UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark one)

| |

|

|

| þ |

|

ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

| |

|

|

| o |

|

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file number 001-31812

BIOSANTE PHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

| |

|

|

| Delaware

|

|

58-2301143 |

| (State or other jurisdiction of incorporation or organization)

|

|

(I.R.S. Employer Identification No.) |

| |

|

|

| 111 Barclay Boulevard |

|

|

| Lincolnshire, Illinois

|

|

60069 |

| (Address of principal executive offices)

|

|

(Zip Code) |

(847) 478-0500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| |

|

|

| Title of each class

|

|

Name of each exchange on which registered |

| Common Stock, par value $0.0001 per share

|

|

The NASDAQ Stock Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of

the Securities Act. YES o NO þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or

Section 15(d) of the Act. YES o NO þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by

Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for

such shorter period that the registrant was required to file such reports), and (2) has been

subject to such filing requirements for the past 90 days. YES þ NO o

Indicate by check mark whether the registrant has submitted electronically and posted on its

corporate Web site, if any, every Interactive Data File required to be submitted and posted

pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period

that the registrant was required to submit and post such files). YES o NO o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K

(§229.405 of this chapter) is not contained herein, and will not be contained, to the best of

registrant’s knowledge, in definitive proxy or information statements incorporated by reference in

Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated

filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

(Check one):

| |

|

|

|

|

|

|

| Large accelerated filer o

|

|

Accelerated filer o

|

|

Non-accelerated filer o

(Do not check if a smaller reporting company)

|

|

Smaller reporting company þ |

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Act).

YES o NO þ

The aggregate market value of the registrant’s common stock, excluding shares beneficially owned by

affiliates, computed by reference to the closing sale price at which the common stock was last sold

as of June 30, 2009 (the last business day of the registrant’s second fiscal quarter) as reported

by The NASDAQ Global Market on that date was approximately $48.8 million.

As of

March 15, 2010, 63,667,194 shares of common stock of the registrant were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this annual report on Form 10-K incorporates by reference information (to the extent

specific sections are referred to herein) from the registrant’s Proxy Statement for its 2010 Annual

Meeting of Stockholders to be held in June 2010.

This annual report on Form 10-K contains or incorporates by reference forward-looking statements.

For this purpose, any statements contained in this Form 10-K that are not statements of historical

fact may be deemed to be forward-looking statements. You can identify forward-looking statements

by those that are not historical in nature, particularly those that use terminology such as

“believe,” “may,” “could,” “would,” “might,” “possible,” “potential,” “project,” “will,” “should,”

“expect,” “intend,” “plan,” “predict,” “anticipate,” “estimate,” “approximate,” “contemplate” or

“continue”, the negative of these words, other words and terms of similar meaning or the use of

future dates. In evaluating these forward-looking statements, you should consider various factors,

including those listed below under the headings “Part I. Item I. Business — Forward-Looking

Statement” and “Part I. Item 1A. Risk Factors.” These factors may cause our actual results to

differ materially from any forward-looking statement.

As used in this report, references to “BioSante,” the “company,” “we,” “our” or “us,” unless the

context otherwise requires, refer to BioSante Pharmaceuticals, Inc.

We own or have the rights to use various trademarks, trade names or service marks, including

BioSante®, LibiGel®, Elestrin™, Bio-T-Gel™, The Pill-Plus™, BioLook™,

BioVant™, BioOral™, BioAir™ and GVAX™. This report also contains trademarks, trade names and

service marks that are owned by other persons or entities.

ii

PART I

Item 1. BUSINESS

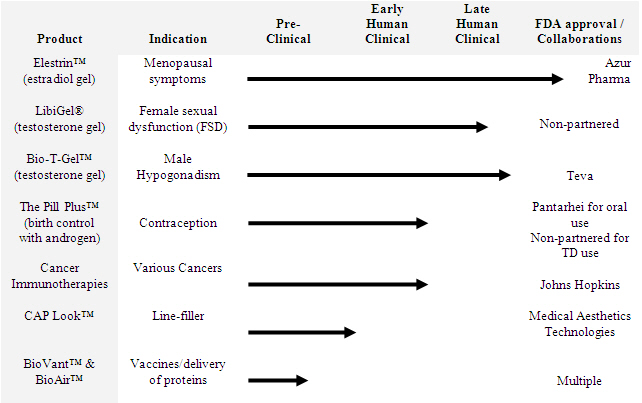

Company Overview

We are a specialty pharmaceutical company focused on developing products for female sexual health,

menopause, contraception and male hypogonadism. In addition, we are evaluating and seeking

opportunities for our GVAX cancer immunotherapies, 2A/Furin and other technologies we acquired in

our merger with Cell Genesys, Inc. in October 2009. We also are developing our calcium phosphate

technology (CaP) for aesthetic medicine (BioLook), as a vaccine adjuvant, including for an H1N1

(swine flu) vaccine, and drug delivery.

Our products for female sexual health, menopause, contraception and male hypogonadism include:

| • |

|

LibiGel — once daily transdermal testosterone gel in Phase III clinical development under

a Special Protocol Assessment (SPA) for the treatment of female sexual dysfunction (FSD). |

| • |

|

Elestrin — once daily transdermal estradiol (estrogen) gel approved by the U.S. Food and

Drug Administration (FDA) indicated for the treatment of moderate-to-severe vasomotor symptoms

(hot flashes) associated with menopause and marketed in the U.S. |

| • |

|

The Pill-Plus (triple component contraceptive) — once daily use of various combinations of

estrogens, progestogens and androgens in development for the treatment of FSD in women using

oral or transdermal contraceptives. |

| • |

|

Bio-T-Gel — once daily transdermal testosterone gel in development for the treatment of

hypogonadism, or testosterone deficiency, in men. |

We believe LibiGel remains the lead pharmaceutical product in the U.S. in active development for

the treatment of hypoactive sexual desire disorder (HSDD) in menopausal women, and that it has the

potential to be the first product approved by the FDA for this common and unmet medical need. We

believe based on agreements with the FDA, including an SPA, that two Phase III safety and efficacy

trials and one year of LibiGel exposure in a Phase III cardiovascular and breast cancer safety

study with a four-year follow-up post-NDA filing and potentially post-FDA approval are the

essential requirements for submission and, if successful, approval by the FDA of a new drug

application (NDA) for LibiGel for the treatment of FSD, specifically, HSDD in menopausal women. We

have three SPAs in place concerning LibiGel. The first SPA agreement covers the pivotal Phase III

safety and efficacy trials of LibiGel in the treatment of FSD for “surgically”

menopausal women. The second SPA covers our LibiGel program in the treatment of FSD, specifically

HSDD, in “naturally” menopausal women. The third SPA agreement covers the LibiGel stability, or

shelf life, studies for the intended commercialization of LibiGel product.

1

Currently, three LibiGel Phase III studies are underway and enrolling women: two LibiGel Phase III

safety and efficacy clinical trials and one Phase III cardiovascular and breast cancer safety

study. Both Phase III safety and efficacy trials are double-blind, placebo-controlled trials that

will enroll up to approximately 500 surgically menopausal women each for a six-month clinical

trial. The Phase III safety study is a randomized, double-blind, placebo-controlled, multi-center,

cardiovascular events driven study of between 2,400 and 3,100 women exposed to LibiGel or placebo

for 12 months after which time we intend to submit an NDA to the FDA. In February 2010, we

announced that based upon the second

review of study conduct and unblinded data from the LibiGel Phase III cardiovascular and breast

cancer safety study, the independent data monitoring committee (DMC) unanimously recommended

continuing the study as described in the FDA-agreed study protocol, with no modifications. The DMC

reviewed all unblinded adverse events in the safety study including “serious adverse events” and

all “adverse cardiovascular and breast cancer events” in almost 1,200 women-years of exposure. As

of such date, there had been no deaths, only six adjudicated cardiovascular events and four breast

cancers reported. In view of the DMC recommendation, we will continue the LibiGel Phase III

development program as planned. We continue to target submission to the FDA of an NDA by mid-2011.

