Attached files

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

X

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

For the Fiscal Year ended December 31, 2009

|

OR

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

Commission File Number 1-7908

|

ADAMS RESOURCES & ENERGY, INC.

(Exact name of registrant as specified in its charter)

|

Delaware

|

74-1753147

|

4400 Post Oak Pkwy Ste 2700

|

77027

|

|

Houston, Texas

|

|||

|

(State of Incorporation)

|

(I.R.S. Employer Identification No.)

|

(Address of Principal executive offices)

|

(Zip Code)

|

Registrant's telephone number, including area code: (713) 881-3600

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which registered

|

|

Common Stock, $.10 Par Value

|

NYSE Amex

|

Indicate by check mark whether the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ___NO _X_

Indicate by check mark whether the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.YES ____ NO _X_

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports, and (2) has been subject to the filing requirements for the past 90 days. YES_X_ NO ___

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES_X_ NO ___

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. _X_

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer” and “accelerated filer and smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ____ Accelerated filer ____

Non-accelerated filer _X_ Smaller reporting company _____

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Act).

YES ___NO _X_

The aggregate market value of the voting and non-voting common equity held by nonaffiliates as of the close of business on June 30, 2009 was $35,874,679 based on the closing price of $17.15 per one share of common stock as reported on the NYSE AMEX Exchange for such date. A total of 4,217,596 shares of Common Stock were outstanding at March 10, 2010.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the Annual Meeting of Stockholders to be held May 19, 2010 are incorporated by reference into Part III of this report.

PART I

Items 1 and 2. BUSINESS AND PROPERTIES

Forward-Looking Statements –Safe Harbor Provisions

This annual report on Form 10-K for the year ended December 31, 2009 contains certain forward-looking statements covered by the safe harbors provided under Federal securities law and regulations. To the extent such statements are not recitations of historical fact, forward-looking statements involve risks and uncertainties. In particular, statements under the captions (a) Production and Reserve Information, (b) Regulatory Status and Potential Environmental Liability, (c) Management’s Discussion and Analysis of Financial Condition and Results of Operations, (d) Critical Accounting Policies and Use of Estimates, (e) Quantitative and Qualitative Disclosures about Market Risk, (f) Income Taxes, (g) Concentration of Credit Risk, (h) Price Risk Management Activities, and (i) Commitments and Contingencies, among others, contain forward-looking statements. Where the Company expresses an expectation or belief regarding future results of events, such expression is made in good faith and believed to have a reasonable basis in fact. However, there can be no assurance that such expectation or belief will actually result or be achieved.

With the uncertainties of forward looking statements in mind, the reader should consider the risks discussed elsewhere in this report and other documents filed by the Company with the Securities and Exchange Commission from time to time and the important factors described under “Item 1A Risk Factor” that could cause actual results to differ materially from those expressed in any forward-looking statement made by or on behalf of the Company.

Business Activities

Adams Resources & Energy, Inc. (“ARE”) and its subsidiaries, collectively (the "Company"), are engaged in the business of marketing crude oil, natural gas and petroleum products, tank truck transportation of liquid chemicals, and oil and gas exploration and production. Adams Resources & Energy, Inc. is a Delaware corporation organized in 1973. The Company’s headquarters are located in 20,700 square feet of leased office space at 4400 Post Oak Parkway, Suite 2700, Houston, Texas 77027 and the telephone number of that address is (713)-881-3600. The revenues, operating results and identifiable assets of each industry segment for the three years ended December 31, 2009 are set forth in Note (9) of Notes to Consolidated Financial Statements included elsewhere herein.

Marketing Segment Subsidiaries

Gulfmark Energy, Inc. (“Gulfmark”), a subsidiary of ARE, purchases crude oil and arranges sales and deliveries to refiners and other customers. Activity is concentrated primarily onshore in Texas and Louisiana with additional operations in Michigan and New Mexico. During 2009, Gulfmark purchased approximately 66,100 barrels per day of crude oil at the wellhead or lease level. Gulfmark also operates 101 tractor-trailer rigs and maintains over 50 pipeline inventory locations or injection stations. Gulfmark has the ability to barge oil from five oil storage facilities along the intercoastal waterway of Texas and Louisiana and maintains 50,000 barrels of storage capacity at certain of the dock facilities in order to access waterborne markets for its products. Gulfmark arranges transportation for sales to customers or enters into exchange transactions with third parties when the cost of the exchange is less than the alternate cost incurred in transporting or storing the crude oil.

Adams Resources Marketing, Ltd. (“ARM”), a subsidiary of ARE, operates as a wholesale purchaser, distributor and marketer of natural gas. ARM’s focus is on the purchase of natural gas at the producer level. During 2009, ARM purchased approximately 363,000 million british thermal units (“mmbtu’s”) of natural gas per day at the wellhead and pipeline pooling points. Business is concentrated among approximately 60 independent producers with the primary production areas being the Louisiana and Texas Gulf Coast and the offshore Gulf of Mexico region. ARM provides value added services to its customers by providing access to common carrier pipelines and handling daily volume balancing requirements as well as risk management services.

1

Ada Resources, Inc. (“Ada”), a subsidiary of ARE, markets branded and unbranded refined petroleum products such as motor fuels and lubricants. Ada makes purchases based on the supplier’s established distributor prices, with such prices generally being lower than Ada’s sales price to its customers. Motor fuel sales include automotive gasoline, biodiesel and conventional diesel fuel. Lubricants consist of passenger car motor oils as well as a full complement of industrial oils and greases. Ada is also involved in the railroad servicing industry, including fueling and lubricating locomotives as well as performing routine maintenance on the power units. Further, the United States Coast Guard has certified Ada as a direct-to-vessel approved marine fuel and lube vendor. Ada’s marketing area primarily includes the Texas Gulf Coast and southern Louisiana. The primary product distribution and warehousing facility is located on 5.5 Company-owned acres in Houston, Texas. The property includes a 60,000 square foot warehouse, 11,000 square feet of office space and bulk storage for 320,000 gallons of lubricating oil.

Operating results are sensitive to a number of factors. Such factors include commodity location, grades of product, individual customer demand for grades or location of product, localized market price structures, availability of transportation facilities, actual delivery volumes that vary from expected quantities, and the timing and costs to deliver the commodity to the customer.

Transportation Segment Subsidiary

Service Transport Company (“STC”), a subsidiary of ARE, transports liquid chemicals on a "for hire" basis throughout the continental United States and Canada. Transportation service is provided to over 400 customers under multiple load contracts in addition to loads covered under STC’s standard price list. Pursuant to regulatory requirements, STC holds a Hazardous Materials Certificate of Registration issued by the U.S. Department of Transportation. Presently, STC operates 262 truck tractors of which 6 are independent owner-operator units and maintains 416 tank trailers. In addition, STC maintains truck terminals in Houston, Corpus Christi, and Nederland, Texas as well as Baton Rouge (St. Gabriel), Louisiana and Mobile (Saraland), Alabama. Transportation operations are headquartered at a terminal facility situated on 22 Company-owned acres in Houston, Texas. This property includes maintenance facilities, an office building, tank wash rack facilities and a water treatment system. The St. Gabriel, Louisiana terminal is situated on 11.5 Company-owned acres and includes an office building, maintenance bays and tank cleaning facilities.

STC is compliant with International Organization for Standardization (“ISO”) 9001:2000 Standard. The scope of this Quality System Certificate covers the carriage of bulk liquids throughout STC’s area of operations as well as the tank trailer cleaning facilities and equipment maintenance. STC’s quality management process is one of its major assets. The practice of using statistical process control covering safety, on-time performance and customer satisfaction aids continuous improvement in all areas of quality service. In addition to its ISO 9001:2000 practices, the American Chemistry Council recognizes STC as a Responsible CareÓ Partner. Responsible Care Partners serve the chemical industry and implement and monitor the seven Codes of Management Practices. The seven codes address compliance and continuing improvement in (1) Community Awareness and Emergency Response, (2) Pollution Prevention, (3) Process Safety, (4) Distribution, (5) Employee Health and Safety, (6) Product Stewardship and (7) Security.

