Attached files

| file | filename |

|---|---|

| EX-21 - EX-21 - A.G. Volney Center, Inc | v182501_ex21.htm |

| EX-3.3 - EX-3.3 - A.G. Volney Center, Inc | v182501_ex3-3.htm |

| EX-2.1 - EX-2.1 - A.G. Volney Center, Inc | v182501_ex2-1.htm |

| EX-10.6 - EX-10.6 - A.G. Volney Center, Inc | v182501_ex10-6.htm |

| EX-10.2 - EX-10.2 - A.G. Volney Center, Inc | v182501_ex10-2.htm |

| EX-10.1 - EX-10.1 - A.G. Volney Center, Inc | v182501_ex10-1.htm |

| EX-10.5 - EX-10.5 - A.G. Volney Center, Inc | v182501_ex10-5.htm |

| EX-10.3 - EX-10.3 - A.G. Volney Center, Inc | v182501_ex10-3.htm |

| EX-10.4 - EX-10.4 - A.G. Volney Center, Inc | v182501_ex10-4.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

FORM

8-K

CURRENT

REPORT

Pursuant

to Section 13 or 15(d) of the

Securities

Exchange Act of 1934

Date of

Report (Date of Earliest event Reported): April 28, 2010

A.G.

Volney Center, Inc.

(Exact

name of registrant as specified in its charter)

|

Delaware

|

000-52269

|

13-4260316

|

||

|

(State

or other jurisdiction of

incorporation

or organization)

|

|

(Commission

File Number)

|

|

(IRS

Employer Identification

No.)

|

Dachang Hui Autonomous

County

Industrial Park

Hebei, 065300 People’s Republic of

China

(Address

of principal executive offices)

Telephone

– +86 316 8864783

(Former

Address)

124

Lincoln Avenue South

Liverpool,

New York 13088

Check the

appropriate box below if the Form 8-K filing is intended to simultaneously

satisfy the filing obligation of the registrant under any of the following

provisions (see

General Instruction A.2. below):

o

Written communications pursuant to Rule 425 under the Securities Act (17 CFR

230.425)

o

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR

240.14a -12)

o

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act

(17 CFR 240.14d -2(b))

o

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act

(17 CFR 240.13e -4(c))

SPECIAL

NOTE REGARDING FORWARD LOOKING STATEMENTS

This

report contains forward-looking statements. The forward-looking statements are

contained principally in the sections entitled “Description of Business,” “Risk

Factors,” and “Management’s Discussion and Analysis of Financial Condition and

Results of Operations.” These statements involve known and unknown risks,

uncertainties and other factors which may cause our actual results, performance

or achievements to be materially different from any future results, performances

or achievements expressed or implied by the forward-looking statements. In some

cases, you can identify forward-looking statements by terms such as

“anticipates,” “believes,” “could,” “estimates,” “expects,” “intends,” “may,”

“plans,” “potential,” “predicts,” “projects,” “should,” “would” and similar

expressions intended to identify forward-looking statements. Forward-looking

statements reflect our current views with respect to future events and are based

on assumptions and subject to risks and uncertainties. Given these

uncertainties, you should not place undue reliance on these forward-looking

statements. These forward-looking statements include, among other things,

statements relating to:

|

|

·

|

Our

ability to produce cold rolled steel at a profitable

margin;

|

|

|

·

|

the

impact that a downturn or negative changes in the steel market may have on

sales;

|

|

|

·

|

our

ability to obtain additional capital in future years to fund our planned

expansion;

|

|

|

·

|

economic,

political, regulatory, legal and foreign exchange risks associated with

our operations; or

|

|

|

·

|

the

loss of key members of our senior management and our qualified sales

personnel.

|

Also,

forward-looking statements represent our estimates and assumptions only as of

the date of this report. You should read this report and the documents that we

reference and filed as exhibits to the report completely and with the

understanding that our actual future results may be materially different from

what we expect. Except as required by law, we assume no obligation to update any

forward-looking statements publicly, or to update the reasons actual results

could differ materially from those anticipated in any forward-looking

statements, even if new information becomes available in the

future.

Use

of Certain Defined Terms

Except

where the context otherwise requires and for the purposes of this report

only:

|

|

·

|

the

“Company,” “we,” “us,” and “our” refer to the combined business of (i)

A.G. Volney Center, Inc. or “AG Volney,” a Delaware corporation, (ii) Gold

Promise Group (Hong Kong) Co., Limited, or “Gold Promise,” a Hong Kong

limited company and wholly-owned subsidiary of AG Volney, (iii)

Hebei Anbang Investment Consultation Co., Ltd., or “Hebei Consulting,” a

Chinese limited company and wholly-owned subsidiary of Gold Promise, and

(iv) Dachang Hui Autonomous County Baosheng Steel Products Co., Ltd., or

“Buddha,” a Chinese limited company which is effectively and substantially

controlled by Hebei Consulting through a series of captive agreements, as

the case may be;

|

|

|

·

|

“BVI”

refers to the British Virgin

Islands;

|

|

|

·

|

“Exchange

Act” refers to the Securities Exchange Act of 1934, as

amended;

|

|

|

·

|

“Hong

Kong” refers to the Hong Kong Special Administrative Region of the

People’s Republic of China;

|

|

|

·

|

“PRC,”

“China,” and “Chinese,” refer to the People’s Republic of China (excluding

Hong Kong and Taiwan);

|

|

|

·

|

“Renminbi”

and “RMB” refer to the legal currency of

China;

|

|

|

·

|

“Securities

Act” refers to the Securities Act of 1933, as amended;

and

|

|

|

·

|

“U.S.

dollars,” “dollars” and “$” refer to the legal currency of the United

States.

|

In this

current report we are relying on and we refer to information and statistics

regarding the steel industry and economy in China and that we have obtained from

various cited government and institute research publications. Much of this

information is publicly available for free and has not been specifically

prepared for us for use or incorporation in this current report on Form 8-K or

otherwise. We have not independently verified such information, and you should

not unduly rely upon it.

ITEM

1.01

ENTRY

INTO A MATERIAL DEFINITIVE AGREEMENT

On April

28, 2010, we entered into and closed a share exchange agreement, or the Share

Exchange Agreement, with Gold Promise Group (Hong Kong) Co., Limited, or “Gold

Promise,” the shareholders of Gold Promise, Joseph C. Passalaqua, Carl E.

Worboys and Dachang Hui Autonomous County Baosheng Steel Products Co.,

Ltd., or “Buddha,” pursuant to which we acquired 100% of the issued and

outstanding capital stock of Gold Promise in exchange for 10,000 shares of our

Series A Convertible Preferred Stock (Series A Preferred Stock), which

constituted 98.75% of our issued and outstanding capital stock on an

as-converted to common stock basis as of and immediately after the consummation

of the transactions contemplated by the Share Exchange Agreement.

The

foregoing description of the terms of the Share Exchange Agreement is qualified

in its entirety by reference to the provisions of the agreement filed as Exhibit

2.1 to this report, which are incorporated by reference herein.

ITEM

2.01

COMPLETION

OF ACQUISITION OR DISPOSITION OF ASSETS

On April

28, 2010, we completed an acquisition of Gold Promise pursuant to the Share

Exchange Agreement. The acquisition was accounted for as a recapitalization

effected by a share exchange, wherein Gold Promise is considered the acquirer

for accounting and financial reporting purposes. The assets and liabilities of

the acquired entity have been brought forward at their book value and no

goodwill has been recognized.

