Attached files

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

Form 10-K

x ANNUAL REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For

the fiscal year ended December 31, 2009

o TRANSITION REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For

the transition period from __________ to __________

Commission

File Number: 001-33884

| GULFSTREAM INTERNATIONAL GROUP, INC. | ||

| (Exact name of registrant as specified in its charter) |

|

Delaware

|

20-3973956

|

|

|

(State

or other jurisdiction of

|

(I.R.S.

Employer

|

|

|

incorporation

or organization)

|

Identification

No.)

|

3201

Griffin Road, 4th

Floor, Fort Lauderdale, Florida 33312

(Address

of principal executive offices, including zip code)

Registrant’s

telephone number, including area code:

(954)

985-1500

Securities

registered pursuant to Section 12(b) of the Act:

|

Title

of each class

|

|

Name

of each exchange on which registered

|

|

Common

Stock of $0.01 par value per share

|

|

NYSE

Amex Stock Exchange

|

Securities

registered pursuant to Section 12(g) of the Act: None

________________

Indicate by check mark if the

registrant is a well-known seasoned issuer, as defined in Rule 405 of the

Securities Act. Yes ¨ No

þ

Indicate by check mark

if the registrant is not required to file reports pursuant to Section 13 or

15(d) of the Exchange Act. Yes ¨ No

þ

Indicate by check

mark whether the registrant (1) has filed all reports required to be filed

by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was

required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days. Yes þ No

¨

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files). Yes ¨ No

þ

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K (§229.405 of this chapter) is not contained herein, and will

not be contained, to the best of registrant’s knowledge, in definitive proxy or

information statements incorporated by reference in Part III of this

Form 10-K or any amendment to this Form 10-K.

Yes ¨ No

þ

Indicate by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer or a smaller reporting company. See

the definitions of “large accelerated filer,” “accelerated filer”

and “smaller reporting company” in Rule 12b-2 of the Exchange

Act.

| Large accelerated filer | o | Accelerated filer | o |

|

Non-accelerated

filer

(Do not

check if a smaller reporting company)

|

o | Smaller reporting company | þ |

Indicate

by check mark whether the registrant is a shell company (as defined in

Rule 12b-2 of the Exchange Act). Yes ¨

No þ

The

aggregate market value of the voting and non-voting common equity held by

non-affiliates of the registrant was approximately $6,244,756 as of June 30,

2009.

As of

March 31, 2010, 3,795,061 shares of the registrant’s common stock, par value

$0.01 per share, were issued and outstanding.

Documents

Incorporated by Reference: None.

GULFSTREAM

INTERNATIONAL GROUP, INC.

2009

FORM 10-K ANNUAL REPORT

TABLE

OF CONTENTS

|

Page

|

|||||

|

PART I

|

|||||

|

Item 1.

|

Business.

|

4 | |||

|

Item 1A.

|

Risk

Factors.

|

14 | |||

|

Item 1B.

|

Unresolved

Staff Comments.

|

28 | |||

|

Item 2.

|

Properties.

|

28 | |||

|

Item 3.

|

Legal

Proceedings.

|

29 | |||

|

Item 4.

|

Submission

of Matters to a Vote of Security Holders.

|

29 | |||

|

PART II

|

|||||

|

Item 5.

|

Market

for Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities.

|

30 | |||

|

Item 6.

|

Selected

Financial Data.

|

33 | |||

|

Item 7.

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations.

|

36 | |||

|

Item

7A.

|

Quantitative

and Qualitative Disclosures About Market Risk.

|

47 | |||

|

Item 8.

|

Financial

Statements and Supplementary Data.

|

49 | |||

|

Item 9.

|

Changes

and Disagreements With Accountants on Accounting and Financial

Disclosure.

|

74 | |||

|

Item 9A.

|

Controls

and Procedures.

|

74 | |||

|

Item 9B.

|

Other

Information.

|

75 | |||

|

PART

III

|

|||||

|

Item 10.

|

Directors,

Executive Officers and Corporate Governance.

|

76 | |||

|

Item 11.

|

Executive

Compensation.

|

79 | |||

|

Item

12.

|

Security

Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters.

|

91 | |||

|

Item

13.

|

Certain

Relationships and Related Transactions, and Director

Independence.

|

93 | |||

|

Item

14.

|

Principal

Accounting Fees and Services.

|

95 | |||

|

PART

IV

|

|||||

|

Item

15.

|

Exhibits,

Financial Statement Schedules.

|

97 | |||

|

Signatures

|

102 | ||||

2

Cautionary

Statement Concerning Forward-Looking Statements

Our representatives and we may from

time to time make written or oral statements that are "forward-looking,"

including statements contained in this Annual Report on Form 10-K and other

filings with the Securities and Exchange Commission, reports to our stockholders

and news releases. All statements that express expectations, estimates,

forecasts or projections are forward-looking statements within the meaning of

the Act. In addition, other written or oral statements which constitute

forward-looking statements may be made by us or on our behalf. Words such as

"expects," "anticipates," "intends," "plans," "believes," "seeks," "estimates,"

"projects," "forecasts," "may," "should," variations of such words and similar

expressions are intended to identify such forward-looking statements. These

statements are not guarantees of future performance and involve risks,

uncertainties and assumptions which are difficult to predict. These risks may relate to,

without limitation:

|

·

|

our

business strategy;

|

|

●

|

our

value proposition;

|

|

●

|

the

market opportunity for our services, including expected demand for our

services;

|

|

●

|

information

regarding the replacement, deployment, acquisition and financing of

certain numbers and types of aircraft, and projected expenses associated

therewith;

|

|

●

|

costs

of compliance with FAA regulations, Department of Homeland Security

regulations and other rules and acts of

Congress;

|

|

●

|

the

ability to pass taxes, fuel costs, inflation, and various expense to our

customers;

|

|

●

|

certain

projected financial obligations;

|

|

●

|

our

estimates regarding our capital

requirements;

|

|

●

|

any

of our other plans, objectives, expectations and intentions contained in

this report that are not historical

facts;

|

|

●

|

changing

external competitive, business, budgeting, fuel supply, weather or

economic conditions;

|

|

●

|

changes

in our relationships with employees or code share

partners;

|

|

●

|

availability

and cost of funds for financing new aircraft and our ability to profitably

manage our existing fleet;

|

|

●

|

adverse

reaction and publicity that might result from any

accidents;

|

|

●

|

the

impact of current or future laws and government investigations and

regulations affecting the airline industry and our

operations;

|

|

●

|

additional

terrorist attacks; and

|

|

●

|

consumer

unwillingness to incur greater costs for

flights.

|

Therefore,

actual outcomes and results may differ materially from what is expressed or

forecasted in or suggested by such forward-looking statements. We undertake no

obligation to publicly revise these forward-looking statements to reflect events

or circumstances that arise after the date hereof. Readers should carefully

review the factors described herein and in other documents we file from time to

time with the Securities and Exchange Commission, including our Quarterly

Reports on Form 10-Q, Annual Reports on Form 10-K, and any Current Reports on

Form 8-K filed by us.

3

ITEM 1. BUSINESS.

