s fruit processing industry issued by Beijing Business & Intelligence Consulting Co. Ltd. (“BBIC,” and such report is hereinafter referred to as the “BBIC Report”), an independent market research firm, China’s fruit processing industry has grown significantly in the past several years. The total output of processed fruit products in China grew from $16.8 billion in 2005 to $49.7 billion in 2009, representing a compound annual growth rate (“CAGR”) of 31.15% . The sales value of processed fruit products in China grew from $17.0 billion in 2005 to $47.0 billion in 2009, representing a CAGR of 28.95% . The following table sets forth the output and CAGR of four categories of processed fruit products.

Output Value Breakdown of Fruit Processing Industry in

China

(in Billions of U.S.$, except for CAGR data)

| 2005 | 2006 | 2007 | 2008 | 2009 | CAGR | |

| Canned Fruit | 3.0 | 3.7 | 4.3 | 6.3 | 7.8 | 26.98% |

| Deep Processed Fruit* | 9.7 | 13.1 | 16.1 | 23.6 | 29.1 | 31.61% |

| Fruit Juice and Beverage | 3.3 | 4.4 | 5.7 | 7.6 | 10.2 | 32.59% |

| Glazed Fruits | 0.7 | 1.0 | 1.4 | 2.0 | 2.6 | 38.83% |

| * Deep processed fruits include nectar, dried fruit and fruit wine, etc. | ||||||

Source: 2006-2009 Fruit processing industry research report, Beijing Business & Intelligence Consulting Co. Ltd.

BBIC projected that the total sales value of processed fruit products in China will reach $68.7 billion in 2012 which equates to growth of 46.2% during the four-year period from 2009 to 2012. The table below sets forth the sales of fruit processing industry in China from 2005 to 2009 and estimated sales of fruit processing industry in China from 2010 to 2012.

Sales and Estimated Sales of Fruit Processing Industry in China, 2005-2012

| (in Billions of U.S. $) | 2005 | 2006 | 2007 | 2008 | 2009 | 2010E | 2011E | 2012E |

| Sales | 16.0 | 21.0 | 26.1 | 37.9 | 47.0 | 53.2 | 61.0 | 68.7 |

| Source: 2006-2009 Fruit processing industry research report, Beijing Business & Intelligence Consulting Co. Ltd. | ||||||||

We anticipate that growth in China’s fruit processing industry, especially, the premium specialty fruit-based products, will mainly be driven by the following factors:

The low per capita rate of fruit consumption in China. With approximately a quarter of the world’s population, China represents a key growth driver for the global fruit food market. Even though China is the largest producer of apples, third largest producer of oranges, and one of the top producers of pears and peaches in the world, per capita fruit juice consumption in China is currently well below that of major developed countries according to Euromonitor.

Growing affluence fosters increased consummation of processed fruit products. China’s economy has grown significantly in recent years. According to the National Bureau of Statistics of China (the “NBS”), China’s gross domestic product (“GDP”) has increased from RMB12.0 trillion ($1.6 trillion) in 2002 to RMB33.5 trillion ($4.9 trillion) in 2007. According to a report issued by the World Bank in March 2010, it is estimated that China’s GDP will grow at an annual growth rate of 9.5% in 2010. China’s economic growth has resulted in a significant increase in household disposable income in China. According to the NBS, between 2002 and 2009, urban household disposable income per capita increased from RMB7,703 ($1,055) to RMB17,175 ($2,512), or a CAGR of 12.1%, and rural per capita cash income increased from RMB2,476 ($339) to RMB5,153 ($754), or a CAGR of 11.0% . We believe that as GDP and disposable income increase, processed fruit products will become more affordable and consumers will generally spend an increasing portion of their disposable income on healthy nutritional products, such as our premium specialty fruit-based products.

3

Greater health awareness is expected to affect consumption of fruit and processed fruit products. We believe that improved living standards and growing household disposable income have led to greater health awareness among the population. As people become more affluent, we believe that their spending on quality health food and nutritional products, like our products, will increase. The juice beverage market in China continued growing steadily in 2009 as the growth in urban population and disposable income continued to drive demand for natural and healthy beverage products. According to the BBIC Report, the world fruit juice consumption is expected to increase from 33 billion liters in 1997 to 74 billion liter in 2020.

Government aims to promote the growth of China’s fruit processing industry. According to the BBIC Report, approximately 20-30% of fruit grown in China is lost, less than 50% of the total harvested fruit can be commercialized, and less than 10% of the total commercialized fruit is processed. We believe that the Chinese government will promote the development of the fruit and fruit processing industry, as evidenced by the “Development Program of Food Processing Industry 2006-2010” report issued by the PRC Ministry of Agriculture (“MOA”). The MOA aims to increase the fruit processing ratio to 10%-15% and the fruit commercialization ratio to above 60%, and to reduce the lost fruit ratio to 10%-15% by 2010. We believe the government’s five year plan will further facilitate the growth of the fruit processing industry in China.

Our Products

Our primary product offering includes fruit concentrate, nectar, glazed fruits and beverages as well as fresh fruits. We are also in the process of developing several new products.

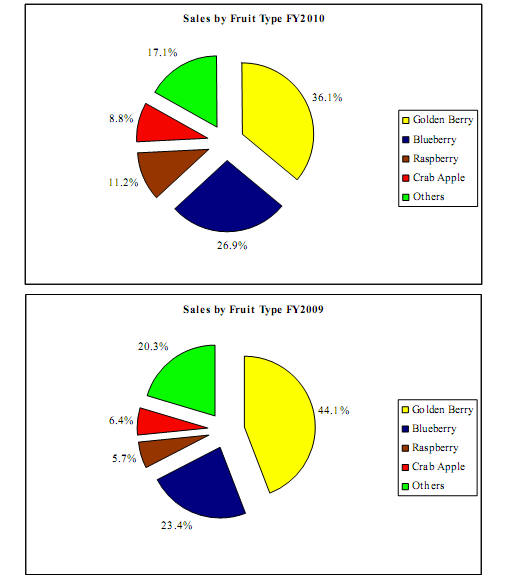

The following charts set forth our products categorized by both products and source fruits type in terms of revenue for the fiscal years 2010 and 2009:

Product Mix – By Product

4

Product Mix – By Fruit Type

5

Fruit Concentrate

Fruit concentrate is our primary product line, accounting for approximately 47.5% and 51.2% of our total revenue in fiscal years 2010 and 2009, respectively. We currently produce four types of fruit concentrate: golden berry, crab apple, blueberry and raspberry. We currently have two concentrate production lines which are allocated for the production of all of four types of concentrates with an annual total production capacity of 9,960 tons. We plan to continue to focus on fruit concentrate which is our fastest growing product line with greatest market demand. To achieve this end, we plan to add one more fruit concentrate juice production line with a production capacity of 6,000 tons in fiscal year 2011.

