Attached files

| file | filename |

|---|---|

| EX-21 - SUBSIDIARIES OF REGISTRANT - Mesa Energy Holdings, Inc. | v181110_ex21.htm |

| EX-32.1 - S-OX 906 CERTIFICATE OF CHIEF EXECUTIVE OFFICER - Mesa Energy Holdings, Inc. | v181110_ex32-1.htm |

| EX-31.2 - S-OX 302 CERTIFICATE OF PRINCIPAL FINANCIAL OFFICER - Mesa Energy Holdings, Inc. | v181110_ex31-2.htm |

| EX-31.1 - S-OX 302 CERTIFICATE OF PRINCIPAL EXECUTIVE OFFICER - Mesa Energy Holdings, Inc. | v181110_ex31-1.htm |

| EX-32.2 - S-OX 906 CERTIFICATE OF ACTING CHIEF FINANCIAL OFFICER - Mesa Energy Holdings, Inc. | v181110_ex32-2.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

(Mark

One)

| x |

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For the

fiscal year ended: December 31, 2009

or

| o |

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For the

transition period from _______________ to _______________

Commission

file number: 333-149338

|

Mesa

Energy Holdings, Inc.

|

|

(Exact

name of registrant as specified in its

charter)

|

|

Delaware

|

98-0506246

|

|

|

(State

or other jurisdiction of incorporation or organization)

|

(IRS

Employer Identification

No.)

|

|

5220

Spring Valley Road, Suite 525, Dallas, TX

|

75254

|

|

|

(Address

of principal executive offices)

|

(Zip

Code)

|

Registrant’s

telephone number, including area code (972)

490-9595

Securities

registered under Section 12(b) of the Act: None

Securities

registered under Section 12(g) of the Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act.

Yes ¨ No x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or 15(d) of the Exchange Act.

Yes ¨ No x

Indicate by check mark whether the

registrant (1) has filed all reports required to be filed by Section 13 or 15(d)

of the Exchange Act during the preceding 12 months (or for such shorter period

that the registrant was required to file such reports), and (2) has been subject

to such filing requirements for the past 90

days. Yes x No ¨

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding

12 months (or for such shorter period that the registrant was required to submit

and post such files). Yes x No ¨

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant's knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. ¨

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, or a smaller reporting company. See the

definitions of the “large accelerated filer,” “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act.

|

Large

Accelerated Filer ¨

|

Accelerated

Filer ¨

|

|

Non-Accelerated

Filer ¨ (Do not check if a smaller

reporting company)

|

Smaller

reporting company x

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). Yes ¨ No x

On June

30, 2009, the last business day of the registrant’s most recently completed

second fiscal quarter, 14,070,000 shares of its common stock, par

value $0.0001 per share (its only class of voting or non-voting common equity),

were held by non-affiliates of the registrant. The aggregate market

value of such shares was approximately $25,125, based on the price at which the

registrant’s common stock was last sold at such time (i.e. approximately $0.0017857

per share on April 5, 2008). For purposes of making this calculation,

shares beneficially owned at such time by each executive officer and director of

the registrant and by each beneficial owner of greater than 10% of the voting

stock of the registrant have been excluded because such persons may be deemed to

be affiliates of the registrant. This determination of affiliate

status is not necessarily a conclusive determination for other

purposes.

As of

April 12, 2010, there were 40,574,611 shares of the registrant's common stock,

par value $0.0001, issued and outstanding.

DOCUMENTS

INCORPORATED BY REFERENCE

None.

TABLE

OF CONTENTS

|

Item

Number and Caption

|

Page

|

||

|

Forward-Looking Statements

|

3

|

||

|

PART I

|

4

|

||

|

1.

|

Business

|

4

|

|

|

1A.

|

Risk Factors

|

30

|

|

|

1B.

|

Unresolved Staff Comments

|

47

|

|

|

2.

|

Properties

|

48

|

|

|

3.

|

Legal Proceedings

|

48

|

|

|

4.

|

Submission of Matters to a Vote of Security

Holders

|

49

|

|

|

PART II

|

50

|

||

|

5.

|

Market for Registrant’s Common Equity, Related

Stockholder Matters and Issuer Purchases of Equity

Securities

|

50

|

|

|

6.

|

Selected Financial Data

|

52

|

|

|

7.

|

Management’s Discussion and Analysis of Financial

Condition and Results of Operations

|

53

|

|

|

7A.

|

Quantitative and Qualitative Disclosures About

Market Risk

|

64

|

|

|

8.

|

Financial Statements and Supplementary

Data

|

64

|

|

|

9.

|

Changes in and Disagreements with Accountants on

Accounting, and Financial Disclosure

|

64

|

|

|

9A(T)

|

Controls and Procedures

|

64

|

|

|

9B.

|

Other Information

|

67

|

|

|

PART III

|

67

|

||

|

10.

|

Directors, Executive Officers, and Corporate

Governance

|

67

|

|

|

11.

|

Executive Compensation

|

71

|

|

|

12.

|

Security Ownership of Certain Beneficial Owners

and Management and Related Stockholder Matters

|

75

|

|

|

13.

|

Certain Relationships and Related Transactions,

and Director Independence

|

78

|

|

|

14.

|

Principal Accounting Fees and

Services

|

79

|

|

|

PART IV

|

80

|

||

|

15.

|

Exhibits, Financial Statement

Schedules

|

80

|

|

2

FORWARD-LOOKING

STATEMENTS

Various

statements in this Annual Report, including those that express a belief,

expectation or intention, as well as those that are not statements of historical

fact, are “forward-looking statements” within the meaning of the United States

Private Securities Litigation Reform Act of 1995. The forward-looking

statements may include projections and estimates concerning the timing and

success of specific projects, revenues, income and capital spending. We

generally identify forward-looking statements with the words “believe,”

“intend,” “expect,” “seek,” “may,” “should,” “anticipate,” “could,” “estimate,”

“plan,” “predict,” “project” or their negatives, and other similar expressions.

These statements are likely to address our growth strategy, financial results

and exploration and development programs, among other things.

Forward-looking

statements are subject to risks and uncertainties that may change at any time,

and, therefore, our actual results may differ materially from those that we

expected. The forward-looking statements contained in this Annual Report are

largely based on our expectations, which reflect many estimates and assumptions

made by our management. These estimates and assumptions reflect our best

judgment based on currently known market conditions and other factors. Although

we believe such estimates and assumptions are reasonable, we caution that it is

very difficult to predict the impact of known factors and it is impossible for

us to anticipate all factors that could affect our actual results. In addition,

management’s assumptions about future events may prove to be

inaccurate. Management cautions all readers that the forward-looking

statements contained in this Annual Report are not guarantees of future

performance, and we cannot assure any reader that such statements will be

realized or the forward looking events and circumstances will

occur. Actual results may differ materially from those anticipated or

implied in the forward-looking statements due to the factors described in the

“Risk Factors” section and elsewhere in this Annual Report. All

forward-looking statements are based upon information available to us on the

date of this Annual Report. We undertake no obligation to update or revise any

forward-looking statements as a result of new information, future events or

otherwise, except as otherwise required by law.

In this

Annual Report, unless the context requires otherwise, references to the

“Company,” “Mesa,” “we,” “our” and “us,” for periods prior to the closing of our

reverse merger on August 31, 2009, refer to Mesa Energy, Inc., a private Nevada

corporation that is now our wholly owned subsidiary, and such references for

periods subsequent to the closing of our reverse merger on August 31, 2009,

refer to Mesa Energy Holdings, Inc., a publicly traded Delaware corporation

formerly known as Mesquite Mining, Inc., together with its subsidiaries,

including Mesa Energy, Inc.

