As filed with the Securities and Exchange Commission on

April 1, 2010

Registration

No. 333-

UNITED STATES SECURITIES AND

EXCHANGE COMMISSION

Washington, D.C.

20549

Form S-1

REGISTRATION

STATEMENT

UNDER

THE SECURITIES ACT OF

1933

| |

|

|

ECA Marcellus Trust I

(Exact name of co-registrant

as specified in its charter)

|

|

Energy Corporation of America

(Exact name of co-registrant

as specified in its charter)

|

Delaware

(State or other jurisdiction

of incorporation or organization)

|

|

West Virginia

(State or other jurisdiction

of incorporation or organization)

|

1311

(Primary Standard Industrial

Classification Code Number)

|

|

1311

(Primary Standard Industrial

Classification Code Number)

|

27-6522024

(I.R.S. Employer

Identification No.)

|

|

84-1235822

(I.R.S. Employer

Identification No.)

|

1209 Orange Street

Wilmington, Delaware 19801

(303) 694-2667

|

|

4643 South Ulster Street

Suite 1100

Denver, Colorado 80237

(303) 694-2667

|

(Address, including zip code,

and telephone number,

including area code, of agent of service)

|

|

(Address, including zip code,

and telephone number,

including area code, of agent of service)

|

Michael S. Fletcher

4643 South Ulster Street

Suite 1100

Denver, Colorado 80237

(303) 694-2667

|

|

Donald C. Supcoe

4643 South Ulster Street

Suite 1100

Denver, Colorado 80237

(303) 694-2667

|

(Name, address, including zip

code, and telephone number,

including area code, of agent for service)

|

|

(Name, address, including zip

code, and telephone number,

including area code, of agent for service)

|

Approximate date of commencement of proposed sale to the

public:

As soon as practicable after this Registration Statement becomes

effective.

Copies to:

| |

|

|

|

|

David P. Oelman

Vinson & Elkins L.L.P.

First City Tower

1001 Fannin Street, Suite 2500

Houston, Texas

77002-6760

(713) 758-2222

|

|

Thomas R. Goodwin

Tammy J. Owen

Goodwin & Goodwin, LLP

300 Summers Street

Suite 1500

Charleston, West Virginia 25301

(304) 346-7000

|

|

Joshua Davidson

Baker Botts L.L.P.

One Shell Plaza

910 Louisiana St.

Houston, Texas 77002

(713) 229-1234

|

If any of the securities being registered on this Form are to be

offered on a delayed or continuous basis pursuant to

Rule 415 under the Securities Act of 1933, check the

following

box. o

If this Form is filed to register additional securities for an

offering pursuant to Rule 462(b) under the Securities Act,

check the following box and list the Securities Act registration

statement number of the earlier effective registration statement

for the same

offering. o

If this Form is a post-effective amendment filed pursuant to

Rule 462(c) under the Securities Act, check the following

box and list the Securities Act registration statement number of

the earlier effective registration statement for the same

offering. o

If this Form is a post-effective amendment filed pursuant to

Rule 462(d) under the Securities Act, check the following

box and list the Securities Act registration statement number of

the earlier effective registration statement for the same

offering. o

Indicate by check mark whether the registrant is a large

accelerated filer, an accelerated filer, a non-accelerated

filer, or a smaller reporting company. See the definitions of

“large accelerated filer,” “accelerated

filer” and “smaller reporting company” in Rule

12b-2 of the

Exchange Act. (Check one):

| |

|

|

|

|

|

|

|

Large accelerated

filer o

|

|

Accelerated

filer o

|

|

Non-accelerated

filer o

|

|

Smaller reporting

company o

|

|

|

|

|

|

(Do not check if a smaller reporting company)

|

|

|

CALCULATION

OF REGISTRATION FEE

| |

|

|

|

|

|

|

|

|

|

|

Proposed Maximum

|

|

|

Amount of

|

Title of Each Class of

|

|

|

Aggregate

|

|

|

Registration

|

|

Securities to be Registered

|

|

|

Offering Price (1)(2)

|

|

|

Fee

|

|

Units of Beneficial Interest in ECA Marcellus Trust I

|

|

|

$217,350,000

|

|

|

$15,498

|

|

|

|

|

|

|

|

|

|

|

|

|

(1)

|

|

Includes common units issuable upon

exercise of the underwriters’ over-allotment option.

|

| |

|

(2)

|

|

Estimated solely for the purpose of

calculating the registration fee pursuant to Rule 457(o).

|

The Registrants hereby amend this Registration Statement on

such date or dates as may be necessary to delay its effective

date until the Registrants shall file a further amendment which

specifically states that this Registration Statement shall

thereafter become effective in accordance with Section 8(a)

of the Securities Act, or until this Registration Statement

shall become effective on such date as the Securities and

Exchange Commission (or the “SEC”), acting pursuant to

said Section 8(a), may determine.

The information in

this preliminary prospectus is not complete and may be changed.

These securities may not be sold until the registration

statement filed with the Securities and Exchange Commission is

effective. This preliminary prospectus is not an offer to sell

these securities, and we are not soliciting an offer to buy

these securities, in any jurisdiction where the offer or sale is

not permitted.

|

Subject to Completion dated

April 1, 2010

PRELIMINARY PROSPECTUS

ECA

Marcellus Trust I

9,000,000 Common

Units

This is an initial public offering of common units representing

beneficial interests in ECA Marcellus Trust I. The trust is

selling all of the units offered hereby. Energy Corporation of

America (“ECA”) has formed the trust and will convey

certain royalty interests and natural gas hedging contracts to

the trust in exchange for a distribution from the net proceeds

of this offering as well as common and subordinated units

representing a 50% beneficial interest in the trust.

Prior to this offering, there has been no public market for the

common units. ECA expects that the public offering price will be

between $ and

$ per common unit. The trust

intends to apply to have the common units approved for listing

on the New York Stock Exchange under the symbol “ECT.”

The Trust Units. Trust units, consisting of the

common and subordinated units, are units of beneficial interest

in the trust and represent undivided interests in the trust.

They do not represent any interest in ECA.

