Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT - NCR CORP | d8k.htm |

| EX-99.2 - PRESS RELEASE OF THE COMPANY, DATED MAY 17, 2010 - NCR CORP | dex992.htm |

NCR Investor

Presentation May, 2010

Exhibit 99.1 |

2

NCR Confidential

Note to Investors

Certain non-GAAP financial information regarding NCR’s operating results may be

discussed during this presentation. Reconciliation of the differences between GAAP and

non-GAAP measures are included elsewhere in this presentation and are available on

the Investor page of NCR’s website at www.ncr.com.

NCR reports its results in accordance with Generally Accepted Accounting Principles in the

United States, or GAAP. However, the Company believes that certain non-GAAP

measures found in this presentation are useful for investors. NCR’s management

evaluates the Company’s results excluding certain items, such as pension expense,

to assess the financial performance of the Company and believes this information is

useful for investors because it provides a more complete understanding of NCR’s

underlying operational performance, as well as consistency and comparability with past

reports of financial results. In addition, management uses earnings per share

excluding these items to manage and determine effectiveness of its business managers

and as a basis for incentive compensation. These non-GAAP measures should not

be considered as substitutes for or superior to results determined

in

accordance

with

GAAP.

A

full

description

of

these

non-GAAP

measures,

including free cash flow, are included in NCR’s SEC reports.

Remarks and responses associated with this presentation include forward-looking

statements that are based on current expectations and assumptions. These forward-looking

statements are subject to a number of risks and uncertainties that

could cause actual results

to

vary

materially.

These

risk

factors

are

detailed

from

time

to

time

in

NCR’s

SEC

reports, including, but not limited to, Forms 10Q, 10K, 8K and NCR’s annual report to

shareholders. NCR does not undertake any obligation to publicly update or revise any

forward-looking statements, whether as a result of new information, future events

or otherwise. These charts and the associated remarks are integrally related and are

intended to be presented and understood together. |

3

NCR Confidential

Vision and Mission

Our

Vision

Our

Vision

Our

Mission

Our

Mission

Leading how the world

Leading how the world

connects, interacts, and

connects, interacts, and

transacts with business.

transacts with business.

“Provide our customers with

the next generation of

productivity gains and

customer experience

innovation through our deep

knowledge of the changing

global consumer and

technology.” |

4

NCR Confidential

The NCR Story

NCR is a global leader in providing products and services that support

customer transactions

•

Number 1 or 2 globally in key solutions

•

At forefront of self-service revolution

•

Top Services provider across end-markets

Consumer demand for self-service technologies creates a global

opportunity that NCR is positioned to capture

•

Consumers are driving demand for self-service across all industries

•

Self-service technologies grow revenues, lower costs and increase

productivity •

Entertainment

market

–

a

$1

billion+

opportunity

over

the

next

5

years

NCR is executing on a multi-year program for improving execution and

efficiency

•

More than $600 million in cost takeout from 2003 to 2011

•

New manufacturing facilities in Brazil and Columbus, Georgia

NCR plans to optimize its capital structure and create value for

shareholders

•

$577 million in stock repurchases in 2007 and 2008

•

Pension strategy underway |

5

NCR Confidential

Revenue up 2% to $1.03B

Gross margin up 120 bps, inclusive of

negative 70 bps effect from Entertainment

NPOI

(1)

up 54% to $43M

Non-GAAP EPS ex pension expense

(1)

$0.15; up 150% from $0.06 in Q1 2009

Improved backlog driven by 18% increase

in orders; Double digit order growth

balanced; Financial & Retail

(1)

See reconciliation of GAAP to non-GAAP measures in the appendix to this

presentation and/or the Investor page of NCR’s

website Q1 2010 vs. Q1 2009 Financial Highlights |

6

NCR Confidential

NCR core vs. key competitors

•

Core produces more

revenue

•

Core produces more

profit

•

Core enterprise value is less than

competitors

Primary competitors

•

Trade at higher EBITDA and EPS

multiples based on 2010 analyst

consensus

Grow revenue

•

Low-mid single digit market growth

in core

•

Select strategic acquisitions to grow

faster than the secular market

•

New markets and new geographies;

adjacencies

Continue to manage costs and

increase productivity

•

Cost savings of $200-$250 million

from 2008 through 2011 (50% re-

invested)

Financials

•

Expect 2010 revenue of $125-

$150 million and approx. $30

million loss from operations

•

Goal to be breakeven

(EBITDA) by Q4 2010; goal

$25M-$35M positive EBITDA

in 2011

•

$1B+ revenue opportunity

Largest competitor

•

Consensus $1B+ revenue in

2010

•

EBITDA margin high-teens+

for DVD rental-only business

Brand

•

License to use Blockbuster

brand in the kiosk channel

Grow revenue

•

Build out kiosk network -

up

to 10k units by year-end 2010

•

Continued domestic and

international build-out in 2011

Create new category; higher

growth and margins than core

•

Only multi-channel, multi-

segment offer in industry

GAAP impacts

•

$1 billion underfunded status as of

2009 year end

•

$215 million expected expense in

2010

•

Majority of pension expense is

amortization of prior losses (non-

cash)

