Attached files

| file | filename |

|---|---|

| EX-31 - Balincan USA, Inc. | v181111_ex31.htm |

| EX-32 - Balincan USA, Inc. | v181111_ex32.htm |

UNITED

STATES SECURITIES AND EXCHANGE COMMISSION

Washington,

D.C. 20549

Form 10-K

|

(Mark

One)

|

|

|

x

|

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

|

For

the fiscal year ended December 31, 2009

|

|

|

OR

|

|

|

o

|

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

|

For

the transition period from

to

|

MOQIZONE

HOLDING CORPORATION

(Exact

name of registrant as specified in its charter)

|

DELAWARE

|

95-4217605

|

|

(State

or other jurisdiction of

incorporation

or organization)

|

(I.R.S.

Employer Identification No.)

|

|

7A-D

Hong Kong Industrial Building

444-452

Des Voeux Road West

Hong

Kong

|

N/A

|

|

(Address

of principal executive offices)

|

(Zip

Code)

|

Registrant’s

telephone number, including area code:

+852

34434384

Securities

registered pursuant to Section 12(b) of the Act:

|

Title

of each class

|

Name

of each exchange on which registered

|

|

None

|

None

|

Securities

registered pursuant to Section 12(g) of the Act:

Common

Stock, par value $0.001 per share

Indicate

by check mark if the registrant is a well-known seasoned issuer as defined in

Rule 405 of the Securities Act.

Yes o No x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days. Yes x No

o

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this

chapter) during the preceding 12 months (or for such shorter period that

the registrant was required to submit and post such files). Yes o No

o

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K (§229.405 of this

chapter) is

not contained herein, and will not be contained, to the best of the registrant’s

knowledge, in definitive proxy or information statements incorporated by

reference in Part III of this Form 10-K or any amendment to this Form

10-K. o

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company. See the definitions of “large accelerated filer,”

“accelerated filer” and “smaller reporting company” in Rule 12b-2 of the

Exchange Act. (Check one):

|

Large

accelerated filer o

|

Accelerated

filer o

|

||

|

Non-accelerated

filer o (Do

not check if a smaller reporting

company) |

Smaller

reporting company

x

|

Indicate

by check mark whether the registrant is a shell company (as defined by Rule

12b-2 of the Act). Yes o No

x

As of June 30, 2009 (last business day of the registrant’s

most recently completed second fiscal quarter), the aggregate market value of the

voting common stock held by non-affiliates of the Registrant (without admitting

that any person whose shares are not included in such calculation is an

affiliate) was approximately $5,375,489. On April 15, 2009, there were 13,667,764 shares of the Registrant’s common stock

outstanding.

|

Page

|

|||

|

PART

I

|

|||

|

Item

1

|

Business

|

3

|

|

|

Item

1A

|

Risk

Factors

|

15

|

|

|

Item

1B

|

Unresolved Staff

Comments

|

26 | |

|

Item

2

|

Properties

|

26

|

|

|

Item

3

|

Legal

Proceedings

|

26

|

|

|

Item

4

|

(Removed and

Reserved)

|

27

|

|

|

PART

II

|

|||

|

Item

5

|

Market

for Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities

|

27

|

|

|

Item

6

|

Selected

Financial Data

|

27

|

|

|

Item

7

|

Management’s

Discussion and Analysis of Financial Conditions and Results of

Operations

|

28

|

|

|

Item

7A.

|

Quantitative

and Qualitative Disclosures about Market Risk.

|

33

|

|

|

Item

8

|

Financial

Statements and Supplementary Data

|

34

|

|

|

Item

9

|

Changes

in and Disagreements with Accountants on Accounting and Financial

Disclosure

|

49

|

|

|

Item

9A

|

Controls

and Procedures

|

49

|

|

|

Item

9B

|

Other

Information

|

49

|

|

|

PART

III

|

|||

|

Item

10

|

Directors

and Executive Officers and Corporate Governance

|

50

|

|

|

Item

11

|

Executive

Compensation

|

53

|

|

|

Item

12

|

Security

Ownership of Certain Beneficial Owners and Management And Related

Stockholder Matters

|

55

|

|

|

Item

13

|

Certain

Relationships and Related Transactions, and Director

Independence

|

56

|

|

|

Item

14

|

Principal

Accounting Fees and Services

|

58

|

|

|

PART

IV

|

|||

|

Item

15

|

Exhibits,

Financial Statements Schedules

|

59

|

|

|

Signatures

|

|||

|

Exhibit

31

|

|||

|

Exhibit

32

|

2

PART

I

Item

1. Business

This

summary highlights selected information appearing elsewhere in this Form 10-K.

While this summary highlights what we consider to be the most important

information about us, you should carefully read this Form 10-K in its entirety

before investing in our common stock, which we discuss later in “Risk

Factors,” and our financial statements and related notes. Unless the context

requires otherwise, the words the “Company” “we,” “us” and “our” refer to

Moqizone Holding Corporation and our subsidiaries including MoqiZone Hong

Kong, MoqiZone Cayman, Shanghai MoqiZone and SZ Alar, the word “MoqiZone”

refers only to Moqizone Holding Corporation.

General

Overview

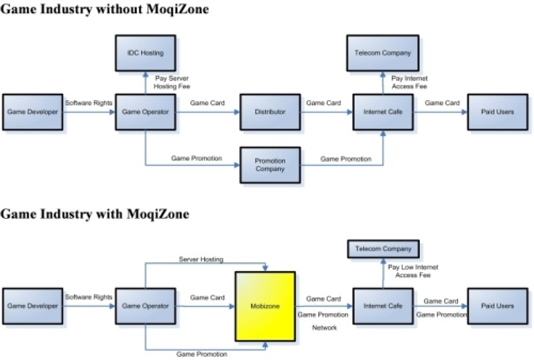

Through

our Shanghai MoqiZone subsidiary, we provide an online game delivery platform

delivering contents of online games that are hosted by us to internet cafes

which have installed Netcafe Farmer and/or our WiMAX equipment in China via our

Netcafe Farmer software or our proprietary MoqiZone WiMAX Network. Our primary

business focus is to provide content delivery to the viral online gaming market

and connect game players to online content providers. Our MoqiZone WiMAX Network

is a wireless virtual proprietary network designed to provide online game

contents hosted by us to the Internet cafes which have installed our WiMAX

equipment. Netcafe Farmer is an online game auto-update distribution system

which enables internet cafés to automatically update the client-end gaming

software with patches on a real time basis for all their personal computers or

PCs in their cafes. The combination of MoqiZone WiMAX Network and Netcafe Farmer

form the backbone of our distribution channel for our online games to our

targeted market, which are licensed Internet cafes in cities where the internet

cafés business is more developed.

Since

November 2009, we have connected approximately 30 Internet cafes in Chengdu and

3 Internet cafes in Suzhou. We have not generated any revenue as of 31st

December 2009, since these Internet cafes have been operating as our pilot trial

sites and are not revenue producing as we are providing our WiMAX installation

to the Internet cafes free of charge. Once there are a substantial number of

WiMAX installed Internet cafes participating in our business, we plan to

commence our charged services to the Internet cafes.

Netcafe

Farmer is currently servicing approximately 700 internet cafés mainly in Henan,

Hebei, Zhejiang, and Northeast of China with a nominal annual subscription fees

and has also established a strong network with major content suppliers to help

them to promote games in internet cafés.