3

PART

I

ITEM

1. BUSINESS

For

definitions of certain oil and gas industry terms used in this Annual Report on

Form 10-K, please see the Glossary beginning on page 24.

Overview

of Our Business

We are an

exploration stage company engaged primarily in the acquisition, development, and

rehabilitation of oil and gas properties.

Our

business plan is to build a strong, balanced and diversified portfolio of oil

and gas reserves and production revenue through the development of highly

diversified, multi-well developmental and defined-risk exploratory drilling

opportunities and the acquisition of solid, long-term existing production with

enhancement potential.

We are

constantly evaluating opportunities in the United States’ most productive

basins, and we currently have interests in two oil and gas

projects:

|

|

·

|

Java

Field, a natural gas development project in Wyoming County in western New

York; and

|

|

|

·

|

Coal

Creek Prospect, a natural gas developmental prospect in the Arkoma Basin

of eastern Oklahoma.

|

Our

operations have generated minimal revenues to date, with the first such revenues

occurring in the third quarter of fiscal 2009.

Our

principal executive offices are located at 5220 Spring Valley Road, Suite 525,

Dallas, Texas 75254. Our telephone number is (972)

490-9595. Our website address is www.mesaenergy.us.

Recent

Developments

As part

of the execution of our business strategy discussed above, we have recently

taken the following steps:

|

|

·

|

We

raised aggregate gross proceeds of $1,945,000 from the sale of 10% secured

convertible notes in several closings of a private placement offering (the

“2009 Private Placement”) from August 31, 2009 through January 25,

2010;

|

|

|

·

|

On

November 6, 2009, we issued an additional $250,000 principal amount of

convertible promissory notes under the terms of the 2009 Private Placement

to an investor in exchange for our previously outstanding 12% convertible

note in the principal amount of

$250,000;

|

4

|

|

·

|

In

the first quarter of 2010, James J. Cerna, Jr., Fred B. Zaziski and

Kenneth T. Hern joined our Board of Directors, resulting in a majority of

the Board being independent;

|

|

|

·

|

We

have formed an Advisory Board chaired by the former Governor of New York

State, George E. Pataki, to provide subject matter expertise and strategic

guidance to management;

|

|

|

·

|

We

have initiated our efforts to increase production from the existing wells

in the Java Field and have begun the testing of the Marcellus Shale in two

of the existing well bores.

|

|

|

·

|

Our

two completed wells in the Coal Creek Prospect, the Cook #1 and Gipson #1,

have been successfully connected to an Arkansas Oklahoma Gas Company (AOG)

sales line, and initial production and sales have begun from these

wells.

|

History

Mesa

Energy, Inc. (“MEI”) is a company whose predecessor entity, Mesa Energy, LLC,

was formed in April 2003 to engage in the oil and gas industry. MEI’s

primary oil and gas operations have historically been conducted through its

wholly owned subsidiary, Mesa Energy Operating, LLC, a Texas limited liability

company (“Mesa Operating”). Mesa Operating is a qualified operator in the states

of Texas, Oklahoma, and Wyoming. Mesa Energy, Inc. is a qualified

operator in the State of New York. Prior to our reverse merger, all

of our historic field operations had been conducted by Mesa

Operating. However, to avoid duplication of expense, we decided that

Mesa Energy, Inc. should be the operator of the Java Field and related

properties in New York. Our operating entities have historically

employed, and will continue in the future to employ, on an as-needed basis, the

services of drilling contractors, other drilling related vendors, field service

companies and professional petroleum engineers, geologists and landmen as

required in connection with future drilling and future production

operations.

MEI was

originally incorporated as North American Risk Management Incorporated on

January 24, 2001, in the State of Colorado. It was organized to

engage in the business of providing insurance to independent and fleet truck

operators as an affiliate and was in the process of acquiring a truck fleet of

some 125 vehicles. However, operations ceased after approximately six

months.

On March

3, 2006, MEI was the surviving entity in a merger with Mesa Energy, LLC, a Texas

limited liability company, whose activities between April 2003 and March 2006

included participation in various drilling projects, both as operator and as a

non-operator, as well as the acquisition of the Frenchy Springs and Coal Creek

acreage positions (described below). Subsequently, MEI reincorporated

in the State of Nevada by merging with and into Mesa Energy, Inc., a Nevada

corporation, on March 13, 2006.

In July

2008, MEI filed with the SEC a Form 1-A and an Offering Circular in connection

with a proposed “small issue” offering of its common stock, with the intent of

raising up to $5,000,000 in investment capital. However, the effort

was abandoned in early 2009 due to a significant drop in oil and gas prices and

the upheaval in the capital markets that began in late 2008.

5

On August

31, 2009, we closed a reverse merger transaction pursuant to which a wholly

owned subsidiary of Mesa Energy Holdings, Inc. merged with and into MEI, and

MEI, as the surviving corporation, became a wholly owned subsidiary of Mesa

Energy Holdings, Inc.

Immediately

following the closing of the reverse merger, under the terms of a Split-Off

Agreement and a General Release Agreement, we transferred all of our pre-merger

operating assets and liabilities to a wholly owned subsidiary of

ours. Thereafter, pursuant to the Split-Off Agreement, we transferred

all of the outstanding shares of capital stock of such subsidiary to Beverly

Frederick, our pre-reverse merger majority stockholder, in exchange for (i) the

surrender and cancellation of all 21,000,000 shares of our common stock held by

that stockholder and (ii) certain representations, covenants and

indemnities.

After the

reverse merger and the split-off, Mesa Energy Holdings, Inc. succeeded to the

business of MEI as its sole line of business, and all of Mesa Energy Holdings,

Inc.’s then-current officers and directors resigned and were replaced by MEI’s

officers and directors.

The

reverse merger was accounted for as a reverse acquisition and recapitalization

of MEI for financial accounting purposes. Consequently, the assets and

liabilities and the historical operations that are reflected in Mesa Energy

Holdings, Inc.’s financial statements for periods prior to the reverse merger

are those of MEI and have been recorded at the historical cost basis of MEI, and

Mesa Energy Holdings, Inc.’s consolidated financial statements for periods after

completion of the reverse merger include both Mesa Energy Holdings, Inc.’s and

MEI’s assets and liabilities, the historical operations of MEI prior to the

reverse merger and Mesa Energy Holdings, Inc.’s operations from and after the

closing date of the reverse merger.

General

Philosophy

Our

business plan is to build a strong, balanced and diversified portfolio of oil

and gas reserves and production revenue through the development of highly

diversified, multi-well developmental and defined-risk exploratory drilling

opportunities and the acquisition of solid, long-term existing production with

enhancement potential. We believe this approach may enable us to

achieve steady reserve growth, strong earnings, and significant capital

appreciation.

With the

exception of the Coal Creek Project, as discussed below, we intend to operate,

or directly control the operation of, through our wholly-owned subsidiaries or

their designees, all properties that we own or acquire. In our

opinion, the lack of control resulting from leaving operational control in the

hands of third parties substantially increases the risks associated with oil and

gas drilling, development and production.