Cash impacts

•

Pre-tax net cash liability of ~$1

billion (~$750 million after-tax) as

of 2009 year end

•

Expect cash contributions of ~$110

million in 2010

Eliminate current underfunded

liability

•

Rebalance asset portfolio to fixed

income by end of 2012

•

Interest rate increases and asset

price improvement would reduce

the underfunded position

Eliminate future volatility of plan

expense and funded status

•

Match assets and liabilities

Overview:

Core Business

Core Business

Entertainment

Entertainment

Pension

Pension

Overview of NCR’s Business

Strategy: |

7

NCR Confidential

Financial Industry Growth Opportunities

Ongoing roll-out of advanced ATM technologies

at large banks

•

Intelligent deposit & remittance are top apps

•

Customers building competitive advantage

•

NCR the global leader in multi-vendor software for self-

service¹

Other sectors of banking industry expected to

narrow the technology gap over the next 12-

36 months

Strong

adoption

rate

of

our

Self-Serv

line

of

ATM’s –

most successful launch in company

history

Continued business strength in emerging

markets

•

Extending ATM leadership in China

•

Continued progress in India –

secured largest ATM

order in country’s history

*1 Source: RBR |

8

NCR Confidential

Emerging Regions will Continue to Grow

Caribbean & Latin America

+58k Units

Target ATM/100K ppl: 40 ATMs

Current Penetration: ~ 22 ATMs

Caribbean & Latin America

+58k Units

Target ATM/100K ppl: 40 ATMs

Current Penetration: ~ 22 ATMs

Middle East & Africa

+278k Units

Target per 100k ppl: 40 ATMs

Current Penetration: ~ 6 ATMs

Middle East & Africa

+278k Units

Target per 100k ppl: 40 ATMs

Current Penetration: ~ 6 ATMs

Eastern Europe

+172k Units

Target per 100k ppl: 80 ATMs

Current penetration: ~ 40 ATMs

Eastern Europe

+172k Units

Target per 100k ppl: 80 ATMs

Current penetration: ~ 40 ATMs

Northern Asia Pacific

+374k Units

Target ATM/100K ppl: 40 ATMs

Current Penetration: ~ 12 ATMs

Northern Asia Pacific

+374k Units

Target ATM/100K ppl: 40 ATMs

Current Penetration: ~ 12 ATMs

Southern Asia Pacific

+587k Units

Target ATM/100K ppl: 40 ATMs

Current Penetration : ~ 5 ATMs

Southern Asia Pacific

+587k Units

Target ATM/100K ppl: 40 ATMs

Current Penetration : ~ 5 ATMs

*Based on target ATM penetration threshold of at least 40 ATMs per hundred thousand

population in all regions except Eastern Europe (80 ATMs per hundred thousand

population) Source:

Worldbank

Database,

Retail

Banking

Research,

NCR

Internal

Analysis

Fewer

than

30

ATM

markets

globally

have

reached

a

“developed

state”

threshold

.

. .

