Attached files

| file | filename |

|---|---|

| 8-K - 8K INVESTOR MEETINGS - PDC ENERGY, INC. | pdc8k20100608.htm |

NASDAQ:PETD

PETROLEUM DEVELOPMENT

CORPORATION

CORPORATION

Investor Meetings

June 2010

See Slide 2 regarding Forward Looking Statements

The following information contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act

of 1995. These forward-looking statements are based on Management’s current expectations and beliefs, as well as a number

of assumptions concerning future events.

of 1995. These forward-looking statements are based on Management’s current expectations and beliefs, as well as a number

of assumptions concerning future events.

These statements are based on certain assumptions and analyses made by Management in light of its experience and its

perception of historical trends, current conditions and expected future developments as well as other factors it believes are

appropriate in the circumstances. However, whether actual results and developments will conform with Management’s

expectations and predictions is subject to a number of risks and uncertainties, general economic, market or business

conditions; the opportunities (or lack thereof) that may be presented to and pursued by Petroleum Development Corporation;

actions by competitors; changes in laws or regulations; and other factors, many of which are beyond the control of Petroleum

Development Corporation.

perception of historical trends, current conditions and expected future developments as well as other factors it believes are

appropriate in the circumstances. However, whether actual results and developments will conform with Management’s

expectations and predictions is subject to a number of risks and uncertainties, general economic, market or business

conditions; the opportunities (or lack thereof) that may be presented to and pursued by Petroleum Development Corporation;

actions by competitors; changes in laws or regulations; and other factors, many of which are beyond the control of Petroleum

Development Corporation.

You are cautioned not to put undue reliance on such forward-looking statements because actual results may vary materially

from those expressed or implied, as more fully discussed in our safe harbor statements found in our SEC filings, including,

without limitation, the discussion under the heading “Risk Factors” in the Company’s 2009 annual report on Form 10-K and in

subsequent Form 10-Qs. All forward-looking statements are based on information available to Management on this date

and Petroleum Development Corporation assumes no obligation to, and expressly disclaims any obligation to, update

or revise any forward looking statements, whether as a result of new information, future events or otherwise.

from those expressed or implied, as more fully discussed in our safe harbor statements found in our SEC filings, including,

without limitation, the discussion under the heading “Risk Factors” in the Company’s 2009 annual report on Form 10-K and in

subsequent Form 10-Qs. All forward-looking statements are based on information available to Management on this date

and Petroleum Development Corporation assumes no obligation to, and expressly disclaims any obligation to, update

or revise any forward looking statements, whether as a result of new information, future events or otherwise.

The SEC permits oil and gas companies to disclose in their filings with the SEC proved reserves, probable reserves and

possible reserves. SEC regulations define “proved reserves” as those quantities of oil or gas which, by analysis of geosciences

and engineering data, can be estimated with reasonable certainty to be economically producible in future years from known

reservoirs under existing economic conditions, operating methods and government regulations; “probable reserves” as

unproved reserves which, together with proved reserves, are as likely as not to be recovered; and “possible reserves” as

unproved reserves which are less certain to be recovered than probable reserves. Estimates of probable and possible reserves

which may potentially be recoverable through additional drilling or recovery techniques are by nature more uncertain than

estimates of proved reserves and accordingly are subject to substantially greater risk of not actually being realized by the

Company. In addition, the Company’s reserves and production forecasts and expectations for future periods are dependent

upon many assumptions, including estimates of production decline rates from existing wells and the undertaking and outcome

of future drilling activity, which may be affected by significant commodity price declines or drilling cost increases.

possible reserves. SEC regulations define “proved reserves” as those quantities of oil or gas which, by analysis of geosciences

and engineering data, can be estimated with reasonable certainty to be economically producible in future years from known

reservoirs under existing economic conditions, operating methods and government regulations; “probable reserves” as

unproved reserves which, together with proved reserves, are as likely as not to be recovered; and “possible reserves” as

unproved reserves which are less certain to be recovered than probable reserves. Estimates of probable and possible reserves

which may potentially be recoverable through additional drilling or recovery techniques are by nature more uncertain than

estimates of proved reserves and accordingly are subject to substantially greater risk of not actually being realized by the

Company. In addition, the Company’s reserves and production forecasts and expectations for future periods are dependent

upon many assumptions, including estimates of production decline rates from existing wells and the undertaking and outcome

of future drilling activity, which may be affected by significant commodity price declines or drilling cost increases.

This material also contains certain non-GAAP financial measures as defined under the Securities and Exchange Commission

rules.

rules.

Disclaimer

2

See Slide 2 regarding Forward Looking Statements

Table of Contents

• PDC Summary

• PDC 2010 Budget & Operational

Guidance

Guidance

• Recent Operational / Transactional

Update

Update

• PDC First Quarter 2010 Results

• Appendix

3

See Slide 2 regarding Forward Looking Statements

PDC SUMMARY

4

See Slide 2 regarding Forward Looking Statements

Reasons to Invest in PDC

• Long term track record of operational excellence

• Diversified operating basins with low risk predictable growth (over

2,200 projects in inventory)

2,200 projects in inventory)

• Emerging opportunity in the Marcellus Shale

• Strong balance sheet with capital available for value added

acquisitions, joint ventures, exploration and partnership

repurchases

acquisitions, joint ventures, exploration and partnership

repurchases

• Trade at discount to peers on operational and financial metrics

• Strong hedge positions that protect cash flow

• Company transitioning from a Partnership company to a more

traditional E&P company

traditional E&P company

5

See Slide 2 regarding Forward Looking Statements

(1) Appalachian Basin (Marcellus and Shallow Devonian) JV

(2) EBITDAX and Cash Flow estimates as per analyst consensus

(3) From 06/09 to 06/10

• Petroleum Development Corporation is an

independent oil and natural gas company

with operations primarily in the Rocky

Mountain region, Appalachian Basin and

Michigan Basin

independent oil and natural gas company

with operations primarily in the Rocky

Mountain region, Appalachian Basin and

Michigan Basin

• PDC was founded in 1969 in Bridgeport, WV

and is now headquartered in Denver, CO

and is now headquartered in Denver, CO

Enterprise Value

Capitalization

Corporate Profile

6

|

|

03/31/2009

|

03/31/2010

|

|

Share Price (06/09 and 06/10)

|

$18.11

|

$21.15

|

|

Diluted Share Outstanding (MM)

|

14.8

|

19.3

|

|

Market Capitalization ($MM)

|

$268

|

$408

|

|

Net debt total

|

382

|

233

|

|

Minority Interest

|

1

|

-

|

|

Enterprise Value

|

$650

|

$641

|

|

52-Week High ($/share) (3)

|

$74.08

|

$26.21

|

|

52-Week Low ($/share) (3)

|

$9.70

|

$12.88

|

Corporate Summary

|

|

03/31/2009

|

03/31/2010

|

|

Net Debt Total

|

$382

|

$233

|

|

Common Equity

|

507

|

515

|

|

Minority Interest (1)

|

1

|

-

|

|

Total Capitalization ($MM)

|

$890

|

$749

|

|

Debt Ratios:

|

|

|

|

Debt/EBITDAX (LTM) (2)

|

1.56x

|

1.33x

|

|

Senior Debt/EBITDAX (LTM) (2)

|

0.52x

|

1.02x

|

|

EBITDAX/ Interest Net (LTM)

