Attached files

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on April 20, 2010

Registration Number 333-164590

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment No. 4

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

DOUGLAS DYNAMICS, INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 3531 | 134275891 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

7777 North 73rd Street

Milwaukee, Wisconsin 53223

(414) 354-2310

(Address, including zip code, and telephone number, including

area code, of registrant's of principal executive offices)

James L. Janik

President and Chief Executive Officer

Douglas Dynamics, Inc.

7777 North 73rd Street

Milwaukee, Wisconsin 53223

(414) 354-2310

(Name, address and telephone number, including area code, of agent for service)

Copies to:

| Bruce D. Meyer Ari B. Lanin Gibson, Dunn & Crutcher LLP 333 South Grand Avenue Los Angeles, CA 90071 (213) 229-7000 |

Gregg A. Noel Skadden, Arps, Slate, Meagher & Flom LLP 300 South Grand Avenue Los Angeles, CA 90071 (213) 687-5000 |

As soon as practicable after this Registration Statement becomes effective.

(Approximate date of commencement of proposed sale to the public)

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

|

||||||

| Title of Each Class of Securities to be Registered |

Amount to be Registered(1) |

Proposed Maximum Aggregate Offering Price(2) |

Amount of Registration Fee |

|||

|---|---|---|---|---|---|---|

Common Stock, $.01 par value |

11,500,000 | $184,000,000 | $13,119.20(3) | |||

|

||||||

- (1)

- Includes 1,500,000 shares that the underwriters have the option to purchase to cover overallotments, if any.

- (2)

- Estimated

solely for the purpose of computing the amount of the registration fee, in accordance with Rule 457(a) promulgated under the Securities Act

of 1933.

- (3)

- A filing fee of $10,695 was previously paid in connection with the filing of this Registration Statement on January 29, 2010. The aggregate filing fee of $13,119.20 is being offset by the $10,695 previously paid.

THE REGISTRANT HEREBY AMENDS THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS MAY BE NECESSARY TO DELAY ITS EFFECTIVE DATE UNTIL THE REGISTRANT SHALL FILE A FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THIS REGISTRATION STATEMENT SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(A) OF THE SECURITIES ACT OF 1933, OR UNTIL THE REGISTRATION STATEMENT SHALL BECOME EFFECTIVE ON SUCH DATE AS THE COMMISSION, ACTING PURSUANT TO SAID SECTION 8(A), MAY DETERMINE.

The information in this prospectus is not complete and may be changed. We and the selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED APRIL 20, 2010

10,000,000 Shares

Douglas Dynamics, Inc.

Common Stock

This is the initial public offering of our common stock. We are selling 4,900,000 shares of common stock and the selling stockholders are selling 5,100,000 shares of common stock. We will not receive any proceeds from the sale of shares of common stock by the selling stockholders. Prior to this offering there has been no public market for our common stock. The initial public offering price of our common stock is expected to be between $14.00 and $16.00 per share. We have applied to list our common stock on the New York Stock Exchange under the symbol "PLOW."

The underwriters have a 30-day option to purchase on a pro rata basis an aggregate of 1,500,000 additional outstanding shares from the selling stockholders to cover over-allotments of shares.

Investing in our common stock involves risks. See "Risk Factors" beginning on page 14.

| |

Price to Public |

Underwriting Discounts and Commissions |

Proceeds to Douglas Dynamics, Inc. |

Proceeds to Selling Stockholders |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Per Share | $ | $ | $ | $ | |||||||||

| Total | $ | $ | $ | $ | |||||||||

Delivery of the shares of our common stock will be made on or about , 2010.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Credit Suisse | Oppenheimer & Co. | |

Baird |

Piper Jaffray |

The date of this prospectus is , 2010.

You should rely only on the information contained in this prospectus. We have not, and the underwriters have not, authorized anyone to provide you with information that is different. The information in this prospectus may only be accurate as of the date on the cover page of this prospectus. This prospectus does not constitute an offer to sell, or a solicitation of an offer to buy, any securities offered hereby in any jurisdiction where, or to any person to whom, it is unlawful to make such offer or solicitation.

Dealer Prospectus Delivery Obligation

Until , 2010 (25 days after the commencement of this offering), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealer's obligation to deliver a prospectus when acting as an underwriter and with respect to their unsold allotments or subscriptions.

The following summary should be read together with, and is qualified in its entirety by, the more detailed information and financial statements and related notes included elsewhere in this prospectus. The following summary does not contain all of the information you should consider before investing in our common stock. For a more complete understanding of this offering, we encourage you to read this entire prospectus, including the "Risk Factors" section, before making an investment in our common stock. All information in this prospectus has been adjusted to give effect to a 23.75-for-one stock split of our common stock that will be effective immediately prior to the consummation of the offering, unless otherwise specified.

In this prospectus, unless the context indicates otherwise: "Douglas Dynamics," the "Company," "we," "our," "ours" or "us" refer to Douglas Dynamics, Inc. (formerly known as Douglas Dynamics Holdings, Inc.) and its subsidiaries and "Douglas Holdings" refers to Douglas Dynamics, Inc. exclusive of its subsidiaries. Douglas Dynamics, Inc. is a Delaware corporation and the issuer of the common stock offered hereby.

Our Company

We are the North American leader in the design, manufacture and sale of snow and ice control equipment for light trucks, which consists of snowplows and sand and salt spreaders, and related parts and accessories. We sell our products under the WESTERN®, FISHER® and BLIZZARD® brands which are among the most established and recognized in the industry. We believe that in 2009 our share of the light truck snow and ice control equipment market was greater than 50%. In 2009, we generated net sales, Adjusted EBITDA (as defined in "—Summary Historical Consolidated Financial and Operating Data") and net income of $174.3 million, $45.2 million and $9.8 million, respectively, as compared to net sales, Adjusted EBITDA and net income of $180.1 million, $47.7 million and $11.5 million, respectively, for 2008. See "—Summary Historical Consolidated Financial and Operating Data" for a discussion of why management uses Adjusted EBITDA to measure our financial performance, and a reconciliation of net income to Adjusted EBITDA.

We offer the broadest and most complete product line of snowplows and sand and salt spreaders for light trucks in the U.S. and Canadian markets. We also provide a full range of related parts and accessories, which generates an ancillary revenue stream throughout the lifecycle of our snow and ice control equipment. For the year ended December 31, 2009, 85% of our net sales were generated from sales of snow and ice control equipment, and 15% of our net sales were generated from sales of parts and accessories.

We sell our products through a distributor network primarily to professional snowplowers who are contracted to remove snow and ice from commercial, municipal and residential areas. Over the last 50 years, we have engendered exceptional customer loyalty for our products because of our ability to satisfy the stringent demands of our customers for a high degree of quality, reliability and service. As a result, we believe our installed base is the largest in the industry with over 500,000 snowplows and sand and salt spreaders in service. Because sales of snowplows and sand and salt spreaders are primarily driven by the need of our core end-user base to replace worn existing equipment, we believe our substantial installed base provides us with a high degree of predictable sales over any extended period of time.

