Attached files

| file | filename |

|---|---|

| EX-14 - CODE OF ETHICS - GOLDEN PHOENIX MINERALS INC | gpxm10k20091231ex14.htm |

| EX-31.2 - CERTIFICATION OF CHIEF FINANCIAL OFFICER PURSUANT TO SECTION 302 - GOLDEN PHOENIX MINERALS INC | gpxm10k20091231ex31-2.htm |

| EX-31.1 - CERTIFICATION OF CHIEF EXECUTIVE OFFICER PURSUANT TO SECTION 302 - GOLDEN PHOENIX MINERALS INC | gpxm10k20091231ex31-1.htm |

| EX-32.1 - CERTIFICATION OF CHIEF EXECUTIVE OFFICER AND CHIEF FINANCIAL OFFICER PURSUANT TO 18 U.S.C. SECTION 1350 - GOLDEN PHOENIX MINERALS INC | gpxm10k20091231ex32-1.htm |

UNITED

STATES SECURITIES AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

|

|

R

|

ANNUAL REPORT PURSUANT TO

SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF 1934

|

For

the Fiscal Year Ended December 31, 2009

OR

|

|

£

|

TRANSITION REPORT PURSUANT TO

SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF 1934

|

Commission

File No. 000-22905

GOLDEN

PHOENIX MINERALS, INC.

(Exact

Name of Registrant as Specified in Its Charter)

|

Nevada

|

41-1878178

|

|

|

(State

or Other Jurisdiction

|

(I.R.S.

Employer Identification

|

|

|

Of

Incorporation or Organization)

|

Number)

|

|

|

1675

East Prater Way, Suite 102, Sparks, Nevada

|

89434

|

|

|

(Address

of Principal Executive Offices)

|

(Zip

Code)

|

Registrant’s

telephone number, including area code (775)

853-4919

Securities

registered pursuant to Section 12(g) of the Act:

Common Stock, par value

$0.001 per share

(Title of

Class)

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. Yes o No þ

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the issuer was required to

file such reports), and (2) has been subject to such filing requirements for the

past 90 days. Yes þNo o

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Website, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such

files). Yes oNo o

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. þ

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company. See the definitions of “large accelerated filer,”

“accelerated filer” and “smaller reporting company” in Rule 12b-2 of the

Exchange Act. (Check one):

|

Large

accelerated filer o

|

Accelerated

filer o

|

Non-accelerated

filer o

(Do

not check if a smaller reporting company)

|

Smaller

reporting company þ

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). £ Yes R

No

The

aggregate market value of voting stock held by non-affiliates computed by

reference to the price at which the common equity was last sold as of the last

business day of the registrant’s most recently completed second fiscal quarter,

June 30, 2009, was $4,054,297. For purposes of this computation, it

has been assumed that the shares beneficially held by directors and officers of

registrant were “held by affiliates”; this assumption is not to be deemed to be

an admission by such persons that they are affiliates of

registrant.

The

number of shares of registrant’s common stock outstanding as of April 5, 2010

was 234,328,762.

TABLE OF

CONTENTS

|

PART

I

|

||||

|

ITEM

1.

|

BUSINESS

|

3

|

||

|

ITEM

1A.

|

RISK

FACTORS

|

13 | ||

|

ITEM

1B.

|

UNRESOLVED

STAFF COMMENTS

|

20 | ||

|

ITEM

2.

|

PROPERTIES

|

20 | ||

|

ITEM

3.

|

LEGAL

PROCEEDINGS

|

20 | ||

|

PART

II

|

||||

|

ITEM

5.

|

MARKET

FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER

PURCHASES OF EQUITY SECURITIES

|

22 | ||

|

ITEM

6.

|

SELECTED

FINANCIAL DATA

|

24 | ||

|

ITEM

7.

|

MANAGEMENT’S

DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

|

24 | ||

|

ITEM

7A.

|

QUANTITATIVE

AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

37 | ||

|

ITEM

8.

|

FINANCIAL

STATEMENTS

|

37 | ||

|

ITEM

9.

|

CHANGES

IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND

FINANCIAL DISCLOSURE

|

37 | ||

|

ITEM

9A(T).

|

CONTROLS

AND PROCEDURES

|

37 | ||

|

ITEM

9B.

|

OTHER

INFORMATION

|

38 | ||

|

PART

III

|

||||

|

ITEM

10.

|

DIRECTORS,

EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

39 | ||

|

ITEM

11.

|

EXECUTIVE

COMPENSATION

|

42 | ||

|

ITEM

12.

|

SECURITY

OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED

STOCKHOLDER MATTERS

|

50 | ||

|

ITEM

13.

|

CERTAIN

RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR

INDEPENDENCE

|

51 | ||

|

ITEM

14.

|

PRINCIPAL

ACCOUNTANT FEES AND SERVICES

|

52 | ||

|

PART

IV

|

||||

|

ITEM

15.

|

EXHIBITS

|

53 | ||

|

SIGNATURES

|

54 | |||

PART

I

ITEM

1. BUSINESS

Description

Of Business

As used

in this Annual Report on Form 10-K, unless otherwise indicated, the terms “we,”

“us,” “our” and “the Company” refer to Golden Phoenix Minerals, Inc., a Nevada

corporation.

Forward-Looking

Statements and Associated Risks. This Annual Report on Form 10-K contains

forward-looking statements. Such forward-looking statements include

statements regarding, among other things, (1) our estimates of mineral reserves

and mineralized material, (2) our projected sales and profitability, (3) our

growth strategies, (4) anticipated trends in our industry, (5) our future

financing plans, (6) our anticipated needs for working capital, (7) our lack of

operational experience and (8) the benefits related to ownership of our common

stock. Forward-looking statements, which involve assumptions and

describe our future plans, strategies, and expectations, are generally

identifiable by use of the words “may,” “will,” “should,” “expect,”

“anticipate,” “estimate,” “believe,” “intend,” or “project” or the negative of

these words or other variations on these words or comparable

terminology. These statements constitute forward-looking statements

within the meaning of the Safe Harbor Provisions of the Private Securities

Litigation Reform Act of 1995. This information may involve known and

unknown risks, uncertainties, and other factors that may cause our actual

results, performance, or achievements to be materially different from the future

results, performance, or achievements expressed or implied by any

forward-looking statements. These statements may be found under

“Management’s Discussion and Analysis of Financial Condition and Results of

Operations” as well as in this filing generally. Actual events or

results may differ materially from those discussed in forward-looking statements

as a result of various factors, including, without limitation, the risks

outlined under Item 1A below and other risks and matters described in this

filing and in our other SEC filings. In light of these risks and

uncertainties, there can be no assurance that the forward-looking statements

contained in this filing will in fact occur as projected. We do not

undertake any obligation to update any forward-looking statements.

The

Company

We are a

mineral exploration, development and production company, formed in Minnesota on

June 2, 1997. On September 21, 2007, our shareholders voted in favor

of a Plan of Merger to reincorporate from the State of Minnesota to the State of

Nevada. The reincorporation was completed on May 30,

2008.

Our

business includes acquiring and consolidating mineral properties that we believe

have a high potential for new mineral discoveries and

profitability. Our primary focus is on properties containing gold,

silver and molybdenum that are located in Nevada.

Our main

remaining mining property assets are the Northern Champion molybdenum property

located in Ontario, Canada and the Duff claim block, located adjacent to the

Ashdown Mine in northwestern Nevada. In February 2007, we completed a

purchase agreement with four individuals for the Northern Champion molybdenum

property located in Ontario, Canada, and we plan to take bulk samples for

metallurgical and market testing, and to actively explore and delineate

molybdenum mineralization on the property as funding is

available. With available funding, we also plan to commence a surface

mapping and sampling program covering sections of the 4,400 acres of claims

within the Duff claim block.