(2) |

12.2x

|

5.4x

|

|

Debt/Book Cap

|

45%

|

33%

|

See Slide 2 regarding Forward Looking Statements

Core Operating Regions

See Slide 2 regarding Forward Looking Statements

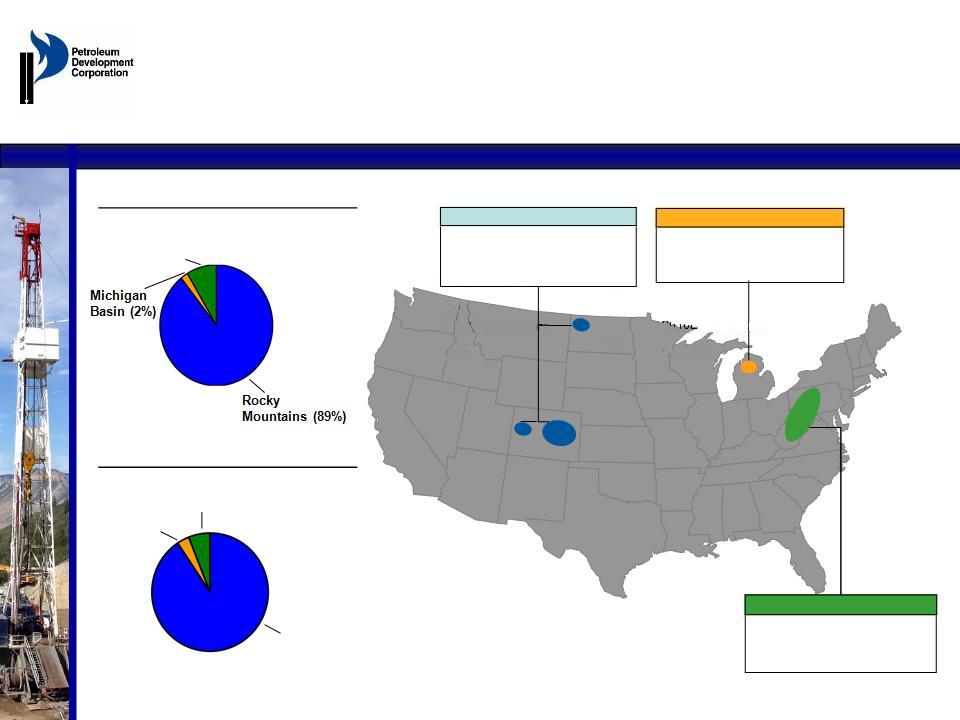

2009 Proved Reserves: 641 Bcfe

2009 Production: 37.8 Bcfe

2010E Production: 31.2 Bcfe

Rocky Mountains

2009 Proved Reserves: 15 Bcfe

2009 Production: 1.4 Bcfe

2010E Production: 1.3 Bcfe

Michigan Basin

2009 Proved Reserves*: 61 Bcfe

2009 Production: 4.1 Bcfe

2010E Production: 3.2 Bcfe

Appalachian Basin

2009 Proved Reserves

717 Bcfe

Appalachian Basin (9%)*

2009 Production

43.3 Bcfe

Michigan

Basin (3%)

Basin (3%)

Appalachian Basin (9%)

Rocky

Mountains (87%)

Mountains (87%)

*Appalachian Basin includes 100% of PDC Mountaineer, LLC Reserves at Year-End 2009

7

See Slide 2 regarding Forward Looking Statements

PDC 2010 BUDGET &

OPERATIONAL GUIDANCE

OPERATIONAL GUIDANCE

8

See Slide 2 regarding Forward Looking Statements

Reserve Summary

at Year-End 2009

at Year-End 2009

753 Bcfe

Revisions &

Pricing

Adjustments

Pricing

Adjustments

Drops /

Scheduling

Adjustments

Scheduling

Adjustments

Production

Adds /

Extensions

Extensions

Revisions, LOE

Improvements,

Operations

Improvements,

Operations

See Slide 2 regarding Forward Looking Statements

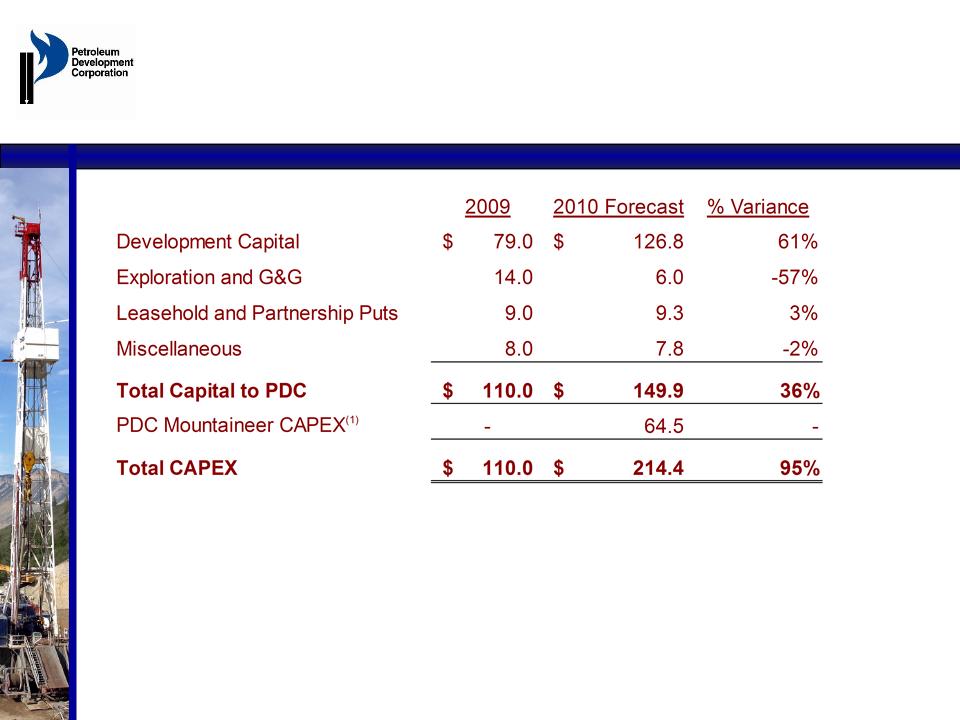

Capital Budget

10

(1) Subject to bi-annual approval by PDC Mountaineer Board of Directors. 2010 CAPEX to be funded by PDC Mountaineer J.V partner. PDC

has no capital investment commitment for 2010.

has no capital investment commitment for 2010.

PDC has announced that it will be updating its 2010 budgets, and production estimates at its 7/15/10 Analyst Day.

($ in millions)