Our key

business development objectives over the next two years are to grow and expand

our business penetration servicing Internet cafes throughout selected targeted

cities in China. These business objectives will require the build out of

our MoqiZone WiMAX Network, marketing Netcafe Farmer, continuous technological

development of our business portals including but not limited to www.moqizone.com and www.53mq.com. Additionally, we plan to

begin aggregating more online games. We will not be able to generate significant

revenue until we have a basic foundation of all these components.

Our

principal executive offices are located at Hong Kong and Shanghai with a branch

office in Chengdu and a representative office in Beijing, and our telephone

number is +852 34434383.

Our

History

Moqizone

Holding Corporation, formerly called Trestle Holdings, Inc., was previously a

non-operating public company which was seeking out suitable candidates for a

business combination with a private company. Trestle originally

developed and sold digital tissue imaging and telemedicine applications linking

dispersed users and data primarily in the healthcare and pharmaceutical

markets.

The

common stock of MoqiZone currently trades on the OTCBB under the symbol

“MOQZ.”

Acquisition

of our Operating Business

On March

15, 2009, Trestle entered into a Share Exchange Agreement with MoqiZone Cayman,

Mr. Lawrence Cheung, the principal shareholder of MoqiZone Cayman, and, MKM

Capital Opportunity Fund Ltd., our former principal stockholder (the

“Agreement”). MoqiZone Cayman is the record and beneficial owner of

100% of the share capital of MoqiZone Hong Kong and MoqiZone Hong Kong is the

record and beneficial owner of 100% of the share capital of Shanghai

MoqiZone. On June 1, 2009, pursuant to the Agreement, and as a result

of MoqiZone Hong Kong’s receipt of approximately $4,345,000 in gross proceeds

from our private financing, Trestle became the record and beneficial owner of

100% of the share capital of MoqiZone Cayman and therefore own 100% of the share

capital of MoqiZone Hong Kong directly and Shanghai MoqiZone indirectly in

exchange for the issuance to Lawrence Cheung and the other shareholders of

MoqiZone Cayman of 10,743 shares of our Series B convertible preferred stock,

which Series B preferred stock was automatically converted (on the basis of

1,000 shares of common stock for each share of Series B preferred stock) into an

aggregate of 10,743,000 shares of our common stock, representing approximately

95% of our issued and outstanding shares of common stock at the time

of conversion (but prior to the conversion of any of the shares our Series A

preferred stock ). The remaining 5% of the then outstanding shares of the

Company’s common stock are publicly traded and are owned by approximately 83

shareholders on record (see Reverse Stock Split below at Page 3).

3

Pursuant

to the terms of the Agreement, Eric Stoppenhagen resigned as our Interim

President, effective at the time of the transaction. Additionally, each of

our former directors tendered their resignation as directors on June 19, 2009,

to our stockholders. Our Board of Directors appointed Lawrence Cheung

to serve as our Chief Executive Officer and director, effective June 19,

2009. Additionally, commencing on that same date, Benjamin Chan was

elected to serve as a director as well.

Recent

developments

Name

Change

On July

16, 2009, a majority of our shareholders, via written consent, approved changing

our corporate name from “Trestle Holdings, Inc.” to “MoqiZone Holding

Corporation”. In connection with our name change, we received a new trading

symbol and cusipnumber. Effective August 31, 2009, we began trading

on the Over the Counter Bulletin Board under the symbol “MOQZ”; and our new

cusip number is 616348108.

Preferred

Stock

On July

8, 2009, a majority of our shareholders approved, via written consent, the

issuance of an additional 10,000,000 shares of preferred stock with a par value

of $0.001. As a result of the issuance, we have a total amount of 15,000,000

shares of preferred stock authorized. These shares are made up of

three classes:

|

(a)

|

14,974,257

shares of preferred stock (“Blank Check preferred

stock”);

|

|

(b)

|

15,000

shares of Series A preferred stock;

|

|

(c)

|

10,743

shares of Series B preferred

stock.

|

Additionally,

we filed a Definitive Schedule 14C regarding the name change and increase in

preferred stock on August 24, 2009 and mailed such notice to our shareholders on

August 28, 2009.

The

Reverse Stock Split

On July

8, 2009, a majority of our shareholders approved a one-for-254.5 reverse stock

split (the “Reverse Stock Split”), via written consent. We were seeking via

reverse split to reduce the number of outstanding shares of our common stock by

reclassifying and converting all outstanding shares of our common stock into a

proportionately fewer number of shares of common stock. On August 31,

2009, the Reverse Stock Split occurred thereby reducing 179,115,573 shares of

common stock to 703,974. Simultaneous with the reverse split, the

Series B Preferred Stock automatically converted into 10,743,000 shares of

common stock. As a result, this left us with 11,446,974 shares of

common stock issued and outstanding as of August 31,

2009.

Additionally,

as of August 28, 2009, our corporate name changed to MoqiZone Holding

Corporation and our authorized capital increased by 10,000,000 shares of

preferred stock. Pursuant to the additional financings we closed in

August 2009 and the authority vested in our Board of Directors, we also filed a

certificate of designation of Series A preferred stock and certificate of

designation of Series B preferred stock with Delaware’s Secretary of State to

designate 15,000 of the 15,000,000 shares of preferred stock as Series A

preferred stock and 10,743 of the 15,000,000 shares of preferred stock as Series

B preferred stock. Upon effectiveness of the Reverse Split on August 31, 2009,

each $1,000 principal amount of Notes was automatically cancelled and exchanged

for one share of Series A Preferred Stock. Since we sold a total of

494.5 Units, upon exchange of the Notes, a total of 4,945 shares of Series A

Preferred Stock were issued, which are convertible into an aggregate of

2,747,222 shares of common stock, subject to anti-dilution and other adjustments

as provided in the Series A Preferred Stock Certificate of

Designations. Additionally, upon effectiveness of the Reverse Split,

the 10,743 shares of Series B preferred stock were automatically converted into

10,743,000 shares of our common stock.

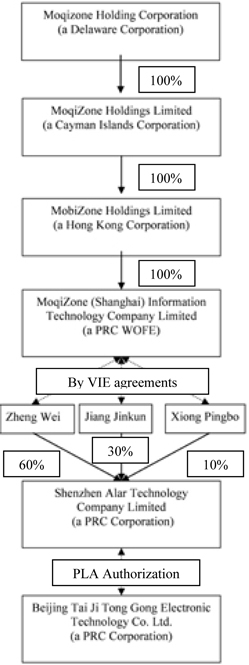

New

VIE Agreements

In

January 2009, Shanghai Moqizone entered into an Exclusive Business Cooperation

Agreement and certain ancillary agreements, including an Equity Pledge

Agreement, Exclusive Option Agreement, Loan Agreement and Irrevocable Power of

Attorney with SZ Mellow. However, as a result of disputes with the shareholders

of SZ Mellow, on September 21, 2009, in accordance with the terms of the SZ

Mellow Agreements, we sent out a 30-day prior written notice to SZ Mellow

stating our intention of terminating the SZ Mellow Agreements. The SZ Mellow

Agreements was terminated at the expiry of the 30-day notice on October 20,

2009.

In order

to continue our business and operations as planned, on September 25, 2009,

Shanghai MoqiZone entered into an Exclusive Business Cooperation and certain

ancillary agreements, including an Equity Pledge Agreement, Exclusive Option

Agreement, Loan Agreement and Irrevocable Power of Attorney with SZ Alar,

effectively gaining indirect control over SZ Alar. Also on September 25, 2009,

Tai Ji agreed to grant the PLA authorization sub-license to SZ Alar and

terminate its current sub-license with SZ Mellow. As a result of the SZ Alar

Agreements between Shanghai MoqiZone and SZ Alar, we do not anticipate any

significant interruption in our business or operations as a result of our

terminating the agreements with SZ Mellow.