Following NDA submission and potential FDA approval, we will continue to follow the subjects in

the safety study for an additional four years.

Elestrin is our first FDA approved product. Azur Pharma International II Limited is marketing

Elestrin in the U.S. using its women’s health sales force that targets estrogen prescribing

physicians in the U.S. comprised mostly of gynecologists. In December 2009, we entered into an

amendment to our original licensing agreement with Azur which permanently reduced the royalty

percentage due to us related to Azur’s sales of Elestrin. Upon signing the amended agreement, Azur

made a $1.0 million nonrefundable payment in December 2009 in exchange for a permanent reduction in

future royalty rates, and received options to make a total of $2.16 million in additional

non-refundable payments (which were exercised during the first quarter of 2010) in exchange for the

elimination of substantially all remaining future royalties and milestone payments due us under the

terms of the original license. The $1.0 million nonrefundable payment was recorded as revenue during

the fourth quarter of 2009 as we had no remaining performance obligations with respect to this

amount. We maintain the right to receive up to $140 million in sales-based milestone payments from

Azur if Elestrin reaches certain predefined sales per calendar year.

As a result of our October 2009 merger with Cell Genesys, we acquired a portfolio of products,

including GVAX cancer immunotherapies. GVAX cancer immunotherapies are cancer vaccines designed to

stimulate the patient’s immune system to effectively fight cancer. Multiple Phase II trials of

these technologies which had been ongoing at the date of the acquisition are continuing at minimal

cost to us at the Johns Hopkins Sidney Kimmel Comprehensive Cancer Center in various cancer

programs, including pancreatic cancer, leukemia and breast cancer.

Our CaP technology is based on the use of extremely small, solid, uniform particles, which we call

“nanoparticles.” We are pursuing the development of three potential initial applications for our

CaP technology. First, CaP technology is being tested in the area of aesthetic medicine. Second,

our CaP technology is being tested for its “adjuvant” activity that enhances the ability of a

vaccine to stimulate an immune response. The same nanoparticles allow for delivery of the vaccine

via alternative routes of administration including non-injectable routes of administration. Third,

we are pursuing the creation of oral, buccal, intranasal, inhaled and longer acting delivery of

drugs that currently must be given by injection (e.g., insulin).

The following is a list of our CaP products in development:

| • |

|

BioLook — facial line filler in development using proprietary CaP technology in the area

of aesthetic medicine, e.g., a facial line filler. |

| • |

|

BioVant — proprietary CaP adjuvant and delivery technology in development for improved

vaccines against viral and bacterial infections and autoimmune diseases, among others.

BioVant also serves as a delivery system for non-injected delivery of vaccines. |

2

| • |

|

BioOral — a delivery system using CaP technology for oral/buccal/intranasal administration

of proteins and other therapies that currently must be injected. |

| • |

|

BioAir — a delivery system using CaP technology for inhalable versions of proteins and

other therapies that currently must be injected. |

BioSante’s Product Portfolio

One of our strategic goals is to continue to seek and implement strategic alternatives with respect

to our products and our company, including licenses, business collaborations and other business

combinations or transactions with other pharmaceutical and biotechnology companies. Therefore, as

a matter of course, we may engage in discussions with third parties regarding the licensure, sale

or acquisition of our products and technologies or a merger or sale of our company. As part of

this process, we merged with Cell Genesys in October 2009. As a result of this transaction,

although we will continue to focus primarily on our LibiGel clinical development program, we also

will seek future development opportunities for our GVAX cancer immunotherapies, including potential

combination with BioVant, our vaccine adjuvant, as well as possible external collaborations, and

also will seek to outlicense or sell other technologies acquired from Cell Genesys. In addition,

as a result of our merger with Cell Genesys, we acquired an investment equivalent to approximately

16 percent of the total equity of Ceregene, Inc., a privately held biotechnology company focused on

the treatment of major neurodegenerative disorders using the delivery of nervous system growth

factors.

3

Description of Our Female Sexual Health, Menopause, Contraception and Male Hypogonadism Products

Overview. Our products for female sexual health, menopause, contraception and male hypogonadism

include our gel formulations of estradiol, testosterone and a combination of estradiol and

testosterone: Elestrin, Bio-T-Gel and LibiGel, and our triple component contraceptive that uses

various combinations

of estrogens, progestogens and androgens in development for the treatment of FSD in women using

oral or transdermal contraceptives, The Pill-Plus.

Our gel products are designed to be quickly absorbed through the skin after application on the

upper arm for the women’s products, delivering the hormone to the bloodstream evenly and in a

non-invasive, painless manner. The gels are formulated to be applied once per day and to be

absorbed into the skin without a trace of residue and to dry in under one to two minutes. We

believe our gel products have a number of benefits over competitive products, including the

following:

| • |

|

our transdermal gels can be spread over areas of skin where they dry rapidly and decrease

the chance for skin irritation versus transdermal patches; |

| • |

|

our transdermal gels may have fewer side effects than many pills which have been known to

cause gallstones, blood clots and complications related to metabolism; |

| • |

|

our transdermal gels have been shown to be well absorbed, thus allowing clinical hormone

levels to reach the systemic circulation; |

| • |

|

transdermal gels may allow for better dose adjustment than either transdermal patches or

oral tablets or capsules; and |

| • |

|

transdermal gels may be more appealing to patients since they are less conspicuous than

transdermal patches, which may be aesthetically unattractive. |

LibiGel. We believe LibiGel, if approved by the FDA, could be a very successful product. LibiGel

is a once daily transdermal testosterone gel designed to treat FSD, specifically HSDD in menopausal

women. The majority of women with FSD are postmenopausal, experiencing FSD due to hormonal changes

due to aging or following surgical menopause. LibiGel successfully has completed a Phase II

clinical trial, and three Phase III safety and efficacy clinical studies are currently underway and

enrolling women.

We believe LibiGel remains the lead pharmaceutical product in the U.S. in active development for

the treatment of HSDD in menopausal women, and that it has the potential to be the first product

approved by the FDA for this common and unmet medical need. We believe based on agreements with

the FDA, including an SPA, that two Phase III safety and efficacy trials and one year of LibiGel

exposure in a Phase III cardiovascular and breast cancer safety study with a four-year follow-up

post-NDA filing and potentially post-FDA approval are the essential requirements for submission

and, if successful, approval by the FDA of an NDA for LibiGel for the treatment of FSD,

specifically HSDD in menopausal women. The SPA process and agreement affirms that the FDA agrees

that the LibiGel Phase III safety and efficacy clinical trial design, clinical endpoints, sample

size, planned conduct and statistical analyses are acceptable to support regulatory approval.

Further, it indicates that these agreed measures will serve as the basis for regulatory review and

any decision by the FDA to approve an NDA for LibiGel. These SPA trials use our validated

instruments to measure the clinical endpoints. We have three SPA agreements in place concerning

LibiGel. The first SPA agreement covers the pivotal Phase III safety and efficacy trials of

LibiGel in the treatment of FSD for “surgically” menopausal women. The second SPA covers LibiGel

for the treatment of FSD, specifically, HSDD in “naturally” menopausal women. The third SPA

agreement covers the LibiGel stability, or shelf life, studies for the intended commercialization

of LibiGel product.

