Attached files

| file | filename |

|---|---|

| EX-23.1 - EXHIBIT 23.1 - HELICOS BIOSCIENCES CORP | a2198049zex-23_1.htm |

| EX-31.2 - EXHIBIT 31.2 - HELICOS BIOSCIENCES CORP | a2198049zex-31_2.htm |

| EX-32.1 - EXHIBIT 32.1 - HELICOS BIOSCIENCES CORP | a2198049zex-32_1.htm |

| EX-31.1 - EXHIBIT 31.1 - HELICOS BIOSCIENCES CORP | a2198049zex-31_1.htm |

| EX-10.43 - EXHIBIT 10.43 - HELICOS BIOSCIENCES CORP | a2198049zex-10_43.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| (Mark One) | ||

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2009 |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

COMMISSION FILE NUMBER 001-33484 |

||

HELICOS BIOSCIENCES CORPORATION

(Exact name of registrant as specified in its charter)

| DELAWARE | 05-0587367 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

One Kendall Square Building 700 Cambridge, Massachusetts (Address of principal executive offices) |

02139 (Zip Code) |

|

Registrant's telephone number, including area code: (617) 264-1800 |

||

Securities registered pursuant to Section 12(b) of the Act: |

||

Title of each class |

Name of each exchange on which registered |

|

| Common Stock, $0.001 par value | The NASDAQ Global Market | |

Securities registered pursuant to Section 12(g) of the Act: None |

||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company ý |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of the registrant's Common Stock held beneficially or of record by stockholders who are not affiliates of the registrant, based upon the closing price of the Common Stock on June 30, 2009, as reported by the NASDAQ Global Market, was approximately $7,736,729. For the purposes hereof, "affiliates" include all executive officers and directors of the registrant.

As of March 31, 2010, the Company had 79,456,334 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

HELICOS BIOSCIENCES CORPORATION (a development stage company)

FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2009

TABLE OF CONTENTS

2

OVERVIEW

Helicos BioSciences Corporation is a life sciences company which has developed proprietary technology focused on the research, drug discovery and clinical diagnostics markets. Our proprietary True Single Molecule Sequencing (tSMS)™ technology enables rapid analysis of large quantities of genetic material by directly sequencing single molecules of DNA or single DNA copies of RNA (cDNA) and our newest approach of direct sequencing of RNA. Our tSMS approach differs from current methods of sequencing DNA or RNA because it analyzes individual molecules of DNA directly instead of analyzing a large number of copies of the molecule produced through complex sample preparation techniques. Our tSMS technology eliminates the need for costly, labor-intensive and time-consuming sample preparation techniques, such as amplification or cloning, which are required by other methods to produce a sufficient quantity of genetic material for analysis.

Our Helicos® Genetic Analysis Platform is designed to obtain sequencing information by repetitively performing a cycle of biochemical reactions on individual DNA or RNA molecules and imaging the results after each cycle. The platform consists of an instrument called the HeliScope™ Single Molecule Sequencer, an image analysis computer tower called the HeliScope™ Analysis Engine, associated reagents, which are chemicals used in the sequencing process, and disposable supplies. The information generated from using our tSMS products may lead to improved drug therapies, personalized medical treatments and more accurate diagnostics for cancer and other diseases.

In the first quarter of 2010, we began a process of considering alternatives to our existing long-term strategic focus, including a repositioning of the company in the genetic analysis markets. We believe that an adjustment to our existing strategy would better position us to take advantage of the unique capabilities of our proprietary platform and to address the growing competition in the genetic research marketplace. Although we made progress during 2009 in the genetic research market as demonstrated by our growing installed base and the number of peer reviewed publications referencing our single molecule sequencing technology, we believe that Helicos must consider a number of alternatives to improving shareholder value and, as a result, have embarked upon this process with a view toward repositioning Helicos' highly differentiated single molecule sequencing solution. In this regard, we have continued our relationship with Thomas Weisel Partners LLC (TWP), a nationally recognized investment bank, to assist us with our evaluation and execution of strategic alternatives and long term financing strategy. We have also engaged a variety of consultants in the genomic research, services and diagnostics industries to evaluate available alternatives.

In particular, we believe that Helicos' technology is well suited for applications in molecular diagnostics. We believe that diagnostics applications may benefit from the specific features for which the Helicos System is uniquely suited, including the platform's quantitative accuracy, the use of small sample quantities in simple preparation methods, and high throughput, as well as lack of biases typically seen with sample amplification.

We anticipate the repositioning evaluation process will take at least several months. There can be no assurance, however, that we will be successful in re-focusing our long-term strategy or that any transaction we undertake to implement a change in strategy will ultimately be completed or, if one is undertaken, there can be no assurance regarding its terms, timing or sources of funding. During this time, we will focus our limited resources on satisfying current customer needs and stabilizing system performance, which has varied at some customer and placement sites. In addition, new initiatives will be prioritized to those that reduce operational risk and conserve resources while we consider our strategic alternatives and direction.

3

BACKGROUND ON DNA STRUCTURE AND FUNCTION

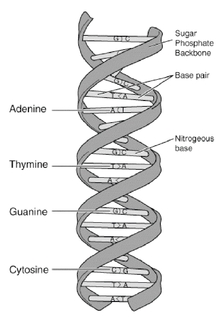

The genetic program that controls a living cell is encoded in its DNA. The diagram below shows the typical double-helix structure of DNA. The two strands are made of subunits called nucleotides, each of which contains a phosphate, a sugar and a side-chain called a base. The phosphates and sugars form the backbone of the polymer, and the bases face each other. The letters A, G, T and C represent the four types of nucleotide bases: adenine, guanine, thymine and cytosine.

The bases align with each other in a complementary structure held together by hydrogen bonds. A "T" on one strand always bonds with an "A" on the other strand, and a "G" on one strand always bonds with a "C" on the other strand. This bonding between DNA strands is called hybridization, and the resulting structure is called a base pair. The genome of an organism is a complete DNA sequence of that organism. The human genome contains about three billion base pairs of DNA, which is represented twice in each cell. In a human, the individual acquires one version of the genome from the mother and one version from the father. |

|

The human genome includes approximately 30,000 genes. Genes are segments of DNA that contain the information needed for a cell to make proteins. Each gene has one or more parts called exons including coding regions that specify the sequence of amino acids for that protein. Genes also contain regulatory elements that determine when, where and how much protein is made. While it is currently understood that approximately 97% of the human genome does not code for proteins, recent research suggests that this non-coding DNA also contains important regulatory elements which plays an important role in controlling when and how much genes are expressed. In addition, new knowledge reveals a wealth of information in the transcribed regions of the genome that do not make up protein coding genes but yet these non-coding RNAs are becoming increasingly important in the study of biology.

The process of making proteins using the information in DNA involves a process called gene expression. To express a gene, enzymes called RNA polymerases transcribe the coding region into molecules of messenger RNA, or mRNA. The mRNA moves from the nucleus into the cytoplasm, where the cell's protein synthesis machinery translates the genetic sequence information and assembles a chain of amino acids into a protein.

GENETIC ANALYSIS INDUSTRY OVERVIEW

Genomic information has become a critical tool to understanding the mechanics of life, the environmental effect on biological systems, diagnosis of disease and treatment of disease. Life science tools that analyze genomic material have provided tremendous insights into the complexity and variability of the genome and have changed the methods and strategies by which scientists conduct their research. Genomic information enables the possibility and promise of personalized medicine and should

4

bring forth a new era in patient knowledge whereby individuals now can have access to their own genetic information to make informed decisions concerning the prevention and treatment of disease.