Still potential for another 1.4 million ATMs in emerging countries

|

9

NCR Confidential

Manufacturing Efficiencies –

New Facilities

Manaus, Brazil

•

Strengthen our position and capabilities in the world’s

3rd

largest ATM market

•

Capitalize on self-service ATM demand in Brazil and

surrounding regions

•

Well positioned for Intelligent Deposit

•

In-country R&D and manufacturing serves as key

competitive advantage

Columbus, Georgia

•

North American ATM manufacturing brought in-house

to

reduce costs and improve lead times

•

Engineering, services and operations co-located

•

Ability to improve products through integration

of manufacturing, design and services

Both facilities shipped product during Q1 2010 |

10

NCR Confidential

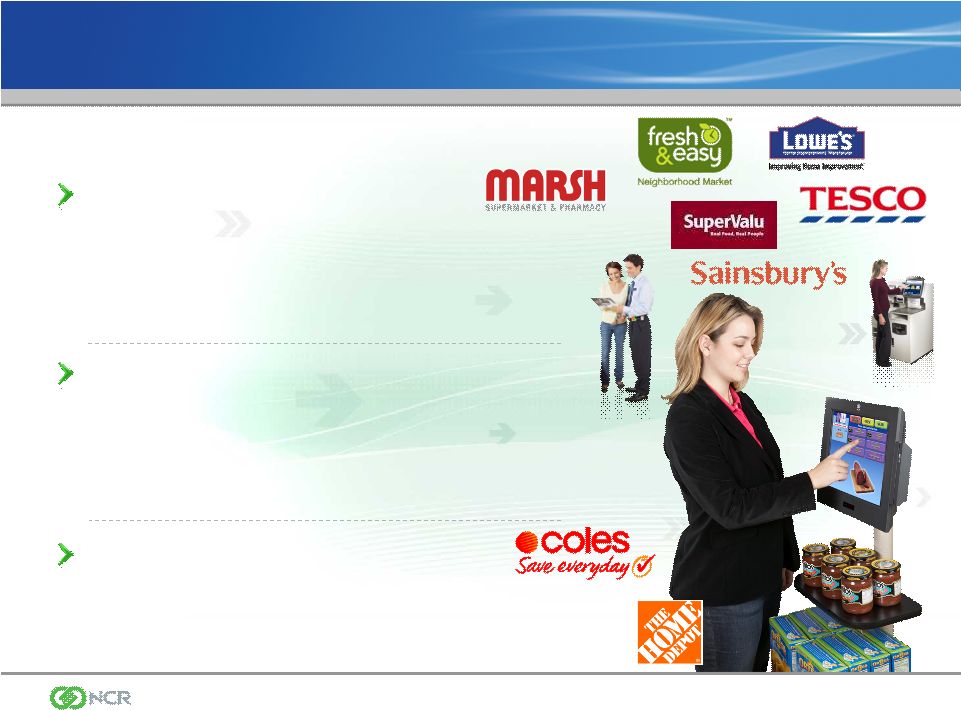

Self-Service Has Become a Retail Imperative

NCR SelfServ

Checkout

•

Market-leading solution installed in 22 countries

•

> 65k units installed at > 150 global retailers;

penetration rate in grocery channel of ~ 20% with

potential to achieve 90% + over the next ten years

•

Strongest value proposition; density of placements

improving from initial 4-unit installation

•

Launched Release 5.0 latest generation

-

Compact design for convenience, drug, and space

constrained retailers

-

Note and Coin Recycling

-

2ST

-

Usability enhancements

-

NCR APTRA Vision for systems management

•

Self-checkout now accounts for 20% of Tesco’s

transactions in U.K., and 100% in US Fresh & Easy

subsidiary

•

"The retailer (ASDA) is saving money with the shift

to self-scan checkouts -

with staff deployed

elsewhere -…" *

*Source: The Guardian |

11

NCR Confidential

Retail Industry Growth Opportunities

Offering leading edge solutions

•

NCR Advanced Marketing Solution in-store offer

delivery platform in use at multiple Tier 1 U.S.

Grocers (Marsh Supermarkets), Drug and C-stores

•

Broadest range of POS applications covering Food,

GMS and Hospitality

•

Software solution more relevant; higher value-add

Strong value proposition

•

Expertise in retail self-service channels. #1 in self-

checkout in key customers such as Tesco, Sainsbury

and SuperValu

•

Self-service offers economic advantages and

ability to differentiate and improve customer service

Expand advance product suite

•

NCR Netkey acquisition –

deliver a growing range of

multi-industry digital signage and self-service applications

|

12

NCR Confidential

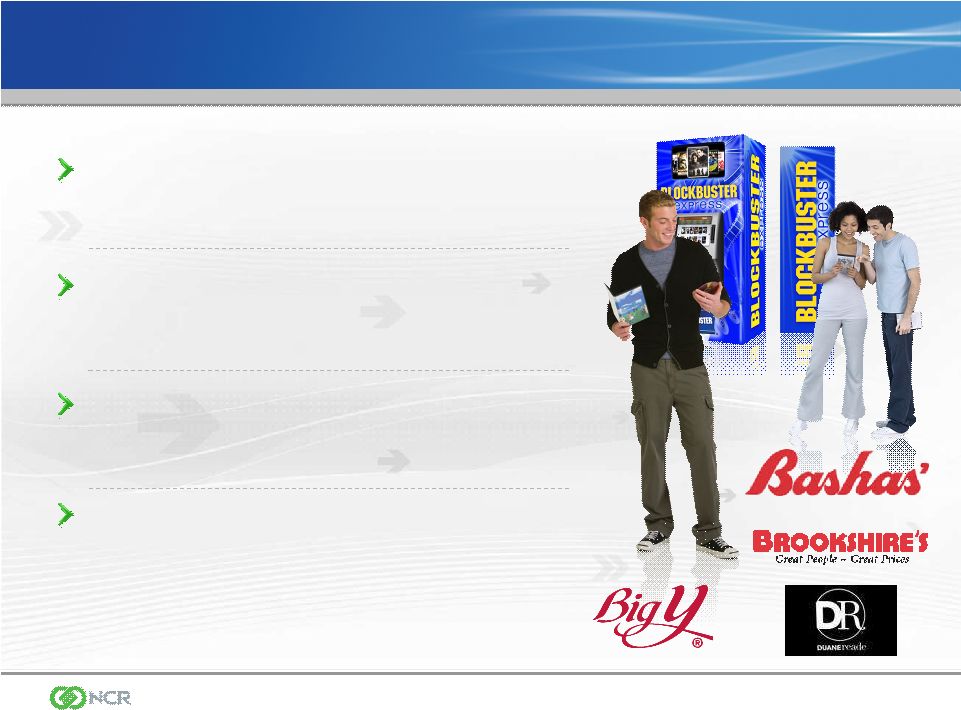

Entertainment: NCR’s 3

rd

Vertical

Entertainment

is

a

$1B

growth

opportunity

currently

available

to

NCR

-

“Third Vertical”

that will validate multi-industry self-service strategy

•

Number 1 or 2 globally in key solutions

•

At forefront of self-service revolution

•

Top services provider across end markets

Acquisition of TNR and DVD Play and partnership with Blockbuster

gives

NCR an installed base and customer relationships from which to ramp under

ISO model.

