Attached files

| file | filename |

|---|---|

| EX-32.1 - EX321 - CONSTITUTION MINING CORP | ex321.htm |

| EX-21.1 - EX211 - CONSTITUTION MINING CORP | ex211.htm |

| EX-32.2 - EX322 - CONSTITUTION MINING CORP | ex322.htm |

| EX-24.1 - EX241 - CONSTITUTION MINING CORP | ex241.htm |

| EX-31.1 - EX311 - CONSTITUTION MINING CORP | ex311.htm |

| EX-31.2 - EX312 - CONSTITUTION MINING CORP | ex312.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

Form

10-K

ý ANNUAL REPORT

UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the

fiscal year ended December 31,

2009.

¨ TRANSITION REPORT UNDER

SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the

transition period from

to _______.

Commission

file number: 000-49725

Constitution

Mining Corp.

(Exact

name of registrant as specified in its charter)

|

Delaware

|

88-0455809

|

|

|

(State

or other jurisdiction of incorporation or organization)

|

(I.R.S.

Employer Identification No.)

|

|

|

Pasaje

Martir Olaya 129, Oficina 1203, Centro Empresarial Jose Pardo Torre A,

Miraflores, Lima, Peru

|

||

|

(Address

of principal executive

offices) (Zip

Code)

|

||

|

Registrant’s

telephone, including area code: +54-1-446-6807

|

||

Securities

registered under Section 12(b) of the Exchange Act: None.

Securities

registered under Section 12(g) of the Exchange

Act:

|

Common

Stock, $0.001 par value

|

Not

Applicable

|

|

(Title

of class)

|

(Name

of each exchange on which

registered)

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No ý

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

past 12 months (or for such shorter period that the registrant was required to

file such reports), and (2) has been subject to such filing requirements for the

past 90 days. Yes ý No ¨

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K (229.405 of this chapter) is not contained herein, and will be

contained, to the best of registrant’s knowledge, in definitive proxy or

information statements incorporated by reference in Part III of this Form 10-K

or any amendment to this Form 10-K. ý

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company. See the definitions of “large accelerated filer,”

“accelerated filer” and “smaller reporting company” in Rule 12b-2 of the

Exchange Act.

Large

accelerated filer ¨ Accelerated

filer ¨

Non-accelerated

filer ¨ (Do not check if a

smaller reporting

company) Smaller

reporting company ý

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). Yes ¨ No ý

As of

June 30, 2009, the aggregate market value of the Company’s common equity held by

non-affiliates computed by reference to the closing price ($0.60)

was: $36,131,674

The

number of shares of our common stock outstanding as of March 1, 2010

was: 78,055,985

Documents

Incorporated by Reference: Parts of our definitive proxy statement to

be prepared and filed with the Securities and Exchange Commission not later than

120 days after December 31, 2009 are incorporated by reference into Part III of

this Form 10-K.

FORM

10-K

CONSTITUTION

MINING CORP.

DECEMBER

31, 2009

| Page | |

| PART I | |

|

Item

1. Business.

|

5

|

|

Item

1A. Risk

Factors.

|

10

|

|

Item

1B. Unresolved Staff Comments.

|

17

|

|

Item

2. Properties.

|

17

|

|

Item

3. Legal Proceedings.

|

30

|

|

Item

4. (Removed and Reserved).

|

30

|

|

PART

II

|

|

32

|

|

|

Item

6. Selected Financial Data.

|

34

|

|

34

|

|

|

40

|

|

|

40

|

|

|

40

|

|

|

Item

9A. Controls and

Procedures.

|

40

|

|

Item

9B. Other

Information.

|

41

|

|

PART

III

|

|

42

|

||

|

Item

11. Executive Compensation.

|

42

|

|

|

42

|

||

|

42

|

||

| Item 14. Principal Accounting Fees and Services. | 42 | |

|

PART

IV

|

Cautionary

Note Regarding Forward Looking Statements

This

annual report contains forward-looking statements as that term is defined in

Section 27A of the Securities Act of 1933, as amended, and Section 21E

of the Securities Exchange Act of 1934, as amended. In some cases,

you can identify forward-looking statements by terminology such as "may,"

"should," "expects," "plans," "anticipates," "believes," "estimates,"

"predicts," "potential," "continue," "intends," and other variations of these

words or comparable words. In addition, any statements that refer to

expectations, projections or other characterizations of events, circumstances or

trends and that do not relate to historical matters are forward-looking

statements. These forward-looking statements are based largely on our

expectations or forecasts of future events, can be affected by inaccurate

assumptions, and are subject to various business risks and known and unknown

uncertainties, a number of which are beyond our control. Therefore,

actual results could differ materially from the forward-looking statements

contained in this document, and readers are cautioned not to place undue

reliance on such forward-looking statements. These statements are

only predictions and involve known and unknown risks, uncertainties and other

factors, including the risks in the section entitled “Risk Factors” that may

cause our or our industry’s actual results, levels of activity, performance or

achievements to be materially different from any future results, levels of

activity, performance or achievements expressed or implied by these

forward-looking statements.

Important

factors that may cause the actual results to differ from the forward-looking

statements, projections or other expectations include, but are not limited to,

the following:

|

·

|

risk

that we fail to meet the requirements of the agreement under which we

acquired our options, including any payments or any exploration

obligations that we have regarding these properties, which could result in

the loss of our right to exercise the options to acquire the mineral and

mining rights underlying these

properties;

|

|

·

|

risk

that we will not be able to complete the possible acquisition of

additional mineral deposits pursuant to terms and conditions outlined in a

letter of intent;

|

|

·

|

risk

that we cannot attract, retain and motivate qualified personnel,

particularly employees, consultants and contractors for our operations in

Peru;

|

|

·

|

risks

and uncertainties relating to the interpretation of drill results, the

geology, grade and continuity of mineral

deposits;

|

|

·

|

results

of initial feasibility, pre-feasibility and feasibility studies, and the

possibility that future exploration, development or mining results will

not be consistent with our

expectations;

|

|

·

|

mining

and development risks, including risks related to accidents, equipment

breakdowns, labor disputes or other unanticipated difficulties with or

interruptions in production;

|

|

·

|

the

potential for delays in exploration or development activities or the

completion of feasibility studies;

|

|

·

|

risks

related to the inherent uncertainty of production and cost estimates and

the potential for unexpected costs and

expenses;

|

|

·

|

risks

related to commodity price

fluctuations;

|

|

·

|

the

uncertainty of profitability based upon our history of

losses;

|

|

·

|

risks

related to failure to obtain adequate financing on a timely basis and on

acceptable terms for our planned exploration and development

projects;

|

|

·

|

risks

related to environmental regulation and liability;

|

|

·

|

risks

that the amounts reserved or allocated for environmental compliance,

reclamation, post-closure control measures, monitoring and on-going

maintenance may not be sufficient to cover such

costs;

|

|

|

|

·

|

risks

related to tax assessments;

|

|

·

|

political

and regulatory risks associated with mining development and exploration;

and

|

|

·

|

other

risks and uncertainties related to our prospects, properties and business

strategy.

|

Although

we believe that the expectations reflected in the forward-looking statements are

reasonable, we cannot guarantee future results, levels of activity, performance

or achievements. You should not place undue reliance on these

forward-looking statements, which speak only as of the date of this

report. Except as required by law, we do not undertake to update or

revise any of the forward-looking statements to conform these statements to

actual results, whether as a result of new information, future events or

otherwise.