Since the development of genetic engineering techniques in the 1970s, the analysis of genetic material has become a mainstay of biological research. The first automated DNA sequencer was invented in 1986, based on technology developed by Frederick Sanger and his colleagues in 1975, which is commonly referred to as Sanger sequencing. Subsequent versions of commercial DNA sequencers have increased the speed of DNA sequencing by 3,000 fold, making possible the Human Genome Project. In 1996 the first commercial microarray was introduced and enabled a new era of RNA analysis by measuring gene expression across many genes in a single experiment. Subsequent versions of the commercial microarrays including DNA and RNA have significantly increased the amount of information per run and provided selected single nucleotide polymorphisms, or SNPs of the whole human genome on a single chip, enabled large scale genome-wide SNP association studies and have been commercialized for several diagnostic applications. Since 2007 there has been significant replacement of both of these existing genetic analysis technologies with 1st and 2nd Next Generation Sequencers (NGS). Today, manufacturers of systems, supplies and reagents for performing genetic analysis, which includes DNA sequencing, genotyping, and gene expression analysis, serve a worldwide market of approximately $5 billion, according to Strategic Directions International with an estimate that DNA sequencing serves approximately $1 billion of this demand for genetic analysis. The remainder of this market is addressed by other genetic analysis methods, such as gene expression analysis and genotyping. Recent studies have demonstrated the complexity and variability of the human genome. This new information will necessitate larger scale studies, and require new methods and strategies that combine different application and data analysis techniques across these larger studies. Since 2007 the market has migrated away from Sanger methods of DNA and RNA sequencing and microarray based technologies because of their inherent technology limitations in throughput, cost and complexity of sample preparation. It is estimated that approximately 30% of the Sanger sequencing systems have been replaced by 1st and 2nd NGS systems.

To explore the next frontier of biomedical research, scientists must design comprehensive experiments on a larger scale than previously thought possible. Current methods of genetic analysis include DNA sequencing, gene expression analysis, genotyping and epigenetics. Until the advent of NGS technologies, researchers were required to use several different platform types each with its own unique sample preparation and data analysis formats. DNA and RNA sequencing provide the most comprehensive genome-wide information without any prior knowledge of the sequence or sequence variation; however, the limitations of Sanger sequencing technologies restrict their use in large-scale studies and as a replacement for multiple technologies. Whole genome scale projects were generally out of the reach of the individual user and were in the exclusive domain of large multi-instrument sequencing centers because of the inherent limitations of low throughput, high cost and complexity of use.

In response to these limitations, next generation sequencing technologies are seeking to improve the speed and reduce the per base cost of sequencing. However, these technologies continue to be limited by their sensitivity to the need for amplification or cloning to obtain enough DNA or RNA from a sample for their instruments to adequately read the sequence. As with Sanger-based sequencing technologies, this requirement for amplification or cloning adds to the cost and complexity of these sequencing methods, limits the scalability of sample preparation and may limit the accuracy of the data they produce. Moreover, many 1st and 2nd NGS technologies appear to possess biases and are hampered by their lack of quantitative accuracy which may limit their applicability to the broader genetic analysis space.

In the past, the prohibitive cost of high-volume sequencing at the genome scale has caused scientists to use other genetic analysis technologies to examine discrete aspects of gene structure or function. For example, researchers use gene expression analysis to compare amounts of mRNA made

5

from different genes, and genotyping to examine specific gene segments known to contain sequence variations, called single nucleotide polymorphisms, or SNPs. Technologies available for gene expression analysis and genotyping include:

- •

- chip- or bead-based microarrays, in which collections of short DNA molecules are attached to the

surface of a glass chip or to beads and used to determine the identity and abundance of particular DNA or RNA molecules in a sample; and

- •

- real-time PCR, also called RT-PCR, which is the method of biochemically copying or amplifying the DNA in a sample through a process called PCR in which the identity and quantity of amplified DNA from the sample is measured as the analysis is performed.

While these other genetic analysis technologies address the cost limitations of DNA and RNA sequencing, they generally provide only limited information and suffer from a range of technical limitations, the most important of which is the high cost of replacement as new sequence information is added and products are updated. NGS technologies that enable a broad range of applications with a relatively similar sample preparation methodology and data analysis format would greatly enable the ability to perform both broad and deep studies of important biological samples. NGS technologies that do not require significant investments in up front automation and infrastructure would also allow large scale studies to be performed in mid to small sized laboratories as well as diagnostic laboratories by allowing continuous use of the same capital equipment for each of the different genetic analysis applications.

The scope and pace of much important research, and the routine application of genomic information in clinical medicine, remain limited by the cost and throughput of the currently available genomic analysis systems. Efforts to overcome this barrier are endorsed by the National Institutes of Health, whose National Human Genome Research Institute established the "Revolutionary Genome Sequencing Technologies—The $1,000 Genome," grant program to fund researchers' efforts to develop technology to enable the complete sequencing of an individual human genome at a cost of approximately $1,000. This goal is measured by the cost of the consumables used in the sequencing of the human genome and without regard to the cost of the sequencing instrument. In September 2006, we received a $2 million grant under this program to foster our technology development on the path to the $1,000 genome. In September 2009, we were awarded a $2.9 million grant as part of the Sequencing Technology Development Program representing NHGRI's Signature Project for the American Recovery and Reinvestment Act. This project was specifically designed to support large-scale, high impact research projects that are expected to accelerate critical scientific breakthroughs and enable growth and investment in biomedical research. In addition, in April 2010, we were awarded a $1.5 million grant from the National Institutes of Health in support of our project titled "True Direct Single Molecule RNA Sequencing."

Scientists have long realized that many of the disadvantages of ensemble based sequencing could be addressed through the direct sequencing of single molecules. This ability to directly measure individual sequences would reduce the cost and complexity of large scale experiments while increasing sensitivity. The simplicity of the sample preparation and detection would also provide the capability to combine multiple application techniques in order to get the most comprehensive view of each sample. For nearly 20 years, researchers have attempted without success to develop such a single molecule sequencing technology. Past efforts fell short largely due to complexity or technological hurdles in signal detection, surface materials, biochemistry, enzymology, bioinformatics, automation or engineering. In 2003, one of our co-founders, Stephen R. Quake, DPhil, demonstrated, we believe for the first time, that sequence information could be obtained from single molecules of DNA. We have replicated and improved upon Professor Quake's approach to develop our True Single Molecule Sequencing (tSMS)TM technology. (Harris T et al. Single Molecule DNA Sequencing of a Viral Genome. Science. Vol. 320, no. 5872, pp. 106-109. 2008.)

6

HELICOS TECHNOLOGY

Our True Single Molecule Sequencing (tSMS)TM technology is a powerful approach that directly measures single molecules. This novel approach allows our system to directly analyze billions of individual sequences in parallel and avoids the need for complex sample preparation techniques, amplification or cloning required by other methods. Our products utilizing our tSMS technology benefit from simple, scalable sample preparation techniques and automated high-throughput sequencing processes that enable sequencing with speed and provide unprecedented sensitivity and quantitative accuracy. This technology provides scientists and clinicians with extensive capabilities for basic and translational research, for pharmaceutical research and development, and for the development and clinical application of genomic diagnostics.

