Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended January 30, 2010

or

| ¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the Transition period from to

Commission File No. 1-11084

KOHL’S CORPORATION

(Exact name of registrant as specified in its charter)

| WISCONSIN | 39-1630919 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| N56 W17000 Ridgewood Drive, Menomonee Falls, Wisconsin |

53051 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code (262) 703-7000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock, $.01 Par Value | New York Stock Exchange | |

| Securities registered pursuant to Section 12(g) of the Act: | NONE | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes X No .

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No X .

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes X No .

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes X No .

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer X Accelerated filer Non-accelerated filer (Do not check if a smaller reporting company) Smaller reporting company

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes No X .

At August 1, 2009, the aggregate market value of the voting stock of the Registrant held by stockholders who were not affiliates of the Registrant was approximately $14.8 billion (based upon the closing price of Registrant’s Common Stock on the New York Stock Exchange on such date). At March 10, 2010, the Registrant had outstanding an aggregate of 306,974,796 shares of its Common Stock.

Documents Incorporated by Reference:

Portions of the Proxy Statement for the Registrant’s Annual Meeting of Shareholders to be held on May 13, 2010 are incorporated into Parts II and III.

Table of Contents

| 3 | ||||

| Item 1. |

3 | |||

| Item 1A. |

7 | |||

| Item 1B. |

11 | |||

| Item 2. |

11 | |||

| Item 3. |

16 | |||

| Item 4. |

16 | |||

| 17 | ||||

| Item 5. |

17 | |||

| Item 6. |

20 | |||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

21 | ||

| Item 7A. |

33 | |||

| Item 8. |

33 | |||

| Item 9. |

Changes In and Disagreements with Accountants on Accounting and Financial Disclosures |

33 | ||

| Item 9A. |

33 | |||

| Item 9B. |

35 | |||

| 36 | ||||

| Item 10. |

36 | |||

| Item 11. |

37 | |||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

37 | ||

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

37 | ||

| Item 14. |

37 | |||

| 38 | ||||

| Item 15. |

38 | |||

| 39 | ||||

| 40 | ||||

| F-1 | ||||

Table of Contents

Kohl’s Corporation (the “Company” or “Kohl’s”) was organized in 1988 and is a Wisconsin corporation. We operate family-oriented department stores that sell moderately priced apparel, footwear and accessories for women, men and children; soft home products such as sheets and pillows; and housewares. Our stores generally carry a consistent merchandise assortment with some differences attributable to regional preferences. Our stores feature quality private and exclusive brands which are found “Only at Kohl’s” as well as national brands. Our apparel and home fashions appeal to classic, modern classic and contemporary customers. As of January 30, 2010, we operated 1,058 stores in 49 states.

As reflected in the table below, our merchandise mix has been consistent over the last three years:

| 2009 | 2008 | 2007 | |||||||

| Women’s |

32 | % | 32 | % | 33 | % | |||

| Men’s |

19 | 19 | 19 | ||||||

| Home |

18 | 18 | 18 | ||||||

| Children’s |

13 | 13 | 13 | ||||||

| Accessories |

10 | 10 | 9 | ||||||

| Footwear |

8 | 8 | 8 |

In addition, Kohl’s offers on-line shopping on our website at www.Kohls.com. Designed as an added service for customers who prefer to shop using the internet, the website has grown to include a selection of items and categories beyond what is available in stores, with a primary focus on extended sizes, product line extensions, and web-exclusive product lines. The website is designed to provide a convenient, easy-to-navigate, on-line shopping environment that complements our in-store focus.

An important aspect of our pricing strategy and overall profitability is a culture focused on maintaining a low-cost structure. Critical elements of this low-cost structure are our unique store format, lean staffing levels, sophisticated management information systems and operating efficiencies which are the result of centralized buying, advertising and distribution.

Our fiscal year ends on the Saturday closest to January 31. Unless otherwise noted, references to years in this report relate to fiscal years, rather than to calendar years. Fiscal year 2009 (“2009”) ended on January 30, 2010. Fiscal year 2008 (“2008”) ended on January 31, 2009. Fiscal year 2007 (“2007”) ended on February 2, 2008. Fiscal 2009, 2008 and 2007 were 52-week years.

Strategic Committees and Initiatives

We have two strategic committees which focus on opportunities to drive our overall profitability. The mission of the Regional Assortment Committee is to accelerate sales growth by varying merchandise assortment, marketing and store presentation by region to reflect the lifestyle preferences and climate needs of our customers. The mission of the In-Store Experience Committee is to consistently deliver an improved store experience that generates loyalty and grows market share.

The following initiatives have been designed to achieve the goals of the strategic committees:

| • | Our merchandise content initiatives are focused on increasing market share by expanding Kohl’s appeal to a broader range of customers and by creating value and differentiation with private and exclusive brands which are available “Only at Kohl’s.” New brand launches in 2009 included: |

| • | Dana Buchman – a classic lifestyle brand, spanning several categories including women’s apparel, intimate apparel, accessories, and footwear, launched in February 2009. Ultimately, the brand may be extended into home, beauty and fragrance categories. |

| • | Hang Ten – a California lifestyle collection for young shoppers launched in Spring 2009. |

3

Table of Contents

| • | Mudd – launched in juniors and girls prior to the 2009 back-to-school shopping season. |

| • | LC Lauren Conrad – exclusive partnership with Lauren Conrad, launched in approximately 300 Kohl’s stores and Kohls.com in October 2009. LC Lauren Conrad will be rolled out to all stores nationwide in March 2010. We accelerated the roll-out due to better than expected sales. Our original plans did not call for roll out until Fall 2010. |

Helix, our newest private brand, launched in February 2010. Helix is an opening-price brand positioned in our Contemporary Good lifestyle/price zone and will be featured in young men’s tops, fashion bottoms and shorts.

The success of our recently launched brands, as well as our other exclusive and private brands, continue to drive increased penetration of our exclusive and private labels. Exclusive and private brand sales as a percentage of total sales increased approximately 220 basis points to 44.3% for 2009.

| • | Our marketing initiatives are designed to differentiate Kohl’s in the marketplace while maximizing the return on our marketing investment. Our 2009 marketing efforts used “The More You Know, The More You Kohl’s” platform to focus on the value of shopping at Kohl’s. Our marketing emphasized the power of Kohl’s savings tools that allow our customer to save more money—like compelling sale events, savings for Kohl’s Charge cardholders, sale events with no exclusions, and unique “Only at Kohl’s” events such as Kohl’s Cash and Power Hours. |

We used all media types to communicate the message including both national and spot television, radio, newspaper tab insertions, direct mail, e-mail and digital media along with our own Kohl’s.com website. Our marketing also emphasized our flexible, no questions asked, return policy.

| • | Our inventory management initiatives are designed to ensure that we have the right inventory, in the right stores, at the right time. Size optimization is focused on ensuring that each of our individual stores has inventory in the correct style, color and size. Markdown optimization is focused on pricing clearance items at the appropriate price for each location’s inventory and sales history. |

Another important inventory management initiative is to increase our speed-to-market through our concept-to customer strategy. Two years ago, it took 45 weeks from the start of development to the delivery of products to the stores. Today, our cycle time is typically 20 to 32 weeks, with our fastest brands delivering in 12 weeks and reorders in four to six weeks.

During 2009, we continued to aggressively manage our inventory levels by reducing seasonal inventory levels, while maintaining levels in basic areas such as hosiery and underwear. As a result of strong inventory management and cycle time reductions, clearance inventory levels have decreased for a second consecutive year. Our year-end inventory per store (on a dollar basis) decreased 0.9% from last year.

| • | The objective of our in-store shopping experience initiative is to satisfy the changing needs and expectations of our customers. Practical, easy shopping is about convenience. At Kohl’s, convenience includes a neighborhood location close to home, convenient parking, easily accessible entry, knowledgeable and friendly associates, wide aisles, a functional store layout, shopping carts/strollers and fast, centralized checkouts. Though our stores have fewer departments than traditional, full-line department stores, the physical layout of the store and our focus on strong in-stock positions in style, color and size is aimed at providing a convenient shopping experience for an increasingly time-starved customer. |

Remodels are also an important part of our in-store shopping experience initiative as we believe it is extremely important to maintain our existing store base, even in this difficult environment. We completed 51 store remodels in 2009—an increase from the 36 stores which were remodeled in 2008—and currently plan to remodel 85 stores in 2010. We have been able to compress the remodel duration period from 16 weeks to nine weeks over the past two years to minimize costs and disruption to our stores, benefiting our sales and customer experience.