As a

result of the acquisition, our consolidated subsidiaries include Gold Promise,

our wholly-owned subsidiary which is incorporated under the laws of Hong Kong,

Hebei Anbang Investment Consultation Co., Ltd., or “Hebei Consulting,” a

wholly-owned subsidiary of Gold Promise which is incorporated under the laws of

the PRC, and Buddha, a limited liability company incorporated under the laws of

the PRC which is effectively and substantially controlled by Hebei Consulting

through a series of captive agreements.

FORM

10 DISCLOSURE

As

disclosed elsewhere in this report, on April 28, 2010, we acquired Gold Promise

in a reverse acquisition transaction. Item 2.01(f) of Form 8-K states that

if the registrant was a shell company like we were immediately before the

reverse acquisition transaction disclosed under Item 2.01, then the registrant

must disclose the information that would be required if the registrant were

filing a general form for registration of securities on Form 10.

Accordingly,

we are providing below the information that would be included in a Form 10 if we

were to file a Form 10. Please note that the information provided below

relates to the combined enterprises after the acquisition of Gold Promise,

except that information relating to periods prior to the date of the reverse

acquisition only relate to Gold Promise and its consolidated subsidiaries unless

otherwise specifically indicated.

DESCRIPTION

OF BUSINESS

Business

Overview

Dachang

Hui Autonomous County Baosheng Steel Products Co., Ltd. (Buddha) was established

in 1999 in Hebei province, Northern China. Buddha is a leading producer

and vendor of high value-added, ultra-thin precision cold rolled steel

products. Buddha’s cold rolled steel is specially engineered and

manufactured using state of the art machinery according to the highest quality

standards, and our premium products are tailor-made to customers’ individual

requirements. Buddha’s steel is further processed by downstream

manufacturers and incorporated into a wide variety of end products including

automobiles, home appliances, packaging, and specialized construction materials

among others. Buddha’s production facilities occupy more than 47 acres and

include 96 annealing furnaces and 17 lines: 13 cold-rolling mills, 1 tin-plate

sheet mill, and 3 leveler stretchers. We employ over 900

employees.

In 2009,

we produced 446,000 MT of steel products, a capacity utilization rate of

95%. As of 2009, we had the capacity to produce 465,000 MT of cold rolled

steel assuming our 2009 product mix. Our capacity tonnage can vary

significantly depending on the types of products produced, and we strive to

maximize profit by producing the largest tonnage of product with the highest

margin available to us. Our products range in thickness from fractions of

millimeters to 7.5mm and can be up to 1450 mm in width. The production

process begins with our major raw material, hot-rolled steel coils, which we

clean, anneal and then stretch in a cold-rolling mill to the desired

specifications.

We sell

products primarily in China, but our distribution network also covers a diverse

export market. Approximately 19% of 2009 sales were eventually further

processed abroad, and our major export markets include Africa and Southeast

Asia.

Our

Corporate History and Background

A.G.

Volney Center, Inc. was originally incorporated under the laws of the State of

Delaware on March 6, 1997 under the name Lottlink Technologies, Inc. From

December 1997 until July 2003, the Company’s charter was suspended for

non-payment of franchise taxes. In July 2003, the company’s charter was

renewed and its certificate of incorporation was amended to change its name to

A.G. Volney Center, Inc. Prior to our reverse acquisition of Gold Promise,

AG Volney was primarily in the business of purchasing and reselling clothing

overruns and excess inventory and was in the development stage and had commenced

only limited business operations, and was looking to find a suitable merger

candidate and/or alternative financing.

On

October 19, 2006, AG Volney filed a Registration Statement on Form 10SB (File

No.: 0-52269) with the Securities and Exchange Commission, or the SEC, to

register our common stock under Section 12(g) of the Exchange Act. The

Registration Statement went effective by operation of law on December 18, 2006,

at which point we became a reporting company under the Exchange

Act.

As a

result of our reverse acquisition of Gold Promise, we are no longer a shell

company and active business operations were revived. We plan to amend our

Certificate of Incorporation to change our name to “Buddha Steel, Inc.” to

reflect the current business of our company.

Acquisition

of Gold Promise Limited

On April

28, 2010, we completed a reverse acquisition transaction through a share

exchange with Gold Promise and its shareholders, or the Shareholders, whereby we

acquired 100% of the issued and outstanding capital stock of Gold Promise in

exchange for 10,000 shares of our Series A Preferred Stock which constituted

98.75% of our issued and outstanding capital stock on a as-converted basis as of

and immediately after the consummation of the reverse acquisition. As a result

of the reverse acquisition, Gold Promise became our wholly-owned subsidiary and

the former shareholders of Gold Promise became our controlling

stockholders. The share exchange transaction with Gold Promise and the

Shareholders was treated as a reverse acquisition, with Gold Promise as the

acquirer and AG Volney as the acquired party. Unless the context suggests

otherwise, when we refer in this report to business and financial information

for periods prior to the consummation of the reverse acquisition, we are

referring to the business and financial information of Gold Promise and its

consolidated subsidiaries.

Immediately

prior to the Share Exchange, the common stock of Gold Promise was owned by the

following persons in the indicated percentages: Crowning Elite Limited (a BVI

company) (66.44%); Meng Li (9.62%); Yonghe Guo (5.01%); Shaochen Hu (5.01%);

William H. Luckman (6.96%); and Joseph J. Meuse (6.96%). Xi Chen, a

Canadian passport holder, owns 100% of the capital stock of Crowning Elite

Limited. Hongzhong Li, our Chief Executive Officer and the majority

shareholder and chairman of Buddha, is also the sole director of Crowning Elite

Limited.

Hongzhong

Li has entered into a call option agreement (the “Call Option Agreement”) with

Xi Chen, a Canadian passport holder and the sole shareholder of Crowning Elite

Limited, our principal shareholder after the reverse acquisition. Under

the Call Option Agreement, Mr. Li has the right to acquire up to 100% or the

shares of Crowning Elite Limited for fixed consideration, with such option

vesting over three years. The Call Option Agreement also provides that Mr.

Chen shall not dispose any of the shares of Crowning Elite Limited without Mr.

Li’s consent.

Hongzhong

Li has also entered into an entrustment agreement (“Entrustment Agreement”) with

Xi Chen, the sole owner of Crowning Elite Limited, under which Mr. Li is

authorized to exercise all shareholders’ and voting rights with respect to

Crowning Elite Limited in accordance with its Memorandum and Articles of

Association and the parameters of BVI law. In addition, pursuant to the

Entrustment Agreement, the Mr. Li has the right to operate and manage, and

designate and appoint all of the directors and senior officers of, Crowning

Elite Limited, and Xi Chen has agreed to waive all the voting and related rights

associated with his shareholdings in Crowning Elite Limited and to procure the

consent of Mr. Li before taking certain actions which would affect Mr. Li’s

interest under the Entrustment Agreement.

As a

result of his control of Crowning Elite Limited, Hongzhong Li, our Chief

Executive Officer, may be considered the beneficial owner of a majority of the

capital stock and voting power of AG Volney, as well as Buddha.

Immediately

following closing of the reverse acquisition of Gold Promise, the shareholders

of Gold Promise transferred 128 of the 10,000 shares of Series A Preferred Stock

issued to them in the Share Exchange to certain persons who provided services to

Gold Promise and its subsidiary and controlled affiliate.