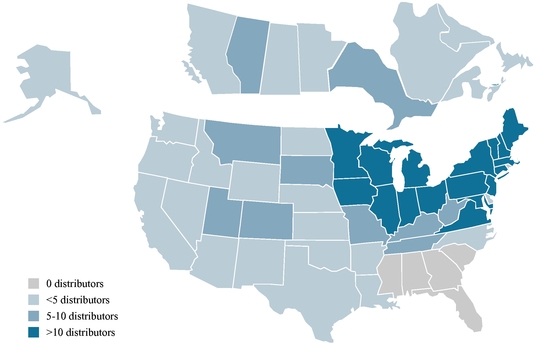

We believe we have the industry's most extensive North American distributor network, which primarily consists of over 720 truck equipment distributors who purchase directly from us and are located throughout the snowbelt regions in North America (primarily the Midwest, East and Northeast regions of the United States as well as all provinces of Canada). Beginning in 2005, we began to extend our reach to international markets, establishing distribution relationships in Northern Europe and Asia, where we believe meaningful growth opportunities exist.

We believe we are the industry's most operationally efficient manufacturer due to our vertical integration, highly variable cost structure and intense focus on lean manufacturing. We continually seek

1

to use lean principles to reduce costs and increase the efficiency of our manufacturing operations. Our manufacturing efficiencies have contributed to the increase of our gross profit per unit by approximately 3.0% per annum, compounded annually, from 2000 to 2009. While we currently manufacture our products in three facilities that we own in Milwaukee, Wisconsin, Rockland, Maine and Johnson City, Tennessee, we have improved our manufacturing efficiency to the point that we will be closing our Johnson City, Tennessee facility effective mid-2010. We expect that the closing of this facility will yield estimated cost savings of approximately $4 million annually, with no anticipated reduction in production capacity. Furthermore, our manufacturing efficiency allows us to deliver desired products quickly to our customers during times of sudden and unpredictable snowfall events when our customers need our products immediately.

Our Industry

The light truck snow and ice control equipment industry in North America consists predominantly of domestic participants that manufacture their products in North America. The annual demand for snow and ice control equipment is driven primarily by the replacement cycle of the existing installed base, which is predominantly a function of the average life of a snowplow or spreader and is driven by usage and maintenance practices of the end-user. We believe actively-used snowplows are typically replaced, on average, every 7 to 8 years.

The primary factor influencing the replacement cycle for snow and ice control equipment is the level, timing and location of snowfall. Sales of snow and ice control equipment in any given year and region are most heavily influenced by local snowfall levels in the prior snow season. Heavy snowfall during a given winter causes equipment usage to increase, resulting in greater wear and tear and shortened life cycles, thereby creating a need for replacement equipment and additional parts and accessories.

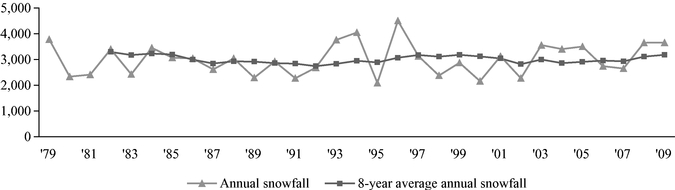

While snowfall levels vary within a given year and from year-to-year, snowfall, and the corresponding replacement cycle of snow and ice control equipment, is relatively consistent over multi-year periods. The following chart depicts aggregate annual and eight-year (based on the typical life of our snowplows) rolling average of the aggregate snowfall levels in 66 cities in 26 snowbelt states across the Northeast, East, Midwest and Western United States where we monitor snowfall levels) from 1980 to 2009. As the chart indicates, since 1982 aggregate snowfall levels in any given rolling eight-year period have been fairly consistent, ranging from 2,742 to 3,295 inches.

Snowfall in Snowbelt States (inches)

(for October 1 through March 31)

- Note:

- The 8-year rolling average snowfall is not presented prior to 1982 for purposes of the calculation due to lack of snowfall data prior to 1975. Snowfall data in this chart is not adjusted for snowfall outside of the 66 cities in the 26 states reflected.

Source: National Oceanic and Atmospheric Administration's National Weather Service.

The demand for snow and ice control equipment can also be influenced by general economic conditions in the United States, as well as local economic conditions in the snowbelt regions in North America. In stronger economic conditions, our end-users may choose to replace or upgrade existing equipment before its useful life has ended, while in weak economic conditions, our end-users may seek

2

to extend the useful life of equipment, thereby increasing the sales of parts and accessories. However, since snow and ice control management is a non-discretionary service necessary to ensure public safety and continued personal and commercial mobility in populated areas that receive snowfall, end-users cannot extend the useful life of snow and ice control equipment indefinitely and must replace equipment that has become too worn, unsafe or unreliable, regardless of economic conditions.

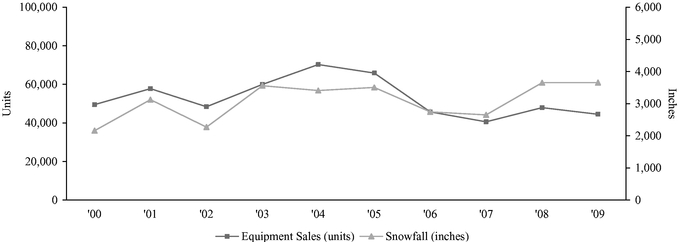

Sales of parts and accessories for 2008 and 2009, respectively, were approximately 85.8% and 58.3% higher than average annual parts and accessories sales over the preceding ten years, which management believes is largely a result of the deferral of new equipment purchases due to the recent economic downturn. Although sales of snow and ice control units increased in 2008 and 2009 as compared to 2007, management believes that absent the recent economic downturn, equipment sales in 2008 and 2009 would have been considerably higher due to the high levels of snowfall during these years, as equipment unit sales in 2008 and 2009 remained below the ten-year average, while snowfall levels in 2008 and 2009 were considerably above the ten-year average. Management believes this deferral of new equipment purchases could result in an elevated multi-year replacement cycle as the economy recovers.

Long-term growth in the overall snow and ice control equipment market also results from geographic expansion of developed areas in the snowbelt regions of North America, as well as consumer demand for technological enhancements in snow and ice control equipment and related parts and accessories that improves efficiency and reliability. Continued construction in the snowbelt regions in North America increases the aggregate area requiring snow and ice removal, thereby growing the market for snow and ice control equipment. In addition, the development and sale of more reliable, more efficient and more sophisticated products have contributed to an approximate 2% to 4% average unit price increase in each of the past five years.

Our Competitive Strengths

We compete solely with other North American manufacturers who do not benefit from our extensive distributor network, manufacturing efficiencies and depth and breadth of products. As the market leader in snow and ice control equipment for light trucks, we enjoy a set of competitive advantages versus smaller, more regionally-focused equipment providers, which allows us to generate robust cash flows in all snowfall environments and to support continued investment in our products, distribution capabilities and brand regardless of annual volume fluctuations. We believe these advantages are rooted in the following competitive strengths and reinforces our industry leadership over time.

Exceptional Customer Loyalty and Brand Equity. Our brands enjoy exceptional customer loyalty and brand equity in the snow and ice control equipment industry with both end-users and distributors which have been developed through over 50 years of superior innovation, productivity, reliability and support, consistently delivered season after season. We believe past brand experience, rather than price, is the key factor impacting snowplow purchasing decisions.

Broadest and Most Innovative Product Offering. We provide the industry's broadest product offering with a full range of snowplows, sand and salt spreaders and related parts and accessories. We believe we maintain the industry's largest and most advanced in-house new product development program, historically introducing several new and redesigned products each year. Our broad product offering and commitment to new product development is essential to maintaining and growing our leading market share position as well as continuing to increase the profitability of our business.

