Attached files

Table of Contents

As filed with the Securities and Exchange Commission on March 24, 2010

Registration No. 333-

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM S-1

REGISTRATION STATEMENT

Under

THE SECURITIES ACT OF 1933

HIGHER ONE HOLDINGS, INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 7389 | 26-3025501 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

25 Science Park

New Haven, Connecticut 06511

(203) 776-7776

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive office)

Thomas D. Kavanaugh, Esq.

General Counsel

Higher One Holdings, Inc.

25 Science Park

New Haven, Connecticut 06511

(203) 776-7776

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| David Lopez, Esq. Cleary Gottlieb Steen & Hamilton LLP One Liberty Plaza New York, NY 10006 (212) 225-2000 |

Jay Clayton, Esq. Sullivan & Cromwell LLP 125 Broad Street New York, NY 10004-2498 (212) 558-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer ¨ |

Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ |

(Do not check if a smaller reporting company)

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered |

Proposed maximum aggregate offering price(1)(2) |

Amount of registration Fee | ||||||||

| Common Stock, par value $.001 per share |

$ | 100,000,000 | $ | 7,130 | ||||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act. |

| (2) | Includes (i) shares of common stock to be offered by the registrant and the selling stockholders in this offering and (ii) shares of common stock that may be purchased by the underwriters from the selling stockholders upon the exercise of the underwriters’ option to purchase additional shares. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion. Dated March 24, 2010.

Shares

Higher One Holdings, Inc.

Common Stock

This is an initial public offering of shares of common stock of Higher One Holdings, Inc.

Higher One Holdings, Inc. is offering of the shares to be sold in the offering. The selling stockholders identified in this prospectus are offering an additional shares. Higher One Holdings, Inc. will not receive any of the proceeds from the sale of the shares being sold by the selling stockholders.

Prior to this offering, there has been no public market for the common stock. It is currently estimated that the initial public offering price per share will be between $ and $ . Higher One intends to list the common stock on The NASDAQ Global Select Market under the symbol “ ”.

See “Risk Factors” on page 11 to read about factors you should consider before buying shares of the common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||

| Initial public offering price |

$ | $ | ||||

| Underwriting discount |

$ | $ | ||||

| Proceeds, before expenses, to |

$ | $ | ||||

| Proceeds, before expenses, to the selling stockholders |

$ | $ | ||||

To the extent that the underwriters sell more than shares of common stock, the underwriters have the option to purchase up to an additional shares from selling stockholders at the initial public offering price less the underwriting discount.

The underwriters expect to deliver the shares against payment in New York, New York on , 2010.

Goldman, Sachs & Co.

UBS Investment Bank

| Piper Jaffray | Raymond James | William Blair & Company |

JMP Securities

Prospectus dated , 2010.

Table of Contents

Prospectus

| Page | ||

| 1 | ||

| 11 | ||

| 32 | ||

| 33 | ||

| 34 | ||

| 35 | ||

| 35 | ||

| Unaudited Pro Forma Condensed Combined Financial Information |

37 | |

| 40 | ||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

43 | |

| 61 | ||

| 81 | ||

| 85 | ||

| 97 | ||

| 100 | ||

| 103 | ||

| 106 | ||

| Material U.S. Federal Tax Considerations to Non-U.S. Holders |

109 | |

| 112 | ||

| 116 | ||

| 116 | ||

| 116 | ||

| F-1 |

We are responsible for the information contained in this prospectus. We have not authorized anyone to give you any other information, and we take no responsibility for any other information that others may give you. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date of this prospectus.

i

Table of Contents

The following summary highlights information appearing elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully. In particular, you should read the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and the notes relating to those statements included elsewhere in this prospectus. Unless the context otherwise requires, in the prospectus, references to the “company,” “Higher One,” “we,” “us,” or “our” refer to Higher One Holdings, Inc. and its consolidated subsidiaries.

Our Company

We are a leading provider of technology and payment services to the higher education industry. We provide the most comprehensive suite of disbursement and payment solutions specifically designed for higher education institutions and their students. We also provide campus communities with convenient and student-oriented banking services, which include extensive user-friendly features.

The disbursement of financial aid and other refunds to students is a highly regulated, resource-consuming and recurrent obligation of higher education institutions. The student disbursement process remains mainly paper-based, costly and inefficient at most higher education institutions. These institutions are facing increasing pressure to improve administrative efficiency and the quality of service provided to students, to streamline regulatory compliance in respect of financial aid refunds, and to reduce expenses.

We believe our products provide significant benefits to both higher education institutions as well as their campus communities, including students. For our higher education institution customers, we offer our OneDisburse® Refund Management® disbursement service. Our disbursement service facilitates financial aid and other refunds to students, while simultaneously enhancing the ability of our higher education institutional clients to comply with the federal regulations applicable to financial aid transactions. By using our refund disbursement solutions, our clients save on the cost of handling disbursements, improve related business processes, increase the speed with which students receive their refunds and ensure compliance with applicable regulations.

For students and other campus community members, we offer our OneAccount service that includes a Federal Deposit Insurance Corporation, or FDIC, -insured deposit account provided by our bank partner, a OneCard, which is a debit MasterCard® ATM card, and other retail banking services. OneAccount is cost competitive and tailored to the campus communities that we serve, providing students with convenient and faster access to disbursement funds.

We also offer payment transaction services which are primarily software-as-a service solutions that facilitate electronic payment transactions allowing higher education institutions to receive easy and cost effective electronic payments from students, parents and others for essential education-related financial transactions. Features of our payment services include online bill presentment and online payment capabilities for tuition and other fees.

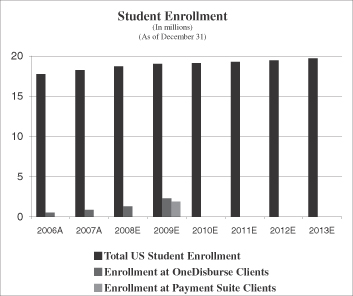

We have experienced significant growth since our inception in 2000, which we believe demonstrates the benefits and convenience our products provide to our customers, as well as the complementary nature of our higher education institution services and student services. As of December 31, 2009, 367 campuses serving approximately 2.3 million students had purchased the OneDisburse service and 255 campuses serving approximately 1.9 million students had contracted to

1

Table of Contents

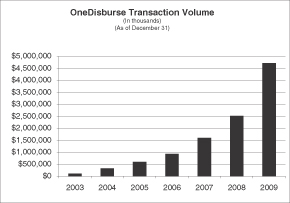

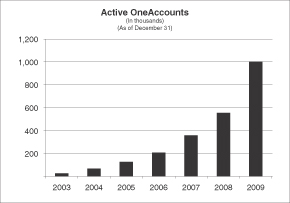

use one or more of our payment products and services. From 2003 through 2009, our disbursement services and our student banking services have experienced consistent annual growth. Since our initial product launch in 2002 and as of December 31, 2009, we have completed disbursement transactions with a total cash value of approximately $10.8 billion. In addition, as of December 31, 2009, we had approximately 1 million OneAccounts, representing growth in the number of OneAccounts of 81% from December 31, 2008.