Overview of Our

Business

Gulfstream

International Group, Inc. is a holding company that operates two independent

subsidiaries: Gulfstream International Airlines, Inc. (“Gulfstream” or “the

Airline”) and Gulfstream Training Academy, Inc. (the “Academy”). References to

“Company” “we,” “our,” and “us,” refer to Gulfstream International Group, Inc.

and either or both of Gulfstream or the Academy.

Gulfstream

is a commercial airline currently operating 147 scheduled flights per day,

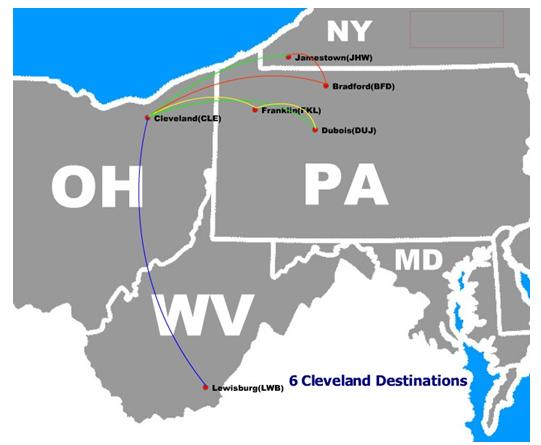

serving nine destinations in Florida, ten destinations in the Bahamas, and five

destinations from Continental Airline’s Cleveland hub under the Department of

Transportation’s Essential Air Service Program. Our fleet consists of 23 B1900D,

19-seat, turbo-prop aircraft. Operating from our headquarters in Fort

Lauderdale, Florida, Gulfstream was the sixteenth largest regional airline group

in the U.S. in 2008 in terms of number of passengers flown, according to the

Regional Airline Association. We operate under a principal code share and

alliance agreement with Continental Airlines. We are also party to code share

agreements with United and Copa Airlines of Panama. In addition to the daily

scheduled flights, Gulfstream also offers frequent charter flights within our

geographic operating region, including licensed flights to Cuba.

The

Academy provides flight training services to fully-licensed commercial pilots.

The Academy’s principal program is our First Officer Program, which allows

participants to obtain a Second-In-Command type rating in approximately four

months. Following receipt of this rating, pilots fly between 250 and 400 hours

performing first officer duties at Gulfstream. By attending the Academy, pilots

are able to enhance their ability to secure a permanent position with a

commercial airline. The Academy’s graduates are typically hired by various

regional airlines, including Gulfstream. In 2009 and 2008, 42 and 59 pilots,

respectively, entered the First Officer Program.

History

Our

business was started by Thomas L. Cooper with the formation of Gulfstream in

1988. Gulfstream began as an airline offering on-demand charter service

utilizing nine-passenger, piston-powered aircraft. In 1990, we initiated

scheduled commercial service by offering flights from Miami to several locations

in the Bahamas. In 1994, after introducing turbo-prop aircraft, we signed our

first code share agreement with United Airlines and expanded our routes in both

Florida and the Bahamas. Since 1994, we have signed a series of code share

agreements with our current code share partners.

Gulfstream

first entered into a code share and alliance agreement with Continental, our

principal alliance partner, in 1997. Gulfstream and Continental have amended the

agreement on several occasions, most recently in March of 2006, which amendment

included an extension of the term to 2012. Prior to our acquisition of

Gulfstream, Continental assisted Gulfstream from time to time with financial

transactions and aircraft acquisitions, and today holds a warrant to purchase

10% of Gulfstream’s outstanding shares.

In

December 2005, Gulfstream International Group, Inc. was incorporated in Delaware

by a group of investors as Gulfstream Acquisition Group, Inc., and changed its

name to Gulfstream International Group, Inc. on June 13, 2007. We were

formed to acquire Gulfstream and the Academy. In March 2006, we acquired

approximately 89% of G-Air Holdings Corp., Inc. (“G-Air”), which owned

approximately 95% of Gulfstream at that time, and 100% of the Academy, which

held the remaining 5% of Gulfstream. Subsequently, we acquired the remaining 11%

of G-Air. Following these transactions, we are the sole owner of Gulfstream and

the Academy, subject to Continental’s warrant to purchase 10% of the outstanding

shares of Gulfstream’s common stock.

Our Competitive

Strengths

· Long-standing code share agreements

with multiple major airlines. Gulfstream has code share agreements with

Continental and United. We have been a partner with each of these airlines for

more than five years. Recently, our code share agreement with Continental was

extended through 2012. We believe that utilizing such agreements enhances our

ability to generate revenue from both local and connecting traffic. We also

believe that through our alliances, we are able to control costs by contracting

for reservations, ground handling and other services at lower costs. In

addition, these code share relationships allow us to offer our passengers easy

booking through reservation systems maintained by our code share partners and

the benefits of associated frequent flier programs.

4

· Well positioned in the Bahamas

market. We are a leading carrier to the Bahamas and serve more

destinations in the Bahamas than any other U.S. airline. We maintain our own

facilities and employees at all ten of our destinations in the Bahamas and we

enjoy a close cooperative relationship with Bahamian business and tourism

officials. We believe that our focus on the Bahamian market allows us to

identify new market opportunities and develop those opportunities more

efficiently than new market entrants.

· Diverse route network and

utilization of small aircraft. We have connecting hubs in several key

Florida cities, daily charter flights to Cuba, and flights from Continental

Airline’s Cleveland hub to five smaller cities in Pennsylvania, New York, and

West Virginia. This network enables us to establish multiple flight crew and

maintenance bases that reduce overall operating costs and enhance operational

reliability. The size and scale of this operation create practical barriers to

entry for new entrants and increases our ability to shift capacity according to

seasonal and business-versus-leisure demand patterns. Additionally, the

relatively small size and efficiency of our turboprop aircraft combine to

produce trip costs that are substantially lower than operators flying larger and

more expensive jet aircraft.

· We offer reliable, quality

service. We have been consistently among the highest-ranked regional

airlines in the country in terms of reliability. For 2009, our on-time

performance was 79.5%, compared to the 79.6% average on-time performance

reported by the Department of Transportation for all reporting airlines.

Gulfstream has received the FAA Diamond Award, the highest level of recognition

for maintenance training, for 13 consecutive years, including 2009.

· The Academy has a unique first officer program. We

believe the Academy has established a strong reputation for quality instruction.

We offer our students the opportunity to accumulate flight hours with an airline

regulated under Part 121 of the FAA regulations, sometimes referred to as Part

121 flight hours. Many airlines require pilot applicants to have a certain

number of Part 121 flight hours or equivalent experience and so our students

enhance their hiring prospects with regional airlines through our first officer

program. In addition, the Academy provides Gulfstream with a reliable and

cost-effective source of first officers and pilots.

Our Strategy

Our

business strategy is to utilize small-capacity aircraft to target markets that

are unserved or underserved by competing airlines. Small capacity aircraft allow

for lower costs per flight, and enable us to operate profitably with fewer

passengers per flight than airlines operating larger equipment.

· Utilize turboprop aircraft to

selectively expand the number of markets we serve. We use 19-passenger

turboprop aircraft. Turboprop aircraft offer substantially lower acquisition

costs than regional jet aircraft and, in addition, tend to be more fuel

efficient than other aircraft. We believe this allows us to provide service on

short, lower volume routes and achieve attractive margins, in contrast to

airlines that have focused their fleets on larger regional jet aircraft,

increasingly in the 70- to 90-seat category. The efficiencies associated with

turboprop aircraft are more pronounced on short haul routes such as ours.