Working

with

movie

studios

–

expect

announcement

over

next

several

months.

Consumption

habits

continue

to

change

-

NCR

is

well

positioned

Packaged media will continue to grow modestly, driven by consumer preference and

migration to Blu-Ray

DVD kiosk business is a proven model with near-term opportunity for competitive entry

– share of video rental market could triple by end of 2010

NCR kiosks deployed are digital download ready

Consumer

shift

to

Kiosks

driven

by

value

and

convenience;

Kiosks

potential

to

be

50%

of ~

$8B

DVD

rental

market

within

3

years

•

•

•

• |

13

NCR Confidential

Differentiated Entertainment Solutions

NCR Application Capabilities

•

DVD Rental

•

Packaged Media Sell-Through

•

Capacity

and Title Depth

•

Digital Download and Portability

•

Games

•

Buy, Sell, Trade

•

In-store and Outdoor Kiosk

•

Home |

14

NCR Confidential

Execution Roadmap

Expect to deploy up to 10,000 kiosks by year-

end 2010 –

capitalize on rapid transition of

DVD rental share

Customer wins underscore market demand

•

Growing customer base -

deployments across high

traffic areas (supermarkets, convenience food shops)

$85 million investment in 2010 ($75M capex)

•

Expect revenue of $125M-$150M in 2010; goal to be

EBITDA break-even in Q4 2010

Expect to generate positive EBITDA in the

range of $25M-$35M in FY 2011 -

Goal to be

EBIT breakeven by Q4 2011 (based on 10K

units installed) |

15

NCR Confidential

Emerging Industry Profiles

Travel & Lodging

Healthcare & Public Sector

Telecom & Technology

•

Patient Registration

•

Revenue Cycle Management

•

Lab Results

•

Patient Portal

•

Rx Management

•

Airline Check-in

•

Car Rental

•

Hotel/Resort Registration

•

Restaurant Order and Pay

•

Gaming

•

Multi-billion dollar market

•

Network design & implementation

•

Wireless implementation

•

Telco Bill Pay

-

No. 1 in Airline Check-in

-

4 of the Top 10 QSR Operators

-

Most widely deployed

CUSS platform

-

No. 1 in Healthcare

Self-Service Patient

Registration

-

Largest Global Postal

Deployment

-

Preferred

international

services

implementation

provider

for

networking

and

telco

solutions

to

global

corporations |

16

NCR Confidential

NCR the Largest Services Provider in Our Industry

NCR the largest provider across our end

markets

•

Powers over 2 million consumer points of service

worldwide

•

Designed to grow/scale capability/leverage into

new industries

•

Strategically aligned with Engineering and

Operations

NCR is also the largest managed service

provider in our industry

Poised to continue as a growth driver for

the company

•

Opportunity for margin expansion through

productivity and innovation

•

Global market leader-in managed services offers |

17

NCR Confidential

Financial Summary

Expecting

improved

performance

in

2010

and

progress

towards

long

term

goals

2010 Guidance

•

Revenue growth of 2-5%; NPOI

(1)

in range of $310-$330 million (includes estimated $30M

loss from Entertainment business)

•

GAAP

diluted

EPS

of

$0.39-$0.49;

non-GAAP

diluted

EPS

excluding

pension

expense

(1)

of

$1.35 -

$1.45 (includes approx. $0.15 negative impact from

Entertainment investment) •

Breakeven free cash flow (includes $85M investment in Entertainment)

Executing our multi-year operating plan calling for NPOI margin

improvement driven by profitable revenue growth, cost structure and

working capital improvements

Self-service demand will be a secular driver of our revenue growth in

core solutions and in new verticals like Entertainment

NCR’s balance sheet and cash flow generation capability support an

environment of growth, investment and enhanced returns to

shareholders

(1)