Among the four types of concentrate, raspberry concentrate has the highest gross margin and crab apple concentrate occupies most of our production capacity even though it has a lower gross margin. We produce more crab apple concentrate despite its relatively lower gross margin mainly because of the high demand for crab apple products and abundant supply of fresh crab apples which has the largest supply in Northeast China as compared to the other three source fruits.

Crab apple is a special species of apple which has much higher acidity than normal species of apple. The apple concentrate produced in China commonly has an acidity of 1.2 to 1.8 while crab apple concentrate typically has acidity over 3.2. The only way to raise the acidity of apple concentrate is to mix it with another apple concentrate with higher acidity. Since the apple concentrates that are exported from China to overseas market are usually required to have an acidity of no less 2.0, the local producers of apple concentrate need large quantity of high acidity apple concentrate to add to its low acidity apple concentrate. Therefore, crab apple concentrate is in high demand in the market.

Nectar

Our nectar product line accounted for approximately 9.5% and 13.2% to our total revenue in fiscal years 2010 and 2009, respectively. Nectar is an unfermented and unconcentrated pulp product. To produce nectar, fresh fruits are crushed and then instantaneously sterilized under high temperature without adding any additives other than citric acid. It preserves the nutrition and flavor of the fresh fruit to the greatest extent and has a long shelf life. Nectar is easy to store and transport, and thus providing the producers of fresh fruit based products a much better alternative material than fresh fruit.

We currently produce and sell nectar products using only golden berries. Our nectar products are commonly re-processed into a wide variety of products, including fruit concentrate, fruit ice cream, nectar beverage, biscuits, fruit jam and fruit yogurt. Our nectar products were certified as green food by China Green Food Development Center in May 2006.

Glazed Fruits

Our glazed fruits product line accounted for approximately 22.8% and 10.9% to our total revenue in fiscal years 2010 and 2009, respectively. Glazed fruit is preserved fruit with high sugar content and is a popular, traditional Chinese food. Glazed fruits have a long shelf life and are commonly consumed as snacks.

We currently produce and sell our glazed fruits products using golden berries and blueberries. We launched our glazed blueberry products in the second quarter of fiscal year 2010 which were well received by our customers. In December 2009, we added a new glazed fruits production line with an annual production capacity of 1,200 tons in our Daqing factory which increased our total annual production capacity of glazed fruit products to 2,400 tons. Our glazed fruits are mainly sold as a premium snack. Due to the special taste of our golden berries and blueberries, our products are also commonly used in a wide variety of foods such as baked foods. Our glazed golden berry fruit products were certified as green food by China Green Food Development Center in May 2006.

Fresh Fruit

Sales from fresh golden berries accounted for approximately 3.0% and 4.3% to our total revenue in fiscal years 2010 and 2009, respectively. We sell fresh golden berries to our distributors during the picking season which is typically mid July to mid November every year. We purchase fresh golden berries from local farmers in Heilongjiang province and sort them into different grades. Only the top-grade golden berries that are freshest and have the best color, shape and aroma are sold as fresh fruit. The rest of the fresh golden berries are further processed into glazed fruits, nectar or concentrate.

6

Golden berries are especially difficult to preserve and usually perish within one week after harvest. To achieve longer shelf life, we keep the fresh fruit in ice houses before we pack them with preservative packing. With these measures, our products can generally remain fresh after long distance transportation and have at least one week longer of shelf life than other similar products in the market.

Beverage and others

Beverage

Beverages accounted for approximately 4.2% and 8.2% of our total revenue in fiscal years 2010 and 2009, respectively. Beverage products usually require large capital for advertising and special sales and marketing efforts. We decided to cease beverage production in March 2010 and believe that we will be more profitable by focusing on our primary high-end premium products.

Others

Since fiscal year 2008, due to demand from our distributors, we started to distribute apple concentrate pulp products and pear concentrate pulp products. These concentrate products are processed by third party vendors according to our technical requirements and standards. Sales from other products contributed approximately 12.9% and 12.2% of our total revenue in fiscal years 2010 and 2009, respectively.

New products under development

We plan to further diversify our product mix to cater to different customer tastes and preferences. We are currently developing glazed blackcurrant and seabuckthorn which are expected to be completed in fiscal year 2011.

Production

Production Facility

Our primary production facility is located in Daqing, Heilongjiang province, which started production in 2004. The facility is located on a 24,217-square-meter tract where we have land use rights until May 2055 and encompasses approximately 5,998 square meters of plant and warehouse space. We built another processing facility in Mu Dan Jiang, Helongjiang province in August 2008 where a 6,000 tons concentrate juice production line is located.

We currently own and operate five fruit processing lines with an aggregate processing capacity of 17,160 tons. The average utilization rate of our fruit processing lines was approximately 94.7% in fiscal year 2010. Since fresh fruits are difficult to preserve in the hot season, we generally keep no inventory of fresh fruits during production. We believe the current utilization rate of the fruit processing lines is the highest rate we can achieve while maintaining no inventory. Our production is mainly conducted from mid July to mid November each year because our primary source fruits are typically harvested during that time and must be processed right away.

To meet the expected growth of our business and to broaden our product portfolio, we are currently building a new fruit and vegetable powder manufacturing facility with an expected annual production capacity of 10,000 tons in Daqing. The new facility is funded by proceeds from our preferred stock offering in 2009 and is expected to begin production in approximately September 2010. The new facility will produce tomato, pumpkin and other popular fruit and vegetable powders that can be used as ingredients in a variety of products, including baby food, ready-to-drink mixes, instant soup mixes, snacks and other confectionery items. We plan to leverage our established supplier relationship and distributor network to cross sell our new fruit and vegetable powder products.