In 2009, our total revenue, adjusted EBITDA, adjusted net income and net income were approximately $75.5 million, $30.5 million, $18.1 million and $14.2 million, respectively, which represents three-year compounded annual growth rates over 2006 of approximately 68%, 192%, 74% and 62%, respectively. See “Summary—Summary Consolidated Financial Data” for definitions of adjusted EBITDA and adjusted net income and reconciliations to net income. In 2009, excluding revenue generated by our recent acquisition of CASHNet, we generated over 90% of our revenue from contracts signed in prior years.

Investment Highlights

We believe that an investment in our common stock benefits from the following key factors:

| Ÿ | Most Comprehensive Suite of Products and Services. We believe that none of our competitors can match our ability to provide solutions to higher education institutions’ financial services needs, including compliance monitoring, while simultaneously meeting the retail banking needs of students. We believe that our unique ability to provide a “one-stop shop” to higher education institutions and their students deepens our relationships with current higher education institutional clients and enhances our attractiveness to other potential clients. |

| Ÿ | Diversified Client Base. Our higher education institutional client base is very diverse, spanning colleges, universities and other higher education institutions in 46 states, with no single campus responsible for more than 4% of our revenue in 2009. We believe our profile among higher education institutional clients enhances our efforts to attract new clients and our experience and stability provides an avenue for references and referrals. These benefits are significant due to the generally long sales cycle and the desire of customers to find a stable and experienced provider. |

| Ÿ | Focus on Customer Service and Satisfaction. We believe our multi-pronged approach to customer service, supported by our approximately 200 after-sales customer service employees, allows us to provide superior customer service and makes us an industry-leader in customer satisfaction. Our after-sales service for higher education institutional clients is focused on person-to-person assistance with our technology and software solutions. Our after-sales service for our student banking customers is designed to provide cost-effective technology-based customer service through a variety of media, including SMS text messaging, Internet and telephone. We believe that our over 97% retention rate since 2003 demonstrates the level of our client and customer satisfaction. |

| Ÿ | Predictable Revenue Streams. We believe we have a recurring and predictable revenue stream and can forecast near-term future revenues with a meaningful degree of reliability due to our stable client base. The majority of our revenue each year is generated through existing relationships with higher education institutions and their campus communities. For example, in 2009, excluding revenue generated by our recent acquisition of CASHNet, we generated over 90% of our revenue from contracts signed in prior years. This, coupled with our over 97% retention rate since 2003, provides a relatively stable and predictable revenue stream. Additionally, we believe the vast majority of our approximately 1 million OneAccount users are |

2

Table of Contents

| students who exhibit common spending habits and demonstrate similar patterns of financial activity. Our focus on higher education enables us to understand this demographic and its spending habits and patterns, which allows us to better forecast near-term future revenues from OneAccounts. This visibility allows us to appropriately manage our expenses and investments. |

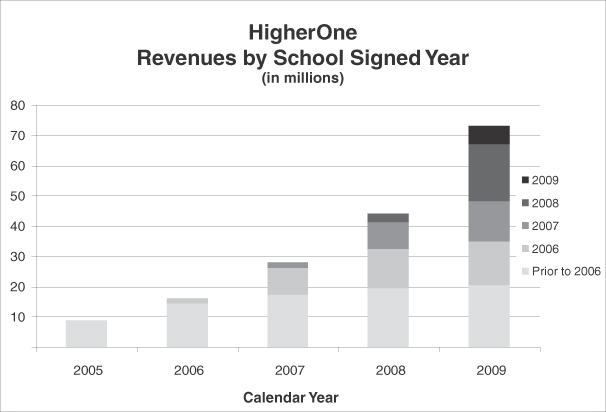

| Ÿ | Scalable Business Model. Our scalable technology and infrastructure permits us to significantly expand our business in a cost-effective manner. Our products and services are based on a combination of our proprietary software applications, third-party technology and infrastructure solutions and business processes that can be used for multiple clients without significant cost implications. Moreover, our historical experience is that the relative expense associated with servicing additional higher education clients and student customers has decreased as our business has expanded. Our total revenue for the years ended December 31, 2007, 2008 and 2009 were approximately $28.0 million, $44.0 million and $75.5 million, respectively, while the ratio of our expenses to our total revenue for those years was approximately 84.9%, 77.4% and 70.0%, respectively. |

| Ÿ | Experienced Management Team With A Proven Track Record. Our senior management team, which includes two of our three founders, has been with us for an average of eight years and is primarily responsible for our company’s rapid growth. Their leadership, combined with their deep and specialized understanding of our industry, have been and continue to be essential components of our growth and success in providing our higher education institutional clients with efficient, technology-driven solutions. |

Our Strategy

We believe that there is a significant opportunity to continue to achieve significant future growth. We intend to continue to increase revenue and profitability by strengthening our position as a leading provider of technology and payment services to the higher education industry. Key elements of our growth strategy include:

| Ÿ | Expand the Number of Contracted Higher Education Institutions. Although we have significantly expanded our higher education institutional client base, there remains a large majority of higher education institutions that are potential clients. We believe that we have only accessed 12% and 10% of the potential market for our disbursement products and payment products, respectively, and that a large proportion of the remaining potential clients still rely primarily on inefficient in-house disbursement and payment solutions and would benefit from our industry-leading suite of electronic products and services. We expect our dedicated sales force to leverage our deep experience in providing the higher education industry with cost-saving disbursement and payment services as we continue to add to our client base. |

| Ÿ | Increase OneAccount Usage. We are focused on increasing the number of OneAccount users at our higher education institutional clients, as well as encouraging OneAccount holders to increase their use of their accounts. We believe there is a significant opportunity to achieve revenue growth by increasing our penetration and usage rates from students at our existing OneDisburse clients. While we have achieved an increasing penetration rate, partially through our joint marketing efforts with our higher education institutional clients, we intend to expand and enhance our efforts in order to reach a greater proportion of the campus communities. |

| Ÿ | Cross-Sell Our Existing Products and Services. We intend to cross-sell our products and services though bundled packages and pricing. By building on our successful cross-selling experience, we intend to pursue the cross-selling opportunities presented by our recent acquisition of CASHNet in November 2009. At the time of the acquisition, only 4% of our |

3

Table of Contents

| combined clients were clients of both Higher One and CASHNet, creating an expansive cross-selling opportunity for us. |

| Ÿ | Enhance and Extend Our Products and Services. We intend to continue to anticipate and monitor customer and client needs and to respond by introducing new products and services and upgrading or modifying our existing offerings to take advantage of market opportunities. We also expect to meet the changing demands of our market by developing and offering new products and services, such as our Payroll and Financial Intelligence products launched in recent years. |

| Ÿ | Pursue Strategic Partnerships and Opportunistic Acquisitions. We intend to selectively consider acquisitions of, and investments in, companies or joint ventures that offer complementary products and services that further develop our business or broaden the scope of our products and services into new areas or strengthen the products and services available to existing clients. We believe each acquisition expands our sales opportunities by allowing us to leverage the existing client relationships of the acquired companies. |

Our Industry

The higher education industry in the United States consists of colleges, universities and other higher education providers. With nearly seven thousand higher education institutions in the United States accepting new students each year and providing finance and payments functions that serve their campus communities, the higher education payments industry is both large and stable. As an industry innovator focused on the needs of higher education institutional clients, we believe we are well positioned to capitalize on several key industry trends and to increase our market share in this large and underserved industry.