The Trust. The trust will own term and perpetual royalty

interests in natural gas properties owned by ECA in the

Marcellus Shale formation in Greene County, Pennsylvania. These

royalty interests will entitle the trust to receive 90% of the

proceeds attributable to ECA’s interest in the sale of

production from 14 producing horizontal Marcellus Shale natural

gas wells located in Greene County, Pennsylvania and 50% of the

proceeds attributable to ECA’s interest in the sale of

production from 52 horizontal Marcellus Shale natural gas

development wells to be drilled on drill sites included within

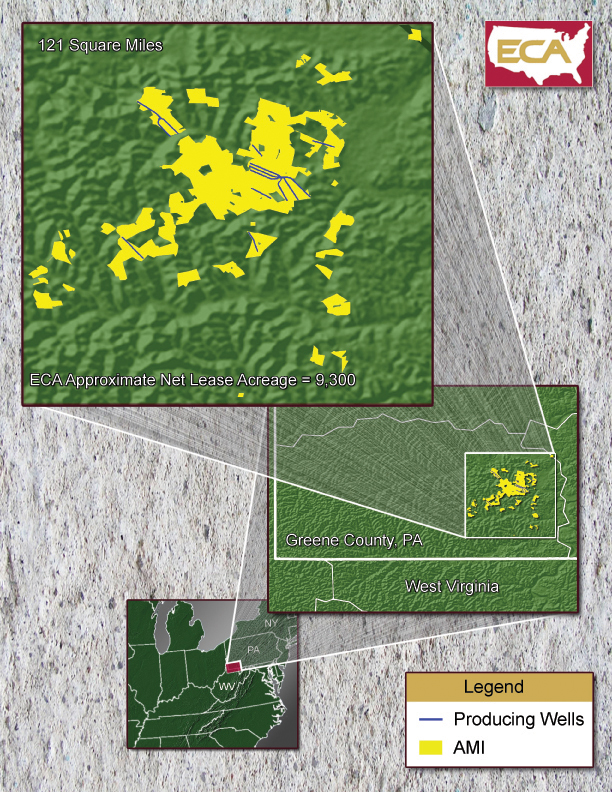

approximately 9,300 net acres held by ECA in Greene County,

Pennsylvania. The trust will be treated as a partnership for

federal income tax purposes.

The Trust Unitholders. As a trust unitholder, you

will receive quarterly distributions of cash from the proceeds

that the trust receives from ECA’s sale of natural gas

subject to the royalty interests held by the trust.

Investing in the common units involves a high degree of risk.

Before buying any common units, you should read the discussion

of material risks of investing in the common units in “Risk

factors” beginning on page 16 of this prospectus.

Neither the Securities and Exchange Commission nor any state

securities commission has approved or disapproved of these

securities or passed upon the adequacy or accuracy of this

prospectus. Any representation to the contrary is a criminal

offense.

| |

|

|

|

|

|

|

|

|

|

|

|

Per Common Unit

|

|

|

Total

|

|

|

|

|

Price to the public

|

|

$

|

|

|

|

$

|

|

|

|

Underwriting discounts and commissions

|

|

$

|

|

|

|

$

|

|

|

|

Proceeds to the trust (before expenses)

|

|

$

|

|

|

|

$

|

|

|

The underwriters may also purchase up to an additional

1,350,000 common units at the initial public offering price,

less underwriting discounts and commissions, to cover

over-allotments, if any, within 30 days of the date of this

prospectus. If the underwriters exercise this option in full,

the total underwriting discounts and commissions will be

$ , and the trust’s total

proceeds, after deducting underwriting discounts and commissions

and before expenses, will be $ .

The net proceeds of any exercise of the underwriters’

over-allotment option will be used to redeem an equal number of

common units held by ECA.

The underwriters are offering the common units as set forth

under “Underwriting.” Delivery of the common units

will be made on or

about ,

2010.

Joint Bookrunning Managers

, 2010

TABLE OF

CONTENTS

Important

Notice About Information in This Prospectus

You should rely only on the information contained in this

prospectus.

Until ,

2010 (25 days after the date of this prospectus), federal

securities laws may require all dealers that effect transactions

in the common units, whether or not participating in this

offering, to deliver a prospectus. This is in addition to the

dealers’ obligation to deliver a prospectus when acting as

underwriters and with respect to their unsold allotments or

subscriptions.

ECA and the trust have not, and the underwriters have not,

authorized anyone to provide you with additional or different

information. If anyone provides you with additional, different

or inconsistent information, you should not rely on it. This

prospectus is not an offer to sell or a solicitation of an offer

to buy the common units in any jurisdiction where such offer and

sale would be unlawful. You should not assume that the

information contained in this prospectus is accurate as of any

date other than the date on the front of this document. The

trust’s business, financial condition, results of

operations and prospects may have changed since such dates or in

any free writing prospectus we may authorize to be delivered to

you.

i

SUMMARY

This summary provides a brief overview of information

contained elsewhere in this prospectus. To understand this

offering fully, you should read the entire prospectus carefully,

including the risk factors and the financial statements and

notes to those statements. Definitions for terms relating to the

natural gas business can be found in “Glossary of certain

oil and natural gas terms and terms related to the trust.”

Ryder Scott Company, L.P., an independent engineering firm,

provided the estimates of proved natural gas reserves as of

March 31, 2010 included in this prospectus. These estimates

are contained in a summary prepared by Ryder Scott of its

reserve report as of March 31, 2010 for the Underlying

Properties held by ECA described below and for the royalty

interests in the Underlying Properties held by the trust, which

royalty interests are referred to herein as the “trust

properties.” This summary is located at the back of this

prospectus as Annex A and is referred to in this prospectus

as the “reserve report.” References to “Energy

Corporation of America” or “ECA” in this

prospectus are to Energy Corporation of America and its

subsidiaries and, when discussing unit ownership and historical

ownership of the royalty interests, includes the private

investors listed in “Certain Transactions” (such

private investors being referred to herein as the “Private

Investors”). Unless otherwise indicated, all information in

this prospectus assumes an initial public offering price of

$ per common unit and no exercise of the

underwriters’ over-allotment option.

ECA

Marcellus Trust I

ECA Marcellus Trust I is a Delaware statutory trust formed

in March 2010 by Energy Corporation of America to own royalty

interests in 14 producing horizontal natural gas wells producing

from the Marcellus Shale formation and located in Greene County,

Pennsylvania (the “Producing Wells”) and royalty

interests in 52 horizontal natural gas development wells to be

drilled to the Marcellus Shale formation (the “PUD

Wells”) within the “Area of Mutual Interest,” or

“AMI”, comprised of 9,300 net acres held by ECA

in Greene County, Pennsylvania. The royalty interests will be

conveyed from ECA’s working interest in the Producing Wells

and the PUD Wells limited to the Marcellus Shale formation (the

“Underlying Properties”). The royalty interest in the

Producing Wells (the “PDP Royalty Interest”) entitles

the trust to receive 90% of the proceeds (after deducting

post-production costs and any applicable taxes) from the sale of

production of natural gas attributable to ECA’s interest in

the Producing Wells. The royalty interest in the PUD Wells (the

“PUD Royalty Interest”) entitles the trust to receive

50% of the proceeds (after deducting post-production costs and

any applicable taxes) from the sale of production of natural gas

attributable to ECA’s interest in the PUD Wells.

Approximately 50% of the estimated natural gas production

attributable to the trust’s royalty interests will be

hedged from April 1, 2010 to March 31, 2014. These

hedging contracts will be transferred to the trust by ECA, and

ECA will be entitled to recoup the costs of establishing the

hedging contracts to the extent cash available for distribution

by the trust exceeds certain levels. Please see “Target

Distributions and Subordination and Incentive Thresholds.”