4

Currently, three LibiGel Phase III studies are underway and enrolling women: two LibiGel Phase III

safety and efficacy clinical trials and one Phase III cardiovascular and breast cancer safety

study. Both Phase III safety and efficacy trials are double-blind, placebo-controlled trials that

will enroll up to

approximately 500 surgically menopausal women each for a six-month clinical trial. The Phase III

safety study is a randomized, double-blind, placebo-controlled, multi-center, cardiovascular events

driven study of between 2,400 and 3,100 women exposed to LibiGel or placebo for 12 months after

which time we intend to submit an NDA to the FDA. In February 2010, we announced that based upon

the second review of study conduct and unblinded data from the LibiGel Phase III cardiovascular and

breast cancer safety study, the independent data monitoring committee unanimously recommended

continuing the study as described in the FDA-agreed study protocol, with no modifications. The DMC

reviewed all unblinded adverse events in the safety study including “serious adverse events” and

all “adverse cardiovascular and breast cancer events” in almost 1,200 women-years of exposure. As

of such date, there had been no deaths, only six adjudicated cardiovascular events and only four

breast cancers reported. In view of DMC recommendation, we will continue the LibiGel Phase III

development program as planned. We continue to target submission to the FDA of an NDA by mid-2011.

Following NDA submission and potential FDA approval, we will continue to follow the subjects in

the safety study for an additional four years.

There is no pharmaceutical product currently approved in the United States for FSD, specifically

HSDD. While several therapies have been tested to treat FSD, thus far testosterone therapy appears

to be the only treatment that results in a consistent significant increase in the number of

satisfying sexual events in women, which represents one of the two key efficacy endpoints chosen by

the FDA for pivotal clinical trials of FSD therapies. We are not aware of another testosterone

therapy product for the treatment of FSD in active clinical development in the U.S. other than

LibiGel.

Although generally characterized as limited to men, testosterone also is present in women and its

deficiency has been found to cause low libido or sex drive. Studies have shown that testosterone

therapy in women can boost sexual desire, sexual activity and pleasure, increase bone density,

raise energy levels and improve mood. According to a study published in the Journal of the

American Medical Association, 43 percent of American women between the ages of 18-59, or about 40

million women, experience some degree of impaired sexual function. Among the more than 1,400 women

surveyed, 32 percent lacked interest in sex (low sexual desire) and 26 percent could not experience

orgasm. Furthermore, according to a study published in the New England Journal of Medicine, 43

percent of American women between the ages of 57-85 experience low sexual desire. Importantly,

according to IMS data, two million testosterone prescriptions were written off-label for women by

U.S. physicians in 2007. Female sexual dysfunction is defined as a lack of sexual desire, arousal

or pleasure. The majority of women with FSD are postmenopausal, experiencing symptoms due to

hormonal changes that occur with aging or following surgical menopause.

Treatment with LibiGel in our Phase II clinical trial significantly increased satisfying

sexual events in surgically menopausal women suffering from FSD. The Phase II trial results showed

LibiGel significantly increased the number of satisfying sexual events by 238 percent versus

baseline; this increase also was significant versus placebo. In this study, the effective dose of

LibiGel produced testosterone blood levels within the normal range for pre-menopausal women and had

a safety profile similar to that observed in the placebo group. In addition, no serious adverse

events and no discontinuations due to adverse events occurred in any subject receiving LibiGel.

The Phase II clinical trial was a double-blind, placebo-controlled trial, conducted in the United

States, in surgically menopausal women distressed by their low sexual desire and activity.

5

Elestrin. Elestrin is our first FDA approved product. Elestrin is a once daily transdermal gel

that delivers estrogen without the skin irritation associated with, and the physical presence of,

transdermal patches, and to avoid the effects of oral estrogen. Elestrin contains estradiol versus

conjugated equine estrogen contained in the most commonly prescribed oral estrogen.

In December 2006, we received FDA approval for the marketing of Elestrin in the United States.

Elestrin is indicated for the treatment of moderate-to-severe vasomotor symptoms (hot flashes)

associated with menopause. Elestrin is administered using a metered dose applicator that delivers

0.87 grams of gel per actuation, thereby allowing for precise titration from dose to dose. Two

doses of Elestrin, 0.87 grams per day and 1.7 grams per day, were approved by the FDA. The 0.87

gram dose of Elestrin, which delivers 12.5 mcg of estradiol per day, is one of the lowest daily

doses of estradiol approved by the FDA for the treatment of hot flashes and is 67 percent lower

than the lowest dose, FDA-approved estrogen patch for hot flashes on the market. The Elestrin FDA

approval was a non-conditional and full approval. In addition, we received three years of

marketing exclusivity for Elestrin.

In December 2008, we entered into a license agreement and an asset purchase agreement with Azur for

the marketing of Elestrin and the sale of certain assets related to Elestrin pursuant to which we

received approximately $3.3 million. Under the license agreement, Azur was to pay us royalties on

sales of Elestrin ranging from 10 percent to 20 percent depending primarily upon the annual sales

levels and additional sales-based milestone payments. In April 2009, we announced the initiation

of sales and marketing activity of Elestrin by Azur. In December 2009, we entered into an

amendment to our original licensing agreement with Azur which permanently reduced the royalty

percentage due to us related to Azur’s sales of Elestrin. Upon signing the amended agreement, Azur

made a $1.0 million nonrefundable payment in December 2009 in exchange for a permanent reduction in

future royalty rates, and received options to make a total of $2.16 million in additional

non-refundable payments (which were exercised during the first quarter of 2010) in exchange for the

elimination of substantially all remaining future royalties and milestone payments due us under the

terms of the original license. The $1.0 million nonrefundable payment was recorded as revenue during

the fourth quarter of 2009 as we had no remaining performance obligations with respect to this

amount. We maintain the right to receive up to $140 million in sales-based milestone payments from

Azur if Elestrin reaches certain predefined sales per calendar year.

In December 2008, we signed an exclusive agreement with PharmaSwiss SA for the marketing of

Elestrin in Israel. PharmaSwiss is responsible for regulatory and marketing activities in Israel.

In June 2009, PharmaSwiss submitted a new drug application to the Israeli authorities based on our

approved U.S. NDA and manufacturing information.

According to The North American Menopause Society, there are more than 40 million postmenopausal

women in the U.S., and this group is expected to grow 25 percent by 2010. Menopause begins when

the ovaries cease to produce estrogen, or when both ovaries are surgically removed prior to natural

menopause. The average age at which women experience natural menopause is 51 years. The average

age of surgical menopause is 41 years. The most common physical symptoms of natural or surgical

menopause and the resultant estrogen deficiency are hot flashes, vaginal atrophy and osteoporosis.

According to the North American Menopause Society, studies show that hot flashes occur in

approximately two-thirds of menopausal women. Hormone therapy in women decreases the chance that

women will experience the symptoms of menopause due to estrogen deficiency. According to industry

estimates, approximately six million women in the U.S. currently are receiving some form of

estrogen or combined estrogen hormone therapy. According to IMS Health, the current market in the

U.S. for single-entity estrogen products was approximately $1.5 billion in 2009, of which the

transdermal segment, mostly patches, is reported at about $316 million. As the “baby boomer”

generation ages, the number of women reaching menopause, a large percentage of whom may need

estrogen or combined estrogen therapy, is between 5,000 and 6,000 women per day in the U.S.