Oil and Gas Segment Subsidiary

Adams Resources Exploration Corporation (“AREC”), a subsidiary of ARE, is actively engaged in the exploration and development of domestic oil and natural gas properties primarily in Texas and the south central region of the United States. Exploration offices are maintained in Houston and the Company holds an interest in 325 wells of which 43 are Company operated.

2

Producing Wells--The following table sets forth the Company's gross and net productive wells as of December 31, 2009. Gross wells are the total number of wells in which the Company has an interest, while net wells are the sum of the fractional interests owned.

|

Oil Wells

|

Gas Wells

|

Total Wells

|

||||||||||||||||||||||

|

Gross

|

Net

|

Gross

|

Net

|

Gross

|

Net

|

|||||||||||||||||||

|

Texas

|

63 | 8.40 | 112 | 11.49 | 175 | 19.89 | ||||||||||||||||||

|

Other

|

94 | 4.19 | 56 | 5.49 | 150 | 9.68 | ||||||||||||||||||

| 157 | 12.59 | 168 | 16.98 | 325 | 29.57 | |||||||||||||||||||

Acreage--The following table sets forth the Company's gross and net developed and undeveloped acreage as of December 31, 2009. Gross acreage represents the Company’s direct ownership and net acreage represents the sum of the fractional interests owned. The Company’s developed acreage is held by current production while undeveloped acreage is held by oil and gas leases with various remaining terms from six months to three years.

|

Developed Acreage

|

Undeveloped Acreage

|

|||||||||||||||

|

Gross

|

Net

|

Gross

|

Net

|

|||||||||||||

|

Texas

|

80,622 | 9,797 | 225,787 | 17,013 | ||||||||||||

|

Kansas

|

- | - | 31,727 | 3,173 | ||||||||||||

|

Other

|

8,260 | 1,004 | 7,288 | 1,174 | ||||||||||||

| 88,882 | 10,801 | 264,802 | 21,360 | |||||||||||||

Drilling Activity--The following table sets forth the Company's drilling activity for each of the three years ended December 31, 2009. All drilling activity was onshore in Texas, Louisiana and Alabama.

|

2009

|

2008

|

2007

|

||||||||||||||||||||||

|

Gross

|

Net

|

Gross

|

Net

|

Gross

|

Net

|

|||||||||||||||||||

|

Exploratory wells drilled

|

||||||||||||||||||||||||

|

- Productive

|

2 | .10 | 2 | .13 | 3 | .15 | ||||||||||||||||||

|

- Dry

|

7 | .94 | 2 | .22 | 2 | .10 | ||||||||||||||||||

|

Development wells drilled

|

||||||||||||||||||||||||

|

- Productive

|

24 | 1.35 | 17 | 1.06 | 18 | 1.37 | ||||||||||||||||||

|

- Dry

|

2 | .10 | 7 | .68 | 6 | .35 | ||||||||||||||||||

Production and Reserve Information--The Company's estimated net quantities of proved oil and natural gas reserves and the standardized measure of discounted future net cash flows calculated at a 10% discount rate for the three years ended December 31, 2009, are presented in the table below (in thousands):

|

December 31,

|

||||||||||||

|

2009

|

2008

|

2007

|

||||||||||

|

Crude oil (thousands of barrels)

|

242 | 230 | 297 | |||||||||

|

Natural gas (thousands of mcf)

|

7,248 | 6,443 | 7,068 | |||||||||

|

Standardized measure of discounted future

|

||||||||||||

|

net cash flows from oil and gas reserves

|

$ | 9,305 | $ | 11,547 | $ | 19,590 | ||||||

The estimated value of oil and natural gas reserves and future net revenues from oil and natural gas reserves was made by the Company's independent petroleum engineers. The reserve value estimates provided at each of December 31, 2009, 2008 and 2007 are based on market prices of $58.43, $37.87 and $92.50 per barrel for crude oil and $4.05, $5.65 and $7.31 per mcf for natural gas, respectively.

3

Reserve estimates are based on many subjective factors. The accuracy of reserve estimates depends on the quantity and quality of geological data, production performance data, and reservoir engineering data, the pricing assumptions utilized as well as the skill and judgment of petroleum engineers in interpreting such data. The process of estimating reserves requires frequent revision of estimates (usually on an annual basis) as additional information is made available through drilling, testing, reservoir studies and acquiring historical pressure and production data. In addition, the discounted present value of estimated future net revenues should not be construed as the fair market value of oil and natural gas producing properties. Such estimates do not necessarily portray a realistic assessment of current value or future performance of such properties. Such revenue calculations are based on estimates as to the timing of oil and natural gas production, and there is no assurance that the actual timing of production will conform to or approximate such estimates. Also, certain assumptions have been made with respect to pricing. The estimates assume prices will remain constant from the date of the engineer's estimates, except for changes reflected under natural gas sales contracts. There can be no assurance that actual future prices will not vary as industry conditions, governmental regulation and other factors impact the market price for oil and natural gas.

The Company's oil and natural gas production for the three years ended December 31, 2009 was as follows:

|

Years Ended

|

Crude Oil

|

Natural

|

||||||

|

December 31,

|

(barrels)

|

Gas (mcf)

|

||||||

|

2009

|

49,500 | 1,304,000 | ||||||

|

2008

|

50,500 | 1,243,000 | ||||||

|

2007

|

69,250 | 1,182,000 | ||||||

Certain financial information relating to the Company's oil and natural gas division revenues and earnings is summarized as follows:

|

Years Ended December 31,

|

||||||||||||

|

2009

|

2008

|

2007

|

||||||||||

|

Average oil and condensate

|

||||||||||||

|

sales price per barrel

|

$ | 58.10 | $ | 99.25 | $ | 70.21 | ||||||

|

Average natural gas

|

||||||||||||

|

sales price per mcf

|

$ | 4.43 | $ | 9.84 | $ | 7.54 | ||||||

|

Average production cost, per equivalent

|

||||||||||||

|

barrel, charged to expense

|

$ | 13.25 | $ | 18.34 | $ | 15.32 | ||||||

North Sea Exploration Licenses—Previously the Company held certain exploration rights in the Central and Southern sectors of the United Kingdom’s North Sea region. These rights afforded the opportunity to analyze and assess licensed acreage for an initial two-year period without accompanying stringent financial requirements. Ultimately, the Company’s investment group was unsuccessful in obtaining a partner to fund drilling on any of the prospective acreage and therefore the license rights were dropped in 2009 at no additional cost to the Company.

The Company has had no reports to federal authorities or agencies of estimated oil and gas reserves. The Company is not obligated to provide any fixed and determinable quantities of oil or gas in the future under existing contracts or agreements associated with its oil and gas exploration and production segment.

Reference is made to Note (10) of the Notes to Consolidated Financial Statements for additional disclosures relating to oil and natural gas exploration and production activities.

