Attached files

| file | filename |

|---|---|

| EX-31.2 - EXHIBIT 31.2 - MPM TECHNOLOGIES INC | a6251729ex31-2.htm |

| EX-32.1 - EXHIBIT 32.1 - MPM TECHNOLOGIES INC | a6251729ex32-1.htm |

| EX-31.1 - EXHIBIT 31.1 - MPM TECHNOLOGIES INC | a6251729ex31-1.htm |

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

Form 10-K

[X] ANNUAL REPORT UNDER SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2009

Commission File Number 0-14910

MPM TECHNOLOGIES, INC.

(Exact Name of Registrant as specified in its Charter)

| WASHINGTON | 81-0436060 |

| (State or other jurisdiction of | (I.R.S. Employer Identification Number) |

| incorporation or organization) |

199 POMEROY ROAD, PARSIPPANY, NEW JERSEY 07054

(Address of principal executive offices)

Registrant’s telephone number, including area code: 973-428-5009

SECURITIES REGISTERED UNDER SECTION 12(B) OF THE EXCHANGE ACT: None

SECURITIES REGISTERED UNDER SECTION 12(g) OF THE EXCHANGE ACT: None

COMMON STOCK, PAR VALUE OF $0.001

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. __Yes _X_ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. __Yes _X No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. X Yes __ No

Indicate by check mark whether the registrant has submitted electronically and posted on it corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ___Yes ___No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule12b-2 of the Exchange Act. (Check one.)

Large accelerated filer __ Accelerated filer __

Non-accelerated filer __ Smaller reporting company X

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). __Yes X No

The aggregate market value of the voting and non-voting equity held by non-affiliates computed by reference to the closing price of $0.90 at which the common equity was sold as of April 9, 2010 was $6,037,016.

The number of shares outstanding of the registrant’s common stock as of April 9, 2010 was 6,707,796.

PART I

Item 1. Business

Incorporated in 1983, MPM Technologies, Inc. (“MPM” or “the Company”) as of year ended December 31, 2009, had three wholly owned subsidiaries: AirPol, Inc. (“AirPol”), NuPower, Inc. (“NuPower”) and MPM Mining Inc. (“Mining”). For the year ended December 31, 2009, AirPol was the only revenue generating entity.

AirPol operates in the air pollution control industry. It sells air pollution control systems to Fortune 500 and other large industrial companies in the U.S and worldwide.

The Company, through its wholly-owned subsidiary, NuPower, Inc., is engaged in the development and commercialization of a waste-to-energy process known as Skygas™. These efforts are largely through NuPower’s participation in NuPower Partnership in which MPM has a 58.21% partnership interest. NuPower Partnership owns 85% of the Skygas Venture. In addition to its partnership interest through NuPower Inc, MPM also owns 15% of the Venture.

Mining operations were discontinued several years ago. Due to the extremely high precious metals prices, MPM management is planning to restart the mining operations. The Company may either restart mining operations using its own resources and personnel or partner with a joint-venture partner. Accordingly, management is actively seeking a joint-venture partner with the necessary financial abilities to further explore and develop the properties. There can be no guarantee that management will be successful in its initiatives.

AIRPOL, INC.

Effective July 1, 1998, the Company acquired certain of the assets and assumed certain of the liabilities of part of a division of FLS miljo, Inc. The agreement called for the Company to pay $300,000 stock and $234,610 in cash. The transaction was accounted for as a purchase.

AirPol designs, engineers, supplies and services air pollution control systems for Fortune 500 and other environmental and industrial companies.

The technologies of AirPol utilize wet and dry scrubbers, wet electrostatic precipitators and venturi absorbers to control air pollution. AirPol brings over 30 years experience through its technologies and employees.

A typical air pollution control system consists of the following components:

|

|

1.

|

A gas duct from the polluting process equipment that can be a boiler, kiln, incinerator or dry;

|

1

|

|

2.

|

A scrubber, or a wet electrostatic precipitator for dust removal purposes;

|

|

|

3.

|

An acid gas absorber for the removal of acid gas from the flue gas;

|

|

|

4.

|

An induced draft fan to provide suction to draw the flue gas through the air pollution control system; and

|

|

|

5.

|

A stack for the discharge of cleaned flue gas into the atmosphere.

|

In building the systems, AirPol personnel conduct engineering design work, and produce design drawings for the fabrication of steel or plastic vessels, steel supports and access facilities. AirPol personnel also prepare equipment specifications for needed equipment such as spray nozzles, pumps, fans, instrumentation and controls. AirPol personnel then retain a fabricator for the fabrication of the system’s components. AirPol personnel arrange for delivery of these to the customer’s location. Normally, AirPol is not responsible for the installation of the systems. In this case, AirPol personnel will arrange for an erection supervisor to make sure the installation meets AirPol quality standards. If AirPol is responsible for the installation, they will hire mechanical and electrical contractors to perform the installation.

NUPOWER, INC.

The Company holds a 58.21% interest in NuPower Partnership through its ownership of NuPower, Inc. No other operations were conducted through NuPower. NuPower Partnership is engaged in the development and commercialization of a waste-to-energy process. This is an innovative technology for the disposal and gasification of carbonaceous wastes such as municipal solid waste, municipal sewage sludge, pulp and paper mill sludge, auto fluff, medical waste and used tires. The process converts solid and semi-solid wastes into a clean-burning medium BTU gas that can be used for steam production for electric power generation. The gas may also be a useful building block for downstream conversion into valuable chemicals. NuPower Partnership owns 85% of the Skygas Venture. In addition to its partnership interest, MPM owns 15% of the Venture.

The United States patent on the Skygas process expired in November 2008. The Company filed a one year provisional new patent for a significantly improved Skygas process in February 2009. In February 2010, a renewal provisional patent application was filed. There can be no guarantee that the new patent will be approved at this time. There was also a Canadian patent on the Skygas process that expired in April 2009.

Due to the expiration of the patents related to the original Skygas technology, the related agreements with the NuPower partnership have also expired. Management expects that the NuPower Partnership will be terminated, or changed if new agreements can be negotiated that recognize the updated technologies. There can be no assurance that new agreements will be achieved.

In 2008 a new company was incorporated named Skygas Energy Ontario Limited (“SEOL”). NuPower, Inc. owns all 100 of the issued and outstanding shares of the new company. Negotiations with unrelated third parties with regard to this venture were terminated when agreements could not be reached with the unrelated third parties. No other activities have been transacted within SEOL.

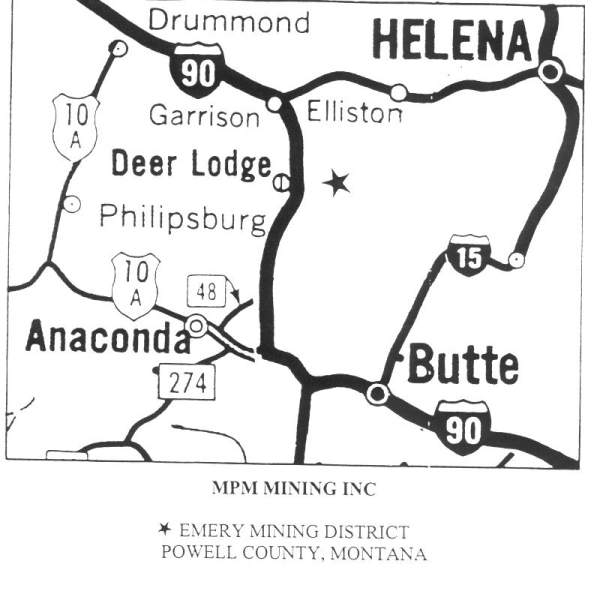

MPM MINING, INC.

The company owns 7.5 patented claims and 2 unpatented claims and leases 7 patented claims with options to purchase on approximately 300 acres in Montana’s historical Emery Mining District. It also owns a 200-ton per day onsite floatation mill. Companies such as Exxon Mobil Corporation, Freeport McMoran Gold Company and Hecla Mining Company in addition to MPM Mining have conducted extensive exploration in the area.