We are also currently upgrading all fruit concentrate production lines at our facilities in Daqing and Mu Dan Jiang, which have a total fruit concentrate annual production capacity of 9,960 tons. The upgrades include purchase of additional equipments and implementation of more advanced production techniques. We expect the upgrading will result in more efficient use of raw materials and have a favorable impact on gross margin. We expect the upgrading to be completed before July 2010.

7

Production Process

The processing of our fruit concentrate, nectar and glazed fruits begins with the collection of fresh fruits from fruit farmers. Fresh fruits are first sorted and washed after arriving in our facility. Clean fresh fruits then go through the following processes to be made into different products.

-

Nectar: crush fresh fruits into tiny granules – beat crushed fruits into raw nectar – homogenize raw nectar in a blending tank – pasteurize and sterilize the raw nectar – fill aseptic bags with sterilized nectar.

-

Fruit concentrate: crush and beat fresh fruits into mashes – press fruit mashes until fruit juice comes out – mix raw fruit juice with proper amount of compound enzyme to remove pectin and starch – filter concentrate fruit juice in three-way concentrators to achieve the target content of soluble solids, acidity and other quality standards as well as no additives – fill the aseptic bags with concentrates.

-

Concentrate pulp: crush and beat fresh fruits into mashes – mix raw fruit pulp – filter concentrate pulp in three-way concentrators to achieve the target content of soluble solids, acidity and other quality standards as well as no additives – fill the aseptic bags with concentrate pulp.

-

Glazed fruits: separate fresh fruits into different grades – go through needling machine to get the fruits needled at the surface – blanch needled fruits in a blanching boiler – evacuate the air from fruits – soak evacuated fruits in sugar solution in a sugaring tank – bake sugared fruits in a group of tunnel dryers.

Quality Control

We place primary importance on quality. Our production facility has ISO 9001 and HACCP series qualifications. We have established quality control and food safety management system for the purchase of raw materials, fruit processing, packaging, storage and distribution. We have also adopted internal quality standards that we believe are stricter than the standards mandated by the PRC government. We have a 16-person quality control team to closely monitor and test the quality of our products to ensure compliance with these standards.

High quality raw materials are crucial to the production of quality fruit products. Therefore, we rigorously examine and test fresh fruits arriving at our plant. Any fruits that fail to meet our quality standard will be rejected. We perform routine product inspection and sample testing at our production facility and adhere to strict hygiene standards. For example, every employee involved in production is required to change into specially made clothes, wear working caps and shoes. No one is allowed to enter our production room unless he or she is directly involved in the production process.

All of our products undergo inspection at each stage of the production process, as well as post production inspection and final checking before distribution for sales. Products in storage or in the course of distribution are also subject to regular quality testing.

Raw Materials and Suppliers

Raw Materials

Our business depends on maintaining a regular, timely and adequate supply of high-quality fresh fruits, which accounted for approximately 74% of our cost of sales in fiscal year 2010. Our facility is strategically located in Heilongjiang province, where abundant supply of source fruits is available. The close proximity of our facility to the orchards enables us to purchase fresh fruits at a lower cost. Our other raw materials mainly include packing materials (e.g. aseptic bags) and auxiliary processing materials (e.g. sugar and additives) that are widely available.

Suppliers and Supply Arrangements

We employ different procurement strategies to support our rapid growth based on the source fruit type. We coordinate primarily with the local government for the supply of golden berries and rely on a large group of vendors for the supply of other source fruits.

8

Golden berries in Heilongjiang are mainly grown in four fruit farms. We estimate that the annual output of golden berries at these four fruit farms is approximately 100,000 tons, which accounts for approximately 50% of the total output of golden berries in Heilongjiang province. Our processing volume of golden berries (including those sold as fresh fruits) in fiscal year 2010 was approximately 33,000 tons. We currently purchase a majority of our golden berries from two of these fruit farms -- Hailun and Nehe. It is costly and inefficient to purchase fresh fruits from each individual farmer so we coordinate with the local governments which plan and coordinate the overall fruit planting activities of individual farmers.

We normally sign written agreements with the local governments of Hailun and Nehe at the beginning of each year, which generally have a one-year term. The agreement typically sets forth the total quantity of golden berries to be purchased by us and a predetermined minimum price. The local governments deliver the demand information to individual farmers and coordinate corresponding growth and harvesting activities. In the picking season, we submit our daily request of golden berries to the local governments, who then instruct the farmers to deliver fresh fruits to our plant on a timely basis. The final purchase price is based on the prevailing market price, subject to a predetermined minimum price. This arrangement cuts down our procurement costs significantly and allows the local governments to protect and maximize the interests of constituent farmers.

We purchase other source fruits, including blueberries, crab apples and raspberries, directly from vendors as there is no centralized farm base for these fruits. As an alternative, we have developed a large group of agents who purchase fruits from the local farmers and then re-sell them to us. Our sourcing staff maintains close communication with our agents to ensure their efficiency and loyalty. Our sourcing staff also spends a lot of time to keep developing new agents in the planting area of these fruits. We believe we have established an effective and loyal group of agents who are able to provide us with sufficient fresh fruits to support our growth.

Marketing, Sales and Distribution

Sales and Distribution

We currently sell our products directly to 75 regional distributors across 20 provinces and 47 cities in China who then sell the products to various customers, including food processors, supermarkets and wholesale stores. As of March 31, 2010, our sales team consisted of 18 employees. We divide the national market into six regions and assign each region a sales team. Northern China is currently our biggest market, accounting for approximately 52% of our total revenue in fiscal year 2010.

We generally require our distributors to pay the full purchase price in cash before we deliver the products. We also offer credit for our products to selected existing distributors with long-term business relationships and excellent credit records. The credit term is generally up to 45 days. We utilize different pricing policies based on the type of source fruit. For instance, the price of our golden berry products is set based on raw material costs to ensure stable profit margin. We believe that we are the largest golden berry processor in China and the only processor in Northeast China which allows us to have strong pricing power. For products based on other source fruits, we price our products at the prevailing market price.