3

Some of our more significant recent

events include the following:

· On

March 10, 2010, subsequent to our year end, we closed the Exploration,

Development and Mining Joint Venture Members’ Agreement (the “Members’

Agreement”) entered into on December 31, 2009 with Scorpio Gold Corporation

(“Scorpio Gold”) and its US subsidiary, Scorpio Gold (US) Corporation (“Scorpio

US”). At the closing, we sold Scorpio US an undivided 70% interest in

the Mineral Ridge mineral properties and various related assets (the “Mineral

Ridge Mine”) for a purchase price of $3,750,000 cash (less those amounts

previously advanced to us by Scorpio Gold) and 7,824,750 common shares of stock

of Scorpio Gold at a deemed price of Cdn $0.50 per share. Immediately

following the sale, the Company and Scorpio US each contributed their respective

interests in the Mineral Ridge Mine to a joint venture formed to own and operate

the Mineral Ridge Mine called Mineral Ridge Gold, LLC, a Nevada limited

liability company (the “Mineral Ridge LLC”). We also contributed to

the Mineral Ridge LLC our interest in the reclamation bonds related to the

Mineral Ridge Mine and Scorpio US contributed a net smelter royalty encumbering

the Mineral Ridge Mine, which Scorpio US had acquired simultaneously with the

closing of the Members’ Agreement. We currently own a 30% membership

interest in the Mineral Ridge LLC. Scorpio US owns a 70% membership

interest in, and is the Manager of, the Mineral Ridge LLC, and has agreed to

carry all finance costs necessary to bring the Mineral Ridge Mine into

production and, provided it does so within 30 months of the closing of the

Members’ Agreement, will then have the right to increase its interest in the

Mineral Ridge LLC by 10% to a total of 80%. In the event Scorpio US

qualifies to increase its ownership interest to 80%, it will also have the

option to purchase our then remaining 20% interest for a period of 24 months

following the commencement of commercial production.. There can be no

assurance that Scorpio US will be successful in its ability to raise sufficient

capital to fund the development of the Mineral Ridge Mine and attain a

successful level of operations.

· On

January 25, 2010, we entered into an Employment Separation and Severance

Agreement with David A. Caldwell, our former Chief Executive Officer and

director (the “Caldwell Separation Agreement”). The Caldwell

Separation Agreement provides that Mr. Caldwell will form a new company, Phoenix

Development Group, LLC, a Nevada limited liability company (“PDG”), to operate

as a mine exploration and evaluation enterprise. It is contemplated

that Mr. Caldwell will serve as the Chief Executive Officer and Exploration

Geologist of PDG and that we will own a 25% ownership interest in PDG in

exchange for ongoing monthly cash payments of $7,500 (“PDG Payments”), such

payments to commence 30 days after the formation of PDG and continue on a

monthly basis for a period of 24 months, to be further detailed in a

contribution agreement by and between PDG and the Company at a later

time. Further, pursuant to the Caldwell Separation Agreement, we will

have a right of first refusal to negotiate with PDG for the purchase

of any mining, mineral or exploration property rights identified and acquired by

PDG. In addition, as set forth in the Caldwell Separation Agreement,

PDG can be issued shares of our common stock in lieu of the PDG

Payments. There can be no assurance that PDG will be successful in

its efforts to identify and acquire mineral property rights that will lead to

significant commercial opportunities for us.

· We

suspended the molybdenum mining operations of the Ashdown Project LLC (the

“Ashdown LLC”) in November 2008 in response to a substantial decline of

molybdenum oxide market prices. On May 13, 2009, we completed an

agreement to sell 100% of our ownership interest in the Ashdown LLC. to

Win-Eldrich Gold, Inc. (“WEG”). WEG was a 40% co-owner of the Ashdown

LLC with the Company since inception of the Ashdown LLC in September

2006. The $5.3 million purchase price due the Company will be payable

over a 72 month term, and WEG assumed substantially all of the liabilities of

the Ashdown LLC. There can be no guarantee or assurance that WEG will

be successful in its ability to raise sufficient capital to fund the operations

of the Ashdown LLC, attain a sustained profitable level of operations from the

Ashdown LLC, or pay the Company the $5.3 million promissory

note.

4

The

Company’s mining properties are discussed in further detail below.

Our

corporate directors and officers have prior management experience with large and

small mining companies. We believe that we have created the basis for

a competitive minerals exploration/development and operational company through

assembling a group of individuals with experience in target generation, ore

discovery, resource evaluation, mine development and mine

operations.

We intend

to continue to explore and develop properties. We plan to provide

joint venture opportunities for mining companies to conduct exploration or

development on mineral properties we own or control. We, together

with any future joint venture partners, intend to explore and develop selected

properties to a stage of proven and probable reserves, at which time we would

then decide whether to sell our interest in a property or take the property into

production alone or with our future partner(s). By joint venturing

our properties, we may be able to reduce our costs for further work on those

properties, while continuing to maintain and acquire interests in a portfolio of

gold and base strategic metals properties in various stages of mineral

exploration and development. We expect that this corporate strategy

will minimize the financial risk that we would incur by assuming all the

exploration costs associated with developing any one property, while maximizing

the potential for success and growth.

Sources

of Available Land for Mining and Exploration

There are

at least five sources of land available for exploration, development and mining:

public lands, private fee lands, unpatented mining claims, patented mining

claims, and tribal lands. The primary sources for acquisition of

these lands are the United States government, through the Bureau of Land

Management and the United States Forest Service, state and Canadian Provincial

governments, tribal governments, and individuals or entities that currently hold

title to or lease government and private lands.

There are

numerous levels of government regulation associated with the activities of

exploration and mining companies. Permits, which we are maintaining

and amending include “Notice of Intent” to explore, “Plan of Operations” to

explore, “Plan of Operations” to mine, “Reclamation Permit,” “Air Quality

Permit,” “Water Quality Permit,” “Industrial Artificial Pond Permit,” and

several other health and safety permits. These permits are subject to

amendment or renewal during our operations. Although there is no

guarantee that the regulatory agencies will timely approve, if at all, the

necessary permits for our current operations or other anticipated operations, we

have no reason to believe that necessary permits will not be issued in due

course. The total cost and effects on our operations of the

permitting and bonding process cannot be estimated at this time. The

cost will vary for each project when initiated and could be

material.

The

Federal government owns public lands that are administered by the Bureau of Land

Management or the United States Forest Service. Ownership of the

subsurface mineral estate can be acquired by staking a twenty (20) acre mining

claim granted under the General Mining Law of 1872, as amended (the “General

Mining Law”). The Federal government still owns the surface estate

even though the subsurface can be controlled with a right to extract through

claim staking. Private fee lands are lands that are controlled by

fee-simple title by private individuals or corporations. These lands

can be controlled for mining and exploration activities by either leasing or

purchasing the surface and subsurface rights from the private

owner. Unpatented mining claims located on public land owned by

another entity can be controlled by leasing or purchasing the claims outright

from the owners. Patented mining claims are claims that were staked

under the General Mining Law, and through application and approval the owners

were granted full private ownership of the surface and subsurface estate by the

Federal government. These lands can be acquired for exploration and

mining through lease or purchase from the owners. Tribal lands are

those lands that are under control by sovereign Native American

tribes. Areas that show promise for exploration and mining can be

leased or joint ventured with the tribe controlling the

land.

5

Competition

And Mineral Prices

The

mining industry has historically been intensely competitive and the increasing

price of gold since 2002 has led a number of companies to begin once again to

aggressively acquire claims and properties.

Capital

Equipment and Expenditures

During

the year ended December 31, 2009, our efforts were primarily focused on

completing the sale of our interest in the Ashdown LLC and the formation of the

joint venture related to the Mineral Ridge property; therefore, no material

capital equipment was acquired by us. The operations of our drilling

department, formed in 2008, were suspended during the early portions of 2009

pending additional funding. However, the drilling equipment was

leased to a third-party operator for latter portions of 2009 and successfully

used for exploratory drilling at the Mineral Ridge property. The

equipment is currently idle, pending future drilling opportunities.