Appointment

of New Director

On

November 3, 2009, we announced that Mr. Paul Lu has been appointed as a director

of our board.

4

Acquisition of

Netcafe Farmer

On

December 21, 2009, we acquired a client-end software called “Netcafe Farmer”

which was originally developed by Mr. Liu Qian in 2006. It is a client-end

software solution that provides an automatic content update distribution system

in internet cafés allowing internet cafés to automatically update their

client-end software on a real time basis for all their computers. Pursuant to

the Agreement, we acquired the ownership of the software “Netcafe Farmer” from

Mr. Liu Qian, including all the intellectual property and all its existing

business has been transferred to Shanghai MoqiZone. The total consideration paid

was RMB650,000 (or approximately US$95,000). By acquiring Netcafe Farmer, the

Company also recruited Mr. Liu Qian and his development team of 4 people. The

incremental salary is approximately $75,500 (RMB516,000) per annum. It is

expected that the income generated from existing Netcafe Farmer business will

substantially subsidize the monthly additional salary expenses.

Netcafe

Farmer is currently servicing approximately 700

internet cafés mainly in Henan, Hebei, Zhejiang, and Northeast of China and has

also established a strong network with major content suppliers to help promote

their games in internet cafés. As a result of the foregoing, we will be able to

bring tremendous synergy to the MoqiZone online game platform business and

improve our services to internet café operators. The existing brand name

“Netcafe Farmer” will be retained and a new version will be developed to support

the MoqiZone WiMAX Network. The acquisition of Netcafe Farmer will also allow us

to cover the internet cafés, which cannot be installed with our WiMAX equipment

due to physical limitation, via fixed line network. Internet cafes installed

with Netcafe Farmer will be able to enjoy the same products and services as

those that are installed with WiMAX equipment, although the revenue sharing will

be different.

Agreements

with Win’s

Entertainment Ltd.

We have

recently established partnership with Win’s Entertainment Limited (“Win’s”), a

major motion picture production company in Hong Kong through a series of

proprietary content agreements. In November 2009, we were contracted to develop

the online game for Win’s movie, Tiger Tang 2 (“Tiger Tang 2

Game”) and we also acquired the exclusive rights from Win’s for publishing Tiger

Tang 2 Game. We are also currently in discussion with Win’s to develop online

games for Win’s other movies as well as publish those games.

The

March 2010 Financing

We

completed a private equity financing of $1,956,200 on March 29, 2010, with 7

accredited investors. Net proceeds from the offering, were approximately

$1,760,400. Pursuant to the financing, we issued a total of 869,422 units of our

securities at $2.25 per unit. Each Unit consists of (i) one (1) share of the

Company’s Series C Convertible preferred stock, par value $0.001 per share,

convertible into one share of the Company’s common stock, par value $0.001 per

share , and (ii) a Series C Warrant and Series D Warrant, with the total amount

of Warrants of each Series exercisable to purchase that number of shares of

common stock as shall be equal to fifty percent (50%) of the number of Units

purchased in the Offering. Each of the Warrants has a term of three (3)

years.

In

connection with this financing, we paid cash compensation to a placement agent

in the amount of $195,620. Additionally, in connection with this financing, we

granted warrants to purchase up to 86,942 shares of common stock, Series C

Warrants to purchase up to 43,471 shares of common stock and Series D Warrants

to purchase 43,471 shares of common stock to the placement agent or its

designees. These warrants have the same terms as the warrants issued to

Investors that are included in the Units.

The

Securities in the Offering were issued pursuant to the exemption from the

registration provisions of the Securities Act of 1933 provided by Section 4(2),

therein, for issuances not involving a public offering.

Our

Corporate Structure

The

following table sets forth our current corporate structure.

5

3.5GMHz

Spectrum License

On

October 31, 2007, the PLA Resource Office granted to Tai Ji an

authorization (the “PLA Authorization”) for the exclusive use for commercial

purposes throughout China of the 3.5GHz radio frequencies belonging to the

PLA. On September 25, 2009, Tai Ji agreed to authorize SZ Alar

to use the PLA Authorization exclusively in the PRC for Internet café network

deployment purposes subject to payment of certain licensing fees. With the

3.5GHz, we can roll out our MoqiZone WiMAX Network to deliver online game

contents of our participating games through www.53mq.com to internet cafes which

have installed our WiMAX equipment. www.53mq.com is our gaming platform

designated to service the internet café customers. The MoqiZone WiMAX

Network also enables direct access between the internet cafes and the content

providers hosted by us at ICDs.

As a

result of the exclusivity granted by the PLA to Tai Ji and as a result of Tai Ji

granting us the exclusive usage of the 3.5GMHz radio frequency for Internet café

business, we believe that the Company is the only Chinese WiMAX carrier with

permitted national coverage license granted indirectly by the PLA to deploy a

network similar to the MoqiZone WiMAX Network. Such exclusivity, however, does

not extend to other potential competitors who may obtain WiMAX radio spectrum

via the MIIT as we are aware of other carriers who may have been granted similar

licenses by the MIIT. Nevertheless, we believe that the PLA

Authorization is the only national WiMAX license for the use of 3.5GMHz radio

frequencies granted by the PLA using the WiMAX

technology.

We are

not aware, however, that any of our potential competitors has any plans to

utilize a WiMAX platform to specifically target the Internet Café business, as

is our current plan. As a result, under our current arrangements, and as long as

the PLA Authorization granted to Tai Ji and its authorization to SZ Alar is

retained, we believe that no existing or potential competitor can foreclose our

access to any market in China for Internet cafés. Accordingly, we

believe that the Company has access to the necessary business and operating

licenses to deploy China’s first national WiMAX network for Internet

cafés.

6

The

advantages and disadvantages of PLA Authorization versus MIIT are summarized as

follows:-

|

a)

|

The license fees for 2009 were

RMB3 million (approximately $439,000) and the maximum annual license fees

are RMB7 million (approximately $1.024 million) per annum. This is

substantially less costly than the WiMAX license fees secured by other

telecom companies via MIIT, and as a result, the upfront capital

requirements are less than MITT WiMAX

;

|

|

|

b)

|

The PLA Authorization allows

national coverage subject to acknowledgement by local provincial military

zone. The tendering of MIIT WiMAX license provincial and each province

will only allow up to 3 companies to

participate;

|

|

|

c)

|

There was official documentation

regarding the tendering of China WiMAX frequency with the

MIIT. With this, the public or potential investor would be able

to verify the substance and approval information of the

licenses.

|

|

|

d)

|

The PLA has the right to control

the use of WiMAX frequency when there are threats to the country or

national crises and in such times this may cause the MoqiZone WiMAX

Network to not function

properly.

|

|

|

e)

|

PLA

Authorization allows automatic annual renewal but the MIIT WiMAX is only

valid for 2 years from the date of issuance. The risks of using the PLA

Authorization are further discussed at Page 15 Item 1A Risk

Factors

|

The

VIE

In July

2007, MoqiZone Hong Kong signed a Memorandum of Cooperation with Tai Ji and

SZ Mellow which also included a draft of Cooperation Agreement to be

entered into among Tai Ji, a WOFE to be established by MoqiZone and SZ

Mellow. According to this Memorandum of Cooperation, the major

terms are:

|

i.

|

Tai

Ji agreed that the MoqiZone Hong Kong can authorize its cooperative

partners or subsidiaries in China (“MoqiZone's Representatives”) to use

the 3.5GMHz radio frequency

resources;

|

|

ii.

|

Tai

Ji will collect an annual license fees of RMB 2,500,000 for Year

2008, RMB 3,000,000 for Year 2009 and thereafter, each year annual license

fee shall be increased by RMB 500,000 per year based on the previous year

annual license fee to a maximum of RMB 7,000,000 per year until the

license expires; and

|

|

iii.

|

Tai

Ji will further collect a usage fee of RMB 20,000 per year per radio base

station.

|

On

January 25, 2009 Shanghai MoqiZone was incorporated, and on January 26, 2009,

Shanghai MoqiZone, Tai Ji and SZ Mellow executed the formal Cooperation

Agreement, under which Tai Ji would provide SZ Mellow and Shanghai MoqiZone the

exclusive use of the 3.5GHz on Internet Cafes gaming business.