Upon the

closing of the reverse acquisition, David F. Stever, our President, CEO, CFO and

a director, and Samantha M. Ford, our Secretary and a director, each submitted a

resignation letter pursuant to which they resigned from all offices that they

held effective immediately and from their positions as our directors that will

become effective on the tenth day following the mailing by us of an information

statement, or the Information Statement, to our stockholders that complies with

the requirements of Section 14f-1 of the Exchange Act. In addition, our

board of directors on April 28, 2010, increased the size of our board of

directors to three directors and appointed Hongzhong Li, Zhenqi Chen and Xianmin

Meng to fill the vacancies created by such resignations and increase in the size

of the board, which appointments will become effective upon the effectiveness of

the resignations of David F. Stever and Samantha M. Ford on the tenth day

following the mailing by us of the Information Statement to our

stockholders. In addition, our executive officers were replaced by

Buddha’s executive officers upon the closing of the reverse acquisition as

indicated in more detail below.

As a

result of our acquisition of Gold Promise, we now own all of the issued and

outstanding capital stock of Gold Promise, which in turn owns all of the issued

and outstanding capital stock of Hebei Consulting. In addition, we

effectively and substantially control Buddha through a series of captive

agreements with Hebei Consulting. Buddha is principally engaged in the

production of cold-rolled steel products in the PRC.

Gold

Promise was established in Hong Kong on January 8, 2010 to serve as an

intermediate holding company. Hebei Consulting was established in the PRC

on April 2, 2010. Buddha, our operating affiliate, was established in the

PRC on September 9, 1999. On March 29, 2010, the local government of the

PRC issued a certificate of approval regarding the foreign ownership of Hebei

Consulting by Gold Promise, a Hong Kong entity.

On April

2, 2010, prior to the reverse acquisition transaction, Hebei Consulting and

Buddha and its shareholders entered into a series of agreements known as

variable interest agreements (the “VIE Agreements”) pursuant to which Buddha

became Hebei Consulting’s contractually controlled affiliate. The use of

VIE agreements is a common structure used to acquire PRC corporations,

particularly in certain industries in which foreign investment is restricted or

forbidden by the PRC government. The VIE Agreements included:

|

|

(1)

|

A

Consulting Services Agreement through which Hebei Consulting has the right

to advise, consult, manage and operate Buddha and collect and own all of

the net profits of Buddha;

|

|

|

(2)

|

an

Operating Agreement through which Hebei Consulting has the right to

recommend director candidates and appoint the senior executives of Buddha,

approve any transactions that may materially affect the assets,

liabilities, rights or operations of Buddha, and guarantee the contractual

performance by Buddha of any agreements with third parties, in exchange

for a pledge by Buddha of its accounts receivable and

assets;

|

|

|

(3)

|

a

Voting Rights Proxy Agreement under which the owners of Buddha have vested

their collective voting control over Buddha to Hebei Consulting and will

only transfer their equity interests in Buddha to Hebei Consulting or its

designee(s);

|

|

|

(4)

|

an

Option Agreement under which the owners of Buddha have granted to Hebei

Consulting the irrevocable right and option to acquire all of their equity

interests in Buddha or, alternatively, all of the assets of Buddha;

and

|

|

|

(5)

|

an

Equity Pledge Agreement under which the owners of Buddha have pledged all

of their rights, titles and interests in Buddha to Hebei Consulting to

guarantee Buddha’s performance of its obligations under the Consulting

Services Agreement.

|

The

foregoing description of the terms of the Consulting Services Agreement, the

Operating Agreement, the Voting Rights Proxy Agreement, the Option Agreement and

the Equity Pledge Agreement is qualified in its entirety by reference to the

provisions of the agreements filed as Exhibits 10.1, 10.2, 10.3, 10.4 and 10.5

to this report, respectively, which are incorporated by reference

herein.

See

“Related Party Transactions” for further information on our contractual

arrangements with these parties.

Because

of the common control between Gold Promise, Hebei Consulting and Buddha, for

accounting purposes, the acquisition of these entities has been treated as a

recapitalization with no adjustment to the historical basis of their assets and

liabilities. The restructuring has been accounted for using the “as if”

pooling method of accounting and the operations were consolidated as if the

restructuring had occurred as of the beginning of the earliest period presented

in our consolidated financial statements and the current corporate structure had

been in existence throughout the periods covered by our consolidated financial

statements.

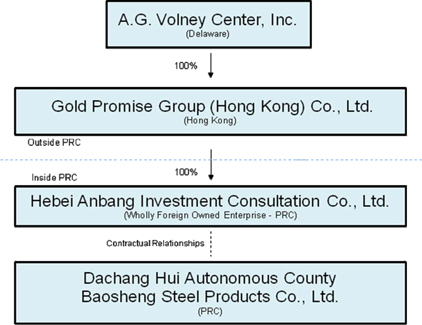

Our

Corporate Structure

All of

our business operations are conducted through our Hong Kong and Chinese

subsidiaries and controlled affiliate. The chart below presents our

corporate structure:

Our

Industry:

The

following industry information has been obtained from various market research

reports and publicly available sources. We believe this information to be

current and reliable.

The

Chinese Economy

Demand

for our products is driven in line with macroeconomic industrial growth both

globally and in the PRC. As our end products range from automobiles to

appliances, general economic growth underlies our success, especially in

China. PRC macroeconomic growth has been strong and positive in recent

years, and GDP grew at a rate of 8.7% in 2009, reaching US$4.9

trillion. Due to job creation and wage increases from various economic

stimulus packages and increased lending in 2009, The Economist Corporate Network

forecasts growth in the PRC economy will reach 9.3% in 2010.

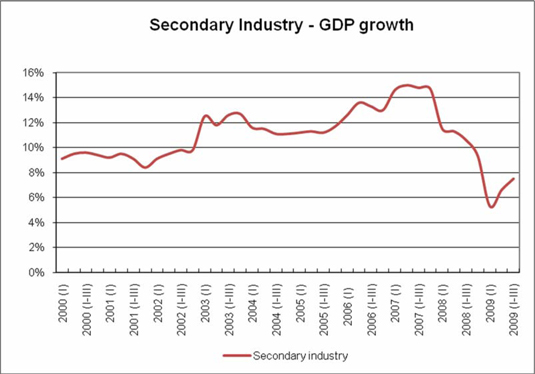

The

secondary sector of the economy in which we operate has maintained strong

positive growth as well:

The

Steel Market:

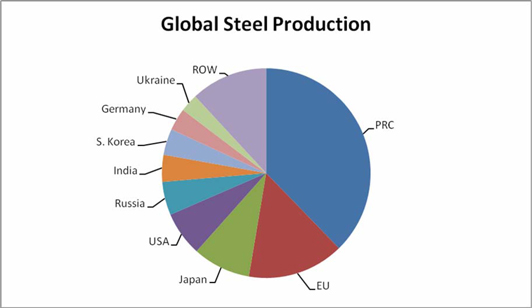

China is

the largest steel producing country in the world. According to the World

Steel Association, in 2008, global steel output was 1.3B tons, of which China

accounted for 38%.

The pie

chart below shows shares of global output by production region for

2008.

Growth in

the steel market has recently been driven by PRC demand, and China has been the

largest producing steel country since the mid 1990s. The PRC accounted for

roughly 34% of total global steel demand in 2006, and PRC demand for steel has

grown at a CAGR of 19.18% in recent history. Chinese steel production is

forecast to grow by 7.3% in 2010, reaching new all time highs through 2011, and

maintain positive growth in the future.

Cold

Rolled Steel Market:

Our

products, custom ultra thin cold-rolled steel sheets and coils, are a

vital component in a variety of industrial products, including but not

limited to roofing, appliances, telecommunications equipment, motor

vehicles and motor vehicle parts and accessories. Demand for high

precision steel in PRC end product manufacturing markets is projected to

grow in the foreseeable future, and we believe we are well positioned to

benefit from this growth.