We

believe that a successful oil and gas development program should

include:

|

|

·

|

Diversification

– variety of location, depth, supporting data, oil vs.

gas;

|

|

|

·

|

Volume

– ownership of and/or participation in a large number of wells;

and

|

6

|

|

·

|

Potential

– the possibility of multiple payback of the initial

investment.

|

We plan

for our portfolio to ultimately consist of a balanced and diversified mix of

multiple asset components that will include existing production plus

developmental and defined-risk exploratory drilling opportunities with special

emphasis on the three keys to success as outlined above. The

developmental drilling program, we believe, should provide a relatively low risk

method of achieving stable, repeatable growth in revenue and

reserves. The existing production acquisition component in our

business plan should provide a strong revenue base resulting in long-term

stability. The exploratory drilling component, although higher risk

than the other two components, provides an opportunity for significant growth

due to higher rates of return on capital (in the form of multiple payback of the

initial investment). We generally look for exploratory projects with

multiple well potential and an estimated payback of at least four times the

amount of capital invested.

Various

Federal and state regulations regarding the discharge of materials into the

environment are applicable to our operations. We maintain strict

compliance with these regulations and endeavor to do all we can to make certain

that the environment is protected in and around our operations. The

cost of environmental control facilities and efforts is included as a line item

in the budget of each operation as appropriate. We anticipate no

extraordinary capital expenditures for environmental control facilities related

to any of our existing operations for the current fiscal year.

Employees

As of

April 12, 2010, we had two full-time employees and three part-time employees,

including our executive officers, as well as two consultants working on a

consistent basis. We believe the relationship we have with our

employees is good. Later in 2010, we anticipate the need for

additional accounting and technical personnel and, although demand for quality

staff is high in the oil and gas industry, we believe we will be able to fill

these positions in a timely manner.

Financial

Statements and “Going Concern” Opinion

The

auditor’s report accompanying our audited financial statements for the years

ended December 31, 2009 and 2008, included in this Annual Report, contained an

explanation that our financial statements were prepared assuming that we will

continue as a going concern. The report cites the generation of

recurring losses from operations and a working capital deficit. Our

ability to continue operating as a going concern will depend on our ability to

derive sufficient funds from sales of equity and/or debt securities and/or

additional loans from officers or our creation of a source of recurring revenue,

to generate operating capital in excess of our required cash expenditures and,

thereafter, to generate sufficient funds to allow us to effectuate our business

plan. We cannot provide any assurance that we will have sufficient

sales or that sufficient financing will be available to us on terms or at times

that we may require. Failure in any of these efforts may materially

and adversely affect our ability to continue our operations.

7

Oil

and Gas Industry Overview

Exploration

and production (“E&P”) companies explore for and develop oil and natural gas

reserves in various basins around the world. The capital spending budgets of

domestic E&P companies have grown in recent years as tight supply conditions

and strong global demand have spurred companies to expand their operations.

According to various industry publications, drilling and completion spending

grew by an estimated 29% from 2002 to 2008. Following a 22% projected decline in

spending from 2008 to 2009, drilling and completion spending is again projected

to grow at a compound annual growth rate of approximately 5% from 2009 to

2014. Much

of this growth is expected to come from a need to compensate for accelerating

depletion rates in existing domestic oil and natural gas reservoirs, improved

E&P technologies and an increase in demand for natural gas, especially from

power generation.

Due to

the unprecedented level of exploration expenditures in recent years, U.S. and

Canadian rig counts increased dramatically between 2002 and

2008. According to a report prepared by Spears & Associates,

Inc., following an approximately 14% and 7% projected decline in U.S. and

Canadian rig counts respectively from 2008 to 2009, U.S. and Canadian rig counts

are again expected to increase at a compound annual growth rate of approximately

3% and 1%, respectively, between 2009 and 2014. Furthermore, more technically

sophisticated drilling methods such as horizontal drilling coupled with higher

oil and natural gas prices relative to long term averages, are making E&P in

previously underdeveloped areas like Appalachia and the Rockies more

economically feasible. As part of this trend, there has been growing commercial

interest in several shale deposit areas in the U.S., including the Bakken,

Barnett, Fayetteville, Haynesville and Marcellus shales.

The

Shale Gas Business

Natural

gas production from hydrocarbon rich shale formations, known as “shale gas,” is

one of the most rapidly expanding trends in onshore domestic oil and gas

exploration and production today. In some areas, this has included bringing

drilling and production to regions of the country that have seen little or no

activity in the past. Natural gas plays a key role in meeting U.S. energy

demands. Natural gas, coal and oil supply about 85% of the nation’s energy, with

natural gas supplying about 22% of the total. The percent contribution of

natural gas to the U.S. energy supply is expected to remain fairly constant for

the next 20 years. The United States has abundant natural gas resources. The

Energy Information Administration estimates that the U.S. has more than 1,744

trillion cubic feet (tcf) of technically recoverable natural gas, including 211

tcf of proved reserves (the discovered, economically recoverable fraction of the

original gas-in-place). Technically recoverable unconventional gas (shale gas,

tight sands, and coalbed methane) accounts for 60% of the onshore recoverable

resource.

Although

forecasts vary in their outlook for future demand for natural gas, they all have

one thing in common: natural gas will continue to play a significant role in the

U.S. energy picture for some time to come. The lower 48 states have a wide

distribution of highly organic shales containing vast resources of natural gas.

Already, the Barnett Shale play in Texas produces 6% of all natural gas produced

in the lower 48 States.

8

Three

factors have come together in recent years to make shale gas production

economically viable: (1) advances in horizontal drilling, (2) advances in

hydraulic fracturing, and (3) rapid increases in natural gas prices in the last

several years as a result of significant supply and demand pressures. Analysts

have estimated that by 2011 most new reserves growth (50% to 60%, or

approximately 3 bcf/day) will come from unconventional shale gas reservoirs. The

total recoverable gas resources in four new shale gas plays (the Haynesville,

Fayetteville, Marcellus, and Woodford) may be over 550 tcf. This potential for

production in the known onshore shale basins, coupled with other unconventional

gas plays, is predicted to contribute significantly to the U.S.’s domestic

energy outlook.

Shale gas

is natural gas produced from shale formations that typically function as both

the reservoir and source for the natural gas. Gas shales are

organic-rich shale formations that were previously regarded only as source rocks

and seals for gas accumulating in the stratigraphically-associated sandstone and

carbonate reservoirs of traditional onshore gas development. Shale is a

sedimentary rock that is predominantly comprised of consolidated clay-sized

particles. Shales are deposited as mud in low-energy depositional environments

such as tidal flats and deep water basins where the fine-grained clay particles

fall out of suspension in these quiet waters. The clay grains tend to lie flat

as the sediments accumulate and subsequently become compacted as a result of

additional sediment deposition. This results in mud with thin laminar bedding

that lithifies (solidifies) into thinly layered shale rock. The very fine

sheet-like clay mineral grains and laminated layers of sediment result in a rock

that has limited horizontal permeability and extremely limited vertical

permeability. This low permeability means that gas trapped in shale

cannot move easily within the rock except over geologic expanses of time

(millions of years).

Shale gas

is stored both as free gas in fractures and as absorbed gas on kerogen and clay

surfaces within the shale matrix.

Oil

and Natural Gas Leases

General.

The

typical oil and natural gas lease agreement provides for the payment of

royalties to the mineral owner for all oil and natural gas produced from any

well(s) drilled on the leased premises. This amount will typically range from

1/8th (12.5%) resulting in a 87.5% net revenue interest to us to 3/16th (18.75%)

resulting in an 81.25% net revenue interest to us, for most leases directly

acquired by us.