ECA is obligated to use commercially reasonable efforts to drill

all of the PUD Wells by March 31, 2013. In the event of

delays, ECA will have until March 31, 2014 to fulfill its

drilling obligation. ECA will grant to the trust a lien on

ECA’s retained interest in the AMI in order to secure the

estimated amount of the drilling costs for the trust’s

interests in the PUD Wells (the “Drilling Support

Lien”). The amount obtained by the trust pursuant to the

Drilling Support Lien may not exceed $91 million, and this

amount will be proportionately reduced as ECA fulfills its

drilling obligation over time. The Drilling Support Lien is

nonrecourse to ECA.

The trust will not be responsible for any costs related to the

drilling of development wells or any other development or

operating costs. The trust’s cash receipts in respect of

the royalties will be determined after deducting post-production

costs and any applicable taxes associated with the

1

PDP and PUD Royalty Interests, and the trust’s cash

available for distribution will include cash receipts from its

hedging contracts and will be reduced by trust administrative

expenses and expenses incurred as a result of being a publicly

traded entity. Post-production costs will generally consist of

costs incurred to gather, compress, transport, process, treat,

dehydrate and market the natural gas produced. Any charge

payable to ECA for such

post-production

costs on its Greene County Gathering System will be limited to

$0.52 per MMBtu gathered until ECA has fulfilled its drilling

obligation (the “Post-Production Services Fee”);

thereafter, ECA may increase the

Post-Production

Services Fee to the extent necessary to recover certain capital

expenditures in the Greene County Gathering System.

As of March 31, 2010 and after giving effect to the

conveyance of the PDP Royalty Interest and the PUD Royalty

Interest, the total gas reserves estimated to be attributable to

the trust interests were 104.6 Bcf. This amount includes

72.4 Bcf attributable to the PUD Royalty Interest and

32.2 Bcf attributable to the PDP Royalty Interest.

ECA’s retained interest in the Underlying Properties

entitles it to 10% of the proceeds from the sale of natural gas

from the Producing Wells as well as 50% of the proceeds from the

sale of future production from the PUD Wells. After giving

effect to the trust’s royalty interests that burden

ECA’s working interests in the Underlying Properties and

taking into account the ownership by ECA of 43% of the trust

units, ECA and its affiliates will retain an approximate 66%

average economic interest in the Underlying Properties. ECA

operates all of the Producing Wells and will agree to operate

not less than 90% of the PUD Wells during the subordination

period as defined below. In addition, ECA has agreed to operate

the gas properties to which the PDP Royalty Interest and the PUD

Royalty Interest relate and to cause to be marketed natural gas

produced from these properties in the same manner it would if

such properties were not burdened by the trust’s royalty

interests.

The trust will make quarterly cash distributions of

substantially all of its cash receipts, after deducting trust

administrative expenses and the costs incurred as a result of

being a publicly traded entity, on or about 60 days

following the completion of each quarter through (and including)

the quarter ending March 31, 2030 (the “Termination

Date”). The first quarterly distribution is expected to be

made on or about August 31, 2010 to record unitholders as

of August 15, 2010. The trust will begin to liquidate on

the Termination Date and will soon thereafter wind up its

affairs and terminate. At the Termination Date, 50% of each of

the PDP Royalty Interest and the PUD Royalty Interest will

revert automatically to ECA. The remaining 50% of each of the

PDP Royalty Interest and the PUD Royalty Interest will be sold,

and the net proceeds therefrom will be distributed pro rata to

the unitholders soon after the Termination Date. ECA will have a

first right of refusal to purchase the remaining 50% of the

royalty interests at the Termination Date. Because payments to

the trust will be generated by depleting assets and the trust

has a finite life with the production from the Underlying

Properties diminishing over time, a portion of each distribution

will represent a return of your original investment.

The business and affairs of the trust will be managed by the

trustee. Although ECA will operate all of the Producing Wells

and substantially all of the PUD Wells, ECA has no ability to

manage or influence the management of the trust.

TARGET

DISTRIBUTIONS AND SUBORDINATION AND INCENTIVE

THRESHOLDS

Subordination

and Incentive Thresholds

ECA has calculated quarterly target levels of cash distributions

for the life of the trust as set forth on Annex B to this

prospectus. The amount of the quarterly distributions may

fluctuate from quarter to quarter, depending on the proceeds

received by the trust, among other factors.

2

Annex B reflects that while target distributions increase

as ECA completes its drilling obligations and production

attributable to the trust increases, over time these target

distributions decline as a result of the depletion of the

reserves in the Underlying Properties. These “target

distributions” do not represent the actual distributions

you should expect to receive with respect to your common units.

Rather, the trust has established the target distributions in

part to calculate the subordination and incentive thresholds

described in more detail below. The target distributions were

derived by assuming that natural gas production from the trust

properties will equal the volumes reflected in the reserve

report attached as Annex A to this prospectus and the

prices received for such production will equal NYMEX forward

pricing as of March 11, 2010 for the thirty-six month

period ending March 31, 2013 and increased thereafter by a

2.5% annual escalator (as adjusted for a basis differential of

$0.15 per MMBtu), capped at $9.00 per MMBtu starting in 2025.

The target distributions also give effect to post-production

expenses projected in the reserve reports and projected trust

administrative expenses, including the expenses incurred as a

result of being a publicly traded entity. For more information

on subordination and incentive thresholds, please read

“— Target Distributions” below.

In order to provide support for cash distributions on the common

units, ECA has agreed to subordinate 4,500,000 of the trust

units it will retain following this offering, which will

constitute 25% of the outstanding trust units. While the

subordinated units will be entitled to receive pro rata

distributions from the trust if and to the extent there is

sufficient cash to provide a cash distribution on the common

units which is no less than the applicable quarterly

subordination threshold, if there is not sufficient cash to fund

such a distribution on all trust units, the distribution to be

made with respect to the subordinated units will be reduced or

eliminated in order to make a distribution, to the extent

possible, of up to the subordination threshold amount on the

common units. Each applicable quarterly subordination threshold

is equal to 80% of the target distribution level for the

corresponding quarter as reflected on Annex B (each, a

“subordination threshold”). In exchange for agreeing

to subordinate these trust units, and in order to provide

additional financial incentive to ECA to perform its drilling

obligation and operations on the Underlying Properties in an

efficient and cost-effective manner, ECA will be entitled to

receive incentive distributions (the “incentive

distributions”) equal to 50% of the amount by which the

cash available for distribution on all of the trust units in any

quarter exceeds 150% of the subordination threshold for such

quarter (which is 120% of the target distribution for such

quarter) (each, an “incentive threshold”). ECA’s

right to receive this incentive distribution will terminate upon

the expiration of the subordination period.

ECA has incurred costs of approximately $5 million in

securing the hedging contracts to be transferred to the trust.

ECA will be entitled to reimbursement for these expenditures

only if and to the extent distributions to trust unitholders

would otherwise exceed the incentive threshold. This

reimbursement will be deducted, over time, from the 50% of cash

available for distribution in excess of the incentive thresholds

otherwise payable to the trust unitholders. ECA’s right to

receive the remaining 50% of such cash in the form of incentive

distributions would not be affected.