See Slide 2 regarding Forward Looking Statements

11

Marcellus

•16 Verticals

•10

Horizontals

Horizontals

Shallow Devonian

•50 Recompletes

•29 Workovers

NECO

•25 New Drills

•50

Workovers

Workovers

Wattenberg

•180 New Drills

-138 Operated New Drills

-42 Non-Op New Drills

•12 Refracs/Recompletes

Piceance

•21 New Drills

-11 Mesa

-10 Valley

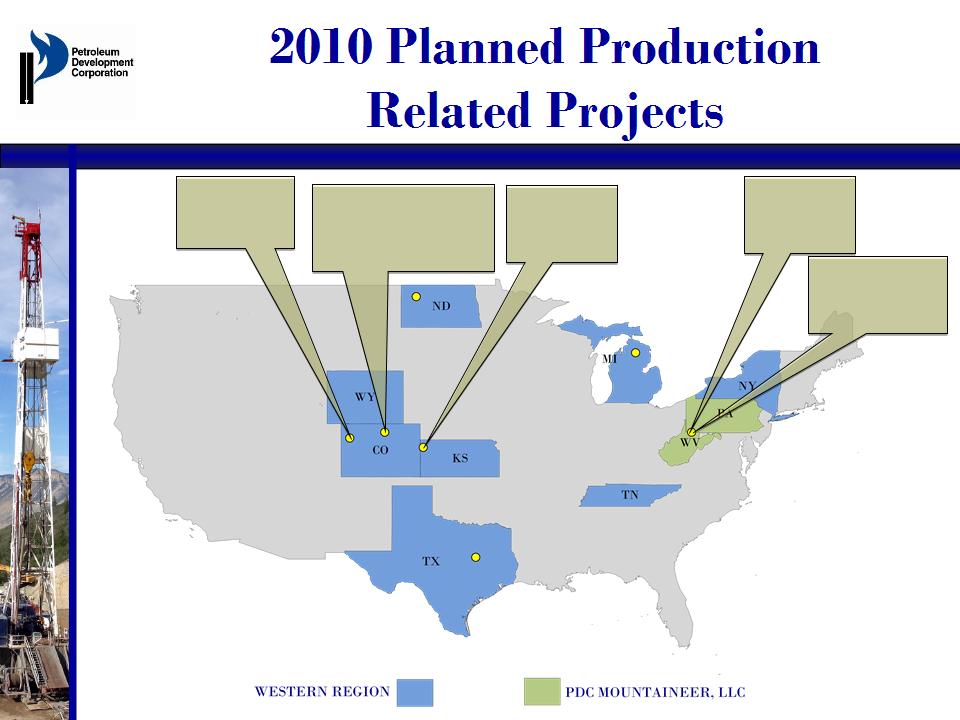

See Slide 2 regarding Forward Looking Statements

PDC has over 2,200 identified

projects in Inventory

projects in Inventory

See Slide 2 regarding Forward Looking Statements

12

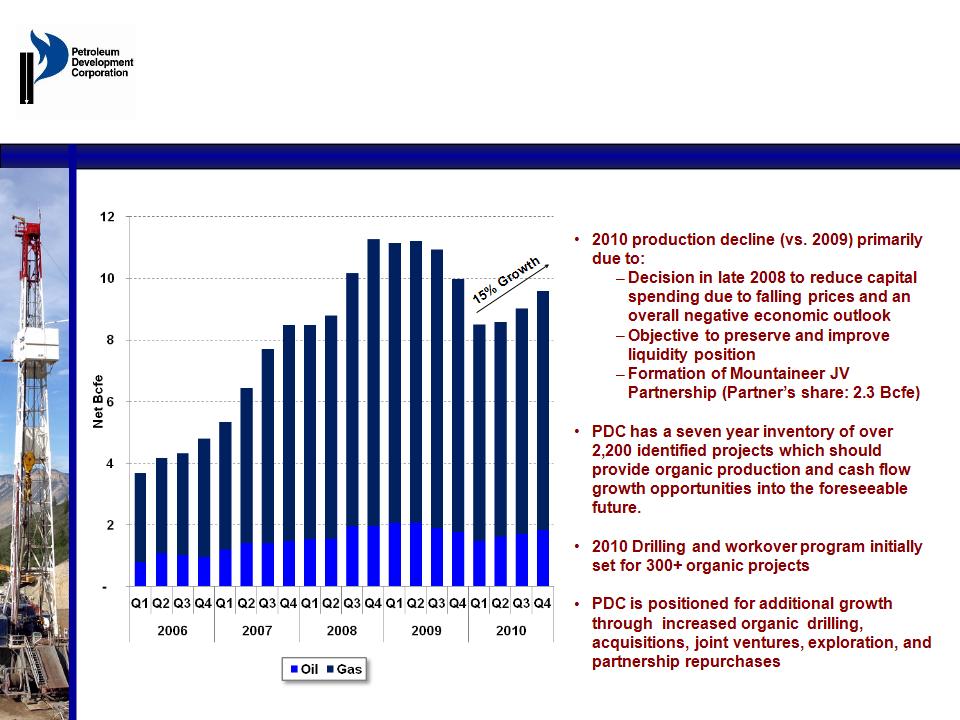

Quarterly Net Production

2010 Production Guidance

E

See Slide 2 regarding Forward Looking Statements

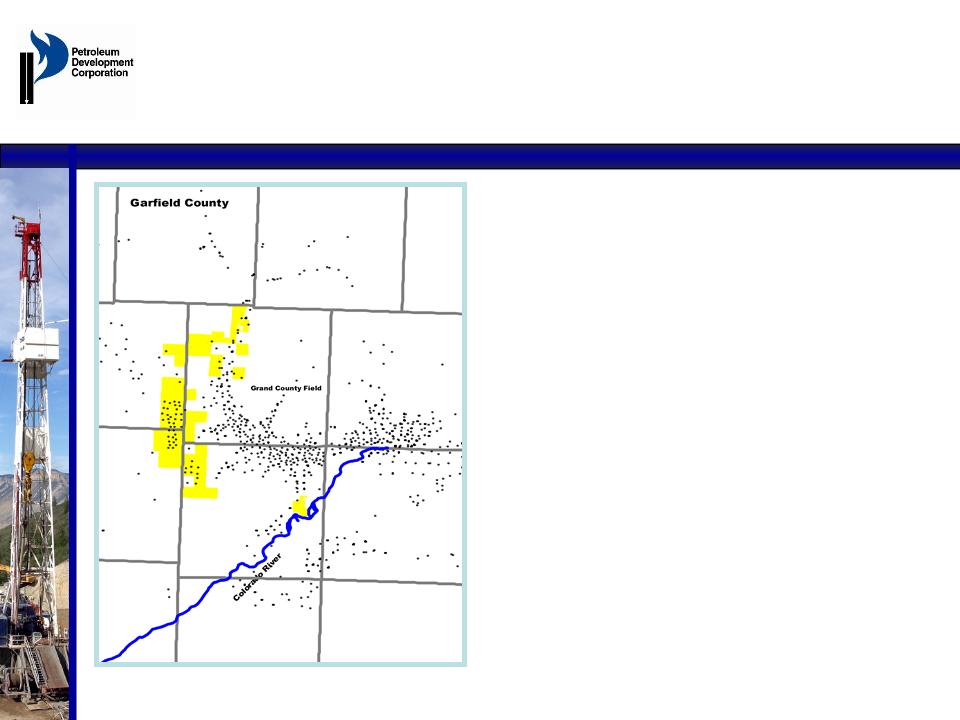

Piceance Basin

at December 31, 2009

at December 31, 2009

• Gross operated wells 288

• Undeveloped acreage 5,300

• Undeveloped, gross,

10-acre locations 433

10-acre locations 433

• 362 total net PDC

• Number of net remaining locations

- PUD 251

- Probable 97

- Possible 14

13

See Slide 2 regarding Forward Looking Statements

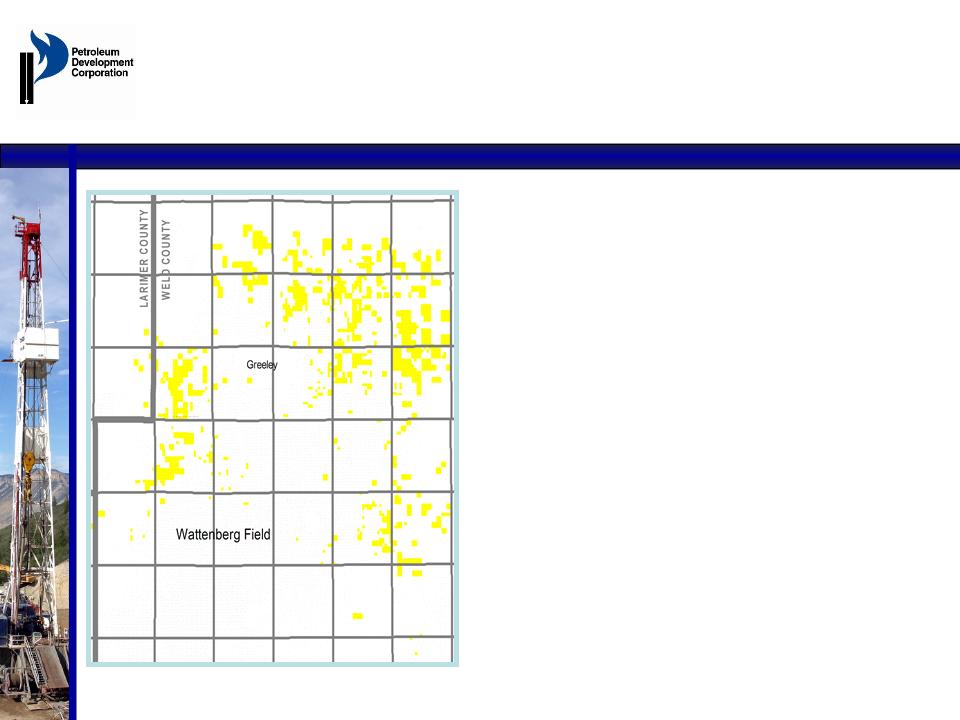

Wattenberg Field

at December 31, 2009

at December 31, 2009

• Gross Operated wells 1,410

• Undeveloped acreage 19,400

• Undeveloped, gross, locations 1,533

• 831 total net PDC

- PUD 373

- Probable 316

- Possible 142

14

See Slide 2 regarding Forward Looking Statements

PDC Undeveloped Northern

Wattenberg Acreage Area

Wattenberg Acreage Area

EOG Niobrara Horizontal Well plus 39

Drilling Permits Approved & Pending

Drilling Permits Approved & Pending

PDC Undeveloped Acreage in

Northern Wattenberg Area.

Approximately 19,400 acres.

Northern Wattenberg Area.

Approximately 19,400 acres.