Because

the acquisition of leases is a very competitive process, and involves certain

geological and business risks to identify productive areas, prospective leases

are often held by other oil and natural gas companies. In order to gain the

right to drill these leases, we may elect to farm-in leases and/or purchase

leases from other oil and natural gas companies. Many times the assignor of such

leases and/or lease brokers or finders will reserve an overriding royalty

interest (an “ORRI”) which may further reduce the net revenue interest available

to us to between 75% and 80%.

9

Oil and

natural gas leases generally have a primary term of three to five years but

provide that if wells on the property are producing or drilling is underway, the

lease continues and is said to be “held by production” (HBP) for as long as the

production continues.

Participations.

On rare

occasions, the mineral owner may elect to joint venture with us and participate

for his royalty interest in the drilling unit. In this event, our working

interest ownership would be reduced by the amount retained by the third party.

In all other instances, we anticipate owning a 100% working interest in newly

drilled wells.

Commodity

Price Environment

Generally,

the demand for and the price of natural gas increases during the colder winter

months and decreases during the warmer summer months. Pipelines, utilities,

local distribution companies and industrial users utilize natural gas storage

facilities and purchase some of their anticipated winter requirements during the

summer, which can lessen seasonal demand fluctuations. Crude oil and the demand

for heating oil are also impacted by seasonal factors, with generally higher

prices in the winter. Seasonal anomalies, such as mild winters, sometimes lessen

these fluctuations.

Our

results of operations and financial condition are significantly affected by oil

and natural gas commodity prices, which can fluctuate dramatically. Commodity

prices are beyond our control and are difficult to predict. We do not currently

plan to hedge any of our production.

During

the first half of 2008, the prices received industry-wide for domestic

production of oil and natural gas increased significantly, which resulted in

increased demand for the equipment and services required to drill, complete and

operate wells. As a result of this increased demand for oil field services,

shortages developed from 2007 into 2008, leading to an escalation in drilling

rig rates, field service costs, material prices and all costs associated with

drilling, completing and operating wells through the first half of

2008. West Texas Intermediate (“WTI”) crude prices, the standard oil

benchmark for the western hemisphere, tumbled from over one hundred forty

dollars ($140) per barrel in mid 2008 to less than forty dollars ($40) per

barrel in early 2009, before rebounding somewhat to approximately seventy-nine

dollars ($79) at year end 2009. During the same period, the

next-month contract price for natural gas price on NYMEX fell from a high of

over $13 per thousand cubic feet (mcf) to below $3/mcf before rebounding

somewhat to around $5.50/mcf at year end 2009.

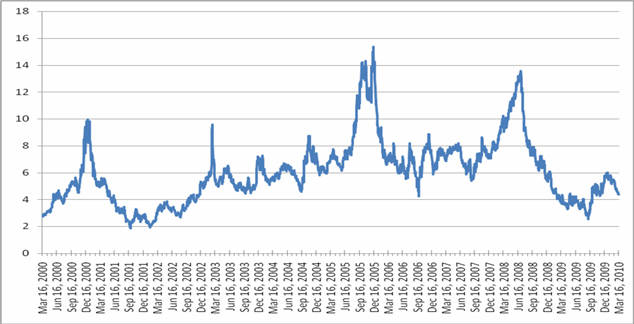

The

following two charts are indicative of oil and natural gas prices in the United

States in recent years:

10

Price

of Crude Oil and Natural Gas

Daily

Spot Prices of West Texas Intermediate (WTI) Crude Oil from March 16, 2000 to

March 16, 2010, US$ per Barrel – source: U.S. Energy Information

Administration.

Daily Next-Month Contract Price for

Natural Gas on NYMEX from March 16, 2000 to March 16, 2010, US$ per thousand

cubic feet – source: U.S. Energy Information

Administration.

11

Java

Field Natural Gas Development Project – Wyoming County, New York

Overview

On August

31, 2009, we acquired the Java Field, a natural gas development project in

Wyoming County in western New York. The acquisition includes a 100%

working interest in 19 leases held by production covering approximately 3,235

mineral acres, 19 existing natural gas wells, two tracts of land totaling

approximately 36 acres and two pipeline systems, including a 12.4 mile pipeline

and gathering system that serves the existing field as well as a separate 2.5

mile system located east of the field. Our average net revenue

interest (NRI) in the leases is approximately 78%. The following map

shows the location of the Java Field.

History

The wells

in the Java Field were originally drilled in the 1970s through the Devonian

Shales to the Medina Sandstone at around 3,000 feet in depth. The

primary intent at that time was to access natural gas production to be used

locally to heat homes, businesses and farms. Many of these wells had

strong gas shows in the Devonian Shale, but the prevailing attitude of the day

was that the shales were not economically viable. The Barnett Shale

of north central Texas was viewed the same way for decades until Mitchell Energy

Company decided in the mid 1990’s to try a new frac technology on one of the

wells they had drilled through the shale. Since then, thousands of

wells have been drilled in the Barnett Shale, and it has become one of the

largest natural gas fields in the United States. It is our belief

that a similar situation may exist in the northern Appalachian basin, and

specifically in the area of the Java Field.

12

Area

Overview

The Java

Field is at the northern end of the Marcellus Shale trend which spans

approximately 600 miles extending from West Virginia to western New

York. In April 2009, the United States Department of Energy estimated

the Marcellus to contain 262 trillion cubic feet of recoverable

gas. Most of the existing activity is farther south in Pennsylvania

and West Virginia. Companies such as Range Resources, Chesapeake

Energy and Atlas Resources hold significant Marcellus acreage positions in

Pennsylvania and West Virginia. They have spent the last few years

leasing acreage and refining their drilling and fracturing techniques and,

according to various industry publications and company news releases, have

recently experienced significant increases in initial production rates from

their Marcellus Shale wells. The Marcellus Shale is deeper in that

area, generally being found at 6,000 to 7,000 feet. However, the

shallower, more northern portion of the play in northern Pennsylvania and

western New York has not yet been extensively explored. The northern

portion of the play is not as deep (resulting in lower drilling costs) and is

close to large domestic markets with extensive pipeline infrastructure already

in place.

13

Marcellus

Shale in the Appalachian Basin

Geologic

Analysis

Currently,

the principal producing zone of the Java Field is the Medina

Sandstone. The Medina Sandstone is a blanket, gas-producing sand at

approximately 3,000 feet that is widely produced in the area. We

believe the Medina has significant potential for expansion using modern

fracturing and/or horizontal technology.

In

addition, there have recently been new wells drilled to the Theresa Sandstone at

approximately 6,000 feet to the southwest of the Java Field, and we believe that

the Theresa fairway may extend southwest to northeast across the southern

portion of the Java Field acreage.

Uphole

from the Medina is the Hamilton Group. Although the primary target is

the Marcellus Shale, which is the deepest member of the Hamilton Group, there

are at least three shale members above the Marcellus, each of which, we believe,

has significant production potential.

14

Reserve

Information

This

presentation of proved reserve quantities provides estimates only and should be

read in connection with Note 11 to our consolidated financial statements –

“Supplemental Information on Oil and Gas Exploration, Development and Production

Activities (Unaudited).” These estimates are consistent with current

knowledge of the characteristics and production history of the

reserves. We emphasize that reserve estimates are inherently

imprecise and that estimates of new discoveries are more imprecise than those of

producing oil and gas properties. Accordingly, significant changes to

these estimates can be expected as future information becomes

available.