As a

result of disputes with the shareholders of Shenzhen Mellow (see below “Legal

Proceeding” for further information), on September 21, 2009, in accordance with

the terms of the SZ Mellow Agreements, we sent out a 30 days' prior written

notice to SZ Mellow stating our intention of terminating the SZ Mellow

Agreements. The SZ Mellow Agreements were terminated at the expiry of the

30-day notice on October 20, 2009. In order to continue our business and

operations as planned, on September 25, 2009, Shanghai MoqiZone, Tai Ji and

SZ Alar executed another Cooperation Agreement, under which Tai Ji will provide

SZ Alar and Shanghai MoqiZone the exclusive use of the 3.5GHz on Internet cafes

gaming business. Certain of our principal shareholders and executive officers

are also affiliated with Tai Ji and the SZ Alar.

Key

Advantages to the Moqizone WiMAX Network

According

to a report published by the CNNIC, the number of Internet users in China

reached 210 million as at December 31, 2007, of which an estimated 120 million

are unique online game players. On January 13, 2009, CNNIC released

the “23rd Statistical Survey Report on the Internet Development in China” in

Beijing. According to the report, by the end of 2008, the Internet penetration

rate of 22.6% in China had surpassed the global average level of 21.9% for the

first time. Meanwhile, the amount of Internet users in China had reached 298

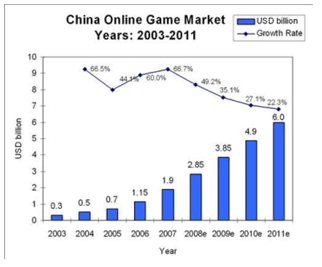

million, with 279 million broadband users. The report further states that the

industry is expected to have a compounded annual growth rate of 28.16% and grow

from $2.85 billion to approximately $6.0 billion by 2011. The top 25

Chinese games sold of $1.4 billion in prepaid cards in 2007 (Please refer to

http://www.cnnic.net.cn/uploadfiles/pdf/2009/11/24/110832.pdf

for the full cite information).

We

believe that our competitive advantages include:

|

i.

|

WiMAX First

Mover Advantage. Through

the PLA Authorization, we are able to invest in WiMAX base station and CPE

and install them more cost-effectively on roof tops of buildings in a way

similar to GSM radio stations. WiMAX is in particularly cost

effective for the “last mile” wireless internet connection. We are

primarily aiming to deliver online game contents of our participating

games to those internet cafes installed with our WiMAX equipment and which

have joined into our MoqiZone WiMAX

Network.

|

7

|

ii.

|

Reallocation

of Online Gaming Value Chain. The

MoqiZone WiMAX Network increases the net economic benefit to the content

providers and the Internet cafés and eliminates the prepaid card

distributors.

|

|

iii.

|

Other

Benefits to Internet Café s. The

MoqiZone WiMAX Network also benefits the Internet Café’s by eliminating

certain duplicative resources and costs and providing

incentives.

|

|

iv.

|

Benefits to

Content Providers. The MoqiZone WiMAX Network benefits

the Content Provider by eliminating server storage and bandwidth hosting

fees, and also protects their IP from piracy and hackers, via a closed

network.

|

|

v.

|

Benefits to

Game Publishers. With our Moqizone business model, game

companies can have one stop shopping with Moqizone and can access all the

Internet cafés at one location.

|

|

vi.

|

Benefits of

MoqiZone Prepaid Card. Our

platform uses a proprietary prepaid game card that is game publisher

agnostic (i.e. accessible for all games), thereby reducing game card

inventory costs for Internet café’s, as well as reducing black marketed

discounted prepaid cards and content theft for the Content

Provider.

|

|

vii.

|

Realtime

Reporting. Our solution shares valuable point of sale

(POS) data throughout the network to allow for real-time reporting,

customer and payment tracking, and targeted marketing; a service that was

previously unavailable to game content providers and publishers and

Internet cafés

|

|

viii.

|

Access to

Extensive Game Content. In addition to our current

arrangements, we expect to execute content agreements with the major

online gaming companies that represent more than 10 million unique

concurrent users.

|

|

ix.

|

Significant

Management Experience. Our management team has long term

business relationships and experience in dealing with the gaming companies

and also leading players in the entertainment industry, including movies

producers, music publishers and distributors of such content and we

believe that we will be able to obtain the best online digital content in

Asia.

|

Key

Corporate Objectives

Our key

business development objectives over the next two years are to build our game

delivery platforms and expand our business penetration in Internet cafes in

China.

|

i.

|

build

out our MoqiZone WiMAX Network, which involves the construction of a WiMAX

base station covering our targeted internet cafes at each

city;

|

|

ii.

|

install

CPE at each internet café;

|

|

iii.

|

set

up server farm in IDC;

|

|

iv.

|

develop

and deploy a online game content delivery platform;

and

|

|

v.

|

develop

and deploy a centralized prepaid card clearing center as well as a

accounting systems for internet cafes revenue distribution

system.

|

So far,

we have already signed up over 100 internet cafés in Chengdu of which 30

internet cafes are connected to our MoqiZone WiMAX Network. We have also

deployed our game delivery platform as well as our prepaid card clearing center

which is www.53mq.com and www.moqizone.com

respectively.

We are

also aiming to service the non-WiMAX internet café by providing them a peer to

peer content updating engine “Netcafe Farmer” which the Company has recently

acquired. Netcafe Farmer can be easily deployed to each internet café for

content updating and we now have approximately 700 internet café subscribed to

the Netcafe Farmer services. Revenue to be generated from Netcafe Farmer has not

been forecasted and projected in our financial budget. As of March 31, 2010, we

are testing the 2nd

generation of Netcafe Farmer which will further enhance stability and the peer

to peer connectivity between each PC as well as allowing a virtual storage for

games updating.

8

Our

business objectives will be required to execute through Shanghai Moqizone and SZ

Alar by implementing the structure portal arrangements described below in order

to allow MoqiZone Hong Kong to have control. Neither our Company nor our

Shanghai MoqiZone subsidiary owns any equity interests in SZ

Alar. Our business relationship withSZ Alar is based on contractual

arrangements which are commonly known as the “Sina Structure Portal Arrangement”

agreements. These agreements may be summarized, as

follows:

Exclusive

Business Cooperation Agreement. Pursuant to the exclusive ten

year business cooperation agreement between the SZ Alar and Shanghai MoqiZone,

Shanghai MoqiZone has the exclusive right to provide to SZ Alar comprehensive

technology and consulting services related to the business of SZ

Alar. In consideration for such services, Shanghai MoqiZone is

entitled to receive 100% of the net income of SZ Alar.