Additionally, turboprop aircraft have the ability to operate out of airports

with runways that are too short for certain regional jets.

We

are actively seeking opportunities to grow by adding new routes, aircraft and

alliance partners,. We look for unserved or underserved short haul city pairs

that have a high degree of potential for long-term profitability. These

opportunities will likely include operating in new geographic areas outside our

current Florida base. For example, in October 2008 we added flights from

Continental Airline’s Cleveland hub to five small cities in Pennsylvania, New

York and West Virginia under the Department of Transportation’s Essential Air

Service program. We have held discussions with various parties concerning new

code share arrangements and additional turboprop aircraft. Any potential

transaction involving a new code share partner would require Continental’s prior

consent. There is no assurance that we will be able to reach acceptable terms

with regard to any potential transaction and if we are able to do so, that

Continental would consent to such a transaction.

· Use of alliance and code share

agreements. Utilizing our alliance and code share agreements enhances our

ability to generate revenue for both local and connecting traffic. By having

multiple code share partners, we are able to increase our revenue per flight by

accessing several sources of connecting passengers relative to what would be

available within a single code share partnership arrangement. This is

particularly true given that our main connecting airports are not hubs for any

of our code share partners. These agreements also provide the opportunity to

contract for services at lower costs, as well as to gain access to airport and

other facilities, relative to what we would be able to do

independently.

Further, we believe that by providing

high quality service under our code share partnerships with multiple airlines in

existing markets, our opportunities for expanding the scope of our relationship

with those carriers may be greater.

5

· Increase enrollment at the

Academy. We seek to increase enrollment at the Academy through

implementation of various marketing initiatives. We believe we can enhance

enrollment by increasing cooperation with other regional airlines and primary

flight training centers in order to produce higher levels of applicant

referrals. We also encourage enrollment by developing closer integration with

accredited higher education institutions offering two- and four-year degrees.

Additionally, we seek to attract prospective First Officer candidates from

different sources by offering training services to other regional air carriers

operating similar aircraft types. We also continuously seek to assist

prospective candidates in obtaining tuition financing from third party

sources.

Gulfstream International

Airlines

Markets

Served

Gulfstream

serves a number of short distance, low volume routes in Florida and the Bahamas,

and offers flights from Continental Airline’s Cleveland hub to five small cities

in Pennsylvania, New York and West Virginia. We offer more Bahamian destinations

with more scheduled daily flights than any other U.S. carrier. Further,

Gulfstream is the sole provider of scheduled service on a number of our routes.

Gulfstream’s current route maps are depicted below.

6

As of

December 31, 2009, we provided non-stop service in 31 city pairs. We believe

that we are the highest-frequency service provider in 26 of these 31 city pairs.

We tailor our flight schedules to individual market demands in order to optimize

both profitability and the number of connecting passengers to and from our code

share partners. In 2009, our average fare was $144 and our average flight length

was 216 miles.

All of

our flights are marketed as Continental. In addition, certain flights are also

marketed through our other code share partners. We estimate that over 65% of our

passengers are derived from local “point to point” traffic within Florida and

the Bahamas. The balance of our passengers are derived from connecting traffic

from our code-share partners and other carriers destined primarily for the

Bahamas. Continental is our largest connecting partner, with 24% of our

passengers connecting to and from Continental flights.

Gulfstream

currently leases an average of one Boeing 737-400 daily round

trip under charter agreements associated with our Cuba

operations and two to three daily round trip flights to Andros Island under an

agreement with a government subcontractor. In addition, Gulfstream operates

on-demand charters for various customers throughout the year.

Code Share

Agreements

Continental Code Share

Agreement

Our

primary alliance partner is Continental. Pursuant to an amended and restated

alliance agreement with Continental dated March 14, 2006, which we refer to as

the Continental code share agreement, Gulfstream displays the Continental “CO”

designator code on all of our flights marketed to the public. Our customers may

participate in Continental’s One Pass frequent flyer program.

Under

this agreement, we pay Continental for various services, including ticketing,

reservations, revenue accounting, and various levels of airport services. We

also incur fees for computerized reservation system transactions and

participation in Continental’s frequent flyer program.

7

Gulfstream

receives all of the revenue generated by “local,” or non-connecting, passengers

flown, and a portion of the total revenue from passengers connecting to or from

Continental. Continental sets all prices for connecting markets, and Gulfstream

sets prices for our local markets. Approximately 24% of our passengers are from

connecting Continental flights.

The term

of this agreement will continue through at least May 3, 2012, unless earlier

terminated for cause. Cause is defined to include:

|

·

|

breach

of any material provision of the agreement that is not cured within a

60-day period;

|

|

·

|

suspension

or revocation of our authority to operate as an airline, either in whole

or with respect to the CO-designated

flights;

|

|

·

|

citation

by any government authority for significant noncompliance with any

material marketing or operation law, rule or regulation with respect to a

CO-designated flight;

|

|

·

|

the

filing of a petition in bankruptcy by or against

us;

|

|

·

|

our

failure to maintain required insurance

coverage;

|

|

·

|

our

failure to maintain any of our aircraft in an airworthy

condition;

|

|

·

|

our

failure to conduct operations in accordance with standards, rules and

regulations promulgated by any government authority;

or

|

|

·

|

except

as otherwise agreed by us and Continental, a completion factor by us of

less than 95% during any 21 day period or 50% during any three day period

with respect to Continental flights operated by us (including in such

calculations all flights canceled less than one week prior to the date of

its scheduled operation and excluding flights not completed due to weather

or ATC).

|

In

addition, Continental may terminate the agreement immediately if there is a

change of control, as defined in the agreement, of Gulfstream without

Continental’s prior written consent.

Continental

has not executed its right to appoint an individual to Gulfstream’s board of

directors. It also has the right to observe the Company’s board meetings.

Continental may also receive our audited financial statements, inspect our

books, accounts and records and audit our operational procedures.

Gulfstream

and Continental have agreed to indemnify each other for any damages arising out

of either party’s acts or omissions related to the agreement. Specifically,

Gulfstream has agreed to indemnify Continental for any losses arising from our

possession and use of Continental’s tickets, boarding passes and other

materials, including, but not limited, to lost or forged tickets.

With

certain exceptions, we are required to obtain Continental’s consent to enter

into additional airline code share agreements. We have also agreed to limit

utilization of the United Airlines designator code to specific numbers of

flights and between specific cities.

In

addition to our long-term principal alliance with Continental, we have the

following code share agreements:

United Airlines Code Share

Agreement

We

entered into a code share agreement with United in 1994, which has been amended

several times, most recently in October of 2006. We provide code share

operations with United to and from Tampa, Orlando, Fort Lauderdale, Miami,

Tallahassee, Pensacola, Key West, and Freeport, and Marsh Harbor, and North

Eleuthera, and Nassau, in the North Bahamas. Approximately 4% of our passengers

are from connecting United flights. The agreement may be cancelled

upon 180 days’ written notice, unless either party breaches the agreement, in

which case it may be terminated upon shorter notice.