Proved

reserves are those estimated reserves of crude oil (including condensate and

natural gas liquids) and natural gas that geological and engineering data

demonstrate with reasonable certainty to be recoverable in future years from

known reservoirs under existing economic and operating

conditions. Proved developed reserves are those expected to be

recovered through existing wells, equipment, and operating methods.

The

reserve estimates set forth below were prepared by Chadwick Energy Consulting,

Inc. (Chadwick), using reserve definitions and pricing requirements prescribed

by the SEC. Chadwick is a professional engineering firm specializing

in the technical and financial evaluation of oil and gas

assets. Chadwick’s report was conducted under the direction of

Jeffrey A. Chadwick, President of Chadwick. At the time of the

report, Chadwick and its employees had no interest in the Company, and were

objective in determining the results of the Company’s

reserves. Chadwick used a combination of production performance,

offset analogies, seismic data and their interpretation, subsurface geologic

data and core data, along with estimated future operating and development costs

as provided by the Company and based upon historical costs adjusted for known

future changes in operations or development plans, to estimate our

reserves. The Company does not operate any of its oil and gas

properties.

We had

total estimated proved developed reserves of 66,821mcf, and no estimated proved

undeveloped reserves, of natural gas at December 31, 2009.

Project

Potential

Operators

in Pennsylvania and West Virginia have had success drilling and completing the

Marcellus Shale using techniques similar to those used in the Barnett

Shale. Although we would not expect the reserves and initial

production rates in the Java Field to be as favorable as the wells being drilled

in Pennsylvania and West Virginia, the drilling and completion costs in our area

should be significantly lower due to the shallower depths, which, we believe,

will result in economics that rival the deeper wells.

We

believe we can potentially drill and complete up to 80 vertical Marcellus Shale

wells on the project acreage at an estimated per well cost of less than $500,000

with very little risk of dry holes. We do not have the capital,

however, to begin drilling these wells at this time and we will need to raise

capital through the sale of our debt or equity to obtain the needed development

funds. There can be no assurance that additional financing will be

available in amounts or on terms acceptable to us, if at all.

15

Many of

the wells drilled in the Marcellus Shale in Pennsylvania and West Virginia are

horizontal, and, at some point, we will probably drill a horizontal well to test

the concept in this field. We believe that a horizontal well at this

depth could be drilled and completed for $1.0 million to $1.2 million and that

it could reasonably be expected to produce at much higher rates than the

vertical wells. However, because Marcellus Shale wells have not yet

been drilled on the property, formal proved reserve reports relating to the Java

Field are not yet possible and there can be no assurance that our expectations

will prove out.

The

current production on the Java Field is being sold to a local manufacturing

plant. However, higher levels of production generated as a result of

field expansion and development would be sold, we expect, not only to the

manufacturing plant but also into a public intrastate transportation line

located approximately 12 miles north of the Java Field. Our Java

Field pipeline system has an existing tap into that line, which leads directly

to the New York City area. Natural gas pricing in the area

historically has averaged above posted NYMEX pricing and has occasionally been

significantly above NYMEX pricing in peak winter months.

We

believe the shale in the Java Field and surrounding area could provide an

excellent opportunity to achieve significant daily production rates at a

relatively low cost. In addition, the project offers the opportunity

to drill a large number of wells in this “blanket” formation, resulting, we

believe, in the potential to book significant reserves and develop a long term,

repeatable drilling program.

Economic

Factors

The Java

Field and the associated pipeline systems were acquired from the seller in a

cash transaction on August 31, 2009. In addition to landowner

royalties, a number of the leases carry additional burdens in the form of

ORRI’s. As a result, the average NRI of the leases prior to closing

was approximately 81%. As a part of the overall consideration to the

seller, the purchase and sale agreement provided that the seller retain a 1%

ORRI on each lease.

We paid

an initial cash finder’s fee for the Java Field of $50,000 to a finder, with the

balance of the finder’s fee to be paid at a rate of $5,000 per month for 12

months. In addition, the agreement with the finder provides that he

receive a 2% ORRI on the existing leases.

As a

result of the above, the overall average NRI to us going forward will be

approximately 78%.

Based on

our internal estimates, we believe that the finding cost of natural gas to be

produced from the Marcellus and associated shales in the Java Field will be

approximately $1/mcf.

Plans

for Development

Two of

the existing wells in the Java Field have never been hooked up to the pipeline

system, and the others have had very little attention in a number of

years. In the fourth quarter of 2009, we initiated efforts to work

over several of the existing wells, replace meters and associated equipment and

set compression in the field which, we expect, should substantially increase

existing production levels.

16

The first

phase of development of the Marcellus Shale was also initiated in the fourth

quarter of 2009. We initially evaluated a number of the existing

wells in order to determine the viability of the re-entry of existing wellbores

for plug-back and re-completion of the wells in the Marcellus

Shale. As a result of this evaluation, we selected the Reisdorf Unit

#1 and the Ludwig #1 as our initial targets. The frac for both wells

has been designed and we are awaiting permits in order to

proceed. Based on the results of these planned re-completions and our

ongoing testing, a second phase of development may be planned to include the

drilling of up to 80 Marcellus Shale wells on our existing acreage as well as on

additional acreage to be leased for future development.

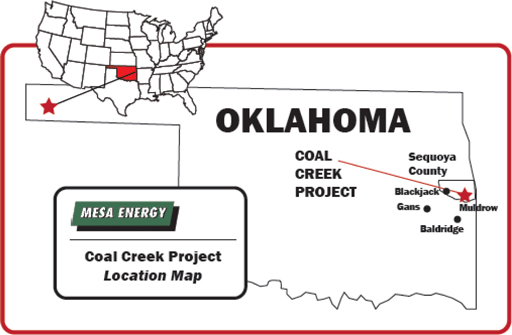

Coal

Creek Prospect – Sequoyah County, Oklahoma

The Coal

Creek Prospect is a developmental prospect targeting the Brent Sand, a shallow

gas reservoir present in the Arkoma Basin of eastern Oklahoma. We

have approximately 677 gross acres under lease near the town of Muldrow,

Oklahoma. The following map shows the location of the Coal Creek

Prospect.

On

December 26, 2007, we closed a “farm-out” transaction with Wentworth Operating

Company of Edmond, OK (“Wentworth”), wherein we sold Wentworth our pipeline

right-of-way and agreed to grant Wentworth an undivided 70% interest in all the

leases following completion by Wentworth of construction of a natural gas

gathering system and approximately three miles of pipeline to connect the Cook

#1 and future wells to an Arkansas Oklahoma Gas Company (AOG) pipeline to the

south. In addition, Wentworth agreed to fund, drill, and complete the

Gipson #1, a direct offset to the Cook #1 and a twin to the Eglinger #1

well.

17

The

Eglinger #1 was drilled in 1944 in search of oil and encountered gas in two

Brent Sand zones between 1,200 and 1,300 feet. It tested 1.5 million

cubic feet per day from these intervals. Due to the lack of pipeline

access and low gas prices, this well was not completed and was later

plugged. Because the Eglinger #1 was drilled so long ago, the

decision was made to drill the Gipson #1 in close proximity as a twin rather

than to attempt to re-enter the old well bore. The Gipson #1 was

recently drilled to a total depth of approximately 3,000 feet to test not only

the Brent Sand but also the Hunton Sand, a gas-bearing sand widely produced in

this area. The well tested over one million cubic feet per day of

gas. The pipeline referenced above was completed, the two wells were

connected and initial production began in the third quarter of

2009.