The subordinated units will automatically convert into common

units on a

one-for-one

basis and ECA’s right to receive incentive distributions

and to recoup the reimbursement amount will terminate, at the

end of the fourth full calendar quarter following ECA’s

satisfaction of its drilling obligation to the trust.

Accordingly, ECA bears the risk that it will not be partially or

fully reimbursed for the hedging contracts it is transferring to

the trust. The trust currently expects that ECA will complete

its drilling obligation on or before March 31, 2013 and

that, accordingly, the subordinated units will convert into

common units on or before March 31, 2014. In the event of

delays, ECA will have until March 31, 2014 to drill all the

PUD Wells, in which event the subordinated units would convert

into common units on or before March 31, 2015. The period

during which the subordinated units are outstanding is referred

to as the “subordination period.”

3

The table below sets forth the target distributions and

subordination and incentive thresholds for each calendar quarter

during the full potential subordination period. The effective

date of the trust is April 1, 2010, meaning it will receive

the proceeds of production attributable to the PDP Royalty

Interest from that date even though the PDP Royalty Interest

will not be conveyed to the trust until the closing of this

offering.

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Subordination

|

|

|

Target

|

|

|

Incentive

|

|

|

Period

|

|

Threshold

|

|

|

Distribution

|

|

|

Threshold

|

|

|

|

|

|

|

|

(per unit)

|

|

|

|

|

|

|

|

2010:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Second Quarter

|

|

$

|

0.217

|

|

|

$

|

0.271

|

|

|

$

|

0.326

|

|

|

Third Quarter

|

|

|

0.298

|

|

|

|

0.372

|

|

|

|

0.447

|

|

|

Fourth Quarter

|

|

|

0.426

|

|

|

|

0.532

|

|

|

|

0.639

|

|

|

2011:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First Quarter

|

|

|

0.413

|

|

|

|

0.516

|

|

|

|

0.619

|

|

|

Second Quarter

|

|

|

0.418

|

|

|

|

0.523

|

|

|

|

0.627

|

|

|

Third Quarter

|

|

|

0.520

|

|

|

|

0.650

|

|

|

|

0.780

|

|

|

Fourth Quarter

|

|

|

0.544

|

|

|

|

0.680

|

|

|

|

0.815

|

|

|

2012:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First Quarter

|

|

|

0.562

|

|

|

|

0.702

|

|

|

|

0.843

|

|

|

Second Quarter

|

|

|

0.595

|

|

|

|

0.744

|

|

|

|

0.893

|

|

|

Third Quarter

|

|

|

0.607

|

|

|

|

0.759

|

|

|

|

0.911

|

|

|

Fourth Quarter

|

|

|

0.688

|

|

|

|

0.859

|

|

|

|

1.031

|

|

|

2013:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First Quarter

|

|

$

|

0.773

|

|

|

$

|

0.967

|

|

|

$

|

1.160

|

|

|

Second Quarter

|

|

|

0.771

|

|

|

|

0.964

|

|

|

|

1.157

|

|

|

Third Quarter

|

|

|

0.717

|

|

|

|

0.896

|

|

|

|

1.075

|

|

|

Fourth Quarter

|

|

|

0.674

|

|

|

|

0.842

|

|

|

|

1.010

|

|

|

2014:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First Quarter

|

|

|

0.623

|

|

|

|

0.779

|

|

|

|

0.935

|

|

|

Second Quarter

|

|

|

0.601

|

|

|

|

0.751

|

|

|

|

0.902

|

|

|

Third Quarter

|

|

|

0.583

|

|

|

|

0.728

|

|

|

|

0.874

|

|

|

Fourth Quarter

|

|

|

0.561

|

|

|

|

0.701

|

|

|

|

0.841

|

|

|

2015:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First Quarter

|

|

|

0.530

|

|

|

|

0.663

|

|

|

|

0.795

|

|

For additional information with respect to the subordination and

incentive thresholds, please see “Target Distributions and

Subordination and Incentive Thresholds” and

“Description of the Royalty Interests.”

4

Target

Distributions

The table below presents the calculation of the target

distributions for each quarter through and including the quarter

ending June 30, 2011. The target distributions were

prepared by ECA on an accrual basis based on production volumes,

pricing and other assumptions. As used herein, accrual basis

means ECA will pay to the trust each quarter an amount equal to

the estimated proceeds of production from the trust properties

during the calendar quarter most recently ended before the

distribution (after deducting post-production costs and any

applicable taxes), regardless of whether such amounts have

actually been received by ECA from the purchaser of the natural

gas produced. Any difference between the payment made by ECA to

the trust with respect to a calendar quarter and the actual cash

production payments relative to the trust properties received by

ECA will be netted against future payments by ECA to the trust.

Actual cash distributions to the trust unitholders will

fluctuate quarterly based on the quantity of natural gas

produced from the Underlying Properties, the prices received for

natural gas production and other factors. Please read

“Target Distributions and Subordination and Incentive

Thresholds — Significant Assumptions Used to Prepare

the Target Distributions.”

ECA does not as a matter of course make public projections as to

future sales, earnings or other results. However, the management

of ECA has prepared the projected operational and financial

information set forth below in order to present the target

distributions attributable to the natural gas sales volumes

reflected in Ryder Scott’s reserve report attached hereto

as Annex A.

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quarters Ending

|

|

|

|

|

June 30,

|

|

|

September 30,

|

|

|

December 31,

|

|

|

March 31,

|

|

|

June 30,

|

|

|

|

|

2010

|

|

|

2010

|

|

|

2010

|

|

|

2011

|

|

|

2011

|

|

|

|

|

(In thousands, except well number, volumetric and per unit

data)

|

|

|

|

|

Number of wells producing at quarter end

|

|

|

8

|

|

|

|

17

|

|

|

|

22

|

|

|

|

25

|

|

|

|

31

|

|

|

Estimated Production from Trust Properties

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Natural Gas PDP Sales Volumes (MMcf)

|

|

|

879

|

|

|

|

1,190

|

|

|

|

1,265

|

|

|

|

1,066

|

|

|

|

962

|

|

|

Natural Gas PUD Sales Volumes (MMcf)

|

|

|

—

|

|

|

|

81

|

|

|

|

514

|

|

|

|

553

|

|

|

|

769

|

|

|

Total Sales Volumes (MMcf)

|

|

|

879

|

|

|

|

1,271

|

|

|

|

1,779

|

|

|

|

1,619

|

|

|

|

1,731

|

|

|

Daily Sales Volumes (Mcf/d)

|

|

|

9,664

|

|

|

|

13,814

|

|

|

|

19,336

|

|

|

|

17,988

|

|

|

|

19,020

|

|

|

Commodity Prices and Hedging Positions (1)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Assumed NYMEX Price ($/MMBtu) (2)

|

|

$

|

4.58

|

|

|

$

|

4.75

|

|

|

$

|

5.27

|

|

|

$

|

5.81

|

|

|

$

|

5.34

|

|

|

Assumed Price ($/Mcf) (2)

|

|

|

4.72

|

|

|

|

4.89

|

|

|

|

5.42

|

|

|

|

5.98

|

|

|

|

5.50

|

|

|

Realized Unhedged Price after Basis Differential ($/Mcf)