6

There are several treatment options for women experiencing menopausal symptoms, which vary

according to which symptoms a woman experiences and whether or not she has had a hysterectomy.

Estrogen is most commonly given orally in pill or tablet form. There are several potential side

effects,

however, with the use of oral estrogen, including insufficient absorption by the circulatory

system, upset stomach, gallstones, blood clots as well as an increase in C-reactive protein, a

possible marker for cardiovascular inflammation. Reports suggest that oral estrogen causes an

increase in strokes and blood clots. Although transdermal, or skin, patches have been shown to

avoid some of these problems or effects, transdermal patches have a physical presence, can fall

off, and can result in skin irritation. However, transdermal delivery of estrogen via patches or

gels may reduce the risks associated with oral estrogen, including having no effect on C-reactive

protein and potentially reduce the risk of breast cancer and cardiovascular disease.

Bio-T-Gel. Bio-T-Gel is our once daily transdermal testosterone gel in development for the

treatment of hypogonadism, or testosterone deficiency, in men. Unlike LibiGel and Elestrin,

Bio-T-Gel is owned by us with no royalty or milestone obligations to any other party.

In December 2002, we entered into a development and license agreement, which was subsequently

amended, with Teva Pharmaceuticals USA, Inc., a wholly-owned subsidiary of Teva Pharmaceutical

Industries Ltd., pursuant to which Teva USA agreed to develop and market Bio-T-Gel for the U.S.

market. The financial terms of the development and license agreement included a $1.5 million

upfront payment by Teva USA, certain milestones and royalties on sales of the product, if and when

approved and marketed, in exchange for rights to develop and market the product. Teva USA also is

responsible under the terms of the agreement for continued development, regulatory filings and all

manufacturing and marketing associated with the product.

Testosterone deficiency in men is known as hypogonadism. Low levels of testosterone may result in

lethargy, depression, decreased sex drive, impotence, low sperm count and increased irritability.

Men with severe and prolonged reduction of testosterone also may experience loss of body hair,

reduced muscle mass, osteoporosis and bone fractures due to osteoporosis. Approximately five

million men in the United States, primarily over age 40, have lower than normal levels of

testosterone. Testosterone therapy has been shown to restore levels of testosterone with minimal

side effects.

There are currently several products on the market for the treatment of low testosterone levels in

men. As opposed to estrogen therapy products, oral administration of testosterone is currently not

possible as the hormone is, for the most part, rendered inactive in the liver making it difficult

to achieve adequate levels of the compound in the bloodstream. Current methods of administration

include testosterone injections, patches and gels. Testosterone injections require large needles,

are often painful and not effective for maintaining adequate testosterone blood levels throughout

the day. Delivery of testosterone through transdermal patches was developed primarily to promote

the therapeutic effects of testosterone therapy without the often painful side effects associated

with testosterone injections. Transdermal patches, however, similar to estrogen patches, have a

physical presence, can fall off, and can result in skin irritation. Testosterone formulated gel

products for men are designed to deliver testosterone without the pain of injections and the

physical presence, skin irritation and discomfort associated with transdermal patches. We are

aware of two gel testosterone products for men currently on the market in the United States.

According to IMS Health, the U.S. market for transdermal testosterone therapies grew approximately

28 percent in 2009 to $968 million from $755 million in 2008.

7

The Pill-Plus. The Pill-Plus is based on three issued U.S. patents claiming triple component

therapy via any route of administration (the combination use of estrogen plus progestogen plus

androgen, e.g. testosterone) and three issued U.S. patents pertaining to triple component

contraception. The Pill-Plus adds a third component, an androgen, to the normal two component

(estrogen and progestogen) oral contraceptive to prevent androgen deficiency which often leads to a

decrease in sexual desire, sexual activity and mood changes. In a completed Phase II double-blind

randomized clinical trial, the addition of an oral androgen resulted in restoration of testosterone

levels to the normal and physiological range for

healthy women. Paradoxically, many women who use oral contraceptives have reduced sexual desire,

arousabilty and activity due to the estrogen and progestogen in normal oral contraceptives. The

Pill-Plus is designed to improve female sexual dysfunction in oral contraceptive users, among other

potential benefits.

We have an exclusive license from Wake Forest University Health Sciences (formerly known as Wake

Forest University) and Cedars-Sinai Medical Center for the three issued U.S. patents for triple

component contraception. The financial terms of the license include an upfront payment, regulatory

milestone payments, maintenance payments and royalty payments by us if a product incorporating the

licensed technology gets approved and subsequently is marketed.

In May 2007, we announced that we sublicensed U.S. rights to The Pill-Plus to Pantarhei Bioscience

B.V. (Pantarhei), a Netherlands-based pharmaceutical company. Pantarhei is responsible under the

agreement for all expenses to develop and market the product. We may receive certain development

and regulatory milestones for the first product developed under the license. In addition, we will

receive royalty payments on any sales of the product in the U.S., if and when approved and

marketed. If the product is sublicensed by Pantarhei to another company, we will receive a

percentage of any and all payments received by Pantarhei for the sublicense from a third party. We

have retained all rights under our licensed patents to the transdermal delivery of triple component

contraceptives.

Other Products. In September 2000, we sublicensed the marketing rights to our gel products in

Canada to Paladin Labs Inc. In exchange for the sublicense, Paladin agreed to make an initial

investment in our company, make future milestone payments and pay royalties on sales of the

products in Canada. The milestone payments are required to be in the form of a series of equity

investments by Paladin in our common stock at a 10 percent premium to the market price of our stock

at the time the equity investment is made. If and when we receive FDA approval for any of our gel

products in the United States, Paladin may be able to use this information to obtain the

appropriate regulatory approvals of such products in Canada.

In August 2001, we entered into a sublicense agreement with Solvay Pharmaceuticals, B.V. (which was

purchased by Abbott Laboratories in February 2010) covering the U.S. and Canadian rights to the

estrogen/progestogen combination therapy gel product licensed from Antares. Under the terms of the

agreement, Solvay sublicenses our estrogen/progestogen combination therapy gel product for an

initial payment of $2.5 million, future milestone payments (of which $950,000 has been received to

date) and sales-based royalties. Solvay has been responsible for all costs of development to date.

We believe that the product licensed to Solvay is not in active development by Solvay, and we do

not expect its active development to occur at any time in the near future.

8

Description of GVAX Cancer Immunotherapies and Other Technologies Acquired in the Cell Genesys

Merger

GVAX Cancer Immunotherapy Technology. GVAX cancer immunotherapies are cancer vaccines designed to

stimulate the patient’s immune system to effectively fight cancer. GVAX cancer immunotherapies are

comprised of tumor cells that are genetically modified to secrete an immune-stimulating cytokine

known as granulocyte-macrophage colony-stimulating factor, or GM-CSF, and are then irradiated for

safety. Since GVAX cancer immunotherapies consist of whole tumor cells, the cancer patient’s

immune system can be activated against multiple tumor cell components, or antigens, potentially

resulting in greater clinical benefit than if the immunotherapy consisted of only a single tumor

cell component. Additionally, the secretion of GM-CSF by the modified tumor cells can enhance

greatly the immune response by recruiting and activating dendritic cells at the injection site, a

critical step in the optimal response by the immune system to any immunotherapy product. The

antitumor immune response

which occurs throughout the body following administration of a GVAX immunotherapy potentially can

result in the destruction of tumor cells that persist or recur following surgery, radiation therapy

or chemotherapy treatment.