Our Helicos® Genetic Analysis System is designed to provide the following benefits:

- •

- Enhanced throughput. Scientists measure the throughput of

a DNA sequencing technology based on the number of bases analyzed per unit of time. By the end of 2009, the HeliScopeTM Single Molecule Sequencer had achieved throughput rates of

approximately 180 million analyzable bases per hour, depending on the application. In addition, we have designed the imaging capability of the HeliScope Sequencer to accommodate a maximum

throughput approaching one billion bases per hour. To achieve this additional increase in throughput, we would need to improve the efficiency and accuracy of the system's sequencing chemistry,

increase the density of strands of DNA that bind to the surface of the flow cell in which the sequencing reactions take place and make corresponding enhancements to the image processing software.

- •

- Simplicity. Because the sample preparation process for

genome sequencing using our HeliScope Sequencer involves only small quantities of reagents and a few simple steps, we believe that it will be less costly, less time-consuming, less error

prone, and require lower amounts of starting material (without amplification) than the sample preparation processes used in current NGS technologies.

- •

- Scalability. The sample preparation process is highly scalable because it does not require the need for the costly automation of complex sample preparation techniques, amplification or cloning required by existing NGS methods and thus makes genomic scale studies possible in small to mid-sized research organizations.

We believe that our Helicos System can be used as a universal method of genetic analysis potentially replacing existing methods of gene expression analysis and genotyping. Based on its anticipated performance, we believe that the Helicos System is capable of performing applications of gene expression analysis at a comparable cost per sample, and in the case of high volume analyses, at lower cost, in comparison with current technologies. Moreover, we believe that performing expression analysis using the tSMS approach provides a more unbiased and accurate measurement of expression. In addition, as we consider our repositioning strategy, we believe that Helicos' technology is uniquely suited for applications in molecular diagnostics. In particular, we believe that our platform's quantitative accuracy, the use of small sample quantities in simple preparation methods, and high throughput, as well as lack of biases typically seen with sample amplification, can be specially useful in the field of molecular diagnostics.

7

Our True Single Molecule Sequencing (tSMS)tm Technology

Our True Single Molecule Sequencing (tSMS)tm technology enables the simultaneous sequencing of large numbers of strands of single DNA molecules. The first step of our single molecule sequencing approach is to cut, or shear, a sample of DNA or RNA into relatively small fragments. The double helix of each fragment is then separated into its two complementary strands. Each strand is used as a template for synthesis of a new complementary strand. This is accomplished through a series of biochemical reactions in which each of the four bases are successively introduced. If the introduced base is complementary to the next base in the template, it will be added to the new strand. Each of the added bases is tagged with a fluorescent dye, which is illuminated, imaged and then removed. The sequence of each new DNA or RNA strand is determined by collating the images of the illuminated bases from each cycle of highly specific incorporation and imaging. The raw sequencing data is then analyzed by computer algorithms. In 2009, our scientists authored or co-authored five scientific manuscripts based on our tSMS technology in several peer-reviewed journals.

The series of figures below outlines an example of how our tSMS technology operates to sequence single molecules from genomic DNA. The actual process our HeliScopetm Single Molecule Sequencer will utilize to sequence DNA molecules will depend on the application. In September of 2009 we published the first demonstration of the direct sequencing of RNA molecules which enables additional potentially significant areas of research.

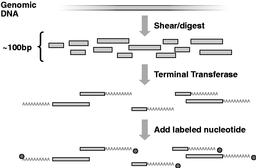

Figure 1 To prepare the sample for sequencing, the genomic DNA is first cut into small pieces of about 100 bases. The enzyme called terminal transferase is then used to add a string of "A" nucleotides to one end of each strand. Then, a nucleotide labeled with a single fluorescent dye molecule is added to the end of the strand. |

|

|

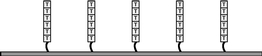

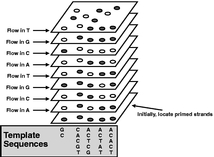

Figure 2 Inside the flow cell, short strands of "T" nucleotides, called primers, have already been attached to the surface. |

|

|

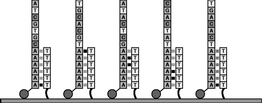

Figure 3 When the DNA sample is added, the strings of "As" on each DNA strand hybridize with the strands of "Ts" on the surface, anchoring the sample strands to be sequenced. The sample strands will act as a template and the strand of Ts as a "primer" for DNA synthesis. A laser subsystem illuminates the flow cell and the camera records the location of each captured sample strand. A mechanical stage moves the flow cell in sequential steps to allow the camera to image the entire active area of the flow cell. The dye molecules are then cleaved and washed away. |

|

8

Figure 4 An enzyme called DNA polymerase and the first of the four types of our proprietary fluorescently labeled nucleotides are added. If the nucleotide is complementary to the next base in the template strand, the polymerase will add it to the primer strand. The nucleotides are designed to inhibit the polymerase from incorporating more than one base at a time on the same strand. Excess polymerase and unincorporated nucleotides are then washed away. |

|

|

Figure 5 The laser subsystem illuminates the flow cell and the camera records the locations where fluorescently labeled nucleotides were added. The fluorescent dye molecules are then cleaved from the labeled nucleotides and washed away. |

|

|

Figure 6 The process outlined in Figures 4 and 5 is repeated with each of the four types of labeled nucleotides. Repeating this cycle for a total of 120 times adds an average of more than 33-35 nucleotides to the primer strand. The number of bases added to a primer is the "read length." |

|

|

Figure 7 The system's computer analyzes the series of images from each cycle and determines the sequence of bases in the template strand. The sequence is "read" by correlating the position of a fluorescent molecule in its vertical track with the knowledge of which base was added at that cycle. Finally, the sequence data is exported to another computer system for further analysis depending on the application. |

|

The Helicos® Genetic Analysis Platform

The Helicos® Genetic Analysis Platform consists of the following components:

- •

- Helicos® Genetic Analysis System—The instrument

component of the Helicos Genetic Analysis Platform which consists of three major components:

- •

- The HeliScope™ Single Molecule Sequencer which performs the True Single Molecule Sequencing (tSMS)™ chemistry and directly analyzes images of single molecules, producing accurate sequences of billions of templates at a time. The HeliScope Sequencer consists of a high-speed mechanical stage and a laser illumination subsystem, an image acquisition subsystem, a fluid handling subsystem and computer subsystems that control and analyze the

9

- •

- HeliScope™ Analysis Engine provides computing power for near

real-time image analysis and on-board data storage. The on-board data storage is appropriately sized to support two complete runs, enabling flexibility of operation

and maximizing uptime. The Analysis Engine operates downstream from the HeliScope™ Sequencer in the data pipeline. It consists of the System Server, Object Finders, and an uninterruptible

power supply (UPS). Components are mounted in a single enclosure for locating convenience and installation ease. Data communication between the HeliScope Sequencer and Analysis Engine is accomplished

across Gigabit Ethernet (GigE) lines, providing high reliability and allowing for considerable physical distance between components.

- •

- HeliScope™ Sample Loader facilitates and speeds the loading of

samples into the Helicos® flow cells. It provides 25 discreet loading ports to ensure proper separation of samples and ease of loading.