Distributors normally have distribution rights to sell our products within a defined territory. We typically enter into a one-year contract with each of our distributors at the beginning of the year. The contract generally requires a 15-day notice of the purchase amount prior to the required delivery date. We have the right to supervise and monitor distributors’ sale of our products. We generally have a no return policy. According to our standard distribution agreement, we are liable for any loss resulted from a quality problem only if the distributor provides certification from relevant authorities. However, distributors will bear any losses caused by their negligence in the storage of the products. We offer no sales rebates or rewards to our distributors.

We believe we maintain stable relationships with our distributors, and many of them have been our distributors for more than three years. Our top ten distributors accounted for approximately 64.6% and 53.9% of our total revenue in fiscal year 2010 and 2009, respectively. The biggest distributor accounted for approximately 13.5% and 9.2% for fiscal years 2010 and 2009, respectively. In fiscal year 2010, our two biggest distributors Laiyang Yitian Fruit Juice Company Limited and Beijing Huanpenyuan Food Company Limited accounted for approximately 13.5% and 11.3% of our total revenue, respectively.

9

Marketing

As of March 31, 2010, we have seven marketing personnel in our department who are responsible for market research, promotion and advertisement. We strengthen our market presence through various types of market campaigns. We participate in several domestic and international trade fairs, such as China National Sugar and Alcoholic Commodities Fair and International China Harbin Fair for Trade and Economic Cooperation. These trade fairs help to promote our reputation and name recognition in the industry.

Our Competition

Since we process premium specialty fruits grown in Northeast China, we face little direct competition from the processors of common fruits or broad-based food processors. Our main competitors are local fruit processors that offer products similar to ours. Most of our competitors are small-sized local processors that process only one or two types of specialty fruits. Compared to these competitors, we believe we have more diversified products, higher production capacity and greater resources. Our major competitors in China include Dalian Xinlian Food Company, Shandong Longkou Fudi Food Co. Ltd., Zhalantun Changzheng Beverage Factory and Muxing Quick Frozen Food Factory.

Research and Development

Our research and development activities focus on new product development for new premium specialty fruits and quality improvement. We currently have five employees dedicated to research and development. We also cooperate with Heilongjiang Ba Yi Land Reclamation University (“HLAU”), an agriculture university in China. Since 2004, our company and HLAU have jointly developed six new products, four of which are now our principal products. On March 7, 2008, we entered into a technology cooperation agreement with HLAU to develop several new products, including glazed blueberry, blackcurrant concentrate, seabuckthorn concentrate and golden berry extracts. Under the agreement, we will provide a total amount of approximately $25,670 (RMB 180,000) to HLAU for the development of the new products and all intellectual property rights of the new products belong to our company. During the year, we have successfully developed the glazed blueberry, blackcurrant concentrate and seabuckthorn concentrate. We are currently developing glazed blackcurrant and seabuckthorn which is expected to be completed in fiscal year 2011.

Newly developed products will be put into production and commercialized when certain criteria are met, including: market demand is material, adequate supplies of raw material are secured to allow for efficient mass production, and production capacity is in place.

Intellectual Property

All of our product formulations are proprietary. We have not registered or applied for protections in China for most of our intellectual property or proprietary technologies relating to the formulations of our products. See Item 1A, “Risk Factors—Risks Related to Our Business—Our inability to protect our trademarks, patent and trade secrets may prevent us from successfully marketing our products and competing effectively.” Although we believe that, as of today, patents and copyrights have not been essential to maintaining our competitive market position, we intend to assess appropriate occasions in the future for seeking patent and copyright protections for those aspects of our business that provide significant competitive advantages.

We sell our fruit concentrate, glazed fruit and nectar products under the brand of “农珍之冠 ”. Our chairman Changjun Yu transferred the trademark for “农珍之冠 ” in both class 29 and class 32 to our company which was approved by the Trademark Office of the State of Administration for Industry and Commerce of China in March 2009. The trademark expires in 2018.

We rely on trade secret protection and confidentiality agreements to protect our proprietary information and know-how. Our management and each of our research and development personnel have entered into a standard annual employment contract, which includes a confidentiality clause and a clause acknowledging that all inventions, designs, trade secrets, works of authorship, developments and other processes generated by them on our behalf are our property, and assigning to us any ownership rights that they may claim in those works. Despite our precautions, it may be possible for third parties to obtain and use, without our consent, intellectual property that we own or are licensed to use. Unauthorized use of our intellectual property by third parties, and the expenses incurred in protecting our intellectual property rights, may adversely affect our business. See Item 1A, “Risk factors—Risks Related to Our Business—Our inability to protect our trademarks, patent and trade secrets may prevent us from successfully marketing our products and competing effectively.”

10

Regulation

Because our operating subsidiaries are located in the PRC, we are regulated by the national and local laws of the PRC. The food industry, of which fruit based products form a part, is subject to extensive regulation in China. The following paragraphs summarize the most significant PRC regulations governing our business in China.

We are also subject to the PRC’s foreign currency regulations. The PRC government has controlled Renminbi reserves primarily through direct regulation of the conversion of Renminbi into other foreign currencies. Although foreign currencies, which are required for “current account” transactions, can be bought freely at authorized PRC banks, the proper procedural requirements prescribed by PRC law must be met. At the same time, PRC companies are also required to sell their foreign exchange earnings to authorized PRC banks and the purchase of foreign currencies for capital account transactions still requires prior approval of the PRC government.

Food Hygiene and Safety Laws and Regulations

As a producer of food products in China, we are subject to a number of PRC laws and regulations governing food safety and hygiene, including:

-

the PRC Product Quality Law;

-

the PRC Food Hygiene Law;

-

the Implementation Rules on the Administration and Supervision of Quality and Safety in Food Producing and Processing Enterprises (trail implementation);

-

the Regulation on the Administration of Production Licenses for Industrial Products;

-

the General Measure on Food Quality Safety Market Access Examination;

-

the General Standards for the Labeling of Prepackaged Foods;

-

the Standardization Law;

-

the Regulation on Hygiene Administration of Food Additive;

-

the Regulation on Administration of Bar Code of Merchandise; and

-

the PRC Metrology Law.