GVAX cancer immunotherapies can be administered conveniently in an outpatient setting as an

injection into the skin, a site where immune cells, including in particular dendritic cells, can be

optimally accessed and activated. GVAX cancer immunotherapies are being tested as

patient-specific, or autologous, products and as non patient-specific, or allogeneic, products.

Multiple Phase II trials of these technologies which had been ongoing at the date of the

acquisition are continuing at minimal cost to us at the Johns Hopkins Sidney Kimmel Comprehensive

Cancer Center in various cancer programs, including pancreatic cancer, leukemia and breast cancer.

2A/Furin Protein Expression Technology. The 2A/furin technology is a novel expression system for

producing high levels of multimeric proteins. The 2A/furin technology allows for continuous,

equimolar expression of at least two proteins at high concentrations from a single expression

vector making it particularly useful for recombinant antibody expression. The technology

expression technology has been used successfully to express antibodies from several species,

including murine, rat and human, as well as a variety of antibody isotypes. The 2A/furin

expression technology has several potential applications including preclinical lead and target

validation, gene therapy, production of stable, high producer antibody cell lines, and commercial

production of antibodies and other proteins. The 2A/furin technology can increase the efficiency of

antibody production by cutting the cost and reducing the time to manufacture antibodies. According

to the Global Monoclonal Antibodies Review, the antibody market in the U.S. is estimated to be more

than $30 billion per year.

Oncolytic VirusTechnology. Our oncolytic virus technology uses replication-competent adenoviruses

derived from Adenovirus type 5, a common “cold” virus that replicate in and selectively kill tumor

cells. The replication of the virus is controlled by replacing the promoter of a gene required for

replication with a promoter that is preferentially expressed only in tumor cells. Furthermore, the

virus may optionally include a gene encoding a cytokine, which enhances immune stimulation to the

tumor, thereby providing a dual mechanism of action for killing targeted cancer cells by direct

cell lysis as well as via cellular and humoral immune responses to the tumor.

Description of Our CaP Technology and Products in Development

We believe our CaP technology can serve as a facial line filler in the area of aesthetic medicine

and as an effective vehicle for delivering drugs and vaccines and enhancing the effects of

vaccines. Our CaP nanoparticles successfully have passed the first stage of toxicity studies for

administration orally, into muscles, under the skin, and into the lungs by inhalation. We

successfully have completed a Phase I human clinical safety trial of CaP. We have entered into

several subcontract or development agreements with various corporate partners and governmental

entities concerning our CaP technology.

Overview of CaP Technology. Research and development involving our CaP technology originated under

an agreement dated April 6, 1989 between the University of California and one of our predecessor

companies, relating to viral protein surface absorption studies. The discovery research was funded

at UCLA School of Medicine and was based, in essence, on the use of extremely small, solid, uniform

particles as components that could increase the stability of drugs and act as systems to deliver

drugs into the body. Research in these areas at UCLA or our laboratory has resulted in the

issuance of a number of patents, which we either license from the University of California or own.

9

These ultra fine particles are made from inert, biologically acceptable materials, such as

ceramics, pure crystalline carbon or biodegradable calcium phosphate-like particles. The size of

the particles is in the

nanometer range. A nanometer is one millionth of a millimeter and typically particles measure

approximately 300 nanometers (nm). Because the size of these particles is measured in nanometers,

we use the term “nanoparticles” to describe them.

We use the nanoparticles as the basis of a delivery system. The critical property of these

nanoparticles is that biologically active molecules, proteins, peptides or pharmacological agents,

for example, vaccine components like bacterial or viral antigens or proteins like insulin, attached

to them, retain their activity and can be protected from natural alterations to their molecular

structure by adverse environmental conditions. It has been shown in studies conducted by us and

confirmed by others that when these combinations are injected into animals, the attachment can

enhance the biological activity as compared to injection of the molecule alone.

We believe our CaP technology has a number of benefits, including the following:

| • |

|

it is biodegradable (capable of being decomposed by natural biological processes) and

non-toxic and therefore potentially safe to use and introduce into the human body; |

| • |

|

it is fast, easy and inexpensive to manufacture, which should keep costs down and

potentially lead to higher profit margins compared to other delivery systems; |

| • |

|

the nanometer (one-millionth of a millimeter) size range makes it ideal for delivering

drugs through aerosol sprays, inhalation or intranasally, instead of using often painful and

inconvenient injections; and |

| • |

|

it has excellent “loading” capacity — the amount of molecules that can bond with the

nanoparticles — thereby potentially decreasing the dose needed to be taken by patients while

enhancing the release capabilities. |

Potential Commercial Applications for CaP. We plan to develop commercial applications of our CaP

technology and any proprietary technology developed as a result of our ongoing research and

development efforts. Initially, we plan to pursue primarily the development of:

| • |

|

a facial line filler using CaP technology in the area of aesthetic medicine; |

| • |

|

injected and non-injected vaccines using CaP as a delivery system and vaccine adjuvant; and |

| • |

|

drug delivery systems, including a method of delivering proteins (e.g., insulin) orally or

buccally, or through intranasal and subcutaneous routes of administration. |

Our pre-clinical research team in our laboratory in Doylestown, Pennsylvania currently is pursuing

the development of our CaP technology in these areas as well as exploring other areas.

10

CaP Products in Development. The following is a list of our CaP products in development:

| • |

|

BioLook — a facial line filler in development using proprietary CaP technology in the area

of aesthetic medicine. |

| • |

|

BioVant — proprietary CaP adjuvant and delivery technology in development for improved

versions of current vaccines and new vaccines against viral and bacterial infections and

autoimmune diseases, among others. BioVant also serves as a delivery system for non-injected

delivery of vaccines. |

| • |

|

BioOral — a delivery system using CaP technology for oral/buccal/intranasal administration

of proteins and other therapies that currently must be injected. |

| • |

|

BioAir — a delivery system using CaP technology for inhalable versions of proteins and

other therapies that currently must be injected. |

Aesthetic Medicine. In November 2007, we signed a license agreement with Medical Aesthetics

Technology Corporation (MATC) covering the use of our CaP as a facial line filler in aesthetic

medicine (BioLook). Under the license agreement, MATC is responsible for continued development of

BioLook, including required clinical trials, regulatory filings and all manufacturing and marketing

associated with the product. In exchange for the license, we received an ownership position in

MATC of approximately five percent of the common stock of MATC. In addition to the ownership

position, we may receive certain milestone payments and royalties as well as share in certain

payments if MATC sublicenses the technology.

Pre-clinical work to date by MATC indicates that our BioLook nanotechnology performs well as a

facial line filler and may be at least as long lasting and safe as other injectable fillers.

Preliminary results indicate long lasting effects with no adverse events. BioLook should be

extremely user friendly with minimal risk of side effects and may improve both facial wrinkles and

fulfill larger facial volume needs. Human clinical testing of BioLook for this use is being

planned and is expected to be initiated by MATC in 2010.

Vaccine Adjuvant and Delivery System. We believe that our CaP nanoparticles may offer a means of

preparing new vaccines that are equal or better in their safety and immunogenicity, that is, in

their capacity to elicit an immune response, compared to alum-formulated (the vaccine adjuvant used

in the vast majority of adjuvanted vaccines in the United States) and non-adjuvanted vaccines but

may be injected in lower concentrations and less often which could result in certain benefits,

including cost savings and improved patient compliance. Further, we believe that CaP will allow

for vaccines to be delivered by alternate routes of administration such as intranasally rather than

by injection.