Due to

lack of quality manufacturing facilities and capability, the PRC has been a net

importer of ultra thin cold-rolled steel products. To meet demand,

manufacturers have imported precision steel products from countries with more

developed high end steel capacity. China’s production of cold rolled steel

has responded to market demand by growing robustly as domestic producers have

moved up the value chain. Market research reports estimate that the market

for cold rolled steel has grown at nearly 20% per annum in recent years.

PRC cold rolled production is anticipated to experience sustained strong growth

in the near future.

Our

Competitive Advantages

We

believe that we posses the following competitive advantages that allow us to

maintain our strong market position and will aid our profit growth in the

future:

Excellent

reputation and rich experience as Hebei’s leading manufacturer of precision

cold-rolled narrow strip steel:

We are

the largest manufacturer in Hebei of high precision cold-rolled narrow strip

steel. Hebei is the largest steel producing province in China. We have a

majority of repeat and long term customers and are recognized as a market leader

in top quality, competitive price, reliability and consistent delivery. We

constantly strive to move up the value chain and provide our customers tailor

made products at their specifications and quality they demand. We believe

we will continue to solidify this position and consolidate market

share.

We

have strong historical growth:

From 2007

through 2009, our revenues have grown at an annualized rate of 28% and we have

increased sales of more profitable product lines so that our profit nearly

doubled from 2008 to 2009. We intend to continue this growth by expanding

our processing capacity of only the highest margin products and increasing our

bottom line.

Lower

than industry average cost structure:

The steel

industry in China is dominated by small lower end private manufacturers and

large State Owned Enterprises with large pension and employment

obligations. Our status as a leading private manufacturer of customized,

high-end niche product affords us higher than industry margins and what we

believe to be long term sustainability and growth opportunities.

Capital

intensive industry presents barriers to competitor entry:

Ultra-thin,

high-precision cold-rolled steel products require a significant investment of

capital and technical know-how in order to be profitably exploited.

Potential new competitors would be subject to the requirements of a highly

technical and capital intensive industry in order to be successful.

Diverse

customer and end product base:

Our

products serve a broad range of markets and industries which insulate us from

concentration risk. We serve the automotive, construction, appliance

manufacturing, and telecommunications industries among others. Market

pressures in one segment of our downstream customers may be softened by

sustained demand in the others.

Superior

management of commodity price fluctuations:

Our

principal raw material, hot-rolled steel, accounts for the vast majority of our

COGS. Due to our inventory systems and controls and sales model, we are able to

protect ourselves to some degree from commodity exposure. We believe we

are able to mitigate the results of a volatile commodity market on our profits

through our diligent management and low inventory.

Our

Growth Strategy

Chinese

demand for cold-rolled steel products has increased at a rate of nearly 20%

annually in recent years. We believe demand for high quality cold-rolled

steel products will continue to grow domestically and globally, thus affording

us opportunity to grow and expand our business operations. Our growth

strategy is primarily focused on increasing production capacity of highest

margin products, ultra thin cold rolled strips and sheets.

We intend

to pursue the following strategies to achieve our goal:

|

1)

|

According

to capital availability, expand new production lines that will

increase capacity of ultra-thin cold-rolled

steel.

|

|

2)

|

Identify

and acquire high quality producers at favorable valuations to capitalize

on economies of scale, as well as increasing our market

share.

|

|

3)

|

Expand

export revenues to emerging markets including but not limited

to Southeast Asia, Africa and Latin

America.

|

|

4)

|

Focus

research and development on advancing processing techniques to develop

more sophisticated products that command higher margins, and continue to

improve margins through increased efficiencies in our production

process.

|

Our

Products:

Our major

products include cold-rolled sheet, tin-plate sheet, and narrow cold-rolled

steel strip. Products are typically made to meet the custom size

specifications of our clients. Our production facilities have the capacity

to produce a large range of different widths and thicknesses, ranging from 350

mm up to 1450 mm and as thin as 0.15 mm up to 0.6 mm respectively.

Buddha’s

Products

We have

steadily increased margins of our products and production of higher margin

products:

|

2009

|

2008

|

2007

|

||||||||||||||||||||||

|

Product Category

|

Margin

|

% of

Sales

|

Margin

|

% of

Sales

|

Margin

|

% of

Sales

|

||||||||||||||||||

|

Black

Strip

|

4.4 | % | 13.1 | % | 5.3 | % | 22.2 | % | 4.3 | % | 42.3 | % | ||||||||||||

|

Welded

Pipe

|

3.7 | % | 0.1 | % | 3.8 | % | 0.7 | % | 2.5 | % | 1.7 | % | ||||||||||||

|

Bright

Strip

|

4.2 | % | 11.0 | % | 5.5 | % | 13.8 | % | 4.1 | % | 15.1 | % | ||||||||||||

|

Cold

Rolled Sheet

|

8.1 | % | 15.1 | % | 7.5 | % | 14.4 | % | 5.1 | % | 8.6 | % | ||||||||||||

|

Cold

Rolled Coil

|

8.5 | % | 53.8 | % | 8.5 | % | 43.6 | % | 5.8 | % | 27.6 | % | ||||||||||||

|

Tin-Plated

Sheet

|

8.9 | % | 5.3 | % | 8.6 | % | 4.1 | % | 6.8 | % | 1.8 | % | ||||||||||||

|

Others

|

3.8 | % | 1.5 | % | 3.7 | % | 1.2 | % | 2.8 | % | 2.9 | % | ||||||||||||

|

Total

|

7.4 | % | 100.0 | % | 7.2 | % | 100.0 | % | 4.7 | % | 100.0 | % | ||||||||||||

Welded

pipe production has been phased out, and we are pursuing new techniques to

produce a variety of higher margin alloyed and plated ultra thin

products.

Our end

customers further process the cold rolled sheet to produce a diverse range of

products and product components including automobile parts, farm equipment,

shipping harnesses, air conditioners, refrigerators, washing machines, and other

home appliances. We estimate that the end products manufactured from our

steel are roughly distributed as follows:

Raw

Materials

The

principal raw material used in our products is hot-rolled coil and hot-rolled

steel strips. In 2009, hot rolled coil and hot rolled steel strips

accounted for more than 80% of our production costs. We purchase our

hot-rolled coil and hot-rolled steel strips from a number of sources and are not

dependent on any single supplier.

|

Supplier

|

Raw Material

Purchase (USD)

|

|||

|

Sinosteel

Company

|

66,731,453 | |||

|

Tangshan

Guofeng Steel Company

|

45,019,911 | |||

|

Sinolight

Materials Company

|

11,187,376 | |||

|

Hebei

Jinxi Steel Company

|

7,439,541 | |||

|

Shandong

Haixin Board Industrial Co.

|

3,491,968 | |||

|

Tangshan

Ruifeng Steel Company

|

2,254,575 | |||

With

larger suppliers, we often secure yearly contracts to ensure a steady supply of

hot rolled raw materials, with flexible pricing based on movements in the spot

price. Smaller suppliers are generally on an as needed basis with

purchases made at market price for the day.

Sales

Channels

We sell

our products based on customer specifications and demand. Currently we

have more than 400 customers of which more than 50% are repeat buyers.

These customers can be divided into two groups, direct manufacturers and trading

companies. Margins for sales to direct manufacturers are higher than to

distributers. Roughly 40% of our sales in 2009 were through distributers

while the remaining 60% were direct to end user sales. Our top five direct

manufacturer customers account for 9% of our total revenue, while our top five

distributor clients account for 12%.