MPM management believes that resuming mining operations is a way to generate positive cash flows and mitigate the continuing losses from other operations given the current market prices and conditions for precious metals. Accordingly, management will investigate its needs to make this happen.

2

Following several geologist reports, assays and recommendations, the company built a 200 ton per day ball mill using floatation tanks to process screened and crushed ore. It took two years to build, equip and test the mill at a cost of approximately $800,000. The mill is in operable condition with all equipment in good repair.

The company has Rake classifier ship, Wilfley Concentrate table, Marcy ball mill 5’x4’, flotation machines and equipment, Denver water pumps, 3 deck concentrate table, Hardinge ball mill and Elmco filter press. There is an office trailer and living quarters for personnel including a deep well and septic system. There are two storage ponds and a creek running through the property.

MPM has spent over $1.3 million on exploration and drilling programs including work done by Exxon, Freeport McMoran, and most recently Hecla Mining Company. Hecla’s drilling results were extremely encouraging in that some drill holes confirmed the possibility of open pit mining and that certain mineral deposits might be enlarged and improved in grade by further drilling. Additionally, there is considerable evidence of significant mineralized materials awaiting drilling programs.

The company has utilized reverse circulation and diamond core drilling techniques in five different programs the total of which are 182 drilled holes averaging 90’ in depth. Additionally, 15 trenches 18’ deep and 6’ wide were dug. All were assayed with all showing mineralization. There have been 5 exploration programs to date:

MPM Mining 6 drill holes 1983-84.

MPM Mining 13 drill holes and 15 trenches 1986

Freeport McMoran Gold Co. 78 drill holes 1988-89

Pegasus Gold Corp 3 drill holes 1990

Hecla Mining Co. 82 drill holes 1991-92

MPM MINING INC

EMERY DISTRICT MINERALIZED MATERIAL

|

Tons

|

Ounces Per Ton

|

|||||||||||

|

Location

|

|

Gold

|

Silver | |||||||||

|

Emery Mine

|

57,941 | 0.372 | 15.39 | |||||||||

|

Emery Stockpiles

|

38,859 | 0.120 | 4.28 | |||||||||

|

Bonanza

|

218,579 | 0.132 | 2.06 | |||||||||

|

Hidden Hand

|

208,619 | 0.123 | -- | |||||||||

The properties are in mineralized zones containing gold, silver, lead and zinc. Located on the properties are former mine shafts, tunnels, mineral stockpiles and stopes (in tunnels) with valuable low-grade mineralization. All areas have been trenched, core drilled and assayed to prove mineralization. The properties contain both underground and near surface minerals. Additionally there are 8 stockpiles with good assayed results of mineralization. The old time miners were after high-grade ore and not interested in lower grade mineral surrounding the vein. The mineral taken from shafts, tunnels and around the high-grade vein was transported to these stockpiles.

The total cost of purchasing the properties, leasing properties, building and equipping the ball mill, infrastructures and bringing power line to replace generators is estimated at $4,000,000. Current expenses that include lease payments and taxes are under $10,000 per year. In the past, power was supplied by two large capacity generators. At a time the mill is reopened, power lines will be brought in from Deer Lodge, Montana at an estimated cost of $200,000. A deep well and Sterret Creek supplies all water needs.

MPM management believes that resuming mining operations is a way to generate positive cash flows and mitigate the continuing losses from other operations given the current market prices and conditions for precious metals. Accordingly, management is in the process of obtaining the necessary financing to restart mining operations. There can be no guarantee that management will be successful in its efforts.

3

FACTORS MANAGEMENT USED TO IDENTIFY REPORTABLE SEGMENTS

Management considers MPM’s reportable segments to be business units that offer different products. The business segments may be reportable because they are each managed separately, or they design and engineer distinct products with different applications in the air pollution control field. Airpol operates in the air pollution control field. MPM’s other segments are essentially non-operational at the present time, and, accordingly have been aggregated for reporting purposes. Accordingly, for the years ended December 31, 2009 and 2008, the Company operated in one segment, and there is no separate segment reporting required.

BACKLOG

MPM had a backlog of orders or work in progress at AirPol of approximately $146,000 at December 31, 2009. It is expected that this backlog will be consumed during the first two quarters of 2010. There is currently no other backlog of orders for any of MPM’s other businesses.

WASTE-TO-ENERGY

MPM’s waste-to-energy process consists of an innovative technology known as “Skygas”. The process is used in the disposal and gasification of various forms of non-metallic wastes. MPM continues to negotiate with interested entities for the manufacture and operation of Skygas units. These negotiations are ongoing, and MPM management is hopeful that there will be formal agreements in place during 2010.

COMPETITIVE CONDITIONS

AirPol operates in extremely competitive environments. There are a number of potential competitors for every job the companies bid on. The number of bidders ranges from two or three to as many as seven or eight depending on the potential customer and the work to be performed. The parts and service side of the business tends to be somewhat less competitive since the parts and service work are generally for units that have previously been sold and/or installed by the companies.

There are a significant number of persons and companies developing or have developed any number of waste-to-energy systems. Management of MPM believes that its development of Skygas™ as a non-polluting and energy efficient system will give it the necessary competitive edge in this area.

Due to the large number of persons and companies engaged in exploration for and production of mineralized material, there is a great degree of competition in the mining part of the business.

SEASONAL VARIATIONS

The impact of seasonal changes is minimal on the air pollution control business of AirPol. There may be some limitations on the installation of the air pollution control units when the weather is more severe in the winter months in those areas of the world where the weather is significantly colder in that season. There have been, however, no discernible variations to date to indicate that the business is subject to seasonal variations.

4

There are currently no seasonal influences on the ongoing development of the Skygas™ process. It is also not expected that there will be any seasonal variations when the Skygas™ units are produced.

EMPLOYEES

At December 31, 2009, MPM had three employees and there were two employees at AirPol. MPM believes that its relations with its employees are good.

Item 2. Properties

AirPol leases its office space under a lease that expires in July of 2010. MPM has no property related to its waste-to-energy operations. MPM believes that its existing facilities are adequate for the current level of operations.

The MPM Mining property is located in the Emery Mining District of Powell County, Montana approximately seven miles northeast of Deer Lodge, Montana. A road maintained by the county runs though or nearby company properties, mill and infrastructures. All titles to the company’s properties are secured. All leased claims are up to date and paid in full.

The company owns 7.5 patented claims, 2 unpatented claims and leases 7 patented claims. Each leased claim contains an option to purchase. The properties are in mineralized zones containing gold, silver, lead and zinc. Located on the properties are former mine shafts, tunnels, mineral stockpiles and stopes (in tunnels) with valuable low-grade mineralization. All areas have been trenched, core drilled and assayed to prove mineralization.

These claims amount to approximately 300 acres of land in the Emery Mining District, Powell County Montana. MPM controls eighteen former mine sites that have been inactive since 1930. Each of these has old adits, tunnels and mineral stockpiles of known mineralized material. All testing and metallurgical work has been completed.

5

Item 3. Legal Proceedings

None

Item 4. Submission of Matters to a Vote of Security Holders

There were no matters submitted to a vote of the shareholders during the fourth quarter of 2009.

PART II

Item 5. Market for the Registrant’s Common Equity and Related Stockholder Matters

a) Market Information

On February 18, 2003 MPM common stock began trading on the OTC Bulletin Board under the trading symbol MPML. The following table shows quarterly high and low bid prices for 2009 and 2008 as reported by the National Quotations Bureau Incorporated. These prices reflect interdealer quotations without adjustments for retail markup, markdown or commission and do not necessarily represent actual transactions.