|

|

|

4.88

|

|

|

|

5.04

|

|

|

|

5.58

|

|

|

|

6.13

|

|

|

|

5.65

|

|

|

Daily Hedged Volumes (MMcf/d) (3)

|

|

|

7.3

|

|

|

|

7.3

|

|

|

|

9.7

|

|

|

|

9.0

|

|

|

|

9.5

|

|

|

Percent of Total Volumes Swapped

|

|

|

75

|

%

|

|

|

53

|

%

|

|

|

38

|

%

|

|

|

40

|

%

|

|

|

38

|

%

|

|

Swap Price ($/MMBtu)

|

|

$

|

6.75

|

|

|

$

|

6.75

|

|

|

$

|

6.75

|

|

|

$

|

6.75

|

|

|

$

|

6.75

|

|

|

Percent of Total Volumes Floored

|

|

|

—

|

|

|

|

—

|

|

|

|

12

|

%

|

|

|

10

|

%

|

|

|

12

|

%

|

5

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quarters Ending

|

|

|

|

|

June 30,

|

|

|

September 30,

|

|

|

December 31,

|

|

|

March 31,

|

|

|

June 30,

|

|

|

|

|

2010

|

|

|

2010

|

|

|

2010

|

|

|

2011

|

|

|

2011

|

|

|

|

|

(In thousands, except well number, volumetric and per unit

data)

|

|

|

|

|

Floor Price ($/MMBtu)

|

|

$

|

—

|

|

|

$

|

—

|

|

|

$

|

5.00

|

|

|

$

|

5.00

|

|

|

$

|

5.00

|

|

|

Realized Hedged Weighted Average Price ($/Mcf) (3)

|

|

$

|

6.55

|

|

|

$

|

6.13

|

|

|

$

|

6.15

|

|

|

$

|

6.53

|

|

|

$

|

6.21

|

|

|

Cash available for distribution

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gas Sales Revenues

|

|

$

|

4,288

|

|

|

$

|

6,408

|

|

|

$

|

9,923

|

|

|

$

|

9,932

|

|

|

$

|

9,786

|

|

|

Swap and Floor Hedge Revenues

|

|

|

1,476

|

|

|

|

1,381

|

|

|

|

1,021

|

|

|

|

635

|

|

|

|

960

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Revenues

|

|

$

|

5,764

|

|

|

$

|

7,788

|

|

|

$

|

10,944

|

|

|

$

|

10,566

|

|

|

$

|

10,746

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Post-Production Services Fee (4)

|

|

$

|

471

|

|

|

$

|

681

|

|

|

$

|

953

|

|

|

$

|

867

|

|

|

$

|

927

|

|

|

Trust Expenses

|

|

|

200

|

|

|

|

200

|

|

|

|

200

|

|

|

|

200

|

|

|

|

201

|

|

|

Franchise Taxes

|

|

|

207

|

|

|

|

207

|

|

|

|

211

|

|

|

|

211

|

|

|

|

211

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash Available for Distribution

|

|

$

|

4,885

|

|

|

$

|

6,701

|

|

|

$

|

9,581

|

|

|

$

|

9,288

|

|

|

$

|

9,407

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Trust Units Outstanding

|

|

|

18,000

|

|

|

|

18,000

|

|

|

|

18,000

|

|

|

|

18,000

|

|

|

|

18,000

|

|

|

Target Distribution Per Trust Unit

|

|

$

|

0.271

|

|

|

$

|

0.372

|

|

|

$

|

0.532

|

|

|

$

|

0.516

|

|

|

$

|

0.523

|

|

|

Subordination Threshold Per Trust Unit

|

|

$

|

0.217

|

|

|

$

|

0.298

|

|

|

$

|

0.426

|

|

|

$

|

0.413

|

|

|

$

|

0.418

|

|

|

Incentive Threshold Per Trust Unit

|

|

$

|

0.326

|

|

|

$

|

0.447

|

|

|

$

|

0.639

|

|

|

$

|

0.619

|

|

|

$

|

0.627

|

|

|

|

|

|

(1)

|

|

For a more detailed description of

the natural gas hedging contracts established for the benefit of

the trust, please see “Description of the Royalty

Interests.”

|

| |

|

(2)

|

|

Based on NYMEX forward pricing as

of March 11, 2010. Assumed price per Mcf calculated based

on an assumed conversion rate of

1.03 MMBtu

per Mcf.

|

| |

|

(3)

|

|

Adjusted for an assumed basis

differential of $0.15 per MMBtu.

|

| |

|

(4)

|

|

Consists of a fee of $0.52 per

MMBtu.

|

ENERGY

CORPORATION OF AMERICA

ECA is a privately held energy company engaged in the

exploration, development, production, gathering, aggregation and

sale of natural gas and oil, primarily in the Appalachian Basin,

Gulf Coast and Rocky Mountain regions in the United States and

in New Zealand. ECA or its predecessors have owned and operated

natural gas properties in the Appalachian Basin for more than

45 years, and ECA is one of the largest natural gas

operators in the Appalachian Basin. As of December 31,

2009, ECA operated approximately 5,100 wells in the

Appalachian Basin and had an aggregate net leasehold position of

approximately one million acres, with 85% of this acreage held

by production. ECA sells gas from its own wells as well as

third-party wells to local gas distribution companies,

industrial end users located in the Northeast, other gas

marketing entities and into the spot market for gas delivered

into interstate pipelines. ECA owns and operates approximately

5,000 miles of gathering lines and intrastate pipelines

that are used in connection with its gas aggregation activities.

During the fiscal year ended June 30, 2009, ECA aggregated

and sold 22.5 Bcf of gas for an average of 62 MMcf of

gas per day, of which 20.7 Bcf, or 57 MMcf per day,

represented sales of gas produced from wells operated by ECA.

6

ECA was formed in September 1992 as a Colorado corporation and

subsequently reincorporated in West Virginia through a merger

with ECA’s predecessor in June 1995. ECA’s predecessor

began operating in the Appalachian Basin in 1963. ECA’s

principal offices are located at 4643 South Ulster Street,

Suite 1100, Denver, Colorado 80237, and its telephone

number is

(303) 694-2667.

For additional information concerning ECA, see “Information

about Energy Corporation of America” beginning on

page ECA-1

of this prospectus. ECA will be required to deliver to the

trustee a statement of the computation of the proceeds for each

computation period, as well as quarterly drilling and production

results. ECA will not be a reporting company following this

offering and will not file periodic reports with the SEC.

Therefore, as a trust unitholder, you will not have access to

financial information of ECA.

The trust

units do not represent interests in or obligations of

ECA.