These laws and regulations set out safety and hygiene standards and requirements for various aspects of food production, such as the use of additives, production, packaging, handling, labeling and storage, as well as facilities and equipment. Failure to comply with these laws and regulations may result in confiscation of our products and proceeds from the sales of non-compliant products, destruction of our products and inventory, fines, suspension of production and operations, product recalls, revocation of licenses, and, in extreme cases, criminal liability.

Environmental Regulations

We are subject to various governmental regulations related to environmental protection. The major environmental regulations applicable to us include:

-

the Environmental Protection Law of the PRC;

-

the Law of PRC on the Prevention and Control of Water Pollution;

-

Implementation Rules of the Law of PRC on the Prevention and Control of Water Pollution;

-

the Law of PRC on the Prevention and Control of Air Pollution;

-

Implementation Rules of the Law of PRC on the Prevention and Control of Air Pollution;

-

the Law of PRC on the Prevention and Control of Solid Waste Pollution; and

-

the Law of PRC on the Prevention and Control of Noise Pollution.

We have obtained all permits and licenses required for production of our products and believe we are in material compliance with all applicable laws and regulations.

11

Environmental Matters

Our manufacturing facilities are subject to various pollution control regulations with respect to noise, water and air pollution and the disposal of waste and hazardous materials. We are also subject to periodic inspections by local environmental protection authorities. We believe we are in material compliance with the relevant PRC environmental laws and regulations and are not currently subject to any pending actions alleging any violations of applicable PRC environmental laws.

Our Employees

As of March 31, 2010, we employed a total of 575 full-time employees. The following table sets forth the number of our employees by function.

| Department | Number of Employees | |

| Senior Management | 12 | |

| Human Resources & Administration | 63 | |

| Production | 407 | |

| Procurement | 3 | |

| Marketing | 7 | |

| Sales | 18 | |

| Logistic | 36 | |

| Research & Development | 5 | |

| Quality Control | 16 | |

| Accounting | 8 | |

| TOTAL | 575 |

Our employees are not represented by a labor organization or covered by a collective bargaining agreement. We have not experienced any work stoppages.

We are required under PRC law to make contributions to the employee benefit plans at specified percentages of the after-tax profit. In addition, we are required by the PRC law to cover employees in China with various types of social insurance. We believe that we are in material compliance with the relevant PRC laws.

Seasonality

As is typical in the fruit processing industry, we experience seasonality in our business. Our fruit processing lines are mainly carried out from mid July to mid November each year because our primary source fruits are typically harvested during that period and must be processed right away. As a result of seasonality in production, our personnel, working capital requirements, cash flow and inventories vary substantially throughout the year. In fiscal year 2010, sales during the second, third and forth fiscal quarters accounted for approximately 26.5%, 24.4% and 36.2% of our total sales revenue respectively. Generally we experience lesser sales in the first fiscal quarter because of lower demand and decreased inventory levels.

Insurance

We have property insurance for our facility located in Daqing and Mu Dan Jiang City. We believe our insurance coverage is customary and standard for companies of comparable size in comparable industries in China.

We do not have any business liability, interruption or litigation insurance coverage for our operations in China. Insurance companies in China offer limited business insurance products. While business interruption insurance is available to a limited extent in China, we have determined that the risks of interruption, cost of such insurance and the difficulties associated with acquiring such insurance on commercially reasonable terms make it impractical for us to have such insurance. Therefore, we are subject to business and product liability exposure. See Item 1A, “Risk Factors—Risks Related to Our Business—We have limited insurance coverage and do not carry any business interruption insurance, third-party liability insurance for our production facilities or insurance that covers the risk of loss of our products in shipment.”

12

Litigation

From time to time, we may become involved in various lawsuits and legal proceedings, which arise, in the ordinary course of business. However, litigation is subject to inherent uncertainties, and an adverse result in these or other matters may arise from time to time that may harm our business. We are currently not aware of any such legal proceedings or claims that we believe will have a material adverse effect on our business, financial condition or operating results.

ITEM 1A.

RISK FACTORS.

The shares of our common stock are highly speculative in nature, involve a high degree of risk and should be purchased only by persons who can afford to lose the entire amount invested in the common stock. Before purchasing any of the shares of common stock, you should carefully consider the following factors relating to our business and prospects. You should pay particular attention to the fact that we conduct all of our operations in China and are governed by a legal and regulatory environment that in some respects differs significantly from the environment that may prevail in the U.S. and other countries. If any of the following risks actually occurs, our business, financial condition or operating results will suffer, the trading price of our common stock could decline, and you may lose all or part of your investment.

RISKS RELATED TO OUR BUSINESS

The recent financial crisis could negatively affect our business, results of operations, and financial condition.

While the financial crisis has stabilized in China, the global economy remains precarious and faces many challenges, which affect our business in a variety of ways. Our ability to access the capital markets may be restricted at a time when we would like, or need, to raise capital, which could have an impact on our flexibility to react to changing economic and business conditions. In addition, these economic conditions also impact levels of consumer spending, which have recently deteriorated significantly and may remain depressed for the foreseeable future. Consumer purchases of discretionary items generally decline during recessionary periods and other periods where disposable income is adversely affected. If demand for our products fluctuates as a result of economic conditions or otherwise, our revenue and gross margin could be harmed.

Any ill effects, product liability claims, recalls, adverse publicity or negative public perception regarding particular fruits we use as raw materials, our products or our industry in general could harm our sales and cause consumers to avoid our products.

The food industry is subject to risks posed by food spoilage and contamination, product tampering, product recall, and consumer product liability claims. Our operations could be impacted by both genuine and fictitious claims regarding our and our competitors’ products. In the event of product contamination or tampering, we may need to recall some of our products. A widespread product recall could result in significant loss due to the cost of conducting a product recall including destruction of inventory and the loss of sales resulting from the unavailability of the product for a period of time.