- •

- Helicos® True Single Molecule Sequencing (tSMS)™ Reagent Kits. Reagent kits for sequencing which consist of proprietary formulations of a DNA polymerase enzyme, our proprietary fluorescently tagged bases, our proprietary imaging reagent, a proprietary formulation of a cleavage reagent and our proprietary application specific flow cells that have a proprietary surface coating with the chemical and optical properties needed for single molecule sequencing.

sequencing reactions. To operate the instrument, a user loads a prepared sample of DNA, complementary DNA (cDNA) or RNA onto our flow cell using the HeliScopeTM Sample Loader, places the flow cell on the mechanical stage and inserts our consumable reagent pack into the fluid handling system. From that point onward, all sequencing reactions are conducted automatically by the instrument. After each base is added, the mechanical stage moves the flow cells under a microscope lens. Four lasers illuminate the fluorescent tags of the bases, and a camera images the flow cells through the microscope lens.

Consumable reagents. The biochemical sequencing reactions that occur in the HeliScope Sequencer involve the use of a proprietary formulation of a DNA polymerase enzyme, proprietary fluorescently tagged bases and proprietary imaging reagents. We have developed proprietary nucleotide triphosphates, called Virtual TerminatorTM Nucleotides, that allow us to add only one base at a time to each DNA strand. Our proprietary imaging reagents improve the stability of our fluorescent tags and increase their brightness. Our cleavage reagents are used to remove the fluorescent tags from the Virtual Terminators nucleotides.

Disposable supplies. The HeliScopeTM Single Molecule Sequencer is designed to perform sequencing reactions inside one or two glass flow cells. When two flow cells are used, the system alternates between the flow cells, performing sequencing reactions in one flow cell while recording images from the other. Each flow cell has an active area of about 16 square centimeters and contains 25 separate channels. Our flow cells are designed to allow researchers to sequence separate samples in each channel, which will enable the simultaneous sequencing of at least 50 different DNA, cDNA or RNA samples. The initial version of our flow cell is designed to permit binding of DNA strands at an average density of approximately 100 million strands of DNA per square centimeter, equaling an average of approximately 2.8 billion strands of DNA for both flow cells. In the first quarter of 2010, we announced the availability of a series of new reagent kits and run configurations that allow customers to choose the use of 1 or 2 flow cells and between 1 and 50 channels, adjust the number of strands of DNA imaged, and select run times between 2.5 and 8 days.

10

APPLICATIONS

The Helicos® Genetic Analysis System provides new opportunities for large scale genomic studies which encompass many areas of research, development and diagnostic use The areas where we believe Helicos' technology offers significant opportunities include:

- •

- Studying the Human Genome. The ENCODE studies published in

2007 and 2008 provided new insights into the complexity of the human genome. These initial studies published in 2007, which examined only 1% of the genome architecture revealed a much more dynamic and

complex genome state at every level including organization, sequence, expression and regulation. New approaches which allow a window into the genome allowing unbiased interrogation are clearly

required to fully understand the genome. During 2008, we saw the emergence of next generation sequencing technology applied to a fuller understanding of the genome with particular emphasis focused on

the transcriptome. Through deep resequencing of the transcriptome, we are gaining new insights in the truly remarkable resilience of the genome and the variety of coding and non-coding

RNAs playing intimate roles in gene regulation. During 2008 and 2009 several publications of complete human genome sequences have demonstrated levels of human genome variation far exceeding initial

expectations. During 2009, full genome sequencing focused on decoding tumor genomes and uncovering rare Mendelian mutations for rare disease causing gene variants. In 2009, Dr. Steven Quake,

Helicos SAB Chair and company founder also published the first single molecule sequencing of a human genome. The pace of technology advancements to drive costs of sequencing down has continued in

earnest. The Helicos System provides an important platform for the depth and breadth of genomic studies required to fully unlock the secrets of the genome and the role of genome variation in health

and disease.

- •

- Disease association studies. 2007 and 2008 represented

landmark years in the search for genes involved in common disease. As we have known, common diseases and conditions involve complex genetic factors and environmental interactions to produce the

visible measurements or features of disease. In 2007, large scale genetic association studies including the Wellcome Trust Case Control Consortium and the Genetic Association Information Network

(GAIN) identified, using high-throughput genotyping technologies, multiple genes and gene regions associated with diseases such as coronary artery disease, Type I and Type II diabetes,

obesity, Crohn's Disease, rheumatoid arthritis, and bipolar disorder. In 2008, additional publications on a broad survey of diseases continued in earnest. Yet what we now have learned is that common

variants associated with these diseases only begin to scratch the surface of the underlying individual variation contributing to these associations. By sequencing the genomes or selected genes from

many individuals with a given condition, it may be possible to identify the causative mutations underlying the disease. Ongoing efforts are focused on the subsequent sequencing of the genomic regions

associated with these common diseases to attempt the search for further genomic factors accounting for disease contributions. This research may lead to breakthroughs in disease diagnosis, prevention

and treatment.

- •

- Molecular diagnostics. Patients who present with the same disease symptoms often have different prognoses and responses to drugs based on their underlying genetic differences. We believe that delivering patient-specific genetic and genomic information at a reasonable cost represents a multi-billion dollar potential market waiting to be fully realized. Commercial markets for molecular diagnostics include gene- or expression-based diagnostic kits and services, targeted gene resequencing for companion diagnostic products offer the opportunity for selecting and monitoring particular therapies, as well as patient screening for early disease detection and disease monitoring. Creating more effective and targeted molecular diagnostics and screening tests requires a better understanding of genes, regulatory factors and other disease- or drug-related factors. We believe that our platform's quantitative accuracy, the use of small sample quantities in simple preparation methods, and high throughput, as well as lack of biases

11

- •

- Cancer research. Cancer genetics involves understanding

the effects of the inherited genome as well as the tumor genome including acquired mutations and other genetic alterations. Diagnosing and treating cancer therefore requires a more comprehensive

understanding of the individual patient tumor genome to better-predict responses to drug therapy. We believe the availability of low-cost genomic analysis including quantitative Digital

Gene Expression, RNA Sequencing and microRNA profiling on small samples, circulating tumor cells, tumor cell biopsies or formalin-fixed paraffin embedded tissue specimens to characterize acquired

changes of the genome that contribute to cancer would enable improved diagnosis and treatment of cancer.

- •

- Pharmaceutical research and development. Genomics touches

every phase of the drug discovery and development process to varying degrees. This includes early target discovery, through candidate selection, clinical trial design and interpretation and ultimately

into the marketplace with diagnostics linking genomic information with therapeutic intervention. In early discovery, single molecule sequencing could enable high-throughput screening in a

cost-effective manner using large scale gene expression analysis, allowing the study of disease and target pathways to better identify promising drug leads. As lead matter is refined into

preclinical candidates, expression profiling may allow a better understanding of compound toxicity and allow those candidates with minimal toxicity profiles to proceed to the clinic. The broad

application of genomics in the later phase of drug development has been hampered by the lack of high throughput, cost effective methods to link patient variation with genomic information. In clinical

development, our technology could potentially be used to generate individual gene profiles that can provide valuable information on likely response to therapy, both efficacy and adverse events, and

provide insight into genomic biomarkers that may provide signatures for patient screening and individualization of therapy.

- •

- Infectious disease. All viruses, bacteria and fungi

contain DNA or RNA. The detection and sequencing of DNA or RNA from pathogens at the single molecule level would provide medically and environmentally useful information for the diagnosis, treatment

and monitoring of infections and to predict potential drug resistance. Such sequencing would not require the growth or purification of organisms that can be difficult to culture or work with.