4

Table of Contents

Our new and remodeled stores continue to reflect our latest thoughts in store design. Recent enhancements include new and updated exteriors and point-of-sale stations; improved fitting rooms, lounges, restrooms and customer service areas; and specialty fixturing. We have also updated the junior’s, kids, young men’s and shoe departments and redesigned our center core to improve sightlines throughout the store. Remodels and new stores in 2010 will contain a dramatically re-designed home area which will allow us to have more capacity on the sales floor and provide more flexibility in our fixtures.

As a result of our in-store experience and other initiatives, we have seen an approximately 7% improvement in our customer service scorecard results in 2009. Customer service scores are delivered from direct customer surveys conducted by an independent research firm.

For discussion of our financial results, see Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Expansion

Our expansion strategy has been, and will continue to be, designed to achieve profitable growth. At the time of our initial public offering in 1992, we had 79 stores in the Midwest. As of year-end 2009, we operated 1,058 stores in 49 states and in every large and intermediate sized market in the United States. As a result of economic conditions throughout the United States, our store growth in 2009 was slower than in prior years.

| Estimated | ||||||||||

| 2008 | Net Additions |

2009 | Net Additions |

2010 | ||||||

| Number of stores |

1,004 | 54 | 1,058 | 30 | 1,088 | |||||

| Gross square footage (in millions) |

89 | 4 | 93 | 2 | 95 | |||||

| Retail selling square footage (in millions) |

75 | 3 | 78 | 2 | 80 | |||||

We expect that the expansion rate in 2009 and 2010 will be more indicative of future expansion than our past history. We will, however, continue to focus our future expansion efforts on opportunistic acquisitions given the current retail environment as well as fill-in stores in our better performing markets.

The Kohl’s concept has proven to be transferable to markets across the country. New market entries are supported by extensive advertising and promotions which are designed to introduce new customers to the Kohl’s concept of brands, value and convenience. Additionally, we have been successful in acquiring, refurbishing and operating locations previously operated by other retailers. Of the 1,058 stores we operated as of January 30, 2010, 237 are take-over locations, which facilitated our initial entry into several markets. Once a new market is established, we add additional stores to further strengthen market share and enhance profitability.

We remain focused on providing the solid infrastructure needed to ensure consistent, low-cost execution. We proactively invest in distribution capacity and regional management to facilitate growth in new and existing markets. Our central merchandising organization tailors merchandise assortments to reflect regional climates and preferences. Management information systems support our low-cost culture by enhancing productivity and providing the information needed to make key merchandising decisions.

We believe the transferability of the Kohl’s retailing strategy, our experience in acquiring and converting pre-existing stores and in building new stores, combined with our substantial investment in management information systems, centralized distribution and headquarters functions provide a solid foundation for further expansion.

Distribution

We receive substantially all of our merchandise at nine retail distribution centers. A small amount of our merchandise is delivered directly to the stores by vendors or their distributors. The retail distribution centers,

5

Table of Contents

which are strategically located through the United Sates, ship merchandise to each store by contract carrier several times a week. We also operate a 940,000 square foot fulfillment center in Monroe, Ohio that services our e-commerce business. Additionally, we plan to open a 970,000 square foot e-commerce fulfillment center in San Bernardino, California in June 2010 to provide increased capacity to support our growing e-commerce business.

See Item 2, “Properties,” for additional information about our distribution centers.

Employees

As of January 30, 2010, we employed approximately 133,000 associates, including approximately 29,000 full-time and 104,000 part-time associates. The number of associates varies during the year, peaking during the back-to-school and holiday seasons. None of our associates are represented by a collective bargaining unit. We believe our relations with our associates are very good.

Competition

The retail industry is highly competitive. Management considers quality, value, merchandise mix, service and convenience to be the most significant competitive factors in the industry. Our primary competitors are traditional department stores, upscale mass merchandisers and specialty stores. Our specific competitors vary from market to market.

Merchandise Vendors

We purchase merchandise from numerous domestic and foreign suppliers. We have Terms of Engagement requirements which set forth the basic minimum requirements all business partners must meet in order to do business with Kohl’s. Our Terms of Engagement include provisions regarding laws and regulations, employment practices, ethical standards, environmental and legal requirements, communication, monitoring/compliance, record keeping, subcontracting and corrective action. Our expectation is that all business partners will comply with these Terms of Engagement and quickly remediate any deficiencies, if noted, in order to maintain our business relationship.

None of our vendors accounted for more than 5% of our net purchases during 2009. We have no long-term purchase commitments or arrangements with any of our suppliers, and believe that we are not dependent on any one supplier. We believe we have good working relationships with our suppliers.

Seasonality

Our business, like that of most retailers, is subject to seasonal influences. The majority of our sales and income are typically realized during the second half of each fiscal year. The back-to-school season extends from August through September and represents approximately 15% of our annual sales. Approximately 30% of our sales occur during the holiday season in the months of November and December. Because of the seasonality of our business, results for any quarter are not necessarily indicative of the results that may be achieved for the fiscal year. In addition, quarterly results of operations depend upon the timing and amount of revenues and costs associated with the opening of new stores.

Trademarks and Service Marks

The name “Kohl’s” is a registered service mark of one of our wholly-owned subsidiaries. We consider this mark and the accompanying name recognition to be valuable to our business. This subsidiary has over 125 additional registered trademarks, trade names and service marks, most of which are used in our private label program.

6

Table of Contents

Available Information

Our internet website is www.Kohls.com. Through the “Investor Relations” portion of this website, we make available, free of charge, our proxy statements, Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, SEC Forms 3, 4 and 5 and any amendments to those reports as soon as reasonably practicable after such material has been filed with, or furnished to, the Securities and Exchange Commission (“SEC”).

The following have also been posted on our website, under the caption “Investor Relations-Corporate Governance:”

| • | Committee charters of our Board of Directors’ Audit Committee, Compensation Committee and Governance & Nominating Committee |

| • | Report to Shareholders on Social Responsibility |

| • | Corporate Governance Guidelines |

| • | Code of Ethics |

Any amendment to or waiver from the provisions of the Code of Ethics that is applicable to our Chief Executive Officer, Chief Financial Officer or other key finance associates will be disclosed on the “Corporate Governance” portion of the website.

Information contained on our website is not part of this Annual Report on Form 10-K. Paper copies of any of the materials listed above will be provided without charge to any shareholder submitting a written request to our Investor Relations Department at N56 W17000 Ridgewood Drive, Menomonee Falls, Wisconsin 53051 or via e-mail to Investor.Relations@Kohls.com.

Forward Looking Statements

Items 1, 2, 3, 5, 7 and 7A of this Form 10-K contain “forward-looking statements,” made within the meaning of the Private Securities Litigation Reform Act of 1995. Words such as “believes,” “anticipates,” “plans,” “may,” “intends,” “will,” “should,” “expects” and similar expressions are intended to identify forward-looking statements. In addition, statements covering our future sales or financial performance and our plans, performance and other objectives, expectations or intentions are forward-looking statements, such as statements regarding our liquidity, debt service requirements, planned capital expenditures, future store openings and adequacy of capital resources and reserves. There are a number of important factors that could cause our results to differ materially from those indicated by the forward-looking statements, including among others, those risk factors described below. Forward-looking statements relate to the date made, and we undertake no obligations to update them.

Declines in general economic conditions, consumer spending levels and other conditions could lead to reduced consumer demand for our merchandise and cause reductions in our sales and/or gross margin.

Consumer spending habits, including spending for the merchandise that we sell, are affected by, among other things, prevailing economic conditions, levels of employment, salaries and wage rates, prevailing interest rates, housing costs, energy costs, income tax rates and policies, consumer confidence and consumer perception of economic conditions. In addition, consumer purchasing patterns may be influenced by consumers’ disposable income, credit availability and debt levels.