The

following table details our top 5 direct manufacturing customers:

|

Top 5 Direct Manufacturing

Customers

|

Sales

|

% of Total

|

||||||

|

Hongyuan

Caituban Co.

|

$ | 9,620,295 | 3.5 | % | ||||

|

Tianjin

Soudragon Steel Co.

|

$ | 5,590,835 | 2.0 | % | ||||

|

Xianghe

Xingang Wuzi Trading Co.

|

$ | 4,583,128 | 1.7 | % | ||||

|

Tangshan

Jiajia Door Industrial Co.

|

$ | 2,818,739 | 1.0 | % | ||||

|

Chendu

Xinhete Door Industrial Co.

|

$ | 2,426,937 | 0.9 | % | ||||

| $ | 25,039,933 | 9.1 | % | |||||

And our

top five distribution customers by revenue:

|

Top 5 Distributors

|

Sales

|

% of Total

|

||||||

|

Jiangsu

Sumeida International Tech. Trade Co.

|

$ | 9,973,299 | 3.6 | % | ||||

|

Xianghe

Kuntai Steel Processing Co.

|

$ | 8,174,849 | 3.0 | % | ||||

|

Wenhan

Xinfeng Steel Business Co.

|

$ | 7,172,211 | 2.0 | % | ||||

|

Wenhan

Xueza Steel Business Co.

|

$ | 5,278,553 | 1.9 | % | ||||

|

Hangzhou

Relian Import and Export Co.

|

$ | 3,363,474 | 1.2 | % | ||||

| $ | 33,962,386 | 11.7 | % | |||||

Though we

have customers in nearly every province in China, local sales in Hebei, Tianjin

and Beijing represent nearly half of our domestic sales volume:

|

Province

|

Domestic

Sales

2009

%

|

|||

|

Hebei

|

29.61 | % | ||

|

Tianjin

|

11.72 | % | ||

|

Jiangsu

|

10.80 | % | ||

|

Zhejiang

|

9.98 | % | ||

|

Beijing

|

7.34 | % | ||

|

Shandong

|

7.25 | % | ||

|

Shanghai

|

5.47 | % | ||

|

Sichuan

|

4.41 | % | ||

|

Liaoning

|

3.03 | % | ||

|

Guangdong

|

2.28 | % | ||

|

Others

|

8.10 | % | ||

|

Total

|

100.00 | % | ||

We also

export products to Africa and Southeast Asia, which comprise roughly 19% of our

revenues.

We have a

sales staff of around 23 individuals who are responsible for generating sales,

attending sales fairs and trade shows. Our sales staff is compensated on a

salary plus commission basis. Our customers often seek us out directly as

we are well known in the industry as a top reliable provider of quality cold

rolled products.

Customers

are responsible for all costs associated with product pickup and transport

arrangements. Our products are manufactured on an on-demand basis and we

generally require full-payment for each order prior to production.

Occasionally, we extend more flexible payment terms to a selected group of

our repeat buyers. These terms typically allow the buyer to pay a 5-20%

deposit to start the production of their order, and require payment in full

prior to delivery. These payment terms ensure that we better control our

inventory and manage our raw material costs.

Employees

We

currently employ a staff of 957 employees, the majority of which are factory

workers. We have a sales staff of 23. We believe we are in material

compliance with all applicable labor and safety laws and regulations in the PRC,

including the PRC Labor Contract Law, the PRC Unemployment Insurance Law,

the PRC Provisional Insurance Measures for Maternity of Employees, PRC Interim

Provisions on Registration of Social Insurance, PRC Interim Regulation on the

Collection and Payment of Social Insurance Premiums and other related

regulations, rules and provisions issued by the relevant governmental

authorities for our operations in the PRC. According to the PRC Labor

Contract Law, we are required to enter into labor contracts with our employees

and to pay them no less than the local minimum wage.

|

Department

|

Employee #

|

|

|

Cold

Rolled Strip Workshop

|

269

|

|

|

Cold

Rolled Sheet Workshop

|

244

|

|

|

Tin

Plating Workshop

|

34

|

|

|

Power

Department

|

34

|

|

|

Mechanical

Department

|

115

|

|

|

Warehouse

|

127

|

|

|

Sales

Department

|

23

|

|

|

Finance

Department

|

9

|

|

|

Administrative, Support and

Logistics

|

102

|

|

|

Total

|

|

957

|

Intellectual

Property Rights

We

protect our intellectual property primarily by maintaining strict control over

the use of production processes. All our employees, including key

employees and engineers, have signed our standard form of labor contracts,

pursuant to which they are obligated to hold in confidence any of our

trade secrets, know-how or other confidential information and not to

compete with us. In addition, for each project, only the personnel

associated with the project have access to the related intellectual

property. Access to proprietary data is limited to authorized personnel to

prevent unintended disclosure or otherwise using our intellectual property

without proper authorization. We will continue to take steps to protect

our intellectual property rights.

We have

registered the brand name, logo and trademark Baosheng in the PRC for steel

products:

The

trademarks are registered through 2018.

Our

Facilities and Property

Our

facilities are in located in Dachang Hui Autonomous County in Northern

Hebei. We are approximately 50 miles from Beijing. In total, we have

leasehold rights to land comprising an area of more than 46 acres. Our

lease is with the local authorities and is valid through 2025.

Our

production facilities occupy 24.7 acres, and we have an office building and

cafeteria on a 1.5 acre plot. Our production facilities include 13

cold-rolling mills, 1 tin-plate sheet mill, and 3 leveler

stretchers.

Buddha

Facilities:

Competition

Competition

within the steel industry in the PRC is intense. There is an

estimated capacity of 40MMT of high precision cold rolled steel capacity in

China. Our competitors range from small private enterprises to extremely

large state owned enterprises. Our operating affiliate Buddha is

located in northern Hebei. Hebei is the largest producer of steel by

province in the PRC, therefore we are located nearby numerous

facilities. We are one of the largest non state owned ultra-thin

high-precision cold-rolled steel manufacturers by capacity in

China.

The table

below details our 2 major competitors in our market:

|

Company

|

Est.

Capacity

|

|

|

Hebei

Dachang Jinming Accurate Cold-Rolling

Steel

Plate Company

|

150,000

MT

|

|

|

Langfang

Jinhua Industry Co. Ltd

|

|

150,000

MT

|

Our

production capacity is higher than these two competitors and we believe we are

able to outperform them in both price and quality. Private steel product

manufacturers in China generally focus on low-end products. Many of our

competitors are significantly smaller than we are and use outdated equipment and

production techniques. Due to our high quality equipment, economies of

scale and management experience, we produce steel at higher efficiencies and

lower prices than these competitors. The larger state owned

enterprises with whom we compete often have oversized, unionized labor forces

and associated pension and healthcare liabilities and cannot match our

production efficiency. We distinguish ourselves in the market based on our

extremely fast turnaround, high quality and low prices.

Regulation

Because

our principal operating affiliate, Buddha, is located in the PRC, our business

is regulated by the national and local laws of the PRC. We believe our conduct

of business complies with existing PRC laws, rules and regulations.

The PRC

government has in the past provided a subsidy by means of a value added tax, or

VAT, rebate to exporters of steel products. This rebate was reduced in April

2007 in response to international pressure on China to curb its exports. A

5% tax rebate currently applies to our high value-add cold-rolled steel

products.

General

Regulation of Businesses

We

believe we are in material compliance with all applicable labor and safety laws

and regulations in the PRC, including the PRC Labor Contract Law, the PRC

Production Safety Law, the PRC Regulation for Insurance for Labor Injury, the

PRC Unemployment Insurance Law, the PRC Provisional Insurance Measures for

Maternity of Employees, PRC Interim Provisions on Registration of Social

Insurance, PRC Interim Regulation on the Collection and Payment of Social

Insurance Premiums and other related regulations, rules and provisions

issued by the relevant governmental authorities from time to time, for our

operations in the PRC.