Mining

Properties And Projects

With the

sale of our interest in the Ashdown, LLC and the formation of the Mineral Ridge

LLC, our primary mining property assets are the Northern Champion molybdenum

property located in Ontario, Canada and the Duff claims block, located adjacent

to the Ashdown Mine in northwestern Nevada. We also have retained a

30% membership in the Mineral Ridge LLC, which plans to bring the Mineral Ridge

Mine into commercial production.

As

further discussed below, we completed a purchase agreement with four individuals

for the Northern Champion molybdenum property located in Ontario, Canada, and we

plan to take bulk samples for metallurgical and market testing, and to actively

explore and delineate molybdenum mineralization on the property as funding is

available. With available funding, we also plan to commence a surface

mapping and sampling program covering sections of the 4,400 acres of claims

within the Duff claims block.

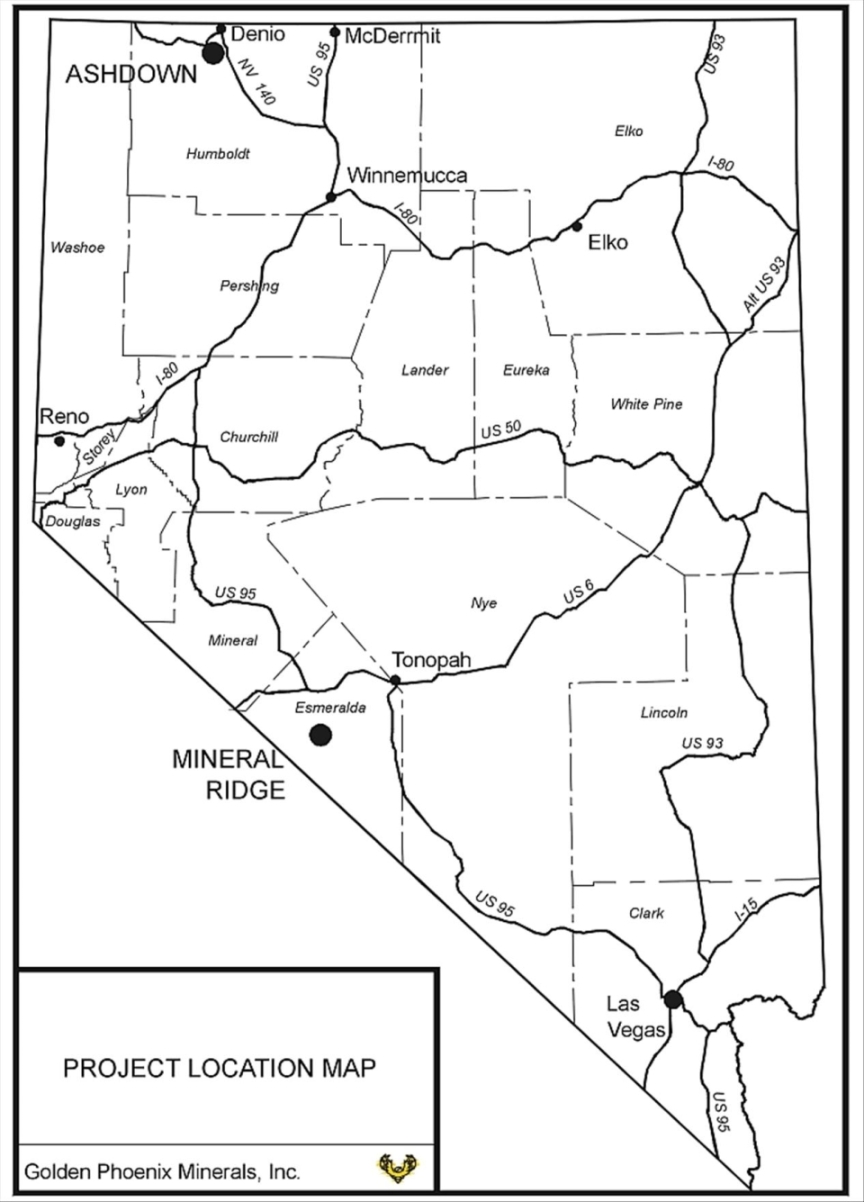

Figures 1 and 2 below display our

mining properties.

6

Figure 1. Map showing the

locations of the Nevada properties discussed in this Annual

Report. Our Duff claims block is located adjacent to the Ashdown

Mine, which we sold our interest in on May 13, 2009, and we currently own a 30%

interest in a joint venture which intends to place the Mineral Ridge Mine in

commercial production.

7

Figure 2. Map showing the

Northern Champion property located within the Province of Ontario, Canada. The

acquisition of this property was completed in February 2007.

8

Northern

Champion Property, Ontario, Canada

The

Northern Champion property consists of approximately 880 acres in Griffith and

Brougham Townships in the Province of Ontario, Canada (“Northern Champion

Property”). On April 18, 2006, we executed a Purchase Agreement with Robert R.

Robitaille, Douglas Lalonde, Sheldon Davis and Ronald E. Dockweiler

(collectively, the “Vendors”) to acquire five (5) registered claims totaling 22

units on the Northern Champion Property together with a NI 43-101 Technical

Report and Feasibility Study describing a molybdenite deposit within the area of

the claims.

Pursuant

to the terms of the agreement, we were obligated to pay $125,000 in four (4)

equal quarterly installments of $31,250 commencing on August 15, 2006. Each

payment was to be distributed as follows, $9,991.50 to Mr. Lalonde, $9,247.45 to

each of Messrs. Robitaille and Davis, and $2,763.61 to Mr. Dockweiler. In

addition, the agreement provided that we would issue 735,000 shares of our

common stock to the Vendors. Mr. Lalonde received 235,000 shares, each of

Messrs. Robitaille and Davis received 217,500 shares and Mr. Dockweiler received

65,000 shares. The agreement also provides that the Vendors will retain a 3.3%

Net Smelter Return (“NSR”) on the sales of minerals taken from the Northern

Champion Property. Each of Messrs. Lalonde, Robitaille and Davis will be

entitled to receive 1% of the Net Smelter Return and Mr. Dockweiler will be

entitled to receive 0.3% of the Net Smelter Return. Additionally, we will have

the right of first refusal to purchase 1.65% of said Net Smelter Return from the

Vendors for $1,650,000. We will have the ability to purchase 0.5% of said Net

Smelter Return from each of Messrs. Lalonde, Robitaille and Davis and 0.15% of

said Net Smelter Return from Mr. Dockweiler.

On

February 12, 2007, the parties agreed to convert the remaining cash payments to

an equivalent number of restricted shares of our common stock valued at the

market close of $0.295 per share on that date. On February 16, 2007, 423,729

restricted shares of our common stock were issued to the Vendors and the

purchase was completed. We now own 100% of the Northern Champion Property

subject to the NSR reserved by the Vendors.

Duff

Claims Block, Humboldt County, Nevada

We own

the Duff claims block comprised of 211 mineral claims located along the western

flank of the Pine Forest Range, 20 miles south of Denio, Humboldt County,

Nevada. The claims block, which was acquired in 2007, abuts the

Ashdown Mine to the north and extends south to the border of the Blue Lake

Wilderness Study Area. The geology of the region is primarily

tertiary cretaceous granites with quartz outcroppings. Metals

historically mined in the general region include gold, molybdenum, copper,

tungsten and antimony.

The major

mine feature of the Duff claims is the Adams Mine, which at one time produced

silica. However, there are historical reports that substantial gold

was also extracted from the quartz rock. Gold has also been mined in

the Vicksburg, Ashdown and Cherry Creek canyons to the north, and Leonard Canyon

to the south of the Duff claims.