6

|

High Bid

|

Low Bid

|

|||||||

|

2009

|

||||||||

|

First Quarter

|

$ | 0.42 | $ | 0.20 | ||||

|

Second Quarter

|

0.25 | 0.10 | ||||||

|

Third Quarter

|

0.16 | 0.10 | ||||||

|

Fourth Quarter

|

1.00 | 0.11 | ||||||

|

2008

|

||||||||

|

First Quarter

|

$ | 0.51 | $ | 0.25 | ||||

|

Second Quarter

|

0.95 | 0.10 | ||||||

|

Third Quarter

|

1.01 | 0.40 | ||||||

|

Fourth Quarter

|

0.80 | 0.25 | ||||||

b) Holders

As of April 11, 2010, there were approximately 1,500 holders of record of the Registrant’s common stock.

c) Dividends

MPM has not paid dividends in the past. It is not anticipated that MPM will distribute dividends for the foreseeable future. Earnings of MPM are expected to be retained to enhance its capital and expand its operations.

d) Recent Sales of Unregistered Securities

None

Item 6. Selected Financial Data

|

Selected Financial Data (Unaudited)

|

||||||||||||||||||||

|

2009

|

2008

|

2007

|

2006

|

2005

|

||||||||||||||||

|

Statement of Operations Data

|

||||||||||||||||||||

|

Revenue

|

$ | 558,444 | $ | 567,343 | $ | 2,715,205 | $ | 1,729,257 | $ | 1,959,353 | ||||||||||

|

Gross margin

|

$ | 271,372 | $ | 318,201 | $ | 829,038 | $ | 673,489 | $ | 787,852 | ||||||||||

|

Operating loss

|

$ | (870,017 | ) | $ | (941,871 | ) | $ | (804,341 | ) | $ | (417,034 | ) | $ | (299,161 | ) | |||||

|

Net income (loss)

|

$ | (1,563,759 | ) | $ | (1,717,511 | ) | $ | (2,301,682 | ) | $ | (1,092,896 | ) | $ | 1,898,498 | ) | |||||

|

Net income (loss) per share basic

|

$ | (0.24 | ) | $ | (0.27 | ) | $ | (0.37 | ) | $ | (0.33 | ) | $ | 0.60 | ||||||

|

Net income (loss) per share diluted

|

$ | (0.24 | ) | $ | (0.27 | ) | $ | (0.37 | ) | $ | (0.33 | ) | $ | 0.40 | ||||||

|

Weighted average shares outstanding - basic

|

6,513,415 | 6,257,025 | 6,263,064 | 3,318,078 | 3,183,064 | |||||||||||||||

|

Weighted average shares outstanding - diluted

|

6,513,415 | 6,257,025 | 6,263,064 | 3,318,078 | 5,067,599 | |||||||||||||||

|

Balance Sheet Data

|

||||||||||||||||||||

|

Total assets

|

$ | 1,224,484 | $ | 1,293,397 | $ | 1,255,550 | $ | 2,082,397 | $ | 1,739,992 | ||||||||||

|

Total liabilities

|

$ | 14,468,674 | $ | 13,470,305 | $ | 11,726,059 | $ | 9,881,008 | $ | 9,215,707 | ||||||||||

|

Stockholders' impairment

|

$ | (13,244,190 | ) | $ | (12,176,908 | ) | $ | (10,470,509 | ) | $ | (7,798,611 | ) | $ | (7,475,715 | ) | |||||

|

Other Information

|

||||||||||||||||||||

|

Net cash provided by (used in) operating activities

|

$ | (230,258 | ) | $ | (545,190 | ) | $ | (1,660,781 | ) | $ | 134,828 | $ | (311,483 | ) | ||||||

|

Working capital deficit

|

$ | (14,453,054 | ) | $ | (13,388,664 | ) | $ | (11,630,782 | ) | $ | (5,889,394 | ) | $ | (5,822,003 | ) | |||||

|

Return on average stockholders' impairment

|

-12.3 | % | -15.2 | % | -24.7 | % | -14.3 | % | 22.5 | % | ||||||||||

|

Stock price at year end

|

$ | 1.00 | $ | 0.25 | $ | 0.30 | $ | 0.50 | $ | 0.22 | ||||||||||

|

Number of employees

|

5 | 5 | 7 | 7 | 8 | |||||||||||||||

|

Number of stockholders

|

1,500 | 1,500 | 1,600 | 1,800 | 1,800 | |||||||||||||||

7

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

In addition to reading this section, you should read the consolidated financial statements that begin on page F-1. That section contains all detailed financial information including our results of operations.

a) Results of Operations

MPM acquired certain of the assets and assumed certain of the liabilities of a part of a division of FLS miljo, Inc. as of July 1, 1998. MPM formed AirPol to run this air pollution control business. The results of operations for the years ended December 31, 2009 and 2008 include the operations of AirPol.

For the year ended December 31, 2009, MPM had consolidated revenues of $558,444. Consolidated revenues for 2008 were $567,343. MPM had a net loss for the year 2009 of $1,563,759, or $0.24 per share. MPM’s net loss for 2008 was $1,717,511, or $0.27 per share. Revenues were again hurt by the lack of enforcement of clean air laws. Air pollution control companies depend heavily on the enforcement of clean air laws.

MPM’s management continues to work to bring the Company to profitability. Other businesses are being evaluated to consider moving the Company’s business toward other more profitable ventures. There have been significant consolidations in the air pollution control industry in the past few years. MPM management’s short- term goal is to operate a lean, profitable company.

2009 COMPARED TO 2008

Revenues decreased $8,899 (or 2%) from $567,343 in 2008 to $558,444 in 2009. This included an increase in project revenues of $103,872, while revenues from parts and service decreased by $112,771. The increase in project revenues was due primarily to there being virtually no projects for the 2008 year. A small project was completed at the beginning of the year 2008, and another small project was started in December 2008. A larger project was started in the fourth quarter 2009. The net loss for 2009 was $1,563,759 or $0.24 per share compared to $1,717,511 or $0.27 per share in 2008.

Selling, general and administrative expenses decreased $118,683 from $1,260,072 in 2008 to $1,141,389 in 2009. This decrease is due primarily to a net increase in payroll and related costs for stock-based compensation for option award modifications net of other salary and benefits, decrease of $74,000, and legal, consulting and licensing fees decrease of approximately $192,000.

The net loss in 2009 includes interest expense of $882,953 as compared to $775,210 in 2008. This is a result of increased borrowings and limited debt repayments. In 2009, the Company realized $189,000 of income from the expiration of patent obligations that were accrued per various patent arrangements which expired in 2009.

LIQUIDITY AND CAPITAL RESOURCES

During 2009, funds for operations were provided primarily by loans from an officer/director. Current cash reserves and continuing operations of AirPol are not believed to be adequate to fund MPM and its subsidiaries’ operations for the foreseeable future. MPM management is considering alternative sources of capital such as private placements, other stock offerings and loans from shareholders and officers to fund its current business and expand in other related areas through more acquisitions.

8

Following is a summary from MPM’s consolidated statements of cash flows:

|

Year ended

December 31

|

||||||||

|

2009

|

2008

|

|||||||

|

Net cash used in operating activities

|

$ | (230,258 | ) | $ | (545,190 | ) | ||

|

Net cash used in investing activities

|

$ | - | $ | (54,375 | ) | |||

|

Net cash provided by financing activities

|

$ | 221,400 | $ | 568,612 | ||||

|

Net decrease in cash and cash equivalents

|

$ | ( 8,858 | ) | $ | (30,953 | ) | ||

Net cash used in operating activities in 2009 and 2008 was due to the net losses of the Company.

The net cash provided by financing activities in 2009 of $221,400 was due to loans from related parties, net of repayments. The net cash provided by financing activities in 2008 of $568,612 was due to loans from related parties.

The Company has a working capital deficiency of $14,453,054 at December 31, 2009. Current liabilities include $8,058,656 of related party debt which management believes can be deferred beyond twelve months. Also included in current liabilities is $5,749,777 of a note payable which management is currently renegotiating. Management is optimistic that the lender will agree to terms that will extend the payment and allow the Company to meet its obligations and continue business for the next twelve months. There is no guarantee of the outcome of these plans.