According

to the PRC Labor Contract Law, we are required to enter into labor contracts

with our employees. We are required to pay no less than local minimum wages to

our employees. We are also required to provide employees with labor safety and

sanitation conditions meeting PRC government laws and regulations and carry out

regular health examinations of our employees engaged in hazardous

occupations.

Foreign

Currency Exchange

The

principal regulation governing foreign currency exchange in China is the Foreign

Currency Administration Rules (1996), as amended (2008). Under these Rules, RMB

is freely convertible for current account items, such as trade and

service-related foreign exchange transactions, but not for capital account

items, such as direct investment, loan or investment in securities outside China

unless the prior approval of, and/or registration with, the State Administration

of Foreign Exchange of the People’s Republic of China, or SAFE, or its local

counterparts (as the case may be) is obtained.

Pursuant

to the Foreign Currency Administration Rules, foreign invested enterprises, or

FIEs, in China may purchase foreign currency without the approval of SAFE for

trade and service-related foreign exchange transactions by providing commercial

documents evidencing these transactions. They may also retain foreign exchange

(subject to a cap approved by SAFE) to satisfy foreign exchange liabilities or

to pay dividends. In addition, if a foreign company acquires a company in China,

the acquired company will also become an FIE. However, the relevant PRC

government authorities may limit or eliminate the ability of FIEs to purchase

and retain foreign currencies in the future. In addition, foreign exchange

transactions for direct investment, loan and investment in securities outside

China are still subject to limitations and require approvals from, and/or

registration with, SAFE.

Regulation

of Income Taxes

On April

16, 2007, the National People’s Congress of China passed a new Enterprise Income

Tax Law, or the New EIT Law, and its implementing rules, both of which became

effective on January 1, 2008. Before the implementation of the New EIT Law, FIEs

established in the PRC, unless granted preferential tax treatments by the PRC

government, were generally subject to an earned income tax, or EIT, rate of

33.0%, which included a 30.0% state income tax and a 3.0% local income tax. The

New EIT Law and its implementing rules impose a unified EIT rate of 25.0% on all

domestic-invested enterprises and FIEs, unless they qualify under certain

limited exceptions.

In

addition to the changes to the current tax structure, under the New EIT Law, an

enterprise established outside of China with “de facto management bodies” within

China is considered a resident enterprise and will normally be subject to an EIT

of 25% on its global income. The implementing rules define the term “de facto

management bodies” as “an establishment that exercises, in substance, overall

management and control over the production, business, personnel, accounting,

etc., of a Chinese enterprise.” If the PRC tax authorities subsequently

determine that we should be classified as a resident enterprise, then our

organization’s global income will be subject to PRC income tax of 25%. For

detailed discussion of PRC tax issues related to resident enterprise status, see

“Risk Factors – Risks Related to Our Business – Under the New EIT Law, we may be

classified as a ‘resident enterprise’ of China. Such classification will likely

result in unfavorable tax consequences to us and our non-PRC

stockholders.”

Our

future effective income tax rate depends on various factors, such as tax

legislation, the geographic composition of our pre-tax income and non-tax

deductible expenses incurred. Our management carefully monitors these legal

developments and will timely adjust our effective income tax rate when

necessary.

For the

years ended December 31, 2009 and 2008, as approved by the local tax authority

of Dachang County, the Company's income tax was assessed annually at a

pre-determined fixed rate as an incentive to stimulate local economy and

encourage entrepreneurship. Although the possibility exists for reinterpretation

of the application of the tax regulations by higher tax authorities in the PRC,

potentially overturning the decision made by the local tax authority, the

Company has not experienced any reevaluation of the income taxes for prior

years. Management believes that the possibility of any reevaluation of income

taxes is remote based on the fact that the Company has obtained the written tax

clearance from the local tax authority.

Dividend

Distribution

Under

applicable PRC regulations, FIEs in China may pay dividends only out of their

accumulated profits, if any, determined in accordance with PRC accounting

standards and regulations. In addition, a FIE in China is required to set aside

at least 10.0% of its after-tax profit based on PRC accounting standards each

year to its general reserves until the accumulative amount of such reserves

reach 50.0% of its registered capital. These reserves are not distributable as

cash dividends. The board of directors of a FIE has the discretion to allocate a

portion of its after-tax profits to staff welfare and bonus funds, which may not

be distributed to equity owners except in the event of liquidation.

The New

EIT Law and its implementing rules generally provide that a 10% withholding tax

applies to China-sourced income derived by non-resident enterprises for PRC

enterprise income tax purposes unless the jurisdiction of incorporation of such

enterprises’ shareholder has a tax treaty with China that provides for a

different withholding arrangement. Hebei Consulting is considered a FIE and is

directly held by our subsidiary Gold Promise in Hong Kong. According to a

2006 tax treaty between the Mainland and Hong Kong, dividends payable by a FIE

in China to the company in Hong Kong who directly holds at least 25% of the

equity interests in the FIE will be subject to a no more than 5% withholding

tax. We expect that such 5% withholding tax will apply to dividends paid

to Gold Promise by Hebei Consulting, but this treatment will depend on our

status as a non-resident enterprise.

Environmental

Matters

Our

manufacturing facilities are subject to various pollution control regulations

with respect to noise, water and air pollution and the disposal of waste and

hazardous materials. We are also subject to periodic inspections by local

environmental protection authorities. Our operating affiliate has received

certifications from the relevant PRC government agencies in charge of

environmental protection indicating that its business operations are in material

compliance with the relevant PRC environmental laws and regulations. We are not

currently subject to any pending actions alleging any violations of applicable

PRC environmental laws.

Insurance

Insurance

companies in China offer limited business insurance products. While business

interruption insurance is available to a limited extent in China, we have

determined that the risks of interruption, cost of such insurance and the

difficulties associated with acquiring such insurance on commercially reasonable

terms make it impractical for us to have such insurance. As a result, we could

face liability from the interruption of our business as summarized under “Risk

Factors – Risks Related to Our Business – We do not carry business interruption

insurance so we could incur unrecoverable losses if our business is

interrupted.”

RISK

FACTORS

An

investment in our common stock involves a high degree of risk. You should

carefully consider the risks described below, together with all of the other

information included in this report, before making an investment decision. If

any of the following risks actually occurs, our business, financial condition or

results of operations could suffer. In that case, the trading price of our

common stock could decline, and you may lose all or part of your investment. You

should read the section entitled “Special Notes Regarding Forward-Looking

Statements” above for a discussion of what types of statements are

forward-looking statements, as well as the significance of such statements in

the context of this report.

RISKS

RELATED TO OUR BUSINESS

We

have a short operating history.

We were

founded in 1999. We may not succeed in implementing our business plan

successfully because of competition from domestic and foreign market entrants,

failure of the market to accept our products, or other reasons. Therefore, you

should not place undue reliance on our past performance as they may not be

indicative of our future results.

We

face risks related to general domestic and global economic conditions and to the

current credit crisis.

Our

current operating cash flows provide us with stable funding capacity. However,

the current uncertainty arising out of domestic and global economic conditions,

including the recent disruption in credit markets, poses a risk to the PRC

economy, and may impact our ability to manage normal relationships with our

customers, suppliers and creditors. If the current situation deteriorates

significantly, our business could be materially negatively impacted, as demand

for our products and services may decrease from a slow-down in the general

economy, or supplier or customer disruptions may result from tighter credit

markets.

Our

business is subject to the health of the PRC economy and our growth may be

inhibited by the inability of potential customers to fund purchases of our

products and services.

Our

products are dependent on the continued growth of infrastructure and

construction projects in the PRC. There is no guarantee that the PRC will

continue to invest in infrastructure and construction.