Joint

Venture Interest in Mineral Ridge Gold Mine, Esmeralda County,

Nevada

The

Mineral Ridge Mine is located four miles northwest of the town of Silver Peak

and thirty-two miles west of Tonopah in Esmeralda County, Nevada. The property

consists of 54 patented and 140 unpatented mining claims totaling nearly 3,880

acres, or 6 square miles. The property is accessed on the east side from state

highway 265 and on the west side from a well-maintained gravel road. Heavy

trucks access the site from the west entrance by way of state highway 264, which

connects to state highway 773 and U. S. highway 6. Also included are

3 private land parcels, which are located outside the main Mineral

Ridge mine area. These are the abandoned Blair town site, the Silver Peak mill

site, and deeded land west of Mineral Ridge over certain springs. These private

lands total about 430 acres. The total combined acreage is equal to

approximately 6.78 square miles.

9

We

purchased the Mineral Ridge mine in late 2000 out of

bankruptcy. Additional commitments were also assumed, including

obligations to pay advanced royalty payments of $60,000 per year and the annual

permit cost for the Nevada Department of Environmental Protection of

approximately $20,000 during the time the permits were being transferred to us

from the previous operator. We believe that prior mine operators had spent about

$30 million on the property, which includes approximately $18 million in office,

process, and ancillary facilities, about $2 million in engineering and

feasibility studies, about $6 million in drilling and assays, $2 million in past

permitting costs, and the remainder in site preparation.

The

Mineral Ridge property holds three separate potentially economic mineable gold

deposits, the Drinkwater, Mary, and Brodie. We believe that the property holds

further mineral potential with identified targets potentially containing

additional gold mineralization. Operations began in 2003 once the

bond (discussed below) was in place, including adding chemicals to the process

solutions, plumbing the pad with drip lines and main trunk pipes, and mining

both new and old stockpiled materials. Our operations have yielded

certain amounts of precious metal product (dore, a mixture of gold and silver)

that has been sold resulting in revenues of approximately $2.3 million in 2005

and 2004. In January 2005, we temporarily idled the mine pending full

reviews of engineering and metallurgy, and optimization of a revised mine and

operations plan.

In 2001,

Golden Phoenix filed a $1.8 million interim reclamation bond, which allowed the

Company to hold the Mineral Ridge property while other permitting was underway.

We negotiated an interim bond amount to keep the project at status quo until a

new plan and bond amount could be negotiated. On May 8, 2003, we received the

new amended operating permit and on June 23, 2003, we filed a $2.7 million

reclamation bond with the Bureau of Land Management with respect to the Mineral

Ridge mine. We utilized an insurance-backed financial assurance program to

acquire the bond. The program structure includes an insurance policy that will

pay reclamation expenses as they occur. The insurance enabled us to acquire the

necessary reclamation bond at a fixed and discounted rate for a term of 12

years. It also allows us the flexibility to increase the bond in the

future as operations recommence at Mineral Ridge.

As

discussed previously, on March 10, 2010, we closed that certain Exploration,

Development and Mining Joint Venture Members’ Agreement (the “Members’

Agreement”) entered into on December 31, 2009 with Scorpio Gold Corporation

(“Scorpio Gold”) and its US subsidiary, Scorpio Gold (US) Corporation (“Scorpio

US”), pursuant to which we sold Scorpio US an undivided 70% interest in our

Mineral Ridge properties and various related assets (collectively referred to

herein as the “Properties”). At the closing, we received a purchase

price of $3,750,000 in cash (less those sums previously advanced to us by

Scorpio Gold), and 7,824,750 common shares of capital stock of Scorpio Gold at a

deemed price of Cdn $0.50 per share (the “Sale”). Immediately

following the Sale, the Company and Scorpio US each contributed their respective

interests in the Properties to a joint venture entity formed to own the

Properties and conduct operations thereon, called Mineral Ridge Gold, LLC, a

Nevada limited liability company (the “Mineral Ridge LLC”). We also

contributed to the Mineral Ridge LLC our interest in the above-referenced

reclamation bonds related to the Properties and Scorpio US contributed that

certain net smelter return royalty encumbering the Properties (the “NSR”), which

NSR was acquired simultaneous with the closing. In exchange for such

contributions, we obtained an initial 30% ownership interest in the Mineral

Ridge LLC and Scorpio US obtained an initial 70% ownership interest in the

Mineral Ridge LLC.

10

Scorpio

US is the Manager of the Mineral Ridge LLC and has agreed to carry all finance

costs necessary to bring the Properties into commercial production and, provided

it does so within 30 months of the Closing, will then have the right to increase

its joint venture interest in the Mineral Ridge LLC by 10% to a total of

80%. In the event Scorpio US qualifies to increase its ownership

interest in the LLC to 80%, it will also have the option to purchase the

Company’s then-remaining 20% interest for a period of 24 months following the

commencement of commercial production.

Bridge

Loan and Debt Restructuring Agreement

As

further detailed below under the section entitled Results of Operations within

the Management’s Discussion and Analysis of Financial Condition and Results of

Operations, on January 30, 2009, we entered into a Bridge Loan and Debt

Restructuring Agreement with one of our investors, Crestview Capital Master, LLC

(“Crestview”), whereby we entered into a bridge loan and a restructuring of

certain original debt owed by the Company to Crestview. The bridge

loan, in the principal amount of $1,000,000, was secured by an interest in the

Mineral Ridge property and was repaid in full at the closing of the joint

venture transaction with Scorpio US on March 10, 2010, at which time Crestview

released its security interest in the property. Crestview maintains

an ongoing security interest in our ownership interest in the Mineral Ridge LLC

until we pay in full the debt restructuring promissory note in the principal

amount of $1,000,000 plus interest accrued thereon, which has a maturity date of

August 6, 2010. Further, we issued Crestview an irrevocable

assignment of fifty percent (50%) of our right to any proceeds from

distributions made by the Mineral Ridge LLC, to be applied as a mandatory

prepayment on the debt restructuring promissory note.

Alaskan

Royalties

We own a

1% net smelter return royalty on two properties located in Alaska, Glory Creek

and Uncle Sam. We are not required to perform any work or make any

payments for these royalties.

The Glory

Creek property is 100% controlled by Great American Mineral Exploration, Inc.

(“GAME”). It is located in the Bonnifield mining district, about 60

miles south of Fairbanks. Exploration work on the property has

defined an anomalous zone of gold mineralization that requires drilling for the

next phase of work. We do not know if or when a discovery of gold

mineralization will be made.

The Uncle

Sam property is also 100% controlled by GAME. The property is located

in the Richardson Gold District, about 60 miles southeast of

Fairbanks. Their work has defined a strongly anomalous gold zone that

requires drilling for the next phase of work. Sumitomo and Kennecott

acquired claims that abut the GAME position, and work by these entities and

their Joint Venture partners have produced very strong results. We do

not know if or when a discovery of gold mineralization will be

made.

Preliminary

negotiations have been entered with GAME to explore the conversion of these

royalty interests into an equity stake in this private company. It is

not certain what the outcome of these discussions will be.

Discontinued

Ashdown Operations

On

February 25, 2009, we entered into a Binding Memorandum of Understanding as well

as two related binding side letter agreements (collectively, the “MOU”) with

Win-Eldrich Gold, Inc. (“WEG”) , whereby we agreed to sell 100% of our ownership

interest in the Ashdown LLC to WEG (the “Ashdown Sale”). WEG was a

co-owner of the Ashdown LLC with the Company since the inception of the Ashdown

LLC in September 2006, with the Company owning a 60% membership interest and WEG

owning a 40% membership interest. The Ashdown LLC placed the Ashdown

property into commercial operation in December 2006, and had sales of

molybdenite concentrates of $10,398,361 for the year ended December 31, 2007 and

sales of $10,537,370 during 2008 prior to suspension of operations in November

2008 due to significant declines in the market price of

molybdenum.