Equity Pledge

Agreement. Under the equity

pledge agreement among SZ Alar, the shareholders of t SZ Alar and Shanghai

MoqiZone, the shareholders of SZ Alar pledged all of their equity interests in

SZ Alar to Shanghai MoqiZone to guarantee SZ Alar’s performance of its

obligations under the exclusive business cooperation agreement. In the

event that SZ Alar were to breach its contractual obligations,

Shanghai MoqiZone, as pledgee, will be entitled to certain rights, including the

right to sell the pledged equity interests. The equity pledge agreement will

expire only after SZ Alar and its shareholders have fully performed their

respective obligations under the exclusive business cooperation

agreement.

Exclusive Option

Agreement. Under an exclusive ten (10) year option agreement

between SZ Alar, the shareholders of SZ Alar and Shanghai MoqiZone, the

shareholders of SZ Alar have irrevocably granted to Shanghai MoqiZone or its

designated person an exclusive option to purchase, to the extent permitted under

PRC law, all or part of the equity interests in SZ Alar for RMB10 or the

evaluation amount of consideration permitted by applicable PRC

law. Shanghai MoqiZone or its designated person has sole discretion

to decide when to exercise the option, whether in part or in full.

Loan

Agreement.

Under the loan agreement between the shareholders of the SZ Alar and

MoqiZone Hong Kong, the parties confirmed that MoqiZone Hong Kong has made an

interest-free loan to the shareholders of the SZ Alar solely to enable the

shareholders of the SZ Alar to fund the initial capitalization of SZ Alar. The

loan can be repaid only by sale of the shareholder’s equity interest in SZ Alar

to MoqiZone Hong Kong. The term of the loan agreement is ten years from the date

thereof.

Irrevocable Power

of Attorney.

The shareholders of SZ Alar have each executed an irrevocable power

of attorney to appoint Shanghai MoqiZone as their exclusive attorneys-in-fact to

vote on their behalf on all SZ Alar matters requiring shareholder

approval. The term of each power of attorney is valid so long as such

shareholder is a shareholder of SZ Alar.

We have

renewed our Memorandum of Understanding with the Beijing Internet Café

Association (“BICA”) on December 1, 2009. Our consultant Mr. Sun Qi is the newly

elected Chairman of the ICA in Beijing for the years 2009 - 2011. Our company

advisor is Madam Wu Yan, and she is also the immediate past Chairman of the

Beijing Internet Café Association. The major terms of the Memorandum of

Understanding are as follows:

|

a.

|

BICA

has a membership base of approximately 1500

members

|

|

b.

|

BICA

will support and promote the MoqiZone WiMAX Network andwww.53mq.com to

its member

|

|

c.

|

BICA

will allow us to promote our services and products at meetings of BICA to

its members

|

|

d.

|

The

term of the MOU shall be 3 years from December 1,

2009

|

There is

no financial obligation between both parties under the MOU which is

non-binding.

We are

also currently discussing various collaborations with the local internet café

associations in Suzhou and Chengdu in order to accelerate our internet café

business deployment.

Content

Providers

|

a.

|

Exclusivity

of the publishing rights to the online

game;

|

|

b.

|

Whether

it is a sole operation by us or a co-operation with the game

publisher;

|

|

c.

|

The

percentage of revenue split or percentage discount on the face value of

the gaming recharge card/prepaid card and payment

terms;

|

|

d.

|

The

territory that the publishing right

covers;

|

|

e.

|

The

term of the agreement;

|

|

f.

|

Any

upfront license fees or minimum guarantee on the amount of recharge

card/prepaid card; and

|

|

g.

|

Service

and technical support from the game

publisher.

|

9

As

abovementioned in Page 5, we have entered into partnership agreement with Win’s

and we are going to publish our own games on our gaming delivery platforms. We

aim to partnership with more movie production companies and replicate the

business model of publishing our own games on our platform.

Proprietary

Prepaid Card

Traditionally

online game revenues are collected through the sale of pre-paid cards issued by

each individual game publishing company, which they sell in both virtual and

physical form, to third party distributors and retailers, including Internet

cafes, as well as, to a lesser extent, through direct online payment systems. In

most cases, game publishers receive cash pre-payments from these parties in

exchange for delivery of the pre-paid cards. Online game companies do

not provide refunds to these distributors or retailers with respect to unsold

inventories of pre-paid cards.

Most

online game companies, especially new games, will encounter the problem that

they need to build “trust” with these distributors before their game is

launched. As a result, online game companies usually have

difficulties introducing their new products to distribution channels effectively

and efficiently. With our business model, these new game publishers

can join our payment system without being exposed to the risk of cash collection

from their distributers. At the same time, since our prepaid cards

can be used on other game, distributors have less financial risk exposure

stocking our cards.

For the

pay-to-play subscription-based model, both prepaid cards and prepaid online

points provide customers with a pre-specified length of game playing time within

a specified period. All prepaid fees received from distributors and end

customers are initially recognized as deposits. Revenue is recognized upon

activation of the prepaid game cards or online points based on the actual

consumption of the game playing time by end customers.

For the

item-billing revenue model, the customers can play the game for free with

limited basic functions. There are also in-game items and premium features sold

in the game by consuming online game points, commonly known as “Virtual Items”,

which are regarded as value-added services and are rendered over a pre-specified

period or throughout the whole game life. The revenue from these Virtual Items

is recognized ratably over the estimated practical usage period or

throughout the whole game life as appropriate. Future usage patterns may differ

from the historical usage patterns on which the item-billing revenue model

revenue recognition is based.

Virtual

item trading between gamers will also become more secure by using our card

together with an online payment system as we are operating under a “close”

network environment. Under the traditional web-based Internet gaming

environment, virtual item trading can become insecure as there could be

“pirated” gaming servers co-exist with the authenticated gaming servers and

such “pirated” server will disturb the regular gaming economies and induce

unfairness to players. Also, theft and virtual item robbery or disappearance is

not uncommon due to the existence of such “fake” and “pirated” servers. With our

MoqiZone WiMAX Network, we are hosting all gaming servers in CERNET IDC and as

our network is physically a private proprietary network, illegal hackers and

“pirated” server operators will find to more difficult to interfere our server

system, as a result of which providing a more secure environment to the

participants in the gaming value chain.

Our

Business Model Economics

The

following table compares the estimated and anticipated allocation of revenues

paid by online game players at Internet cafés who purchase prepaid game playing

cards under current arrangements in China and as expected commencing in 2009 and

thereafter from the use of the MoqiZone Network.

|

MoqiZone

|

Traditional Revenue

Model |

|||||||

|

Allocation of Revenues

|

Revenue Share

Percentage |

Revenue Share

Percentage |

||||||

|

Online

game software provider

|

25

|

%

|

20

|

%

|

||||

|

Online

game publisher

|

29

|

%

|

36

|

%

|

||||

|

Telecom

Internet data center

|

0

|

%

|

5

|

%

|

||||

|

Regional

prepay card distributor

|

0

|

%

|

8

|

%

|

||||

|

Inner-city

prepaid card distributor

|

0

|

%

|

8

|

%

|

||||

|

Regional

marketing and promotions

|

3

|

%

|

10

|

%

|

||||

|

Internet

café income

|

13

|

%

|

8

|

%

|

||||

|

MoqiZone

revenue retention

|

25

|

%

|

0

|

%

|

||||

|

Taxes

|

5

|

%

|

5

|

%

|

||||

|

Total

|

100

|

%

|

100

|

%

|

||||

Our

business will involve no charges to Internet cafés in China for all data

transmission via the MoqiZone Network at the very beginning. We

believe that this will provide a significant direct benefit to internet café

owners because Internet cafés currently pay internet data transmission charges

of approximately $1,450 (RMB10,000) to $2,900 (RMB20,000) per month to Telecom

providers. This is the single largest cost element for Internet café

operators in China after their rental fee.