4

Environmental Compliance and Regulation

The Company is subject to an extensive variety of evolving United States federal, state and local laws, rules and regulations governing the storage, transportation, manufacture, use, discharge, release and disposal of product and contaminants into the environment, or otherwise relating to the protection of the environment. Presented below is a non-exclusive listing of the environmental laws that potentially impact the Company’s activities.

|

-

|

The Solid Waste Disposal Act, as amended by the Resource Conservation and Recovery Act of 1976, as amended.

|

|

-

|

Comprehensive Environmental Response, Compensation and Liability Act of 1980 ("CERCLA" or "Superfund"), as amended.

|

|

-

|

The Clean Water Act of 1972, as amended.

|

|

-

|

Federal Oil Pollution Act of 1990, as amended.

|

|

-

|

The Clean Air Act of 1970, as amended.

|

|

-

|

The Toxic Substances Control Act of 1976, as amended.

|

|

-

|

The Emergency Planning and Community Right-to-Know Act.

|

|

-

|

The Occupational Safety and Health Act of 1970, as amended.

|

|

-

|

Texas Clean Air Act.

|

|

-

|

Texas Solid Waste Disposal Act.

|

|

-

|

Texas Water Code.

|

|

-

|

Texas Oil Spill Prevention and Response Act of 1991, as amended.

|

Railroad Commission of Texas (“RRC”)--The RRC regulates, among other things, the drilling and operation of oil and natural gas wells, the operation of oil and gas pipelines, the disposal of oil and natural gas production wastes and certain storage of unrefined oil and gas. RRC regulations govern the generation, management and disposal of waste from such oil and natural gas operations and provide for the clean up of contamination from oil and natural gas operations. The RRC has promulgated regulations that provide for civil and/or criminal penalties and/or injunctive relief for violations of the RRC regulations.

Louisiana Office of Conservation--This agency has primary statutory responsibility for regulation and conservation of oil, gas, and other natural resources in the State of Louisiana. Their objectives are to (i) regulate the exploration and production of oil, natural gas and other hydrocarbons; (ii) control and allocate energy supplies and distribution and (iii) protect public safety and the State’s environment from oilfield waste, including regulation of underground injection and disposal practices.

State and Local Government Regulation--Many states are authorized by the United States Environmental Protection Agency (“EPA”) to enforce regulations promulgated under various federal statutes. In addition, there are numerous other state and local authorities that regulate the environment, some of which impose more stringent environmental standards than federal laws and regulations. The penalties for violations of state law vary, but typically include injunctive relief, recovery of damages for injury to air, water or property and fines for non-compliance.

Oil and Gas Operations--The Company's oil and gas drilling and production activities are subject to laws and regulations relating to environmental quality and pollution control. One aspect of the Company's oil and gas operation is the disposal of used drilling fluids, saltwater, and crude oil sediments. In addition, low-level naturally occurring radiation may, at times, occur with the production of crude oil and natural gas. The Company's policy is to comply with environmental regulations and industry standards. Environmental compliance has become more stringent and the Company, from time to time, may be required to remediate past practices. Management believes that such required remediation in the future, if any, will not have a material adverse impact on the Company's financial position or results of operations.

5

All states in which the Company owns producing oil and gas properties have statutory provisions regulating the production and sale of crude oil and natural gas. Regulations typically require permits for the drilling of wells and regulate the spacing of wells, the prevention of waste, protection of correlative rights, the rate of production, prevention and clean-up of pollution and other matters.

Marketing Operations--The Company's marketing facilities are subject to a number of state and federal environmental statutes and regulations, including the regulation of underground fuel storage tanks. While the Company does not own or operate underground tanks as of December 31, 2009, historically the Company has been an owner and operator of underground storage tanks. The EPA's Office of Underground Tanks and applicable state laws establish regulations requiring owners or operators of underground fuel tanks to demonstrate evidence of financial responsibility for the costs of corrective action and the compensation of third parties for bodily injury and property damage caused by sudden and non-sudden accidental releases arising from operating underground tanks. In addition, the EPA requires the installation of leak detection devices and stringent monitoring of the ongoing condition of underground tanks. Should leakage develop in an underground tank, the operator is obligated for clean up costs. During the period when the Company was an operator of underground tanks, it secured insurance covering both third party liability and clean up costs.

Transportation Operations--The Company's tank truck operations are conducted pursuant to authority of the United States Department of Transportation (“DOT”) and various state regulatory authorities. The Company's transportation operations must also be conducted in accordance with various laws relating to pollution and environmental control. Interstate motor carrier operations are subject to safety requirements prescribed by DOT. Matters such as weight and dimension of equipment are also subject to federal and state regulations. DOT regulations also require mandatory drug testing of drivers and require certain tests for alcohol levels in drivers and other safety personnel. The trucking industry is subject to possible regulatory and legislative changes such as increasingly stringent environmental regulations or limits on vehicle weight and size. Regulatory change may affect the economics of the industry by requiring changes in operating practices or by changing the demand for common or contract carrier services or the cost of providing truckload services. In addition, the Company’s tank wash facilities are subject to increasingly stringent local, state and federal environmental regulations.

The Company has implemented security procedures for drivers and terminal facilities. Satellite tracking transponders installed in the power units are used to communicate en route emergencies to the Company and to maintain constant information as to the unit’s location. If necessary, the Company’s terminal personnel will notify local law enforcement agencies. In addition, the Company is able to advise a customer of the status and location of their loads. Remote cameras and better lighting coverage in the staging and parking areas have augmented terminal security.

Regulatory Status and Potential Environmental Liability--The operations and facilities of the Company are subject to numerous federal, state and local environmental laws and regulations including those described above, as well as associated permitting and licensing requirements. The Company regards compliance with applicable environmental regulations as a critical component of its overall operation, and devotes significant attention to providing quality service and products to its customers, protecting the health and safety of its employees, and protecting the Company’s facilities from damage. Management believes the Company has obtained or applied for all permits and approvals required under existing environmental laws and regulations to operate its current business. Management has reported that the Company is not subject to any pending or threatened environmental litigation or enforcement action(s), which could materially and adversely affect the Company's business. The Company has, where appropriate, implemented operating procedures at each of its facilities designed to assure compliance with environmental laws and regulation. However, given the nature of the Company’s business, the Company is subject to environmental risks and the possibility remains that the Company's ownership of its facilities and its operations and activities could result in civil or criminal enforcement and public as well as private action(s) against the Company, which may necessitate or generate mandatory clean up activities, revocation of required permits or licenses, denial of application for future permits, and/or significant fines, penalties or damages, any and all of which could have a material adverse effect on the Company. At December 31, 2009, the Company is unaware of any unresolved environmental issues for which additional accounting accruals are necessary.

6

Employees

At December 31, 2009 the Company employed 679 persons, 14 of whom were employed in the exploration and production of oil and gas, 286 in the marketing of crude oil, natural gas and petroleum products, 356 in transportation operations, and 23 in administrative capacities. None of the Company's employees are represented by a union. Management believes its employee relations are satisfactory.

Federal and State Taxation

The Company is subject to the provisions of the Internal Revenue Code of 1986, as amended (the “Code”). In accordance with the Code, the Company computes its income tax provision based on a 35 percent tax rate. The Company's operations are, in large part, conducted within the State of Texas. Texas operations are subject to a one-half percent state tax on its revenues net of cost of goods sold as defined by the state. Oil and gas activities are also subject to state and local income, severance, property and other taxes. Management believes the Company is currently in compliance with all federal and state tax regulations.

Available Information

The Company is required to file periodic reports as well as other information with the Securities and Exchange Commission (“SEC”) within established deadlines. Any document filed with the SEC may be viewed or copied at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Additional information regarding the Public Reference Room can be obtained by calling the SEC at (800) SEC-0330. The Company’s SEC filings are also available to the public through the SEC’s web site located at http://www.sec.gov.

The Company maintains a corporate website at http://www.adamsresources.com, on which investors may access free of charge the annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports as soon as is reasonably practicable after filing or furnishing such material with the SEC. Additionally, the Company has adopted and posted on its website a Code of Business Ethics designed to reflect requirements of the Sarbanes-Oxley Act of 2002, NYSE Amex Exchange rules and other applicable laws, rules and regulations. The Code of Business Ethics applies to all of the Company’s directors, officers and employees. Any amendment to the Code of Business Ethics will be posted promptly on the Company’s website. The information contained on or accessible from the Company’s website does not constitute a part of this report and is not incorporated by reference herein. The Company will provide a printed copy of any of these aforementioned documents free of charge upon request by calling ARE at (713)-881-3600 or by writing to:

Adams Resources & Energy, Inc.