In

order to grow at the pace expected by management, we will require additional

capital to support our long-term growth strategies. If we are unable to obtain

additional capital in future years, we may be unable to proceed with our plans

and we may be forced to curtail our operations.

We will

require additional working capital to support our long-term growth strategies,

which includes identifying suitable points of market entry for expansion growing

the number of points of sale for our products, so as to enhance our product

offerings and benefit from economies of scale. Our working capital requirements

and the cash flow provided by future operating activities, if any, may vary

greatly from quarter to quarter, depending on the volume of business during the

period. We may not be able to obtain adequate levels of additional financing,

whether through equity financing, debt financing or other sources. Additional

financings could result in significant dilution to our earnings per share or the

issuance of securities with rights superior to our current outstanding

securities. In addition, we may grant registration rights to investors

purchasing our equity or debt securities in the future. If we are unable to

raise additional financing, we may be unable to implement our long-term growth

strategies, develop or enhance our products and services, take advantage of

future opportunities or respond to competitive pressures on a timely

basis.

If

we are unable to attract and retain senior management and qualified technical

and sales personnel, our operations, financial condition and prospects will be

materially adversely affected.

Our

future success depends in part on the contributions of our management team and

key technical and sales personnel and our ability to attract and retain

qualified new personnel. In particular, our success depends on the

continuing employment of our Chief Executive Officer, Mr. Hongzhong Li, our

Chief Technology Officer, Mr. Hongzhi Fang, and our Chief Financial Officer, Mr.

Zhenqi Chen. There is significant competition in our industry for

qualified managerial, technical and sales personnel and we cannot assure you

that we will be able to retain our key senior managerial, technical and sales

personnel or that we will be able to attract, integrate and retain other such

personnel that we may require in the future. If we are unable to attract and

retain key personnel in the future, our business, operations, financial

condition, results of operations and prospects could be materially adversely

affected.

We

do not carry business interruption or other insurance, so we have to bear losses

ourselves.

We are

subject to risk inherent to our business, including equipment failure, theft,

natural disasters, industrial accidents, labor disturbances, business

interruptions, property damage, product liability, personal injury and death. We

do not carry any business interruption insurance or third-party liability

insurance or other insurance to cover risks associated with our business. As a

result, if we suffer losses, damages or liabilities, including those caused by

natural disasters or other events beyond our control and we are unable to make a

claim again a third party, we will be required to bear all such losses from our

own funds, which could have a material adverse effect on our business, financial

condition and results of operations.

Our

quarterly operating results are likely to fluctuate, which may affect our stock

price.

Our

quarterly revenues, expenses, operating results and gross profit margins vary

from quarter to quarter. As a result, our operating results may fall below the

expectations of securities analysts and investors in some quarters, which could

result in a decrease in the market price of our common stock. The reasons our

quarterly results may fluctuate include:

|

|

·

|

variations

in the price of hot- and cold-rolled

steel;

|

|

|

·

|

changes

in the general competitive and economic conditions;

and

|

|

|

·

|

delays

in, or uneven timing in the delivery of, customer

orders.

|

Period to

period comparisons of our results should not be relied on as indications of

future performance.

Our

limited ability to protect our intellectual property, and the possibility that

our technology could inadvertently infringe technology owned by others, may

adversely affect our ability to compete.

We rely

on a combination of trade secret laws and confidentiality procedures to protect

the technological know-how that comprise much of our intellectual property. We

protect our technological know-how pursuant to non-disclosure and

non-competition provisions contained in our employment agreements, and

agreements with them to keep confidential all information relating to our

customers, methods, business and trade secrets during and after their employment

with us. Our employees are also required to acknowledge and recognize that all

inventions, trade secrets, works of authorship, developments and other processes

made by them during their employment are our property.

A

successful challenge to the ownership of our intellectual property could

materially damage our business prospects. Our competitors may assert that our

technologies or products infringe on their patents or proprietary rights. We may

be required to obtain from others licenses that may not be available on

commercially reasonable terms, if at all. Problems with intellectual property

rights could increase the cost of our products or delay or preclude our new

product development and commercialization. If infringement claims against

us are deemed valid, we may not be able to obtain appropriate licenses on

acceptable terms or at all. Litigation could be costly and time-consuming

but may be necessary to defend against infringement claims.

RISKS

RELATING TO THE VIE AGREEMENTS

The

PRC government may determine that the VIE Agreements are not in compliance with

applicable PRC laws, rules and regulations

Hebei

Consulting manages and operates our steel production business through Buddha

pursuant to the rights its holds under the VIE Agreements. Almost all

economic benefits and risks arising from Buddha’s operations are transferred to

Hebei Consulting under these agreements. Details of the VIE Agreements are

set out in “DESCRIPTION OF BUSINESS - Acquisition of Gold Promise Limited” above.

There are

risks involved with the operation of our business in reliance on the VIE

Agreements, including the risk that the VIE Agreements may be determined by PRC

regulators or courts to be unenforceable. Our PRC counsel has provided a

legal opinion that the VIE Agreements are binding and enforceable under PRC law,

but has further advised that if the VIE Agreements were for any reason

determined to be in breach of any existing or future PRC laws or regulations,

the relevant regulatory authorities would have broad discretion in dealing with

such breach, including:

|

·

|

imposing

economic penalties;

|

|

·

|

discontinuing

or restricting the operations of Buddha or Hebei

Consulting;

|

|

|

·

|

imposing

conditions or requirements in respect of the VIE Agreements with which

Buddha or Hebei Consulting may not be able to

comply;

|

|

|

·

|

requiring

our company to restructure the relevant ownership structure or

operations;

|

|

|

·

|

taking

other regulatory or enforcement actions that could adversely affect our

company’s business; and

|

|

|

·

|

revoking

the business licenses and/or the licenses or certificates of Hebei

Consulting, and/or voiding the VIE

Agreements.

|

Any of

these actions could adversely affect our ability to manage, operate and gain the

financial benefits of Buddha, which would have a material adverse impact on our

business, financial condition and results of operations.

Our

ability to manage and operate Buddha under the VIE Agreements may not be as

effective as direct ownership

We

conduct our steel production business in the PRC and generate virtually all of

our revenues through the VIE Agreements. Our plans for future growth are based

substantially on growing the operations of Buddha. However, the VIE

Agreements may not be as effective in providing us with control over Buddha as

direct ownership. Under the current VIE arrangements, as a legal matter,

if Buddha fails to perform its obligations under these contractual arrangements,

we may have to (i) incur substantial costs and resources to enforce such

arrangements, and (ii) rely on legal remedies under PRC law, which we cannot be

sure would be effective. Therefore, if we are unable to effectively control

Buddha, it may have an adverse effect on our ability to achieve our business

objectives and grow our revenues.

As

the VIE Agreements are governed by PRC law, we would be required to rely on PRC

law to enforce our rights and remedies under them; PRC law may not provide us

with the same rights and remedies as are available in contractual disputes

governed by the law of other jurisdictions.

The VIE

Agreements are governed by the PRC law and provide for the resolution of

disputes through arbitral proceedings pursuant to PRC law. If Buddha or its

shareholders fail to perform the obligations under the VIE Agreements, we would

be required to resort to legal remedies available under PRC law, including

seeking specific performance or injunctive relief, or claiming damages. We

cannot be sure that such remedies would provide us with effective means of

causing Buddha to meet its obligations, or recovering any losses or damages as a

result of non-performance. Further, the legal environment in China is not as

developed as in other jurisdictions. Uncertainties in the application of various

laws, rules, regulations or policies in PRC legal system could limit our

liability to enforce the VIE Agreements and protect our

interests.