The recent slowdown has caused disruptions and significant volatility in financial markets, increased rates of default and bankruptcy and declining consumer and business confidence, which has led to decreased levels of

7

Table of Contents

consumer spending, particularly on discretionary items. A continued or incremental slowdown in the U.S. economy and the uncertain economic outlook could continue to adversely affect consumer spending habits resulting in lower net sales and profits than expected on a quarterly or annual basis. As all of our stores are located in the United States, we are especially susceptible to deteriorations in the U.S. economy.

Consumer confidence is also affected by the domestic and international political situation. The outbreak or escalation of war, or the occurrence of terrorist acts or other hostilities in or affecting the United States, could lead to a decrease in spending by consumers.

Actions by our competitors could adversely affect our operating results.

The retail business is highly competitive. We compete for customers, associates, locations, merchandise, services and other important aspects of our business with many other local, regional and national retailers. Those competitors, some of which have a greater market presence than Kohl’s, include traditional store-based retailers, internet and catalog businesses and other forms of retail commerce. Unanticipated changes in the pricing and other practices of those competitors may adversely affect our performance.

Product safety concerns could adversely affect our sales and operating results.

If our merchandise offerings do not meet applicable safety standards or our customers’ expectations regarding safety, we could experience lost sales, experience increased costs and/or be exposed to legal and reputational risk. Events that give rise to actual, potential or perceived product safety concerns could expose us to government enforcement action and/or private litigation. Reputational damage caused by real or perceived product safety concerns, could have a negative impact on our sales.

If we do not offer merchandise our customers want and fail to successfully manage our inventory levels, our sales and/or gross margin may be adversely impacted.

Our business is dependent on our ability to anticipate fluctuations in consumer demand for a wide variety of merchandise. Failure to accurately predict constantly changing consumer tastes, preferences, spending patterns and other lifestyle decisions could create inventory imbalances and adversely affect our performance and long-term relationships with our customers. Additionally, failure to accurately predict changing consumer tastes may result in excess inventory, which could result in additional markdowns and adversely affect our operating results.

Ineffective marketing could adversely affect our sales and profitability.

In 2009, advertising costs, net of related vendor allowances, were $846 million. We believe that differentiating Kohl’s in the marketplace is critical to our success. We design our marketing programs to increase awareness of our brands, which we expect will create and maintain customer loyalty, increase the number of customers that shop our stores and increase our sales. If our marketing programs are not successful, our sales and profitability could be adversely affected.

We may be unable to raise additional capital, if needed, or to raise capital on favorable terms.

Recently, the general economic and capital market conditions in the United States and other parts of the world have deteriorated significantly and have adversely affected access to capital and increased the cost of capital. If our existing cash, cash generated from operations and funds available on our lines of credit are insufficient to fund our future activities, including capital expenditures, or repay debt when it becomes due, we may need to raise additional funds through public or private equity or debt financing. If unfavorable capital market conditions exist if and when we were to seek additional financing, we may not be able to raise sufficient capital on favorable terms and on a timely basis (if at all). Failure to obtain capital on acceptable terms, or at all, when required by our business circumstances could have a material adverse effect on us including an inability to fund new growth and other capital expenditures.

8

Table of Contents

Inefficient or ineffective allocation of capital could adversely affect our operating results and/or shareholder value.

Our goal is to invest capital to maximize our overall long-term returns. This includes spending on inventory, capital projects and expenses, managing debt levels, and periodically returning value to our shareholders through share repurchases. To a large degree, capital efficiency reflects how well we manage our other key risks. The actions taken to address other specific risks may affect how well we manage the more general risk of capital efficiency. If we do not properly allocate our capital to maximize returns, we may fail to produce optimal financial results and we may experience a reduction in shareholder value.

Changes in our credit card operations could adversely affect our sales and/or profitability.

Our credit card operations facilitate sales in our stores and generate additional revenue from fees related to extending credit. In connection with the April 2006 sale of our proprietary credit card accounts to JPMorgan Chase & Co. (“JPMorgan Chase”), we entered into a revenue-sharing agreement with JPMorgan Chase, which issues Kohl’s branded private label credit cards to new and existing Kohl’s customers. Net revenues of the program are shared with JPMorgan Chase according to a fixed percentage and are settled monthly. Net revenues include finance charge and late fee revenues, less write-offs of uncollectible accounts and other expenses.

The Credit Card Accountability Responsibility and Disclosure Act of 2009 (the “CARD Act”) mandates fundamental changes to many of our current business practices, including marketing, underwriting, pricing and billing. Most of the requirements became effective in February 2010 and others will become effective in August 2010. Legislation has been proposed to accelerate the effective date of all of the CARD Act provisions effective as soon as the legislation is enacted, but prospects for enactment are uncertain. Although the Federal Reserve has issued final rules implementing most of the provisions of the CARD Act, it has yet to issue rules implementing the provisions that take effect in August 2010. Accordingly, it is difficult to assess the impact of those provisions at this time. While we have already made, and anticipate making additional, changes designed to lessen the impact of the changes required by the CARD Act, there is no assurance that we will be successful. If we are not able to lessen the impact of the changes required by the CARD Act, the changes could adversely impact the profitability of our credit operations and make it more difficult to extend credit to our customers and collect payments which would have a material adverse effect on our results of operations.

Changes in credit card use, payment patterns and default rates may also result from a variety of economic, legal, social and other factors that we cannot control or predict with certainty. Changes that adversely impact our ability to extend credit and collect payments could negatively affect our results.

Our current agreement with JPMorgan Chase expires in 2011. We are currently exploring various alternatives to this agreement, including entering into a new agreement with an alternative partner and expect to reach a decision by Fall 2010. This timing could be impacted by the timing of the issuance of final CARD Act regulations. We may be unable to negotiate a new contract at comparable terms which could significantly reduce the net revenues which we currently earn under this program. Should we be unable to negotiate a new agreement, we may repurchase the receivables. We currently expect to use a combination of cash and cash equivalents on hand and new debt to finance such a repurchase. As of January 30, 2010, outstanding receivables totaled approximately $3 billion. The outstanding receivable balance fluctuates during the year and typically reaches its highest level during the holiday season and its lowest level during the first quarter of the year.

Weather conditions could adversely affect our sales and/or profitability by affecting consumer shopping patterns.

Because a significant portion of our business is apparel and subject to weather conditions in our markets, our operating results may be adversely affected by severe or unexpected weather conditions. Frequent or unusually heavy snow, ice or rain storms or extended periods of unseasonable temperatures in our markets could adversely affect our performance by affecting consumer shopping patterns or diminishing demand for seasonal merchandise.

9

Table of Contents

Our business is seasonal, which could adversely affect the market price of our common stock.

Our business is subject to seasonal influences, with a major portion of sales and income historically realized during the second half of the fiscal year, which includes the back-to-school and holiday seasons. This seasonality causes our operating results to vary considerably from quarter to quarter and could materially adversely affect the market price of our common stock.

We may be unable to source merchandise in a timely and cost-effective manner, which could adversely affect our sales and operating results.

Approximately 20% of the merchandise we sell is sourced through a third party purchasing agent. The remaining merchandise is sourced from a wide variety of domestic and international vendors. All of our vendors must comply with applicable laws and our required Terms of Engagement. Our ability to find qualified vendors and access products in a timely and efficient manner is a significant challenge which is typically even more difficult with respect to goods sourced outside the United States. Political or financial instability, trade restrictions, tariffs, currency exchange rates, transport capacity and costs and other factors relating to foreign trade, and the ability to access suitable merchandise on acceptable terms are beyond our control and could adversely impact our performance.

If any of our vendors were to become subject to bankruptcy, receivership or similar proceedings, we may be unable to arrange for alternate or replacement contracts, transactions or business relationships on terms as favorable as current terms, which could adversely affect our sales and operating results.

An inability to attract and retain quality employees could result in higher payroll costs and adversely affect our operating results.

Our performance is dependent on attracting and retaining a large and growing number of quality associates. Many of those associates are in entry level or part-time positions with historically high rates of turnover. Our ability to meet our labor needs while controlling costs is subject to external factors such as unemployment levels, prevailing wage rates, minimum wage legislation and changing demographics. Changes that adversely impact our ability to attract and retain quality associates could adversely affect our performance.

An inability to open new stores could adversely affect our financial performance.

Our plan to continue to increase the number of our stores will depend in part upon the availability of existing retail stores or store sites on acceptable terms. Increases in real estate, construction and development costs could limit our growth opportunities and affect our return on investment. There can be no assurance that such stores or sites will be available for purchase or lease, or that they will be available on acceptable terms. If we are unable to grow our retail business, our financial performance could be adversely affected.