Revenue

sharing formulas for proration of revenue are set forth in a separate prorate

agreement, which is amended or replaced bi-annually. Our passengers may also

participate in the United frequent flyer program.

Northwest Airlines Code Share

Agreement

Gulfstream

entered into a code share agreement and related prorate agreement, each dated

February 11, 2000, with Northwest. On May 15th 2009

Gulfstream and Northwest executed an agreement to terminate its code-share

agreement. Approximately 1% of our passengers were from connecting

Northwest flights.

8

Copa Code Share

Agreement

We

entered into a code share agreement on July 1, 2005 with Copa Airlines, to

permit us to use the “CM” designator code on Gulfstream’s flights from Miami to

Orlando, Tampa and Key West. The agreement requires us to provide certain

minimal operational standards. Copa Airlines, a Continental alliance partner,

handles reservation services for passengers of CM-designated flights, as it

would for all other Copa Airlines flights, through the Continental reservation

system and provides check-in and ticketing services. We receive a standard

prorated amount for each passenger we fly on a CM-designated flight. To date,

this has not been a material source of our revenue.

Marketing

Under our

code share agreement, Continental provides all reservations and related services

for sales and marketing for CO-designated flights. United and Copa Airlines are

responsible for reservations of connecting passengers marketed under their

respective codes.

We are

responsible for the scheduling of all of our flights and are also responsible

for setting prices and managing revenue for our local passengers. Local

passengers are passengers whose itinerary is not constructed using a single fare

over multiple flight segments. Our code share partners are responsible for

setting prices and managing revenue for our connecting passengers. We retain all

of the revenue associated with our local passengers and a portion of the revenue

associated with connecting passengers pursuant to revenue sharing agreements

with our code share partners.

Flight

Equipment

Our fleet

currently consists of B1900D aircraft. The average age of our B1900D fleet is 15

years. The B1900D aircraft is a 19-seat, twin engine turbo prop that has a

pressurized, stand-up cabin, and cruises at 300 miles per hour. It is ideal for

short trips, and its lower operating costs make it much more economical than

larger mid-sized aircraft for the frequent, short flights that we operate. We

lease 23 B1900Ds under agreements that expire in 2010 and 2011; however, at our

option, we can extend 15 of these leases. We also have the option to purchase up

to 21 of these aircraft.

In

December 2004, we purchased seven EMB-120 aircraft from Atlantic Southeast

Airlines. In March of 2007, we purchased an additional EMB-120, which entered

into revenue service in December 2007. These aircraft were operated until

September and October 2008, when all eight aircraft were sold.

We

believe that our B1900D aircraft fleet is well suited for the markets we serve.

Our turbo-prop aircraft allow us to operate short distance sectors efficiently

and achieve break-even revenues at lower levels than larger jet aircraft. This

allows us to operate more flights per day and target smaller markets, which we

believe provides us with a key advantage at non-hub airports. In addition, by

operating only one aircraft type (since October, 2008), we are able to

simplify our maintenance training, documentation, parts inventory and achieve

lower overall operating costs. The B1900D aircraft are no longer being

manufactured and there is a limited supply of used aircraft of this

type.

Training and

Aircraft Maintenance

Airframe

maintenance performed on our aircraft can be divided into two general

categories: line maintenance and heavy maintenance. Line maintenance consists of

routine, scheduled maintenance checks, including pre-flight, daily and overnight

checks, and any diagnostics and routine repairs. Heavy maintenance consists of

more complex inspections and overhauls, and servicing of the aircraft. Most of

our line maintenance and heavy maintenance is performed by our own highly

experienced technicians at our hangar in Fort Lauderdale. Parts and supply

inventories are primarily maintained in Fort Lauderdale and, in smaller amounts,

at our locations in Miami, Tampa and West Palm Beach in Florida, and Dubois,

Pennsylvania. Some line maintenance is also carried out at other locations in

Florida by employees or third-party contractors. Maintenance checks are

performed in accordance with the guidelines established by the aircraft

manufacturer. These checks are based on the number of hours or calendar months

flown by each individual aircraft.

We employ

over approximately 140 or 24% of our total employees, as maintenance

professionals, including engineers, supervisors, technicians and mechanics and

their support staff, who perform airframe maintenance in accordance with

maintenance programs that are established by the manufacturer and approved and

certified by international aviation authorities. Every mechanic is trained in

manufacturer-specified procedures and goes through our rigorous in-house

training program. Each of our mechanics is licensed by the Federal Aviation

Authority (“FAA”). Our safety and maintenance procedures are reviewed and

periodically audited by the FAA. We have received the FAA Diamond Award, the

highest level of recognition for maintenance training, for 13 consecutive years,

including 2009.

9

We have

agreements for maintaining our engines, propellers, landing gears and avionics

with FAA certified third-party contractors. Our engines are maintained under a

long-term agreement with a third party provider, which provides for engine

maintenance under a fleet management program.

Pricing and

Revenue Management

We

believe effective revenue management, particularly during peak periods,

contributes to our strong operating performance. We are responsible for setting

prices in local markets and our code share partners are responsible for setting

prices in connecting markets. We try to maximize the overall revenue of our

flights by utilizing certain revenue management policies. Our revenue management

systems and procedures enable us to understand markets, anticipate customer

demand and respond quickly to revenue enhancement opportunities.

The

number of seats offered at each fare is established through a continual process

of forecasting and analysis. Generally, past booking history and seasonal trends

are used to forecast anticipated demand. These historical forecasts are combined

with current bookings, upcoming events, competitive pressures and other factors

to establish a mix of fares designed to maximize revenue. This allows us to

balance loads and capture more revenue from existing capacity.

Seasonality

Our

business is subject to substantial seasonality, primarily due to leisure and

holiday travel patterns, particularly in the Bahamas. Traditionally, we

experience the strongest demand from February to July, and the weakest demand

from August to October, during which period we typically suffer operating

losses. As a result, our operating results for a quarterly period are not

necessarily indicative of operating results for an entire year, and historical

operating results are not necessarily indicative of future operating results.

Our results of operations generally reflect this seasonality. Our operating

results are also impacted by numerous other cycles and factors that are not

necessarily seasonal.

Government

Regulation

All

interstate air carriers, including Gulfstream, are subject to regulation by the

Department of Transportation (“DOT”), the FAA and other governmental agencies.

Regulations promulgated by the DOT primarily relate to economic aspects of air

service. The FAA requires operating, air worthiness and other certificates and

certain record-keeping procedures. FAA approval is required for personnel who

engage in flight, maintenance or operating activities and flight training and

retraining programs. Generally, governmental agencies enforce their regulations

through certifications, which are necessary for the continued operations of

Gulfstream, and proceedings, which can result in civil or criminal penalties or

revocation of operating authority. The FAA can also issue maintenance directives

and other mandatory orders relating to, among other things, grounding of

aircraft, inspection of aircraft, installation of new safety-related items and

the mandatory removal and replacement of aircraft parts.

We

believe Gulfstream is operating in compliance with FAA regulations and holds all

necessary operating and airworthiness certificates and licenses. We incur

substantial costs in maintaining current certifications and otherwise complying

with the laws, rules and regulations to which Gulfstream is subject. Our flight

operations, maintenance programs, record keeping and training programs are

conducted under FAA-approved procedures. We do not operate at any airports where

the FAA has restricted landing slots.