We believe the higher education industry is one of the most stable and least cyclical industries in the United States. Most higher education institutions are potential clients, as these institutions face increasing pressure to reduce expenses, improve the quality of services provided to students and streamline regulatory compliance in their disbursement and payment systems. In addition, we believe that institutions and their students are increasingly attracted to the convenience, security and enhanced services associated with electronic payment systems that meet and comply with applicable regulations.

Risk Factors

We face risks in operating our business, including risks that may prevent us from achieving our business objectives or that may materially and adversely affect our business, financial condition and operating results. You should carefully consider these risks, including the risks discussed in the section entitled “Risk Factors” beginning on page 11, before investing in our company. Risks relating to our business and industry include:

| Ÿ | we may face substantial and increasing competition in the industries in which we do business; |

| Ÿ | the fees that we generate are subject to competitive pressures and are subject to change; |

| Ÿ | fees for financial services are subject to increasingly intense legislative and regulatory scrutiny; |

| Ÿ | the convenience fees that we charge are subject to change; |

| Ÿ | we depend on the availability of financial aid and the current government financial aid regime that relies on the outsourcing of financial aid disbursements through higher education institutions; |

4

Table of Contents

| Ÿ | we depend on our relationship with higher education institutions and, in turn, student usage of our products and services for future growth of our business; |

| Ÿ | we outsource critical operations, including certain banking services, which exposes us to risks related to our third-party vendors; |

| Ÿ | we may face breaches of security measures, unauthorized access to or disclosure of data relating to our clients, fraudulent activity and infrastructure failures; |

| Ÿ | our disbursement services to higher education institutions is an emerging and uncertain business; and |

| Ÿ | we depend on a strong brand and a failure to maintain and develop our brand in a cost-effective manner may hurt our ability to expand our customer base. |

Our Corporate History and Other Information

Higher One, Inc. was founded in 2000 in New Haven, Connecticut by Mark Volchek, Miles Lasater and Sean Glass. In July 2008, Higher One, Inc. formed Higher One Holdings, Inc., which is now the holding company for all of our operations. In November 2009, we acquired Informed Decisions Corporation, which we renamed Higher One Payments, Inc. and which does business as CASHNet. CASHNet is a leader in providing cashiering and payment solutions for higher education.

Our principal executive offices are located at 25 Science Park, New Haven, Connecticut 06511. Our telephone number at that location is (203) 776-7776. We maintain a website at www.higherone.com on which we will post all reports we file with the Securities and Exchange Commission, or the SEC, under Section 13(a) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, after the closing of this offering. We also will post on this site our key corporate governance documents, including our board committee charters, our ethics policy and our principles of corporate governance. Information on our website is not a part of this prospectus and should not be relied upon in determining whether to make an investment decision.

5

Table of Contents

The Offering

| Common stock offered by us |

shares | |

| Common stock offered by the selling stockholders |

shares | |

| Common stock to be outstanding after this offering |

shares | |

| Use of proceeds |

We estimate that the net proceeds to us from this offering will be approximately $ million. | |

| We will not receive any proceeds from the sale of shares by the selling stockholders. | ||

| We intend to use $ million of the net proceeds we receive from this offering for the repayment of amounts outstanding under our senior secured revolving credit facility, or Credit Facility, and $ million to satisfy our post-closing obligations under the CASHNet stock purchase agreement dated November 19, 2009. We intend to use the remaining net proceeds to pursue our strategic objectives and for general corporate purposes. See “Use of Proceeds.” | ||

| Dividends |

We do not anticipate paying any cash dividends in the foreseeable future. | |

| Proposed NASDAQ Global Select Market symbol |

||

| Risk Factors |

See “Risk Factors” beginning on page 11 and other information included in this prospectus for a discussion of factors that you should carefully consider before investing in our common stock. | |

The number of shares of common stock that will be outstanding after this offering in the table above includes shares of restricted stock issued but not yet vested under our 2000 Stock Option Plan and excludes shares of common stock issuable upon exercise of outstanding stock options with a weighted average exercise price of $ per share, of which were vested as of , 2010.

Except as otherwise noted, all information in this prospectus:

| Ÿ | assumes that the underwriters do not exercise their option to purchase up to additional shares of common stock from the selling stockholders; |

| Ÿ | assumes our second amended and restated certificate of incorporation and amended and restated bylaws have become effective; and |

| Ÿ | gives effect to the conversion of all outstanding shares of our convertible preferred stock that were outstanding prior to this offering into an aggregate of 12,975,169 shares of our common stock. |

6

Table of Contents

Summary Consolidated Financial Data

You should read the data set forth below in conjunction with our consolidated financial statements and related notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and other financial information included elsewhere in this prospectus. We derived the summary financial data as of December 31, 2008 and 2009 and for each of the three years ended December 31, 2007, 2008 and 2009 from our audited consolidated financial statements and the related notes appearing elsewhere in this prospectus. We derived the summary financial data as of December 31, 2007 from our audited financial statements and the related notes not included in this prospectus. Our historical results are not necessarily indicative of our results for any future period.

The pro forma income statement data for the year ended December 31, 2009 set forth below gives pro forma effect to our acquisition of CASHNet in November 2009 as if the acquisition occurred on January 1, 2009. The pro forma financial data was derived from our “Unaudited Proforma Financial Information” included elsewhere in this prospectus. The pro forma summary financial data is not necessarily indicative of our results for any future period.