Regulatory and litigation developments could adversely affect our business operations and financial performance.

Various aspects of our operations are subject to federal, state or local laws, rules and regulations, any of which may change from time to time. We continually monitor the state and federal employment law environment for developments that may adversely impact us. Failure to detect changes and comply with such laws and regulations may result in an erosion of our reputation, disruption of business and/or loss of employee morale. Additionally, we are regularly involved in various litigation matters that arise in the ordinary course of our business. Litigation or regulatory developments could adversely affect our business operations and financial performance.

Damage to the reputation of our private and exclusive brands could adversely affect our sales.

We develop and promote private and exclusive brands that have generated national recognition. In some cases, the brands or the marketing of such brands are tied to or affiliated with well-known individuals. Damage to

10

Table of Contents

the reputations of our private and exclusive label brand names or any affiliated individuals, could arise from product failures, litigation or various forms of adverse publicity and may generate negative customer sentiment, potentially resulting in a reduction in sales, earnings, and shareholder value.

Disruptions in our information systems could adversely affect our sales and profitability.

The efficient operation of our business is dependent on our information systems. In particular, we rely on our information systems to effectively manage sales, distribution, merchandise planning and allocation functions. We also generate sales though the operations of our Kohls.com website. The failure of our information systems to perform as designed could disrupt our business and harm sales and profitability.

Unauthorized disclosure of sensitive or confidential customer information could severely damage our reputation, expose us to risks of litigation and liability, disrupt our operations and harm our business.

As part of our normal course of business, we collect, process and retain sensitive and confidential customer information. Despite the security measures we have in place, our facilities and systems, and those of our third party service providers, may be vulnerable to security breaches, acts of vandalism, computer viruses, misplaced or lost data, programming and/or human errors, or other similar events. Any security breach involving the misappropriation, loss or other unauthorized disclosure of confidential information, whether by us or our vendors, could severely damage our reputation, expose us to risks of litigation and liability, disrupt our operations and harm our business.

New legal requirements could adversely affect our operating results.

Our sales and results of operations may be adversely affected by new legal requirements, including proposed health care reform legislation and climate change and other environmental legislation and regulations. The costs and other effects of new legal requirements cannot be determined with certainty. For example, new legislation or regulations may result in increased costs directly for our compliance or indirectly to the extent such requirements increase prices of goods and services because of increased compliance costs or reduced availability of raw materials. At this point, we are unable to determine the impact that healthcare reform could have on our employer-sponsored medical plans.

Item 1B. Unresolved Staff Comments

Not applicable

Stores

As of January 30, 2010, we operated 1,058 stores in 49 states. Our typical, or “prototype,” store has 88,000 gross square feet of retail space and serves trade areas of 150,000 to 200,000 people. Most “small” stores are 68,000 square feet and serve trade areas of 100,000 to 150,000 people. Our “urban” stores, currently located in the New York and Chicago markets, serve very densely populated areas of up to 500,000 people and average approximately 125,000 gross square feet of retail space.

Our typical lease has an initial term of 20-25 years and two to eight renewal options for consecutive five or ten-year extension terms. Substantially all of our leases provide for a minimum annual rent that is fixed or adjusts to set levels during the lease term, including renewals. Approximately one-fourth of the leases provide for additional rent based on a percentage of sales over designated levels.

11

Table of Contents

The following tables summarize key information about our stores.