11

On May

13, 2009, pursuant to the material terms of the MOU, as further revised,

negotiated and mutually agreed to by the Parties, we entered into definitive

agreements that superseded the MOU, including a Purchase and Sale of LLC

Membership Interest Agreement with WEG, to effectuate the Ashdown Sale (the

“Purchase Agreement”). As consideration for the Ashdown Sale and the

Parties’ mutual release of certain claims against the other pursuant to the

terms of a Settlement and Release Agreement (the “Release”), WEG will pay $5.3

million (the “Purchase Price”) to the Company, which will be satisfied by the

issuance of a Limited Recourse Secured Promissory Note (the “Note”), for the

full amount of the Purchase Price.

In

particular, WEG will pay the Company $5.3 million and assume the majority of all

obligations and liabilities held by the LLC, all as detailed and more fully set

forth in the Purchase Agreement. Pursuant to the terms and conditions

of the Purchase Agreement and the Note, the Company, WEG and the LLC have also

entered into a Security Agreement, a Short Form Deed of Trust and Assignment of

Rents Agreement (the “Deed of Trust”), and certain other releases and side

letter agreements (together with the Purchase Agreement and the Note,

collectively, the “Transaction Documents”).

The terms

and conditions of the Note, including term, interest rate and description of

security interest are as follows: the terms of the Note include the payment of

the Purchase Price together with simple interest on the unpaid principal amount

of the Note at rate equal to the Wall Street Journal Prime rate plus two percent

(2.00%), computed on a quarterly basis beginning April 1, 2009, for a term of 72

months, with the first payment due one (1) year from the date of

Closing. As security for the Note, the Purchase Price shall be

secured by the assets and property of the LLC as well as one hundred percent

(100%) of WEG’s ownership interest in the LLC (the “Collateral”). The

sole recourse of the Company under the Note for the collection of amounts owed

and in the event of default shall be foreclosure as to the Collateral, as

further detailed in the Security Agreement and Deed of Trust by and between the

Parties.

Because

of the current uncertainty of collecting the Note or realizing any value from

the assets and property of the LLC upon foreclosure, the Note has been reduced

100% by an allowance account and recorded at no value in the accompanying

consolidated balance sheet as of December 31, 2009, and no gain on disposition

of our interest in the Ashdown LLC attributed to the $5.3 million Note has been

recorded in the accompanying consolidated statements of operations for the year

ended December 31, 2009. We did, however, record a loss on sale of

interest in joint venture of $235,303 for year ended December 31, 2009 resulting

from our assumption of certain liabilities in the transaction and the

elimination of all investment and loan accounts related to the Ashdown

LLC. Further gain, if any, on disposition of the interest in the

Ashdown LLC will be recorded as cash payments are received on the Note or, if

required, upon disposition of any assets or property of the Ashdown LLC due to

foreclosure on the Note.

Pursuant

to the Release, the Parties agreed to terminate any and all litigation and

ongoing disputes existing between the Parties effective at Closing.

Finally,

pursuant to the Purchase Agreement, Perry Muller, President of WEG, or his

assignee, agreed to pay up to $100,000 of all payments made in settlement of the

amounts owed by the Ashdown LLC to Retrievers LLC, and we secured a release from

Retrievers LLC of any claim or title in or to the Ashdown Mill property, with

Mr. Muller becoming the sole owner of the Ashdown Mill property (the “Retriever’s

Settlement”). Upon completion of the Retriever’s Settlement, Mr.

Muller agreed to lease the Ashdown Mill property to the Ashdown LLC and convey

the Ashdown Mill to the Ashdown LLC upon repayment to Mr. Muller by the Ashdown

LLC of $100,000, plus a loan fee amount of $10,000, all as pursuant to that

certain Ashdown Mill Binding Side Letter Agreement, dated May 13,

2009.

12

Employees

Corporate

Office

We have 2

key professionals and 2 support staff to perform management functions. We intend

to employ independent contractors to fulfill short-term needs for accounting,

permitting, and other administrative functions, and may staff further with

employees as we bring new projects on line.

Drilling

Services Division

We have

suspended the operations of our drilling services division, pending additional

funding and project opportunities, and currently do not have any employees in

this division.

ITEM 1A. RISK FACTORS

The risks

described below are the ones we believe are most important for you to

consider. These risks are not the only ones that we

face. If events anticipated by any of the following risks actually

occur, our business, operating results or financial condition could suffer and

the price of our common stock could decline.

We Have A Limited Operating History

With Significant Losses And Expect Losses To Continue For The Foreseeable

Future.

We have

yet to establish any history of profitable operations. We have incurred net

losses of $2,798,747 and $7,056,582 for the years ended December 31, 2009 and

2008, respectively. As a result, at December 31, 2009 we had an

accumulated deficit of $47,421,049 and a total stockholders’ deficit of

$6,355,454. Our revenues have not been sufficient to sustain our

operations. We recently sold our member interest in the Ashdown

LLC. The Ashdown LLC has been the only source of our operating

revenues for the past three years. We expect that our revenues will

not be sufficient to sustain our operations for the foreseeable

future. Our profitability will require the successful

commercialization of our mineral interest. We may not be able to successfully

commercialize our mineral interests or ever become profitable.

There Is Doubt About Our Ability To

Continue As A Going Concern Due To Recurring Losses From Operations,

Accumulated Deficit And Working Capital Deficit All Of Which Means That We

May Not Be Able To Continue Operations.

Our

independent auditors have added an explanatory paragraph to their audit opinion

issued in connection with our consolidated financial statements for the years

ended December 31, 2009 and 2008 with respect to the uncertainty of our ability

to continue as a going concern. As discussed in Note 2 to our

consolidated financial statements for the year ended December 31, 2009, we have

generated significant losses from operations, and had an accumulated deficit of

$47,421,049 and a total stockholders’ deficit of $6,355,454 at December 31,

2009, which together raises doubt about our ability to continue as a going

concern. Management’s plans in regard to these matters are also

described in Note 2 to our consolidated financial statements for the year ended

December 31, 2009.

13

The

Consideration Received From The Sale Of Our Interest In The Ashdown LLC Is A

Promissory Note For $5.3 million, The Collection Of Which Is

Uncertain.

As

consideration for the sale of our interest in the Ashdown LLC on May 13, 2009,

WEG is obligated to pay us $5.3 million , which was satisfied by the issuance of

a Limited Recourse Secured Promissory Note. The Note bears interest

at a rate equal to the Wall Street Journal Prime rate plus 2.0%, computed on a

quarterly basis beginning April 1, 2009, for a term of 72 months, with the first

payment due May 13, 2010. The Note is secured by the assets and

property of the LLC as well as 100% of WEG’s ownership interest in the

LLC. Our sole recourse under the Note for the collection of amounts

owed and in the event of default shall be foreclosure as to the collateral, as

further detailed in the Security Agreement and Deed of Trust by and between the

Parties. Because of the current uncertainty of collecting the Note or

realizing any value from the assets and property of the LLC upon foreclosure,

the Note has been reduced 100% by an allowance account and recorded at no value

in the accompanying consolidated balance sheet as of December 31, 2009, and no

gain on disposition of our interest in the Ashdown LLC attributed to the $5.3

million Note has been recorded in the accompanying consolidated statements of

operations for the year ended December 31, 2009.