See

reconciliation

of

GAAP

to

non-GAAP

measures

in

the

Appendix

to

this

presentation

and/or

the

Investor

page

of

NCR’s

website. |

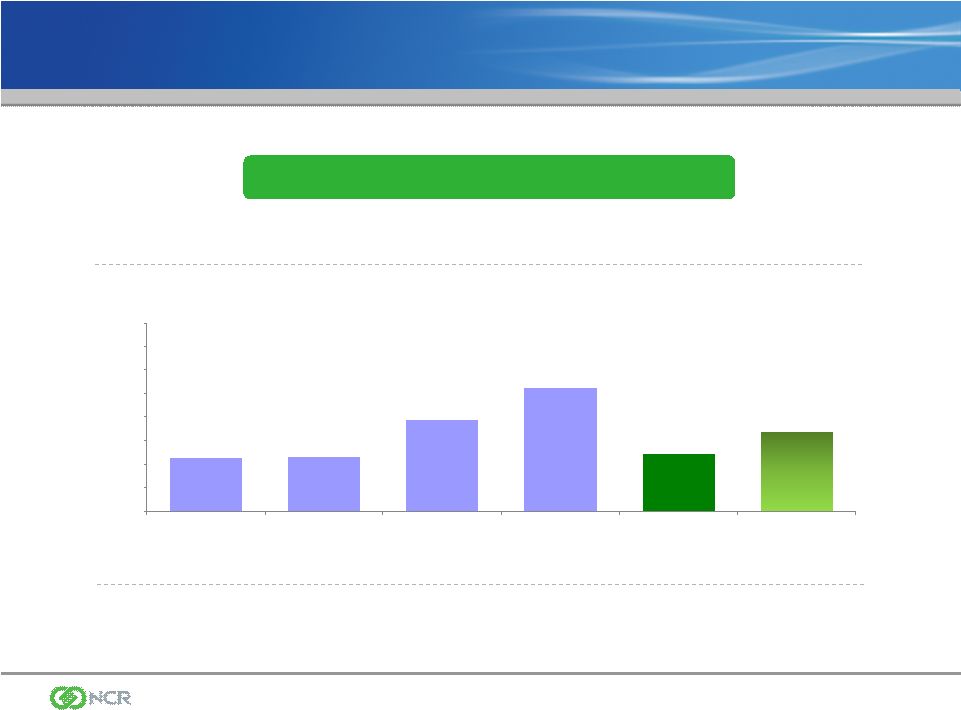

18

NCR Confidential

Revenue Performance

Revenue from Continuing Operations

$4,000

$4,250

$4,500

$4,750

$5,000

$5,250

$5,500

$5,750

$6,000

2005

2006

2007

2008

2009

2010(e)

$4,561m

$4,582m

$4,970m

$5,315m

$4,612m

+1%

+8%

+7%

-12%

+2% to 5% |

19

NCR Confidential

Managing for Margin

Reducing our Cost Structure

Key Initiatives

•

Value engineering

•

Product lifecycle management

•

Efx

= Servicability, manufacturability and quality

•

Continuous improvement organization installed

•

Streamlined organization

•

Accelerating labor costs & expense reduction

$200 million to $250 million savings for

the period 2008-2011 (50% reinvested) |

20

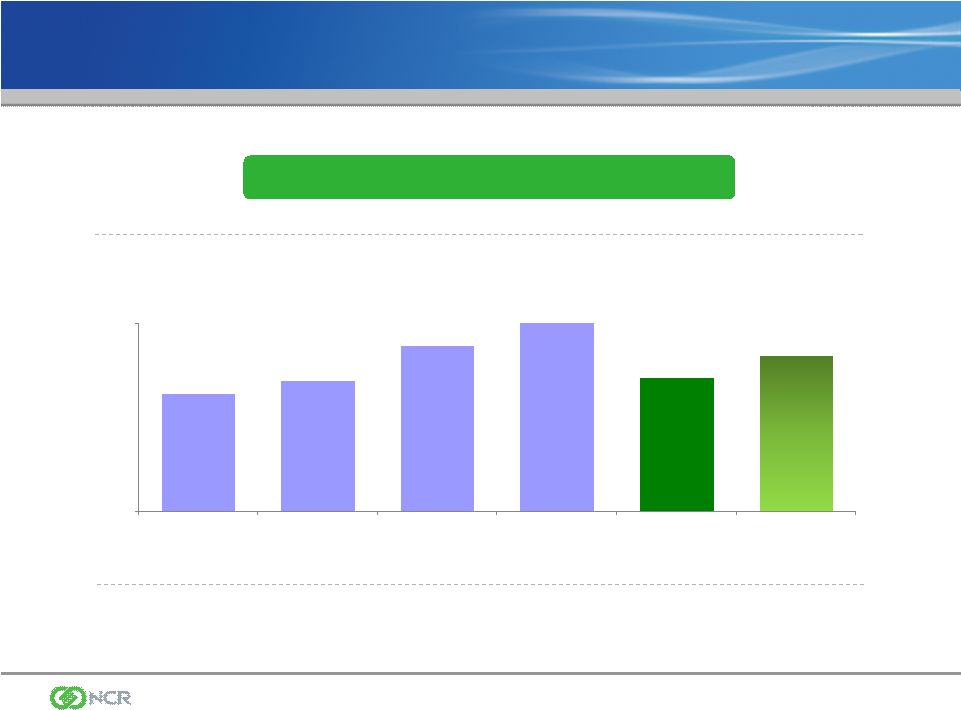

NCR Confidential

NPOI: Poised to Return to Growth

NPOI: Non Pension Operating Income

(1)

$0

$400

2005

2006

2007

2008

2009

2010(e)

$248m

$276m

$349m

$400m

$284m

$310m -

$330M

+11%

+26%

+15%

-29%

+9% to 16%

(1)

See reconciliation of GAAP to non-GAAP measures in the Appendix to this presentation

and/or on the Investor page of NCR’s

website

|

21

NCR Confidential

Strong Balance Sheet

Cash balance

$451

Debt balance

$ 15

Net cash position

$436

12.31.09

12.31.09

Near Term Objectives

•

Liquidity

•

Financial Flexibility

•

Working Capital Improvements

Long Term Objectives

•

Free Cash Flow generation

($ in Millions) |

22

NCR Confidential

Pension Management Strategy

•

Global underfunded status of $1,048M at 12/31/09; improved to approximately $990M

(A)

underfunded status at 3/31/10 (see appendix #29)