China

currently has content censoring policy. Internet cafés are subject to

attack by hackers and other political news groups. Our MoqiZone

Network is able to provide them all the necessary tools to meet government’s

objectives. Also, as it is a closed network, they are not as vulnerable as they

would be outside of our network.

10

The

entire MoqiZone Network, whether with WiMAX or Netcafe Farmer, comes with a

POS-alike system for all online games. This system is similar to any

internet bank system, so that each game player, content provider, and Internet

café will be able to access online for their billing and profit sharing detail

similar to bank statements. This way each party will have an accurate

reporting on billing and profit sharing, in an easy to manage

manner.

Traditionally,

a content publisher will be required to host their content at Internet Data

Center (“IDC”) for server storage and bandwidth costs. This is one of

the highest expenses for publishing online game. The total cost

per month can be as high as 20% of their gaming revenue. The MoqiZone Network

eliminates the server and bandwidth costs for the content publishers as we will

be paying the IDC for the hosting fees. The reason we are able to offer this

business term to the content provider is that we do not have to bear the cost to

access the Internet as we have our own network to connect directly to all

Internet cafés. Also our MoqiZone Network infrastructure will allow

us to use fewer IDCs than the traditional Internet based online game

environment. Conventional IDC’s biggest cost is Internet bandwidth

costs. Therefore, we believe that we will be able to capture this

extra 20% of gaming revenue and pay IDC hosting costs for less than 1% for

physical floor area rental only.

One of

the current challenges for online game companies is to be able to control the

final retail price for their pre-pay cards and to prevent price variation from

parallel trading, even between province to province. As this product

has no differentiation from whom a game player buys it from, price cut strategy

is usually adopted by the “next-door” stores in order to sell as many cards

as possible. Therefore Internet café or grocery stores are currently

both unable to earn their “theoretical” profit margin for selling these prepaid

cards in stores. Our system is different, we only pay when a user

consumes the game at the café, then the café will get the commission regardless

where the end user purchased the pre-paid cards. Under this system, better

performing internet cafés are rewarded with bonuses so they have an incentive to

promote our system and encourage gamers to spend more to buy virtual items at

the café on our system.

We also

offer a profit sharing platform detailing all the transactions for game

companies so that they know exactly when and where their users spend the

money. Such information will be crucial for online game companies to

improve their service and marketing activity. Currently no telecom

company is able to provide such figure to online game companies. Game companies

also will be able to know the performance for their sponsored Internet

cafes.

Research

and Development

Our

recent research and development efforts have focused on the development of an

online e-payment system to manage profit sharing information among content

providers, internet cafés, and promoters. Game players also have

“pre-paid” accounts with MoqiZone. MoqiZone has total ownership over

the payment system. Although we do not have any proprietary

technology for WiMAX, we will integrate existing technology to manage our

network as required.

11

Customers

and Market Potential

There are

about 150,000 licensed internet café in China, with an average of 100 sets of PC

in each café. The top three applications in any internet café are:

(a) online games, (b) Instant messaging and online chatting; and (c) online

TV/Movie streaming. Each set of PC is shared by three users each day

in internet café, and this has covered 45 millions unique users per

day.

On

November 24, 2009, CNNIC published an analysis of the Chinese Online Gaming

market, called “China Online Game Market Research Report 20091” The

following is a summary of its major findings and the implications that we

believe they have on our business development in China.-

|

Report

Findings

|

Implications and Importance to our business evaluation

|

||

|

l

|

China

has 69.31 million online gamers, up 24.8% from 2008

|

Online

game is still a growing business in China

|

|

|

l

|

Large-scale

casual game and MMORPG (i.e. Massivs (Massivel) Multiplayer Online

Role-Playing Game) users account for 67.9% and 61% of the total

respectively, up 19.8% and 11% from the previous year, while 38.9% of

total users are female

|

Causal

game and MMORPG are still the major trend in China online games business.

This influence the selection of our gaming contents

|

|

|

l

|

Students

comprise 37.2% of online gamers, with 46.1% of the online gamers between

the ages of 10-19, the report said

|

The

demographic is important for marketing campaign planning

execution.

|

|

|

l

|

By

the end of June, 222 million of China's 338 million Internet users used

online video sites, up 23.8% year-on-year

|

Our

business intends to include other forms of digital entertainment contents

other than online gaming in the near future and the trend of such contents

is vital to our business planning

|

|

|

l

|

Home

use and internet cafe remain to be the major venues for online gaming, the

ratio of user is 79.7% and 59.6% respectively

|

Our

major business revenue will be generated from internet café and therefore

such statistic is important to our business evaluation.

|

|

|

l

|

The

value of Internet café sales channel increases gradually. Internet café

becomes the most important online game point cards selling point with

52.8% slightly higher than traditional convenience store.

|

Our

major business revenue will be generated from prepaid sold in internet

cafés and therefore such statistic is important to our

valuation.

|

|

|

l

|

Ratio

of internet café in Farming district is higher than those in major cities,

internet café users ratio in farming district is 69.4% higher than 57.9%

in major cities

|

Farming

districts will be the next great leap to our business development strategy

as the local GDP as the living standard gradually increases since the cost

of WiMAX deployment will be lower versus fixed line. The developed cities

in China will become saturated, although ARPU is still relatively higher

in the developed cities.

|

|

|

l

|

Internet

café monitor policy further strengthen, 46.4% teenage users choose

internet café for internet gaming, with 25.7% choose internet café as the

major online gaming location.

|

Our

MoqiZone WiMAX Network is a closed virtual private network and therefore

allows us to closely monitor any contents to be distributed to our

internet cafes, as a result, we can provide necessary information to the

relevant authorities on an as needed

basis.

|

1 Source:

CNNIC, China Internet Network Information Centre, http://www.cnnic.net.cn/uploadfiles/pdf/2009/11/24/110832.pdf

12

The

Growing Chinese Internet and Internet Café market

According

the New York Times2, the

number of Internet users in the China reached about 253 million in June 2008,

thereby, putting it ahead of the United States as the world’s biggest Internet

market. Reports from the government-controlled Chinese Academy of Sciences

indicated that the number of Internet users jumped more than 50 percent, or by

about 90 million people, during 2007. This new estimate represents only about 19

percent of China’s population, underscoring the potential for growth. The survey

found that nearly 70 percent of China’s Internet users were 30 or younger, and

that in the first half of this year, high school students were, by far, the

fastest-growing segment of new users, accounting for 39 million of the 43

million users during the period. According to the extract summary of

Niko Partners’ report on China ’ s Internet Café s Study 2008, there are

estimated 185,000 Internet cafés nationwide in China, 71,000 of which are

unlicensed with approximately 22 million PCs installed throughout China.