ATTN: Richard B. Abshire

4400 Post Oak Parkway, Suite 2700

Houston, Texas 77027

Item 1A RISK FACTORS

Worldwide economic developments could damage operations and materially reduce profitability and cash flows.

Since mid 2008, disruptions in the credit markets and concerns about global economic growth have had a significant adverse impact on global financial markets and commodity prices. At times, these factors have contributed to a decline in the Company’s stock price and corresponding market capitalization. Further commodity price decreases during 2010 could result in reduced earnings. Since the Company has no bank debt obligations nor covenants tied to its stock price, potential declines in the Company’s stock price do not affect the Company’s liquidity or overall financial condition. Should the capital and credit markets continue to experience volatility and the availability of funds remains limited, the Company’s customers and suppliers may incur increased costs associated with issuing commercial paper and/or other debt instruments and this, in turn, could adversely affect the Company’s ability to secure supply and make profitable sales.

7

General economic conditions could reduce demand for chemical based trucking services.

Customer demand for the Company’s products and services is substantially dependent upon the general economic conditions for the United States which have generally been slow over the past year and continue to be challenging. In particular, demand for liquid chemical truck transportation services is dependent on activity within the petrochemical sector of the U. S. economy. Chemical sector demand typically varies with the housing and auto markets as well as the relative strength of the U. S. dollar to foreign currencies. A relatively strong U.S. dollar exchange rate tends to suppress export demand for petrochemicals which is adverse to the Company’s transportation operation. Conversely, a weak U. S. dollar exchange rate tends to stimulate export demand for petrochemicals.

The Company’s business is dependent on the ability to obtain trade and other credit.

The Company’s future development and growth depends in part on its ability to successfully obtain credit from suppliers and other parties. Credit arrangements are relied upon as a significant source of liquidity for capital requirements not satisfied by operating cash flow.

Current global financial markets and economic conditions have been, and may continue to be, disrupted and volatile. As a result of concerns about the stability of financial markets generally and the solvency of creditors specifically, the availability of money from the credit markets is reduced as many lenders and institutional investors have enacted tighter lending standards, refused to refinance existing debt on terms similar to current debt and in some cases, ceased to provide funding to borrowers. These issues, along with significant write-offs in the financial services sector and the current weak economic conditions have made, and may continue to make, it more difficult for the Company and its suppliers and customers to obtain funding.

If the Company is unable to obtain trade or other forms credit on reasonable and competitive terms, its ability to continue its marketing and exploration businesses, pursue improvements, and continue future growth will be limited. There is no assurance that the Company will be able to maintain future credit arrangements on commercially reasonable terms.

The financial soundness of customers could affect our business and operating results

As a result of constraints in the financial markets and other macro-economic challenges currently affecting the economy of the United States and other parts of the world, the Company’s customers may experience cash flow concerns. As a result, if customers’ operating and financial performance deteriorates, or if they are unable to make scheduled payments or obtain credit, customers may not be able to pay, or may delay payment of, accounts receivable owed to the Company. Any inability of current and/or potential customers to pay for services may adversely affect the Company’s financial condition and results of operations.

Counterparty credit default could have an adverse effect on the Company.

The Company’s revenues are generated under contracts with various counterparties. Results of operations would be adversely affected as a result of non-performance by any of these counterparties of their contractual obligations under the various contracts. A counterparty’s default or non-performance could be caused by factors beyond the Company’s control. A default could occur as a result of circumstances relating directly to the counterparty, or due to circumstances caused by other market participants having a direct or indirect relationship with such counterparty. The Company seeks to mitigate the risk of default by evaluating the financial strength of potential counterparties; however, despite mitigation efforts, defaults by counterparties may occur from time to time.

8

Fluctuations in oil and gas prices could have an effect on the Company.

The Company’s future financial condition, revenues, results of operations and future rate of growth are materially affected by oil and natural gas prices. Oil and natural gas prices historically have been volatile and are likely to continue to be volatile in the future. Moreover, oil and natural gas prices depend on factors outside the control of the Company. These factors include:

|

·

|

supply and demand for oil and gas and expectations regarding supply and demand;

|

|

·

|

political conditions in other oil-producing countries, including the possibility of insurgency or war in such areas;

|

|

·

|

economic conditions in the United States and worldwide;

|

|

·

|

governmental regulations and taxation;

|

|

·

|

impact of energy conservation efforts;

|

|

·

|

the price and availability of alternative fuel sources;

|

|

·

|

weather conditions;

|

|

·

|

availability of local, interstate and intrastate transportation systems; and

|

|

·

|

market uncertainty.

|

Revenues are generated under contracts that must be renegotiated periodically.

Substantially all of the Company’s revenues are generated under contracts which expire periodically or which must be frequently renegotiated, extended or replaced. Whether these contracts are renegotiated, extended or replaced is often subject to factors beyond the Company’s control. Such factors include sudden fluctuations in oil and gas prices, counterparty ability to pay for or accept the contracted volumes and, most importantly, an extremely competitive marketplace for the services offered by the Company. There is no assurance that the costs and pricing of the Company’s services can remain competitive in the marketplace or that the Company will be successful in renegotiating its contracts.

Anticipated or scheduled volumes will differ from actual or delivered volumes.

The Company’s crude oil and natural gas marketing operation purchases initial production of crude oil and natural gas at the wellhead under contracts requiring the Company to accept the actual volume produced. The resale of such production is generally under contracts requiring a fixed volume to be delivered. The Company estimates its anticipated supply and matches such supply estimate for both volume and pricing formulas with committed sales volumes. Since actual wellhead volumes produced will never equal anticipated supply, the Company’s marketing margins may be adversely impacted. In many instances, any losses resulting from the difference between actual supply volumes compared to committed sales volumes must be absorbed by the Company.

Environmental liabilities and environmental regulations may have an adverse effect on the Company.

The Company’s business is subject to environmental hazards such as spills, leaks or any discharges of petroleum products and hazardous substances. These environmental hazards could expose the Company to material liabilities for property damage, personal injuries and/or environmental harms, including the costs of investigating and rectifying contaminated properties.

Environmental laws and regulations govern many aspects of the Company’s business, such as drilling and exploration, production, transportation and waste management. Compliance with environmental laws and regulations can require significant costs or may require a decrease in production. Moreover, noncompliance with these laws and regulations could subject the Company to significant administrative, civil and/or criminal fines and/or penalties.

9

Operations could result in liabilities that may not be fully covered by insurance.

The oil and gas business involves certain operating hazards such as well blowouts, explosions, fires and pollution. Any of these operating hazards could cause serious injuries, fatalities or property damage, which could expose the Company to liability. The payment of any of these liabilities could reduce, or even eliminate, the funds available for exploration, development, and acquisition, or could result in a loss of the Company’s properties and may even threaten survival of the enterprise.

Consistent with the industry standard, the Company’s insurance policies provide limited coverage for losses or liabilities relating to pollution, with broader coverage for sudden and accidental occurrences. Insurance might be inadequate to cover all liabilities. Moreover, from time to time, obtaining insurance for the Company’s line of business can become difficult and costly. Typically, when insurance cost escalates, the Company may reduce its level of coverage and more risk may be retained to offset cost increases. If substantial liability is incurred and damages are not covered by insurance or exceed policy limits, the Company’s operation and financial condition could be materially adversely affected.

Changes in tax laws or regulations could adversely affect the Company.

The Internal Revenue Service, the United States Treasury Department and Congress frequently review federal income tax legislation. The Company cannot predict whether, when or to what extent new federal tax laws, regulations, interpretations or rulings will be adopted. Any such legislative action may prospectively or retroactively modify tax treatment and, therefore, may adversely affect taxation of the Company.