MPM may need to raise additional capital in the future to expand its business and develop mineral properties. MPM cannot be certain that additional financing will be available when and to the extent required or that, if available, it will be on acceptable terms. If adequate funds are not available on acceptable terms, MPM may not be able to fund its operations, develop or enhance its products or services or respond to competitive pressures.

APPLICATION OF CRITICAL ACCOUNTING POLICIES

In preparing our financial statements we are required to formulate working policies regarding valuation of our assets and liabilities and to develop estimates of those values. In our preparation of the financial statements for 2008, there were at least two estimates made which were (a) subject to a high degree of uncertainty and (b) material to our results. These estimates were our determination, detailed in the footnotes to the financial statements on our Mineral Properties and Income Taxes, and our valuation allowances, if any, on them. We have not reserved our mineral properties but we have recorded a valuation allowance for the full value of the deferred tax asset created by our net operating loss carry forward. The primary reason for our determination of our mineral properties is our knowledge of increasing market prices for precious metals, our expectation that such precious metals are contained within these properties, and our current cost and carrying value of the properties are less than the undiscounted cash flows expected to result from the use and eventual disposition of the properties. We have reserved an allowance against our deferred tax assets from our net operating loss carryforwards due to the lack of certainty as to whether MPM will carry on profitable operations in the future in order to utilize such tax benefits before they expire.

We made no material changes to our critical accounting policies in connection with the preparation of financial statements for 2009.

9

OFF-BALANCE SHEET ARRANGEMENTS

We do not have any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition or results of operations.

IMPACT OF RECENTLY ISSUED ACCOUNTING STANDARDS

Effective July 1, 2009, the Company adopted the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 105-10, Generally Accepted Accounting Principles — Overall (“ASC 105-10”). ASC 105-10 establishes the FASB Accounting Standards Codification (the “Codification”) as the source of authoritative accounting principles recognized by the FASB to be applied by nongovernmental entities in the preparation of financial statements in conformity with U.S. GAAP. Rules and interpretive releases of the SEC under authority of federal securities laws are also sources of authoritative U.S. GAAP for SEC registrants. All guidance contained in the Codification carries an equal level of authority. The Codification superseded all existing non-SEC accounting and reporting standards. All other non-grandfathered, non-SEC accounting literature not included in the Codification is non-authoritative. The FASB will not issue new standards in the form of Statements, FASB Staff Positions or Emerging Issues Task Force Abstracts. Instead, it will issue Accounting Standards Updates (“ASUs”). The FASB will not consider ASUs as authoritative in their own right. ASUs will serve only to update the Codification, provide background information about the guidance and provide the bases for conclusions on the change(s) in the Codification. References made to FASB guidance throughout this document have been updated for the Codification.

Effective January 1, 2008, the Company adopted FASB ASC 820-10, Fair Value Measurements and Disclosures — Overall (“ASC 820-10”) with respect to its financial assets and liabilities. In February 2008, the FASB issued updated guidance related to fair value measurements, which is included in the Codification in ASC 820-10-55, Fair Value Measurements and Disclosures — Overall — Implementation Guidance and Illustrations. The updated guidance provided a one year deferral of the effective date of ASC 820-10 for non-financial assets and non-financial liabilities, except those that are recognized or disclosed in the financial statements at fair value at least annually. Therefore, the Company adopted the provisions of ASC 820-10 for non-financial assets and non-financial liabilities effective January 1, 2009, and such adoption did not have a material impact on the Company’s results of operations or financial condition.

IMPACT OF INFLATION

Although inflation has been low in recent years, it is still a factor in our economy and MPM continually seeks ways to mitigate its impact. To the extent permitted by competition, AirPol passes increased costs on to its customers by increasing prices over time. Management estimates that the impact of inflation on the revenues for 2009 was negligible.

Since MPM did not engage in any mining operations, sales of metals or metal bearing ores, and was in the development stage of the waste-to-energy process, inflation did not materially impact the financial performance of those segments of the MPM’s business. Management estimates that the operations of MPM were only nominally impacted by inflation.

SAFE HARBOR STATEMENT UNDER THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

Forward-looking statements in this report, including without limitation, statements relating to MPM’s plans, strategies, objectives, expectations, intentions and adequacy of resources, are made pursuant to the safe harbor provisions of the Private Securities Reform Act of 1995. Investors are cautioned that such forward-looking statements involve risks and uncertainties including without limitation the following: (i) MPM’s loans, strategies, objectives, expectations and intentions are subject to change at any time at the discretion of MPM’s management; (ii) MPM’s plans and results of operations will be affected by its ability to manage its growth and (iii) other risks and uncertainties indicated from time to time in MPM’s filings with the Securities and Exchange Commission.

10

Item 8. Financial Statements

The financial statements follow on the next page.

11

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2009 AND 2008

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

|

Report of Independent Registered Public Accounting Firm

|

F-2

|

|

Consolidated Balance Sheets as of December 31, 2009 and 2008

|

F-3

|

|

Consolidated Statements of Operations for the years ended December 31, 2009 and 2008

|

F-4

|

|

Consolidated Statement of Stockholders’ Equity for the years ended December 31, 2009 and 2008

|

F-5

|

|

Consolidated Statements of Cash Flows for the years ended December 31, 2009 and 2008

|

F-6

|

|

Notes to Consolidated Financial Statements

|

F-7 to F-17

|

Report of the Independent Registered Public Accounting Firm

To the Board of Directors and Stockholders of

MPM Technologies, Inc. and Subsidiaries

We have audited the accompanying consolidated balance sheets of MPM Technologies, Inc. and Subsidiaries as of December 31, 2009 and 2008 and the related consolidated statements of operations, stockholders’ equity (impairment) and cash flows for each of the two years in the two-year period ended December 31, 2009. MPM Technologies, Inc. and Subsidiaries’ management is responsible for these financial statements. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. The company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the consolidated financial position of MPM Technologies, Inc. and Subsidiaries as of December 31, 2009 and 2008, and the consolidated results of its operations and cash flows for each of the two years in the two-year period ended December 31, 2009 in conformity with accounting principles generally accepted in the United States of America.

The accompanying consolidated financial statements have been prepared assuming the Company will continue as a going concern. As discussed in the notes to the Consolidated Financial Statements, the Company has not been able to generate any significant revenues and has a working capital deficiency of $14,453,054 at December 31, 2009. These conditions raise substantial doubt about the Company’s ability to continue as a going concern without the raising of additional debt and/or equity financing to fund operations. Management’s plans in regard to these matters are described in the notes to the Consolidated Financial Statements. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/ Rosenberg Rich Baker Berman & Company