Extensive North American Distributor Network. With over 720 direct distributors, we benefit from having the most extensive North American direct distributor network in the industry, providing a significant competitive advantage over our peers. Our distributors function not only as sales and support agents (providing access to parts and service), but also as industry partners providing real-time

3

end-user information, such as retail inventory levels, changing consumer preferences or desired functionality enhancements, which we use as the basis for our product development efforts.

Leader in Operational Efficiency. We believe we are a leader in operational efficiency in our industry, resulting from our application of lean manufacturing principles and a highly variable cost structure. By utilizing lean principles, we are able to adjust production levels easily to meet fluctuating demand, while controlling costs in slower periods. This operational efficiency is supplemented by our highly variable cost structure, driven in part by our access to a sizable temporary workforce (comprising approximately 10-15% of our total workforce), which we can quickly adjust, as needed. These manufacturing efficiencies enable us to respond rapidly to urgent customer demand during times of sudden and unpredictable snowfalls, allowing us to provide exceptional service to our existing customer base and capture new customers from competitors that we believe cannot service their customers' needs with the same speed and reliability.

Strong Cash Flow Generation. We are able to generate significant cash flow as a result of relatively consistent high profitability (Adjusted EBITDA Margins averaged 25.4% for the three-year period from 2007 to 2009), low capital spending requirements and predictable timing of our working capital requirements. Our cash flow results will also benefit substantially from approximately $18 million of annual tax-deductible intangible and goodwill expense over the next ten years, which has the impact of reducing our corporate taxes owed by approximately $6.7 million on an annual basis during this period, in the event we have sufficient taxable income to utilize such benefit. Our significant cash flow has allowed us to reinvest in our business, pay down long term debt by approximately $17 million over the past six years and pay substantial dividends on a pro rata basis to our stockholders, although no such dividends have been declared since 2006.

Experienced Management Team. We believe our business benefits from an exceptional management team that is responsible for establishing our leadership in the snow and ice control equipment industry for light trucks. Our senior management team, consisting of four officers, has an average of approximately 19 years of weather-related industry experience and an average of over nine years with our company. James Janik, our President and Chief Executive Officer, has been with us for over 17 years and in his current role since 2000, and through his strategic vision, we have been able to expand our distributor network and grow our market leading position.

Our Business Strategy

Our business strategy is to capitalize on our competitive strengths to maximize cash flow to pay dividends, reduce indebtedness and reinvest in our business to create stockholder value. The building blocks of our strategy are:

Continuous Product Innovation. We believe new product innovation is critical to maintaining and growing our market-leading position in the snow and ice control equipment industry. We will continue to focus on developing innovative solutions to increase productivity, ease of use, reliability, durability and serviceability of our products and on incorporating lean manufacturing concepts into our product development process, which has allowed us to reduce the overall cost of development and, more importantly, to reduce our time-to-market by nearly one-half. As a result of these efforts, approximately $73 million or 50% of our 2009 equipment sales came from products introduced or redesigned in the last five years.

Distributor Network Optimization. Over the last ten years, we have grown our network by over 250 distributors. We will continually seek opportunities to continue to expand our extensive distribution network by adding high-quality, well-capitalized distributors in select geographic areas and by cross-selling our industry-leading brands within our distribution network to ensure we maximize our ability to generate revenue while protecting our industry leading reputation, customer loyalty and brands. We will also focus on optimizing this network by providing in-depth training, valuable distributor support and

4

attractive promotional and incentive opportunities. As a result of these efforts, we believe a majority of our distributors choose to sell our products exclusively. We believe this sizable high quality network is unique in the industry, providing us with valuable insight into purchasing trends and customer preferences, and would be very difficult to replicate.

Aggressive Asset Management and Profit Focus. We will continue to aggressively manage our assets in order to maximize our cash flow generation despite seasonal and annual variability in snowfall levels. We believe our ability is unique in our industry and enables us to achieve attractive margins in all snowfall environments. Key elements of our asset management and profit focus strategies include:

- •

- employment of a highly variable cost structure, which allows us to quickly adjust costs in response to

real-time changes in demand;

- •

- use of enterprise-wide lean principles, which allow us to easily adjust production levels up or down to meet

demand;

- •

- implementation of a pre-season order program, which incentivizes distributors to place orders prior to the

retail selling season and thereby enables us to more efficiently utilize our assets; and

- •

- development of a vertically integrated business model, which we believe provides us cost advantages over our competition.

Additionally, although modest, our capital expenditure requirements and operating expenses can be temporarily reduced in response to anticipated or actual lower sales in a particular year to maximize cash flow.

Flexible, Lean Enterprise Platform. We will continue to utilize lean principles to maximize the flexibility, efficiency and productivity of our manufacturing operations while reducing the associated costs, enabling us to increase distributor and end-user satisfaction. For example, in an environment where shorter lead times and near-perfect order fulfillment are important to our distributors, we believe our lean processes have helped us to improve our shipping performance and build a reputation for providing industry leading shipping performance. In 2009, we fulfilled 98.2% of our orders on or before the requested ship date, without error in content, packaging or delivery, representing our strongest shipping performance to date, as compared to 71.0% in 2005 and 81.5% in 2008.

Our cost reduction efforts also include the rationalization of our supply base and implementation of a global sourcing strategy, resulting in approximately $3.2 million of cumulative annualized cost savings from 2006 to 2009 with the goal of an additional $1.1 million in annualized cost savings in 2010. In January 2009, we opened a sourcing office in China, which will become our central focus for specific component purchases and will provide a majority of our procurement cost savings in the future.

Our Growth Opportunities

Increase Our Industry Leading Market Share. We plan to leverage our industry leading position, distribution network and new product innovation capabilities to capture market share in the North American snow and ice control equipment market, focusing our primary efforts on increasing penetration in those North American markets where we believe our overall market share is less than 50%. We also plan to continue growing our presence in the snow and ice control equipment market outside of North America, particularly in Asia and Europe, which we believe could provide significant growth opportunities in the future.

Opportunistically Seek New Products and New Markets. We will consider external growth opportunities within the snow and ice control industry and other equipment or component markets. We plan to continue to evaluate acquisition opportunities within our industry that can help us expand our distribution reach, enhance our technology and as a consequence improve the breadth and depth of our product lines. We also consider diversification opportunities in adjacent markets that complement our business model and could offer us the ability to leverage our core competencies to create stockholder value.

5

Recent Developments

As described under "Management's Discussion and Analysis—Seasonality and Year-To-Year Variability," our revenue and operating results tend to be lowest during the first quarter, during which period we typically experience negative earnings as the snow season draws to a close. Our first quarter revenue has varied from approximately $7.9 million to approximately $22.4 million between 2005 and 2009. Management expects revenue for the period ended March 31, 2010 to be approximately in line with the middle of the range of first quarter revenue for the period from 2005 to 2009. During this five-year period, net income during the first quarter has varied from a net loss of approximately $2.9 million to a net loss of approximately $6.5 million, with an average net loss of $4.7 million. Consistent with this historical seasonality, management currently expects to have a net loss for the period ended March 31, 2010 at the higher end of our historical experience over the last five years, due largely to costs associated with the closure of our Johnson City, Tennessee facility.

