Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Argo Group International Holdings, Ltd. | d8k.htm |

Macquarie Small-

& Mid-

Cap Conference

June 2010

Exhibit 99.1 |

2.

Forward-Looking Statements

This presentation contains “forward-looking statements” which are made pursuant to the

safe harbor provisions of the Private Securities Litigation Reform Act of 1995. The

forward-looking statements are based on the Company's current expectations and beliefs

concerning future developments and their potential effects on the Company. There can be no

assurance that actual developments will be those anticipated by the Company. Actual results may

differ materially from those projected as a result of significant risks and uncertainties,

including non-receipt of the expected payments, changes in interest rates, effect of the

performance of financial markets on investment income and fair values of investments,

development of claims and the effect on loss reserves, accuracy in projecting loss reserves, the

impact of competition and pricing environments, changes in the demand for the Company's

products, the effect of general economic conditions, adverse state and federal legislation,

regulations and regulatory investigations into industry practices, developments relating

to existing agreements, heightened competition, changes in pricing environments, and

changes in asset valuations. The Company undertakes no obligation to publicly update any

forward-looking statements as a result of events or developments subsequent to the

presentation. |

3.

An international specialty underwriter of property/casualty

insurance and reinsurance products

Headquartered in Bermuda

Operations in 50 states and worldwide

Total capitalization of $2.0 billion

Operations conducted through four business segments

Our Strategy

Deploy

capital

in

the

international

specialty

market

for

maximum

return

Continuous focus on new business development and organic growth

Grow strategically through acquisitions

Prudent management of our balance sheet and investment portfolio

Maximize shareholder value through our focus on Return on Capital

Argo Group Today

Major business segment locations

Bermuda Headquarters

Brussels

London |

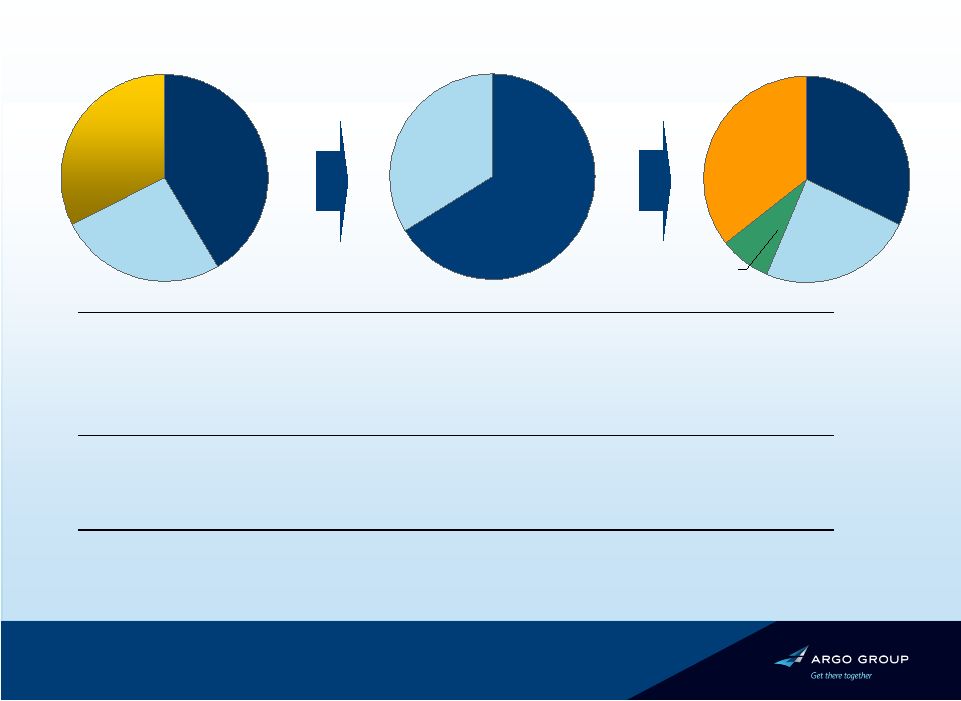

4.

Argo

in

Perspective:

Building

a

Specialty

Platform

2002

-

2009

Commercial

Specialty

$162.3 26.1%

Risk

Management

$201.9 32.5%

Excess &

Surplus

$257.9 41.5%

GWP

2002

2006

2009

Excess &

Surplus

$642.3 32.3%

Commercial

Specialty

$475.7 23.9%

Argo

International

$706.0 35.5%

Excess &

Surplus

$761.5 36.8%

Commercial

Specialty

$391.8 34.0%

(1) Includes what was the Public Entity segment and the Specialty Commercial

segment. (2) Includes Public Entity segment and Select Markets segment and

excludes $2.2 million previously written under Risk Management segment. (3)

Book value per common share - outstanding, includes the impact of the Series A Mandatory Convertible Preferred Stock on an as if converted basis.