- •

- Autoimmune conditions. Autoimmune conditions, such as

multiple sclerosis, Type I diabetes and lupus, have important genetic components which can be reflected at both the DNA and RNA level. Monitoring the underlying genetic background of patients

as well as monitoring RNA expression changes associated with these diseases and corresponding treatment may enable better patient management.

- •

- Agriculture. Agricultural research has increasingly turned to genomics for the discovery, development and design of genetically superior animals and crops. The agribusiness industry has been a large consumer of genetic technologies—particularly microarrays—to identify relevant genetic variations across varieties or populations which will be especially useful in species not well studied in the past. Our sequencing technology may provide a more powerful, direct and cost-effective approach to gene expression analysis and population studies for this industry.

typically seen with sample amplification, can be particularly useful in the field of molecular diagnostics.

As we consider a repositioning of the Company in the genetic analysis markets, we are evaluating the areas where we believe Helicos' technology offers significant opportunity and, in particular, we believe that Helicos' technology is uniquely suited for applications in molecular diagnostics.

12

RESEARCH AND DEVELOPMENT

The wide variety of technical disciplines required for the development of a commercial single molecule sequencing system is represented within our research and development organization, which includes the following functional groups: methods development, organic synthesis, engineering, sequencing development and scientific informatics. Our research and development staff includes PhD scientists and PhD engineers.

We have rapidly advanced the development of our True Single Molecule Sequencing (tSMS)™ technology since we began operations in 2003. In 2004, we began to produce sequence data from single molecules of DNA and in 2005, we sequenced genomic DNA from a small virus called M13 using our tSMS technology. Also in 2005, we began to design the Helicos® Genetic Analysis System. In 2006, we received a $2 million grant from the National Human Genome Research Institute and completed the design of the critical components of the Helicos System. In 2007, we substantially finished the assembly of five commercial grade Helicos Systems and began shipping our Helicos Systems to initial customers in 2008. Our initial shipment to our first customer, Expression Analysis, Inc. ("EA"), was made on March 5, 2008. This system was an early version and did not consistently achieve our commercial specification levels at EA and, as a result, on January 27, 2009, we agreed to have EA return the Helicos System that was installed at EA. Following EA's return of this system, our commercial relationship with EA was suspended. EA did not make any payments for this Helicos System that was ultimately returned.

Our systems are subject to extensive verification and validation testing with reagents and flow cells produced by our operations group in order to validate the performance that will be achieved by the customer. Our engineers play a key role in developing robust manufacturing and installation processes and identifying key areas for improving system reliability and system cost. Also in 2008, we introduced a second generation Virtual Terminator™ Nucleotides with improved performance and shelf-life and introduced a second generation image analysis software with improved performance. During 2009, we continued to invest in research and development activities to further improve the performance of our Helicos System beyond its initial performance characteristics, albeit at a reduced pace given our limited resources and as a result of our December 2008 decision to implement a 30% reduction in our workforce and take other measures to reduce our operating costs.

With additional investments in research and development activities, we believe that a further reduction of DNA sequencing cost per base of approximately 100 fold may be achieved without requiring major modifications to the HeliScope™ Single Molecule Sequencer. The pace of these research and development activities is expected to be limited during 2010, however, as a result of our limited resources. We describe below some of the ways in which we have improved the performance of the tSMS technology for use in the HeliScope Sequencer and ways in which performance can be improved on an ongoing basis.

- •

- Improved flow cell surface stability. By optimizing the

surface coating of the flow cell and the reagents used in the HeliScope Sequencer, we have increased the stability of DNA attachment to the flow cell surface. We believe that further increases in

stability would increase the number of strands that remain present at the end of a run and thus the amount of sequence data produced.

- •

- Increased sequencing reaction efficiency and accuracy. In the course of developing our proprietary sequencing process and reagents, we have significantly increased the efficiency with which new bases are added to a growing DNA strand and the accuracy with which they are detected. We believe that further increases in efficiency and accuracy at each step of the sequencing process would continue to increase the number of DNA strands that are useful for genetic analysis.

13

- •

- Increased density of DNA strands. We have successfully

developed the flow cells in our HeliScope Sequencer to permit binding of DNA strands at an average density of approximately 100 million strands per square centimeter. We believe that additional

development work in the area of surface chemistry would increase the number of DNA strands that can be anchored to the surface of the flow cells up to 400 million per square centimeter.

- •

- Enhanced speed of image processing subsystem. We have

developed high speed image processing that enables analysis of the images produced by the HeliScope Sequencer. We believe that enhancements to the speed of the image processing subsystem would enable

reduction in the server hardware included as a part of the cost of a Helicos System.

- •

- Reduced instrument cost. We believe that efforts to evaluate new camera and laser technology would give us the opportunity to both reduce the material cost of the instrument and increase sequencing performance.

We believe that each of the above improvements, if successful, would increase the throughput of the HeliScope Sequencer and reduce the cost per base of sequencing. We believe that other improvements, such as reducing reagent consumption, reducing image acquisition time, and enhancing the performance of the system's mechanical components, with the goal of further increasing throughput and reducing cost, are feasible depending on our ability to make additional levels of investment in research and development activities. As we reevaluate our long-term strategy, we may elect to pursue some or none of these potential performance enhancements depending on the availability of resources and the importance of such enhancements to our long-term strategy.

In 2009 we continued our forward thinking research activities in genomic and measurement sciences. Our Applications, Methods and Collaborations group emerged as a result of the intimate relationship between genomic sciences, applications and methods. This group spends a significant amount of time supporting customers, prospective customers and collaborators who now can benefit from our expertise in sample preparation and novel methods for the application of single molecule sequencing to address important questions in biology. These efforts have resulted in the publication of several studies which highlight the versatility and breadth of scientific studies which are enabled on our platform. We have continued our work with world class leaders in the field of genomics including members of the ENCODE consortium, genome sequencing centers and academic research institutions. Our applications research areas include:

- •

- Transcriptome analyses: Digital gene expression and RNA

Sequencing provides a hypothesis free, global, and quantitative analysis of the transcriptome. Our research focuses on developing the single molecule sequencing method to allow the quantitative

measurement of virtually all genes in a sample by counting the number of individual mRNA molecules produced from each gene. This allows one to examine all the genes present in a cell or tissue in a

hypothesis independent manner with no bias toward the genes believed to be expressed. We believe the end result is a highly sensitive and quantitative measurement which will allow not only for the

detection of highly expressed transcripts but also for the detection of very rare transcripts represented by only a few molecules of RNA per cell.

- •

- Direct RNA Sequencing: The traditional approaches to transcriptome analyses have been typically dependent on the creation of a cDNA intermediate, an indirect measurement of the RNA in the cell. As such, we embarked on a program to develop the methodology required for the direct sequencing of RNA. While still in the research phase during 2009, our research program definitively demonstrated the direct sequencing of RNA without cDNA-intermediate and published this work in the prestigious journal Nature in October, 2009. In the first quarter of 2010, we have implemented direct RNA sequencing on the Helicos System and began an early access program to provide key scientific leaders with data to demonstrate the unique attributes of the technology.

14

- •

- Chromatin Immunoprecipitation sequencing (ChIP Seq)

studies: In 2009 we worked with world leaders in the epigenomics field to develop the methodology required for ChIP Seq studies.