In addition, any adverse publicity or negative public perception regarding particular fruits we use as raw materials, our products, our actions relating to our products, or our industry in general could result in a substantial drop in demand for our products. This negative public perception may include publicity regarding the safety or quality of particular fruits we use as raw materials or products in general, of other companies or of our products specifically. Negative public perception may also arise from regulatory investigations or product liability claims, regardless of whether those investigations involve us or whether any product liability claim is successful against us. We could also suffer losses from a significant product liability judgment against us. Either a significant product recall or a product liability judgment, involving either our company or our competitors, could also result in a loss of consumer confidence in our products or the food category, and an actual or perceived loss of value of our brands, materially impacting consumer demand.

Any fluctuations in raw material supply and prices may negatively impact our revenue.

A secure supply of principal raw materials is crucial to our operation. Fresh fruits accounted for approximately 74% of our cost of sales in fiscal year 2010. The per unit costs of producing our products are subject to the supply and price volatility of raw materials, especially fresh fruits which are affected by factors such as weather, growing condition and pest that are beyond our control. According to the BBIC Report, approximately 20-30% of fruit grown in China is lost. Historically, we have been able to meet our fresh fruit supply needs by building our processing facilities in close proximity to orchards and by collaborating with local government and establishing an effective group of vendors. Increases in the price of fresh fruits would negatively impact our gross margins if we are not able to offset such price increases through increases in our selling price or changes in our product mix.

13

If we cannot maintain a consistent and cost-effective supply of source fruits, our results of operations, financial condition and business prospects will deteriorate.

The availability, size, quality and cost of source fruits for the production of our products are subject to operational risks inherent to farming, such as crop size, quality, and yield fluctuation caused by poor weather and growing conditions, pest and disease problems, and other factors beyond our control. These and other operational risks could cause significant fluctuations in the availability and cost of the source fruits we use as raw materials. The prices of our fresh source fruits and other raw materials are generally determined by the market, and may change at any time. Increases in prices for any of these raw materials could have a material adverse impact on our ability to achieve profitability.

Currently, we source our fresh golden berries primarily from two fruit farms pursuant to cooperation agreements with local governments and other fruits from agents who procure fruit for us from individual farmers. While we believe that we have adequate sources of raw materials and that we in general maintain good supplier relationships, if we are unable to continue to find adequate suppliers for our raw materials on economic terms acceptable to us, it will adversely affect our results of operations, financial condition and business prospects.

We compete in an industry that is brand-conscious, and unless we are able to establish and maintain brand name recognition our sales may be negatively impacted.

Our business is substantially dependent upon awareness and market acceptance of our products and brand by our targeted consumers. In addition, our business depends on acceptance by our independent distributors and consumers of our brand. Although we believe that we have made progress towards establishing market recognition for our brand “农珍之冠 ” in the Chinese fruit products industry, it is too early in the product life cycle of the brand to determine whether our products and brand will achieve and maintain satisfactory levels of acceptance by independent distributors and retail consumers.

We compete in an industry characterized by rapid changes in consumer preferences, so our inability to continue developing new products to satisfy our consumers’ changing preferences would have a material adverse effect on our sales volumes.

Our products are processed from premium specialty fruits and sell at a high price. A decline in the consumption of our products could occur as a result of a change in consumer preferences, perceptions and spending habits at any time. Future success will depend partly on our ability to anticipate or adapt to such changes and to offer, on a timely basis, new products that meet consumer preferences. Our failure to adapt our product offering to respond to such changes may result in reduced demand and lower prices for our products, resulting in a material adverse effect on our sales volumes, sales and profits.

Our current market distribution and penetration is limited as compared with the potential market and so our initial views as to customer acceptance of a particular product can be erroneous, and there can be no assurance that true market acceptance will ultimately be achieved. In addition, customer preferences are also affected by factors other than taste. If we do not adjust to respond to these and other changes in customer preferences, our sales may be adversely affected.

We rely primarily on third-party distributors, which could affect our ability to efficiently and profitably distribute and market our products, maintain our existing markets and expand our business into other geographic markets.

We do not sell our products directly to end customers. Instead, we rely on third-party distributors for the sale and distribution of our products. We sell our products through an extensive nationwide sales and distribution network covering 20 provinces and 47 cities in China. As of March 31, 2010, this network comprised 75 distributors. We typically do not enter into long-term agreements with distributors and have no control over their everyday business activities. To the extent that our distributors are distracted from selling our products or do not expend sufficient efforts in managing and selling our products, our sales will be adversely affected. Our ability to maintain our distribution network and attract additional distributors will depend on a number of factors, many of which are outside of our control. Some of these factors include: (i) the level of demand for our brand and products in a particular distribution area; (ii) our ability to price our products at levels competitive with those offered by competing products and (iii) our ability to deliver products in the quantity and at the time ordered by distributors.

14

There can be no assurance that we will be able to meet all or any of these factors in any of our current or prospective geographic areas of distribution. Furthermore, shortage of adequate working capital may make it impossible for us to do so. Our inability to achieve any of these factors in a geographic distribution area will have a material adverse effect on our relationships with our distributors in that particular geographic area, thus limiting our ability to maintain and expand our market, which will likely adversely effect our revenues and financial results.

We generally do not have long-term agreements with our distributors, and we may need to spend significant time and incur significant expense in attracting and maintaining key distributors.

Our marketing and sales strategy presently, and in the future, will rely on the performance of our independent distributors and our ability to attract additional distributors. We generally have one-year written agreements with our distributors which are renewable at the beginning of every year. In addition, despite the terms of the written agreements with certain of our significant distributors, we have no assurance as to the level of performance under those agreements, or that those agreements will not be terminated. There is also no assurance that we will be able to maintain our current distribution relationships or establish and maintain successful relationships with distributors in new geographic distribution areas. Moreover, there is the additional possibility that we will have to incur significant expenses to attract and maintain key distributors in one or more of our geographic distribution areas in order to profitably exploit our geographic markets. We may not have sufficient working capital to allow us to do so.

Failure to execute our business expansion plan could adversely affect our financial condition and results of operations.