During the second quarter of 2010 we expect to incur non-cash charges related to the exercise of outstanding options by management and other optionholders and the write-off of deferred financing fees incurred in connection with our senior notes. In addition, we will incur cash expenses of $5.8 million related to the termination of our Management Services Agreement and $2.9 million related to the premium paid in connection with the redemption of our senior notes in connection with this offering.

Summary Risk Factors

An investment in our common stock involves a high degree of risk. You should carefully consider the risks summarized below, the risks described under "Risk Factors" beginning on page 14 and the other information contained in this prospectus, including our consolidated financial statements and the related notes, before deciding to purchase any shares of our common stock:

- •

- our results of operations depend primarily on the level, timing and location of snowfall in the regions in which we offer

our products;

- •

- the seasonality and year-to-year variability of our business can cause our results of operations

and financial condition to be materially different from quarter-to-quarter and from year-to-year;

- •

- if economic conditions in the United States continue to remain weak or deteriorate further, our results of operations and

ability to pay dividends may be adversely affected;

- •

- our failure to maintain good relationships with our distributors, the loss or consolidation of our distributor base or the

actions or inactions of our distributors could have an adverse effect on our results of operations and ability to pay dividends;

- •

- if we are unable to develop new products or improve upon our existing products on a timely basis, our business and

financial condition could be adversely affected;

- •

- if our costs of labor or the price of steel or other components of our products increase, our gross margins could decline;

- •

- you may not receive the level of dividends provided for in the dividend policy that our Board of Directors will adopt or

any dividends at all; and

- •

- satisfying our debt service obligations and paying dividends may leave us with insufficient cash to fund unexpected cash needs and growth.

Contemplated Financing Transactions in Connection with this Offering

In connection with this offering, we intend to increase our existing term loan facility by $40 million. We will use the proceeds from this offering together with proceeds from this increase in our term loan facility to redeem the outstanding 73/4% Senior Notes due 2012, which we refer to in this prospectus as our senior notes, issued by our direct wholly-owned subsidiaries, Douglas Dynamics, L.L.C. which we refer to in this prospectus as Douglas LLC, and Douglas Dynamics Finance

6

Company, which we refer to in this prospectus as Douglas Finance. The total redemption amount is expected to be approximately $157.3 million, which amount includes accrued and unpaid interest and the associated redemption premium. Concurrent with the consummation of this offering, we also intend to amend our existing term loan and revolving credit facilities to permit the redemption of our senior notes.

Interests of Certain Affiliates in this Offering

Certain of our officers, directors and other affiliates may stand to benefit as a result of this offering.

Specifically, certain of our executive officers will exercise stock options and sell the underlying shares of common stock in this offering and will also be entitled to payments under our Liquidity Bonus Plan that provides for an aggregate cash bonus payment of $1 million to be distributed to eligible employees, including our officers. Additionally, our Chief Executive Officer holds deferred stock units that will convert into an equivalent number of shares of our common stock upon expiration of the lock-up agreement entered into by him. Certain of our officers and directors will also receive grants of restricted stock immediately prior to the pricing of our common stock sold in this offering.

The Aurora Entities and Ares, together with certain of our other stockholders, will also sell a portion of their shares of our common stock in this offering. We will also redeem the one share of Series B preferred stock and Series C preferred stock held respectively by Aurora Equity Partners II L.P. and Ares Corporate Opportunities Fund, L.P., which we refer to in this prospectus as Ares, at a price of $1,000 per share. In addition, Aurora Management Partners LLC, an affiliate of the Aurora Entities, together with ACOF Management, L.P., an affiliate of Ares, will receive an aggregate payment of approximately $5.8 million in connection with the amendment and restatement of our Amended and Restated Joint Management Services Agreement, which we refer to in its current form in this prospectus as the Management Services Agreement.

For a description of the interests of these parties in this offering, see "Interests of Certain Affiliates in this Offering."

Company Information

Douglas Holdings is a holding corporation that was formed and capitalized by Aurora Equity Partners II L.P., a Delaware limited partnership, and Aurora Overseas Equity Partners II, L.P., a Cayman Islands exempt limited partnership, which we collectively refer to in this prospectus as the Aurora Entities.

Douglas Holdings was formed for the purpose of effectuating the acquisition of our business in March 2004 from AK Steel Corporation, which we refer to in this prospectus as the Acquisition. Douglas Holdings owns all of the issued and outstanding limited liability company interests of Douglas LLC, our operating company, together with its subsidiaries.

We maintain our principal executive offices at 7777 North 73rd Street, Milwaukee, Wisconsin 53223, and our telephone number is (414) 354-2310. We maintain a website at www.DouglasDynamics.com. Information contained on our website is not a part of, and is not incorporated by reference into, this prospectus.

"WESTERN," "FISHER" and "BLIZZARD" and their respective logos are trademarks. Solely for convenience, from time to time we refer to our trademarks in this prospectus without the ® symbols, but such references are not intended to indicate that we will not assert, to the fullest extent under applicable law, our rights to our trademarks.

7

Issuer |

Douglas Dynamics, Inc. | |

Common stock offered by us |

4,900,000 shares |

|

Common stock offered by the selling stockholders |

5,100,000 shares |

|

Over-allotment option |

The selling stockholders have granted the underwriters a 30-day option to purchase up to 1,500,000 additional outstanding shares of common stock from the selling stockholders at the initial public offering price less underwriting discounts and commissions. The option may be exercised only to cover any over-allotments. |

|

Common stock outstanding after this offering |

19,769,539 shares. |

|

Use of proceeds |

We will use the net proceeds from this offering together with an increase in our term loan facility to redeem our senior notes, including accrued and unpaid interest and the related redemption premium, for an estimated total of $157.3 million. We will not receive any proceeds from the sale of shares by the selling stockholders, including any shares sold pursuant to the underwriters' over-allotment option. See "Use of Proceeds." |

|

Dividend policy |

Our Board of Directors will adopt a dividend policy, effective upon the consummation of this offering, that reflects an intention to distribute to our stockholders a regular quarterly cash dividend, commencing during the first full fiscal quarter following the consummation of this offering at an initial annual rate of $0.78 per share. The declaration and payment of these dividends will be at the discretion of our Board of Directors and will depend upon many factors, including our financial condition and earnings, legal requirements, taxes, the terms of our indebtedness and other factors our Board of Directors may deem to be relevant. See "Dividend Policy and Restrictions." |

|

Risk factors |

See "Risk Factors" beginning on page 14 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

|

Proposed NYSE symbol |

PLOW |

8

Unless otherwise noted, all information in this prospectus assumes:

- •

- no exercise of the underwriters' over-allotment option;

- •

- the repurchase, after the consummation of this offering, of all of our senior notes, including accrued and unpaid interest

through the anticipated redemption date (30 days following the consummation of this offering) and the associated redemption premium for a total of approximately $157.3 million;

- •

- a 23.75-for-one stock split of our common stock that will occur prior to the consummation of this offering; and

- •

- a public offering price of $15.00 per share of our common stock, which is the mid-point of the range set forth on the cover page of this prospectus.

9

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL AND OPERATING DATA

The following summary consolidated financial information as of and for the years ended December 31, 2007, 2008 and 2009 are derived from our audited consolidated financial statements which are included elsewhere in this prospectus.