Consolidated Statement of Income Data

| Historical | Pro Forma | |||||||||||||||

| Year Ended December 31, | ||||||||||||||||

| 2007 | 2008 | 2009 | 2009 | |||||||||||||

| (unaudited) | ||||||||||||||||

| (in thousands, except share and per share amounts) | ||||||||||||||||

| Revenue |

$ | 27,978 | $ | 44,006 | $ | 75,517 | $ | 92,549 | ||||||||

| Cost of revenue |

11,140 | 16,302 | 24,440 | 36,494 | ||||||||||||

| Gross margin |

16,838 | 27,704 | 51,077 | 56,055 | ||||||||||||

| Operating expenses |

12,625 | 17,753 | 28,396 | 35,436 | ||||||||||||

| Income from operations |

4,213 | 9,951 | 22,681 | 20,619 | ||||||||||||

| Other income (expense) |

(569 | ) | (26 | ) | (537 | ) | (1,436 | ) | ||||||||

| Income before income taxes |

3,644 | 9,925 | 22,144 | 19,183 | ||||||||||||

| Income tax expense |

1,362 | 3,547 | 7,925 | 6,423 | ||||||||||||

| Net income |

2,282 | 6,378 | 14,219 | 12,760 | ||||||||||||

| Less: Net income allocable to participating securities |

1,808 | 5,102 | 11,477 | 10,299 | ||||||||||||

| Net income available to common shareholders |

$ | 474 | $ | 1,276 | $ | 2,742 | $ | 2,461 | ||||||||

| Net income per common share: |

||||||||||||||||

| Basic |

$ | 0.13 | $ | 0.37 | $ | 0.88 | $ | 0.79 | ||||||||

| Diluted |

$ | 0.12 | $ | 0.34 | $ | 0.80 | $ | 0.72 | ||||||||

| Weighted average common shares outstanding: |

||||||||||||||||

| Basic |

3,652,611 | 3,435,464 | 3,099,377 | 3,099,377 | ||||||||||||

| Diluted |

19,033,687 | 18,652,916 | 17,802,709 | 17,802,709 | ||||||||||||

7

Table of Contents

Consolidated Balance Sheet Data

| As of December 31, | |||||||||||||

| 2007 | 2008 | 2009 Actual |

2009 As Adjusted(1) | ||||||||||

| (in thousands) | |||||||||||||

| Cash and cash equivalents |

$ | 9,755 | $ | 1,488 | $ | 3,339 | |||||||

| Total assets |

18,423 | 13,662 | 59,904 | ||||||||||

| Total debt and capital lease obligations, including current maturities |

1,172 | 18,934 | 27,647 | ||||||||||

| Total liabilities |

22,675 | 25,402 | 52,800 | ||||||||||

| Total stockholders’ equity |

(4,252 | ) | (11,740 | ) | 7,104 | ||||||||

| (1) | Gives effect to (a) the sale by us of common stock in this offering, at an initial public offering price of $ per share, after deducting the underwriting discounts and commissions and estimated offering expenses payable by us, (b) the use of $ million of the net proceeds of this offering for the repayment of amounts outstanding under our Credit Facility and (c) the use of $ million of the net proceeds of this offering for certain post-closing costs related to our acquisition of CASHNet. See “Use of Proceeds.” |

Consolidated Other Data

| Year Ended December 31, | |||||||||

| 2007 | 2008 | 2009 | |||||||

| (in thousands) | |||||||||

| Adjusted EBITDA(1) |

$ | 5,473 | $ | 13,141 | $ | 30,516 | |||

| Adjusted net income(2) |

$ | 2,434 | $ | 7,725 | $ | 18,091 | |||

| Number of students enrolled at OneDisburse client higher education institutions at end of period |

1,011 | 1,605 | 2,331 | ||||||

| Number of students enrolled at payment transaction client higher education institutions at end of period |

3 | 30 | 1,949 | ||||||

| Number of OneAccounts at end of period |

359 | 554 | 1,004 | ||||||

| (1) | We define adjusted EBITDA as net income before interest, taxes, depreciation and amortization and warrant fair value adjustment, adjusted to eliminate stock-based customer acquisition expense related to our grant of common stock in connection with our acquisition of EduCard in 2008, stock-based compensation expense and a nonrecurring milestone bonus paid to non-executive employees in 2009 upon our reaching a particular long-term operational target. Adjusted EBITDA should not be considered as an alternative to net income, operating income or any other measure of financial performance calculated and presented in accordance with United States generally accepted accounting principles, or GAAP. Our adjusted EBITDA may not be comparable to similarly titled measures of other organizations because other organizations may not calculate adjusted EBITDA in the same manner as we do. We prepare and present adjusted EBITDA to eliminate the effect of items that we do not consider indicative of our core operating performance. You are encouraged to evaluate our adjustments and the reasons we consider them appropriate. |

8

Table of Contents

We believe adjusted EBITDA is useful to our board of directors, management and investors in evaluating our operating performance for the following reasons:

| Ÿ | adjusted EBITDA is widely used by investors to measure a company’s operating performance without regard to items, such as interest expense, income tax expense, depreciation and amortization, warrant fair value adjustment, stock-based expenses and certain nonrecurring items, that can vary substantially from company to company and from period to period depending upon their financing and accounting methods, the book value of their assets, their capital structures and the method by which their assets were acquired; |

| Ÿ | securities analysts use adjusted EBITDA as a supplemental measure to evaluate the overall operating performance of companies; |

| Ÿ | because non-cash equity grants made at a certain price and point in time do not necessarily reflect how our business is performing at any particular time, stock-based customer acquisition expense and stock-based compensation expense are not key measures of our core operating performance; and |

| Ÿ | because the milestone bonus was a nonrecurring expense that we recorded upon reaching a particular long-term operational target that we do not expect to incur again in the near-term, the milestone bonus does not necessarily reflect how our business is performing at any particular time and is therefore not a key measure of our core operating performance. |

The following table presents a reconciliation of adjusted EBITDA to net income, the most comparable GAAP measure, for each of the periods indicated:

| Year Ended December 31, | ||||||||||||

| 2007 | 2008 | 2009 | ||||||||||

| (in thousands) | ||||||||||||

| Net income |

$ | 2,282 | $ | 6,378 | $ | 14,219 | ||||||

| Interest income |

(291 | ) | (152 | ) | (4 | ) | ||||||

| Interest expense |

115 | 357 | 558 | |||||||||

| Other income |

— | (234 | ) | (17 | ) | |||||||

| Income tax expense |

1,362 | 3,547 | 7,925 | |||||||||

| Depreciation and amortization |

1,114 | 1,452 | 2,969 | |||||||||

| Warrant fair value adjustment |

745 | 55 | — | |||||||||

| EBITDA |

5,327 | 11,403 | 25,650 | |||||||||

| Stock-based customer acquisition expense |

— | 1,240 | 2,385 | |||||||||

| Stock-based compensation expense |

146 | 498 | 1,387 | |||||||||

| Milestone bonus |

— | — | 1,094 | |||||||||

| Adjusted EBITDA |

$ | 5,473 | $ | 13,141 | $ | 30,516 | ||||||

| (2) | We define adjusted net income as net income, adjusted to eliminate (a) stock-based compensation expense related to incentive stock option grants and (b) after giving effect to tax adjustments, stock-based compensation expense related to non-qualified stock option grants, stock-based customer acquisition expense related to our grant of common stock in connection with our acquisition of EduCard in 2008, a non-recurring milestone bonus paid to non-executive employees in 2009 upon our reaching a particular long-term operational target and amortization expenses related to intangible assets and financing costs. Adjusted net income should not be considered as an alternative to net income, operating income or any other measure of financial performance calculated and presented in accordance with GAAP. Our adjusted net income may not be comparable to similarly titled measures of other organizations because other organizations |

9

Table of Contents

| may not calculate adjusted net income in the same manner as we do. We prepare adjusted net income to eliminate the effect of items that we do not consider indicative of our core operating performance. You are encouraged to evaluate our adjustments and the reasons we consider them appropriate. |