All air

carriers are required to comply with federal laws and regulations pertaining to

noise abatement and engine emissions. All air carriers are also subject to

certain provisions of the Federal Communications Act of 1934, as amended,

because of their extensive use of radio and other communication facilities.

Gulfstream is also subject to certain other federal and state laws relating to

protection of the environment, labor relations and equal employment opportunity.

We believe that Gulfstream is in compliance in all material respects with these

laws and regulations.

Safety and

Security

We are

committed to the safety and security of our passengers and employees. Since the

September 11, 2001 terrorist attacks, Gulfstream has taken many steps, both

voluntarily and as mandated by governmental agencies, to increase the safety and

security of our operations. Some of the safety and security measures we have

taken, along with our code share partners, include: establishing a Safety and

Security Committee of the Board of Directors, aircraft security and

surveillance, positive bag matching procedures and enhanced passenger and

baggage screening and search procedures. We are committed to complying with

future safety and security requirements.

10

Charter

Services

Gulfstream

Air Charter, Inc. (“GAC”), a related company which is owned by Thomas L. Cooper,

operates licensed charter flights between Miami and Havana. GAC is licensed by

the Office of Foreign Assets Control of the U.S. Department of the Treasury as a

carrier and travel service provider for charter air transportation between

designated U.S. and Cuban airports.

Pursuant

to a services agreement between Gulfstream and GAC, Gulfstream provides use of

its aircraft and flight crews at the option of GAC, as well as Gulfstream’s

name, insurance, and service personnel, including passenger, ground handling,

security, and administrative. Gulfstream also maintains the financial records

for GAC. Gulfstream receives 75% of the operating profit generated by GAC’s

Cuban charter operation.

In June

2006, Gulfstream began charter services under a long-term subcontract with

Computer Sciences Corporation to operate daily flights between West Palm Beach

and Andros Town, Bahamas. This contract provides for approximately two to three

daily round trips and had an initial period of 21 months from inception, with

extensions up to an additional 12 years. The latest 3-year extension was signed

on April 1, 2008. The contract is structured as a fixed-fee arrangement, with

adjustments for market fuel prices. It further specifies performance standards,

as well as bonus payments for exceeding those standards. As part of this

agreement, Gulfstream leases two B1900D aircraft from Computer Sciences

Corporation to support the contract.

In

preparation for this operation, Gulfstream obtained certification from the

Commercial Airline Review Board of the U.S. Department of Defense (“DOD”).

Having this certification could have the effect of increasing the number of

opportunities for Gulfstream to provide additional charter flights to the

DOD.

Gulfstream

also provides on-demand passenger charter services based on aircraft

availability.

The Academy

The

Academy offers training programs for pilots holding commercial, multi-engine,

and instrument certifications. Pilots with these ratings are qualified to fly

commercial aircraft but seek to improve their marketability by accumulating

additional training and flying time. The Academy enhances our student’s career

prospects by providing them with the training and experience necessary to obtain

pilot positions with commercial airlines.

Traditionally,

pilots can work as flight instructors for up to two years to gain this

additional training and flying time. The Academy offers an alternative to this

traditional means of gathering additional flight experience. By enrolling in the

Academy, students are able to more quickly accumulate the qualifications

demanded by the commercial airlines. A number of U.S. airlines accept Academy

graduates with a lower total flight time than these airlines require of other

newly hired pilots, reflecting the value they place on the Academy’s training.

The Academy graduates have also experienced a high success rate in completing

training at airlines, which translates into cost savings for the

airlines.

The

principal program offered by the Academy is the First Officer Program, which is

a comprehensive program designed to prepare pilots for their commercial airline

careers. The program entails a “train to proficiency” concept, typically

resulting in well over 500 hours of training time, including ground school,

simulator time and observation flights. This first portion of the program can be

completed in three months. The second portion of the program involves up to 400

hours of FAA Regulation Part 121 commercial airline flight hours as a First

Officer at Gulfstream. FAA Regulation Part 121 established operating standards

and is the principal operating regulation applicable to all major US airlines.

Gulfstream relies on the Academy as its preferred source of pilots, and nearly

all of our permanent pilots are graduates of the First Officer

Program.

The

Academy also provides training services to Gulfstream. While the Academy holds a

FAA Part 142 certificate, enabling us to operate a flight training center on

behalf of other airlines, we presently do not provide any training services to

other airlines.

As of

December 31, 2009 the Academy employed five full-time flight and ground

instructors. The Academy’s instructors have, on average, been providing training

for approximately 12 years each and have cumulatively amassed in excess of

68,000 actual flight hours. The Academy enrolled 59 and 42 students in 2008 and

2009, respectively. The Company estimates that 95% were or will be hired by

airlines after graduation, including those hired by Gulfstream.

11

The

Academy’s training facility in Fort Lauderdale has several ground school

classrooms, a series of flight training devices used for procedural training and

cockpit familiarization, as well as two non-motion flight simulators, one of

which is for B1900D aircraft training. The Academy contracts for full-motion

flight simulators at facilities in Orlando, Florida

Ground Operations

In the

Bahamas, we lease ticket counters, check-in and boarding and other facilities

and Gulfstream’s employees provide substantially all of the operations

services.

In Key

West, Florida, we lease our facilities and Gulfstream’s employees provide

operations services. At all other Florida airports, Gulfstream contracts out all

or a portion of our ground operations. From time to time, Gulfstream reviews

these arrangements and evaluates the most economical operations

structure.

In the

markets we serve from Continental’s Cleveland hub, we lease ticket counters,

check-in and boarding and other facilities, and Gulfstream’s employees provide

substantially all of the operations services. We also lease gate and ramp space

in Dubois and Franklin, Pennsylvania, as well as a 20,000 square foot hangar in

Dubois.

Insurance

We

maintain insurance policies that we believe are of types customary in the

industry and in amounts we believe are adequate to protect against material

loss. These policies principally provide coverage for public liability,

passenger liability, baggage and cargo liability, property damage, including

coverage for loss or damage to our flight equipment, and workers’ compensation

insurance. We cannot assure, however, that the amount of insurance we carry will

be sufficient to protect us from a material loss.

Environmental

Matters

We are

subject to various federal, state, local and foreign laws and regulations

relating to environmental protection matters. These laws and regulations govern

such matters as environmental reporting, storage and disposal of materials and

chemicals and aircraft noise. We are, and expect in the future to be, involved

in environmental matters and conditions at, or related to, our properties, but

we do not expect the resolution of any such matters to have a material adverse

effect on the Company’s operations. We are not currently subject to any material

environmental cleanup orders or actions imposed by regulatory authorities. We

are not aware of any active material environmental investigations related to our

assets or properties.