The results indicated below and elsewhere in this prospectus are not necessarily indicative of our future performance. You should read this information together with "Selected Consolidated Financial Data," "Capitalization," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes included elsewhere in this prospectus.

| |

For the year ended December 31 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2007 | 2008 | 2009 | |||||||

| |

(in thousands) |

|||||||||

Consolidated Statement of Operations Data |

||||||||||

Equipment sales |

$ | 122,091 | $ | 151,450 | $ | 147,478 | ||||

Parts and accessories sales |

17,974 | 28,658 | 26,864 | |||||||

Net sales |

140,065 | 180,108 | 174,342 | |||||||

Cost of sales |

97,249 | 117,911 | 117,264 | |||||||

Gross profit |

42,816 | 62,197 | 57,078 | |||||||

Selling, general and administrative expense(1) |

22,180 | 26,561 | 27,639 | |||||||

Income from operations |

20,636 | 35,636 | 29,439 | |||||||

Interest expense, net |

(19,622 | ) | (17,299 | ) | (15,520 | ) | ||||

Loss on extinguishment of debt |

(2,733 | ) | — | — | ||||||

Other income (expense), net |

(87 | ) | (73 | ) | (90 | ) | ||||

Income (loss) before taxes |

(1,806 | ) | 18,264 | 13,829 | ||||||

Income tax expense (benefit) |

(749 | ) | 6,793 | 3,986 | ||||||

Net income (loss) |

$ | (1,057 | ) | $ | 11,471 | $ | 9,843 | |||

Cash Flow |

||||||||||

Net cash provided by operating activities |

$ | 20,040 | $ | 23,411 | $ | 25,571 | ||||

Net cash used in investing activities |

(1,045 | ) | (3,113 | ) | (8,200 | ) | ||||

Net cash provided by (used in) financing activities |

$ | 4,083 | $ | (2,265 | ) | $ | (1,850 | ) | ||

Other Data |

||||||||||

Adjusted EBITDA |

$ | 32,745 | $ | 47,742 | $ | 45,180 | ||||

Capital expenditures(2) |

$ | 1,049 | $ | 3,160 | $ | 8,200 | ||||

| |

As of December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2007 | 2008 | 2009 | |||||||

| |

(in thousands) |

|||||||||

Selected Balance Sheet Data |

||||||||||

Cash and cash equivalents |

$ | 35,519 | $ | 53,552 | $ | 69,073 | ||||

Total assets |

375,649 | 391,264 | 404,619 | |||||||

Total debt |

234,363 | 233,513 | 232,663 | |||||||

Total liabilities |

283,705 | 293,203 | 296,395 | |||||||

Total redeemable stock and stockholders' equity |

91,944 | 98,061 | $ | 108,224 | ||||||

- (1)

- Includes

management fees incurred with respect to related parties.

- (2)

- Capital expenditures for the year ended December 31, 2009 include $5 million related to the investments in our Milwaukee, Wisconsin and Rockland, Maine manufacturing facilities to support the closure of our Johnson City, Tennessee manufacturing facility.

10

Discussion of Adjusted EBITDA

In addition to our results under United States generally accepted accounting principles, which we refer to in this prospectus as GAAP, we also use Adjusted EBITDA and Adjusted EBITDA Margin, non-GAAP financial measures, which we consider to be important and supplemental measures of our performance. Adjusted EBITDA represents net income before interest, taxes, depreciation and amortization, as further adjusted for certain non-recurring charges related to the closure of our Johnson City, Tennessee manufacturing facility, certain unrelated legal expenses and a one-time stock option repurchase, as well as management fees paid by us to Aurora Management Partners LLC, a Delaware limited liability company and an affiliate of the Aurora Entities, and ACOF Management, L.P., a Delaware limited partnership and an affiliate of Ares. Adjusted EBITDA Margin is defined as Adjusted EBITDA as a percentage of net sales. We use, and we believe our investors, and in particular, the Aurora Entities and Ares, which we collectively refer to as our principal stockholders in this prospectus, benefit from the presentation of Adjusted EBITDA and Adjusted EBITDA Margin in evaluating our operating performance because they provide us and our investors with additional tools to compare our operating performance on a consistent basis by removing the impact of certain items that management believes do not directly reflect our core operations. In addition, we believe that Adjusted EBITDA and Adjusted EBITDA Margin are useful to investors and other external users of our consolidated financial statements in evaluating our operating performance as compared to that of other companies, because they allow them to measure a company's operating performance without regard to items such as interest expense, taxes, depreciation and depletion, and amortization and accretion, which can vary substantially from company to company depending upon accounting methods and book value of assets and liabilities, capital structure and the method by which assets were acquired. Our management also uses Adjusted EBITDA and Adjusted EBITDA Margin for planning purposes, including the preparation of our annual operating budget and financial projections and believes Adjusted EBITDA Margin is useful in assessing the profitability of our core businesses. Management also uses Adjusted EBITDA to evaluate our ability to make certain payments, including dividends, in compliance with our senior credit facilities, which is determined based on a calculation of "Consolidated Adjusted EBITDA" that is substantially similar to Adjusted EBITDA. The definition of Consolidated Adjusted EBITDA under our senior credit facilities after giving effect to the amendments thereto will differ from our definition of Adjusted EBITDA in this prospectus primarily because the definition in our senior credit facilities after giving effect to the amendments thereto will exclude additional non-cash charges and non-recurring expenses, which we have not incurred during the periods presented. Specifically, Consolidated Adjusted EBITDA under our senior credit facilities after giving effect to the amendments thereto will be comprised of net income before interest, taxes, depreciation and amortization as further adjusted to exclude the effect of:

- •

- expenses for management fees and termination fees paid by us pursuant to our Management Services Agreement;

- •

- non-cash items resulting in an increase in net income for such period that are unusual or otherwise non-recurring items;

- •

- certain non-cash charges including:

- •

- non-cash impairment charges;

- •

- non-cash expenses resulting from the grant of stock and stock options and other compensation to our management pursuant to

a written incentive plan or agreement;

- •

- other non-cash items that are unusual or otherwise non-recurring items;

- •

- certain non-recurring expenses including:

11

- •

- any extraordinary losses and non-recurring charges during any period (including severance, relocation costs, one-time

compensation charges and losses or charges associated with interest rate agreements);

- •

- restructuring charges or reserves (including costs related to closure of facilities);

- •

- any transaction costs incurred in connection with the issuance of securities or any refinancing transaction, in each case

whether or not such transaction is consummated;

- •

- any fees and expensed related to certain acquisitions permitted under by our senior credit facilities;

- •

- fees, expenses and other transaction costs incurred in connection with this offering and the concurrent amendments to our senior credit facilities;

and to include as a deduction in calculating Consolidated Adjusted EBITDA:

- •

- certain cash payments made during the applicable period reducing reserves or liabilities for accruals made in prior

periods but only to the extent such reserves or accruals were excluded from Consolidated Adjusted EBITDA in a prior period; and

- •

- restricted payments made during such period to Douglas Holdings to pay its general administrative costs and expenses (other than restricted payments made to Douglas Holdings for the payment of fees, expenses and other transaction costs incurred in connection with this offering or the concurrent amendments to our senior credit facilities).