PDC NECO Area: Niobrara

Biogenic Gas Production

Biogenic Gas Production

Pawnee

National

Grasslands

National

Grasslands

Pawnee National

Grasslands

Grasslands

Base Map Source

USGS

USGS

15

See Slide 2 regarding Forward Looking Statements

Wattenberg Field:

Niobrara Formation Overview

Niobrara Formation Overview

• Covers the bulk of the Rocky Mountain region and has been being

developed in the DJ Basin for 30+ years on a veritcal basis with

mixed results

developed in the DJ Basin for 30+ years on a veritcal basis with

mixed results

• Economics improved in the late 90’s with modern hydraulic

fracturing technology for vertical development

fracturing technology for vertical development

• PDC developed and enhanced a geologic model which

incorporates recent horizontal drilling and production results by

EOG Resources and Noble

incorporates recent horizontal drilling and production results by

EOG Resources and Noble

• In Q2 2010 PDC purchased the 5,500 net acre “Krieger Prospect”

as an anticipated horizontal project for approximately $1,000 per

acre

as an anticipated horizontal project for approximately $1,000 per

acre

• Spacing request, hearing and permit submittal should occur by the

end of July 2010

end of July 2010

• Expect to spud and achieve first production Q4 2010

• Anticipate drilling 4-6 horizontal wells in 2011 and will continue to

evaluate farm-in opportunities

evaluate farm-in opportunities

16

See Slide 2 regarding Forward Looking Statements

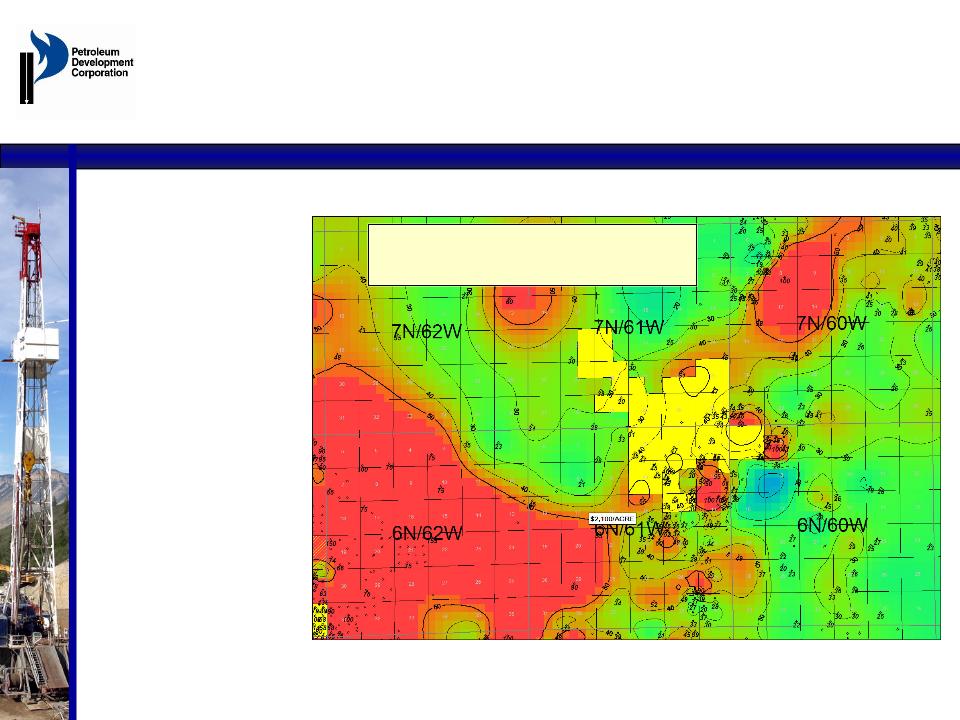

PDC Krieger Horizontal

Niobrara Drilling Prospect

Niobrara Drilling Prospect

17

Mapped on maximum Deep Rt in Niobrara B Zone.

CI = 10 ohm up to 50 ohm. Blue is lowest Rt, red highest Rt.

All above 50 ohm undifferentiated & shown in red.

PDC leases in yellow.

• Mapped on a greater

than 50 ohm Rt fairway

trending northeast from

Wattenberg Field.

than 50 ohm Rt fairway

trending northeast from

Wattenberg Field.

•Existing 3D Seismic helps

confirm wellbore planning.

confirm wellbore planning.

• Approximately 5,500

acres net to PDC.

acres net to PDC.

• Anticipate 12+ horizontal

well locations based on

640 acre spacing.

well locations based on

640 acre spacing.

• Drill initial well in 4th

Quarter 2010.

Quarter 2010.

• Vertical Niobrara tests in

the area provide evidence

of oil in the Niobrara

system.

the area provide evidence

of oil in the Niobrara

system.

• Offset full State section

sold for $2,100 per acre in

May 2010 lease sale.

sold for $2,100 per acre in

May 2010 lease sale.

See Slide 2 regarding Forward Looking Statements

18

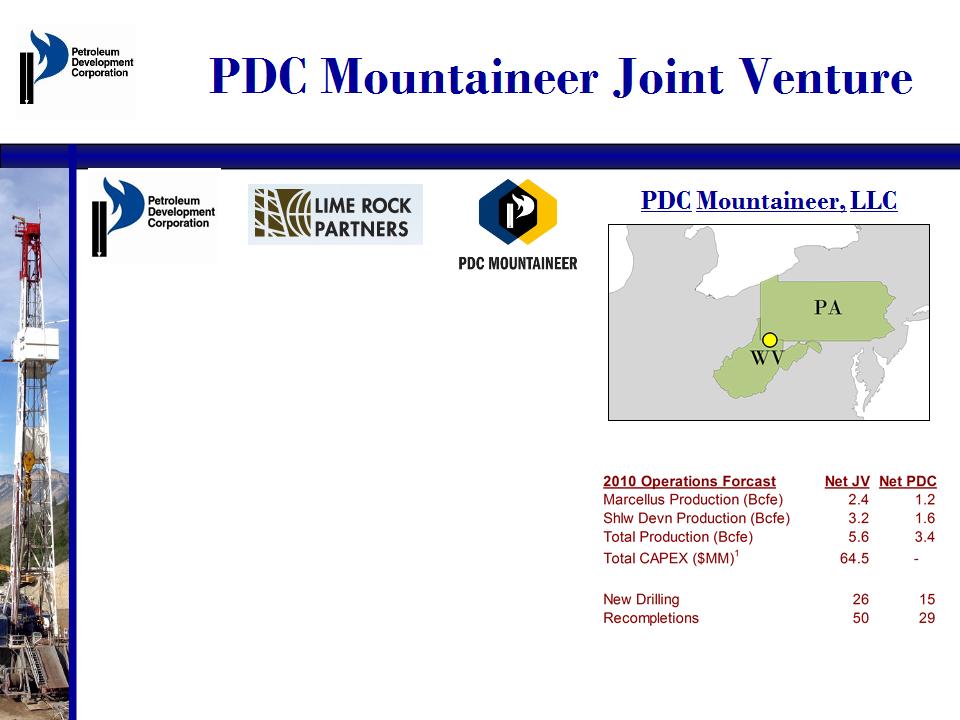

• $158 MM Appalachian JV formed with Lime Rock Partners

(“LRP”) effective 10/1/09; PDC contributed Marcellus

acreage and Shallow Devonian production and acreage.

(“LRP”) effective 10/1/09; PDC contributed Marcellus

acreage and Shallow Devonian production and acreage.

• Provided PDC an alternative capital source as LRP funded

PDC $45 MM upon closing, and a commitment to invest the

first $68.5 MM of capital investment. LRP will become a

50% partner once it satisfies it’s capital investment

obligation.

PDC $45 MM upon closing, and a commitment to invest the

first $68.5 MM of capital investment. LRP will become a

50% partner once it satisfies it’s capital investment

obligation.

• Provides opportunity to accelerate development of the JV

assets.

assets.

• PDC’s ability to raise capital through the JV structure,

provides financial flexibility and opportunities to increase

development capital spending and /or pursue acquisitions.

provides financial flexibility and opportunities to increase

development capital spending and /or pursue acquisitions.

• The JV is governed and managed by a Board of Directors

comprised of equal representation by PDC and LRP. PDC

will manage the operations of the JV.

comprised of equal representation by PDC and LRP. PDC

will manage the operations of the JV.

+

=

Marcellus & Devonian Shallow

(1) 2010 CAPEX to be funded by PDC Mountaineer partner, PDC has no capital investment obligation.