| Number of Stores | Selling Square Footage | |||||||||||||

| 2008 | Additions/ (Closures) |

2009 | 2008 | Additions/ (Closures) |

2009 | |||||||||

| Mid-Atlantic: |

||||||||||||||

| Delaware |

5 | — | 5 | 399 | — | 399 | ||||||||

| Maryland |

17 | — | 17 | 1,301 | — | 1,301 | ||||||||

| Pennsylvania |

43 | — | 43 | 3,165 | — | 3,165 | ||||||||

| Virginia |

27 | (1 | ) | 26 | 1,988 | (70 | ) | 1,918 | ||||||

| West Virginia |

7 | — | 7 | 503 | — | 503 | ||||||||

| Total Mid-Atlantic |

99 | (1 | ) | 98 | 7,356 | (70 | ) | 7,286 | ||||||

| Midwest: |

||||||||||||||

| Illinois |

61 | — | 61 | 4,706 | — | 4,706 | ||||||||

| Indiana |

37 | — | 37 | 2,711 | — | 2,711 | ||||||||

| Iowa |

14 | — | 14 | 954 | — | 954 | ||||||||

| Michigan |

46 | (1 | ) | 45 | 3,421 | (68 | ) | 3,353 | ||||||

| Minnesota |

25 | — | 25 | 1,923 | — | 1,923 | ||||||||

| Nebraska |

7 | — | 7 | 486 | — | 486 | ||||||||

| North Dakota |

3 | — | 3 | 217 | — | 217 | ||||||||

| Ohio |

56 | — | 56 | 4,190 | — | 4,190 | ||||||||

| South Dakota |

2 | — | 2 | 169 | — | 169 | ||||||||

| Wisconsin |

39 | — | 39 | 2,850 | — | 2,850 | ||||||||

| Total Midwest |

290 | (1 | ) | 289 | 21,627 | (68 | ) | 21,559 | ||||||

| Northeast: |

||||||||||||||

| Connecticut |

18 | — | 18 | 1,367 | — | 1,367 | ||||||||

| Maine |

5 | — | 5 | 388 | — | 388 | ||||||||

| Massachusetts |

21 | — | 21 | 1,682 | — | 1,682 | ||||||||

| New Hampshire |

8 | 1 | 9 | 567 | 73 | 640 | ||||||||

| New Jersey |

36 | 2 | 38 | 2,777 | 145 | 2,922 | ||||||||

| New York |

44 | 1 | 45 | 3,411 | 73 | 3,484 | ||||||||

| Rhode Island |

3 | — | 3 | 227 | — | 227 | ||||||||

| Vermont |

1 | — | 1 | 77 | — | 77 | ||||||||

| Total Northeast |

136 | 4 | 140 | 10,496 | 291 | 10,787 | ||||||||

| South Central: |

||||||||||||||

| Arkansas |

8 | — | 8 | 572 | — | 572 | ||||||||

| Kansas |

9 | 1 | 10 | 663 | 53 | 716 | ||||||||

| Louisiana |

4 | 1 | 5 | 291 | 60 | 351 | ||||||||

| Missouri |

23 | — | 23 | 1,726 | — | 1,726 | ||||||||

| Oklahoma |

9 | — | 9 | 668 | — | 668 | ||||||||

| Texas |

78 | 2 | 80 | 5,754 | 135 | 5,889 | ||||||||

| Total South Central |

131 | 4 | 135 | 9,674 | 248 | 9,922 | ||||||||

| Southeast: |

||||||||||||||

| Alabama |

10 | — | 10 | 689 | — | 689 | ||||||||

| Florida |

43 | 5 | 48 | 3,213 | 375 | 3,588 | ||||||||

| Georgia |

31 | 2 | 33 | 2,298 | 145 | 2,443 | ||||||||

| Kentucky |

15 | — | 15 | 1,061 | — | 1,061 | ||||||||

| Mississippi |

4 | — | 4 | 302 | — | 302 | ||||||||

| North Carolina |

26 | 1 | 27 | 1,906 | 72 | 1,978 | ||||||||

| South Carolina |

12 | — | 12 | 880 | — | 880 | ||||||||

| Tennessee |

19 | — | 19 | 1,345 | — | 1,345 | ||||||||

| Total Southeast |

160 | 8 | 168 | 11,694 | 592 | 12,286 | ||||||||

12

Table of Contents

| Number of Stores | Selling Square Footage | |||||||||||

| 2008 | Additions/ (Closures) |

2009 | 2008 | Additions/ (Closures) |

2009 | |||||||

| West: |

||||||||||||

| Northwest: |

||||||||||||

| Alaska |

— | 1 | 1 | — | 73 | 73 | ||||||

| Idaho |

4 | — | 4 | 269 | — | 269 | ||||||

| Montana |

1 | — | 1 | 72 | — | 72 | ||||||

| Oregon |

9 | — | 9 | 593 | — | 593 | ||||||

| Washington |

15 | — | 15 | 1,016 | — | 1,016 | ||||||

| Wyoming |

1 | — | 1 | 52 | — | 52 | ||||||

| Total Northwest |

30 | 1 | 31 | 2,002 | 73 | 2,075 | ||||||

| Southwest: |

||||||||||||

| Arizona |

25 | 1 | 26 | 1,881 | 73 | 1,954 | ||||||

| California |

90 | 31 | 121 | 7,037 | 1,792 | 8,829 | ||||||

| Colorado |

22 | 1 | 23 | 1,698 | 74 | 1,772 | ||||||

| Nevada |

8 | 3 | 11 | 611 | 190 | 801 | ||||||

| New Mexico |

4 | — | 4 | 249 | — | 249 | ||||||

| Utah |

9 | 3 | 12 | 667 | 209 | 876 | ||||||

| Total Southwest |

158 | 39 | 197 | 12,143 | 2,338 | 14,481 | ||||||

| Total West |

188 | 40 | 228 | 14,145 | 2,411 | 16,556 | ||||||

| Total Kohl’s |

1,004 | 54 | 1,058 | 74,992 | 3,404 | 78,396 | ||||||

13

Table of Contents

| Number of Stores by Greater Metropolitan Area | |||||||

| 2008 | Additions/ (Closures) |

2009 | |||||

| New York City |

60 | 2 | 62 | ||||

| Los Angeles |

41 | 12 | 53 | ||||

| Chicago |

50 | — | 50 | ||||

| Philadelphia |

34 | — | 34 | ||||

| Atlanta |

25 | 2 | 27 | ||||

| Dallas/Fort Worth |

25 | — | 25 | ||||

| Detroit |

25 | (1 | ) | 24 | |||

| Boston |

23 | 1 | 24 | ||||

| San Francisco |

16 | 8 | 24 | ||||

| Washington DC |

23 | — | 23 | ||||

| Milwaukee |

22 | — | 22 | ||||

| Minneapolis/St. Paul |

22 | — | 22 | ||||

| Phoenix |

21 | 1 | 22 | ||||

| Houston |

19 | — | 19 | ||||

| Cleveland/Akron |

18 | — | 18 | ||||

| Denver |

17 | 1 | 18 | ||||

| Indianapolis |

17 | — | 17 | ||||

| Sacramento |

13 | 4 | 17 | ||||

| Columbus |

15 | — | 15 | ||||

| Orlando |

13 | 2 | 15 | ||||

| St. Louis |

14 | — | 14 | ||||

| Hartford/New Haven |

13 | — | 13 | ||||

| Cincinnati |

12 | — | 12 | ||||

| Salt Lake City |

9 | 3 | 12 | ||||

| Miami |

9 | 2 | 11 | ||||

| Kansas City |

10 | — | 10 | ||||

| Pittsburgh |

10 | — | 10 | ||||

| Charlotte |

10 | — | 10 | ||||

| San Diego |

7 | 3 | 10 | ||||

| Raleigh Durham |

9 | 1 | 10 | ||||

| Seattle/Tacoma |

10 | — | 10 | ||||

| Other |

392 | 13 | 405 | ||||

| 1,004 | 54 | 1,058 | |||||

| Number of Stores by Store Type | |||||||

| 2008 | Net Additions |

2009 | |||||

| Prototype |

918 | 44 | 962 | ||||

| Small |

82 | 10 | 92 | ||||

| Urban |

4 | — | 4 | ||||

| 1,004 | 54 | 1,058 | |||||

14

Table of Contents

| Number of Stores by Ownership |

|||||||

| 2008 | Net Additions |

2009 | |||||

| Owned |

363 | 9 | 372 | ||||

| Leased |

396 | 3 | 399 | ||||

| Ground leased |

245 | 42 | 287 | * | |||

| 1,004 | 54 | 1,058 | |||||

| * Ground leased includes both ground leases and certain takeover leases where significant capital expenditures were made to the existing store. |

| ||||||

| Number of Stores by Location |

|||||||

| 2008 | Net Additions |

2009 | |||||

| Strip centers |

717 | 29 | 746 | ||||

| Community & regional malls |

66 | 7 | 73 | ||||

| Free standing |

221 | 18 | 239 | ||||

| 1,004 | 54 | 1,058 | |||||

| Number of Stores by Building Type |

|||||||

| 2008 | Net Additions |

2009 | |||||

| One-story |

930 | 41 | 971 | ||||

| Multi-story |

74 | 13 | 87 | ||||

| 1,004 | 54 | 1,058 | |||||

Distribution Centers

The following table summarizes key information about each of our retail distribution centers.

| Location |

Year Opened |

Square Footage |

States Serviced |

Approximate Store Capacity | ||||

| Findlay, Ohio |

1994 | 780,000 | Ohio, Michigan, Indiana | 125 | ||||

| Winchester, Virginia |

1997 | 420,000 | Pennsylvania, Virginia, Maryland, Delaware, West Virginia | 100 | ||||

| Blue Springs, Missouri |

1999 | 540,000 | Minnesota, Colorado, Missouri, Iowa, Kansas, Montana, Nebraska, North Dakota, South Dakota, Wyoming | 105 | ||||

| Corsicana, Texas |

2001 | 540,000 | Texas, Oklahoma, Arkansas, Mississippi, Louisiana | 110 | ||||

| Mamakating, New York |

2002 | 605,000 | New York, New Jersey, Massachusetts, Connecticut, New Hampshire, Rhode Island, Maine, Vermont | 140 | ||||

| San Bernardino, California |

2002 | 575,000 | California, Arizona, Nevada, Utah, New Mexico | 110 | ||||

| Macon, Georgia |

2005 | 560,000 | Alabama, Tennessee, Georgia, South Carolina, Florida, Kentucky, North Carolina | 125 | ||||

| Patterson, California |

2006 | 360,000 | Alaska, California, Oregon, Washington, Idaho | 110 | ||||

| Ottawa, Illinois |

2008 | 328,000 | Indiana, Illinois, Michigan, Wisconsin | 165 |

15

Table of Contents

We own all of the retail distribution centers except Corsicana, Texas, which is leased. We also own our corporate headquarters in Menomonee Falls, Wisconsin and a 940,000 square foot e-commerce fulfillment center in Monroe, Ohio. Additionally, we plan to open a 970,000 square foot e-commerce fulfillment center in San Bernardino, California in June 2010 to provide increased capacity to support our growing e-commerce business.

During the fourth quarter of 2009, we closed our Menomonee Falls, Wisconsin distribution center, the oldest and least efficient distribution center in our network. Stores previously supplied by this distribution center will be serviced by one of our nine remaining distribution centers, primarily the Ottawa, Illinois distribution center.

We are not currently a party to any material legal proceedings, but are subject to certain legal proceedings and claims from time to time that are incidental to our ordinary course of business.

16

Table of Contents

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

(a) Market information

Our Common Stock has been traded on the New York Stock Exchange since May 19, 1992, under the symbol “KSS.” The prices in the table set forth below indicate the high and low sales prices of our Common Stock per the New York Stock Exchange Composite Price History for each quarter in 2009 and 2008.

| Price Range | ||||||

| High | Low | |||||

| 2009 |

||||||

| Fourth Quarter |

$ | 58.07 | $ | 49.87 | ||

| Third Quarter |

$ | 60.89 | $ | 48.43 | ||

| Second Quarter |

$ | 50.39 | $ | 40.64 | ||

| First Quarter |

$ | 46.50 | $ | 32.50 | ||

| 2008 |

||||||

| Fourth Quarter |

$ | 39.74 | $ | 24.28 | ||

| Third Quarter |

$ | 56.00 | $ | 25.18 | ||

| Second Quarter |

$ | 50.81 | $ | 36.81 | ||

| First Quarter |

$ | 50.93 | $ | 38.40 | ||

We have filed with the Securities and Exchange Commission (“SEC”), as Exhibits 31.1 and 31.2 to this Annual Report on Form 10-K, the Sarbanes-Oxley Act Section 302 certifications. In 2009, Kevin Mansell, our Chief Executive Officer, submitted a certification with the New York Stock Exchange (“NYSE”) in accordance with Section 303A.12 of the NYSE Listed Company Manual stating that, as of the date of the certification, he was not aware of any violation by us of the NYSE’s corporate governance listing standards.