As used

in this annual report, “Constitution Mining,” the “Company,” “we,” “us,” or

“our” refer to Constitution Mining Corp., unless otherwise

indicated.

If you

are not familiar with the mineral exploration terms used in this

report, please refer to the definitions of these terms under the caption

“Glossary” at the end of Item 15 of this report.

PART

I

ITEM 1. Business.

Corporate

History

We were

incorporated in the state of Nevada under the name Crafty Admiral Enterprises,

Ltd. on March 6, 2000. Our original business plan was to sell classic

auto parts to classic auto owners all over the world through an Internet

site/online store; however, we were unsuccessful in implementing the online

store and were unable to afford the cost of purchasing, warehousing and shipping

the initial inventory required to get the business started. As a

result, we ceased operations in approximately July 2002.

During

our fiscal year ended December 31, 2006, we reorganized our operations to pursue

the exploration, development, acquisition and operation of oil and gas

properties. On June 27, 2006, we acquired a leasehold interest in a

mineral, oil and gas property located in St. Francis County, Arkansas for a cash

payment of $642,006, pursuant to an oil and gas agreement we entered into on

April 29, 2006 (the “Tombaugh Lease”). Shortly after acquiring the

Tombaugh Lease, we suspended our exploration efforts on the property covered by

the Tombaugh Lease in order to pursue business opportunities developing nickel

deposits in Finland, Norway and Western Russia. On January 18, 2008,

we assigned all of our right, title and interest in and to the Tombaugh Lease to

Fayetteville Oil and Gas, Inc., which agreed to assume all of our outstanding

payment obligations on the Tombaugh Lease as consideration for the

assignment. On March 9, 2007, we changed our name to better reflect

our business to “Nordic Nickel Ltd.” pursuant to a parent/subsidiary merger with

our wholly-owned non-operating subsidiary, Nordic Nickel Ltd., which was

established for the purpose of giving effect to this name change. We

were not successful pursuing business opportunities developing nickel deposits

in Finland, Norway and Western Russia and again sought to reorganize our

operations in November 2007.

In

November 2007, we reorganized our operations and changed our name to

“Constitution Mining Corp.” to better reflect our current focus which is the

acquisition, exploration, and potential development of mining

properties. Since November 2007, we entered into agreements to secure

options to acquire the mineral and mining rights underlying properties located

in the Salta and Mendoza provinces of Argentina (the "Argentinean Properties")

and in northeastern Peru. In 2009, we determined that it was in our

best interest to no longer pursue the exploration and development of the

Argentinean Properties and terminated our option agreements to acquire the

mineral and mining rights underlying these properties. We are now

exclusively pursuing the exploration and development of our property interests

in Peru.

On

October 21, 2009, we completed a reincorporation merger from the State of Nevada

to the State of Delaware.

Our

common stock is quoted on the OTC Bulletin Board under the symbol

“CMIN.” We conduct our business from Pasaje Martir Olaya 129, Oficina

1203, Centro Empresarial Jose Pardo Torre A, Miraflores, Lima, Peru. Our

telephone number is +54-1-446-6807.

Exploration

Stage Company

We are

considered an exploration or exploratory stage company because we are involved

in the examination and investigation of land that we believe may contain

valuable minerals, for the purpose of discovering the presence of ore, if any,

and its extent. There is no assurance that a commercially viable

mineral deposit exists on the properties underlying our mineral property

interests and a great deal of further exploration will be required before a

final evaluation as to the economic and legal feasibility for our future

exploration is determined. We have no known reserves of any type of

mineral. To date, we have not discovered an economically viable

mineral deposit on the property underlying our mineral property interests, and

there is no assurance that we will discover one. If we cannot acquire

or locate mineral deposits, or if it is not economical to recover any mineral

deposits that we do find, our business and operations will be materially and

adversely affected.

Surplus

Strategy

Our

current business plan calls for investing any surplus operating capital

resulting from retained earnings into bullion accounts and does not include

holding retained earnings, if any, in cash or cash equivalents. In

the event that commercially exploitable reserves of minerals exist on any of our

property interests and we are able to make a profit, our business plan is to

sell enough mineral reserves to satisfy all of our expenses and invest all

retained mineral reserves in bullion accounts established in Zurich,

Switzerland. The price of precious and base metals such as gold and

silver has fluctuated widely in recent years, and is affected by numerous

factors beyond our control, including international, economic and political

trends, expectations of inflation, currency exchange fluctuations, interest

rates, global or regional consumptive patterns, speculative activities and

increased production due to new extraction developments and improved extraction

and production methods. The effect of these factors on the price of

base and precious metals, and, therefore, the change in the value of our

retained earnings, if any, held in bullion accounts cannot accurately be

predicted and is subject to significant fluctuation. There can be no

assurance that the value of any bullion accounts established by us in the future

to hold retained mineral reserves, if any, will not be adversely impacted by

fluctuations in the price of base and precious metals resulting in significant

losses.

Summary

of our Mineral Property Interests

A

description of each of our options to acquire the mineral and mining rights

underlying properties located in Peru and the conditions that we must meet to

exercise these options is set forth in Item 2 of this annual

report.

Effect

of Governmental Regulation on Our Business

We will

be required to comply with all regulations, rules and directives of governmental

authorities and agencies applicable to the exploration of minerals in

Peru. The discussion that follows is a summary of the most

significant government regulations which we anticipate will impact our

operations.

Peru is

located on the western coast of South America and has a population of

approximately 28 million. It covers a geographic area of

approximately 1.3 million square kilometres and is bordered by Bolivia, Brazil,

Chile, Colombia and Ecuador. Lima is Peru's capital and principal

city and has a population of approximately 7 million people.

Peru has

become a leading country for mining activities. No special taxes or

registration requirements are imposed on foreign-owned companies and foreign

investment is treated as equal to domestic capital. Peruvian law

allows for full repatriation of capital and profits and the country’s mining

legislation provides access to mining concessions under an efficient

registration system.