See Slide 2 regarding Forward Looking Statements

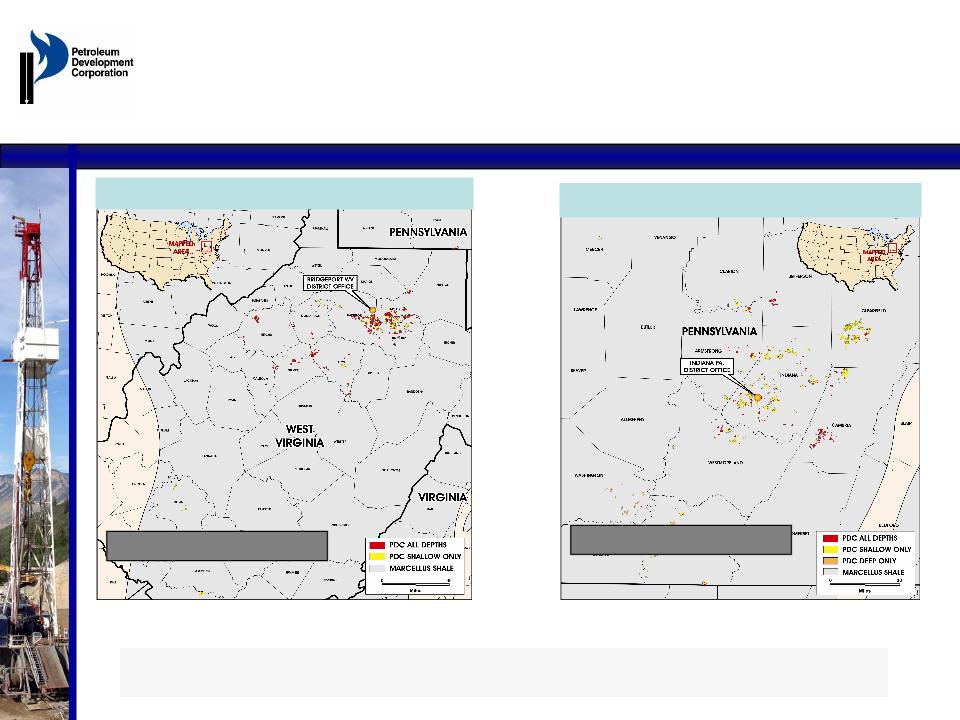

Pennsylvania Acreage Map

15,219 Net Marcellus Rights

42,354 Net Marcellus Rights

West Virginia Acreage Map

Appalachian Basin Acreage -

Marcellus Shale

|

|

HBP NET

ACRES |

UNDEVELOPED

NET ACRES

|

TOTAL

NET ACRES

|

AVERAGE

NRI |

|

As of 2-22-2010

|

PA: 9,981

WV: 38,395

|

PA: 5,238

WV: 3,959

|

PA: 15,219

WV: 42,354

|

82.80%

86.70%

|

19

See Slide 2 regarding Forward Looking Statements

Income Statement and

Cash Flow Analysis

Cash Flow Analysis

20

1) Other income: income from gas marketing activities, well ops and pipeline income

• Despite 17.6% reduction in

production in 2010 versus 2009,

the Company budgeted 2010 net

income versus a loss in 2009 and

budgeted strong year over year

adjusted cash flow from

operations.

production in 2010 versus 2009,

the Company budgeted 2010 net

income versus a loss in 2009 and

budgeted strong year over year

adjusted cash flow from

operations.

• Year-over-year change in net

income and cash flow from

operations were primarily due to

improved:

income and cash flow from

operations were primarily due to

improved:

• Price realizations

• Capital efficiency

• G&A expense - non-

recurrence of 2009 one time

items.

recurrence of 2009 one time

items.

|

($ in MM except per share data)

|

2009

Actual

|

2010

Low

|

2010

High

|

|

Bcfe

|

43.3

|

35.7

|

35.7

|

|

|

|

|

|

|

Total O&G Revenue

|

$286

|

$239

|

$258

|

|

Other Income(1)

|

14

|

12

|

12

|

|

Total Revenue

|

$300

|

$251

|

$270

|

|

O&G Production & Well Ops Cost

|

65

|

59

|

63

|

|

G&A Expense

|

54

|

43

|

39

|

|

Adjusted EBITDAX

|

$181

|

$150

|

$169

|

|

|

|

|

|

|

Exploration Expense/Dry Hole Cost

|

23

|

9

|

8

|

|

DD&A

|

131

|

116

|

116

|

|

Net Interest Expense

|

37

|

34

|

34

|

|

Taxes/ (Benefit)

|

(7)

|

(4)

|

4

|

|

Adjusted Net Income (loss)

|

($3)

|

($6)

|

$7

|

|

|

|

|

|

|

Stock-based Compensation

|

6

|

7

|

5

|

|

DD&A

|

131

|

116

|

116

|

|

Exploratory/Dry Hole Cost

|

1

|

2

|

1

|

|

Other

|

35

|

28

|

28

|

|

Adjusted Cash Flows From Operations

|

$170

|

$148

|

$158

|

|

Weighted # of share outstanding

|

16,448

|

19,300

|

19,300

|

|

CFFO/Share

|

$10.35

|

$7.67

|

$8.17

|

|

EPS

|

($0.18)

|

($0.32)

|

$0.34

|

See Slide 2 regarding Forward Looking Statements

Oil and Gas Hedges

(1) Based on 12/31/09 PDP curve (i.e., may represent 50% or less of actual production for the future year)

(2) Based on forward pricing curves as of 3/31/2010

(3) Blended price for forecasted production at hedged and at forward prices

Continued focus on hedging enabled the Company to protect its cash flow, capital programs,

and organic drilling economics from commodity price fluctuations

and organic drilling economics from commodity price fluctuations

• Realized gains of $108MM

• Substantial hedge positions through 2013 via swaps (2010-2011) and collars (2012-2013) at solid historical

commodity price levels should continue to provide on-going protection

commodity price levels should continue to provide on-going protection

• Price sensitivity of 2010’s budget has been significantly mitigated. Variation of $1.00/Mcfe for natural gas

and $10.00/bbl for oil results in less than a 5% variation in cash flow from operations

and $10.00/bbl for oil results in less than a 5% variation in cash flow from operations

21

|

As of April 30, 2010

|

|

2010

|

2011

|

2012

|

2013

|

|

Weighted Average Hedge Price (Mcfe) (1)

|

|||||

|

With Floors

|

$7.44

|

$6.83

|

$6.39

|

$6.37

|

|

|

With Ceilings

|

$8.22

|

$7.64

|

$7.96

|

$8.20

|

|

|

% of Forecasted Production(1)

|

77%

|

73%

|

59%

|

58%

|

|

|

Weighted Avg Forward Price(2)

|

$5.94

|

$6.76

|

$7.11

|

$7.30

|

|

|

Weighted Avg Price of Forecasted

Production(3) |

$7.10

|

$6.81

|

$6.68

|

$6.77

|

|

See Slide 2 regarding Forward Looking Statements

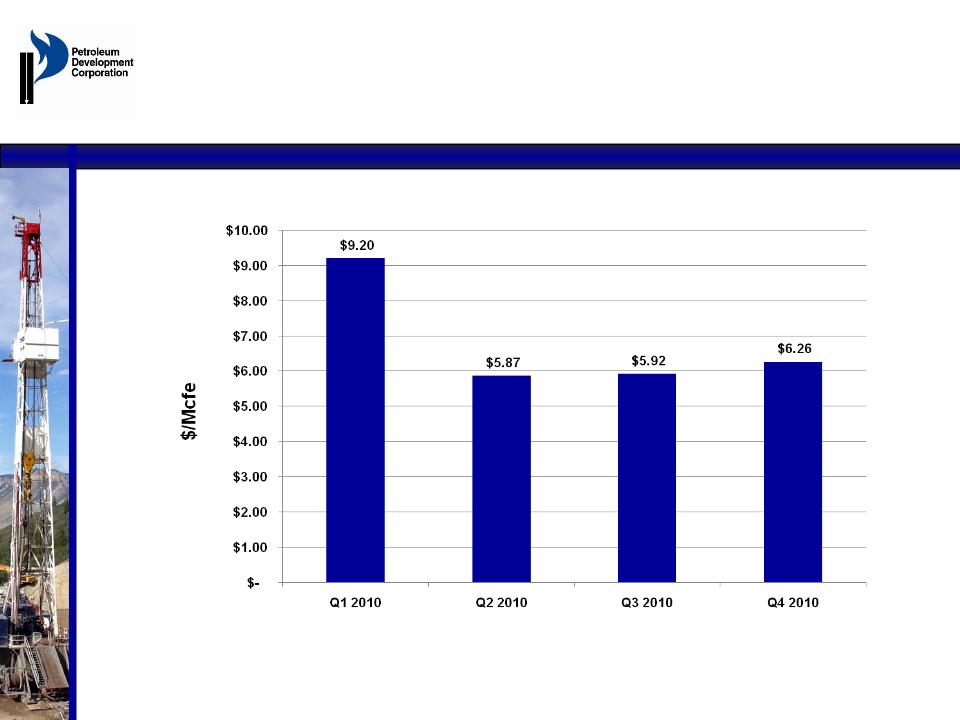

Quarterly Realized Hedge Price

(as of 4/30/2010)