•

Historically NCR has seen significant volatility (see appendix #33 and 34). Pension

strategy is to reduce

volatility

and

riskiness

of

plan

assets

over

a

three

year

period

•

Shift asset allocation of US Pension Plans to 100% fixed income by the end of 2012

–

Target 60% by end of 2010, 80% by end of 2011, and 100% by end of 2012. Mostly high grade

corporate bonds

with

an

overall

duration

that

approximates

the

duration

of

the

liability

–

No cash contribution for U.S. qualified plan is expected to be required until 2012 (see

appendix #29) –

Pension legislation could provide significant relief (see appendix #32)

–

US underfunded position at $822M at 12/31/09. Significant upside if interest rates rise

or asset returns improve (see sensitivity appendix on #35)

•

For International Pension Plans, work with local pension trustee

boards to make similar changes

in asset allocation

–

International underfunded position of $226M at 12/31/09 ($470M of underfunded plans offset by

$244M overfunded plans (see appendix #29)

–

Funding

of

international

plans

expected

to

decline

significantly

after

2013,

reaching

an

annual

amount of

$10-$20M

(excluding

the

funding

of

future

service

cost)

by

2015

as

some

underfunded

plans

reach

fully

funded status (see appendix #29)

–

Due

to

pension

plan

closures,

service

cost

expected

to

gradually

decline

from

~$15M

in

2010

to

~$10M

per year (see appendix #34)

Actions to Address Pension

(A)

Estimated

based

on

data

available

at

March

31,2010;

for

accounting

purposes

the

pension

plans

are

not

marked-to-market

on

a

quarterly

basis |

23

NCR Confidential

3-Year Vision for NCR

Leading Financial Solutions

provider

Leading Retail Solutions

provider

Leader in Hospitality, Travel,

Gaming and Healthcare

Solutions

Multi-Channel leadership

Leader in Managed Services;

50% recurring revenue

stream

Sustainable, industry

leading cost structure

Continued significant cash

flow production

#1 or #2 market share

leader in DVD Kiosk Market

(US & Intl)

Physical DVD rental & sell-

through; digital download

leadership “Automated

Retail”

Market leader in multi-

channel distribution of

digital entertainment media

High growth; Significant

EBITDA; Positive cash flow

Brand leadership

Under-funded pension

position significantly

reduced

Volatility and risk of

current pension asset

allocation eliminated

Core Business

Entertainment

Pension |

24

NCR Confidential

NCR Value Equation

Strong NPOI, EBITDA and

Operational EPS

Core Markets (excluding

Entertainment business)

NPOI of $340-$360M in 2010

EBITDA pre Pension of $465-

$485M in 2010

Operational EPS of $1.50 to

$1.60 in 2010

PE and EBITDA multiples

should

increase

to

historical

averages due to reduced

pension volatility and leadership

position in core markets

Bulk of investing

complete by 2010 y/e

–

$85M investment, $30M

NPOI loss and approx.

negative $0.15 EPS in

2010

+ $25-$35M of EBITDA

in 2011

Potential EBITDA multiple

of 10X or $250 -

$350M

valuation benefit

Less

after tax

underfunded position of

~$750M at 12/31/09

Less

after tax present

value of future service

cost (not included in

liability above) of ~$90M

Less

after

tax

present

value of post retirement

obligation of ~$80M at

12/31/09

Plus

net cash on balance

sheet of ~$436M at

12/31/09

Core Business

Entertainment

Pension + Other B/S

Items |

25

NCR Confidential

Why Invest in NCR?

Positioned for success

•

Growth strategy

•

Expanding market leadership

•

Global share and balance

•

Marquee customers

•

Strong balance sheet

•

Compelling value propositions

•

World-class employees

•

Track record is one of execution

•

Growth initiatives

•

Cost structure initiatives |

26

NCR Confidential

Appendix |

27

NCR Confidential

Reconciliation of GAAP to non-GAAP Measures

$ 284

$310 -

$330

$ 28

$ 43

Non-Pension Operating Income (non-GAAP)

159

215

38

56

Pension Expense

6

5

-

5

Global Headquarters Relocation

22

-

-

-

Impairment of Assets Related to Equity Investment

$ 97

$90 -

$110

$ (10)

$ (18)

Income (Loss) from Operations (GAAP)

FY 2009

FY 2010

2009

2010

Actual

Guidance

Q1

Q1

$ 1.27

$1.35 -

$1.45

$ 0.06

$ 0.15

Diluted Earnings Per Share (non-GAAP)

(0.67)

(0.94)

(0.15)

(0.25)

Pension Expense

(0.03)

-

-

-

Litigation Charge

(0.03)

(0.02)

-

(0.02)

Global Headquarters Relocation

(0.18)

-

(0.03)

-

Impairment of Equity Investment and Related Assets

(0.57)

-

0.03

-

Fox River Environmental Matter, Net

$ (0.21)

$0.39 -

$0.49

$ (0.09)

$ (0.12)

Diluted Earnings (Loss) Per Share (GAAP)

FY 2009

FY 2010

2009

2010

Actual

Guidance

Q1

Q1

$ 50

$ -

Free Cash Flow (non-GAAP)

(173)