Peruvian

Mining Law

Under

Peru’s Uniform Text of Mining Law (“UTM”), the right to explore for and exploit

minerals is granted by the government by way of concessions. A

Peruvian mining concession is a property right, independent from the ownership

of surface land on which it is located. There are no restrictions or

special requirements applicable to foreign companies or individuals regarding

the holding of mining concessions in Peru unless the concessions are within 50

kilometres of Peru's borders. The rights granted by a mining

concession can be transferred, or sold and, in general, may be the subject of

any transaction or contract. Mining concessions may be privately

owned and no state participation is required.

The

application for a mining concession involves the filing of documents before the

mining administrative authority. The mining concession boundaries are

specified in the application documents, with no requirement to mark the

concession boundaries in the field since the boundaries are fixed by UTM

coordinates. In order to conduct exploration or mining activities,

the holder of a mining concession must purchase the surface land required for

the project or reach agreement with the owner for its temporary

use. If any of this is not possible, a legal easement may be

requested from the mining authorities, although these easements have been rarely

granted.

Mining

concessions are irrevocable as long as their holders pay an annual fee of US $3

per hectare and reach minimum production levels within the terms set forth by

law or otherwise pay penalties, as applicable. Non-compliance with

any of these mining obligations for two consecutive years will result in the

cancellation of the mining concession.

Pursuant

to the original legal framework in force since 1992, holders of mining

concessions are obliged to achieve a minimum production of US $100 per hectare

per year within six years following the year in which the respective mining

concession title is granted. If this minimum production is not

reached, as of the first six months of the seventh year, the holder of the

concession shall pay a US $6 penalty per hectare per year until such production

is reached and penalties increase to US $20 in the twelfth

year. Likewise, it is possible to avoid payment of the penalty if

evidence is submitted to the mining authorities that an amount ten times the

applicable penalty or more had been invested.

However,

this regime has been recently and partially amended providing for, among other

matters, increased minimum production levels, new terms for obtaining such

minimum production, increased penalties in case such minimum production is not

reached, and even the cancellation of mining concessions if minimum production

is not reached within certain terms. Pursuant to this new regime, the

holder of the mining concession should achieve a minimum production of at least

one tax unit (S/. 3,500, approximately US $1,100) per hectare per year, within a

ten-year term following the year in which the mining concession title is

granted. If such minimum production is not reached within the

referred term, the holder of the concession shall pay penalties equivalent to

10% of the tax unit.

If the

minimum production is not reached within a fifteen-year term following the

granting of the concession title, the mining concession shall be cancelled by

the mining authority, unless (i) a qualified force majeure event is evidenced to

and approved by the mining authority, or (ii) by paying the applicable penalties

and concurrently evidencing minimum investments of at least ten times the amount

of the applicable penalties; in which cases the concession may not be cancelled

up to a maximum term of five additional years. If minimum production

is not reached within a twenty-year term following the granting of the

concession title, the concession shall inevitably be cancelled.

This

amended regime is currently applicable to all new mining concessions granted

since October 11, 2008. Regarding those mining concessions existing prior to

such date, the new term for obtaining the increased minimum production level or

otherwise pay the increased penalties pursuant to the amended regime shall be

counted as from the first business day of 2009. Nevertheless, until

such new term for obtaining the increased minimum production level does not

expire, the minimum production level, the term for obtaining such minimum

production, the amount of the penalties and the causes for cancellation of the

mining concessions shall continue to be those provided in the original legal

framework existing since 1992.

The

amended regime shall not be applicable to (i) those concessions handed by the

Peruvian State through private investment promotion procedures, which shall

maintain the production and investment obligations contained in their respective

agreements, and/or (ii) to titleholders of concessions with mining stability

agreements in force.

Environmental

Laws

The

Peruvian Ministry of Energy and Mines ("MEM") regulates environmental affairs in

the mining sector, including establishing an environmental protection

regulations; while the Organism for Supervising Investment in Energy and Mining

verifies environmental compliance and imposes administrative sanctions, although

it is likely that in the near future this functions be assumed by the recently

created Ministry of Environment.

Each

stage of exploration or mining requires some type of authorization or permit,

beginning with an application for an environmental permit for initial

exploration and continuing with an Environmental Impact Assessment ("EIA") for

mining, which includes public hearings.

For

permitting purposes, exploration activities in Peru are classified in two

categories:

|

·

|

Category

I projects: Mining exploration activities that comprise

any of the following: (i) a maximum of twenty drilling

platforms; (ii) a disturbed area of less than ten hectares considering

drilling platforms, trenches, auxiliary facilities and access means; and,

(iii) the construction of tunnels with a total maximum length of fifty

meters. Holders of these projects must submit an Environmental

Impact Statement (“EIS”) before the MEM, which in principle, is subject to

automatic approval upon its filing, and subject to subsequent (ex post)

review by the latter. Nevertheless, in any of the following

cases, the project shall not be subject to automatic approval and shall

necessarily obtain an express prior approval by MEM, which should be

granted, in principle, within a term of two months since filing the EIS:

(i) the project is located in a protected natural area or its buffer zone;

(ii) the project is oriented to determining the existence of radioactive

minerals; (iii) the platforms, drill holes, trenches, tunnels or other

components would be located within certain specially environmental

sensitive areas specified in the applicable regulations (e.g., glaciers,

springs, water wells, groundwater wells, protection lands, primary woods,

etc.); (iv) the project covers areas where mining environmental

contingencies or non-environmental rehabilitated previous mining works,

already exist.

|

|

·

|

Category

II projects: Mining exploration activities that comprise

any of the following: (i) more than twenty drilling platforms; (ii) a

disturbed area of more than ten hectares considering drilling plants,

trenches, auxiliary facilities and access means; and, (iii) the

construction of tunnels over a total length of fifty

meters. These projects require an authorization that should be

granted once the semi-detailed Environmental Impact Assessment ("EIA") is

approved by the MEM. Such authorization should, in principle, take

approximately four months.

|

Before

initiating construction or exploitation activities or the expansion of existing

operations, an EIA should be approved. This process of authorization

involves public hearings in the place where the project is located and, in

general, should conclude within a term of 120 calendar days, although such

process can require between eight months and one year.

Holders

of mining activities performing mining exploration shall conduct remediation

works of disturbed areas, as part of the progressive closure of the

project. Likewise, they are required to undertake the final closure

and post closure actions as set forth in the terms and conditions in the

approved environmental instrument.

If the

holder carries out mining exploration activities involving the removal of more

than 10,000 tonnes of material, or more than 1,000 tonnes of material with a

potential neutralization ("PN") over potential acidity (“PA”) relation lower

than 3 (PN/PA<3), then they shall be required to file a Mine Closure Plan

(“MCP”) along with the corresponding environmental instrument, as well as to

establish a financial guarantee to secure compliance with such MCP.

Holders

of mining exploitation activities must file a MCP before the MEM within one year

of the approval of their EIA. The MCP must be implemented from the

beginning of the mining operation. Semi-annual reports must be filed

evidencing compliance with the MCP. An environmental guarantee

covering the MCP’s estimated costs is also required to be granted.