Raw Materials and

Energy

Fuel

costs are a major component of our operating expenses. We contract with World

Fuel Services to provide approximately half of our fuel, principally for

international destinations. Most of our domestic fuel consumption is provided by

Continental. The following chart summarizes our fuel consumption and

costs:

|

|

Years

Ended December 31,

|

|||||||

|

|

2008

|

2009

|

||||||

|

Gallons

consumed, in thousands

|

8,479

|

6,182

|

||||||

|

Total

cost, in thousands (1)

|

$

|

28,452

|

$

|

12,375

|

||||

|

Average

price per gallon (2)

|

$

|

3.36

|

$

|

2.00

|

||||

|

Percent

of airline revenue (3)

|

29.6

|

%

|

16.3

|

%

|

||||

(1)

Total cost excludes into-plane service fees.

(2)

Average price per gallon excludes into-plane service fees.

(3)

Includes into-plane service fees.

12

Fuel

costs are extremely volatile, as they are subject to many global economic and

geopolitical factors that we can neither control nor accurately predict.

Significant increases in fuel costs would have a material adverse effect on our

operating results.

We

purchase bonded fuel for our international flights on a purchase-order basis

from World Fuel Services, which are exempt from federal excise taxes. Therefore,

our fuel costs may not be directly comparable to costs incurred by other

airlines. Gulfstream has, from time to time, implemented limited fuel cost

management programs in the form of pre-ordering of specific quantities of fuel

at specific locations at then-market rates. These cost management programs have

not had a material impact on our financial results.

In the

past, we have not experienced difficulties with fuel availability and we

currently expect to be able to obtain fuel at prevailing market prices in

quantities sufficient to meet our future needs. Pursuant to our contract flying

arrangements with our code share partners, we bear the economic risk of fuel

price fluctuations.

Gulfstream

was a party to derivative instruments for the purpose of hedging the risks of

increases in jet fuel prices through February 2009 covering approximately 20% of

its estimated fuel usage. These fuel hedge contracts were established effective

September 1, 2008 as a requirement of a financing completed at that

time.

Gulfstream

recognized a loss on settled hedges of $337,000 for 2009. We are not a

party to any derivative or other arrangements designed to hedge against or

manage the risk of an increase in fuel prices subsequent to February

2009.

Trademarks and Trade

Names

Our

flights are operated under the names of our code share partners, including

Continental, United Airlines, and Copa Airlines. Because we do not operate

scheduled flights under our trade names, we have not registered any Airline

trademarks or trade names.

Employee and Labor

Relations

As of

December 31, 2009, we had 604 full time employees, of which 592 were employed by

Gulfstream and 12 were employed by the Academy. Of the 592 employees of

Gulfstream, 139 are union employees.

As of

December 31, 2009, Gulfstream employed the following:

|

Classification

|

||||

|

Pilots

and First Officers

|

139 | |||

|

Station

personnel

|

220 | |||

|

Maintenance

personnel

|

142 | |||

|

Administrative

and sales personnel

|

37 | |||

|

Management

|

8 | |||

|

Other

flight operations

|

46 | |||

|

Total

employees

|

592 | |||

Gulfstream’s

tenured pilots are represented under a collective bargaining agreement with the

Teamsters Union. A new agreement was ratified by the members in June 2006 and

continued through June 2009. The Company is currently negotiating the collective

bargaining agreement renewal with the Teamsters Union. Currently, no other

employees are represented by unions. We have never experienced a work stoppage

and no labor disputes, strikes or labor disturbances are currently pending or

threatened against us. We believe we have good relations with our union

employees at each of our facilities. During 2009, we reduced the number of

Pilots and First Officers by approximately 30 employees as a result of declining

demand and the 2008 sale of our eight Embraer aircraft.

As of

December 31, 2009, the Academy employed 7 full-time administrative employees and

4 full-time flight and ground instructors. None of our Academy employees are

represented by labor unions.

13

ITEM 1A. Risk FACTORS.

An

investment in our common stock is risky. You should carefully consider the

following risks, as well as the other information contained in this Form 10-K,

before investing. If any of the following risks actually occurs, our business,

business prospects, financial condition, cash flow and results of operations

could be materially and adversely affected. In this case, the trading price of

our common stock could decline, and you might lose part or all of your

investment. We may amend or supplement the risk factors described below

from time to time by other reports we file with the SEC in the

future.

Risks

Related To Our Industry

If

the global economic downturn continues or worsens, our revenues and

profitability could decline further.

Consumer

demand for our products and services is closely linked to the performance of the

general economy and is sensitive to business and personal discretionary spending

levels. Declines in consumer demand due to adverse general economic conditions,

risks affecting or reducing travel patterns, lower consumer confidence or

adverse political conditions can lower our revenues and

profitability. Our business is also linked to cycles in the general

economy and consumer discretionary spending. As a result, changes in consumer

demand and general business cycles can subject and have subjected our revenues

to significant volatility.

Accordingly,

the current global economic downturn has led to a significant decline in demand

for our services, which has lowered our revenues and negatively affected our

profitability. For the year ended December 31, 2009, compared to the year ended

December 31, 2008, our total revenues decreased by $18.0 million.

We

anticipate that recovery of demand for our services will lag an improvement in

economic conditions. We cannot predict how severe or prolonged the global

economic downturn will be. Furthermore, current global economic conditions have

significantly impacted consumer confidence and behavior and, as a result,

historical marketing information that we have collected may be less effective as

a means of predicting future demand and operating results. We cannot assure you

that we will be able to increase our revenues at the same rate at which they

have recently declined, even after the current downturn ends. An extended period

of economic weakness would likely have a further adverse impact on our revenues,

and financial position, and we my be unable to fund continued operations or

meet our financial obligations.

The airline

industry is unpredictable.

The

airline industry has experienced tremendous challenges in recent years and will

likely remain volatile for the foreseeable future. Among other factors, the

financial challenges faced by major carriers, including Delta Airlines, United

Airlines and Northwest Airlines, and increased hostilities in the Middle East

and other regions have significantly affected, and are likely to continue to

affect, the U.S. airline industry. These conditions have resulted in declines

and shifts in passenger demand, increased insurance costs, volatile fuel prices,

increased government regulations and tightened credit markets, all of which have

affected, and will continue to affect, the operations and financial condition of

participants in the industry, including us, major carriers (including our code

share partners), competitors and aircraft manufacturers. These industry

developments raise substantial risks and uncertainties which will affect us,

major carriers (including our code share partners), competitors and aircraft

manufacturers in ways that we currently are unable to predict.

The airline

industry is subject to the impact of terrorist activities or

warnings.

The

terrorist attacks of September 11, 2001 and their aftermath negatively impacted

the airline industry in general, including our operations. In particular, the

primary effects experienced by the airline industry included a substantial loss

of passenger traffic and revenue. While airline passenger traffic and revenue

have recovered since the terrorist attacks of September 11, 2001, additional

terrorist attacks could have a similar or even more pronounced effect. Even if

additional terrorist attacks are not launched against the airline industry,

there will be lasting consequences of the September 11, 2001 attacks, including

increased security and insurance costs, increased concerns about future

terrorist attacks, increased government regulation and airport delays due to

heightened security. Additional terrorist attacks or warnings of such attacks,

and increased hostilities or prolonged military involvement in the Middle East

or other regions, could negatively impact the airline industry, and result in

decreased passenger traffic and yields, increased flight delays or cancellations

associated with new government mandates, as well as increased security, fuel and

other costs. There can be no assurance that these events will not harm the

airline industry generally or our operations or financial condition in

particular.