(b) Holders

At March 10, 2010, there were 5,003 record holders of our Common Stock.

(c) Dividends

We have never paid a cash dividend. The payment of future dividends, if any, will be determined by our Board of Directors in light of existing business conditions, including our earnings, financial condition and requirements, restrictions in financing agreements and other factors deemed relevant by the Board of Directors.

(d) Securities Authorized For Issuance Under Equity Compensation Plans

See the information provided in the “Equity Compensation Plan Information” section of the Proxy Statement for our May 13, 2010 Annual Meeting of Shareholders, which information is incorporated herein by reference.

17

Table of Contents

(e) Performance Graph

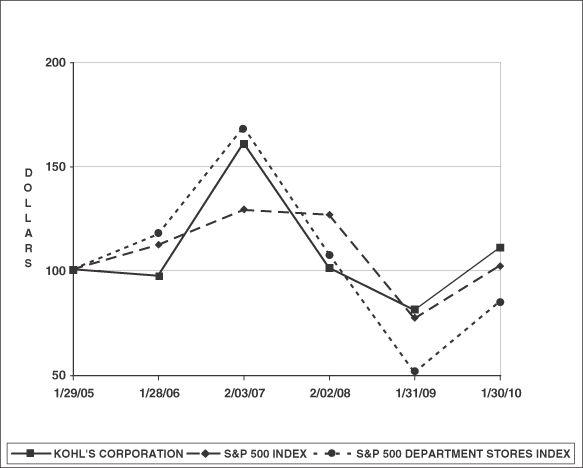

The graph below compares our cumulative five-year stockholder return to that of the Standard & Poor’s 500 Index and the S&P 500 Department Stores Index. The S&P 500 Department Stores Index was calculated by Standard & Poor’s Investment Services and includes Kohl’s; JCPenney Company, Inc.; Dillard’s, Inc.; Macy’s, Inc.; Nordstrom Inc.; and Sears Holding Corporation. The graph assumes investment of $100 on January 29, 2005 and reinvestment of dividends. The calculations exclude trading commissions and taxes.

| 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | |||||||||||||

| Kohl’s Corporation |

$ | 100.00 | $ | 96.89 | $ | 160.35 | $ | 100.68 | $ | 80.47 | $ | 110.41 | ||||||

| S&P 500 Index |

100.00 | 111.63 | 128.37 | 126.05 | 76.43 | 101.76 | ||||||||||||

| S&P 500 Department Stores Index |

100.00 | 116.76 | 167.93 | 107.22 | 50.65 | 84.67 | ||||||||||||

(f) Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities

We did not sell any equity securities during 2009 which were not registered under the Securities Act.

(g) Purchases of Equity Securities by the Issuer and Affiliated Purchasers

In September 2007, our Board of Directors authorized a $2.5 billion share repurchase program which is intended to return excess capital to our shareholders. As a result of the current economic environment, we have not purchased any shares under this program since July 2008. The program does not have a specified termination date.

18

Table of Contents

The following table contains information for shares acquired from employees in lieu of amounts required to satisfy minimum tax withholding requirements upon the vesting of the employees’ restricted stock during the three fiscal months ended January 30, 2010:

| Period |

Total Number of Shares Purchased During Period |

Average Price Paid Per Share |

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs |

Maximum Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||

| (In millions) | ||||||||||

| Nov. 1 – Nov. 28, 2009 |

999 | $ | 55.52 | — | $ | 1,866 | ||||

| Nov. 29, 2009 – Jan. 2, 2010 |

306 | $ | 56.18 | — | 1,866 | |||||

| Jan. 3 – Jan. 30, 2010 |

— | — | — | 1,866 | ||||||

| Total |

1,305 | $ | 55.67 | — | $ | 1,866 | ||||

19

Table of Contents

Item 6. Selected Consolidated Financial Data

The selected consolidated financial data presented below should be read in conjunction with our consolidated financial statements and related notes included elsewhere in this document. The Statement of Income and Balance Sheet Data have been derived from our audited consolidated financial statements.

| 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

| (Dollars in Millions, Except Per Share and Per Square Foot Data) | ||||||||||||||||||||

| Statement of Income Data: |

||||||||||||||||||||

| Net sales |

$ | 17,178 | $ | 16,389 | $ | 16,474 | $ | 15,597 | $ | 13,444 | ||||||||||

| Cost of merchandise sold |

10,680 | 10,334 | 10,460 | 9,922 | 8,664 | |||||||||||||||

| Gross margin |

6,498 | 6,055 | 6,014 | 5,675 | 4,780 | |||||||||||||||

| Selling, general and administrative expenses |

4,144 | 3,936 | 3,697 | 3,422 | 2,981 | |||||||||||||||

| Depreciation and amortization |

590 | 541 | 452 | 388 | 339 | |||||||||||||||

| Preopening expenses |

52 | 42 | 61 | 50 | 44 | |||||||||||||||

| Operating income |

1,712 | 1,536 | 1,804 | 1,815 | 1,416 | |||||||||||||||

| Interest expense, net |

124 | 111 | 62 | 41 | 70 | |||||||||||||||

| Income before income taxes |

1,588 | 1,425 | 1,742 | 1,774 | 1,346 | |||||||||||||||

| Provision for income taxes |

597 | 540 | 658 | 665 | 504 | |||||||||||||||

| Net income |

$ | 991 | $ | 885 | $ | 1,084 | $ | 1,109 | $ | 842 | ||||||||||

| Net income per share: |

||||||||||||||||||||

| Basic |

$ | 3.25 | $ | 2.89 | $ | 3.41 | $ | 3.34 | $ | 2.45 | ||||||||||

| Diluted |

$ | 3.23 | $ | 2.89 | $ | 3.39 | $ | 3.31 | $ | 2.43 | ||||||||||

| Operating Data: |

||||||||||||||||||||

| Comparable store sales growth (a) |

0.4 | % | (6.9 | %) | (0.8 | %) | 5.9 | % | 3.4 | % | ||||||||||

| Net sales per selling square foot (b) |

$ | 217 | $ | 222 | $ | 249 | $ | 256 | $ | 252 | ||||||||||

| Total square feet of selling space |

78,396 | 74,992 | 69,889 | 62,357 | 56,625 | |||||||||||||||

| Number of stores open |

1,058 | 1,004 | 929 | 817 | 732 | |||||||||||||||

| Return on average shareholders’ equity (c) |

13.8 | % | 14.0 | % | 18.5 | % | 19.5 | % | 15.5 | % | ||||||||||

| Balance Sheet Data (end of period): |

||||||||||||||||||||

| Working capital |

$ | 3,095 | $ | 1,884 | $ | 1,952 | $ | 1,481 | $ | 2,520 | ||||||||||

| Property and equipment, net |

7,018 | 6,984 | 6,510 | 5,353 | 4,616 | |||||||||||||||

| Total assets |

13,160 | 11,363 | 10,575 | 9,046 | 9,146 | |||||||||||||||

| Long-term debt and capital leases |

2,052 | 2,053 | 2,052 | 1,040 | 1,046 | |||||||||||||||

| Shareholders’ equity |

7,853 | 6,739 | 6,102 | 5,603 | 5,956 | |||||||||||||||

| (a) | Comparable store sales growth is based on sales for stores (including e-commerce sales and relocated or expanded stores) which were open throughout both the full current and prior year periods. Fiscal 2006 was a 53-week year. Comparable store sales growth for 2006 is presented for the 52-weeks ended January 27, 2007 and excludes approximately $200 million in sales which were earned in the 53rd week of that year. |

| (b) | Net sales per selling square foot is based on stores open for the full current period, excluding e-commerce. Fiscal 2006 excludes the impact of the 53 rd week. |

| (c) | Average shareholders’ equity is based on a 5-quarter average. |

20

Table of Contents

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Executive Summary

The current economic slowdown has caused disruptions and significant volatility in financial markets, increased rates of mortgage loan default and personal bankruptcy, and declining consumer and business confidence, which has led to decreased levels of consumer spending, particularly on discretionary items. Though we have seen some improvement throughout 2009, as evidenced by increases in our comparable store sales, we believe that our core customer continues to face economic challenges which will result in a very competitive 2010.