We believe adjusted net income is useful to our board of directors, management and investors in evaluating our operating performance for the following reasons:

| Ÿ | because non-cash equity grants made at a certain price and point in time do not necessarily reflect how our business is performing at any particular time, stock-based customer acquisition expense and stock-based compensation expense are not key measures of our core operating performance; |

| Ÿ | because the milestone bonus was a nonrecurring expense that we recorded upon reaching a particular long-term operational target that we do not expect to incur again in the near-term, the milestone bonus does not necessarily reflect how our business is performing at any particular time and is therefore not a key measure of our core operating performance; and |

| Ÿ | amortization expenses can vary substantially from company to company and from period to period depending upon their financing and accounting methods, the fair value and average expected life of their acquired intangible assets, their capital structures and the method by which their assets were acquired. |

The following table presents a reconciliation of adjusted net income to net income, the most comparable GAAP measure, for each of the periods indicated:

| Year Ended December 31, | ||||||||||||

| 2007 | 2008 | 2009 | ||||||||||

| (in thousands) | ||||||||||||

| Net income |

$ | 2,282 | $ | 6,378 | $ | 14,219 | ||||||

| Stock-based customer acquisition expense |

— | 1,240 | 2,385 | |||||||||

| Stock-based compensation expense—ISO |

128 | 312 | 610 | |||||||||

| Stock-based compensation expense—NQO |

18 | 186 | 777 | |||||||||

| Milestone bonus expense |

— | — | 1,094 | |||||||||

| Amortization of intangibles |

21 | 153 | 710 | |||||||||

| Amortization of finance costs |

— | 31 | 113 | |||||||||

| Total pre-tax adjustments |

167 | 1,922 | 5,689 | |||||||||

| Tax rate |

37.4 | % | 35.7 | % | 35.8 | % | ||||||

| Tax adjustment |

15 | 575 | 1,817 | |||||||||

| Adjusted net income |

$ | 2,434 | $ | 7,725 | $ | 18,091 | ||||||

10

Table of Contents

An investment in our common stock involves a number of risks. You should carefully consider the following information about these risks, together with the other information contained in this prospectus, before investing in our common stock. If any of the following risks actually materializes, our business, financial condition and operating results could be materially and adversely affected. As a result, the trading price of our common stock could decline and you could lose all or part of your investment.

Risks Related to Our Business

Our operating results may suffer because of substantial and increasing competition in the industries in which we do business.

The market for our products and services is competitive, continually evolving and, in some cases, subject to rapid technological change. Our disbursement services compete against all forms of payment, including paper-based transactions (principally cash and checks), electronic transactions such as wire transfers and Automated Clearing House, or ACH, payments and other electronic forms of payment, including card-based payment systems. Many competitors, including Sallie Mae, TouchNet Information Systems, Inc. and Nelnet, Inc., provide payment software, products and services that compete with those we offer. In addition, our OneAccount and OneCard products and services, which we provide through our bank partner, also compete with banks active in the higher education market, including U.S. Bancorp and Wells Fargo & Company. Future competitors may begin to focus on higher education institutions in a manner similar to us.

Many of our competitors have substantially greater financial and other resources than we have, may in the future offer a wider range of products and services and may use advertising and marketing strategies that achieve broader brand recognition or acceptance. In addition, our competitors may develop new products, services or technologies that render our products, services or technologies obsolete or less marketable. If we cannot continue to compete effectively against our competitors, our business, financial condition and results of operations will be materially and adversely affected.

The fees that we generate through our relationships with higher education institutions and their campus communities are subject to competitive pressures and are subject to change, which may materially and adversely affect our revenue and profitability.

We generate revenue from, among other sources, the banking services fees charged to our OneAccount holders, interchange fees related to purchases made through our OneCard debit and ATM cards, which our bank partner charges and remits to us, convenience fees from processing tuition payments on behalf of students, fees charged to our higher education institution clients and service fees that we receive from our bank partner based on amounts deposited in OneAccounts and prevailing interest rates.

In an increasingly price-conscious and competitive market, it is possible that to maintain our competitive position with higher education institutions, we may have to decrease the fees we charge institutions for our services. Similarly, in order to maintain our competitive position with our OneAccount holders, we may need to work with our bank partner to reduce banking services fees charged to our OneAccount holders.

MasterCard could reduce the interchange rates, which it unilaterally sets and adjusts from time to time, and upon which our interchange revenue is dependent. In addition, our OneAccount holders may modify their spending habits and increase their use of ACH relative to their use of OneCards, as ACH

11

Table of Contents

payments are generally free, which could reduce the interchange fees remitted to us. Students may also become less willing to pay convenience fees when using our payment transaction services. If our fees are reduced as described above, our business, results of operations and prospects for future growth could be materially and adversely affected.

Fees for financial services are subject to increasingly intense legislative and regulatory scrutiny, which could have a material adverse effect on business, financial conditions, results of operations and prospects for future growth.

In 2009, approximately 88% of our revenue was generated from interchange fees, ATM fees, non-sufficient fund fees, other banking services fees and convenience fees. These fees, as well as the financial services industry in general, could undergo substantial change in the near future. Legislation passed by the U.S. House of Representatives, or House Bill, would further increase regulation and oversight of the financial services industry and impose restrictions on the ability of firms within the industry to conduct business consistent with historical practices. For example, under the House Bill, a Consumer Financial Protection Agency would be established to regulate any person engaged in a “financial activity” in connection with a consumer financial product or service, including those that process financial services products and services. The U.S. Senate is expected to consider its version of this legislation, or Senate Bill shortly. Although it is unclear at this time whether the Senate Bill will provide for a separate Consumer Financial Protection Agency, it is expected that the Senate Bill will include some consumer protection measures.

In addition, in 2009, the U.S. House of Representatives introduced a bill seeking to regulate interchange fees by allowing merchants to collectively seek to lower their interchange costs by exempting such action from the U.S. antitrust laws. Individual state legislatures are also reviewing interchange fees, and legislators in a number of states have proposed bills that purport to limit interchange fees or merchant discount rates or to prohibit their application to portions of a transaction.

The Federal Reserve Board recently amended Regulation E to limit the ability of financial institutions, effective July 1, 2010, to assess an overdraft fee for paying ATM and one-time debit card transactions that overdraw a consumer’s account, unless the consumer affirmatively consents, or opts in, to the institution’s payment of overdrafts for these services. In the absence of such a consent, a financial institution may not assess an overdraft fee on a consumer for an ATM or one-time debit card transaction.

Federal and state legislatures and regulatory agencies also frequently propose and adopt changes to their laws and regulations or change the manner in which existing laws and regulations are applied. We cannot predict the substance or impact of pending or future legislation or regulation, or the application thereof, but such measures could affect how we and our bank partner operate and could significantly reduce the interchange fees, ATM fees, non-sufficient fund fees, other banking services fees and convenience fees charged in respect of our services and that drive our financial results. These regulatory and legislative changes could also increase our costs, impede the efficiency of our internal business processes or limit our ability to pursue business opportunities in an efficient manner. The occurrence of any of these risks could materially and adversely affect our business, financial condition and results of operations.

The convenience fees that we charge in connection with payment transactions are subject to change.