Our nanoparticles when combined with vaccine antigens have been shown in animal studies conducted

by us and others to possess an ability to elicit a higher immune response than non-adjuvanted

vaccines and an immune response of the same magnitude as alum-formulated vaccines. These

preclinical studies also have shown that our CaP nanoparticles also may sustain higher antibody

levels over a longer time period than both alum-formulated vaccines and non-adjuvanted vaccines.

Because our CaP nanoparticles are made of calcium phosphate-like material, which has a chemical

nature similar to normal bone material and therefore is natural to the human body, as opposed to

aluminum hydroxide, or alum, which is not natural to the human body, we believe that our

nanoparticles may be safer to use than alum especially for intranasal delivery. In our animal

studies, we observed no material adverse reactions when our CaP nanoparticles were administered at

effective levels.

11

We filed an investigational new drug, or IND, application with the FDA and have conducted a Phase I

human clinical trial of CaP as a vaccine adjuvant and delivery system, which we call BioVant. As

discussed in more detail under the heading “Government Regulation,” the purpose of a Phase I trial

is to evaluate the metabolism and safety of the experimental product in humans, the side effects

associated with increasing doses, and, if possible, to gain early evidence of possible

effectiveness. The Phase I trial of our CaP specifically looked at safety parameters, including

local irritation and blood chemistry changes. The Phase I trial was a double blind, placebo

controlled trial, in 18 subjects to determine the safety of CaP as a vaccine adjuvant. The trial

results showed that there was no apparent difference in side-effect profile between CaP and

placebo. Phase I and or Phase II clinical trials will need to be repeated for each CaP/vaccine and

CaP/protein drug developed.

Drug Delivery Systems. The third field of use in which we are exploring applying our CaP

technology involves creating novel and improved forms of delivery of drugs, especially proteins

(e.g., insulin). The attachment of drugs to CaP may enhance their effects in the body or enable

the addition of further protective coatings to permit oral, delayed-release and mucosal (through

mucous membranes) applications. Currently, insulin is given by frequent, inconvenient and often

painful injections. However, several companies are in the process of developing and testing

products that will deliver insulin orally or through inhalation. We have shown pre-clinical

efficacy in the oral delivery of insulin in normal and diabetic mouse models.

We were awarded a $150,000 Small Business Innovation Research (SBIR) grant from the National

Institutes of Health (NIH) to support our development of formulations for the pulmonary delivery of

interferon alpha (IFN-a) using our CaP technology. The grant was used to fund product development

for IFN-a formulated with CaP particles for administration via inhalation. The desired outcome is

safe and effective treatment of hepatitis B and C. An inhaled product may allow for convenient

self treatment which would be an improvement over the current injectable IFN-a. We are in the

process of applying for additional government grants to help fund our CaP drug delivery

development.

License and Development Activities. In addition to continuing our own research and development in

the potential commercial applications of our CaP technology, we have sought and continue to seek

opportunities to enter into business collaborations or joint ventures with vaccine companies and

others interested in development and marketing arrangements with respect to our CaP technology. We

believe these collaborations may enable us to accelerate the development of potential improved

vaccines and the delivery of injectable drugs by other routes of administration, such as orally,

buccally, intranasally or through needle-free administration. Our out-licensing activities with

respect to our CaP vaccine adjuvant and delivery system for use in other companies’ vaccines, have

to date included meeting with target sub-licensees and, in some cases, agreeing that the target

sub-licensee will test our CaP adjuvant or delivery system in their animal models. Thereafter, the

target sub-licensee may send to us its vaccine antigen or DNA that we will then formulate with our

nanoparticles and return for use in the target sub-licensee’s animal models. Once this is

completed, if the results are positive, we would seek to negotiate an out-license agreement with

the target sub-licensee.

It is important to point out that vaccine development is an expensive and long-term process. We

have used our strategy of utilizing primarily outside resources to fund CaP’s development in order

to leverage the expertise of other companies and the United States government and to minimize our

spending on this expensive and long-term development work. Our strategic plan is to focus on our

nearer-term products and to seek collaborations and funding for our CaP technology.

Sales and Marketing

We currently have no sales and marketing personnel to sell any of our products on a commercial

basis. Under our license agreements, our licensees have agreed to market the products covered by

the agreements in certain countries. For example, under our license agreement with Azur, Azur has

agreed to use commercially reasonable efforts to manufacture, market, sell and distribute Elestrin

for commercial sale and distribution throughout the United States.

12

If and when we are ready to launch commercially a product not covered by our license agreements, we

will either contract with or hire qualified sales and marketing personnel or seek a joint marketing

partner or licensee to assist us with this function.

Research and Product Development

We spend a significant amount of our financial resources on product development activities, with

the largest portion being spent on clinical trials of our products, including in particular

LibiGel. We spent approximately $13.7 million in 2009, $15.8 million in 2008 and $4.8 million in

2007 on research and development activities. We spent an average of approximately $1.1 million per

month on our research and development activities during 2009. The decrease in 2009 research and

development expenses compared to 2008 was primarily the result of our decision in April 2009 to

delay screening new subjects for our LibiGel Phase III safety study to conserve cash. We

reinitiated screening and enrollment in our safety study in August 2009. We expect our monthly

research and development expenses to increase significantly in 2010 compared to 2009. The amount

of our actual research and development expenditures, however, may fluctuate from quarter-to-quarter

and year-to-year depending upon: (1) the amount of resources, including cash and cash equivalents,

available; (2) our development schedule, including the timing of our clinical trials; (3) results

of studies, clinical trials and regulatory decisions; (4) whether we or our licensees are funding

the development of our products; and (5) competitive developments.

Manufacturing

We currently do not have any facilities suitable for manufacturing on a commercial scale basis any

of our products nor do we have any experience in volume manufacturing. We currently use

third-party current Good Manufacturing Practices, or cGMP, manufacturers to manufacture our

products in accordance with FDA and other appropriate regulations. LibiGel for clinical studies

and Elestrin for commercial supplies are currently manufactured by an approved U.S.-based

manufacturer under FDA-approved, cGMP conditions.

Patents, Licenses and Proprietary Rights

Our success depends and will continue to depend in part upon our ability to maintain our exclusive

licenses, to obtain and maintain patent protection for our products and processes, to preserve our

proprietary information, trademarks and trade secrets and to operate without infringing the

proprietary rights of third parties. Our policy is to attempt to protect our technology by, among

other things, filing patent applications or obtaining license rights for technology that we

consider important to the development of our business.

Gel Products. We licensed the technology underlying LibGel, Elestrin and certain of our other gel

products, other than Bio-T-Gel, from Antares Pharma, Inc. Under the agreement, Antares granted us

an exclusive license to certain patents and patent applications covering these gel products,

including rights to sublicense, in order to develop and market the products in certain territories.

We are the exclusive licensee in certain territories for issued U.S. patents for these products

and additional patent applications have been filed for this licensed technology in the U.S. and

several foreign jurisdictions. Under the agreement, we are required to pay Antares certain

development and regulatory milestone payments and royalties based on net sales of any products we

or our sub-licensees sell incorporating the in-licensed technology. The patents covering the

formulations used in these gel products are expected to expire in 2022. Bio-T-Gel was developed

and is fully-owned by us and not covered under the Antares license.