Benefiting from the simplicity of single molecule sequencing, the Helicos ChIP Seq method provides rapid DNA sample preparation combined with the ability to work with small DNA sample quantities to

reveal an unbiased, genome-wide and quantitative view of protein-DNA interactions and chromatin structure. During 2009, we published our work on ChIP Seq with scientists at the Broad

Institute, Inc. and Massachusetts General Hospital demonstrating these principles.

- •

- miRNA measurements: microRNA (miRNA) represent important

regulators of gene expression and are becoming increasingly important in disease studies, especially cancer. Helicos is using single molecule sequencing to investigate the ability to quantitatively

measure miRNAs from human samples as well as identify novel miRNAs which have been missed because of previous requirements for amplification and limited depth of coverage. In these studies we

demonstrate the unique attributes of single molecule sequencing for accurate miRNA quantitation as compared to quantitation obtained using amplification based methods.

- •

- Candidate region sequencing: Currently the cost of

sequencing an entire human genome remains too high to enable routine whole genome sequencing. New methods are currently under development to allow a simplified, highly multiplexed candidate region

capture method to facilitate large-scale studies of genomic regions of interest. Our technology enables sample barcoding which allows multiplexed sequencing of up to 15 samples per HeliScope Sequencer

channel, resulting in the analysis of up to 750 samples per sequencing run.

- •

- Paired reads: A paired read methodology is desirable for comprehensive whole genome sequencing. Our paired-read development efforts are focused on reading two portions of a DNA molecule using a defined gap size between sequence reads to accurately recapitulate the structural context of the genome to be sequenced. Optimizing the gap sizes for our paired read strategy to allow both short gaps (250-500 base pairs) and longer gaps (1 to 10 kb) remains our focus. Proof of principle was demonstrated on the HeliScopeTM Single Molecule Sequencer for both transcriptome and genome analyses.

Depending on the outcome of our repositioning strategy in the genetic analysis markets and strategic direction, we may decide to continue our applications research in some or all of the aforementioned areas or focus on new areas that would benefit from the unique capabilities of our proprietary platform.

In the years ended December 31, 2007, 2008, and 2009 we incurred $24.8 million, $24.6 million and $18.3 million respectively, of research and development expenses.

PRODUCT DEMONSTRATION ARRANGEMENTS

Our strategy in the research markets has been to establish the Helicos® Genetic Analysis Platform as the platform of choice for analyzing diverse genomic information and to expand the applications of our technology. Accordingly, we entered into product demonstration arrangements with outside parties which were designed to enhance our commercial prospects by demonstrating through publication our technology as a viable platform for analyzing large quantities of genetic information and to expand the potential applications for our technology. These product demonstration arrangements include the transfer of genetic samples from third parties for us to process and analyze using our internal Helicos Systems.

Our product demonstration arrangements also included the outright placement of Helicos Systems at reference sites for scientific and commercial evaluation. In 2009, we had placed Helicos Systems at the following reference sites for evaluation: Dana Farber Cancer Institute (Dana Farber), Massachusetts

15

General Hospital Cancer Center (MGH) and Ontario Institute for Cancer Research (OICR). These reference sites may have the opportunity to purchase their system outright or return the system to us. Entering the second quarter of 2010, the Dana Farber and MGH placements remained ongoing, however, OICR returned its system at the end of the first quarter 2010.

As we consider our repositioning strategy in the genetic analysis markets and strategic direction, we may decide to continue to engage in these types of joint activities with third parties or focus on new relationships with third parties in areas such as molecular diagnostics or others that we believe would benefit from the unique capabilities of our proprietary platform. In any case, these arrangements and any future similar arrangements are not guaranteed to generate any revenue from system sales and are not expected to generate new material intellectual property or new technology for our business.

MANUFACTURING AND RAW MATERIALS

We have manufactured our products using a combination of outsourced components and subassemblies. In addition to our in-house production capability, we have utilized subcontractors for parts of the manufacturing process where we have determined it is in our best interest to do so. As a result of our efforts to reposition the Company in the genetic analysis markets, we do not plan to allocate substantial resources to increasing our manufacturing process capability or capacity.

MARKETING, SALES, SERVICE AND SUPPORT

As a result of our limited resources, we have operated, and expect during 2010 to continue to operate, with a limited number of sales, marketing and service personnel while we develop our strategy to reposition the Company in the genetic analysis markets.

OUR SCIENTIFIC ADVISORY BOARD

We have established a scientific advisory board consisting of individuals whom we have selected for their particular expertise in the fields of genomics, physics, molecular biology, chemistry and engineering. We anticipate that our scientific advisory board members will consult with us on matters relating to:

- •

- our research and development efforts;

- •

- opportunities for strategic collaborations;

- •

- new technologies relevant to our research and development efforts;

- •

- scientific and technical issues relevant to our business; and

- •

- our sales and marketing strategy.

16

All of our advisors are employed by organizations other than us and may have commitments to or consulting or advisory agreements with other entities that may limit their availability to us. Our scientific advisory board currently consists of the following members:

SAB Member

|

Current Affiliations

|

|

|---|---|---|

| Stephen R. Quake, DPhil Chairman of the Scientific Advisory Board |

Professor of Bioengineering at Stanford University and Investigator of the Howard Hughes Medical Institute | |

George Church, PhD |

Professor of Genetics at Harvard Medical School |

|

Leroy Hood, PhD |

President and co-founder of the Institute for Systems Biology in Seattle, Washington |

|

David R. Liu, PhD |

Professor of Chemistry and Chemical Biology at Harvard University; Investigator of the Howard Hughes Medical Institute and Associate Member of the Broad Institute of MIT and Harvard |

|

Eugene W. Myers, PhD |

Group Leader at the Janelia Farm Research Campus of the Howard Hughes Medical Institute |

|

John Quackenbush, PhD |

Faculty Member at the Dana-Farber Cancer Institute and Professor of Biostatistics and Computational Biology and Professor of Computational Biology and Bioinformatics at the Harvard School of Public Health |

|

Floyd Romesberg. PhD |

Associate Professor of Chemistry at The Scripps Research Institute in La Jolla, California |

|

Victor E. Velculescu, MD, PhD |

Assistant Professor of Oncology at The Sidney Kimmel Comprehensive Cancer Center at Johns Hopkins |

COMPETITION IN THE GENETIC ANALYSIS MARKET

Competition among entities developing or commercializing instruments, research tools or services for genetic analysis is intense. A number of companies offer DNA sequencing equipment or consumables, including Life Technologies, Inc., Beckman Coulter, Inc., the Life Sciences Division of GE Healthcare, Illumina, Inc., Complete Genomics, Inc. and Roche Applied Science. Furthermore, a number of other companies and academic groups are in the process of developing novel techniques for DNA sequencing. These companies include, among others, Ion Torrent, Genizon BioSciences, Intelligent Bio-Systems, Lucigen, Microchip Biotechnologies, Pacific Biosciences, Shimadzu Biotech, ZS Genetics, Oxford Nanopore, NabSys and IBM. For RNA analysis and/or genotyping there are a number of companies that offer equipment and supplies including Affymetrix, Inc., Agilent Technologies, Applera Corporation, Bio-Rad Laboratories, Luminex and Nanostring. Three companies provide a wide range of products that span both DNA and RNA analysis—Life Technologies, Inc., Affymetrix, Inc. and Illumina, Inc. However, the solutions that are provided are separate applications that require different sample preparation techniques, consumables, analysis software and instrumentation with limited correlation between platforms.