Most credit and debit card associations and networks permit us to charge convenience fees to students, parents or other payers who make online payments to our higher education institutional clients through the SmartPay feature of our ePayment product using a credit or debit card. In 2009,

12

Table of Contents

these convenience fees accounted for substantially all of our payment transaction revenue, which is a trend we expect to continue going forward. While the majority of credit and debit card associations and networks routinely permit merchants and other third parties to charge these fees, it is not a ubiquitous practice in the payment industry. If these credit and debit card associations and networks change their policies in permitting merchants and other third-parties to charge these fees or otherwise restrict our ability to do so, our business, financial condition and results of operations could be materially and adversely affected.

In addition, certain states, including California, New York, Florida and Texas, have laws that generally prohibit merchants from charging fees to customers when they use credit cards to make payments. State authorities have generally interpreted and applied these laws in a manner which has allowed us to charge convenience fees for online payments made with our ePayment product in many of these states. If one or more states alter their interpretation or application of these laws in a manner that restricts our ability to charge convenience fees or a change in the interpretation or application of these laws diminishes ability to retain existing or attract new ePayment clients, our business, financial condition and results of operations could be materially and adversely affected.

Our business depends on the current government financial aid regime that relies on the outsourcing of financial aid disbursements through higher education institutions.

In general, the U.S. federal government distributes financial aid to students through higher education institutions as intermediaries. Following the receipt of financial aid funds and the payment of tuition and other expenses, higher education institutions have typically processed refund disbursements to students by preparing and distributing paper checks. Our OneDisburse service provides our higher education institutional clients an electronic system for improving the administrative efficiency of this refund disbursement process. If the government, through legislation or regulatory action, restructured the existing financial aid regime in such a way that reduced or eliminated the intermediary role played by higher education financial institutions or limited or regulated the role played by service providers such as us, our business, results of operations and prospects for future growth could be materially and adversely affected.

We depend on our relationship with higher education institutions and, in turn, student usage of our products and services for future growth of our business.

Our future growth depends, in part, on our ability to enter into agreements with higher education institutions. While we have experienced significant growth since 2002 in the number of our higher education institutional clients, our contracts with these clients can generally be terminated at will and, therefore, there can be no assurance that we will be able to maintain these clients. We may also be unable to maintain our agreements with these clients on terms and conditions acceptable to us. In addition, we may not be able to continue to establish new relationships with higher education institutional clients at our historical growth rate or at all. The termination of our current client contracts or our inability to continue to attract new clients could have a material adverse effect on our business, financial condition and results of operations.

Not only are establishing new client relationships and maintaining current ones critical to our business, but they are also essential components of our strategy for maximizing student usage of our products and services and attracting new student customers. A reduction in enrollment, a failure to attract and maintain student customers, as well as any future demographic trends that reduce the number of higher education students could materially and adversely affect our capability for both revenue and cash generation and, as a result, could have a material adverse effect on our business, financial condition and results of operations.

13

Table of Contents

A change in the availability of financial aid, as well as budget constraints, could materially and adversely affect our financial performance by reducing demand for our services.

The higher education industry depends heavily upon the ability of students to obtain financial aid. As part of our contracts with our higher education institutional clients that use OneDisburse, students’ financial aid and other refunds are sent to us for disbursement. The fees that we charge most of our OneDisburse clients are based on the number of financial aid disbursements that we make to students. In addition, our relationships with OneDisburse higher education institutional clients provide us with a market for OneAccounts, from which we derive a significant proportion of our revenues. Consequently, a change in the availability of financial aid that restricted client use of our OneDisburse product or otherwise limited our ability to attract new higher education institutional clients could materially and adversely affect our financial performance. Future legislative and executive branch efforts to reduce the U.S. federal budget deficit or worsening economic conditions may require the government to severely curtail its financial aid spending, which could materially and adversely affect our business, financial condition and results of operation.

Global economic and other conditions may adversely affect trends in consumer spending, which could materially and adversely affect our business, financial condition and results of operation.

A decrease in consumer confidence due to the weakening of the global economy may cause decreased spending among our student customers and may decrease the use of our OneAccount and OneCard products and services. Increases in college tuition alongside stagnation or reduction in available financial aid may also restrict spending among college students and the size of disbursements, reducing the use of our OneAccount and OneCard products and services and demand for our disbursement services, which could materially and adversely affect our business, financial condition and results of operation.

We rely on our bank partner for certain banking services, and a change in relationship with our bank partner or its failure to comply with certain banking regulations could materially and adversely affect our business.

As the provider of FDIC-insured depository services for all of our OneAccounts, as well as other banking functions, such as supplying cash for our ATM machines, The Bancorp Bank, our bank partner, provides third-party services that are critical to our student-oriented banking services. If any material adverse event were to affect The Bancorp Bank, including a significant decline in its financial condition, a decline in the quality of its service, loss of deposits, systems failure or its inability to pay us fees, our business, financial condition and results of operations could be materially and adversely affected. If we were required to change banking partners, we could not accurately predict the success of such change or that the terms of our agreement with a new banking partner would be as favorable to us, especially in light of the recent consolidation in the banking industry, which has rendered the market for FDIC-insured retail banking services less competitive.

In addition, while we are not directly subject to banking regulations, some of our products and services are regulated, and we therefore rely on the ability of The Bancorp Bank to comply with applicable banking and financial service requirements. Its failure to do so could cause an interruption in the banking services we provide or require us to seek alternative solutions or relationships, either of which could materially and adversely affect our business. See “Legal and Regulatory Risks—We are subject to substantial federal and state governmental regulation that could change and thus force us to make modifications to our business. Compliance with the various complex laws and regulations is costly and time consuming, and failure to comply could have a material adverse effect on our business. Additionally, increased regulatory requirements on our services may increase our costs, which could materially and adversely affect our business, financial condition and results of operations.”

14

Table of Contents

We outsource critical operations, which exposes us to risks related to our third-party vendors.

We have entered into contracts with third-party vendors to provide critical services, technology and software in our operations. These outsourcing partners include: Fiserv, which provides back-end account and transaction data processing for OneAccounts and OneCards; MasterCard, which provides the payment network for our OneCards, as well as for certain other transactions; Comerica Incorporated and Global Payments, which provide transaction processing and banking services for payment processing related to the SmartPay feature of our ePayment service; and Terremark and Neospire, which provide web and application hosting services in secure data centers. See “Business—Key Relationships with Third Parties.”

Accordingly, we depend, in part, on the services, technology and software of these and other third-party service providers. In the event that these service providers fail to maintain adequate levels of support, do not provide high quality service, discontinue their lines of business, terminate our contractual arrangements or cease or reduce operations, we may be required to pursue new third-party relationships, which could materially disrupt our operations and could divert management’s time and resources. We may also be unable to establish comparable new third-party relationships on as favorable terms or at all, which could materially and adversely affect our business, financial condition and results of operations.

Even if we are able to obtain replacement technology, software or services there may be a disruption or delay in our ability to operate our business or to provide our products and services, and the replacement technology, software or services might be more expensive than those we have currently. The process of transitioning services and data from one provider to another can be complicated, time consuming and may lead to significant disruptions in our business. If we are unable to complete a transition to a new provider on a timely basis, or at all, we could be forced to temporarily or permanently discontinue certain services, which could disrupt services to our customers and adversely affect our business, financial condition and results of operations. In addition, any failure by third-party service providers to maintain adequate internal controls could negatively affect our internal control over financial reporting, which could impact the preparation and quality of our financial statements.