13

The Pill Plus. We licensed the technology underlying our triple component contraceptives, or The

Pill Plus, from Wake Forest University Health Sciences and Cedars-Sinai Medical Center. The

financial terms of this license include regulatory milestone payments, maintenance payments and

royalty payments by us if a product incorporating the licensed technology gets approved and

subsequently is marketed. The patents covering the technology underlying The Pill Plus are

expected to expire in 2016.

GVAX Cancer Immunotherapy Technology. We own development and commercialization rights to our GVAX

cancer immunotherapy technology as a result of our merger with Cell Genesys in October 2009. The

original core patent applications covering our GVAX cancer immunotherapy technology were licensed

exclusively to Cell Genesys from Johns Hopkins University and The Whitehead Institute for

Biomedical Research in 1992. Rights to additional patents and patent applications were licensed

from Johns Hopkins University in 2001. In addition, we own several patents and patent applications

that build upon our in-licensed technology, and provide for significant additional patent term.

Our GVAX patent estate broadly covers our GVAX cancer immunotherapy products and pipeline. The

GVAX patent estate includes 17 patent families, comprising over 60 issued US and foreign patents,

directed to various aspects of the GVAX cancer immunotherapy technology. The patents are expected

to expire between 2012 and 2026.

Under the various agreements, we are required to pay Johns Hopkins University and The Whitehead

Institute for Biomedical Research certain development and regulatory milestone payments and

royalties based on net sales of any products we or our sub-licensees sell incorporating the

in-licensed technology.

2A/Furin Protein Expression Technology. We own development and commercialization rights to our

2A/furin protein expression technology as a result of our merger with Cell Genesys in October 2009.

Our 2A/furin patent estate includes five patent families, including four issued US patents and

additional patent applications, directed to various aspects of the 2A/furin technology, including

compositions and methods for producing recombinant antibodies. The patents are expected to expire

between 2023 and 2026.

Oncolytic Virus Technology. We also own development and commercialization rights to our oncolytic

virus technology as a result of our merger with Cell Genesys in October 2009. The oncolytic virus

patent estate includes eight patent families, comprising over 24 issued US and foreign patents,

directed to various aspects of the oncolytic virus technology, including CG0070 which has completed

a Phase 1 trial for non-muscle, invasive transitional cell bladder cancer. The patents are

expected to expire between 2018 and 2023.

CaP Technology. In June 1997, we entered into a licensing agreement with the Regents of the

University of California, which subsequently has been amended, pursuant to which the University

granted us an exclusive license to certain United States patents owned by the University, including

rights to sublicense such patents, in fields of use pertaining to vaccine adjuvants and drug

delivery systems. The last of the expiration dates for these patents is 2014. Importantly, we own

several of our own additional patents and patent applications covering the CaP technology expiring

beginning in 2021. The University of California also has filed patent applications for this

licensed technology in several foreign jurisdictions, including Canada, Europe and Japan. The

license agreement requires us to pay royalties to the University based on a percentage of the net

sales of any products we sell or a licensee sells incorporating the licensed technology until

expiration of the licensed patents.

14

As described earlier in this report, we have entered into agreements with respect to our CaP

technology, including a license agreement covering the use of our CaP as a facial line filler

(BioLook) in aesthetic medicine.

Other License Agreements. As described earlier in this report, we have entered into several other

license agreements pursuant to which we have sublicensed to third parties certain rights with

respect to our products, none of which we view as material to our business. The financial terms of

these agreements generally include an upfront license fee and subsequent milestone and royalty

payments to us if a product incorporating the licensed technology gets approved and subsequently is

marketed and a portion of any payments received from subsequent successful out-licensing efforts.

Trademarks and Trademark Applications/Registrations. We own trademark registrations in the U.S.

and/or in certain foreign jurisdictions for the marks BIOSANTE®, LIBIGEL®,

BIO-E-GEL®, BIOAIR™ and GVAX™. In addition, we have filed trademark applications for

several other marks including ELESTRIN™ (pursuant to our license of Elestrin to Azur in the U.S.,

we transferred the Elestrin trademark in the U.S. to Azur), BIO-T-GEL™, BIOVANT™ and covering goods

that include or are closely related to products, vaccines and vaccine adjuvants and drug delivery

platforms. In addition, we own common law rights to several trademarks, including

BIOSANTE®, LIBIGEL®, ELESTRIN™, BIO-E-GEL®, BIO-T-GEL™, THE

PILL-PLUS™, LIBIGEL-E/T™, BIO-E/P-GEL™, BIOLOOK™, CAP-ORAL™, BIOVANT™, BIOAIR™ and GVAX™. For

those trademarks for which registration has been sought, registrations have issued for some of

those trademarks in certain jurisdictions and others currently are in the application/prosecution

phase.

Confidentiality and Assignment of Inventions Agreements. We require our employees, consultants and

advisors having access to our confidential information to execute confidentiality agreements upon

commencement of their employment or consulting relationships with us. These agreements generally

provide that all confidential information we develop or make known to the individual during the

course of the individual’s employment or consulting relationship with us must be kept confidential

by the individual and not disclosed to any third parties. We also require all of our employees and

consultants who perform research and development for us to execute agreements that generally

provide that all inventions and works-for-hire conceived by these individuals during their

employment by us will be our property.

Competition

There is intense competition in the biopharmaceutical industry, the market for prevention and/or

treatment of the same infectious diseases we target and in the acquisition or licensing of new

products. Potential competitors in the United States are numerous and include major pharmaceutical

and specialized biotechnology companies, universities and other institutions. In general,

competition in the pharmaceutical industry can be divided into four categories: (1) corporations

with large research and developmental departments that develop and market products in many

therapeutic areas; (2) companies that have moderate research and development capabilities and focus

their product strategy on a small number of therapeutic areas; (3) small companies with limited

development capabilities and only a few product offerings; and (4) university and other research

institutions. Many of our competitors have longer operating histories, greater name recognition,

substantially greater financial resources and larger research and development staffs than we do, as

well as substantially greater experience than us in developing products, obtaining regulatory

approvals, and manufacturing and marketing pharmaceutical products. A significant amount of

research is carried out at academic and government institutions. These institutions are aware of

the commercial value of their findings and are becoming more aggressive in pursuing patent

protection and negotiating licensing arrangements to collect royalties for use of technology that

they have developed.

15

There are several firms currently marketing or developing products that may be competitive with

ours; they include Upsher-Smith Laboratories, Inc., Noven Pharmaceuticals, Inc. (a subsidiary of

Hisamitsu Pharmaceutical Co., Inc.), Pfizer Inc., Auxilium Pharmaceuticals, Inc., Ascend

Therapeutics, Inc., Watson Pharmaceuticals, Inc., KV Pharmaceutical Co., and Abbott Laboratories.

Competitor products include oral tablets, transdermal patches, a spray and gels. We expect our

FDA-approved product, Elestrin, and our other products, if and when approved for sale, to compete

primarily on the basis of product efficacy, safety, patient convenience, reliability and patent

position. In addition, the first product to reach the market in a therapeutic or preventative area

is often at a significant competitive advantage relative to later entrants in the market and may

result in certain marketing exclusivity as per federal legislation.

Acceptance by physicians and other health care providers, including managed care groups, also is

critical to the success of a product versus competitor products.

With regard to our CaP technology, the international vaccine industry is dominated by three

companies: GlaxoSmithKline plc, Sanofi-aventis (through its subsidiaries, including Institut

Merieux International S.A., Pasteur Merieux Serums et Vaccins, S.A., Connaught Laboratories Limited

and Connaught Laboratories, Inc.) and Merck & Co., Inc. The larger, better known pharmaceutical

companies generally have focused on a traditional synthetic drug approach, although some have

substantial expertise in biotechnology. During the last decade, however, significant research

activity in the biotechnology industry has been completed by smaller research and development

companies, like us, formed to pursue new technologies.