Somerset, New Jersey

April 15, 2010

F-2

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

|

ASSETS

|

|

|||||||

|

December 31,

|

||||||||

|

2009

|

2008

|

|||||||

|

Current assets:

|

||||||||

|

Cash and cash equivalents

|

$ | 7,432 | $ | 16,290 | ||||

|

Accounts receivable, net of allowance for doubtful

|

||||||||

|

accounts of $-0-

|

8,188 | 57,101 | ||||||

|

Other current assets

|

- | 8,250 | ||||||

|

Total current assets

|

15,620 | 81,641 | ||||||

|

Property, plant and equipment, net (note 4)

|

2,121 | 5,013 | ||||||

|

Mineral properties held for sale (note 11)

|

1,070,368 | 1,070,368 | ||||||

|

Other assets, net (note 15)

|

136,375 | 136,375 | ||||||

| 1,224,484 | 1,293,397 | |||||||

|

LIABILITIES AND STOCKHOLDERS' EQUITY

|

||||||||

|

Current liabilities:

|

||||||||

|

Accounts payable

|

227,471 | 350,741 | ||||||

|

Accrued expenses

|

286,603 | 395,841 | ||||||

|

Billings in excess of costs and estimated earnings

|

146,167 | 49,498 | ||||||

|

Notes payable (note 5)

|

5,749,777 | 5,457,565 | ||||||

|

Related party debt (note 6)

|

8,058,656 | 7,216,660 | ||||||

|

Total current liabilities

|

14,468,674 | 13,470,305 | ||||||

|

Commitments and contingencies

|

- | - | ||||||

|

Stockholders' equity (impairment):

|

||||||||

|

Preferred stock, no stated value, 10,000,000 shares

|

||||||||

|

authorized, no shares issued or outstanding

|

- | - | ||||||

|

Common stock, $.001 par value, 100,000,000 shares

|

||||||||

|

authorized, 6,707,796 and 6,307,510 shares issued

|

||||||||

|

and outstanding, respectively

|

6,708 | 6,308 | ||||||

|

Additional paid-in capital

|

12,775,775 | 12,279,698 | ||||||

|

Accumulated deficit

|

(26,026,673 | ) | (24,462,914 | ) | ||||

|

Total stockholders' equity (impairment)

|

(13,244,190 | ) | (12,176,908 | ) | ||||

| $ | 1,224,484 | $ | 1,293,397 | |||||

See accompanying summary of accounting policies and notes to the consolidated financial statements.

F-3

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

|

Year Ended December 31,

|

||||||||

|

2009

|

2008

|

|||||||

|

Revenues – Projects (Note 3)

|

$ | 143,304 | $ | 39,432 | ||||

|

Revenues – Parts and service (Note 3)

|

415,140 | 527,911 | ||||||

|

Total Revenues

|

558,444 | 567,343 | ||||||

|

Cost of sales – Projects

|

90,981 | 7,821 | ||||||

|

Cost of sales – Parts and service

|

196,091 | 241,321 | ||||||

|

Total cost of sales

|

287,072 | 249,142 | ||||||

|

Gross margin

|

271,372 | 318,201 | ||||||

|

Selling, general and administrative expenses

|

1,141,389 | 1,260,072 | ||||||

|

Loss from operations

|

(870,017 | ) | (941,871 | ) | ||||

|

Other income (expense):

|

||||||||

|

Expiration of patent obligations (Note 12 )

|

189,000 | - | ||||||

|

Interest expense (Note 5and 6)

|

(882,953 | ) | (775,800 | ) | ||||

|

Other income (expense), net

|

211 | 160 | ||||||

|

Net other expense

|

(693,742 | ) | (775,640 | ) | ||||

|

Net (loss)

|

$ | (1,563,759 | ) | $ | (1,717,511 | ) | ||

|

Loss per share – basic and diluted

|

$ | (0.24 | ) | $ | (0.27 | ) | ||

|

Weighted average shares of common stock outstanding – basic and diluted

|

6,513,415 | 6,257,025 | ||||||

See accompanying summary of accounting policies and notes to the consolidated financial statements.

F-4

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY

|

Common Stock

|

Additional Paid-In

|

Accumulated

|

Total

Stockholders’

Equity

|

|||||||||||||||||

|

Shares

|

Amount

|

Capital

|

Deficit

|

(Impairment)

|

||||||||||||||||

|

Balance, January 1, 2008

|

6,263,064 | $ | 6,263 | $ | 12,268,631 | $ | (22,745,403 | ) | $ | (10,470,509 | ) | |||||||||

|

Stock isssued for options exercised

|

44,446 | 45 | 11,067 | - | 11,112 | |||||||||||||||

|

Net loss

|

- | - | - | (1,717,511 | ) | (1,717,511 | ) | |||||||||||||

|

Balance, December 31, 2008

|

6,307,510 | 6,308 | 12,279,698 | (24,462,914 | ) | (12,176,908 | ) | |||||||||||||

|

Stock issued on related party debt conversion

|

100,000 | 100 | 99,900 | - | 100,000 | |||||||||||||||

|

Stock issued for deferred compensation payable

|

300,286 | 300 | 185,877 | - | 186,177 | |||||||||||||||

|

Stock based compensation for option award modifications

|

- | - | 210,300 | - | 210,300 | |||||||||||||||

|

Net loss

|

- | - | - | (1,563,759 | ) | (1,563,759 | ) | |||||||||||||

|

Balance, December 31, 2009

|

6,707,796 | $ | 6,708 | $ | 12,775,775 | $ | (26,026,673 | ) | $ | (13,244,190 | ) | |||||||||

See accompanying summary of accounting policies and notes to the consolidated financial statements.

F-5

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

Year Ended December 31,

|

||||||||

|

2009

|

2008

|

|||||||

|

Cash flows from operating activities:

|

||||||||

|

Net loss

|

$ | (1,563,759 | ) | $ | (1,717,511 | ) | ||

|

Adjustments to reconcile net (loss) to net cash

provided by (used in) operating activities:

|

||||||||

|

Depreciation and amortization

|

2,892 | 2,892 | ||||||

|

Stock based compensation

|

210,300 | - | ||||||

|

Allowance for doubtful accounts

|

- | (10,000 | ) | |||||

|

Accrued interest and expenses on note payable

|

292,212 | 277,362 | ||||||

|

Accrued interest and deferred expenses on related party debt

|

720,596 | 670,556 | ||||||

|

Changes in assets and liabilities:

|

||||||||

|

Accounts receivable

|

48,913 | (23,185 | ) | |||||

|

Other current assets

|

8,250 | 15,868 | ||||||

|

Accounts payable and accrued expenses

|

(46,331 | ) | 189,330 | |||||

|

Billings in excess of costs and estimated earnings

|

96,669 | 49,498 | ||||||

|

Net cash used in operating activities

|

(230,258 | ) | (545,190 | ) | ||||

|

Cash flows from investing activities:

|

||||||||

|

Cash paid for patent costs

|

- | (54,375 | ) | |||||

|

Net cash used in investing activities

|

- | (54,375 | ) | |||||

|

Cash flows from financing activities:

|

||||||||

|

Proceeds from related party debt

|

322,400 | 557,500 | ||||||

|

Repayments on related party debt

|

(101,000 | ) | - | |||||

|

Stock issued for exercised options

|

- | 11,112 | ||||||

|

Net cash provided by financing activities

|

221,400 | 568,612 | ||||||

|

Net decrease in cash and cash equivalents

|

(8,858 | ) | (30,953 | ) | ||||

|

Cash and cash equivalents, beginning of year

|

16,290 | 47,243 | ||||||

|

Cash and cash equivalents, end of year

|

$ | 7,432 | $ | 16,290 | ||||

| Supplemental Disclosures Of Cash Flow Information | ||||||||

| Cash paid during the year for: | ||||||||

| Interest |

$

|

-

|

598

|

|||||

| Income taxes |

$

|

-

|

3,680

|

|||||

|

Due to the expiration of certain patents and related agreements in April 2009, the Company realized a net gain of $189,000 from the reversal of amounts accrued against estimated future income from such patents. No revenues were realized from the patents.

|

||||||||

|

In June 2009, accrued deferred compensation of $186,177 was converted to 300,286 shares of common stock.

|

||||||||

|

In July 2009, the Company issued 100,000 shares of common stock at $1.00 per share, to an officer/ director in conversion of $100,000 of related party notes payable.

|

||||||||

See accompanying summary of accounting policies and notes to the consolidated financial statements.

F-6

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Nature of Operations, Principles of Consolidation and Basis of Presentation

Nature of Operations

MPM Technologies, Inc. (the Company) was incorporated as Okanogan Development, Inc. on July 18, 1983, under the laws of the State of Washington. It was formed primarily for the purpose of investing in real estate and interests in real estate. On April 25, 1985, the Company combined with MADD Exploration (MADD), a Montana partnership, and changed its name to Montana Precision Mining, Ltd. In August 1995, the Company changed its name to MPM Technologies, Inc. As a result of the combination with MADD, the Company acquired mining properties located in Powell County, Montana. The Company is not currently engaged in exploration or developmental mining activities in regard to these properties.