(as of 4/30/2010)

22

• Weighted average for full-year 2010 is $6.81/Mcfe

• Excludes Michigan Divestiture & Permian acquisitions

See Slide 2 regarding Forward Looking Statements

RECENT OPERATIONAL /

TRANSACTIONAL UPDATE

TRANSACTIONAL UPDATE

23

See Slide 2 regarding Forward Looking Statements

PDC Wolfberry Acquisition in

West Texas Key Highlights

West Texas Key Highlights

24

• Acquired producing assets from private seller in Wolfberry

Trend for $45 mm plus PDC’s producing Michigan Gas assets

valued by the seller at $30 million

Trend for $45 mm plus PDC’s producing Michigan Gas assets

valued by the seller at $30 million

• Includes 72 wells on approximately 8,300 net acres

• Should add approximately 900 boe/d over the next 12 months

and strong multi-year production growth is projected

and strong multi-year production growth is projected

• Proved plus probable (2P) reserve add of approximately 8.5

million BOE (70% oil)

million BOE (70% oil)

• Effective date of transaction is May 1, 2010 with projected

closing date of July 30, 2010

closing date of July 30, 2010

• Acquisition driven by US onshore basin study findings

• Must identify asset team to execute development plan and

grow the position

grow the position

See Slide 2 regarding Forward Looking Statements

PDC Wolfberry Acquisition

Wolfberry Acreage Overview with Surrounding Activity

Wolfberry Acreage Overview with Surrounding Activity

25

Key Development Areas

• Roy Parks area

• Mabee areas

• Ratliff area

• Other Permian

Development Potential

• 120 Wolfberry locations

• Anticipate 1 rig program starting 4Q

2010

2010

• Multiple re-completion

targets

targets

• Production optimization

Key Offset Operators

• Concho

• Devon

• Cabot

• Endeavor

See Slide 2 regarding Forward Looking Statements

Partnership Purchases:

Three-Year Plan

Three-Year Plan

• Limited Partners’ non-operated interest is typically 60-80% of

certain PDC operated wells (Rockies principally)

certain PDC operated wells (Rockies principally)

• 28 Limited Partnerships have net reserves of approximately 125

Bcfe and net production of approximately 25 MMcfe/d owned by

the Limited Partners

Bcfe and net production of approximately 25 MMcfe/d owned by

the Limited Partners

• PDC strategy to purchase Limited Partners’ interest over next

three years

three years

– Production and reserve adds in existing operated core acreage

– Reduction/optimization of internal G&A costs

– 9 SEC compliant partnerships represent over 60% of net reserves

and over 75% of total cash flows owned by the Limited Partners

and over 75% of total cash flows owned by the Limited Partners

– Elimination of Limited Partnerships through repurchases would

finalize PDC’s transition to a traditionally capitalized E&P company

finalize PDC’s transition to a traditionally capitalized E&P company

26

See Slide 2 regarding Forward Looking Statements

IncreasingValue in

2010 and Beyond

2010 and Beyond

• Additional Organic Drilling - Possibly beginning 2nd half 2010

- Ramp up in Piceance and Wattenberg

- Focus on enhancing Piceance economics

• Marcellus JV - drilling 26 horizontal and vertical wells in 2010

- Large operator in WV achieved reserves of 3.6 Bcfe per

horizontal well near PDC acreage

horizontal well near PDC acreage

- Over 150 Marcellus permits issued in WV counties surrounding

PDC position

PDC position

• Partnership Purchases - Three Year Plan

- Non-operated interests in certain existing PDC operated

Wattenberg and Piceance Assets

Wattenberg and Piceance Assets

• Acquisitions - Asset and Small Corporate

- Anticipate substantial A&D deal flow in 2010

• Exploration - Moderate Risk Resource Plays

- Niobrara Wattenberg; Mancos Shale Piceance; Bakken; Others

27

See Slide 2 regarding Forward Looking Statements

28

Peer Group: BBG, BRY, COG, CRZO, GDP, PVA, ROSE

See Slide 2 regarding Forward Looking Statements

• Strong Focus on creating Shareholder value

• Strong core asset base with improved drilling economics

• Marcellus Shale JV with Lime Rock partners provides potential

catalyst for strong production and cash flow growth

catalyst for strong production and cash flow growth

• Evaluating potential acquisition, joint venture, and exploration

opportunities which could provide value-added growth

opportunities which could provide value-added growth

• Strong balance sheet with liquidity of ~$250 million

• Experienced and highly effective management team

• PDC is undervalued and poised for growth

Summary

29

See Slide 2 regarding Forward Looking Statements

PDC FIRST QUARTER

2010 RESULTS

2010 RESULTS

30

See Slide 2 regarding Forward Looking Statements

First Quarter 2010 Highlights

31

• Net income of $23.7 million, or $1.23 per diluted share

• Gas and oil revenues up 52% over same period 2009 on Q1

2010 realized prices of $9.20 per Mcfe over Q1 2009 realized

prices of $7.08 per Mcfe

2010 realized prices of $9.20 per Mcfe over Q1 2009 realized

prices of $7.08 per Mcfe

• Adjusted cash flow of $49.3 million, or $2.56 per diluted share

• Q1 2010 adjusted cash flow up approximately $10 million over

same period 2009 on 20% lower volumes

same period 2009 on 20% lower volumes

• Production of 9.1 Bcfe, 7% above Q1 guidance of 8.5 Bcfe

• Drilled 38.6 net wells vs. 24.9 net wells in Q1 2009

• Liquidity improved to $254 million

See Slide 2 regarding Forward Looking Statements

2010 Q1 Operations Highlights

• Quarterly production exceeded budget by 7%

• Integrated $10MM Wattenberg acquisition

– Suncor preferential right

• Marcellus

– Drilled first horizontal well with completion pending

– Drilling second horizontal well

• Wattenberg

– Major gas system operator is installing pipe and compression that

will reduce line pressure and may further enhance production

will reduce line pressure and may further enhance production

– Completion practices continue to improve

– Second rig reached efficiency very quickly

• Piceance

– Fit for purpose rig achieving new level of drilling pace

– Anticipating permit of water disposal well in next 30 days

32

See Slide 2 regarding Forward Looking Statements

Lifting Costs

33

|

Area

|

Full Year

2008 Actual |

Full Year

2009 Actual |

Q1 2010

Actual

|

|

Direct Costs ($/Mcfe)

|

$0.84

|

$0.59

|

$0.75

|

|

Indirect Costs ($/Mcfe)

|

$0.23

|

$0.24

|

$0.29

|

|

Total Lifting Cost ($/Mcfe)

|

$1.07

|

$0.83

|

$1.04

|

|

Production (MMcfe/d)

|

106

|

119

|

101

|

• Q1 2010 per unit costs increased as a result of:

• Winter operations

• Decreased production

• EH&S expenses

• Location and road maintenance

• Water hauling and disposal

See Slide 2 regarding Forward Looking Statements

Summary Financial Results

(1) O&G operating margin is defined as O&G revenue less O&G production and well operations costs.

(2) See appendix for GAAP reconciliation of Adjusted Cash Flow and Adjusted EBITDA, respectively.