(4) Net Run-Off Reserves include Risk Management. 2002 Net Reserves for Risk

Management are an appoximation based on statutory filings. (5) Total Segment

Pre-tax Operating Income calculated as the sum of the above segments' pre-tax operating incomes: excludes certain holding company expenses.

(6) Includes $0.3mm of operating income from the public entity segment.

(7) Includes $6 million of losses from the Risk Management Segment and $67.8 million

of losses from runoff lines. (8) Includes $9.9 million of losses from runoff

lines and $25.5 million of pre-tax operating income from Risk Management segment.

Reinsurance

$162.9 8.2%

Financial Highlights ($ in mm, except per share data)

2002

2006

2009

Book Value per Share

$23.40

(3)

$39.08

(3)

$52.36

Pre-tax Operating Income

(47.7)

141.8

164.8

Total Capital

327.7

992.0

1,995.5

Net Run-Off Reserves as a % of Equity

163.1%

(4)

66.0%

(4)

26.2%

Net Run-Off Reserves as a % of Total Net Reserves

63.8%

(4)

36.5%

(4)

19.1%

Segment

Contribution

to

Total

Segment

Pre-tax

Operating

Income

(5)

Excess & Surplus

41.6%

60.3%

33.8%

Commercial Specialty

24.3%

(6)

30.0%

23.9%

Runoff / Risk Management

(165.8%)

(7)

9.3%

(8)

3.3%

Reinsurance

0.0%

0.5%

26.3%

Argo International

0.0%

0.0%

12.6% |

5.

Argo Today –

A Diversified Business Model

US International

YTD as of March 31, 2010

Note: Based on gross written premiums (GWP)

Insurance Reinsurance

Property Casualty

~70%

~30%

14%

86%

24%

76% |

6.

What We Do

Combined

Ratio*

Insureds

Segment Profile

Excess and

Surplus Lines

•

Commercial Property and

Casualty on a non-admitted

basis

•

Distribution through wholesale

agents and brokers

Commercial

Specialty

Argo

International

•

Argo Managing Agency plc

•

Short-tail risks with an

emphasis on commercial

specialty, and non-US

professional indemnity

insurance

99%

74%

Reinsurance

•

Insureds include US regional

carriers and international multi-

line carriers

•

Casualty clients are

predominately US Fortune

1000 companies written on a

primary basis

•

Argo Re (class 4 specialty

reinsurance platform)

•

Provides property CAT

reinsurance, excess casualty

116%

*

GWP and Combined Ratio for YTD 2010

%

GWP*

31%

24%

14%

30%

100%

•

Representative insureds

include restaurants,

contractors, day care centers,

apartment complexes, and

others

•

Commercial Property and

Casualty on an admitted basis

•

Distribution through select

independent agents, brokers,

wholesalers and program

managers

•

Food and hospitality, specialty

retail, grocery stores, mining

industry and public entities

•

Insureds include US and

international small/medium

commercial businesses,

transportation, fine arts and

specie, financial institutions and

others |

Status

Combined ratio in low 90% range

Colony, Argonaut Specialty & Argo Pro

Competitive advantages

Excellent

infrastructure

–

broad

geography

Underwriting expertise

Broad product portfolio for small account

underwriters

Controlled distribution

Wholesale agents

Benefits from a category XII ‘A’

(Excellent) rating by A.M. Best

7.

Pre-Tax Operating Income

($mm)

Excess & Surplus Lines

Largest and Most Profitable Segment

100%

Combined Ratio

89%

93%

100%

$113

$98

$65

$13

2007

2008

2009

YTD 2010 |

8.

Pre-Tax Operating Income

($mm)

Commercial Specialty

Specialty

Niche Segment

Status

Historical combined ratio in low 90% range

Primarily admitted, retail-driven

Competitive advantages

Expertise in niche markets

–

grocery stores

–

mining operations

–

laundry & dry cleaners

–

small/medium-size public entities

Benefits from a category XII ‘A’

(Excellent)

rating by A.M. Best

89%

97%

96%

Combined Ratio

99%

$61

$43

$46

$8

2007

2008

2009

YTD 2010 |

9.

Status

•

Underwriting on $1.2 billion of capital today

•

Achieved desired diversification in second

year

•

Appointed Andrew Carrier as Argo Re

President and Nigel Mortimer as head of

Excess Casualty

•

New casualty underwriting team in place

Competitive advantages

•

Utilize established infrastructure

•

Built diversified book of business

•

Proven record of leadership

•

Benefits from a category XII ‘A’

(Excellent)

rating by A.M. Best

Reinsurance

Argo Re –

Well Established

74%

78%

Pre-Tax Operating Income

($mm)

Combined Ratio

52%

$25

$50

$8

2008

2009

YTD 2010 |

10.