FORMATION

TRANSACTIONS

At or prior to the closing of this offering, the following

transactions, which are referred to as the “formation

transactions,” will occur:

|

|

|

| |

•

|

ECA will convey to a wholly owned subsidiary a term royalty

interest entitling the holder of the interest to receive 45% of

the proceeds from the sale of production of natural gas

attributable to ECA’s interest in the Producing Wells

(after deducting post-production costs and any applicable taxes)

for a period of 20 years commencing on April 1, 2010

(the “Term PDP Royalty”) and a term royalty interest

entitling such holder of the interest to receive 25% of the

proceeds from the sale of the production of natural gas

attributable to ECA’s interest in the PUD Wells (after

deducting

post-production

costs and any applicable taxes) for a period of 20 years

commencing on April 1, 2010 (the “Term PUD

Royalty”) in exchange for a demand note in the principal

amount of $ million. The Term

PDP Royalty and the Term PUD Royalty are collectively referred

to as the “Term Royalties.”

|

| |

| |

•

|

ECA and the Private Investors will convey to the trust perpetual

royalty interests entitling the trust to receive, in the

aggregate, 45% of the proceeds from the sale of production of

natural gas attributable to the interests of ECA in the

Producing Wells (after deducting post-production costs and any

applicable taxes) (the “Perpetual PDP Royalty”) and

ECA will convey to the trust a perpetual royalty interest

entitling the trust to receive an additional 25% of the proceeds

from the sale of production of natural gas attributable to

ECA’s interest in the PUD Wells (after deducting

post-production

costs and any applicable taxes) (the “Perpetual PUD

Royalty”) in exchange for, in the case of ECA,

3,186,117 common units constituting 17.7% of the trust

units outstanding and 4,500,000 subordinated units

constituting 25% of the trust units outstanding and, in the case

of the Private Investors, 1,313,883 common units

constituting 7.3% of the trust units outstanding. The Perpetual

PDP Royalty and the Perpetual PUD Royalty are collectively

referred to as the “Perpetual Royalties.”

|

| |

| |

•

|

The trust will sell the 9,000,000 common units offered

hereby to the public, representing a 50% interest in the trust.

|

| |

| |

•

|

ECA will convey to the trust the natural gas hedging contracts.

|

| |

| |

•

|

ECA’s subsidiary will convey the Term Royalties to the

trust in exchange for a distribution from the net proceeds of

this offering and will use the net proceeds to repay the demand

note to ECA.

|

7

|

|

|

| |

•

|

ECA will purchase 209,316 common units from the Private

Investors at the initial offering price.

|

| |

| |

•

|

ECA and the trust will enter into an Administrative and Drilling

Services Agreement outlining the provision of administrative

services to the trust and its compensation therefor and

ECA’s drilling obligation to the trust with respect to the

PUD Wells. Please see “The Trust — Administrative

and Drilling Services Agreement.”

|

| |

| |

•

|

ECA will grant to the trust the Drilling Support Lien which is

nonrecourse to ECA.

|

| |

| |

•

|

ECA will grant to the trust a lien, which is nonrecourse to ECA,

on the PDP Royalty Interest and the PUD Royalty Interest (the

“Royalty Interest Lien”) to provide protection to the

trust, in the event of a bankruptcy of ECA, against the risk

that the PDP Royalty Interest or PUD Royalty Interest were not

considered a real property interest.

|

STRUCTURE

OF THE TRUST

The following chart shows the relationship of ECA, the trust and

the public unitholders.

KEY

INVESTMENT CONSIDERATIONS

The following are some key investment considerations related to

the Underlying Properties, the royalty interests, and the common

units:

|

|

|

| |

•

|

Royalty interests not burdened by operating or capital

costs. The trust will not be responsible for any

operating or capital costs associated with the Underlying

Properties, including the costs to drill the PUD Wells. As a

result, the trust’s burden to pay costs associated with any

particular well will not arise until such well is producing

natural gas attributable to the trust’s interest. The

principal costs the trust will bear are the Post-Production

Services Fee; property, ad valorem, production, severance,

excise,

|

8

|

|

|

| |

|

franchise and similar taxes, if any; and trust administrative

expenses including costs incurred as a result of being a

publicly traded entity. In addition, the trust will be obligated

to reimburse ECA for approximately $5 million incurred in

establishing the hedging contracts to be transferred to the

trust if and to the extent cash available for distribution by

the trust exceeds certain levels.

|

|

|

|

| |

•

|

Downside protection against natural gas price volatility

through natural gas hedging contracts for 50% of estimated

production through March 31, 2014. ECA will

transfer to the trust hedging contracts covering approximately

50% of the expected production volumes attributable to the trust

from April 1, 2010 through March 31, 2014. These

hedging contracts will consist of swap contracts and floor price

hedging contracts. The swap contracts will relate to

approximately 7,500 MMBtu per day at an average price of

$6.78 per MMBtu for the period from April 1, 2010 through

June 2012. The floor price of any floor price hedging contract

will be $5.00 per MMBtu. These hedging contracts should

reduce commodity price risks inherent in holding interests in

natural gas through the end of March 31, 2014.

|

| |

| |

•

|

Alignment of interests between ECA and the trust

unitholders. ECA is significantly incentivized to

complete its drilling obligation, to increase production from

the Underlying Properties and to obtain the best prices for the

natural gas production from the Underlying Properties as a

result of the following factors:

|

|

|

|

| |

-

|

ECA will retain an approximate average of 66% total economic

interest in the Underlying Properties through its retained

interest in the Underlying Properties and its ownership of

approximately 43% of the trust units.

|

| |

| |

-

|

A portion of the trust units that ECA will own, constituting 25%

of the outstanding trust units, will be subordinated units that

will not be entitled to receive distributions unless there is

sufficient cash to pay the subordination threshold to the common

units. These subordinated units will only convert into common

units upon completion of the subordination period.

|

| |

| |

-

|

To the extent that the trust has cash available for distribution

in excess of the incentive thresholds during the subordination

period, ECA will be entitled to receive 50% of such cash as

incentive distributions and 50% of such cash as recoupment of

its costs for establishing the hedge contracts until it has

recouped approximately $5 million.

|

|

|

|

| |

-

|

ECA will not be permitted to drill and complete any development

wells in the Marcellus Shale formation on the lease acreage

within the AMI for its own account or sell the Underlying

Properties until it has satisfied its drilling obligation.

|

|

|

|

| |

•

|

Potential for initial depletion to be offset by results of

development drilling. ECA is obligated to drill the PUD

Wells by March 31, 2014. Furthermore, ECA is incentivized

to increase production in the near term in order to receive

incentive distributions. While production from the trust

properties will decline in the long term, production from the

PUD Wells will offset depletion of the Producing Wells in the

near term.

|

| |

| |

•

|

ECA’s experience and position as Marcellus Shale

operator. Since January 1, 2006, ECA has drilled

over 160 Marcellus Shale wells throughout the Appalachian Basin

and operates Marcellus Shale wells in New York, Pennsylvania and

West Virginia. ECA was one of the earliest operators in the

Marcellus Shale region, having drilled test wells in this play

in the late 1970s in partnership with the U.S. Department

of Energy, and on April 18, 2008, it drilled and completed

the Consol USX-13 well, which was one of the

|

9

|

|

|

| |

|

first horizontal Marcellus Shale wells in Greene County,

Pennsylvania. ECA has drilled 141 gross vertical

development wells and 21 gross horizontal wells in the

Marcellus Shale formation, and it has successfully completed

100% of these wells. ECA is currently the operator of all of the

Producing Wells and will agree to operate not less than 90% of

the PUD Wells during the subordination period, allowing ECA to

control the timing and amount of discretionary expenditures for

operational and development activities with respect to

substantially all of the PUD Wells. ECA’s senior managers

possess an average of 27.5 years of industry experience

with an extensive focus on operations in the Appalachian Basin

and Marcellus Shale.