The

Mineral Ridge LLC Has Been Recently Formed And Its Ultimate Success Is

Uncertain

We

currently own a 30% membership interest in the Mineral Ridge LLC which was

formed on March 10, 2010. Scorpio US owns a 70% membership interest

in and is the Manager of the Mineral Ridge LLC, and has agreed to carry all

finance costs necessary to bring the Mineral Ridge Mine into production and,

provided it does so within 30 months of the closing of the Members’ Agreement,

will then have the right to increase its interest in the Mineral Ridge LLC by

10% to a total of 80%. In the event Scorpio US qualifies to increase

its ownership interest to 80%, it will also have the option to purchase our then

remaining 20% interest for a period of 24 months following the commencement of

commercial production.. There can be no assurance that Scorpio US

will be successful in its ability to raise sufficient capital to fund the

development of the Mineral Ridge Mine and attain a successful level of

operations.

We

May Not Have Access To Capital In The Future As A Result Of Disruptions In

Capital And Credit Markets.

Our

ability to access capital or credit necessary to continue operations may be

hindered by the continuing difficulties in the capital and credit markets both

in the U.S. and internationally. Moreover, longer term volatility and

continued disruptions in the capital and credit markets as a result of

uncertainty, changing or increased regulation of financial institutions, reduced

alternatives or failures of significant financial institutions could affect

adversely our access to the liquidity needed for our business in the longer

term. Such disruptions could require us to take measures to conserve

cash until the markets stabilize or until alternative credit arrangements or

other funding for our business needs can be arranged. The disruptions

in the capital and credit markets have also resulted in higher interest rates on

publicly issued debt securities and increased costs under credit

facilities. The continuation of these disruptions could increase our

interest expense and capital costs and could affect adversely our results of

operations and financial position including our ability to grow our business

through joint ventures, sales or acquisitions.

We

May Not Be Able To Secure Additional Financing To Meet Our Future Capital Needs

Due To Changes In General Economic Conditions.

We

anticipate needing significant capital to conduct further exploration and

development needed to bring our existing mining properties into production, meet

certain debt obligations and/or to continue to seek out

appropriate joint venture partners or buyers for certain mining

properties. We may use capital more rapidly than currently

anticipated and incur higher operating expenses than currently expected, and we

may be required to depend on external financing to satisfy our operating and

capital needs. We may need new or additional financing in the future

to conduct our operations or expand our business. Any sustained

weakness in the general economic conditions and/or financial markets in the

United States or globally could affect adversely our ability to raise capital on

favorable terms or at all. From time to time we have relied, and may

also rely in the future, on access to financial markets as a source of liquidity

to satisfy working capital requirements and for general corporate

purposes. We may be unable to secure additional debt or equity

financing on terms acceptable to us, or at all, at the time when we need such

funding. If we do raise funds by issuing additional equity or

convertible debt securities, the ownership percentages of existing stockholders

would be reduced, and the securities that we issue may have rights, preferences

or privileges senior to those of the holders of our common stock or may be

issued at a discount to the market price of our common stock which would result

in dilution to our existing stockholders. If we raise additional

funds by issuing debt, we may be subject to debt covenants, which could place

limitations on our operations including our ability to declare and pay

dividends. Our inability to raise additional funds on a timely basis

would make it difficult for us to achieve our business objectives and would have

a negative impact on our business, financial condition and results of

operations.

14

We

May Not Be Able to Bring Our Obligations Current.

Due to

the financial hardships we faced with the discontinuance of operations at

Ashdown and subsequent sale of our membership interest in the Ashdown LLC,

certain vendors and lenders of the Company have initiated actions to collect

balances that are passed due. We are attempting to negotiate mutually

beneficial settlements with such vendors and lenders. However, in the

event that we do not have or are unable to raise sufficient capital to bring our

obligations current or cannot negotiate settlements, we will experience

difficulty in achieving our business objectives and will likely experience a

negative impact on our business, financial condition and results of

operations.

The

Validity Of Our Unpatented Mining Claims Could Be Challenged, Which Could Force

Us To Curtail Or Cease Our Business Operations.

A

majority of our properties consist of unpatented mining claims, which we own or

lease. These claims are located on federal land or involve mineral

rights that are subject to the claims procedures established by the General

Mining Law. We must make certain filings with the county in which the

land or mineral is situated and with the Bureau of Land Management and pay

annual holding fees of $133.50 per claim. If we fail to make the

annual holding payment or make the required filings, our mining claim could be

void or voidable. Because mining claims are self-initiated and

self-maintained rights, they are subject to unique vulnerabilities not

associated with other types of property interests. It is difficult to

ascertain the validity of unpatented mining claims from public property records

and, therefore, it is difficult to confirm that a claimant has followed all of

the requisite steps for the initiation and maintenance of a

claim. The General Mining Law requires the discovery of a valuable

mineral on each mining claim in order for such claim to be valid, and rival

mining claimants and the United States may challenge mining

claims. Under judicial interpretations of the rule of discovery, the

mining claimant has the burden of proving that the mineral found is of such

quality and quantity as to justify further development, and that the deposit is

of such value that it can be mined, removed and disposed of at a

profit. The burden of showing that there is a present profitable

market applies not only to the time when the claim was located, but also to the

time when such claim’s validity is challenged. However, only the

federal government can make such challenges; they cannot be made by other

individuals with no better title rights than us. It is therefore

conceivable that, during times of falling metal prices, claims that were valid

when they were located could become invalid if challenged. Title to

unpatented claims and other mining properties in the western United States

typically involves certain other risks due to the frequently ambiguous

conveyance history of those properties, as well as the frequently ambiguous or

imprecise language of mining leases, agreements and royalty

obligations. No title insurance is available for

mining. In the event we do not have good title to our properties, we

would be forced to curtail or cease our business

operations.

15

Environmental Controls Could Curtail

Or Delay Exploration And Development Of Our Mines And Impose Significant

Costs On Us.

We are

required to comply with numerous environmental laws and regulations imposed by

federal and state authorities. At the federal level, legislation such

as the Clean Water Act, the Clean Air Act, the Resource Conservation and

Recovery Act, the Comprehensive Environmental Response Compensation Liability

Act and the National Environmental Policy Act impose effluent and waste

standards, performance standards, air quality and emissions standards and other

design or operational requirements for various components of mining and mineral

processing, including molybdenum, gold and silver mining and

processing. In addition, insurance companies are now requiring

additional cash collateral from mining companies in order for the insurance

companies to issue a surety bond. This addition of cash collateral

for a bond could have a significant impact on our ability to bring properties

into production.

Many

states, including the State of Nevada (where our Mineral Ridge and Ashdown

properties are located), have also adopted regulations that establish design,

operation, monitoring, and closing requirements for mining

operations. Under these regulations, mining companies are required to

provide a reclamation plan and financial assurance to ensure that the

reclamation plan is implemented upon completion of mining

operations. Additionally, Nevada and other states require mining

operations to obtain and comply with environmental permits, including permits

regarding air emissions and the protection of surface water and

groundwater. Although we believe that we are currently in compliance

with applicable federal and state environmental laws, changes in those laws and

regulations may necessitate significant capital outlays or delays, may

materially and adversely affect the economics of a given property, or may cause

material changes or delays in our intended exploration, development and

production activities. Any of these results could force us to curtail

or cease our business operations.

Proposed Legislation Affecting The

Mining Industry Could Have An Adverse Effect On Us.

During

the past several years, the United States Congress considered a number of

proposed amendments to the General Mining Law of 1872, which governs mining

claims and related activities on federal lands. For example, a broad

based bill to reform the General Mining Law of 1872, the Hardrock Mining and

Reclamation Act of 2007 (H.R. 2262) was introduced in the U.S. House of

Representatives on May 10, 2007 and was passed by the U.S. House of

Representatives on November 1, 2007, and has been submitted to the U.S. Senate

where no action has been taken to date.