AirPol, Inc. (AirPol), a wholly owned subsidiary, was acquired on July 2, 1998. AirPol designs, engineers, supplies and services air pollution control systems. AirPol’s systems utilize wet and dry scrubbers, wet electrostatic precipitators and venturi absorbers to control air pollution.

The Company holds a 58.21% interest in NuPower Partnership through its ownership of NuPower, Inc. (NuPower), its wholly-owned subsidiary. No other operations were conducted through NuPower. NuPower Partnership is engaged in the development and commercialization of a waste-to-energy process. This is an innovative technology for the disposal and gasification of carbonaceous wastes such as municipal solid waste, municipal sewage sludge, pulp and paper mill sludge, auto fluff, medical waste and used tires. The process converts solid and semi-solid wastes into a clean-burning medium BTU gas that can be used for steam production for electric power generation. The gas may also be a useful building block for downstream conversion into valuable chemicals. NuPower Partnership owns 85% of the Skygas Venture. In addition to its partnership interest, MPM owns 15% of the Venture.

In 2008 a new company was incorporated named Skygas Energy Ontario Limited (“SEOL”). NuPower owns all 100 of the issued and outstanding shares of the new company. This company is seeking a business venture in Canada to commercialize the Skygas process. Management was in negotiations with unrelated third parties with regard to this venture, however, such negotiations were terminated when agreements could not be reached. It is unclear at this time what form this venture will take.

The United States patent on the Skygas process expired in November 2008. The Company filed a one-year provisional new patent for a significantly improved Skygas process in February 2009. In February 2010, a renewal patent application was filed. There can be no guarantee that the new patent will be approved at this time. There was also a Canadian patent on the Skygas process that expired in April 2009.

Principles of Consolidation

The accompanying consolidated financial statements include the accounts of the Company and the following subsidiaries and other entities controlled by the Company: AirPol, Inc. (AirPol), MPM Mining, Inc., NuPower, Inc. (NuPower), NuPower Partnership (a General Partnership), Skygas Venture (Skygas) and SEOL. Intercompany accounts and transactions among the companies have been eliminated.

Segment Reporting

Management considers MPM’s reportable segments to be business units that offer different products. The business segments may be reportable because they are each managed separately, or they design and engineer distinct products with different applications in the air pollution control field. AirPol operates in the air pollution control field. MPM’s other segments are essentially non-operational at the present time, and, accordingly have been aggregated for reporting purposes. Accordingly, for the years ended December 31, 2009 and 2008, the Company operated in one segment, and there is no separate segment reporting required.

F-7

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

2. Going Concern

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. As of December 31, 2009, the Company has a working capital deficiency, an accumulated deficit, and has not been able to generate any significant revenues. These conditions raise substantial doubt about the ability of the Company to continue as a going concern. The Company plans to raise additional capital in the future. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty. The Company has a working capital deficiency of $14,453,054. Current liabilities include $8,058,656 of related party debt which management believes can be deferred beyond twelve months. Also included in current liabilities is $5,749,777 of a note payable which management is currently renegotiating. Management is optimistic that the lender will agree to terms that will extend the payment and allow the Company to meet its obligations and continue business for the next twelve months. There is no guarantee of the outcome of these plans.

3. Summary of Significant Accounting Policies

Revenue Recognition

Contract revenue is recognized on the percentage-of-completion method in the ratio that costs incurred bear to estimated costs at completion. Costs include all direct material and labor costs, and indirect costs, such as supplies, tools, repairs and depreciation. Selling, general and administrative costs are charged to expense as incurred. Other revenue is recorded on the basis of shipment or performance of services or shipment of products. Provision for estimated contract losses, if any, is made in the period that such losses are determined. During 2009 and 2008, no amounts were recognized for estimated contract losses.

The asset “costs and estimated earnings in excess of billings” represents revenues recognized in excess of amounts invoiced. The liability “billings in excess of costs and estimated earnings” represents invoices in excess of revenues recognized.

Property, Plant and Equipment

Property, plant and equipment are stated at cost, less accumulated depreciation. For financial reporting purposes, the costs of plant and equipment are depreciated over the estimated useful lives of the assets, which range from three to fifteen years, using the straight-line method.

Asset Impairment

The Company evaluates its long-lived assets for financial impairment, and continues to evaluate them as events or changes in circumstances indicate that the carrying amount of such assets may not be fully recoverable. The Company evaluates the recoverability of long-lived assets by measuring the carrying amount of the assets against the estimated undiscounted future cash flows associated with them. At the time such evaluations indicate that the future undiscounted cash flows of certain long-lived assets are not sufficient to recover the carrying value of such assets, the assets are adjusted to their fair values.

F-8

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Income Taxes

The Company accounts for income taxes under the provisions of Financial Accounting Standards Board (FASB) Accounting Standards Modification (ASC) 740-10 “Income Taxes”. FASB ASC 740-10 uses the asset and liability method so that deferred taxes are determined based on the estimated future tax effects of differences between the financial statement and tax basis of assets and liabilities given the provisions of enacted tax laws and tax rates. Deferred income tax expense or benefit is based on the changes in the financial statement basis versus the tax bases in the Company’s assets or liabilities from period to period.

Research and Development Costs

Research and development costs are charged to expense as incurred.

Advertising Costs

Advertising costs are charged to operations when incurred. Advertising expense was $-0- and $3,167 for the years ended December 31, 2009 and 2008, respectively.

Estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions. Those estimates and assumptions affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Stock Based Compensation

The Company accounts for stock, stock options and stock warrants issued for services and compensation by employees under FASB Accounting Standards Codification 718. For non-employees, the fair market value of the Company’s stock is measured on the date of stock issuance or the date an option/warrant is granted. The Company determined the fair market value of the warrants/options issued under the Black-Scholes Pricing Model. Under the provisions of FASB ASC 718, share-based compensation cost is measured at the grant date, based on the fair value of the award, and is recognized as an expense over the employee's requisite service period (generally the vesting period of the equity grant).

Concentrations of Credit Risk

Financial instruments, which potentially subject the Company to a concentration of credit risk, consist of cash and cash equivalents. The Company places its cash and cash equivalents with various high quality financial institutions; these deposits may exceed federally insured limits at various times throughout the year. The Company provides credit in the normal course of business. The Company performs ongoing credit evaluations of its customers and maintains allowances for doubtful accounts based on factors surrounding the credit risk of specific customers, historical trends, and other information.

Fair Value of Financial Instruments

The carrying amounts reported in the balance sheet as of December 31, 2009 for cash equivalents, investments, accounts payable and accrued expenses approximate fair value because of the immediate or short-term maturity of these financial instruments. The fair value of notes payable and long-term debt approximates their carrying value as the stated or discounted rates of the debt reflect recent market conditions.

F-9

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Limitations

Fair value estimates are made at a specific point in time, based on relevant market information and information about the financial statement. These estimates are subjective in nature and involve uncertainties and matters of significant judgment and therefore cannot be determined with precision. Changes in assumptions could significantly affect the estimates.

Cash and Cash Equivalents

For purposes of balance sheet classification and the statements of cash flows, the Company considers all highly liquid investments purchased with an original maturity of three months or less to be cash equivalents.

Warranty Reserve

The Company warranties its pollution control units for defects in design, materials, and workmanship generally for a period of 18 months from date sold or 12 months from date placed in service. Provision for estimated warranty costs is recorded upon completion of the project and periodically adjusted to reflect actual experience.

Earnings Per Share

FASB ASC requires dual presentation of basic earnings per share and diluted earnings per share on the face of all income statements issued after December 15, 1997 for all entities with complex capital structures. Basic earnings (loss) per share includes no dilution and is calculated by dividing income available to common shareholders by the weighted average number of shares actually outstanding during the period. Diluted earnings per share, computed using the treasury stock method, reflects the potential dilution of securities (such as stock options, warrants and securities convertible into common stock assuming all in-the-money) that could share in the earnings of an entity. At December 31, 2009 and 2008, outstanding options to purchase 2,085,084 shares of the Company’s common stock were not included in the computation of diluted earnings per share as their effect would have been antidilutive.