34

|

|

Three Months Ended

|

|

|

March 31,

|

||

|

($ in millions)

|

2010

|

2009

|

|

O&G revenues

|

$60.4

|

$39.7

|

|

O&G production & well operations costs

|

$15.7

|

$16.4

|

|

O&G operating margin(1)

|

$44.7

|

$23.3

|

|

Adjusted cash flow from operations(2)

|

$49.3

|

$39.7

|

|

Adjusted EBITDA(2)

|

$53.7

|

$46.2

|

|

DD&A

|

$28.4

|

$34.4

|

|

G&A

|

$10.7

|

$12.1

|

See Slide 2 regarding Forward Looking Statements

Summary Financial Results

|

|

Three Months Ended

March 31, |

|

|

(in millions except per share data)

|

2010

|

2009

|

|

Income (loss) from operations

|

$45.7

|

($1.6)

|

|

Net Income (loss) attributable to

shareholders |

$23.7

|

($5.7)

|

|

Diluted earnings (loss) per share attributable

to shareholders |

$1.23

|

($0.38)

|

|

|

Three Months Ended

March 31, |

|

|

|

2010

|

2009

|

|

Adjusted net income attributable to

shareholders(1) |

$10.9

|

$4.1

|

|

Adjusted earnings per share attributable to

shareholders(1) |

$0.57

|

$0.27

|

35

(1) See appendix for GAAP reconciliation of Adjusted Net Income.

See Slide 2 regarding Forward Looking Statements

APPENDIX

36

See Slide 2 regarding Forward Looking Statements

Acreage Inventory

|

Area

|

Lease Gross

Acres |

PDC Net Acres

|

Net Developed

Acres |

Net Undeveloped

Acres |

State

|

|

Grand Valley

|

8,000

|

8,000

|

2,700

|

5,300

|

Colorado

|

|

Wattenberg

|

72,200

|

64,900

|

45,500

|

19,400

|

Colorado

|

|

NECO

|

127,100

|

105,100

|

19,600

|

85,500

|

Colorado/Kansas

|

|

Michigan

|

26,800

|

23,300

|

14,800

|

8,500

|

Michigan

|

|

New York

|

18,700

|

15,900

|

0

|

15,900

|

New York

|

|

North Dakota

|

66,800

|

30,200

|

4,600

|

25,600

|

North Dakota

|

|

Appalachian Basin

|

120,900

|

117,600

|

106,800

|

10,800

|

WV / PA

|

|

Wyoming

|

19,500

|

19,300

|

100

|

19,200

|

Wyoming

|

|

Texas Barnett

|

8,900

|

6,000

|

400

|

5,600

|

Texas

|

|

Total

|

468,900

|

390,300

|

194,500

|

195,800

|

|

|

|

|

|

PDC TOTAL NET

|

390,300

|

|

37

See Slide 2 regarding Forward Looking Statements

Proved Reserves/Bcfe

by Area at Year-End 2009

by Area at Year-End 2009

38

|

Area

|

2008

|

2009

|

2008

|

2009

|

2008

|

2009

|

2008

|

2009

|

|

Wattenberg

|

79

|

89

|

1

|

1

|

119

|

140

|

199

|

230

|

|

Piceance

|

107

|

103

|

6

|

0

|

260

|

275

|

373

|

378

|

|

NECO

|

40

|

31

|

3

|

0

|

5

|

0

|

48

|

31

|

|

Appalachia

|

53

|

42

|

21

|

13

|

39

|

6

|

113

|

61

|

|

Other

|

20

|

16

|

0

|

1

|

0

|

0

|

20

|

17

|

|

TOTAL

|

299

|

281

|

31

|

15

|

423

|

421

|

753

|

717*

|

|

% Total Proved

|

40%

|

39%

|

4%

|

2%

|

56%

|

59%

|

100%

|

100%

|

Bcfe = One billion cubic feet of natural gas equivalent.

* Using year-end spot pricing methodology, as was used at year-end 2008, total reported reserves would have been 811 Bcfe.

See Slide 2 regarding Forward Looking Statements

3P Reserves(1)/Bcfe

by Area at Year-End 2009

by Area at Year-End 2009

39

|

Proved + Probable

|

||||||

|

Area

|

2008

|

2009

|

2008

|

2009

|

2008

|

2009

|

|

Wattenberg

|

199

|

230

|

236

|

305

|

241

|

332

|

|

Piceance

|

373

|

378

|

486

|

449

|

538

|

465

|

|

NECO

|

48

|

31

|

57

|

31

|

74

|

31

|

|

Appalachia

|

113

|

61

|

126

|

113

|

136

|

145

|

|

Other

|

20

|

17

|

20

|

17

|

20

|

17

|

|

TOTAL

|

753

|

717

|

925

|

915

|

1,009

|

990

|

Bcfe = One billion cubic feet of natural gas equivalent.

(1) 3P estimates are non-SEC.

See Slide 2 regarding Forward Looking Statements

Production/Bcfe by Area

40

|

Area

|

2008

|

2009

|

% Increase/

(Decrease)

|

2010E

|

% Increase/

(Decrease)

|

|

Wattenberg

|

15.4

|

16.3

|

6%

|

14.1

|

-13%

|

|

Piceance

|

12.5

|

15.8

|

26%

|

11.9

|

-25%

|

|

NECO

|

5.0

|

5.3

|

6%

|

4.6

|

-11%

|

|

Appalachia

|

3.9

|

4.1

|

5%

|

3.4

|

-17%

|

|

Other (ND, TX, WY, MI)

|

1.9

|

1.8

|

5%

|

1.7

|

-11%

|

|

TOTAL

|

38.7

|

43.3

|

12%

|

35.7

|

-18%

|

Bcfe = One billion cubic feet of natural gas equivalent.

See Slide 2 regarding Forward Looking Statements

41

2009 Metrics

Natural Gas Equivalent(1)

Natural Gas Equivalent(1)

Oil & Gas Production and Well

Operations Costs(2)

Operations Costs(2)

(Bcfe)

($/Mcfe)

($MM)

Capital Spending

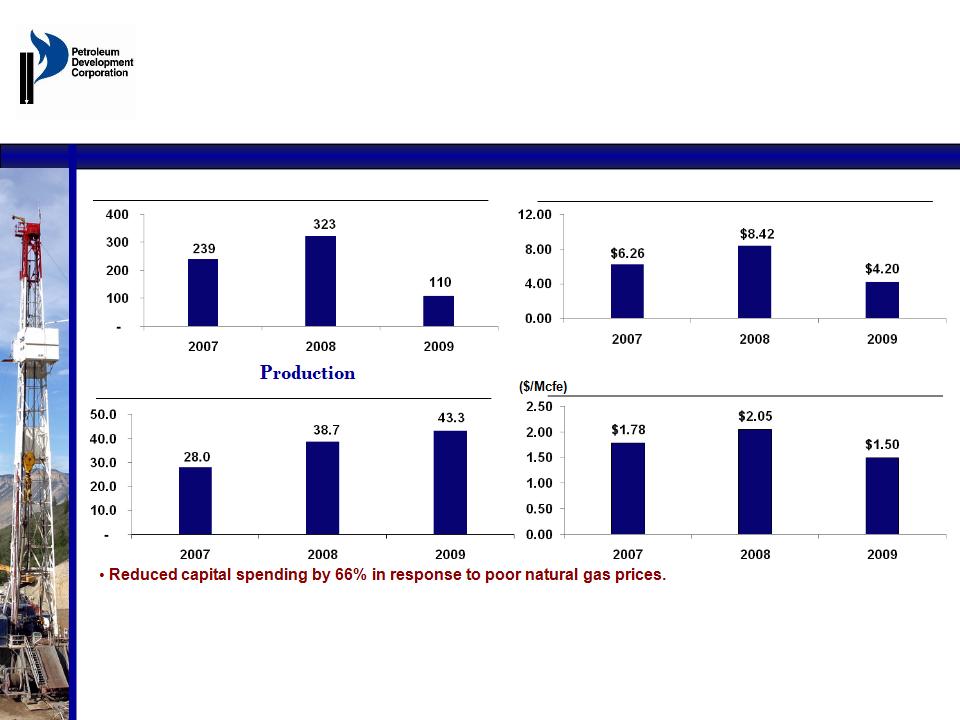

• Increased production by 12% and reduced L.O.E $/Mcfe by just under 30%.

• Improved L.O.E $/Mcfe should be sustainable beyond 2009 and should improve incremental capital investment

returns.

returns.

(1) Average Sales Price excluding gain/loss on derivatives

(2) Includes direct and indirect well expenses, production taxes, and overhead and other production expenses.