With regard to our GVAX cancer immunotherapy technology and other recently acquired technologies,

we face substantial competition in the development of products for cancer and other diseases. This

competition from other manufacturers is expected to continue in both U.S. and international

markets. Cancer immunotherapies and oncolytic virus therapies are evolving areas in the

biotechnology industry and are expected to undergo many changes in the coming years as a result of

technological advances. We currently are aware of a number of groups that are developing cancer

immunotherapies and oncolytic virus therapies including early-stage and established biotechnology

companies, pharmaceutical companies, academic institutions, government agencies and research

institutions. Examples in the cancer immunotherapy area include Dendreon Corporation, which has

completed a Phase III trial for its product in prostate cancer and has filed a Biologics License

Application (BLA) with the FDA, and Onyvax Ltd., which has commenced Phase II trials in prostate

cancer. Antigenics, Inc., Oncothyreon Inc., Warner Chilcott plc and Boerhinger Ingelheim USA

Corporation also are developing immunotherapy products for other types of cancers.

Governmental Regulation

Pharmaceutical companies are subject to extensive regulation by national, state and local agencies

in countries in which they do business. Pharmaceutical products intended for therapeutic use in

humans are governed by extensive FDA regulations in the United States and by comparable regulations

in foreign countries. Any products developed by us will require FDA approvals in the United States

and comparable approvals in foreign markets before they can be marketed. The process of seeking

and obtaining FDA approval for a previously unapproved new human pharmaceutical product generally

requires a number of years and involves the expenditure of substantial resources.

16

Following drug discovery, the steps required before a drug product may be marketed in the United

States include:

| • |

|

completion of preclinical laboratory and animal testing; |

| • |

|

the submission to the FDA of an investigational new drug application, commonly known as an

IND application, which must be evaluated and found acceptable by the FDA before human clinical

trials may commence; |

| • |

|

the completion of clinical and other studies to assess safety and parameters of use; |

| • |

|

the completion of multiple adequate and well-controlled human clinical trials to establish

the safety and effectiveness of the drug product for its intended use; |

| • |

|

the submission to the FDA of a new drug application, commonly known as an NDA, or an

abbreviated NDA, commonly known as an ANDA; |

| • |

|

satisfactory completion of an FDA pre-approval inspection of manufacturing facilities at

which the drug product is produced, and potentially other involved facilities as well, to

assess compliance with current good manufacturing practice, or cGMP, regulations and other

applicable regulations; and |

| • |

|

FDA approval of the NDA or ANDA prior to any commercial sale or shipment of the product. |

Pre-Clinical Studies and Clinical Trials. Typically, preclinical studies are conducted in the

laboratory and in animals to gain preliminary information on a product’s uses and physiological

effects and harmful effects, if any, and to identify any potential safety problems that would

preclude testing in humans. The results of these studies, together with the general investigative

plan, protocols for specific human studies and other information, are submitted to the FDA as part

of the IND application. The FDA regulations do not, by their terms, require FDA approval of an

IND. Rather, they allow a clinical investigation to commence if the FDA does not notify the sponsor

to the contrary within 30 days of receipt of the IND. As a practical matter, however, FDA approval

is often sought before a company commences clinical investigations. That approval may come within

30 days of IND receipt but may involve substantial delays if the FDA requests additional

information.

Our submission of an IND, or those of our collaboration partners, may not result in FDA

authorization to commence a clinical trial. A separate submission to an existing IND also must be

made for each successive clinical trial conducted during product development. Depending on its

significance, the FDA also must approve changes to an existing IND. Further, an independent

institutional review board, or IRB, for each medical center proposing to conduct the clinical trial

must review and approve the plan for any clinical trial before it commences at that center and it

must monitor the study until completed. Alternatively, a central IRB may be used instead of

individual IRBs. The FDA, the IRB or the sponsor may suspend a clinical trial at any time on

various grounds, including a finding that the subjects or patients are being exposed to an

unacceptable health risk. Clinical testing also must satisfy extensive Good Clinical Practice

requirements and regulations for informed consent.

The sponsor of a drug product typically conducts human clinical trials in three sequential phases,

but the phases may overlap or not all phases may be necessary. The initial phase of clinical

testing, which is known as Phase I, is conducted to evaluate the metabolism, uses and physiological

effects of the experimental product in humans, the side effects associated with increasing doses,

and, if possible, to gain early evidence of possible effectiveness. Phase I studies can also

evaluate various routes, dosages and schedules of product administration. These studies generally

involve a small number of healthy volunteer subjects, but may be conducted in people with the

disease the product is intended to treat. The total number of subjects is generally in the range

of 20 to 80. A demonstration of therapeutic benefit is not required in order to complete Phase I

trials successfully. If acceptable product safety is demonstrated, Phase II trials may be

initiated.

17

Phase II trials are designed to evaluate the effectiveness of the product in the treatment of a

given disease and involve people with the disease under study. These trials often are well

controlled, closely monitored studies involving a relatively small number of subjects, usually no

more than several hundred. The optimal routes, dosages and schedules of administration are

determined in these studies. If Phase II trials are completed successfully, Phase III trials are

often commenced, although Phase III trials are not always required.

Phase III trials are expanded, controlled trials that are performed after preliminary evidence of

the effectiveness of the experimental product has been obtained. These trials are intended to

gather the

additional information about safety and effectiveness that is needed to evaluate the overall

risk/benefit relationship of the experimental product and provide the substantial evidence of

effectiveness and the evidence of safety necessary for product approval. Phase III trials are

usually conducted with several hundred to several thousand subjects.

A clinical trial may combine the elements of more than one phase and typically two or more Phase

III studies are required. A company’s designation of a clinical trial as being of a particular

phase is not necessarily indicative that the trial will be sufficient to satisfy the FDA

requirements of that phase because this determination cannot be made until the protocol and data

have been submitted to and reviewed by the FDA. In addition, a clinical trial may contain elements

of more than one phase notwithstanding the designation of the trial as being of a particular phase.

The FDA closely monitors the progress of the phases of clinical testing and may, at its

discretion, re-evaluate, alter, suspend or terminate the testing based on the data accumulated and

its assessment of the risk/benefit ratio to patients. It is not possible to estimate with any

certainty the time required to complete Phase I, II and III studies with respect to a given

product.

New Drug Applications. Upon the successful completion of clinical testing, an NDA is submitted to

the FDA for approval. This application requires detailed data on the results of preclinical

testing, clinical testing and the composition of the product, specimen labeling to be used with the

drug, information on manufacturing methods and samples of the product. The FDA reviews all NDAs

submitted before it accepts them for filing and may request additional information rather than

accepting an NDA for filing. Once the submission is accepted for filing, the FDA begins an

in-depth review of the NDA. Under the policies agreed to by the FDA under the Prescription Drug

User Fee Act, or PDUFA, the FDA has 10 months in which to complete its initial review of a standard

NDA and respond to the applicant. The review process and the PDUFA goal date may be extended by

three months if the FDA requests or the NDA sponsor otherwise provides additional information or

clarification regarding information already provided in the submission within the last three months

of the PDUFA goal date. The FDA typically takes from 10 to 18 months to review an NDA after it has

been accepted for filing. Following its review of an NDA, the FDA invariably raises questions or

requests additional information. The NDA approval process can, accordingly, be very lengthy.