4. Property, Plant and Equipment

Property, plant and equipment consist of the following at:

|

December 31,

|

||||||||

|

2009

|

2008

|

|||||||

|

Equipment

|

$ | 153,265 | $ | 271,437 | ||||

|

Furniture and fixtures

|

31,008 | 31,008 | ||||||

|

Leasehold improvements

|

8,321 | 8,321 | ||||||

| 192,594 | 310,766 | |||||||

|

Less accumulated depreciation

|

190,473 | 305,753 | ||||||

| $ | 2,121 | $ | 5,013 | |||||

Depreciation expense charged to operations was $2,892 and $2,892 in 2009 and 2008, respectively.

F-10

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

5. Note Payable and Long-Term Debt

In December 2002, the Company entered into a revolving credit agreement with an insurance company. Under the terms of its agreement, the Company could borrow up to $500,000 at 5.25% per annum, which was increased to $3,000,000 in 2003. As of December 31, 2009 and 2008, the Company had $4,326,499 and $4,326,499, respectively, of principal advances and accrued interest of $1,423,278 and $1,131,066, respectively, outstanding under the agreement. During the years ended December 31, 2009 and 2008, the Company recorded interest expense of $292,212 and $277,362, respectively. The note is secured by stock and mineral property held for investment and matured on January 2, 2008. This note payable has not been paid at maturity and management is currently renegotiating its terms with the lender. Through the date of this report, no revised terms have been arranged on this defaulted debt.

6. Related Party Debt

Related party debt consists of the following at:

|

December 31,

|

||||||||

|

2008

|

2008

|

|||||||

|

Due to an officer/director

|

$ | 4,565,771 | $ | 4,138,449 | ||||

|

Due to a trust for which an officer/director is trustee

|

2,649,000 | 2,239,525 | ||||||

|

Due to a partnership for which the above trust and another

|

||||||||

|

officer/director are partners

|

422,653 | 388,453 | ||||||

|

Due to another officer/director

|

421,232 | 450,133 | ||||||

| $ | 8,058,656 | $ | 7,216,660 | |||||

The related party debt consists of advances received from and deferred expenses and reimbursements to the parties shown above. Interest expense accrued on this related party debt for the years ended December 31, 2009 and 2008 was $590,741 and $670,556, respectively. The debt is unsecured, bears interest at 12% per annum, and is due on demand.

7. Commitments and Contingencies

The Company leases office space and mineral properties under operating leases that expire at various dates through 2010. Future minimum rental payments required under operating leases that have initial and remaining non-cancellable terms in excess of one year are as follows: $50,023 for the year ending December 31, 2010.

Rent expense for the years ended December 31, 2009 and 2008 was $81,908 and $87,341, respectively.

In December 2007, the Company entered an agreement with an officer/director regarding payroll reductions in 2003. Under the terms of the agreement, the Company will retroactively reimburse the officer/director for salary reductions from April 2003 if certain conditions are met. These include the profitability of the Company and its ability to repay the amounts due. Additionally, under the terms of the agreement, unpaid accrued amounts will bear interest at 8% per annum beginning January 1, 2008. For the years ended December 31, 2009 and 2008, amounts accrued and charged to expense were $32,117 and $40,238, respectively, which includes accrued interest of $7,807 and $12,134, respectively. In June 2009, the officer/director converted $186,177 of the accrued deferred compensation into 300,286 shares of common stock of the Company. As of December 31, 2009 and 2008, amounts owed to this officer/director were $19,672 and $173,732, respectively, recorded within the caption “Accrued expenses”.

The Company has a contract with R.D. Little Co. to provide shareholder and investor relations services. During 2008, the Company renewed this contract for five more years. Robert D. Little, Secretary of the company, owns R.D. Little Co. For the years ended December 31, 2009 and 2008, MPM paid $83,400 and $74,000, respectively, for these services. As of December 31, 2009 and 2008, amounts owed to R.D. Little Co. were $102,179 and $79,454, respectively, recorded within the caption “Accrued expenses”.

F-11

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

8. Income Taxes

The significant components of the Company’s net deferred tax asset is as follows as of December 31:

|

2009

|

2008

|

|||||||

|

Net operating loss carryforward

|

$ | 5,100,000 | $ | 4,200,000 | ||||

|

Differences between book and tax depreciation

|

20,000 | 20,000 | ||||||

|

Goodwill and purchase asset adjustments

|

- | - | ||||||

|

Write-down of mineral properties

|

136,000 | 136,000 | ||||||

|

Other

|

40,000 | 40,000 | ||||||

| 5,296,000 | 5,206,000 | |||||||

|

Less: valuation allowance

|

5,296,000 | 5,206,000 | ||||||

| $ | - | $ | - | |||||

As management of the Company cannot determine that it is more likely than not that the Company will realize the benefit of the net deferred tax asset, a valuation allowance equal to the net deferred tax asset has been established at December 31, 2009 and 2008. The valuation allowance increased $90,000 since December 31, 2008.

At December 31, 2009, the Company had net operating loss carryforwards for federal income tax purposes totaling approximately $11.4 million that expire in the years 2010 through 2029. MPM files income tax returns in various states. At December 2009, the Company has net operating loss carryforwards for state income tax purposes totaling ranging from approximately $2.7 to approximately $5.1 million, depending on the state, that expire in the years 2010 through 2029.

9. Stockholders’ Equity

Stock Option Plan

On May 22, 1989, the shareholders of the Company voted to approve a stock option plan (the Plan) for selected key employees, officers and directors of the Company. The Plan is administered by a Compensation Committee of the Board of Directors (the “Committee”) consisting of those directors of the Company and individuals who are elected annually by the Board of Directors to the Committee. The Board of Directors has chosen one of the Company’s directors and one outside individual to serve on the Committee. No director eligible to receive options under the Plan may vote upon the granting of an option or Stock Appreciation Rights (SAR) to himself or herself or upon any decision of the Board of Directors or the Committee relating to the Plan. Under the Plan, a maximum of 236,667 shares were approved to be granted, which in 2003 was increased by 300,000. During the 2008 shareholders’ meeting the shareholders voted to increase the number of shares authorized to be granted under the plan by 500,000 shares. Generally, the Plan provides that the terms under which options may be granted are to be determined by a Committee subject to certain requirements as follows: (1) the exercise price will not be less than 100% of the market price per share of the common stock of the Company at the time an Incentive Stock Option is granted, or as established by the Committee for Non-qualified Stock Options or Stock Appreciation Rights; and (2) the option purchase price will be paid in full on the date of purchase.

F-12

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Qualified stock option activity under the Plan and non-qualified stock option activity outside the Plan are summarized as follows:

|

Weighted

|

||||||||

|

Average

|

||||||||

|

Option

|

||||||||

|

Options

|

Price

|

|||||||

|

Outstanding at January 1, 2008

|

2,186,675 | $ | 0.90 | |||||

|

Granted

|

- | - | ||||||

|

Exercised

|

44,446 | 0.25 | ||||||

|

Expired

|

(57,145 | ) | - | |||||

|

Outstanding at January 1, 2008

|

2,085,084 | $ | 0.78 | |||||

|

Granted

|

- | - | ||||||

|

Exercised

|

- | - | ||||||

|

Expired

|

- | - | ||||||

|

Outstanding at December 31, 2008

|

2,085,084 | $ | 0.78 |

The Company accounts for stock and stock options issued for services and compensation by employees under the fair value method. For non-employees, the fair market value of the Company's stock on the date of stock issuance or option/grant is used. The Company determined the fair market value of the options issued under the Black-Scholes Pricing Model. The Company adopted the provisions of FASB ASC 718 SHARE-BASED PAYMENT, which establishes accounting for equity instruments exchanged for employee services. Under the provisions of FASB ASC 718, share-based compensation cost is measured at the grant date, based on the fair value of the award, and is recognized as an expense over the employee's requisite service period (generally the vesting period of the equity grant). The Company used the following assumptions in its calculation: Dividend yield-$0; Expected volatility 23%; Risk-free interest rate 3.49%; Expected life 5 years. The Company recorded expenses of $34,692 in 2007 related to the 280,000 options that were issued. No options were issued in 2009 or 2008.