The Company’s business is subject to changing government regulations.

Federal, state or local government agencies may impose environmental, labor or other regulations that increase costs and/or terminate or suspend operations. The Company’s business is subject to federal, state and local laws and regulations. These regulations relate to, among other things, the exploration, development, production and transportation of oil and natural gas. Existing laws and regulations could be changed, and any changes could increase costs of compliance and costs of operations.

Estimating reserves, production and future net cash flow is difficult.

Estimating oil and natural gas reserves is a complex process that involves significant interpretations and assumptions. It requires interpretation of technical data and assumptions relating to economic factors such as future commodity prices, production costs, severance and excise taxes, capital expenditures and remedial costs, and the assumed effect of governmental regulation. As a result, actual results may differ from the Company’s estimates. Also, the use of a 10 percent discount factor for reporting purposes, as prescribed by the SEC, may not necessarily represent the most appropriate discount factor, given actual interest rates and risks to which the Company’s business is subject. Any significant variations from the Company’s valuations could cause the estimated quantities and net present value of the Company’s reserves to differ materially.

The reserve data included in this report is only an estimate. The reader should not assume that the present values referred to in this report represent the current market value of the Company’s estimated oil and natural gas reserves. The timing of the production and the expenses from development and production of oil and natural gas properties will affect both the timing of actual future net cash flows from the Company’s proved reserves and their present value.

10

The Company’s business is dependent on the ability to replace reserves.

Future success depends in part on the Company’s ability to find, develop and acquire additional oil and natural gas reserves. Without successful acquisition or exploration activities, reserves and revenues will decline as a result of current reserves being depleted by production. The successful acquisition, development or exploration of oil and natural gas properties requires an assessment of recoverable reserves, future oil and natural gas prices and operating costs, potential environmental and other liabilities, and other factors. These assessments are necessarily inexact. As a result, the Company may not recover the purchase price of a property from the sale of production from the property, or may not recognize an acceptable return from properties acquired. In addition, exploration and development operations may not result in any increases in reserves. Exploration or development may be delayed or canceled as a result of inadequate capital, compliance with governmental regulations or price controls or mechanical difficulties. In the future, the cost to find or acquire additional reserves may become prohibitive.

Fluctuations in commodity prices could have an adverse effect on the Company.

Revenues depend on volumes and rates, both of which can be affected by the prices of oil and natural gas. Decreased prices could result in a reduction of the volumes of crude oil and natural gas produced by the Company and/or its marketing segment suppliers. The success of the Company’s operations is, in part, subject to continued development of additional oil and natural gas reserves. A decline in energy prices could precipitate a decrease in these development activities leading to a decrease in the volume of reserves available for production, processing and transmission. Fluctuations in energy prices are caused by a number of factors, including:

|

·

|

regional, domestic and international supply and demand;

|

|

·

|

availability and adequacy of transportation facilities;

|

|

·

|

energy legislation;

|

|

·

|

federal and state taxes, if any, on the sale or transportation of natural gas;

|

|

·

|

abundance of supplies of alternative energy sources;

|

|

·

|

political unrest among oil producing countries; and

|

|

·

|

opposition to energy development in environmentally sensitive areas.

|

Revenues are dependent on the ability to successfully complete drilling activity.

Drilling and exploration are one of the main methods of replacing reserves. However, drilling and exploration operations may not result in any increases in reserves for various reasons. Drilling and exploration may be curtailed, delayed or cancelled as a result of:

|

·

|

lack of acceptable prospective acreage;

|

|

·

|

inadequate capital resources;

|

|

·

|

weather;

|

|

·

|

title problems;

|

|

·

|

compliance with governmental regulations; and

|

|

·

|

mechanical difficulties.

|

Moreover, the costs of drilling and exploration may greatly exceed initial estimates. In such a case, the Company would be required to make additional expenditures to develop its drilling projects. Such additional and unanticipated expenditures could adversely affect the Company’s financial condition and results of operations.

Security issues related to drivers and terminal facilities

The Company transports liquid combustible materials such as gasoline and petrochemicals and such materials may be a target for terrorist attacks. Therefore, the Company employs a variety of security measures to mitigate the risk of such events.

11

Current and future litigation could have an adverse effect on the Company.

The Company is currently involved in several administrative and civil legal proceedings in the ordinary course of its business. Moreover, as incidental to operations, the Company sometimes becomes involved in various lawsuits and/or disputes. Lawsuits and other legal proceedings can involve substantial costs, including the costs associated with investigation, litigation and possible settlement, judgment, penalty or fine. Although insurance is maintained to mitigate these costs, there can be no assurance that costs associated with lawsuits or other legal proceedings will not exceed the limits of insurance policies. The Company’s results of operations could be adversely affected if a judgment, penalty or fine is not fully covered by insurance.

Item 1B UNRESOLVED STAFF COMMENTS

None.

Item 3. LEGAL PROCEEDINGS

From time to time as incident to its operations, the Company may become involved in various lawsuits and/or disputes. Primarily as an operator of an extensive trucking fleet, the Company is a party to motor vehicle accidents, worker compensation claims and other items of general liability as would be typical for the industry. Management of the Company is presently unaware of any claims against the Company that are either outside the scope of insurance coverage, or that may exceed the level of insurance coverage, and could potentially represent a material adverse effect on the Company’s financial position or results of operations.

Item 4. RESERVED

12

PART II

|

Item 5.

|

MARKET FOR THE REGISTRANT'S COMMON STOCK, RELATED SECURITY HOLDER MATTERS AND ISSUER REPURCHASE OF EQUITY SECURITIES

|

The Company's common stock is traded on the NYSE Amex Exchange. The following table sets forth the high and low sales prices of the common stock as reported by the American Stock Exchange for each calendar quarter since January 1, 2008.

|

American Stock Exchange

|

||||||||

|

High

|

Low

|

|||||||

|

2008

|

||||||||

|

First Quarter

|

$ | 28.65 | $ | 22.00 | ||||

|

Second Quarter

|

35.35 | 26.35 | ||||||

|

Third Quarter

|

34.95 | 22.32 | ||||||

|

Fourth Quarter

|

23.00 | 13.55 | ||||||

|

2009

|

||||||||

|

First Quarter

|

$ | 18.40 | $ | 12.66 | ||||

|

Second Quarter

|

18.49 | 12.75 | ||||||

|

Third Quarter

|

21.95 | 14.83 | ||||||

|

Fourth Quarter

|

25.18 | 19.18 | ||||||

At March 10, 2010 there were approximately 253 shareholders of record of the Company's common stock and the closing stock price was $22.70 per share. The Company has no securities authorized for issuance under equity compensation plans. The Company made no repurchases of its stock during 2009 and 2008.

On December 15, 2009, the Company paid an annual cash dividend of $.50 per common share to common stockholders of record on December 1, 2009. On December 16, 2008, the Company paid an annual cash dividend of $.50 per common share to common stockholders of record on December 2, 2008. Such dividends totaled $2,108,798 and $2,108,798 for each of 2009 and 2008, respectively.