We are currently building a new fruit and vegetable powder facility which is expected to start production in fiscal year 2011. Our decision to increase our production capacity was based in part on our projections of increases in our sales volume and growth in the size of the premium specialty fruit and vegetable based product market in China. If actual customer demand does not meet our projections, we will likely suffer overcapacity problems and may have to leave capacity idle, which may reduce our overall profitability and adversely affect our financial condition and results of operations. Our future success depends on our ability to expand our business to address growth in demand for our current and future products. Our ability to add production capacity and increase output is subject to significant risks and uncertainties, including:

-

the unavailability of additional funding to expand our production capacity, purchase additional fixed assets and purchase raw materials on favorable terms or at all;

-

delays and cost overruns as a result of a number of factors, many of which may be beyond our control, such as problems with equipment vendors and suppliers of raw materials;

-

failure to maintain high quality control standards;

-

shortage of source fruits;

-

our inability to obtain, or delays in obtaining, required approvals by relevant government authorities;

-

diversion of significant management attention and other resources; and

-

failure to execute our expansion plan effectively.

As our business grows, we will need to implement a variety of new and upgraded operational and financial systems, procedures and controls, including improvements to our accounting and other internal management systems by dedicating additional resources to our reporting and accounting functions, and improvements to our record keeping and contract tracking system. We will need to respond to competitive market conditions and continue to enhance existing products and develop new products, and retain existing customers and attract new customers. We will also need to recruit more personnel and train and manage our growing employee base. Furthermore, we will need to maintain and expand our relationships with our current and future customers, suppliers, distributors and other third parties, and there is no guarantee that we will succeed.

If we encounter any of the risks described above, or are otherwise unable to establish or successfully operate additional production capacity or to increase production output, we may be unable to grow our business and revenues, reduce our operating costs, maintain our competitiveness or improve our profitability, and our business, financial condition, results of operations and prospects may be adversely affected.

15

Because we experience seasonal fluctuations in our sales, our quarterly results will fluctuate and our annual performance will depend largely on results from three quarters.

Our business is highly seasonal in production, reflecting the harvest season of our primary source fruits during the months from mid-July to mid-November. Typically, a substantial portion of our revenues are earned during our second, third and forth fiscal quarters. We generally experience lowest revenues during our first fiscal quarter. Sales in the second, third and forth fiscal quarters accounted for approximately 26.5%, 24.4% and 36.3% of our total revenues for the fiscal year ended March 31, 2010, respectively. If sales in these quarters are lower than expected, our operating results would be adversely affected, and it would have a disproportionately large impact on our annual operating results.

Due to our rapid growth in recent years, our past results may not be indicative of our future performance and evaluating our business and prospects may be difficult.

Our business has grown and evolved rapidly in recent years as demonstrated by our growth in net sales for the fiscal year ended March 31, 2010 to $72.9 million from $56.4 million during the prior fiscal year. We may not be able to achieve similar growth in future periods, and our historical operating results may not provide a meaningful basis for evaluating our business, financial performance and prospects. Moreover, our ability to achieve satisfactory production results at higher volumes is unproven. Therefore, you should not rely on our past results or our historical rate of growth as an indication of our future performance.

We depend heavily on key personnel, and turnover of key employees and senior management could harm our business.

Our future business and results of operations depend in significant part upon the continued contributions of our key technical and senior management personnel, including Changjun Yu, our Chairman, Jinglin Shi, our Chief Executive Officer, Colman Cheng, our Chief Financial Officer, and Manjiang Yu, our Vice President of Sales. None of these key management members currently owns any shares of common stock or any other equity interest in the Company. Although they have signed employment agreements with our subsidiary Fezdale which include a non-competition provision which prohibits them from engaging in the food processing industry during the term of the agreement and for two years after the termination of employment, such employment agreements can be terminated at will. If we lose any of these key employees and are unable to find a qualified replacement in a timely manner, our business will be negative impacted. In addition, if a key employee fails to perform in his or her current position, or if we are not able to attract and retain skilled employees as needed, our business could suffer. Significant turnover in our senior management could significantly deplete the institutional knowledge held by our existing senior management team. We depend on the skills and abilities of these key employees in managing the reclamation, technical, and marketing aspects of our business, any part of which could be harmed by turnover in the future.

The concentration of ownership of our securities by our controlling stockholders who do not participate in the management of our business can result in stockholder votes that are not in our best interests or the best interests of our minority stockholders.

Mr. Yiu Fai Kung and Mr. Kwan Mo Ng, collectively own approximately 79% of our outstanding voting securities, giving them controlling interest in the Company. However, neither Mr. Kung nor Mr. Ng is an executive officer or director of the Company and is not a participant in any way in the day to day affairs of the Company. Mr. Kung and Mr. Ng may have little or no knowledge of the details of the Company’s operations and do not participate in the corporate governance of the Company. In addition, this concentration of ownership may also have the effect of discouraging, delaying or preventing a future change of control, which could deprive our stockholders of an opportunity to receive a premium for their shares as part of a sale of our company and might reduce the price of our shares.

Our inability to protect our trademarks, patent and trade secrets may prevent us from successfully marketing our products and competing effectively.

Failure to protect our intellectual property could harm our brands and our reputation, and adversely affect our ability to compete effectively. Further, enforcing or defending our intellectual property rights, including our trademarks, patents, copyrights and trade secrets, could result in the expenditure of significant financial and managerial resources. We produce, market and sell our products under “农珍之冠 .” We regard our intellectual property, particularly our trademarks and trade secrets to be of considerable value and importance to our business and our success. We rely on a combination of trademark, patent, and trade secrecy laws, and contractual provisions to protect our intellectual property rights. There can be no assurance that the steps taken by us to protect these proprietary rights will be adequate or that third parties will not infringe or misappropriate our trademarks, trade secrets (including our flavor concentrate trade secrets) or similar proprietary rights. In addition, there can be no assurance that other parties will not assert infringement claims against us, and we may have to pursue litigation against other parties to assert our rights. Any such claim or litigation could be costly and we may lack the resources required to defend against such claims. In addition, any event that would jeopardize our proprietary rights or any claims of infringement by third parties could have a material adverse affect on our ability to market or sell our brands, and profitably exploit our products.

16

We may be exposed to potential risks relating to our internal controls over financial reporting and our ability to have those controls attested to by our independent auditors.