As a

result of amendments to the farm-out agreement with Wentworth, we now own 35% of

the working interest in the Cook #1 and 25% of the working interest in the

Gipson #1, with Wentworth and other industry partners owning the

balance. We believe there are multiple offset drilling locations and

expect those locations to be drilled in 2010 as part of the overall development

plan for the Coal Creek prospect.

Although

our general philosophy is to operate all of our properties, we have a

long-standing relationship with Wentworth and are comfortable with that company

as the operator of this property. Wentworth has a similar property

that is only a few miles away and, as a result of this arrangement, both

projects will be able to share a pipeline tap and processing facilities

resulting in a significant cost savings to us. We believe other

operational efficiencies will also result from this arrangement.

Economic

Factors

The Coal

Creek leases have various landowner royalties ranging from 12.5% to

18.75%. The acquisition of the Coal Creek leases provides for a 78%

NRI to be delivered to us, with the difference between the landowner royalty and

22% to be retained by Wentworth. In addition, a 1% ORRI is to be

delivered to Cold Water Creek Exploration, LLC, a finder. As a

result, the net NRI to us on all Coal Creek leases, both the original leases and

any new leases taken in the area, is 77%.

Prior

Activities

In the

last three years, we have drilled one exploratory well, the Frenchy Springs

23-22, and one developmental well, the Gipson #1 described above. In

November 2008, we commenced operations to plug and abandon the Frenchy Springs

well as discussed below.

Main Pass

35 Project – Plaquemines Parish, Louisiana; IP #1 Re-completion - Hancock

County, Mississippi

In

January, 2008, we acquired Poydras Energy, LLC, a New Orleans-based Louisiana

operating company, along with the Main Pass 35 Project. The Project

was producing approximately 150 barrels of oil per day prior to being shut down

in advance of Hurricane Katrina. The wells were undamaged but there

was extensive damage to the processing facility. We commenced

rehabilitation of the processing facility in April 2008.

18

In

October 2008 we commenced the re-completion of the IP #1 well in the Ansley

Field in Hancock County, Mississippi. Initial testing indicated fluid

entry of approximately 350 barrels per day with an oil cut of 10% to

12%. Several potential completion scenarios were subsequently

evaluated. At the end of 2008, Mesa sold 25% of the

working interest in the well to its executive officers and a third party in

order to raise cash to assist in the payment of the cost of completion of the

well and expected to retain 75% of the working interest in the

well.

As a

result of multiple factors including delays during the summer of 2008 associated

with Hurricane Gustav and Hurricane Ike, high construction costs and lack of

availability of equipment and personnel after the hurricanes and the subsequent

collapse of oil prices, Poydras Energy, LLC, experienced severe cash flow

constraints and had difficulty in meeting short-term cash commitments,

particularly with its vendors. As a result, we reached an agreement with the

prior owners of Poydras Energy, LLC, wherein as of June 1, 2009, we transferred

our ownership interest in Poydras for no cash consideration to the prior owners

in exchange for the assumption of all liabilities and a release of any

responsibility for the liabilities and contractual obligations of Poydras. We

also agreed to assign the lease for the IP #1 well. As a result, we

are no longer involved in the Main Pass 35 Project or the IP #1

well.

Frenchy

Springs Prospect – Johnson County, Wyoming

An

initial test well, the Mesa Energy #23-22, was drilled by Mesa Energy Operating,

LLC, in August 2006, to a total vertical depth of 4,026 feet. The

deepest zone, the second Wall Creek, showed good potential for both oil and gas,

and an effort to complete the well took place in early January

2007. However, we were unable to establish production in the second

Wall Creek or in one of the up-hole zones. Due to weather issues and

environmental restrictions (no surface disturbing activities between February 1

and July 31 of each year), we deferred further attempts to complete the well

until a later date. Additional geological and engineering testing

took place in May 2008. As a result of those tests and additional

data gathered in November 2008, we elected to plug the well and abandon the

associated lease, which has since expired. Mesa Energy, Inc. owned a

50% working interest in the well.

Planned

Acquisitions and Drilling

Acquisition

and Testing of Low-Risk Drilling Prospects with Significant Expansion

Potential:

In

keeping with our philosophy of balance and diversification, we are currently

evaluating a number of oil and gas drilling prospects with existing production

as well as significant expansion potential. The types of properties we are

interested in are shallow drilling prospects in shale (both oil and gas), tight

gas or coal bed methane reservoirs with significant acreage positions and the

potential to drill hundreds of wells and book extensive reserves. We

believe that these types of reservoirs are relatively low-risk, because they

have hydrocarbons in place, and we expect the likelihood of dry holes to be

relatively small.

Our

short-term strategy called for the acquisition and early stage testing of one of

these prospects in 2009 with a large-scale developmental drilling program to get

underway in 2010. In implementing this strategy, we recently acquired the Java

Field as described above. This property has existing production with enhancement

potential as well as large-scale development potential in the Marcellus

Shale.

19

In

keeping with our philosophy, we intend to acquire and develop multiple

properties of this type, encompassing both oil and natural gas drilling and

production. As an exploration stage public company seeking to rapidly

accumulate reserves and build significant shareholder equity, we believe that

this kind of large-scale, low-risk, developmental drilling may result in stable,

long term growth in revenue, reserve base and shareholder value.

Producing

Properties

In

keeping with our long-term business plan, we are constantly evaluating producing

oil and gas properties generating significant monthly net revenue with

re-completion and offset developmental drilling

potential. Acquisitions of this type could accelerate our growth, add

proved developed reserves to our asset base and provide a strong foundation for

future growth.

There can

be no assurance, however, that any acquisitions of the types described above

will be consummated or, if consummated, will prove productive or

profitable.

Governmental

Regulation

Our

operations are or will be subject to various types of regulation at the federal,

state and local levels. Such regulation includes requiring state (and sometimes

local) permits for the drilling of wells; maintaining bonding or escrow

requirements in order to drill or operate wells; implementing spill prevention

plans; submitting notification and receiving permits relating to the presence,

use and release of certain materials incidental to oil and gas operations; and

regulating the location of wells, the method of drilling and casing wells, the

use, transportation, storage and disposal of fluids and materials used in

connection with drilling and production activities, surface usage and the

restoration of properties upon which wells have been drilled, the plugging and

abandoning of wells and the transporting of production. Our

operations are or will also be subject to various conservation matters,

including the regulation of the size of drilling and spacing units or proration

units, the number of wells which may be drilled in a unit and the unitization or

pooling of oil and gas properties. In this regard, some states allow

the forced pooling or integration of tracts to facilitate exploration while

other states rely on voluntary pooling of lands and leases, which may make it

more difficult to develop oil and gas properties. In addition, state

conservation laws typically establish maximum rates of production from oil and

gas wells, generally limit the venting or flaring of gas, and impose certain

requirements regarding the transportation of production. The effect

of these regulations is to limit the amounts of oil and gas we may be able to

produce from the wells and to limit the number of wells or the locations at

which we may be able to drill.

Our

business is affected by numerous laws and regulations, including energy,

environmental, conservation, tax and other laws and regulations relating to the

oil and gas industry. We plan to develop internal procedures and

policies to ensure that operations are conducted in full and substantial

environmental regulatory compliance.