Adjusted EBITDA and Adjusted EBITDA Margin have limitations as analytical tools. As a result, you should not consider them in isolation, or as substitutes for net income, operating income, operating income margin, cash flow from operating activities or any other measure of financial performance or liquidity presented in accordance with GAAP. Some of these limitations are:

- •

- Adjusted EBITDA and Adjusted EBITDA Margin do not reflect our cash expenditures or future requirements for capital

expenditures or contractual commitments;

- •

- Adjusted EBITDA and Adjusted EBITDA Margin do not reflect changes in, or cash requirements for, our working capital needs;

- •

- Adjusted EBITDA and Adjusted EBITDA Margin do not reflect the interest expense, or the cash requirements necessary to

service interest or principal payments, on our indebtedness;

- •

- Although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will

often have to be replaced in the future, and Adjusted EBITDA and Adjusted EBITDA Margin do not reflect any cash requirements for such replacements;

- •

- Other companies, including other companies in our industry, may calculate Adjusted EBITDA and Adjusted EBITDA Margin

differently than we do, limiting their usefulness as comparative measures; and

- •

- Adjusted EBITDA and Adjusted EBITDA Margin do not reflect tax obligations whether current or deferred.

The Securities and Exchange Commission, which we refer to in this prospectus as the SEC, has adopted rules to regulate the use in filings with the SEC and public disclosures and press releases of non-GAAP financial measures, such as Adjusted EBITDA and Adjusted EBITDA Margin, that are derived on the basis of methodologies other than in accordance with GAAP. These rules require, among other things:

- •

- a presentation with equal or greater prominence of the most comparable financial measure or measures calculated and presented in accordance with GAAP; and

12

- •

- a statement disclosing the purposes for which our management uses the non-GAAP financial measure.

The rules prohibit, among other things:

- •

- exclusion of charges or liabilities that require cash settlement or would have required cash settlement absent an ability

to settle in another manner, from non-GAAP liquidity measures;

- •

- adjustment of a non-GAAP performance measure to eliminate or smooth items identified as

non-recurring, infrequent or unusual, when the nature of the charge or gain is such that it is reasonably likely to recur; and

- •

- presentation of non-GAAP financial measures on the face of any financial information.

The following table presents a reconciliation of net income (loss), the most comparable GAAP financial measure, to Adjusted EBITDA as well as the resulting calculation of Adjusted EBITDA Margin, for each of the periods indicated:

| |

For the year ended December 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2007 | 2008 | 2009 | ||||||||

| |

(in thousands) |

||||||||||

Net income (loss) |

$ | (1,057 | ) | $ | 11,471 | $ | 9,843 | ||||

Interest expense—net |

19,622 | 17,299 | 15,520 | ||||||||

Loss on extinguishment of debt |

2,733 | — | — | ||||||||

Income taxes |

(749 | ) | 6,793 | 3,986 | |||||||

Depreciation expense |

4,632 | 4,650 | 5,797 | ||||||||

Amortization |

6,164 | 6,160 | 6,161 | ||||||||

EBITDA |

31,345 | 46,373 | $ | 41,307 | |||||||

Management fees |

1,400 | 1,369 | 1,393 | ||||||||

Stock option repurchase |

— | — | 732 | (1) | |||||||

Other non-recurring charges |

— | — | 1,748 | (2) | |||||||

Adjusted EBITDA |

$ | 32,745 | $ | 47,742 | $ | 45,180 | |||||

Adjusted EBITDA Margin(3) |

23.4% | 26.5% | 25.9% | ||||||||

- (1)

- Reflects

the stock-based compensation expense associated with the repurchase of stock options from certain of our executives.

- (2)

- Reflects

severance expenses and one-time, non-recurring expenses for facility preparation and moving costs related to the closure of

our Johnson City, Tennessee facility of $1,054 and certain unrelated legal expenses of $694.

- (3)

- Adjusted EBITDA Margin is defined as Adjusted EBITDA as a percentage of net sales.

13

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below and all of the other information contained in this prospectus before deciding whether to purchase our common stock. Our business, prospects, financial condition and operating results could be materially adversely affected by any of these risks, as well as other risks not currently known to us or that we currently consider immaterial. The trading price of our common stock could decline due to any of these risks, and you may lose all or part of your investment. In assessing the risks described below, you should also refer to the other information contained in this prospectus, including our consolidated financial statements and the related notes, before deciding to purchase any shares of our common stock.

Risks Related to Our Business and Industry

Our results of operations depend primarily on the level, timing and location of snowfall. As a result, a decline in snowfall levels in multiple regions for an extended time could cause our results of operations to decline and adversely affect our ability to pay dividends.

As a manufacturer of snow and ice control equipment for light trucks, and related parts and accessories, our sales depend primarily on the level, timing and location of snowfall in the regions in which we offer our products. A low level or lack of snowfall in any given year in any of the snowbelt regions in North America (primarily the Midwest, East and Northeast regions of the United States as well as all provinces of Canada) will likely cause sales of our products to decline in such year as well as the subsequent year, which in turn may adversely affect our results of operations and ability to pay dividends. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Seasonality and Year-to-Year Variability." A sustained period of reduced snowfall events in one or more of the geographic regions in which we offer our products could cause our results of operations to decline and adversely affect our ability to pay dividends.

The year-to-year variability of our business can cause our results of operations and financial condition to be materially different from year-to-year; whereas the seasonality of our business can cause our results of operations and financial condition to be materially different from quarter-to-quarter.

Because our business depends on the level, timing and location of snowfall, our results of operations vary from year-to-year. Additionally, because the annual snow season typically only runs from October 1 through March 31, our distributors typically purchase our products during the second and third quarters. As a result, we operate in a seasonal business. We not only experience seasonality in our sales, but also experience seasonality in our working capital needs. Consequently, our results of operations and financial condition can vary from year-to-year, as well as from quarter-to-quarter, which could affect our ability to pay dividends. If we are unable to effectively manage the seasonality and year-to-year variability of our business, our results of operations, financial condition and ability to pay dividends may suffer.

If economic conditions in the United States continue to remain weak or deteriorate further, our results of operations, financial condition and ability to pay dividends may be adversely affected.

Historically, demand for snow and ice control equipment for light trucks has been influenced by general economic conditions in the United States, as well as local economic conditions in the snowbelt regions in North America. During the last few years, economic conditions throughout the United States have been extremely weak, and may not improve in the foreseeable future. Weakened economic conditions may cause our end-users to delay purchases of replacement snow and ice control equipment and instead repair their existing equipment, leading to a decrease in our sales of new equipment. Weakened economic conditions may also cause our end-users to delay their purchases of new light trucks. Because our end-users tend to purchase new snow and ice control equipment concurrent with their purchase of new light trucks, their delay in purchasing new light trucks can also result in the

14

deferral of their purchases of new snow and ice control equipment. The deferral of new equipment purchases during periods of weak economic conditions may negatively affect our results of operations, financial condition and ability to pay dividends.

Weakened economic conditions may also cause our end-users to consider price more carefully in selecting new snow and ice control equipment. Historically, considerations of quality and service have outweighed considerations of price, but in a weak economy, price may become a more important factor. Any refocus away from quality in favor of cheaper equipment could cause end-users to shift away from our products to less expensive competitor products, or to shift away from our more profitable products to our less profitable products, which in turn would adversely affect our results of operations and our ability to pay dividends.