Many of these companies have substantially greater capital resources, research and product development capabilities and greater financial, scientific, manufacturing, marketing, and distribution experience and resources, including human resources, than we do. These companies may develop or commercialize genetic analysis technologies before us or that are more effective than those we are

17

developing, and may obtain patent protection or other intellectual property rights that could limit our rights to offer genetic analysis products or services

As we consider the repositioning of the Company in the genetic analysis markets, we will need to continue to assess our ability to successfully compete against existing and future technologies. Moreover, we will need to demonstrate that the price and performance of our technologies and platform applied to our target markets are competitive with those of competing technologies.

INTELLECTUAL PROPERTY

Developing and maintaining a strong intellectual property position is an important element of our business strategy. Our patent portfolio relating to our proprietary technology is comprised, on a worldwide basis, of various patents and pending patent applications, which, in either case, we own directly or for which we are the exclusive or semi-exclusive licensee. A number of these patents and patent applications are foreign counterparts of U.S. patents or patent applications. Among other things, our patent estate includes patents and/or patent applications having claims directed to:

- •

- the overall True Single Molecule Sequencing (tSMS)tm method;

- •

- certain components of the Helicos® Genetic Analysis Platform, including our laser illumination subassembly,

our flow cells and various methods for using our HeliScope Sequencer;

- •

- methods for focusing our lasers and imaging our flow cell surfaces, and our use of combinations of laser optical paths;

- •

- our Virtual TerminatorTM Nucleotides and other nucleotides;

- •

- various aspects of our sample preparation processes;

- •

- algorithms for analysis of our data; and

- •

- reagent formulations for imaging and for sequencing.

Within broad technological categories, our patent portfolio can be broken down as follows: most of our issued (81%) and pending (60%) patents are directed to sequencing by synthesis, primarily at the single molecule level; the smallest portion of the patent portfolio (3% of issued patents and 3% of pending applications) involves bioinformatics and data processing; the remainder of the portfolio is roughly evenly split among sample preparation (6% of issued patents and 12% of pending applications), instrumentation (10% of issued patents and 11% of pending applications), and commercial applications (14% of pending patent applications). The last-mentioned of these groups—commercial applications—encompasses wide areas of scientific and commercial interest including direct RNA sequencing, single-cell analysis, high-throughput screening, digital gene expression, and candidate region re-sequencing.

Our patents generally have terms of 20 years from their respective non-provisional priority filing dates. The first non-provisional patent applications prosecuted by Helicos were filed in 2004 and thus our issued patents are not scheduled to expire until 2024 or later. We have filed terminal disclaimers in certain later-filed patents, which means that such later-filed patents are scheduled to expire earlier than the twentieth anniversary of their respective non-provisional priority filing dates, although not earlier than 2024 with respect to patent applications prosecuted by Helicos. We have also in-licensed patents and patent applications. All of the material patents and patent applications to which we have licensed rights are scheduled to expire in 2017 or later.

Patent law relating to the scope of claims in the technology field in which we operate is still evolving. The degree to which we will be able to protect our technology with patents, therefore, is uncertain. Others may independently develop similar or alternative technologies, duplicate any of our technologies and, if patents are licensed or issued to us, design around the patented technologies

18

licensed to or developed by us. In addition, we could incur substantial costs in litigation if we are required to defend ourselves in patent suits brought by third parties or if we initiate such suits.

We regard as proprietary any technology that we or our exclusive licensors have developed or discovered, including technologies disclosed in our patent estate, and that was not previously in the public domain. Aspects of our technology that we consider proprietary may be placed into the public domain by us or by our licensors, either through publication or as a result of the patent process. We may choose for strategic business reasons to make some of our proprietary technology publicly available whether or not it is protected by any patent or patent application.

With respect to proprietary know-how that is not patentable and for processes for which patents are difficult to obtain or enforce, we may rely on trade secret protection and/or confidentiality agreements to protect our interests. While we require all employees, consultants, collaborators, customers and licensees to enter into confidentiality agreements, we cannot be certain that proprietary information will not be disclosed or that others will not independently develop substantially equivalent proprietary information.

In addition to our patents, patent applications, confidential know-how, and potential trade secrets, we license technology that we consider to be material to our business.

Roche License Agreement. In June 2004, we entered into a license agreement with Roche Diagnostics (the "Roche License Agreement") which granted us a worldwide, semi-exclusive royalty-bearing license, with the right to grant sublicenses under a patent relating to sequencing methods. In connection with the Roche License Agreement, we paid an upfront fee of 175,000 Euros and committed to pay an annual license fee ranging from 10,000 to 40,000 Euros. There are no milestone payments potentially payable by us under the Roche License Agreement in addition to those described above. We have an option to convert the license to non-exclusive beginning in 2008, in which case the annual license fees would be reduced to 10,000 Euros beginning in 2008. We have the right to terminate the Roche License Agreement at any time for convenience upon 90 days prior written notice to Roche Diagnostics. We both have the right to terminate the Roche License Agreement upon breach by the other party, subject to notice and an opportunity to cure. The Roche License Agreement also terminates upon the occurrence of specified bankruptcy events. As part of the Roche License Agreement, we agreed to pay single digit royalties based on a percentage of defined net sales. We also agreed to pay half of our income amounts that we receive based on sublicenses that we grant to third parties. Our royalty obligation, if any, extends until the expiration of the last-to-expire of the licensed patents. Through December 31, 2009, no royalty payments have been made. All license fee amounts paid to date have been expensed to research and development expense as technological feasibility had not established and the technology had no alternative future use. The total expense recognized under the Roche License Agreement for the years ended December 31, 2007, 2008 and 2009, and the period from May 9, 2003 (date of inception) through December 31, 2009 was $39,000, $62,000, $54,000 and $421,000, respectively.

AZTE License Agreement. In March 2005, we entered into a license agreement with Arizona Technology Enterprises (the "AZTE License Agreement") that granted us a worldwide, exclusive, irrevocable, royalty-bearing license, with the right to grant sublicenses, under specified patents and patent applications exclusively licensed by AZTE from Arizona State University and the University of Alberta. In connection with the AZTE License Agreement, we paid an upfront fee of $350,000, committed to an annual license fee of $50,000, which has increased to $100,000 upon the successful issuance of a U.S. patent, committed to pay a three-year maintenance fee of $50,000, payable in equal annual installments beginning in March 2006, and issued 88,888 shares of restricted common stock, which vest in two equal installments upon the achievement of separate milestones. There are no milestone payments potentially payable by us under the AZTE License Agreement in addition to those described above. We are obligated to use reasonable commercial efforts to develop, manufacture and.

19

In addition, if we fail to to use commercially-reasonable efforts to develop, manufacture and sell licensed products, the AZTE License Agreement converts from exclusive to non-exclusive. The AZTE License Agreement will remain in force until terminated. We have the right to terminate the AZTE License agreement at any time for convenience upon 60 days prior written notice to Arizona Technology Enterprises. We both have the right to terminate the agreement upon breach by the other party, subject to notice and an opportunity to cure. The AZTE License Agreement also terminates upon the occurrence of specified bankruptcy events.