|

|

|

|

| |

•

|

ECA’s prior experience sponsoring a royalty

trust. In 1993, ECA sponsored the formation of the

Eastern American Natural Gas Trust (NYSE: NGT), a publicly

traded Delaware trust (“NGT”), to which it contributed

term net profits interests in Appalachian Basin natural gas

properties. In connection with the formation of this trust, ECA

agreed to drill 65 development wells over five years from which

NGT would be entitled to a specified percentage of the proceeds

from the natural gas production. ECA completed its obligation

within the stipulated period. The historical results of

operations and performance of NGT should not be relied on as an

indicator of how the trust will perform.

|

In mid-2005, ECA entered into a term royalty transaction with a

private investor. ECA conveyed to the private investor a 90%

royalty interest in 312 producing gas wells located in the

Appalachian Basin in West Virginia, Pennsylvania and Kentucky,

as well as a 50% royalty interest in 180 development wells that

were subsequently drilled by ECA in Kentucky and West Virginia.

Although the parties originally contemplated that ECA would

drill relatively shallow wells, 105 of the 180 development wells

were completed to the deeper Marcellus Shale formation.

|

|

|

| |

•

|

Experience of ECA marketing natural gas

production. As the operator of all of the Producing

Wells and substantially all the PUD Wells, ECA will have the

responsibility to market or cause to be marketed the natural gas

production related to the Underlying Properties. During the

fiscal year ended June 30, 2009, ECA and its affiliates

aggregated and sold domestically an average of 62 MMcf of

gas per day, of which 57 MMcf per day represented sales of

natural gas produced from wells operated by ECA.

|

| |

| |

•

|

Proximity of the Appalachian Basin to major

markets. The Appalachian Basin is located close to a

substantial number of large commercial and industrial gas

markets, including natural gas powered electricity plants, and

major residential markets in the northeastern United States.

This proximity, together with the stable nature of Appalachian

Basin production and the availability of transportation

facilities, has resulted in generally higher realized prices for

Appalachian Basin natural gas (including Marcellus Shale

formation natural gas) than realized prices available in other

regions of the United States.

|

The average realized sales prices for gas gathered and sold on

ECA’s Greene County Gathering System (prior to any

deduction for post-production costs) for each year in the three

year period ended June 30, 2009 and the average NYMEX price

for the same period are detailed in the table below:

| |

|

|

|

|

|

|

|

|

|

|

|

Average Greene County

|

|

Average NYMEX

|

|

Year

|

|

Gathering Price/MMBtu

|

|

Price/MMBtu

|

|

|

|

2007

|

|

$

|

7.17

|

|

|

$

|

6.86

|

|

|

2008

|

|

|

8.46

|

|

|

|

8.02

|

|

|

2009

|

|

|

6.85

|

|

|

|

6.39

|

|

10

During this three year period, ECA’s Greene County

Gathering System received an average price that was $0.40 per

MMBtu higher than the average NYMEX price for the same period.

In establishing the subordination and incentive thresholds, ECA

has assumed a basis differential of $0.15 per MMBtu.

RISK

FACTORS

An investment in the common units involves risks associated

with, among other things, energy commodity prices, the operation

of the Underlying Properties, measurement of reserves,

post-production expenses and any applicable taxes payable by the

trust, the ability of ECA to drill the PUD Wells, the financial

condition of ECA, certain regulatory and legal matters, the

structure of the trust and the characteristics of the trust

units. Please read carefully these risks and other risks

described under “Risk Factors” on page 16.

PROVED

RESERVES

Proved reserves of Underlying Properties and royalty

interests. The following table, effective as of

March 31, 2010, sets forth certain estimated proved

reserves, estimated future net revenues and the discounted

present value thereof attributable to the Underlying Properties,

the PDP Royalty Interest and the PUD Royalty Interest, in each

case derived from the reserve report. The reserve report was

prepared by Ryder Scott in accordance with criteria established

by the Securities and Exchange Commission, or “SEC.”

In accordance with the SEC’s new rules, the reserves

presented below were determined using the twelve month

unweighted arithmetic average of the

first-day-of-the-month

price for the period from April 1, 2009 through

March 1, 2010, without giving effect to the derivative

transactions, and were held constant for the life of the

properties. This yielded a price for natural gas of $3.984 per

MMBtu. Proved reserve quantities attributable to the royalty

interests are calculated by multiplying the gross reserves for

each property by the royalty interest assigned to the trust in

each property. The net revenues attributable to the trust’s

reserves are net of the trust’s obligation to reimburse ECA

for post-production costs. The reserves related to the

Underlying Properties include all proved reserves expected to be

economically produced from the Marcellus Shale formation during

the life of the properties. The reserves and revenues

attributable to the trust’s interests include only the

reserves attributable to the Underlying Properties that are

expected to be produced within the 20-year period in which the

trust owns the royalty interest as well as the 50% residual

interest in the reserves that the trust will own on the

Termination Date. A summary of the reserve report is included as

Annex A to this prospectus.

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proved Gas

|

|

|

|

|

|

Discounted

|

|

|

|

|

Reserves

|

|

|

Estimated Future

|

|

|

Estimated Future

|

|

|

Proved Reserves

|

|

(Bcfe)

|

|

|

Net Revenues

|

|

|

Net Revenues (1)

|

|

|

|

|

(Dollars in thousands)

|

|

|

|

|

Underlying Properties

|

|

|

193.8

|

|

|

$

|

507,289

|

|

|

$

|

168,687

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Royalty Interests:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PDP Royalty Interest (90%) (2)

|

|

|

32.2

|

|

|

$

|

119,757

|

|

|

$

|

67,161

|

|

|

PUD Royalty Interest (50%)

|

|

|

72.4

|

|

|

$

|

269,175

|

|

|

$

|

133,109

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total

|

|

|

104.6

|

|

|

$

|

388,932

|

|

|

$

|

200,270

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1)

|

|

The present values of future net

revenues for the Underlying Properties and the royalty interests

were determined using a discount rate of 10% per annum.

|

| |

|

(2)

|

|

Includes reserves currently behind

pipe in existing wells which are in the process of being

completed.

|

11

Annual production attributable to royalty

interests. The following bar graph shows estimated

annual production from the Underlying Properties attributable to

the royalty interests based on the pricing and other assumptions

set forth in the reserve report. The production estimates

include the impact of additional production that is expected as

a result of the drilling of the PUD Wells. The net production

for 2010 only includes the nine months from April 1, 2010.