In particular, we and our bank partner, which issues our OneCards, are subject to MasterCard association rules that could subject us to a variety of fines or penalties that may be levied by MasterCard for acts or omissions by us or businesses that work with us. The termination of the card association registration held by us or our bank partner or any changes in card association or other network rules or standards, including interpretation and implementation of existing rules or standards, that increase the cost of doing business or limit our ability to provide our products and services could materially and adversely affect our business, financial condition and results of operation.

Breaches of security measures, unauthorized access to or disclosure of data relating to our clients, fraudulent activity, and infrastructure failures could materially and adversely affect our reputation or harm our business.

Our higher education institution clients and student OneAccount holders disclose to us certain “personally identifiable” information, including student contact information, identification numbers and the amount of credit balances, which they expect we will maintain confidentially. It is possible that hackers, customers or employees acting unlawfully or contrary to our policies, or other individuals, could improperly access our or our vendors’ systems and obtain or disclose data about our customers. Further, because customer data may also be collected, stored, or processed by third party vendors, it is possible that these vendors could intentionally or negligently disclose data about our clients or customers.

15

Table of Contents

We rely to a large extent upon sophisticated information technology systems, databases, and infrastructure, and take reasonable steps to protect them. However, due to their size, complexity, content and integration with or reliance on third party systems they are potentially vulnerable to breakdown, malicious intrusion, natural disaster and random attack, all of which pose a risk that sensitive data may be exposed to unauthorized persons or to the public.

A breach of our information systems could lead to fraudulent activity, including with respect to our OneCards, such as identity theft, losses on the part of our banking customers, additional security costs, negative publicity and damage to our reputation and brand. In addition, our customers could be subject to scams that may result in the release of sufficient information concerning themselves or their accounts to allow others unauthorized access to their accounts or our systems (e.g., “phishing” and “smishing”). Claims for compensatory or other damages may be brought against us as a result of a breach of our systems or fraudulent activity. If we are unsuccessful in defending against any resulting claims against us, we may be forced to pay damages, which could materially and adversely affect our profitability.

In addition, a significant incident of fraud or an increase in fraud levels generally involving our products, such as our OneCards, could result in reputational damage to us, which could reduce the use of our products and services. Such incidents of fraud could also lead to regulatory intervention, which could increase our compliance costs. See “Legal and Regulatory Risks—We are subject to substantial federal and state governmental regulation that could change and thus force us to make modifications to our business. Compliance with the various complex laws and regulations is costly and time consuming, and failure to comply could have a material adverse effect on our business. Additionally, increased regulatory requirements on our services may increase our costs, which could materially and adversely affect our business, financial condition and results of operations.” Accordingly, account data breaches and related fraudulent activity could have a material adverse effect on our future growth prospects, business, financial condition and results of operations.

A disruption to our systems or infrastructure could damage our reputation, expose us to legal liability, cause us to lose customers and revenue, result in the unintentional disclosure of confidential information or require us to expend significant efforts and resources or incur significant expense to eliminate these problems and address related data and security concerns. The harm to our business could be even greater if such an event occurs during a period of disproportionately heavy demand for our products or services or traffic on our systems or networks.

Providing disbursement services to higher education institutions is an emerging and uncertain business; if the market for our products does not continue to develop, we will not be able to grow this portion of our business.

Our success will depend, in part, on our ability to generate revenues by providing financial transaction services to higher education institutions and their students. The market for these services has only recently developed and the viability and profitability of this market is unproven. Our business will be materially and adversely affected if we do not develop and market products and services that achieve and maintain market acceptance. Outsourcing disbursement services may not become as widespread in the higher education industry as we anticipate, and our products and services may not achieve continued commercial success. In addition, higher education institutional clients could discontinue using our services and return to in-house disbursement and payment solutions. If outsourcing disbursement services do not become widespread or if institutional clients return to their prior methods of disbursement, our growth prospects, business, financial condition and results of operations could be materially and adversely affected.

16

Table of Contents

Our business depends on a strong brand and a failure to maintain and develop our brand in a cost-effective manner may hurt our ability to expand our customer base.

Maintaining and developing the “Higher One” and “CASHNet” brand is critical to expanding and maintaining our base of higher education institution clients and student OneAccount holders. We believe the importance of brand recognition will increase as competition in our market further intensifies. Maintaining and developing our brand will depend largely on our ability to continue to provide high-quality products and services at cost effective and competitive prices, as well as after-sale customer service. While we intend to continue investing in our brand, we cannot predict the success of these investments. If we fail to maintain and enhance our brand, if we incur excessive expenses in this effort or if our reputation is otherwise tainted, including by association with the wider financial services industry, we may be unable to maintain loyalty among our existing customers or attract new customers, which could materially and adversely affect our business, financial condition and results of operations.

Our business will suffer if we fail to successfully integrate acquired businesses and technologies or to appropriately assess the risks in particular transactions.

We have in the past acquired, and may in the future acquire, businesses, technologies, services, product lines and other assets. For example, in November 2009 we acquired CASHNet, which provides payment services to higher education institutions, and have begun to integrate its operations with our business. The successful integration of CASHNet into our operations, along with any other businesses that we acquire in the future, on a cost-effective basis, may be critical to our future performance. If we do not successfully integrate a strategic acquisition, or if the benefits of the transaction do not meet the expectations of financial or industry analysts, the market price of our common stock may decline. The amount and timing of the expected benefits of any acquisition, including potential synergies between our current business and the acquired business, are subject to significant risks and uncertainties. These risks and uncertainties include, but are not limited to:

| Ÿ | the diversion of management’s time and resources from our core business; |

| Ÿ | our ability to retain or replace key personnel of the acquired business, including management and key sales force members; |

| Ÿ | our ability to maintain relationships with the customers of the acquired business; |

| Ÿ | our ability to integrate common disclosure controls and procedures, internal controls over financial reporting and accounting policies; |

| Ÿ | the assumption of disclosed and undisclosed liabilities, including tax liabilities; |

| Ÿ | the indemnification agreements with the sellers of the acquired business may be unenforceable or insufficient to cover tax or other liabilities; |

| Ÿ | our ability to educate and train a combined sales force and cross-sell the combined products and services to our combined client base; |

| Ÿ | our ability to integrate the combined products, services and technology; |

| Ÿ | flaws in the acquired business’ technology; |

| Ÿ | inaccuracies in the acquired business’ books and records and any weaknesses in its internal controls; |

| Ÿ | the existence of intellectual property infringement claims; |

| Ÿ | our ability to coordinate organizations that are geographically diverse and that have different business cultures; |

17

Table of Contents

| Ÿ | our ability to integrate common legal, compliance, operational, financial and informational processes and systems; and |

| Ÿ | our ability to comply with the regulatory requirements applicable to the acquired business. |

As a result of these risks, we may not be able to achieve the expected benefits of any acquisition. If we are unsuccessful in integrating CASHNet or completing an acquisition that we may pursue in the future, we would be required to reevaluate our growth strategy and we may have incurred substantial expenses and devoted significant management time and resources in seeking to complete and integrate the acquisition. Even if we are successful in completing and integrating an acquired business, the acquired businesses may not perform as we expect or enhance the value of our business as a whole.