Status

•

Acquired Heritage in May 2008

•

Appointed Julian Enoizi as CEO

in June 2009

•

Worldwide property

•

Direct and Facultative

•

North American and International

Binding Authority

•

Non-U.S. liability

•

Professional indemnity

•

General liability

Competitive advantages

•

Specialist knowledge

•

Access to decision makers

•

Carries the Lloyd’s market ratings

of ‘A’

(Excellent) rating by A.M.

Best, and ‘A+’

by S&P

Argo International

Lloyd’s Underwriting Agency

116%²

102%

Pre-Tax Operating Income

($mm)

Note:

1

Data is for the full year ending Dec. 31, 2008

2

Includes 22.1 points of catastrophe losses

Combined Ratio

96%

$11

$24

($11)

2008¹

2009

YTD 2010 |

11.

Combined Business Mix

Established platform to write business

worldwide and penetrate niche markets

Specialty Insurance

Excess & Surplus Lines

Commercial Specialty

Reinsurance/Insurance

Quota share reinsurance

of business partners

Property reinsurance

Excess casualty and

professional liability insurance

Argo International (Lloyd’s)

Worldwide property insurance

Non-U.S. liability

56%

14%

30%

As of March 31, 2010 |

12.

Growth in Key Profit Drivers

Net Premium Earned

Gross Written Premium

Investment Income

$622

$1,989

2002

2009

18%

CAGR

$378

$1,415

2002

2009

21%

CAGR

$53

$146

2002

2009

16%

CAGR

($mm) |

13.

$53.81

$39.08

$33.52

$30.36

$27.22

$23.40

$45.15

$44.18

$52.36

2002

2003

2004

2005

2006

2007

2008

2009

2010-Q1

Growth of Book Value

BVPS Growth Since 2002

12.2%

CAGR

*

Book value per

common

share

-

outstanding,

includes

the

impact

of

the

Series

A

Mandatory

Convertible

Preferred

Stock on

an as if converted basis. Preferred stock had fully converted into common

shares as of Dec. 31, 2007. |

14.

Argo Group 2009 Financial Highlights

2008

2009

Change

Gross Written Premium

24%

Net Earned Premium

25%

Total Revenue

24%

Net Operating Income Per Share

35%

Net Income Per Share

86%

** Impacted by $17.4M of pre-tax losses from U.S. storms in Q2 and $74M from

hurricanes Gustav and Ike in Q3. Net Investment Income

3%

YTD Growth in Book Value Per Share

$ 1.6B

$ 1.1B

$ 1.2B

$ 3.17

$ 2.05**

$ 150M

(2.1%)

$ 2.0B

$ 1.4B

$ 1.5B

$ 4.28

$ 3.81

$ 146M

18.5% |

15.

2009

Three

Months

2010

Three

Months

Change

Gross Written Premium

$

496M

18%

Net Earned Premium

$

343M

6%

Total Revenue

$

370M

1%

Net Operating Income Per Share

$

1.13

72%

Net Income Per Share

$ 0.88

24%

Net Investment Income

$

39M

14%

YTD Growth in Book Value Per Share

(2.2%)

Argo Group 2010 First Quarter Results

$

405M

$

324M

$

372M

$

0.32

$ 0.67

$

34M

2.7% |

16.

Strong Balance Sheet and Capital Base

In millions except for book value and leverage data

*Includes $311.4 mm of Junior Subordinated Debentures

Dec 31, 2009

3,203

19.1%

1,996

1,615

6,897

$4,334

381

$52.36

Dec 31, 2008

2,997

24.1%

1,782

1,353

6,382

$4,001

429

$44.18

Reserves

Total Leverage*

Total Capital

Shareholders’