Our failure to maintain good relationships with our distributors, the loss or consolidation of our distributor base or the actions or inactions of our distributors could have an adverse effect on our results of operations and our ability to pay dividends.

We depend on a network of truck equipment distributors to sell, install and service our products. Nearly all of these sales and service relationships are at will, and less than 1% of our distributors have agreed not to offer products that compete with our products. As a result, almost all of our distributors could discontinue the sale and service of our products at any time, and those distributors that primarily sell our products may choose to sell competing products at any time. Further, difficult economic or other circumstances could cause any of our distributors to discontinue their businesses. Moreover, if our distributor base were to consolidate or if any of our distributors were to discontinue their business, competition for the business of fewer distributors would intensify. If we do not maintain good relationships with our distributors, or if we do not provide product offerings and pricing that meet the needs of our distributors, we could lose a substantial amount of our distributor base. A loss of a substantial portion of our distributor base could cause our sales to decline significantly, which would have an adverse effect on our results of operations and ability to pay dividends.

In addition, our distributors may not provide timely or adequate service to our end-users. If this occurs, our brand identity and reputation may be damaged, which would have an adverse effect on our results of operations and ability to pay dividends.

Lack of available financing options for our end-users or distributors may adversely affect our sales volumes.

Our end-user base is highly concentrated among professional snowplowers, who comprise over 50% of our end-users, many of whom are individual landscapers who remove snow during the winter and landscape during the rest of the year, rather than large, well-capitalized corporations. These end-users often depend upon credit to purchase our products. If credit is unavailable on favorable terms or at all, our end-users may not be able to purchase our products from our distributors, which would in turn reduce sales and adversely affect our results of operations and ability to pay dividends.

In addition, because our distributors, like our end-users, rely on credit to purchase our products, if our distributors are not able to obtain credit, or access credit on favorable terms, we may experience delays in payment or nonpayment for delivered products. Further, if our distributors are unable to obtain credit or access credit on favorable terms, they could experience financial difficulties or bankruptcy and cease purchases of our products altogether. Thus, if financing is unavailable on favorable terms or at all, our results of operations and ability to pay dividends would be adversely affected.

15

The price of steel, a commodity necessary to manufacture our products, is highly variable. If the price of steel increases, our gross margins could decline.

Steel is a significant raw material used to manufacture our products. During 2007, 2008 and 2009, our steel purchases were approximately 12%, 15% and 18% of our revenue, respectively. The steel industry is highly cyclical in nature, and steel prices have been volatile in recent years and may remain volatile in the future. Steel prices are influenced by numerous factors beyond our control, including general economic conditions domestically and internationally, the availability of raw materials, competition, labor costs, freight and transportation costs, production costs, import duties and other trade restrictions. After experiencing a downward trend in steel prices throughout most of 2009, steel prices may increase as a result of increased demand from the automobile and consumer durable sectors. If the price of steel increases, our variable costs may increase. We may not be able to mitigate these increased costs through the implementation of permanent price increases or temporary invoice surcharges, especially if economic conditions remain weak and our distributors and end-users become more price sensitive. If we are unable to successfully mitigate such cost increases in the future, our gross margins could decline.

We depend on outside suppliers who may be unable to meet our volume and quality requirements, and we may be unable to obtain alternative sources.

We purchase certain components essential to our snowplows and sand and salt spreaders from outside suppliers, including off-shore sources. Most of our key supply arrangements can be discontinued at any time. A supplier may encounter delays in the production and delivery of such products and components or may supply us with products and components that do not meet our quality, quantity or cost requirements. Additionally, a supplier may be forced to discontinue operations. Any discontinuation or interruption in the availability of quality products and components from one or more of our suppliers may result in increased production costs, delays in the delivery of our products and lost end-user sales, which could have an adverse effect on our business and financial condition.

In addition, we have begun to increase the number of our off-shore suppliers. Our increased reliance on off-shore sourcing may cause our business to be more susceptible to the impact of natural disasters, war and other factors that may disrupt the transportation systems or shipping lines used by our suppliers, a weakening of the dollar over an extended period of time and other uncontrollable factors such as changes in foreign regulation or economic conditions. In addition, reliance on off-shore suppliers may make it more difficult for us to respond to sudden changes in demand because of the longer lead time to obtain components from off-shore sources. We may be unable to mitigate this risk by stocking sufficient materials to satisfy any sudden or prolonged surges in demand for our products. If we cannot satisfy demand for our products in a timely manner, our sales could suffer as distributors can cancel purchase orders without penalty until shipment.

We do not sell our products under long-term purchase contracts, and sales of our products are significantly impacted by factors outside of our control; therefore, our ability to estimate demand is limited.

We do not enter into long-term purchase contracts with our distributors and the purchase orders we receive may be cancelled without penalty until shipment. Therefore, our ability to accurately predict future demand for our products is limited. Nonetheless, we attempt to estimate demand for our products for purposes of planning our annual production levels and our long-term product development and new product introductions. We base our estimates of demand on our own market assessment, snowfall figures, quarterly field inventory surveys and regular communications with our distributors. Because wide fluctuations in the level, timing and location of snowfall, economic conditions and other factors may occur, each of which is out of our control, our estimates of demand may not be accurate. Underestimating demand could result in procuring an insufficient amount of materials necessary for the production of our products, which may result in increased production costs, delays in product delivery,

16

missed sale opportunities and a decrease in customer satisfaction. Overestimating demand could result in the procurement of excessive supplies, which could result in increased inventory and associated carrying costs.

If we are unable to enforce, maintain or continue to build our intellectual property portfolio, or if others invalidate our intellectual property rights, our competitive position may be harmed.

We rely on a combination of patents, trade secrets and trademarks to protect certain of the proprietary aspects of our business and technology. We hold approximately 20 U.S. registered trademarks (including the trademarks WESTERN®, FISHER® and BLIZZARD®), 5 Canadian registered trademarks, 28 U.S. issued patents and 15 Canadian patents. Although we work diligently to protect our intellectual property rights, monitoring the unauthorized use of our intellectual property is difficult, and the steps we have taken may not prevent unauthorized use by others. In addition, in the event a third party challenges the validity of our intellectual property rights, a court may determine that our intellectual property rights may not be valid or enforceable. An adverse determination with respect to our intellectual property rights may harm our business prospects and reputation. Third parties may design around our patents or may independently develop technology similar to our trade secrets. The failure to adequately build, maintain and enforce our intellectual property portfolio could impair the strength of our technology and our brands, and harm our competitive position. Although the Company has no reason to believe that its intellectual property rights are vulnerable, previously undiscovered intellectual property could be used to invalidate our rights.

If we are unable to develop new products or improve upon our existing products on a timely basis, it could have an adverse effect on our business and financial condition.

We believe that our future success depends, in part, on our ability to develop on a timely basis new technologically advanced products or improve upon our existing products in innovative ways that meet or exceed our competitors' product offerings. Continuous product innovation ensures that our consumers have access to the latest products and features when they consider buying snow and ice control equipment. Maintaining our market position will require us to continue to invest in research and development and sales and marketing. Product development requires significant financial, technological and other resources. We may be unsuccessful in making the technological advances necessary to develop new products or improve our existing products to maintain our market position. Industry standards, end-user expectations or other products may emerge that could render one or more of our products less desirable or obsolete. If any of these events occur, it could cause decreases in sales, a failure to realize premium pricing and an adverse effect on our business and financial condition.