Failure to manage future growth effectively could have a material adverse effect on our business, financial condition and results of operations.

The continued rapid expansion and development of our business may place a significant strain upon our management and administrative, operational and financial infrastructure. As of December 31, 2009, we had approximately 1 million OneAccounts, representing growth of 81.2% from December 31, 2008. In 2009, our total revenue, adjusted EBITDA, adjusted net income and net income were approximately $75.5 million, $30.5 million, $18.1 million and $14.2 million, respectively, which represents three-year compounded annual growth rates over 2006 of approximately 68%, 192%, 74% and 62%, respectively. See “Summary—Summary Consolidated Financial Data” for definitions of adjusted EBITDA and adjusted net income and reconciliations to net income. Our growth strategy contemplates further increasing the number of our higher education institutional clients and student banking customers at relatively similar growth rates, however, the rate at which we have been able to establish relationships with our customers in the past may not be indicative of the rate at which we will be able to establish additional customer relationships in the future.

Our success will depend in part upon the ability of our executive officers to manage growth effectively. Our ability to grow also depends upon our ability to successfully hire, train, supervise, and manage new employees, obtain financing for our capital needs, expand our systems effectively, allocate our human resources optimally, maintain clear lines of communication between our operational functions and our finance and accounting functions, and manage the pressures on our management and administrative, operational and financial infrastructure. There can be no assurance that we will be able to accurately anticipate and respond to the changing demands we will face as we continue to expand our operations or that we will be able to manage growth effectively or to achieve further growth at all. If our business does not continue to grow or if we fail to manage any future growth effectively our business, financial condition and results of operations could be materially and adversely affected.

The length and unpredictability of the sales cycle for signing potential higher education institutional clients could delay new sales of our products and services, which could materially and adversely affect our business, financial condition and results of operations.

The sales cycle between our initial contact with a potential higher education institutional client and the signing of a contract with that client can be lengthy. As a result of this lengthy sales cycle, our ability to forecast accurately the timing of revenues associated with new sales is limited. Our sales cycle varies widely due to significant uncertainties, over which we have little or no control, including:

| Ÿ | the individual decision-making processes of each higher education institutional client, which typically include extensive and lengthy evaluations and require us to spend substantial time, effort and money educating each client about the value of our products and services; |

18

Table of Contents

| Ÿ | the budgetary constraints and priorities and budget cycle of each higher education institutional client; and |

| Ÿ | the reluctance of higher education staff to change or modify existing processes and procedures. |

In addition, there is no guarantee that a potential client will sign a contract with us even after we spend substantial time, effort and money on the potential client. A delay in our ability or a failure to enter into new contracts with potential higher education institutional clients could materially and adversely affect our business, financial condition and results of operations.

Our business and future success may suffer if we are unable to cross-sell our products and services.

A significant component of our growth strategy is dependent on our ability to cross-sell products and services to new and existing customers. In particular, we expect our ability to successfully cross-sell our disbursement services to our payment services clients and our payment services to our disbursement services clients, to be a material part of this strategy. We may not be successful in cross-selling our products and services because our customers may find our additional products and services unnecessary or unattractive. Our failure to sell additional products and services to new and existing customers could have a material adverse effect on our prospects, business, financial condition and results of operations.

Our ability to generate revenue could suffer if we do not continue to update and improve our existing products and services and develop new ones.

The industry for electronic financial transactions, including disbursement services, is generally subject to rapid and significant technological changes, including continuing developments of technologies in the areas of smart cards, radio frequency and proximity payment devices (such as contactless cards), electronic commerce and mobile commerce, among others. While we cannot predict how these technological changes will affect our business, we believe that disbursement services to the higher education industry will be subject to a similar degree of technological change and that new services and technologies for the industry will emerge in the medium-term. As a result, these new services and technologies may be superior to, or render obsolete, the technologies we currently use in our products and services. In addition, the products and services we develop may not be able to compete with the alternatives available to our customers. Our future success will depend, in part, on our ability to adapt to technological changes and evolving industry standards.

We make substantial investments in improving our products and services, but we have no assurance that our investments will be successful. Our growth prospects, business, financial condition and results of operations will be materially and adversely affected if we do not develop products and services that achieve broad market acceptance with our current and potential customers.

We depend on our founders and other key members of executive management and the loss of their services could have a material adverse effect on our business.

We substantially depend on the efforts, skill and reputations of our founders and senior management team including: Dean Hatton (President and CEO), Mark Volchek (Founder and CFO), Miles Lasater (Founder and COO), Casey McGuane (Chief Service Officer) and Robert Reach (Chief Sales Officer). We do not currently maintain key person life insurance policies with respect to our executive officers. None of our executive officers have entered into employment agreements with us, leaving them free to terminate their involvement with us at any time and/or to pursue other

19

Table of Contents

opportunities. The loss of any of our executive officers or founders could have a material adverse effect on our ability to manage our company, growth prospects, business financial condition and results of operations.

Our success depends in part on our ability to identify, recruit and retain skilled sales, management and technical personnel.

Our future success depends upon our continued ability to identify, attract, hire and retain highly qualified personnel, including skilled technical, management, product and technology and sales and marketing personnel, all of whom are in high demand and are often subject to competing offers. Competition for qualified personnel in the technology industry is intense and there can be no assurance that we will be able to hire or retain a sufficient number of qualified personnel to meet our requirements, or that we will be able to do so at salary, benefit and other compensation costs that are acceptable to us. A loss of a substantial number of qualified employees, or an inability to attract, retain and motivate additional highly skilled employees required for the expansion of our business, could have a material adverse effect on our business and growth prospects.

We may be liable to our customers or lose customers if we provide poor service or if our systems or products experience failures.

We must fulfill our contractual obligations with respect to our products and services and maintain high quality service to meet the expectations of our customers. Failure to meet these expectations or fulfill our contractual obligations could cause us to lose customers and bear additional liability.

Because of the large amount of data we collect and manage, hardware failures and errors in our systems could result in data loss or corruption or cause the information that we collect to be incomplete or contain significant inaccuracies. For example, errors in our processing systems could delay disbursements or cause disbursements to be made in the wrong amounts or to the wrong person. Our systems may also experience service interruptions as a result of undetected errors or defects in our software, fire, natural disasters, power loss, disruptions in long distance or local telecommunications access, fraud, terrorism, accident or other similar reason, in which case we may experience delays in returning to full service, especially with regard to our data centers and customer service call centers. If problems such as these occur, our customers may seek compensation, withhold payments, seek full or partial refunds, terminate their agreements with us or initiate litigation or other dispute resolution procedures. In addition, we may be subject to claims made by third parties also affected by any of these problems.

Our ability to limit our liabilities by contract or through insurance may be ineffective or insufficient to cover our future liabilities.