Equity

Total Assets

Investment Portfolio

Indebtedness*

Book Value Per Share

Mar 31, 2010

3,232

1,609

6,632

$4,289

$53.81

377

1,987

19.0% |

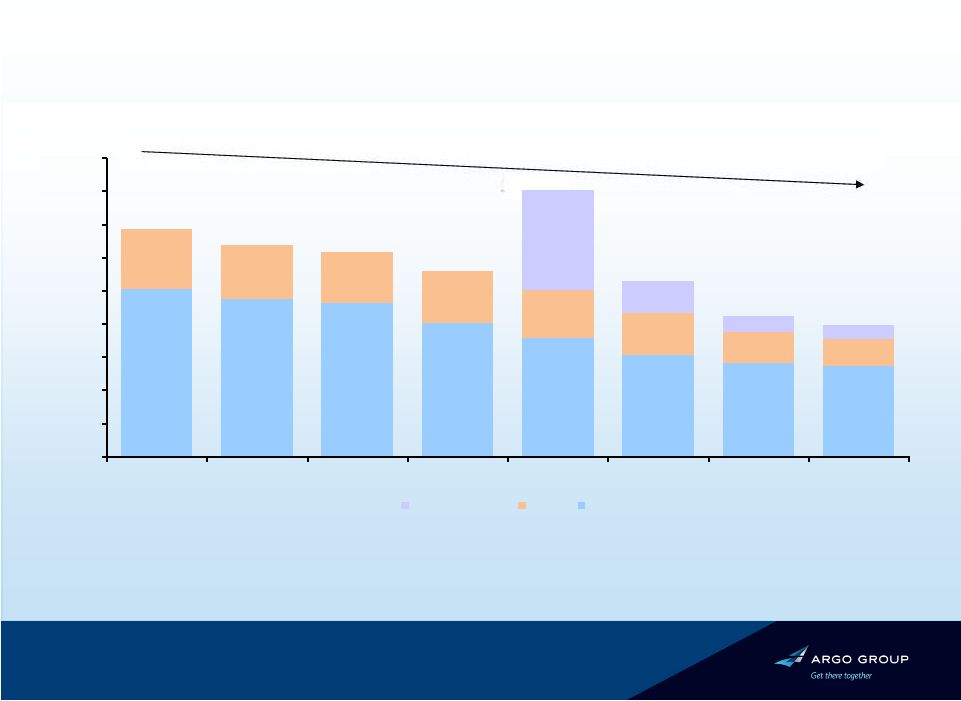

Run-Off Reserves

Net Run-Off Reserve Summary 2003-

Q1 2010

(b)

17.

$505mm

$476mm

$463mm

$402mm

$357mm

$306mm

$280mm

$273mm

$180mm

$162mm

$154mm

$157mm

$141mm

$125mm

$93mm

$82mm

$302mm

(a)

$98mm

$50mm

$42mm

$0.0

$100.0

$200.0

$300.0

$400.0

$500.0

$600.0

$700.0

$800.0

$900.0

2003

2004

2005

2006

2007

2008

2009

Q1 2010

PXRE Runoff

A&E

WC

$685mm

$617mm

$638mm

$529mm

$801mm

$559mm

$423mm

$397mm

Note: WC represents Risk Management and A&E represents IROC; 12/31/2002 net runoff reserves

were internally approximated to be $450mm for Risk Management and

$245mm for IROC. (a) Includes $104.2mm of net reserves related to PXRE Reinsurance Company

sold in 2008. (b) Risk Management Reserves include reserves for other run-off lines

|

Net

Reserves Run-off as a % of total equity declined from 127% to 22%;

Run-off

as

a

%

of

net

reserves¹

declined

from

71%

to

16%

Note:

1 Excludes PXRE reserves

18.

$685mm

$638mm

$632mm

$564mm

$499mm

$432mm

$373mm

$355mm

$539mm

$603mm

$716mm

$848mm

$1,385mm

$1,353mm

$1,615mm

$1,609mm

$966mm

$1,061mm

$1,395mm

$1,531mm

$1,561mm

$2,018mm

$2,163mm

$2,229mm

0%

20%

40%

60%

80%

100%

120%

140%

$0mm

$600mm

$1,200mm

$1,800mm

$2,400mm

2003

2004

2005

2006

2007

2008

2009

Q1-2010

Net-Run-Off Reserves¹

Total Equity

Net Reserves¹

Net-Run-Off Reserves¹ as a % Equity

Net-Run-Off Reserves¹ as a % of Net Reserves¹ |

19.

Conservative Investment Portfolio

Fixed income (94%)

Equities (6%)

Total: $3.9bn

Total: $0.3bn

•

Average Rating of AA

•

Duration of 3.2 years

•

Internally and externally managed

•

Conservative focus on large cap

34%

15%

17%

17%

7%

U.S. Government

State / Muni

Corporate

Structured

Short Term

Other

10%

Financials

Industrial & Other

14%

86% |

20.

Focus Areas for the Coming Year

•

Investments in people

•

Investment in IT

•

Expense savings

•

Controlled expansion in the US and London

•

Focus on clients

•

Focus on distribution partners

•

Focus on the competitive environment

Internal

External

Premiums / Risk Selection

Levers to Drive a Profitable Organization

Investment Leverage / Yields

Financial Leverage / Capital Structure

Infrastructure Cost |

21.

Why Argo?

•

Broadly diversified insurance and reinsurance platform

•

Deep product expertise in niche focus areas

•

Proven track record of growth and profitability

•

Proven ability to manage through insurance cycle

•

Prudent risk management and controls

•

Strong leadership

•

Significant room for future growth

•

ROE driven focus |

Thank you

Q&A |