Mining

Royalties

Peruvian

law requires that concession holders pay a mining royalty as consideration for

the extraction of mineral resources. The mining royalty is payable

monthly on a variable cumulative rate of 1% to 3% of the value of the ore

concentrate or equivalent, calculated in accordance with price quotations in

international markets, subject to certain deductions such as indirect taxes,

insurance, freight and other specified expenses. The mining royalty

payable is determined based on the following schedule: (i) under US $60 million

of annual sales of concentrates: 1% royalty; (ii) in excess of US $60 million

and up to US $120 million of annual sales: 2% royalty; and (iii) in excess

of US $120 million of annual sales: 3% royalty.

Competition

We are an

exploration stage mineral resource exploration company that competes with other

mineral resource exploration companies for financing and for the acquisition of

new mineral properties. Many of the mineral resource exploration

companies with whom we compete have greater financial and technical resources

than those available to us. Accordingly, these competitors may be

able to spend greater amounts on acquisitions of mineral properties of merit, on

exploration of their mineral properties and on development of their mineral

properties. In addition, they may be able to afford more geological

expertise in the targeting and exploration of mineral

properties. This competition could result in competitors having

mineral properties of greater quality and interest to prospective investors who

may finance additional exploration and development. This competition

could adversely impact on our ability to achieve the financing necessary for us

to conduct further exploration of our mineral properties. We will

also compete with other mineral exploration companies for financing from a

limited number of investors that are prepared to make investments in mineral

exploration companies. The presence of competing mineral exploration

companies may impact on our ability to raise additional capital in order to fund

our exploration programs if investors are of the view that investments in

competitors are more attractive based on the merit of the mineral properties

under investigation and the price of the investment offered to

investors. We will also be compete with other mineral companies for

available resources, including, but not limited to, professional geologists,

camp staff, mineral exploration supplies and drill rigs.

Intellectual

Property

We do not

own, either legally or beneficially, any patent or trademark.

Employees

We have

no full-time employees at the present time. Our executive officers do

not devote their services full time to our operations. We engage

contractors from time to time to consult with us on specific corporate affairs

or to perform specific tasks in connection with our exploration

programs. As of December 31, 2009, we engaged approximately 21

contractors that provided work to us on a recurring basis.

Research

and Development Expenditures

We have

not incurred any research or development expenditures since our

incorporation.

Subsidiaries

Constitution

Mining SA is a subsidiary entity which was registered with the General

Inspection of Corporations in Argentina on March 4, 2008 and formed for the

purpose of acquiring and exploring natural resource properties in

Argentina.

We own a

50% interest in the issued and outstanding stock of Bacon Hill Invest Inc.

(“Bacon Hill”), a corporation incorporated under the laws of

Panama. The remaining 50% interest in the issued and outstanding

stock of Bacon Hill is owned by Temasek Investments Inc., a company incorporated

under the laws of Panama. Bacon Hill indirectly owns the mineral and

mineral rights to certain properties located in Peru held by its subsidiary,

Compañía Minera Marañón S.A.C.

ITEM 1A. Risk

Factors.

You

should carefully consider the following risk factors in evaluating our business

and us. The factors listed below represent certain important factors

that we believe could cause our business results to differ. These

factors are not intended to represent a complete list of the general or specific

risks that may affect us. It should be recognized that other risks

may be significant, presently or in the future, and the risks set forth below

may affect us to a greater extent than indicated. If any of the

following risks occur, our business, financial condition or results of

operations could be materially and adversely affected. You should

also consider the other information included in this annual report and

subsequent quarterly reports filed with the SEC.

Risk

Factors

Risks

Associated With Our Business

Our

accountants have raised substantial doubt with respect to our ability to

continue as a going concern.

As noted

in our financial statements, we have incurred a net loss of $16,662,828 for the

period from inception on March 6, 2000 to December 31, 2009 and have no present

source of revenue. At December 31, 2009, we had a working capital

deficiency of $14,807,730. As of December 31, 2009, we had cash and

cash equivalents in the amount of US $205,125. We will have to raise

additional funds to meet our currently budgeted operating requirements for the

next twelve months.

The audit

report of James Stafford, Inc., Chartered Accountants, for the fiscal year ended

December 31, 2009 and 2008 contained a paragraph that emphasizes the substantial

doubt as to our continuance as a going concern. This is a significant

risk that we may not be able to generate and/or raise enough resources to remain

operational for an indefinite period of time.

We

own the options to acquire the mining and mineral rights underlying certain

properties and if we fail to perform the obligations necessary to exercise these

options we will lose our options and cease operations.

We hold

options to acquire the mineral and mining rights underlying certain properties

located in northeastern Peru, subject to certain conditions. If we

fail to meet the requirements of the amended agreement under which we acquired

such options, including any payments and/or any exploration obligations that we

have regarding these properties, we may lose our right to exercise the options

to acquire the mineral and mining rights underlying these

properties. If we do not fulfill these conditions, then our ability

to commence or continue operations could be materially limited. In

addition, substantially all of our assets will be put into commercializing our

rights to the areas covered by these options. Accordingly, any

adverse circumstances that affect the areas covered by these option agreements

and our rights thereto would affect us and your entire investment in shares of

our common stock. If any of these situations were to arise, we would

need to consider alternatives, both in terms of our prospective operations and

for the financing of our activities. Management cannot provide

assurance that we will ultimately achieve profitable operations or become

cash-flow positive, or raise additional debt and/or equity

capital. If we are unable to raise additional capital in the near

future, we will experience liquidity problems and management expects that we

will need to curtail operations, liquidate assets, seek additional capital on

less favorable terms and/or pursue other remedial measures, including ceasing

operations.

We

have a limited operating history and have incurred losses that we expect to

continue into the future.

We have

not yet located any mineral reserve, nor are there any proven reserves on any of

the properties for which we hold options, and we have never had any revenues

from our operations. In addition, we have a very limited operating

history upon which an evaluation of our future success or failure can be

made. We have only recently taken steps in a plan to engage in the

acquisition of interests in exploration and development properties, and it is

too early to determine whether such steps will prove successful. Our

business plan is in its early stages and faces numerous regulatory, practical,

legal and other obstacles. At this early stage of our operation, we

also expect

to face

the risks, uncertainties, expenses and difficulties frequently encountered by

companies at the start-up stage of their business development. We cannot be sure

that we will be successful in addressing these risks and uncertainties, and our

failure to do so could have a materially adverse effect on our financial

condition.