(215)

Net Capital Expenditures

$ 223

$ 215

Cash Provided by Operating Activities (GAAP)

FY 2009

FY 2010

Actual

Guidance

Income (Loss) from Operations (GAAP) to Non-Pension Operating Income (non-GAAP)

Diluted Earnings (Loss) Per Share (GAAP) to Diluted Earnings Per

Share (non-GAAP)

Cash Provided by Operating Activities (GAAP) to Free Cash Flow (non-GAAP)

|

28

NCR Confidential

NCR trades at a material discount to the market and its peers, largely due

to the current pension situation

Pension assets invested in equities are not only volatile, but correlated with

NCR’s operating businesses

A significant portion of NCR’s capital is allocated to its “pension-

management”

business

•

This allocation has limited NCR’s ability to invest in our core operating businesses and

to provide immediate shareholder returns

•

Under-utilization of NCR balance sheet

To fix the valuation gap, NCR plans to:

•

Reduce risk and volatility by re-allocating our domestic pension portfolio to

fixed- income securities by year-end 2012

•

Direct freed-up risk-taking capacity to the highest value-added investment

alternatives: organic investments, strategic acquisitions

•

Fund the pension plan according to regulatory requirements (i.e., do not pre-fund)

Addressing NCR’s Valuation Gap |

29

NCR Confidential

NCR Pension Update –

Q1 2010

Cash

Funding

for

Pension

Plans

2008

2009

2010E

2011E

2012E

2013E

US Qualified Plan**

0

0

0

0

125

175

US Non-qualified Plan

9

9

10

10

10

10

International Plans***

74

74

100

115

115

115

Total

83

83

110

125

250

300

Pension

Metrics

&

Funded

Status

Asset

Return Discount rate

Funded

Status

3/31/10

YTD

(A)

12/31/09

3/31/10

(A)

12/31/09

3/31/10

(A)

US Plans

3.5%

5.75%

5.88%

(822)

(740)

International Plans

2%

4.9%

4.8%

(226)*

(250)

Global

2.9%

5.4%

5.45%

(1,048)

(990)

( $ Millions)

( $ Millions)

The estimated improvement in the global funded status was approximately $58m in

Q1 *The ($226m) net funded status of international plans is comprised

underfunded plans of ($470m), and overfunded plans of $244m The overfunded

plans are a result of local funding methodologies that use more conservative

actuarial assumptions than GAAP ** The funding requirement for

the US qualified plan assumes no funding relief legislation *** The funding of

international plans is expected to decline significantly after 2013 reaching an annual amount of $10-$20 million

(excluding the funding of future service cost) by 2015 as some of the underfunded

plans reach fully funded status Due to pension plan closures, service

cost is expected to decline to a level of about $10m per year (see slide #34)

All future funding estimates are approximations based on expected asset returns,

discount rates, and local requirements (A) Estimated based on data available at March

31,2010; for accounting purposes the pension plans are not marked-to-market on a quarterly basis |

30

NCR Confidential

US Plans Only

–

Funded Status Bridge

•

Funded

Status

of

US

Plans

improved

~$82m

in

Q1

to

(740m)

•

Improvement

was

due

to

good

asset

returns

and

a

13bp

increase

in

discount

rate

Liabilities

Assets

Benefit

Payments

Asset

Returns

Fees &

Expenses

Asset Value,

12/31/09

(52)

(6)

2,610

Asset Value,

3/31/10

Benefit

Payments

Interest

Liability Value,

12/31/09

(54)

46

3,350

Liability Value,

3/31/10

88

2,580

3,402

(44)

Discount Rate

Movement

($Millions)

Funded Status

(822)

(740)

+2

+38

+42

(A)

(A)

(A)

(A)

(A) Estimated based on data available at March 31,2010; for accounting purposes the pension

plans are not marked-to-market on a quarterly basis |

31

NCR Confidential

Shift pension asset allocation to 100% fixed income by end of 2012

•

Risk of equity exposure in pension plan must be reduced

–

Size of NCR pension plan (and therefore the associated risk) is disproportionate to the size

of NCR –

Riskiness and volatility of pension plan increases stock price volatility and places a

discount on the stock price –

The US pension plan is closed and the duration of the liability is becoming shorter

•

Shifting over 3 years allows for some additional recovery from the recent market downturn

–

Potential additional upside in the equity markets and/or benefit from increase in the

discount rate Pre-fund of US pension plan analyzed

•

Given NCR’s tax position, there is not a compelling financial benefit for NCR to fund

early –

NCR has minimal near-term U.S. tax liability, so cannot take advantage of accelerating

tax deductions by funding earlier than required

–

Similarly,

would

not

be

able

to

take

advantage

of

tax

deductions

for

interest

expense

(if

funded

with

debt)

•

Inefficient capital allocation

–

The

underfunded

pension

liability

is

analogous

to

unsecured

debt

of

NCR.

NCR

has

no

other

outstanding

debt.