14

Our operations

may be adversely impacted by increased security measures mandated by regulatory

authorities.

Because

of significantly higher security and other costs incurred by airports since

September 11, 2001, many airports significantly increased their rates and

charges to air carriers, including us, and may do so again in the future. On

November 19, 2001, the U.S. Congress passed, and the President signed into law,

the Aviation and Transportation Security Act, also referred to as the Aviation

Security Act. This law federalized substantially all aspects of civil aviation

security and created the Transportation Security Administration (“TSA”) to which

the security responsibilities previously held by the Federal Aviation

Administration (“FAA”) were transitioned. The TSA is an agency of the Department

of Homeland Security. The Department of Homeland Security and the TSA and other

agencies within the Department of Homeland Security have implemented numerous

security measures, including the passing of the Aviation Security Act, that

affect airline operations and costs, and are likely to implement additional

measures in the future. The Department of Homeland Security has announced

greater use of passenger data for evaluating security measures to be taken with

respect to individual passengers, expanded use of federal air marshals on

flights (thus displacing revenue passengers), investigating a requirement to

install aircraft security systems (such as active devices on commercial aircraft

as countermeasures against portable surface to air missiles) and expanded cargo

and baggage screening. Funding for airline and airport security required under

the Aviation Security Act is provided in part by a $2.50 per segment passenger

security fee for flights departing from the U.S., subject to a $10 per roundtrip

cap; however, airlines are responsible for costs incurred to meet security

requirements beyond those provided by the TSA. There is no assurance this fee

will not be raised in the future as the TSA’s costs exceed the revenue it

receives from these fees. We could also be adversely affected by any

implementation of stricter security measures by the Bahamian government. Fees

paid to the TSA are approximately 9 months in arrears which could adversely

impact the airline due to a suspension or revocation of the airlines eligibility

for licenses, permits, or privileges. We cannot provide assurance that

additional security requirements or security-related fees enacted in the future

will not adversely affect us financially.

The airline

industry is heavily regulated.

All

interstate airlines are subject to regulation by the Department of

Transportation (the “DOT”), the FAA and other governmental agencies. Regulations

promulgated by the DOT primarily relate to economic aspects of air service. The

FAA requires operating, air worthiness and other certificates; approval of

personnel who may engage in flight, maintenance or operation activities; record

keeping procedures in accordance with FAA requirements; and FAA approval of

flight training and retraining programs. We cannot predict whether we will be

able to comply with all present and future laws, rules, regulations and

certification requirements or that the cost of continued compliance will not

have a material adverse effect on our operations. We incur substantial costs in

maintaining our certifications and otherwise complying with the laws, rules and

regulations to which we are subject. A decision by the FAA to ground, or require

time-consuming inspections of, or maintenance on, all or any of our aircraft for

any reason may have a material adverse effect on our operations. In addition to

state and federal regulation, airports and municipalities enact rules and

regulations that affect our operations. From time to time, various airports

throughout the country have considered limiting the use of smaller aircraft,

such as our aircraft, at such airports. The imposition of any limits on the use

of our aircraft at any airport at which we operate could have a material adverse

effect on our operations. Because we operate only one type of aircraft and have

our operations centered at Fort Lauderdale Airport, we are particularly

susceptible to any such limitations.

The FAA may

change its method of collecting revenues.

The FAA

funds its operations largely through a tax levied on all users of the system

based on ticket sales as well as a tax on fuel. As the airline industry changes,

the trust fund that provides funding for the FAA’s capital accounts and all or

some portion of its operations has experienced an increase in its costs without

a corresponding rise in its revenue such that in its fiscal 2004, the FAA’s

costs exceeded its revenues by more than $4 billion. Further, the existing

authority for the current FAA taxing system expired on September 30, 2007. After

almost two years of short-term extensions and continuing resolutions, the

Subcommittee on Aviation of the House Committee on Transportation and

Infrastructure is presently conducting hearings concerning the FAA. The

committee is hoping to have a long-term funding law in place this year. At times

during this reauthorization process, eliminating or amending the current tax

system and implementing user fees have been discussed that could cause us to

incur potentially significant additional expenses. There can be no assurance

that the final version of the FAA reauthorization bill would exempt small

commercial aircraft such as those operated by Gulfstream from these new charges.

If such a user fee or tax rate increase is implemented, we may not be able to

pass this increased expense on to our customers. Such an expense could have a

material adverse impact on our ability to conduct business.

15

A Senate

draft version of the FAA Reauthorization Bill has proposed a $25 per-flight fee

be charged on all flights, regardless of aircraft size. The recently passed

House version of the Bill does not include such a fee.

The airline

industry is characterized by low profit margins and high fixed

costs.

The

airline industry is characterized generally by low profit margins and high fixed

costs, primarily for personnel, debt service and rent. The expenses of an

aircraft flight do not vary significantly with the number of passengers carried

and, as a result, a relatively small change in the number of passengers or in

pricing could have a disproportionate effect on an airline’s operating and

financial results. Accordingly, a minor shortfall in our expected revenue levels

could harm our business.

The airline

industry is highly competitive.

In

general, the airline industry is highly competitive. Gulfstream not only

competes with other regional airlines, some of which are owned by or operated as

code share partners of major airlines, but we also face competition from low

cost carriers and network airlines on many of our routes. One of our primary

competitors in the Bahamas market, Bahamasair, is owned by the government of the

Bahamas and receives substantial subsidies to fund operating losses. The receipt

of these subsidies may reduce the airline’s requirement to take necessary

actions to improve profitability, including raising prices to offset fuel costs.

Gulfstream also competes with alternative forms of transportation, such as

charter aircraft, automobiles, commercial and private boats and

trains.

Barriers

to entry in most of Gulfstream’s markets are limited, and some of its

competitors are larger and have significantly greater financial and other

resources. Moreover, federal deregulation of the industry allows competitors to

rapidly enter markets and to quickly discount and restructure fares. The airline

industry is particularly susceptible to price discounting because airlines incur

only nominal costs to provide service to passengers occupying otherwise unsold

seats.

Risks

Related To Our Business

We have

substantial fixed obligations.

As of

December 31, 2009, we had $6.3 million of long-term debt and related warrant

liabilities. In addition, we have lease payments of approximately $5.7 million

per year on our fleet of 23 B1900D aircraft, as well as restructured creditor

obligations of $4.2 million for the return of engines borrowed from the lessor,

and other matters, payable over the next several years.

On

February 11, 2010, the Company received a notice of default (the “Default

Notice”) from Raytheon Aircraft Credit Corporation (“RACC”), the Company’s

principal aircraft lessor, pursuant to which RACC notified the Company that the

Company is in default of the payment of certain obligations under Airliner

Operating Lease Agreements, each dated August 7, 2003, and amended on

August 2, 2005, and March 15, 2006 (the “Lease Agreements”), by and

between the Company and RACC, pursuant to which the Company currently leases

from RACC twenty-one (21) Beech 1900D Airliners. The default resulted as a

result of the Company’s failure to make its scheduled lease payments for the

month of February. Accordingly, RACC demanded that the Company make such

payments on or before February 19, 2010. The failure to make such payment

would have given RACC the right to terminate the Lease Agreements, thereby

prohibiting the Company from using such airplanes. Also pursuant to the Default

Notice, RACC claimed that the Company is in default in make certain other

payments under a separate agreement dated as of December 19, 2008 by and

the Company and RACC (the “December Agreement”), which defaults are also

considered to be defaults under the Lease Agreements. RACC indicated in the

Default Notice that if the Company made the required payments under the Lease

Agreements by February 19, 2010, it is prepared to discuss the manner in

which the Company can cure or otherwise address the December Agreement

defaults.