No

assurances can be given that we will be able to successfully complete the

purchase of mining rights to any properties, including the ones for which we

currently hold options. Our ability to achieve and maintain

profitability and positive cash flow over time will be dependent upon, among

other things, our ability to (i) identify and acquire properties or interests

therein that ultimately have probable or proven mineral reserves, (ii) sell such

mining properties or interests to strategic partners or third parties or

commence the production of a mineral deposit, (iii) produce and sell minerals at

profitable margins and (iv) raise the necessary capital to operate during this

possible extended period of time. At this stage in our development,

it cannot be predicted how much financing will be required to accomplish these

objectives.

We

have no known reserves and we may not find any mineral resources or, if we find

mineral resources, the deposits may be uneconomic or production from those

deposits may not be profitable.

Our due

diligence activities have been limited, and to a great extent, have relied upon

information provided to us by third parties. We have not established

that any of the properties for which we hold options contain adequate amounts of

gold or other mineral reserves to make mining any of the properties economically

feasible to recover that gold or other mineral reserves, or to make a profit in

doing so. If we do not, our business will fail. If we

cannot find economic mineral resources or if it is not economic to recover the

mineral resources, we will have to cease operations.

We

may not have access to all of the supplies and materials we need to begin

exploration that could cause us to delay or suspend operations.

Competition

and unforeseen limited sources of supplies in the industry could result in

occasional spot shortages of supplies, such as explosives, and certain

equipment, such as bulldozers and excavators, that we might need to conduct

exploration. We have not attempted to locate or negotiate with any

suppliers of products, equipment or materials. We will attempt to

locate products, equipment and materials. If we cannot find the

products and equipment we need, we will have to suspend our exploration plans

until we do find the products and equipment we need.

We

do not have enough money to complete our exploration and consequently may have

to cease or suspend our operations unless we are able to raise additional

financing.

We

presently do not have sufficient capital to exercise our options to acquire the

mineral and mining rights underlying certain property located in northeastern

Peru. Although management believes that sources of financing are

available to complete the acquisition of these property interests over time, no

assurances can be given that these financing sources will ultimately be

sufficient or available when required. Other forms of financing, if

available, may be on terms that are unfavorable to our

stockholders.

As we

cannot assure a lender that we will be able to successfully explore and develop

our mineral properties, we may find it difficult to raise debt financing from

traditional lending sources. We have traditionally raised our

operating capital from sales of equity and debt securities, but there can be no

assurance that we will continue to be able to do so. If we cannot

raise the money that we need to continue exploration of our mineral properties,

we may be forced to delay, scale back, or eliminate our exploration

activities. If any of these were to occur, there is a substantial

risk that our business would fail.

Our

proposed acquisition of certain mining claims and leasehold interests for

exploration properties located in Nevada is subject to numerous conditions and

contingencies.

On

December 2, 2009, we entered into a letter of intent with Seabridge Gold Inc., a

Canadian corporation (“Seabridge”), to acquire all of Seabridge’s interests in

certain mining claims and leasehold interests for certain exploration properties

located in Nevada. The parties are negotiating the final terms of a

definitive agreement. The

terms of

the definitive agreement being negotiated between the parties contemplates that

closing of the transaction is anticipated to occur on or about May 15,

2010. Closing of the transaction is subject to a number of conditions

and contingences, including the following:

|

·

|

the

approval of the parties’ respective board of directors;

and

|

|

·

|

receipt

of all necessary third party consents, approval and

waivers.

|

We can

give no assurance that these and other conditions will ever be satisfied to

allow us to complete the proposed acquisition in accordance with the proposed

terms or at all.

In

the event that we successfully complete the proposed acquisition of certain

mining claims and leasehold interests for exploration properties located in

Nevada, the consideration payable on the closing of this transaction would have

a significant adverse impact on our resources.

On

December 2, 2009, we entered into a letter of intent with Seabridge to acquire

all of Seabridge’s interests in certain mining claims and leasehold interests

for certain exploration properties located in Nevada. The

consideration for these exploration properties was contemplated in the letter of

intent to consist of the following: staged cash payments totaling $3

million; a $1 million convertible debenture; and 3 million shares of our common

stock. We have to raise additional funds to meet our currently

budgeted operating requirements for the next twelve months and presently would

be unable to meet any obligations we may incur in connection with the

contemplated acquisition of Seabridge’s interests in certain mining claims and

leasehold interests for exploration properties located in Nevada. If

we are unable to raise additional capital in the near future, we will experience

liquidity problems and management expects that we will need to curtail

operations, liquidate assets, seek additional capital on less favorable terms

and/or pursue other remedial measures including ceasing

operations. Even if we succeed in raising additional capital in the

near future, the consideration payable on the closing of the contemplated

transaction with Seabridge would have a significant adverse impact on our

resources and may still result in the need to curtail operations, liquidate

assets, seek additional capital on less favorable terms and/or pursue other

remedial measures including ceasing operations

Our

success is dependent upon a limited number of people.

The

ability to identify, negotiate and consummate transactions that will benefit us

is dependent upon the efforts of our management team. The loss of the

services of any member of our management could have a material adverse effect on

us.

Our

business will be harmed if we are unable to manage growth.

Our

business may experience periods of rapid growth that will place significant

demands on our managerial, operational and financial resources. In

order to manage this possible growth, we must continue to improve and expand our

management, operational and financial systems and controls, particularly those

related to subsidiaries that will be doing business in Peru. We will

need to expand, train and manage our employee base and/or retain qualified

contractors. We must carefully manage our mining exploration

activities. No assurances can be given that we will be able to timely

and effectively meet such demands.

We

may not be able to attract and retain qualified personnel necessary for the

implementation of our business strategy and mineral exploration

programs.

Our

future success depends largely upon the continued service of board members,

executive officers and other key personnel. Our success also depends

on our ability to continue to attract, retain and motivate qualified personnel,

particularly employees, consultants and contractors for our operations in

Peru. Personnel represents a significant asset, and the competition

for such personnel is intense in the mineral exploration industry. We

may have particular difficulty attracting and retaining key personnel in the

initial phases of our operations, particularly in Peru.

Our

officers and directors may have conflicts of interest and do not devote full

time to the our operations.

Our

officers and directors may have conflicts of interest in that they are and may

become affiliated with other mining companies. In addition, our

officers do not devote full time to our operations. Until such time

that we can afford executive compensation commensurate with that being paid in

the marketplace, our officers will not devote their full time and attention to

our operations. No assurances can be given as to when we will be

financially able to engage our officers on a full-time basis.

Some

of our officers and directors are located outside of the United States, you may

have no effective recourse against our us or our management for misconduct and

may not be able to enforce judgment and civil liabilities against our officers,

directors, experts and agents.

Some of

our directors and officers are nationals and/or residents of countries other

than the United States, and all or a substantial portion of such persons’ assets

are located outside the United States. As a result, it may be

difficult for investors to enforce within the United States any judgments

obtained against our officers or directors, including judgments predicated upon

the civil liability provisions of the securities laws of the United States or

any state thereof.