12

THE

OFFERING

|

|

|

|

Common units offered to public |

|

9,000,000 common units |

| |

|

|

|

10,350,000 common units, if the underwriters exercise their

over-allotment option in full |

| |

|

Trust units owned by ECA after the offering |

|

3,395,433 common units and 4,500,000 subordinated units |

| |

|

|

|

2,045,433 common units and 4,500,000 subordinated

units, if the underwriters exercise their over-allotment option

in full |

| |

|

Common units owned by the Private Investors |

|

1,104,567 common units. For more information on the common units

owned by the Private Investors, please read “Certain

Transactions.” |

| |

|

Total units outstanding after the offering |

|

13,500,000 common units and 4,500,000 subordinated

units |

| |

|

Use of proceeds |

|

The trust is offering the common units to be sold in this

offering. Assuming no exercise of the underwriters’

over-allotment option and an initial public offering price of

$ per common unit, the

estimated net proceeds of this offering will be approximately

$ million, after deducting

underwriting discounts and commissions and offering expenses.

The trust will use the net proceeds to pay a wholly-owned

subsidiary of ECA for the conveyance of the Term Royalties. In

turn, such subsidiary will use such amount to repay a

$ million demand note payable

to ECA to be issued as consideration for the transfer of the

Term Royalties thereto. |

| |

|

|

|

The trust will use the net proceeds from any exercise of the

underwriters’ over-allotment option to repurchase an equal

number of common units from ECA at the initial public offering

price, after deducting underwriting discounts and commissions. |

| |

|

|

|

ECA will use the proceeds received both from the repayment of

the demand note by ECA’s subsidiary and from any exercise

of the underwriters’ over-allotment option for general

corporate purposes, including for the drilling of PUD Wells. |

| |

|

Proposed NYSE symbol |

|

“ECT” |

| |

|

Quarterly cash distributions |

|

Actual cash distributions to the trust unitholders will

fluctuate quarterly based on the quantity of natural gas

produced from the Underlying Properties, the prices received for

natural gas production and other factors. |

13

|

|

|

|

|

|

Because payments to the trust will be generated by depleting

assets and the trust has a finite life with the production from

the Underlying Properties initially increasing and subsequently

diminishing over time, a portion of each distribution will

represent a return of your original investment and the target

distributions will decline over time. Production declines are

expected to be offset in the near term by production realized

from the drilling and successful completion of the PUD Wells. |

| |

|

|

|

It is expected that quarterly cash distributions during the term

of the trust will be made by the trustee on or about the 60th

day following the end of each calendar quarter to the trust

unitholders of record on or about the 45th day following each

calendar quarter. The first distribution from the trust to the

trust unitholders will be made on or about August 31, 2010.

The first distribution to the trust unitholders will be based

upon amounts to be received from ECA for estimated production

attributable to the royalty interests and proceeds attributable

to the hedging contracts for the period commencing on

April 1, 2010 and ending on June 30, 2010, regardless

or whether such amounts have actually been received by ECA from

the purchaser of the natural gas produced. |

| |

|

Termination of the trust |

|

The trust will begin to liquidate on the Termination Date and

will soon thereafter wind up its affairs and terminate. The Term

Royalties will automatically revert to ECA at the Termination

Date, while the Perpetual Royalties will be sold and the

proceeds thereof will be distributed to the unitholders at the

Termination Date or soon thereafter. ECA will have a first right

of refusal to purchase the Perpetual Royalties at the

Termination Date. |

| |

|

Summary of income tax considerations |

|

The trust will be treated as a partnership for federal income

tax purposes. Consequently, the trust will not incur any federal

income tax liability. Instead, trust unitholders will be

allocated an amount of the trust’s income, gain, loss, or

deductions corresponding to their interest in the trust, which

amounts may differ in timing or amount from actual

distributions. The Term PDP Royalty will and the Term PUD

Royalty should be treated as debt instruments for federal income

tax purposes, and the trust will be required to treat a portion

of each payment it receives with respect to each such royalty

interest as interest income in accordance with the

“noncontingent bond method” under the original issue

discount rules contained in the Internal Revenue Code of 1986,

as amended, and the corresponding regulations. The Perpetual PDP

Royalty will and the Perpetual PUD Royalty should be treated as

mineral royalty interests for federal income tax purposes, which

generates |

14

|

|

|

|

|

|

ordinary income subject to depletion. Please read “Federal

income tax considerations.” |

| |

|

Estimated ratio of taxable income to distributions |

|

The trust estimates that if you own the units you purchase in

this offering through the record date for distributions for the

period ending December 31, 2012, you will be allocated, on

a cumulative basis, an amount of federal taxable income for that

period that will be % or less of

the cash distributed to you with respect to that period. For

example, if you receive an annual distribution of

$ per unit, the trust estimates

that your average allocable federal taxable income per year will

be no more than approximately $

per unit. Please read “Federal income tax

considerations.” |

15

RISK

FACTORS

Drilling and completion of the development wells on the

underlying PUD properties are high risk activities with many

uncertainties that could delay ECA’s anticipated drilling

schedule and adversely affect future production from the

Underlying Properties. Any such delays or reductions in

production could decrease future revenues that are available for

distribution to unitholders.

The drilling and completion of the development wells on the

underlying PUD properties are subject to numerous risks beyond

ECA’s and the trust’s control, including risks that

could delay ECA’s current drilling schedule for the PUD

Wells and the risk that drilling will not result in commercially

viable natural gas production. ECA’s decisions to develop

or otherwise exploit certain areas within the AMI will depend in

part on the evaluation of data obtained through geophysical and

geological analyses, production data and engineering studies,

the results of which are often inconclusive or subject to

varying interpretations. ECA’s costs of drilling,

completing and operating wells are often uncertain before

drilling commences. Overruns in budgeted expenditures are common

risks that can make a particular project uneconomical. Further,

ECA’s future business, financial condition, results of

operations, liquidity or ability to finance planned capital

expenditures could be materially and adversely affected by any

factor that may curtail, delay or cancel drilling, including the

following:

|

|

|

| |

•

|

delays imposed by or resulting from compliance with regulatory

requirements including permitting;

|

| |

| |

•

|

unusual or unexpected geological formations;

|

| |

| |

•

|

shortages of or delays in obtaining equipment and qualified

personnel;

|

| |

| |

•

|

equipment malfunctions, failures or accidents;

|

| |

| |

•

|

lack of available gathering facilities or delays in construction

of gathering facilities;

|

| |

| |

•

|

lack of available capacity on interconnecting transmission

pipelines;

|

| |

| |

•

|

unexpected operational events and drilling conditions;

|

| |

| |

•

|

pipe or cement failures;

|

| |

| |

•

|

casing collapses;

|

| |

| |

•

|

lost or damaged drilling and service tools;

|

| |

| |

•

|

loss of drilling fluid circulation;

|

| |

| |

•

|

uncontrollable flows of natural gas and fluids;

|

| |

| |

•

|

fires and natural disasters;

|

| |

| |

•

|

environmental hazards, such as natural gas leaks, pipeline

ruptures and discharges of toxic gases;

|

| |

| |

•

|