On

February 19, 2010, the Company made the required payment to RACC which

allowed it to continue operating the airplanes covered by the Lease Agreements.

In addition, on February 19, 2010, RACC advised the Company that it would

forebear from exercising any of its rights under the December Agreement or

the Lease Agreements, provided, that the Company remains current in payment of

future lease payments and provides RACC over the next two months with a mutually

acceptable debt and financial restructuring plan that provides for a feasible

basis to enable the Company to continue to meet its ongoing financial

obligations under the Lease Agreement and commence to repay amounts due under

the December Agreement. Although the Company believes that it will be able

to establish a plan that is acceptable to RACC, there can be no assurance that

the Company will be able to do so, or will not otherwise default in future

payments under the Lease Agreements.

16

On February 26, 2010, the Company and

Shelter Island entered into a Forbearance Agreement and Amendment to Debenture

(the “Forbearance Agreement”) which reduced the Company’s potential liability

under the put option from $3,000,000 to $1,050,000 and rescheduled certain

principal and interest payments under the Debenture (as defined below) to reduce

near-term liquidity requirements.

Under the terms of Forbearance

Agreement, Shelter Island agreed to forbear from exercising its rights and

remedies under the Shelter Island Agreement until the occurrence of (a) the

failure by the Company to comply with the terms, covenants and agreements of the

Forbearance Agreement; and (b) the occurrence of any event of default under the

Debenture or the Shelter Island Purchase Agreement (collectively, a “Termination

Event”). One of the covenants to be performed by the Company under

the Forbearance Agreement is the obligation of the Company to raise an

additional $1.5 million of debt or equity financing by March 26, 2010,

subsequently changed to March 31, 2010, or otherwise satisfy Shelter Island

that the Company has adequate liquidity and working capital. Shelter Island

confirmed on March 31, 2010 that the Company complied with this covenant based

primarily on the first closing under a Series A Convertible Preferred Stock

Purchase Agreement.

Pursuant to the Forbearance Agreement

the parties amended the Debenture, as follows (i) the Company shall pay interest

on the outstanding principal amount monthly in cash, commencing March 31, 2010;

(ii) the Company shall pay monthly installments on the outstanding principal

amount commencing April 30, 2010 and on the last trading day of each month

thereafter until the August 31, 2011 maturity date of the Debenture; and (iii)

the Company may prepay all or any portion of the outstanding principal amount of

the Debenture together with a premium equal to 5% of outstanding principal

amount being prepaid; provided that, if such prepayment is made in 2011, there

shall be no premium applicable. The Company, each of its

subsidiaries and Shelter Island also entered into an Omnibus Amendment to the

Guaranty Agreements pursuant to which, without limitation, the parties agreed to

amend the existing guarantees to include the repayment of the Shelter Island

Note (see below).

Shelter Island currently holds a first

priority lien and security interest on all of the assets of the Company and its

subsidiaries. Under the terms of the Intercreditor Agreement, Shelter

Island agreed to subordinate its first priority lien on the accounts receivable

of the Company and its subsidiaries and the proceeds thereof, to the lien

granted to the Investors under the Security Agreement with TBI to the extent of

the deferred principal and accrued interest under the Notes. Shelter

Island retained its first priority security interest in all of the other assets

and properties of the Company and its subsidiaries.

As consideration for its financial

accommodations, the Company paid Shelter Island an additional $250,000 as a

forbearance fee, by delivering a $250,000 promissory note (the “Shelter Island

Note”) due on the earlier of (i) August 31, 2011, and (ii) the date the

Debenture is permitted or required to be paid in accordance with its

terms. The Shelter Island Note accrues interest at a rate of 9% per

annum and is payable in cash on a monthly basis beginning on February 26,

2011.

The

Shelter Island Agreement contains Events of Default, which if not waived by the

lender, would entitle the lender to accelerate the due date of the Senior

Debenture. See Note 20 “Subsequent Events”. The company anticipates not

achieving the “minimum quarterly EBITDA” Events of Default and therefore at

December 31, 2009, the Company classified all future debenture payments as a

short term balance sheet liability.

Although

the Company believes that its revenues and liquidity will improve, the Company

is also actively seeking short-term debt financing to meet its near-term

liquidity requirements and to allow sufficient time to increase its equity

capital base to support long-term growth opportunities. The Company has received

non-binding proposals for additional debt financing which it is seeking to

consummate. In addition, the Company has engaged an investment banking firm to

assist the Company in connection with equity financing efforts.

These

near-term financing transactions and payment deferrals are essential due to our

current liquidity level and several additional factors, including a seasonal

business slowdown that is typical in September and October, the ongoing

risk posed by a relatively weak economy, the potential for continued volatility

in the price of jet fuel, a negotiated settlement of the civil penalty proposed

by the Federal Aviation Administration, and scheduled repayments of debt and

restructured creditor obligations over the next two years.

We can

make no assurance that our near-term efforts to improve liquidity or to obtain a

longer-term growth-oriented equity financing will be completed successfully, or

that alternative sources of capital will be available under terms acceptable to

us, or at all. If an additional financing is not completed in the near-term, we

would experience an immediate and significant liquidity shortfall, and would be

unable to fund operations or meet our financial obligations.

17

Our

debentures and warrants create additional risks and

obligations.

In

September 2008, we consummated a financing in which we issued debentures for

$5.1 million (the “Senior Debentures”) and warrants to purchase 578,870 shares

of common stock (the “Senior Warrants”) to Shelter Island Opportunity Fund, LLC.

As a result of this financing, we face additional risks and uncertainties,

including those relating to the floating interest rate on the Senior Debentures,

the financial covenants of the Senior Debentures, the repayment of the Senior

Debentures and the repurchase of the Senior Warrants.

The

Senior Debentures bear interest at the higher of (i) a floating rate of prime

plus 4% or (ii) a fixed rate of 11%. A significant increase in the prime rate

could cause our interest expense to increase and might impair our ability to

service this debt. In addition, the Senior Debentures subject the Company to

certain covenants, (See Note

20 Subsequent Events) including covenants that we have (i) consolidated

minimum quarterly EBITDA starting in the quarter ending December 31, 2008, (ii)

six month EBITDA averages starting in the six months ending June 30, 2011, (iii)

minimum monthly accounts receivable balance of $3.5 million, and (iv) minimum

monthly cash balance of $750,000. If we are not able to comply with these

covenants, we would be in default under the Senior Debentures and the holder

could elect to accelerate our repayment obligation. On September 30, 2008, we

were in violation of the covenant to maintain a minimum monthly accounts

receivable balance of $3.5 million, with an accounts receivable balance on such

date of $3.1 million. For the quarters ended December 31, 2008, and

2009, we were in violation of the covenant for consolidated minimum