As part of the AZTE License Agreement, we agreed to pay a single digit percentage royalty based on defined net sales. We also agreed to pay a mid-teens percentage of specified sublicense income amounts that are received based on sublicenses granted to third parties which increases to 30 percent after we receive an aggregate of $50,000 of such amounts. Our royalty obligation, if any, extends until the expiration of the last-to-expire of the licensed patents. Through December 31, 2009, no royalty payments have been made. All license fee amounts paid to date have been expensed to research and development expense as technological feasibility had not been established and the technology had no alternative future use. In May 2006, in accordance with the license agreement, due to the successful issuance of a U.S. patent, the committed annual license fee increased from $50,000 to $100,000 and 44,444 shares of the restricted common stock vested. The vesting of 44,444 shares of restricted common stock resulted in a charge to research and development expense of $127,000 based on the fair value of our common stock at the time the milestone was achieved. The remaining 44,444 shares of restricted common stock vested immediately upon the successful issuance of a second U.S. patent on January 12, 2010. The total expense recognized under the AZTE License Agreement for the years ended December 31, 2007, 2008 and 2009, and the period from May 9, 2003 (date of inception) through December 31, 2009 was $117,000, $103,000, $141,000 and $990,000, respectively.

Caltech License Agreement. In November 2003, we entered into a license agreement with California Institute of Technology (the "Caltech License Agreement") that granted us a worldwide, exclusive, royalty-bearing license, with the right to grant sublicenses, under specified patents and patent applications, and a worldwide, non-exclusive royalty bearing license, with the right to grant sublicenses, under specified technology outside the scope of the licensed patents. In connection with the Caltech License Agreement, we issued 46,514 shares of common stock, and recorded a charge of $20,000. In addition, we pay an annual license fee of $10,000 per year. The license fee payments are creditable against single digit royalties calculated upon sales of products covered by patents licensed under the agreement. We are also obligated to pay California Institute of Technology a single digit percentage of specified license and sublicense income, a single digit percentage of proceeds from sales of specified intellectual property and a single digit percentage of service revenue amounts that we receive based on licenses and sublicenses that we grant, sales of intellectual property and services that we provide to third parties. The royalty obligation with respect to any licensed product extends until the later of the expiration of the last-to-expire of the licensed patents covering the licensed product and three years after the first commercial sale of the licensed product in any country for non-patented technology covered under the agreement. Through December 31, 2009, no royalty payments have been made. In March 2007, we amended the Caltech License Agreement to provide rights under an additional patent application under the terms of the existing license in exchange for a one-time payment of $50,000 to the California Institute of Technology. There are no milestone payments potentially payable by us under the Caltech License Agreement in addition to those described above. All license fee amounts paid to date and the value of the common stock issued have been expensed to research and development expense as technological feasibility had not been established and the technology had no alternative future use. The total expense recognized under the Caltech License Agreement for the years ended December 31, 2007, 2008 and 2009, and the period from May 9, 2003 (date of inception) through December 31, 2009 was $60,000, $10,000, $10,000 and $123,000, respectively.

20

PerkinElmer License Agreement. In April 2007, we entered into an agreement with PerkinElmer LAS, Inc. ("PerkinElmer"), in which PerkinElmer granted us a worldwide, non-exclusive, non-transferable, non-sublicensable, royalty bearing license under specified patents. Our license from PerkinElmer grants us rights under certain patents to produce and commercialize certain of the reagents used in some applications on the Helicos System, which contain chemicals purchased from PerkinElmer. In exchange for rights licensed from PerkinElmer, we are obligated to pay PerkinElmer a single digit percentage of our net revenue from the sale of reagents that contain chemicals covered by the patents licensed under the PerkinElmer agreement. There are no milestone payments potentially payable by us under this agreement with PerkinElmer. We have the right to terminate the agreement at any time upon 90 days written notice to PerkinElmer. Each party has the right to terminate the agreement upon breach by the other party subject to notice and an opportunity to cure. The agreement also terminates upon the occurrence of specified bankruptcy events. PerkinElmer has the sole right under the agreement to enforce the licensed patents. There has been no expense recorded for this agreement for any period from May 9, 2003 (inception) through December 31, 2009.

See Note 7 to the Consolidated Financial Statements contained in this Form 10-K for additional information on license agreements.

CORPORATE INFORMATION

We were incorporated in Delaware in May 2003. In 2003, one of our co-founders, Professor Stephen R. Quake, who was then at the California Institute of Technology, demonstrated, we believe for the first time, that sequence information could be obtained from a single strand of DNA. Shortly thereafter, Noubar Afeyan, Chief Executive Officer of Flagship Ventures, and Stanley Lapidus, then a Venture Partner at Flagship Ventures, met with Professor Quake and agreed to found a company to develop and commercialize technology based on Professor Quake's single molecule approach. Combining the experience of Professor Quake in single molecule methods, Dr. Afeyan in the sequencing technology and life sciences businesses, and Mr. Lapidus in diagnostics and entrepreneurship, we focused exclusively on the technical and commercial development of technology based on Professor Quake's approach. Professor Eric Lander, Director of the Broad Institute of MIT and Harvard, and a leader in the DNA sequencing field, provided helpful guidance and advice during our founding stages.

EMPLOYEES

We had 80 full time employees at December 31, 2009. We have never had a work stoppage and none of our employees are covered by collective bargaining agreements. We believe our employee relations are good. Our success depends in large part on our ability to attract and retain skilled and experienced employees.

AVAILABLE INFORMATION

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, definitive proxy statements on Form 14A, current reports on Form 8-K, and any amendments to those reports are made available free of charge on our website, www.helicosbio.com, as soon as reasonably practicable after such reports are electronically filed with or furnished to the Securities and Exchange Commission ("SEC"). Statements of changes in beneficial ownership of our securities on Form 4 by our executive officers and directors are made available on our website by the end of the business day following the submission to the SEC of such filings. In addition, the SEC's website, www.sec.gov, contains reports, proxy statements, and other information regarding reports that we file electronically with the SEC.

21

The following important factors could cause our actual business, prospects, financial results or financial condition to differ materially from those contained in forward-looking statements made in this Annual Report on Form 10-K or elsewhere by management from time to time.

RISKS RELATED TO OUR BUSINESS

We are exploring various alternatives to the Company's existing long-term strategic focus. If we are unsuccessful in pursuing any of these new business initiatives, our business, financial condition, results of operations and prospects will be materially adversely affected and we may have to cease operations.

We are reevaluating our long-term strategic focus and considering various alternatives to reposition our business, by exploring various opportunities including the use of our technology for diagnostic applications in the genetic analysis market. It will take us at least several months to pursue any of these opportunities. While any of these new business opportunities will rely upon the capabilities of our proprietary Helicos® Genetic Analysis Platform, the business model, including the revenue and expense models and the potential marketing and distribution channels, for these opportunities may be materially different than that which we have engaged in before. We are unable to give any assurance we will be commercially successful in any opportunity we pursue. Our failure to be commercially successful in any such new business opportunity would materially adversely impact our business, financial condition, results of operations and prospects and could ultimately require that we cease operations.

Any successful shift in our strategic focus will likely require significant organizational changes. We will need to attract, train and retain qualified sales, marketing and service personnel, engineers, scientists and other technical and management personnel with appropriate expertise for our new strategic focus. These areas of expertise may be different than the skills of our existing employees. Given the potential uncertainty about our strategic focus and long term roles within our organization, morale may be lowered, key employees may be distracted and our business may experience a loss of continuity while we reevaluate our long-term strategic focus. Our inability retain existing personnel during this period of uncertainty or our inability to attract new personnel that fit within a new strategic focus once it is identified, would prevent our exploiting fully any new business alternative and thereby cause a material adverse effect on our business, financial condition, results of operations and prospects.