(http://www.nikopartners.com/press-release-china-internet-cafe-2008.asp)

According to public information

available from several NASDAQ and Hong Kong Stock Exchange listed online game

companies in China, the Average revenue per user per month (ARPU per month) for

each gamer in China is in the range of $5 to $40 per game depending on the

game. Item-Billing business model often leads to a higher ARPU

figures (please refer to online game publisher Giant, Nasdaq code: GA) This is

important to our business evaluation and forecast as it shows the consumption

behavior of games in China, most of gamers are willing to pay $5 to $40 for game

contents per month, we can use it as reference in setting our price strategy on

pre-paid cards.

Our

MoqiZone Network Deployment Strategy

The

following table sets forth our strategy for installing our MoqiZone WiMAX

Network and Netcafe Farmer throughout China over the next three

years. Our ability to achieve these goals is subject to receipt of

approximately $25.0 million in financing over such period, including the net

proceeds from the June 2009, August 2009 and March 2010 Financings.

|

Year

|

Cities

|

Cumulative

Internet Cafés

|

Cumulative

Cities

|

MoqiZone Network

coverage as a % of

total Internet Cafés

|

|||||||||

|

2010

|

Beijing,

Chengdu, Hangzhou, Nanjing, Suzhou, Chongqing, Yangzhou, Zhenjiang,

Jinhua, Ningbo, Kunming, Fuzhou, Xiamen, Qingdao, Jinan

|

11,400

|

15

|

7.5

|

%

|

||||||||

|

2011

|

Shanghai,

Guangzhou, Shenzhen, Zhuhai, Dongguan, Nanning, Hefei, Wuhu, Wuhan,

Changsha, Xian, Shijiazhuang, Shenyang, Dalian, Harbin, Guangzhou,

Wenzhou, Wuxi, Changshou, Nanchang, Lanzhou, Zhengzhou, Luoyang, Datong,

Hainan

|

20,206

|

40

|

13.5

|

%

|

||||||||

|

2012

|

Seven

cities per month

|

35,000

|

124

|

23.0

|

%

|

||||||||

Our cost

analysis indicates that it will cost approximately $400,000 to deploy our

MoqiZone Network system to service 100 Internet cafés. Estimated

costs per 100 Internet cafés include establishment of approximately 10 base

stations, installation of CPE receivers at each of the 100 Internet café

locations, purchase and installation of five content servers,

rental payment of Internet Data Center, implementation and maintenance

expenses. Our deployment process includes obtaining letters of intent from the

Internet cafés in any given city or area, GPS data collection,

determination of the required number and installation of base stations and

simultaneously setting up regional service centers, offices and

IDCs.

Once our

MoqiZone Network is established, a game player who purchases our prepaid card

from the Internet café can clicks on our logo, inputs his password, logs in to

his personal account and “clicks and plays.”

Competition

Although

we have no direct competitor using our WiMAX Network model, we will be competing

with some of the larger game providers in the PRC, most of which have

substantially greater revenues and financial resources than our

Company.

As some

of the functions in the current online game industry chain can be replaced by

our MoqiZone Network, we believe that certain parties who are currently

fulfilling certain functions in the online game value chain might be affected in

some ways.

2 “ China Surpasses U.S. in Number of

Internet Users” , 7/26/08 by David Barboza

13

Wholesale

distributors: Due to the large physical area of China, most online game

companies will appoint different levels of wholesale distributors to help them

to distribute their pre-paid cards to retailers and internet

café. They are usually required to stock the prepaid cards and make

advance payments to the online game companies. We believe our

business model will eliminate the need for our customers to do business with

some of these distributers by allowing us to work directly with internet

cafes. Although these distributors will continue to exist, we believe

that they will have only limited influence on our business. Major wholesale

distributors in China include: Junnet; www.untx.com; SIFANG TECHNOLOGY and

Federal Soft.

Last mile

internet connection providers (ADSL/T1): Our MoqiZone WiMAX Network

only connects internet cafés which are installed with our WiMAX equipment

wirelessly to access our online game contents hosted in our CERNET IDC. We will

divert some internet traffic for online games, and therefore internet cafés can

reduce their bandwidth requirement from their current telecom

providers. Internet cafés will still require Internet bandwidth

access for non-game functions such as Internet browsing, emails, other portal

access, or other web based function such as online chats as we are providing a

closed network environment and do not access the Internet (or world wide web).

The bandwidth demand, however, will become much lower. We assume that

broadband service provision to internet cafés generates a very small

business income for local telecom companies, and, as a result, it is very

unlikely that we will significantly affect their major revenue.

Employees

As of

December 31, 2009, we have 9 executive officers. We currently have a total of

37 paid employees comprising of the following:

|

Chief

Executive Officer

|

1

|

|||

|

Chief

Technology Officer

|

1

|

|||

|

Shanghai

Office Manager and Financial Controller

|

1

|

|||

|

Vice

Presidents (Finance, Sales and Marketing, Technology Development and

System Control)

|

4

|

|||

|

Product

Development Department

|

5

|

|||

|

Business

Development Department

|

1

|

|||

|

Marketing

and Promotion Department

|

2

|

|||

|

Internet

café Channel Development Department

|

7

|

|||

|

Software

Development, Technology and R&D Department

|

3

|

|||

|

Finance

Department

|

3

|

|||

|

Human

Resources and Administration Department

|

2

|

|||

|

Design

Department

|

2

|

|||

|

MIS

Department

|

1

|

|||

|

Customer

Services

|

2

|

|||

|

Consultant

|

2

|

|||

|

TOTAL

|

37

|

14

Investment

in our securities involves risk. You should carefully consider the risks we

describe below before deciding to invest. The market price of our securities

could decline due to any of these risks, in which case you could lose all or

part of your investment. In assessing these risks, you should also refer to the

other information included in this filing. You should pay particular attention

to the fact that a substantial amount of our operations in China are subject to

legal and regulatory environments that in many respects differ from that of the

United States. Our business, financial condition or results of operations could

be affected materially and adversely by any of the risks discussed below and any

others not foreseen. This discussion contains forward-looking

statements.

Risks

Related to Our Business and Industry

We

depend on the PLA’s approval and our cooperation relationship with Tai Ji

as low cost WiMAX network provider. The termination or

alteration of the PLA’s approval or the termination of our cooperation

relationship with Tai Ji would materially and adversely impact our business

operations and financial conditions.

Tai Ji

was authorized to exclusively use the 3.5GHz radio frequency resources by an

approval letter issued by the PLA Resource Office dated October 31, 2007 (“PLA

Approval Letter”). However, we cannot assure you that (i) the PLA

Resource Office or its higher authority will not revoke their approval by

issuing another letter; (ii) whether the PLA Resource Office has the authority

to grant an “exclusive” right to Tai Ji to use the 3.5GHz radio frequency

resources; (iii) whether the 3.5GHz radio frequency resources authorized by the

PLA Approval Letter can be widely used for commercial purpose. If the PLA

Approval Letter is revoked, the Company may be forced to purchase T1 ADSL

bandwidth from the incumbent telecom carriers, which will increase our

operational cost and materially and adversely impact our business operations and

financial conditions.

Notwithstanding

the Cooperation Agreement (see further below the discussion of “VIE” at Page 44)

among Tai Ji, SZ Alar and Shanghai MoqiZone and the fact that there are

common members among the management teams of the Company and Tai Ji, we cannot

assure you that (i) the cooperation relationship between Shanghai MoqiZone and

Tai Ji will be maintained, and (ii) the Cooperation Agreement will be fully

performed. In the event that Tai Ji breaches the Cooperation

Agreement, or we cannot get a renewal of the cooperation relationship

after it expires, we will not be able to use the 3.5GHz radio frequency

resources, which could cause significant disruptions to our business

operations or may materially adversely affect our business, financial

condition and results of operations.