Risks

Associated With Mining

All

of our properties are in the exploration stage. There is no assurance

that we can establish the existence of any mineral resource on any of our

properties in commercially exploitable quantities. Until we can do

so, we cannot earn any revenues from operations and if we do not do so we will

lose all of the funds that we expend on exploration. If we do not

discover any mineral resource in a commercially exploitable quantity, our

business will fail.

We have

not established that any of our properties contain any commercially exploitable

mineral reserve, nor can there be any assurance that we will be able to do

so. If we do not, our business will fail. A mineral

reserve is defined by the Securities and Exchange Commission in its Industry

Guide 7 (which can be viewed over the Internet at http://www.sec.gov/divisions/corpfin/forms/industry.htm#secguide7)

as that part of a mineral deposit which could be economically and legally

extracted or produced at the time of the reserve determination. The

probability of an individual prospect ever having a “reserve” that meets the

requirements of the Securities and Exchange Commission’s Industry Guide 7 is

extremely remote; in all probability, our mineral resource property does not

contain any ‘reserve’ and any funds that we spend on exploration will probably

be lost.

Even if

we do eventually discover a mineral reserve on one or more of our properties,

there can be no assurance that we will be able to develop our properties into

producing mines and extract those resources. Both mineral exploration

and development involve a high degree of risk and few properties that are

explored are ultimately developed into producing mines. If we do

discover mineral resources in commercially exploitable quantities on any of our

properties, we will be required to expend substantial sums of money to establish

the extent of the resource, develop processes to extract it and develop

extraction and processing facilities and infrastructure.

The

commercial viability of an established mineral deposit will depend on a number

of factors including, by way of example, the size, grade and other attributes of

the mineral deposit, the proximity of the resource to infrastructure, such as a

smelter, roads and a point for shipping, government regulation and market

prices. Most of these factors will be beyond our control, and any of

them could increase costs and make extraction of any identified mineral resource

unprofitable.

Mineral

operations are subject to applicable law and government regulation. Even if we

discover a mineral resource in a commercially exploitable quantity, these laws

and regulations could restrict or prohibit the exploitation of that mineral

resource. If we cannot exploit any mineral resource that we might

discover on our properties, our business may fail.

Both

mineral exploration and extraction require permits from various foreign,

federal, state, provincial and local governmental authorities and are governed

by laws and regulations, including those with respect to prospecting, mine

development, mineral production, transport, export, taxation, labor standards,

occupational health,

waste

disposal, toxic substances, land use, environmental protection, mine safety and

other matters. There can be no assurance that we will be able to

obtain or maintain any of the permits required for the continued exploration of

our mineral properties or for the construction and operation of a mine on our

properties at economically viable costs. If we cannot accomplish

these objectives, our business could fail.

We

believe that we are in compliance with all material laws and regulations that

currently apply to our activities, but there can be no assurance that we can

continue to do so. Current laws and regulations could be amended and

we might not be able to comply with them, as amended. Further, there

can be no assurance that we will be able to obtain or maintain all permits

necessary for our future operations, or that we will be able to obtain them on

reasonable terms. To the extent such approvals are required and are

not obtained, we may be delayed or prohibited from proceeding with planned

exploration or development of our mineral properties.

If

we establish the existence of a mineral reserve on any of our properties, we

will require additional capital in order to develop the property into a

producing mine. If we cannot raise this additional capital, we will not be able

to exploit the reserve and our business could fail.

If we do

discover a mineral reserve on any of our properties, we will be required to

expend substantial sums of money to establish the extent of the reserve, develop

processes to extract it and develop extraction and processing facilities and

infrastructure. Although we may derive substantial benefits from the

discovery of a reserve, there can be no assurance that it will be large enough

to justify commercial operations, nor can there be any assurance that we will be

able to raise the funds required for development on a timely

basis. If we cannot raise the necessary capital or complete the

necessary facilities and infrastructure, our business may fail.

Because

our property interest and exploration activities in Peru are subject to

political, economic and other uncertainties, situations may arise that could

have a significantly adverse material impact on us.

Our

activities in Peru are subject to political, economic and other uncertainties,

including the risk of expropriation, nationalization, renegotiation or

nullification of existing contracts, mining licenses and permits or other

agreements, changes in laws or taxation policies, currency exchange

restrictions, changing political conditions and international monetary

fluctuations. Future government actions concerning the economy,

taxation, or the operation and regulation of nationally important facilities

such as mines could have a significant effect on our plans and on our ability to

operate. No assurances can be given that our plans and operations

will not be adversely affected by future developments in those jurisdictions

where we hold property interests.

Because

we presently do not carry title insurance and do not plan to secure any in the

future, we are vulnerable to loss of title.

We do not

maintain insurance against title. Title on mineral properties and

mining rights involves certain inherent risks due to the difficulties of

determining the validity of certain claims as well as the potential for problems

arising from the frequently ambiguous conveyance history characteristic of many

mining properties. Disputes over land ownership are common,

especially in the context of resource developments. We cannot give

any assurance that title to such properties will not be challenged or impugned

and cannot be certain that we will have or acquire valid title to these mining

properties. The possibility also exists that title to existing

properties or future prospective properties may be lost due to an omission in

the claim of title. As a result, any claims against us may result in

liabilities we will not be able to afford, resulting in the failure of our

business.

Because

we are subject to various governmental regulations and environmental risks, we

may incur substantial costs to remain in compliance.

Our

activities in Peru are subject to Peruvian and local laws and regulations

regarding environmental matters, the abstraction of water, and the discharge of

mining wastes and materials. Any significant mining operations will

have some environmental impact, including land and habitat impact, arising from

the use of land for mining and related activities, and certain impact on water

resources near the project sites, resulting from water use, rock disposal and

drainage run-off. No assurances can be given that such environmental

issues will not cause our operations in the future to fail.

The

Peruvian and/or local government in the jurisdictions where we currently hold

property interests could require us to remedy any negative environmental

impact. The costs of such remediation could cause us to

fail. Future environmental laws and regulations could impose

increased capital or operating costs on us and could restrict the development or

operation of any mines.

We have,

and will in the future, engage consultants to assist us with respect to our

operations in Peru. We are beginning to address the various

regulatory and governmental agencies, and the rules and regulations of such

agencies, in connection with the options for the properties in

Peru. No assurances can be given that we will be successful in our

efforts. Further, in order for us to operate and grow our business in

Peru, we need to continually conform to the laws, rules and regulations of such

country and local jurisdiction where we operate. It is possible that

the legal and regulatory environment pertaining to the exploration and

development of mining properties will change. Uncertainty and new

regulations and rules could dramatically increase our cost of doing business, or

prevent us from conducting our business; both situations could cause us to

fail.

Mineral

exploration and development is subject to extraordinary operating

risks. We do not currently insure against these risks. In

the event of a cave-in or similar occurrence, our liabilities may exceed our

resources, which could cause our business to fail.