In 1992,

a federal holding fee of $100 per claim was imposed upon unpatented mining

claims located on federal lands. This fee was increased to $125 per

claim in 2005 ($133.50 total with the accompanying County fees

included). Beginning in October, 1994, a moratorium on processing of

new patent applications was approved. In addition, a variety of

legislation over the years has been proposed by the United States Congress to

further amend the General Mining Law. If any of this legislation is

enacted, the proposed legislation would, among other things, change the current

patenting procedures, limit the rights obtained in a patent, impose royalties on

unpatented claims, and enact new reclamation, environmental controls and

restoration requirements.

For

example, the Hardrock Mining and Reclamation Act of 2007 (H.R. 2262), if

enacted, would have several negative impacts on the Company including but not

limited to: requiring royalty payments of 8% of

gross income from mining a claim on Federal land, or 4% of claims on Federal

land that existed prior to the passage of this act; and prohibition of certain

areas from being open to the location of mining claims, including wilderness

study areas, areas of critical environmental concern, areas included in the

National Wild and Scenic Rivers System, and any area included in maps made for

the Forest Service Roadless Area Conservation Final Environmental Impact

Statement.

16

The

extent of any such changes to the General Mining Law of 1872 that may be enacted

is not presently known, and the potential impact on us as a result of future

congressional action is difficult to predict. If enacted, the

proposed legislation could adversely affect the economics of developing and

operating our mines because many of our properties consist of unpatented mining

claims on federal lands. Our financial performance could therefore be

materially and adversely affected by passage of all or pertinent parts of the

proposed legislation, which could force us to curtail or cease our business

operations.

The Development And Operation Of Our

Mining Projects Involve Numerous Uncertainties.

Mine

development projects, including our planned projects, typically require a number

of years and significant expenditures during the development phase before

production is possible.

Development

projects are subject to the completion of successful feasibility studies,

issuance of necessary governmental permits and receipt of adequate

financing. The economic feasibility of development projects is based

on many factors such as:

|

|

•

|

estimation

of reserves;

|

|

|

•

|

anticipated

metallurgical recoveries;

|

|

|

•

|

future

molybdenum, gold and silver prices;

and

|

|

|

•

|

anticipated

capital and operating costs of such

projects.

|

Our mine

development projects may have limited relevant operating history upon which to

base estimates of future operating costs and capital

requirements. Estimates of proven and probable reserves and operating

costs determined in feasibility studies are based on geologic and engineering

analyses.

Any of

the following events, among others, could affect the profitability or economic

feasibility of a project:

|

|

•

|

unanticipated

changes in grade and tonnage of material to be mined and

processed;

|

|

|

•

|

unanticipated

adverse geotechnical conditions;

|

|

|

•

|

incorrect

data on which engineering assumptions are

made;

|

|

|

•

|

costs

of constructing and operating a mine in a specific

environment;

|

|

|

•

|

availability

and cost of processing and refining

facilities;

|

|

|

•

|

availability

of economic sources of power;

|

|

|

•

|

adequacy

of water supply;

|

17

|

|

•

|

adequate

access to the site;

|

|

|

•

|

unanticipated

transportation costs;

|

|

|

•

|

government

regulations (including regulations relating to prices, royalties, duties,

taxes, restrictions on production, quotas on exportation of minerals, as

well as the costs of protection of the environment and agricultural

lands);

|

|

|

•

|

fluctuations

in metal prices; and

|

|

|

•

|

accidents,

labor actions and force majeure

events.

|

Any of

the above referenced events may necessitate significant capital outlays or

delays, may materially and adversely affect the economics of a given property,

or may cause material changes or delays in our intended exploration, development

and production activities. Any of these results could force us to

curtail or cease our business operations.

Mineral Exploration Is Highly

Speculative, Involves Substantial Expenditures, And Is Frequently

Non-Productive.

Mineral

exploration involves a high degree of risk and exploration projects are

frequently unsuccessful. Few prospects that are explored end up being

ultimately developed into producing mines. To the extent that we

continue to be involved in mineral exploration, the long-term success of our

operations will be related to the cost and success of our exploration

programs. We cannot assure you that our mineral exploration efforts

will be successful. The risks associated with mineral exploration

include:

|

|

•

|

The

identification of potential economic mineralization based on superficial

analysis;

|

|

|

•

|

the

quality of our management and our geological and technical expertise;

and

|

|

|

•

|

the

capital available for exploration and

development.

|

Substantial

expenditures are required to determine if a project has economically mineable

mineralization. It may take several years to establish proven and

probable reserves and to develop and construct mining and processing

facilities. Because of these uncertainties, our current and future

exploration programs may not result in the discovery of reserves, the expansion

of our existing reserves or the further development of our mines.

The Price Of Molybdenum, Gold and

Silver are Highly Volatile And A Decrease In The Price Of Molybdenum, Gold or Silver

Would Have A Material Adverse Effect On Our Business.

The

profitability of mining operations is directly related to the market prices of

metals. The market prices of metals fluctuate significantly and are

affected by a number of factors beyond our control, including, but not limited

to, the rate of inflation, the exchange rate of the dollar to other currencies,

interest rates, and global economic and political conditions. Price

fluctuations of metals from the time development of a mine is undertaken to the

time production can commence can significantly affect the profitability of a

mine. Accordingly, we may begin to develop one or more of our mines

at a time when the price of metals makes such exploration economically feasible

and, subsequently, incur losses because the price of metals

decreases. Adverse fluctuations of the market prices of metals may

force us to curtail or cease our business operations.

18

Our Mineral Reserve Estimates are

Potentially Inaccurate.

We

estimate our mineral reserves on our properties as either “proven reserves” or

“probable reserves.” Our mineral reserve figures and costs are

primarily estimates and are not guarantees that we will recover the indicated

quantities of these metals. We estimate proven reserve quantities

based on sampling and testing of sites conducted by us and by independent

companies hired by us. Probable reserves are based on information

similar to that used for proven reserves, but the sites for sampling are less

extensive, and the degree of certainty is less. Reserve estimation is

an interpretive process based upon available geological data and statistical

inferences and is inherently imprecise and may prove to be

unreliable.

Our

reserves are reduced as existing reserves are depleted through

production. Reserves may be reduced due to lower than anticipated

volume and grade of reserves mined and processed and recovery

rates.

Reserve

estimates are calculated using assumptions regarding metals

prices. These prices have fluctuated widely in the

past. Declines in the market price of metals, as well as increased

production costs, capital costs and reduced recovery rates, may render reserves

uneconomic to exploit. Any material reduction in our reserves may

lead to increased net losses, reduced cash flow, asset write-downs and other

adverse effects on our results of operations and financial

condition. Reserves should not be interpreted as assurances of mine

life or of the profitability of current or future operations. No

assurance can be given that the amount of metal estimated will be produced or

the indicated level of recovery of these metals will be realized.

Mining Risks And Insurance Could Have

An Adverse Effect On Our Profitability.

Our

operations are subject to all of the operating hazards and risks normally

incident to exploring for and developing mineral properties, such as unusual or

unexpected geological formations, environmental pollution, personal injuries,

flooding, cave-ins, changes in technology or mining techniques, periodic

interruptions because of inclement weather and industrial

accidents. Although we currently maintain insurance to ameliorate

some of these risks, more fully described in the description of our business in

this filing, such insurance may not continue to be available at economically

feasible rates or in the future be adequate to cover the risks and potential

liabilities associated with exploring, owning and operating our

properties. Either of these events could cause us to curtail or cease

our business operations.

The Market Price Of Our Common Stock

Is Highly Volatile, Which Could Hinder Our Ability To Raise Additional

Capital.

The

market price of our common stock has been and is expected to continue to be

highly volatile. Factors, including regulatory matters, concerns

about our financial condition, operating results, litigation, government

regulation, developments or disputes relating to agreements, title to our

properties or proprietary rights, may have a significant impact on the market

price of our stock. The range of the high and low bid prices of our

common stock over the last three (3) years has been between $0.35 and

$0.01. In addition, potential dilutive effects of future sales of

shares of common stock by shareholders and by us, and subsequent sale of common

stock by the holders of warrants and options could have an adverse effect on the

price of our securities, which could hinder our ability to raise additional

capital to fully implement our business, operating and development

plans.