We face competition from other companies in our industry, and if we are unable to compete effectively with these companies, it could have an adverse effect on our sales and profitability.

We primarily compete with regional manufacturers of snow and ice control equipment for light trucks. While we are the most geographically diverse company in our industry, we may face increasing competition in the markets in which we operate. In saturated markets, price competition may lead to a decrease in our market share or a compression of our margins, both of which would affect our profitability. Moreover, current or future competitors may grow their market share and develop superior service and may have or may develop greater financial resources, lower costs, superior technology or more favorable operating conditions than we maintain. As a result, competitive pressures we face may cause price reductions for our products, which would affect our profitability or result in decreased sales and operating income. Additionally, the potential for saturation of the markets in which we compete or channel conflicts among our brands and shifts in consumer preferences may increase these competitive pressures and affect our sales and profitability. Management believes that after Douglas, the next largest competitors in the market for snow and ice control equipment for light trucks

17

are BOSS and Meyer, respectively, and accordingly represent our primary competitors for market share.

We are subject to complex laws and regulations, including environmental and safety regulations, that can adversely affect the cost, manner or feasibility of doing business.

Our operations are subject to certain federal, state and local laws and regulations relating to, among other things, the generation, storage, handling, emission, transportation, disposal and discharge of hazardous and non-hazardous substances and materials into the environment, the manufacturing of motor vehicle accessories and employee health and safety. We cannot be certain that existing and future laws and regulations and their interpretations will not harm our business or financial condition. We currently make and may be required to make large and unanticipated capital expenditures to comply with environmental and other regulations, such as:

- •

- applicable motor vehicle safety standards established by the National Highway Traffic Safety Administration;

- •

- reclamation and remediation and other environmental protection; and

- •

- standards for workplace safety established by the Occupational Safety and Health Administration.

While we monitor our compliance with applicable laws and regulations and attempt to budget for anticipated costs associated with compliance, we cannot predict the future cost of such compliance. During 2009 we expended approximately $450,000 related to compliance with such regulations and could expend similar or greater amounts in the future in the event of future legislation changes or unforeseen events, such as a workplace accident or environmental discharge, or if we otherwise discover we are in non-compliance with an applicable regulation. In addition, under these laws and regulations, we could be liable for:

- •

- product liability claims;

- •

- personal injuries;

- •

- investigation and remediation of environmental contamination and other governmental sanctions such as fines and penalties;

and

- •

- other environmental damages.

Our operations could be significantly delayed or curtailed and our costs of operations could significantly increase as a result of regulatory requirements, restrictions or claims. We are unable to predict the ultimate cost of compliance with these requirements or their effect on our operations.

Financial market conditions have had a negative impact on the return on plan assets for our pension plans, which may require additional funding and negatively impact our cash flows.

Our pension expense and required contributions to our pension plan are directly affected by the value of plan assets, the projected rate of return on plan assets, the actual rate of return on plan assets and the actuarial assumptions we use to measure the defined benefit pension plan obligations. Due to the significant financial market downturn during 2008, the funded status of our pension plans has declined. As of December 31, 2009, our pension plans were underfunded by approximately $9 million. In 2009, contributions to our defined benefit pension plans were approximately $1.4 million. If plan assets continue to perform below expectations, future pension expense and funding obligations will increase, which would have a negative impact on our cash flows. Moreover, under the Pension Protection Act of 2006, it is possible that continued losses of asset values may necessitate accelerated funding of our pension plans in the future to meet minimum federal government requirements.

18

The statements regarding our industry, market positions and market share in this prospectus are based on our management's estimates and assumptions. While we believe such statements are reasonable, such statements have not been independently verified.

Information contained in this prospectus concerning the snow and ice control equipment industry for light trucks, our general expectations concerning this industry and our market positions and other market share data regarding the industry are based on estimates our management prepared using end-user surveys, anecdotal data from our distributors and distributors that carry our competitors' products, our results of operations and management's past experience, and on assumptions made, based on our management's knowledge of this industry, all of which we believe to be reasonable. These estimates and assumptions are inherently subject to uncertainties, especially given the year-to-year variability of snowfall and the difficulty of obtaining precise information about our competitors, and may prove to be inaccurate. In addition, we have not independently verified the information from any third-party source and thus cannot guarantee its accuracy or completeness, although management also believes such information to be reasonable. Our actual operating results may vary significantly if our estimates and outlook concerning the industry, snowfall patterns, our market positions or our market shares turn out to be incorrect.

We are subject to product liability claims, product quality issues, and other litigation from time to time that could adversely affect our operating results or financial condition.

The manufacture, sale and usage of our products expose us to a risk of product liability claims. If our products are defective or used incorrectly by our end-users, injury may result, giving rise to product liability claims against us. If a product liability claim or series of claims is brought against us for uninsured liabilities or in excess of our insurance coverage, and it is ultimately determined that we are liable, our business and financial condition could suffer. Any losses that we may suffer from any liability claims, and the effect that any product liability litigation may have upon the reputation and marketability of our products, may divert management's attention from other matters and may have a negative impact on our business and operating results. Additionally, we could experience a material design or manufacturing failure in our products, a quality system failure or other safety issues, or heightened regulatory scrutiny that could warrant a recall of some of our products. A recall of some of our products could also result in increased product liability claims. Any of these issues could also result in loss of market share, reduced sales, and higher warranty expense.

We are heavily dependent on our Chief Executive Officer and management team.

Our continued success depends on the retention, recruitment and continued contributions of key management, finance, sale and marketing personnel, some of whom could be difficult to replace. Our success is largely dependent upon our senior management team, led by our Chief Executive Officer and other key managers. The loss of any one or more of such persons could have an adverse effect on our business and financial condition.

Our indebtedness could adversely affect our operations, including our ability to perform our obligations and pay dividends.

As of December 31, 2009, as adjusted to give effect to this offering and the application of the proceeds therefrom (including the redemption of our senior notes), we would have had approximately $122.7 million of senior secured indebtedness and $52 million of available borrowings under our revolving credit facility. We may also be able to incur substantial indebtedness in the future, including senior indebtedness, which may or may not be secured. For example, concurrent with this offering, we intend to increase our existing term loan facility by $40 million. Further, if this offering is completed and all our senior notes are redeemed, our revolving credit facility will mature in May 2012 and our term loan facility will mature in May 2013 with respect to the existing term loans and May 2016 with respect to the additional $40 million of term loans. See "Description of Indebtedness—Senior Credit Facilities."

19

Our indebtedness could have important consequences to you, including the following:

- •

- we could have difficulty satisfying our debt obligations, and if we fail to comply with these requirements, an event of

default could result;

- •

- we may be required to dedicate a substantial portion of our cash flow from operations to required payments on

indebtedness, thereby reducing the cash flow available to pay dividends or fund working capital, capital expenditures and other general corporate activities;

- •

- covenants relating to our indebtedness may restrict our ability to make distributions to our stockholders;

- •

- covenants relating to our indebtedness may limit our ability to obtain additional financing for working capital, capital

expenditures and other general corporate activities, which may limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate;

- •

- we may be more vulnerable to general adverse economic and industry conditions;

- •

- we may be placed at a competitive disadvantage compared to our competitors with less debt; and

- •

- we may have difficulty repaying or refinancing our obligations under our senior credit facilities on their respective maturity dates.