Mineral

exploration, development and production involves many risks which even a

combination of experience, knowledge and careful evaluation may not be able to

overcome. Our operations will be subject to all the hazards and risks

inherent in the exploration, development and production of resources, including

liability for pollution, cave-ins or similar hazards against which we cannot

insure or against which we may elect not to insure. Any such event

could result in work stoppages and damage to property, including damage to the

environment. We do not currently maintain any insurance coverage

against these operating hazards. The payment of any liabilities that

arise from any such occurrence could cause us to fail.

Mineral

prices are subject to dramatic and unpredictable fluctuations.

We expect

to derive revenues, if any, from the extraction and sale of precious and base

metals such as gold and silver. The price of those commodities has

fluctuated widely in recent years, and is affected by numerous factors beyond

our control including international, economic and political trends, expectations

of inflation, currency exchange fluctuations, interest rates, global or regional

consumptive patterns, speculative activities and increased production due to new

extraction developments and improved extraction and production

methods. The effect of these factors on the price of base and

precious metals, and, therefore, the economic viability of any of our

exploration projects, cannot accurately be predicted.

The

mining industry is highly competitive and there is no assurance that we will

continue to be successful in acquiring property interests. If we

cannot continue to acquire interests in properties to explore for mineral

resources, we may be required to reduce or cease operations.

The

mineral exploration, development, and production industry is largely

unintegrated. We compete with other exploration companies looking for

mineral resource properties. While we compete with other exploration

companies in the effort to locate and license mineral resource properties, we

will not compete with them for the removal or sales of mineral products from our

properties if we should eventually discover the presence of them in quantities

sufficient to make production economically feasible. Readily

available markets exist worldwide for the sale of gold and other mineral

products. Therefore, we will likely be able to sell any gold or

mineral products that we identify and produce.

We

compete with many companies possessing greater financial resources and technical

facilities. This competition could adversely affect our ability to

acquire suitable prospects for exploration in the future as well as our ability

to recruit and retain qualified personnel. Accordingly, there can be

no assurance that we will acquire any interest in additional mineral resource

properties that might yield reserves or result in commercial mining

operations.

Risks

Associated With Our Common Stock

Trading on the over-the-counter

bulletin board may be volatile and sporadic, which could depress the market

price of our common stock and make it difficult for our stockholders to resell

their shares.

Our

common stock is quoted on the over-the-counter bulletin board service of the

Financial Industry Regulatory Authority (the “OTCBB”). Trading in

stock quoted on the OTCBB is often thin and characterized by wide fluctuations

in trading prices, due to many factors that may have little to do with our

operations or business prospects. This volatility could depress the

market price of our common stock for reasons unrelated to operating

performance. Moreover, the OTCBB is not a stock exchange, and trading

of securities on the OTCBB is often more sporadic than the trading of securities

listed on a quotation system like Nasdaq or a stock exchange like

Amex. These factors may result in investors having difficulty

reselling any shares of our common stock.

Because

our common stock is quoted and traded on the OTCBB, short selling could increase

the volatility of our stock price.

Short

selling occurs when a person sells shares of stock which the person does not yet

own and promises to buy stock in the future to cover the sale. The

general objective of the person selling the shares short is to make a profit by

buying the shares later, at a lower price, to cover the

sale. Significant amounts of short selling, or the perception that a

significant amount of short sales could occur, could depress the market price of

our common stock. In contrast, purchases to cover a short position may have the

effect of preventing or retarding a decline in the market price of our common

stock, and together with the imposition of the penalty bid, may stabilize,

maintain or otherwise affect the market price of our common stock. As

a result, the price of our common stock may be higher than the price that

otherwise might exist in the open market. If these activities are

commenced, they may be discontinued at any time. These transactions

may be effected on the OTCBB or any other available markets or

exchanges. Such short selling if it were to occur could impact the

value of our stock in an extreme and volatile manner to the detriment of our

shareholders.

Because

the SEC imposes additional sales practice requirements on brokers who deal in

our shares that are penny stocks, some brokers may be unwilling to trade them.

This means that you may have difficulty in reselling your shares and may cause

the price of the shares to decline.

Our stock

is a penny stock. The Securities and Exchange Commission has adopted

Rule 15g-9 which generally defines “penny stock” to be any equity security that

has a market price (as defined) less than $5.00 per share or an exercise price

of less than $5.00 per share, subject to certain exceptions. Our

securities are covered by the penny stock rules, which impose additional sales

practice requirements on broker-dealers who sell to persons other than

established customers and “accredited investors”. The term

“accredited investor” refers generally to institutions with assets in excess of

$5,000,000 or individuals with a net worth in excess of $1,000,000 or annual

income exceeding $200,000 or $300,000 jointly with their spouse. The

penny stock rules require a broker-dealer, prior to a transaction in a penny

stock not otherwise exempt from the rules, to deliver a standardized risk

disclosure document in a form prepared by the SEC which provides information

about penny stocks and the nature and level of risks in the penny stock

market. The broker-dealer also must provide the customer with current

bid and offer quotations for the penny stock, the compensation of the

broker-dealer and its salesperson in the transaction and monthly account

statements showing the market value of each penny stock held in the customer’s

account. The bid and offer quotations and the broker-dealer and

salesperson compensation information must be given to the customer orally or in

writing prior to effecting the transaction and must be given to the customer in

writing before or with the customer’s confirmation. In addition, the

penny stock rules require that prior to a transaction in a penny stock not

otherwise exempt from these rules, the broker-dealer must make a special written

determination that the penny stock is a suitable investment for the purchaser

and receive the purchaser’s written agreement to the

transaction. These disclosure requirements may have the effect of

reducing the level of trading activity in the secondary market for the stock

that is subject to these penny stock rules. Consequently, these penny

stock rules may affect the ability of broker-dealers to trade our

securities. We believe that the penny stock rules discourage investor

interest in, and limit the marketability of, our common stock.

In

addition to the “penny stock” rules promulgated by the Securities and Exchange

Commission, Financial Industry Regulatory Authority (“FINRA”) has adopted rules

that require that in recommending an investment to a customer, a broker-dealer

must have reasonable grounds for believing that the investment is suitable for

that customer. Prior to recommending speculative, low-priced

securities to their non-institutional customers, broker-dealers must make

reasonable efforts to obtain information about the customer’s financial status,

tax status, investment objectives and other information. Under

interpretations of these rules, FINRA believes that there is a high probability

that speculative low-priced securities will not be suitable for at least some

customers. The FINRA requirements make it more difficult for

broker-dealers to recommend that their customers buy our common stock, which may

limit your ability to buy and sell our stock.

Indemnification

of officers and directors.

Our

Articles of Incorporation and Bylaws contain broad indemnification and liability

limiting provisions regarding our officers, directors and employees, including

the limitation of liability for certain violations of fiduciary

duties. Our stockholders therefore will have only limited recourse

against the individuals.