The

payment arrangement under the VIE Agreements may be challenged by the PRC tax

authorities

We

generate our revenues through the payments we receive pursuant to the VIE

Agreements. We could face adverse tax consequences if the PRC tax authorities

determine that the VIE Agreements were not entered into based on arm’s length

negotiations. For example, PRC tax authorities may adjust our income and

expenses for PRC tax purposes which could result in our being subject to higher

tax liability, or cause other adverse financial consequences.

Our

Shareholders have potential conflicts of interest with our company which may

adversely affect our business

Hongzhong

Li is our chief executive officer, and is also the largest shareholder of

Buddha. There could be conflicts that arise from time to time between our

interests and the interests of Mr. Li. There could also be conflicts that arise

between us and Buddha that would require our shareholders and Buddha’s

shareholders to vote on corporate actions necessary to resolve the conflict.

There can be no assurance in any such circumstances that Mr. Li will vote his

shares in our best interest or otherwise act in the best interests of our

company. If Mr. Li fails to act in our best interests, our operating

performance and future growth could be adversely affected.

We

rely on the approval certificates and business license held by Hebei Consulting

and any deterioration of the relationship between Hebei Consulting and Buddha

could materially and adversely affect our business operations

We

operate our steel production business in China on the basis of the approval

certificates, business license and other requisite licenses held by Hebei

Consulting and Buddha. There is no assurance that Hebei

Consulting and Buddha will be able to renew their licenses or certificates

when their terms expire with substantially similar terms as the ones they

currently hold.

Further,

our relationship with Buddha is governed by the VIE Agreements that are intended

to provide us with effective control

over the business operations of Buddha. However, the VIE Agreements may

not be effective in providing control over the application for and maintenance

of the licenses required for our business operations. Buddha could violate the

VIE Agreements, go bankrupt, suffer from difficulties in its business or

otherwise become unable to perform its obligations under the VIE Agreements and,

as a result, our operations, reputations and business could be severely

harmed.

If

Hebei Consulting exercises the purchase option it holds over Buddha’s share

capital pursuant to the VIE Agreements, the payment of the purchase price could

materially and adversely affect our financial position

Under the

VIE Agreements, Buddha’s shareholders have granted Hebei Consulting

an option for the maximum period of time permitted by law to purchase all

of the equity interest in Buddha at a price equal to the capital paid

in by the transferors, adjusted pro rata for purchase of less than all of

the equity interest, unless applicable PRC laws and regulations require an

appraisal of the Equity Interest or stipulate other restrictions regarding the

purchase price of the equity interest. As Buddha is already our

contractually controlled affiliate, Hebei Consulting’s exercising of the option

would not bring immediate benefits to our company, and payment of the purchase

prices could adversely affect our financial position.

RISKS

RELATED TO DOING BUSINESS IN CHINA

Changes

in China's political or economic situation could harm us and our operating

results.

Economic

reforms adopted by the Chinese government have had a positive effect on the

economic development of the country, but the government could change these

economic reforms or any of the legal systems at any time. This could either

benefit or damage our operations and profitability. Some of the things that

could have this effect are:

|

|

·

|

Level

of government involvement in the

economy;

|

|

|

·

|

Control

of foreign exchange;

|

|

|

·

|

Methods

of allocating resources;

|

|

|

·

|

Balance

of payments position;

|

|

|

·

|

International

trade restrictions; and

|

|

|

·

|

International

conflict.

|

The

Chinese economy differs from the economies of most countries belonging to the

Organization for Economic Cooperation and Development, or OECD, in many ways.

For example, state-owned enterprises still constitute a large portion of the

Chinese economy and weak corporate governance and a lack of flexible currency

exchange policy still prevail in China. As a result of these differences, we may

not develop in the same way or at the same rate as might be expected if the

Chinese economy was similar to those of the OECD member countries.

Uncertainties

with respect to the PRC legal system could limit the legal protections available

to you and us.

We

conduct substantially all of our business through our operating subsidiary and

affiliate in the PRC. Our principal operating subsidiary and affiliate,

Hebei Consulting and Buddha, are subject to laws and regulations applicable to

foreign investments in China and, in particular, laws applicable to

foreign-invested enterprises. The PRC legal system is based on written statutes,

and prior court decisions may be cited for reference but have limited

precedential value. Since 1979, a series of new PRC laws and regulations have

significantly enhanced the protections afforded to various forms of foreign

investments in China. However, since the PRC legal system continues to evolve

rapidly, the interpretations of many laws, regulations and rules are not always

uniform and enforcement of these laws, regulations and rules involves

uncertainties, which may limit legal protections available to you and us. In

addition, any litigation in China may be protracted and result in substantial

costs and diversion of resources and management attention. In addition, all of

our executive officers and all of our directors are residents of China and not

of the United States, and substantially all the assets of these persons are

located outside the United States. As a result, it could be difficult for

investors to effect service of process in the United States or to enforce a

judgment obtained in the United States against our Chinese operations,

subsidiary and affiliate.

You

may have difficulty enforcing judgments against us.

We are a

Delaware holding company, but Gold Promise is a Hong Kong company, and our

principal operating affiliate and subsidiary, Buddha and Hebei Consulting, are

located in the PRC. Most of our assets are located outside the United

States and most of our current operations are conducted in the PRC. In addition,

most of our directors and officers are nationals and residents of countries

other than the United States. A substantial portion of the assets of these

persons is located outside the United States. As a result, it may be difficult

for you to effect service of process within the United States upon these

persons. It may also be difficult for you to enforce in U.S. courts judgments

predicated on the civil liability provisions of the U.S. federal securities laws

against us and our officers and directors, most of whom are not residents in the

United States and the substantial majority of whose assets are located outside

the United States. In addition, there is uncertainty as to whether the courts of

the PRC would recognize or enforce judgments of U.S. courts. The recognition and

enforcement of foreign judgments are provided for under the PRC Civil Procedures

Law. Courts in China may recognize and enforce foreign judgments in accordance

with the requirements of the PRC Civil Procedures Law based on treaties between

China and the country where the judgment is made or on reciprocity between

jurisdictions. China does not have any treaties or other arrangements that

provide for the reciprocal recognition and enforcement of foreign judgments with

the United States. In addition, according to the PRC Civil Procedures Law,

courts in the PRC will not enforce a foreign judgment against us or our

directors and officers if they decide that the judgment violates basic

principles of PRC law or national sovereignty, security or the public interest.

So it is uncertain whether a PRC court would enforce a judgment rendered by a

court in the United States.

The

PRC government exerts substantial influence over the manner in which we must

conduct our business activities.

The PRC

government has exercised and continues to exercise substantial control over

virtually every sector of the Chinese economy through regulation and state

ownership. Our ability to operate in China may be harmed by changes in its laws

and regulations, including those relating to taxation, import and export

tariffs, environmental regulations, land use rights, property and other matters.

We believe that our operations in China are in material compliance with all

applicable legal and regulatory requirements. However, the central or local

governments of the jurisdictions in which we operate may impose new, stricter

regulations or interpretations of existing regulations that would require

additional expenditures and efforts on our part to ensure our compliance with

such regulations or interpretations.

Accordingly,

government actions in the future, including any decision not to continue to

support recent economic reforms and to return to a more centrally planned

economy or regional or local variations in the implementation of economic

policies, could have a significant effect on economic conditions in China or

particular regions thereof and could require us to divest ourselves of any

interest we then hold in Chinese properties or joint ventures.

Future

inflation in China may inhibit our ability to conduct business in

China.

In recent

years, the Chinese economy has experienced periods of rapid expansion and highly