Significant

changes in policies or guidelines of the PLA may result in lower revenue or

additional costs for us and materially adversely affect our financial condition

or results of operations.

It is

possible that the PLA will from time to time issue policies or guidelines,

requesting or stating its preference for certain actions to be taken by Tai Ji

using its networks, including changing the usable frequency from 3400-3430 MHz

and 3500-3530 MHz to other range. Due to our reliance on the PLA as low-cost

network resources provider, a significant change in its policies or guidelines

may have a material effect on us. Such change in policies or guidelines may

result in lower revenues or additional operating costs for us, and we cannot

assure you that our financial condition and results of operation will not be

materially adversely affected by any policy or guideline change by the PLA in

the future.

If

the PRC government believes that the agreements that establish the structure for

operating our business do not comply with PRC government restrictions on foreign

investment in the value-added telecommunications industry, we could be subject

to severe penalties.

In

December 2001, in order to comply with China’s commitments with respect to its

entry into the World Trade Organization, or WTO, the State Council promulgated

the Administrative Rules for Foreign Investments in Telecommunications

Enterprises, or the Telecom FIE Rules. The Telecom FIE Rules set forth detailed

requirements with respect to capitalization, investor qualifications and

application procedures in connection with the establishment of a

foreign-invested telecommunications enterprise. Pursuant to the Telecom FIE

Rules, the ultimate ownership interest of a foreign investor in a foreign-funded

telecommunications enterprise that provides value-added telecommunication

services, shall not exceed 50%.

We

(including Shanghai MoqiZone), are considered as foreign persons or

foreign-invested enterprises under PRC laws. As a result, we operate our

wireless value-added services in China through the VIE, which is owned by PRC

citizens. We do not have any direct equity interest in the operating company but

instead, the Company will only share its economic benefits derived through

contractual arrangements, including agreements on provision of services, license

of intellectual property, and certain corporate governance and shareholder

rights matters. The VIE conducts portion of our operations and generates portion

of our revenues. It also holds the licenses (including the Content Provider

License) and approvals that are essential to our business.

There are

substantial uncertainties regarding the interpretation and application of

current or future PRC laws and regulations, including but not limited to the

laws and regulations governing the validity and enforcement of our contractual

arrangements. Accordingly, we cannot assure you that PRC regulatory authorities

will not determine that our contractual arrangements with the VIE violate PRC

laws or regulations.

If we or

our operating company were found to violate any existing or future PRC laws or

regulations, the relevant regulatory authorities would have broad discretion in

dealing with such violation, including, without limitation, the

following:

15

|

(a)

|

levying

fines;

|

|

(b)

|

confiscating

our or our operating company’s

income;

|

|

(c)

|

revoking

our or our operating company’s business licenses and other operating

licenses;

|

|

(d)

|

shutting

down the servers or blocking our or our operating company’s web

sites;

|

|

(e)

|

restricting

or prohibiting our use of the proceeds from this offering to finance our

business and operations in China;

|

|

(f)

|

requiring

us to restructure our ownership structure or operations;

and/or

|

|

(g)

|

requiring

us or our operating company to discontinue our wireless value-added

services business.

|

Any of

these or similar actions could cause significant disruptions to our business

operations or render us unable to conduct our business operations and may

materially adversely affect our business, financial condition and results of

operations.

Our

contractual arrangement with the VIE and their shareholders may not be as

effective in providing operational control as direct ownership of these

businesses and may be difficult to enforce. We were not able to maintain

operational control of SZ Mellow under prior agreements.

PRC laws

and regulations currently restrict foreign ownership of companies that provide

value-added telecommunication services, which include wireless value-added

services and Internet content services. As a result, we conduct a portion of our

operations and could generate revenues through the VIE pursuant to a series of

contractual arrangements with it and its respective shareholders. These

agreements may not be as effective in providing control over our operations as

direct ownership of these businesses. Direct ownership would allow us, for

example, to directly exercise our rights as a shareholder to effect changes in

the board of the VIE, which, in turn, could affect changes, subject to any

applicable fiduciary obligations, at the management level. However, under the

current contractual arrangements, as a legal matter, if the VIE or its

shareholders fail to perform their respective obligations under these

contractual arrangements, we may have to incur substantial costs and expend

significant resources to enforce those arrangements, and rely on legal remedies

under PRC law. These remedies may include seeking specific performance or

injunctive relief, and claiming damages, any of which may not be effective. For

example, if the VIE’s shareholders refuse to transfer their equity interest in

the VIE to us or our designee when we exercise the purchase option pursuant to

these contractual arrangements, or if any of those individuals otherwise act in

bad faith towards us, we may have to take legal action to compel them to fulfill

their contractual obligations. This was the case with regard to the shareholders

of SZ Mellow. When these persons refused to cooperate with our

management with regard to the use and operation of SZ Mellow’s ISP license, we

were forced to hire PRC litigation counsel to terminate the agreements with SZ

Mellow. Additionally, we were forced to seek out a new VIE company in

order to continue to operate our business as planned. Although we

were able to enter into new agreements with SZ Alar and, as a result, our

dispute with the owners of SZ Mellow did not materially disrupt our business, we

cannot guarantee that we will not have similar problems with SZ Alar in the

future or that we will be able to prevent further disruption to our business and

operations as a result.

Additionally,

all of these contractual arrangements are governed by PRC laws and provide for

the resolution of disputes through arbitration in the PRC. Accordingly, these

contracts would be interpreted in accordance with PRC laws and any disputes

would be resolved in accordance with PRC legal procedures. The legal environment

in the PRC is not as developed as in other jurisdictions, such as the United

States. As a result, uncertainties in the PRC legal system could limit our

ability to enforce these contractual arrangements. In the event we are unable to

enforce these contractual arrangements, which relate to critical aspects of our

operations, we may be unable to exert effective control over the VIE and our

ability to conduct our business may be negatively affected.

If we are unable to get additional

online games that are attractive to players and result in overall revenue

growth, our business, financial condition and results of operations may be

materially and adversely affected and our ability to recover related costs may

become limited .

In order

to maintain our long-term profitability and financial and operational success,

we must continually get new online games that are attractive to players. To

date, we have signed up 4 online game companies with approximately 30 games.

These games may or may not attract players away from other games companies and

may or may not be profitable or popular among the online game players in China.

If these games fail to attract new players and fail to drive our online game

revenues, our business, financial condition and results of operations may be

materially and adversely affected.

Our

ability to purchase or license successful online games will depend on their

availability at acceptable terms, including price, our ability to compete

effectively against other potential purchasers or licensees to attract the

developers of these games, and our ability to obtain government approvals

required for the purchase or licensing and operation of these

games.

The games

that we purchase or license may not be attractive to players, may be viewed by

the regulatory authorities as not complying with content restrictions, may not

be launched as scheduled or may not compete effectively with our competitors’

games. Additionally, new technologies in our competitors’ online game

programming or operations could render our games obsolete or unattractive to

players, thereby limiting our ability to recover related product development

costs, purchase costs and licensing fees. If we are not able to develop,

purchase or license successfully online games appealing to players, our future

profitability and growth prospects will decline.

16

Our

limited operating history and the unproven long-term potential of our business