ITEM 1B. Unresolved Staff

Comments.

None.

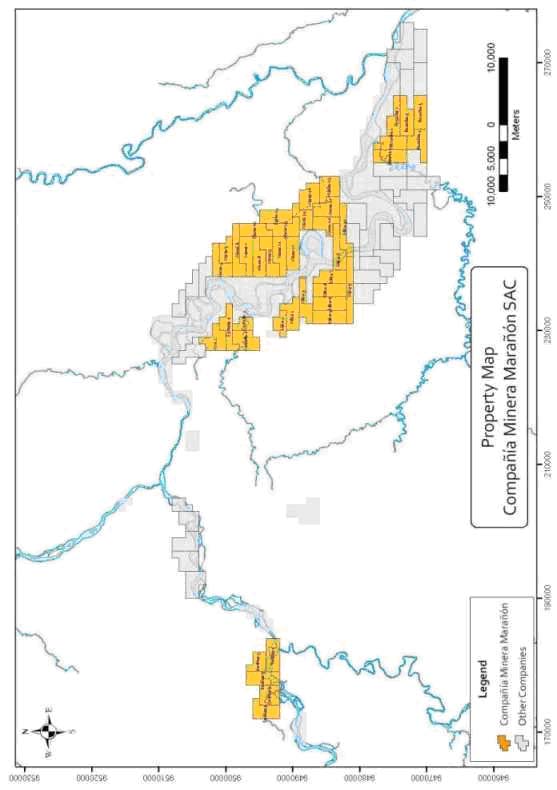

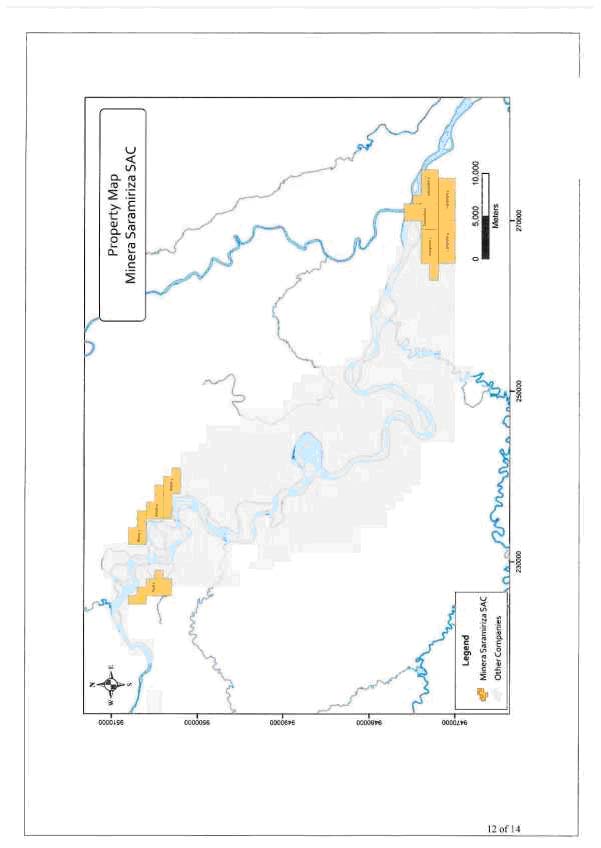

ITEM 2. Properties.

Description

of our Mineral Property Interests

The

Peru Property

Our

property interests located in Peru are in the exploration

stage. These properties are without known reserves and the proposed

plan of exploration detailed below is exploratory in nature. These

properties are described below.

We

entered into a Mineral Right Option Agreement with Temasek Investments Inc.

(“Temasek”), a company incorporated under the laws of Panama, on

September 29, 2008 (the “Effective Date”), as amended and supplemented by

Amendment No. 1, dated May 12, 2009 (“Amendment No. 1”) and Amendment No. 2,

dated October 29, 2009 (“Amendment No. 2”) (collectively, the “Option

Agreement”), in order to acquire four separate options from Temasek, each

providing for the acquisition of a twenty-five percent interest in certain

mineral rights (the “Mineral Rights”) in certain properties in Peru, potentially

resulting in the Company's acquisition of one hundred percent of the Mineral

Rights upon exercise of all four options. The Mineral Rights are

currently owned by Compañía Minera Marañón S.A.C. (“Minera

Marañón”). Bacon Hill Invest Inc. (“Bacon Hill”), a corporation

incorporated under the laws of Panama, owns 999 shares of the 1,000 shares of

Minera Marañón that are issued and outstanding. Temasek owns the

single remaining share of Minera Marañón. The acquisition of each

twenty-five percent interest in the Mineral Rights will occur through the

transfer by Temasek to us of twenty-five percent of the outstanding shares of

Bacon Hill upon exercise of each option.

A

description of the Mineral Rights is set forth below:

|

Name

|

Area

(hectares)

|

Dept.

|

Province

|

Province

|

Observation

|

|

Aixa

2

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Alana

10

|

900

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

11

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

12

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

13

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

14

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

15

|

800

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

16

|

800

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

17

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

18

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

19

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

4

|

900

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

5

|

700

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

6

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

7

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

8

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Alana

9

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Fully

overlap Zona de Amortiguamiento ANP

|

|

Bianka

5

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Castalia

1

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Castalia

2

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Castalia

3

|

500

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

| Name | Area

(hectares)

|

Dept.

|

Province

|

Province

|

Observation

|

|

Delfina

1

|

900

|

Amazonas

|

Condorcanqui

|

Nieva

|

Partially

overlap Zona de Amortiguamiento ANP

|

|

Delfina

2

|

900

|

Amazonas

|

Condorcanqui

|

Nieva

|

Partially

overlap Zona de Amortiguamiento ANP

|

|

Delfina

3

|

1000

|

Amazonas

|

Condorcanqui

|

Nieva

|

Partially

overlap Zona de Amortiguamiento ANP

|

|

Delfina

4

|

700

|

Amazonas

|

Condorcanqui

|

Nieva

|

Partially

overlap Zona de Amortiguamiento ANP

|

|

Delfina

5

|

1000

|

Amazonas

|

Condorcanqui

|

Nieva

|

Partially

overlap Zona de Amortiguamiento ANP

|

|

Mika

1

|

600

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Mika

10

|

900

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Partially

overlap Zona de Amortiguamiento ANP

|

|

Mika

2

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Mika

3

|

900

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Mika

4

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Mika

5

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Mika

6

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Mika

7

|

900

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Mika

8

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

Partially

overlap Zona de Amortiguamiento ANP

|

|

Mika

9

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Rosalba

1

|

900

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Rosalba

2

|

900

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Rosalba

3

|

1000

|

Loreto

|

Datem

del Marañon

|

Manseriche

|

|

|

Rosalba

4