See Slide 2 regarding Forward Looking Statements

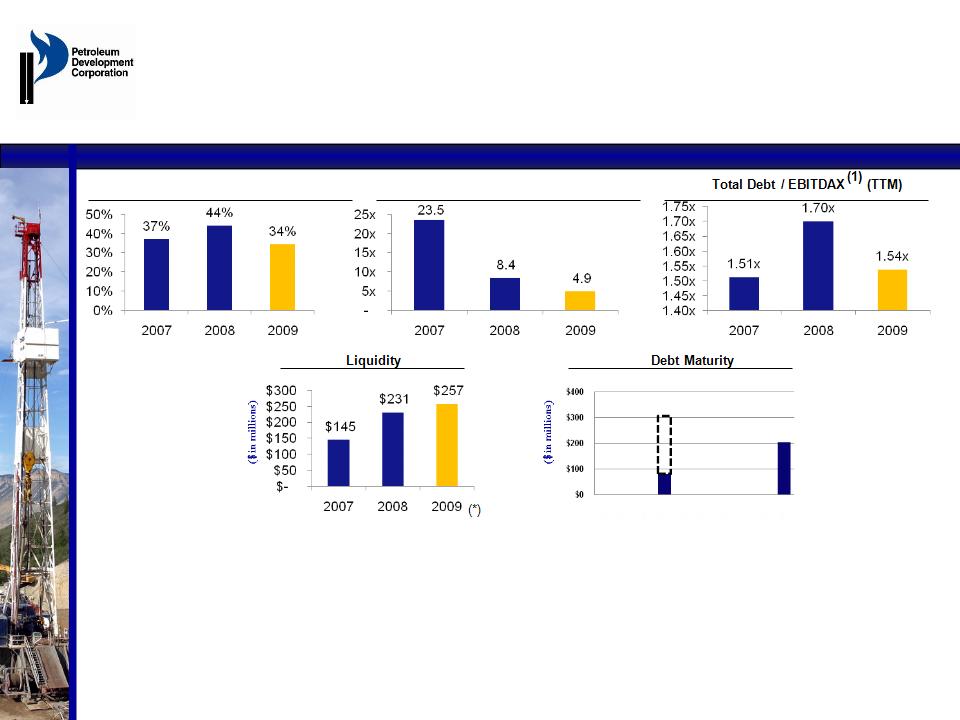

2009 Credit Ratios

Total Debt / Capital Base

(%)

(1) EBITDAX: Earnings before Interest, Taxes, Depreciation, Depletion and Amortization , unrealized hedge gains/losses, and Exploration Expense.

EBITDAX (1)/ Interest, net (TTM)

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

• Reduced capital spending and operating costs improvements resulted in substantial available liquidity

and improvement in leverage and coverage measures

and improvement in leverage and coverage measures

• ~$50MM equity raise, and ~$160MM PDC and Lime Rock Partners joint venture to develop Marcellus

Shale and Shallow Devonian assets, reflected the company’s ability to access alternative capital

markets, and improve liquidity, leverage and coverage measures

Shale and Shallow Devonian assets, reflected the company’s ability to access alternative capital

markets, and improve liquidity, leverage and coverage measures

* Liquidity excludes $18.7 million L.C.

42

$305

$203

x

x

x

$80

See Slide 2 regarding Forward Looking Statements

2009 Adjusted Net

Income Reconciliation

Income Reconciliation

43

(1) Includes natural gas marketing activities.

|

|

Year Ended

|

|

|

December 31,

|

||

|

($ in millions, except per share data)

|

2009

|

2008

|

|

Net Income (loss) attributable to shareholders

|

($79.3)

|

$113.3

|

|

Unrealized loss (gain) on derivatives, net (1)

|

116.6

|

(117.5)

|

|

Provision for underpayment of gas sales

|

2.7

|

4.0

|

|

Tax effect of above adjustment

|

(43.0)

|

39.9

|

|

Adjusted Net Income (loss) attributable to

shareholders |

($2.9)

|

$39.7

|

|

Weighted average diluted shares outstanding

|

16,448

|

14,848

|

|

Adjusted diluted earnings (loss) per share

|

($0.18)

|

$2.67

|

See Slide 2 regarding Forward Looking Statements

2009 Adjusted Cash

Flow Reconciliation

Flow Reconciliation

44

|

|

Year Ended

|

|

|

December 31,

|

||

|

($ in millions, except per share data)

|

2009

|

2008

|

|

Net Cash provided by operating activities

|

$143.9

|

$139.1

|

|

Changes in assets and liabilities related to

operations |

26.3

|

60.8

|

|

Adjusted cash flow from operations

|

$170.2

|

$199.9

|

|

Weighted average diluted shares outstanding

|

16,448

|

14,848

|

|

Adjusted cash flow per share

|

$10.35

|

$13.46

|

See Slide 2 regarding Forward Looking Statements

2009 Adjusted

EBITDA Reconciliation

EBITDA Reconciliation

(1) Includes natural gas marketing activities.

45

|

|

Year Ended

|

|

|

December 31,

|

||

|

($ in millions, except per share data)

|

2009

|

2008

|

|

Net Income (loss) attributable to shareholders

|

($79.3)

|

$113.3

|

|

Unrealized loss (gain) on derivatives, net (1)

|

116.6

|

(117.5)

|

|

Interest, net

|

37.0

|

27.5

|

|

Income taxes expense (benefit)

|

(45.6)

|

61.5

|

|

Depreciation, depletion & amortization

|

131.0

|

104.6

|

|

Adjusted EBITDA

|

$159.7

|

$189.4

|

|

Weighted average diluted shares outstanding

|

16,448

|

14,848

|

|

Adjusted EBITDA per share

|

$9.71

|

$12.76

|

See Slide 2 regarding Forward Looking Statements

Q1 2010 Adjusted

Net Income Reconciliation

Net Income Reconciliation

46

(1) Includes natural gas marketing activities.

|

|

Three Months Ended

|

|

|

March 31,

|

||

|

(in millions, except per share data)

|

2010

|

2009

|

|

Net income (loss) attributable to shareholders

|

$23.7

|

($5.7)

|

|

Unrealized loss (gain) on derivatives, net (1)

|

(20.5)

|

13.2

|

|

Provision for underpayment of gas sales

|

-

|

2.6

|

|

Tax effect of above adjustments

|

7.7

|

(6.0)

|

|

Adjusted net income attributable to shareholders

|

$10.9

|

$4.1

|

|

Weighted average diluted shares outstanding

|

19.3

|

14.8

|

|

Adjusted diluted earnings per share

|

$0.57

|

$0.27

|

* Amounts may not foot due to rounding.

See Slide 2 regarding Forward Looking Statements

Q1 2010 Adjusted

Cash Flow Reconciliation

Cash Flow Reconciliation

47

|

|

Three Months Ended

|

|

|

March 31,

|

||

|

(in millions, except per share data)

|

2010

|

2009

|

|

Net cash provided by operating activities

|

$51.3

|

$35.9

|

|

Changes in assets and liabilities related to

operations |

(2.0)

|

3.9

|

|

Adjusted cash flow from operations

|

$49.3

|

$39.7

|

* Amounts may not foot due to rounding.

See Slide 2 regarding Forward Looking Statements

Q1 2010 Adjusted

EBITDA Reconciliation

EBITDA Reconciliation

(1) Includes natural gas marketing activities.

48

|

|

Three Months Ended

|

|

|

March 31,

|

||

|

(in millions, except per share data)

|

2010

|

2009

|

|

Net income (loss) attributable to shareholders

|

$23.7

|

($5.7)

|

|

Unrealized loss (gain) on derivatives, net(1)

|

(20.5)

|

13.2

|

|

Interest expense, net

|

7.8

|

8.4

|

|

Income tax expense (benefit)

|

14.3

|

(4.0)

|

|

Depreciation, depletion & amortization

|

28.4

|

34.4

|

|

Adjusted EBITDA

|

$53.7

|

$46.2

|

|

Weighted average diluted shares outstanding

|

19.3

|

14.8

|

|

Adjusted EBITDA per share

|

$2.78

|

$3.12

|

* Amounts may not foot due to rounding.

NASDAQ:PETD

PETROLEUM DEVELOPMENT

CORPORATION

CORPORATION

Investor Meetings

June 2010