13

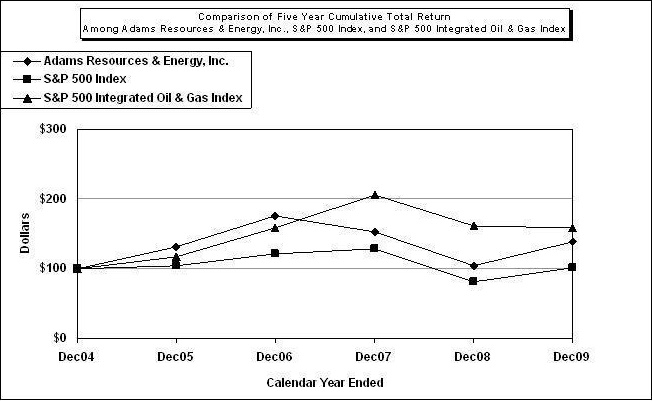

Performance Graph

The performance graph shown below was prepared under the applicable rules of the SEC based on data supplied by Standard & Poor’s Compustat. The purpose of the graph is to show comparative total stockholder returns for the Company versus other investment options for a specified period of time. The graph was prepared based upon the following assumptions:

|

1.

|

$100.00 was invested on December 31, 2004 in the Company’s common stock, the S&P 500 Index, and the S&P 500 Integrated Oil and Gas Index.

|

|

2.

|

Dividends are reinvested on the ex-dividend dates.

|

Note: The stock price performance shown on the graph below is not necessarily indicative of future price performance.

|

Total Return To Shareholders

|

||||||||||||||||||||||||

|

(Includes reinvestment of dividends)

|

||||||||||||||||||||||||

|

INDEXED RETURNS

|

||||||||||||||||||||||||

|

Base

|

Years Ending

|

|||||||||||||||||||||||

|

Period

|

||||||||||||||||||||||||

|

Company / Index

|

Dec04

|

Dec05

|

Dec06

|

Dec07

|

Dec08

|

Dec09

|

||||||||||||||||||

|

Adams Resources & Energy, Inc.

|

100 | 131.64 | 175.94 | 153.01 | 104.58 | 138.92 | ||||||||||||||||||

|

S&P 500 Index

|

100 | 104.91 | 121.48 | 128.16 | 80.74 | 102.11 | ||||||||||||||||||

|

S&P 500 Integrated Oil & Gas Index

|

100 | 117.63 | 158.61 | 205.96 | 161.08 | 159.00 | ||||||||||||||||||

14

Item 6. SELECTED FINANCIAL DATA

FIVE YEAR REVIEW OF SELECTED FINANCIAL DATA

|

Years Ended December 31,

|

||||||||||||||||||||

|

2009

|

2008

|

2007

|

2006

|

2005

|

||||||||||||||||

|

Revenues:

|

(In thousands, except per share data)

|

|||||||||||||||||||

|

Marketing

|

$ | 1,889,583 | $ | 4,074,677 | $ | 2,558,545 | $ | 2,167,502 | $ | 2,292,029 | ||||||||||

|

Transportation

|

44,895 | 67,747 | 63,894 | 62,151 | 57,458 | |||||||||||||||

|

Oil and gas

|

8,650 | 17,248 | 13,783 | 16,950 | 15,346 | |||||||||||||||

| $ | 1,943,128 | $ | 4,159,672 | $ | 2,636,222 | $ | 2,246,603 | $ | 2,364,833 | |||||||||||

|

Operating Earnings:

|

||||||||||||||||||||

|

Marketing

|

$ | 17,487 | $ | (2,704 | ) | $ | 20,152 | $ | 12,975 | $ | 22,481 | |||||||||

|

Transportation

|

2,128 | 4,245 | 5,504 | 5,173 | 5,714 | |||||||||||||||

|

Oil and gas operations

|

(3,625 | ) | (3,348 | ) | (2,853 | ) | 5,355 | 6,765 | ||||||||||||

|

Oil and gas property sale

|

- | - | 12,078 | - | - | |||||||||||||||

|

General and administrative

|

(9,589 | ) | (9,667 | ) | (10,974 | ) | (8,536 | ) | (9,668 | ) | ||||||||||

| 6,401 | (11,474 | ) | 23,907 | 14,967 | 25,292 | |||||||||||||||

|

Other income (expense):

|

||||||||||||||||||||

|

Interest income

|

125 | 1,103 | 1,741 | 965 | 188 | |||||||||||||||

|

Interest expense

|

(25 | ) | (187 | ) | (134 | ) | (159 | ) | (128 | ) | ||||||||||

|

Earnings (loss) from continuing operations

|

||||||||||||||||||||

|

before income taxes

|

6,501 | (10,558 | ) | 25,514 | 15,773 | 25,352 | ||||||||||||||

|

Income tax (provision) benefit

|

(2,352 | ) | 4,986 | (8,458 | ) | (5,290 | ) | (8,583 | ) | |||||||||||

|

Earnings (loss) from continuing operations

|

4,149 | (5,572 | ) | 17,056 | 10,483 | 16,769 | ||||||||||||||

|

Earnings (loss) from discontinued

|

||||||||||||||||||||

|

operations, net of taxes

|

- | - | - | - | 872 | |||||||||||||||

|

Net earnings (loss)

|

$ | 4,149 | $ | (5,572 | ) | $ | 17,056 | $ | 10,483 | $ | 17,641 | |||||||||

|

Earnings (Loss) Per Share

|

||||||||||||||||||||

|

From continuing operations

|

$ | .98 | $ | (1.32 | ) | $ | 4.04 | $ | 2.49 | $ | 3.97 | |||||||||

|

From discontinued operations

|

- | - | - | - | .21 | |||||||||||||||

|

Basic earnings (loss) per share

|

$ | .98 | $ | (1.32 | ) | $ | 4.04 | $ | 2.49 | $ | 4.18 | |||||||||

|

Dividends per common share

|

$ | .50 | $ | .50 | $ | .47 | $ | .42 | $ | .37 | ||||||||||

|

Financial Position

|

||||||||||||||||||||

|

Working capital

|

$ | 38,372 | $ | 41,559 | $ | 50,572 | $ | 35,208 | $ | 39,321 | ||||||||||

|

Total assets

|

249,401 | 210,926 | 357,075 | 289,287 | 312,662 | |||||||||||||||

|

Long-term debt, net of

|

||||||||||||||||||||

|

current maturities

|

- | - | - | 3,000 | 11,475 | |||||||||||||||

|

Shareholders’ equity

|

83,801 | 81,761 | 89,442 | 74,368 | 65,656 | |||||||||||||||

|

Dividends on common shares

|

2,109 | 2,109 | 1,982 | 1,771 | 1,560 | |||||||||||||||

________________________________

Notes:

|

-

|

In 2007, certain oil and natural gas producing properties were sold for $14.9 million producing a net gain of $12.1 million.

|

15

|

|

Item 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

Results of Operations

- Marketing

Marketing revenues, operating earnings and depreciation are as follows (in thousands):

|

2009

|

2008

|

2007

|

||||||||||

|

Revenues

|

||||||||||||

|

Crude oil

|

$ | 1,770,600 | $ | 3,849,531 | $ | 2,373,838 | ||||||

|

Natural gas

|

14,232 | 11,586 | 13,764 | |||||||||

|

Refined products

|

104,751 | 213,560 | 170,943 | |||||||||

|

Total

|

$ | 1,889,583 | $ | 4,074,677 | $ | 2,558,545 | ||||||

|

Operating Earnings (loss)

|

||||||||||||

|

Crude oil

|

$ | 15,404 | $ | (4,545 | ) | $ | 15,321 | |||||

|

Natural gas

|

2,749 | 2,247 | 4,999 | |||||||||

|

Refined products

|

(666 | ) | (406 | ) | (168 | ) | ||||||

|

Total

|

$ | 17,487 | $ | (2,704 | ) | $ | 20,152 | |||||

|

Depreciation

|

||||||||||||

|

Crude oil

|

$ | 1,997 | $ | 2,039 | $ | 657 | ||||||

|

Natural gas

|

166 | 163 | 162 | |||||||||

|

Refined products

|

533 | 565 | 457 | |||||||||

|

Total

|

$ | 2,696 | $ | 2,767 | $ | 1,276 | ||||||

Supplemental volume and price information is:

|

2009

|

2008

|

2007

|

|

|

Field Level Purchases per day (1)

|

|||

|

Crude Oil – barrels

|

66,100

|

67,800

|

61,500

|

|

Natural Gas – mmbtu’s

|

363,000

|

437,000

|

423,000

|

|

Average Purchase Price

|

|||

|

Crude Oil – per barrel

|

$ 58.32

|

$ 99.72

|

$ 70.70

|

|

Natural Gas – per mmbtu

|

$ 3.75

|

$ 8.63

|

$ 6.79

|

|

|

(1) Reflects the volume purchased from third parties at the oil and natural gas field level and pipeline pooling points.