We

believe

we

have

better

investment

uses

for

our

cash

balances

and

operating

cash

flow

than

choosing

to

pre-pay

debt

at

the present time

•

Cash flow deployed into business opportunities

–

No cash funding is projected to be required for the U.S. qualified pension plan in 2010 or

2011 –

A

pre-fund

now

does

not

materially

change

required

funding

in

2012

and

2013

Rationale –

Analyzed Various Options |

NCR Confidential 32

Possible Impact of Pension Funding Relief

Legislation on NCR

Two relief options; 2+7 and 15-year vs. current

law

Two options potentially subject to “cash flow

rules”

(e.g., limits on employee compensation,

dividends, and stock redemption)

Balanced legislation passed in Senate –

provides relief; currently bill in House Ways and

Means Committee; anticipated closure by Q3

2010

Key

Provisions

Impact on NCR

Conditions

Status

2+7 vs.

Current Law

Provides marginal

relief. NCR not

likely to use.

Senate: 2 yrs of

cash flow rules

House: 3 yrs TBD

Senate: passed

House: TBD

15-Year vs.

Current Law

Likely provides

meaningful relief for

NCR.

Senate: 5 yrs of

cash flow rules

House: 3-5 yrs of

cash flow rules

and “active plan”

requirement

Senate: passed

House: active

plan issue

Investment

Expenses not

Included in

Normal Cost

Helpful to NCR.

N/A

Senate: not

addressed

House: TBD

NCR Leading Industry Coalition to

Secure Passage of Pension Relief

Possible Impact of Pension Funding

Relief Legislation on NCR

Pension Legislation Could Provide Relief |

33

NCR Confidential

Plan

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

U.S. Plans

$3,026

$2,686

$2,208

$2,797

$3,016

$3,098

$3,385

$3,423

$2,208

$2,582

International Plans

1,514

1,089

1,138

1,397

1,658

1,748

2,085

2,114

1,467

1,737

Total Plans

$4,540

$3,775

$3,346

$4,194

$4,674

$4,846

$5,470

$5,537

$3,675

$4,319

Plan

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

U.S. Plans

$2,408

$2,494

$2,700

$2,960

$3,194

$3,372

$3,290

$3,199

$3,227

$3,404

International Plans

1,185

1,127

1,380

1,635

1,939

1,932

2,046

2,020

1,645

1,963

Total Plans

$3,593

$3,621

$4,080

$4,595

$5,133

$5,304

$5,336

$5,219

$4,872

$5,367

Plan

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

U.S. Plans

$618

$192

($492)

($163)

($178)

($274)

$95

$224

($1,019)

($822)

International Plans

329

(38)

(242)

(238)

(281)

(184)

39

94

(178)

(226)

Total Plans

$947

$154

($734)

($401)

($459)

($458)

$134

$318

($1,197)

($1,048)

Pension Assets

Pension Liability

Funded Status

($ Millions)

NCR Historical Pension Overview |

34

NCR Confidential

Historical Funded Status, Funding and Expense

($ Millions)

Plan

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

U.S. Plans

126%

108%

82%

94%

94%

92%

103%

107%

68%

76%

International Plans

128%

97%

82%

85%

86%

90%

102%

105%

89%

88%

Total Plans

126%

104%

82%

91%

91%

91%

103%

106%

75%

80%

Plan

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

All Plans

62

59

55

70

111

110

112

92

83

83

Plan

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

All Plans

(124)

(124)

(74)

105

135

150

145

44

25

159

Plan

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

All Plans

78

77

76

88

89

87

89

38

27

17

Funded Status

Pension Funding

Pension Expense / (Income)

Service Cost

NCR has experienced significant volatility in the funded status of its pension plans

over the years NCR’s focus moving forward will be to manage and reduce

the risk of funded status volatility Due to pension plan closures, the annual

service cost is expected to continue to decline to approximately $10m There are approximately 20

international plans, with approximately half still open at this time. |

35

NCR Confidential

(A) Assumes 6% at end 2010, 6.25% at end of 2011, and 6.5% at end of 2012

(B) Contribution required for US Qualified plan in 2012 (no required contribution

expected in 2010 or 2011), also assumes no pension reform legislation

(C) Includes the impact of contributions on funded status

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

10 yr

avg

20 yr

avg

Asset Returns

-2%

-6%

-12%

36%

15%

10%

16%

7%

-31%

28%

4%

10%

Discount Rate

7.5%

7.3%

6.8%

6.3%

5.8%

5.5%

5.8%

6.3%

6.3%

5.8%

6.3%

7.0%

Historical Asset Returns and discount Rates for US Plan

($ Millions)

Projected Funded Status $ Contributions –

Sensitivity Analysis

Discount Rate remains at 5.75%

Discount Rate increases to 6.5%

(A)

Scenario

Annual Equity

Returns

through 2012

Required

Contribution in

2012

(B)

Projected

Funded Status

12/31/2012

(C)

Required

Contribution in

2012

(B)

Projected

Funded Status

12/31/2012

(C)

3 yr. shift to 100% fixed income

5%

$145

($880)

$130

($770)

3 yr. shift to 100% fixed income

10%

$125

($775)

$115

($670)

3 yr. shift to 100% fixed income

15%

$115

($670)

$100

($565)

Funded Status as of 12/31/2009 = ($822)

Sensitivity Analysis -

US Plans ONLY |