As directed by Section 404 of the Sarbanes-Oxley Act of 2002, or “SOX 404”, the SEC adopted rules requiring public companies to include a report of management on the company’s internal controls over financial reporting in their annual reports, including Form 10-K. In addition, the independent registered public accounting firm auditing a company’s financial statements must also attest to the operating effectiveness of the company’s internal controls. Under current law, we were subject to these requirements beginning with our annual report for the fiscal year ending March 31, 2008, although the auditor attestation was not required until our annual report for the fiscal year ending March 31, 2011. We can provide no assurance that we will comply with all of the requirements imposed thereby. There can be no positive assurance that we will receive a positive attestation from our independent auditors. In the event we identify significant deficiencies or material weaknesses in our internal controls that we cannot remediate in a timely manner or we are unable to receive a positive attestation from our independent auditors with respect to our internal controls, investors and others may lose confidence in the reliability of our financial statements.

We have limited insurance coverage and do not carry any business interruption insurance, third-party liability insurance for our production facilities or insurance that covers the risk of loss of our products in shipment.

Operation of our facilities involves many risks, including equipment failures, natural disasters, industrial accidents, power outages, labor disturbances and other business interruptions. Furthermore, if any of our products are faulty, then we may become subject to product liability claims or we may have to engage in a product recall. We do not carry any business interruption insurance, product recall or third-party liability insurance for our production facilities or with respect to our products to cover claims pertaining to personal injury or property or environmental damage arising from defects in our products, product recalls, accidents on our property or damage relating to our operations. Therefore, our existing insurance coverage may not be sufficient to cover all risks associated with our business. As a result, we may be required to pay for financial and other losses, damages and liabilities, including those caused by natural disasters and other events beyond our control, out of our own funds, which could have a material adverse effect on our business, financial condition and results of operations.

We may be exposed to liabilities under the Foreign Corrupt Practices Act, and any determination that we violated the Foreign Corrupt Practices Act could have a material adverse effect on our business.

We are subject to the Foreign Corrupt Practice Act, or the “FCPA”, and other laws that prohibit improper payments or offers of payments to foreign governments and their officials and political parties by U.S. persons and issuers as defined by the statute for the purpose of obtaining or retaining business. We have operations, agreements with third parties and make sales in China, which may experience corruption. Our activities in China create the risk of unauthorized payments or offers of payments by one of the employees, consultants, sales agents or distributors of our company, because these parties are not always subject to our control. It is our policy to implement safeguards to discourage these practices by our employees. Also, our existing safeguards and any future improvements may prove to be less than effective, and the employees, consultants, sales agents or distributors of our Company may engage in conduct for which we might be held responsible. Violations of the FCPA may result in severe criminal or civil sanctions, and we may be subject to other liabilities, which could negatively affect our business, operating results and financial condition. In addition, the government may seek to hold our Company liable for successor liability FCPA violations committed by companies in which we invest or that we acquire.

17

RISKS RELATED TO DOING BUSINESS IN CHINA

Adverse changes in political and economic policies of the PRC government could impede the overall economic growth of China, which could reduce the demand for our products and damage our business.

We conduct substantially all of our operations and generate most of our revenue in China. Accordingly, our business, financial condition, results of operations and prospects are affected significantly by economic, political and legal developments in China. The PRC economy differs from the economies of most developed countries in many respects, including:

-

a higher level of government involvement;

-

a early stage of development of the market-oriented sector of the economy;

-

a rapid growth rate;

-

a higher level of control over foreign exchange; and

-

the allocation of resources.

As the PRC economy has been transitioning from a planned economy to a more market-oriented economy, the PRC government has implemented various measures to encourage economic growth and guide the allocation of resources. While these measures may benefit the overall PRC economy, they may also have a negative effect on us.

Although the PRC government has in recent years implemented measures emphasizing the utilization of market forces for economic reform, the PRC government continues to exercise significant control over economic growth in China through the allocation of resources, controlling the payment of foreign currency-denominated obligations, setting monetary policy and imposing policies that impact particular industries or companies in different ways.

Any adverse change in economic conditions or government policies in China could have a material adverse effect on the overall economic growth in China, which in turn could lead to a reduction in demand for our services and consequently have a material adverse effect on our business and prospects.

PRC food hygiene and safety laws may become more onerous, which may adversely affect our operations and financial performance and lead to an increase in our costs which we may be unable to pass on to our customers.

Operators within the PRC fruit processing industry are subject to compliance with PRC food hygiene and safety laws and regulations. Such laws and regulations require all enterprises engaged in the production of fruit based products to obtain a hygiene license. They also set out hygiene standards with respect to food and food additives, packaging and containers, labeling on packaging as well as hygiene requirements for food production and sites, facilities and equipment used for the transportation and the sale of food. Failure to comply with PRC food hygiene and safety laws may result in fines, suspension of operations, loss of hygiene license and, in certain cases, criminal proceedings against an enterprise and its management. Although we are in compliance with current PRC food hygiene and safety laws and regulations, in the event that such laws and regulations become more stringent or widen in scope, we may fail to comply with such laws, or if we comply, our production and distribution costs may increase, and we may be unable to pass these additional costs on to our customers.

Uncertainties with respect to the PRC legal system could limit the legal protections available to you and us.

We conduct substantially all of our business through our operating subsidiary in the PRC. Our operating subsidiary is generally subject to laws and regulations applicable to foreign investments in China and, in particular, laws applicable to foreign-invested enterprises. The PRC legal system is based on written statutes, and prior court decisions may be cited for reference but have limited precedential value. Since 1979, a series of new PRC laws and regulations have significantly enhanced the protections afforded to various forms of foreign investments in China. However, since the PRC legal system continues to rapidly evolve, the interpretations of many laws, regulations and rules are not always uniform and enforcement of these laws, regulations and rules involve uncertainties, which may limit legal protections available to you and us. In addition, any litigation in China may be protracted and result in substantial costs and diversion of resources and management attention. In addition, all of our executive officers and all of our directors are residents of China and not of the United States, and substantially all the assets of these persons are located outside the United States. As a result, it could be difficult for investors to affect service of process in the United States or to enforce a judgment obtained in the United States against our Chinese operations and subsidiary.

18

You may have difficulty enforcing judgments against us.