Our

failure to comply with any laws and regulations may result in the assessment of

administrative, civil and criminal penalties, the imposition of injunctive

relief or both. Moreover, changes in any of these laws and

regulations could have a material adverse effect on our business. In

view of the many uncertainties with respect to current and future laws and

regulations, including their applicability to us, we cannot predict the overall

effect of such laws and regulations on future operations.

20

We

believe that our operations comply in all material respects with applicable laws

and regulations and that the existence and enforcement of such laws and

regulations have an effect no more restrictive on our operations than on other

similar companies in the energy industry. We do not anticipate any

material capital expenditures to comply with federal and state

requirements.

Environmental

Regulation

Our

operations on properties in which we have an interest are subject to extensive

federal, state and local environmental laws that regulate the discharge or

disposal of materials or substances into the environment and otherwise are

intended to protect the environment. Numerous governmental agencies

issue rules and regulations to implement and enforce such laws, which are often

difficult and costly to comply with and which carry substantial administrative,

civil and criminal penalties and in some cases injunctive relief for failure to

comply.

Some

laws, rules and regulations relating to the protection of the environment may,

in certain circumstances, impose “strict liability” for environmental

contamination. These laws render a person or company liable for

environmental and natural resource damages, cleanup costs and, in the case of

oil spills in certain states, consequential damages without regard to negligence

or fault. Other laws, rules and regulations may require the rate of

oil and gas production to be below the economically optimal rate or may even

prohibit exploration or production activities in environmentally sensitive

areas. In addition, state laws often require some form of remedial

action, such as reclamation of inactive pits and plugging of abandoned wells, to

prevent pollution from former or suspended operations.

Legislation

has been proposed in the past and continues to be evaluated in Congress from

time to time that would reclassify certain oil and gas exploration and

production wastes as “hazardous wastes.” This reclassification would

make these wastes subject to much more stringent storage, treatment, disposal

and clean-up requirements, which could have a significant adverse impact on our

operating costs. Initiatives to further regulate the disposal of oil and gas

wastes are also proposed in certain states from time to time and may include

initiatives at the county, municipal and local government

levels. These various initiatives could have a similar adverse impact

on our operating costs.

The

regulatory burden of environmental laws and regulations increases the cost and

risk of doing business and consequently affects profitability. The

federal Comprehensive Environmental Response, Compensation and Liability Act, or

CERCLA, also known as the “Superfund” law, imposes liability, without regard to

fault, on certain classes of persons with respect to the release of a “hazardous

substance” into the environment. These persons include the current or

prior owner or operator of the disposal site or sites where the release occurred

and companies that transported or disposed, or arranged for the transport or

disposal, of the hazardous substances found at the site. Persons who

are or were responsible for releases of hazardous substances under CERCLA may be

subject to joint and several liability for the costs of cleaning up the

hazardous substances that have been released into the environment and for

damages to natural resources, and it is not uncommon for the federal or state

government to pursue such claims.

21

It is

also not uncommon for neighboring landowners and other third parties to file

claims for personal injury or property or natural resource damages allegedly

caused by the hazardous substances released into the

environment. Under CERCLA, certain oil and gas materials and products

are, by definition, excluded from the term “hazardous substances.” At

least two federal courts have held that certain wastes associated with the

production of crude oil may be classified as hazardous substances under

CERCLA. Similarly, under the federal Resource, Conservation and

Recovery Act, or RCRA, which governs the generation, treatment, storage and

disposal of “solid wastes” and “hazardous wastes,” certain oil and gas materials

and wastes are exempt from the definition of “hazardous wastes.” This

exemption continues to be subject to judicial interpretation and increasingly

stringent state interpretation. During the normal course of our

operations on properties in which we have an interest, exempt and non-exempt

wastes, including hazardous wastes, that are subject to RCRA and comparable

state statutes and implementing regulations are generated or have been generated

in the past. The federal Environmental Protection Agency and various

state agencies continue to promulgate regulations that limit the disposal and

permitting options for certain hazardous and non-hazardous wastes.

We have

established guidelines and management systems to ensure compliance with

environmental laws, rules and regulations. The existence of these

controls cannot, however, guarantee total compliance with environmental laws,

rules and regulations. We believe that with respect to the

Properties, we are in substantial compliance with applicable environmental laws,

rules and regulations. We do not currently maintain any insurance

against the risks described above, and there is no assurance that we will be

able to obtain insurance that is adequate to cover all such costs or that

insurance will be available at premium levels that justify

purchase. The occurrence of a significant event not fully insured or

indemnified against could have a material adverse effect on our financial

condition and operations. Compliance with environmental requirements,

including financial assurance requirements and the costs associated with the

cleanup of any spill, could have a material adverse effect on our capital

expenditures, earnings or competitive position. We do believe,

however, that the operators are in substantial compliance with current

applicable environmental laws and regulations. Nevertheless, changes

in environmental laws have the potential to adversely affect our

operations. At this time, we have no plans to make any material

capital expenditures for environmental control facilities.

Competition

The oil

and gas industry is intensely competitive with respect to the acquisition of

prospective oil and natural gas properties and oil and natural gas

reserves. Our ability to effectively compete is dependent on our

geological, geophysical and engineering expertise and our financial

resources. We must compete against a substantial number of major and

independent oil and natural gas companies that have larger technical staffs and

greater financial and operational resources than we do. Many of these

companies not only engage in the acquisition, exploration, development and

production of oil and natural gas reserves, but also have refining operations,

market refined products and generate electricity. We also compete

with other oil and natural gas companies to secure drilling rigs and other

equipment necessary for drilling and completion of wells. Consequently, drilling

equipment may be in short supply from time to time. With the recent

decline in crude oil and natural gas prices, access to drilling equipment is

currently more available.

22

Research

and Development

We have

not spent any amounts on research and development activities during either of

the last two fiscal years.

Plan

of Operation for the Remainder of 2010

Two wells

in our Coal Creek project have been completed and are currently

producing. In addition, fifteen of the wells included in the

acquisition of the Java Field are currently producing at a low rate (the

Reisdorf Unit #1 and the Ludwig #1 have been plugged back in preparation for

testing the Marcellus Shale). See “Item 1. Business—Java Field

Natural Gas Development Project – Wyoming County, New

York—Economics.”

In

addition to our planned development program for the Java Field, and contingent

upon our ability to raise additional capital, we may engage in additional

expenditures over the next 12 months for the acquisition of new land and

drilling rights, the drilling and/or re-completion of additional wells on owned

or acquired acreage as well as the acquisition of existing

production. However, we are not yet ready to move forward on any

additional projects and would require additional financing in order to proceed

with any such project.

If the

testing of the Marcellus Shale in the Java Field is successful, then we

anticipate the drilling of up to 8 developmental wells in 2010 at an aggregate

cost of approximately $4,000,000 and we will likely hire additional

administrative and/or field personnel in the second or third quarter of 2010 to

support that effort.

There can

be no assurance, however, that financing the development of the Java Field or

for one or more future projects will be available to us or, if it is available,

that it will be available on terms acceptable to us and that it will be

sufficient to fund our needs. If we are unable to obtain the financing necessary

to support these expenditures, we may not be able to proceed with our plan of

operation.