|

16

Comparison 2009 to 2008

Crude oil revenues declined for 2009 by 54 percent because of significantly lower average crude oil prices as shown in the table above. While comparative overall crude oil prices were reduced in 2009, the direction of change in price was generally increasing during the period. The average acquisition cost of crude oil moved from the $41 per barrel level at the beginning of the year to $75 per barrel for the December 2009 average price. This event produced an inventory liquidation gain of $5,780,000 for the year. The opposite event occurred in 2008 as crude oil prices declined from the $90 per barrel range in January 2008 to the $41 per barrel range in December 2008 causing an $11.8 million inventory liquidation loss. The Company’s inventory holdings result from shipments in transit and as of December 31, 2009 the Company held 189,079 barrels of crude oil at an average price of $74.32 per barrel. Excluding inventory related gains and losses, comparative operating earnings would have been $9,624,000 for 2009 and $7,338,000 for 2008. The 2009 improvement resulted from reduced prices for diesel fuel consumed in the trucking function of this business. Diesel fuel expense was $4.6 million in 2009 versus $7.3 million in 2008.

Natural gas sales are reported net of underlying natural gas purchase costs and thus reflect gross margins. As shown above, such margins were fairly consistent between the periods. Natural gas lease purchase volumes were reduced in the current year as generally low natural gas prices caused production curtailments and delayed drilling plans by the Company’s supplier group. Despite reduced volumes and based on historical trends, the year 2009 should have produced significantly improved operating earnings relative to 2008 because of the volatile weather patterns that occurred as compared to the mild conditions existing in 2008. Traditionally, the Company captures improved unit margins during periods of rapidly changing weather. However, the continued development of the nations natural gas infrastructure both in terms of more diverse areas of production and expanded pipeline and storage capacity have served to reduce unit margin even during periods of severe weather. This development may limit future opportunities to profit from natural gas marketing operations. To counteract this dynamic, the Company has begun recruiting additional producer suppliers in the expanding production areas.

Contraction in the United States economy has adversely affected refined product segment revenues and operating earnings. Both 2009 and 2008 suffered from the downturn in the domestic economy which began during the third quarter of 2008. Operating earnings were additionally impacted in 2009 and 2008 when the bad debt provision was increased by approximately $560,000 and $700,000, respectively, due to customer financial stability concerns. The Company has focused on cost controls and instituted personnel cut-backs in the fourth quarter of 2009 in an effort to restore profitability to this segment.

Comparison 2008 to 2007

Crude oil revenues increased by 62 percent in 2008 relative to 2007 due to significantly increased commodity prices during major portions of the year. The Company’s monthly average crude oil acquisition price rose from the $91 per barrel level at year-end 2007 to the $133 per barrel level in June 2008 with a subsequent steep decline beginning in August 2008 to the $41 per barrel range by year-end. Net inventory driven losses for 2008 were $11.8 million. In contrast, rising prices produced $4.3 million of inventory liquidation gains in 2007. Excluding the impact of inventory values as described above, crude oil operating earnings for 2008 and 2007 would have been $7,338,000 and $11,021,000, respectively. Absent the inventory items, crude oil earnings from operations were reduced in 2008 as a result of escalated prices for the diesel fuel. Diesel fuel expense was $7.3 million in 2008 compared to $4.3 million for 2007.

Natural gas operating earnings were reduced in 2008 relative to 2007 as the marketplace in 2008 provided few opportunities to enhance margins by meeting short-term day-to-day demand needs. In part, such conditions existed because 2008’s mild weather patterns did not stimulate localized demand spikes.

17

Refined products revenues increased during 2008 consistent with increased commodity prices partially offset by reduced volumes as the Company reduced its sales activity to less creditworthy accounts. Refined product driven operating earnings were reduced during 2008 because of an increased allowance for doubtful accounts receivable through a bad debt charge of $700,000. The Company has a number of construction industry customers that experienced significantly increased fuel costs coupled with a downturn in the housing development market. With an elevated likelihood of this class of customer experiencing financial insolvency, the Company’s bad debt provision was increased accordingly.

Historically, prices received for crude oil, natural gas and refined products have been volatile and unpredictable with price volatility expected to continue. See also discussion under Item 3 – Commodity Price Risk.

- Transportation

The transportation segment revenues and operating earnings were as follows (in thousands):

|

2009

|

2008

|

2007

|

||||||||||||||||||||||

|

Amount

|

Change(1)

|

Amount

|

Change(1)

|

Amount

|

Change(1)

|

|||||||||||||||||||

|

Revenues

|

$ | 44,895 | (34 | )% | $ | 67,747 | 6 | % | $ | 63,894 | 3 | % | ||||||||||||

|

Operating earnings

|

$ | 2,128 | (50 | )% | $ | 4,245 | (23 | )% | $ | 5,504 | 6 | % | ||||||||||||

|

Depreciation

|

$ | 3,970 | 3 | % | $ | 3,843 | (10 | )% | $ | 4,275 | (6 | )% | ||||||||||||

______________

|

(1)

|

Represents the percentage increase (decrease) from the prior year.

|

Comparison 2009 to 2008

Revenues and operating results turned downward for the transportation segment in 2009 due to reduced customer demand beginning in the third quarter of 2008. The Company’s customers are predominately the domestic United States petrochemical industry, and demand for such products is driven primarily by activity within the housing and automotive sectors. The current national economic recession has severely and adversely impacted this segment of the Company’s business. Customer demand is down approximately 30% and through year-end 2009 showed only limited signs of recovery. Typically, as revenues decline, operating earnings decline at a faster rate, as measured by percentage, due to the fixed cost components of operating costs. In March 2009, the Company instituted cost cutting measures including a reduction in personnel levels in order to better align costs with the Company’s level of revenues. As a result, the rate of decline in operating earnings slowed relative to the rate of decline in revenues beginning in the second quarter of 2009. In addition during the third quarter of 2009 the Company earned an approximate $467,000 credit against its automobile and workers compensation insurance premiums. Such premium credits served to reduce operating expenses and were a direct result of reduced activity within the transportation segment.

Based on the current level of infrastructure, the Company’s transportation segment is designed to maximize efficiency when revenues excluding fuel adjustments are in the $60 million per year range. The Company’s transportation business tends to contract when United States and world economies weaken and also fluctuates with the exchange value for the U.S. dollar. A strong dollar exchange rate generally suppresses demand and reduces earnings. Other important factors include levels of competition within the tank truck industry as well as competition from the railroads. Some demand improvement, most likely the result of shifting traffic patterns from rail to truck, occurred in January 2010 and has continued to date.

18

Comparison 2008 to 2007

Transportation revenues include various component parts, the most significant being standard line haul charges, fuel adjustment charges and demurrage. Line haul revenues declined slightly during 2008 to $48.3 million versus $49.2 million in 2007 as the average annual demand for the Company’s services generally remained consistent. Fuel adjustment billings increased to $12.6 million in 2008 compared to $7.6 million in 2007 for comparative additional 2008 revenue of $5 million. However, actual fuel expense incurred increased by $5.6 million during 2008 to $17.1 million. The partial inability to fully pass along fuel increases coupled with increased salary and wage cost during 2008 reduced operating earnings for the year.