Total net sales for 2009 were $17.2 billion, a 4.8% increase from 2008. Comparable store sales increased 0.4% over 2008. The Southwest region and the Accessories business reported the strongest comparable store sales growth.

Gross margin as a percent of net sales for the year increased approximately 88 basis points over the 2008 rate to 37.8%. Strong inventory management as well as increased penetration of private and exclusive brands contributed to the margin strength. Ending inventory per store (in dollars) decreased 0.9% compared to 2008.

Selling, general and administrative expenses (“SG&A”) increased approximately 5% compared to the prior year. SG&A as a percentage of net sales, increased, or “deleveraged” primarily due to increased incentive compensation and changes made to our non-management compensation structure. SG&A expenses for the year increased at a rate faster than sales, but at a rate slower than new store growth of 5.5%. Our cost control initiatives are focused on sustainable productivity improvements, not one-time cutting of expenses. While we will continue to look for ways to become more efficient, we intend to keep the customer experience in our stores a priority in order to provide consistency across our stores and intend to continue to invest more in store payroll to improve our customer service.

Net income increased approximately 12% for 2009 to $991 million, or $3.23 per diluted share, compared to $885 million, or $2.89 per diluted share for 2008.

We ended the year with 1,058 stores in 49 states, including 56 which were successfully opened in 2009. We completed 51 store remodels, compared to 36 stores last year. In fiscal 2010, we expect to open approximately 30 stores and remodel 85 stores. Remodels remain a critical part of our long-term strategy as we believe it is extremely important to maintain our existing store base, even in this difficult economic environment.

Our current expectations for fiscal 2010 assume that consumer spending will continue to be weak throughout 2010. We expect comparable store sales will be driven by increased market share as we expect average transaction value to remain under pressure. Our current expectations for both the first quarter and fiscal 2010 compared to comparable fiscal 2009 periods are as follows:

| • | Total sales increase of 4% to 6% |

| • | Comparable store sales increase of 1% to 3% |

| • | Gross margin increase of 20 to 30 basis points |

| • | SG&A dollars to increase 4% to 5% |

| • | Earnings per diluted share of $0.48 to $0.52 for the first quarter of 2010 and $3.40 to $3.63 for fiscal 2010. |

Results of Operations

Our fiscal year ends on the Saturday closest to January 31. Unless otherwise noted, references to years in this report relate to fiscal years, rather than to calendar years. Fiscal year 2009 (“2009”) ended on January 30, 2010, fiscal year 2008 (“2008”) ended on January 31, 2009 and fiscal year 2007 (“2007”) ended on February 2, 2008. All three years were 52-week years.

21

Table of Contents

Net sales.

| 2009 | 2008 | 2007 | ||||||||||

| Net sales (in millions) |

$ | 17,178 | $ | 16,389 | $ | 16,474 | ||||||

| Number of stores: |

||||||||||||

| Open at end of period |

1,058 | 1,004 | 929 | |||||||||

| Comparable stores (a) |

929 | 817 | 732 | |||||||||

| Sales growth: |

||||||||||||

| All stores |

4.8 | % | (0.5 | %) | 5.6 | % | ||||||

| Comparable stores (a) |

0.4 | % | (6.9 | %) | (0.8 | %) | ||||||

| Net sales per selling square foot (b) |

$ | 217 | $ | 222 | $ | 249 | ||||||

| (a) | Comparable store sales growth is based on sales for stores (including e-commerce sales and relocated or expanded stores) which were open throughout both the full current and prior year periods. |

| (b) | Net sales per selling square foot is based on stores open for the full current period, excluding e-commerce. |

Net sales for 2009 increased $789 million, or 4.8%, over 2008. New stores contributed $719 million to the increase in net sales over the prior year. Comparable store sales increased $70 million. We opened 56 new stores in 2009, 75 stores in 2008 and 112 stores in 2007. As we open new stores, especially in existing markets, sales may be transferred from existing stores. We estimate that opening new stores in existing markets negatively impacted comparable store sales by approximately 1% in 2009.

Drivers of the changes in comparable stores sales were as follows:

| 2009 | 2008 | 2007 | |||||||

| Selling price per unit |

2.3 | % | 1.9 | % | (0.3 | )% | |||

| Units per transaction |

(4.3 | ) | (2.9 | ) | 0.9 | ||||

| Average transaction value |

(2.0 | ) | (1.0 | ) | 0.6 | ||||

| Number of transactions |

2.4 | (5.9 | ) | (1.4 | ) | ||||

| Comparable store sales |

0.4 | % | (6.9 | )% | (0.8 | )% | |||

Net sales, especially in the Southwest region, were favorably impacted by the closure of Mervyn’s department stores. We continue to aggressively pursue former Mervyn’s customers through increased advertising efforts and targeted efforts in stores most likely to benefit from former Mervyn’s customers. In these stores, we have increased staffing levels and provided higher inventory levels and wider assortments in selected categories. We estimate that the Mervyn’s closure increased our comparable store sales by approximately 140 basis points for the year.

The Southwest region reported the strongest 2009 sales growth with comparable store sales increases in the high single digits. We expect to continue to produce strong results in the Southwest in 2010, but we believe our other hot and mild regions will benefit more substantially in 2010 from the merchandising and marketing tactics we developed in 2009 in the Southwest.

Lower units per transaction resulted in negative comparable store sales in all regions other than the Southwest and Northwest.

By line of business, Accessories, Footwear and Home outperformed our comparable store sales for the year. Accessories was led by strength in sterling silver jewelry, fashion jewelry, and handbags. In Footwear, women’s, athletic and children’s shoes performed best. Home was strong in small electrics, bedding and bath. Men’s was similar to the company average and was led by active, basics and casual sportswear. Children’s and Women’s were below the company average. The Children’s business had strength in toys, infants/toddlers and boys.

22

Table of Contents

Women’s was strongest in intimate and both classic and updated sportswear, driven by substantial improvement in key private brands such as Sonoma, Croft and Barrow and Apt 9 which achieved strong fourth quarter increases.

E-commerce revenues increased 38.0% to $492 million for 2009. The sales growth is primarily the result of increased style and size selections offered on-line compared with our in-store selection as well as the expansion of product categories not available in our stores.

Net sales per selling square foot decreased 2% to $217 in 2009. The decrease is primarily due to the underperformance of stores opened in 2008.

Net sales for 2008 decreased $85 million, or 0.5%, from 2007. New stores contributed $1.0 billion to the increase in net sales over the prior year. Comparable store sales decreased $1.1 billion, or 6.9% (see the table above for drivers of the change). From a line of business perspective, Accessories reported the strongest comparable store sales in 2008 with strength in sterling silver jewelry and accessories/handbags. Children’s, Men’s and Footwear outperformed the comparable store sales for the year, while Women’s and Home trailed the company. The Northeast, Midwest and Mid-Atlantic regions reported the strongest comparable store sales for 2008. E-commerce revenues increased 48% to $356 million for 2008 as we continued to expand the selections offered on-line.

As reflected in the table below, our merchandise mix has remained relatively constant over the last three years:

| 2009 | 2008 | 2007 | |||||||

| Women’s |

32 | % | 32 | % | 33 | % | |||

| Men’s |

19 | 19 | 19 | ||||||

| Home |

18 | 18 | 18 | ||||||

| Children’s |

13 | 13 | 13 | ||||||

| Accessories |

10 | 10 | 9 | ||||||

| Footwear |

8 | 8 | 8 |

Gross margin.

| 2009 | 2008 | 2007 | ||||||||||

| (Dollars in millions) | ||||||||||||

| Gross margin |

$ | 6,498 | $ | 6,055 | $ | 6,014 | ||||||

| As a percent of net sales |

37.8 | % | 36.9 | % | 36.5 | % | ||||||

Gross margin includes the total cost of products sold, including product development costs, net of vendor payments other than reimbursement of specific, incremental and identifiable costs; inventory shrink; markdowns; freight expenses associated with moving merchandise from our vendors to our distribution centers; shipping and handling expenses of e-commerce sales; and terms cash discount. Our gross margin may not be comparable with that of other retailers because we include distribution center costs in selling, general and administrative expenses while other retailers may include these expenses in cost of merchandise sold.