Legacy

Business Formation and Split-Off

The

registrant was incorporated in the State of Delaware, as “Mesquite Mining,

Inc.,” on October 23, 2007 to engage in the acquisition and exploration of

mining properties (the “Legacy Business”). In mid 2009, the

registrant’s Board of Directors decided to redirect the registrant’s efforts

towards identifying and pursuing a new business plan and

direction. Amid discussions with Mesa Energy, Inc. regarding a

potential business combination, on June 19, 2009, the registrant changed its

name to Mesa Energy Holdings, Inc.

On August

31, 2009, we closed a reverse merger transaction pursuant to which a wholly

owned subsidiary of Mesa Energy Holdings, Inc. merged with and into Mesa Energy,

Inc., and Mesa Energy, Inc., as the surviving corporation, became a wholly owned

subsidiary of Mesa Energy Holdings, Inc. (the “reverse

merger”).

23

Immediately

following the closing of the reverse merger, under the terms of a Split-Off

Agreement, we transferred all of our pre-merger operating assets and liabilities

to our wholly owned subsidiary, Mesquite Mining Group, Inc. (“Split-Off

Subsidiary”), a Delaware corporation formed on August 13,

2009. Thereafter, pursuant to the Split-Off Agreement, we transferred

all of the outstanding shares of capital stock of Split-Off Subsidiary to

Beverly Frederick, our pre-reverse merger majority stockholder and sole

executive officer and director, in exchange for the surrender and cancellation

of all 21,000,000 shares of our common stock held by that

stockholder.

As of

August 31, 2009, Ms. Frederick is no longer a stockholder, executive officer or

director of the registrant.

In

conjunction with the Split-Off Agreement and effective as of August 31, 2009, we

entered into a General Release Agreement with Split-Off Subsidiary and Ms.

Frederick, whereby Split-Off Subsidiary and Ms. Frederick pledged not to sue us

from any and all claims, actions, obligations, liabilities and the like,

incurred by Split-Off Subsidiary or Ms. Frederick arising from any fact, event,

transaction, action or omission that occurred or failed to occur on or prior to

August 31, 2009 and related to the Legacy Business.

GLOSSARY

OF OIL AND GAS TERMS

The

following are the meanings of some of the oil and gas industry terms that may be

used in this prospectus.

2-D

seismic: (two-dimensional seismic data) Geophysical data that

depicts the subsurface strata in two dimensions. A vertical section of seismic

data consisting of numerous adjacent traces acquired sequentially.

3-D

seismic: A set of numerous closely-spaced seismic lines that provide a

high spatially sampled measure of subsurface reflectivity. Events are placed in

their proper vertical and horizontal positions, providing more accurate

subsurface maps than can be constructed on the basis of more widely spaced 2D

seismic lines. In particular, 3D seismic data provide detailed information about

fault distribution and subsurface structures.

Annular

injection: Injection of water, gas or other substances down the well-bore

between the production casing and tubing for purposes of water disposal or

pressure maintenance.

Arkoma

Basin: A structural feature located in southern Oklahoma and western

Arkansas consisting of Middle Cambrian to Late Mississippian age carbonate,

shale, and sandstone sediments.

Barnett

Shale: A geological formation consisting of sedimentary rocks of

Mississippian age (354–323 million years ago) in north central

Texas.

Basin: A depression of the

earth's surface into which sediments are deposited, usually characterized by

sediment accumulation over a long interval; a broad area of the earth beneath

which layers of rock are inclined, usually from the sides toward the

center.

24

BCF:

Billion cubic feet; BCFD:

Billion cubic feet per day

Block: Subdivision

of an area for the purpose of licensing to a company or companies for

exploration/production rights.

BOPD: Abbreviation

for barrels of oil per day, a common unit of measurement for volume of crude

oil. The volume of a barrel is equivalent to 42 US gallons.

Brent

Sand: A sandstone member of the Pennsylvanian age Atoka Group, a sequence

of marine, silty sandstones and shales generally located in eastern Oklahoma and

western Arkansas.

Cash call:

Request for pro-rata funding of drilling operations per approved

budgets.

Completion: The

installation of permanent equipment for the production of oil or natural gas, or

in the case of a dry hole, the reporting of abandonment to the appropriate

agency.

Compression:

Each gas well has natural wellhead pressure from the formation which varies from

each other well. In order to make the wells flow into a common gas

transmission line at the rate of their individual ability to produce, the

pressure from each well needs to exceed the flowing pressure in the gas

transmission line. To accomplish this, a mechanical engine compresses

the gas from each well into a higher amount of pressure than the pressure in the

transmission line so the well can produce its gas into the gas transmission

line. This is commonly called adding “compression”.

Crude oil:

A general term for unrefined petroleum or liquid petroleum.

Defined-risk:

Projects defined by multiple evaluation techniques in order to estimate

more reasonably the potential for success. These techniques may

include 2-D or 3-D seismic, geo-chemistry, subsurface geology, surface mapping,

data from surrounding wells, and/or satellite imagery.

Developmental

drilling: Drilling that occurs after the initial discovery of

hydrocarbons in a reservoir.

Devonian

Shale: Shale formed from organic mud deposited during the Devonian Period

(416–359 million years ago).

Dry

hole: A well found to be incapable of producing hydrocarbons

in sufficient quantities such that proceeds from the sale of such production

would exceed production expenses and taxes.

E&P: Exploration

and production.

Exploration: The

initial phase in petroleum operations that includes generation of a prospect or

play or both, and drilling of an exploration well. Appraisal,

development and production phases follow successful

exploration.

25

Exploratory

well: A well drilled to find and produce oil and gas reserves

that is not a development well.

Fairway: A

term used in the industry to describe an area believed to contain the most

productive mineral acreage in a play.

Farm-out:

An agreement whereby the owner of a lease (farmor) agrees to assign part

or all of a leasehold interest to a third party (farmee) in return for drilling

of a well or wells and/or the performance of other required

activities. The farmee is said to “farm-in.”

Field: An

area consisting of either a single reservoir or multiple reservoirs, all grouped

on or related to the same individual geological structural feature and/or

stratigraphic condition.

Finding

cost: The total cost to drill, complete and hook up a well divided by the

mcf or barrels of proved reserves.

Formation: An

identifiable layer of rocks named after the geographical location of its first

discovery and dominant rock type.

Fracturing: Hydraulic

fracturing is a method used to create fractures that extend from a borehole into

rock formations, which are typically maintained by a proppant, a material such

as grains of sand, ceramic beads or other material which prevent the fractures

from closing. The method is informally called fracking or

hydro-fracking. The technique of hydraulic fracturing is used to

increase or restore the rate at which fluids, such as oil, gas or water, can be

produced from the desired formation. By creating fractures, the reservoir

surface area exposed to the borehole is increased.

Gas

show: While drilling a well through different rock formations,

gas may appear in the drilling mud which is circulating through the drill pipe,

which indicates the presence of gas in the formation being drilled; drillers

call this a “gas show”.

Hamilton

Group: A bedrock unit in New York, Pennsylvania, Maryland and

West Virginia; the oldest strata of the Devonian gas shale sequence. In the

interior lowlands of New York, the Hamilton Group contains the Marcellus,

Skaneateles, Ludlowville, and Moscow Formations, in ascending order, with the

Tully Limestone above.

Horizontal

well: a well in which the borehole is deviated from vertical

at least 80 degrees so that the borehole penetrates a productive formation in a

manner parallel to the formation. A single horizontal lateral can

effectively drain a reservoir and eliminate the need for several vertical

boreholes.

Hunton

Sand: A Devonian-Silurian age group of interbedded limestone