- Oil and Gas

Oil and gas segment revenues and operating earnings are primarily derived from crude oil and natural gas production volumes and prices. Comparative amounts for revenues, operating earnings and depreciation and depletion were as follows (in thousands):

|

2009

|

2008

|

2007

|

||||||||||||||||||||||

|

Amount

|

Change(1)

|

Amount

|

Change(1)

|

Amount

|

Change(1)

|

|||||||||||||||||||

|

Revenues

|

$ | 8,650 | (50 | )% | $ | 17,248 | 25 | % | $ | 13,783 | (19 | )% | ||||||||||||

|

Operating earnings (loss)

|

(3,625 | ) | 8 | % | (3,348 | ) | 17 | % | (2,853 | ) | (153 | )% | ||||||||||||

|

Depreciation and depletion

|

3,654 | (46 | )% | 6,763 | 16 | % | 5,833 | 62 | % | |||||||||||||||

|

Producing property impairments

|

1,350 | (56 | )% | 3,078 | 153 | % | 1,216 | 43 | % | |||||||||||||||

______________

|

(1)

|

Represents the percentage increase (decrease) from the prior year.

|

Comparative volumes and prices were as follows:

|

2009

|

2008

|

2007

|

|

|

Production Volumes

|

|||

|

- Crude Oil

|

49,500 bbls

|

50,500 bbls

|

69,250 bbls

|

|

- Natural Gas

|

1,304,000 mcf

|

1,243,000 mcf

|

1,182,000 mcf

|

|

Average Price

|

|||

|

- Crude Oil

|

$ 58.10/bbl

|

$ 99.25/bbl

|

$ 70.21/bbl

|

|

- Natural Gas

|

$ 4.43/mcf

|

$ 9.84/mcf

|

$ 7.54/mcf

|

The revenue and earnings decline for the oil and gas segment in 2009 is attributable to decreased crude oil and natural gas prices as shown in the tables above. Depreciation and depletion expense is reduced in the current period because a significant decline in hydrocarbon prices at year-end December 31, 2008 caused producing property impairment provisions to be recorded. Such charges reduced the level of capitalized costs for amortizing in the current period. Improved oil and gas segment revenues for 2008 in comparison to 2007 resulted from increased overall average commodity prices for both crude oil and natural gas as shown above. Crude oil volumes are reduced in 2009 and 2008 as a result of normal production declines while natural gas volumes increased for each year with favorable drilling results.

19

Operating earnings were burdened in 2009, 2008 and 2007 with exploration expenses incurred as follows (in thousands):

|

2009

|

2008

|

2007

|

||||||||||

|

Dry hole expense

|

$ | 661 | $ | 2,421 | $ | 3,187 | ||||||

|

Prospect abandonment

|

2,423 | 2,834 | 845 | |||||||||

|

Seismic and geological

|

734 | 775 | 1,475 | |||||||||

|

Total

|

$ | 3,818 | $ | 6,030 | $ | 5,507 | ||||||

During 2009, the Company participated in the drilling of 35 wells with 26 successful and 9 dry holes. Additionally, the Company had seven wells in process on December 31, 2009 with ultimate evaluation anticipated during 2010. Converting natural gas volumes to equate with crude oil volumes at a ratio of six to one, oil and gas production and proved reserve volumes are summarized as follows on an equivalent barrel (Eq. Bbls) basis:

|

2009

|

2008

|

2007

|

||||||||||

|

(Eq. Bbls.)

|

(Eq. Bbls.)

|

(Eq. Bbls.)

|

||||||||||

|

Beginning of year

|

1,304,000 | 1,475,000 | 1,779,000 | |||||||||

|

Estimated reserve additions

|

439,000 | 395,000 | 246,000 | |||||||||

|

Production

|

(267,000 | ) | (258,000 | ) | (266,000 | ) | ||||||

|

Reserves sold

|

- | - | (245,000 | ) | ||||||||

|

Revisions of previous estimates

|

(26,000 | ) | (308,000 | ) | (39,000 | ) | ||||||

|

End of year

|

1,450,000 | 1,304,000 | 1,475,000 | |||||||||

During 2009 and in total for the three year period ended December 31, 2009, estimated reserve additions represented 164 percent and 136 percent, respectively, of production volumes.

The Company’s current drilling and exploration efforts are primarily focused as follows:

East Texas Project

Beginning in 2005, the Company began acquiring acreage interests in Nacogdoches and Shelby counties of East Texas. Subsequent drilling activity produced 26 productive wells through the end of 2009. Four of the successful wells targeted the Haynesville Shale Play of Nacogdoches County with the Hill #1, the Pop Pop Gas Unit #1 and the Hassell Gas Unit #1 each beginning initial production rates from 12,000 to in excess of 15,000 mcf per day of natural gas with flowing tubing pressures in excess of 7200 psi. The Company has a five percent working interest in these three wells and holds a five percent working interest in approximately 43,000 acres, which includes the area of the Haynesville wells. A two percent working interest is held in approximately 24,000 additional adjacent acres. Drilling activity will continue on this project with six rigs scheduled during 2010.

Eaglewood Project

The Eaglewood project encompasses a ten county area from South Texas along the Gulf Coast and northward into East Texas. In this area, the Company purchased existing 3-D seismic data and reprocessed it using proprietary techniques. During 2008, five wells were successfully drilled. In 2009, activity was curtailed due to reduced prices for natural gas. Active efforts resumed in 2010 with one successful well drilled in the first quarter and three wells approved for drilling. The Company anticipates additional economically viable prospects will be identified for future drilling. The Company has a five percent working interest in this project.

20

Southwestern Arkansas

The Company participated in three 3-D seismic surveys in Southwestern Arkansas covering approximately 160 square miles. After initially drilling two unsuccessful test wells on this project in 2008, additional study was completed and a successful well was drilled in 2010 and is presently completing. Indications continue to suggest that multiple drillable shallow oil prospects will be identified. The Company’s working interest in this project varies from 4.5 percent to 11.6 percent.

South Central Kansas

The Company is participating with a 10 percent working interest in a large 3-D seismic survey in South Central Kansas. A number of prospects have been identified with the first well scheduled to spud in the first quarter of 2010.

|

-

|

Oil and gas property sale

|

In May 2007, the Company sold its interest in certain Louisiana producing oil and gas properties. Sale proceeds totaled $14.9 million resulting in a pre-tax gain on sale of approximately $12.1 million.

|

-

|

General and administrative, interest income and income tax

|

General and administrative expenses were elevated during 2007 due primarily to federally mandated Sarbanes-Oxley compliance costs. Interest income declined in 2009 and 2008 as interest rates on overnight deposits declined to near zero following the significant turmoil that occurred in the financial markets during the fall of 2008. The provision for income taxes is based on Federal and State tax rates and variations are consistent with taxable income in the respective accounting periods.

|

|

-

|

Outlook

|

Recent successful results in the Haynesville Shale formation of East Texas should boost 2010 natural gas volumes and revenues. Further for 2010, emphasis will be on development drilling which should reduce the level of exploration expense charged to earnings. The marketing and transportation segments are also forecasting stable profitability during 2010. Absent declines in crude oil and natural gas prices, upcoming 2010 results should show improvement over the current level of earnings.

The Company has the following major objectives for 2010:

|

-

|

Maintain marketing operating earnings at the $10 million level exclusive of inventory valuation gains or losses.

|

|

-

|

Establish transportation operating earnings at the $3 million level.

|

|

-

|

Establish oil and gas operating earnings at the $5 million level and replace 2010 production with current reserve additions.

|

21

Liquidity and Capital Resources

The Company’s liquidity primarily derives from net cash provided from operating activities, which was $22,285,000, $13,639,000 and $9,201,000 for each of 2009, 2008 and 2007, respectively. As of December 31, 2009 and 2008, the Company had no bank debt or other forms of debenture obligations. Cash and cash equivalents totaled $16,806,000 as of December 31, 2009, and such balances are maintained in order to meet the timing of day-to-day cash needs. Working capital, the excess of current assets over current liabilities, totaled $38,372,000 as of December 31, 2009.