The $443 million, or 7.3%, increase in gross margin dollars for 2009 compared to 2008 reflects higher sales volume including incremental sales at newly-opened stores. Gross margin as a percentage of sales increased 88 basis points to 37.8% for 2009. Strong inventory management and increased penetration of private and exclusive brands contributed to the margin strength. In addition to carrying a lower level of inventory per store, we continue to focus on receiving merchandise in season as needed through our cycle time reduction initiatives. This strategy reduces our seasonal merchandise clearance inventories. Sales of private and exclusive brands reached 44% of net sales for 2009, an increase of 220 basis points over 2008. Additionally, our ongoing markdown and size optimization initiatives continue to develop and have favorable impacts on our gross margin as a percent of net sales.

23

Table of Contents

Gross margin for 2008 increased $41 million, or 0.7%, over 2007. The improvement in gross margin as a percent of net sales for 2008 compared to 2007 was driven by the continued impact of our merchandise and inventory management initiatives and increased penetration of private and exclusive brands. Sales of private and exclusive brands were approximately 42% of net sales for 2008, an increase of over 260 basis points over 2007.

Selling, general and administrative expenses.

| 2009 | 2008 | 2007 | ||||||||||

| (Dollars in millions) | ||||||||||||

| Selling, general, and administrative expenses |

$ | 4,144 | $ | 3,936 | $ | 3,697 | ||||||

| As a percent of net sales |

24.1 | % | 24.0 | % | 22.4 | % | ||||||

Selling, general and administrative expenses (“SG&A”) include compensation and benefit costs (including stores, headquarters, buying and merchandising and distribution centers); occupancy and operating costs of our retail, distribution and corporate facilities; freight expenses associated with moving merchandise from our distribution centers to our retail stores, and among distribution and retail facilities; advertising expenses, offset by vendor payments for reimbursement of specific, incremental and identifiable costs; net revenues from the Kohl’s credit card agreement with JPMorgan Chase; and other administrative costs. We do not include depreciation and amortization and preopening expenses in SG&A. The classification of these expenses varies across the retail industry.

SG&A for 2009 increased $208 million, or 5.3%, over 2008. SG&A increased primarily due to store growth and increased incentive compensation and changes made to our non-management compensation structure.

Hourly store payroll costs as a percentage of net sales decreased, or “leveraged,” in 2009 as reduced inventory and clearance levels resulted in fewer hours spent on replenishment and inventory markdowns. We were able to shift some of these savings to provide additional customer assistance on the selling floor and at point-of-sale. This emphasis on customer service contributed to an approximately 7% improvement in our customer service scores over the prior year. Customer service scores are derived from direct customer surveys conducted by an independent research firm.

Distribution center costs, which are included in SG&A, totaled $168 million for 2009, $166 million for 2008 and $165 million for 2007. Payroll costs increased as increased sales required additional processing hours to facilitate the transfer of merchandise to the stores. These increases were offset by the benefits of technology investments in our distribution centers that continue to generate operating efficiencies. Lower fuel costs also contributed to the decrease.

In connection with the April 2006 sale of our proprietary credit card accounts to JPMorgan Chase & Co. (“JPMorgan Chase”), we entered into a service and revenue-sharing agreement. Pursuant to this agreement, JPMorgan Chase issues Kohl’s branded private label credit cards to new and existing Kohl’s customers. Since we do not own the receivables, the receivables and the related allowance for bad debt reserve are not reported on our balance sheets. Risk-management decisions are jointly managed by JPMorgan Chase and us. We handle all customer service functions and are responsible for all advertising and marketing related to credit card customers and the majority of the associated expenses. Net revenues of the program are shared with JPMorgan Chase according to a fixed percentage and are settled monthly. Net revenues include finance charge and late fee revenues, less write-offs of uncollectible accounts and other expenses. Net revenues from the credit card program increased in 2009 as growth in finance charges and late fee revenues exceeded increases in write-offs of uncollectible accounts.

Advertising and information services expenses, measured in both dollars and as a percentage of net sales, decreased in 2009 compared to 2008. Advertising expenses, net of vendor allowances, were $846 million for 2009 and $890 million for 2008.

24

Table of Contents

Partially offsetting these expense reductions were higher fixed occupancy and variable store costs due primarily to an increase in the number of stores and higher accrued incentive expenses as a result of improved performance for 2009 and changes to our non-management compensation structure.

SG&A for 2008 increased $239 million, or 6.5%, over 2007. The net increase in SG&A dollars reflects incremental costs at newly-opened stores, partially offset by decreases at comparable stores reflecting our commitment to control costs in a difficult economic environment. SG&A increased more than sales, but less than new store growth of 8.1%.

Depreciation and amortization.

| 2009 | 2008 | 2007 | |||||||

| (In millions) | |||||||||

| Depreciation and amortization |

$ | 590 | $ | 541 | $ | 452 | |||

The increases in depreciation and amortization are primarily due to the addition of new stores and remodels.

Preopening expenses.

| 2009 | 2008 | 2007 | |||||||

| Preopening expenses (in millions) |

$ | 52 | $ | 42 | $ | 61 | |||

| Number of stores opened |

56 | 75 | 112 | ||||||

Preopening expenses include the costs incurred prior to new store openings, such as advertising, hiring and training costs for new employees, processing and transporting initial merchandise, and rent expense. The average cost per store fluctuates based on the mix of stores opened in new markets compared to existing markets, with new markets being more expensive.

Preopening expenses for 2009 increased despite a decrease in the number of stores opened primarily due to an increase in the number of leased stores which opened in 2009. Under Generally Accepted Accounting Principles (“GAAP”), we are required to recognize rent expense when we take possession of the property, so we must recognize rental expense for ground leased properties several months prior to the actual opening of the store and, in most cases, before rental payments are due.

Preopening expense for 2008 decreased compared to 2007 primarily due to a decrease in the number of stores slightly offset by an increase in cost per store due to the number of ground lease stores.

Operating income.

| 2009 | 2008 | 2007 | ||||||||||

| (Dollars in millions) | ||||||||||||

| Operating income |

$ | 1,712 | $ | 1,536 | $ | 1,804 | ||||||

| As a percent of net sales |

10.0 | % | 9.4 | % | 11.0 | % | ||||||

The changes in operating income and operating income as a percent of net sales are due to the factors discussed above.

Interest expense.

| 2009 | 2008 | 2007 | |||||||

| (In millions) | |||||||||

| Interest expense, net |

$ | 124 | $ | 111 | $ | 62 | |||

25

Table of Contents

Net interest expense for 2009 increased $13 million, or 12%, over 2008. The increase is attributable to lower interest income due to lower interest rates on our investments, partially offset by higher average investments. A reduction in capitalized interest due to lower capital expenditures in 2009 also contributed to the increase in interest expense.

Net interest expense for 2008 increased $49 million, or 79%, over 2007 primarily due to $1 billion in new debt that was issued in September 2007. Reductions in capitalized interest due to lower capital expenditures also contributed to the increase.

Income taxes.

| 2009 | 2008 | 2007 | ||||||||||

| (Dollars in millions) | ||||||||||||

| Provision for income taxes |

$ | 597 | $ | 540 | $ | 658 | ||||||

| Effective tax rate |

37.6 | % | 37.9 | % | 37.8 | % | ||||||

The effective tax rate for 2009 was comparable to the 2008 and 2007 tax rates.

Inflation

Although we expect that our operating results will be influenced by general economic conditions, including fluctuations in food, fuel and energy prices, we do not believe that inflation has had a material effect on our results of operations during the periods presented. However, there can be no assurance that our business will not be affected by inflation in the future.

Liquidity and Capital Resources

Our primary ongoing cash requirements are for capital expenditures in connection with our expansion and remodeling programs and seasonal and new store inventory purchases. Our primary sources of funds are cash flow provided by operations, short-term trade credit and our lines of credit. Short-term trade credit, in the form of extended payment terms for inventory purchases, represents a significant source of financing for merchandise inventories. Seasonal cash needs may be met by the line of credit available under our revolving credit facility. Our working capital and inventory levels typically build throughout the fall, peaking during the November and December holiday selling season.

We anticipate that we will be able to satisfy our working capital requirements, planned capital expenditures and debt service requirements with available cash and cash equivalents, proceeds from cash flows from operations, short-term trade credit, seasonal borrowings under our revolving credit facility and other sources of financing. We expect to generate adequate cash flow from operating activities to sustain current levels of operations.