19

Penny Stock Regulations Affect Our

Stock Price, Which May Make It More Difficult For Investors To Sell Their

Stock.

Broker-dealer

practices in connection with transactions in “penny stocks” are regulated by

certain penny stock rules adopted by the SEC. Penny stocks generally

are equity securities with a price per share of less than $5.00 (other than

securities registered on certain national securities exchanges or quoted on the

NASDAQ Stock Market, provided that current price and volume information with

respect to transactions in such securities is provided by the exchange or

system). The penny stock rules require a broker-dealer, prior to a

transaction in a penny stock not otherwise exempt from the rules, to deliver a

standardized risk disclosure document that provides information about penny

stocks and the risks in the penny stock market. The broker-dealer

must also provide the customer with current bid and offer quotations for the

penny stock, the compensation of the broker-dealer and its salesperson in the

transaction, and monthly account statements showing the market value of each

penny stock held in the customer’s account. In addition, the penny

stock rules generally require that prior to a transaction in a penny stock the

broker-dealer make a special written determination that the penny stock is a

suitable investment for the purchaser and receive the purchaser’s written

agreement to the transaction. These disclosure requirements may have

the effect of reducing the level of trading activity in the secondary market for

a stock that becomes subject to the penny stock rules. Our securities

are subject to the penny stock rules, and investors may find it more difficult

to sell their securities.

ITEM

1B. UNRESOLVED STAFF COMMENTS

Not applicable.

ITEM

2. PROPERTIES

Our

principal executive office consists of 7,000 square feet located at 1675 East

Prater Way, Suite 102, Sparks, Nevada 89434. The principal offices are leased

from WDCI, Inc in Sparks Nevada. The lease has a seven (7) year term

signed May 12, 2004, and is renewable. We consider our existing

facilities to be adequate for our foreseeable needs. See the

discussion above for a description of our mineral properties.

ITEM

3. LEGAL PROCEEDINGS

With the

shutdown of Ashdown operations, the sale of our interest in the Ashdown LLC and

the ongoing difficulty raising capital, certain of our vendors and lenders have

initiated actions to collect balances that are past due. We are

negotiating mutually beneficial settlements and payment plans with these

parties. However, our ability to bring such obligations current is

dependent on our ability to raise additional capital. There can be no

assurance that we will be successful in these efforts.

Tetra Financial

Group, LLC – On January 29, 2009, Tetra Financial Group, LLC (“Tetra”)

filed a complaint in the Third District Court of Utah in Salt Lake County

against the Ashdown Project, LLC, the Company, Win-Eldrich Mines Limited and

certain principals of each company, claiming the breach of a lease agreement for

the lease of two (2) ten-ton hauler trucks. In February 2010, a

settlement agreement was reached with Tetra resulting in no material financial

impact to the Company.

Earl

Harrison - We received a default judgment dated February 2, 2009 from the

Second District Court of the State of Nevada in Washoe County entered in favor

of Mr. Earl Harrison, awarding Mr. Harrison $165,197 plus accrued interest

through December 31, 2008 of $5,094 and additional interest that accrues at a

daily rate of $18.66 until the obligation is paid in full. The

judgment relates to a promissory note and accrued interest stemming from the

lease of Mr. Harrison’s mining equipment and other amounts due him

prior to the formation of the Ashdown LLC. Additionally, on May 1,

2009, we received an Execution Order providing for attachment of personal

property and/or certain specified amounts of earnings of the

Company. We have been in discussions with Mr. Harrison, and expect to

reach an amicable resolution to this outstanding obligation and to extinguish

this debt as funding allows.

20

Ed Staub &

Sons Petroleum, Inc. - On April 16, 2009, a complaint was filed in the

Sixth District Court of the State of Nevada in Humboldt County against Ashdown

LLC, the Company and WEG, requesting payment of $107,992 owed to them by the

Ashdown LLC under an Application for Credit for the provision of fuel by the

plaintiff, as well as seeking certain other relief, including a temporary

restraining order on the proposed sale of the Company’s interest in Ashdown

LLC. The parties have been in discussions and expect to reach an

amicable resolution to this outstanding obligation and to extinguish this debt

as funding allows.

DMC-Dynatec

Mining Services Corporation - On February 13, 2009, DMC Mining Services

Corporation filed a complaint against the Company and the Ashdown Project, LLC

in the U.S. District Court, District of Nevada (Reno), claiming approximately

$108,448 due for mechanic’s labor based on a service contract A

default judgment as to both the Company and the Ashdown LLC was entered on July

26, 2009, which obligation was expressly assumed by WEG in connection with the

closing of the sale of the Company’s interest in the Ashdown LLC on May 13,

2009. As of the date of this Report, it is our understanding that WEG

has negotiated a settlement with DMC Mining with respect to such obligation and

that we will be indemnified and held harmless for any liability or obligation to

DMC Mining in connection with the sale of our interest in

Ashdown.

21

PART

II

ITEM 5. MARKET FOR COMMON

EQUITY, RELATED STOCKHOLDER MATTERS AND SMALL BUSINESS ISSUER PURCHASES OF

EQUITY SECURITIES

Our

common stock has been publicly traded since August 6, 1997. The

securities are traded on the OTC Bulletin Board, and quoted on the OTC Bulletin

Board under the symbol “GPXM.OB.” The following table sets forth for

the periods indicated the range of high and low bid quotations per share as

reported by the OTC Bulletin Board for our past 2 years. These

quotations represent inter-dealer prices, without retail markups, markdowns or

commissions and may not necessarily represent actual transactions.

|

Year

2008

|

High

|

Low

|

|

First

Quarter

|

$0.31

|

$0.17

|

|

Second

Quarter

|

$0.22

|

$0.16

|

|

Third

Quarter

|

$0.19

|

$0.07

|

|

Fourth

Quarter

|

$0.08

|

$0.01

|

|

Year

2009

|

High

|

Low

|

|

First

Quarter

|

$0.03

|

$0.01

|

|

Second

Quarter

|

$0.05

|

$0.01

|

|

Third

Quarter

|

$0.04

|

$0.02

|

|

Fourth

Quarter

|

$0.09

|

$0.03

|

Holders

On April

5, 2010, the closing price of our common stock as reported on the

Over-the-Counter Bulletin Board was $0.05 per share. On April 5,

2010, we had approximately 270 holders of record of common stock and 234,328,762

shares of our common stock were issued and outstanding, plus an additional

33,897,259 shares issuable upon the exercise of outstanding options and

warrants.

Dividend

Policy

We have

not paid any dividends on our common stock and do not anticipate paying any cash

dividends in the foreseeable future. We intend to retain any earnings

to finance the growth of the business. We cannot assure you that we

will ever pay cash dividends. Whether we pay any cash dividends in

the future will depend on the financial condition, results of operations and

other factors that the Board of Directors will consider.

Securities

Authorized for Issuance under Equity Compensation Plans

In April

1998, the Board approved the Golden Phoenix Minerals, Inc. Stock Option

Incentive Plan (the “1997 Stock Option Incentive Plan”), under which employees

and directors of the Company are eligible to receive grants of stock

options. The Company has reserved a total of 1,000,000 shares of

common stock under the 1997 Stock Option Incentive Plan. Subsequent

to this, the Employee Stock Incentive Plan of 2002 amended the 1997 Stock Option

Incentive Plan and allows for up to 4,000,000 options to be granted (the “2002

Stock Option Incentive Plan”). In addition to these qualified plans,

the Company created a class of non-registered, non-qualifying options in 2000 to

compensate its three principal employees for deferred salaries. The

Company’s executive management administers the plan. Subject to the