On April 15, 2009, the Company’s Board of Directors authorized a five-year extension of the expiration dates for 847,667 options outstanding that were due to expire in April and May, 2009. In accordance with Financial Accounting Standards Board Accounting Codification Topic 718-10-10, “Accounting for Stock Based Compensation” (ASC 718), the Company recorded incremental compensation for the amended stock options based on the excess of the fair value of the amended option agreements over the fair value of the original options immediately before the amendment. Fair value was determined using a Black-Scholes Pricing Model, using the following assumptions: Dividend yield $-0-; Expected volatility range of 1% (pre-amendment) to 258% (post-amendment); Risk-free interest rate of 1.71%; Expected lives of 4 or 34 days (pre-amendment) to 5 years (post-amendment). The Company recorded stock-based compensation in the second quarter of 2009 in the amount of $210,300 related to the amended option agreements.

The following table summarizes information about stock options outstanding at December 31, 2009:

|

Options

|

||||||||||||||||

|

Number

|

Weighted

|

Outstanding and

|

||||||||||||||

|

Range of

|

Outstanding

|

Average

|

Exercisable Weighted

|

|||||||||||||

|

Exercise

|

and Exercisable

|

Exercise

|

Average Remaining

|

|||||||||||||

|

Prices

|

at 12/31/08

|

Price

|

Contractual Life (Years)

|

|||||||||||||

| $ | 0.10 | 85,000 | $ | 0.10 | 6.8 | |||||||||||

| $ | 0.22 | 370,750 | $ | 0.22 | 4.7 | |||||||||||

| $ | 0.30 | 130,000 | $ | 0.30 | 8.8 | |||||||||||

| $ | 0.31 | 100,000 | $ | 0.31 | 8.1 | |||||||||||

| $ | 0.50 | 437,000 | $ | 0.50 | 4.2 | |||||||||||

| $ | 0.75 | 450,000 | $ | 0.75 | 2.7 | |||||||||||

| $ | 1.00 | 141,667 | $ | 1.00 | 4.5 | |||||||||||

| $ | 2.00 | 334,000 | $ | 2.00 | 4.3 | |||||||||||

| $ | 3.00 | 36,667 | $ | 3.00 | 4.4 | |||||||||||

|

|

$ | 0.10 - 3.00 | 2,085,084 | $ | 0.78 | 5.4 | ||||||||||

F-13

MPM TECHNOLOGIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

10. Valuation and Qualifying Accounts

Allowance for doubtful account activity was as follows:

|

December 31,

|

||||||||

|

2009

|

2008

|

|||||||

|

Balance, beginning of year

|

$ | - | $ | 10,000 | ||||

|

Charged to (deducted from) expense

|

- | (10,000 | ) | |||||

|

Balance, end of year

|

$ | - | $ | - | ||||

11. Mineral Properties

In accordance with guidelines established by the American Institute of Certified Public Accountants, we conducted impairment testing on these assets. Factors evaluated included whether there was a significant decrease in the market prices of the assets. Impairment testing was necessary because of the Company’s current period operating and cash flow losses, and its history of operating and cash flow losses. Impairment is defined in the accounting literature as the condition that exists when the carrying amount of a long-lived asset exceeds its fair value. An impairment loss shall be recognized only if the carrying amount of a long-lived asset is not recoverable and exceeds its fair value. The carrying amount of a long-lived asset is not recoverable if it exceeds the sum of the undiscounted cash flows expected to result from the use and eventual disposition of the asset.

The mineral property and related equipment is carried on the balance sheet at December 31, 2009 and 2008 in the amount of $1,070,368. In performing impairment testing, we based our assessment on the carrying amount of the assets as of the date of the impairment testing for recoverability. As part of our testing, we made certain assumptions about the use of the assets and assigned probability levels based on assumptions of activity levels involved in the use of the assets. The result of our testing was that there was no impairment in the carrying amount of the mineral property.

12. Prepaid Royalty

During 1994, the Company entered into an agreement to sell certain equipment related to the SkyGas technology to the inventor of this technology in exchange for a $275,000 note receivable. The note was collateralized by the equipment sold. Under the agreement, the note was due in a balloon payment of $275,000 on December 1, 1995 or at such time the Skygas process is placed into sustainable commercial production. Additional renewals have not been negotiated and the Company has re-characterized this former note receivable as prepaid royalties, recoverable from future revenues resulting from the operation of the equipment. The balance at December 31, 2009 of $273,000 has been offset against royalties payable to the estate of the inventor. In 2009, the patent on the Skygas process expired. As a result, prepaid royalties and royalties payable were written off, yielding a $189,000 gain on expiration of patent agreements for the year ended December 31, 2009.

13. Related Party Transactions

At December 31, 2009 and 2008, the Company owed $8,058,656 and $7,216,660, respectively, to an officer/director, a trust for which an officer/director is trustee, a partnership for which the trust and another officer/director are partners, and another officer/director. During 2009 and 2008, an officer/director loaned $70,000 and $217,500, respectively, to the Company. The Company made repayments during 2009 of $86,000. No repayments were made in 2008. During 2009, another officer/director loaned $40,400 to the Company, of which $15,000 was repaid. No loans or repayments were made in 2008 from this officer/director. Additionally, this officeer/director converted $100,000 of amounts owed to him for 100,000 shares of the Company’s common stock in 2009. A trust for which an officer/director is trustee loaned $202,000 and $340,000 for 2009 and 2008, respectively. These loans are unsecured, bear interest at 12% per annum, and are due on demand.

The Company contracts for its shareholder relations services with an officer of the Company. The Company incurred expenses to this related party for services in 2009 and 2008 of $83,400 and $74,400, respectively. As of December 31, 2009 and 2008, amounts accrued and unpaid to this officer amounted to $102,179 and $79,454, respectively.

F-14

14. Other Assets, net

Other Assets, net consist of the following at:

|

December 31,

|

||||||||

|

2009

|

2008

|

|||||||

|

Security deposit

|

$ | 50,000 | $ | 50,000 | ||||

|

Patent

|

86,375 | 86,375 | ||||||

| $ | 136,375 | $ | 136,375 | |||||

15. 401(k) Plan

The Company (Airpol) maintains a 401(k) employee retirement plan for its eligible full-time employees with at least one year of service. The Company makes matching contributions equal to 50% up to a maximum 4% deferral. Contributions to the plan for the years ended December 31, 2009 and 2008 were $4,027 and $5,369, respectively.

|

16.

|

Memorandum of Understanding

|

On December 26, 2009, the Company entered into a memorandum of understanding (“MOU”) with a potential investor interested in acquiring a majority of the common stock of the Company from two of its officers/directors. Under the terms of the MOU, the potential investor paid $25,000 upon signing the MOU with a balance of $225,000 being provided, and the officers/directors’ stock being acquired upon the satisfactory completion of the potential investor’s due diligence. In exchange for the $250,000, the Company is to issue a note payable that is convertible into the Company’s common stock. The Company received the initial $25,000 at the end of December, and has recorded this amount in the caption “Accrued expenses” pending completion or cancellation of the transaction. Subsequent to yearend, the potential investor provided additional proceeds of $25,000 to the Company.

The potential investor is currently performing the due diligence. There can be no assurances that the due diligence will be of a satisfactory nature to facilitate completion of the transaction.

|

17.

|

New Accounting Pronouncements

|